SOaAL WORK - Digital Howard @ Howard University | Howard ...

Upload

the-howard-groupCategory

view

3.248download

0

: The Little Technology Company That Could!

1 | P a g e

THE HOWARD GROUP INC. PERSPECTIVE

April 2014

By: Grant Howard

Contributions from: Dave Burwell, Jeff Walker & Miliya Davidov

There’s an old saying that the company you keep will affect and influence the opportunities you

meet.

With that thought in mind, one must ask, how did an up and coming Toronto based company

attract so many household names to sign on the dotted line?

2 | P a g e

– The Little Technology Company That Could!

The company of which we speak is called YANGAROO, a name born in the time when marketing companies were

concocting “Google type” names for technology companies. It was 1999 and the founders believed a sizeable

business could be built by developing a software technology to transfer and manage the thousands of audio files for

broadcasters that are a daily part of their life. Fast forward to 2012 and $30 million later, revenues were small, debt

was piling up and YOO was saddled with an unwieldy share structure. The company was close to being on life

support and needed a new leader or a magician or both.

Enter Gary Moss, the former Chief Operating Office of IMAX Corporation who was a director of YANGAROO.

Major shareholders wanted him to take over the CEO role. A healthy dose of persistence, experience and deal

making in combination with a highly supportive core group at YANGAROO, an astute investment banker by the

name of Phil Benson and several major shareholders who stepped up to back “the plan”, the story was quite

different by the fall of 2013.

The shares were consolidated 10 - 1,

The balance sheet was strengthened through an over-subscribed equity offering,

Debt was reduced to $2 million from $6 million along with the interest rates on the notes falling to 10%

from 14% resulting in an annual saving of $700 thousand,

A new, advertising industry centric, robust cloud-based technology was completed - DMDS (Digital Media

Distribution System) and

YOO dramatically expanded its opportunities.

The business quickly gained traction resulting in the announcement this past January that “for the first time in the

company’s history, it surpassed $1 million in revenues” in the fourth quarter of 2013!

By way of disclosure: The Howard Group is a shareholder in YANGAROO and receives fees for its capital market and investor

out-reach programs on behalf of YANGAROO. HG is not a registered investment advisor. As such, this commentary solely

deals with HG’s perspectives on why it is aligned with YANGAROO. Readers should carefully consider all opinions and seek

registered investment advice.

THE COMPANY

You may be surprised to learn that YOO plays a pivotal, behind-the-scenes role to a number of major organizations

and leading brand names. If you listen to an English-speaking radio station in Canada, virtually every song you

hear has been delivered to the station through a technology developed and owned by YANGAROO. If you watch

MTV or any other major music video broadcaster in North America, 90% of the music videos you see are managed

by YOO.

The Company’s patented cloud-based Digital Media Distribution System (DMDS) was developed to rapidly and

seamlessly transfer, organize and manage massive amounts of audio and video files, which is a fundamental tool to

awards shows, music and advertising industries.

To put it simply, YANGAROO provides a platform for agencies and individuals to quickly, efficiently and securely

send music and video files to broadcasters and media outlets.

3 | P a g e

– The Little Technology Company That Could!

Not only does DMDS replace the need for

physical servers and satellites, but it also

manages the entire process through

automated quality control checks, advanced

file formatting capabilities and content

organization features - a huge advantage to

outlets and agencies receiving countless files

of various formats and sizes per day. We’ll

have more to say about the technology.

COMPANY HISTORY

Initially, music and audio files had to be transferred physically through cassettes, CD’s and hard drives. Eventually,

file transferring began to go digital with servers, satellites and digital tapes being utilized instead.

YANGAROO was formed in 1999 during the start of the digital phase when peer-to-peer services like Napster

started to pop up in the online world, enabling users to illegally download and distribute music files.

At the time, YANGAROO was operating under the name Musicrypt, which accurately depicted the purpose of the

business. Musicrypt was formed to offer a technological solution to the music industry through a software program

that provided increased security and accountability for music sharing.

