Wyncrest Group Inc.

15

Analyst: Victor Sula, Ph.D. Initial Report September 11th, 2009 Company Introduction Wyncrest Group Inc. 9654 West 131st Street Suite 215 Palos Park, IL 60464 USA Tel : 630-215-5171 Fax : 866-536-2883 Email: [email protected] MARKET DATA Symbol Exchanges Current Price Price Target Rating Outstanding Shares Market Cap. Average 3-m Volume Source: Yahoo Finance, Analyst Estimates WNCG OTC PK $0.07 $0.43 Speculative Buy 47.07 Million $3.29 Million n/a The Wyncrest Group Inc. (WNCG) provides insurance products and services through its Southwest Financial Group subsidiary (SFG) and Wyncrest Offshore Services. SFG has been in business for 21 years, has 18,000 clients, and sells through 85 representatives nationwide generating approximately $22 million in gross insurance policy sales during 2008 and resulting in $1.1 million of commission revenues. WNCG plans to continue to grow SFG through acquisitions of competing agencies that will enable it to exploit its IT advantage. The Company has a U.S. patent pending automated business method for managing acquired client books to improve policy renewal retention and up-selling. The Company anticipates that its automated process will reduce cost of sales by half compared to traditional origination methods. The Company is in negotiations with numerous acquisition targets it has identified during a two-year campaign to find distressed agencies, then consolidate contract assets under one lower cost roof. Through its Wyncrest Offshore Services Division, the Company is expanding into the growing offshore insurance and reinsurance market by offering a variety of services and insurance products, including a liability program for helicopter flight training schools and non-owner helicopter pilots, and a line of Warranty Service Policies operating as a controlled foreign corporation. Royalty income may be generated from licensing insurance products patented under a new category of business methods. This strategy, 9/11/09 volume 0.25 0.20 0.15 0.10 0.05 3 2 1 0 © BigCharts.com WNCG daily Jul Aug Sep Millions

-

Upload

beacon-equity -

Category

Documents

-

view

218 -

download

2

description

Wyncrest Group Inc.

Transcript of Wyncrest Group Inc.

Analyst: Victor Sula, Ph.D.Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 1

Analyst: Victor Sula, Ph.D.Initial Report

September 11th, 2009

Company Introduction

Wyncrest Group Inc.9654 West 131st StreetSuite 215Palos Park, IL 60464 USATel : 630-215-5171 Fax : 866-536-2883 Email: [email protected]

MARKET DATA

SymbolExchangesCurrent PricePrice TargetRatingOutstanding SharesMarket Cap.Average 3-m Volume

Source: Yahoo Finance, Analyst Estimates

WNCGOTC PK

$0.07$0.43

Speculative Buy47.07 Million$3.29 Million

n/a

The Wyncrest Group Inc. (WNCG) provides insurance products and services through its Southwest Financial Group subsidiary (SFG) and Wyncrest Offshore Services. SFG has been in business for 21 years, has 18,000 clients, and sells through 85 representatives nationwide generating approximately $22 million in gross insurance policy sales during 2008 and resulting in $1.1 million of commission revenues.

WNCG plans to continue to grow SFG through acquisitions of competing agencies that will enable it to exploit its IT advantage. The Company has a U.S. patent pending automated business method for managing acquired client books to improve policy renewal retention and up-selling. The Company anticipates that its automated process will reduce cost of sales by half compared to traditional origination methods.

The Company is in negotiations with numerous acquisition targets it has identified during a two-year campaign to find distressed agencies, then consolidate contract assets under one lower cost roof.

Through its Wyncrest Offshore Services Division, the Company is expanding into the growing offshore insurance and reinsurance market by offering a variety of services and insurance products, including a liability program for helicopter flight training schools and non-owner helicopter pilots, and a line of Warranty Service Policies operating as a controlled foreign corporation.

Royalty income may be generated from licensing insurance products patented under a new category of business methods. This strategy,

9/11/09

volume

0.25

0.20

0.15

0.10

0.05

3

2

1

0

© BigCharts.com

WNCG daily

Jul Aug Sep

Mill

ions

Analyst: Victor Sula, Ph.D. Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 2

Analyst: Victor Sula, Ph.D.Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 2

being used by new class of small insurance companies may transform the industry.

Business model focused on product creation and growth through acquisitions

WNCG plans to deliver innovative insurance products of its own creation that target small, underserved niches. The Company is in the process of securing financing for a series of planned acquisitions that will double the number of contracts controlled by its SFG operating subsidiary at a much reduced cost compared to originating them in-house. The acquired assets show improved ROI resulting from reduced overhead and efficiencies from a novel automated management system.

Market opportunity

Global insurance premiums topped $4.1 trillion in 2007. The global recession has negatively impacted every insurance segment, with life insurance revenues and profits being particularly hard hit. World insurance premium volume fell for the first time in more than 30 years in 2008, according to a report released by Swiss Re. Shareholder capital in the life insurance industry has shrunk by 30%-40% on average, with some companies suffering declines of up to 70%. As the economy recovers, life premiums and investment returns are expected to rise. WNCG has found opportunity in distressed agencies to acquire undervalued insurance assets now and capitalize on adding efficiencies and their improving value as the economy recovers.

