YOUR QUESTIONS ANSWERED - Alexander Forbes

16

YOUR QUESTIONS ANSWERED WEBINAR: 27 MAY 2020 Advice-related pages 1 to 2 Advice and retirement options page 2 Alexander Forbes Retirement Income Solution (AFRIS) page 3 Cash withdrawals at retirement pages 3 to 4 COVID-19-related page 4 Delay (defer) retirement page 5 Early retirement page 6 Fees page 6 Group life cover at retirement page 7 Guaranteed pension for life page 7 Investment choice pages 8 to 9 Medical page 9 Questions about Michael Prinsloo’s presentation pages 10 to 11 Retirement options pages 11 to 12 Retirement planning pages 12 to 14 Retrenchment page 14 Staying invested (preservation) page 14 Tax pages 14 to 15 Topics

Transcript of YOUR QUESTIONS ANSWERED - Alexander Forbes

YOUR QUESTIONS ANSWERED WEBINAR: 27 MAY 2020

Advice-related pages 1 to 2

Advice and retirement options page 2

Alexander Forbes Retirement Income Solution (AFRIS) page 3

Cash withdrawals at retirement pages 3 to 4

COVID-19-related page 4

Delay (defer) retirement page 5

Early retirement page 6

Fees page 6

Group life cover at retirement page 7

Guaranteed pension for life page 7

Investment choice pages 8 to 9

Medical page 9

Questions about Michael Prinsloo’s presentation pages 10 to 11

Retirement options pages 11 to 12

Retirement planning pages 12 to 14

Retrenchment page 14

Staying invested (preservation) page 14

Tax pages 14 to 15

Topics

Do you have information on advisers available to me, cost of these and how these are normally paid1

To get help with your individual circumstances, you need to consult a financial adviser. Financial adviser fees are based on what solutions they implement for you, for example if you use your retirement savings to buy a flexible or guaranteed pension. Fees can be charged when a solution is implemented, and on an ongoing basis where you receive ongoing advice, or a combination of these. The upfront fee a financial adviser charges is limited to 1.5% + VAT of the amount you use to buy a pension, but the actual amount is negotiated between you and the adviser. Please contact our My Retirement and Money Matter Centre where you can receive retirement benefit counselling and advice from our qualified consultants: phone 0860 000 381 or email: [email protected]

Is it advisable to sell share stock to top up a pension or keep these separate?2

It depends on your circumstances. The most important aim is to have enough income for the rest of your life. How well prepared you are financially for retirement as well as the type of pension you choose could influence your decision. A professional financial adviser can help you decide which option is best for you based on your circumstances.

There was talk about the union approaching government to allow a drawdown on pension of 6 × monthly salary to assist during the pandemic. I’m assuming if it is approved, it will be part of the non-taxable portion that we are allowed to draw on retirement. Would you recommend this for people close to retirement?

3

The most important thing to keep in mind with any decision relating to your retirement savings is what will give you the best chance of having enough income in retirement for the rest of your life. If the withdrawal you mention is allowed, any decision should be based on your personal circumstances. A professional financial adviser can help you make your decision. We do not know what tax rules would apply if the withdrawal is allowed. However, it is likely that any withdrawal you make would reduce the amount you can take in cash tax free at retirement.

| 1 |

Category: Advice-related

How do we ensure the financial adviser provides independent advice?4

Licensed financial advisers from Alexander Forbes provide professional advice in accordance with professional industry body and regulatory standards. Our advisers provide advice based on the best-practice frameworks of Alexander Forbes. Best practice seeks to make cost-effective solutions with excellent features available to retirement funds. Where these solutions are offered to fund trustees to select as a default option on a fund and have been selected as a default option, our advisers will advise individuals on these solutions where they are appropriate based on individual circumstances as well as providing other options. The solutions that will be proposed to an individual by an Alexander Forbes adviser will be the ones they think are most appropriate based on the features of the solutions (such as cost and benefits) and the person’s individual needs. Alexander Forbes is in a position to review all suitable credible solutions and to recommend those that are most likely to meet needs of individuals based on their personal circumstances. We believe that the value we can add to the lives of our clients using this approach outweighs the value of a purely independent approach.

