Life expectancy and healthy life expectancy in Scotland Alison Burlison, ISD ScotPHO team.

UBS CIO Wealth Management Research 3Q 2014

Your Wealth & Life

Navigating longevity

Personal strategies for wealth management

Inside: An interview with the head of MIT’s AgeLab, Joe Coughlin

ContentsNavigating longevity

02 Editorial

03 Introduction: Planning for longevity risk certainty

06 Interview: David McWilliams speaks with Joe Coughlin

08 Longevity planning for retirees

Safe spending rates, revisited Personal pensions Efficientwithdrawalstrategies Prudent leverage Demographics and asset returns

17 Millennials and longevity

Human capital, the hidden asset Human capital and asset allocation Insurance implications of a longer life Locatingassetsduringwealthaccumulation

23 Wealth transfer and legacy

Trusts:focusonflexibility Longevityandtheannualgifttaxexclusion Givingwhileliving

31 Disclaimer

Inearly2013,weasked2,056investorsabouttheirtopfinan-cial concerns (UBS Investor Watch,Q12013).Nearlyallofthetoptenresponseswerestrategicinnature.HowdoIknowifI’msavingenough?HowdoIknowifI’lloutlivemyassets?HowcanIavoidmajorfinancialmistakes?HowdoIprepare forhealthcareexpensesinretirement?HowdoIensurethefinancialwell-beingofmychildrenandgrandchildren?

Wewerenotsurprisedbytheseresults.Duringtherecoveryfollowingthefinancialcrisis,we’venoticedaseaofchangeinourclients’perspectivesaboutmanagingtheirwealth.Perhapsitwasarecognitiondrawnfromdevastatedhouseholdbalancesheetsin2008andearly2009,butachievinggoalshaselevatedinimportancewhereastheephemeral“outperformance”bogeyseemstohavetakenabackseat.

Inordertoaddressthesemore-strategicquestions,we’repleasedtolaunchthefirsteditionofournewquarterlyflag-ship, Your Wealth & Life.Thispublicationwillprimarilyfocusonwhatacademicsandpractitionersrefertoasthelifecycletheoryofwealthmanagement.

Ultimately,savingsandinvestmentarevehiclesforshiftingconsumptionintothefuture,butasmanyinvestorshavedis-covered,successfullyaccomplishingthattaskisfraughtwithchallenges.Withthisnewflagshipreport,weendeavortoofferrigorousanswerstotheseveryimportanttopics.

Ourfirsteditionfocusesonlongevity.Whetheryou’re25,55or75,thechangingnatureofhumanlongevityimpactshowyoushouldsave,invest,plan,spend,give,andbequest.Wehopeyoufindthiscomprehensiveoverviewbothinterestingand enlightening.

Dear reader,

MichaelCrook

MikeRyan

Mike Ryan, CFAChief Investment Strategist, WMARegional CIO, Wealth Management US

Michael Crook, CAIAHead of Portfolio & Planning Research

CIO, Wealth Management US

2 September2014Your Wealth & Life

Your Wealth & LifeSeptember20143

Introduction Planning for longevity risk certainty

Michael Crook, CAIA, Head of Portfolio & Planning Research

Imagineyouwerea40-year-oldmalein1940.Youhadsurviveda15%chanceofpassingawayduringyourfirstyearoflife(anda1.5%probabil-ityofpassingawayduringWWI),butyourfuturemortalityremainedveryuncertain.Eventhoughyourremainingmedianlifeexpectancywasprettyreasonableat30to40moreyears,youhadaslightlyhigherprobabilityofpassingawayinyourmid-60sthaninyourmid-80s.1Livingwellintoyour80sand90swasafairlylow-probabilityrisk.Certainlysuchanoutlookwouldhaveanimpactonhowyousavedandinvestedoveryourlifetime.

4 September2014Your Wealth & Life

Introduction

Fast forward to 2014Theoutlookforlongevityhasshiftedsignifi-cantly.Notonlyhasinfantmortalitydeclinedbyover98%in100years,butdueinparttomajorpublichealthgains,likedeclinesinsmoking-related illness and car fatalities, end-of-life lon-gevityhasimprovedsignificantlyaswell.Peopleare living longer, healthier lives. Mostlongevitydiscussionsfocusonextensionsofmedianlifeexpectancy.Thesehavebeenimpres-siveandshouldn’tbeunderstated–particularlybecausemanystudiesindicateindividualssys-tematicallyunderestimatehowlongtheywilllive.2Lifeexpectancyfora65-year-oldintheUSjumpedfrom12.7yearsto15yearstonearly20yearsbetween1940,1970,and2010,respec-tively.3Keepinmindthatlifeexpectancynum-bersaremediannumbersandthatfullyhalfofall65-year-oldswilllivepastthemedianexpectancy. Assuch,usingmedianlifeexpectancynumbersdesigned to represent an entire population can beamisleadingguidetolongevity.Becauseoffactorssuchasobesityandsocioeconomic

status,“average”longevitycanbehighlyvariedamongdifferentpopulationsandcohorts.Forinstance,individualsthatretainahealthybodymassindexthroughouttheirlivescanreasonablyadd2to3yearstothemediannumbers.

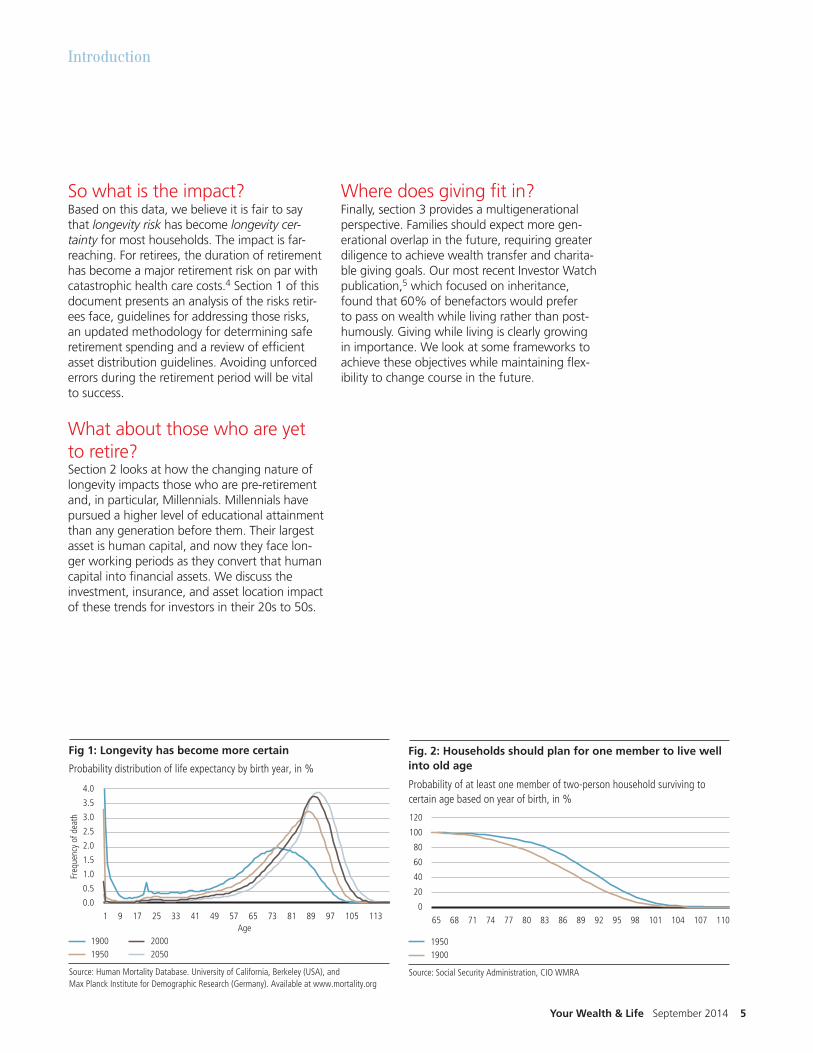

Perhapsanequallyimportantbutoftenover-lookedaspectoflongevityisthechangingdistri-butionofmortalityoverthelifecycle(seeFig.1).Only50yearsago,a65-year-oldfacedroughlyanequalprobabilityofdeatheveryyearuntiltheywere85,atwhichpoint80%hadpassedaway.Asitisnow,deathwasguaranteed;onlythetimingofitwasextraordinarilyuncertain. Today,thedistributionsurroundingtheproba-bilityofdeathhasbecomemuchmorepeaked.Survivalintoaperson’s80sand90sismuchmorelikely.Infact,anaverage65-year-oldfemaletodayhasagreaterthan30%chanceoflivingto90.Survivorshipoddsforacouplecompound these statistics further. There’s a 50%probabilitythatatleastonememberofatwo-personhouseholdcurrentlyaged65willlivetobe90.

25%Decline between 1981 and 2009 in age-adjusted death rate for all causes of death among people age 65 and over.2

Retirement ≠ Old84% of investors say retirement is not a sign of being old (UBS Investor Watch).1

50%Decline in death rates for heart disease and stroke between 1981 and 2009.2

Lung cancerThe decrease in smok-ing has been a major factor in the decline of the US cancer death rate overall – especially the lung cancer death rate among men.3

Feeling goodDuring the period of 2008–2010, 76 percent of people age 65 and over rated their health as good, very good, or excellent.2

Wheredoesgivingfitin?Finally,section3providesamultigenerationalperspective.Familiesshouldexpectmoregen-erational overlap in the future, requiring greater diligencetoachievewealthtransferandcharita-blegivinggoals.OurmostrecentInvestorWatchpublication,5whichfocusedoninheritance,foundthat60%ofbenefactorswouldprefertopassonwealthwhilelivingratherthanpost-humously.Givingwhilelivingisclearlygrowinginimportance.Welookatsomeframeworkstoachievetheseobjectiveswhilemaintainingflex-ibilitytochangecourseinthefuture.

Sowhatistheimpact?Basedonthisdata,webelieveitisfairtosaythat longevity riskhasbecomelongevity cer-tainty for most households. The impact is far-reaching.Forretirees,thedurationofretirementhasbecomeamajorretirementriskonparwithcatastrophic health care costs.4 Section 1 of this documentpresentsananalysisoftherisksretir-eesface,guidelinesforaddressingthoserisks,anupdatedmethodologyfordeterminingsaferetirementspendingandareviewofefficientassetdistributionguidelines.Avoidingunforcederrorsduringtheretirementperiodwillbevitalto success.

Whataboutthosewhoareyetto retire?Section2looksathowthechangingnatureoflongevityimpactsthosewhoarepre-retirementand, in particular, Millennials. Millennials have pursued a higher level of educational attainment thananygenerationbeforethem.Theirlargestassetishumancapital,andnowtheyfacelon-gerworkingperiodsastheyconvertthathumancapitalintofinancialassets.Wediscusstheinvestment, insurance, and asset location impact ofthesetrendsforinvestorsintheir20sto50s.

Source: Human Mortality Database. University of California, Berkeley (USA), andMax Planck Institute for Demographic Research (Germany). Available at www.mortality.orgor www.humanmortality.de (data downloaded on 7/30/2014); CIO WMRA

19501900 2000

2050

2.0

1.5

0.0

0.5

1.0

3.5

3.0

2.5

4.0

1 9 17 25 33 41 49 57 65 73 81 1059789 113

Fig 1: Longevity has become more certain

Probability distribution of life expectancy by birth year, in %

Freq

uenc

y of

dea

th

Age

Source: Social Security Administration, CIO WMRA

19001950

40

20

0

100

80

60

120

65 68 71 74 77 80 83 86 89 92 95 10410198 107 110

Fig. 2: Households should plan for one member to live wellinto old age

Probability of at least one member of two-person household surviving tocertain age based on year of birth, in %

Your Wealth & LifeSeptember20145

Introduction

David McWilliams: You recently conducted a survey that looked at concerns about the future. What were the top concerns that the participants reported?

Joe Coughlin: Weconductedanonlinestudytobetterunderstand,acrossthelifespanregardlessofgeneration,theworriesthatpeoplehavefortheirfutureolderlives.Considerthefollowing:youarelikelytoliveatleast20,30,maybeeven40yearspastretirementageifyouchooseyourparentswellandmanageyourownwell-being.Wewantedtounderstandhowdifferentagegroupsthoughtaboutthoseconcerns.Acrossallgroupsthenumberoneconcernwasfinan-cialstability.Healthcertainlybecomesatop-tworelatedissue–butagainthedefinitionofcon-cernabouthealthisalsotiedtowhosehealthyouareconcernedabout.Whenyou’reyoungerit’saboutyou.Whenyou’reolder,andthatstartstochangearound55,westartbeingmorecon-cernedaboutthehealthandwealthofothers.

In what other ways do concerns change based on age?Inthe45-to54-year-oldgroupthenumberoneconcernisindeedfinancialstability.It’snotjustamatterofhowmuchmoneywillIhave,butwillIhaveastableandsteadyincometohavethelifestylethatIwant.Andthatbeginstochangealittlelateron.Now,there’sanumberofotherissuesthatbecomemorepronouncedasweage.Findingcare,makingsurethatwehaveaccesstocarethatwemayneed,lossofcognitivefunc-tion,etc.It’sveryinterestingthatinmanycasesdeathislessofafearthanlossofcognitiveabil-ityduetoAlzheimer’sordementia.Nextwaslossofmobility,whichbeginswithdriving.Thinkaboutthis:70%ofAmericansoverage50live

insuburbanandruralareas.Chancesaretheydon’tlivenearmasstransitorwithinwalkingdistanceofmostplaces.Iftheydon’tdrive,theybecomeeffectivelyprisonersintheirownhomes.