SFG acquisition provides platform for future growth

Southwest Financial Group (SFG) has operated for 21 years and has interests in businesses ranging from life insurance and long-term care to insuring a specialized aviation and construction market. SFG has 18,000 clients and 85 representatives nationwide, and generated approximately $22 million in gross insurance policy sales in 2008. SFG markets a variety of life protection products and services including: family and personal insurance; real estate and asset insurance products and services; niche tax and wealth building strategies; employee group benefits; 401K retirement plans; earthquake, flood and disaster insurance; debt reduction; alternative investments; and mortgage purchasing and refinancing.

Investment Highlights

Analyst: Victor Sula, Ph.D.Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 3

Analyst: Victor Sula, Ph.D.Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 3

Aggressive acquisition strategy

WNCG’s plan is to acquire companies in specific insurance growth areas. In July 2009, the Company announced it was negotiating six business acquisitions, all of which have synergies with its flagship SFG subsidiary. WNCG anticipates closing all six acquisitions in the second half of 2009, pending financial audits for each of the companies. Full-time staffers are dedicated to prospecting and qualifying prospective actuations and quickly moving toward merger talks.

Offshore services growth opportunity

WNCG’s Offshore Services Division capitalizes on a growing trend favouring offshore insurance. It provides services to offshore insurance and banking companies and up-to-date tools in the areas of tax planning and tax optimization. It also creates insurance products that are patentable at USPTO for license and warranty service policies for delivery through a controlled foreign entity. Like offshore banks, insurance companies formed in offshore jurisdictions benefit from lower taxes and a more liberal regulatory environment.

Acquisition of Florida Insurance Consulting likely to close in Q3 09

The Company has signed a non-disclosure agreement as the first step in the process of acquiring Florida Insurance Consulting. A letter of intent is likely to follow, then due diligence with the expectation of closing the acquisition in Q3 09. Florida Insurance Consulting has more than 100 insurance agents in Florida and generates roughly $10 million - $15 million in premium sales per year.

WNCG’s SFG subsidiary plans to capitalize on synergies with Florida Insurance Consulting to develop additional business in the Latin American community. Hispanics represent the largest minority group in the United States at 44.3 million or 14.8% of the population.

Strong premium growth outlook

SFG generated approximately $22 million in premium sales in 2008. With the business climate beginning to improve in Q2 09, SFG management anticipates comparable sales volume in 2009. The acquisition of Florida Insurance Consulting may add another $10 million to $15 million to premium sales and another acquisition, Cleverbiz, may add $30 million to premium sales. Assuming these acquisitions close as planned in 2009 and the Company makes another one or two acquisitions next year, we estimate WNCG revenues could exceed $50 million in 2010 and net income could reach a $2.5 million range.

Fast payback on investment

Acquisitions are limited to a book of business that has predictable revenue from policy renewal commissions. Costs are reduced through a consolidated database administered to improve customer retention and up-selling. Typical deals will payback in three years using basic assumptions, but Wyncrest believes efficiencies may reduce payback to as little as two years.

Analyst: Victor Sula, Ph.D. Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 4

Analyst: Victor Sula, Ph.D. Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 4

WNCG is a holding company with subsidiaries in international financial services and insurance. The Company is expanding into the offshore insurance market and capitalizing on growing demand for specialty insurance products and services lines in areas underserved by existing providers.

WNCG plans to acquire insurance and financial services businesses that can be stripped of their sole asset of interest (the customer database) with servicing contracts. These acquired customers and agent relationships should provide immediate cash flow with little variable cost as well as fertile prospects for adding on business with new clients and affiliate agents.

Acquisitions may be used to extend market reach where SFG already has a discernable presence in a particular segment, notably, within the Filipino and Latino ethnic communities in certain areas and with various teachers unions. The products offered have been customized for these markets and are supported by specialized agents and a targeted marketing effort.

WNCG has assembled a team of acquisition experts with strong financial backgrounds and expertise in sales and marketing. As a parent company, WNCG will acquire and support businesses, negotiate strategic alliances, develop proprietary financial tools, and apply the skills and experience of management to enhance shareholder value.

WNCG as a parent company

Source: Company’s presentations and releases

Business Model

Analyst: Victor Sula, Ph.D.Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 5

Southwest Financial Group

WNCG acquired Southwest Financial Group (SFG) in February 2007. Southwest Financial Group has operated for 21 years and has interests in business ranging from life insurance and long-term care to sporting events insurance and pet insurance. It mainly sells family and personal insurance; real estate and asset insurance products and services; niche tax and wealth building consulting; employee group benefits; 401K retirement plans; earthquake, flood and disaster insurance; debt reduction; alternative investments; and mortgage purchasing and refinancing.

SFG has 18,000 clients and 85 representatives nationwide and generated approximately $22 million in gross insurance sales during 2008. In addition to its core offerings, SFG also has growing interests in long-term care for student sports programs and student athletes, as well as pet insurance. SFG offers an exclusive program of accident and sickness insurance for college students and handles all administration of the program, including underwriting and quoting, policy issuance, eligibility and billing and paying claims. There are currently more than 100 colleges and universities covered by the program.

