Yearbook 2003 - Assaereo

81

cargolux Yearbook 2003 Association of European Airlines

Transcript of Yearbook 2003 - Assaereo

cargolux

Yearbook 2003

Association of European Airlines

July 2003 Dear Reader of the AEA Yearbook, The AEA Yearbook has always been the benchmark for the European aviation industry. It is a source of information on current trends supported by facts, figures and careful analysis. This yearbook is no different. It seeks to outline and explain the impact on our industry of one of the toughest periods in the history of aviation. Against a background of global economic slowdown, the war with Iraq, and SARS, global airlines have suffered four consecutive years of losses and no growth. The continued crisis however, has been a catalyst for change and it has energised us to develop new solutions to meet the changing needs of our customers and the marketplace. AEA member airlines have dramatically reduced their overall cost of operations and many are re-evaluating core elements of their current business model, addressing structural inefficiencies, particularly in the short-haul sector. This Yearbook details the problems and the solutions we are seeking to implement to ensure European aviation is healthy and vibrant.

During my chairmanship of the AEA in 2003, we have undertaken a root and branch review to raise awareness of its role and effectiveness as an industry body. The web-site has been revamped and well received and our communications have greatly improved. Without doubt, this has been a very critical year for the industry as a result of external pressures - the continued threat of terrorist activity, the Iraq war and the weak global economy. However, it has also been an historic year. The European Commission has been granted the mandate to negotiate a new air treaty with the US. If it comes to fruition we will achieve true liberalisation and create a vibrant, competitive market which the AEA has long called for. I hope you enjoy reading this document and that it will provide the basis for a continued discussion about the future of European aviation.

Rod Eddington Chief Executive of British Airways AEA Chairman 2003

Avenue Louise 350 B - 1050 BrusselsTel. +32 (0)2 639 89 89 Fax 639 89 99 E-mail [email protected]

_________

Association of European Airlines

Adria Airways, Aer Lingus, Air France, Air Malta, Alitalia, Austrian Airlines, BMI, British Airways, Cargolux, Croatia Airlines, CSA, Cyprus Airways, Finnair, Iberia, Icelandair, JAT, KLM,LOT, Lufthansa, Luxair, Malev, Meridiana, Olympic Airways, SAS, SN Brussels Airlines,Spanair, SWISS, TAP Air Portugal, Tarom, Turkish Airlines, Virgin Atlantic Airways.

ASSOCIATION OF EUROPEAN AIRLINES I - 1

CONTENTS SECTION I AEA AIRLINES IN 2002 I-1 At a Glance I-2 Welcome to Virgin Atlantic Airways I-4 The Global Economic Environment I-5 Traffic Development 2002 I-7 ‘No-frills’ carriers l-8 Spotlight on the North Atlantic I-10 Spotlight on the Far East I-11 Operating Results 2002 I-12 Punctuality Performance I-14 SECTION II OUTLOOK FOR 2003 II-1 The Story so Far.. II-2 Traffic Development II-3 Operating Results II-4 SECTION III LOOKING FORWARD III-1 Towards an Efficient European Air Transport System III-2 Are Air Transport Networks Sustainable? III-4 Improving the Industry’s Regulatory Framework III-5 The Dynamics of the Value Chain III-6 A transatlantic Open Aviation Area ? III-7 Bilateral Agreements – Where now ? III-8 Denied Boarding Compensation III-9 External Shocks – Security and Insurance III-10 SECTION IV SPOTLIGHT ON THE AEA IV-1 AEA Highlights IV-3 Airline Profiles & Review of 2002 IV-6 SECTION V KEY STATISTICS V-1 Key Statistics - Total AEA V-2 Key Statistics - By Carrier V-4 AEA Fast Facts V-11 What do we mean by…? V-12

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5

3.0 billion current US$ after interest

02010099989796959493929190

US$ -3.02 bn (€ -3.2 bn)

US$ -0.87 bn(€ -0.94 bn)

OPERATING PROFIT / LOSS TOTAL SCHEDULED ROUTES

Source: AEA

AEA_YB_03_01

-0.87 billion US$Total Financial Loss (-0.94 € bn)

-2.4 bn US$ Revenue lessTotal Scheduled Revenue all services (-2.5 € bn)

-13.8 million fewer PassengersTotal Scheduled Passenger numbers

-4.8% Passenger Traffic lossTotal Scheduled Passenger Kms

-8.7% reduction in CapacityTotal Scheduled Seat Kms on offer

2002 over 2001

AT A GLANCE

I – 2 ASSOCIATION OF EUROPEAN AIRLINES

Markets which should have beenrecovering from their prolongedweakness were belaeguered once againin early 2003 , first by the Iraq War, thenby the wholly disproportionate effect ofthe SARS outbreak.

A graphic reminder of the shockwavesent through the market by the events ofSeptember 11.

-35

-30

-25

-20

-15

-10

-5

0

5

10

15

20

25

30% change in RPKs

MAY-03JUN-02JUN-01

MONTHLY TRAFFIC MONITOR

Source: AEA

AEA_YB_03_03

September 11th

Geographical Europe

North Atlantic

Far East / Australasia

Geographical Europe

North Atlantic

Far East / Australasia

Geographical Europe

North Atlantic

Far East / Australasia

Middle East

Gulf War II(20-Mar/14-Apr)

-60

-50

-40

-30

-20

-10

0

10% change in RPKs

W50W45W40W37

SEP-DEC 2001

Source: AEA

AEA_YB_03_04

-60

-50

-40

-30

-20

-10

0

10

20% change in RPKs

W25W20W15W12

MAR-JUL 2003

Source: AEA

AEA_YB_03_02

ASSOCIATION OF EUROPEAN AIRLINES I – 3

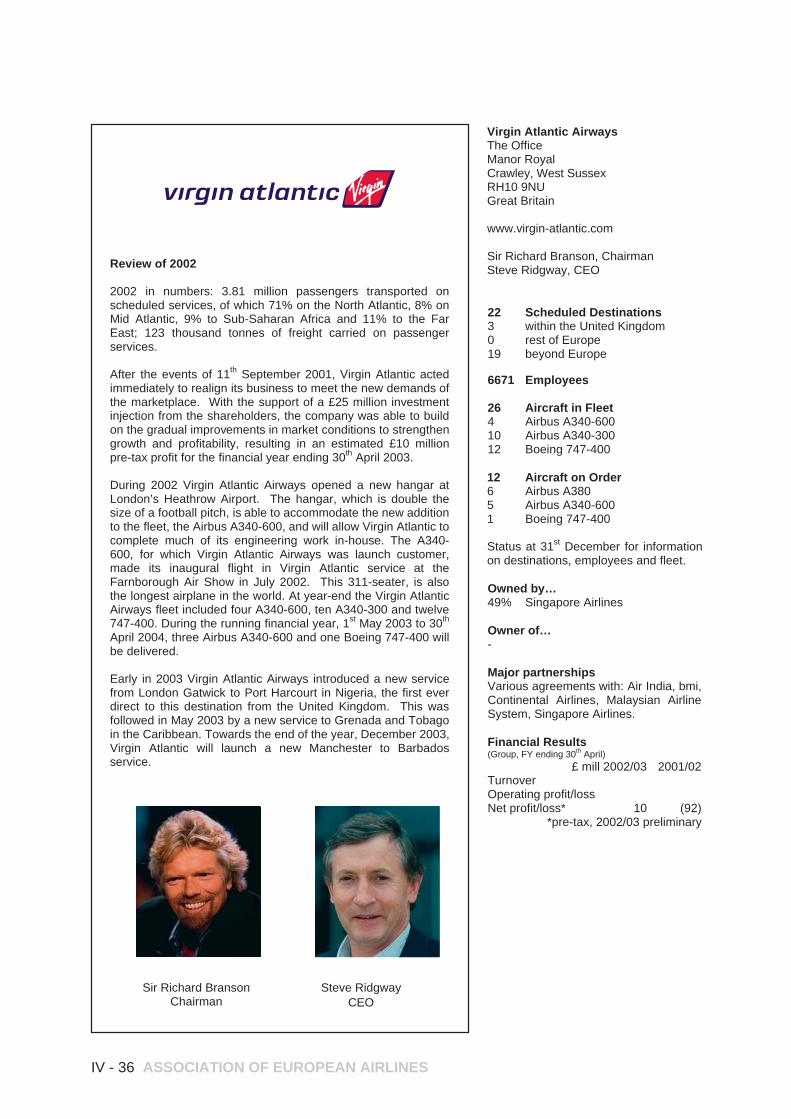

WELCOME TO VIRGIN ATLANTIC AIRWAYS

I – 4 ASSOCIATION OF EUROPEAN AIRLINES

AEA gained its newest member on July1st 2003, with Virgin Atlantic Airwaysformally joining the Association.

Virgin’s membership application wasunanimously approved by the AEA Presidents’Assembly held in Brussels in May.

Virgin Atlantic began operations in 1984with a single aircraft on a single route(Gatwick-Newark). From the outset, ithas been seen as a pacesetter, with astrong public image combining both valueand service elements – in the words offounder Sir Richard Branson, “a brandname that is known internationally forinnovation, quality and a sense of fun”.On early flights, performers were offeredfree passage if they would entertain theirfellow-passengers en route.

From these modest beginnings, VirginAtlantic has grown into a major globalplayer. Its exclusively long-haul networklinks London (Heathrow and Gatwick)and Manchester with nine USdestinations, five in the Caribbean, four inWest and South Africa and four in Asia.

In 2002 passenger-kilometre terms, the airlineranked seventh among AEA airlines overall,fifth in long-haul and fourth across the NorthAtlantic. The passenger count for the yearexceeded 3.8 million.

The fleet, amongst the youngest in theindustry, consists of twelve Boeing 747sand 14 Airbus A340s. These latterinclude four dash-600 models – thelongest civil aircraft in existence – forwhich Virgin was the launch customer.

In December 1999, Singapore Airlinesacquired a 49% stake in Virgin Atlantic.The two airlines cooperate on theLondon-Singapore route and offerreciprocal frequent-flyer and loungebenefits. Virgin also has commercialagreements with other airlines, includingContinental, Malaysian and bmi.

