Your FutureStep™ Group RRSP Enrolment Guide -...

36

Your FutureStep™ Group RRSP Enrolment Guide

Transcript of Your FutureStep™ Group RRSP Enrolment Guide -...

Your FutureStep™ Group RRSP Enrolment Guide

➥

About this Enrolment GuideThis guide provides information you will need to enroll in your company’s Group RRSP. Your employer is investing in your

future by providing an easy to understand Group RRSP.

You have two enrolment options:1. If you want to enroll in minutes and you don’t plan on spending a lot of time monitoring your investments,

determine the Retirement Date Fund closest to the year you plan to retire from the table below and write it in the

box at the top of page four of the application on the next page.

Tear out the application, complete the required sections, and send it to Manulife Financial using the instructions on

the application.

2. If you would like to take more time to determine your investor style and select your investments, a colour coded,

step by step process starts on page 6 that will help you navigate through this guide. Each step includes a ‘To Do’ box

showing what you must complete to enroll. The boxes separate what you must do from what you should

simply keep in mind.

2

If you plan to retire duringthe period…

The Retirement Date Fund for you is… Fund code

2011 – 2015 Manulife Retirement Date 2015 2015

2016 – 2020 Manulife Retirement Date 2020 2020

2021 – 2025 Manulife Retirement Date 2025 2025

2026 – 2030 Manulife Retirement Date 2030 2030

2031 – 2035 Manulife Retirement Date 2035 2035

2036 – 2040 Manulife Retirement Date 2040 2040

2041 – 2045 Manulife Retirement Date 2045 2045

2046 or later Manulife Retirement Date 2050 2050

If you are already retired orapproaching retirement...

The Retirement Date Fund for you is… Fund code

Manulife Retirement Income Fund 2000

Fast path!

3

Application FormGroup Retirement Savings Plan (RSP)

Name your beneficiary (or beneficiaries)If you do not name a beneficiary, proceeds will be paid to your estate.

Check here if you have attached a separate page listing your beneficiaries. Please sign and date.

The above beneficiary designations are considered revocable unless you write “irrevocable” in the chart above.

For Quebec only:The designation of a spouse as a beneficiary is deemed to be irrevocable unless specified here: Revocable

Tell us about the planIf you aren’t sure how to completeany of these boxes, your PlanAdministrator can help you or youcan call Customer Service at1-888-727-7766.

Your personal information

Tell us about the contributor (the member)Complete this section only if theapplication is for you as a SpousalMember. Otherwise, leave thissection blank.

Please print clearly in the blank boxes.Important: If this application is for a spousal RSP, the spouse (i.e. Spousal Member) must complete this form.

Send your completed form to:Manulife FinancialAttn: GRS Client ServicesPO BOX 396 STN WATERLOOWATERLOO, ON N2J 4A9

Check one:This RSP is for you as a Member (i.e. employee)This RSP is for you as a Spousal Member

Plan Sponsor/Employer Group annuity policy number

Member number Division Member Class

Date you are joining the plan (mmm/dd/yyyy) Date you started with your employer (mmm/dd/yyyy)

Gender First name Middle initial Last name

Mailing address (number, street and apartment number)

City Province Country Postal Code

Date of birth (mmm/dd/yyyy) Social Insurance Number (SIN) Marital status

Your preferred language Telephone number* Ext.* Email address*

First name Middle initial Last name

Date of birth (mmm/dd/yyyy) Social Insurance Number (SIN)

Trustee name Relationship

Name Relationship Percentage of proceeds

A revocable beneficiary can bechanged at anytime.

An irrevocable beneficiary canonly be changed with writtenconsent from that beneficiary. Youwill also need your beneficiary’sconsent to withdraw or transfermoney from your account. A parentor guardian cannot provide consenton behalf of a minor who has beennamed as irrevocable beneficiary.

If you want to name more thanthree beneficiaries, attach aseparate page with the names andthe percentage of proceeds foreach beneficiary.

If you have locked-in money in yourRSP and you have a spouse on thedate of your death, the law mayrequire any death benefit be paid toyour spouse, regardless of otherbeneficiaries you’ve named.

If you die while your beneficiary isstill a minor, the trustee you nameon this form will act on the child’sbehalf.

The Manufacturers Life Insurance Company R etain a copy for your files.Page 1 of 3

Trustee for a minor beneficiary named above (not applicable in Quebec) Any payment to a beneficiary who is a minor will be paid in trust to the trustee named below.In Quebec, the proceeds will be paid in trust to the minor child's tutor.

*These fields are optional.

Not Applicable Not Applicable

4

If you do not complete this section,or the total does not add up to100%, your contributions will beinvested in the Retirement Date Fund

You can go online at anytime tochange the funds you have chosen.

The minimum amount you can investin a fund is 5%.

Percentages must be whole numbers.

Note: The investmentperformance of a market-basedfund is not guaranteed.

