Your 2015 Guide to Benefits For Employees in Canada · Your 2015 Guide to Benefits ... ©2015 Xerox...

30

Your 2015 Guide to Benefits For Employees in Canada

Transcript of Your 2015 Guide to Benefits For Employees in Canada · Your 2015 Guide to Benefits ... ©2015 Xerox...

Your 2015 Guide to Benefits For Employees in Canada

©2015 Xerox Corporation and Buck Consultants, LLC. All rights reserved. Xerox® and Xerox and Design® are trademarks of Xerox Corporation in the United States and/or other countries. Buck Consultants® is a registered trademark of Buck Consultants, LLC in the United States and/or other countries. BRP2825

Not to be copied in whole or in part in any form, electronic or otherwise, or provided to any party other than as originally intended without express written permission from Buck Consultants Limited.

2015 Benefits for Employees in Canada i

Table of Contents

Introduction .................................................................................... 2

Canada’s Demographic .................................................................. 4

Retirement Benefits ........................................................................ 5 Social Security .................................................................................................... 5 Personal Savings ............................................................................................... 7 Private Pension Plan Practices ........................................................................... 9

Disability Benefits ......................................................................... 16 Social Security .................................................................................................. 16 Workers Compensation .................................................................................... 17 Private Employment Practices .......................................................................... 18

Death Benefits/Life Insurance Lizann ........................................... 20 Social Security .................................................................................................. 20 Private Employment Practices .......................................................................... 21

Medical/Dental Benefits ................................................................ 23 Social Security .................................................................................................. 23 Private Employment Practices .......................................................................... 24

Vacation and Wellness Programs ................................................. 26 Federal Statutory Holidays 2015 ...................................................................... 26

Contact Us ................................................................................... 28 About Buck Consultants at Xerox ..................................................................... 28

2015 Benefits for Employees in Canada 2

Introduction Canadians enjoy broad social benefits throughout the country, including comprehensive income maintenance benefits such as the Canada Pension Plan/Quebec Pension Plan (CPP/QPP), Old Age Security (OAS), and Employment Insurance (EI).

These programs are administered federally and require nationwide coordination, with the exception of the Quebec programs, the Quebec Pension Plan (QPP) and the Quebec Parental Insurance Plan (QPIP). In addition to the abovementioned programs, there are several income-tested programs provided by the federal government and various provinces.

Publicly-funded hospitalization and medical programs cover virtually all Canadians. Provincial and territorial governments are responsible for the administration of health services, and often exercise considerable influence over matters that have been delegated to them by provincial legislatures. Although patterns of health services in the provinces are similar to each other, their organization, system of financing, and administration vary from province to province. These programs are funded through a combination of federal transfers to the provinces, provincial taxes raised through a combination of sales and payroll taxes, and, in certain provinces, premiums or special taxes payable by the residents.

Most employers in Canada have established private employee benefit plans to supplement the government-sponsored hospital and medical plans. These plans include coverage for medically-required services such as drugs, private duty nursing, semi-private hospital, paramedical practitioners, vision care, and out-of-province/out-of-country care. Private employee benefit plans are not allowed to cover services that are covered through publicly-funded programs. The vast majority of Canadian employers also sponsor dental care plans for their employees.

In addition, most employers sponsor short-term and long-term disability plans to supplement the Canada Pension Plan/Quebec Pension Plan and Workers’ Compensation disability income benefit plans, as well as Employment Insurance sickness benefits. Most employers provide coverage for, or access to, a full range of death benefits, including basic life insurance, optional life insurance, and accidental death and dismemberment coverage, with similar options available for spouses and/or dependent children. Other benefits offered to employees through employer sponsorship include critical illness insurance, employee assistance programs, and group home and automobile insurance.

Interest in flexibility in benefits continues to grow in Canada. With the demographic changes facing Canadian employers as baby boomers age, and new generations enter the workforce, flexibility in plan design can address the different needs of these employees.

Employer-sponsored benefit programs usually terminate at the earlier of age 65 or retirement, although with the end of mandatory retirement at age 65, many benefits are being extended to active employees beyond age 65. While some employers offer a reduced amount of life insurance and/or extended health and dental coverage to retirees, many of those that do are looking for ways to eliminate or reduce retiree coverage wherever possible, due to the expenses associated with future liabilities.

Employers are not required to sponsor a pension plan, but when they do, they must follow the minimum regulatory standards. Legislation governing private pension plans was first enacted in certain provinces in the 1960s, and minimum standards were in place for most provinces by the mid-1970s. Initially, pension standards legislation tended to be reasonably uniform. Significant differences have since emerged as jurisdictions have enacted legislation to respond to local concerns.

2015 Benefits for Employees in Canada 3

Most employer-sponsored plans come under provincial laws based on each employee’s province of employment, although certain types of employment come under federal jurisdiction.

2015 Benefits for Employees in Canada 4

Canada’s Demographic

Population 35,540,419 (July 1, 2014, Statistics Canada) CAD 1.00 = (USD) 0.860 (January 1, 2015, Bank of Canada) GDP CDN (January 2015) 1,653 billion (Statistics Canada) 2014 Inflation 2.0% (Statistics Canada) Unemployment rate 6.7% (December 2014, Statistics Canada)

2015 Benefits for Employees in Canada 5

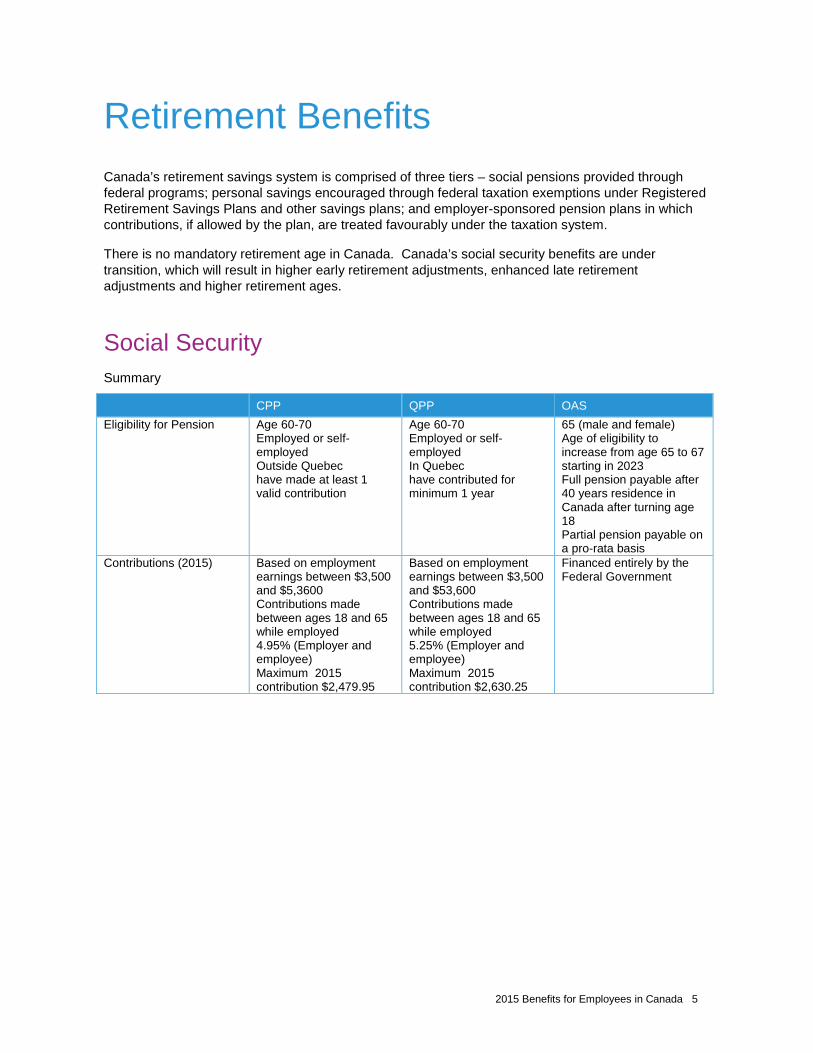

Retirement Benefits Canada’s retirement savings system is comprised of three tiers – social pensions provided through federal programs; personal savings encouraged through federal taxation exemptions under Registered Retirement Savings Plans and other savings plans; and employer-sponsored pension plans in which contributions, if allowed by the plan, are treated favourably under the taxation system.

There is no mandatory retirement age in Canada. Canada’s social security benefits are under transition, which will result in higher early retirement adjustments, enhanced late retirement adjustments and higher retirement ages.