Virgin Atlantic is part of the highly diversifiedVirgin Holdings group (retailing, publishing,financial services, telecommunications…).The group also includes low-fare airlinebrands in Europe (Virgin Express) andAustralia (Virgin Blue).

THE GLOBAL ECONOMIC ENVIRONMENT

ASSOCIATION OF EUROPEAN AIRLINES I – 5

While 9/11, the Iraq War and SARS havedominated the airline-related headlines since2001, it should not be overlooked that duringthis time the industry has been strugglingthrough a serious economic downturn – adownturn, indeed, not unconnected withthese events.

The global economic slowdown of 2001-3has been the most severe since the USeconomy slumped in 1991, followed byEurope two years later. This timearound, US and European economieshave weakened more or lesssimultaneously.

The slump in the US economy, from aGDP growth of close to 4% in 2000 tojust above zero in 2001, was followed in2002 by a partial recovery to 2.5%.

In Europe, the drop in 2001 was less severe,but worsened again in 2002 and is projectedto mount only the weakest of recoveries in2003. The three-year compound growth inthe EU economy from 2000 to 2003, isexpected to total 3.9% – equivalent to oneyear of strong increase.

The European airlines’ second-largestoverseas market, Japan, has under-performed both the EU and the US withclose-to-zero growth in both 2001 and2002. Japan has in fact suffered anextended period of depression, havingposted only two GDP increases in excessof 2% (and one decrease) in elevenyears.

Sustained powerful increases in theChinese economy, pushing thepassenger market into a position where itchallenges Japan in importance for AEAairlines, have come to an abrupt end in2003 with the devastating impact ofSARS.

Within the EU, the largest nationaleconomy, Germany, has also been themost depressed, with GDP growth of only0.2% in 2002 and a projected 0.4% in2003. Fourth-place Italy and sixth-placeNetherlands have been scarcely anystronger.

-2

-1

0

1

2

3

4

5

6

7% growth in real GDP

04E03E200220001998199619941992199019881986

Japan

USA

EU

REAL GDP GROWTH RATES

Source: OECD Economic Outlook n.73

AEA_YB_03_05

Germany

United Kingdom

France

Italy

Spain

Netherlands

Belgium

Sweden

Austria

Denmark

Finland

Portugal

Ireland

Greece

Luxembourg

2108

1661

1521

1258

694

444

261

256

217

183

140

129

115

99

19

EU15

0.2

1.8

1.2

0.4

2.0

0.3

0.7

1.9

1.0

1.6

1.6

0.5

6.0

4.0

0.4

1.0

0.4

2.2

1.1

1.0

2.0

0.5

1.2

1.4

1.2

1.5

2.2

0.5

3.3

3.6

1.1

1.2

Size of Economy2002 GDP levels

€ bn

GDP growth rate1995 prices

2002 2003

Source: EUROSTAT

AEA_YB_03_06

I – 6 ASSOCIATION OF EUROPEAN AIRLINES

The other major European economies – UK,France and Spain – are experiencing 2002/3growth at or above the EU average, but stillwell below levels commensurate with ahealthy momentum.

A number of specific macro-economicfactors have impacted the marketsituation. The stock-market slump whichbegan in 2000 has affected consumerwealth and confidence – more so than inthe past, since many more individuals areaffected, if not directly, then indirectlythrough their involvement in pensionfunds.

The USA in 2002 experienced the virtuallyunheard-of phenomenon of tumbling stockprices during an economic recovery, possiblymitigating the beneficial effect on traveldemand of an improving economy.

Government monetary policy to counteractthe weak economy has included historicallylow interest rates, to boost householdspending and encourage businessinvestment.

Nevertheless, investment in business inOECD countries decreased by 4.25% in2002, on top of a -2.25% in 2001 – amuch larger decline than in recentrecessions. As well as the falling shareprices, other factors have included afocus on reducing debt burden andgenerating cash and – not insignificantly– avoiding the legal and reputation riskstriggered by a series of well-publicisedcorporate governance scandals.

Full recovery for the OECD economies isforeseen to begin around the end of 2003or early 2004. However, this scenario isdependent on a pick-up in investment, forwhich the situation of depressedbusiness confidence in early 2003 wasnot an encouraging pointer.

Finally, the recovery in Europe could behampered by the appreciation of theEuro, which began in the last quarter of2002, slowing down the growth ofEuropean exports and reducing the valueof profits earned abroad – as well,evidently, as making Europe a moreexpensive destination for US and othertravellers.

50

100

150

200

250

300

350 index (1995 = 100)

200220012000199919981997199619951994

EURO area

USA

SHARE PRICE INDEX

Source: OECD Main Economic Indicators - Dow Jones EURO STOXX Broad, NYSEAEA_YB_03_07

-3.0-2.5-2.0-1.5-1.0-0.50.00.51.01.52.02.53.0 index of confidence

200220001998199619941992199019881986

EURO area

USA

BUSINESS EXPECTATIONS

Source: OECD Main Economic Indicators - normalised series in units of standard deviationAEA_YB_03_09

0

2

4

6

8

10

12

14

16

18% interest rate

2000199519901985198019751970196519601955

US FEDERAL FUND RATE

Source: Federal ReserveAEA_YB_03_08

TRAFFIC DEVELOPMENT 2002

ASSOCIATION OF EUROPEAN AIRLINES I – 7

Total scheduled traffic on AEA carriersdeclined by 4.8% in 2002. For the firsteight months of the year, comparisonwas with the pre-9/11 situation and thedecrease was 10%, with no significantevidence of a diminution of the traffic lossfrom one month to the next.

In the last three months of the year,traffic increased 12%, which representeda recapture of only about 45% of the losttraffic in the previous year. By the end ofthe year ‘real’ traffic losses (measuredagainst a year 2000 baseline) werebeginning to diminish.

Making up the total picture weresubstantial regional variations, althoughall route groups reported minuses in Jan-Aug and plusses in Oct-Dec.

On the North Atlantic, hardest-hit after 9/11,Jan-Aug traffic was down 18.2%. Growth inthe final quarter was 21.1% but the total forthe year was 8.7% lower than in 2001.

Within Europe, the corresponding figureswere: before September -9.6%, afterSeptember +7.9%, overall -3.7%.

Of the main traffic flows, Europe-Far Eastsuffered the least: before -5.0%, after+15.8%, overall -1.0%. The traffic growth in

the final quarter represented a better than fullrecovery of the previous year’s lost traffic.

Among the lower-volume markets for theAEA carriers, two figures stood out:Europe-Sub Saharan Africa was the onlyroute group to record a plus for the year,at +2.6%. The South Atlantic result ofminus 13.0% probably owed more to theeconomic crisis in Argentina than to post-9/11 effects.

A positive aspect in 2002 was that, in overallterms, the airlines succeeded in tailoringcapacity to the much-weakened demand andload factors did not suffer; in fact they weregenerally higher than in 2001.

Total Scheduled seat-km for the year werereduced by 8.7%, resulting in a three-pointimprovement in load factor, to 73.6%, whichwas actually the highest on record.

North Atlantic capacity was down 15.2% forthe year, with a reduction in the Summerschedule of about 21%. Consequently, loadfactors were high, reaching 80.0% for theyear and surpassing the previous high pointof 78.4% in 1997.

In Europe, capacity was reduced by7.1%, and the load factor of 64.7%equalled the previous highest.

-20% RPK growth -15 -10 -5 0 5 10

-20

-15

-10

-5

0

5

10% ASK growth

2002 RPK VS ASK % GROWTH BY REGION

Source: AEA

AEA_YB_03_10

South Atlantic North Atlantic

Eur-North Africa

Eur-Middle East

Total Europe

Mid Atlantic

Eur- Far East & Australasia

Eur-Sub Saharan Africa

Load Factor improved

Load Factor deteriorated

‘NO-FRILLS’ CARRIERS

I – 8 ASSOCIATION OF EUROPEAN AIRLINES

2002, and early 2003, has been aperiod of substantial development in theindustry sector variously labelled ‘no-frills’, ‘low-cost’ or ‘low-fare.

Successive AEA Yearbooks havetracked the progress of this sector sincethe mid-1990s, when it comprised onlyRyanair and Virgin Express, shortlyjoined by Easyjet.

Since that time, the number of playershas increased. While no definition of a‘no-frills’ carrier exists, it was commonlyaccepted that by 2002 the original threehad been joined by Go, Buzz andbmibaby.

Although all these carriers shared somecharacteristics, all were, equally,substantially different from each other.

Since mid-2002, the sector hasundergone an upheaval of fundamentalproportions. Go and Buzz have beenabsorbed by Easyjet and Ryanairrespectively. KLM subsidiary Transaviahas created a no-frills brand, Basiq Air.

There have been dramaticdevelopments, too, in the Germanmarket. Eurowings, a Lufthansa affiliate,introduced the Germanwings brand witha hub at Cologne. Leisure airline AirBerlin set up a subsidiary, City Shuttle,connecting several German cities withEuropean business destinations.Similarly, Hapag-Lloyd Express hasintroduced services from twin hubs atCologne and Hannover.

Another newcomer to the market, is anew UK airline, MyTravelLite. Alsoscheduled for 2003 introduction are a no-frills subsidiary of the Italian airlineVolare, and possible startups in Franceand Ireland.

SAS have set up a stand-alone low-fareoperation, Snowflake, to mainly leisuredestinations with – unusual for this sector– less than daily frequency.

While the no-frills sector is still dominatedby operations involving UK points, 2003has seen a huge upsurge in serviceswithin Continental Europe, accounting for

0

300

600

900

1 200

1 500 seats (000)

Snowflake MyTravelLiteAir Berlin CS Basiq AirGermanwings Hapag-Ll. Expbmibaby BuzzGo DebonairEasyjet Virgin ExpRyanair

200320022001200019991998199719961995

"NO-FRILLS" WEEKLY SEATS - SUMMER SCHEDULE

Source: OAG; Airline websites

AEA_YB_03_11

ASSOCIATION OF EUROPEAN AIRLINES I – 9

28.7% of seats offered, compared with13.6% in 2002.