How do you ensure you ‘get’ the right financial adviser? I don’t want someone “allocat-ed’’ to me with whom I don’t identify.

5

We suggest that you start with the person who is allocated to your fund. If you would prefer to be advised by someone else, we can very easily find someone you would feel more comfortable with. If for example you prefer a person who can speak a specific language, please let us know so that we can match you with someone more suitable. If you don’t feel comfortable with the advice you get, ask for a second opinion.

Will I or should I consider taking out a living annuity as well as a life annuity with my pension when I actually retire? In other words, maybe put half into a life annuity and half into a living annuity?

6

This is possible and something to consider. The Alexander Forbes Retirement Income Solution (AFRIS) product discussed at the webinar offers this type of solution. Your HR representative will be able to tell you if your employer has chosen the AFRIS product for your fund. If not, you could still choose some combination of a flexible and guaranteed pension for your retirement. A financial adviser can help you decide what’s best for you considering your circumstances.

Category: Advice and retirement options

I have two or three sets of ‘funds’ from two different employers. Is there someone who is available to help sort through what I have? And, if so, are there fees attached to this counselling?

7

If your fund has signed up for enhanced retirement benefit counselling, you can speak to a counsellor who will explain your options at no cost to you. Counselling aims to provide information about fund options. To get help with your individual circumstances, you need to consult a financial adviser. Financial adviser fees are based on what solutions they implement for you. The fee a financial adviser charges is agreed between you and your adviser. Please contact our My Retirement and Money Matter Centre where you can receive retirement benefit counselling and advice from our qualified consultants: phone 0860 000 381 or email: [email protected].

| 2 |

I retire in four months. What advice do you have about investing guaranteed and living annuities together?

8

A combination of a guaranteed pension (annuity) and a flexible pension (living annuity) can be a very good one because it offers some of the benefits of each type of solution. It is well suited to those who would like to leave behind some money for others and who would also like to manage the risk of outliving their money. There are different ways to allocate between these two types of pensions. This option may not be best for everybody. For these reasons, the Alexander Forbes combined (hybrid) pension solution requires anybody considering the solution to get advice. A professional financial adviser will help you make a decision that’s right for you based on your circumstances and goals.

| 3 |

Category: Alexander Forbes Retirement Income Solution (AFRIS)

Does the AFRIS option have inflation cover?9

AFRIS includes an option to use a with-profit guaranteed pension as part of the solution which helps manage inflation risk.

Average fees seem to be about 2% on a living annuity. How much lower are AFRIS fees in comparison to average industry fees?

10

The average fee discount on AFRIS against other flexible pensions (living annuities) you can access in the market is approximately 0.53% a year.

If one opts to defer taking pension for now, does the AFRIS option remain open to us when we do take our pension?

11

Yes. If the AFRIS option is available on your fund (check with your HR person if you’re not sure), you can still decide to get a pension using the AFRIS solution when you’re ready. If you decide to take a pension later rather than now, you don’t need to decide up front that you are interested in AFRIS. You can defer your retirement for months or years before deciding to use the AFRIS solution.

There was mention of eligibility relating to AFRIS. Please advise the parameters. 12

You can check with your retirement fund trustees or HR person if AFRIS is available on your fund. If you are part of the Alexander Forbes retirement fund, the AFRF, you are already approved for AFRIS.

Is it possible to withdraw a complete pension at retirement?12

Members of provident funds can draw the full amount in cash. Pension fund members are limited to one-third of the benefit in cash. If the total saved is less than R247 500, the whole amount can be taken in cash. It is very important to make sure that you will have enough to live on for as long as you live.