I’m just surprised you’re worried about mobility when you’re 54 years old. Thinkaboutwhatyou’redoingwhenyouare45to54.You’recallingyourparentsnotjusttosayhello.You’recallingyourparentsoftentothankGodthattheyanswerthetelephone.SoIthinkthat’swhereyoustarttoseethatyourownagingasarealconcern.Andfranklythisisaper-fecttimeforthinkingabouthowtomanagethecomplexitiesofretirement.

Okay – that’s helpful. Then what happens when you reach your mid-50s and early 60s?Financialstabilityisstillnumberone,butnowyoustarttobecomemoreconcernedaboutyourgrandchildrenandtheirchildren’sfinancialstabil-ity.Butreallywhatchangesprofoundlyisthenextconcern–lossofcognitivefunction.Manyofourrespondentsbegintothinkabouthavingtoplanforthepossibilityoflong-termcareformemoryloss,forformalcareathome,forthetimewhenyouoryourpartnermightlosecognitiveabil-ity.Somethingthatistotallynewasareportedconcernforthisgroupisthefearofbecomingaburden.Beginninginthe60’s,respondentsshow

Interview David McWilliams, Head of Wealth Management Transformation at UBS,recentlysatdownwithJoseph F. Coughlin, Ph.D., Director of the MassachusettsInstituteofTechnologyAgeLab.Hisresearchexamineshowthedisruptivedemographicsofanagingsociety,socialtrendsandtechnol-ogywillshapefutureinnovationsinbusinessandgovernment.Wefeatureexcerptsoftheirdiscussionbelow.

You may be able to climb that ladder at age 80 or 85, but do you want to take the risk, and do you want to hear your spouse or your adult children yelling at you as you’re doing it?

6 September2014Your Wealth & Life

The last one, “Who will you have lunch with?”Yes,“Whowillyouhavelunchwith?”Andcommonsenseandverygoodsocialbehavioralresearch has demonstrated that a strong social networkiscriticaltoagingwell.Arecentmedi-calstudycameoutshowingthat60%ofolderadults over the age of 70 come into hospital emergencyroomsmalnourished,regardlessofincomeandeducation.Why?They’renoteat-ingcorrectly.Andoneofthereasonsthey’renot,particularlywomenwholivealone,isthateat-ingisasocialactivity.Wemakemeals,wehavecelebrations,weenjoybreakingbreadwithoth-ers.However,whenwelivebyourselvesorwedon’thavethatstrongsocialnetwork,wetendtogetalittlelazyandallofasuddenasliceofcheeseandawiltedpieceoflettucebecomesameal.Soweneedtohavefriendsaroundtorein-forcehealthybehaviors,togetusout,toensurethatweadheretoourmedicationregimens,justfranklytoremainvitalpeople.Ifyou’regoingtobeliving20or30yearsbeyondretirement,that’saboutthesamedistanceyouhadfromhigh school graduation to midlife crisis. That’s a longtimeandyouneedalonglistofthingstoremainhealthy,happy,vitalandinteresting.

Any final thoughts?Ithinktheonethingthatwetendtoforgetaboutisthatasweageandaswechange,retirementhasgottenfarmorecomplexthaneverbefore.Wenowneednotjustanadvi-sor,notjustafinancialplanner,butsomeonetohelpusnavigatelongevity.Wearenowliv-inginatimeinwhichwehavefewerchildrenwithus,andwehavenorealmentalmodelorexampleofwhatourparentsdidinthesamesituation.Thelast20to30yearsofourlifecanbeamongthemostcomplextimes.Andsoaswethinkaboutplanningforretirement,theconcernshouldbe“WhatamIgoingtodoandneedregardingresources?Myphysical,cogni-tive,financial,andsocialresourceswillbecomestrained in old age. What do I need to do to ensurethehighestqualityoflifeIcanhave?”

interestonwhatarethethingsthatIcandotoplantoavoidbecomingaburden,notjusttomypartnerbuttomyadultchildrenaswell.

You sometimes use three questions, I under-stand, to illustrate needs in retirement. Why do you choose these questions and what do they mean? Ithinkoneofthethingsthatweneedtostartthinkingaboutis,“Arewedoingretirementplan-ning,arewedoingfinancialplanning,orarewedoinglongevityplanning?”SoIposedthreeques-tionsthatareprofoundlysimple,butthey’rethepartsofretirementwenevertalkabout.Wetalkaboutvolunteering,wespeakofvacations,wespeakofgrandchildren.Thosearethethingswelookforwardto,butthere’salsothemundanethatweoftendon’tthinkabout.Thefirstques-tionis“Whowillchangeyourlightbulbs?”Wetendtoforgetthatthelittlethingswedoeverydayreallycontributetoourcapacitytoremainindependent.Youmaybeabletoclimbthatlad-deratage80or85,butdoyouwanttotaketherisk,anddoyouwanttohearyourspouseoryouradultchildrenyellingatyouasyou’redoingit?Soyouhavetostartthinkingnow,“Whatisthecostandtheplanningnecessaryforservicesto‘age-in-place,’tomakeitpossibleforyoutostayinthehomethatyouwanttobein?”

I think this is spectacular. Well your next one is, “Where will you get an ice-cream cone?”Yes,wellthisismyfavorite.AndthisislargelybecauseoriginallywhenIstartedstudyingagingIstartedstudyingitfromatransportationpointofview.Forme,chocolateice-creamisahugequalityoflifeissue.Butthinkaboutthefol-lowing:ifyoudonotdriveoryoucannotwalktoyourfavoriteicecreamshop,howwillyougetthere?Areyougoingtotakeataxi?Areyougoingtocallafriend?AreyougoingtobotheranadultchildforthatlittlespontaneousmomentonahotJulynightwhenyousimplywantachocolatesoftserve?Theanswerisprob-ably‘no.’Andwhilethecapacitytohavethatice-creamconeisaboutseamlesstransportation,italsohighlightstheimportanceof,whatyou’replanningforthat20,30,maybeeven40yearsofretirement,ensuringthatyouknowandhaveaccesstowhatisdesired,notjustneeded.

Interview with Joe Coughlin

Joe Coughlin and David McWilliams are employees of MIT and UBS Wealth Management Transformation, respectively. They are not members of CIO Wealth Management Research (CIO WMR). CIO WMR may have views that differ or are contrary to the views expressed herein.

Your Wealth & LifeSeptember20147

8 September2014Your Wealth & Life

Longevity planning for retirees

Retiredinvestorsfaceamultitudeofrisks,allofwhichfoldupintoasingleoverarchingone:longevity.Willyououtliveyourmoney?Inadditiontofocus-ingoninvestmentreturnsandspendingrates,weendorseacomprehensiveapproachthatincludesmoreefficientmanagementofliabilities,anintelligentwithdrawalstrategyandgreaterincorporationofannuities.

Longevity:Althoughmortalitydataindicatesthatliving30ormoreyearsafterretirementisincreasinglylikely,longevityremainsariskfromaport-foliostandpoint.31%ofthevarianceintherequiredstartingvalueinourmodelwasduetouncertaintyaroundlongevity.Notonlydolongerretire-mentdurationsincreasetheriskthatanotherriskwilleventuallyoccur,buttheysignificantlyincreasethedollaramountofassetsnecessarytoinitiallyfundretirement.Broad-basedfinancialplanningonaconsistentbasisisthefirststepformanaginglongevityriskoverthecourseofretire-ment,butaddinganexplicitlongevityhedgeintheformofadeferredannuityshouldbeacorepartofmosthouseholds’balancesheets.– continues next page

The risks facing retirees (in order of relative importance)

31%

A multitude of risks, all surmountableTheGreatRecessionandfollowingperiodoflowinterestratesandanemiceconomicgrowthhavehighlightedtherisksfacedbyinvestorsnearingretirement.Unfortunately,manyretireesdon’tfeelliketheyhaveasolidgraspoftherelativesignificanceofthemajorriskstheyfaceduringretire-ment.Asaresult,wehavedevelopedamarket-basedforward-lookingmeasureofthecontribu-torstoastartingbalancethatisneededforasuccessfulretirement(definedasnotrunningoutofmoney).Wehopeitcanhelpbetterillustratewhichfactorsaremostimportanttomanagingfinancesduringretirement.

Michael Crook, CAIA, Head of Portfolio & Planning Research

Your Wealth & LifeSeptember20149

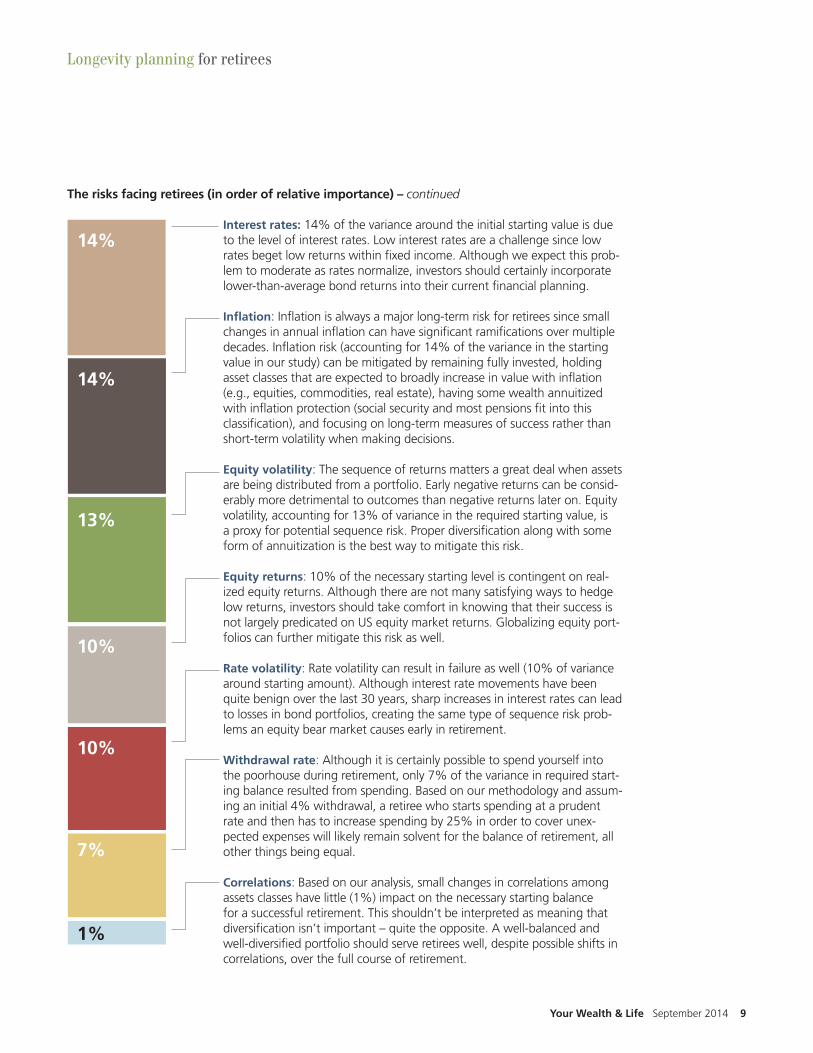

Interest rates:14%ofthevariancearoundtheinitialstartingvalueisduetothelevelofinterestrates.Lowinterestratesareachallengesincelowratesbegetlowreturnswithinfixedincome.Althoughweexpectthisprob-lemtomoderateasratesnormalize,investorsshouldcertainlyincorporatelower-than-averagebondreturnsintotheircurrentfinancialplanning.

Inflation:Inflationisalwaysamajorlong-termriskforretireessincesmallchangesinannualinflationcanhavesignificantramificationsovermultipledecades.Inflationrisk(accountingfor14%ofthevarianceinthestartingvalueinourstudy)canbemitigatedbyremainingfullyinvested,holdingassetclassesthatareexpectedtobroadlyincreaseinvaluewithinflation(e.g.,equities,commodities,realestate),havingsomewealthannuitizedwithinflationprotection(socialsecurityandmostpensionsfitintothisclassification),andfocusingonlong-termmeasuresofsuccessratherthanshort-termvolatilitywhenmakingdecisions.

Equity volatility:Thesequenceofreturnsmattersagreatdealwhenassetsarebeingdistributedfromaportfolio.Earlynegativereturnscanbeconsid-erablymoredetrimentaltooutcomesthannegativereturnslateron.Equityvolatility,accountingfor13%ofvarianceintherequiredstartingvalue,isaproxyforpotentialsequencerisk.Properdiversificationalongwithsomeformofannuitizationisthebestwaytomitigatethisrisk.

Equity returns:10%ofthenecessarystartingleveliscontingentonreal-izedequityreturns.Althoughtherearenotmanysatisfyingwaystohedgelowreturns,investorsshouldtakecomfortinknowingthattheirsuccessisnotlargelypredicatedonUSequitymarketreturns.Globalizingequityport-folioscanfurthermitigatethisriskaswell.

Rate volatility:Ratevolatilitycanresultinfailureaswell(10%ofvariancearoundstartingamount).Althoughinterestratemovementshavebeenquitebenignoverthelast30years,sharpincreasesininterestratescanleadtolossesinbondportfolios,creatingthesametypeofsequenceriskprob-lemsanequitybearmarketcausesearlyinretirement.

