Languages

Pages

Legal

20-1

Corporations: Formation and CapitalStock Transactions

Corporations: Formation and CapitalStock Transactions

Section 1: Forming a Corporation

Chapter

20

Section Objectives

1. Explain the characteristics of a corporation.

2. Describe special “hybrid” organizations that have some characteristics of partnerships and some characteristics of corporations.

McGraw-Hill © 2009 The McGraw-Hill Companies, Inc. All rights reserved.

20-3

Created by corporate charter issued by state government.

Can enter into contracts and own property.

Can have few or many owners.

Can be privately held or publicly held.

Explain the characteristics ofa corporation

Objective 1

20-4

Advantages Disadvantages

Ease of raising capital

Limited liability

Restricted agency

Continuous existence

Transferability of ownership rights

Corporate income tax

Governmental regulation

Corporations

20-5

Subchapter S corporation.

Limited liability partnership (LLP).

Limited liability company (LLC).

“Hybrid” Business Entities

Hybrid entities have characteristics of partnerships and corporations.

Describe special “hybrid” organizations

Objective 2

20-6

Known as S corporation.

Meets Subchapter S requirements of Internal Revenue Code to be treated as a partnership.

Subchapter S Corporation

Shareholders include their share of corporate profits on their individual tax returns.

The S corporation does not pay income taxes.

20-7

Partners are responsible and have liability for their own actions and actions of those they control or supervise.

Partners are not liable for the actions or malfeasance of another partner.

Limited Liability Partnership (LLP)

20-8

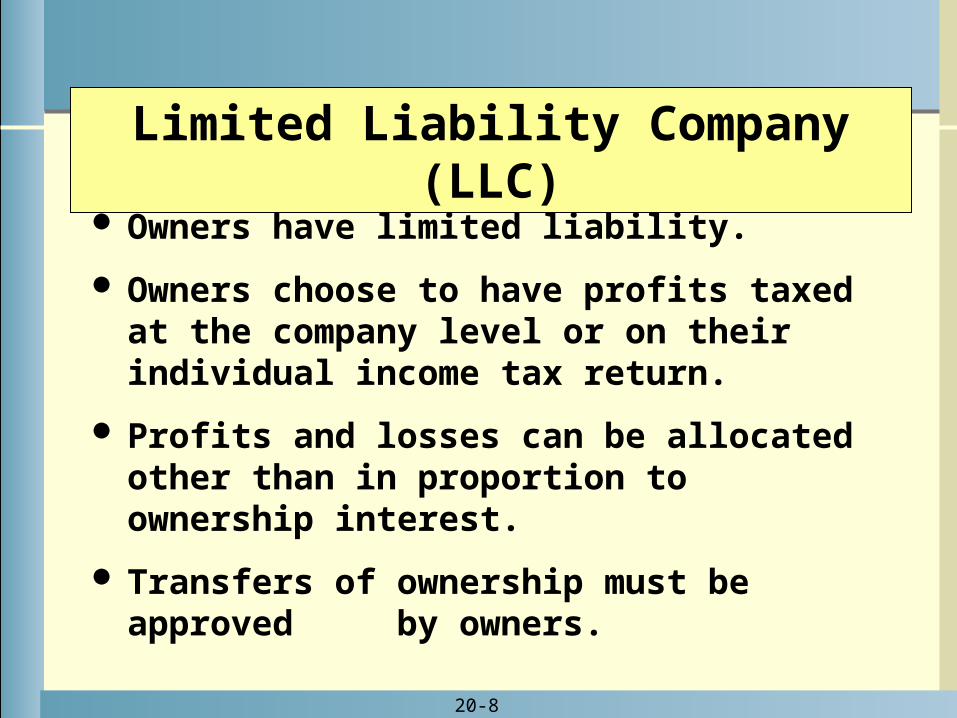

Limited Liability Company (LLC)

Owners have limited liability.

Owners choose to have profits taxed at the company level or on their individual income tax return.

Profits and losses can be allocated other than in proportion to ownership interest.

Transfers of ownership must be approved by owners.

20-9

After a Corporate Charter Is Issued

Shareholders elect permanent directors.

Directors or shareholders approve bylaws.

Board selects corporate officers.

Shares are issued to individuals who have paid full purchase price of the stock.

Organizers elect an acting board of directors.

Officers hire employees and begin operations.