The German market climbed fromseventh to second in importance, with amore than five-fold increase in capacity.The number of seats on offer more thandoubled in the Italian and Netherlandsmarkets.

As regards airports, the two Londonsatellites of Stansted and Luton aredominant with, between them, more than20% of capacity in this sector. Both arehubs for major players, but alsodestination airports for many of the newMainland Europe start-up carriers.

Cologne, with two resident carriers, hasthe next largest share. Subsequentairports ranked by no-frills capacity aregenerally major hubs or larger regionalairports. Of the remote airports whichare supposed to typify this sector,Frankfurt-Hahn, Milan-Bergamo andBrussels-Charleroi (all Ryanair mini-hubs) would rank 12th, 14th and 17th

respectively.

Among airports without a no-frillsresident, the leisure destinations of Nice(served by 7 carriers), Malaga (6) andAlicante (5) are prominent.

within Continental Europe

British Isles-Continental Europe

within British Isles

2003 2002

28.7%

48.2%

23.1%

"NO-FRILLS" WEEKLY SEATS - SUMMER SCHEDULE

13.6%

53.8%

32.6%

Source: OAG; Airline websites

AEA_YB_03_13

Source: OAG; Airline websites

AEA_YB_03_12

London-Stansted 482 AB HV U2 4U FR

London-Luton 134 U2 X3 FR

Cologne 118 4U X3

Dublin 112 WW FR SK

Amsterdam 112 HV WW U2 VZ TV

Belfast 79 WW U2 VZ

London-Gatwick 77 U2 FR

East Midlands 76 WW U2,

Edinburgh 70 WW U2 4U FR

Nice 70 HV WW U2 X3 SK TV

Liverpool 65 U2 FR

Frankfurt-Hahn 64 FR

Barcelona 64 AB HV WW U2 4U VZ SK TV

Milan-Bergamo 61 AB HV WW X3 FR

Brussels 59 WW TV

Malaga 57 HV WW U2 VZ SK TV

Brussels-Charleroi 48 FR

Glasgow 47 WW U2

Alicante 45 HV WW U2 VZ SK

Rome-Ciampino 44 AB U2 X3 FR

TOP 20 AIRPORTS SERVICED BY THE "NO-FRILLS"WEEKLY SEATS (000)

4U - Germanwings, AB - Air Berlin, FR - Ryanair HV- Basiq Air,SK - Snowflake, TV - Virgin Express, U2 - easyJet, VZ - MyTravelLiteX3 - Hapag-Lloyd Express, WW- bmibaby

SPOTLIGHT ON THE NORTH ATLANTIC

I – 10 ASSOCIATION OF EUROPEAN AIRLINES

In 2000, the North Atlantic marketgenerated for AEA carriers 29.3% of totalpassenger-km and US$ 11.3 billion inrevenue. By 2002 these figures hadfallen to 27.8% and $9.1bn respectively.

Throughout the 1990s, the market wasexhibiting very high growth rates. In theeight years 1993-2000, the average year-on-year increase for AEA carriers was8.5%. In the last three years of thisperiod, it was even higher, at 9.4%.

In this context, the dramatic downturn inthe North Atlantic market for AEA carriersis all the more remarkable. 2002 totalpassenger traffic was at about the samelevel as in the 12 months to September1998 – in other words, four and a quarteryears of market growth had been lost.

Since the beginning of 2003, the markethas again been fluctuating strongly. InJanuary, double-digit growth wasrecorded, in effect recovering about halfthe previous year’s lost traffic, butthereafter conditions weakened greatly inthe countdown to the Iraq conflict.

A traffic loss was posted in nine of thetwelve weeks from mid-March. Thisperiod of depression was undoubtedlyextended by SARS concerns, bothspecifically related to Canadian traveland a more general disinclination to fly.

The accompanying graph shows trendsin the Europe/US market before and afterSeptember 2001. Clearly evident is thedecrease in the market prior to 9/11.

Immediately after 9/11 high-yield trafficposted the largest decreases, althoughultimately it was economy-class travelwhich suffered the greatest decline. Itwas very evident, however, that the nextmarket shock, in the shape of the 2003

Iraq War, had its immediate impact againon the high-yield traffic.

AEA airlines moved decisively to adjustNorth Atlantic capacity to the new marketconditions in 2002. In each of the twelvemonths, load factor improved andreached a record 80.0% for the year.

In the 2002 Summer schedule, AEAcarriers reduced their Europe-USoperations by 19.3%, from 1289 to 1040weekly roundtrips – the equivalent of 35fewer flights per day in each direction.

In 2002, twenty-one AEA and five otherEuropean airlines contested theEurope/US market with six US carriers.

In sharp contrast to the Europeans, theUS carriers made much smaller capacitycutbacks in 2002. In the peak Summerschedule, their weekly seats were downonly 6.4% and weekly flights -7.8%,compared with around 20% for theEuropean airlines.

Consequently, the US carriers’ share ofthe market increased from 41.8% to46.1% in seats offered and – given theirsmaller average aircraft size – from46.3% to 49.9% in number of flights.

65

70

75

80

85

90

95

100

105

110 index of annualised passenger numbers

200220012000

NORTH ATLANTIC TRAFFIC DEVELOPMENT

Source: AEA

AEA_YB_03_14

Aug 2001

First and Business Class

Economy Class

SPOTLIGHT ON THE FAR EAST

ASSOCIATION OF EUROPEAN AIRLINES I – 11

AEA members’ traffic on Far Eastern routesfell by 17% in the immediate aftermath ofSeptember 11, recovered to about -7% bythe end of 2001 and averaged about -5%through the Summer of 2002.

In the final quarter of 2002, traffic hadalmost returned to 2000 levels, with twoyears of growth lost.

As with other regions, the recovery in FarEastern traffic faltered in early 2003 inanticipation of the Iraq War. From thebeginning of February the market growthevaporated. At the outbreak of war, in lateMarch, the traffic decrease reached 11-12%.

Such figures were, however, totallyovershadowed by the subsequentupheaval in the market caused by theSARS outbreak – impacting not onlyaffected areas as travel destinations, butalso creating uneasiness about in-flighthealth issues.

The issue was fuelled by over-reactionon the part of the World Healthorganisation, compounded by mediahype (‘SARS Sweeps Asia’).

While the incidence of the disease wasconcentrated in four main areas – China,Hong Kong, Singapore and Vietnam,market effects were felt over a muchbroader range of destinations.

For eight straight weeks from mid-April toearly June 2003, AEA carriers’ traffic onFar East/Australia routes recordeddecreases in the range 26-31%. Losses

of this magnitude had been measured onlyonce before in any of the AEA’s majormarkets, when very similar figures wereposted on the North Atlantic inOctober/November 2001.

The phenomenon impacted markets whichhad previously been among the strongestperformers within the AEA members’networks. In particular, China – includingHong Kong – would probably in 2003 haveovertaken Canada and Japan as theAEA’s largest longhaul market after theUSA.

Indicative of the size and importance ofthe China market, AEA member airlineshad scheduled an average of 20 directflights daily in Summer 2003, a 50%increase in just four years.

Many of these flights – and those to otheraffected destinations in the region – weresuspended as the severity of the marketreaction became apparent. However,substantial traffic losses had alreadyoccurred before significant capacity cutscould be realised.

In the early stages of the outbreak, loadfactor on all Eastern routes plummettedto just above 60%, and two months intothe crisis had recovered only to about70%, compared to near-80% levels whichwould normally have been anticipated.-80% passenger movements

-70

-60

-50

-40

-30

-20

-10

0

TRAFFIC LOSSES AT SELECTEDASIAN AIRPORTS (APR-03/APR-02)

Source: ACI/Centre for Asia Pacific Aviation

AEA_YB_03_15

HONG

KONG

TAIPEI

JAKARTA

SINGAPORE

SEOUL

BANGKOK

BEIJING

TOKYO

OPERATING RESULTS 2002

Note:Data in this section are aggregated frommembers’ financial year results and maydiffer slightly from the calendar yearfigures elsewhere in the document. Loadfactors refer to passenger and freightcapacity utilisation. Figures refer to totalscheduled services, including Domestic.

AEA airlines suffered their fourthsuccessive annual loss in 2002. Figurespoint to an operating loss, after interest,of US$870 million, following the worst-ever $3.02 billion deficit in 2001.

This represented an improvement inoperating ratio (revenue:expenditure)from 95.4 to 98.6

As might be expected, most AEAmember airlines improved their operatingratio from 2001 to 2002.

The main source of improvement wasamong the mid-size carriers; the group ofsmaller airlines provided the onlyexamples of worsening results, while thelarger carriers in general experiencedless variability.

The main contributor to the operatingratio improvement was the increase inload factor, by 3.6 percentage points to68.5%.

A yield increase (in current US$) of 6.9%was matched by a similar increase in unitcosts, giving a more or less neutralcost/revenue development effect.

The net interest burden, which added2.5% to operating expenses, was higherthan in 2001 and made a small negativecontribution to the change between thetwo years.

70

80 90 100 110 12070

80

90

100

110

120 Operating Ratio*

70

80 90 100 110 12070

80

90

100

110

120

TOTAL SCHEDULED OPERATING RATIOS* BY CARRIER

Source: AEA

AEA_YB_03_17

7 large

9 medium

12 small

2 0 0 1

2002

Operating Ratio deteriorated

Operating Ratio improved

(*) after interest

Operating Ratio after interest

2001 2002

95.4 98.6

Points change in OR as a result of:

Change in Load Factor +3.6

+0.1

-0.3

+3.2

Cost vs Revenue Development

Change in net interest

Total Change

Source: AEA

AEA_YB_03_16

I – 12 ASSOCIATION OF EUROPEAN AIRLINES

Following a very difficult 2001, quarterlyresults for 2002 returned to a ‘normal’profile with profitable operations duringthe two Summer quarters offset by lossesat the beginning and end of the year.

Comparing 2002 with 2000 in the graphbelow, any benefits realised by the relativelymodest losses in the first quarter – whichrepresented a substantial turnaroundfollowing the catastrophic impact of 9/11 –were lost in a poor fourth quarter.