Social Security Summary

CPP QPP OAS Eligibility for Pension

Age 60-70 Employed or self-employed Outside Quebec have made at least 1 valid contribution

Age 60-70 Employed or self-employed In Quebec have contributed for minimum 1 year

65 (male and female) Age of eligibility to increase from age 65 to 67 starting in 2023 Full pension payable after 40 years residence in Canada after turning age 18 Partial pension payable on a pro-rata basis

Contributions (2015)

Based on employment earnings between $3,500 and $5,3600 Contributions made between ages 18 and 65 while employed 4.95% (Employer and employee) Maximum 2015 contribution $2,479.95

Based on employment earnings between $3,500 and $53,600 Contributions made between ages 18 and 65 while employed 5.25% (Employer and employee) Maximum 2015 contribution $2,630.25

Financed entirely by the Federal Government

2015 Benefits for Employees in Canada 6

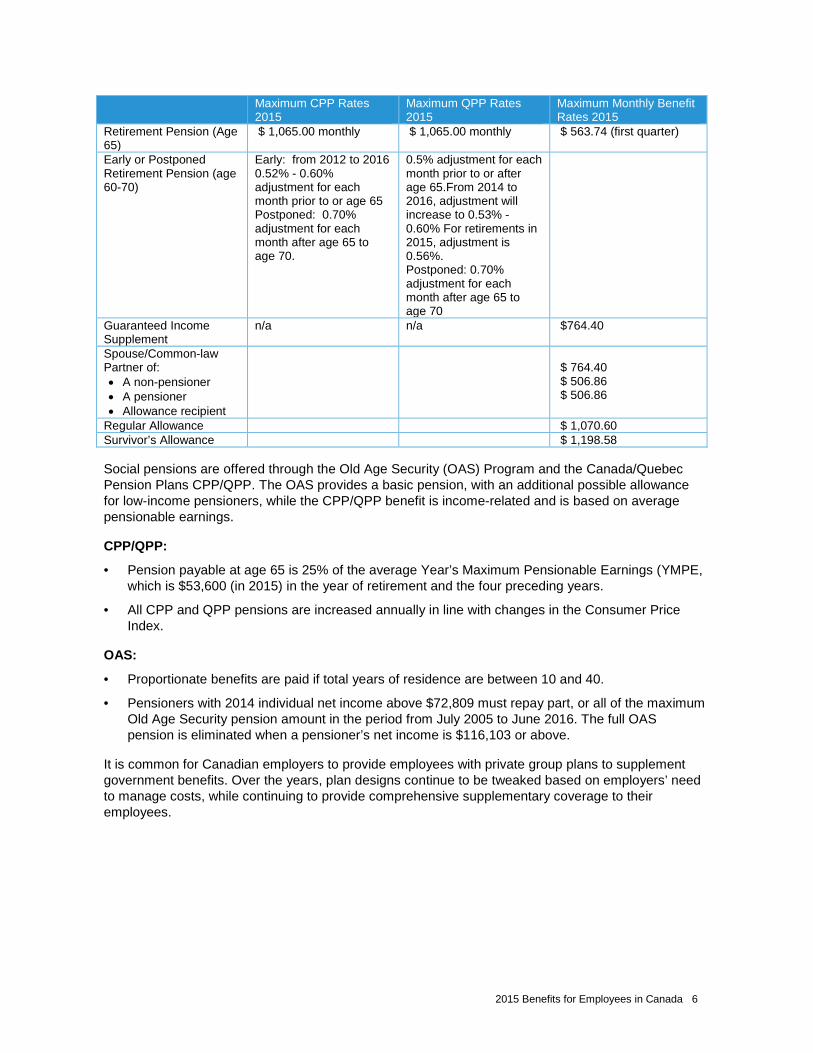

Maximum CPP Rates 2015

Maximum QPP Rates 2015

Maximum Monthly Benefit Rates 2015

Retirement Pension (Age 65)

$ 1,065.00 monthly $ 1,065.00 monthly $ 563.74 (first quarter)

Early or Postponed Retirement Pension (age 60-70)

Early: from 2012 to 2016 0.52% - 0.60% adjustment for each month prior to or age 65 Postponed: 0.70% adjustment for each month after age 65 to age 70.

0.5% adjustment for each month prior to or after age 65.From 2014 to 2016, adjustment will increase to 0.53% - 0.60% For retirements in 2015, adjustment is 0.56%. Postponed: 0.70% adjustment for each month after age 65 to age 70

Guaranteed Income Supplement

n/a n/a $764.40

Spouse/Common-law Partner of: • A non-pensioner • A pensioner • Allowance recipient

$ 764.40 $ 506.86 $ 506.86

Regular Allowance $ 1,070.60 Survivor’s Allowance $ 1,198.58

Social pensions are offered through the Old Age Security (OAS) Program and the Canada/Quebec Pension Plans CPP/QPP. The OAS provides a basic pension, with an additional possible allowance for low-income pensioners, while the CPP/QPP benefit is income-related and is based on average pensionable earnings.

CPP/QPP:

• Pension payable at age 65 is 25% of the average Year’s Maximum Pensionable Earnings (YMPE, which is $53,600 (in 2015) in the year of retirement and the four preceding years.

• All CPP and QPP pensions are increased annually in line with changes in the Consumer Price Index.

OAS:

• Proportionate benefits are paid if total years of residence are between 10 and 40.

• Pensioners with 2014 individual net income above $72,809 must repay part, or all of the maximum Old Age Security pension amount in the period from July 2005 to June 2016. The full OAS pension is eliminated when a pensioner’s net income is $116,103 or above.

It is common for Canadian employers to provide employees with private group plans to supplement government benefits. Over the years, plan designs continue to be tweaked based on employers’ need to manage costs, while continuing to provide comprehensive supplementary coverage to their employees.

2015 Benefits for Employees in Canada 7

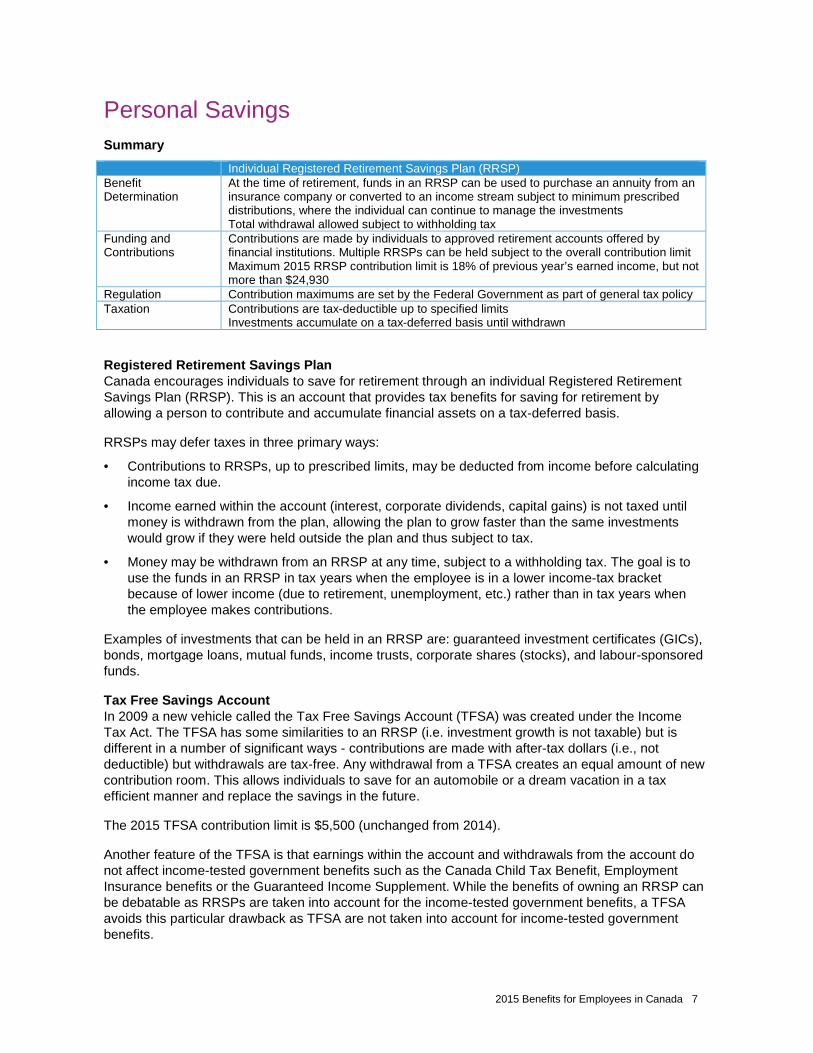

Personal Savings Summary

Individual Registered Retirement Savings Plan (RRSP) Benefit Determination

At the time of retirement, funds in an RRSP can be used to purchase an annuity from an insurance company or converted to an income stream subject to minimum prescribed distributions, where the individual can continue to manage the investments Total withdrawal allowed subject to withholding tax

Funding and Contributions

Contributions are made by individuals to approved retirement accounts offered by financial institutions. Multiple RRSPs can be held subject to the overall contribution limit Maximum 2015 RRSP contribution limit is 18% of previous year’s earned income, but not more than $24,930

Regulation Contribution maximums are set by the Federal Government as part of general tax policy Taxation Contributions are tax-deductible up to specified limits

Investments accumulate on a tax-deferred basis until withdrawn

Registered Retirement Savings Plan Canada encourages individuals to save for retirement through an individual Registered Retirement Savings Plan (RRSP). This is an account that provides tax benefits for saving for retirement by allowing a person to contribute and accumulate financial assets on a tax-deferred basis.

RRSPs may defer taxes in three primary ways:

• Contributions to RRSPs, up to prescribed limits, may be deducted from income before calculating income tax due.

• Income earned within the account (interest, corporate dividends, capital gains) is not taxed until money is withdrawn from the plan, allowing the plan to grow faster than the same investments would grow if they were held outside the plan and thus subject to tax.

• Money may be withdrawn from an RRSP at any time, subject to a withholding tax. The goal is to use the funds in an RRSP in tax years when the employee is in a lower income-tax bracket because of lower income (due to retirement, unemployment, etc.) rather than in tax years when the employee makes contributions.

Examples of investments that can be held in an RRSP are: guaranteed investment certificates (GICs), bonds, mortgage loans, mutual funds, income trusts, corporate shares (stocks), and labour-sponsored funds.

Tax Free Savings Account In 2009 a new vehicle called the Tax Free Savings Account (TFSA) was created under the Income Tax Act. The TFSA has some similarities to an RRSP (i.e. investment growth is not taxable) but is different in a number of significant ways - contributions are made with after-tax dollars (i.e., not deductible) but withdrawals are tax-free. Any withdrawal from a TFSA creates an equal amount of new contribution room. This allows individuals to save for an automobile or a dream vacation in a tax efficient manner and replace the savings in the future.

