Your First Year Service Plan

10

Technology, Media & Telecommunications Time to stand up and be counted. Services to an Emerging Technology Company

Transcript of Your First Year Service Plan

8/14/2019 Your First Year Service Plan

http://slidepdf.com/reader/full/your-first-year-service-plan 1/10

Technology, Media & Telecommunications

Time to stand upand be counted . Services to an Emerging Technology Company

8/14/2019 Your First Year Service Plan

http://slidepdf.com/reader/full/your-first-year-service-plan 2/10

© 2007 Deloitte & Touche LLP Services to an Emerging Technology Company i

Table of Contents

Introduction................................................................................................... 1

Fees ........................................................................................................ 1

Other Work .............................................................................................. 1

Contents of the Document.......................................................................... 1

Your First Year Service Plan ............................................................................. 2

Business Plan ...........................................................................................2

SR&ED Investment Tax Credits ................................................................... 2

Cash Flow Plan.......................................................................................... 3

Financial Statements and Disclosure............................................................ 3

Accounting Policies .................................................................................... 3

Financial Records ...................................................................................... 4

Financing ................................................................................................. 4

Review Corporate Structure........................................................................ 4

Quarterly Meetings....................................................................................4

ViaTech.................................................................................................... 4

Areas of Interest ............................................................................................ 5 Corporate Taxation: The Basics...................................................................5

Scientific Research and Experimental Development (SR&ED) Tax Incentive ...... 5

Stock Option Plans .................................................................................... 6

$750,000 Capital Gains Exemptions ............................................................ 7

About Deloitte ................................................................................................ 8

Deloitte – Burlington Region.......................................................................8

Deloitte Canada ........................................................................................ 8 Deloitte Touche Tohmatsu.......................................................................... 8

8/14/2019 Your First Year Service Plan

http://slidepdf.com/reader/full/your-first-year-service-plan 3/10

1

Introduction

The purpose of this document is to outline briefly our service plan to an emergingtechnology company. In this regard, we believe that our service plan approach canadd substantial value for you and your business.

You will see from our approach that we are committed to you, and your business,and are prepared to make an investment to see you succeed. In short, if yousucceed, we succeed.

FeesA common question or concern is how will I be charged for all of these serviceswhen I am dealing with a big firm.

As indicated, we are prepared to make aninvestment in your business. Our first year feequote covers all of the services outlined in oursection entitled “Your First Year Service Plan”.

At the end of the year we will show you the totalcosts incurred so that you can see the investmentthat we have made.

We should point out however, that if you do an IPOor sell the business, we would like to recover thisinvestment. This would be spelled out in detail inan engagement letter.

Other WorkThis document outlines in general terms the work that we will perform for our

“base” proposed fees. There may be other projects however that we would proposeand invoice separately.

Contents of the DocumentThe remainder of this document discusses the services that an emerging technologycompany would typically require in its first year of working with us, and providessome level of detail on certain areas that are typically of significant interest to suchcompanies. The topics are chosen based on our significant experience working withemerging technology companies in Waterloo region.

“We are prepared tomake an investment inyour business”

8/14/2019 Your First Year Service Plan

http://slidepdf.com/reader/full/your-first-year-service-plan 4/10

2

Your First Year Service Plan

Below is an outline of the services that we would normally provide within the firstyear of our relationship with a relatively new, emerging technology client. However,the actual services will of course depend on your unique business as well as yourneeds.

Business PlanThere are many reasons why a business plan is prepared. Some of these reasonsmay include:

• Putting your plan on paper helps to get you focused.

• The plan can help you share the vision for the business with other partnersor employees in the business.

• The plan can help to get employee buy-in and be a motivator if theyparticipate in the development of the plan.

• If any form of financing is required, a business plan is mandatory.

With respect to our role we will do the following:

1. If you do not have a business plan, we will give you some guidance as to the

construction of such a plan, as well as some initial input related to how youmay wish to develop your plan in light of our understanding of your business

and industry, or

2. If you have a draft business plan, we will review this plan and meet with youto provide our initial thoughts and comments.