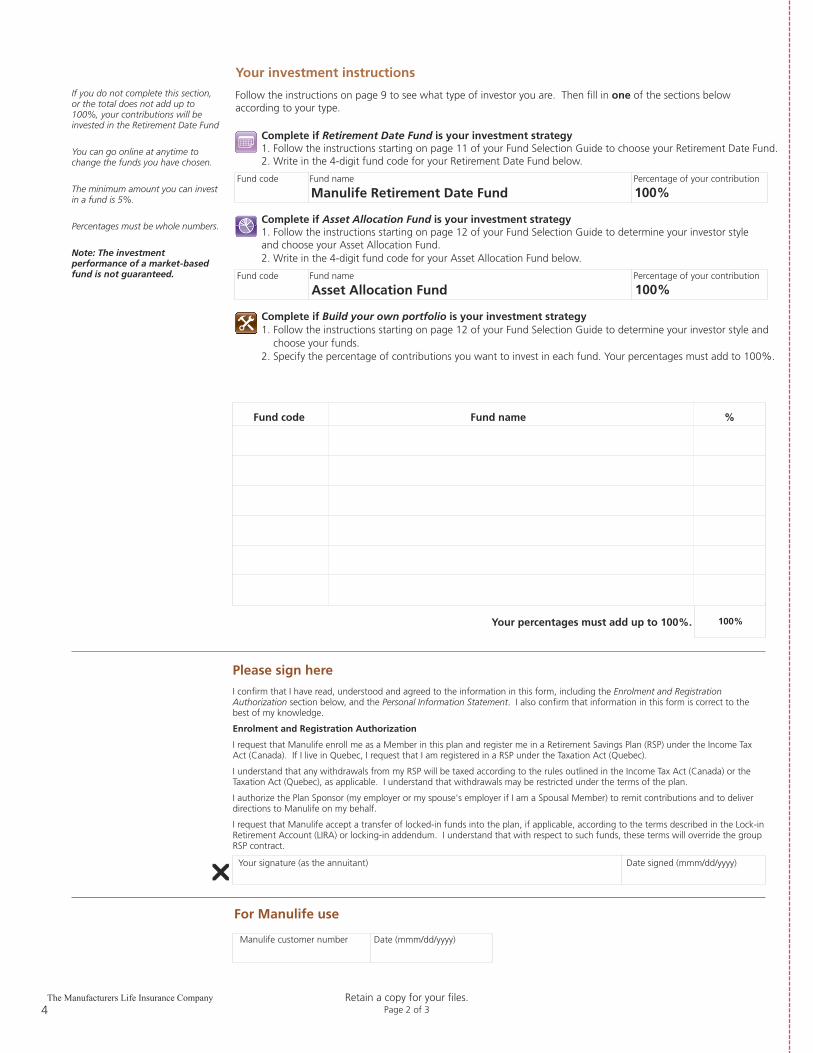

Please sign here

I confirm that I have read, understood and agreed to the information in this form, including the Enrolment and RegistrationAuthorization section below, and the Personal Information Statement. I also confirm that information in this form is correct to thebest of my knowledge.

Enrolment and Registration Authorization

I request that Manulife enroll me as a Member in this plan and register me in a Retirement Savings Plan (RSP) under the Income TaxAct (Canada). If I live in Quebec, I request that I am registered in a RSP under the Taxation Act (Quebec).

I understand that any withdrawals from my RSP will be taxed according to the rules outlined in the Income Tax Act (Canada) or theTaxation Act (Quebec), as applicable. I understand that withdrawals may be restricted under the terms of the plan.

I authorize the Plan Sponsor (my employer or my spouse's employer if I am a Spousal Member) to remit contributions and to deliverdirections to Manulife on my behalf.

I request that Manulife accept a transfer of locked-in funds into the plan, if applicable, according to the terms described in the Lock-inRetirement Account (LIRA) or locking-in addendum. I understand that with respect to such funds, these terms will override the groupRSP contract.

Your signature (as the annuitant) Date signed (mmm/dd/yyyy)

Manulife customer number Date (mmm/dd/yyyy)

100%

For Manulife use

Fund code Fund name %

Your percentages must add up to 100%.

The Manufacturers Life Insurance Company Retain a copy for your files.Page 2 of 3

Your investment instructions

Follow the instructions on page 9 to see what type of investor you are. Then fill in one of the sections belowaccording to your type.

Complete if Retirement Date Fund is your investment strategy1. Follow the instructions starting on page 11 of your Fund Selection Guide to choose your Retirement Date Fund. 2. Write in the 4-digit fund code for your Retirement Date Fund below.

Complete if Asset Allocation Fund is your investment strategy 1. Follow the instructions starting on page 12 of your Fund Selection Guide to determine your investor styleand choose your Asset Allocation Fund. 2. Write in the 4-digit fund code for your Asset Allocation Fund below.

Complete if Build your own portfolio is your investment strategy 1. Follow the instructions starting on page 12 of your Fund Selection Guide to determine your investor style and

choose your funds. 2. Specify the percentage of contributions you want to invest in each fund. Your percentages must add to 100%.

Fund code Fund name Percentage of your contribution

Fund code Fund name Percentage of your contribution

Manulife Retirement Date Fund

Asset Allocation Fund

100%

100%

��

5

The personal information statementYour consent to use your personal informationBy signing this Application form, you give your consent for us to obtain, verify, and share your personal information, as set out below, in administering youraccount, now and in the future, with the plan sponsor, the plan administrator, the plan advisor and its employees and other parties in the performance oftheir duties for us.

You authorize us to use your Social Insurance Number (SIN) if applicable, to uniquely identify you during the administration of your account.

How we will maintain and use your personal informationYou agree that we may use the personal information that we collect to:

� comply with legal and regulatory requirements,� confirm your identity and the accuracy of the information you’ve provided,� conduct searches to locate you and update your member information,� administer this plan while you actively work for your employer, and after you no longer work with your employer,� administer any other products and service that we provide to you, and� determine your eligibility for, and provide you with details of, other select financial products or services that may be of interest to you that are

offered by us, our affiliates or other select financial product providers.

Who may access your personal informationThe following individuals may have access to your personal information:

� our employees and representatives who require this information to do their jobs,� the plan advisor, including its employees, appointed by your Plan Sponsor to provide ongoing benefit counselling or plan administrative

services,� people to whom you have granted access,� people who are legally authorized to view your personal information, and� service providers who require this information to do their jobs.

This may include data processing, programming, printing, mailing, distribution, research and marketing or administration and investigation services.

Asking us not to use your personal informationYou may withdraw your consent for us to use your SIN for non-tax administration purposes. You may also withdraw your consent for us to use yourpersonal information to provide you with other product or service offerings, except those that are mailed with your statements.

If you wish to withdraw your consent for us to collect, use, retain or share your personal information, you may contact us by phoning our customer servicecentre at 1-888-727-7766 or by writing to the Privacy Officer at the address below.

How long we can keep your personal informationYou authorize us to keep your personal information for the longer of:

� the time period required by law and by guidelines set for the financial services industry, and� the time period required to administer the products and services we provide.

The information we collect with your consent will be protected and maintained in your Manulife plan member file.

The personal information that we must haveYou may not withdraw your consent for us to collect, use, retain or share personal information that we need to issue or administer your account unlessfederal or provincial laws give you this right. If you do so, we may no longer be able to properly administer your account and this is what could happen:

� benefits will not be payable as provided under the plan,� we may treat your withdrawal of consent as a request to terminate your contract, and� your rights, and the rights of your beneficiary or estate under the plan may be limited.

Recording your customer service calls to usWe may record your customer service calls to us for the following reasons:

� quality service controls,� information verification, and� training.

If you do not wish to have your calls recorded, you must communicate with us in writing to Group Savings and Retirement Solutions, 25 Water StreetSouth, Kitchener, ON N2G 4Y5, and request that any response by us also be in writing.

