Languages

Pages

Legal

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 1/56

REAL ESTATE FINANCINGby Maya Bandolon-Cartojano, REC, REA, REB

PHILIPPINE ASSOCIATION OF

REAL ESTATE BOARDS, INC (PAREB)Gensan-Sarangani REB

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 2/56

TOPIC AREAS – 4hrsO Debt Financing

O Time Value of Money

O Cash Flow AnalysisO Financing Terminologies

O HDMF/PAGIBIG Financing, Principles and Guidelines

REAL ESTATE FINANCING

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 2

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 3/56

Debt Financing for Real Estate

O Discussion Outline

O Why Investors Use Leverage

O Behavioral Effects of Financing

O Types of Loans

O Legal Issues in Real Estate Finance

REAL ESTATE FINANCING

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 3

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 4/56

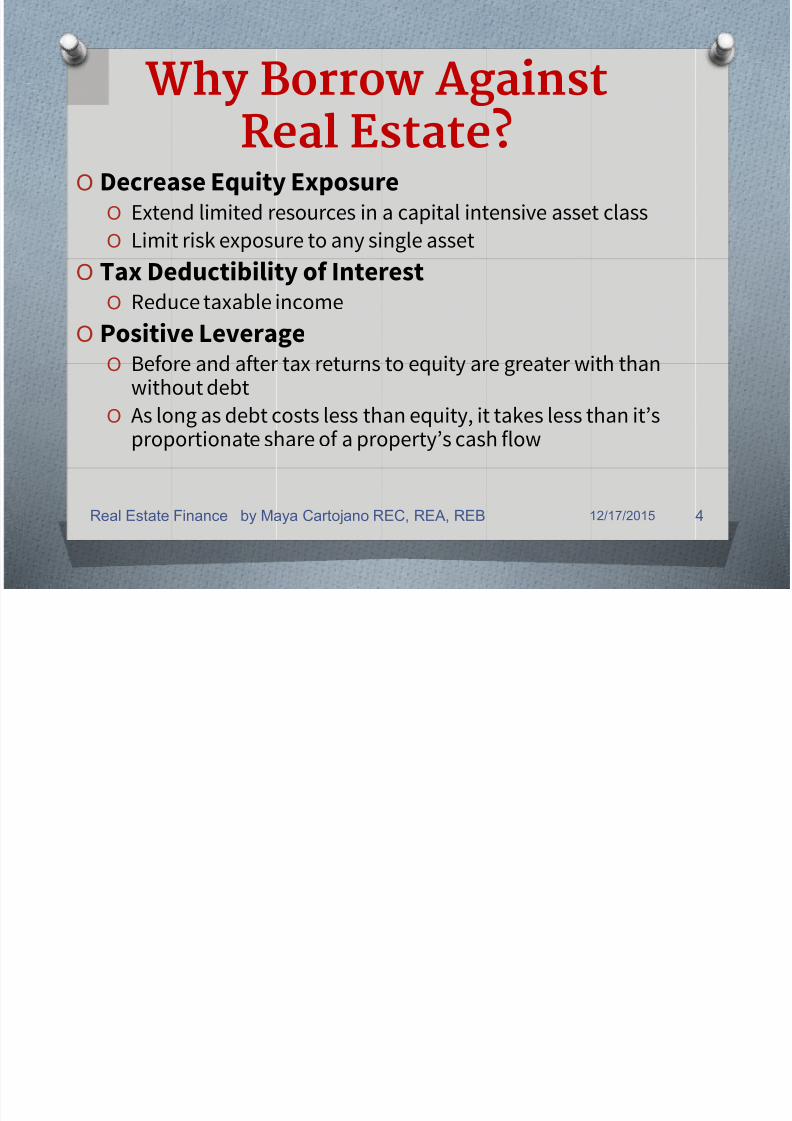

Why Borrow Against

Real Estate?O Decrease Equity Exposure

O Extend limited resources in a capital intensive asset class

O Limit risk exposure to any single asset

O Tax Deductibility of InterestO Reduce taxable income

O Positive LeverageO Before and after tax returns to equity are greater with than

without debt

O As long as debt costs less than equity, it takes less than it’sproportionate share of a property’s cash flow

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 4

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 5/56

How Debt Affects Real

Estate Investment BehaviorO Influences value at the margin

O Increases focus on operational efficiency

O Lengthens holding periods by reducingliquidity

O Increases risk of loss of investment capital

O Causes tax driven behaviors

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 5

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 6/56

REAL ESTATE FINANCE TERMS

Mortgages – borrowed money, considered capital

instruments because payback periods are usuallymore than 10 years

Equity– buyer’s contribution, usually downpayment

Original Loan Amount – face amount of loan

Amortization– monthly payments over a specified

time period to retire a mortgage. Consist ofPRINCIPAL + INTEREST

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 6

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 7/56

REAL ESTATE FINANCE

Interest – money earned for the right to use the

capital. Usually compound interest method

Payment or Debt Service– comprise both interest

and principal

Loan to Value Ratio – percentage of the original

loan amount to the value of the property (OLA/PV).BSP allows LTV ratio up to 80%.

Annual Constant – ratio of mortgage payment to

the original loan amount (MP/OLA)

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 7

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 8/56

Debt and Market LiquidityOStructure and terms of most long term debtincreases holding periods, illiquidity in themarket

O Loans are structured to lock in lender yieldsO Prepayment prohibitions, penalties

O Features compensate lenders for risks ofextending creditO Default – loss of principal

O Prepayment – potential opportunity cost of lost yieldO Interest rate risk – loss of value due to changes in the yield

curve

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 8

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 9/56

Debt and Equity

Principal RiskO Debt has legal priority over equity ownership

O Equity owners must balance the benefits of

positive leverage with the risk of foreclosureand loss of capital

O Equity often accepts lower levered returns for reducedrisk (ie, REITs, core investment funds)

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 9

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 10/56

Debt and TaxesODeductibility of interest expense enhances

the “tax shield” already in place from

depreciation

OTax impact is generally an individual issueO Private markets hold real estate primarily in “flow

through” vehicles (partnerships, etc.)