SFG is developing new products for insuring sporting events such as PGA tournaments, the NBA Playoffs, and city marathons. It also acquired the business resources of Cleverbiz, which had more than 200 agents in the Chicago market, last year. Cleverbiz will help SFG grow in the single annuity premium and life insurance premium segments.

Offshore services

WNCG’s dedicated Offshore Division will provide services to offshore insurance companies and banks and offer the most up-to-date tools in the areas of tax planning and optimization. Insurance companies formed in offshore jurisdictions can benefit from lower taxes and a more liberal regulatory environment.

Offshore insurance offers the following benefits:• Minimal interventions from authorities and institutions;• Lower capital requirements than other jurisdictions;• Tax aspects, they are often exempted from all forms of direct taxes;• Tax on profits are replaced with lump-sum taxes;• Low establishment and license fees;• Liberal operating requirements;• Generally not subject to foreign exchange restrictions;• Licenses are easily available in many offshore jurisdictions;• In a number of countries no obligation of capital adequacy maintenance; and• Possibility of offering all types of insurance policies,

including life policies.

WNCG’s Offshore Services Division offers: • Catastrophic insurance• Extended warranty insurance • Captive insurance • Aviation insurance

Analyst: Victor Sula, Ph.D. Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 6

Analyst: Victor Sula, Ph.D. Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 6

Pending acquisitions

WNCG plans to acquire businesses in insurance growth areas and other financial services niches. It has a goal of acquiring businesses representing revenues of between $25 million and $75 million each year over the next five years.

During July 2009, the Company announced that it was negotiating six acquisitions. Each of the acquisition candidates have been evaluated for potential synergies with SFG. Completion of the acquisitions is dependent on the completion of timely financial audits for each company.

The first acquisition likely to close is Florida Insurance Consulting, which is based in Bartow, Florida. The Company has signed a letter of intent and following further due diligence completion of the acquisition is expected in Q3 2009. Florida Insurance Consulting has five agents and generates $10 million - $15 million in premium insurance and financial sales each year.

SFG plans to work through Florida Insurance Consulting to develop additional business in the Latin American community. Hispanics represent the largest minority group in the U.S. at 44.3 million or 14.8% of the population and are also the fastest-growing minority group, accounting for nearly 50% of U.S. population growth in 2006.

The relatively young Hispanic population has impressive purchasing power. Many Latin Americans have successfully started their own businesses, as evidenced by the 1.2 million Hispanic-owned firms in the U.S. Health insurance providers and hospitals are advertising online to build brand awareness within the Hispanic community, and tax preparation and accounting services are advertising through Spanish-language media.

The Company plans to extend its market penetration within the Hispanic community by recruiting new agents and associates with strong family backgrounds and ties to Latin America, Cuba, the Caribbean and South America.