Questions, updates and requests for additional informationIf you have a request, a concern, or wish to receive more information about our privacy policies, or if you wish to review your personal information in ourfiles or correct any inaccuracies, you may contact us by sending a written request to: Privacy Officer, Group Savings and Retirement Solutions, 25 WaterStreet South, Kitchener ON N2G 4Y5.

The Manufacturers Life Insurance Company Retain a copy for your files.Page 3 of 3

6

Stepone

Step one: Learn about the advantages of your group savings program

Step two: Enroll in your Group RRSP

Step three: Decide how to invest

Step four: Transfer RRSP assets into this Group RRSP

Step five: Check to see you’ve completed each step

Here’s what you need to do...

Let’s Get Started...

7

Stepone

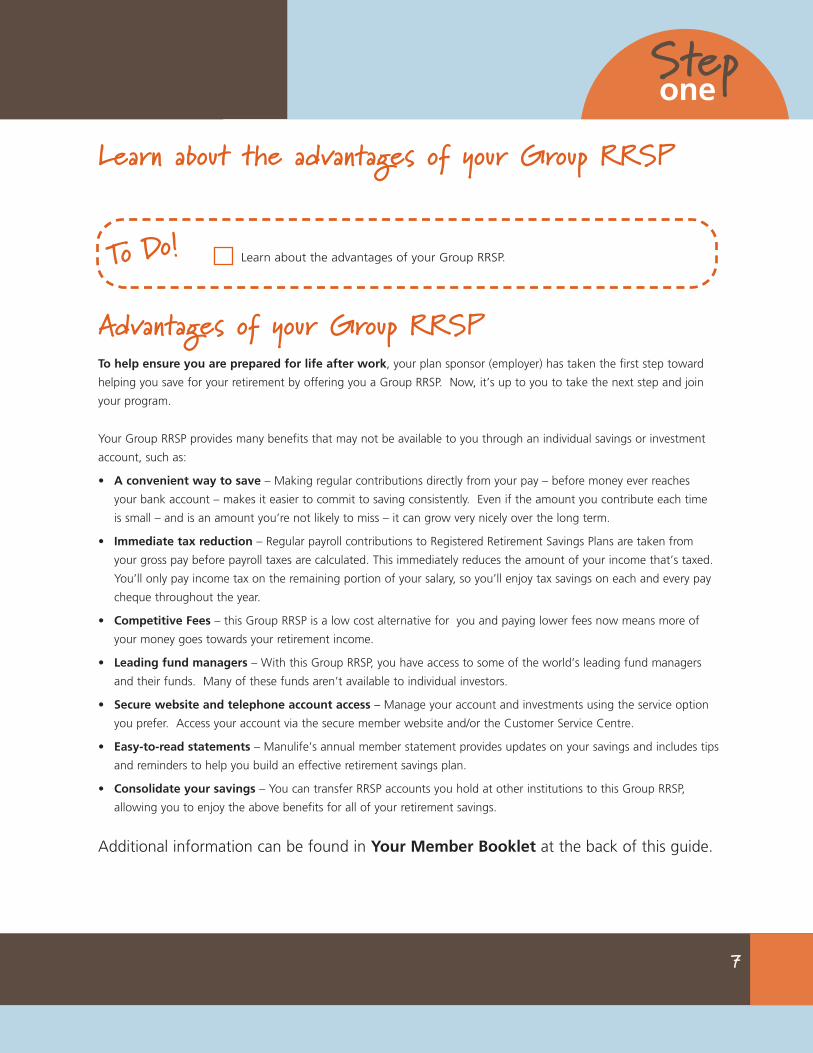

Learn about the advantages of your Group RRSP

Advantages of your Group RRSPTo help ensure you are prepared for life after work, your plan sponsor (employer) has taken the first step toward

helping you save for your retirement by offering you a Group RRSP. Now, it’s up to you to take the next step and join

your program.

Your Group RRSP provides many benefits that may not be available to you through an individual savings or investment

account, such as:

• A convenient way to save – Making regular contributions directly from your pay – before money ever reaches

your bank account – makes it easier to commit to saving consistently. Even if the amount you contribute each time

is small – and is an amount you’re not likely to miss – it can grow very nicely over the long term.

• Immediate tax reduction – Regular payroll contributions to Registered Retirement Savings Plans are taken from

your gross pay before payroll taxes are calculated. This immediately reduces the amount of your income that’s taxed.

You’ll only pay income tax on the remaining portion of your salary, so you’ll enjoy tax savings on each and every pay

cheque throughout the year.

• Competitive Fees – this Group RRSP is a low cost alternative for you and paying lower fees now means more of

your money goes towards your retirement income.

• Leading fund managers – With this Group RRSP, you have access to some of the world’s leading fund managers

and their funds. Many of these funds aren’t available to individual investors.

• Secure website and telephone account access – Manage your account and investments using the service option

you prefer. Access your account via the secure member website and/or the Customer Service Centre.

• Easy-to-read statements – Manulife’s annual member statement provides updates on your savings and includes tips

and reminders to help you build an effective retirement savings plan.

• Consolidate your savings – You can transfer RRSP accounts you hold at other institutions to this Group RRSP,

allowing you to enjoy the above benefits for all of your retirement savings.

Additional information can be found in Your Member Booklet at the back of this guide.

To Do! Learn about the advantages of your Group RRSP.

8

Steptwo

Enroll in your Group RRSP

Included with this Guide is an application form on page 3 for you to tear out and complete.

Complete the following sections on the Application form:

• Tell us about your plan

• Your personal information

• Name your beneficiary (or beneficiaries)

Once you have completed these sections on the Application form, go to the next step in this Guide.

Follow the instructions to enroll in your Group RRSP.To Do!

9

To Do!

Note - If you consult a Financial Planner for advice regarding funds for this Group RRSP, provide him or her with

this Guide. If you do not generally seek the advice of a financial planner before making investment decisions, please

continue reading.

threeStep

Decide how to invest

Follow the instructions on the following pages to determine your investor style.

Review the Group Investment Report and Rate of Return Overview included with this

Guide for detailed information about the funds available for you to invest in.

Specify the percentage of contributions you want to invest in each fund in the Your

Investment Instructions section on the Application form.

10

threeStep

Answer the questions below to determine the type of investments that

best suit you.To Do!

Determine what type of investor you are

If you chosetwo or more

responses from...The best investment strategy for you is...

Look for thissymbol

throughoutthis Guide

Turnto

page...

