Wcp 2001 03 rpt responsesofmountaincariboutolinearfeaturesinawestcentralablandscape

You’re in good company You’re in good company You’re in good company

Results presentation for the year ended 29 February 2012

Results presentation 2012

Agenda

2

Highlights

Business model

Operational performance

Financial results

Board changes

Strategy and prospects

Highlights

Results presentation 2012

Highlights

11th successive year of record turnover and profits – coming off an increasingly high base 11– coming off an increasingly high base – coming off an increasingly high base

Milestone R2 billion revenue exceeded Milestone Milestone

Milestone R400 million operating profit exceeded - 15% growth on prior year Milestone 15% growth on prior yearMilestone

Operating margin maintained at record 19.1% - strong “claw back” in second half Operating margin maintained at record strong “claw back” in second halfOperating margin maintained at record strong “claw back” in second half

Net borrowing to equity improves to a 5 year low of 10% Net borrowing to equity improves to a 5 year low of Net borrowing to equity improves to a 5 year low of

Total dividends to shareholders 200 cents per share - an increase of 29% Total dividends to shareholders 200 cents per share - an increase of Total dividends to shareholders 200 cents per share - an increase of

Attained landmark share price of 5 000 cents Attained landmark share price of Attained landmark share price of

4

Results presentation 2012

Highlights

Awarded 10th position in Sunday Times Top 100 Companies Survey Awarded Companies Survey Awarded Companies Survey

Opened 146 new restaurants, surpassing goal of 2000

Opened 2000 Opened 2000

Successful integration of F2011 acquisitions Successful Successful

Traction gained in Africa: 21% growth in system-wide sales Traction gained in Africa: system-wide salesTraction gained in Africa: system-wide sales

Manufacturing and distribution capability continue to expand Manufacturing and distribution capability expandManufacturing and distribution capability expand

Clean sweep of all relevant Leisure Options consumer awards Clean sweep consumer awardsClean sweep consumer awards

5

Business model

Results presentation 2012

Business model

7

Franchising Division

Franchising Division

Franchising Division

Franchising Division The MAD Lab

Food Services Division

New Business Division

Development Division

Procurement Division

Manufacturing Division

Logistics Division

Corporate

International Domestic (Mainstream

Brands)

Domestic (Developing

Brands)

Domestic (Theatre of

Foods)