Category: Cash withdrawals at retirement

| 4 |

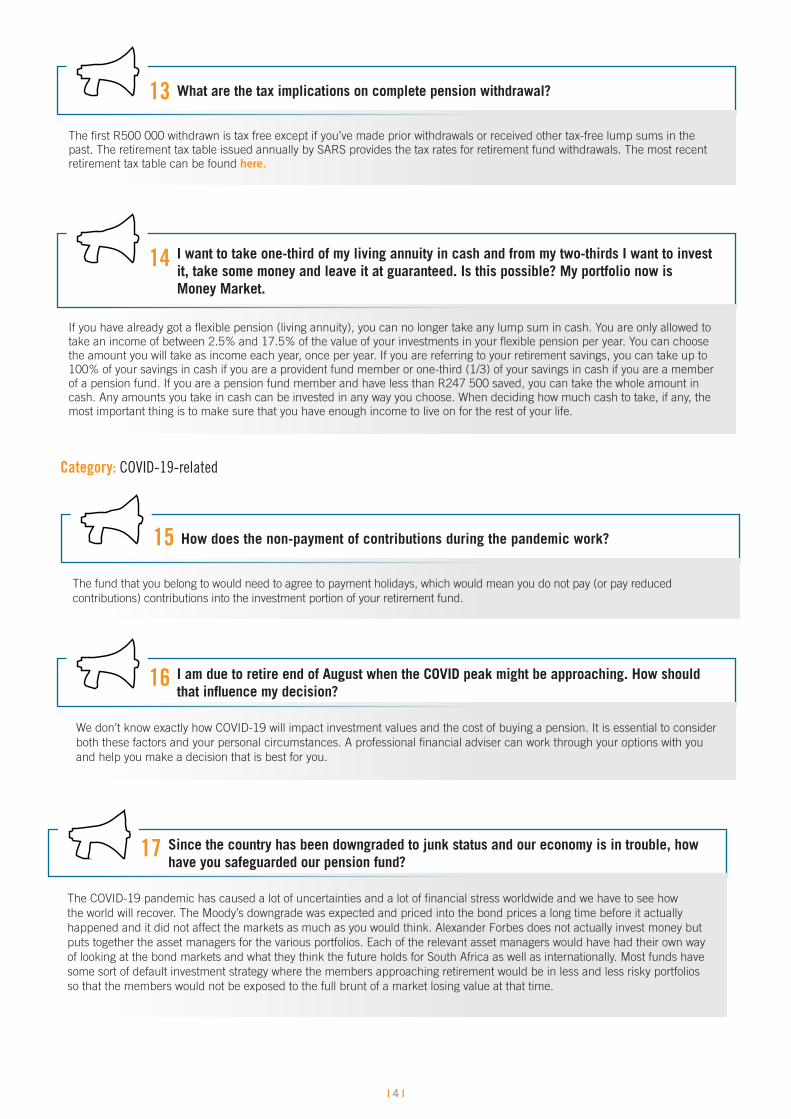

What are the tax implications on complete pension withdrawal?13

The first R500 000 withdrawn is tax free except if you’ve made prior withdrawals or received other tax-free lump sums in the past. The retirement tax table issued annually by SARS provides the tax rates for retirement fund withdrawals. The most recent retirement tax table can be found here.

I want to take one-third of my living annuity in cash and from my two-thirds I want to invest it, take some money and leave it at guaranteed. Is this possible? My portfolio now is Money Market.

14

If you have already got a flexible pension (living annuity), you can no longer take any lump sum in cash. You are only allowed to take an income of between 2.5% and 17.5% of the value of your investments in your flexible pension per year. You can choose the amount you will take as income each year, once per year. If you are referring to your retirement savings, you can take up to 100% of your savings in cash if you are a provident fund member or one-third (1/3) of your savings in cash if you are a member of a pension fund. If you are a pension fund member and have less than R247 500 saved, you can take the whole amount in cash. Any amounts you take in cash can be invested in any way you choose. When deciding how much cash to take, if any, the most important thing is to make sure that you have enough income to live on for the rest of your life.

How does the non-payment of contributions during the pandemic work?15

The fund that you belong to would need to agree to payment holidays, which would mean you do not pay (or pay reduced contributions) contributions into the investment portion of your retirement fund.

Category: COVID-19-related

I am due to retire end of August when the COVID peak might be approaching. How should that influence my decision?

16

We don’t know exactly how COVID-19 will impact investment values and the cost of buying a pension. It is essential to consider both these factors and your personal circumstances. A professional financial adviser can work through your options with you and help you make a decision that is best for you.

Since the country has been downgraded to junk status and our economy is in trouble, how have you safeguarded our pension fund?