The 2015 TFSA contribution limit is $5,500 (unchanged from 2014).

Another feature of the TFSA is that earnings within the account and withdrawals from the account do not affect income-tested government benefits such as the Canada Child Tax Benefit, Employment Insurance benefits or the Guaranteed Income Supplement. While the benefits of owning an RRSP can be debatable as RRSPs are taken into account for the income-tested government benefits, a TFSA avoids this particular drawback as TFSA are not taken into account for income-tested government benefits.

2015 Benefits for Employees in Canada 8

Group RRSP and TFSA Both RRSPs and TFSAs can be set up by employers as group plans with contributions made to them by the employer and employee.

Pooled Registered Pension Plans

Pooled Registered Pension Plans (PRPPs) are a new type of savings plan designed to provide a simple, low-cost savings vehicle for small to mid-size employers who do not offer a Company sponsored pension plan, and for self-employed individuals. It is a tax-assisted DC type savings arrangement where assets from multiple unrelated employers are pooled for investment purposes, professionally managed and administered by approved licensed financial institutions, such as insurance companies and banks. The PRPP administrator and not the Company would be responsible for managing the PRPP investments and for communications with plan members on matters relating to the PRPP. All PRPP contributions made by a PRPP member for a year or on behalf of such a member (if any) are subject to the member’s available RRSP contribution for the year. Employee contributions are tax deductible and investment growth is tax sheltered. To be approved as a PRPP Administrator who can market PRPPs, financial institutions in each province must satisfy the PRPP legislative requirements established by each respective provincial government. A key requirement is that costs associated with the PRPP, such as investment management fees and administration fees be kept low. For federal PRPPs, the benchmark used for comparison is a traditional DC plan with membership of 500 or more. Other provinces may mandate low costs through regulations. PRPPs were first made available to federally regulated employers in 2012, followed by Quebec employers in 2014, but on a phased in basis depending on the size of the employer. Many other provinces have expressed an interest in implementing PRPPs, so this initiative is still developing. Ontario is considering a PRPP framework similar to the federal PRPP model.

Other Employment Savings Plans In addition to personal savings through RRSPs, TFSAs and PRPPs, employers in Canada offer deferred profit sharing plans (DPSP), employee profit sharing plans (EPSP), and employee share ownership plans (ESOP).

2015 Benefits for Employees in Canada 9

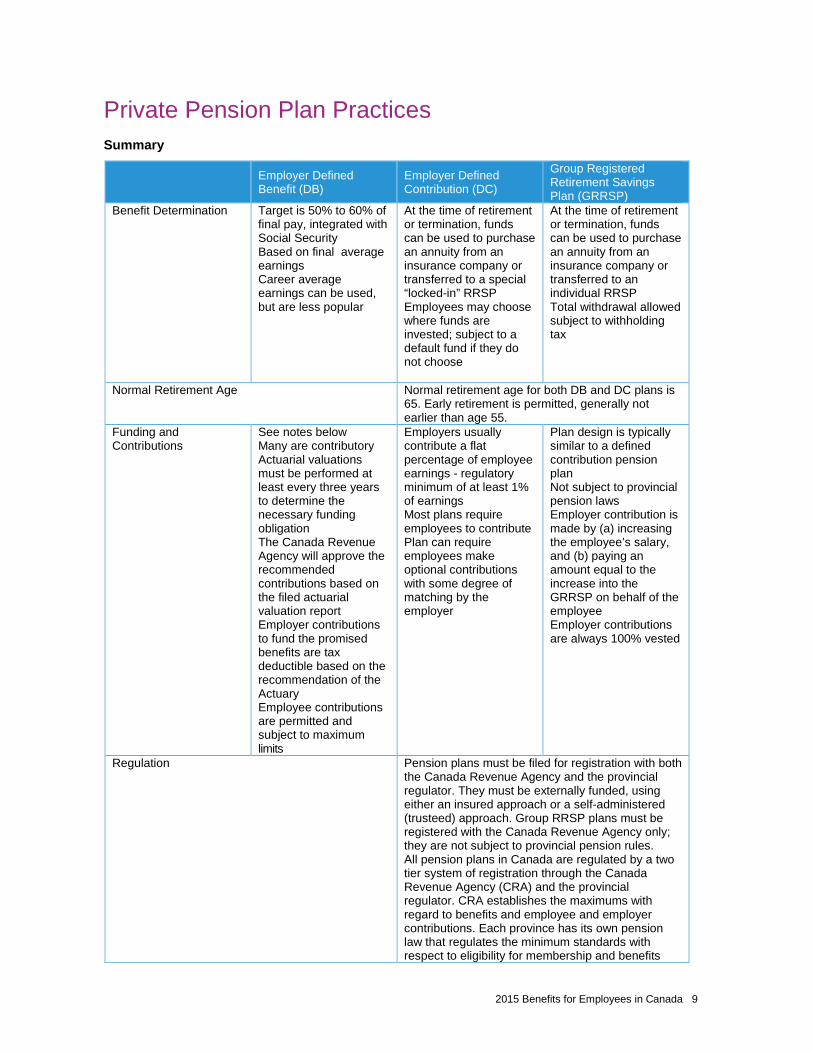

Private Pension Plan Practices Summary

Employer Defined Benefit (DB)

Employer Defined Contribution (DC)

Group Registered Retirement Savings Plan (GRRSP)

Benefit Determination Target is 50% to 60% of final pay, integrated with Social Security Based on final average earnings Career average earnings can be used, but are less popular

At the time of retirement or termination, funds can be used to purchase an annuity from an insurance company or transferred to a special “locked-in” RRSP Employees may choose where funds are invested; subject to a default fund if they do not choose

At the time of retirement or termination, funds can be used to purchase an annuity from an insurance company or transferred to an individual RRSP Total withdrawal allowed subject to withholding tax

Normal Retirement Age Normal retirement age for both DB and DC plans is 65. Early retirement is permitted, generally not earlier than age 55.

Funding and Contributions

See notes below Many are contributory Actuarial valuations must be performed at least every three years to determine the necessary funding obligation The Canada Revenue Agency will approve the recommended contributions based on the filed actuarial valuation report Employer contributions to fund the promised benefits are tax deductible based on the recommendation of the Actuary Employee contributions are permitted and subject to maximum limits

Employers usually contribute a flat percentage of employee earnings - regulatory minimum of at least 1% of earnings Most plans require employees to contribute Plan can require employees make optional contributions with some degree of matching by the employer

Plan design is typically similar to a defined contribution pension plan Not subject to provincial pension laws Employer contribution is made by (a) increasing the employee’s salary, and (b) paying an amount equal to the increase into the GRRSP on behalf of the employee Employer contributions are always 100% vested

Regulation Pension plans must be filed for registration with both the Canada Revenue Agency and the provincial regulator. They must be externally funded, using either an insured approach or a self-administered (trusteed) approach. Group RRSP plans must be registered with the Canada Revenue Agency only; they are not subject to provincial pension rules. All pension plans in Canada are regulated by a two tier system of registration through the Canada Revenue Agency (CRA) and the provincial regulator. CRA establishes the maximums with regard to benefits and employee and employer contributions. Each province has its own pension law that regulates the minimum standards with respect to eligibility for membership and benefits

2015 Benefits for Employees in Canada 10

Less than 40% of the Canadian working population participates in employer-sponsored group pension plans. Unionized employees sometimes participate in the same plan as their salaried counterparts; however, there are noticeable exceptions where union groups are administered through separate pension trusts.

Pension plans must be registered under the Income Tax Act and under one of the provincial pension benefits acts. The Income Tax Act provides a preferred tax structure to registered pension plans but limits

• the amount of pension that can be paid from a defined benefit plan, and

• the amount that can be contributed to a defined contribution plan.

Employers often supplement the registered plan with a non-registered supplemental plan that typically tops up the registered plan’s benefit due to the limitations in federal tax policy on providing benefits under a registered pension plan.

The following pages describe the main provisions of typical Canadian employer-sponsored registered pension plans. Pension standards vary based on the province of employment, making it increasingly important for employers to work closely with their plan administrator to ensure compliance.

Since non-registered plans are not subject to the various pension benefits acts, most of the following does not apply to the non-registered supplemental plans. Non-registered supplemental plans are generally not pre-funded. If these plans are pre-funded then they are classified as a Retirement Compensation Arrangements (RCA) under the Income Tax Act and a refundable tax must be paid to the Canada Revenue Agency.