In addition to combating music piracy, the industry was also looking to find a more efficient and cost effective way

to distribute music, as in the late 90’s to early 2000’s, music files were still being burned onto CD’s and then

couriered to radio stations, promoters etc.

This would be the first example of the company developing a customized technology to meet the unique demands of the music industry.

EARLY SUCCESS IN THE MUSIC INDUSTRY

Musicrypt launched the first version of DMDS in late 2003 and saw an immediate interest from the music industry,

quickly expanding its reach to claim approximately 75% of the market share in Canada.

By the end of 2004, DMDS was being utilized by almost every major broadcaster in the country including Standard

Broadcasting, Rogers and Chorus Media and every major record label in the country.

4 | P a g e

– The Little Technology Company That Could!

Musicrypt essentially owned the audio delivery business in Canada, with the exception of a few French-speaking

locations that still distributed content physically. However, the reality was that revenues could never grow to a

material amount strictly based on the relatively small size of the digital audio delivery market.

At that point, the company began to focus on building a technology for delivering video files as well as recognizing

that there was a huge market opportunity beyond the music industry. Musicrypt became YANGAROO and thus

began the long and expensive R & D journey to build the perfect software technology.

TARGETING THE ADVERTISING INDUSTRY

In 2009, YANGAROO signed an agreement with Horizon Media with the

intent of gaining the American-based media giant as a client. Horizon saw

potential in the early DMDS technology, resulting in a strategic relationship.

Through the five year agreement, Horizon would provide YANGAROO with

inside knowledge on what the advertising industry would ideally like to see

in a new technology and also assist with unlocking the footprint with U.S.

based broadcasters. In return, Horizon would receive a determined percent

of revenue share and 750,000 warrants. (Of note: the five year agreement is

set to expire mid 2014 and renewal discussions are already underway.)

The company originally launched DMDS 5.0 in April 2009. YANGAROO’s

relationship with Horizon was based on DMDS 5.0. As a result, Horizon

provided YANGAROO with valuable feedback and spelled out exactly what

the industry required. YANGAROO rose to the occasion, invested millions of

dollars and delivered an industry-tailored DMDS 5.0, in February of 2012.

DMDS TECHNOLOGY

Digital Media Distribution System 5.0 is a patented, cloud-based software technology that enables large files to be

digitally transferred and managed. DMDS involves no physical elements and works from the user’s desktop.

There are a handful of companies that brand themselves as “digital distributors” but still require physical elements

such as satellites or servers in order to function. There are also a handful of companies that currently have the

ability to “distribute” files but act more as a dropbox than a true distributor with limited file management and

content organization capabilities.

The real difference and advantage with DMDS is what occurs between the moment the file is sent until it’s received,

and what can be done with the file afterwards.

Horizon Media is the world’s

largest privately held media

buyer. The private company is

headquartered in New York City

and provides communication and

media services including

broadcasting, cable syndication

and branded entertainment.

Horizon media represents

household brand names including

Cadbury, Kraft and Crown

Imports and generates several

billion dollars in annual revenue.

5 | P a g e

– The Little Technology Company That Could!

DMDS has the ability to fundamentally change the way agencies and broadcasters operate, offering advanced data

management, reporting, analytics and the ability to send traffic instructions, resulting in compounded cost saving

for YANGAROO’s clients. When used by clients to its fullest capabilities, DMDS is a very effective productivity tool,

enabling changes to client’s workflows, introducing process improvements and efficiencies and ultimately saving

client’s money, beyond a reduction in distribution fees.

The point on cost savings is not to be understated. What Horizon Media experienced with DMDS was so significant

that its testimonial is central to YANGAROO’s presentation.

6 | P a g e

– The Little Technology Company That Could!

PROBLEM:

People are often resistant in adopting a new technology or software program.

• DMDS was developed to be simple and easy to use. • The open architecture design allows DMDS to “talk” to and work alongside of any other

program the user is currently using.

PROBLEM:

When it comes to adopting a technology, there is often the mentality of “don’t fix what’s not broken”.