The load factor required to break even –which is in fact the simple relationshipbetween yields and unit costs – was69.4% in 2002, a level which has beenvirtually unchanged for three years. Allthree of these annual figures have beenabove the highest ever AEA annual loadfactor – 69.2%, achieved in 1997 andagain in 2000.

This highlights an essential structuraldilemma in the industry. It is almostinconceivable that further load factorimprovements can be squeezed out –certainly not sufficient to surpass breakevensof around 70% by an adequate margin.

Therefore, the breakevens themselvesmust be brought down. This can be donein one of only two ways – increase yields,or reduce costs. The yield solution wouldinvolve reversing the steady downwardtrend which is a characteristic of themodern-day industry.

Reducing costs is, of course, a priority inthe industry and had been so for manyyears. And so the dilemma becomesmore acute, since a cost saved alreadycan not be saved a second time.

85

90

95

100

105

110 operating ratio

Q4Q3Q2Q1Q4Q3Q2Q1Q4Q3Q2Q1

OPERATING RATIO AFTER INTEREST

2000 2001 2002Source: AEA

AEA_YB_03_19

60

62

64

66

68

70% load factor

200119991997199519931991

TOTAL SCHEDULED OVERALL VS BREAK-EVEN L/F

Source: AEA

AEA_YB_03_18

Break even load factor (after interest)

Overall load factor

ASSOCIATION OF EUROPEAN AIRLINES I – 13

PUNCTUALITY PERFORMANCE

I – 14 ASSOCIATION OF EUROPEAN AIRLINES

2002 saw a reduction in delay rate for AEAmembers. Within Europe, 19.9% ofdepartures were delayed more than 15minutes, down from 24.2% in 2001. The2002 figure was the lowest for five years, butstill very far from the levels around 13% whichprevailed as recently as 1993-94.

A major contributory factor was thereduction in flights in 2002. By the end ofthe year, however, a slight growth intraffic had been resumed, accompaniedby a deterioration in the delay trend.

Eurocontrol’s own figures bear out the AEA’sexperience. For ten months of the year, ‘slot’delay imposed by their Central FlowManagement Unit was down on 2001, butincreased in the last two months of the year,coincidental with a resumption of growth in thenumber of flights through European airspace.

The system is still close to saturationdespite the ‘breathing space’ created bythe drop in airspace utilisation.

Another ‘breathing space’ was achievedearly in 2002 by the introduction ofReduced Vertical Separation Minima inEuropean upper airspace. From 29,000

feet upwards, new flight levels werecreated at 1,000-feet intervals, replacingthe former 2,000-feet spacing.

The change was made possible by muchgreater accuracy in onboard altitude-measuring equipment and substantiallyincreased the capacity of upper airspace.

The Eurocontrol delay figures attribute asubstantial proportion of the slot delay toproblems with the UK system. Normally, nosingle part of Europe’s fragmented systemwill contribute more than 20% of total annualdelay. In 2002, the UK was responsible for36.5% of the total – up from 13.9% in 2001.

Next, in order, were France (13.0%),Germany (9.4%) and Italy andSwitzerland (both 8.4%).

AEA measures departure delay at airports,although the airports themselves are notnecessarily the source of the delay. In 2002,the most frequent delays to AEA airlines wereexperienced at Madrid, with just over 30% ofmembers’ flights more than 15 minutes late.Other airports with delays substantially abovethe average included Dublin, Rome, LondonGatwick and Paris CDG.

500

550

600

650

700

750

800 flights (000) - CFMU

20022001200019991998

EUROPEAN FLIGHT & PUNCTUALITY TRENDS

Source: AEA; EUROCONTROL/CODA

AEA_YB_03_20

10

15

20

25

30

35

40% flights delayed > 15 minutes (AEA)

Restructuring of airspaceover France and Switzerland

Introduction ofRVSMKosovo crisis September 11th Gulf War II

Total flights (CFMU)%flights delayed > 15 mins

ASSOCIATION OF EUROPEAN AIRLINES II - 1

CONTENTS

SECTION I AEA AIRLINES IN 2002 I-1

At a Glance I-2Welcome to Virgin Atlantic Airways I-4 The Global Economic Environment I-5

Traffic Development 2002 I-7 ‘No-frills’ carriers l-8

Spotlight on the North Atlantic I-10 Spotlight on the Far East I-11 Operating Results 2002 I-12

Punctuality Performance I-14

SECTION II OUTLOOK FOR 2003 II-1 The Story so Far.. II-2 Traffic Development II-3

Operating Results II-4

SECTION III LOOKING FORWARD III-1 Towards an Efficient European Air Transport System III-2

Are Air Transport Networks Sustainable? III-4 Improving the Industry’s Regulatory Framework III-5

The Dynamics of the Value Chain III-6 A transatlantic Open Aviation Area ? III-7 Bilateral Agreements – Where now ? III-8

Denied Boarding Compensation III-9 External Shocks – Security and Insurance III-10

SECTION IV SPOTLIGHT ON THE AEA IV-1

AEA Highlights IV-3 Airline Profiles & Review of 2002 IV-6

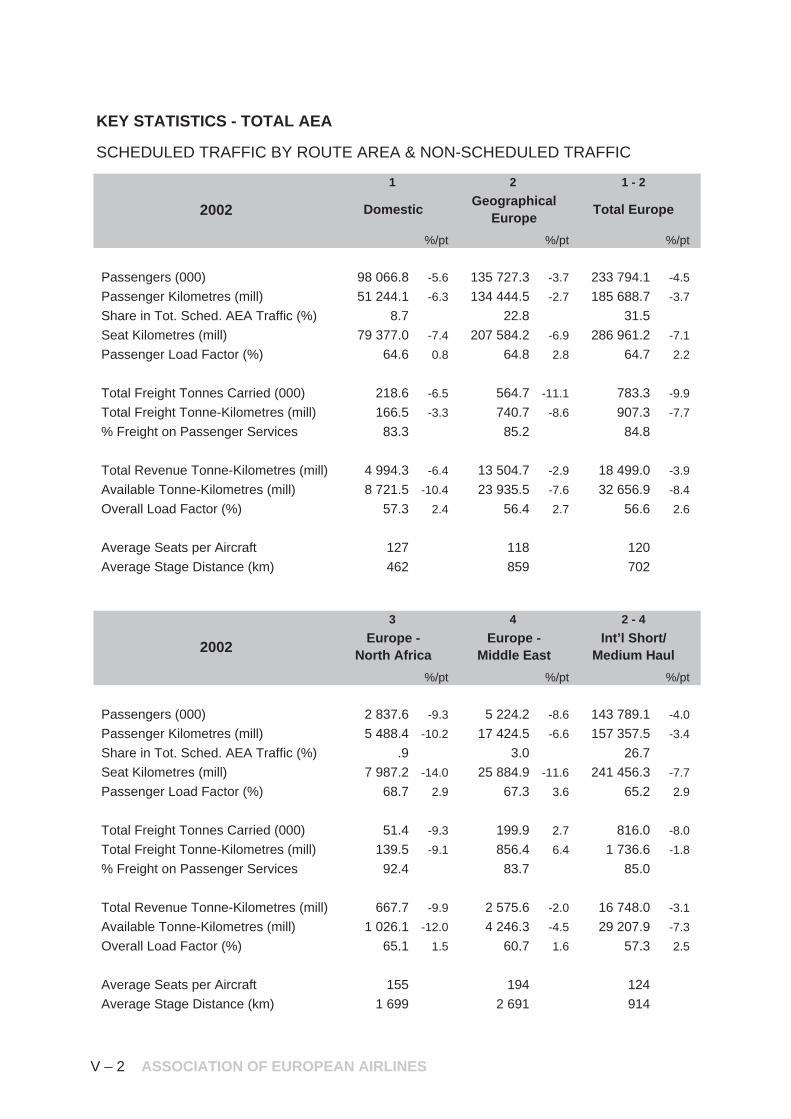

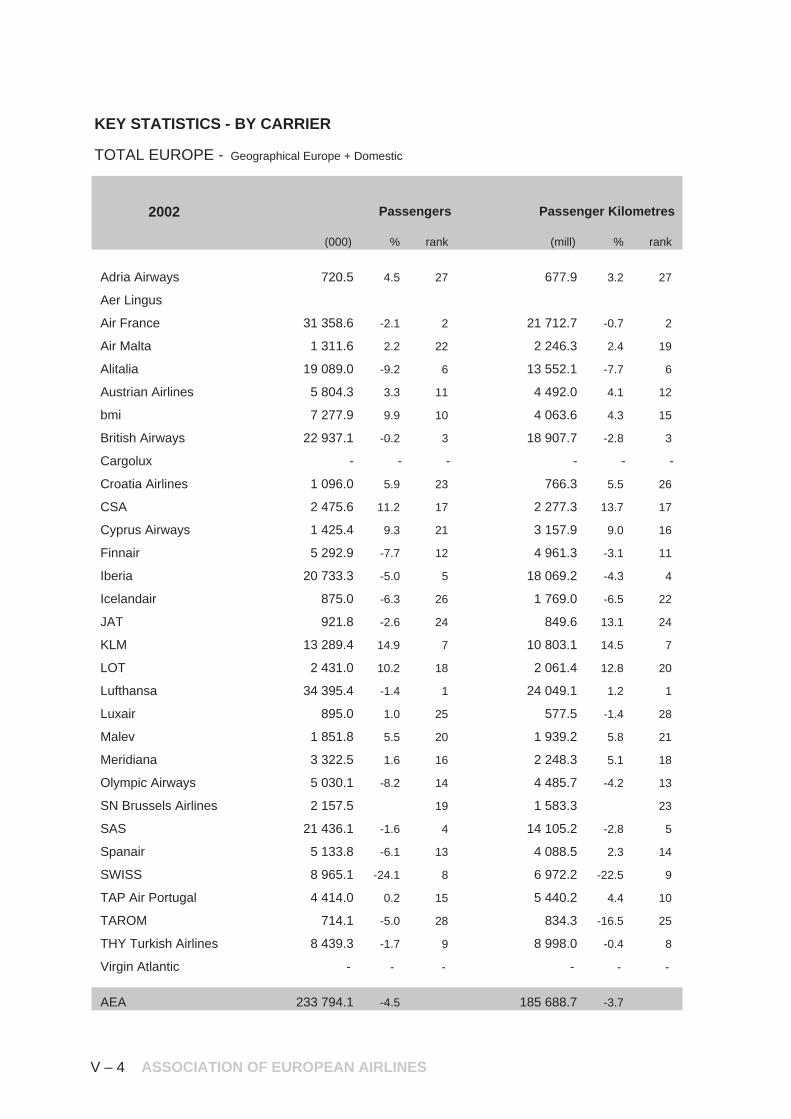

SECTION V KEY STATISTICS V-1 Key Statistics - Total AEA V-2 Key Statistics - By Carrier V-4

AEA Fast Facts V-11 What do we mean by…? V-12

II – 2 ASSOCIATION OF EUROPEAN AIRLINES

THE STORY SO FAR…

The Iraq War effect in weeks 11-13 hadscarcely begun to moderate before themarket was hit by another huge shock asSARS caused the market to plummet tominus 30% - a level at which it wasanchored for eight weeks.