Column A ...to select a Retirement Date Fund.

A Retirement Date Fund offers a well-balanced investmentportfolio inside a single fund. Each fund is identified by its year ofmaturity, and as the maturity date approaches the fund graduallyrebalances to become more conservative.

11

Column B ...to select an Asset Allocation Fund.

Asset Allocation Funds offer a well-balanced portfolio inside asingle fund, and a professional fund manager monitors andrebalances these portfolios for you. There is an Asset AllocationFund that is suitable for you – whether you’re a conservativeinvestor or an aggressive one.

12

Column C ...to build your own portfolio.

Choose from the individual funds available through your programto build your own portfolio.

12

1. How interested are you in selectinginvestment funds for your retirementsavings?

2. How likely are you to monitor andrebalance your investments on anannual basis?

3. How would you rate your investmentknowledge?

I have someinterest.

I review myinvestmentsannually.

I understandthe basics ofinvesting.

I am very interested.

I check myinvestments on aregular basis (atleast quarterly).

I am confident in my investmentknowledge.

I am not interested.

I don’t want to review myinvestments.

I have little to no knowledgeabout investing.

A B C

11

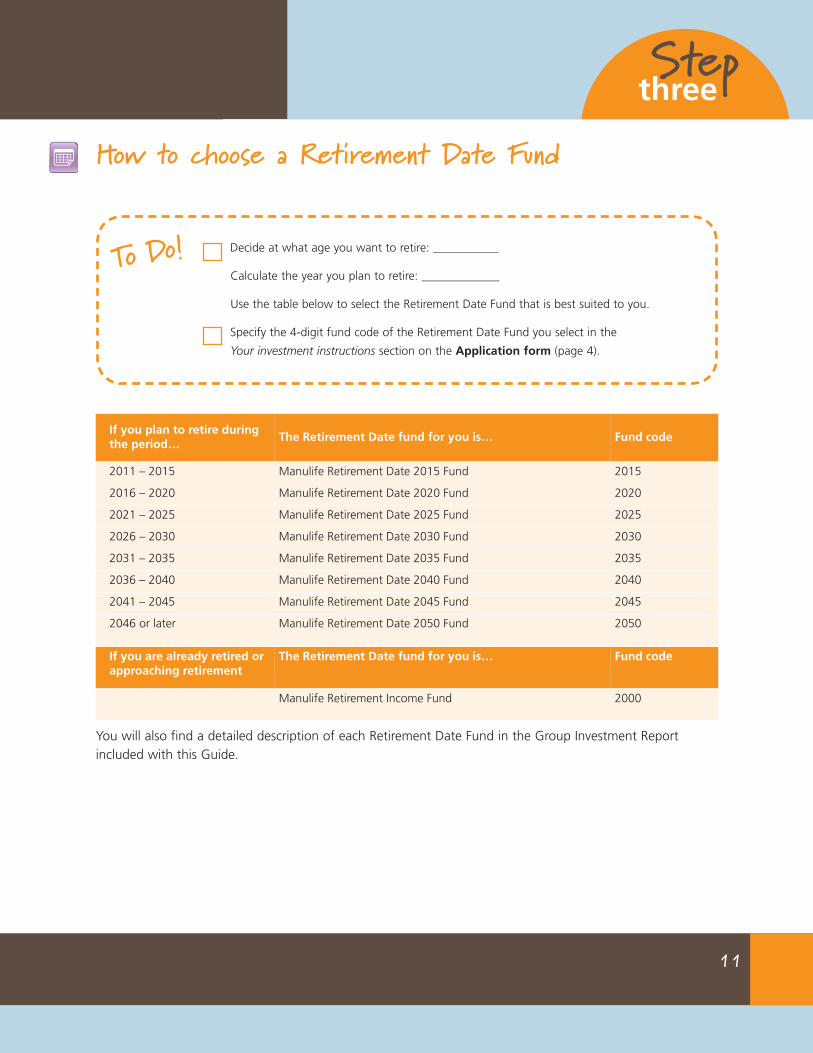

Stepthree

If you plan to retire duringthe period…

The Retirement Date fund for you is… Fund code

2011 – 2015 Manulife Retirement Date 2015 Fund 2015

2016 – 2020 Manulife Retirement Date 2020 Fund 2020

2021 – 2025 Manulife Retirement Date 2025 Fund 2025

2026 – 2030 Manulife Retirement Date 2030 Fund 2030

2031 – 2035 Manulife Retirement Date 2035 Fund 2035

2036 – 2040 Manulife Retirement Date 2040 Fund 2040

2041 – 2045 Manulife Retirement Date 2045 Fund 2045

2046 or later Manulife Retirement Date 2050 Fund 2050

If you are already retired orapproaching retirement

The Retirement Date fund for you is… Fund code

Manulife Retirement Income Fund 2000

You will also find a detailed description of each Retirement Date Fund in the Group Investment Reportincluded with this Guide.

How to choose a Retirement Date Fund

Decide at what age you want to retire: ___________

Calculate the year you plan to retire: _____________

Use the table below to select the Retirement Date Fund that is best suited to you.

Specify the 4-digit fund code of the Retirement Date Fund you select in the

Your investment instructions section on the Application form (page 4).

To Do!

12

threeStep

If you are choosing...

...an Asset Allocation Fund

Complete the Investor Style questionnaire starting on page 13.

Refer to page 16 for help selecting the Asset Allocation Fund that is

right for you.

Specify the 4-digit fund code of the Asset Allocation Fund you select

in the Your investment instructions section on the Application form (page 4).

...to build your own portfolio

Complete the Investor Style questionnaire starting on page 13.

Refer to page 17 for help selecting the investments that are right for you.

Specify the percentage of contributions you want to invest in each fund in the Your

investment instructions section on the Application form.

To Do!

13

Stepthree

Your age, the number of years remaining until you retire, and how you feel about risk will determine your investor style.

Once you know your investor style, you can choose funds for your retirement savings.

Your score

1. What is your investment horizon – when will you need this money?

a. Within 3 years (0)

b. 3-5 years (3)

c. 6-10 years (5)

d. 11-15 years (8)

3. 15 + years (10)

2. What is your most important investment goal?

a. To preserve your money (0)

b. To see modest growth in your account (4)

c. To see more significant growth in your account (7)

d. To earn the highest return possible (10)

3. Please indicate which statement reflects your overall view of managing risk:

a. I don’t like risk and I am not prepared to expose my investments to any market fluctuations in orderto earn higher long-term returns. (0)

b. I am prepared to experience modest short-term market fluctuations in order to generate growth ofcapital. (2)

c. I am prepared to experience average short-term market fluctuations in order to achieve a higherlong-term return. (4)

d. I want to maximize my long-term returns and am comfortable with significant short-term marketfluctuations. (6)

Circle one answer for each question.