Corporations: Formation and CapitalStock Transactions

Corporations: Formation and CapitalStock Transactions

Section 2: Types of

Capital Stock

Chapter

20

Section Objectives

3. Describe the different types of stock.

4. Compute the number of shares of common stock to be issued on the conversion of convertible preferred stock.

5. Compute dividends payable on stock.

McGraw-Hill © 2009 The McGraw-Hill Companies, Inc. All rights reserved.

20-11

Capital Stock

Authorized shares: The number of shares that can be sold.

Issued shares: The number of shares that have been sold.

Outstanding shares: The number of shares still in circulation.

Outstanding stock = Issued stock – Treasury stock

20-12

The price per share at which stock is bought and sold.

Specified in the corporate charter and assigned to each share of stock for accounting purposes.

A value assigned to no-par stock by the board of directors for accounting and legal purposes.

Par Value

Stated Value

Market Value

Capital Stock Values

20-13

Common Preferred

Stock Classes

If there is only one class of stock, common stock is issued. Each share carries the same rights and privileges as every other share.

Preferred stock has special claims on a corporation’s profits or, in case of liquidation, corporate assets.

Describe the different types of stock

Objective 3

20-14

Compute the number of shares of common stock to be issued on the conversion of convertible preferred stock.

Objective 4

20-15

Owners have the right to convert their shares into common stock after a specified date.

Convertible Preferred Stock

400 shares of preferred, with a 1:2 conversion ratio equals 2 shares of common for each share of preferred.

The number of shares of common stock into which a preferred stock can be converted.

ConversionRatio

Example:

400 X 2 = 800 shares of common stock

20-16

Dividends are distributions of the profits of a corporation to its shareholders.

ANSWER:

QUESTION:

What are dividends?

The board of directors declares dividends.

Compute dividends payable on stock

Objective 5

20-17

Dividend Rights on Preferred Stock

Cumulative preferred stock

Noncumulative preferred stock

Nonparticipating preferred stock

Participating preferred stock

20-18

Cumulative Preferred Stock

Has right to receive preference dividend each year before any dividend can be paid on common stock.

If dividend is passed (not paid) in one year, the amount not paid carries over and must be fully paid in a subsequent year before any dividend can be paid on common stock.

20-19

Noncumulative Preferred Stock

Has right to receive preference dividend each year before any dividend can be paid on common stock.

Stockholders have no rights to dividend for years in which none were declared.

20-20

Nonparticipating Preferred Stock

Has right to receive preference dividend each year before any dividend can be paid on common stock.

Does not have the right to any dividend in excess of the preference dividend.

20-21

Participating Preferred Stock

Has right to receive preference dividend each year before any dividend can be paid on common stock.

After common shareholders have received specified amount, preferred and common stock share in further dividends.

20-22

Common Stock

Common stockholders receive remaining dividends only after dividends have been paid on preferred stock in accordance with contractual obligations.

20-23

Dividend Calculations

The following slides show three scenarios:

A. Only common stock issued and 5 percent dividend declared.

B. Common stock and noncumulative, nonparticipating preferred stock issued and $20,000 dividend declared.

C. Common stock and noncumulative, nonparticipating preferred stock issued and $9,000 dividend declared.

20-24

Scenario A: 15,000 shares issued, authorized, and outstanding $50 par value 5% dividend declared

QUESTION:

What is the dividend calculation?

ANSWER:

15,000 shares

X $ 50 par value

$ 750,000

X 0.05 dividend declared $ 37,500 total dividends

Only Common Stock Issued

20-25

Preferred Stock, noncumulative, nonparticipating

(10%, $50 Par Value, 1,000 Shares) $ 50,000

Common Stock ($20 Par Value, 10,000 Shares) 200,000

Total Capital Stock $250,000

Dividend declared $ 20,000

Scenario B:

Common and Noncumulative, Nonparticipating Preferred Stock Issued

Dividend per share for common stock = $15,000 ÷ 10,000 shares = $1.50

Remaining dividend to common stockholders $ 15,000

Dividend due to preferred stockholders

(1,000 Shares x $50 x 10%) $ 5,000

20-26

Dividend declared $ 9,000

Scenario C:

Dividend due to preferred stockholders:

Dividends in arrears $ 2,000

(1,000 Shares x $50 x 10%) $ 5,000

Common and Cumulative, Nonparticipating Preferred Stock Issued when $2,000 of preferred dividends are in arrears.