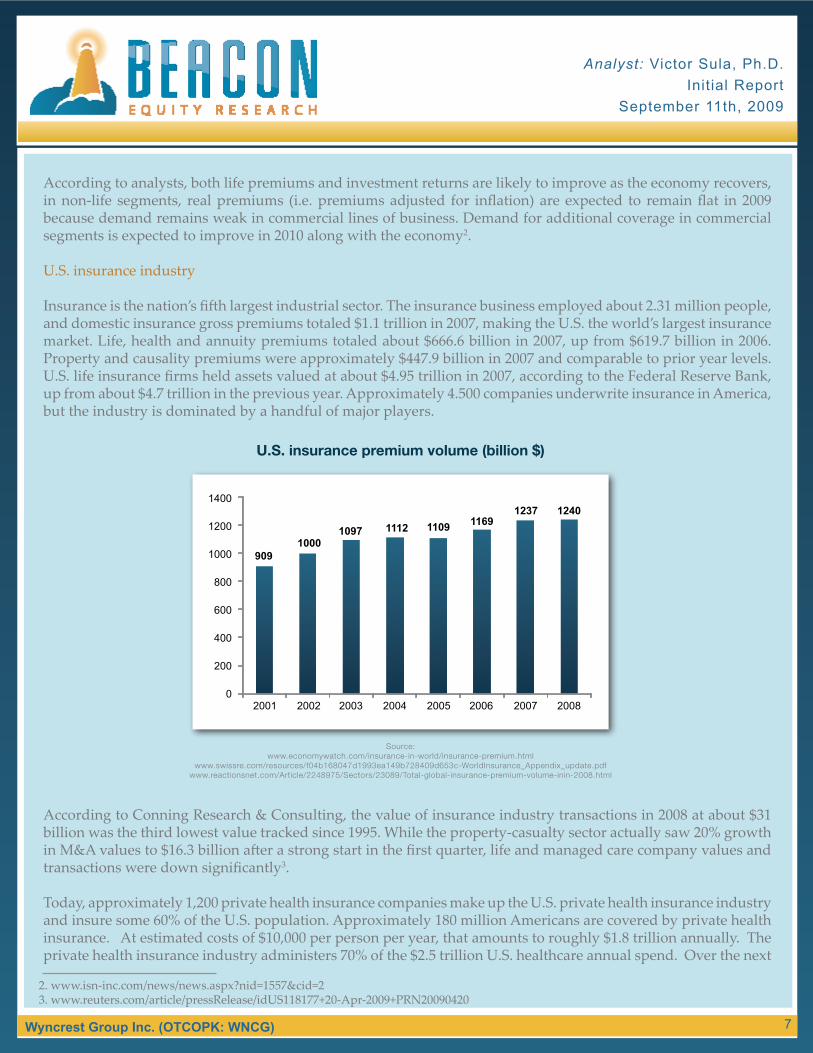

Global insurance premiums were $4.1 trillion in 2007. Premiums fell for the first time in 30 years in 2008 as the global recession hurt all segments of the insurance industry, with revenues and profits especially hard hit in life insurance. Life premiums dropped by 2%, according to a report released by Swiss Re, and non-life premiums shrank by 0.8%, compared to the previous year’s 15% growth. The global life insurance sector shrank by 3.5% last year after rising 5.1% in 2007.

The declines took place in most industrialized countries while emerging markets continued to register double-digit growth. North America had the biggest decline at 2.8% while the United Kingdom, Germany, Japan, Italy, Spain and Switzerland all experienced drops in premium volume. Sales remained strong in the newly industrialized Asian economies at 7.1% (down from a long-term trend of 8.7%) and increased marginally in a few European markets. Overall, global premium income rose slightly from $4.13 billion in 2007 to $4.27 billion in 20081.

As a result of the turmoil in financial markets last year, shareholder capital in the life insurance industry shrank by 30%-40% on average, with some companies suffering declines of up to 70%. Though financial markets remain vulnerable, values have stabilized recently, reducing pressure on asset prices and shareholder capital.

1. www.property-casualty.com/News/2009/6/Pages/Global-Insurance-Premiums-Fall-For-1st-Time-Since-1980.aspx

Industry Outlook

Analyst: Victor Sula, Ph.D.Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 7

According to analysts, both life premiums and investment returns are likely to improve as the economy recovers, in non-life segments, real premiums (i.e. premiums adjusted for inflation) are expected to remain flat in 2009 because demand remains weak in commercial lines of business. Demand for additional coverage in commercial segments is expected to improve in 2010 along with the economy2.

U.S. insurance industry

Insurance is the nation’s fifth largest industrial sector. The insurance business employed about 2.31 million people, and domestic insurance gross premiums totaled $1.1 trillion in 2007, making the U.S. the world’s largest insurance market. Life, health and annuity premiums totaled about $666.6 billion in 2007, up from $619.7 billion in 2006. Property and causality premiums were approximately $447.9 billion in 2007 and comparable to prior year levels. U.S. life insurance firms held assets valued at about $4.95 trillion in 2007, according to the Federal Reserve Bank, up from about $4.7 trillion in the previous year. Approximately 4.500 companies underwrite insurance in America, but the industry is dominated by a handful of major players.

According to Conning Research & Consulting, the value of insurance industry transactions in 2008 at about $31 billion was the third lowest value tracked since 1995. While the property-casualty sector actually saw 20% growth in M&A values to $16.3 billion after a strong start in the first quarter, life and managed care company values and transactions were down significantly3.

Today, approximately 1,200 private health insurance companies make up the U.S. private health insurance industry and insure some 60% of the U.S. population. Approximately 180 million Americans are covered by private health insurance. At estimated costs of $10,000 per person per year, that amounts to roughly $1.8 trillion annually. The private health insurance industry administers 70% of the $2.5 trillion U.S. healthcare annual spend. Over the next

2. www.isn-inc.com/news/news.aspx?nid=1557&cid=23. www.reuters.com/article/pressRelease/idUS118177+20-Apr-2009+PRN20090420

U.S. insurance premium volume (billion $)

Source: www.economywatch.com/insurance-in-world/insurance-premium.html

www.swissre.com/resources/f04b168047d1993ea149b728409d653c-WorldInsurance_Appendix_update.pdfwww.reactionsnet.com/Article/2248975/Sectors/23089/Total-global-insurance-premium-volume-inin-2008.html

Analyst: Victor Sula, Ph.D. Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 8

Analyst: Victor Sula, Ph.D. Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 8

10 years, private health insurance could potentially become a $24 trillion industry that includes $7.7 trillion of operational costs and income4.

According to Small Business Trends, premiums in the U.S. pet insurance industry rose 20% to $271 million last year from approximately $220 million in 2007. Premiums are forecast to grow to $328 million in 2009 and $500 million by 2012. At present, there are 11 pet insurance companies in the U.S. selling under 15 brands.

Offshore insurance

A booming economy requires large productivity gains, which in turn, requires rapid changes in technology and work processes. To meet these demands, large risks must be insured. Many insurers are moving offshore to obtain better investment returns on reserve funds (through significant tax incentives) and returning home with innovative insurance products that provide risk coverage for large industrial projects previously believed to be uninsurable5.

