Ws Day 2015

25

Wilson Sons Meet the Management Day 2015

-

Upload

wilsonsonsri -

Category

Documents

-

view

143 -

download

0

Transcript of Ws Day 2015

Wilson SonsMeet the Management Day 2015

What Drives Wilson Sons?

2

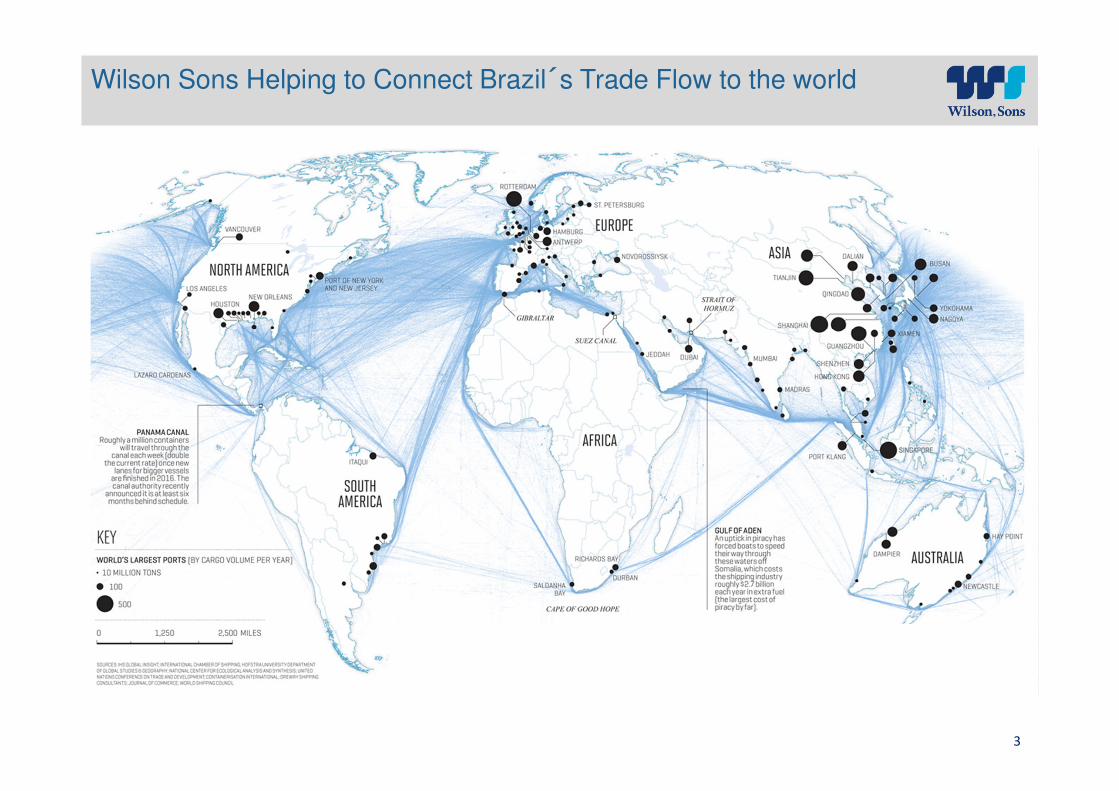

Trade Flow

Wilson Sons Helping to Connect Brazil´s Trade Flow to the world

3

4

Total Trade to GDP ratio in BrazilSource: World Bank

25.3% 25.1%27.1%

21.9% 22.3%24.1%

26.1% 27.0%

52.2% 52.6%54.4%

47.0%

51.7%

55.1% 55.4% 55.6%

2006 2007 2008 2009 2010 2011 2012 2013

Brazil Average of G7

Trade Flow Value v Tonnes (2009 - 2014)

5

Trade Flow (US$ Billion)Source: Central Bank 2014

CAGR: 10.1% CAGR: 5.8%

Trade Flow (Billion tonnes)Source: Central Bank 2014

280.7

383.6

482.2465.7 481.7

454.2

2009 2010 2011 2012 2013 2014

559.3

658.3692.9 688.0

718.0742.0

2009 2010 2011 2012 2013 2014

1Q2015 Trade Flow Value v Trade Tonnes

6

Trade Flow (US$ Billion)Source: Central Bank 2014

Change: -13.4% Change: 9.0%

36.1 30.5

33.9

27.0

35.1

33.4

1Q14 1Q15

March

February

January

105.2

91.1

54.2 54.8

50.0 51.2

53.065.4

1Q14 1Q15

March

February

January

157.3

171.5

Trade Flow (Billion tonnes)Source: Central Bank 2014

Export Trade Partner Distribution

7

40.6

27.0

14.2

13.0

6.7

6.6

4.9

4.7

4.6

4.0

China

US

Argentina

Netherlands

Japan

Germany

Chile

India

Venezuela

Italy

Main Export Partners (US$ Million)Source: MDIC 2014

Main Product Export PartnersSource: MDIC 2014 and FMI 2015

Brazil - -1,0

World - 3,5

CountryShare of Brazil

Total Exports (%)

Projection (Real

GDP 2015)

China 18.0 6.8

United States 12.0 3.1

Argentina 6.3 -0.3

Netherlands 5.8 1.6

Japan 3.0 1.0

Germany 2.9 1.6

Chile 2.2 2.7

India 2.1 7.5

Venezuela 2.1 -7.0

Italy 1.8 0.5

Main partners weighted

average3.2

How do we see our trade flow driven assets?

