![Business Model and Introduction to Digital Metricspalmeida/Balanceamento_Jogos_15_16/Farley_Aula2_BMC.pdf · Agenda [1/2] Recap Business model Business model canvas Lean Canvas Introduction](https://static.fdocuments.in/doc/165x107/5c5fb10209d3f26c398b466c/business-model-and-introduction-to-digital-palmeidabalanceamentojogos1516farleyaula2bmcpdf.jpg)

Languages

Pages

Legal

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Capital Markets Day

Introduction &

strategic recap

CEO Terje Mjøs

1

11 June 2014

Overall agenda CMD

Introduction

2

Capital Markets Day 2014

08:30 – 09:00

09:00 – 09:30

09:30 – 10:00

10:00 – 10:30

10:30 – 10:45

10:45 – 11:15

11:15 – 11:45

11:45 – 12:15

12:15 – 13:00

13:00 – 14:00

14:00

| Registration & breakfast

| Welcome & introduction, Terje Mjøs, CEO

| Market dynamics, Terje Mjøs, CEO and Stig Mjølsnes, IT-advisor

| Financial services growth, Wiljar Nesse, EVP Financial Services

| Coffee break

| Selected Industries growth,

Anne-Cecilie Fagerlie, EVP Industries Norway and Niclas Ekblad, EVP EVRY Sweden

| SME Regions growth, Kurt Helland, EVP Regions Norway

| Managed Services growth, Lars Ringvold, SVP Future Proof and Robin Blomquist, SVP EVRY Mobility

| Lunch

| Financials and guiding, Terje Mjøs, CEO and Morten Frogner, acting CFO

| Q&A

Long-standing frame agreement is renewed

SpareBank 1 agreement

3

Capital Markets Day 2014

TCV NOK 2.0 bn• 4 years from 1.1 2015

• Option for further 2+2 years

• SpareBank 1 will migrate to EVRY`s next generation banking platform

Ready to launch next generation core bank and payment solutions• SpareBank 1 will be our first customer

• Significant Nordic growth potential

EVRY – the most local IT company in the Nordics

Introduction

4

Capital Markets Day 2014

# 1 Total market share 31%

# 1 Bank & finance 56%

# 1 SME segment 22%

# 1 Outsourcing 37%

# 1 Consulting 20%

# 4 Total market share 7.5%

# 1 SME segment 17%

# 5 Outsourcing 6%

# 3 Consulting 7.5%

Finland: SME-focus

Denmark: SAP-focus

Latvia: Nearshore Help Desk

India: Offshore Operations & AD/AM

Ukraine: Offshore AD/AM

Global sourcingNorway

Sweden

5

Capital Markets Day 2014

A part of everyday life for millions of Nordic citizens

Introduction

When you

• receive a package notification via SMS from the Post

• withdraw cash from an ATM in Norway or Sweden

• are being credit evaluated

• receive the tax assessment from the Norwegian tax authority

• pass a toll road station

• do a lookup in the national register of motor vehicles

• use your credit card or mobile banking services

• pick up an e-prescription at an Norwegian pharmacy

• buy a ticket with the Swedish railways

EVRY`s organisation and executive management

Introduction

6

Capital Markets Day 2014

*) Global Sourcing managed from Corporate Development, reported in Norway segment

Norway SwedenFinancial

Services

Reporting

segment

Business Area

Nordic Operations

Financial

Services

Global Sourcing*

Regions/ SME

Norway

Industries

Norway

Industries

Sweden

Regions/ SME

Sweden

EVRY Financial Services content and figures

Segment introduction

7

Capital Markets Day 2014

Revenue distribution

MarketshareKey figures

3 554 MNOK1 490 Employees 9 Offices

24%

75%

UK

Nordic

Norway

13%

26%58%

4%

OperationsBanking services

Card servicesCustom solutions

0

10

20

30

40

50

60

Total market Banking

0

5

10

15

20

Banking

SwedenNorway

1.000

1.500

2.000

2.500

3.000

3.500

4.000

7%

1Q

2013

1Q

2014

1Q

2012

1Q

2011

Revenue LTM

(MNOK) YoY average

Total market

Source: Gartner & IDC

Revenue distribution

Marketshare

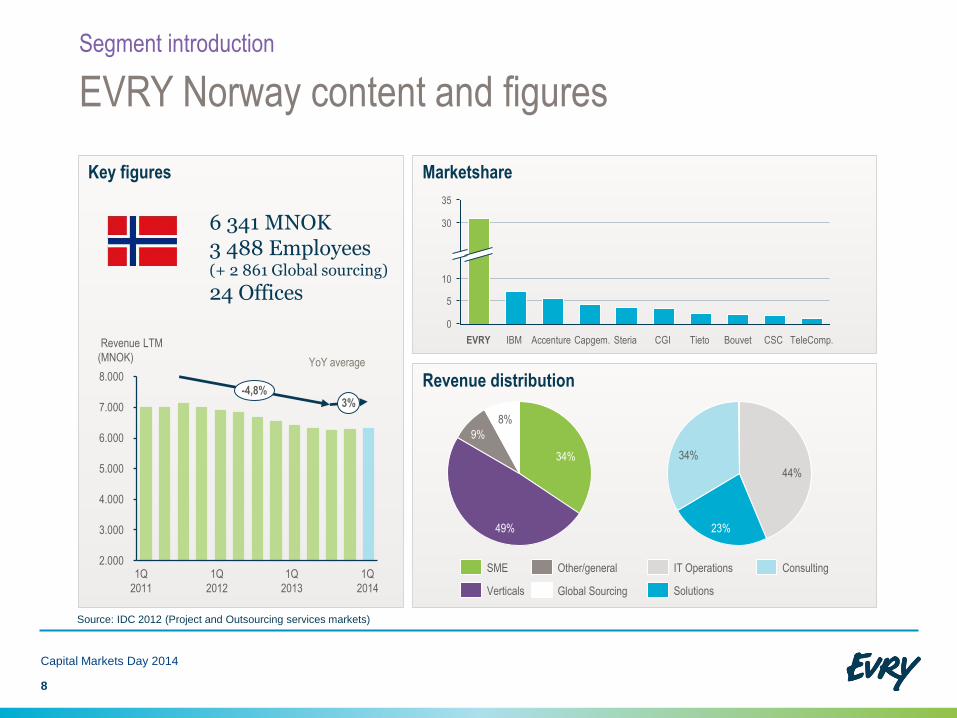

EVRY Norway content and figures

Segment introduction

8

Capital Markets Day 2014

Key figures

8%

9%

49%

34%

44%

34%

23%

5

0

10

30

35

TeleComp.CSCBouvetTietoCGISteriaCapgem.AccentureIBMEVRY

6 341 MNOK3 488 Employees(+ 2 861 Global sourcing)

24 Offices

2.000

3.000

4.000

5.000

6.000

7.000

8.000-4,8%

3%

1Q

2013

1Q

2014

1Q

2011

1Q

2012

YoY average

Source: IDC 2012 (Project and Outsourcing services markets)

Other/general

Verticals

SME

Solutions

ConsultingIT Operations

Global Sourcing

Revenue LTM

(MNOK)

Key figures

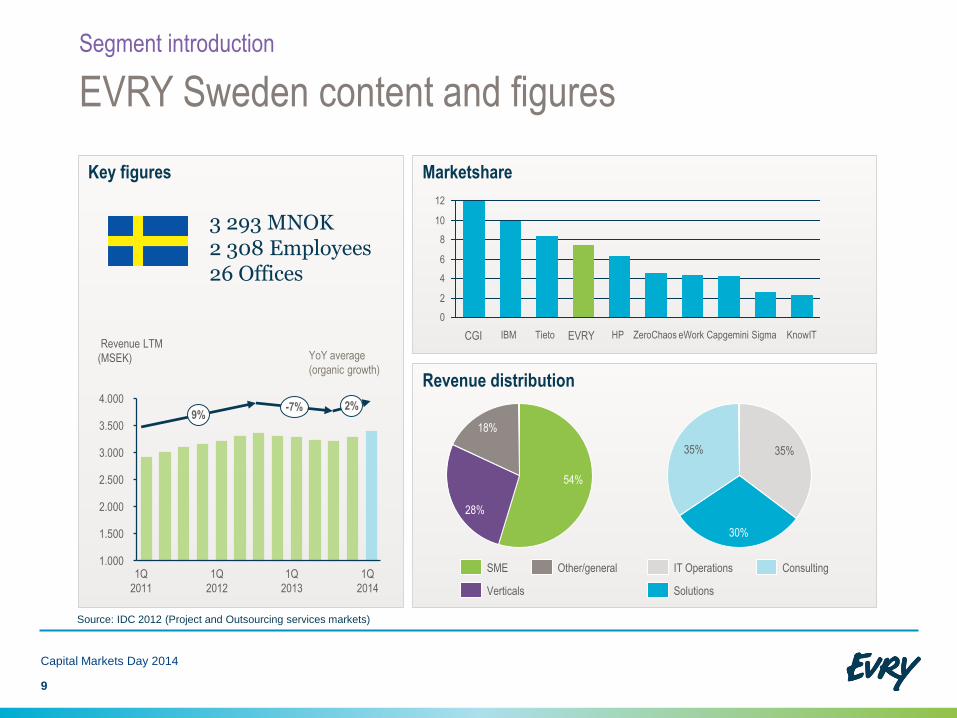

EVRY Sweden content and figures

Segment introduction

9

Capital Markets Day 2014

Revenue distribution

Marketshare

3 293 MNOK2 308 Employees 26 Offices

Source: IDC 2012 (Project and Outsourcing services markets)

Other/general

Verticals

SME

Solutions

ConsultingIT Operations

18%

28%

54%

30%

35%35%

0

2

4

6

8

10

12

KnowITSigmaCapgeminieWorkZeroChaosHPEVRYTietoIBMCGI

1.000

1.500

2.000

2.500

3.000

3.500

4.0002%-7%

9%

YoY average

(organic growth)

1Q

2013

1Q

2014

1Q

2011

1Q

2012

Revenue LTM

(MSEK)

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Strategic recap

EVRY

1

0

A majority of our business grows faster than the market

Strategic recap

11

Capital Markets Day 2014

Sweden geography Financial Services

SME IT-Operations

5

2

3

1

0

4

+4%

+8%

2013201220112010

SEK billion

0,5

1,0

1,5

0,02010 2011 20132012

NOK billion

+9%

3,0

1,5

0,5

0,0

1,0

2,5

2,0

NOK billion

2010

+4%

2011 20132012

CAGR

CAGR

CAGR

Structured approaches to quality

Action taken – major quality improvement

for core bank clients

Strategic recap

12

Capital Markets Day 2014

Critical incidents significantly reduced

18

36

124

161

Target

2014

2011

-89%

20132012

LEAN

Renovated coreinfrastructure

“Customer HSE”(implemented safety measures

from oil&gas industry)

Improved EBITA and changed business mix & risk

Strategic recap

13

Capital Markets Day 2014

* Global oriented enterprise (single engagements ) as part of Group revenue

EBITA improvements and enhanced cost control

Better business mix & reduced exposure

Q1

2011

Q1

2014

Q1

2013

Q1

2012

21,0%17,0% 14,0%

7,0%

2016 est.201320102008

EBITA

(LTM)

IT Operations Enterprise customers

• Synergies according to plan

• Procurement effects

• Pension liabilities

• Reduced overhead

• New HQ effects

• Reduced dependency of global oriented enterprise customer

• SME & Solutions share of revenue increasing

• Reduced exposure through issues resolved (eg ERV, City of Oslo, Pension conflict)

753749733714680685671690681663

555

481501

400

500

600

700

800

+272

14

Capital Markets Day 2014

Transition completed - ready to accelerate growth

Strategic recap

Cost base

Working capital

Quality

Business mix

Reduced risk

.......