• YANGAROO encourages potential clients to trial DMDS alongside whatever program is currently being used so the advantages can clearly be seen and the transition is a simple process.

• No costly hardware is required to trial DMDS. Users can begin to test the program following a simple download on their own systems.

COMPETITION

There were two and now there is one!

Digital Generation was the biggest kid on the block. DG (Digital Generation) was formed in 2006 following the

merger of DG Systems and FastChannel Networks. It subsequently divided its business into two distinct categories,

providing file distribution services for both television and the web.

To make a long story short, a spate of acquisitions and a heavy debt load lead to an opportunity for two of the

company’s founders. They left DG in the early days before the spending spree and launched what would become

DG’s biggest competitor – Extreme Reach.

To its credit, Extreme Reach continued to grow even through the financial crisis of 2008 while DG’s business was

going in the opposite direction. Just this past February, Extreme completed the acquisition of DG’s television

advertising distribution solutions division for $485 million (USD) in cash.

The combined entities have revenues of $270 million and 750 employees.

Through Extreme Reach’s acquisition of DG, the Number Two industry giant swallowed Number One and created

an almost monopolized environment.

So, what does this mean for YANGAROO? How does it go toe to toe against Goliath?

Most agencies have a policy of using at least two approved vendors meaning any organization that had been

primarily using DG and Extreme Reach will now have to look elsewhere.

As results speak louder than words, a review of what YOO has accomplished by way of new business over the past

year is worthy of review as it addresses the question of whether or not there are growth opportunities available.

7 | P a g e

– The Little Technology Company That Could!

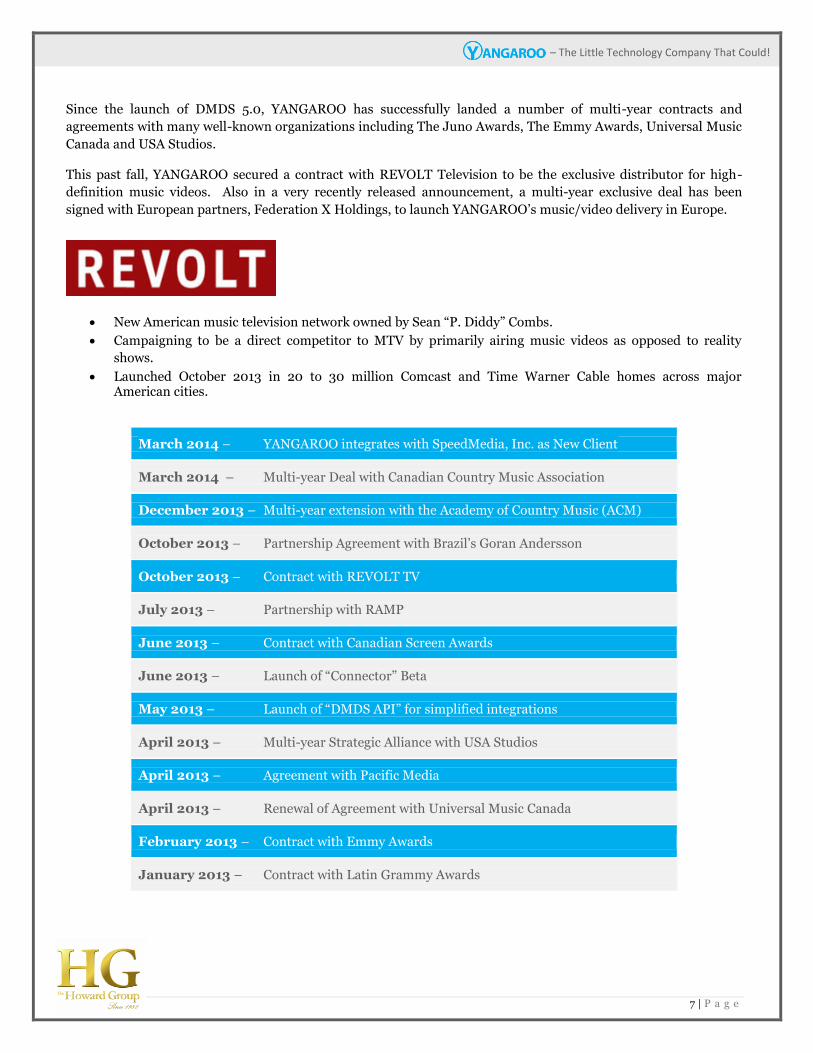

Since the launch of DMDS 5.0, YANGAROO has successfully landed a number of multi-year contracts and

agreements with many well-known organizations including The Juno Awards, The Emmy Awards, Universal Music

Canada and USA Studios.