Traffic between Europe and the MiddleEast, weakening since the start of theyear in anticipation of the start of the IraqWar, collapsed to less than half 2002levels before recovering to about minus10% shortly after direct hostilities ceased.

-60% change in RPKs

-50

-40

-30

-20

-10

0

W20W18W16W14W12W10

2003 WEEKLY TRAFFIC EUROPE-MIDDLE EAST

Source: AEA

AEA_YB_03_21

Beginning of Gulf War II20-Mar-03

End of "hostilities"14-Apr-03

-35

-30

-25

-20

-15

-10

-5

0

5

10% change in RPKs

W25W20W15W10W05

2003 WEEKLY TRAFFICEUROPE-FAR EAST AUSTRALASIA

Source: AEA

AEA_YB_03_22

SARS virus first recognisedend Feb-03

"Disease contained"05-Jul-03

-1.1 to -2.4 bn US$ Financial Result*Total Scheduled (-1.0 to -2.1 € bn)

+2% growth in Passenger Traffic*Total Scheduled RPKs

(*) estimates for 2003

TRAFFIC DEVELOPMENT 2003

ASSOCIATION OF EUROPEAN AIRLINES II – 3

The year 2003 began with traffic growthin all major AEA markets – as might havebeen anticipated, given the severelydepressed situation at the beginning of2002, just 16 weeks after the attacks ofSeptember 11.

Regions most hard-hit after 9/11 – theNorth Atlantic and the Middle East –were,evidently those in which nominal growthwas strongest, both posting double-digitincreases in January 2003.

The situation was not to last long. By theend of January the markets hadweakened and by mid-February intra-Europe, the Middle East and the Far Eastwere again in decline.

The most obvious cause of this instabilitywas the well-signposted preparation forthe Iraq conflict. Even before hostilitiescommenced on 20th March, all the AEA’smajor markets had gone into reverse withthe Middle East recording decreases inexcess of 20%.

The immediate impact of the war was tocause traffic decreases of about 50% onMiddle Eastern routes, about 10% inEurope and to the Far East, and about5% on the North Atlantic – all of thesefigures, of course, applying to underlyingtrends which themselves were distortedby post-9/11 effects.

The duration of the war-related effect isdifficult, if not impossible, to determine,since another and potentially moredamaging phenomenon intervened –SARS – with consequences for the FarEastern market becoming visible in thethird week of the War.

By the beginning of June, the MiddleEastern market had returned to growth,eliminating the last indication of Iraq War

effect, eleven weeks on from thecommencement of hostilities. There was,however, no sign of a diminution of theSARS effect on Far Eastern routes,which had resulted in an eight-weeksequence of traffic losses in the range27-30%.

For the remainder of 2003 the marketsare expected to return to growth,although in the case of Far Easternroutes this may not materialise until thefourth quarter.

Strongest increases are expected on theNorth Atlantic, although evidently this is afunction of the depth of the 2002 lossesrather than any inherent buoyancy in themarket.

For the year as a whole, an overall trafficincrease of just under 2% is foreseen.Had it not been for the Gulf War andSARS effect, the increase would havebeen in the order of 7% – in other words,these events cost the industry almostthree-quarters of its projected growth thisyear.

450

500

550

600

650

700

750 billion RPKs (12 month moving total)

2004200320022001200019991998

AEA TOTAL SCHEDULED RPKs

Source: AEA

AEA_YB_03_23

NO September 11th

NO Gulf War II/SARS

Actual + Outlook

OPERATING RESULTS – OUTLOOK FOR 2003

The AEA airlines’ market environment in2003 has confounded any earlierpredictions made in the context of a post9/11 recovery phase.

Given the ongoing traffic losses of 2002, theoperating result of -$870m, was no worsethan might have been anticipated. With trafficpicking up at the end of the year and loadfactors still high, a reasonable recovery wasin prospect for 2003.

While certain cost items – notably securityand insurance – had spiralled upwards, fuelwas relatively cheap. Crisis-related cost-cutting programmes were also widely inplace. Question-marks remained, however,over the recovery in premium traffic andthe effect on yields of substantially increasedno-frills competition in Europe.

While AEA has made no projectionsbased on this scenario, it mightreasonably be assumed that a positiveresult for 2003 in the region of $1bnmight have been foreseen.

By the start of 2003, however, the industrywas already making projections for the yearbased on the impact of the anticipatedsecond Iraq War, including substantial traffic

losses, fuel price increases, and possiblefurther impacts in security and insurance.

While the war impacts contained nomajor surprises for the airlines, they weretotally unprepared for the subsequentdevastating effect on their traffic –particularly in the vital Far Easternmarket – of the SARS phenomenon.

While a small traffic increase for the yearis anticipated – much lower than whatshould have been achieved in a recoveryyear, it will almost certainly fall below thelevel of capacity increase, leading to adrop in load factor.

The indications are that 2003 yields will bedepressed, in the range 4.5% - 7%. This willprobably be mitigated by a correspondingdrop in unit costs as ongoing cost-cuttingprogrammes contribute their effect.

As for the outcome, a range ofpossibilities is foreseen, with the mostfavourable already slightly worse than the2002 outcome at minus $1.1bn, and thisloss more than doubled in the worst-casescenario. For the AEA airlines as awhole, a fifth consecutive year of lossesis in prospect.

-3.0

-2.5

-2.0

-1.5

-1.0

-0.5

0.0

0.5

1.0

1.5

2.0

2.5 billion current US$ after interest

03E02010099989796959493929190

OPERATING PROFIT / LOSS TOTAL SCHEDULED ROUTES

-1.1 billion US$

-2.4 billion US$

possible outcome

Source: AEA

AEA_YB_03_24

II – 4 ASSOCIATION OF EUROPEAN AIRLINES

ASSOCIATION OF EUROPEAN AIRLINES III - 1

CONTENTS

SECTION I AEA AIRLINES IN 2002 I-1

At a Glance I-2Welcome to Virgin Atlantic Airways I-4 The Global Economic Environment I-5

Traffic Development 2002 I-7 ‘No-frills’ carriers l-8

Spotlight on the North Atlantic I-10 Spotlight on the Far East I-11 Operating Results 2002 I-12

Punctuality Performance I-14

SECTION II OUTLOOK FOR 2003 II-1 The Story so Far.. II-2 Traffic Development II-3

Operating Results II-4

SECTION III LOOKING FORWARD III-1 Towards an Efficient European Air Transport System III-2

Are Air Transport Networks Sustainable? III-4 Improving the Industry’s Regulatory Framework III-5

The Dynamics of the Value Chain III-6 A transatlantic Open Aviation Area ? III-7 Bilateral Agreements – Where now ? III-8

Denied Boarding Compensation III-9 External Shocks – Security and Insurance III-10

SECTION IV SPOTLIGHT ON THE AEA IV-1

AEA Highlights IV-3 Airline Profiles & Review of 2002 IV-6

SECTION V KEY STATISTICS V-1 Key Statistics - Total AEA V-2 Key Statistics - By Carrier V-4

AEA Fast Facts V-11 What do we mean by…? V-12

TOWARDS AN EFFICIENT EUROPEAN AIR TRANSPORT SYSTEM

Around the world, airlines are in trouble. In the USA, the world’s five largest airlineshave had to face the very real threat of bankruptcy – two have already been operatingunder protection from their creditors. In Europe, the members of the AEA havecollectively lost US $ 8.5 billion in the last thirteen years.

The AEA has commissioned a far-reaching study into the structure – and the structuraldeficiencies – of the European air transport industry. This study – entitled ‘Towardsan Efficient European Air Transport System’ – provides AEA airlines with a frameworkwithin which they can analyse their strengths and weaknesses and identify policyareas which need to be addressed if the sector is to avoid following its US counterpartto the brink of life-threatening crisis.

WHY ARE AIR TRANSPORT NETWORKS IMPORTANT?

III – 2 ASSOCIATION OF EUROPEAN AIRLINES

Essential components of the modernworld are Communication and Mobility.Mobile phones … laptop and palm-topcomputers … the internet … ten ortwelve years ago, the world functionedwithout them; today it could not. Mass-market air transport has been around forrather longer, and as such is an evenmore essential facilitator ofcommunication and mobility.

Efficient, affordable air transport hasbecome commonplace, so much so thatit is taken for granted that, for everyjourney requirement, a convenientsolution exists. This is because themajor airlines function as Networks.

How do networks function?

Just as, on the London Underground orthe Paris Metro, you can get from anystation to any other station with a singlechange – at a single fare, on a singleticket – if you are connected to an airline‘hub’, you are interconnected to everydestination served from that hub.

Why are networks so important?Consider: after a long haul fromAustralia, the Far East, North or SouthAmerica, virtually every city in Europe isjust a short connecting flight away.

Europe’s regions become every bit asmuch a part of the ‘Global Village’ as thecapital cities and great conurbations.