O Tax motivated investors may structure deals for

maximum tax benefitO Typically, does not effect pricing at the margin

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 10

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 11/56

Is Inflation Good for

Levered Real Estate?O In inflationary times, leverage benefits real

estate equity returns

O Debt principal is paid in the future with pesos thatare worth less

O Holds true only in hyper-inflationary

periods

O Loan pricing reflects the yield curve

OShould have inflationary expectations built in

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 11

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 12/56

Residential vs.

Commercial LendingOResidential lending:O Smaller in size

O Non-recourse to the borrower

O Totally dependent on market value of home for collateral

O Fully pre-payable at any time

O High percentage of prepayments at any given time

O government heavily involved in pricing and

structuringO Loan terms largely standardized, un-negotiable

O Widely disseminated pricing information12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 12

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 13/56

Residential vs.

Commercial LendingOCommercial Lending

O Dominated by private sources of capital

OA “relationship” business

O Increasingly influenced by the public

O Highly dependent on local market information

O Lender specialization by loan type

OSource of funding, market knowledge

O Terms and conditions highly negotiable

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 13

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 14/56

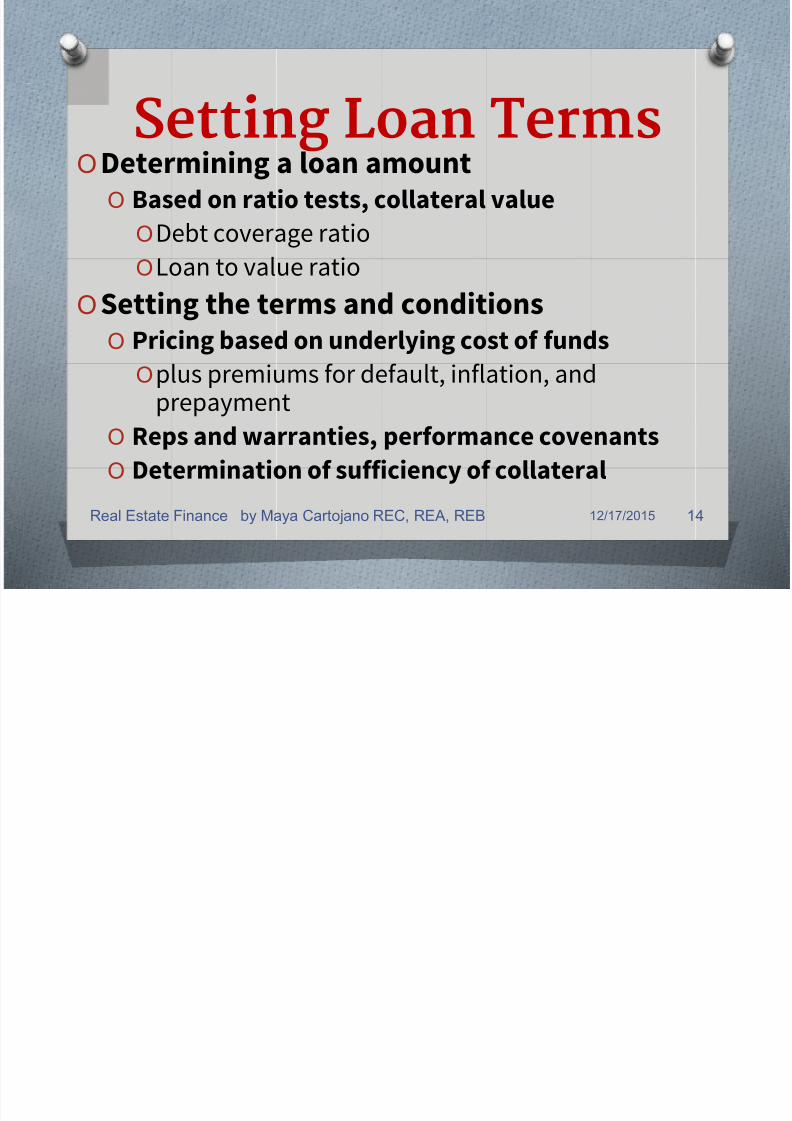

Setting Loan TermsO Determining a loan amountO Based on ratio tests, collateral value

ODebt coverage ratio

OLoan to value ratioO Setting the terms and conditions

O Pricing based on underlying cost of funds

Oplus premiums for default, inflation, and

prepaymentO Reps and warranties, performance covenants

O Determination of sufficiency of collateral

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 14

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 15/56

Alternative Loan StructuresO Loan structures reflect a trade off of risk and

return between lender and borrowerO Lender evaluates borrower capacity (ie., more

risk) for greater return

O Borrower evaluates more or less debt proceedsversus

OTiming and security of cash flowsO The “financial leverage” effect

OCurrent return (less risk) vs. residual return (morerisk)