Marketing, Artistry and

Design

Retail and

Wholesale

•!Wimpy UK •!Steers

•!Wimpy

•!Debonairs Pizza

•!FishAways

•!Mugg & Bean

•!KEG

•!Milky Lane

•!Giramundo

•!Brazilian Café

•!House of Coffees

•!McGinty’s

•!The Brewers Guild

•!O’Hagan’s

•!tashas

•!Vovo Telo

•!Juicy Lucy

•!Group marketing and social media

•!Group restaurant design

•!Group product development

•!Steers

•!Wimpy

•!Baltimore

•!TruFruit

•!Aqua Monte

•!Mugg & Bean

•!Site selection

•!Franchisee selection

•!Lease negotiation

•!Strategic alliance management

•!Drawings

•!Costing

•!Procurement

•!Project management

•!Supplier appointment and audits

•!Price negotiations

•!New business integration

•!Planning and forecasting

•!Sauces and spices

•!Meat and chicken products

•!Bakery

•!Ice-cream

•!Fruit juice

•!Mineral water

•!Telesales

•!Warehousing

•!Distribution

•!Human Resources

•!Finance

•!Information Technology

•!Legal

Operational performance

Results presentation

Franchising division

9

Results presentation 2012

System–wide sales growth

10

7,7%

21,0%

8,5%

0%

5%

10%

15%

20%

25%

Domestic Rest of Africa Total

Results presentation 2012

Like-on-Like sales growth

11

5,1%

7,0%

5,2%

0%

1%

2%

3%

4%

5%

6%

7%

8%

Domestic Rest of Africa Total

Results presentation 2012

New restaurants opened

19 21

48

12

17

2 1

5 6 9

1 1 2 2

0

10

20

30

40

50

60

12

Total 146

Results presentation 2012

Franchise network

521

121

533

371

123 128

81

24 14 48

4 19 4 12 2 9 8 8 13 0

100

200

300

400

500

600

13

Total 2 043

Results presentation 2012

Trading footprint

14

South Africa 1 767

Namibia 25 Botswana 26

Zambia 19

Nigeria 3

Ivory Coast 4

UK 121

Dubai 2

Sudan 5

Kenya 12

Malawi 4 Mozambique 3

Tanzania 3

Zimbabwe 11 Mauritius 27

Swaziland 8 Lesotho 3

South Africa 1 767 Rest of Africa 155 United Kingdom 121

Results presentation 2012

Highlights – Domestic – Mainstream Brands

15

Launched new Steers image and positioning - REAL BURGERS

Innovation around core products

Increased focus on chicken

Results presentation 2012

Highlights – Domestic – Mainstream Brands

16

New design roll-out continues to gain momentum

Maiden entry into Mauritius

Re-focus on breakfast market

continues to gain momentum

Maiden entry into Mauritius

Re-focus on breakfast market

Results presentation 2012

Remains at forefront of per capita consumption growth amongst Black consumers

Accountable for 40% of Group’s Africa turnover

First to market with technology, innovation, trading format and value for money

Highlights – Domestic – Mainstream Brands

17

Remains at forefront of per capita consumption

Accountable for 40% of Group’s Africa turnover

Results presentation 2012

“On the Move” model with Total continues to gain traction – ten new sites this year

Maiden entry into Zambia and Mauritius

“Metro” trading format launched in Newcastle

Highlights – Domestic – Mainstream Brands

18

Results presentation 2012

Competitive climate fuels growth in the category

Record 15% growth in system-wide sales

Highlights – Domestic – Mainstream Brands

19

Competitive climate fuels

Results presentation 2012

Highlights – Domestic – Mainstream Brands

20

Successfully integrated into franchising and supply chain structures

New corporate identity launched and roll-out commencing

Results presentation 2012

Highlights – Domestic – Mainstream Brands

21

Re-launch delayed due to Gauteng liquor license moratorium

“Rehabilitation” of existing network well under way

Results presentation 2012

Highlights – Domestic – Developing Brands

22

Customer acceptance continues to grow

2nd restaurant opened in Musina and push into mass market commencing

Slow start but gaining momentum – McGinty’s OR Tambo

Results presentation 2012

Highlights – Domestic – Theatre of Foods Brands

23

Phenomenal organic growth continues Flagship “le parc” format launched at Hyde Park to extraordinary acclaim Export of concept under consideration

Phenomenal organic growth continues Flagship “le parc” format launched at Hyde Park to extraordinary acclaim Export of concept under consideration

Results presentation 2012

Highlights – Domestic – Theatre of Foods Brands

24

First to market in pioneering artisan bakery category

Ready to expand to Western Cape and KwaZulu Natal

Results presentation 2012

Highlights – Domestic – Theatre of Foods Brands

25

Brand completely re-invented

Re-launch of high street offering imminent

Brand completely re-invented

Results presentation 2012

Food for thought

26

1.5 million breakfasts

3.4 million burgers 3.4 million3.4 million

4 million cups of coffee 4 million4 million

2 million ice cream cones 2 million2 million

1.8 million pizzas

Average monthly sales of key line items

Results presentation 2012

Highlights – United Kingdom

27 27

Severe economic conditions prevail - tough market to trade in

Nominal contributor to Group revenue (only 3.8%)

Right-sizing concluded, business is profitable, and no distraction to management

“The business isn’t shabby, it’s the UK that’s shabby” Keith McLachlan, Thebe Securities

Results presentation 2012 Results presentation

Manufacturing division

28

Results presentation 2012

Gross Revenue % Growth - Manufacturing

15,1%

7,7%

11,0%

15,4%

6,0%

-2,9%

27,3%

-5%

0%

5%

10%

15%

20%

25%

30%

Meat Plant Bakery Sauces & Spices

WCP Meat Plant

WCP Bakery Fruit Juice Ice-Cream

29

Growth 12.6%

Results presentation 2012

Highlights - Manufacturing

Contended with 30% average increase in beef price and 17% increase in paraffin price

Operating margin unchanged at 11.7%

Chicken fillet plant commissioned in November 2011

Successful take-on of Milky Lane soft serve volumes concluded in October

30

Contended with 30% average increase in beef price and 17% increase in in beef price and 17% increase in Contended with 30% average increase in beef price and 17% increase in