Dividend per share of common stock is $2,000 ÷ 10,000 shares = $0.20

Remaining dividend to common stockholders $ 2,000

Preferred Stock, noncumulative, nonparticipating

(10%, $50 Par Value, 1,000 Shares) $ 50,000

Common Stock ($20 Par Value, 10,000 Shares) 200,000

Total Capital Stock $250,000

20-27

Capital Stock on the Balance Sheet Capital Stock on the Balance Sheet

Capital stock represents the equity in a corporation.

Common stock and preferred stock are reported separately.

Since the owners of a corporation are stockholders, the equity section of the balance sheet is titled “Stockholders’ Equity.”

Corporations: Formation and Capital

Stock Transactions

Corporations: Formation and Capital

Stock Transactions Section 3: Recording

Capital Stock Transactions

Chapter

20

Section Objectives6. Record the issuance of capital stock at par value.7. Prepare a balance sheet for a corporation. 8. Record organization costs.9. Record stock issued at a premium, and stock with

no par value. 10. Record transactions for stock subscriptions.11. Describe the capital stock records for a corporation.

McGraw-Hill © 2009 The McGraw-Hill Companies, Inc. All rights reserved.

20-29

Cash

Noncash assets

Services rendered

Recording the Issuance of Stock

Stock is issued after the purchaser has paid for it in full with one of the following:

Record the issuance of capital stock at par value

Objective 6

20-30

Stock Issued at Par Value for Cash

When stock is issued for cash equal to the par value of the shares, cash proceeds are credited to the capital stock account.

20--

Dec. 31 Cash ($15,000 + $40,000) 55,000.00

Common Stock (600 X $25) 15,000.00Preferred Stock (400 X $100) 40,000.00

Issuance of stock to Karen Wilcox: 600 shares of common at par ($25 per share) and 400 shares ofpreferred at par ($100 per share).

20-31

The net value of assets transferred is the sum of all noncash assets less liabilities (such as Accounts Payable).

Noncash assets include:

Merchandise Inventory Land Building Equipment and Fixtures Accounts Receivable

Stock Issued at Par Value for Noncash Assets

The Allowance for Doubtful Accounts is recorded separately.

20-32

Preparing a Balance Sheet for a Corporation

Camping Supply Center, Inc.Balance Sheet (Partial)

December 31, 20--

Liabilities and Stockholders’ Equity:

Current Liabilities Accounts Payable $19,200.00

Stockholders’ Equity Preferred Stock (10%, $100 par value, 8,000 shares authorized) At Par Value (1,600 shares issued) $160,000.00 Common Stock ($25 par value, 40,000 shares authorized) At Par Value (5,300 shares issued) 132,500.00 Total Stockholders’ Equity 292,500.00 Total Liabilities and Stockholders’ Equity $311,700.00

Objective 7

20-33

Organization costs are charged to an intangible asset account and then amortized over a period of time.

20--

Dec. 31 Organization Expenses 2,000.00

Cash 2,000.00Payment of legal fees, charter fee, and cost of printing stock certificates.

Record organization costsObjective 8

20-34

When stock is issued for more than its par value, it is issued at a premium.

Premiums on stock are usually credited to an account titled Paid-in Capital in Excess of Par Value.

Separate accounts are set up for different classes of stock.

20--

Mar. 2 Cash 42,000.00Preferred Stock 40,000.00Paid-in Capital in Excess of Par Value—Preferred Stock 2,000.00

Issuance of 400 sharesfor $105 per share

Record stock issued at a premium and stock with no par value

Objective 9

20-35

Recording Rules for Par and No-Par Stock

Par-Value Stock No-Par-Value Stock

Stated Value No Stated Value

Par value is specified in corporate charter.

Stock certificate indicates par value.

Stated value is assigned by directors. Corporate charter indicates that stock is no-par-value stock.

Stock certificate does not generally show stated value.

Corporate charter indicates that stock is no-par-value stock.

Stock certificate shows that stock is no-par-value stock.

20-36

Recording Rules for Par and No-Par Stock (cont.)

Par-Value Stock No-Par-Value Stock

Stated Value No Stated Value

Change in par value requires revision of charter.

On issue of stock, par value is credited to capital stock account.

Stated value can be changed by directors.

On issue of stock, stated value is credited to capital stock account.

On issue of stock, entire proceeds are credited to capital stock account.