Bermuda is now the world’s largest offshore insurance market with approximately 1,650 insurance companies and insurance assets of $172.6 billion. Bermuda also dominates in offshore re-insurance and is the world’s third largest reinsurance market with 13 of the world’s top 40 reinsurers based in Bermuda, including American International Underwriters Group, HSBC Insurance Solutions, XL Capital Limited and ACE Limited.

Captive insurance

In the early 1960s, a number of major U.S. companies began forming their own insurance subsidiaries which today are known as “captives,” primarily in offshore financial centers. A captive insurance company is usually a subsidiary of a large company and is formed to offer insurance to the parent company or group, thus reducing outside costs and generating profits by locating in low tax jurisdictions. Tax benefits are not necessarily the driving factor but can be substantial. As with traditional insurance, captive companies are essentially self-insuring against certain risks. However, this method of self-insurance does generate valid deductions since the premium payments to the captive company are deductable. Big financial services companies typically spend $25 million to $100 million a year on insurance coverage. Insuring through a captive can cut these costs by 5% to 20%.

4. www.democracyforamerica.com/groups/544-democracy-for-washington/blog_posts/28413-analysis-of-private-health-insurance-industry-2-trillion-%E2%80%9Csavings%E2%80%9D-proposal 5. www.allbusiness.com/business-finance/business-insurance/1170899-1.html

Traditional Insurance Captive Insurance

Source: http://thecaptiveblog.com/diagrams.html

Analyst: Victor Sula, Ph.D.Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 9

The growth of the captive insurance industry through the 1980s and 1990s was dramatic, although major changes in international business sentiment resulting from events such as Hurricane Andrew and the 9/11 attacks resulted in temporary setbacks. One-parent captives were followed offshore by reinsurance companies, both because the captives needed to reinsure and because a reinsurance subsidiary can assist its insurance parent in the same way an insurance captive helps its corporate parent6.

Many captive insurers make their home offshore in Belize, Bermuda, The Cayman Islands, Guernsey, Luxembourg, Barbados, Malta, Singapore and the British Virgin Islands. Overall, there are more than 50 jurisdictions actively competing for a slice of the captive pie. Bermuda is the leading captive domicile, although its market dominance has declined as many other jurisdictions have enacted captive-friendly legislation to attract or preserve this business.

In the United States, Vermont is home to more captive insurers than any other U.S. state, with more than 800 licensed captive companies. More than 560 U.S. companies, including Wal-Mart, Starbucks and McGraw-Hill have set up Vermont-based captive entities to insure major risks and liabilities and gain a tax benefit in the process. Vermont now rivals the Cayman Islands and Bermuda as the insurance destination of choice for American companies. Other U.S. states with significant numbers of captive insurers include Hawaii, South Carolina, Arizona, Montana, Nevada and New York7.

6. www.lowtax.net/newsletter/content_update_VIII.asp7. Source : www.nytimes.com/2007/04/04/business/04vermont.html

Main captive domiciles (100% = 4966 companies)

Source: http://en.wikipedia.org/wiki/Captive_insurance

Analyst: Victor Sula, Ph.D. Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 10

Analyst: Victor Sula, Ph.D. Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 10

WNCG’s Southwest Financial Group subsidiary is a commission and fee-based business. It markets intangible assets requiring no inventories. Most sales are made through commissioned sales representatives who do most of their own marketing and prospecting.

When WNCG sells an insurance product owned by another company, it receives commission income on the sale. The total value of the sale is not recorded as revenue because it does not pass through WNCG hands. The Company records only commission income.

Vermont captive insurers’ growth

Source : www.nytimes.com/2007/04/04/business/04vermont.html

Financial Analysis

Total Income, includingCommision Income Other incomeTotal Operating Expenses, includingProfessional Fees Payroll & Commissions expensesOther operating expensesOperating IncomeOther Income/ExpenseNet IncomeEPS

667,110516,335150,774

1,778,5981,275,674

296,905206,019

-1,111,48934,905

-1,076,583-0.36

1,077,8961,075,096

2,8002,461,1591,464,425

698,640298,094

-1,383,263-4,317

-1,387,581-0.40

61.6%108.2%-98.1%38.4%14.8%

135.3%44.7%

n/mn/mn/mn/m

283,820269,649

14,170405,848174,403126,562104,883

-122,028-747

-122,775

2007 2008 % Chg 2Q 09

Income Statement, $

Source: Company 10-Q and 10-K reports

Analyst: Victor Sula, Ph.D.Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 11