Write your score – indicated in brackets at the end of each answer – in the box to the

right of each question.

Tally the scores you record for each question to get your total.

To Do!

Determine your investor style

14

threeStep

4. If you owned an investment that declined by 20% over a short period, what

would you do?

a. Sell all of the remaining investment (0)

b. Sell a portion of the remaining investment (2)

c. Hold the investment and sell nothing (4)

d. Buy more of the investment (6)

5. If you could increase your chances of improving your investment returns by

taking more risk, would you:

a. Be unlikely to take more risk (0)

b. Be willing to take a little more risk with some of your portfolio (2)

c. Be willing to take a lot more risk with some of your portfolio (4)

d. Be willing to take a lot more risk with your entire portfolio (6)

6. The following picture shows three

model portfolios and the highest and

lowest returns each is likely to earn in

any given year. Which portfolio would

you be most likely to hold?

a. Portfolio A (0)

b. Portfolio B (3)

c. Portfolio C (6)

7. After several years of following your retirement plan, you review your progress

and determine you are behind schedule and will need to modify your strategy in

order to retire at your preferred age. What would you do?

a. Keep the same investments you currently hold, but increase your contributions

as much as possible. (0)

b. Slightly increase your exposure to riskier investments and slightly increase your contributions. (3)

c. Move your entire portfolio to riskier investments, hoping to achieve the highest long-term return. (6)

-15

-10

-5

0

5

10

15

20

25

Portfolio A

Ret

urn

(%

)

Portfolio B Portfolio C

-1

-6

-12

8

15

22

15

Stepthree

8. Which statement best applies to your approach regarding achieving your retirementincome goals on time?

a. I must achieve my financial goal by my target retirement date. (0)

b. I would like to come close to achieving my financial goal by my target retirement date. (2)

c. If I have not reached my financial goal by my target retirement date, I have the flexibility to delay my

target retirement date. (4)

d. I re-evaluate my financial goals and target retirement date regularly and have the flexibility to adjust

them to align with the performance of my investments. (6)

If your score isbetween…

Your investor style is… About your investor style

0 – 7 Conservative Protecting your money is your chief concern. You may be approachingretirement, or simply prefer to take a cautious approach to investing andpreserve your money.

8 – 22 Moderate You want your money to grow, but are more concerned about protectingit. Retirement may be in your near future or you may prefer to becautious with your investments and preserve your money.

23 – 37 Balanced You want a balance between growth and security although you willaccept some risk to have the potential for higher returns over time.

38 – 48 Growth You want to increase your money and are somewhat comfortable ridingthe ups and downs of the market in exchange for the possibility ofhigher returns over the long term. You may have time on your side untilyou retire.

49 – 56 Aggressive You want to maximize the long-term growth of your retirement savings.You understand the ups and downs of the markets and are comfortabletaking more risk to maximize potential returns. You have plenty of timeto wait out market cycles until you retire.

Your total score:

Match your score to an investor style below.

My investor style is: __________________________

16

threeStep

Your investor style (from page 15): ____________________________________

Choose the Asset Allocation (AA) Fund that matches your investor style.

How to choose an Asset Allocation Fund

Note – Although these funds are rebalanced periodically to ensure they meet the objectives for each investor style, we

recommend you complete the Investor Style Questionnaire at least annually to ensure your style has not changed.

If your investor style is... The Asset Allocation fund for you is… Fund code

Conservative Manulife Conservative Asset Allocation Fund 2001

Moderate Manulife Moderate Asset Allocation Fund 2002

Balanced Manulife Balanced Asset Allocation Fund 2003

Growth Manulife Growth Asset Allocation Fund 2004

Aggressive Manulife Aggressive Asset Allocation Fund 2005

Specify the 4-digit fund code of the Asset Allocation Fund you select in the

Your investment instructions section on the Application form (page 4).To Do!

17

Stepthree

Your investor style (from page 15): ____________________________________

Find the sample portfolio that matches your investor style.

You can use the sample portfolios as a guideline to help you choose individual funds. To ensure you create a well-

diversified portfolio, select at least one fund from each asset class.

Each asset class in the sample portfolio is represented by a different colour. When choosing funds, look for pages

printed in the same colour in the Group Investment Report included with this Guide.

How to build your own portfolio

Conservative

If your investor style is...

Canadian Money Market and GIAs – 12%

Fixed Income – 68%

Canadian Large Cap Equity – 10%

U.S. Equity – 5%

International Equity and Global Equity– 5%

F –

–

–

–

Moderate

Choose the funds you want to use to build your own portfolio..

Specify the percentage of contributions you want to invest in each fund in the Your

investment instructions section on the Application form (page 4).

To Do!

Fixed Income – 53%

Canadian SmallCap Equity – 5%

Canadian Large Cap Equity – 20%

–

U.S. Equity – 7%

U

Canadian Money Market and GIAs – 7%

International Equity and Global Equity– 8%

M

–

–

A recommended asset mix for you is...

18

threeStep

Balanced

If your investor style is... A recommended asset mix for you is...

–

–

Fixed Income – 35%

F –

–

Canadian SmallCap Equity – 6%

Canadian Large Cap Equity – 30%

U.S. Equity – 11%

International Equity and Global Equity– 13%

U

Canadian Money Market and GIAs – 5%

Growth

Fixed Income – 20%

–

Canadian Large Cap Equity – 39%

–

Canadian SmallCap Equity – 9%

U.S. Equity – 15%

International Equity and Global Equity– 17%

C

–

Aggressive

–

Canadian Large Cap Equity – 44%

Canadian SmallCap Equity – 16%

–

U.S. Equity – 19%

International Equity and Global Equity– 21%

U

–

–

Actions canadiennes à faible et moyenne capitalisation – 9 %

Actions canadiennes à faible et moyenne capitalisation – 6 %

Actions canadiennes à forte capitalisation – 30 %

Actions américaines – 7 %

Actions américaines – 11 %

Actions internationales et mondiales – 13 %

Actions américaines – 19 %

Actions internationales et mondiales – 21 %

Actions américaines – 15 %

Actions internationales et mondiales – 17 %

Marché monétaire et comptes à intérêt garanti – 7 %

Marché monétaire et comptes à intérêt garanti – 5 %

Actions internationales et mondiales – 8 %

19

Stepthree

Notes:

• Balanced funds are not included in the sample portfolios. These funds are already well-diversified and generally invest

40% in fixed income investments and 60% in equity investments. Keep this in mind when you are using the

guidelines shown.