Growth

Market dynamics

CEO Terje Mjøs and IT-advisor Stig Mjølsnes

11 June 2014

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

1

5

16

Capital Markets Day 2014

The World is Changing… …and it’s changing fast

Market dynamics

Disruptive forces in play

IT-services eats products

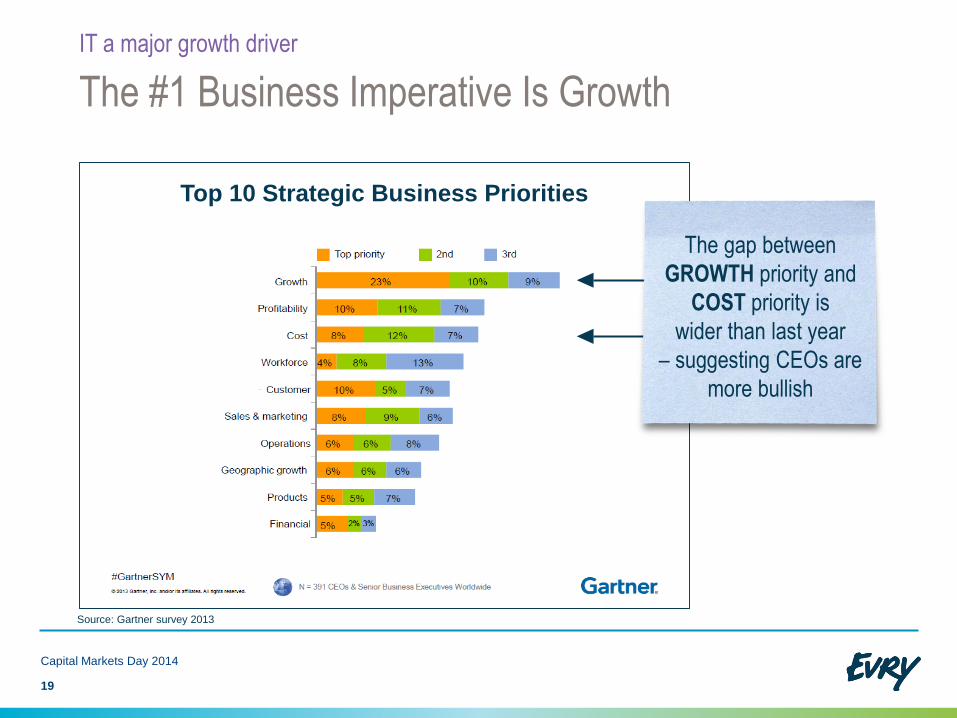

IT a major growth driver

17

Capital Markets Day 2014

Unprecedented growth rates with new technologies

Disruptive forces

18

Capital Markets Day 2014

The World is Changing… …and it’s changing fast

Market dynamics

Disruptive forces in play

IT-services eats products

IT a major growth driver

The #1 Business Imperative Is Growth

Top 10 Strategic Business Priorities

IT a major growth driver

19

Capital Markets Day 2014

Source: Gartner survey 2013

The gap between

GROWTH priority and

COST priority is

wider than last year

– suggesting CEOs are

more bullish

20

Capital Markets Day 2014

Technology is shaping the future of the enterprise

IT a major growth driver

Source: IBM survey

Also supported by

World Economic Forum:

“There is a strong

correlation between

companies’

competitiveness and

their ability to adopt

technologies”

CIO focus:

60% of CIO’s intend to

increase level of sourcing

Renovate the Core

Cost optimizing to

stay competitive

70

30

New functions Run & Manage

• Business requirements

• Operational stability

• Security & compliance

21

Capital Markets Day 2014

IT is strategic and critical to any business

IT a major growth driver

Line of Business focus: Exploit new Technologies

Setting the

digital agenda

IT spend outside IT org.

• Business growth

• Strategic positioning

against competition

Source: Gartner, IDC

22

Capital Markets Day 2014

The World is Changing… …and it’s changing fast

Market dynamics

Disruptive forces in play

IT-services eats products

IT a major growth driver

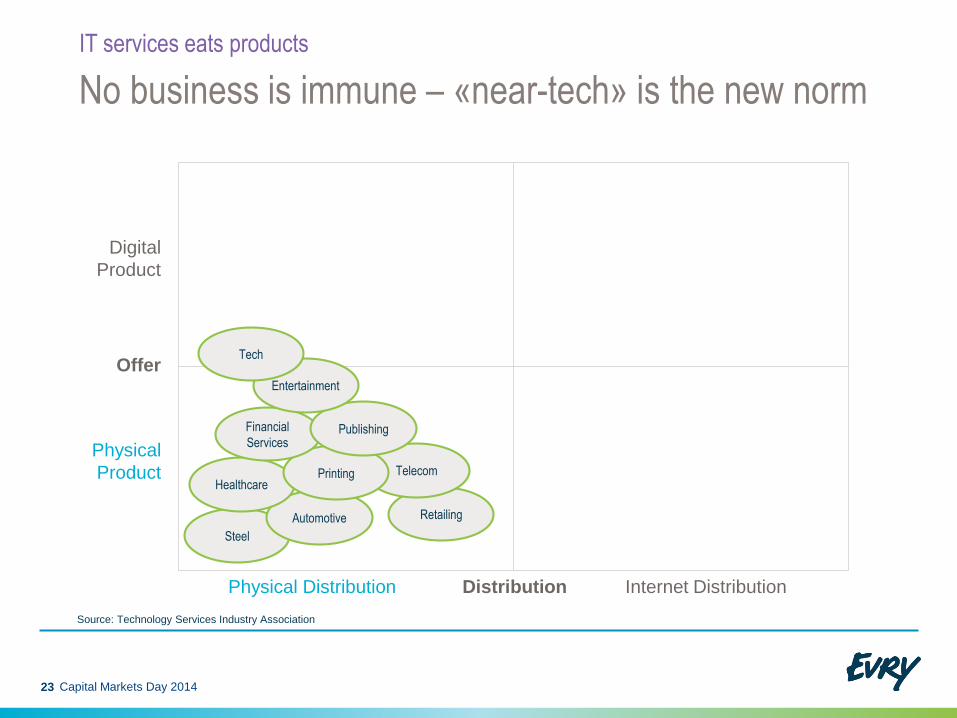

No business is immune – «near-tech» is the new norm

IT services eats products

23 Capital Markets Day 2014

Source: Technology Services Industry Association

Physical

Product

Physical Distribution

Offer

Digital

Product

Distribution Internet Distribution

Retailing

Steel

Automotive

HealthcareTelecomPrinting

Financial

ServicesPublishing

Entertainment

Tech

No business is immune – «near-tech» is the new norm

IT services eats products

24

Source: Technology Services Industry Association

Physical

Product

Physical Distribution

Offer

Digital

Product

Distribution Internet Distribution

Retailing

Steel

Automotive

Healthcare

Telecom

Printing

Financial

Services

Publishing

EntertainmentTech

Capital Markets Day 2014

EMRs and

Home Health Care

Online Banking/Trading

Software-Driven Trading

Tablets

Replacing

Paper

S/W Functionality

Web Shopping

Web Shopping

SaaS/

Cloud

Streaming

VoIP

E-Books

Self-Publishing

• Stable industries

• Predictable competition

• Price and quality

• IT challenging High tech

• New technologies and business models

• New competition

• Time to market

• Internet of Things

25

Capital Markets Day 2014

No business is immune – «near-tech» is the new norm

IT services eats products

Source: Technology Services Industry Association

Line of Business expecting

specialised solutions for increased business value

IT departments embracing

industrialised production for cost efficiency

26

Capital Markets Day 2014

IT-spending increasing but focus is shifting

Market dynamics conclusions

Source: IDC

2 - 4% CAGR

Traditional IT

Next

generation ITMobile devices and Apps

PC and Internet

Manfraime and Terminal

27

Capital Markets Day 2014

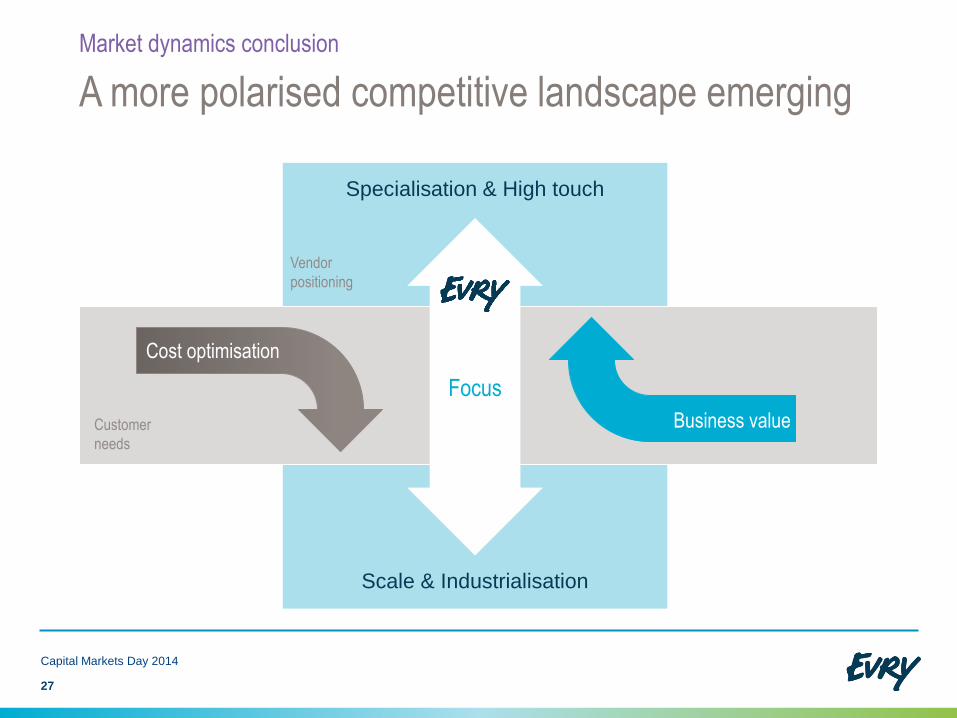

A more polarised competitive landscape emerging

Market dynamics conclusion

Scale & Industrialisation

Specialisation & High touch

Focus

Business value

Cost optimisation

Vendor

positioning

Customer

needs

Streamline Operations –

transforming the business

Adapting to changing market conditions

EVRY’s strategic priorities

Drive business towards vertical

and industry-specific solutions

Focus on

verticals

Reduce

complexity

Reinforce local footprint

and grow regional business

Local

footprint

28

SME/Regions• Business lines

• Packaged services

Financial Services• Nordic expansion

• Core renewal

Selected industries• Gather around industries

• Build true verticals

Managed services• Future Proof

• Cloud & Mobility

• Standard platform

Capital Markets Day 2014

Divest non-core

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Financial Services growth

EVP Financial Services, Wiljar Nesse

2

9

11 June 2014

IT spending Norway vs Sweden (Banking)