If you then require other specific work to help you with your business plan, such asmarket validation studies or preparation of cash flows, we would discuss with youwhat our fee arrangement would be.

SR&ED Investment Tax CreditsIf you are developing, adapting, or otherwise improving technology, then you maybe eligible for scientific research and experimental development (SR&ED)investment tax credits. These credits, which may total up to 68% of your costs, areoften fully refundable, providing significant cash inflows.

If appropriate, we will discuss the SR&ED program with you in detail to ensure thatyou can take maximum advantage of the incentives that are available under the

program.Further to the above, after discussing what projects you may undertake, we canalso assist you in making contact with a number of other agencies, such as IRAP,,that can provide additional assistance, whether it be financial or otherwise, withrespect to the development of your products. It is very common for research anddevelopment projects to be eligible for both IRAP and SR&ED funding, whichtogether may fund nearly 80% of eligible project costs!

8/14/2019 Your First Year Service Plan

http://slidepdf.com/reader/full/your-first-year-service-plan 5/10

3

Cash Flow PlanIn a start up, or growing technology business, cash is king. Therefore, we willreview with you a number of areas and strategies to either preserve or enhancecash flow. Some of these strategies include the following:

• Tax effective remuneration strategies.

• Expediting scientific research and experimental development investment taxcredit refunds.

• Assistance in identifying other funding sources.

• Expediting GST refunds.

• Effective loss utilization strategy.

Financial Statements and DisclosureThere are 3 levels of assurance that we can provide on a company’s financialstatements:

1. Notice to Reader – we provide no assurance that the financial statements

are correct but simply compile them from information provided bymanagement. A notice to the reader explaining this fact is included with thefinancial statements. These financial statements only include a basic levelof note disclosure.

2. Review Engagement Report – we provide negative assurance to the reader.That is, we indicate that in the course of our review we have not discoveredanything that makes us believe the financial statements are not materiallycorrect. These financial statements include full note disclosure.

3. Audit Report – we provide positive assurance to the reader that the financialstatements are materially correct. These financial statements include fullnote disclosure.

The appropriate level of financial statement assurance varies depending on thesituation. Obviously the more assurance provided, the greater the scope of work tobe performed. In many cases, Notice to Reader financial statements are sufficientand are prepared primarily for the purpose of tax filings. This typically changeswhen a company seeks third party investment. An angel investor or venturecapitalist will likely demand a Review Engagement or Audit Report as a condition of their financing.

One note of caution, if an Initial Public Offering is planned within 5 years, an AuditReport may be appropriate from the outset. In most cases, a 5 year history of audited financial statements is a mandatory requirement for an IPO.

Accounting PoliciesEven for emerging companies, proper selection and a thorough understanding of accounting policies is critical. Nothing will tarnish a company’s credibility fasterthan errors in published financial statements. Some of the recent accounting rulesunder Canadian and US Generally Accepted Accounting Policies are extremelycomplex, particularly around the issue of revenue recognition. We will typicallywork with a company to ensure they establish sound policies right from the outset.

Of course, if we provide a Review Engagement or Audit Report on the financialstatements, we conduct a detailed reviewed of the accounting policies used inpreparing the financial statements, and provide full disclosure of such policies in thenotes to the financial statements.

8/14/2019 Your First Year Service Plan

http://slidepdf.com/reader/full/your-first-year-service-plan 6/10

4

Financial RecordsAlthough mundane, it is critical that you set up an accounting system so that youcan obtain timely financial information with which to manage your business, and tobenchmark against your plan. In general, it is recommended that you do thebookkeeping and accounting work in-house, as it allows you to better manage andcontrol your business. If you have a system, we will provide our comments.

In some cases, you may simply not have the resources to do the bookkeeping work,or set up a system. In that case we can make an introduction to a local bookkeeperthat would be cost effective.