This past fall, YANGAROO secured a contract with REVOLT Television to be the exclusive distributor for high-

definition music videos. Also in a very recently released announcement, a multi-year exclusive deal has been

signed with European partners, Federation X Holdings, to launch YANGAROO’s music/video delivery in Europe.

New American music television network owned by Sean “P. Diddy” Combs.

Campaigning to be a direct competitor to MTV by primarily airing music videos as opposed to reality

shows.

Launched October 2013 in 20 to 30 million Comcast and Time Warner Cable homes across major American cities.

March 2014 – YANGAROO integrates with SpeedMedia, Inc. as New Client

March 2014 – Multi-year Deal with Canadian Country Music Association

December 2013 – Multi-year extension with the Academy of Country Music (ACM)

October 2013 – Partnership Agreement with Brazil’s Goran Andersson

October 2013 – Contract with REVOLT TV

July 2013 – Partnership with RAMP

June 2013 – Contract with Canadian Screen Awards

June 2013 – Launch of “Connector” Beta

May 2013 – Launch of “DMDS API” for simplified integrations

April 2013 – Multi-year Strategic Alliance with USA Studios

April 2013 – Agreement with Pacific Media

April 2013 – Renewal of Agreement with Universal Music Canada

February 2013 – Contract with Emmy Awards

January 2013 – Contract with Latin Grammy Awards

8 | P a g e

– The Little Technology Company That Could!

INDUSTRY SIZE = OPPORTUNITY

An independent voice has lent itself to the question of competition and YOO’s opportunity. In early March of this

year, Global Maxfin analyst Joseph MacKay initiated research coverage on YANGAROO. His extensive report

included this comment, “Within the Advertising segment, we believe that YANGAROO is on the cusp of generating

significant revenue growth due to changes within the industry as well as changes in its NYC (New York) office.”

The size of the pie is huge and even if YANGAROO has only moderate success, it will still be a very profitable

business.

YANGAROO is structured as a technology provider, as opposed to a full-service operator, which means it is able to

remain a nimble organization and retain high gross margins. Its General and Administrative costs are low as is its

employee count. While headquartered in Toronto, the New York office is the main point of contact for U.S.

advertising business generation.

Management has publicly stated that it believes 2014 is the start of a long growth curve as there is ample

opportunity in the marketplace. While it is under no illusions of becoming the biggest player in the space, it is

focused on profitability. YOO certainly won’t be paying taxes for quite some time as it has $22 million in tax loss

carry-forwards from the days of old.

Management is cautious when discussing future opportunities, potential deals, or projections. It has stated

however, that small to mid-sized advertising customers typically deliver approximately $350 to $500 thousand in

revenues per year.

To provide an example, if YANGAROO were to sign between 8 to 12 new advertising customers, revenues could

reasonably be expected to land around the $8 million mark. Such an example would see YANGAROO taking less

than 3% of the North American market share, demonstrating how the business model’s high gross margins allow

the Company to achieve significant increases to revenue without requiring market domination.

MUSIC & AWARDS ADVERTISING

Market Opportunity

In North America $15 million $250- 300 million

Market Opportunity

Globally $30 million $1 billion

Example Of How DMDS Is Used

Music video and audio digital file delivery from music labels to broadcasters.

Complete management of award show process from submission to voting.

Distribution of TV commercials and radio advertising, in addition to process management and digital content

management.