Airline networks – passenger and cargo –are essential for world trade. Companiesengaged in globalised production anddistribution need to be in easy reach ofboth their suppliers and their customers.

Consider also the effect of airlinenetworks on the cohesion of the SingleMarket. A business, located almostanywhere in Europe, is one connection

5 AIRCRAFT

A B

C D

E F

G H

I J

5 ROUTES

5 AIRCRAFT

AB

CD

EJ

I

HG

F

55 CONNECTIONS

2 NETWORKS/ALLIANCES

210 CONNECTIONS

EFFICIENCIESOF NETWORKS

Source: AEA

AEA_YB_03_25

ASSOCIATION OF EUROPEAN AIRLINES III – 3

away from a customer located almostanywhere else. This is especiallyimportant for the peripheral regions: inmany countries in Europe the nationalairline is a major contributor to theeconomy and the social fabric. Incountries which rely heavily on tourism,their importance is self-evident. In allcountries, they are major employers, bothdirectly and indirectly.

Consider some figures: The thirtymember airlines of the AEA aloneemployed, in 2002, 358,000 employees.It is estimated that every airline jobgenerates between 4 and 10 airport jobs,as well as 3 in the neighbourhood of theairport. For AEA airlines alone thisamounts to employment for about 4-5million people. Add to this the tourismindustry in Europe which generatesreceipts amounting to 700 million € perday, and the aircraft and enginemanufacturing industry.

To take just a single one of thosemember airlines as an example, Air Maltais estimated to generate 7.6% of thenational GDP.

It is not an exaggeration to say that,without the airline networks, the SingleMarket simply could not function.

What other benefits do networksbring?

In recent years, the major Europeanairlines have worked hard to develop aseamless product across their networks.Through ticketing and baggage transferhas always been available, as hasthrough pricing for unrestricted tickets.

To this has been added through fares ateconomy prices, simplified and shortertransfer procedures, and a vastlyincreased range of destinations,sometimes served through partner andaffiliate airlines.

A consequence of this increase in scalehas been that, for the vast majority ofpotential journeys, passengers have achoice of carrier, as several networkscompete for their business.

Connectivity on this scale does nothappen by accident. It is a productfeature which carries a cost – thedistribution cost of offering throughpricing and ticketing, the infrastructurecost of guaranteeing efficient baggagetransfer, the operational cost ofcoordinating schedules, and the costsinvolved in operating a mixed fleet oflarger and smaller aircraft, in larger andsmaller markets.

Air transport is an innovative industry that drives economic and social progress Over 1.6 billion passengers rely every year on the world’s airlines for business and vacation travel and estimates suggest that by 2010, the number of people travelling by air could exceed 2.3 billion. The total economic impact of air transport on gross world output amounts to at least US$1,360 billion –which comprises US$320 billion in direct impact, US$390 billion in indirect impact, and US$650 billion in induced impact. Over 29 million tonnes of freight a year are transported by air, representing 40%, by value, of the world’s manufactured exports. Air transport is one of the fastest growing sectors of the world economy with expansion rates 2.4 times above Gross Domestic Product (GDP) rates on average. Air transport has provided 28 million jobs worldwide –and is expected to provide 31 million by 2010. This includes direct employment of nearly 4 million people,over 8 million who are employed indirectly, and induced employment conservatively estimated at more than 15 million jobs.

Source: AEA

AEA_YB_03_26

ARE AIR TRANSPORT NETWORKS SUSTAINABLE?

III – 4 ASSOCIATION OF EUROPEAN AIRLINES

In recent years, the network airlines havestruggled financially. The increase incompetition which accompaniedEuropean liberalisation in the early 1990scoincided with a period of sustainedeconomic depression for the industrywhich had begun in 1990, continuedthrough the Gulf War of 1991, and did notend until 1995.

In 5 consecutive unprofitable yearsbetween 1990 and 1994, AEA airlineslost an accumulated US $ 10.3bn. In foursubsequent profitable years, to 1998, thenet benefit was just $ 6.0bn.

This was followed by three more leanyears with an accumulated loss of $4.2bn. Even in the good years, it isarguable whether the network airlines, asa group, succeed in recovering their costof capital.

What about non-network airlines?

The last two or three years have seen thephenomenon of the so-called ‘no-frills’ (or‘low-cost’, or ‘low-fare’) carriersexpanding very rapidly, and doing so – atleast in the case of the two largest – withapparently a high degree of profitability.

The no-frills carriers have not wasted anyopportunity to announce the end of anera, so far as the network carriers areconcerned. They represent the future ofthe industry, they say. They havedetermined what the market wants –which is very low fares, and little else,and the market has responded in theirfavour.

They have also raided some of thenetworks’ more important city-pairsegments, further weakening theestablished structure.

How do they affect the networkairlines?

Once again, the focus is on costs.Although the network airlines areenormously more efficient than they werebefore the 1990-1 crisis, they are still at asubstantial seat-cost disadvantagecompared to the no-frills carriers.

The dual questions arise: how muchmore can they strip out of their cost basewhilst preserving the quality of theproduct, and is the quality of the productworth preserving, in that it can commanda premium in the market?

The success of the no-frills carrierssuggests that the market’s expectations,at least for short-haul travel, have movedaway from the product traditionallyoffered by the quality airlines. To remainresponsive to their market, these airlineswill have to re-analyse their businessplans.

One consequence is that carriers mustre-analyse their relationships withsuppliers and service providers. Airlinesspend money in a ‘Value Chain’ whichstretches from manufacturers of aircraftand engines, through infrastructureproviders such as airports and air trafficcontrol services, to marketing anddistribution systems. Airline workforcesare, of course, part of the chain too.

An important consideration in thisprocess is: what kind of living do theairline industry’s ‘dependents’ enjoy, inthe current circumstances?

IMPROVING THE INDUSTRY’S REGULATORY FRAMEWORK

ASSOCIATION OF EUROPEAN AIRLINES III – 5

The European airline industry operatesunder a regulatory regime whereby wehave de facto liberalisation within theSingle Market, yet many other aspects ofthe EU’s regulatory blueprint for airtransport are incomplete, inconsistentand in some cases contradictory.

How are the regulators inconsistent?

Europe’s regulators are frequently to beheard calling for the industry toconsolidate, yet many of their policies aredesigned to hinder consolidation, andpromote a proliferation of small airlines.

Throughout the liberalisation process, theEuropean Commission was very publiclycommitted to achieving low fares, yetairlines continue to face a range ofregulatory measures which eitherincrease their costs, or hamper theirefforts to reduce them.

An obvious consequence of lower faresis increased demand, yet the regulatorshave been very slow to promoteinfrastructure growth in the area of airtraffic control, and have done nothing toencourage an increase in airport capacityin Europe.

Do the regulators recognise theimportance of networks?

EU competition policy, notably as appliedto airline alliances, has consistently failedto grasp the importance of networks andthe need for network carriers to have astrong presence at their hub airports.

Recent developments in EU externalaviation relations, as exemplified by thedecision of the Court of Justice, havebeen cited by the Commission asstrengthening the position of Europeanairlines worldwide, yet have had the

effect of creating uncertainty andinstability throughout the framework ofbilateral aviation agreements on whichthe global air transport structure isfounded.

Regulatory processes within the USA –European airlines’ major external market,and their major external competitors –have always had a clear focus, topromote and support the US networkcarriers. European policy-making has nosuch focus.

Clearly, it is overwhelmingly in theEuropean interest that there is a strongand dynamic airline infrastructure of bothinternal and external networks. Atpresent, the long-term future of thosenetworks are threatened. It must besecured by interdependent measurestaken by governments and airlines; thedilemma can only be resolved bycollective will on both sides.

Source: AEA

AEA_YB_03_27

We are facing a structural crisis...

AEA airlines are adjusting their business models

ATC, airports and other service providers must

also become flexible and cost efficient

We must redefine our business relationships

We need intense dialogue with regulators

...the Road Map to recovery:

THE DYNAMICS OF THE VALUE CHAIN

III – 6 ASSOCIATION OF EUROPEAN AIRLINES

Many industry sectors earn their livingfrom air transport, and available datasuggests that most of them earnsubstantially higher rates of return thanthe airlines themselves.

Who are the winners in the airtransport business?

AEA airlines, which invariably use newequipment, obtain their aircraft eitherdirectly from the manufacturer or fromleasing companies. While these sectorsalso have good and bad years, onaverage they achieve returns of about15-16%, well above their cost of capital.

Airports, too, can be prosperousbusinesses. In many countries whereairports are in public ownership, profitsfrom major airports are sufficient tosubsidise those serving small and remotecommunities.

Where airports are privatised, profitmargins are often far higher than those ofthe airlines who serve them. The sameis true for other support servicesoperating at airports, such as ground-handling companies and aircraft caterers.

Probably the largest profits in the valuechain are earned by the computerreservations systems (CRSs), which areable to earn margins of 30% or more.

One link in the chain which is not profit-oriented is Air Traffic Control (ATC). Itdoes not need to be, since, in Europe, itoperates on a cost-recovery basisadministered by Eurocontrol. In otherwords, whatever is spent, on facilities,equipment, staff and running costs ispassed directly to the airlines throughuser charges.

Why do these sectors benefit at theairlines’ expense?

All these elements in the value chainhave a characteristic which sets themapart from the airlines: they are allmonopolies or oligopolies.

Two airframe manufacturers, and threeengine-makers, provide all the Western-built jets of over 100 seats. The twolargest leasing companies have 45% ofthe market.

Very few airports offer a choice of morethan two ground handling and cateringservice providers, while these sectors arealso consolidating on a worldwide scale.Four CRSs provide distribution globally,but in individual local and regionalmarkets, one or other is dominant.

Airports compete with each other only atthe margins of the air travel business.Hub-based networks certainly docompete with each other, but these arethe creation of airlines, not airports.

Insofar as ATC is concerned, it is obviousthat, with airspace divided into country-sized national systems and intopredetermined airway networks, airlineshave little flexibility in choosing theirroutings from departure to destination.