Opportunity

Nordic Banking IT Services market

Market size IT services Nordic

Banking is the largest vertical market in the Nordic

Financial Services market

30

8,9

5,9

3,1

4,5

84% 16%

Sweden FinlandNorway Denmark

Banking

140 NOK billion

22,7 NOK billion

Market segments Nordics

57%

43%

IT services In-house

SwedenNorway

38%

62%

Tier 1

Tier 2

Source: Gartner, Radar & IDC, internal analysis

Capital Markets Day 2014

• Move to mobile solutions

• Large Nordic banks increase use of services

• Industrialisation of services

31

Capital Markets Day 2014

Market drivers and customer agenda

Market dynamics

• End customer driven innovation

• Regulatory demands

• Industry convergence

Sources: Gartner, IDC, Radar

Mobile vs Internet banking

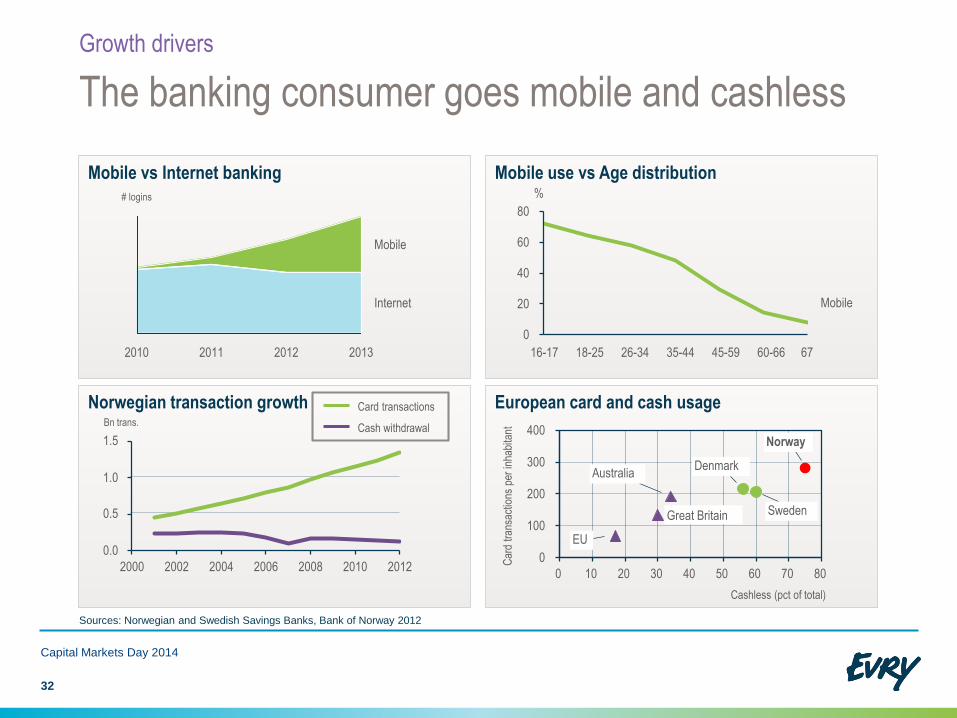

The banking consumer goes mobile and cashless

Growth drivers

Capital Markets Day 2014

Mobile use vs Age distribution

0

20

40

60

80

Mobile

6760-6645-5935-4426-3418-2516-17

European card and cash usageNorwegian transaction growth

2000 2002 2004 2006 2008 2010 2012

1.5

1.0

0.5

0.0

Cash withdrawal

Card transactions

0

100

200

300

400

0 10 20 30 40 50 60 70 80

Car

d tr

ansa

ctio

ns p

er in

habi

tant

Norway

Australia

Sweden

EU

Great Britain

Cashless (pct of total)

Denmark

20112010

# logins

2013

Internet

Mobile

2012

Sources: Norwegian and Swedish Savings Banks, Bank of Norway 2012

32

%

Bn trans.

33

Capital Markets Day 2014

Portfolio of offerings

EVRY capabilities

Revenue mix

Focus areas

32%

24%

42%

Customer Interfaces

Cards

Banking Services

Mobility

Card

Loan services and daily banking

ATM

Core & Payment

*) Banking Services Europe 2012, Gartner 2013

Marketshare Europe*

BT

TC

S

EY

Del

oitte

Info

sys

Cog

niza

nt

EV

RY

HP

CG

I

Sop

ra

Ato

s

Acc

entu

re

Other

Services

Nordic

Champion

Delivery models

Software as a Service

Asset based appl.

Software package delivery

Extended Lifecycle

Management

Business Process

Outsourcing

Basic IT Operations Outsourcing

Application Operations Outsourcing

Next generation of core systems a global phenomenon

Financial Services growth

A core bank system

• Is the heart of the bank’s systems

• Enables an accurate and clear picture of a customer’s total commitment

• Is the basis for regulatory reporting

Strategy to bring together

• Banks

• Vendors

Focus

• Standards

• Service-oriented architecture

Core systems

Internet bank

Mobile bank

Reporting

Payment

Loan/ Credit

Branch systems

Capital Markets Day 2014

34

EVRY to host

international BIAN

conference in Oslo

June 24-27, 2014

35

Capital Markets Day 2014

Nordic core renewal

Financial Services growth

EVRY development principles for

next generation core system

• An evolutionary approach with phased implementation

• Based on BIAN architecture

• Modular approach

• Master data is key component

• Platform independence

• Development work done by Financial Services centre in India

Next generation core system addresses

• Time to market to meet new customer demands

• Reduced complexity

• Increasing regulatory requirements

• Cost optimisation

• Operational performance

• Reduced migration risk

• Nordic expansion

Agreement includes renewal of core and payment modules

36

Capital Markets Day 2014

Case studies

EVRY capabilities

Cost effective

outsourcing based on a

proven solution

ATM management

delivered as a

service

State of the art cash

pooling solution for

corporate clients

Cash Pool solution

for corporate

Banking

An improved payment

experience

Contactless

cards

Recent achievements

• Renewal of large banking services contracts,2/3 of the banking platform portfolio

• Acquired TAG Systems establishing presence in Finland and the Baltics

• Signed Swedbank for a 5-year contract for asset based delivery

• Next generation banking services

• Financial Services global development teams

Roadmap 2016 priorities

• Nordic expansion growing banking services in Sweden and Finland

• Card expansion Sweden/Finland/Baltics/UK

• Address new emerging opportunities within payment and card (Industry convergence)

37

Capital Markets Day 2014

Enforce leadership position in Nordic banking

EVRY priorities and ambitions

Nordic services expansion and

niche solutions globally

Differentiated EVRY capabilities

Nordic

banking

Software as

a Service

Innovative

digital user

interaction

Full card

services

value chain

EVRY portfolio of clients and offerings

Shaping trends

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Card services growth

3

8

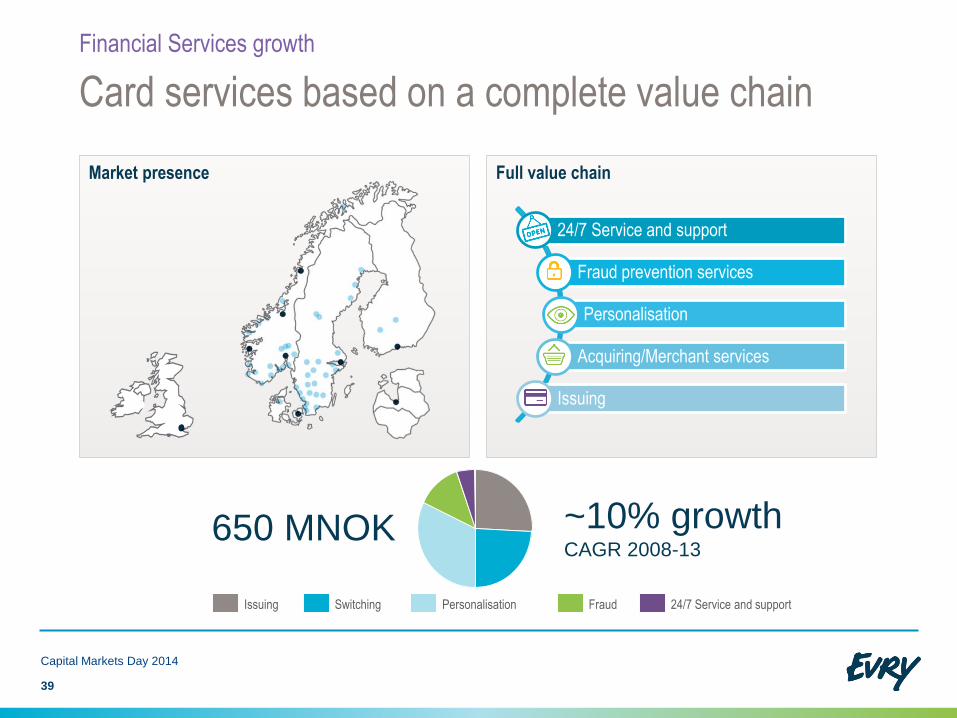

Full value chainMarket presence

Card services based on a complete value chain

Financial Services growth

24/7 Service and support

Fraud prevention services

Personalisation

Acquiring/Merchant services

Issuing

FraudPersonalisationIssuing Switching 24/7 Service and support

650 MNOK ~10% growthCAGR 2008-13

Capital Markets Day 2014

39

40

Capital Markets Day 2014

EVRY in the changing card market

Financial Services growth

Structural

changes

Partnerships

for innovation

Fraud

increase

Technology

shifts

70%

EVRYreduces

fraud up to

• Volume growth and new services to existing customers

• Expansion in Finland and the Baltics

• Full value chain deliveries

• Emerging technologies and opportunities

o Industry convergence

o Contactless

o Context relevant banking services

41

Capital Markets Day 2014

Technology and consumerisation drive growth with Card

Financial Services growth

0

50

100

150

200

250

300

350

New customers/

New markets

Expansion existing

customers

2016 Ambition

MNOK

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Summary

4

2

43

Growing from a solid foundation of offerings and customers

Financial Services ambitions

Banking expertise

close to the

customer

Integrated use of

global sourcing

capabilities

• Market dynamics and industry convergence drive demand for banking specific know-how and solutions

• Mobility is a key to attract and retain banking customers

• Delivery models suited for different customer requirements

• A customer drive for service deliveries versus traditional IT projects

Capital Markets Day 2014

0

100

200

300

400

500

600

CardCustomer

Interfaces

MNOK

2016

Ambition

Banking

Services

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Selected Industries growth

EVP Industries Norway, Anne-Cecilie Fagerlie and EVP EVRY Sweden, Niclas Ekblad

4

4

11 June 2014

Cloud services shares

Market size IT services (Nor+Swe)

Representing more than half of IT services market

Selected industries

45

IT-services spending by industry

Private cloud services market outlook

30.5

16.5

29%

54%

17%

NorwaySweden

Local

Manufacturing / Oil & Gas 15.4

Retail

Insurance

3.6Healthcare

7.7

4.9

14.7Banking & Securities

4.4

Central 8.3

Education

Communications & Media 14.9

2.7

Transportation

5.5Utilities

0.8

3.8

Wholesale TradeBanking

Selected Industries

87 NOK billion

(NOK billion)

47 NOK billion

8.0

4.0

86% 14%

Private cloudPublic cloudCloud services

87 NOK billion 12 NOK billion 24

14

10

16

0

5

10

15

20

25

2

3

4

5

6

1

0

NO

K b

illio

n

CA

GR

% 2013

-17

PaaS IaaSSaaSBPaaS

Source: Gartner, PAC & IDC 2012/13

Capital Markets Day 2014

46

Capital Markets Day 2014

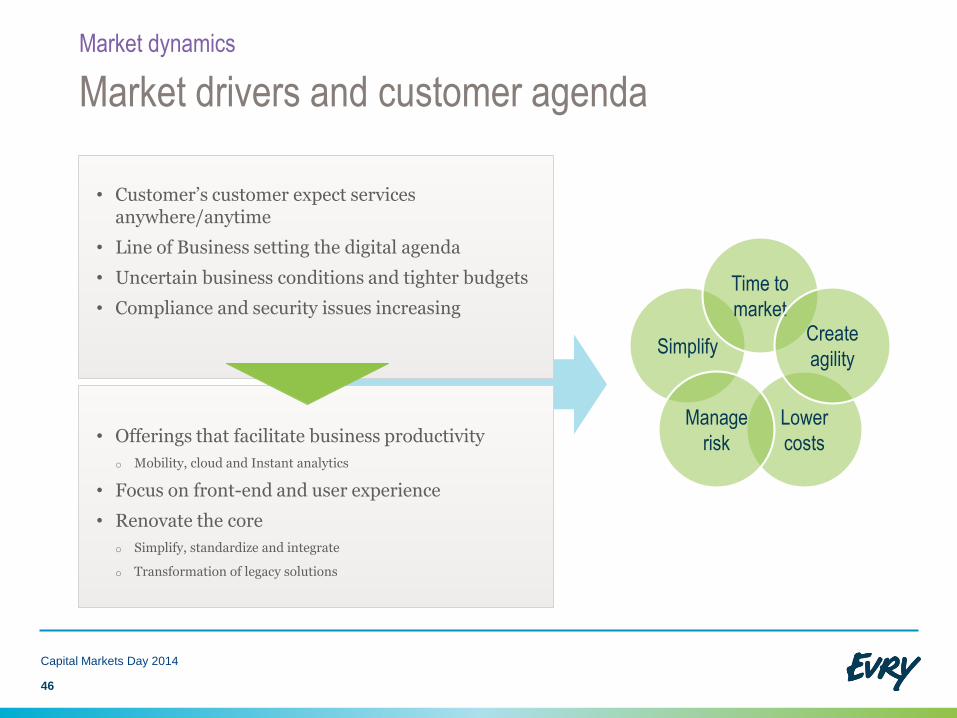

Market drivers and customer agenda

Market dynamics

Simplify

Time to

market

Lower

costs

Manage

risk

Create

agility

• Customer’s customer expect services anywhere/anytime

• Line of Business setting the digital agenda

• Uncertain business conditions and tighter budgets

• Compliance and security issues increasing

• Offerings that facilitate business productivity

o Mobility, cloud and Instant analytics

• Focus on front-end and user experience

• Renovate the core

o Simplify, standardize and integrate

o Transformation of legacy solutions

47

Capital Markets Day 2014

Broad portfolio of offerings and customers

EVRY capabilities

Market shares

Revenue mix Revenue distribution*

Selected customers

25%

14%

36%

25%Infrastructure services

Application Services

Sector solutions

Consulting

Trade & Industry

Oil & Gas

Insurance

Health

Local Gvmt

Central Gvmt

Telecom

Logistic

Retail & Utility

0

5

10

30

35

CS

CB

ouvetT

ieto

CG

I

Steria

Capgem

iniA

ccentureIB

M

EV

RY

TeleC

omp.