FinancingYour financing needs may be immediate or not for a year or two. Either way, wewill arrange a meeting with our corporate finance group to discuss your businessand your financing needs. Out of this meeting, you can expect the development of a plan of action that you would need to begin to follow in order to attract financing.

Note that if you wanted to then pursue this plan of action, we would discuss withyou at that time our fee arrangement to actively assist you in attracting financing.

Review Corporate StructureIn many cases, your focus is simply on the business. However, we will discuss withyou a number of options and alternatives related to the corporate structure toensure that it is the most advantageous structure for purposes of raising financingor going public, as well as to ensure that the initial shareholders’ estate and taxplanning opportunities are taken into account.

Quarterly MeetingsAlthough we are accessible at any time, we like toinitially diarize quarterly meetings to ensure thatwe get together to keep abreast as to the progressthat you are making in your business. In somecases, it may be most efficient to discuss businessover the telephone, however, we are certainlyavailable for a breakfast or lunch in order to getcaught up.

Again, although we try to formally set up thesemeeting times, we are always accessible if youhave an immediate need. If other thoughts oropportunities come to our mind, we would of coursecall.

ViaTechViaTech is a group of professionals that work with growing technology companies.The purpose of the group is to be a sounding board for you and to provide generalinput or to assist you with any specific issues or concerns that you may have. Thisservice is provided by the group free of charge.

As a member of this group, we would be pleased to coordinate a meeting. At thismeeting, it is typical that you would tell the group a bit about your background,where you are today and what your future plans are. At that point, you may eitherhave specific issues or questions that you would like to discuss or alternatively thegroup can simply probe further into your plans and provide insights as to areas toconsider.

“We get together to keepabreast as to theprogress that you aremaking in your business”

8/14/2019 Your First Year Service Plan

http://slidepdf.com/reader/full/your-first-year-service-plan 7/10

5

Areas of Interest

The purpose of this section is to simply give you an overview of a number of topicsof common interest to emerging technology companies.

Corporate Taxation: The BasicsThe following is a very brief overview of some of the taxation basics of a corporationthat is a Canadian Controlled Private Corporation.

• Losses can be carried back three years and forward twenty years.

• The first $400,000 (calendar 2007) of taxable income attracts tax atapproximately 19%.

• For taxable income in excess of $400,000, the tax rate is approximately36%. Income taxed at this rate is effectively “double taxed” whenwithdrawn from the corporation.

• Monthly income tax instalments are required. They are based on the lesserof last year’s actual tax, and your estimated tax for the current year.

• In general, your final tax payment is due 3 months after the fiscal year end.

Scientific Research and Experimental Development (SR&ED) TaxIncentiveCanada has one of the most generous tax incentive programs in the world foreligible SR&ED work.

The Benefits

For a qualifying Canadian Controlled Private Corporation, the benefits include thefollowing:

• Federal refundable credit of 35%

• Ontario refundable credit of 10%

• 100% write-off of certain capital expenditures

EligibilityIt is important to note that there is specific eligibility criteria that must be met inorder to obtain these tax incentives. If any of the following indicators are present,you may be doing qualifying SR&ED work.

• You are developing something faster, more efficient, stronger, etc.

• You have successfully applied under the IRAP program.

• You have a number of engineers or PhDs on staff.

• You have tried several different approaches to solve a technical problem.

How to ClaimThe submission for eligible SR&ED is made with your annual tax return. There areessentially two components. The first is the technical write-up for each project,which is generally no more than 3-4 pages per project.