20-37

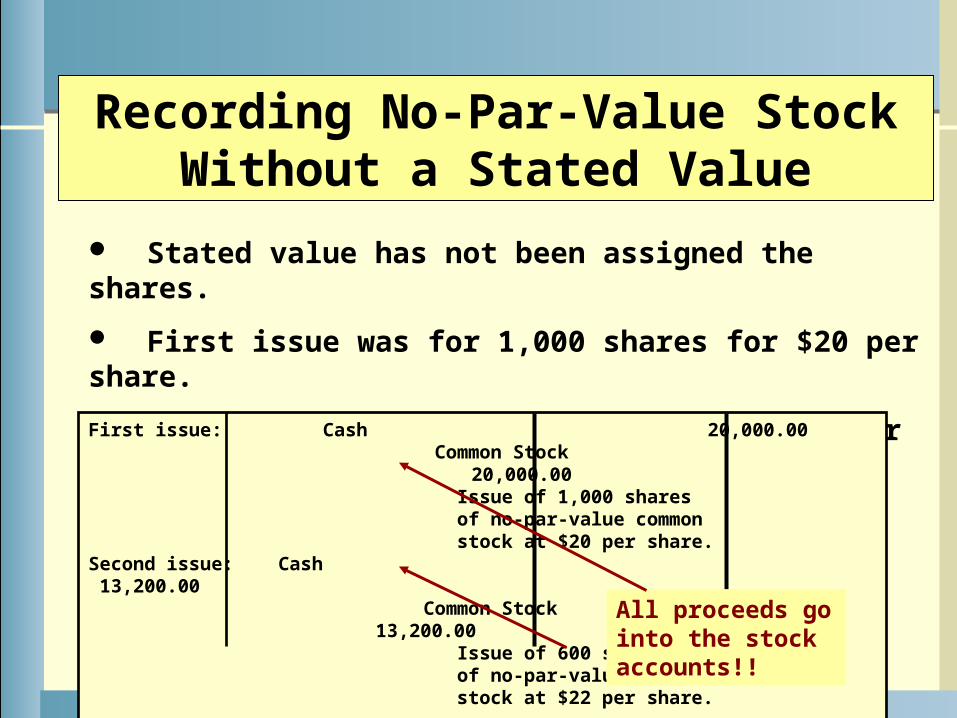

Stated value has not been assigned the shares.

First issue was for 1,000 shares for $20 per share.

Second issue was for 600 shares for $22 per share.

Recording No-Par-Value Stock Without a Stated Value

First issue: Cash 20,000.00 Common Stock 20,000.00 Issue of 1,000 shares of no-par-value common stock at $20 per share.Second issue: Cash 13,200.00 Common Stock 13,200.00 Issue of 600 shares of no-par-value common stock at $22 per share.

All proceeds go into the stock accounts!!

20-38

2,400 X $25 = $60,000

Cash 62,400.00 Common Stock 60,000.00 Paid-in Capital in Excess

of Stated Value 2,400.00 Issued 2,400 shares of

common stock at $26 per share.

Sold 2,400 shares of stated value $25 per share stock for $26 per share.

Stated value is credited to the capital stock account—just like par.

Recording No-Par-Value Stock With a Stated Value

20-39

Subscriptions for Capital Stock

Stockholder signs a subscription contract. (It details stock price and payment plan.)

Stockholder pays for stock at a later date.

Stockholder receives stock when payment is made.

Record transactions for stock subscriptions

Objective 10

20-40

A stock subscription gives the corporation a receivable from the subscriber and an obligation to hold enough stock for issue when the subscription is paid in full.

20--

May 1 Subscriptions Receivable—Common 20,000.00Common Stock Subscribed 20,000.00

Subscription from Tyrone Coles to buy 400 shares of common stock at par value of $50 per share.

The Common Stock Subscribed account appears in the Stockholder’s Equity section of the Balance Sheet. It will remain there until the stock is actually issued.

20-41

The stock is issued when full payment has been received for the subscription.

20--

June 1 Cash 20,000.00Subscriptions Receivable—Common 20,000.00

Received Tyrone Coles’ subscription in full.

Common Stock Subscribed (400 shares) 20,000.00Common Stock (400 shares) 20,000.00

Issued 400 shares ofcommon stock to Tyrone Cole.

1

20-42

Special Corporation Records and Agents

Corporations keep detailed records of stockholders’ equity and special corporate records such as:

Meeting minutes

Corporate bylaws

Stock certificate books

Stock ledgers

Stock transfer records

Describe the capital stock records for a corporation

Objective 11

20-43

Thank Youfor using

College Accounting, 12th Edition

Price • Haddock • Farina

Top Related