Operating margin unchanged at 11.7% Operating margin unchanged at 11.7%

Chicken fillet plant commissioned in November 2011 November 2011 Chicken fillet plant commissioned in November 2011

Successful take-on of Milky Lane soft serve volumes concluded in October serve volumes concluded in October Successful take-on of Milky Lane soft serve volumes concluded in October

Results presentation 2012 Results presentation

Logistics division

31

Results presentation 2012

Gross Revenue % Growth - Logistics

18,1% 17,4%

24,5%

8,0%

48,9%

0%

10%

20%

30%

40%

50%

60%

Midrand, Gauteng KwaZulu Natal Western Cape Eastern Cape Free State

32

Growth 20.1%

Results presentation 2012

Highlights - Logistics

Contended with 16% increase in diesel price

Operating margin improves to best ever at 3.5%

Take-on of all newly acquired brands concluded: 43% increase in line items ex-warehouse

Owner driver model continues to gain momentum: 49% and 41% of volume delivered from KZN and Western Cape respectively

New Nelspruit depot commissioned

33

Contended with 16% increase in diesel price price Contended with 16% increase in diesel price

Operating margin improves to best ever at 3.5% at 3.5% Operating margin improves to best ever at 3.5%

Take-on of all newly acquired brands concluded: 43% increase in line items concluded: 43% increase in line items Take-on of all newly acquired brands concluded: 43% increase in line items

Owner driver model continues to gain momentum: 49% and 41% of volume momentum: 49% and 41% of volume Owner driver model continues to gain momentum: 49% and 41% of volume

New Nelspruit depot commissioned New Nelspruit depot commissioned

Financial results

Results presentation 2012

Salient features

F 2012 % Change

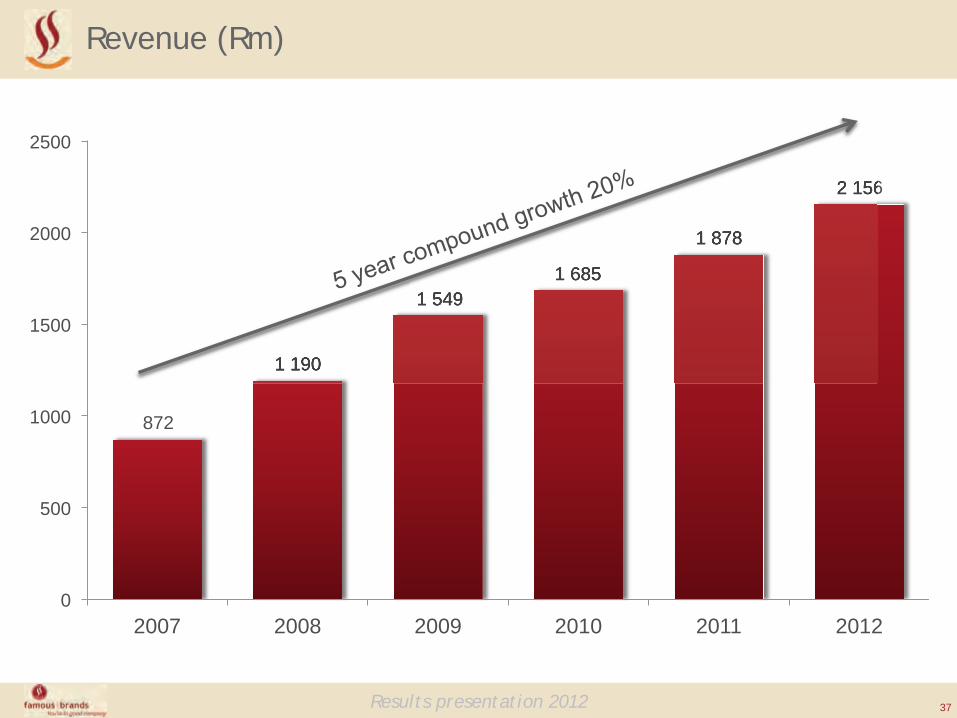

Revenue (Rm) 2 156 15

Operating profit (Rm) 413 15

Cash generated by operations before changes in working capital (Rm) 452 15

Earnings per share (cents) 278 15

Headline earnings per share (cents) 278 15

Total dividends per share (cents) 200 29

Net debt/equity (%) 10 14 (py)