8/14/2019 Your First Year Service Plan

http://slidepdf.com/reader/full/your-first-year-service-plan 8/10

6

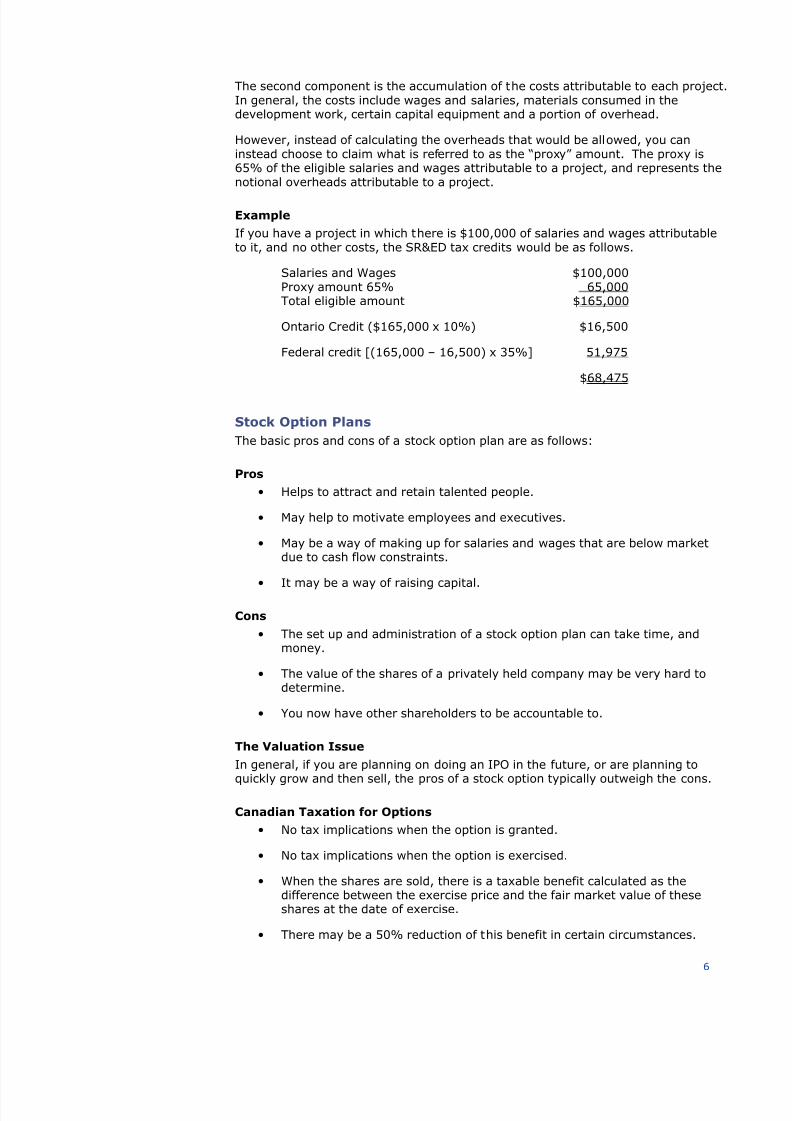

The second component is the accumulation of the costs attributable to each project.In general, the costs include wages and salaries, materials consumed in thedevelopment work, certain capital equipment and a portion of overhead.

However, instead of calculating the overheads that would be allowed, you caninstead choose to claim what is referred to as the “proxy” amount. The proxy is65% of the eligible salaries and wages attributable to a project, and represents thenotional overheads attributable to a project.

ExampleIf you have a project in which there is $100,000 of salaries and wages attributableto it, and no other costs, the SR&ED tax credits would be as follows.

Salaries and Wages $100,000Proxy amount 65% 65,000Total eligible amount $165,000

Ontario Credit ($165,000 x 10%) $16,500

Federal credit [(165,000 – 16,500) x 35%] 51,975

$68,475

Stock Option PlansThe basic pros and cons of a stock option plan are as follows:

Pros• Helps to attract and retain talented people.

• May help to motivate employees and executives.

• May be a way of making up for salaries and wages that are below marketdue to cash flow constraints.

• It may be a way of raising capital.

Cons• The set up and administration of a stock option plan can take time, and

money.

• The value of the shares of a privately held company may be very hard todetermine.

• You now have other shareholders to be accountable to.