17

The COVID-19 pandemic has caused a lot of uncertainties and a lot of financial stress worldwide and we have to see how the world will recover. The Moody’s downgrade was expected and priced into the bond prices a long time before it actually happened and it did not affect the markets as much as you would think. Alexander Forbes does not actually invest money but puts together the asset managers for the various portfolios. Each of the relevant asset managers would have had their own way of looking at the bond markets and what they think the future holds for South Africa as well as internationally. Most funds have some sort of default investment strategy where the members approaching retirement would be in less and less risky portfolios so that the members would not be exposed to the full brunt of a market losing value at that time.

| 5 |

If I defer the pension, does the pension appreciate or depreciate in value subject to the market return? Does the deferred pension earn dividends if applicable while it is deferred?

18

The answer to both your questions is ‘yes’.

Category: Delay (defer) retirement

How long can you defer before you are forced to take the money and purchase a pension?19

There are no legal restrictions. Check with your employer about any employer-specific rules.

Once the funds have been deferred, when and how are they accessible?20

If you have deferred your retirement in your employer’s retirement fund, you can access your retirement savings at any time in the future. There is no notice period or need to pre-select a retirement date. The process is that you contact your adviser or the Alexander Forbes contact centre if you are not sure who to speak to and tell them that you would like to retire from your deferred fund. You will need to keep a record of the fund you deferred in so that we can assist you. It is important to keep in mind that the retirement process takes approximately six weeks. This period starts from when we receive your retirement notice and ends when the funds are transferred or taken in cash according to your instruction. This means that if you buy a pension with your retirement fund savings, you will only receive your first pension payment two to three months after you give notice. When you are planning for retirement, please factor this administration period into your plans.

If I defer my retirement, will there always be the tax-free R500 000 cash option when I take it later?21

Yes, but it is important to note that any previous cash withdrawals from retirement savings when changing jobs or receiving tax-free lump sums, such as if you get retrenched, reduce the R500 000 tax-free amount at retirement. A professional financial adviser can help you work out the tax-free amount applicable to you at retirement based on your circumstances.

Please advise whether a deferred pension continues to increase in value (subject to market conditions). Please advise whether the deferred pension earns dividends?22

Yes, a deferred pension is still invested in the portfolio you have chosen and you should still be able to switch the portfolio while you are deferred, depending on the fund rules. As you suggest, the value of your savings will depend on changes in investment values in the portfolio your savings are invested in. If there are shares in that portfolio, it can receive dividends. There is no tax on dividends or interest or capital gains tax (CGT) payable in a pension or provident fund, so any growth in the value of your savings is tax free.