Dividend cover (times) 1.4 1.6 (py)

Return on equity (ROE) (%) 35 36 (py)

35

Results presentation 2012

Income statement

Rm F 2012 F 2011 %

Revenue 2 156 1 878 15

Cost of sales (1 233) (1 065)

Gross profit 923 813 14

Selling and administrative expenses (510) (455)

Operating profit 413 358 15

Net interest paid (11) (15)

Profit before tax 402 343 17

Taxation (134) (112)

Profit for the year 268 231 16

Adjustments (1) -

Headline earnings (Rm) 267 231 16

Headline earnings per share (cents) 278 242 15

Earnings per share (cents) 278 242 15

36

Results presentation 2012

Revenue (Rm)

0

500

1000

1500

2000

2500

2007 2008 2009 2010 2011 2012

37

872

1 190

1 549 1 685

1 878

2 156

1 190

1 549 1 685

1 878

2 156

Results presentation 2012

Operating profit (Rm)

151 217

262 308

358 413

17,3%

18,3%

16,9%

18,3%

19,1%

19,1%

15,5%

16,0%

16,5%

17,0%

17,5%

18,0%

18,5%

19,0%

19,5%

0

50

100

150

200

250

300

350

400

450

2007 2008 2009 2010 2011 2012 Operating Profit Operating Margin

38

358 413 413

17,3% 17,3% 17,3% 17,3%

18,3% 18,3% 18,3%

16,9% 16,9%

18,3% 18,3% 18,3%

19,1%

19,1% 19,1%

Results presentation 2012

Statement of financial position (Rm)

F 2012 F 2011 Move

Assets

Property, plant and equipment 156 131 25

Intangible assets 695 660 35

Working capital 128 77 51

979 868 111

Funding Equity 840 709 131

Net borrowings 82 101 (19)

Deferred liabilities and current tax balances 57 58 (1)

979 868 111

39

Results presentation 2012

Cash flow (Rm)

86 41

0

50

100

150

200

250

300

350

400

450

500

Opening cash Closing cash

40

!"#$!%&$

399 Cash from operations

132 Tax

159 Dividends

84 Capex (net)

11 Interest

58 Funding (net)

Results presentation 2012

Segmental analysis

% of Total

F 2012 Rm

F 2011 Rm

Change %

Revenue Franchising – Local 20 440 386 14

Supply chain 76 1 614 1 383 17

United Kingdom 4 82 95 (13)

Corporate 20 14

100 2 156 1 878 15 Operating Profit Franchising – Local 64 265 235 13

Supply chain 34 141 116 21

United Kingdom 2 7 11 (30)

Corporate - - (4)

100 413 358 15

Operating Margin % % Franchising – Local 60.2 60.9 Supply chain 8.7 8.4 United Kingdom 9.2 11.3 Group 19.1 19.1

41

Board changes

Results presentation 2012

Stanley Aldridge Kevin Hedderwick Bheki Sibiya

Panagiotis Halamandaris Periklis Halamandaris

Theofanis Halamandaris John Lee Halamandres

Hymie Levin Christopher Boulle

Board changes

43

Strategy and prospects

Results presentation 2012

Strategy

Pursue acquisitive brand growth in new markets Pursue acquisitive brand growth in new markets Pursue acquisitive brand growth in new markets

Leverage our exclusive Netcare hospital service provider status Leverage our exclusive Netcare hospital service provider status Leverage our exclusive Netcare hospital service provider status

Build manufacturing capability, push for new business - existing plants and new opportunities Build manufacturing capability, push for new business - existing plants and new opportunities Build manufacturing capability, push for new business - existing plants and new opportunities

Expand logistics capability - capacity and owner driver Expand logistics capability - capacity and owner driver Expand logistics capability - capacity and owner driver

Build procurement capability and further develop “lowest cost producer” status Build procurement capability and further develop “lowest cost producer” status Build procurement capability and further develop “lowest cost producer” status

Open 250 new restaurants - 47 in rest of Africa Open 250 new restaurants - 47 in rest of Africa Open 250 new restaurants - 47 in rest of Africa