The Valuation IssueIn general, if you are planning on doing an IPO in the future, or are planning toquickly grow and then sell, the pros of a stock option typically outweigh the cons.

Canadian Taxation for Options• No tax implications when the option is granted.

• No tax implications when the option is exercised.

• When the shares are sold, there is a taxable benefit calculated as thedifference between the exercise price and the fair market value of theseshares at the date of exercise.

• There may be a 50% reduction of this benefit in certain circumstances.

8/14/2019 Your First Year Service Plan

http://slidepdf.com/reader/full/your-first-year-service-plan 9/10

7

• When a share is sold, there may also be a capital gain calculated as thedifference between the selling price and the fair market value of the shareat the date the option was exercised.

• The company will not receive any deduction in respect of the options.

Alternatives

There are alternatives to a stock option plan that can be implemented that avoid theintroduction of new shareholders yet provide employees with similar incentives. Theviable options depend on the particular situation. We would discuss thesealternatives with you prior to establishing a stock option plan.

$750,000 Capital Gains ExemptionsEvery Canadian individual taxpayer has a $750,000 capital gains exemptionavailable. The exemption is only available to be used against gains realized oncertain qualifying property.

Shares of a qualifying small business corporation (QSBC) qualify for the $750,000capital gains exemption. In order to be a QSBC, the following, simplified criteriamust be met.

• The company must be a Canadian Controlled Private Corporation.

• You (or someone you are related to) must have owned the shares for 24months.

• During the last 24 months, at least 50% of the assets of the company musthave been used in an active business carried on in Canada.

• At the date that the gain on the shares is realized, at least 90% of the fairmarket value of the assets must be used in an active business carried on inCanada.

Tax Savings and Proliferation of Exemptions

Each $750,000 exemption can save you as much as $172,500 in income tax. Assuch, it is very important that you gain access to the exemption. In addition, withproper planning you can also access the exemptions of your spouse and children.

What to Watch ForIn terms of ensuring that you gain access to your $750,000 capital gains exemption,the following are a number of areas to watch out for.

• Ensuring that you meet the 50% and 90% rules where you have done afinancing and, therefore may have excess cash in the company.

• Again, ensuring that you meet the 50% and 90% rules where you have setup foreign subsidiaries or branches. Note that these foreign assets are notassets of a business carried on in Canada, and therefore not eligible assets

in determining the 50% and 90% thresholds.• The manner in which you incorporate your business can have an impact on

the 24 month holding period rules.

• How the business has been financed can have an impact on the availabilityof your exemption. In addition, your other personal investments may havean impact on the availability of the exemption.