Withdrawal rate:Althoughitiscertainlypossibletospendyourselfintothepoorhouseduringretirement,only7%ofthevarianceinrequiredstart-ingbalanceresultedfromspending.Basedonourmethodologyandassum-inganinitial4%withdrawal,aretireewhostartsspendingataprudentrateandthenhastoincreasespendingby25%inordertocoverunex-pectedexpenseswilllikelyremainsolventforthebalanceofretirement,allotherthingsbeingequal.

Correlations:Basedonouranalysis,smallchangesincorrelationsamongassetsclasseshavelittle(1%)impactonthenecessarystartingbalanceforasuccessfulretirement.Thisshouldn’tbeinterpretedasmeaningthatdiversificationisn’timportant–quitetheopposite.Awell-balancedandwell-diversifiedportfolioshouldserveretireeswell,despitepossibleshiftsincorrelations, over the full course of retirement.

The risks facing retirees (in order of relative importance) – continued

Longevity planning for retirees

14%

14%

13%

10%

10%

7%

1%

10 September2014Your Wealth & Life

Although our research indicates that spending is onlyoneofmanyimportantfactorsthatcontrib-utetotheriskoffailureinretirement,balancingconsumptionwithbequestandcharitablegoalscanbequitechallengingasinvestmentportfo-liosriseandfall,householdsage,andobjectivesevolve over time. Manyhouseholdshavebeeninfluencedbythesafewithdrawalrate(SWR)concept,colloquiallyknownasthe“4%rule.”The4%rulesaysthata65-year-oldcanwithdraw4%oftheassetsfromherportfolioduringthefirstyearofretire-ment,growthoseassetsbyinflationinsubse-quentyears,andhaveaminimalprobabilityofrunningoutofmoneyoverthenext30years.The“4%”numberonlyhasrelevanceduringthefirstyearofretirementsincespendingisthengrownbyinflation–resultinginaconstantstan-dardoflivingduringtheretirementyears.

The4%ruleiseffectivebecauseitissimpleandeasytoapply,buttherearealsomajorproblemsthatlimititsutility.First,thenatureofthe4%rule detaches spending from changes in portfolio value.Theresponsefunctioneachyearisexactly

thesame–increasespendingbyinflation–nomatterhowwellorpoorlytheportfoliohasper-formed.Thedetachmentfromrealityalsotendstomakeittooconservativebecause,withoutanyadjustmentovertime,therulehastobeori-entedtowardworst-caseoutcomes.Additionally,aspendingruleshouldincorporatelongevityandrecognizethataprudentconsumptionlevel,asapercentage of portfolio value, is higher for those intheir80sthanthoseintheir60s.Ultimately,followingthe4%rulehasresultedinportfoliosthathavegrownby100%ininflation-adjustedtermsoverthecourseofretirement–assetsthatcouldeasilyhavebeenusedtoimprovethestan-dard of living during retirement. Instead,amoreeffectiverulewouldbeonethatinitiatesspendingataprudentlevel,butenablesforstep-upsbasedongoodportfolioperfor-manceanddecreasinglifeexpectancywithoutleavingthehouseholdsubjecttotheneedtoreducelivingstandards.Wecallthisadynamicsafe depletion rate (DSDR).

TheDSDRworkslikeanSWRinthatitisaspeci-fiedinflation-adjustedamountofspendingthatcanbemaintainedthroughretirement,withtheimportant caveat that it is revised on an annual basis.Essentially,eachyearthehouseholdspendsthegreaterof(1)lastyear’sspendingadjustedforinflation(thesameasanSWR)or(2)thecurrentportfoliovaluemultipliedbythenewDSDR.Thatnewspendinglevelsetsanupdatedflooronfuturespending,withthepossibilityoffurtherincreasesbasedonmarketperformance.These potential step-ups are important (and can bequitesizable),particularlyduringthefirst10

Safe spending rates, revisited

Longevity planning for retirees

Source: MSCI, UBS CIO WMR

50

40

30

20

10

0

70

60

80

31 7 2725232119171513119 29 315

Fig. 2: A dynamic approach can enable increased consumption

Average inflation-adjusted spending per year, in thousands USD

4% RuleDSDR

Michael Crook, CAIA, Head of Portfolio & Planning Research

Fig. 1: Dynamic safe depletion rates

DSDR based on retirement horizon

Retirement Duration

DSDR Retirement Duration

DSDR

30 4.0% 22 4.5%

29 4.1% 21 4.6%

28 4.1% 20 4.8%

27 4.2% 19 4.9%

26 4.2% 18 5.0%

25 4.3% 17 5.2%

24 4.4% 16 5.5%

23 4.4% 15 5.7%

Source: MSCI, UBS CIO WMR

Your Wealth & LifeSeptember201411

to15yearsofretirementwhenmanyhouse-holdsreportthattheywouldprefertoprudentlymaximizespending.1

Basedondatafrom1963to2013,Fig.1pro-videsDSDRsforaportfoliocomprisedof50%large-capequities,10%small-capequities,and40%intermediate-terminvestment-gradecor-poratebonds,rebalancedannually.Again,thesearewithdrawalratesthatcanbemultipliedbythe current value of the portfolio to determine whetherornotaspendingstep-upisprudentbasedoninvestmentperformanceandupdatedretirementduration.Ofcourse,we’dadviseagainst using medianlifeexpectancyforsuchanexercise.Avaluethatreflectsatleastonemem-berofthehouseholdlivingintotheirmid-orlate-90sprovidesforahighermarginofsafety. ComparingtheresultsoftheDSDRstrategytothe4%ruleforthesameperiodfrom1963to2014isillustrativeinregardtothetrade-offs.Inregardtoconsumption,theDSDRenabledhouseholdstoprudentlyincreaseaveragespend-ingby40%and80%duringthefirst10and15yearsofretirement,respectively.Anexampleof this increase in consumption for a household startingwith1mmUSDcanbeseenbelow(seeFig.2).Thesespendingincreasestakeplacelead-inguptoandduringthe“mytime”(late-60stoearly-80s)phaseofretirement,duringwhichhouseholds report increased spending and a focus on travel and leisure. Thetrade-off,ofcourse,isthepotentialbequest.FollowingtheDSDRframeworkcertainlyleads,onaverage,tolowerterminalportfoliovalues.

However,corpusvaluesremainquitesubstantial–80%oftheinflation-adjustedvalueoftheini-tialportfolioafter30yearscomparedto200%forthe4%rule(seeFig.3).Suchanoutcomereflectsapreferablebalancebetweenconsump-tionandbequestformosthouseholdsandcan,ofcourse,betweakedupordowntoreflectpreferences in either direction.

Figure4illustratesinflation-adjustedconsump-tionpathsforthreedifferentretirementyearcohorts, assuming an initial portfolio value of$100:1968(ahorribleretirementcohort),1985(agoodretirementcohort),and1992(anaverageretirementcohort).Basedonabove-averagemarketreturns,theDSDRrulewouldhaveenabledhouseholdsinthe1985and1992cohortstosafelyincreasespendingby100%duringthefirstdecadeofretirement.Conversely,itwouldhaveprudentlyrestrainedspendingforthe1968cohortbasedonpoorratesofreturnandhighinflationduringthe1970s.

Ultimately,anyheuristicforretirementspend-ing,includingboththe4%ruleandtheDSDR,issimplyastartingpointfordiscussion.Safespendinglevelsarecontingentonmanyfactors,including asset allocation, asset location, and bequestmotives,allofwhicharelikelytochangeover the course of retirement. Comprehensive financialplanningistheonlywaytofullyincor-porateallofthehousehold-specificissuesneces-sarytomakeaprudentdecision.Accordingly,weadvisehouseholdstofeelcomfortableusingtheDSDRforguidancebasedonlong-termhistoricaldata,buttoupdatetheirfinancialplanbeforemakingbigshiftsinspendingduringretirement.

Source: MSCI, UBS CIO WMR

2,000

1,500

1,000

500

0

2,500

31 7 2725232119171513119 29 315

Fig. 3: Increased consumption results in lower terminal wealth

Real value of portfolio, in thousands USD

4% RuleDSDR

Source: MSCI, UBS CIO WMR

19851992 1968

8

6

0

2

4

14

12

10

16

1 3 5 7 9 11 13 15 17 19 21 272523 29

Fig. 4: Prudent spending step-ups can be substantial

DSDR step-ups based on retirement year

With

draw

al (r

eal,

$s)

Years aer retirement

Longevity planning for retirees

Pensionsaregenerallytreasuredretirementassetsbythosethatownthemsincetheyofferthe“definedbenefit”ofsafeinflation-adjustedincome streams for the duration of retirement. Theyeffectivelysolveinflationrisk,longev-ityrisk,andinvestmentriskallinoneproduct.Unfortunately,onlyabout40%1 of Americans overtheageof60arecoveredbydefined-bene-fitpensions,anumberthatisdecliningeachyear.

Fortunately,householdsarenotheldhostagetoemployersforattainingdefinedincomeinretirement. Those that don’t have access to pensionscan“pensionize”partoftheirport-foliothroughannuitization.However,thisisastepthatisrarelytaken.Oneexplanationisthatinvestorsappeartosuccumbtowhat’sknownastheendowmenteffect.Theyvaluethepensionsendowedtothemveryhighly,butarenotwillingtoconvertassetstoanannuityatretirement.

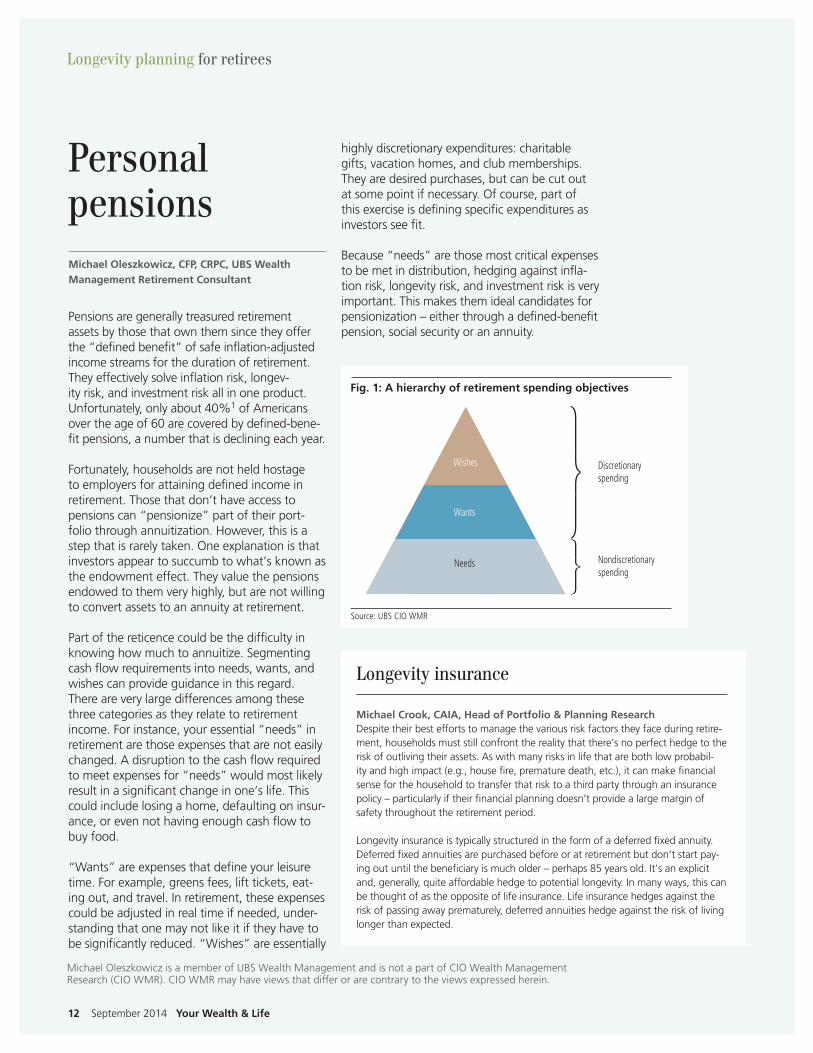

Partofthereticencecouldbethedifficultyinknowinghowmuchtoannuitize.Segmentingcashflowrequirementsintoneeds,wants,andwishescanprovideguidanceinthisregard.Thereareverylargedifferencesamongthesethreecategoriesastheyrelatetoretirementincome.Forinstance,youressential“needs”inretirementarethoseexpensesthatarenoteasilychanged.Adisruptiontothecashflowrequiredtomeetexpensesfor“needs”wouldmostlikelyresultinasignificantchangeinone’slife.Thiscould include losing a home, defaulting on insur-ance,orevennothavingenoughcashflowtobuyfood.

“Wants”areexpensesthatdefineyourleisuretime.Forexample,greensfees,lifttickets,eat-ingout,andtravel.Inretirement,theseexpensescouldbeadjustedinrealtimeifneeded,under-standingthatonemaynotlikeitiftheyhavetobesignificantlyreduced.“Wishes”areessentially

highlydiscretionaryexpenditures:charitablegifts,vacationhomes,andclubmemberships.Theyaredesiredpurchases,butcanbecutoutatsomepointifnecessary.Ofcourse,partofthisexerciseisdefiningspecificexpendituresasinvestorsseefit.

Because“needs”arethosemostcriticalexpensestobemetindistribution,hedgingagainstinfla-tionrisk,longevityrisk,andinvestmentriskisveryimportant.Thismakesthemidealcandidatesforpensionization–eitherthroughadefined-benefitpension,socialsecurityoranannuity.