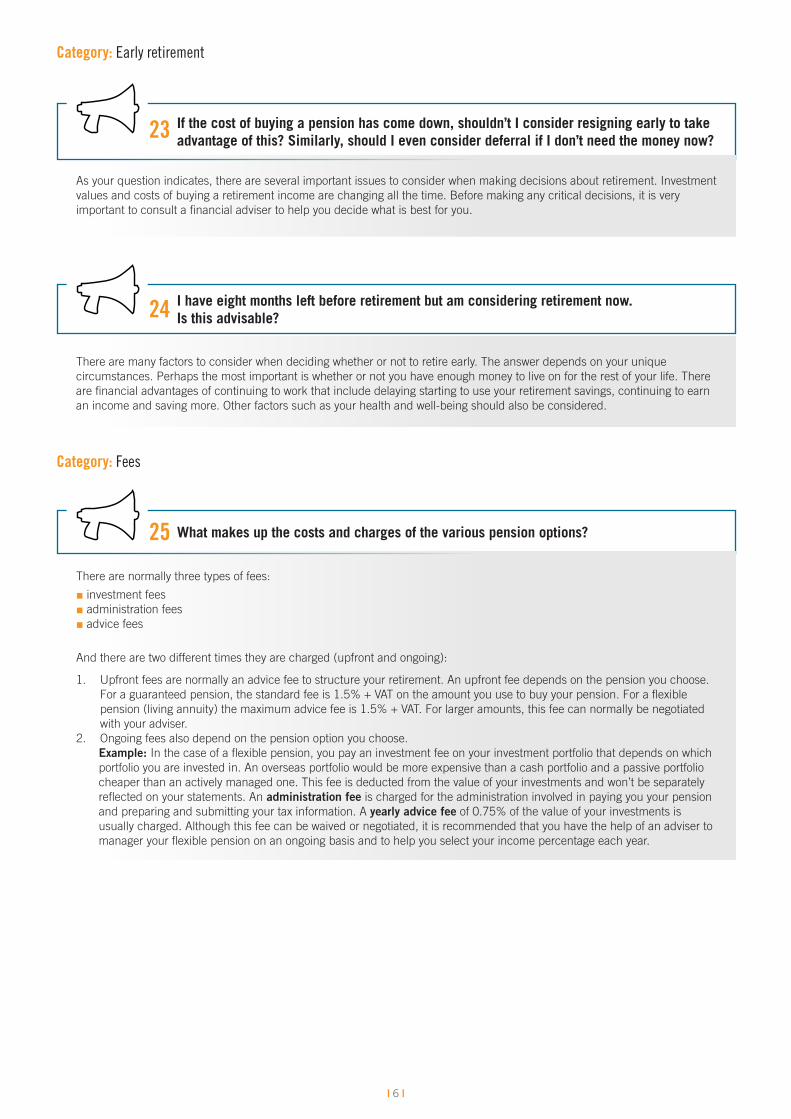

If the cost of buying a pension has come down, shouldn’t I consider resigning early to take advantage of this? Similarly, should I even consider deferral if I don’t need the money now?23

As your question indicates, there are several important issues to consider when making decisions about retirement. Investment values and costs of buying a retirement income are changing all the time. Before making any critical decisions, it is very important to consult a financial adviser to help you decide what is best for you.

Category: Early retirement

I have eight months left before retirement but am considering retirement now. Is this advisable?24

There are many factors to consider when deciding whether or not to retire early. The answer depends on your unique circumstances. Perhaps the most important is whether or not you have enough money to live on for the rest of your life. There are financial advantages of continuing to work that include delaying starting to use your retirement savings, continuing to earn an income and saving more. Other factors such as your health and well-being should also be considered.

| 6 |

Category: Fees

What makes up the costs and charges of the various pension options?25

There are normally three types of fees:

■ investment fees■ administration fees ■ advice fees

And there are two different times they are charged (upfront and ongoing):

1. Upfront fees are normally an advice fee to structure your retirement. An upfront fee depends on the pension you choose. For a guaranteed pension, the standard fee is 1.5% + VAT on the amount you use to buy your pension. For a flexible pension (living annuity) the maximum advice fee is 1.5% + VAT. For larger amounts, this fee can normally be negotiated with your adviser.

2. Ongoing fees also depend on the pension option you choose. Example: In the case of a flexible pension, you pay an investment fee on your investment portfolio that depends on which portfolio you are invested in. An overseas portfolio would be more expensive than a cash portfolio and a passive portfolio cheaper than an actively managed one. This fee is deducted from the value of your investments and won’t be separately reflected on your statements. An administration fee is charged for the administration involved in paying you your pension and preparing and submitting your tax information. A yearly advice fee of 0.75% of the value of your investments is usually charged. Although this fee can be waived or negotiated, it is recommended that you have the help of an adviser to manager your flexible pension on an ongoing basis and to help you select your income percentage each year.

I’ll be retiring in three years’ time. What happens to the group life cover beyond retirement date?26

Additional benefits such as group life generally stop when you retire. However, if your fund has a continuation option, your cover can continue if you sign up for it.

Category: Group life cover at retirement

How or why is income from pension dependent on gender? Why does that make a difference?27

On average females live longer than males, which would mean that the average female would need more income over her lifetime in relation to a male of the same age.

Category: Guaranteed pension for life

Can you pay some funds from a guaranteed option into a flexible option?28

No, unfortunately you can’t transfer any portion from a guaranteed option into a flexible option once the guarantees structure is set up.

| 7 |

What happens to the capital amount of the pension under the guaranteed pension scheme when I die say in the first year?29

It depends on what options you’ve selected when buying a guaranteed pension. If you have not selected a guarantee period and have not elected for your spouse to continue receiving a pension when you die, then all payments will stop when you die. If you have elected for pension payments to continue to your spouse after your death until their death, then these payments will continue when you die. If you select a guarantee period, then your beneficiaries will continue to get the same income as your pension when you die. This is important if there are family members who depend on you. Some pension providers offer the option for the payments to be made in a lump sum once off when you die. For example: If you chose a guaranteed pension with a ten-year guarantee and you pass away after one year, your beneficiaries will receive the same amount you were receiving for another nine years.