0

2

4

6

8

10

12

Sigm

a

EV

RY

Tieto

IBM

CG

I

Know

IT

Capgem

ini

eWork

ZeroC

haos

HP

Norway Sweden

*) Bank & Finance not included

Source: IDC (Nordic Outsourcing and Project Services markets)

Strategies for growth

Established positions

Different strategies exploring attractive opportunities

EVRY capabilities

48

Capital Markets Day 2014

Mature solutions

portfolio,

+300 customers

Core solutions

and domain

expertise

Comprehensive

engagements and

customer insight

Consulting & Services

Operations

Solutions

86%

14%

Outsourced

Increase

IT services

Central govmt

Expand and

cross-sellSol. Sol.

Take footholds

with strategic

consulting

Invest in clinical

suite across

Nordics

Sol.Partnerships for

core solutions

Cons.Develop domain &

process skills

Cons.Renovate and

transformOper.

Public sector InsuranceHealthcare

Source: Radar

Bilde

49

Capital Markets Day 2014

Case studies

EVRY capabilities

«Paperless, flexible, stable,

safe, secure, effective.

70% share of volumes and

increasing»

«EVRY is a strategic partner for

our 2014-17 IT investment

plan»

Providing a realtime

solution to monitor user

experiences on the net

«A decisive step to offer the

best net-shopping experience in

our industry»

Comprehensive

engagements operating

and managing core

systems

Streamlining and secure

the processes related to

prescriptions

Recent achievements

• Organisation aligned for enforced customer focus

• Double digit growth in Healthcare

• Key customer engagements reconfirmed

• Recruited top industry experts in key positions

• Launched Oil & Gas vertical

Roadmap 2016 priorities

• Healthcare Nordic expansion

• Positioning for Public sector sourcing engagements

• Oil & Gas targeted approach

• Retail targeted approach with Financial Services

50

Capital Markets Day 2014

Taking a position in selected industries

EVRY priorities and ambitions

Recognised leader with revenue

growth above market

Differentiated EVRY capabilities

Full service

portfolio with

lifecycle

commitment

We know the

challenges

and

opportunities

facing Nordic

CIO’s

Skills and

methods to

drive trans-

formation

EVRY portfolio of clients and offerings

Shaping trends

Healthcare growth

EVRY

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

5

1

IT spending profileMarket size Total IT spending

Healthcare – a large and dynamic regional market

Selected industries growth

Personal

health

Tech trendsMobility, Internet of things

Productivity+ compliance & security

Cost pressure10% GDP

Common set

of challenges

and priorities

cross Nordic

National eHealthinitiatives

System

Consolidation

37%

22% 21%

20%

20 NOK billion

14%

30%36%

38%35%

22% 15%

10%Healthcare Government

Internal IT spend

HW/SW

Outsourcing

Projects

Sweden

Norway

Finland

Denmark

Capital Markets Day 2014

Source: Gartner, Radar and EVRY Internal analysis

52

53

Capital Markets Day 2014

Strong growth…

Metavision

High end

solution

“E-resept”Only private

alternative

Norway

…delivering critical solutions to society

450 MNOK2013

+18% growth2013/2012

Administrative

Personal healthClinical

Managed services

ORBIT

50,000

users

“Journalen

på nätet”

Clinic

solution

suite

Sweden

Selected industries growth

EVRY health care capabilities and performance

54

Capital Markets Day 2014

Aging population/health spend affecting

Nordic health strategy…

Selected industries growth

E-health opportunities for EVRYChallenges

Cost reductions / “Warm hands”

• Outourcing

• Standardized systems & processes

New health care services & settings

• Based on BIG DataNordics in 2030 will have almost as large a percent of people over 65 as Japan has today.

Delivering service experiences

• Personal health services

• New services based on CRM, BI, mobility etc

Satisfied customers cost less to serve

• Designed memorable serviceSteady increased number of health alternatives – from patient to customer

• Ability to grow in an immature outsourcing market and need for growth in Cloud services

• Solutions driven by standardized processes and consolidation

• Clinical suite consisting of own IPR and partnerships aligned for growth cross Nordic

• Vast volumes of stored data to be transformed to knowledge

55

Strong market trends in Healthcare support ambitious target

Selected industries growth

0

100

500

400

200

300

600

Clinical solutionsManaged services Administrative

solutions

2016

MNOK

Capital Markets Day 2014

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Summary

5

6

0

100

200

300

400

500

600

700

• Market growth in attractive industriesdrive demand for IT services

• Mobility key enabler for customers to grow business

• Future Proof address customer’simperative need for transformation to next generation managed services

• Implementation of Business Lines cater for increased cross-sales

57

Capital Markets Day 2014

Growth initiatives contribution to segments

Selected industries ambitions and summary

Oil & GasHealthcare Public sector 2016

Ambition

MNOK

50%50%

Norway

Sweden

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

SME Regions growth

EVP Regions Norway, Kurt Helland

5

8

11 June 2014

Market size IT services (Nor+Swe)

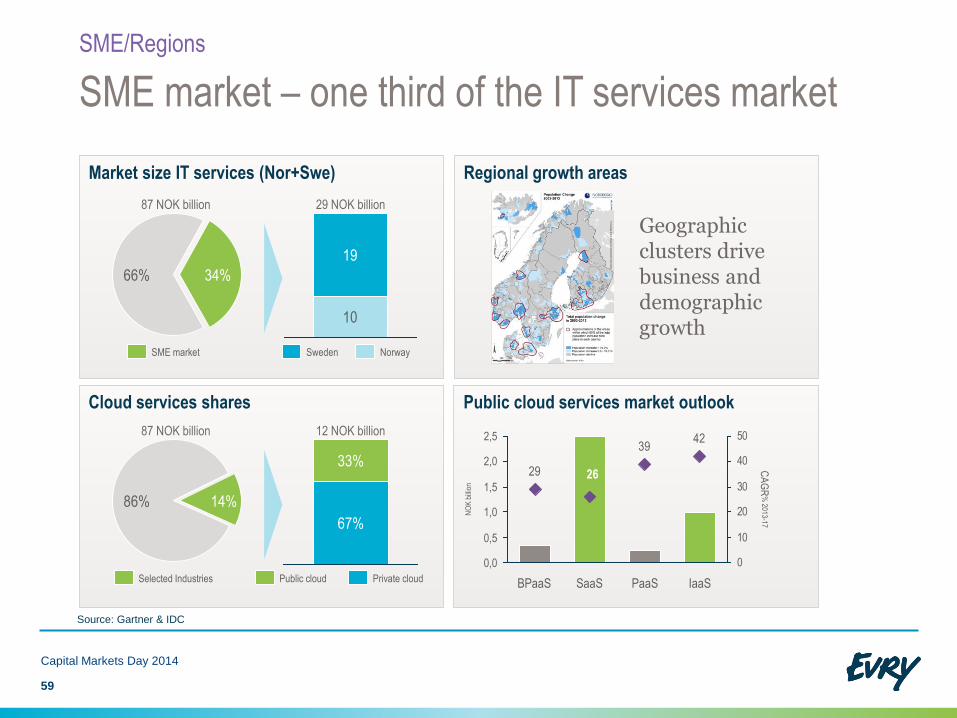

SME market – one third of the IT services market

SME/Regions

59

Capital Markets Day 2014

Regional growth areas

19

10

66% 34%

NorwaySwedenSME market

87 NOK billion 29 NOK billion

Cloud services shares Public cloud services market outlook

67%

33%

14%86%

Public cloud Private cloudSelected Industries

87 NOK billion 12 NOK billion

Geographicclusters drive business and demographicgrowth

Source: Gartner & IDC

4239

29 26

0

10

20

30

40

50

0,0

0,5

2,0

1,0

1,5

2,5

PaaSSaaS IaaSBPaaS

NO

K b

illio

n

CA

GR

% 2013-17

• More for less

• Packaged services supporting business

• Single point of contact

60

Capital Markets Day 2014

Market drivers and customer agenda

Market dynamics Regional market

• Standardized, optimized and dynamic offerings

• Business value

• Line of business own an increased share of total IT spend

Local

footprint

Business

PortfolioOne voice

Revenue mix New offerings

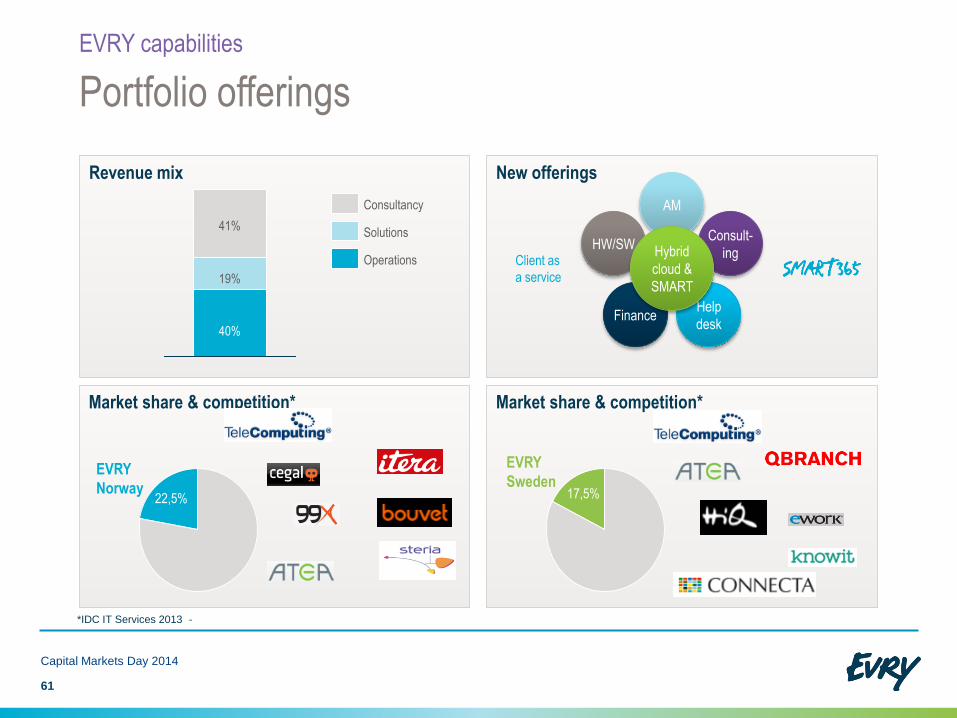

Market share & competition* Market share & competition*

61

Capital Markets Day 2014

Portfolio offerings

EVRY capabilities

17,5%

40%

19%

41%Solutions

Consultancy

Operations

22,5%

EVRY

Norway

EVRY

Sweden

*IDC IT Services 2013 -

Client as

a service

AM

Finance

HW/SW

Help

desk

Consult-

ingHybrid

cloud &

SMART

Market opportunities includes 4,000 customers

White space

Exploiting the broad portfolio of solutions and customers

EVRY capabilities

62

Capital Markets Day 2014

Packaged offerings Cross & up-selling

• NEW Packaged services will be able to address a potential of 4,000 existing customers

• Untapped potential addressing NEW customers

• High hit rate within existing customer base

• High customer satisfaction and good reference base.