OCost of incremental debt versus additional equity

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 15

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 16/56

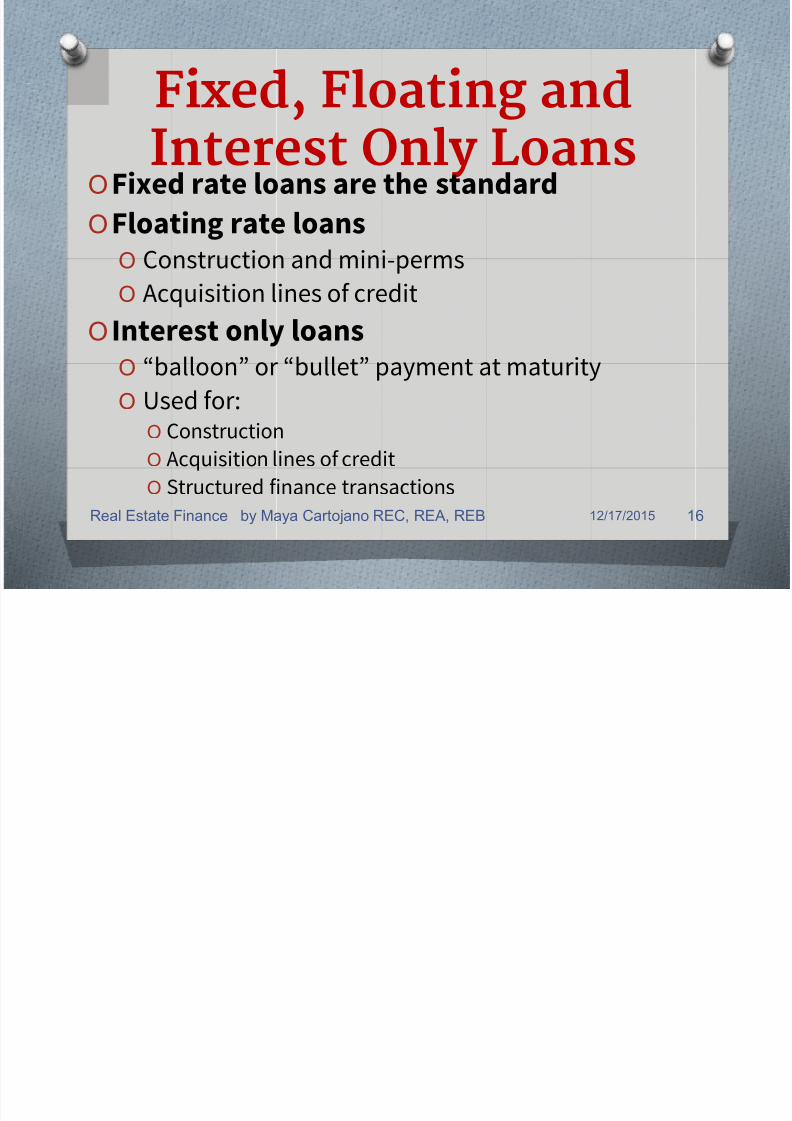

Fixed, Floating and

Interest Only LoansOFixed rate loans are the standard

OFloating rate loansO Construction and mini-perms

O Acquisition lines of credit

O Interest only loansO “balloon” or “bullet” payment at maturity

O Used for:O Construction

O Acquisition lines of credit

O Structured finance transactions12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 16

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 17/56

Participating LoansOLender trades risk for higher potential

returns

O Reduces LTV coverage

→ Increases loan amountO Takes a percentage of after debt service cash

flows

OStructured as “additional interest”

O Total of fixed payment and percentageinterest creates higher total yield on loan

dollars invested

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 17

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 18/56

More on Participating LoansOBorrower benefits:

O Greater loan proceedsO Often cheaper than equity which might have to be raised

from outside sources

O Lower fixed debt paymentsO Less pressure on short term NOI

OBorrower decision:O What is the incremental cost of borrowing the extra

loan amount, vs. cost of equity?

O If the deal IRR is weighted toward the residual, thelender’s participation in the residual is probablyless than an equity investor’s would be

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 18

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 19/56

More AlternativesOLand Sale LeasebackO Financing land separately from improvements