YOO Contract Lifespan

3 years 3 to 7 years

Contract Exclusivity to YOO

Music/Radio – 90% market share Awards Show – Yes

No - Varied

File Transfer Frequency

Constant Constant

YOO $ per HD Delivery

Music/Radio – $5 - $60 Awards Shows – Flat annual fee

~$35 - $100

9 | P a g e

– The Little Technology Company That Could!

Below is the low and high scenario that management is looking at for 2014.

2014 LOW 2014 HIGH

(Example for illustrative purposes only)

Advertising $5,300,000 $6,500,000

Music $1,950,000 $2,500,000

Awards $750,000 $1,000,000

Total Revenue $8,000,000 $10,000,000

Gross Margin (~86%) $6,880,000 $8,600,000

Overhead Expenses 4,700,000 $5,200,000

Operating Income $2,180,000 $3,400,000

Net Income (Loss) $1,600,000 $2,800,000

EBITDA $1,800,000 $3,600,000

While the DMDS technology may be developed, proven, in use and reputable, the Company has its work cut out for

it in terms of claiming its piece of the market. The success of YANGAROO will depend on the success of its sales

force landing new contracts. With limited manpower and resources available, the Company has a lot of ground to

cover and a massive competitor to go up against.

The Company does not currently have any true form of recurring revenue, as revenues are generated based upon a

client’s use of DMDS. Each file delivered through DMDS is done so at a charge, which varies depending on the file

and the contract agreement. However, having a contract in place does not guarantee the client will actually be

utilizing the program, therefore it cannot guarantee revenues. With that said, each company or organization that

has signed with YANGAROO has done so because its business relies upon the transfer of audio or video files,

making it reasonable to assume the program will in fact be put to use. However, to what extent DMDS is used will

always be an unknown factor at the discretion of the client.

10 | P a g e

– The Little Technology Company That Could!

That being said, we again refer to analyst Joseph MacKay’s expectations for YOO. His forecast for the 2014 through 2016 period is below:

The analyst has a $0.60 target price for the stock in the report entitled, “YANGAROO – Turning The Corner”.

To read The Howard Group’s commentary on the research report click on the link below where you can also access his full report.

http://www.howardgroupinc.com/Portals/0/YANGAROO/Analyst%20Coverage/YANGAROO%20Inc%20Initiating%2003102014.pdf

Share Structure:

Common shares 40,089,271

Warrants 12,897,055 3.3M warrants are @ $1.00, balance at $0.25

Stock options – Non vested 893,548 Majority of options are $1.00

Stock options – Vested 212,750 Majority of options are $1.00

Total 54,092,624

$6.39

$1.74

$8.70

$2.66

$9.29

$2.83

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

$8.00

$9.00

$10.00

Revenue (M) EBITDA (M)

F2014E F2015E F2016

*All figures are in Millions

11 | P a g e

– The Little Technology Company That Could!

MANAGEMENT TEAM

Executive Team

Gary Moss – President and CEO

Former Chief Operating Officer at IMAX Corporation

Held senior executive roles in the entertainment industry, including, Live Nation Artists,

EMI Music Canada and Sega of Canada.

Actively involved with the Canadian Recording Industry Association.

Member of the Canadian Academy of Recording Arts and Sciences.

Cliff Hunt – Founder, Vice-Chairman and Chief Operating Officer

25 years of business and music industry experience as a founder and partner of a major

JUNO Award winning artist management and record production company.

Has worked with some of Canada's most successful artists both domestically and

internationally.

Negotiated over 35 major Canadian and International record deals and was

instrumental in coordinating world-wide tours for his artists.

Contributing writer to The Huffington Post and Fortune Magazine.

Richard Klosa – Chief Technology Officer

Digital media innovator with more than 13 years of IT development and management

experience.

Built large scale distribution platforms and analytical data management systems in

successful previous entrepreneurial ventures.

Considered to be an authoritative voice on digital media distribution.

Sarah Foss – President of Advertising Division

NEW SALES HIRE AS OF AUGUST 2013 – Based out of New York City

Over 20 years of sales and marketing experience across multiple sectors, including

digital technology services, broadcast cable and network media, and advertising.