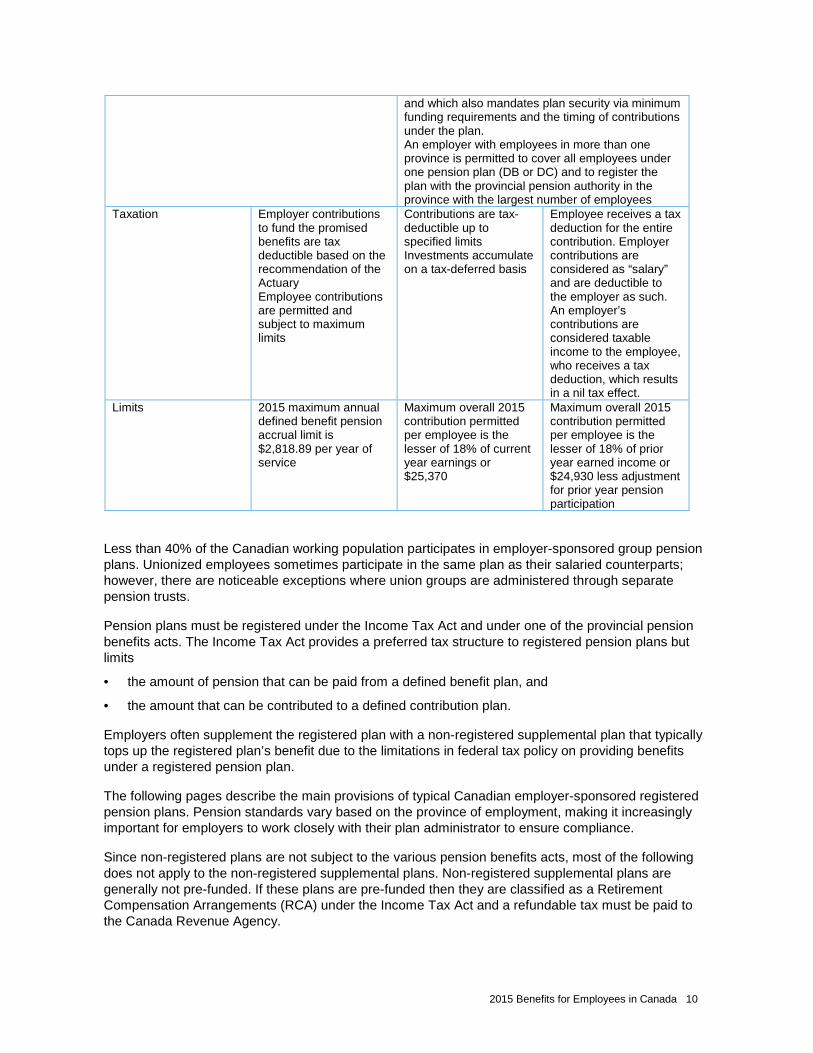

and which also mandates plan security via minimum funding requirements and the timing of contributions under the plan. An employer with employees in more than one province is permitted to cover all employees under one pension plan (DB or DC) and to register the plan with the provincial pension authority in the province with the largest number of employees

Taxation Employer contributions to fund the promised benefits are tax deductible based on the recommendation of the Actuary Employee contributions are permitted and subject to maximum limits

Contributions are tax-deductible up to specified limits Investments accumulate on a tax-deferred basis

Employee receives a tax deduction for the entire contribution. Employer contributions are considered as “salary” and are deductible to the employer as such. An employer’s contributions are considered taxable income to the employee, who receives a tax deduction, which results in a nil tax effect.

Limits 2015 maximum annual defined benefit pension accrual limit is $2,818.89 per year of service

Maximum overall 2015 contribution permitted per employee is the lesser of 18% of current year earnings or $25,370

Maximum overall 2015 contribution permitted per employee is the lesser of 18% of prior year earned income or $24,930 less adjustment for prior year pension participation

2015 Benefits for Employees in Canada 11

Nature of Pension Program DB plans are common with the vast majority of large employers. However, there has been a trend in recent years towards a defined contribution approach, or towards hybrid combination plans (comprised of a non-contributory defined benefit plan in combination with a contributory defined contribution plan). Smaller employers tend to favour the defined contribution approach.

Eligibility for Plan Participation All jurisdictions have legislation to ensure that pension plans permit full-time employees who meet minimum regulatory requirements to join the plan (i.e., typically 2 years of continuous service).

All jurisdictions have legislation to ensure that pension plans extend coverage to part-time employees who meet minimum regulatory requirements (for example, part-time employees who have earned at least 35% of the YMPE in each of two consecutive years).

Typically, membership is compulsory in the majority of plans, although it is sometimes optional until a certain age (when participation becomes compulsory). This area is expected to attract greater attention in the future, with the likely outcome being optional participation rights.

Employee Contributions Based on our 2011 Canadian Pension Survey, approximately 80% of defined benefit pension plans for non-union salaried employees in the private sector are contributory. For defined contribution plans approximately 80% are contributory. Plans covering bargaining unit employees tend not to require employees to contribute.

Typical DB plan contributions are in the range of 4 – 6% of earnings, less the employee’s required contribution to the Canada/Quebec Pension plan (CPP/QPP). Where contributions are integrated with the contributions required under the CPP/QPP the rate would be 1% to 2% lower for earnings under the YMPE. Most jurisdictions have enacted legislation which requires both a minimum level of interest credits on employee contributions, and that at least 50% of an employee’s vested pension is financed by employer contributions.

Contributions to DC plans are described under “Benefit Formula – DC” below. Required employee contributions to registered pension plans are tax-deductible for the employee.

Normal Retirement Normal retirement is defined as age 65. Most plans permit postponement of retirement beyond age 65. All Canadian provinces expressly prohibit mandatory retirement due to age qualifications except where there are bona fide occupational requirements.

Benefit Formula – DB plans Large organizations typically provide salaried employees with final average earnings defined benefit pension plans (the average of the three or five highest consecutive years). Assuming a full-career employee, together with CPP/QPP and Old Age Security benefits, this usually produces retirement income ranging from 40 – 80% of the employee’s highest earnings. Defined benefit plans are required to accommodate different provincial pension requirements for eligibility, early retirement rights, vesting, pre-retirement death benefits, etc.

The pension formula can either be expressed as a flat percentage of final pay or integrated with the government sponsored CPP/QPP. The maximum permissible benefit formula is 2% of final earnings (2015 maximum benefit of $2,818.89 per year of credited service); most formulas tend to fall within the range of 1% to 2%. Integration with the government sponsored CPP/QPP is most often achieved through an additive step-rate formula (e.g., 1.3% of highest earnings up to the CPP/QPP earnings base, plus 2% of highest earnings in excess of the YMPE). Relatively few plans use the subtractive direct offset integration approach.

2015 Benefits for Employees in Canada 12

Benefit Formula – DC plans Under a DC pension plan, the formula is essentially the sum of employee and employer contributions.

Employee contribution requirements are in the range 1% to 4% of earnings – which accounts for almost 90% of plans.

Most employers require employees to contribute and 65% of employers have set their basic contribution below 5% of employee earnings. Most employers also contribute additional amounts based on employee optional contributions. These additional contributions are typically structured as a 50% match of employee optional contributions. Total employer contributions fall in the range of 3 to 6.9% of employee earnings.

Contributions are invested as directed by the employee in some mix of equities, balanced funds, bonds or fixed income funds, money market funds, GICs and lifestyle funds.

There has been a shift towards offering employees a greater number of investment options. However, there is concern that offering too many choices simply confuses employees, who then simply stick with the plan’s default fund. There is no “safe harbour” protection in Canada for sponsors. Member use of the default fund needs to be actively managed by the plan’s governance committee.

Early Retirement Early retirement is available at any time within 10 years of normal retirement date.

Small employers with a defined benefit plan typically provide an early retirement pension that is equal to the accrued normal retirement pension, actuarially reduced to the actual retirement date.

Larger employers may subsidize early retirement under a defined benefit plan by modifying the reduction in accrued pension. Often, there is little or no reduction in the accrued pension when employees retire after age 60 or 62 and certain service criteria are met. Early retirement before then will usually be designed to decrease the employee’s pension by approximately 3 – 5% for each year of early retirement.

The typical criteria for unreduced early retirement benefits under a defined benefit plan include:

• Combined age plus service equal to 80, 85, or 90 years;

• Age 55 with 30 years of service; or

• Age 60 with 25 years of service.

Union plans may allow unreduced early retirement after 30 years of service regardless of the employee’s age.

Post-Retirement Death Benefits All pensions are payable for a member’s lifetime. It is not unusual for payment to be guaranteed for a minimum of five years after retirement. All jurisdictions have legislation that provides for spousal protection once pensions commence. The legislation requires that pensions be paid in a joint and survivor form if the employee has a spouse who has not signed a special waiver. The percentage amount of the joint and survivor pension is typically 60%. A full actuarial reduction to the pension is permitted to provide the spousal pension but there is a trend for defined benefit plans to fully or partially subsidize an employee’s joint and survivor optional form of pension.

Post-Retirement Pension Adjustments Few defined benefit plans have contractually committed to making automatic adjustments in pensions once payments have commenced. However, it is common practice under defined benefit plans to make periodic ad hoc adjustments. Typically, post-retirement adjustments replace 33 – 67% of the value lost through increases in the Consumer Price Index.

2015 Benefits for Employees in Canada 13

Pre-Retirement Death Benefits All jurisdictions require a deceased employee’s spouse to be paid a percentage (usually 60% or 100%) of the commuted value of the employee’s vested pension that accrued after a prescribed date and up to the date of death. A few jurisdictions accommodate integrating this pension death benefit with employer-funded group life insurance benefits that are payable to the deceased employee’s spouse. Defined contribution plans pay the full value of the investment account.

The member’s spouse is the preferred beneficiary, unless the spouse waives that right. However, administration of pre-retirement death benefits varies considerably between jurisdictions. Some jurisdictions require the spouse to use death benefit proceeds for the purpose of providing a lifetime pension only, while others permit (or require) a lump sum cash option. The definition of “spouse” also varies by jurisdiction.

Vesting on Termination of Service All jurisdictions provide for minimum vesting requirements for the employer-provided portion of an employee’s accrued benefits/contributions. The regulatory trend is to immediate vesting; a few jurisdictions still require vesting after two years of plan participation. However, employers may offer immediate vesting. The employee’s contributions are always vested.

Employee Representation in Plan Administration In some jurisdictions (i.e., Ontario, Manitoba, British Columbia, and Saskatchewan), a special pension committee must be established, with direct member representation when requested by the majority of plan members. In these jurisdictions, the pension committee serves only in an advisory capacity. However, very few advisory committees have been established.

Pension plans registered in Quebec must be administered by a pension committee having both member representation and a third-party individual. This rule became effective beginning in 1990. The committee has full responsibility for interpreting plan provisions, determining member benefits, establishing pension fund investment policies, monitoring contribution remittances, and generating government filings. Also Manitoba requires that (with certain exceptions) a pension plan must be administered by a pension committee.