• You should consider how your savings outside of this plan are invested. Your other investments may already fulfill

some parts of the sample portfolios in the above table. The guidelines provided are only suggestions.

• You can change your investment options or complete an inter-fund transfer at any time by:

• Accessing the secure Member Internet site @ www.manulife.ca/GRO,

• Dialing the Interactive Voice Response (IVR) @ 1-888-727-7766, 24 hours a day, seven days a week, or

• Contacting a Client Service Representatives available at the same number from 8AM to 8PM ET, Monday to Friday

or by email at [email protected].

Where to find detailed fund information

You will find a summary of the funds available through your group program in the Group Investment Report included

with this Guide.

Stepfour

Consider transferring RRSP assets you alreadyhave to this Group RRSP

Here are a couple of important reasons why you may want to transfer existing RRSP assets you may already have to this

Group RRSP:

Low Fees

When fees are low, savings grow faster. The investment management fees (IMFs) in the Group RRSP are typically lower

than the Management Expense Ratio (MER) fees in RRSPs charged by individual mutual funds or at a bank.

Member Reward Program

Once your Group RRSP account is valued at over $25,000, you can take advantage of our Member Reward Program.

This lets you enjoy even lower investment management fees (IMFs), and higher guaranteed interest account

(GIA) rates.

If you transfer funds from your RRSPs at other institutions to this Group RRSP, you will be able to take advantage of the

Member Reward Program even faster!

If you have existing RRSP assets you would like to transfer, please complete the transfer form on the next page. If you

need assistance, please call a Financial Education Specialist from Manulife at 1-888-727-7766.

Decide if you would like to transfer assets into this Group RRSP.

Locate your RRSP account number(s). Contact the financial institution where your

RRSP is if you do not know the account number (you will need this number to complete

the transfer).

Complete the transfer form on the next page. Contact Manulife Financial at

1-888-727-7766 for help and additional transfer forms if necessary

To Do!

20

21

Transfer Authorization for Registered Investments(RSP, TFSA, LIRA, LRSP, RPP)

Manulife (The institution receiving your funds)

Your personal information

Your direction to relinquishing institution

Please print clearly in the blank boxes.

If your plan offers Group IncomePlusnote this option is intended toprovide you with guaranteedretirement income. Before you selectGroup IncomePlus, review The BoldPrint for more information.

If you transfer funds to your existingGroup IncomePlus, please rememberthat a contribution exceeding 20% ofyour Guaranteed Benefit Base willreset your Minimum Five (5) YearHolding period whether you makeone large contribution or a series ofsmaller transfers and contributionsover a 365 day period.

The Manufacturers Life Insurance Company Retain a copy for your files.Page 1 of 2

GP0807E Wat (07/2010)

• Complete Sections below and forward to the institution that will transferyour funds to Manulife.

• Completing this transfer will NOT result in reporting of income orissuance of a tax receipt as your savings remain in registered funds.

Last name First name Middle Initial

Mailing address (number, street & apartment number) City Province Postal Code

S.I.N. Telephone number* Ext.* Email address (if applicable)*

Relinquishing institution name

Address City Province Postal Code

Account/policy number Group plan number Member certificate number OR

FROM:

All in cash* Partial* - as listed below or on attached list

All Investment amount Symbol and/or certificate number or policy number Delay delivery until (dd/mmm/yyyy)

Dollars Investment description

All Investment amount Symbol and/or certificate number or policy number Delay delivery until (dd/mmm/yyyy)

Dollars Investment description

All Investment amount Symbol and/or certificate number or policy number Delay delivery until (dd/mmm/yyyy)

Dollars Investment description

Transfer:(check one box only)

* Please refer to statement inbold in Client authorization section below

Receiving institution

Group policy number Member number Customer number

Manulife Financial, Group Retirement Solutions, KC6PO BOX 396 STN WATERLOO, WATERLOO ON N2J 4A9

Fund code Fund name $ %

Investment instruction for this deposit. Fund code names and details appear online at www.manulife.ca/GRO or inthe Group Investment Report.

Do not use this form for transfers due to death or marriage breakdown.

This form is also available online at www.manulife.ca/GRO

*These fields are optional

100%

Must equal 100%

22

Your authorizationI hereby request the transfer of my account and its investments as described above.

* I have requested a transfer in cash, I authorize the liquidation of all or part of my investments and agree to pay anyapplicable fees, charges or adjustments.

If I have selected Group IncomePlus, I acknowledge that I have read and understood The Bold Print and by signing below, I agree tothe terms, conditions and fees applicable to that option

The Manufacturers Life Insurance Company Retain a copy for your files.Page 2 of 2

GP0807E Wat (07/2010)

For use by relinquishing institution only

Signature of Account Holder Date (dd/mmm/yyyy)

Signature of irrevocable beneficiary (if applicable) Date (dd/mmm/yyyy)

Irrevocable Beneficiary: I consent to the transfer of the account.

Account type: RSP TFSA LIRA LRSP RPP

Spousal Plan? No Yes - if "Yes," Contributor's information:

Last name First name Initial S.I.N

Contact name Title Telephone number Fax number

Authorized signature Date (dd/mmm/yyyy)

Locked-In funds Governing legislationYes, confirmation attached No

Stepfive

23

➥

Make sure you’ve completed the Application form.

Have you:

Completed the Your personal information section?

Named your beneficiary (or beneficiaries)?

Selected your funds?

Signed and dated the form?

To Do!

Check to see you’ve completed each step

Refer to the checklist below.

Return the completed form(s) included with this Guide to Manulife Financial using the

instructions on the forms.

You’ve successfully enrolled

What’s next?

You’ll receive a letter from Manulife welcoming you to the Group RRSP. This letter will provide your Customer number

and explain how you can get your Personal Identification Number (PIN). With your Customer number and PIN, you can

access the online tools Manulife offers to help you track and manage your savings.

How can I track the progress of my account?

• Member statements – You’ll receive an annual member statement updating you about your account activity

and growth.