Personal pensions

Longevity insurance

Michael Crook, CAIA, Head of Portfolio & Planning ResearchDespitetheirbesteffortstomanagethevariousriskfactorstheyfaceduringretire-ment,householdsmuststillconfronttherealitythatthere’snoperfecthedgetotheriskofoutlivingtheirassets.Aswithmanyrisksinlifethatarebothlowprobabil-ityandhighimpact(e.g.,housefire,prematuredeath,etc.),itcanmakefinancialsenseforthehouseholdtotransferthatrisktoathirdpartythroughaninsurancepolicy–particularlyiftheirfinancialplanningdoesn’tprovidealargemarginofsafetythroughouttheretirementperiod.

Longevityinsuranceistypicallystructuredintheformofadeferredfixedannuity.Deferredfixedannuitiesarepurchasedbeforeoratretirementbutdon’tstartpay-ingoutuntilthebeneficiaryismucholder–perhaps85yearsold.It’sanexplicitand,generally,quiteaffordablehedgetopotentiallongevity.Inmanyways,thiscanbethoughtofastheoppositeoflifeinsurance.Lifeinsurancehedgesagainsttheriskofpassingawayprematurely,deferredannuitieshedgeagainsttheriskoflivinglongerthanexpected.

Michael Oleszkowicz, CFP, CRPC, UBS Wealth Management Retirement Consultant

Longevity planning for retirees

Source: UBS CIO WMR

Fig. 1: A hierarchy of retirement spending objectives

Wishes Discretionaryspending

Nondiscretionaryspending

Wants

Needs

12 September2014Your Wealth & Life

MichaelOleszkowiczisamemberofUBSWealthManagementandisnotapartofCIOWealthManagementResearch(CIOWMR).CIOWMRmayhaveviewsthatdifferorarecontrarytotheviewsexpressedherein.

Your Wealth & Life August 2014 13

Mostinvestorsaccumulatethemajorityoftheirtotallifetimewealthbythetimetheyreachretire-ment.Withlowerincomestreamsbutpotentiallyhighercostsoflivinggoingforward,aninves-tor’sassetbasemustgeneratesustainablereturnscompatiblewithamodestspendingratethatgrowswithinflationovertime.Manyinvestorsearlyinretirementmightwronglybelievethattheirassetswillsafelycarrythemtoage80or90withahighdegreeofcertainty.Butfailingtoaccountforassetlocationinwithdrawalscandra-maticallyincreasetheriskofoutlivingone’sassets.

Asset location in the accumulation phase is a keydeterminantofaportfolio’slongevityinthewithdrawalphase.Reallocatingbetweentax-ableandtax-deferredaccountsisdifficult,anddramaticallyalteringthemakeupofone’stax-ableportfoliocanresultinlargetax-relatedandtransactioncoststhatincreaselongevityrisk.Ouranalysisindicatesthatminimizingunnecessarilylargetaxliabilitiesearlyinretirementisthelynch-pinofprolongingaportfolio’slongevity.Thisis

accomplishedbyoptimizingone’swithdrawalsbyassetlocation.

Figure1showsthebenefitofefficientwithdrawalpolicyinretirement.Itchartsthepathoftwoidenticalportfoliosheldbynewlyretired60-year-oldswith4%spendingrates,demonstratingthedramaticallydifferentresultsdependingontheorderinwhichthevariousaccountsaredepleted.Intheoptimalstrategy,requiredminimumdis-tributions(RMDs)fromtax-deferredaccountsarethefirstsourceofwithdrawalsalongwithcashflowsfromassetsheldintaxableaccounts.Nextcomeliquidationsofassetsheldintax-ableaccounts.Onlyaftertheseholdingsarefullydepleteddoessellingassetsheldintax-deferredaccountsbeyondRMDsbecomeprudent.

Investorswholiquidatetheirtax-deferredaccountstooearlywill,onaverage,severelycurtailtheirportfolios’longevity.Whyisthis?Withdrawalsfromtax-deferredaccountsaresubjecttoordinaryincometaxes,andtriggeringthosepotentiallyhightaxpaymentstoosoonintoretirementshrinksthebasefromwhichtheportfoliocangrowinfutureyears.Properassetlocationplacestheleasttax-efficientassetclassesintax-deferredaccountswhich,ifallowedtogrowtax-freeforlonger,cansupportaretiree’slifestyleforlongerandallowforalargerlegacygifttobeneficiariesorcharitiesupondeath.Ouranalysisshowsthata$10millionportfoliocanhaveitslongevityextendedbytentotwelveyearsiftheinvestormovesfromaninefficienttoanoptimalwithdrawalstrategy.Fig.2showsthe optimal order to fund retirees’ costs of living fromtheirassetbase.

Efficient withdrawal strategies

Source: UBS CIO WMR

$14$12$10

$8$6$4$2$0

$16

6559 77 8983 9571

Fig. 1: Efficient withdrawal strategy yields powerful results

Simulated retirement portfolio values in $mlns under different sequenceof withdrawals

Sell tax-deferred last Sell tax-deferred first

Longevity planning for retirees

Fig. 2: Avoid triggering highest tax liabilities early in retirement

Efficient sequence of withdrawal by account type for retirement spending needs

1. 401(k) or IRA required minimum distributions (70 1/2 & up)

2. Cash flows generated by assets in taxable accounts

3. Sale of assets in taxable accounts

4. Sale of assets in tax-deferred accounts

5. Sale of assets in tax-free accounts*

*Assumes investor does not move into higher tax bracket during retirement Source: UBS CIO WMR

Brian Nick, CAIA, Senior Investment Strategist

14 September2014Your Wealth & Life

Investorstendtospendquiteabitoftimeandefforttryingtooptimizetheirassetallocations,butfrequentlygiveshortshrifttotheliabilitysideofthebalancesheet.Conventionalwisdomalsosaysthatretireesshouldtypicallyavoiddebt.Unfortunately,suchaviewcanhaveanegativeimpact in regard to total resources and the cash flowavailableformeetingobjectives.Thecur-rentperiodofhistoricallylowrealinterestratesprovidesatacticalopportunityandincentivetoextenddebtmaturitiesandlockinlowrateswhileprovidinganimplicitinflationhedgeforthebalancesheet.

WeexpecttheFederalReservetomaintainaFedFundstargetof0-0.25%untilmid-2015.Aslongasshort-terminterestratesremainbelowthepre-vailingrateofinflationthecostofholdingdebttiedtoshort-termratesonabalancesheetisrela-tivelylow.Mortgagedebtprovidesoneexample,althoughthiscanbebroadlyextendedtoalltypesofresponsibledebt.Forexample,thepub-lishedannualpercentagerate(APR)foraJumbo7/1ARMfromUBSMortgagewas3.026%on7/31.Weexpectinflationtoaverageabout2.5%forthenextdecade,implyinganannualinflation-adjustedcostofonly0.526%forsevenyears.Totheextentthattheinvestor’sassetsareexpected

toreturnmorethan0.526%,maintainingthoseassetsinsteadofpayingoffdebtcanleadtoalargerbalancesheetinadditiontoprovidinggreatercashflowflexibility.

Aftersevenyearsourinterestratemodelsimplytherateonthemortgagewouldresetto4.76%andthento6.26%(seeFig.1)asone-yearLIBORincreases over time. At this point, the mortgage couldberefinancedorpaidoff,dependingontheinterest rate environment at that point in time.

Toseehowthisworksinpractice,supposeacoupleisreachingretirementwith$3millionintotalassets,includingtheircurrentprimaryresi-dence.Theywanttodownsizeintoa$500,000homeandaredeterminingwhetheritmakessensetouseanARMmortgagetofinance80%ofthecostoftheirnewproperty.Additionally,theyholdamoderateinvestmentproposalwithanestimatedreturnof6%peryearandexpectamarginaltaxrateof33%inretirement.Despitepayingabout$90,000ininterestthrough2021,thenetbalancesheetresult,onaverage,isagainofjustover$92,000(seeFig.2).

Inadditiontotheestimatedbalancesheetben-efit,there’sonemoreadvantagetothisstrategythatisworthmentioning:inflationprotection.Manyofourclientsareconcernedaboutabove-averageinflationinthefuture.Holdingfixed-ratedebtisonewaytoexpress,andhedgeagainst,thatview.Ifrealizedinflationishigherthanweexpect,thevalueofthedebtobligationwillbeeroded–makingthehouseholdbetteroff.

Prudent leverage

Source: Bloomberg, CIO WMRA, as of 7/30/2014

ARM Rate Modeled Index Rate

4

3

0

1

2

7

6

5

8

2014 2018 2022 2026 203820342030 2042

Fig. 1: We expect interest rates to rise gradually over time

Modeled rate path of 1-year LIBOR and a 7/1 ARM mortgage, in %

Inte

rest

Rat

e

Source: CIO WMRA

100,000

50,000

0

250,000

150,000

200,000

2014 2016 2018 2020 2022 2024 2026

Fig. 2: Estimated benefit of utilizing low-cost debt

Balance sheet differential, 7/1 ARM vs. no mortgage

Longevity planning for retirees

Michael Crook, CAIA, Head of Portfolio & Planning Research

We’d like to thank Jeff Gray for his consultation on this article.

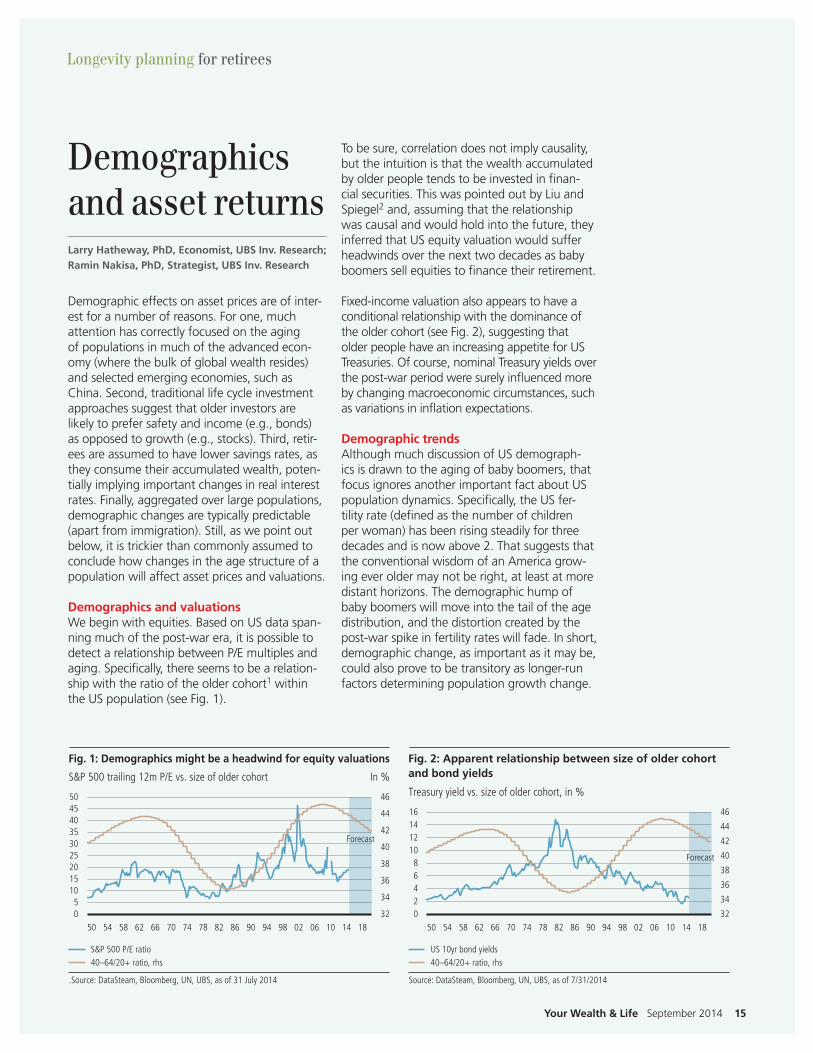

Demographiceffectsonassetpricesareofinter-estforanumberofreasons.Forone,muchattentionhascorrectlyfocusedontheagingof populations in much of the advanced econ-omy(wherethebulkofglobalwealthresides)and selected emerging economies, such as China.Second,traditionallifecycleinvestmentapproaches suggest that older investors are likelytoprefersafetyandincome(e.g.,bonds)asopposedtogrowth(e.g.,stocks).Third,retir-eesareassumedtohavelowersavingsrates,astheyconsumetheiraccumulatedwealth,poten-tiallyimplyingimportantchangesinrealinterestrates.Finally,aggregatedoverlargepopulations,demographicchangesaretypicallypredictable(apartfromimmigration).Still,aswepointoutbelow,itistrickierthancommonlyassumedtoconcludehowchangesintheagestructureofapopulationwillaffectassetpricesandvaluations.

Demographics and valuationsWebeginwithequities.BasedonUSdataspan-ningmuchofthepost-warera,itispossibletodetectarelationshipbetweenP/Emultiplesandaging.Specifically,thereseemstobearelation-shipwiththeratiooftheoldercohort1withintheUSpopulation(seeFig.1).

Demographics and asset returns

Tobesure,correlationdoesnotimplycausality,buttheintuitionisthatthewealthaccumulatedbyolderpeopletendstobeinvestedinfinan-cialsecurities.ThiswaspointedoutbyLiuandSpiegel2 and, assuming that the relationship wascausalandwouldholdintothefuture,theyinferredthatUSequityvaluationwouldsufferheadwindsoverthenexttwodecadesasbabyboomerssellequitiestofinancetheirretirement.