O Higher total loan proceeds

OFinances 100% of land value, vs. LTV if includedin typical loan calculation

O 100% of payments are tax deductible

OVs. only interest portion if financed by loan

ORisk is in subordination provisions

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 19

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 20/56

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 20

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 21/56

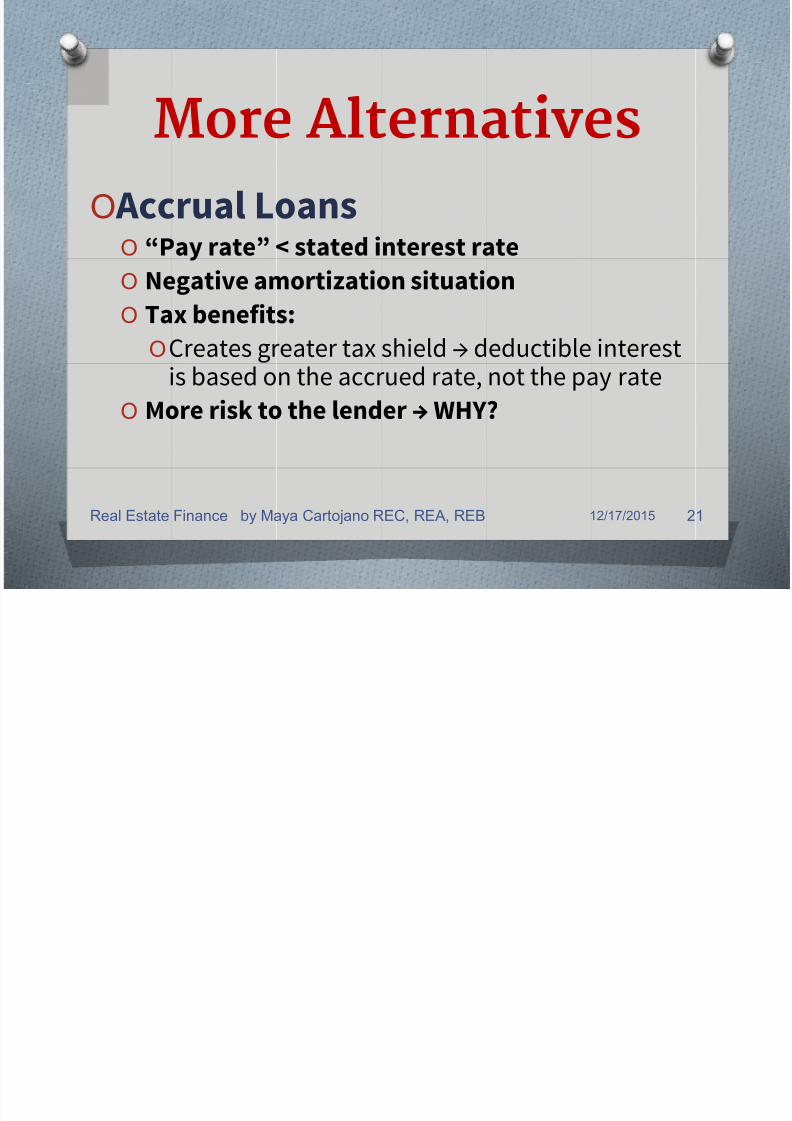

More AlternativesO Accrual Loans

O “Pay rate” < stated interest rate

O Negative amortization situationO Tax benefits:

OCreates greater tax shield → deductible interestis based on the accrued rate, not the pay rate

O More risk to the lender → WHY?

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 21

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 22/56

OConvertible LoansO Lender has an option to “convert” – ie, swap loan

proceeds for partial equity ownership

OWould convert if the equity value of the interest

exceeds the mortgage balance at conversion date

O Borrower benefits

OLower interest rate, greater current cash flow inexchange for potential loss of equity value in the

future

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 22

More Alternatives

S O O S

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 23/56

TYPES OF LOANS

Fixed Rate Mortgages – interest is fixed for the

term of the loan. Some fixed for 5-7 years, thenreadjusted for the remainder of term.

Adjustable Rate Mortgages – interest is based

on a certain index (eg TBills) plus spread

Buydowns – variation of FRM & ARM, but

interest is prepaid to lower payments in the

early years of the term. Prepaid interest usuallyby developers

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 23

FORMS OF MORTGAGES

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 24/56

FORMS OF MORTGAGES

Conventional Mortgages – most common,

secured by RE collateral, available throughbankers, banks and savings & loan institutions.

Usually safe instruments to trade in Secondary

Market for Morgages

Insured Loans – include guarantee or insurance

to protect the lender in case of default by the

borrower

Blanket Mortgage– secured by group ofproperties or number of lots

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 24

FORMS OF MORGAGES

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 25/56

FORMS OF MORGAGES

Chattel Mortgages – loan for personal

property and secured by personal property

Package Mortgages – loan on both real and

personal property. (eg. Factory can bemortgaged on the land, improvements and

equipments)

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 25

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 26/56

Legal Considerations In

Real Estate FinancingOReal estate cash flows can be legally allocated

to different “interest” holders via the capital

structure

OThe PV of each of these streams = value of theinterests claimed by each layer of capital

OThe legal system also establishes control over

other, non-monetary “interests”O Equity owners don’t necessarily get 100% of the “value”

of real estate interests

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 26

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 27/56

Possessory InterestsOPossessory (current or potential)

interest is a right to control some of

the rights through some form of

financial consideration

O “Fee simple” ownership interest

O Tenant’s leasehold interest

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 27

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 28/56

Non- Possessory InterestsONon-possessory interest is a right to use real

estate without ownership or financialconsideration

OMost pervasive form is the easementO Provides a right to use, but not legally own, an interest

O Power lines, fire access

O Some easements may be irrevocable

O An easement can affect value+ Right of way to reach the street

- Power line running down the center of property

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 28

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 29/56

REAL ESTATE

FINANCINGO SPOT CASH

O DEFERRED CASH PAYMENT

O LONG TERM FINANCING

Each type of financing scheme has its ownadvantages and disadvantages. Todetermine which one is appropriate to you,

it is best to start looking at your ownbudget and financial capabilities

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 29

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 30/56

BANK FINANCING SAMPLE

COMPUTATIONS

O *Let's say Bank Loan interest is 9.25% and the loan

term is 12 years -- therefore the Amortization Factor

(based on the table) is .0116637. There are manywebsites that provide an automated Mortgage

Calculator

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 30

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 31/56

SAMPLE COMPUTATIONSGiven:

Actual Value of Property: P1,000,000

Borrower's Equity: 30%

Loanable Amount: 70%

Bank Loan interest: 9.25%

How much monthly amortization?

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 31

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 32/56

MONTHLY AMORTIZATIONS PROBLEMSSELLING

PRICE/PROPERTY VALUE

less: DOWNPAYMENT

BALANCE

multiply: MONTHLY AMORTIZATION FACTOR*

MONTHLY AMORTIZATION

* Factor is usually given in the problem or a factor table is provided.

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 32

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 33/56

SAMPLE COMPUTATIONSGiven:

Actual Value of Property: P1,000,000

Borrower's Equity: 30%

Loanable Amount: 70%

Bank Loan interest: 9.25%

Amortization Factor: .0116637.

How much monthly amortization?

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 33

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 34/56

SAMPLE COMPUTATIONSGiven:Actual Value of Property: P1,000,000Borrower's Equity: 30%Loanable Amount: 70%

Bank Loan interest: 9.25%

Amortization Factor: .0116637.