Future provincial legislation is expected to strengthen the requirement to implement advisory committees in many jurisdictions.

Financing of Private Pension Plans From a funding perspective, registered pension plans are either fully insured or “trusteed”. The majority of plans for small employers are fully insured. The majority of plans for mid- to large-sized employers are funded through a corporate trust or through an insurance company “segregated fund” policy. The larger the employer, the more likely it will be that either an outside or inside investment counselor is used to direct investments.

Minimum funding standards for defined benefit plans are prescribed by provincial law. The funding rules for a particular plan’s jurisdiction of registration apply to the whole plan. Usually, the jurisdiction of registration has plurality of membership. These laws generally permit amortization of unfunded liabilities over as long a period as 15 years. Where a plan’s assets are insufficient to cover the benefit obligations that would exist on windup, amortization must, in some cases, be accelerated to five years. Historically, funding valuations were required at least every three years; however, underfunded plans are increasingly subject to annual valuations if funding ratios are below prescribed ratios.

Pension plan sponsors are subject to Canadian accounting standards for determination and reporting of pension obligations in corporate financial statements. Canadian pension accounting rules are almost identical to those required in the United States and internationally.

2015 Benefits for Employees in Canada 14

Phased Retirement In late 2007, the Federal government amended the Income Tax Act (Canada) Regulations to allow a registered pension plan to offer phased retirement benefits in order to encourage the retention of older “key” employees. Qualifying employees would be able to accrue current service pension benefits under a defined benefit registered pension plan, while at the same time receiving a pension from that plan or another defined benefit plan of the employer or a related employer. Previously, the accrual and payment of a pension at the same time was not permitted.

Qualifying employees must be at least age 60 or, 55 years of age and eligible to receive an unreduced pension. The latter requirement greatly limits the employees that will be able to take advantage of this new provision. Effectively, employees will have to be aged 55 and have 25 or 35 years of service or 85 points, for instance (depending on the plan requirements for an unreduced pension), prior to being eligible for phased retirement.

The phased retirement pension amount would be up to 60% of accrued pension benefits, including both lifetime and bridge pensions, as if the employee were fully retired. The new provisions for phased retirement do not require that an employee work part-time to be eligible for phased retirement. In light of the introduction of phased retirement provisions under the Canadian Income Tax Act, a number of provinces have introduced or have committed to accommodate phased retirement provisions in their minimum standards legislation.

New and Pending Developments

Provincial Pension Laws

Ontario, Alberta, British Columbia, and Nova Scotia have, over the past number of years, conducted sweeping pension reform studies and made recommendations to strengthen the private employment pension system. These recommendations cover such areas as governance, plan funding, security, and surpluses. New Brunswick enacted pension legislation in 2012 which permits shared cost pension plans – a first in Canada. Alberta’s pension reform legislation came into force in 2014. Nova Scotia introduced pension reform legislation in 2011 which is expected to come into force in 2015. And British Columbia introduced pension reform legislation in 2012 which is also expected to come into force in 2015.

Currently, Prince Edward Island has no pension legislation in place but intends to remedy that in 2015.

In July, 2012, Ontario brought into force several aspects of their pension reform legislation (including immediate vesting, enhanced disclosure of information, and elimination of partial plan wind-ups); the balance of Ontario’s pension reform changes are expected over the course of 2015.

Overall, the pace of pension reform in Canada has been frustratingly slow. However, we do expect to see more progress throughout Canada in 2015 and 2016.

Target Benefit Plans

Target benefit plans (TBP) have been gaining attention at both the provincial and federal levels of government in recent years, largely due to the issues surrounding inadequate pension coverage and funding volatility in the private sector. The TBP model is based on features that currently exist in many multi-employer collectively bargained pension plans. TBAs incorporate the favourable features of both DC and DB plans, such as fixed contributions for the employer and more predictable target benefits for the employee. However, the ability to reduce benefits if the pension fund is not sufficient to provide the target benefits is another key feature of a TBP, and this has created challenges for pension regulators as they work towards developing strong legislative frameworks so that the necessary governance structures, funding requirements and member communications are put in place to avoid the last resort of benefit reductions. Currently, New Brunswick is the only province that has legislation in force for their version of TBPs, which they refer to as “shared risk plans”.

2015 Benefits for Employees in Canada 15

PRPPs

The federal government enacted legislation in 2012 to create PRPP. A PRPP is DC plan which is administered by a financial institution, rather than the employer. A PRPP allows employees from unrelated employers to pool their assets together in order to lower investment costs.

When the federal PRPP legislation was first enacted, it was available only to federally regulated employers and the provinces needed to enact their own legislation in order to allow other employers to offer a PRPP to its employees. Since that time, several provinces have either passed or introduced legislation to permit PRPPs, and it is anticipated that the remaining provinces will follow suit.

2015 Benefits for Employees in Canada 16

Disability Benefits Canadians who become disabled and are unable to work, either temporarily or on a long term basis, rely on income-replacement and other benefits provided by the various provincial and federal government-sponsored income protection programs and / or their employer sponsored - programs. The federal government administers the Employment Insurance (EI) program, providing income-replacement for short term disabilities but also for maternity and parental benefits. Quebec opts out of the EI program for maternity and parental benefits and administers the Quebec Parental Insurance Plan directly. For longer disabilities that are deemed severe and prolonged in nature, the Quebec and federal governments administer and offer protection under the Canada / Quebec Pension Plan.

Social Security Summary

EI QPIP CPP/QPP Eligibility for Benefits Weekly earnings

decreased by more than 40% Worked 600 hours in previous 52 weeks Contributed to EI

Quebec resident Parent of children born / adopted after Dec. 31 2005 Earned min. $2,000 insurable income during qualifying period Contributed to QPIP

Under age 65 Contributed for 4 of the last 6 years, or at least 3 of the last 6 years if more than 25 years of contribution Must have a severe and prolonged disability (subject to adjudication)

Short Term Disability Benefits

55% of gross weekly insurable earnings (max $524) Two-week waiting period Sickness benefit and maternity leave paid up to 15 weeks Parental leave paid up to 35 weeks Taxable income

Maternity: 70% of insurable earnings for 18 weeks (basic plan) or 75% for 15 weeks (special plan) Paternity: 70% of insurable earnings for 5 weeks (basic plan) or 75% for 3 weeks (special plan) Parental: 70% of insurable earnings for 7 weeks and 55% for 25 weeks (basic plan) or 75% for 25 weeks (special plan) Adoption: 70% of insurable earnings for 12 weeks and 55% for 25 weeks (basic plan) or 75% for 28 weeks (special plan)

n/a

Long Term Disability Benefit

n/a n/a Flat amount plus 75% of calculated retirement pension, up to a monthly maximum of $1,264.59 Taxable income Indexed

Supplement for Dependent Child

n/a n/a Flat amount of $234.87 per month

2015 Benefits for Employees in Canada 17

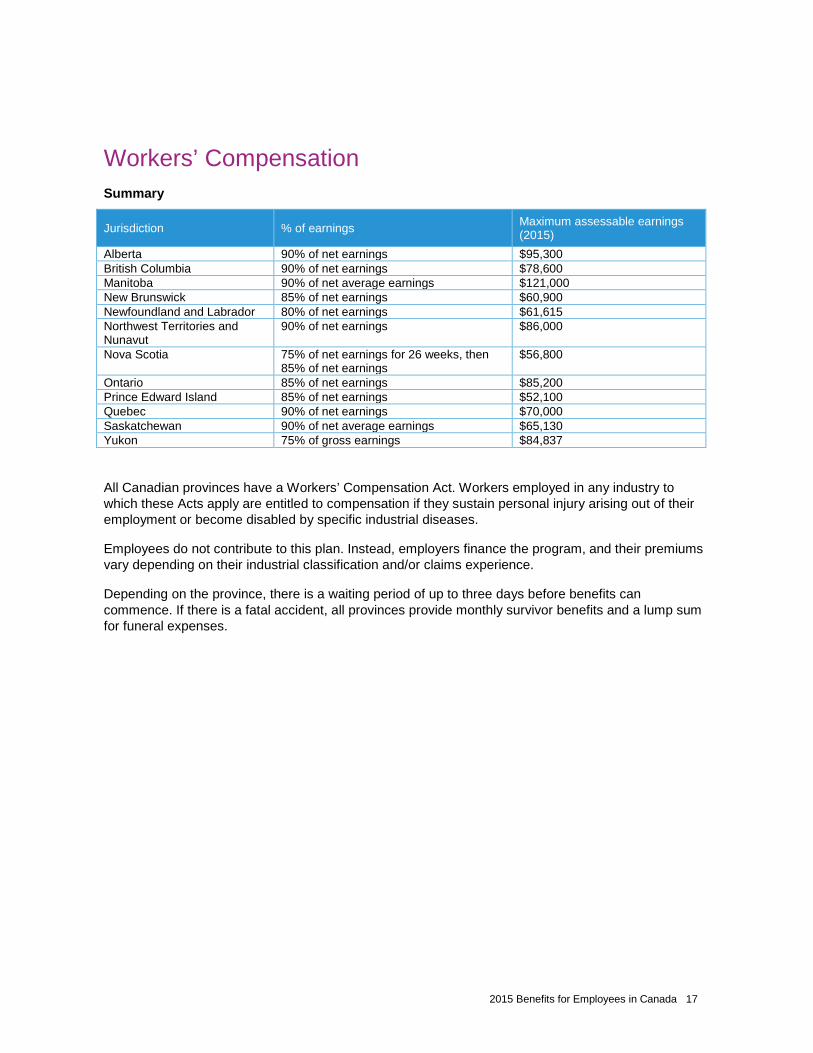

Workers’ Compensation Summary

Jurisdiction % of earnings Maximum assessable earnings (2015)

Alberta 90% of net earnings $95,300 British Columbia 90% of net earnings $78,600 Manitoba 90% of net average earnings $121,000 New Brunswick 85% of net earnings $60,900 Newfoundland and Labrador 80% of net earnings $61,615 Northwest Territories and Nunavut

90% of net earnings $86,000

Nova Scotia 75% of net earnings for 26 weeks, then 85% of net earnings

$56,800

Ontario 85% of net earnings $85,200 Prince Edward Island 85% of net earnings $52,100 Quebec 90% of net earnings $70,000 Saskatchewan 90% of net average earnings $65,130 Yukon 75% of gross earnings $84,837

All Canadian provinces have a Workers’ Compensation Act. Workers employed in any industry to which these Acts apply are entitled to compensation if they sustain personal injury arising out of their employment or become disabled by specific industrial diseases.