Even sectors not normally connectedwith the mainstream of air transportoperation can find themselves in verystrong bargaining positions vis-à-vis theairlines. Recent experience has shownthat the insurance community can makedemands of the airlines which, if not met,can threaten their continued operation.

A TRANSATLANTIC OPEN AVIATION AREA?

ASSOCIATION OF EUROPEAN AIRLINES III – 7

The early part of 2003 has seen amomentous development in thegeopolitical infrastructure within whichairlines operate.

In June, a decision of the EuropeanCouncil granted to the Commission amandate to negotiate a multilateral airlineservice agreement between theCommunity and the United States, whichwill replace the current structure ofindividual bilateral agreements, somerestrictive, some liberal.

This development was made all the morelikely following the late 2002 decision ofthe European Court of Justice that‘nationality clauses’ in bilateralagreements – inasmuch as they limitedoperations from an EU country to airlinesof that country (and its bilateral partner,evidently) – were inconsistent with single-market rules.

Within the liberalised European aviationarea there is, for practical purposes, nosuch thing as a national airline; all are‘Community Carriers’ and as such haveaccess to the entire market.

One of the earliest manifestations of thenew direction in Europe/US aviationrelations is likely to be an extension ofthis concept to transatlantic routes,permitting any airline from an EU countryto operate to the US from anyCommunity airport.

That is not to say that immediate anddramatic developments can beanticipated. The experience of Europeanliberalisation is that airlines with a strongnational identity have opted toconcentrate their resources in their homemarkets and develop their hub-basednetworks.

A more likely consequence may be thatthe new arrangements remove anobstacle to cross-border investmentbetween airlines in Europe. In recentyears, proposed mergers and otherpartnerships involving financialparticipation have faltered because ofconcerns that an airline losing its‘nationality’ would also lose its trafficrights.

Any agreement between the EU and theUS would, of course, concern itselfchiefly with EU and US airlines. Any fifth-freedom operation by, for example,Middle Eastern or Asian carriers wouldbe closely regulated, as it is today.

The status of EU airlines as CommunityCarriers requires them to be majority-owned by EU nationals – i.e. with nomore than 49% foreign ownership. USrules are much more severe, with anupper limit of 25%.

In the European vision of an OpenAviation Area – shared by the AEA – anultimate development could be theremoval of ownership limits, allowingEuropeans to invest in, or establish, UScarriers – and vice versa.

At a more immediate level, the events ofSeptember 11 and their aftermath havecreated a new landscape in EU-USrelations. Issues such as security,information exchange and privacyprotection, insurance and financialassistance urgently require moreharmonised policies.

All of these areas, along with marketaccess, investment and competitionrules, are essential components of the‘level playing field’ which would benefitairlines – on both sides of the Atlantic –and customers alike.

BILATERAL AGREEMENTS – WHERE NOW?

III – 8 ASSOCIATION OF EUROPEAN AIRLINES

The decision of the European Court ofJustice, that the nationality clausescontained in the ‘Open Skies’ EU-USbilaterals were contrary to European law,had repercussions far beyond the eightagreements under investigation.

Evidently, what is contrary to the law inone case, is contrary in all cases, and allbilateral treaties between EU MemberStates and ‘Third Countries’ – totallingsome 2000 agreements – can beassumed to include restrictive (i.e.discriminatory) nationality provisions.

In other words, the agreeement between,for example, Austria and Australia willrestrict services to airlines which areeither Austrian or Australian.

Remedying such anomalies will not be astraightforward process. While amultilateral approach is seen asappropriate for the huge US market,which is comparable in size to the EU,other country markets are much smaller.Even the next-largest non-EU markets –Japan, Canada and China/Hong Kong –are dwarfed by the US, which generatesbetween six and seven times as muchtraffic for AEA airlines.

Where a multilateral solution is not likelyto be appropriate, it may be imaginedthat the third-countries involved couldquestion why they should agree to re-word their agreements with EU statessuch that it would grant additionalopportunities only to the European side.

Into this scenario of uncertainty, theairlines – European and non-European –urgently need to see introduced a note ofclarity, stability and commercial certainty.

Bilateral agreements, concluded andamended over the years, are a

fundamental part of the industry’s politicaland commercial infrastructure. Thetraffic rights enshrined in them areamong the airlines’ most valuable assets.

So far, the European Commission hasgiven every indication that it will bepragmatic and flexible in the transition toa new formula for bilateral agreements.

Less clear is whether, in a new regime inwhich the Commission joins – andultimately monitors – the negotiationsbetween an EU state and its bilateralcounterpart , the airlines will be permittedto maintain their traditional place at thenegotiating table.

For years, airlines have individually anddirectly participated to bilateralnegotiations with their Member States.Such participation has allowed airlines toprovide expertise from a technical andcommercial point of view.

Such involvement in negotiations withthird countries is essential for AEAmembers to support their interests andcontinue business as usual.

There is no doubt whatever that thedelegation from the non-European partyto any such agreement will include fullparticipation from that country’sinterested airlines, ensuring that theirown interests are fully represented.

Whatever the strict legalities, theCommunity policy for external relations inthe field of air transport should seek tocreate a European framework allowingthe airline industry to prosper and furtherreinforce its unique and indispensiblecontribution to the mobility of Europeancitizens, economic growth and politicalcohesion.

DENIED BOARDING COMPENSATION

ASSOCIATION OF EUROPEAN AIRLINES III – 9

A recent decision of the EuropeanParliament has paved the way towards asubstantial increase in the scale andscope of the statutory compensation tobe paid to passengers who are not ableto be accommodated on the flight onwhich they are booked.

Existing rules, which date from 1991,fixed compensation levels of €150 forshorthaul flights and €300 for longhaul.The proposed amendment would doublethe higher figure and set levels of €400and €250 for shorter flights.

The proposal contains a number of othermajor changes. The provisions areapplied to non-scheduled airlines for thefirst time, and are also extended to coverflight cancellations.

Another important aspect of the proposedlegislation is the requirement for airlinesto call for volunteers to surrender theirseats. In such a situation, everyone whodid not travel would do so voluntarily andcome away satisfied with the deal theyhad struck with the airline. Only ifvolunteers were not found would thestatutory compensation levels come intoplay.

In the USA, which has had a volunteersystem in place for some time, 95% ofpassengers who surrender their seats doso willingly.

The AEA has long argued in favour of asystem of volunteer calls, and memberairlines have largely put in place such asystem following the implementation ofthe Airline Passenger ServiceCommitment, which the Associationpioneered in 2001-2 and which nowprotects the majority of air travellers inEurope.

A common perception is that deniedboarding incidents are invariably theresult of systematic overbooking byairlines.

This is far from being the case. Acommon problem is that of passengerswho present themselves at check-in with‘OK’ tickets but for whom there is norecord in the airline’s reservationssystem.

Equally significant is the standardpractice among network airlines ofroutinely accommodating passengerswho have missed their connecting flighton the next available service – whether itis already full or not.

The high incidence of delay in Europe inrecent years, much of it outside theairlines’ control, has contributed to thisproblem. Nevertheless, denied boardingremains, statistically, an extremely rareevent on European airlines.

< 1 500 km €250

1 500 - 3500 km €400

€150

> 3 500 km €600 €300

Include flight cancellations Yes No

Applicable to non-scheduled Yes No

Volunteer calls Mandatory Discretionary

REVISING THE DENIED BOARDING REGULATION

Proposed Existing

Source: EU Parliament

AEA_YB_03_28

}

EXTERNAL SHOCKS – SECURITY AND INSURANCE

III – 10 ASSOCIATION OF EUROPEAN AIRLINES

The terrorist attacks in New York andWashington on September 11 2001turned the public spotlight on aviationand its specificities. One consequencewas the establishment in the USA of anew agency which has as its coremission the enhancement of ‘homelandsecurity’.

This agency, and security agenciesworldwide, have increased securitymeasures at airports and for airlines,which have added substantially to theindustry’s cost burden.

The tempo of enhanced security hasfurther increased with additionalmeasures taken in relation to the 2003Iraq War.

So far, AEA airlines have absorbed about€800 million in costs for such additionalmeasures.

In 2001, and again in 2003, the USgovernment paid billions of dollars tocompensate their aviation industry for thecosts of additional security measures.

In contrast, European governments haveso far declined to bear the costs foraviation security measures that aim atthe protection of society in general.

In addition, European states applydiffering policies with regard to thefinancing of aviation security measures.An obvious consequence is distortion ofcompetition.

The airlines are not seeking State Aid;simply that governments assume theresponsibility and funding for securitymeasures that aim at the protection ofthe general public against terroristattacks.

As well as escalating security costs,insurance premiums for AEA airlineshave soared. In addition to normal hull-loss and passenger cover, payments byAEA airlines for third party war andterrorism liability have increased from€80 million in 2001 to an expected €400million in 2003.

Through late 2001 and much of 2002,European airlines had their third-partywar risk underwritten by governments ina scheme approved by the EU. Thisapproval was discontinued in October2002; subsequently the airlines have hadto rely on inferior – and expensive –commercial cover which can becancelled at short notice.

By comparison, the US airlines havebenefitted from a government schemewhich provides twice their pre-9/11 warliability cover at a fraction of the pricepaid by European carriers on thecommercial market. The US scheme willcontinue until at least December 2006.

The US, in supporting its airlines’ security andinsurance programmes, clearly takes theview that war and terrorism are governmentrisks – i.e. threats against the state.European governments, singly or collectivelywithin the EU, have shown little enthusiasmfor acknowledging a responsibility in thesematters.