8/14/2019 Your First Year Service Plan

http://slidepdf.com/reader/full/your-first-year-service-plan 10/10

8

About Deloitte

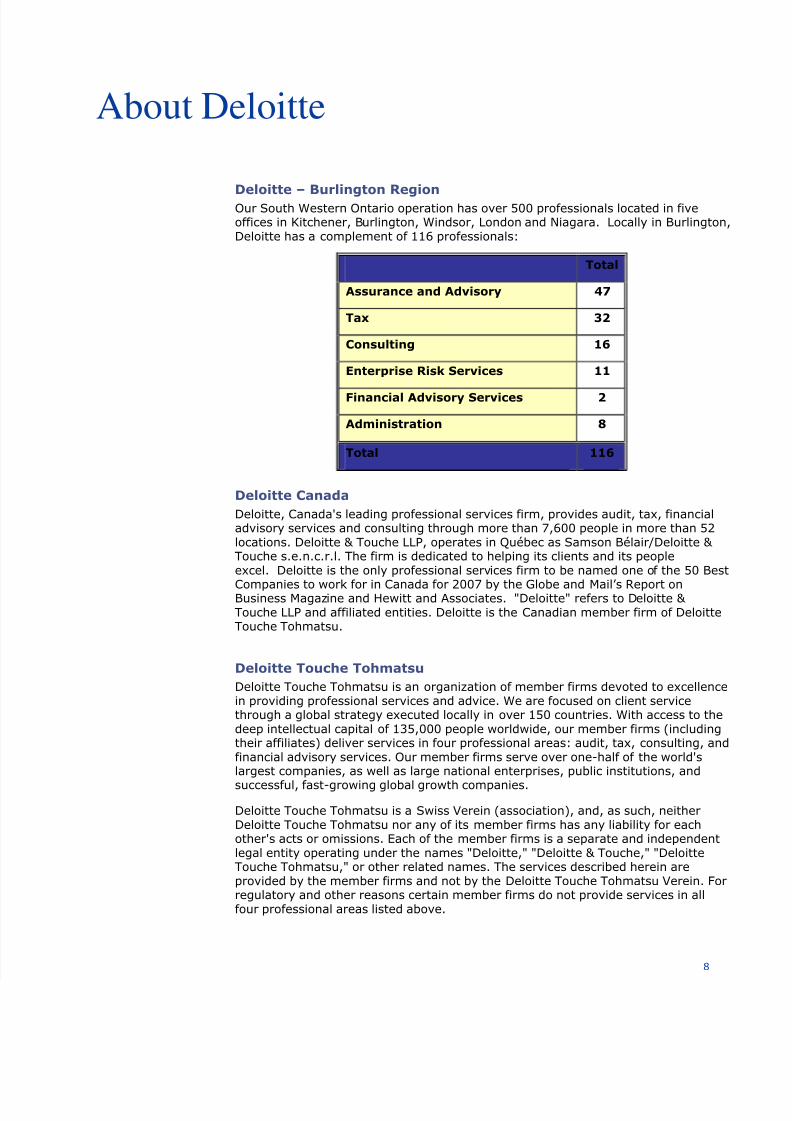

Deloitte – Burlington RegionOur South Western Ontario operation has over 500 professionals located in fiveoffices in Kitchener, Burlington, Windsor, London and Niagara. Locally in Burlington,Deloitte has a complement of 116 professionals:

Total

Assurance and Advisory 47

Tax 32

Consulting 16

Enterprise Risk Services 11

Financial Advisory Services 2

Administration 8

Total 116

Deloitte CanadaDeloitte, Canada's leading professional services firm, provides audit, tax, financialadvisory services and consulting through more than 7,600 people in more than 52locations. Deloitte & Touche LLP, operates in Québec as Samson Bélair/Deloitte & Touche s.e.n.c.r.l. The firm is dedicated to helping its clients and its peopleexcel. Deloitte is the only professional services firm to be named one of the 50 Best

Companies to work for in Canada for 2007 by the Globe and Mail’s Report onBusiness Magazine and Hewitt and Associates. "Deloitte" refers to Deloitte & Touche LLP and affiliated entities. Deloitte is the Canadian member firm of DeloitteTouche Tohmatsu.

Deloitte Touche TohmatsuDeloitte Touche Tohmatsu is an organization of member firms devoted to excellencein providing professional services and advice. We are focused on client servicethrough a global strategy executed locally in over 150 countries. With access to thedeep intellectual capital of 135,000 people worldwide, our member firms (includingtheir affiliates) deliver services in four professional areas: audit, tax, consulting, andfinancial advisory services. Our member firms serve over one-half of the world'slargest companies, as well as large national enterprises, public institutions, and

successful, fast-growing global growth companies.

Deloitte Touche Tohmatsu is a Swiss Verein (association), and, as such, neitherDeloitte Touche Tohmatsu nor any of its member firms has any liability for eachother's acts or omissions. Each of the member firms is a separate and independentlegal entity operating under the names "Deloitte," "Deloitte & Touche," "DeloitteTouche Tohmatsu," or other related names. The services described herein areprovided by the member firms and not by the Deloitte Touche Tohmatsu Verein. Forregulatory and other reasons certain member firms do not provide services in allfour professional areas listed above.