Employees do not contribute to this plan. Instead, employers finance the program, and their premiums vary depending on their industrial classification and/or claims experience.

Depending on the province, there is a waiting period of up to three days before benefits can commence. If there is a fatal accident, all provinces provide monthly survivor benefits and a lump sum for funeral expenses.

2015 Benefits for Employees in Canada 18

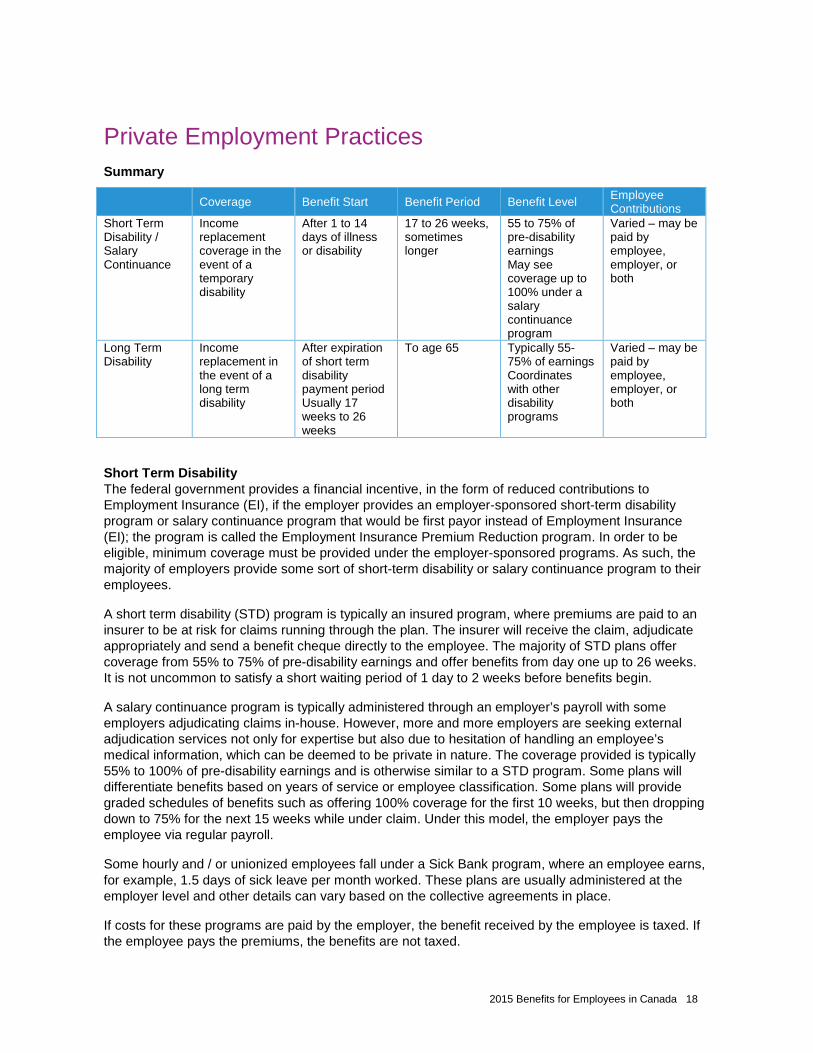

Private Employment Practices Summary

Coverage Benefit Start Benefit Period Benefit Level Employee Contributions

Short Term Disability / Salary Continuance

Income replacement coverage in the event of a temporary disability

After 1 to 14 days of illness or disability

17 to 26 weeks, sometimes longer

55 to 75% of pre-disability earnings May see coverage up to 100% under a salary continuance program

Varied – may be paid by employee, employer, or both

Long Term Disability

Income replacement in the event of a long term disability

After expiration of short term disability payment period Usually 17 weeks to 26 weeks

To age 65 Typically 55-75% of earnings Coordinates with other disability programs

Varied – may be paid by employee, employer, or both

Short Term Disability The federal government provides a financial incentive, in the form of reduced contributions to Employment Insurance (EI), if the employer provides an employer-sponsored short-term disability program or salary continuance program that would be first payor instead of Employment Insurance (EI); the program is called the Employment Insurance Premium Reduction program. In order to be eligible, minimum coverage must be provided under the employer-sponsored programs. As such, the majority of employers provide some sort of short-term disability or salary continuance program to their employees.

A short term disability (STD) program is typically an insured program, where premiums are paid to an insurer to be at risk for claims running through the plan. The insurer will receive the claim, adjudicate appropriately and send a benefit cheque directly to the employee. The majority of STD plans offer coverage from 55% to 75% of pre-disability earnings and offer benefits from day one up to 26 weeks. It is not uncommon to satisfy a short waiting period of 1 day to 2 weeks before benefits begin.

A salary continuance program is typically administered through an employer’s payroll with some employers adjudicating claims in-house. However, more and more employers are seeking external adjudication services not only for expertise but also due to hesitation of handling an employee’s medical information, which can be deemed to be private in nature. The coverage provided is typically 55% to 100% of pre-disability earnings and is otherwise similar to a STD program. Some plans will differentiate benefits based on years of service or employee classification. Some plans will provide graded schedules of benefits such as offering 100% coverage for the first 10 weeks, but then dropping down to 75% for the next 15 weeks while under claim. Under this model, the employer pays the employee via regular payroll.

Some hourly and / or unionized employees fall under a Sick Bank program, where an employee earns, for example, 1.5 days of sick leave per month worked. These plans are usually administered at the employer level and other details can vary based on the collective agreements in place.

If costs for these programs are paid by the employer, the benefit received by the employee is taxed. If the employee pays the premiums, the benefits are not taxed.

2015 Benefits for Employees in Canada 19

Long Term Disability Long Term Disability (LTD) programs are typically insured programs providing income-replacement benefits if an employee is deemed to be disabled beyond the STD period. As with the insured STD program mentioned above, the insurer will be at risk for any claims paid out under the LTD program in return for premium submitted. Benefits are similar to those provided under the STD program but usually will be paid out until the disabled claimant reaches age 65, if continuously disabled. Many LTD programs have rehabilitation programs built in, in hopes of being able to return a claimant back to work, either with the original employer if the employee can perform the duties of his / her job, or to another employer if the claimant is unable to perform the duties of his / her job and / or the original employer is unable to accommodate the employee based on their post-disability skill set.

As with STD, when the premium is paid by the employer, the benefit is taxable.

2015 Benefits for Employees in Canada 20

Death Benefits/Life Insurance

Social Security Summary

CPP QPP Eligibility for survivor benefits

Spouse/Common Law Partner of a contributor or pensioner Dependent child of a contributor or pensioner

Spouse/Common Law Partner of a contributor or pensioner Dependant child of a contributor or pensioner

Maximum CPP rates 2015 Maximum QPP rates 2015 Lump sum death benefit $2,500 $2,500 Surviving Spouse’s benefit

Under 65, $567.91 65 or over $623.00

Under 45, no child $506.56 Under 45, with child $814.23 Under 45, disabled $846.94 45 to 64 $846.94 65 or over $623.00