60%

15%

25%

40%

85%

75%

Consulting

Solutions

Operations

Bilde

63

Capital Markets Day 2014

Case studies

EVRY capabilities

“EVRY is supporting our

continued growth in

many markets”

“EVRY is handling operation

of our IT services with high

predictability of client services

and costs”

Develop IT-solution to

stream line work

process in services.

Enable customers to be

connected - as a single point

of contact for all clients

Increase control and

steering with quick

payback for corporate

finance

“We expect EVRY to

reduce the invoicing time

on standard service jobs

by an automated flow ”

Recent achievements

• Strong pipeline development

• Business line development

• Strong presence in the cloud service market

• Winning large deals based on one stop shopping

Roadmap 2016 priorities

• Develop packaged services based on cloud principles/next generation services

• Implement business lines across Nordics, build structural capital

• Single point of contact

• Outsourcing leadership

64

Capital Markets Day 2014

Enforcing unique positions

EVRY priorities and ambitions

Regional champion

Differentiated EVRY capabilities

Unique local

presence

and

customer

base

One stop

shopping

Life cycle

commitment

EVRY portfolio of clients and offerings

Shaping trends

Business lines

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Business lines growth

6

5

Increased cross sales and new offerings in 50 locations

66

Close to our customers• Delivery capacity in

50 cities

• No competitor close to our profile and presence

• Closeness is key factor in the SME segment

Operational efficiency

• Improved service levels

• Scalable offers- andproduction processes

• Increasing mix of offshoring in the SME`s

Targeted market approach• Leverage product innovation

• Expanded product offering through Business Lines

• IT services and specialist offerings close to customers demands

Geographic expansion

• Wherever the need is, we are there

• Close enough to be quick, big enough to establish presence

• Our regional model is equipped for both organic-and acquired growth

SME Regions growth

Capital Markets Day 2014

100+ employees

67

Capital Markets Day 2014

Growing from the core – stretching into adjacencies

SME Regions growth

A B C D

Geography Geography Geography Geography

Dedicated resources in customer channel

Sal

es &

cus

tom

er d

evel

opm

ent

Line organization (channel) Business lines

Business Line & Network

Mobility

Collaboration

Business Management

Operations/Cloud

IT/Infrastructure

Application Management

Building

structural

capital

68

Capital Markets Day 2014

Business Lines value propositions

SME Regions growth

E-Commerce IT-operations/

Cloud/PaaS - SME

Mobility

• We transform business by combining

digital expertise, business sense

and customer insight

• A secure and self serviced

IT platform for the future.

• Transforming business combining

connectivity, efficiency, intelligence

and innovation.

Application management/SaaS

• AM together with our operation and

cloud services gives our customers a

possibility to focus fully on their own

needs with 100 % IT back up.

Business

Intelligence

• By using our deep knowledge about

both BIG and small data we combine

our business knowledge and

business intelligence to help out

customers to predict the future

IT Infrastructure

• Companies often has a legacy in IT-

infrastucture we specialize in helping

them get rid of the legacy and focus

on their own business.

• Cloud & Operations growth platform for new packaged services.

• Mobility high growth based on capabilities and market expectations

69

Capital Markets Day 2014

Growth ambitions with Business lines

SME Regions growth

0

50

100

150

200

250

300

350

Collaboration Business

management

Mobility IT Infra-

structure

Application

Management

Operations

/ Cloud

2016

Ambition

MNOK

70

Capital Markets Day 2014

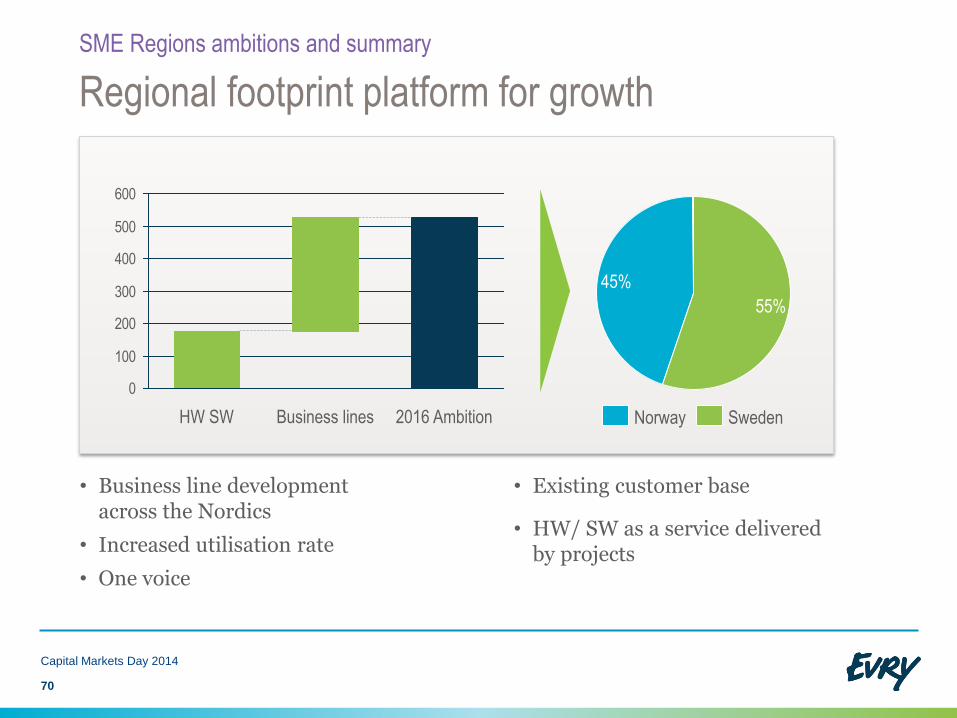

Regional footprint platform for growth

SME Regions ambitions and summary

• Business line development across the Nordics

• Increased utilisation rate

• One voice

• Existing customer base

• HW/ SW as a service delivered by projects

0

100

200

300

400

500

600

HW SW 2016 AmbitionBusiness lines

45%

55%

SwedenNorway

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Managed services growth

SVP Future Proof, Lars Ringvold and SVP EVRY Mobility, Robin Blomquist

7

1

11 June 2014

Management

72

Capital Markets Day 2014

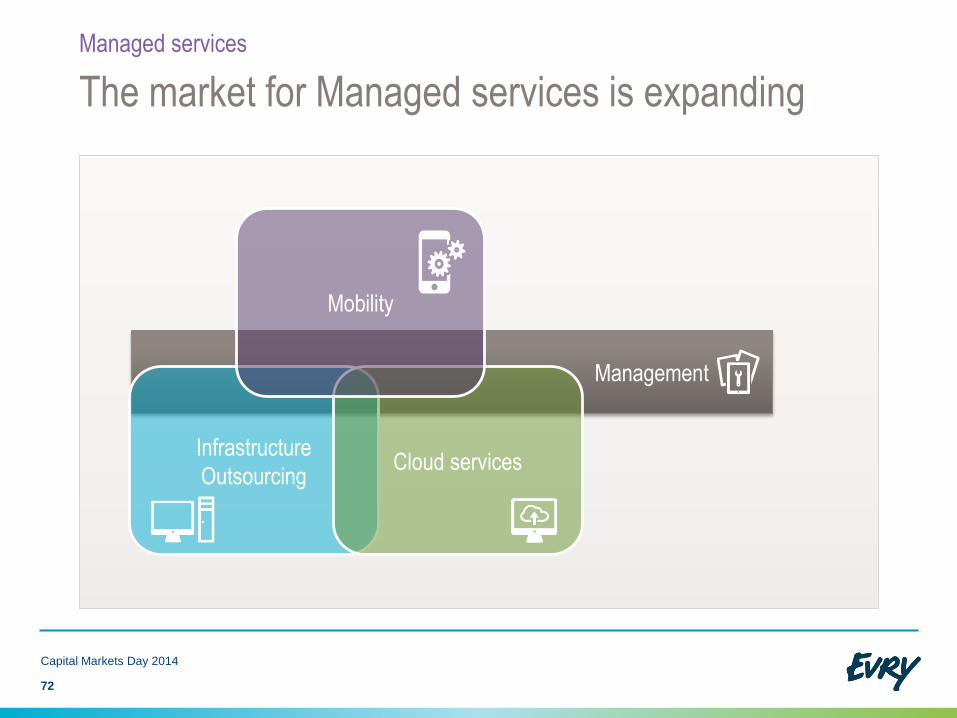

The market for Managed services is expanding

Managed services

Infrastructure

OutsourcingCloud services

Mobility

Transforming EVRY and the operations offerings

Managed services

73

Capital Markets Day 2014

2013 2014 2016

Applications

Operation

LegacyDedi-cated

Private Cloud

Public Cloud

Cloud services distribution

Market size IT services (Nor+Swe)

Addressing more than half of the IT services market

Managed services

74

Capital Markets Day 2014

Size & growth rates sub-segments

Sourcing in Nordic

19

31

58%

42%

NorwaySwedenOutsourcing services

87 NOK billion 50 NOK billion

1,5

10

0

5

10

15

20

25

30

0

5

10

35

40

45

NO

K b

illio

n

Managed

mobile

Managed

cloud

Traditional

outsourcing

CA

GR

% 2013-17

35%

50%

15%

In-houseMixed modelOutsourced

51%

27%

13%

Sourcing plans 2014Current sourcing

8.0

4.0

14%86%

Public cloud Private cloudCloud services

87 NOK billion 12 NOK billion

Source: Gartner, PAC & IDC

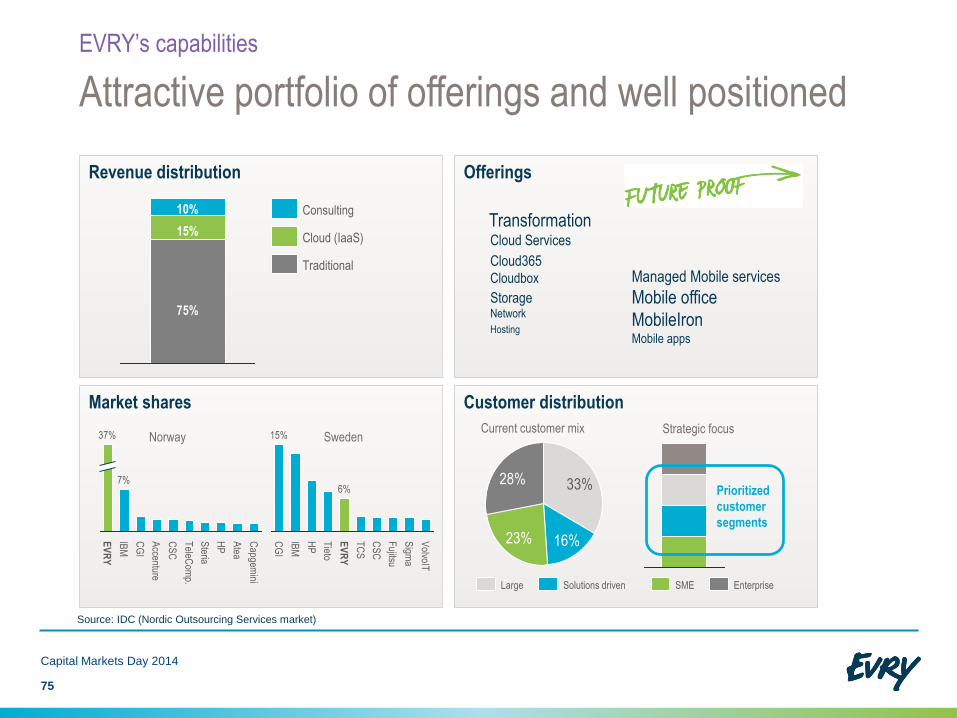

75

Capital Markets Day 2014

Attractive portfolio of offerings and well positioned

EVRY’s capabilities

Market shares

Revenue distribution Offerings

Customer distribution

10%

75%

15%

Traditional

Cloud (IaaS)

Consulting

37%

7%

Steria

HP

EV

RY

Atea

CS

C

CG

I

IBM

TeleC

omp.