How much monthly amortization?

12/17/2015Real Estate Finance by Maya Cartojano REC, REA, REB 34

MONTHLY AMORTIZATION

Contract Price: = P1,000,000

less Equity: 30% 300,000

Balance 700,000multiply Factor: 0.0116637

Monthly Amortization P8,164.59

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 35/56

Real Estate Finance Tools:

Present Value and MortgageMathematics

Real Estate Finance by Maya Cartojano REC, REA, REB 12/17/2015 35

Major Topics

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 36/56

Major Topics

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ Time value of money calculations

♦ Present value of a single sum or annuity payment

♦Future value of a single sum or annuity

♦ Mortgage loan constants

♦ Mortgage balance calculations

♦ Point charges and their effects on borrowing costs or yields

♦ Annual Percentage Rate

♦ Effective Cost of Borrowing♦ Net present value and IRR calculations

♦ Refinancing decisions

♦ Adjustable Rate Mortgage or ARM Calculations

♦ Price Level Adjusted Mortgage

♦ Reverse Annuity Mortgages (Future Value of Annuity)♦ Supportable mortgage calculations

12/17/2015 36

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 37/56

Introduction to the Time

Value of Money

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ A peso today is worth more than a pesoreceived in future

♦ In most economies we expect a return

on money or capital related to theproductivity of things capital can buy

♦ This is the fundamental source of thereal returns (not just inflationary

increases)♦ The required returns are cumulatively

known as the opportunity cost ofcapital

12/17/2015 37

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 38/56

Present & Future Value of a Single Sum

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ PV = FV / (1+r)

♦ FV = PV (1+r)

♦ PV is the present value

♦ FV is future value

♦ r is the total expected rate of return▪ r includes the risk free and risk

premium rates

▪ r is called “discount rate” when solving

for PV

▪ r is called “rate of return” when solving

for FV

12/17/2015 38

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 39/56

PV & FV over MultiplePeriods of Time

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ General formula for PV and FV acrossmultiple periods:

♦ PV = FV / (1+r)N

♦ FV = PV (1+r)N

♦ N is the number of periods between FV andPV

♦ If FV and PV are known the rate of returncan be found by the formula:

r = (FV/PV) 1/N – 1

12/17/2015 39

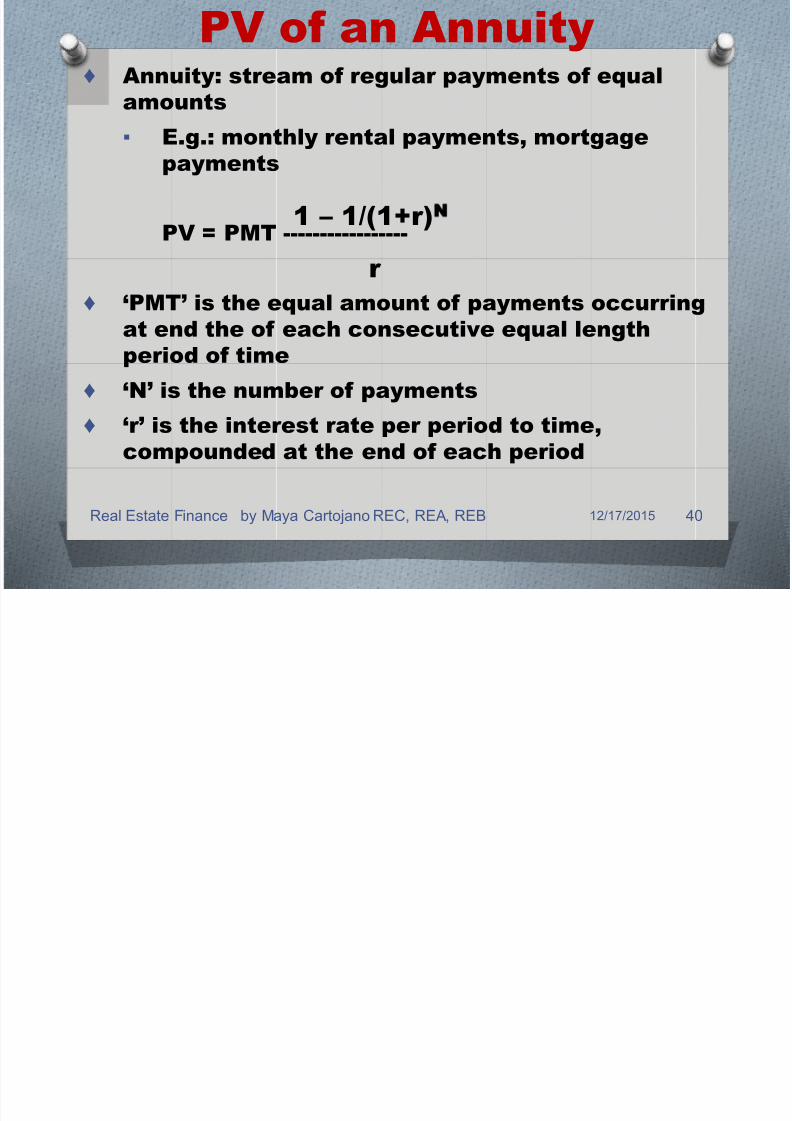

PV of an Annuity

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 40/56

PV of an Annuity

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ Annuity: stream of regular payments of equalamounts

▪ E.g.: monthly rental payments, mortgagepayments

PV = PMT -----------------

♦ ‘PMT’ is the equal amount of payments occurring

at end the of each consecutive equal lengthperiod of time

♦ ‘N’ is the number of payments

♦ ‘r’ is the interest rate per period to time,compounded at the end of each period