Fixed-incomevaluationalsoappearstohaveaconditionalrelationshipwiththedominanceoftheoldercohort(seeFig.2),suggestingthatolder people have an increasing appetite for US Treasuries.Ofcourse,nominalTreasuryyieldsoverthepost-warperiodweresurelyinfluencedmorebychangingmacroeconomiccircumstances,suchasvariationsininflationexpectations.

Demographic trendsAlthough much discussion of US demograph-icsisdrawntotheagingofbabyboomers,thatfocusignoresanotherimportantfactaboutUSpopulationdynamics.Specifically,theUSfer-tilityrate(definedasthenumberofchildrenperwoman)hasbeenrisingsteadilyforthreedecadesandisnowabove2.ThatsuggeststhattheconventionalwisdomofanAmericagrow-ingeveroldermaynotberight,atleastatmoredistanthorizons.Thedemographichumpofbabyboomerswillmoveintothetailoftheagedistribution,andthedistortioncreatedbythepost-warspikeinfertilityrateswillfade.Inshort,demographicchange,asimportantasitmaybe,couldalsoprovetobetransitoryaslonger-runfactorsdeterminingpopulationgrowthchange.

.Source: DataSteam, Bloomberg, UN, UBS, as of 31 July 2014

40–64/20+ ratio, rhsS&P 500 P/E ratio

2015

05

10

4540353025

50

34

32

44

42

40

38

36

46

50 54 58 62

Forecast

66 70 74 78 82 86 90 141006029894 18

Fig. 1: Demographics might be a headwind for equity valuations

S&P 500 trailing 12m P/E vs. size of older cohort In %

Source: DataSteam, Bloomberg, UN, UBS, as of 7/31/2014

40–64/20+ ratio, rhsUS 10yr bond yields

420

14121086

16

34

32

44

42

40

38

36

46

50 54 58 62

Forecast

66 70 74 78 82 86 90 141006029894 18

Fig. 2: Apparent relationship between size of older cohortand bond yields

Treasury yield vs. size of older cohort, in %

Longevity planning for retirees

Larry Hatheway, PhD, Economist, UBS Inv. Research; Ramin Nakisa, PhD, Strategist, UBS Inv. Research

Your Wealth & LifeSeptember201415

Research on valuation tends to focus on the dominanceofthemiddle-to-oldcohortsbecausethesehaveshownassetvaluationrelationshipsinthepast.However,webelievethatthismaybemisleadingwhenextrapolatingintothefuture.Theoverwhelmingtrend,bothregionallyandglobally,isoneofincreasinglifeexpectancyasa consequence of medical advances, improv-ingdietandlifestylechange.Suchadramaticincreaseinthenumberofhealthyover-65scouldwellleadtosocialtransformation.Inparticular,agingbabyboomersmaynotwantto,orindeedbeableto,retiregiventhenecessityoffundinganincreasinglylengthyretirement.

International capital marketsMostworklinkingdemographicstoassetpref-erenceassumesaclosedeconomyandcapitalmarkets(forsimplicity).Butinaworldofincreas-inglyintegratedeconomiesandassetmarkets,thatassumptionisprobablytoostrong.Theincreasingintegrationofcapitalmarketsandtheriseofwealthinemergingeconomies,suchasChina,matters.Akeyconsequenceofglobaliza-tion,quitepossibly,willbeadeclinein“homecountrybias”asinvestorsseekgreaterdiversifi-cationandreturnonaworldwidebasis.Inthatenvironment, domestic preferences (including thosedrivenbyaging)willplayasmallerroleindetermining domestic asset prices.

Fadingdomesticpreferenceinassetpurchaseswillbecomeevenmoreimportant,giventhegrowingpoolsofinvestiblefundsoverseas.Indeed,therapidriseofawealthymiddleclassinChinaandelsewhereinthedevelopingworld

hascausedasharpriseinforeignownershipofUSassets(seeFig.3).Inshort,domesticdemo-graphicinfluencesonassetpricesmaybeoffsetbychangingglobaldemandforinvestibleassets.

Inthatregard,itisinterestingtolookatthecompositionofassetsownedbyforeigninves-tors. In the past, US investors sought higher returnsinforeignmarkets,whereasnon-USinvestorswerelookingforsafetyintheUS.Forexample,sovereignwealthfundslookingforasafestoreofwealthderivedfromcommoditiesoratradesurpluswouldpurchaseUSTreasuries.ThispatternseemstobechangingasforeignholdingsofUSTreasuriesarenowfalling,whileownershipofUSequitiescontinuesitssteadyrise.ForeignholdingsofUSequities,whichweresmallin2000,arenowrisingrapidly(seeFig.4).Forexample,ChineseownershipofUSstocksincreased26%between2010and2011(fromUSD127billiontoUSD159billion).

Inconclusion,wedonotbelievethereisastraightforwardcasetobemadethatdemo-graphicswillsignificantlyimpactassetreturnsover the coming decades. Although there is a theoreticalbasisforassuminganimpact,mostofthatworkassumesaclosedeconomy.Overall,theresearchthatwehavedonesuggeststhattherelationshipbetweenassetclassreturnsanddemographicshasbeentenuousatbest.Accordingly,wewouldencourageinvestorstofocus on more fundamental factors (e.g., valua-tions,corporateearnings,GDPgrowth,interestrates)whenprojectingfutureassetclassreturns.

Source: Haver, UBS, as of 31 July 2014

TreasuriesEquities

Agencies (rhs)Corporate Bonds

0

50

40

30

20

10

60

0.20.0

1.21.00.80.60.4

1.81.61.4

2.0

52 56 60 64 68 72 76 80 84 88 92 1208040096

Fig. 3: Foreign ownership of US assets continues to climb

Foreign ownership of US assets (% of total market)

Source: Haver, UBS

1000800600400200

0

14001200

1600

Hong

Kon

g

Mid

dle

East

oil e

xpor

ters

Irela

nd

Switz

erla

nd

Belg

ium

Cana

da

Luxe

mbo

urg

Caym

anIsl

andsUK

Japa

n

Chin

a

Rest

of

Wor

ld

Fig. 4: Foreign holdings of US equities have also been increasing

Foreign holdings of US equities (US$ bn)

2000 20132010

Longevity planning for retirees

16 September2014Your Wealth & Life

Larry Hatheway and Ramin Nakisa are members of UBS Investment Research and are not a part of CIO Wealth Man-agement Research (CIO WMR). CIO WMR may have views that differ or are contrary to the views expressed herein.

Your Wealth & LifeSeptember201417

Millennials’mostvaluableassetisn’ttheirstockorbondportfolio,theirprimaryresidence,oranyotherfinancialasset.Theirlargestassetistheirhuman capital.1Humancapitalcanbedefinedas the (present) value of an individual’s future earnings.Justasabondderivesitsvaluefromtheexpectedflowoffutureincome,humancapi-talderivesitsvaluefromtheexpectedflowoffuturelaborincome.Humancapitalistypicallythegreatestduringthefirsthalfofanindividual’scareer. Over time, as income is earned, saved and invested,humancapitaldiminisheswhilefinan-cialassetsgrowasapercentageofnetworth.

Millennials,whohavepursuedmoreeducationalattainmentthananyothergenerationinhistoryandgraduatedintotheworstlabormarketin50years,mightnotfeelwealthyatthisstageintheirlives. But once human capital is incorporated into theirbalancesheets,manyMillennialsareactuallyquitewealthy.Theysimplyneedtimetoextracttheir hard-earned human capital in the form of laborincomeandconvertitintofinancialassets.Longevityplaysanimportantroleinthiscalcula-tion,asMillennialshavegreatercertaintyaroundlongerworkinglifetimesandpost-workretire-mentperiodsthanthegenerationsbeforethem.

Howishumancapitalcalculated?Thevalueofhumancapitaliseffectivelythenetpresentvalueofestimatedfutureearnings.Fromafinancialstandpoint, high-income individuals have more humancapitalthanlow-incomeindividuals,althoughthequantitymattersmoreforinsuranceconsiderations than asset allocation decisions. The percentage of human capital as a portion ofone’soverallbalancesheetisaboutthesameacrossthelifecycleregardlessofincome,assum-ing similar savings rates.

Becausehumancapitalisquantifiedthrougha net present value calculation, future earn-ingsshouldbediscountedatanappropriateratebasedonpotentialriskiness.Acareerwithhighlysecureandpredictableincome(e.g.,ten-uredprofessor,physician)isalmostbond-like,whereasalessstablecareer(e.g.,commissionedsales,actor,investmentbanker)providesincomethatismoreequity-like.

Theimplicationisthatthemorestock-likeaninvestor’s human capital is, the more he or she shouldtrytodiversifyawayfromequitiesintoless correlated investments.2Arelativelysecurejobwithsteadyearningsenablestheindividualtotakemorerisksinhisorherinvestmentport-folio,butlessstableemploymentmightwarrantholding a greater allocation in more conserva-tiveassetsthatcanprovidestableincomewhennecessary.Humancapitalalsomattersfromaninsurance standpoint. Households should hedge riskstotheirlargestassets,andhumancapitalcertainlyqualifiesinthatregard.Inthefollowingtwoarticles,we’lldigintobothoftheseimplica-tionsabitmore.

Millennialsand longevity

LongevitymaynotbeatthefrontofmostMillennials’minds,butisnonethe-less relevant. A longer life implies a longer career and a longer retirement. WeuseahumancapitalframeworktodevelopourviewsonhowMillennialsshouldinvestandhedgetheirbalancesheets.Wealsoprovideadviceonoptimalassetlocationforyoungerinvestors.

Human capital, the hidden assetMatthew Baredes, Strategist

18 September2014Your Wealth & Life

Is human capital different for Millennials?

Stephen Freedman, PhD, CFA

Thereisaninclinationtoestimatethatthehumancapitalofyoungadultsmaybesomewhatmorebond-likethanequity-likeonthebond-equityspectrum.Thisisbecauseundernormalcircumstances,salariesandwagescanbedependedonwithreasonableregularityandunemploymentbenefitshelpbridgethegapincaseofjobloss.However,inthecaseofMillennialsthereareseveralfactorsthatcanmakehumancapitalappearmoreequity-likethanitwasforpriorgenerations.

First,thereisawidelyheldbeliefthatMillennialsaremorelikelytobecomeentrepreneursthanpriorgenera-tions.Asentrepreneurshiptypicallypeaksmid-career,itwilltaketimetotellwhetherthisexpectationiscon-firmed.Ifitis,thiswouldmakethehumancapitalofmanyMillennialsmoreequity-likeastheriskofstartupfailuresisconsiderableand,onceabusinessisestablished,entrepreneurialprofitswillvarywiththebusinesscycletoamuchlargerdegreethansalaries.Second,Millennialsaremorelikelytoswitchemployers.Whileanygivenemployerchangemaybringopportunitiesandcareerupside,frequentswitchesalsobearriskssuchassignalinglowloyaltytofutureemployers.Finally,Millennialstypicallyrankdoing“meaningfulwork”highonthelistofjobattributestheyseek.Thissuggeststhatbeyondsimplechangeswithinthesamesector,theymayalsobemorelikelytocompletelychangecareerpathsatsomepointduringtheiractivelife.This,too,createsrisksandopportunities.

Millennials by the numbersTheMillennialGenerationgenerallyincludesthosewhowerebornfromtheearly1980stotheearly2000s.Wehighlightsomekeyfiguresbelow.

Millennials and longevity

English and ...38% of Millennials are bilingual, up from 22% in 2003.5

Well educated23% have a Bachelor’s degree or higher, making them the most educated generation.4

87%of Millennials consider a company’s commit-ment to social and environmental causes when deciding where to work.2

71%of Millennials at “regu-lar” jobs would prefer to quit their current job to work for themselves (Millennial Branding and oDesk) and 60% of them plan to do so in the next two years.1

26% of Millennials are married, down from 36% of GenXer’s, 48% of Boomers and 65% of the Silent Majority (based on percentage of each generation married at age 18-32).3

Staying single

Your Wealth & LifeSeptember201419

Aswestatedatthebeginningofthispiece,people are living longer. There is a good chance thatlifeexpectancieswillbeevenhigherbythetime Millennials reach middle age. The general increaseinlifeexpectancyhasvariousimplica-tions for saving and investment, as Millennials arelikelytoworklongerandhavealongerretirement than their parents.

So if Millennials are going to retire at an older agethanpreviousgenerations,howshouldtheyinvest?Well,whenwethinkofMillennials’over-allassetallocation,wemustonceagainreturntotheconceptofhumancapital.ThevastmajorityofMillennials’assetsarenon-financial,buttheseassetsstillmustbeconsideredwhenmakinginvestment decisions.

Ifhumancapitalismorebond-likethanstock-like,itimpliesthatMillennialsshouldholdmoreequities in their investment portfolio. This is becausetheirhumancapitalfunctionsasanimplicitbondontheirbalancesheet. (Also, givenyoungerinvestors’lesserliquidityneeds

comparedtoolderinvestors,theyshouldbewill-ingtotoleratemorevolatilityinexchangeforgreaterabsolutereturns.Therefore,theyshouldalreadyhaveasignificantlyhigherallocationinequities,allotherthingsbeingequal.)Infact,whenlookingatMillennials’overallbalancesheets,thepercentageallocationinequitieswillchangedramaticallyovertime.