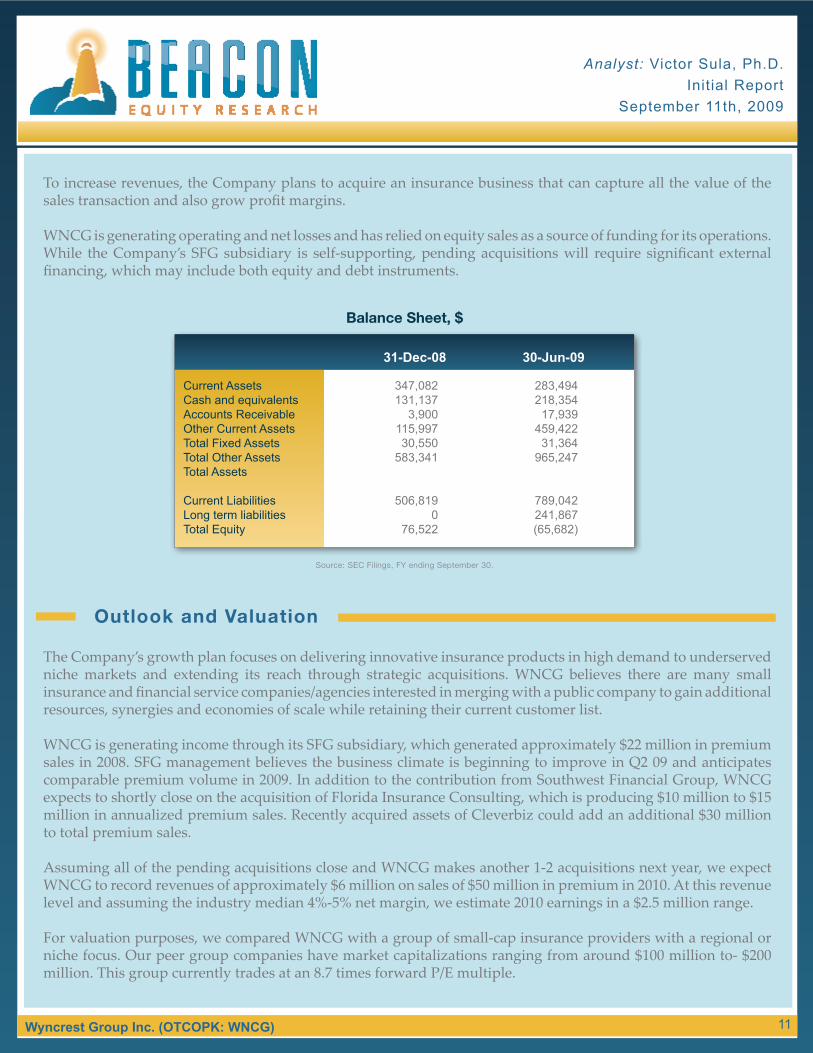

To increase revenues, the Company plans to acquire an insurance business that can capture all the value of the sales transaction and also grow profit margins.

WNCG is generating operating and net losses and has relied on equity sales as a source of funding for its operations. While the Company’s SFG subsidiary is self-supporting, pending acquisitions will require significant external financing, which may include both equity and debt instruments.

The Company’s growth plan focuses on delivering innovative insurance products in high demand to underserved niche markets and extending its reach through strategic acquisitions. WNCG believes there are many small insurance and financial service companies/agencies interested in merging with a public company to gain additional resources, synergies and economies of scale while retaining their current customer list.

WNCG is generating income through its SFG subsidiary, which generated approximately $22 million in premium sales in 2008. SFG management believes the business climate is beginning to improve in Q2 09 and anticipates comparable premium volume in 2009. In addition to the contribution from Southwest Financial Group, WNCG expects to shortly close on the acquisition of Florida Insurance Consulting, which is producing $10 million to $15 million in annualized premium sales. Recently acquired assets of Cleverbiz could add an additional $30 million to total premium sales.

Assuming all of the pending acquisitions close and WNCG makes another 1-2 acquisitions next year, we expect WNCG to record revenues of approximately $6 million on sales of $50 million in premium in 2010. At this revenue level and assuming the industry median 4%-5% net margin, we estimate 2010 earnings in a $2.5 million range.

For valuation purposes, we compared WNCG with a group of small-cap insurance providers with a regional or niche focus. Our peer group companies have market capitalizations ranging from around $100 million to- $200 million. This group currently trades at an 8.7 times forward P/E multiple.

Current AssetsCash and equivalentsAccounts Receivable Other Current Assets Total Fixed Assets Total Other Assets Total Assets

Current LiabilitiesLong term liabilitiesTotal Equity

347,082131,137

3,900115,997 30,550

583,341

506,8190

76,522

283,494218,354

17,939459,422

31,364965,247

789,042241,867(65,682)

31-Dec-08 30-Jun-09

Balance Sheet, $

Source: SEC Filings, FY ending September 30.

Outlook and Valuation

Analyst: Victor Sula, Ph.D. Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 12

Analyst: Victor Sula, Ph.D. Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 12

We note that WNCG’s aggressive acquisition program could require substantial equity financing and be dilutive to existing shareholders. We estimate equity sales will increase WNCG’s number of shares outstanding from approximately 47 million currently to 50 million in 2010. Using our $2.5 million earnings estimate and 50 mil-lion shares outstanding, we derive a 2010 EPS estimate of $0.05. We apply the peer group 8.7 times forward P/E multiple to our $0.05 EPS estimate to obtain our $0.43 target price for WNCG shares.

Accordingly, we are initiating coverage of The Wyncrest Group Inc., with a Speculative Buy rating and a $0.43 price target. However, we strongly advise investors to consider the risks discussed below, which accentuate the “Speculative” aspect of our rating.

Mercer Insurance Group Inc. Specialty Underwriters’ Alliance Inc.Hallmark Financial Services Inc. Nymagic Inc. American Safety Insurance Holdings Ltd. Kingsway Financial Services Inc. American Physicians Service Group Inc. United America Indemnity Ltd Median

Wyncrest Group Inc.