1 – 1/(1+r)N

r

12/17/2015 40

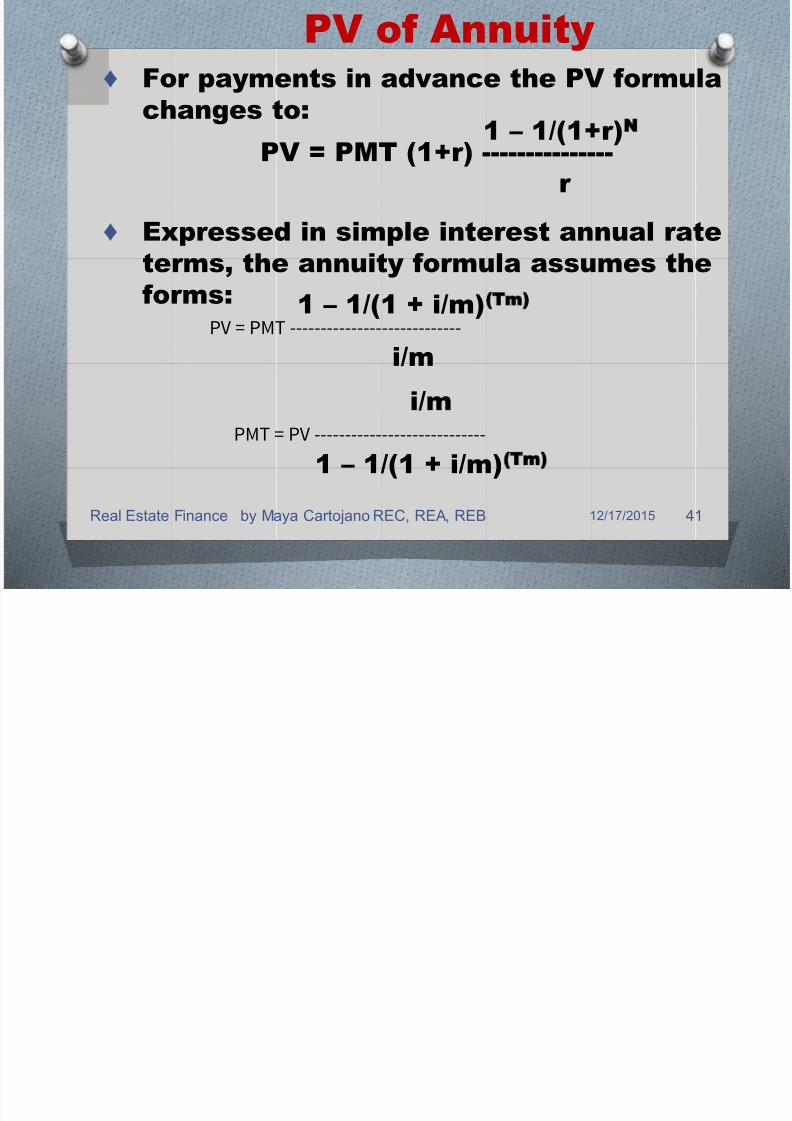

PV of Annuity

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 41/56

PV of Annuity

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ For payments in advance the PV formulachanges to:

PV = PMT (1+r) ---------------

♦ Expressed in simple interest annual rateterms, the annuity formula assumes theforms:

1 – 1/(1+r)

N

r

PV = PMT ----------------------------1 – 1/(1 + i/m) Tm)

i/m

PMT = PV ----------------------------

i/m

1 – 1/(1 + i/m) Tm)

12/17/2015 41

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 42/56

Real Estate Finance by Maya Cartojano REC, REA, REB

Mortgage Constant

♦‘MMC’ is the monthly mortgage constant

♦It is the monthly payment per dollar of loan and it

includes both interest and principal amortization

MMC = ------------------

♦Here N & r are in months

r

1 – 1/(1+r)N

12/17/2015 42

Calculating a Loan Balance

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 43/56

Calculating a Loan Balance

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ Outstanding Loan Balance (OLB) equalsthe present value of the remaining loanpayments

♦ Original mortgage was for ‘T’ years at a

rate of ‘i’

♦ If ‘q’ payments have been made, the

formula will be:

OLB = PMT ----------------------------

OLB = PMT ----------------------------

(with m=12)

1 – 1/(1 + i/m) mT-q)

i/m

1 – 1/(1 + i/12) 12T-q)

i/12

12/17/2015 43

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 44/56

Calculating the Principal and InterestSeparation of a Mortgage

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ Example: A P150,000 30yr mortgage at 9%

12/17/2015 44

Future Value of an Annuity

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 45/56

Future Value of an Annuity

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ The FV of an annuity is the result of equalpayments compounding over time at a given

interest rate♦ Used in RAM (Reverse Annuity Mortgage)

♦ Formula:

FV = PMT -----------------

♦ ‘PMT’ is the annuity paid every month

♦ ‘r’ is the interest per period (month)

♦ ‘n’ is the number of months

(1+r)N – 1

r

12/17/2015 45

Calculating Yields or Borrowing Costs

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 46/56

Calculating Yields or Borrowing Costs

Real Estate Finance by Maya Cartojano REC, REA, REB

Recap of terms:

♦ Contract interest rate♦ Index♦ Spread♦ Prime♦ Prime Rate of Interest♦ Discount Rate♦ Carry cost♦ Effective or true cost of borrowing♦ Effective yield