• Internet – You can access your account information 24 hours a day, 7 days a week at www.manulife.ca/GRO.

• Phone – You can call 1-888-727-7766 to speak with a Customer Service Representative from Manulife.

Representatives are available Monday to Friday from 8 a.m. to 8 p.m. ET.

• Take the time to review Your Member Booklet starting on the next page

24

25

Any tax-deferred group savings plan that lets you choose between two or more investment options is known as a

Capital Accumulation Plan (CAP).

As a CAP member, you have these responsibilities:

• Deciding how much to contribute.

• Making use of the tools and information available to you through your program.

• Selecting your investments.

• Reviewing your investments regularly to ensure they continue to meet your retirement savings

and investment goals.

You should also consider obtaining investment advice from an appropriately qualified independent advisor.

Manulife’s Customer Service Representatives and Financial Education Specialists are available at 1-888-727-7766 to help

you understand the many planning tools and services you can use.

Customer Service Representatives are available Monday to Friday, from 8 a.m. to 8 p.m. ET. Financial Education

Specialists are available Monday to Friday, from 9 a.m. to 5 p.m. ET.

Your Member Booklet

Your plan sponsor (employer) has established this Group RRSP with Manulife Financial toassist you in saving money for retirement.

What are my responsibilities as a plan member?

26

How your Group RRSP works:

• This is a registered retirement savings plan (RRSP), sponsored by your plan sponsor, for the purpose of assisting

you in saving money for your retirement.

• An account is set up in your name at Manulife Financial.

• All contributions made by you and your plan sponsor are tax deductible and any investment earnings grow

tax-deferred.

• You choose how contributions are invested from the choices available under the plan.

• The amount available for your retirement depends on the total contributions made and the investment returns

they earn.

• You will receive an annual statement and access to information and tools to help you manage your account.

• Your plan has been established based on certain participation assumptions provided to Manulife Financial by your

plan sponsor. If these assumptions are not met, the plan may be terminated and your assets will be transferred to

another group RRSP sponsored by Manulife.

Your personal information:

Your plan sponsor and Manulife Financial require personal information to administer your account. The plan advisor as

designated by your plan sponsor will have access to your personal information to assist you in managing your account.

By enrolling in this Group RRSP, you will have authorized access to this information. Details are available on the back of

your application and in the Manulife Financial privacy policy.

27

When can I join?

Your plan sponsor will tell you when you are eligible to join.

Enrolment

To become a member, you must enroll.

If you choose to contribute on behalf of your spouse or common-law partner, your spouse or common-law partner must

also complete and sign an enrolment form indicating you as the contributor.

Once Manulife Financial receives your completed and signed application, contributions can begin.

Default investment option

If you do not select an investment option, all your contributions will be directed to a Retirement Date Fund. If Manulife

does not have your date of birth, and you have not selected an investment option, all contributions will be deposited to

the Moderate Asset Allocation Fund.

You can change your investment options or complete an inter-fund transfer at any time. A fee may apply to complete an

inter-fund transfer, refer to the “What fees may apply to me?” section.

How much will be contributed to my account?

Member Required Contributions

Your plan sponsor will tell you if you have to contribute, and if so, how much.

Plan Sponsor Contributions

Your plan sponsor will tell you if they are contributing on your behalf, and if so, how much.

Member Voluntary Contributions

You may always make voluntary contributions.

28

Spousal Contributions

You can make contributions on behalf of your spouse or common-law partner. These contributions are included in your

maximum contribution limit the same as contributions made to your own RRSP. You receive the tax deduction for the

contributions made to a spousal RRSP, but the assets belong to your spouse or common-law partner. Only they can make

decisions including withdrawals, investments and designating of a beneficiary.

Earnings

If contributions are based on earnings, your plan sponsor can tell you the definition of earnings your contributions

are based.

Contribution Limits and Tax

Contributions made to this Group RRSP or any other registered plan by you or on your behalf may not exceed the overall

tax assisted retirement savings maximum allowed under the Income Tax Act (Canada). In general, this amount will be a

maximum of 18% of your employment income for the year, subject to a maximum dollar limit.

You will receive a “Notice of Assessment” from Canada Revenue Agency (CRA) following the filing of your income tax

return. This Notice of Assessment will notify you of your RRSP maximum contribution limit for the current year.

If you do not contribute the maximum limit allowable in a given year you may “carry forward” the unused limit amount.

This means that you can increase your allowable contribution for the next year or future years. You can also carry

forward the deduction to a future year when your taxable income may be higher.

Over-contributions

It is your responsibility to ensure you do not make contributions in excess of the maximum amounts.

If you do over-contribute, Canada Revenue Agency (CRA) will charge a penalty tax on the amount contributed in excess

of your maximum RRSP contribution room for the year.

If you do over-contribute unintentionally, it is wise to remove the over-contribution. Failure to remove over-contributions

will result in you paying tax on those amounts when paid out as a benefit, without having received a deduction for them

when contributed. In effect, double taxation. Also, contributions that exceed your RRSP contribution room are not tax

deductible in the year in which they are made. You can call Manulife Financial at 1-888-727-7766 for the appropriate

method of retrieving any over-contributions made to the plan.

29

Can I make withdrawals from my account while I am employed?

If permitted, you may withdraw any contributions at any time provided they are not transferred in amounts from a

registered plan that is subject to locking-in provisions. The amount withdrawn may be taken in cash, transferred to

another registered plan or used to participate in the Home Buyers’ or Lifelong Learning Plan(s).

Amounts taken in cash are subject to immediate tax withholding. The amount of tax withheld will depend on the

amount being withdrawn. Since cash withdrawal amounts will be included in your taxable income, you may end up

paying additional tax. Keep in mind any cash withdrawals will reduce your potential retirement savings.

Fees in relation to withdrawals are indicated under the “What fees apply to me?” section.

Your plan sponsor can tell you if you are permitted to make withdrawals while employed. The withdrawal of voluntary

contributions is always permitted.

What happens if I terminate employment prior to my normalretirement date?

The value of your account will be transferred to the Manulife Financial Personal Plan RRSP when you terminate

employment. You will receive confirmation of this transfer.

Under the Manulife Financial Personal Plan RRSP you will have the right to select any one of the following options at any time:

1. Remain in the Manulife Financial Personal Plan RRSP (registered retirement savings plan), and enjoy the same services

you are already using,

2. Transfer your assets to another registered plan at a financial institution of your choice, or

3. Receive a lump sum cash payment subject to withholding tax.

Written confirmation from you will be required to select options 2 or 3 above.