Accenture

Capgem

ini

CG

I

IBM

TC

S

Fujitsu

Tieto

VolvoIT

15%

EV

RY

HP

Sigm

a

CS

C

6%

Cloud365

Cloud Services

Managed Mobile services

Mobile office

MobileIronMobile apps

Cloudbox

Transformation

Norway Sweden

16%

28%

23%

33%

EnterpriseSMESolutions drivenLarge

Hosting

StorageNetwork

Prioritized

customer

segments

Current customer mix Strategic focus

Source: IDC (Nordic Outsourcing Services market)

Bilde Bilde Bilde

76

Capital Markets Day 2014

Case studies

EVRY’s capabilities

Using IaaS and PaaS to maintain

better control and reduced costA mobile office that increase

the resources efficiency and

quality of work

A secure and self serviced

IT platform for the future

Transformation and

update of business

critical systems

and services

Mobile and hybrid

client with PC and

tablet functionality

Managed

infrastructure

flexibility, from

legacy to cloud

Business model is evolving

Potential in top end of prioritised segment

Increasing EVRY’s value creation

Evolution and opportunities

77

Capital Markets Day 2014

Legacy

infra-

structure

operation

Consulting

“Commodity” pricing

T&M pricing

Customer

dedicated

Legacy

Consulting

projects

Cloud

services

Value pricing

Customer specific pricing

Pay pr use pricing

76%

16%

24%

84%

Norway Sweden

Share top 50*

PotentialNew

customers

New

business

Potential for all

services

Future Proof

Transformation

Managed mobility

*) Largest customers in prioritized segment (Global Enterprises excluded)

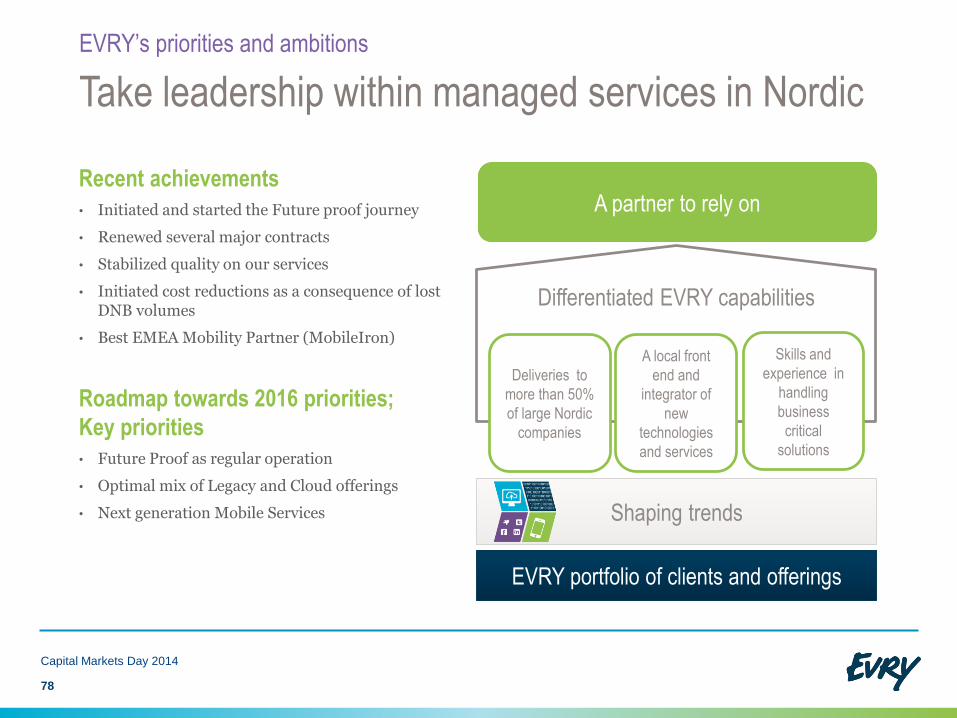

Recent achievements

• Initiated and started the Future proof journey

• Renewed several major contracts

• Stabilized quality on our services

• Initiated cost reductions as a consequence of lost DNB volumes

• Best EMEA Mobility Partner (MobileIron)

Roadmap towards 2016 priorities;

Key priorities

• Future Proof as regular operation

• Optimal mix of Legacy and Cloud offerings

• Next generation Mobile Services

78

Capital Markets Day 2014

Take leadership within managed services in Nordic

EVRY’s priorities and ambitions

A partner to rely on

Differentiated EVRY capabilities

Deliveries to

more than 50%

of large Nordic

companies

A local front

end and

integrator of

new

technologies

and services

Skills and

experience in

handling

business

critical

solutions

EVRY portfolio of clients and offerings

Shaping trends

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Future Proof growth

Managed services

7

9

Going to market with standardized suite of services

• Agile and ScalablePlatform

• Productive CollaborationWorkspace

• Compliance and Risk MitigationSecurity

• Modernize and IntegrateTransformation

In partnerships with:

Future Proof program

Capital Markets Day 2014

80

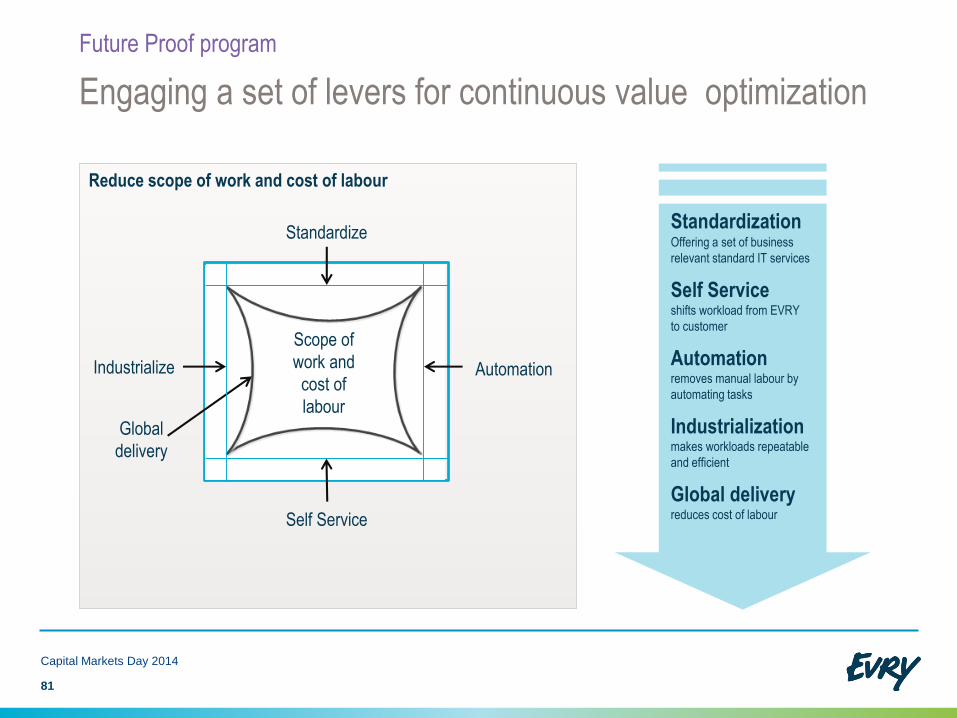

Reduce scope of work and cost of labour

Engaging a set of levers for continuous value optimization

Future Proof program

81

Capital Markets Day 2014

StandardizationOffering a set of business

relevant standard IT services

Self Service shifts workload from EVRY

to customer

Automation removes manual labour by

automating tasks

Industrialization makes workloads repeatable

and efficient

Global deliveryreduces cost of labourSelf Service

Standardize

Industrialize Automation

Scope of

work and

cost of

labour

Global

delivery

• New business from selected industry customers

• Customers transformations to Future Proof

• Private and partner cloud share increasing

82

Transforming and repositioning the operations business

Managed services growth

0

100

200

300

400

500

600

Sweden 2016

Ambition

MNOK

Norway Consultants

utilization

Customer

dedicated

Legacy

Consulting

projects

Managed

cloud

10-15%

35-40%

45-50%

Capital Markets Day 2014

Mobility growth

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

8

3

450+Mobile Apps

100K+Ticket resolved in

the last 12 months

400+Global Delivery

Mobility Developers

250+MDM

deployments

5K+

Devices

deployed

per month

400K+devicesdeployed

63%+projected sales

by 2016

Global

Capabilities

2011 – Partner of the year (EMEA)

2012 – Partner of the year (EMEA)

2013 – Partner of the year (EMEA)

2014 – Outstanding Engineer (EMEA)

2014 – Top Performance (EMEA)

2014 – EMEA Partner Awards – Excellence in Marketing

Best in

class

260+Local

Mobility Experts

EVRY Enterprise Mobility in the Nordics

Managed services growth

84

Capital Markets Day 2014

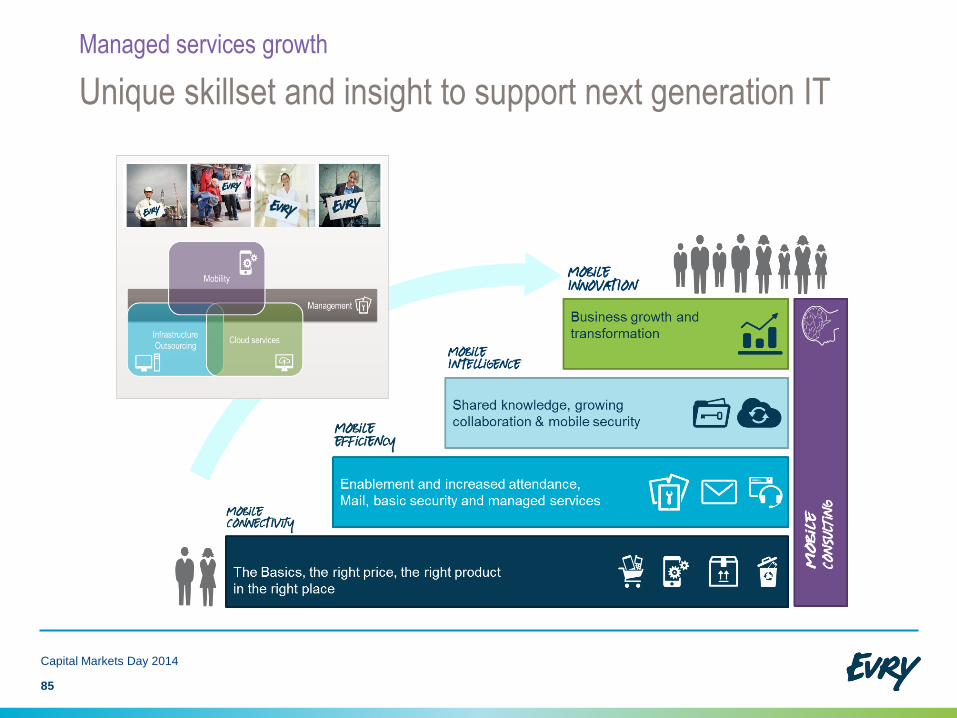

Unique skillset and insight to support next generation IT

85

Managed services growth

Capital Markets Day 2014

Mobile collaboration drive innovation

Managed services growth

Mobile App

Internet of Things

Managed Services

Mobility

One stop shop

Next Generation

IT

“If we wait with mobility, it’s a loss of opportunity,

we can never keep up with competition later on”

“Smart device solutions is a game changer”