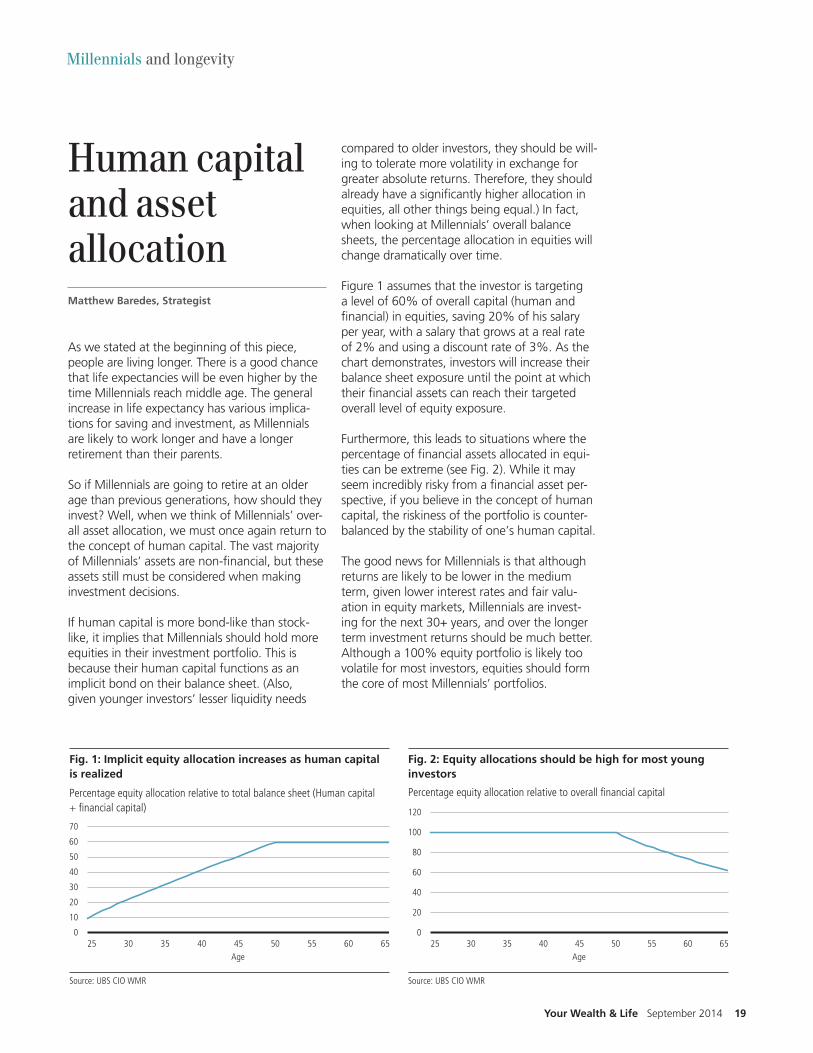

Figure1assumesthattheinvestoristargetingalevelof60%ofoverallcapital(humanandfinancial)inequities,saving20%ofhissalaryperyear,withasalarythatgrowsatarealrateof2%andusingadiscountrateof3%.Asthechartdemonstrates,investorswillincreasetheirbalancesheetexposureuntilthepointatwhichtheirfinancialassetscanreachtheirtargetedoveralllevelofequityexposure.

Furthermore,thisleadstosituationswherethepercentageoffinancialassetsallocatedinequi-tiescanbeextreme(seeFig.2).Whileitmayseemincrediblyriskyfromafinancialassetper-spective,ifyoubelieveintheconceptofhumancapital,theriskinessoftheportfolioiscounter-balancedbythestabilityofone’shumancapital.

ThegoodnewsforMillennialsisthatalthoughreturnsarelikelytobelowerinthemediumterm,givenlowerinterestratesandfairvalu-ationinequitymarkets,Millennialsareinvest-ingforthenext30+years,andoverthelongerterminvestmentreturnsshouldbemuchbetter.Althougha100%equityportfolioislikelytoovolatile for most investors, equities should form the core of most Millennials’ portfolios.

Human capital and asset allocation

Source: UBS CIO WMR

10

0

30

20

50

40

605550 65

60

70

4540Age

353025

Fig. 1: Implicit equity allocation increases as human capitalis realized

Percentage equity allocation relative to total balance sheet (Human capital+ financial capital)

Matthew Baredes, Strategist

Millennials and longevity

Source: UBS CIO WMR

20

0

60

40

100

80

605550 65

120

4540Age

353025

Fig. 2: Equity allocations should be high for most younginvestors

Percentage equity allocation relative to overall financial capital

20 September2014Your Wealth & Life

As discussed in the previous article, the per-centage concentration of human capital on a balancesheetmattersmorethantheabsolutevaluewhenitcomestoimpactingassetalloca-tiondecisions.Conversely,thevalueofhumancapital is one important consideration for insur-ance planning. Because loss of human capital represents a catastrophic outcome for most householdsbutcannoteasilybetradedordiver-sified,it’simportanttoconsiderwaystohedgethrough insurance.

Thefinancialassetcorollaryisreceivingallofafamily’sincomefromonebondissuedbyonefirm.Itisobviouslyprudenttodiversifythatriskintoothersecuritiesinsuchasituation.Absenttheabilitytodoso,purchasinginsuranceagainstdefaultisthenext-bestoption.

Therearetwokindsofinsurancethatareofparticular importance to Millennials: life insur-anceanddisabilityinsurance.Lifeinsurancehelpsprotectagainstprematuremortalityandthelossoffutureincomeforafamilythatwouldfollowsuchanevent.Givenourpreviousdis-cussionaboutthelargevalueofhumancapitalthatMillennialscurrentlypossess,itisimperativeforanyMillennialwithfinancialdependentstohedgetheirmortalityriskthroughlifeinsurance.Disabilityinsurancecanprovideanimportanthuman capital hedge for non-fatal situations. Givenlongerlifespans,individualswhoareunfortunateenoughtobecomepermanentlydisabledatayoungagearelikelytolivelongerthantheywouldhaveinthepastandthereforearegoingtoneedmoreforlivingexpenses.Inaddition,temporarydisabilityisnotuncommon,withsomeexpertsestimatingthatoneinfourMillennialswillbedisabledforsomeperiodoftimebeforetheyretire.1

Householdsfrequentlyprotecttheirbalancesheetsbyholdinghomeownersinsuranceandautoinsurance.Forthesamereasons,lifeanddisabilityinsurancealsoprotectbalancesheethealthbyhedgingriskstohumancapital.Theseshouldbeviewedasvitalcomponentsofawell-constructedbalancesheet,particularlyforthosewhohaven’tyetaccumulatedenoughfinancialresources to last a lifetime.

Insurance implications of a longer life

Thinking about disability insuranceJay Rabinowitz, Insurance consultant, UBS Wealth Management Americas

Whenlookingtobuydisabilitycoveragethereareseveralchoicestoconsider.Thefirstplacetocheckiswithyouremployer.Mostjobsprovidebothshort-termandlong-termcoverage,typicallyupto60%ofyoursalarybutoftenwithacap.

Ifyouareself-employedordonothavesufficientcoverageatwork,buyingpersonalcoverageisimportant. One important advantage of direct coverageisthatthebenefitwillbereceivedonatax-freebasis.Benefitsunderanemployer-providedplanarealmostalwaystaxable.Thecostofanypolicywillbedrivenprimarilybyyourage,thetypeofworkyoudoandyourincome.Youthenhavetomakedecisionsaboutthefeatures,whichinclude:

• Coveragefortheinabilitytodoyourjob(“ownoccupation”)orcoverageforgeneraldisability.Wehighlyrecommendoptingfor“ownoccupa-tion”coverage.

• Theeliminationperiod–howlongyouneedtobedisabledbeforethebenefitsbegin.Theshorterthewaitingperiod,themoreexpensivetheplanwillbe.Ifyouhavesetasideenoughmoneytocoveryourexpensesforseveralmonths,youcanlowerthepremiumbyelectingalongerelimina-tion period.

• Howlongwillthebenefitbepaid?Plansoffercoverageforasetperiodofyearsoruntil65.Werecommendensuringyouhaveenoughcoveragetofillwhatevergapdisabilitywouldleaveinyourfinancialplan.

• Increasesincoverage–thisfeatureallowsyoutoautomaticallyincreasethebenefitwithoutgoingthroughunderwritingagain.Thisisveryimpor-tantforMillennialswhoseincomeisexpectedtoincrease over time.

Millennials and longevity

Matthew Baredes, Strategist

Your Wealth & LifeSeptember201421

Assetlocation(i.e.,thedistributionofassetswithindifferentaccounttypes)isanimportantbutoftenovelookedaspectofassetaccumula-tion.Iwouldimaginemanyinvestorsworkdili-gentlytodeterminetheirfinancialgoals,figureouttheirrisktolerance,buildtheirassetalloca-tionandwatchtheirassetsgrow,withoutreal-izingthemonetarybenefitsofoptimallylocatingassets.Increasinglifespanandlowerexpectedreturns across asset classes heighten the impor-tanceofincreasedportfoliolongevity.

Becauseitcanbedifficulttoshiftassetsbetweenaccounttypes(e.g.,taxabletonon-taxable),optimizingassetlocationismostimportantforthoseinthewealthaccumulationphase.Asinvestorsaccumulatewealthanddistributeassetsbetweentheir401(k),taxableaccountandtheirRothIRA,theyshouldfocusonfillingtheirtax-shelteredaccount(s)withthemosttax

inefficientassetsfirst,andthenaccumulatingmoretaxefficientassetsintheirtaxableaccount.

Forinstance,sincecouponpaymentsaretaxedatordinaryincometaxrates,taxablefixedincomeisbestheldintax-deferredaccounts,wherecouponpaymentscanbereinvestedandcompoundedtax-free.Thesamethingholdsforothertax-inefficientequities,suchasREITs,activelymanagedequityfundswithhighturn-overratesandcapitalgainsdistributions,andlong/short managed funds.

Ontheotherhand,tax-efficientequityholdings,suchasindexfundsorexchange-tradedfunds(ETFs),shouldbeplacedintaxableaccountsbecausecapitalgainsdistributionsareminimalandtheseassetstypicallyexhibitlowturnover.Allowingcapitalgainstogrowtax-freeforaslongaspossibleinthoseaccountsisoptimal.

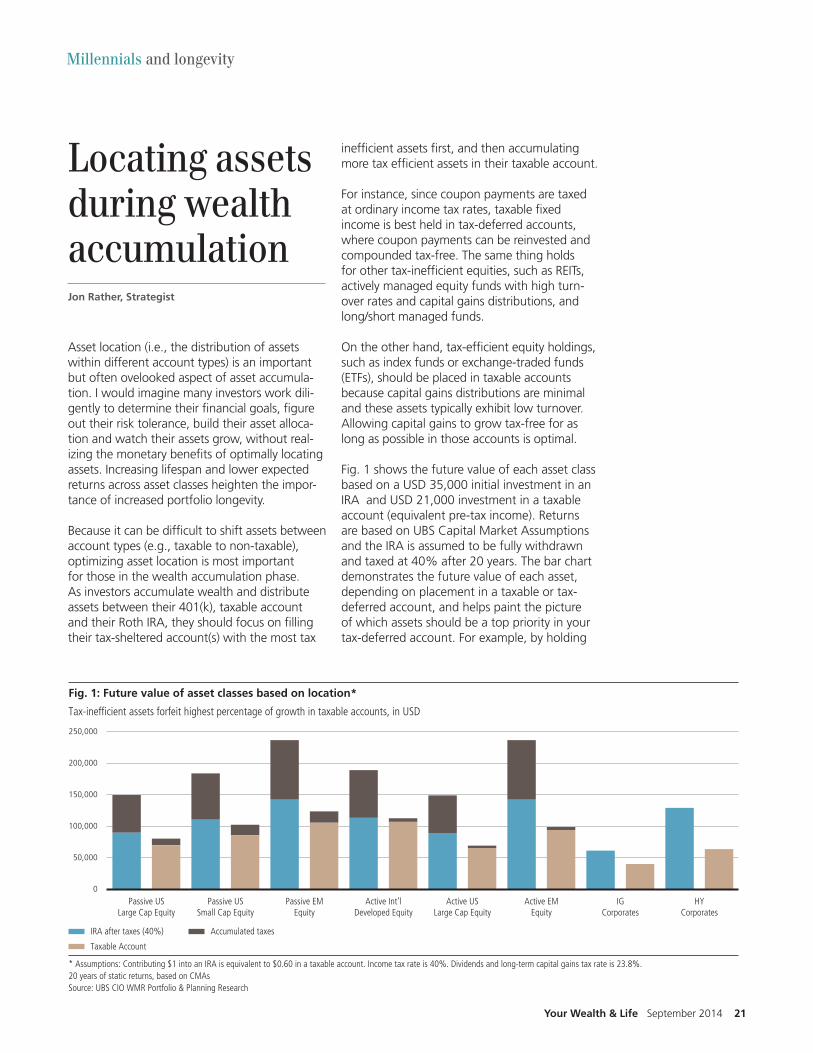

Fig.1showsthefuturevalueofeachassetclassbasedonaUSD35,000initialinvestmentinanIRAandUSD21,000investmentinataxableaccount(equivalentpre-taxincome).ReturnsarebasedonUBSCapitalMarketAssumptionsandtheIRAisassumedtobefullywithdrawnandtaxedat40%after20years.Thebarchartdemonstrates the future value of each asset, dependingonplacementinataxableortax-deferred account, and helps paint the picture ofwhichassetsshouldbeatoppriorityinyourtax-deferredaccount.Forexample,byholding

Locating assets during wealth accumulation

* Assumptions: Contributing $1 into an IRA is equivalent to $0.60 in a taxable account. Income tax rate is 40%. Dividends and long-term capital gains tax rate is 23.8%.20 years of static returns, based on CMAsSource: UBS CIO WMR Portfolio & Planning Research

Taxable Account

IRA aer taxes (40%) Accumulated taxes

200,000

150,000

100,000

50,000

0

250,000

Passive USLarge Cap Equity

Fig. 1: Future value of asset classes based on location*

Tax-inefficient assets forfeit highest percentage of growth in taxable accounts, in USD

Passive USSmall Cap Equity

Passive EMEquity

Active Int’lDeveloped Equity

Active USLarge Cap Equity

Active EMEquity

IGCorporates

HYCorporates

Millennials and longevity

Jon Rather, Strategist

22 September2014Your Wealth & Life

high-yieldcorporatesinataxableaccount,weestimatethataninvestorisforfeiting51%oftheasset’sfuturevalue,onaverage,after20years.Fixedincomeandactiveequitymanag-ersdisplaythebiggestdifferenceinfuturevaluebasedonlocation,andshouldbeatoppriorityinatax-shelteredaccount.Figure2summarizestheoptimallocationforanumberofdifferentasset classes.