Embark on a major step change surrounding innovation - leverage our investment in “the Mad Lab” Embark on a major step change surrounding innovation - leverage our investment in “the Mad Lab” Embark on a major step change surrounding innovation - leverage our investment in “the Mad Lab” Improve and expand our retail and wholesale market presence Improve and expand our retail and wholesale market presence market presence

45

Results presentation 2012

Prospects

Consumer spending, especially middle income, expected to be muted Consumer spending, especially middle income, expected to be muted Consumer spending, especially middle income, expected to be muted

Competitive climate and category fragmentation will persist Competitive climate and category fragmentation will persist Competitive climate and category fragmentation will persist

Margins will continue to come under pressure, across the total business Margins will continue to come under pressure, across the total business Margins will continue to come under pressure, across the total business

Speed, convenience, innovation and value for money will remain key drivers Speed, convenience, innovation and value for money will remain key drivers Speed, convenience, innovation and value for money will remain key drivers

The Group will remain a sound business / investment proposition The Group will remain a sound business / investment proposition The Group will remain a sound business / investment proposition

46

Results presentation 2012

Questions

47

You’re in good company You’re in good company You’re in good company

Results presentation for the year ended 29 February 2012

Group information

Results presentation 2012

Strategic intent

Our business is focused on growth and development of

best-in-class franchised leisure brands supported by a business model which

maximises stakeholder value creation

50

Results presentation 2012

Famous Brands “Recipe”

Our primary orientation remains that of an integrated franchise system Our primary orientation remains that of an integrated franchise system Our primary orientation remains that of an integrated franchise system Building great and enduring brands will always be our obsession Building great and enduring brands will always be our obsession Building great and enduring brands will always be our obsession Our franchisees are our #1 customer and we must unshakeably offer them a business model that works Our franchisees are our #1 customer and we must unshakeably offer them a business model that works Our franchisees are our #1 customer and we must unshakeably offer them a business model that works We must be consumer driven – always affordable, available and accessible We must be consumer driven – always affordable, available and accessible We must be consumer driven – always affordable, available and accessible

Within our industry we will be the lowest cost producer Within our industry we will be the lowest cost producer Within our industry we will be the lowest cost producer

We will stay out of anything that is not leisure, food and beverage We will stay out of anything that is not leisure, food and beverage We will stay out of anything that is not leisure, food and beverage Remain a ‘family’ but never lose our high performance culture Remain a ‘family’ but never lose our high performance culture Remain a ‘family’ but never lose our high performance culture South Africa and rest of Africa are our #1 priority trading markets South Africa and rest of Africa are our #1 priority trading markets South Africa and rest of Africa are our #1 priority trading markets

51

Results presentation 2012

Business model

Franchising division

International - Houses the Group’s offshore intellectual property and brands This division is responsible for development of the existing Wimpy brand Domestic Mainstream Brands - Houses the Group’s brands that are of a mainstream nature, namely those brands which have broad consumer appeal and are wholly-owned trademarks. Whilst contained within a single business unit, the model of ‘brand stewardship’, or competition between brands is firmly entrenched through standalone strategic structures Domestic Developing Brands - Houses brands that are in a development phase, or are being restructured to compete tactically within clearly defined trade channels Theatre of Food Brands - Houses the Group’s niche brand trademarks which are held through joint venture partnerships in which the Group has a controlling interest

Franchising division Franchising division

52

Results presentation 2012

Business model

MAD Lab MAD is the acronym for Marketing . Artistry . Design. This newly created business unit has been established to bring about a significant step change in the Group’s marketing, new product development and restaurant design functions

MAD LabMAD Lab

Food Services Responsible for extending the Group’s trademarks into the FMCG retail and wholesale markets

Food Services Food Services

Procurement Custodian of the Group’s centralised procurement function. Accountable for procurement of all product, capital equipment, services and the like. Also serves as the Group’s sales forecasting and stock movement resource

Procurement Procurement

Development Provides a turnkey service to all of the Group’s brands and their respective franchise partners, offering a comprehensive range of services surrounding all new restaurant openings, revamps and relocations