Category: Investment choice

If I am close to retirement, what flexibility do I have to make different investment options?30

Check with your retirement fund whether you have member investment choice (MIC), which will give you flexibility when choosing your investment strategy.

What is advisable – saving extra cash in pension funds or other instruments?31

Since retirement fund contributions are tax deductible up to 27.5% of your yearly taxable salary, up to a limit of R350 000 a year, if you’re below this limit saving more in your retirement fund is usually a good idea. However, where you save extra money depends on your investment objective. For example, retirement funds have investment limits imposed by regulations. Other savings products may have fewer restrictions. A financial adviser can assist you to make the choice that’s right for you.

With the myriad challenges facing South Africa in the near future – SOEs, effects of COVID-19 and so on – should one be considering options which allow maximum offshore investment?

32

Regulation 28 of the Pension Funds Act limits offshore investments to 30% of total assets. Investment managers take into account prevailing conditions such as the ones you mention when deciding how much to allocate to offshore investments. A financial adviser can help you work out the most appropriate allocation between domestic and offshore investments for you based on your personal circumstances.

What is your view on gold, silver and bitcoin as investment vehicles in the current market or near future?33

The investment managers that the Alexander Forbes investment team appoint consider all investments that are allowed by the Pension Funds Act. Investments are managed by selecting asset managers and allocating funds to these managers through mandates that comply with regulatory limits. Regulations do not currently allow for the inclusion of bitcoin in retirement funds. Gold and other commodities like silver are allowed.

| 8 |

Please explain the lifestage model.34

The lifestage model automatically starts moving your retirement savings from growth investments (more risky) such as shares into less risky assets such as cash funds as you get closer to retirement. A person one year from retirement, for example, will still have some growth investments but most of their savings will be invested in less risky investments whereas a person further from retirement will have a higher amount of growth investments and less cash-type investments.

As it advisable to pay in extra to the provident fund at this time when the markets are so volatile?

35

Since retirement fund contributions are tax deductible up to 27.5% of your yearly taxable salary up to a limit of R350 000 a year, if you’re below this limit saving more in your retirement fund is usually a good idea. If you’re worried about the share market, you can select a less risky fund to put your money into. Although we can’t say for sure what will happen now, after all the market crashes since 1969 share markets have recovered within one to three years.

Given what you showed about market turbulence in March and the offset of bond yields in buying a pension, why does one need to become more defensive in one’s portfolio as retirement approaches?

36

Bond interest rates don’t always improve when share markets are down as they did during this period. This is why a gradual reduction in shares (and other riskier investments) is still recommended if you are planning to buy a guaranteed pension at retirement.

As a current employee still saving towards retirement, if one wants to effect a switch on an investment vehicle, there is an indeterminate delay between instructing that switch to happen and when the switch is actually effected. Why can this not be on the same day in this day and age with the technology available to us? The market could quite conceivably move by 5% during the delay I refer to.

37

A retirement fund is unfortunately not a direct share portfolio that you could be referring to where trades can be done immediately. There are certain procedures and checks to protect the member and assets have to be sold not only out of a single share portfolio but also out of cash and bonds and internationally held investments even for basic switches. Retirement fund investment strategies also do not try to time the market, as it has been shown repeatedly that time in the market gives more value over time that trying to time the market by switching in and out of portfolios. We don’t recommend switching portfolios unless your risk or investment requirements change and in that case your risk or requirements shouldn’t change so quickly that a switch needs to take place immediately.

| 9 |

Category: Medical

Will I still have medical aid cover after retirement? If so, how much is it going to cost me?38

Yes, your medical cover should continue after retirement, but you become responsible for paying the premiums. The cost depends on the medical aid provider and the option you choose. A financial adviser can advise you on the best options to meet your individual needs.

Medical aid: on retirement does my employer continue to contribute to medical aid? 39

Most pensioners have to pay their own medical aid premiums in retirement. Please check with your employer if there are any medical subsidies available to you.

Is the R7 269 after tax?40

Your question refers to the slide in which we show an example of the impact of the changes in financial markets in March 2020 on the cost of buying a retirement income. The amounts shown are estimates and are before any tax has been deducted.