Awordofcaution:Eachinvestor’sfinancialsitu-ationisdifferent,andthereisnoone-size-fits-allanswertothequestionofoptimalassetlocation.Liquidityneeds,taxbrackets,timehorizon,assetallocation,rebalancingpreferences,sequenceofreturns,andrelativesizeofaccountsareall factors that can disrupt these guidelines. Nevertheless,theseillustrationsshouldmakeclearthatefficientassetlocationisavitalcom-ponent,alongwithassetallocation,ofinvest-ment planning.

Fig. 2: Where to locate assets

Taxable Account 401(k) Roth IRA

Municipal bonds High yield bonds Small-cap active managers

Index funds Investment grade bonds Emerging markets active managers

ETFs Government fixed income

Tax-managed mutual funds REITs

Low dividend yielding equities Actively managed equities

Long/short hedge funds

Source: UBS CIO WMR Portfolio & Planning Research

Millennials and longevity

The most common reason for creating trusts istohelppreservewealthfortheuseoffuturegenerations.Familieswanttaxefficiencyandcreditorprotectionwithaminimumofadminis-trative friction.

Evenforfamilieswithverycleargoals,extendedlongevitycomplicateswealthtransfer.Withbeneficiariesfrequentlylivingintotheir90sandbeyond,balancingtheneedsofoverlappinggenerationsisagrowingchallengeandtheideathatanyonealivetodaycouldwriteanoptimalset of rules for the operation of a trust over the next100yearsbordersonhubris.Asaresult,well-draftedtrustsincreasinglymustprovidemultiple mechanisms to give future generations ofbeneficiaries,fiduciaries,andtheiradvisorstheflexibilityneededtoadapttochangesinthelaw,family,andsociety.

Beforediscussingspecificmechanismsthatcanbeincludedintrusts,it’sworthtakingamomenttothinkaboutsomeofthechallengesatrustmayfaceovertime.Forexample,ben-eficiarieschange.Today,abenefactormightsee

grandchildren and great-grandchildren reach adulthoodduringtheirlifetimes.Beneficiariesalsomove.Theymaymovetootherstates,buttheycanalsomovetocountriesthatdonotrec-ognizethelegalconceptofatrust.Furthermore,wecanbesurethetaxrulesgoverningtrustswillchange,althoughpredictingexactlywhatthosechangeswillbeisimpossible.And,ofcourse,whilewehopeforthebest,it’sreasonabletoexpectsomefuturedescendantwillhaveadis-ability(whetherphysical,mentalorotherwise)thatmakesitinappropriatetograntthempow-ersandresponsibilitiesthatotherdescendantscaneasilyhandle.

Withallthatsaid,thefollowingisasampleofcommontrustprovisionsthatcreateflexibility,sotrustscreatedtodaycanadaptandcontinuetoserveafamilywellfordecadestocome.

1. Absolute Discretion Distribution Standard: The mostflexibleofdistributionstandards,thisallowsatrusteecompletefreedominmakingdistributions.Thetrusteecanpayoutevery-thing(ifthelawchangesandthetrustisnolongerefficient)ornothing(ifachildissuc-cessfulandhasnoneedfortrustdistributions)withoutfearabeneficiaryorcreditorwillchal-lenge the decision.

2. Lifetime Power of Appointment:Allowsonetrustbeneficiary(usuallytheoldestgeneration)todirecttrustpropertytootherindividualsortocharity(eitheroutrightorinfurthertrust).

Wealth transfer and legacy

Oneimpactofenhancedlongevityisthatmultiplegenerationswillincreas-inglyoverlap.Thishasanimpactontheeffectivenessofcertainwealthtransferandcharitablegivingstrategies.Theannualgifttaxexclusion,forinstance,becomesverypowerfuloverlongtimehorizons,whereasrigidtrustarrangementsmayprecludefamiliesfromachievingtheirgoals.

Trusts: focus on flexibilityStephen Liss, Senior Wealth Strategist, UBS Advanced Planning Group

Your Wealth & LifeSeptember201423

3. Testamentary Power of Appointment: When theprimarybeneficiaryofatrustdiesheorshecanexercisethispowerbywilltodirecttrustpropertytootherbeneficiariesortochar-ity(eitheroutrightorinfurthertrust).Decadesfromnow,thispowercanbeusedbyachildtocustomizefurthertrustsforgrandchildrenbasedoninformationwesimplydonothavetoday.

4. Power to Remove and Replace Trustees: Createsa“checkandbalance”byallowingsomeonetochangethetrustee.Thispowercouldbelongtotheprimarybeneficiary,amajorityofbeneficiaries,afamilyfriendoranyother person the donor selects.

5.Power to Amend Trust Administrative Provisions: These are the provisions controlling thingsliketheinvestmentoftrustassets,thecalculation of income, and accountings (of the use of trust funds).

6.Power to Distribute in Further Trust:Allowsthetrustee to transfer assets to another trust and

24 September2014Your Wealth & Life

Wealth transfer and legacy

therebymateriallychangethetermsofthetrust.

7. Power to Change the Governing Law of the Trust:Enablesthetrusteetochangethegov-erninglawtoamorefavorablejurisdictionatafuture time.

Youwillnoticethatsomeoftheseprovisionsgrantadditionalpowerstothetrustees,whileotherscanbeexercisedbythebeneficiariesthemselves.Checksandbalancescanbecre-atedinmanyotherways,forexamplebyimpos-ingagerestrictions,requiringmajorityaction,or mandating that someone consent to certain decisionsbeforetheybecomelegallyeffective.Trustscanbecustomizedtomeettheneedsofanyfamilyandtheabovelistisnotintendedtobeexhaustive.Itshould,however,giveasenseofthevarietyofoptionsthatexisttobuildflexibilityintotrustsandensurethatthebenefactor’smainobjectivesaremetwellintothefuture.

Stephen Liss is a member of UBS Advanced Planning Group and is not a part of CIO Wealth Management Research (CIO WMR). CIO WMR may have views that differ or are contrary to the views expressed herein.

Acommongoalofmanyfamiliesistotransferwealthtothenextgenerationandbeyondinatax-efficientmanner.Theobjectivemaybetopayforcollegeformultiplegenerations,tohelpchildrenmakeadownpaymentonahome,tocreateafamilybanktohelpfuturegenerationsstartanewbusinessorotherentrepreneurialendeavor,orsimplytotransferwealthintacttothechildren.Thedesiretotransferwealthcanbeimpairedbythefederalestateandgifttaxsystem.Underfederalrules,anindividualmaytransferuptoUSD5.34millionduringhisorherlifeorupondeathtax-free(thisamountisindexedtoinflation).Anycumulativetransfersabovethethresholdaresubjecttogiftorestatetaxatarateof40%.Inaddition,manystateshaveestateandinheritancetaxesaswell,whichcompoundstheproblem.

Theestateandgifttaxmaysignificantlyimpairyourwealthtransfergoals.Oneofthesim-plestwaystotransferwealthtoyourchildrenorotherfamilymembersduringyourlifetimeandminimizethetaxcostisthroughtheuseofthegifttaxannualexclusion.Eachyear,anindividualmaygiftUSD14,000toasmanypeopleasthedonorwishesfreeofthegifttax.Thisamountisreferredtoasthegifttaxannualexclusion,andisanannual“freebie”thatmustbeusedinthecalendaryearorthebenefitislost.GiftsundertheannualexclusiondonotcountagainsttheUSD5.34milliongiftandestatetaxexemptionamount.

Thereareawidevarietyofstructuresthatyoucanemploytomakeannualexclusiongifts.Forgiftstoadults,youcansimplygiftcashorassetsdirectlytoanindividual.Forgiftstominors,youcangiftassetstothebeneficiaryinacustodial

account under the Uniform Transfers to Minors ActorUniformGifttoMinorsAct.Whilethesearesimpleandeasytoimplement,theminorbeneficiaryofacustodialaccountwillhavecon-troloverthegiftedassetsatage18or21(and,inlimitedcircumstances,25),dependingonthestatelawgoverningtheaccount.Manyclientsdon’tlikethisrule.Todelaythetimebywhichyourbeneficiaryobtainscontroloverthegiftedasset,youcanchooseinsteadtomakeagiftintrustforyourintendedbeneficiary.Withincertainlimits,atrustallowsyoutosettherulesunderwhichyourbeneficiarywillreceiveeco-nomicbenefitoforcontrolovertheassets.Giftsintrustcanbestructuredtoqualifyforthegifttaxannualexclusion.

Averypopularmethodofmakingannualexclu-siongiftsisviaa529collegesavingsplan.Contributionstoa529plancanbeinvestedin plan-approved mutual funds (including age-

weightedallocationfunds)togrowonatax-freebasisforfutureusebythebeneficiaryforquali-fiedhighereducationexpenses.Giftsto529plansareallowedauniquebenefit–fiveyearsofgiftsmaybemadeinalumpsum,butforannualexclusionpurposesthegiftisproratedoverthefive-yearperiod,therebytakingadvantageoftheannualgifttaxexclusionforeachyear.Totakeadvantageofthisfront-loadingbenefit,youmustfileagifttaxreturnelectingtospreadthegiftoverfiveyears.

Longevitycangreatlybenefitaplanofmakingannualexclusiongifts.Theearlieryoubeginaprogram of annual giving and the longer the giftingprogramcontinues,themoreyoucanmoveoutofyourestatecompletelyfreeofthegiftandestatetax.Thefollowingchartshowsthesimulatedgrowthofmaximumannualexclu-siongifts(USD14,000eachin2014,increasingwithinflationovertime)fromtwoparentstoatrustforthebenefitofonechildeveryyearfor30years,assumingtheassetsareinvestedinamoderate portfolio. Based on these assumptions,

Longevity and the annual gift tax exclusion

Wealth transfer and legacy

Erin Wilms, Co-Head, UBS Advanced Planning Group

Your Wealth & LifeSeptember201425

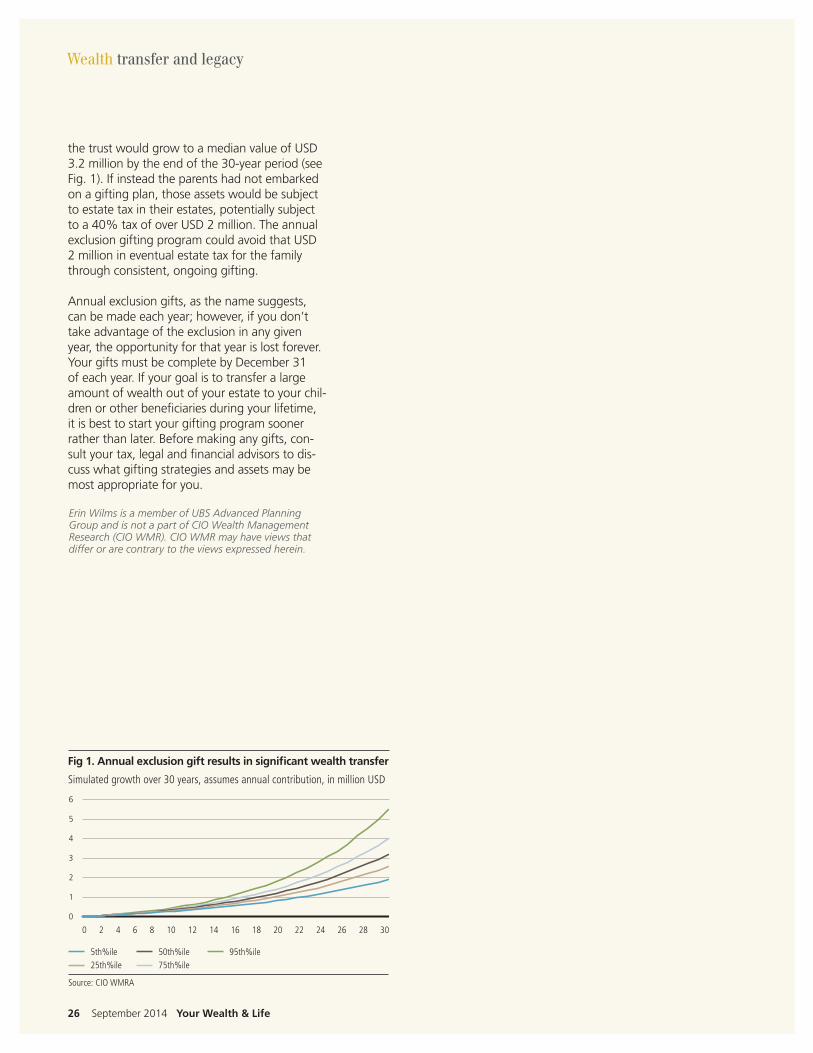

The earlier you begin a program of annual giving and the longer the gifting program continues, the more you can move out of your estate completely free of the gift and estate tax.

thetrustwouldgrowtoamedianvalueofUSD3.2millionbytheendofthe30-yearperiod(seeFig.1).Ifinsteadtheparentshadnotembarkedonagiftingplan,thoseassetswouldbesubjecttoestatetaxintheirestates,potentiallysubjecttoa40%taxofoverUSD2million.TheannualexclusiongiftingprogramcouldavoidthatUSD2millionineventualestatetaxforthefamilythroughconsistent,ongoinggifting.