Any amounts transferred in originating from a registered plan that is subject to locking-in provisions cannot be taken in cash.

What happens when I retire?

You may choose to start your retirement income at any time prior to the end of the calendar year in which you reach

age 71 (or such other age required by the Income Tax Act (Canada)) for any amounts in your account not subject to any

locking-in provisions. Your employment with your plan sponsor must cease prior to electing early retirement.

30

What are my retirement income choices?

The value of your account will be transferred to the Manulife Financial Personal Plan RRSP when you retire. You will

receive confirmation of this transfer.

Under the Manulife Financial Personal Plan RRSP you will have the right to select any one of the following options at any time:

1. Remain in the Manulife Financial Personal Plan RRSP, and enjoy the same services you are already using,

2. Transfer your assets to a Registered Retirement Income Fund at Manulife Financial,

3. Transfer your assets to a Group Registered Income Plan at Manulife Financial,

4. Transfer your assets to another registered plan at a financial institution of your choice,

5. Receive a lump sum cash payment subject to withholding tax, or

6. Purchase an annuity.

Written confirmation from you will be required for options 2 through 6 above.

Any amounts transferred in originating from a registered plan that is subject to locking-in provisions cannot be taken in cash.

What happens if I die before I terminate employment or retire?

If you die before you terminate employment or retire, Manulife Financial will pay a death benefit to your designated

beneficiary. More information regarding the amounts and options available will be provided to your beneficiary upon request.

If your spouse is your designated beneficiary, your spouse can choose one of the following options:

1. Transfer your assets to another registered plan at a financial institution of their choice, or

2. Receive a lump sum cash payment subject to withholding tax.

Any amounts transferred in originating from a registered plan that is subject to locking-in provisions will be subject to

applicable legislation and may have different rules.

Any benefit paid to any other beneficiary or estate must be paid as a lump sum cash payment, less income tax withholding.

Who is your beneficiary?

You may name a beneficiary to receive any death benefit payable from this Group RRSP. Your beneficiary may be

changed at any time, subject to any legal restrictions. If you do not name a beneficiary, any death benefit would be

payable to your estate.

31

What about RRSP receipts for income tax purposes?

Manulife Financial will issue RRSP tax receipts twice a year. The first receipt will be issued in January covering

contributions received by Manulife Financial’s head office between March and December of the preceding calendar year.

The second receipt will be issued in March covering the contributions received at Manulife Financial’s head office in the

first 60 days of the current calendar year (January – February).

You may choose to claim all or a portion of the amount reported on the second receipt as a deduction from your taxable

income for the previous calendar year or for the year in which the contributions were made.

Manulife Financial will mail receipts directly to your mailing address.

What fees may apply to me?

• Replacement Tax Forms/Receipts – A charge of $10 per request will apply to paper receipts. This fee will be

deducted from your account. You may go on-line to request a replacement tax form/receipt free of charge.

• Inter-Fund Transfer Fee (see the “How can I get help selecting investment options?” section above) – There

is no fee for your first four requests in any calendar year if your request is made in writing. A fifth written request will

incur a $25 fee and will be deducted from your account. An additional fee will apply for each successive request in a

calendar year. Inter-fund transfer requests made on-line or by calling 1-888-747-7766 are free.

• Interim Financial Statement Fee – A charge of $5 per requested interim financial statement will apply for each

request and will be deducted from your account.

• In Service Withdrawal Fee (where permitted – see the “Can I make withdrawals from my account while I

am employed” on page 29) – Each calendar year your first in service withdrawal is free. Any subsequent in service

withdrawals will incur a charge of $25 per request. This fee will be deducted from your withdrawal amount. In

service withdrawal includes cash withdrawal or transfer to another carrier.

• Investment Management Fees (IMFs) – You pay the IMFs that apply to Market Based Funds available under this

Group RRSP. You may contact your plan sponsor or go on-line to request this information.

32

Questions?

Under the Income Tax Act (Canada), who qualifies as a spouse or common-law partner?

A spouse means a person of the opposite or same sex who is married. A common-law partner means a person who lives

and has a conjugal relationship with a person of the opposite or same sex to whom any of the following applies.

He or she:

• is the natural or adoptive parent (legal or in fact) of that person's child,

• has been living with that person for at least 12 continuous months, or

• lived with that person previously for at least 12 continuous months and is living with the person again.

The above includes any period that they were separated for less than ninety (90) days because of a breakdown in

their relationship;

Note: a different definition of spouse will apply for any transfers in from products other than an RRSP that may or may

not be subject to locking-in provisions in accordance to any provincial legislation.

What happens to my benefits if my marriage ends?

The value of your account accumulated during the period of your marriage may be split between you and your spouse

or common-law partner as part of the division of assets. You should consult a lawyer about the laws governing this

situation and the options available to you and your former spouse.

What happens if I’m taking a leave from work?

Talk to your plan sponsor, who can explain the different rules that may apply to different types of leaves.

33

Your Notes:

34

Your Notes:

You need your Customer number (found onpage 1 of your statement) and PersonalIdentification Number (PIN) to access youraccount online. Call the number on the frontof this card if you need a PIN.

You can reach Customer ServiceRepresentatives and Financial EducationSpecialists using this number

My Customer number is:_________________

Group Retirement Solutions' products and services are offered throughManulife Financial (The Manufacturers Life Insurance Company).

Manulife, Manulife Financial, Manulife Financial For Your Future logo and the block designare service marks and trademarks of The Manufacturers Life Insurance Company and areused by it and its affiliates under license.

Questions?Contact Manulife

( Call 1-888-727-7766 to speak with a Customer Service Representative, Monday to Friday from 8 a.m. to 8 p.m. ET.

If you have questions about your investment choices, you can contact a Manulife Financial EducationSpecialist by calling 1-888-727-7766 from Monday to Friday between 9 a.m. and 5 p.m. ET. Be sure toselect option 4 then option 1 after you choose your language preference.

@ Via e-mail at [email protected]

8 Visit us at www.manulife.ca/GRO

You can also reach us via TTY service at 1-866-391-7788.

Contact Manulife

( Call 1-888-727-7766

@ Via e-mail at [email protected]

8 Visit us at www.manulife.ca/GRO

You can also reach us via TTY service at 1-866-391-7788.

0237

4b