Capital Markets Day 2014

86

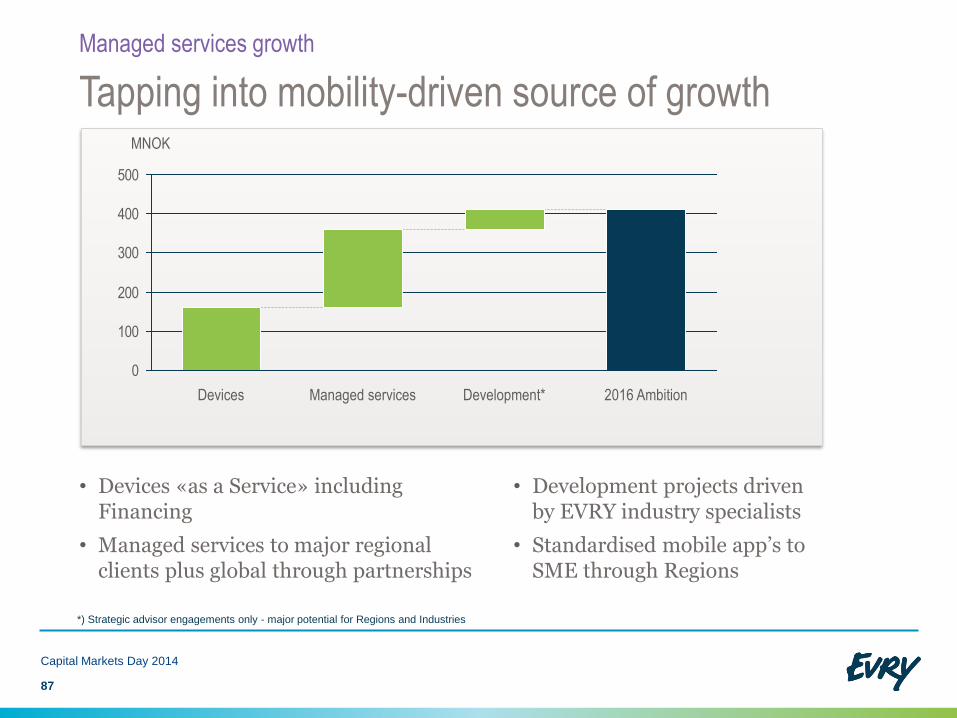

• Devices «as a Service» includingFinancing

• Managed services to major regional clients plus global through partnerships

• Development projects driven by EVRY industry specialists

• Standardised mobile app’s to SME through Regions

87

Capital Markets Day 2014

Tapping into mobility-driven source of growth

Managed services growth

*) Strategic advisor engagements only - major potential for Regions and Industries

0

100

200

300

400

500

2016 AmbitionDevelopment*Managed servicesDevices

MNOK

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Summary

8

8

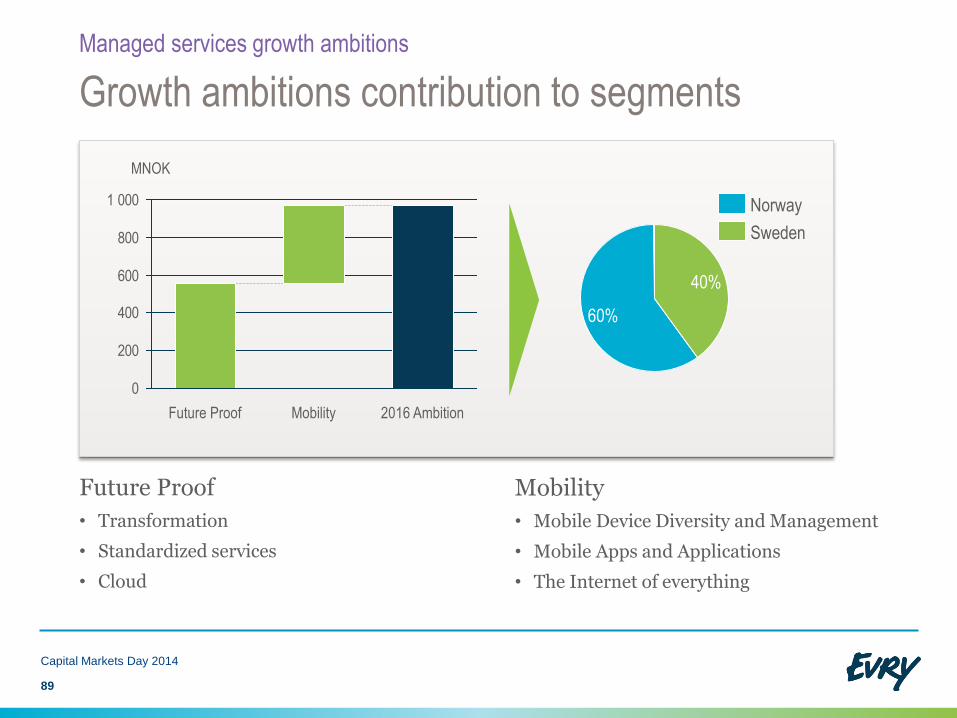

Future Proof

• Transformation

• Standardized services

• Cloud

Mobility

• Mobile Device Diversity and Management

• Mobile Apps and Applications

• The Internet of everything

89

Capital Markets Day 2014

Growth ambitions contribution to segments

Managed services growth ambitions

0

200

400

600

800

1 000

Future Proof 2016 AmbitionMobility

MNOK

60%

40%

Norway

Sweden

Financials & guiding

CEO Terje Mjøs and acting CFO Morten Frogner

11 June 2014

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

9

0

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Next phase: Accelerate growth

9

1

Capital Markets Day 2014

Projected growth in the Nordic market for IT services

Revenue growth

IT services market growth

0

1

2

3

4

5

2010 2011 2012 2013 2014 2015 2016

Outsourcing services Project services

Driven primarily by next generation IT

• Volatile situation 2010 – 2013 affected by stalling global economy

• IT services growth tracking above GDP growth

• Higher spread (between analysts) for growth projections going forward, next generation IT growth less predictable

Source: Nordic IT Services Analysis IDC, May 2013

92

2-4%

CAGR

Initiatives drive topline growth

Capital Markets Day 2014

EVRY has ambitious targets driven by growth initiatives

Revenue growth

2013 adjusted

baseline*

2016 TargetBase revenue

growth

Managed

Services

Financial

Services

Selected

Industries

Regions SME

Above market growth

• Global

sourcing

• Other

businesses

• Future

Proof

• Mobility

• Next

generation

Core and

Payment

solutions

• Nordic

expansion

• Card

services

• Targeting

industries

• Cross

selling

• Packaged

services

• Building

structural

capital

Key drivers

12.5

11.5

13.0

12.0

11.0

DNB

2013

NOK billion

*) Baseline adjusted for lost DNB revenues

93

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Profitability improvement continues

9

4

Capital Markets Day 2014

Lifting margins to the next level

Improving profitability

Historic EBITA

Improvements from

strong cost discipline

Baseline

EBITA margin

5,9%

Target

margin 2016

95

Future EBITA

Margin improvements facilitated by GROWTH

and continued cost discipline

GROW400

450

500

550

600

650

700

750

800

481

Q2

2011

753

+272MNOK

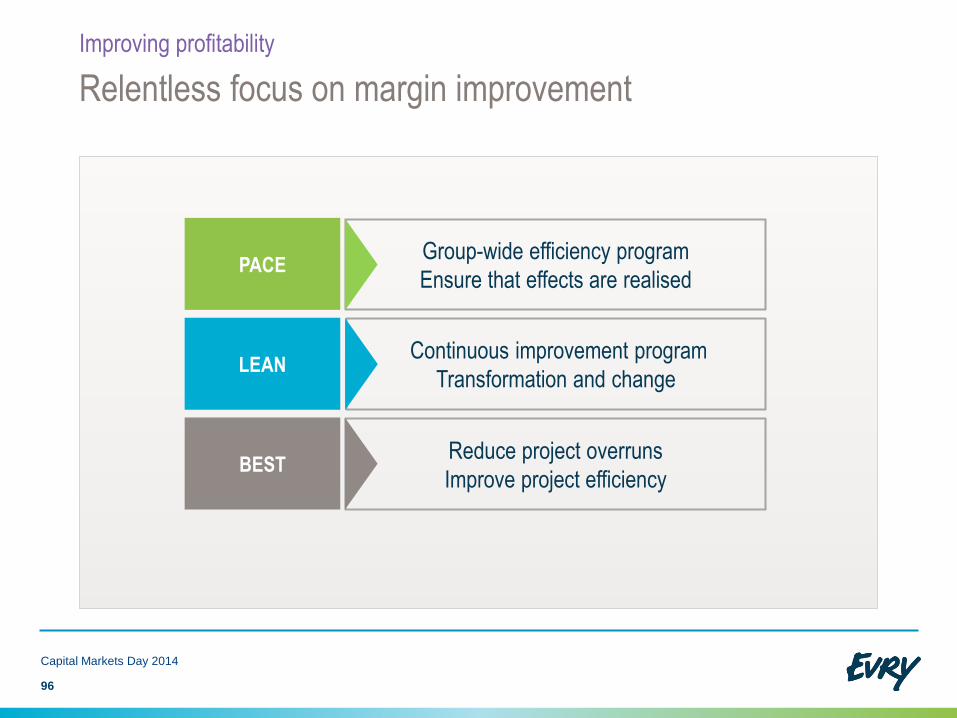

Relentless focus on margin improvement

Improving profitability

Group-wide efficiency program

Ensure that effects are realised

Reduce project overruns

Improve project efficiency

Continuous improvement program

Transformation and changeLEAN

PACE

BEST

96

Capital Markets Day 2014

Program approach

• Align projects and monitor interdependencies

• Ensure that effects are realised

Capital Markets Day 2014

PACE – Ensure corporate efficiency

Improving profitability

Program scope

• Restructuring to fit scope (DNB, Posten)

• Restructuring of low performing units

• Optimize banking value chain

• Industrialize and standardize operations – execute the cost side of Future Proof

• Streamlining staff and support functions

• Reduction of 400 FTEs in 2014/2015, restructuring costs of NOK 140 million(previously announced)

97

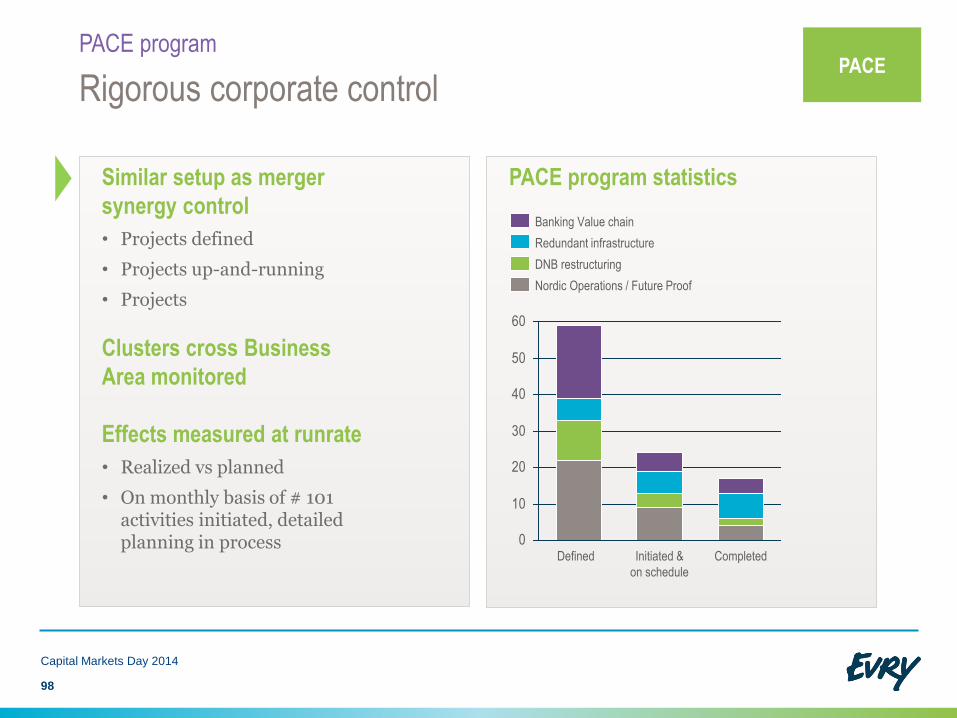

PACE

Capital Markets Day 2014

Rigorous corporate control

PACE program

PACE program statistics

0

10

20

30

40

50

60

Defined Initiated &

on schedule

Completed

DNB restructuring

Banking Value chain

Redundant infrastructure

Nordic Operations / Future Proof

98

Similar setup as merger

synergy control

• Projects defined

• Projects up-and-running

• Projects

Clusters cross Business

Area monitored

Effects measured at runrate

• Realized vs planned

• On monthly basis of # 101 activities initiated, detailed planning in process

PACE

Scope

• Fulfill contractual commitment and manage transition of deliveries

• Downsize and transform to realize a soft landing for the cost portfolio

Approach and impact

• Terminate redundant infrastructure

• Restructure and/or reallocate affected employees

• Scale staff and support functions

• Prolongation agreement ensuring controlled transition and wind-down

• New Master Service Agreement announced (Mainframe +)

• Transition of services during first half of 2015

• Reduction of 300 FTEs*, restructuring costs of NOK 100 million*

• NOK 600 million drop in revenue in 2016 and EBITA down by NOK 50million**

DNB – Neutral EBITA effect despite revenue drop

Improving profitability

*) Included in total 400 FTEs and MNOK 140 restructure costs announced.