Category: Questions about Michael Prinsloo’s presentation

Who are the pension providers?41

Pension fund providers can be life insurance companies and other companies, such as asset managers who have life insurance licences. Pension providers have to comply with laws that protect your pension.

What is the cost of buying a pension – is it a lumpsum cost or it is deducted monthly?42

You buy a retirement income (pension) with a lump sum. Depending on which pension option you choose, there may be upfront fees or ongoing monthly fees or both.

What is the ‘personal’ inflation of the South African upper middle class?43

The personal inflation of each individual depends on what they spend their income on. Each person would need to calculate their own inflation. The easiest way to do this would be to measure how prices increase every year based on your unique spending pattern.

| 10 |

Is the R7 290.00 that can be purchased per R1m referred to by Michael Prinsloo after tax and fees? Would this be the members’ net monthly income?44

Your question refers to the slide in which we show an example of the impact of the changes in financial markets in March 2020 on the cost of buying a retirement income. The amounts shown are estimates and are before any tax has been deducted.

Is the example of the AFRIS living annuity before tax on the slide What’s the benefit to you?45

Yes, the amounts shown in the example are before any tax is deducted.

Please expand on the role of the bond rate in the cost of a pension.46

Higher long-term government bond interest rates mean you can get a higher pension for the same amount of money than you can when long-term government bond interest rates are lower. This relates to the ease with which a pension provider can fund its payments to you when they receive higher income on their investments.

Does Alexander Forbes manage the investment?47

Alexander Forbes Investments manages your retirement savings using a multi-manager approach. This involves deciding how to allocate retirement fund money to different types of investments managed by different asset managers who manage the underlying investments (such as shares, bonds, property and cash) in a specific way. Alexander Forbes Investments monitors these asset managers and their performance.

Do I have to use one pension provider or could I use say Alexander Forbes for my employer’s provident fund pension and another provider for the remainder of retirement funds?

48

Yes, you can use more than one pension provider.

Category: Retirement options

Can you pay into a fund from other savings?49

Yes, this is possible. The process for adding money to your retirement savings will differ from fund to fund.

| 11 |

Can I buy two pensions – one now with my funds from my current employer’s retirement fund and one in a few years with my retirement annuities?50

Yes, you can.

Will you be able to draw a government pension while you draw an Alexander Forbes pension?51

The older person’s grant, as it is now called, requires you to be a South African citizen or permanent resident, have income and assets less than a certain amount and not receive another social grant. The limits that apply and other rules can be found here.

Can I take more than one option – and change if I like another option?52

It is always possible to convert a flexible pension or the flexible part of a combined (hybrid) pension to a guaranteed pension. It is not possible to change a guaranteed pension once it has been bought.

I have a portion of my pension – the old Super flex – and that is separate to my current portion. What do I do in a case like this?53

If you set up a flexible pension (living annuity), you can combine all your external pre-retirement funds into one flexible pension irrespective of who the service provider is. You don’t have to keep your savings with the pre-retirement service provider. You can in most cases also merge existing flexible pensions and you can also top up an existing flexible pension with maturing retirement annuities or pension or provident funds and preservation funds.

Is saving realistically for retirement enough to fund longevity?54

Yes, by choosing the correct annuity at retirement you can mitigate longevity risk.

Everybody always asks you the question: Do you want the same lifestyle after your retirement as before? Is this the right question to ask? I personally do not want the same lifestyle.

55

This is a personal decision and it depends on each individual’s objectives for retirement.

Category: Retirement planning

| 12 |

Can one stagger drawing from a retirement annuity then from a provident fund? Is this sequence advisable?56

This is possible. There is no rule of thumb for what is best to do. What is best for you will depend on your circumstances. A financial adviser can help you make these decisions, taking your unique circumstances into account.

Have any comparative studies been done between drawing to start a business compared with buying a pension?57

According to the University of the Western Cape, 70% to 80% of small businesses fail within 5 years. If you use your retirement savings to buy a guaranteed pension for life, you will be certain about what you will receive for the rest of your life. What you decide to do in your retirement years should depend on your needs and circumstances. All retirement decisions are important. Some retirement decisions are riskier than others. It would be essential to consult a professional financial adviser before making this decision.