Reinforced cockpit doorsOnboard means of surveillanceNew operational onboard procedures Anti-terror crew trainingIntensified guarding of aircraftRegular background checks on staffStaff screeningIndirect costs for catering and cleaning servicesPNR access provision

Some areas in which additional security hasdirectly impacted airline costs:

Source: AEA

AEA_YB_03_29

ASSOCIATION OF EUROPEAN AIRLINES IV - 1

CONTENTS

SECTION I AEA AIRLINES IN 2002 I-1

At a Glance I-2Welcome to Virgin Atlantic Airways I-4 The Global Economic Environment I-5

Traffic Development 2002 I-7 ‘No-frills’ carriers l-8

Spotlight on the North Atlantic I-10 Spotlight on the Far East I-11 Operating Results 2002 I-12

Punctuality Performance I-14

SECTION II OUTLOOK FOR 2003 II-1 The Story so Far.. II-2 Traffic Development II-3

Operating Results II-4

SECTION III LOOKING FORWARD III-1 Towards an Efficient European Air Transport System III-2

Are Air Transport Networks Sustainable? III-4 Improving the Industry’s Regulatory Framework III-5

The Dynamics of the Value Chain III-6 A transatlantic Open Aviation Area ? III-7 Bilateral Agreements – Where now ? III-8

Denied Boarding Compensation III-9 External Shocks – Security and Insurance III-10

SECTION IV SPOTLIGHT ON THE AEA IV-1

AEA Highlights IV-3 Airline Profiles & Review of 2002 IV-6

SECTION V KEY STATISTICS V-1 Key Statistics - Total AEA V-2 Key Statistics - By Carrier V-4

AEA Fast Facts V-11 What do we mean by…? V-12

IV – 2 ASSOCIATION OF EUROPEAN AIRLINES

Rod Eddington, Chief Executive of British Airways and 2003 Chairman of the AEA.

AEA HIGHLIGHTS

ASSOCIATION OF EUROPEAN AIRLINES IV - 3

At the start of the year 2002 Leo van Wijk, CEO of KLM, took up the post of Chairman of the AEA. The position is held for one calendar year, by a member airline’s President or CEO. Together with the Presidents’ Committee, the Chairman has the task of overseeing the work of the AEA Secretariat office in Brussels. The newly elected Chairman for 2003 is Rod Eddington, Chief Executive of British Airways. Ulrich Schulte-Strathaus joined the Association of European Airlines as its new Secretary General from 1st September, 2002. Formerly Corporate Vice President International Relations at Lufthansa, Schulte-Strathaus succeeded Karl-Heinz Neumeister who left his position after nineteen years of very valuable contributions to the Association.

Left to right: Karl-Heinz Neumeister, retiring AEA Secretary General, Leo van Wijk, CEO of KLM, and Ulrich Schulte-Strathaus, incoming Secretary General, at the official ceremony held on the occasion of the Autumn 2002 Assembly of Presidents.

Two new airlines joined the AEA in 2002: LOT Polish Airlines and SN-Brussels Airlines, the successor to Sabena as Brussels’s hub airline.

On 1st July 2003 AEA welcomed its thirty-first member, Virgin Atlantic Airways. A profile of each member airline can be found on pages IV-6 to IV-36.

The activities of the AEA in 2002 and early 2003 were clearly focused on the tasks in hand. The economic slowdown, the events of September 11th, the Iraq war and the SARS epidemic left the industry facing an unprecedented crisis. This Yearbook gives an assessment of the current state of the European airline industry in section I. Whilst the industry addressed its structural problems, AEA worked, on behalf of, and with, its members on a broad range of issues from efforts to minimize the cost burden of additional legislation on the airlines, to arguing for a level-playing field with the American aviation industry, and reassessing every link in the aviation chain on a cost-benefit basis. These and other topics are elaborated on in this Yearbook, to be found under section III.

IV – 4 ASSOCIATION OF EUROPEAN AIRLINES

Ulrich Schulte-Strathaus, AEA Secretary General

MISSION STATEMENT

ASSOCIATION OF EUROPEAN AIRLINES IV – 5

The AEA is a non-profit making association. The AEA is represented jointly by all its members or by persons named for this purpose. The AEA shall serve the common interests of its Members. It shall represent the interests of its Members to the institutions of the European Union, to the European Civil Aviation Conference, to any other international organisation or association involved in or likely to be involved in issues of interest to AEA members and, as appropriate, to individual governments. It shall advance co-operation amongst its Members on any matter likely to be of interest to the membership as a whole and permitted by the laws of the countries in which they operate, whilst respecting the independence of action of its members individually. AEA STRUCTURE Twice a year the Presidents of the member airlines meet to discuss the state of the industry. Each year a Chairman is elected from amongst the Presidents, to preside the Assemblies and the AEA for a period of one year. The Chairman is assisted by the Presidents’ Committee, which is composed of the past and present Chairmen and seven other Presidents elected by the Assembly, with a total of nine representatives. The AEA Secretariat, with at its head the Secretary General, is located in Brussels and has a staff of twenty. AEA Chairman for 2003 Rod Eddington British Airways Presidents’ Committee Jean-Cyril Spinetta Air France Francesco Mengozzi Alitalia

Vagn Soerensen Austrian Airlines Rod Eddington British Airways

Ivan Misetic Croatia Airlines Wolfgang Mayrhuber Lufthansa Fernando Conte Iberia Leo van Wijk KLM Jørgen Lindegaard SAS AEA Secretariat Ulrich Schulte-Strathaus Secretary General

'

Association of European Airlines

ˇ

IV – 6 ASSOCIATION OF EUROPEAN AIRLINES

Review of 2002 2002 in numbers: 0.81 million passengers transported, 88% on scheduled services within Europe, 12% on charter services; 4.6 thousand tonnes of freight carried on passenger services. On a turnover up 4% over 2001, Adria Airways posted a positive operating result just over € 3 million in 2002, compared to € 2.6 million in 2001. Net profit (after taxes) stood at € 0.5 million. Adria implemented some measures to deal with the difficult economic climate the industry is operating in, which included cost-cutting measures, such as a reduction in staff numbers, and the generation of extra income from the servicing of foreign aircraft. In July Bombardier Aerospace appointed Adria Airways as the first Bombardier recognised Canadair CRJ aircraft heavy maintenance facility in Europe. Adria is thus authorised to perform the so-called ‘C’ check and other heavy maintenance on the 50-seater CRJ -100 and -200, the 70 seater CRJ-700 and the 86-seater CRJ-900, as well as aircraft modifications and upgrades. As of 30 th June, 2002 there were 211 CRJ aircraft in service with, or on firm order from, European airlines. Adria took delivery of its first Bombardier CRJ series regional jet in January 1998, and at year-end 2002 operated four CRJ-200s, as well as its three A320s. In early 2003 an additional CRJ was leased from Bombardier, for a period of two years, bringing the total of this aircraft type in the fleet to five. Adria’s established code-share partners include Air France co-operating on the Ljubljana-Paris route, Austrian Airlines with an agreement on Ljubljana-Vienna services and Lufthansa on the Ljubljana to Frankfurt and Munich routes. In November of the previous year (2001) Adria launched flights between Germany and Austria, on the Vienna-Frankfurt route, in direct competition with Austrian Airlines and Lufthansa, on a so-called 7th freedom service. In May 2002 Adria started operating between the Slovenian capital and Podgorica, the capital of Montenegro, following an agreement with Montenegro Airlines. London operations were switched from Heathrow to Gatwick airport with effect from the Summer timetable. In June Adria’s Moscow services were moved from Sheremetyevo airport to the recently upgraded Domodedovo airport.

Adria Airways Kuzmiceva 7 1000 Ljubljana Slovenia www.adria.si Branko Lucovnik, President & CEO 19 Scheduled Destinations 1 within Slovenia 17 rest of Europe 1 beyond Europe 555 Employees 7 Aircraft in Fleet 3 Airbus A320 4 Canadair CRJ-200 0 Aircraft on Order Status at 31st December for information on destinations, employees and fleet. Owned by… 55.8% Slovenian Pension Fund 20% Slovenian Restitution Fund 10.3% National Finance Corporation 9% Nova Ljubljanska Banka 3.4% Porbanka 1.5% Zlata Moneta Owner of… - Major partnerships Code-share agreements with Air France, Austrian Airlines, Croatia Airlines, Lufthansa. Financial Results

€ ‘000 2002 2001 Turnover 112066 107672 Operating profit/loss 3121 2634 Net profit/loss 521 752

Branko Lucovnik President

ˇ

ˇ

ˇ

ASSOCIATION OF EUROPEAN AIRLINES IV - 7

Review of 2002 2002 in numbers: Not available. 2002 was a year of major change for Aer Lingus. The airline made substantial progress in moving the business from the threat of financial crisis at the outset of the year to a return to profitability by year end, recording a net profit of € 35.3 million. Following the terrorist attacks of 11th September, 2001 a radical Survival Plan was prepared by the Board and management of Aer Lingus and was implemented with great speed. Subsequently the company took steps to put in place a new business model which incorporated reductions in its cost base, significant reductions in its business and leisure fares and the introduction of a series of popular, direct routes out of Ireland. Nine new routes were added in 2002, all through greater utilisation of existing aircraft and staff resources. Business and leisure fares were reduced by up to 60% and over 3 million customers availed of low fares seats in 2002. Aer Lingus dotcom became the airline’s main distribution point, with over 40% of all the airline’s bookings being made online by year end, compared with just 2% at the start of 2002. The results of these actions have been dramatic and have led to the transformation in the performance of the business in 2002. The outcome is a return to profitability for Aer Lingus, ahead of the projections in the Survival Plan.

Aer Lingus Dublin Airport Dublin Ireland www.aerlingus.com Tom Mulcahy, Chairman William Walsh, Chief Executive 37 Scheduled Destinations 3 within Ireland 29 rest of Europe 5 beyond Europe 4500 Employees (at 31st Dec ’01) 34 Aircraft in Fleet 4 Airbus A330-300 3 Airbus A330-200 6 Airbus A321-200 4 Airbus A320-200 8 Boeing 737-500 3 Boeing 737-400 6 BAe 146-300 0 Aircraft on Order Status at 31st December for information on destinations, employees and fleet. Owned by… 95% State ownership 5% Aer Lingus employees Owner of… - Major partnerships Member of the Oneworld Alliance. Code-share agreements with: American Airlines, British Airways, Iberia, KLM. Financial Results (Group)

€ mill 2002 2001 Turnover 958.6 1097.2 Operating profit/loss 63.8 (52.1) Net profit/loss 35.3 (139.9)

Tom Mulcahy Chairman

William Walsh Chief Executive

IV – 8 ASSOCIATION OF EUROPEAN AIRLINES