MIGPSUAIHALLNYMASIKFS

AMPHINDM

WNCG

18.176.406.67

17.1913.773.07

22.695.16

0.09

117101139145142169157164

0.37

8.7818.29

5.3415.21

7.52n/m

8.106.888.10

8.6520.00

5.4718.48

7.1343.86

8.737.708.69

5.38%3.25%4.63%

n/m-0.08%

-32.47%27.59%

n/m3.94%

Company NameJul-29-2009

Tickersymbol

Shareprice $ 2009E

P/E2010E

Mrkt. Cap.$ Mn

Net profitmargin, ttm

Comparative analysis

Source: Yahoo Finance

Analyst: Victor Sula, Ph.D.Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 13

Inherent business risks

The Company is undertaking an aggressive acquisition program to capitalize on currently undervalued assets and generate synergies and economies of scale. However WNCG’s progress can be impeded by any of the follow-ing: 1) failure to find and close acquisition; 2) inability to generate desired synergies or economies of scale through integration; 3) inability to secure acquisition funding; 4) increased competition due to greater visibility; and 5) a competitive and rapidly changing operating environment.

Going concern risks

The Company is not currently profitable and relies on external financing to fund its operations. There is no guar-antee that WNCG will be able to implement its business plan or ever build a profitable business.

Intense competition

The financial services market is highly competitive. There are many companies, both public and private, involved in offshore insurance and niche financial services operations that have superior access to capital, larger marketing and sales budgets and greater visibility than WNCG. There is no assurance that WNCG can compete successfully.

Need for additional funding

The Company has incurred losses from operations and has minimal cash, which raise substantial doubts about its viability as a going concern. WNCG must secure additional capital to implement its acquisition plan. There is no guarantee that it can raise the necessary funding on favorable terms, if at all. In addition, issuing debt increases financial risk and selling equity dilutes the interests of current shareholders.

Risk Factors

Analyst: Victor Sula, Ph.D. Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 14

Analyst: Victor Sula, Ph.D. Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 14

Management

Bill McFarland recently sold his last auto dealership after 32 years in the business. He spent his first six years in sales and sales management, assisting dealers in building “sales volume” and creating “complete satisfaction” before these terms became industry buzzwords. He spent the next eight years in finance and insurance, building lending relations between finance institutions and his customers. From 1990 until re-cently, Mr. McFarland owned and operated four automotive dealerships in the Chicago metro market. He built multiple sales and management teams with the ability to react quickly to the changing marketplace while consistently exceeding customer expectations, a key factor in the success of his dealerships. Mr. Mc-Farland also served as president of Steel City Reinsurance Company from 1995 through 2005. Steel City Life was an offshore insurance company licensed in Illinois to sell life and disability insurance products as well as automobile warranty service agreements.

Bill McFarlandChairman

Keith Lanzara is responsible for creating the business base for providing financial services to offshore insurance captive corporations, catastrophic insurance, aviation insurance and extended warranties. Mr. Lanzara brings to his position more than 25 years of leadership, management and executive experience. He successfully built, managed and operated auto dealerships in the world’s largest automotive market and directed all marketing, sales and business development activities for these businesses for 25 years before leaving to join WNCG as CEO.

Mr. Lanzara was instrumental in growing companies from small family-owned operations into large, re-gionally recognized names, with more than a dozen locations in the Chicago area. He worked in vari-ous capacities for several automobile franchises including Chrysler, Dodge, Ford, Honda, Hyundai, Jeep, Oldsmobile and Pontiac.

Keith LanzaraCEO/President

Chris Zaal has been in the financial services and insurance industry for more than 26 years. He began his career in 1980 with Penn Corp Financial in Silver Springs, Maryland, working as an independent sales agent. In 1981, Mr. Zaal became a participating partner and moved to Oklahoma City to open a branch office. The Oklahoma office grew to become one of the top three Penn Corp. offices. In 1986, he became regional manager for Oklahoma and Texas and grew his regional office into Penn Corp. Financial’s No. 1 sales region.

In October of 1992, Mr. Zaal formed Z&Z International Inc., combining two marketing groups - Southwest Financial Group and American Teacher Retirement Services. SFG has grown to more than 18,000 customers nationwide, 85 agents and $22 million in annualized gross premium sales.

Christopher A. ZaalSouthwest Finance Group President/CEO

Richard Whitaker has worked within the Southwest Financial Group network of contacts and agents for the last five years. He has extensive sales and marketing experience. He obtained his general insurance li-cense and securities license in 1998 and opened his own branch office, which quickly grew to 20 agents and $5.0 million in annual sales. From 2002 to 2005, Mr. Whitaker owned and operated a marketing organiza-tion that recruited, trained, and facilitated new agents in the insurance, financial, and mortgage industries. During that period, Mr. Whitaker recruited and trained some 4,000 agents and opened new branch offices in three different states.