Annualexclusiongifts,asthenamesuggests,canbemadeeachyear;however,ifyoudon’ttakeadvantageoftheexclusioninanygivenyear,theopportunityforthatyearislostforever.YourgiftsmustbecompletebyDecember31ofeachyear.Ifyourgoalistotransferalargeamountofwealthoutofyourestatetoyourchil-drenorotherbeneficiariesduringyourlifetime,itisbesttostartyourgiftingprogramsoonerratherthanlater.Beforemakinganygifts,con-sultyourtax,legalandfinancialadvisorstodis-cusswhatgiftingstrategiesandassetsmaybemostappropriateforyou.

Source: CIO WMRA

25th%ile5th%ile

75th%ile50th%ile 95th%ile

5

4

3

2

1

0

6

302826242220181614121086420

Fig 1. Annual exclusion gi results in significant wealth transfer

Simulated growth over 30 years, assumes annual contribution, in million USD

Wealth transfer and legacy

26 September2014Your Wealth & Life

Erin Wilms is a member of UBS Advanced Planning Group and is not a part of CIO Wealth Management Research (CIO WMR). CIO WMR may have views that differ or are contrary to the views expressed herein.

America is good at giving. In 2013, Americans gaveaworld-leadingUSD335billiontocharity.1 The traditional concept of leaving a portion of yournetworthtocharitywhenyoupassawayisfamiliar to most Americans.

Unfortunately,sincewe’renowlivinglonger,ourcharitableimpact–withoutplanning–isdecreasing.Ifyoulive20yearslongerthanexpected,thecharityincludedinyourwillortrustwillhavetowaitthatsame20yearsforyourgift.Inaddition,about60,000UScharitiescloseeachyear,sowithoutyourgift,yourtargetcharitymaynotevenexist,ortheirmissioncouldchangebythetimeyoupass.2

Sohowdoyouavoidoutlivingyourphilan-thropiclegacy?Herearethreewaystogivewhileyoulive:

1. Start early and start nowGivingattheendofyourlifeisaneasywaytoensurethatsomeofyourassetsareeventuallygiventocharity.However,sincethecharitywillnotseeadimeuntilyoupassaway,considerusingthefollowingoptionstohaveanimpacttoday:

Donor-advised funds–Agivingvehiclethatallowsyoutomakeanirrevocablecontributionofassets,receiveataxdeduction,andgivetovariouscharitiesovertimeastheassetsgrowtax-free.

Private foundations–Agivingvehiclethatoffersyoumaximumcontrolandflexibilityoverphilan-thropic giving and assets.

2. Involve your familyInvolvingyourfamilyinyourphilanthropicgoalsisessentialtomaximizingyourimpactlongafteryou’vepassed.

Spouse/partner–Yourspouseorpartnermightinherityourwealthbeforeyourchildrendo,andlikelyviewsgivingdifferentlythanyoudo.Women-ledhouseholdstendtogivetwiceasmuch as male-led households.3Involvingyourspousecanalignyourintereststocreatealastingphilanthropiclegacy.

Children/grandchildren–Involvingchildreninyourgivingcanjump-startyourimpactwhileyoulive.Regardingphilanthropy,89%ofNextGensareinfluencedbytheirparents,and75%ofHNW investors under 40 cite social impact as extremely/veryimportant.4NextGenfamilymem-berscanbecomeactiveleadersoffamilydonor-advised funds and private foundations, and their involvementisanexcellentwaytobringfamiliestogether to create a lasting impact.

3. Use strategic philanthropyManyindividualsgiveassetstocharitywithouttrackingtheresults.This“sprayandpray”model–whiletraditional–canbeapoormatchwithlongevityifthecharityrunsthroughitsassetsandasksforadonationagainthenextyearwithoutmakingameasurabledifference.

Today,applyingsimpleconceptsofsustainabilityandmeasurabilitytoyourphilanthropicdeci-sionscansignificantlyincreaseyourimpact.Forexample,usingGuideStarandothertrackingsourcescanhelpyouunderstandwhereyourdollarsgoandhowtheyareusedtowardyourgoals.Maximizetheimpactofyourdonationsbyfocusingonthesocialreturnofeachdollaryoudonate,andconcentrateyourfinancialsupportonorganizationsthatwillstillbearoundlongafteryouare.

4. Surround an issueWhile donations are important, there are other waysyoucangivetomaximizeyourimpact.

Investing–Therearenumeroussociallyrespon-sibleinvestmentvehiclesandimpactinvesting

Your Wealth & Life August 2014 27

Giving while living

Wealth transfer and legacy

Zach Graumann, Philanthropy Strategist, UBS Client Philanthropy Services Team; Bill Sutton, Head of UBS Client Philanthropy Services Team

If you live 20 years longer than expected, the charity included in your will or trust will have to wait that same 20 years for your gift.

optionstobringfor-profitdollarstocausesyou’repassionateabout.

Lending–Certainfor-profitandnon-profitorga-nizationscanlendmoneytocompaniesandindi-vidualstosupportyourcausefromtheothersideofthebalancesheet.

Buying–Companieswithasocialmission,suchasFEED,LibertyUnited,TOMSShoesorWarbyParker,makeagifttocharityeachtimeyoupur-chase their products.

Fundraising and networking–Youcanopenyournetworktofundraisers,thoughtleadersandinnovatorsinthearenaswhereyougive.

Time and talent–Non-profitscanbestarvedfortalentedindividuals,andyourtimeandinsightsmaybethegreatestassetsyoucangive.

Giving while livingOneofthebestreasonstogivewhileyouliveistoenjoythedifferenceyouaremakingnowwhileinvolvingfamilyandfriendsinyourphilanthropy.

28 September2014Your Wealth & Life

Wealth transfer and legacy

Zach Graumann and Bill Sutton are members of UBS Client Philanthropy Services and are not a part of CIO Wealth Management Research (CIO WMR). CIO WMR may have views that differ or are contrary to the views expressed herein.

Matthew BaredesisaStrategistwithintheCIOPortfolio& Planning Research group in CIO Wealth Management Research. He focuses on advice related to investment strat-egy,portfolioconstruction,behavioralinvestingandfinancialplanning.

Joseph F. Coughlin, PhD is Director of the Massachusetts InstituteofTechnologyAgeLab.Hisresearchexamineshowthedisruptivedemographicsofanagingsociety,socialtrendsandtechnologywillshapefutureinnovationsinbusinessandgovernment.Coughlinteachespolicyandsystemsinnova-tioninMIT’sEngineeringSystemsDivisionandhaspublishednearly100peer-reviewedpublicationsandreports.

Michael Crook isanExecutiveDirectorandHeadofPortfolioandPlanninginCIOWealthManagementResearch,wherehe advises investors on asset allocation, portfolio construc-tion,andfinancialplanning.Heistheauthorofnumerousacademicandprofessionalarticlesincludingpublicationsinthe Journal of Wealth Management, the Journal of Investing, andtheJournalofIndexInvestingandisaformeradjunctprofessorofeconomicsatMarymountManhattanCollege.He’salsoareviewerfortheJournalofInvestingandtheJournalofIndexInvesting.

Zach GraumannisaPhilanthropyStrategistontheUBSClientPhilanthropyServicesteam,specializinginNextGeneration giving. He is also the founder and CEO of SuitUp, anon-profitthathelpscompaniesruncommunityserviceeventsinschoolsthroughoutNewYorkCity.

Larry Hatheway, PhD, is Chief Economist at the UBS InvestmentBank.HeisamemberoftheSecuritiesResearchExecutiveCommitteeoftheUBSInvestmentBankandalsoservesasamemberoftheGlobalInvestmentCommittee(UBS Wealth Management).

Stephen Liss is a Senior Wealth Strategist in the Advanced PlanningGroup.HehelpseducateUBSclientsontax,estateplanning,philanthropyandlifeinsurance.

David McWilliams is the Head of Wealth Management Transformation at UBS. Wealth Management Transformation isaneworganizationthathelpsFinancialAdvisors,throughteaming,training,planning,increasingproductivityanddeliv-eringholisticwealthmanagement.

About the authors

Your Wealth & LifeSeptember201429

Ramin Nakisa, PhD,isDeputyHeadoftheGlobalAssetAllocationteam,partofMacroStrategyResearchintheUBSInvestmentBank.

Brian Nick is a Senior Strategist in the Portfolio & Planning Research group in CIO Wealth Management Research. He providesadvicetoinvestorsregardingmarketdevelopments,portfolio construction, and short- and long-term asset alloca-tion.BrianalsoservesasliaisonbetweenCIOWMRandtheUBS Private Wealth Management division.

Mike Oleszkowicz CFP, CRPC is a Wealth Management RetirementConsultantwhohelpsUBSfinancialadvisorsandclientsrecognizetherisksonemayfaceinretirementandidentifysolutionsthatmayhelpmitigatethoserisksthroughafinancialplanningprocess.

Jay RabinowitzisanInternalInsuranceConsultantwhoworkswithUBSfinancialadvisorsindeveloping,presentingandimplementinginsurance-basedsolutionstoourclients.

Jon RatherisaStrategistwithintheCIOPortfolio&PlanningResearch group in CIO Wealth Management Research. He focusesonadvicerelatedtoinvestmentstrategy,portfolioconstruction,andfinancialplanning.

Bill Sutton, Jr.isHeadofUBSClientPhilanthropyServices,providingsubjectmatterexpertise,adviceandsolutionsthatenableUBSclients’wealthtoreflecttheirvaluesthroughgiv-ing,investing,andcommunityservice.

Erin Wilms is the Co-Head of the Advanced Planning Group. SheleadsateamthathelpseducateUBSclientsontax,estateplanning,philanthropyandlifeinsurance.

30 September2014Your Wealth & Life

EndnotesIntroduction: Planning for longevity certainty 1http://www.ssa.gov/OACT/NOTES/as120/LifeTables_

Tbl_7_1900.html 2https://www.soa.org/News-and-Publications/

Newsroom/Press-Releases/2012-07-30-retirees-under.aspx

3HumanMortalityDatabase.UniversityofCalifornia,Berkeley(USA),andMaxPlanckInstituteforDemographicResearch(Germany).Availableatwww.mortality.orgorwww.humanmortality.de(datadown-loaded on 7/30/2014).

4VanDerhei,J.“WhyDoesRetirementReadinessVary:ResultsfromEBRI’s2014RetirementSecurityProjectionModel.”TheJournalofRetirement,Vol.1,No.4(2014),pp.95-117.

5UBSInvestorWatch,“Beginbeforetheend,”Q32014

Introduction: Infographic 1UBSInvestorWatch:80isthenew60,4Q2013 2FederalInteragencyForumonAging-relatedStatistics,

“OlderAmericans2012:KeyIndicationsofWell-being,”June2012

3FactSheet:Cancer,NationalInstitutesofHealth,October2010

Safe spending rates, updated 1UBSInvestorWatch:80isthenew60,Q42013

Personal pensions 1NationalInstituteonRetirementSecurity

Demographics and asset returns 1 The proportion of the population in the range of 40

to64yearsoverthatofthepopulationabovetheageof 20.

2“BoomerRetirement:HeadwindsforUSEquityMarkets,”LiuandSpiegel,FRBSFEconomicLetter(2011)

Human capital, the hidden asset 1SeeMilevsky,Moshe.AreYouaStockoraBond?

2012,FTPress. 2SeeJagannathan,Ravietal.“WhyShouldOlderPeople

InvestLessinStocksthanYoungerPeople?”1996,MinneapolisFed

Millienials by the numbers 1Millennials&theFutureofWork.MillennialBranding

andoDesk,2013. 22010ConeCauseEvolutionStudy,ConeLLC 3TheDeclineofMarriageandRiseofNewFamilies,Pew

Research Center, 2010 4,5Millennials:BreakingtheMyths.Nielsen,2014

Insurance implications of a longer life 1USSocialSecurityAdministrationfactsheet,February

7, 2013.

Giving while living 1GivingUSA2014:TheAnnualReportonPhilanthropy

fortheYear2013(includesindividuals,privatefounda-tionsandbequests)

2http://philanthropy.com/blogs/giveandtake/have-100000-nonprofit-groups-failed-in-the-recession/25952

3http://www.tbf.org/tbf/14/women-in-philanthropy 4“#NextGenDonors:RespectingLegacy,Revolutionizing

Philanthropy,”21/64&JohnsonCenterforPhilanthropy,2013

4 CapGemini World Wealth Repo