Previous executive roles include EVP, Sales and Client Services, at Encompass Digital

Media; CEO at VCI Solutions and President, Question d'Image, for Harris Broadcast

Has consulted with a number of media technology firms building strategic growth

plans, business development pipelines, and product roadmaps that exceed market and

client needs.

12 | P a g e

– The Little Technology Company That Could!

Joanne Eckert – VP of Sales/Business Development for Advertising Division

NEW SALES HIRE AS OF NOVEMBER 2013 – Based out of New York City

20 years of experience in sales, business development and marketing within the

advertising and media industry.

Held positions of VP, Sales and Partnerships for LodgeNet and Senior Director,

National Sales/Advanced Advertising for ROVI Corporation.

Extensive advertising sales experience for both high-growth and emerging cable

networks including BBC America, CMT, Versus, Turner Broadcasting and A&E Network.

SUMMARY

YANGAROO’s stock chart closely reflects its changing fortunes. This past summer, the stock was trading in the

$0.15 to $0.20 range (post-consolidation) as the market awaited news on the re-structuring of the balance sheet

and the financing. With the successful completion of those efforts, the market began to focus more attention on the

business. With each new announcement, trading volumes began to increase as liquidity was a major concern prior

to last summer. In the past six months, the stock has gone from comatose to where more than six million shares

have changed hands and it has slowly moved to the $0.40 range (as of this writing).

YANGAROO has arrived at the right place at the right time. Investment firms, small cap fund managers and

individual investors have been rewarding industrial and technology companies over the last year in particular.

Many have become very tired of too many companies staking their future and their shareholders’ fortunes on a drill

core that too often became just another hole in the ground.

YANGAROO is most certainly being watched and by more eyes than this time last year. A company doesn’t have to

be the biggest to be the best but it does have to remain nimble and hungry.

13 | P a g e

– The Little Technology Company That Could!

To receive future news and commentary on YANGAROO Email: [email protected]

Please provide us with relevant contact information and whether or not you are an individual investor, investment advisor, analyst or fund manager. Also, please indicate if you would like someone to call you to discuss YANGAROO. We also appreciate your comments & feedback.

You can also sign up for updates on our website at: http://www.howardgroupinc.com/master/Register.aspx

Contact Information:

Dave Burwell

The Howard Group Inc.

Toll Free: 1-888-221-0915

Phone: (403) 221-0915

Email: [email protected]

Website: http://www.howardgroupinc.com/Clients/YangarooInc.aspx

Newsletter Direct: http://howardgroupinsightnewsletter.blogspot.com/

DISCLAIMER

The Howard Group is not a registered investment advisor and as such, individuals should consult a registered investment advisor prior to

making investment decisions in relation to the company discussed in this commentary. The information presented in these website pages was

obtained from sources believed to be reliable but is not guaranteed, is not all conclusive and should not be relied upon as the sole source of

information/opinion for making an investment decision. The Howard Group or its employees may own securities in the company discussed in

this commentary. The Howard Group receives remuneration for Investor Relations activities from the company discussed in this commentary

Except for the statements of historical fact contained herein, certain statements contained in this presentation constitute “forward-looking

statements” as such term is used in applicable Canadian and US laws. These statements relate to analyses and other information that are based

on forecasts of future results and assumptions of management. Any statements that express or involve discussions with respect to predictions,

expectations, beliefs, plans or future events or performance (often, but not always, using words or phrases such as “expects” or “does not

expect”, “is expected”, “anticipates” or “does not anticipate”, “plans”, “estimates” or “intends”, or stating that certain actions, events or results

“may”, “could”, “would”, “might” or “will” be taken, occur or be achieved) are not statements of historical fact and should be viewed as “forward-

looking statements”.

Forward-looking statements are made based on management’s beliefs, estimates and opinions on the date the statements are made and the

Corporation undertakes no obligation to update forward-looking statements if these beliefs, estimates and opinions or other circumstances

should change, except as required by applicable law.

THIS IS NOT A RECOMMENDATION TO BUY OR SELL ANY SECURITY