Monthly orphan’s benefit $230.72/ child $230.72 Survivor’s Allowance n/a n/a

2015 Benefits for Employees in Canada 21

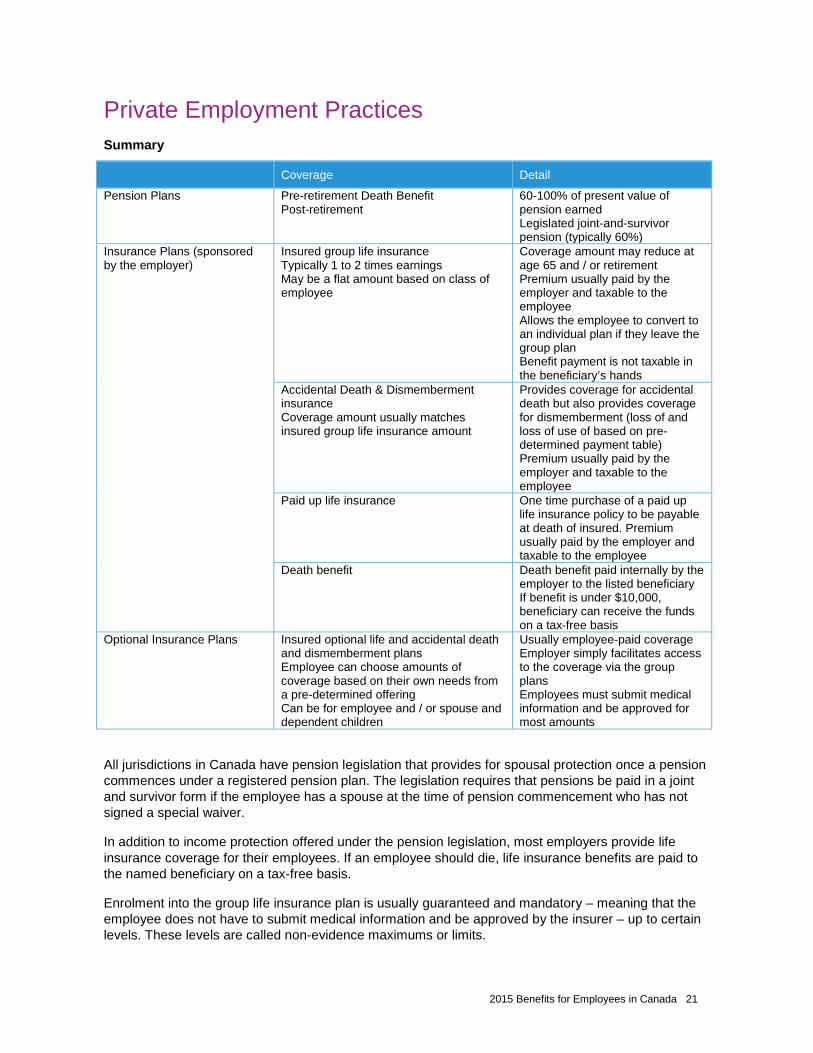

Private Employment Practices Summary

Coverage Detail Pension Plans Pre-retirement Death Benefit

Post-retirement 60-100% of present value of pension earned Legislated joint-and-survivor pension (typically 60%)

Insurance Plans (sponsored by the employer)

Insured group life insurance Typically 1 to 2 times earnings May be a flat amount based on class of employee

Coverage amount may reduce at age 65 and / or retirement Premium usually paid by the employer and taxable to the employee Allows the employee to convert to an individual plan if they leave the group plan Benefit payment is not taxable in the beneficiary’s hands

Accidental Death & Dismemberment insurance Coverage amount usually matches insured group life insurance amount

Provides coverage for accidental death but also provides coverage for dismemberment (loss of and loss of use of based on pre-determined payment table) Premium usually paid by the employer and taxable to the employee

Paid up life insurance One time purchase of a paid up life insurance policy to be payable at death of insured. Premium usually paid by the employer and taxable to the employee

Death benefit Death benefit paid internally by the employer to the listed beneficiary If benefit is under $10,000, beneficiary can receive the funds on a tax-free basis

Optional Insurance Plans Insured optional life and accidental death and dismemberment plans Employee can choose amounts of coverage based on their own needs from a pre-determined offering Can be for employee and / or spouse and dependent children

Usually employee-paid coverage Employer simply facilitates access to the coverage via the group plans Employees must submit medical information and be approved for most amounts

All jurisdictions in Canada have pension legislation that provides for spousal protection once a pension commences under a registered pension plan. The legislation requires that pensions be paid in a joint and survivor form if the employee has a spouse at the time of pension commencement who has not signed a special waiver.

In addition to income protection offered under the pension legislation, most employers provide life insurance coverage for their employees. If an employee should die, life insurance benefits are paid to the named beneficiary on a tax-free basis.

Enrolment into the group life insurance plan is usually guaranteed and mandatory – meaning that the employee does not have to submit medical information and be approved by the insurer – up to certain levels. These levels are called non-evidence maximums or limits.

2015 Benefits for Employees in Canada 22

All life insurance premiums, paid by the employer on behalf of the employee, are deemed to be a taxable benefit at the federal level and are included on an employee’s T4 at year-end.

Employers in Canada usually also provide Accidental Death & Dismemberment coverage for their employees, where the beneficiary will receive an additional insurance benefit if the employee should die accidentally. Under this coverage, the employee would also receive benefits, based on a graded schedule, if they were to be dismembered or lose the use of a body part.

Effective January 1, 2013, accidental death and dismemberment premiums, along with critical illness insurance premiums, paid by the employer on behalf of the employee, are also deemed to be a taxable benefit at the federal level and are included on an employee’s T4 at year-end.

Many employers provide optional employee, spousal or dependent child life insurance benefits. Under optional plans, the employee usually pays 100% of the costs and the insurers will usually request medical information, based on which they will either further approve or decline enrolment. Employers will put these plans into place as premiums tend to be lower under a group plan than if the employee were to shop for individual insurance on his/her own.

2015 Benefits for Employees in Canada 23

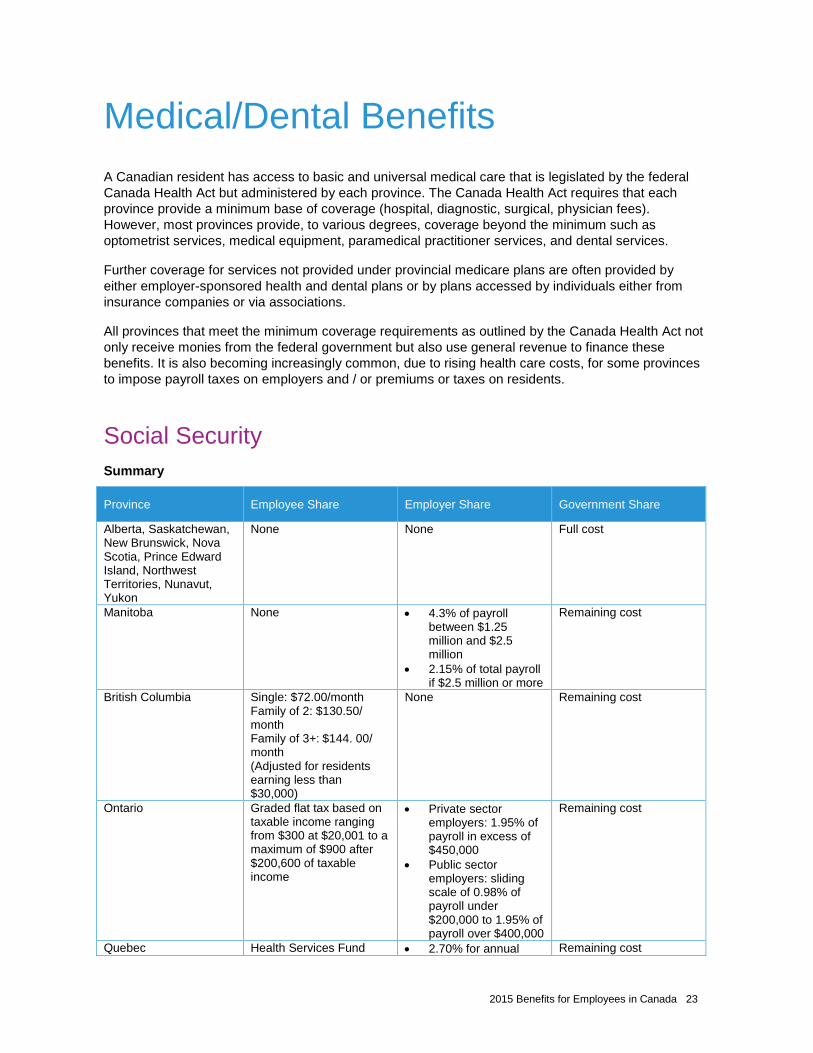

Medical/Dental Benefits A Canadian resident has access to basic and universal medical care that is legislated by the federal Canada Health Act but administered by each province. The Canada Health Act requires that each province provide a minimum base of coverage (hospital, diagnostic, surgical, physician fees). However, most provinces provide, to various degrees, coverage beyond the minimum such as optometrist services, medical equipment, paramedical practitioner services, and dental services.

Further coverage for services not provided under provincial medicare plans are often provided by either employer-sponsored health and dental plans or by plans accessed by individuals either from insurance companies or via associations.

All provinces that meet the minimum coverage requirements as outlined by the Canada Health Act not only receive monies from the federal government but also use general revenue to finance these benefits. It is also becoming increasingly common, due to rising health care costs, for some provinces to impose payroll taxes on employers and / or premiums or taxes on residents.

Social Security Summary

Province Employee Share Employer Share Government Share

Alberta, Saskatchewan, New Brunswick, Nova Scotia, Prince Edward Island, Northwest Territories, Nunavut, Yukon

None None Full cost

Manitoba None • 4.3% of payroll between $1.25 million and $2.5 million

• 2.15% of total payroll if $2.5 million or more

Remaining cost

British Columbia Single: $72.00/month Family of 2: $130.50/ month Family of 3+: $144. 00/ month (Adjusted for residents earning less than $30,000)

None Remaining cost

Ontario Graded flat tax based on taxable income ranging from $300 at $20,001 to a maximum of $900 after $200,600 of taxable income

• Private sector employers: 1.95% of payroll in excess of $450,000

• Public sector employers: sliding scale of 0.98% of payroll under $200,000 to 1.95% of payroll over $400,000

Remaining cost

Quebec Health Services Fund • 2.70% for annual Remaining cost

2015 Benefits for Employees in Canada 24

contribution based on income to a maximum contribution of $1,000

payroll of $1 million or less

• 4.26% for annual payroll of $5 million or more and all Public Sector employees

• Between 2.70% and 4.26% for annual payroll of more than $1 million and less than $5 million

Newfoundland and Labrador

None 2% of payroll over $1 million if annual payroll exceeds $1.2 million

Remaining cost

Private Employment Practices As the provincial medicare plans only provide basic coverage for medical needs, it is common for employers to provide group health and dental plans to supplement the provincial medicare plans. Coverage is typically provided to active employees. Coverage for retired employees is sometimes provided but has been introduced less and less due not only to rising health care costs but also the requirement of publicly-traded employers to report the present value of the future liabilities associated with providing retiree health and dental benefits on their financial statements.