**) Compared with 2013

Capital Markets Day 2014

99

PACE

Future Proof Program scope

• Develop new portfolio of services

• Implement standardized production platforms

• Transition & transformation to upgraded platforms (services & customers)

Approach and effects

• SW consolidation and cost reduction from standardization

• Shut-down of obsolete infrastructure (HW/SW)

• Change of workforce

• Headcount reductions from greater use of automation and self service

• Increase offshore ratio for infrastructure operation, large customers, from 25% (2013) to 60% (2017)

• Reduce hired consultants with 100 FTEs

• Change of competencies

• Datacenter consolidation

Capital Markets Day 2014

Future Proof – Realize effects from industrialization

Improving profitability

100

PACE

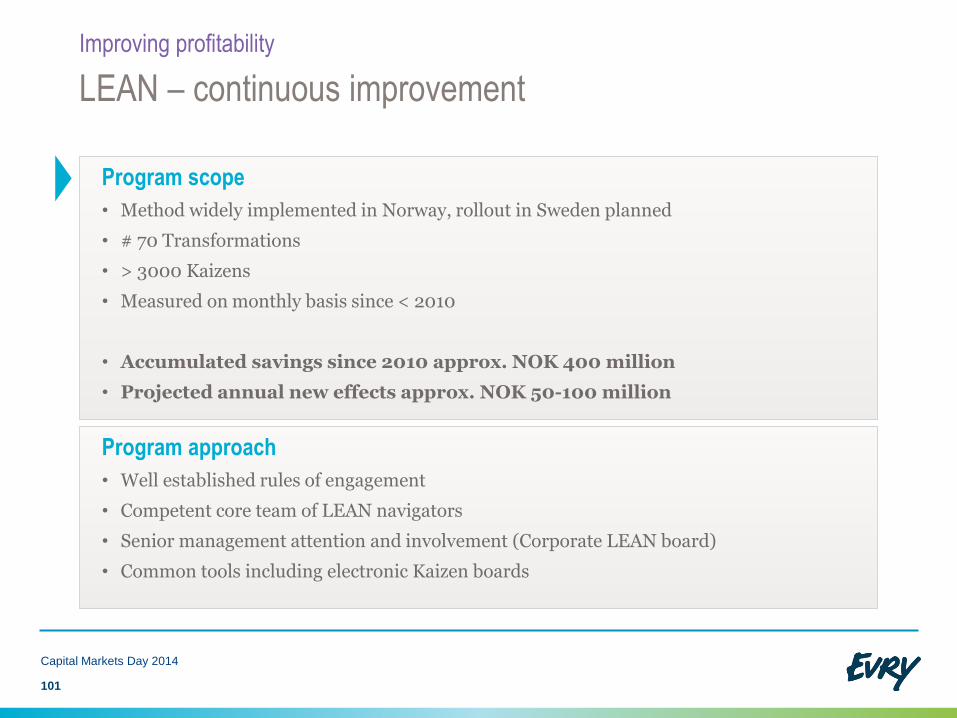

Program approach

• Well established rules of engagement

• Competent core team of LEAN navigators

• Senior management attention and involvement (Corporate LEAN board)

• Common tools including electronic Kaizen boards

Capital Markets Day 2014

LEAN – continuous improvement

Improving profitability

Program scope

• Method widely implemented in Norway, rollout in Sweden planned

• # 70 Transformations

• > 3000 Kaizens

• Measured on monthly basis since < 2010

• Accumulated savings since 2010 approx. NOK 400 million

• Projected annual new effects approx. NOK 50-100 million

101

Program approach

• Project Management Office (PMO) structure in Corporate and Business Areas

• Transparent reporting at all management levels

• Consistent KPI-measurements and monitoring

• Formal certification (PMI/P3M3)

• Common toolbox and methodologies

Capital Markets Day 2014

BEST – Reduce project overruns

Improving profitability

Program scope

• Corporate program since 2H 2013

• Leverage resources and competencies

• Streamline deliveries throughout the value chain from sales to production

• Portfolio of +140 large projects (NOK 1 – 1.4 billion)

• Reduce project overruns and improve efficiency in projects

102

8% EBITA margin target in 2016

5,9%

Target

margin 2016

Baseline

EBITA margin

> 8.0%

Future EBITA

Margin improvements facilitated by GROWTH

and continued cost discipline

Capital Markets Day 2014

Improving profitability

Other• Quality

cost

• Utilisation

BESTLEANPACEGROW

103

Historic EBITA

Improvements from

strong cost discipline

400

450

500

550

600

650

700

750

800

481

Q2

2011

753

+272MNOK

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Value creation through

strong focus on cash flow

EVRY

1

0

4

Capital Markets Day 2014

Historic performance

Financials & guiding

Cash flow last four quarters*

EBITA last four quarters* Order backlog

Dividend per share

*) Comparable, restated figures

105

753749733714680685671690681663

555

481501

400

500

600

700

800

Q2

11

Q1

11

Q4

12

Q3

12

Q2

12

Q1

12

Q4

11

Q3

11

MNOK

Q1

14

Q4

13

Q3

13

Q2

13

Q1

13

10

12

14

16

18

Q3

13

MNOK

Q2

14

Q1

14

16,5

Q4

13

16,6

Q4

11

16,1

Q3

11

16,8

Q2

11

17,1

Q1

11

17,7

Q4

10

17,8

14,2

Q2

13

15,1

Q1

13

15,3

Q4

12

15,3

Q3

12

15,0

Q2

12

15,3

Q1

12

15,5

1 065

1 0991 049

1 011957

807721

801808

597

322250

375

200

400

600

800

1 000

1 200

MNOK

Q1

11

Q2

11

Q2

13

Q3

13

Q4

13

Q1

13

Q1

14

Q3

12

Q4

11

Q4

12

Q1

12

Q3

11

Q2

12

0,0

0,1

0,2

0,3

0,4

NOK

201420132012

375

250 322

597

808 801 721

807

957 1.011

1.049 1.099 1.065

328

160

(175)

97

204 156

86

207

366

461 469 405 409

0

1

2

3

4

5

6

7

Q3 11 Q4 12Q3 12Q4 11 Q1 14Q1 13 Q2 13Q1 12 Q4 13Q3 13Q2 12Q2 11Q1 11

Operational Cash Flow

Working Capital (% of rev)

Free Cash Flow

Capital Markets Day 2014

Managing cashflow pays off

MNOK

Cash flow focus

• Cash conversion improved• Working capital reductions realized• CAPEX discipline

• Future EBITDA increase, smaller increase in tax payable, will add to cash flow

106

% of revenue

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Segment guiding

EVRY

1

0

7

Growth contribution from initiatives Corridor, status and target

• Nordic expansion for banking solutions

• Cost initiatives ensure soft landing from loss of DNB contract

• Investment in core banking and payment services builds a platform for further growth in banking from 2016

• Cards continue to deliver better than average margins and outperform market growth

Capital Markets Day 2014

Margin corridor of 9-12% maintained

EVRY Financial Services

108

2 000

2 200

2 400

2 600

2 800

3 000

3 200

3 400

3 600

Target 2016

(range)

CardBanking

MNOK

Adjusted

baseline

2013

8

9

10

11

12

13

EBITA%

2016

2013

9,2%

Growth contribution from initiatives

3 000

3 200

3 400

3 600

3 800

4 000

4 200

MNOK

Selected

industries

SME

Regions

Target

2016

(range)

Baseline

2013

Managed

Services

Corridor, status and target

Margin corridor of 8-10% maintained

EVRY Sweden

• Restructuring of low performing units has been initiated

• Better utilization rates and slight increase in hourly prices are expected

• Growth in high margin products and services through focus on business lines and cross selling

• Competitive mobility offer drives growth in managed services

Capital Markets Day 2014

109

6

7

8

9

10

11

EBITA%

2016

2013

6,4%

Growth contribution from initiatives Corridor, status and target

Capital Markets Day 2014

Margin corridor of 7-9% maintained

EVRY Norway

• Anticipated exit from non-core, high margin businesses will reduce margins to some extent

• Several comprehensive cost initiatives benefit this segment. The comprehensive program of work in the Future Proof program is expected to lower costs and secure new growth through increased competitiveness

• Increased profitability through operational efficiency, e.g. improvements in utilization rates

110

6 000

6 200

6 400

6 600

6 800

7 000

7 200

7 400

MNOK

SME

Regions

Managed

Services

Selected

industries

Baseline

2013

Target

2016

(range) 5

6

7

8

9

10

EBITA%

2013

5,5%

2016

Managing CAPEX in line with guidance

0

1

2

3

4

5

6

0

200

400

600

800

Capital Markets Day 2014

CAPEX within target corridor

Finance & guiding

Managing CAPEX in line with guidance

• Presently CAPEX is at the higher end of the target corridor, mainly driven by investments related to Future Proof

• Software developed in-house will increase due to core banking renewal and payment projects, and will keep investments above the mid range also in 2015

• High growth units driving investment spending

• Sale of non-core assets will reduce net CAPEX in the short term

20122011

% of revenueMNOK

20162013 Q1

2014

Percentage

Ordinary capex

Own developed software

Target

corridor

111

Capital Markets Day 2014

Key ratios and sensitivities

Financials & guiding

Hourly rates

Target:

Slight yearly increase in hourly ratesSensitivity:

NOK 30 million/year for every NOK 10 per hour

Offshore ratio in Future Proof program

Target:

60% offshore ratio in 2017, up from 25%Sensitivity:

Savings per 100 FTEs exceed NOK 50 million

Utilisation rates

Target:

2-4 percentage point improvementSensitivity:

EBITA effect of NOK 40 million/year for every percentage point

Working days

Sensitivity:

Norway: NOK 7 million/daySweden: NOK 6 million/day

112

*) Within infrastructure operations large customers

Capital Markets Day 2014

Value creation and financial flexibility

Financial & guiding

• Increased EBITA through growth and cost control

• Investment level within corridor

• Further improvement in working capital

Targets

PolicyStrengthened financial position

Dividend

Equity ratio > 40 %

Gearing ratio < 2,0

Dividend 20-50%

Growth Debt reduction

113

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

Summary

1

1

4

Ready and able to grow

• Ready for next phase – Growth- Key Projects in strategic areas established

• Continued focus on Cost competitiveness- Corporate Programs up & running

• IT market expected to grow faster than GDP- 2-4% CAGR

Targets• Grow more than the market*

• Deliver EBITA margin > 8% in 2016

Financials & guiding

115

Capital Markets Day 2014

*) Baseline adjusted for DNB

C

a

p

i

t

a

l

M

a

r

k

e

t

s

D

a

y

2

0

1

4

1

1

6

Top Related