♦ Contract rate♦ Points♦ Yield

12/17/2015 46

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 47/56

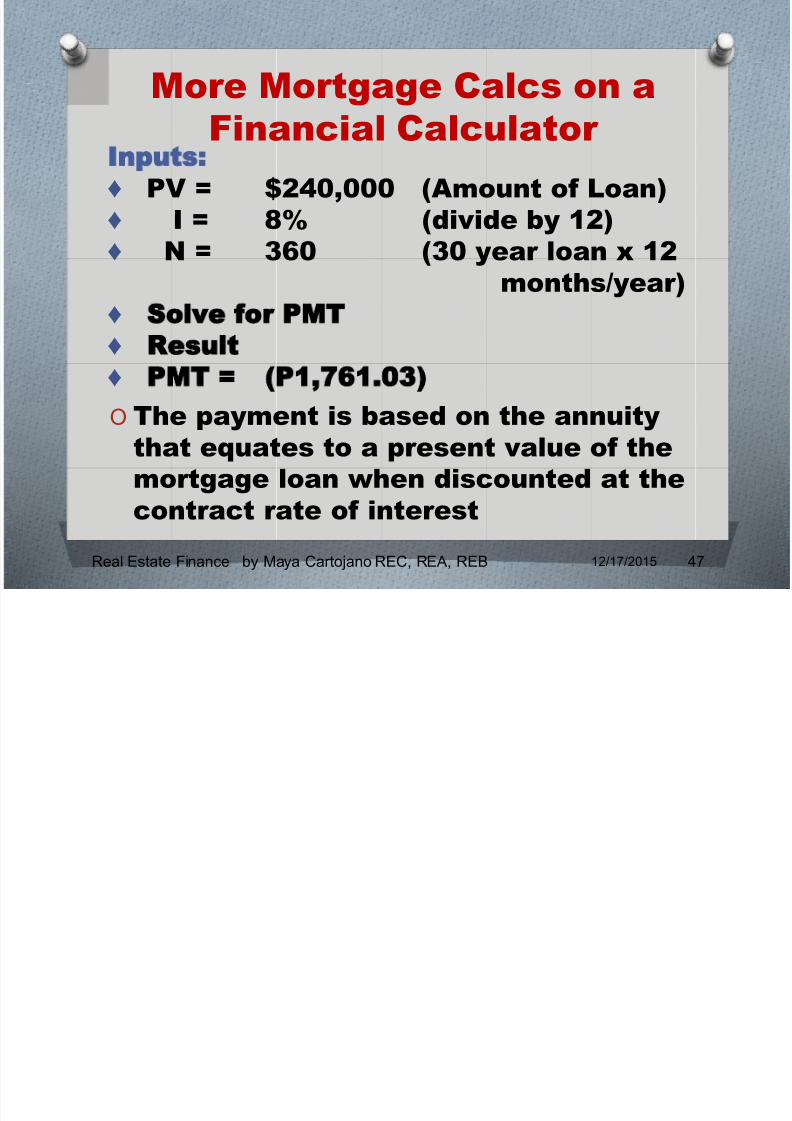

More Mortgage Calcs on a

Financial Calculator

O The payment is based on the annuitythat equates to a present value of themortgage loan when discounted at thecontract rate of interest

Real Estate Finance by Maya Cartojano REC, REA, REB

Inputs:

♦ PV = $240,000 (Amount of Loan)♦ I = 8% (divide by 12)♦ N = 360 (30 year loan x 12

months/year)♦ Solve for PMT

♦ Result

♦ PMT = P1,761.03)

12/17/2015 47

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 48/56

Effective Yield Calculation

Real Estate Finance by Maya Cartojano REC, REA, REB

Loan Amount is P240,000 with 1.5 points andprepayment expected in 10 years withoutpenaltyStep 1: Calculate actual loan amountLoan Amount Disbursed

= P240,000 – 1.5%(240,000)= P236,400 netStep 2: Calculate loan balance due at end of 10yearsPMT = (P1,761.03)

I = 8% (convert to monthly)N = 240 (Months Remaining on the loan)Compute

PV = P(210,539) (Use as FV input)

12/17/2015 48

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 49/56

Effective Yield Calculation

Real Estate Finance by Maya Cartojano REC, REA, REB

Step 3: Calculate the lender's yield on theamount disbursed, considering earlyrepaymentEnter PV = P 236,400

Enter PMT = P(1,761.03)Enter N = 120 (The expected time untilprepayment)