The pension planning tool on AF Online – what assumptions does it make when calculating the monthly pension that one’s fund credit can buy? Does it assume that the current fund credit is what will be available on a ‘normal’ retirement age of 60 and calculate accordingly with regard to gender, living expenses and so on?

58

A full description of how to use the tool to find out what estimated pension you might receive can be found here. The online calculator allows you to capture the savings you expect to buy a pension with, a retirement age and other options to provide an estimate of various types of guaranteed pension income.

The investment retirement options are applicable when you are wanting to retire ... correct? So to choose between a guaranteed or flexible option is a decision when you actually want to retire now. Correct?

59

Yes, that is correct.

What is a good ratio of savings to retirement income required if one wants to consider retiring early, say at 60 or 61 years? Can you share a table as a basic guide? 60

The most important thing is to make sure that you will have enough income to live on for the rest of your life. As a starting point, it is essential to work out how much you will need when you retire. This means preparing a realistic budget that considers your expense needs as you age, including likely medical costs.

| 13 |

How can I follow up on this webinar to start actively planning for my retirement (two years from now)?61

It’s a good idea to speak to a professional financial adviser to start planning for your retirement. Having a bit of time to go means that you have more options. You can also check to see if you’re on track by logging in to our website and following the relevant steps in this guide.

When I retire, how will my pension payout be calculated?62

If you set up a guaranteed income, your monthly income will be calculated based on your age, sex and the amount you have to buy the monthly income. They also take into account if you are married and your spouse’s age and sex. If you opt for a flexible pension at retirement, you will specify the income you want. The younger you are at retirement, the smaller your drawdown rate should be.

In the event of retrenchment, would it be advisable to use the pension or provident fund and pay off the biggest debt (home loan)?

63

The most important thing is to make sure that you have enough money to live on for as long as you need it – especially in these uncertain times when we expect the unemployment rate to rise. Things to factor into your decision: Interest rates are at their lowest levels in 40 years, therefore having debt is relatively cheap. If you have other debt, it will most likely be more expensive than your home loan. If you’re going to reduce your debt, reduce more expensive debt first. If you use your savings to reduce or pay off your home loan, try to make sure that you can get access to the money again if you need it to live on. A financial adviser can help you decide what’s best for you considering your personal circumstances.

Should I be retrenched today, how will my pension be calculated? Will there be a benefit for me?

64

If you are in a defined contribution (DC) fund, your retirement benefit would be the value that you have in the fund when you retire. If you are in a defined benefit (DB) fund, the retirement benefit is calculated based on your salary and years of service. If you are being retrenched, it might be possible to negotiate that the penalties for early retirement be waived on your DB fund. Irrespective of whether you are on a DC or DB fund, if you are over the age of 55 when you get retrenched, then you can choose to retire if you want to receive a monthly income.

What is a preservation fund and can my provident fund be turned into such a fund?65

A preservation fund is a type of retirement fund which allows you to keep your savings invested. You could transfer your retirement savings to a preservation fund when you change jobs or at retirement if you don’t want to leave your savings in your employer’s fund. Before retirement, you can make a once-off withdrawal from a preservation fund. After retirement, you can use a preservation fund if you don’t want to start receiving a pension yet and don’t want to defer your retirement (only buy a pension later) in your employer’s fund.

Category: Staying invested (preservation)

| 14 |

I currently receive a disablement salary and do not pay tax. When I retire in February 2021, do I have to pay tax?66

Whether or not you will pay tax when you retire depends on your income and the tax rules and tax tables applicable to you. A professional financial adviser can help you work out if you will pay any tax after you retire and if so, how much.

Category: Tax

Category: Retrenchment

What happens if you emigrate before retirement? What are the tax implications and can you withdraw in full? Do you have the option of leaving your money in South Africa?67

If you are emigrating, you can withdraw your full benefit in cash and the withdrawal tax table will apply. You also have the option of leaving your money in South Africa. In that case, normal tax and pension rules will apply.

Where can one find tax tables applicable to pension fund monthly payouts?68

The applicable tax table is the same as the table applicable to you as an employee and can be found here.

Credit: Alexander Forbes Communications (production) 19854-FAQ-2020-06-18

| 15 |