The health coverage is usually referred to as extended or supplementary health care, and is provided, along with dental coverage, under an insured or self-insured funding arrangement.

It is against the law for a private health or dental program to pay for services that are covered under a provincial medicare plan.

Usual coverage under an employer-sponsored health care plan is:

• Prescription drugs

• Private duty nursing

• Medical supplies

• Paramedical practitioners – massage therapist, chiropractors, physiotherapist

• Vision care including eye exams

• Hearing aids

• Out of country emergency expenses

• Hospital room upgrade to semi-private or private (provincial plans must pay for ward coverage)

2015 Benefits for Employees in Canada 25

Coverage for dental expenses is also popular, as very little coverage is provided under provincial medicare plans. Examples of coverage include:

• Preventative services - routine checkups and cleanings

• Basic services – periodontal scaling, filings, root canals

• Major restorative services – bridges, crowns, dentures

• Orthodontics services – retainers and braces, usually for dependent children under age 18

Most dental plans provide for preventative and basic services. Not all plans provide for major restorative and / or orthodontics coverage.

Under both the health and dental plans, coverage is usually provided at 80% to 100% reimbursement levels. For major restorative and orthodontics coverage, reimbursement is generally provided between 50% and 60%.

It is not uncommon to also see deductibles and fixed annual or lifetime maximums in place to limit the liability of the plans paying out indefinitely, although most Health plans are still unlimited.

In addition to co-pays mentioned above, some employers will have their employees contribute to the monthly premium costs of the plans via payroll deductions. The percentage of employee contribution varies, if it exists at all, and is most commonly maxed out at 25%.

Health Spending Account Health Spending Accounts (HSA) have become a part of many group benefit plans in Canada. They are a practical, affordable and cost-effective way to meet the changing needs of today’s employers and employees.

Qualifying as a Private Health Services plan under section 248 of the Income Tax Act, HSA’s provide a way for clients to deliver tax-effective compensation to their employees, tax-free dollars. At the beginning of the year, the employer decides on the amount to be available in the HSA. Throughout the year, plan members can claim reimbursement from their HSA to cover the cost of health-related expenses allowable under the Income Tax Act. The HSA offers a vaster list of coverage than that which is provided under the employer-sponsored health and dental plans. To receive this favourable tax status, HSA funds operate on a “use it or lose it” basis. They can be set up to provide a 1 year carry forward of either unused expenses or unpaid balances. Unused balances are forfeited by employees.

Critical Illness Insurance Critical illness insurance is growing in popularity in Canada. When added to the benefit coverage at work, it offers employees help paying costs associated with life-altering illnesses. If an employee become sick with an illness covered by the employer’s policy, and survives the waiting period (usually 30 days), the beneficiary (the employee) receives a lump sum cash payment. This can be used at the employee’s discretion to help cover lost income, to pay for private nursing or out-of-country treatment, for medical equipment, or even to pay off a mortgage. The benefit is not taxable in the beneficiary’s hands.

2015 Benefits for Employees in Canada 26

Vacation and Wellness Programs

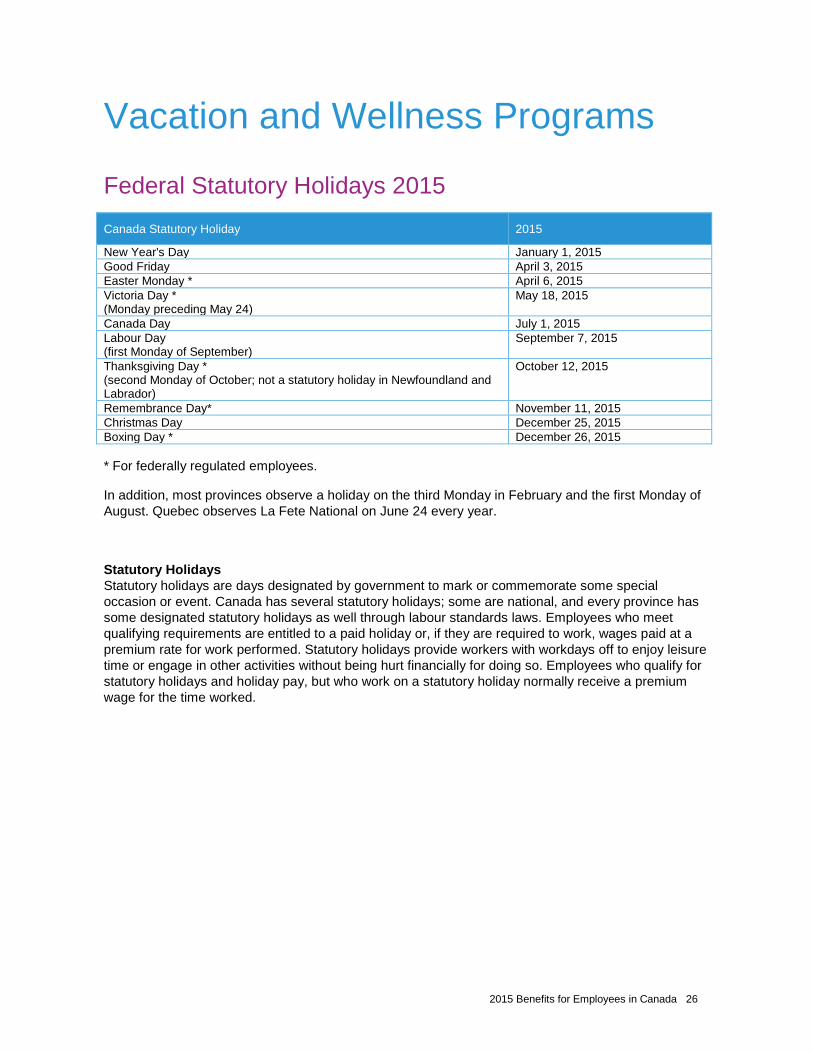

Federal Statutory Holidays 2015 Canada Statutory Holiday 2015

New Year's Day January 1, 2015 Good Friday April 3, 2015 Easter Monday * April 6, 2015 Victoria Day * (Monday preceding May 24)

May 18, 2015

Canada Day July 1, 2015 Labour Day (first Monday of September)

September 7, 2015

Thanksgiving Day * (second Monday of October; not a statutory holiday in Newfoundland and Labrador)

October 12, 2015

Remembrance Day* November 11, 2015 Christmas Day December 25, 2015 Boxing Day * December 26, 2015

* For federally regulated employees.

In addition, most provinces observe a holiday on the third Monday in February and the first Monday of August. Quebec observes La Fete National on June 24 every year.

Statutory Holidays Statutory holidays are days designated by government to mark or commemorate some special occasion or event. Canada has several statutory holidays; some are national, and every province has some designated statutory holidays as well through labour standards laws. Employees who meet qualifying requirements are entitled to a paid holiday or, if they are required to work, wages paid at a premium rate for work performed. Statutory holidays provide workers with workdays off to enjoy leisure time or engage in other activities without being hurt financially for doing so. Employees who qualify for statutory holidays and holiday pay, but who work on a statutory holiday normally receive a premium wage for the time worked.

2015 Benefits for Employees in Canada 27

Vacation In all jurisdictions, eligible employees are entitled to at least two weeks of annual vacation with pay after each completed year of employment. The exception is Saskatchewan, where employers must provide no less than three weeks of vacation with pay to employees who have completed one year of service.

In 11 jurisdictions, employees are entitled to an additional week of vacation with pay after a specified period of service.

Although the formula used to calculate vacation pay – annual wages times 4% (or 6% if the employee is entitled to three weeks’ vacation) – is common to most jurisdictions, there is relatively little consistency across Canada as regards the types of earnings (e.g., salary, tips, holiday pay) that are to be considered as “wages”.

Wellness Programs Workplace wellness programs are on the rise, according to our Working Well: A Global Survey of Health Promotion and Workplace Wellness Strategies. Seventy-six percent of the North American organizations surveyed indicated that they have a wellness strategy.

Immunizations and flu shots top the list of wellness program components in North America, followed by health portals and websites. These programs have been around for years but are increasing in popularity as companies struggle to better manage absenteeism and disability claims. Executive screening programs are third on the list for Canadian employers. Other popular offerings include health risk appraisals, fitness membership discounts and caregiver support.

In Canada, the interest in wellness strategies continues to grow. Since our country is fortunate enough to have a robust public health system, Canadian employers will likely achieve the greatest return on investment in wellness by focusing on workplace culture. A number of survey respondents’ comments suggest that their vision is to create an organization-wide culture of health and well-being. With the recent surge in absences related to workplace stress and mental health, it would appear that their efforts are well placed. Providing an environment that respects employees, promotes fairness and work/life balance, and offers outlets for workplace stress will go a long way toward achieving the vision of a healthy, motivated workforce.

2015 Benefits for Employees in Canada 28

Contact Us About Buck Consultants at Xerox Within Xerox, Buck is the consulting strength of the Human Resource Services (HRS) division. Buck offers advisory, technology, and administration solutions to help you effectively manage your programs while engaging your employees in their health, wealth, and career. By integrating our HR consulting know-how with HRS’ core services, we can offer additional innovative and customized solutions to help you overcome your HR challenges.

Together, we can ensure you have the right people in the right positions at the right time to save money and achieve your business goals. Learn more at www.xerox.com/hrconsulting.

Since the invention of Xerography more than 75 years ago, the people of Xerox (NYSE: XRX) have helped businesses simplify the way work gets done. Today, we are the global leader in business process and document management, helping organizations of any size be more efficient so they can focus on their real business. Headquartered in Norwalk, Conn., we have more than 140,000 Xerox employees and do business in more than 180 countries, providing business services, printing equipment and software for commercial and government organizations. Learn more at www.xerox.com.