Enter FV = P (210,539)Compute I = 8.23%

This is the effective cost of borrowing

12/17/2015 49

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 50/56

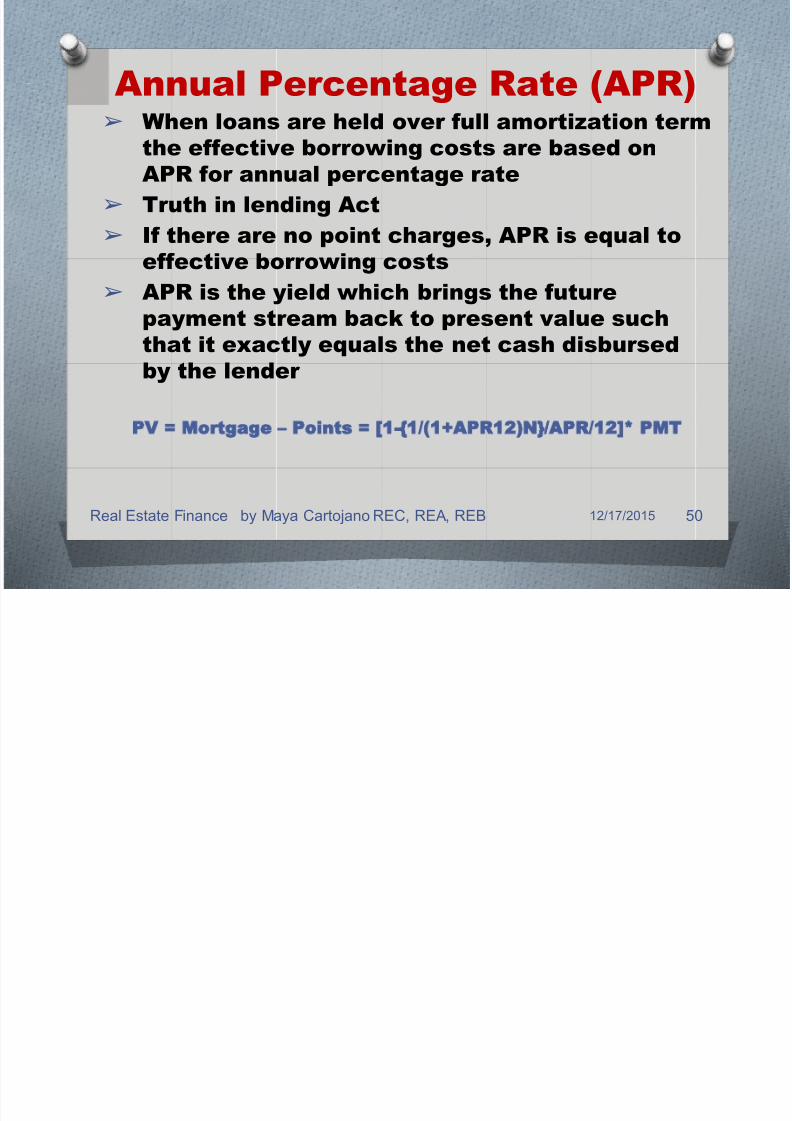

Annual Percentage Rate (APR)

Real Estate Finance by Maya Cartojano REC, REA, REB

➢ When loans are held over full amortization term

the effective borrowing costs are based onAPR for annual percentage rate

➢ Truth in lending Act

➢ If there are no point charges, APR is equal toeffective borrowing costs

➢ APR is the yield which brings the futurepayment stream back to present value suchthat it exactly equals the net cash disbursedby the lender

PV = Mortgage Points = [1-{1/ 1+APR12)N}/APR/12]* PMT

12/17/2015 50

Points – A tool to increase Yield

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 51/56

Points A tool to increase Yield

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ Lender’s perspective: Decrease contractrate (looks attractive to borrower) andincrease points to compensate for it

♦ Question: How many points are needed tobring a mortgage yield up given thecontract rate is lower than required yield?

♦ Steps (using business calculator)

▪ Find monthly payment and input as PMT

▪ Find mortgage balance (consideringpayout) input as FV

▪ Input monthly interest rate (Requiredyield/12)

▪ Input the number of periods

▪ Compute for PV

▪ Loan amount – PV will give the points

12/17/2015 51

Mortgage Pricing

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 52/56

Mortgage Pricing

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ Which loan is best for a borrower depends onthe expected tenure or time they expect tohold the loan

♦ The 7.5% loan with 7 points is better if theborrower is fairly certain they will hold theloan for more then 10 years and if they don’t

believe rates will come down allowing themto refinance before 10 years

♦If the borrower is uncertain about holdingperiods or future rates, the 8.6% loan is thebest choice with the lowest cost for anythingunder a 10 year hold

12/17/2015 52

ARM and FRM

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 53/56

ARM and FRM

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ Fixed Rate Mortgage (FRM), where therate of interest charged remains

constant throughout the term♦ Adjustable Rate Mortgage (ARM),

where the rate of interest and hencethe mortgage payment is variable due

to the link with an index♦ Spread is the amount above the index

that is added to determine the newcontract rate of interest

♦ Typically ARMs are priced atsignificantly lower interest rates asmuch of the future interest rate risk isborne by the borrower

12/17/2015 53

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 54/56

ARM and FRM

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ Annual rate caps is the maximum increase inthe rate that is possible per year

♦ Life time caps is the maximum total increasein the rate that is possible during the loanterm

♦ A 1.0% to 2.0% annual rate cap is common

♦ Typical life caps are 5% or 6% over thecourse of the loan, so a loan that starts at 6%can never be higher then 11% if the life cap is5%

♦ To calculate the new payment we first needthe balance of the loan and then we use thisbalance over the remaining term or N tocalculate payments at the new rate

12/17/2015 54

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 55/56

Choosing b/w FRMs and ARMs

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ FRM interest rate risk is borne by lender

♦ With ARMs much of the interest rate risk isborne by the borrower

♦ Borrowers who are just able to qualify for the

mortgage with little excess in their budget forthe risk of higher payments will often opt for theFRM, while wealthier borrowers with fewliquidity concerns will often opt for the ARMS

♦ Rather than lower aspirations many households

will start to consider taking on the risk of anARM as rate rise and the spread in the marketbetween FRMs and ARMs increases

12/17/2015 55

7/23/2019 4 Real Estate Finance Mbc Dec2015

http://slidepdf.com/reader/full/4-real-estate-finance-mbc-dec2015 56/56

Refinancing

Real Estate Finance by Maya Cartojano REC, REA, REB

♦ Refinancing can save borrower money if

there is a drop in mortgage interest rates♦ Situations when refinancing is not advisable:

▪ Remaining term of the loan is short orexpected tenure with new loan is short

▪ Mortgage rates are expected to further

drop▪ Prepayment penalties are higher than

benefits

♦ Deciding whether refinancing is profitable ornot:

▪ NPV of expected savings exceeds thecost of refinancing then it is advisableand vice-versa

12/17/2015 56