In 2005, Mr. Whitaker was approached by a group of investors to set up and ultimately lead a mortgage bank as CEO. The mortgage bank produced $1.0 million in gross revenues in its first year and opened branch offices in five states. In 2008, Mr. Whitaker became vice-president of a large mortgage bank and facilitated 100% growth in its business in one year.

Richard WhitakerSouthwest Finance Group Vice-President of Sales & Marketing

Analyst: Victor Sula, Ph.D.Initial Report

September 11th, 2009

Wyncrest Group Inc. (OTCOPK: WNCG) 15

Disclaimer

DO NOT BASE ANY INVESTMENT DECISION UPON ANY MATERIALS FOUND ON THIS REPORT. We are not registered as a securities broker-dealer or an investment adviser either with the U.S. Securities and Exchange Commission (the “SEC”) or with any state securities regulatory authority. We are neither licensed nor qualified to provide investment advice.

The information contained in our report should be viewed as commercial advertisement and is not intended to be investment advice. The report is not provided to any particular individual with a view toward their individual circumstances. The information contained in our report is not an offer to buy or sell securities. We distribute opinions, comments and information free of charge exclusively to individuals who wish to receive them.

Our newsletter and website have been prepared for informational purposes only and are not intended to be used as a complete source of information on any particular company. An individual should never invest in the securities of any of the companies profiled based solely on information contained in our report. Individuals should assume that all information contained in the report about profiled companies is not trustworthy unless verified by their own independent research.

Any individual who chooses to invest in any securities should do so with caution. Investing in securities is speculative and carries a high degree of risk; you may lose some or all of the money that is invested. Always research your own investments and consult with a registered investment advisor or licensed stock broker before investing.

The report is a service of BlueWave Advisors, LLC, a financial public relations firm that has been compensated by the companies profiled. All direct and third party compensation received has been disclosed within each individual profile in accordance with section 17(b) of the Securities Act of 1933. This compensa-tion constitutes a conflict of interest as to our ability to remain objective in our communication regarding the profiled companies. BlueWave Advisors, LLC, and/or its affiliated will hold, buy, and sell securities in the companies profiled. When compensated in shares, all readers should be aware that is our policy to liquidate all shares immediately. We reserve the right to buy or sell the shares of any the companies mentioned in any materials we produce at any time. This compensation constitutes a conflict of interest as to our ability to remain objective in our communication regarding the profiled companies. BeaconEquity is a Web site wholly owned by BlueWave Advisors, which has been compensated six thousand five hundred dollars from WNCG as a marketing budget to manage a comprehensive investor awareness program including the creation and distribution of this report as well as other investor relations efforts.

Information contained in our report will contain “forward looking statements” as defined under Section 27A of the Securities Act of 1933 and Section 21B of the Securities Exchange Act of 1934. Subscribers are cautioned not to place undue reliance upon these forward looking statements. These forward looking state-ments are subject to a number of known and unknown risks and uncertainties outside of our control that could cause actual operations or results to differ ma-terially from those anticipated. Factors that could affect performance include, but are not limited to, those factors that are discussed in each profiled company’s most recent reports or registration statements filed with the SEC. You should consider these factors in evaluating the forward looking statements included in the report and not place undue reliance upon such statements.

We are committed to providing factual information on the companies that are profiled. However, we do not provide any assurance as to the accuracy or com-pleteness of the information provided, including information regarding a profiled company’s plans or ability to effect any planned or proposed actions. We have no first-hand knowledge of any profiled company’s operations and therefore cannot comment on their capabilities, intent, resources, nor experience and we make no attempt to do so. Statistical information, dollar amounts, and market size data was provided by the subject company and related sources which we believe to be reliable.

To the fullest extent of the law, we will not be liable to any person or entity for the quality, accuracy, completeness, reliability, or timeliness of the information provided in the report, or for any direct, indirect, consequential, incidental, special or punitive damages that may arise out of the use of information we provide to any person or entity (including, but not limited to, lost profits, loss of opportunities, trading losses, and damages that may result from any inaccuracy or incompleteness of this information).

We encourage you to invest carefully and read investment information available at the websites of the SEC at http://www.sec.gov and FINRA at http://www.finra.org.

All decisions are made solely by the analyst and independent of outside parties or influence.

I, Victor Sula, Ph.D, the author of this report, certify that the material and views presented herein represent my personal opinion regarding the content and securities included in this report. In no way has my opinion been influenced by outside parties, nor has my compensation been either directly or indirectly tied to the performance of any security listed. I certify that I do not currently own, nor will own and shares or securities in any of the companies featured in this report.

Victor Sula, Ph.D. - Senior Analyst

Victor Sula, Ph.D. has held the position of Senior Analyst with several independent investment research firms since 2004. Prior to 2004, Mr. Sula held Senior Financial Consultant positions within the World Bank sponsored Agency for Restructuring and Enterprise Assistance and TACIS sponsored Center for Produc-tivity and Competitiveness of Moldova, where he was involved in corporate reorganization and liquidation. He is also employed as Associate Professor at the Academy of Economic Studies of Moldova. Mr. Sula earned his Ph.D. degree in 2001 and bachelor’s degree in Finance in 1997 from the Academy of Economic Studies of Moldova. Mr. Sula is currently a level III candidate in the CFA program.