Development Development

53

Results presentation 2012

Business model

New business Responsible for the centralised processing and approval of all new franchisee and landlord / developer enquiries. Accountable for all lease negotiations ensuring optimum rental agreements are negotiated on behalf of our franchise partners. Resourced also to manage the Group’s strategic alliance partners

New businessNew business

Manufacturing Represents a key part of the Group’s backward integration model, tasked with manufacturing a range of licensed products for use by the franchise network. Also accountable for quality assurance of all manufactured and outsourced products required by the various brands

Manufacturing Manufacturing

Logistics Represents the Group’s route-to-market, delivering to the franchise network a complete basket of products required for brand-specific menus

Logistics Logistics

Corporate Houses the Group’s ‘back of house’ functions which provide a service to the various operating business units

Corporate Corporate

54

Results presentation 2012

Current shareholding

Coronation Life Managers

Peter Halamandaris

Theofanis Halamandaris

Perikles Halamandaris

John Halamandres

Enderle SA (Pty) Ltd

Other

55

28.7%

11.7%

10.4% 8.2%

6.3%

5.0%

29.7%

Results presentation 2012

Operating profit – Local franchising

112 142

186 204

235 265

49,3%

54,8%

62,0% 62,5%

60,9% 60,2%

48%

50%

52%

54%

56%

58%

60%

62%

64%

0

50

100

150

200

250

300

2007 2008 2009 2010 2011 2012 Operating Profit Operating Margin

56

5 year compound growth 19% 62,0% 62,0%

62,5%

60,9% 60,2%

5 year compound growth 19%

5 year compound growth 19%

5 year compound growth 19%

Rm

Results presentation 2012

Operating profit – Supply chain

36

61 61

94 116

141

5,6%

8,1%

5,7%

7,8% 8,4%

8,7%

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

10%

0

20

40

60

80

100

120

140

160

2007 2008 2009 2010 2011 2012 Operating Profit Operating Margin

57

94 116

141

5,6% 5,6%

8,1%

5,7%

7,8% 8,4% 8,4%

8,7%

Rm

Results presentation 2012

Operating margin percentages – by division

49,3

54,8

62,0 62,5 60,9 60,2

17,3 18,3 16,9 18,3 19,1 19,1

10,9 9,6 10,1 11,3 9,2

5,6 8,1

5,7 7,8 8,4 8,7

0

10

20

30

40

50

60

70

2007 2008 2009 2010 2011 2012 Local Franchising Group United Kingdom Supply chain

58

Results presentation 2012

Operating margin percentages – Supply chain

9,5

7,3

9,7

11,7 11,7

2,1 2,4 3,0 3,0

3,5

0

2

4

6

8

10

12

14

2008 2009 2010 2011 2012 Manufacturing Logistics

59

Results presentation 2012

Ratios

42,0 45,2

37,4 38,2

42,5 44,5

36,1 38,0

33,4 36,1 35,7 34,5

2,4 2,5

2,2 2,1

2,2 2,3

2,4 2,2

2,1

1,8 1,6

1,4

1,0

1,5

2,0

2,5

3,0

3,5

4,0

0

5

10

15

20

25

30

35

40

45

50

2007 2008 2009 2010 2011 2012

Rona (%) ROE (%) Net Asset Turn (times) Dividend Cover (times)

60

% Times

Results presentation 2012

Ratios continued

3,5 4,3

5,2

6,2

7,4

8,7

7,0

30,3

45,8

27,5

14,3 9,7

0

5

10

15

20

25

30

35

40

45

50

0

1

2

3

4

5

6

7

8

9

10

2007 2008 2009 2010 2011 2012

Net asset value per share (R) (NAV) Debt/Equity (%)

61

NAV Debt/Equity %

Results presentation 2012

Consumer Recognition

62

BEST burger for the 16th consecutive year

BEST chips for the 14th consecutive year

BEST pizza for the 12th time

BEST coffee shop for the 12th consecutive year

BEST Breakfast

BEST New Restaurant

Source: Leisure Options

Results presentation 2012

Contact information

63

Kevin Hedderwick Chief Executive Officer +27 11 651 5812

Stan Aldridge Group Financial Director +27 11 651 5902

Del-Maree English Investor Communications +27 83 395 8608

You’re in good company You’re in good company You’re in good company

Results presentation for the year ended 29 February 2012