8

This picture is property of Wilson Sons and can not be used or reproduced without written permission

Wilson Sons Container Terminal Efficiency Reduces Turnaround and Waiting Time for Shipowners

9Tecon Rio Grande

Road Access BR 392 conected to BR-471,

BR-116 e BR-293

Rail Access –Malha Sul operated

by Brado Logistica

Tecon Rio Grande

Inland Waterway Access via Lagoa dos Patos

This picture is property of Wilson Sons and can not be used or reproduced without written permission

Wilson Sons Container Terminals Create new Transport solutions for Exporters and Importers

10

Soya - New Product Containerisation -Tecon Rio Grande

Rice in Tecon Rio Grande

Celullose in Tecon Salvador

11

1.1 1.11.2

1.4

1.71.8

2.2

2008 2009 2010 2011 2012 2013 2014

Cabotage Growth in Brazil (# TEU M)Source: Datamar

Historical CAGR 12.2%

5,000 tons of cargo requiries:

- Cabotage: 1 vessel; or

- Rail: 72 railway carriages; or

- Road: 143 trucks.

Cabotage – National growth and growing importance for Wilson Sons

Comparative between transport typesSource: Confederação Nacional do Transporte (CNT) 2013

Transport distribution in Brazil (% tons)Source: Adapted from ILOS 2014

Historical CAGR 8.9%

51.9 53.7

66.672.7 71.6

80.986.8

2008 2009 2010 2011 2012 2013 2014

Cabotage at Wilson Sons Terminals (# TEU ‘000)Source: Wilson Sons (Tecon SSA + Tecon RG)

65.6%

19.5%

9.6%

3.4%1.8%

0.1%

Road

Rail

Cabotage

Pipeline

Water way

Air

12

Towage – Meeting the demand throughout Brazils PortsSource Wilson Sons As of March/2015

North8 tugboats

Northeast33 tugboats

Southeast21 tugboats

South14 tugboats

173,694,974

170,521,854

161,139,464

144,233,177

53,335,016

50,242,097

44,968,614

44,843,492

40,023,838

85,851,207

Rio de Janeiro

Espírito Santos

São Paulo

Maranhão

Rio grande do sul

Pará

Paraná

Santa catarina

Bahia

Others

Total cargo handled in Brazil in 2014 (ton.)Source: ANTAQ, 2014

This picture is property of Wilson Sons and can not be used or reproduced without written permission

Wilson Sons Towage increases berth productivity for ports and helps ship owners reduce fuel consumption with increased safety

13

Special Operation for Fire in the port of Santos

This picture is property of Wilson Sons and can not be used or reproduced without written permission

Wilson Sons Towage COR increases berth productivity for ports and helps ship owners reduce fuel consumption with increased safety

14

Towage Centralised Operations Room (COR)

What Drives Wilson Sons?

15

Oil & Gas

16

Oil and Gas is a Relevant and Increasing Part of Brazils GDP

The importance of Oil sector to the Brazilian GDPSource: IBP 2014

Contribution of Oil sector to the Brazilian GDP

0%

3%

6%

9%

12%

15%

-

100.0

200.0

300.0

400.0

500.0

Oil sector contribution to the Brazilian GDP, 2009 (R$ Billion) Participation in the Brazilian GDP

17

3.016.0

42.0

119.0

169.0

301.0

412.0

2008 2009 2010 2011 2012 2013 2014

The growing Brazilian Pre-Salt Oil Production (k bpd)Source: Petrobras

Pre-salt fields alreadycontributes more than27% of total oilproduction in Brazil

Brazil Has Significant and Increasing Oil Reserves and Production Particularly in Presalt

18

Wilson Sons Helping to Unlock Brazils Oil and Gas

125 km

Average Campos Basin Distances

300 km

Pre-salt Distances

Significantly Increased Distances to new Oil Rigs

Offshore Vessels – Global Fleet Utilisation v Brazil Fleet UtilisationSource: Offshore Merchant Partners AS (15 May 2015)

19

How do we see our Oil & Gas driven assets?

20

21

BRAZIL

AR

UY

CH

BO

PA

PE

Buenos Aires

Montvideo

Equatorial Margin

5% current OSV fleet

North - East

15% of current OSV fleet

Santos, Campos and Espírito Santo

80% of current OSV fleet 91% of O&G production in Brazil

The Evolving Exploration of Brazils Oil Reserves

Guarujá II Facilities

Wilson Sons Shipyard Consistently Delivering World Class Vessels

23

43.9 45.773.0

86.9109.0 109.2 108.3

152.0 146.3

182.8160.1

4.0 3.4

3.24.5

12.9 19.2 13.1

11.3 16.0

23.139.2

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

EBITDA (IFRS)

EBITDA (Offshore Vessels)

47.9 49.1

76.291.4

122.7 128.4 121.4

163.3 162.3

205.9 199.3

EBITDA

Costs

Revenue

R$ Source/Denominated

US$ Source/Denominated

Net Revenues (Proforma) not correlated to exchange rate US$ M

EBITDA (Proforma) not correlated to exchange rate US$ M

Net Revenues & EBITDA

CAGR: 12.6%

CAGR: 15.3%

Estimated (Proforma) Revenue, Costs and EBITDA(Year ended Dec/14)

Annual Average Exchange RatesUS$ - R$

CAGR: -2.2%

10%90%

53% 47%

211.2278.0

325.7393.3

476.7 439.8547.6

656.6610.4

660.1 633.5

6.5

7.28.4

10.7

21.6 38.1

28.0

41.447.0

54.4 76.8

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

Net Revenues (IFRS)

Net Revenues (Offshore Vessels)

217.7

285.2334.1

404.0

498.3477.9

575.6

657.4698.0 714.5 710.3

2.93

2.43

2.18

1.951.84

1.99

1.761.67

1.96

2.162.35

2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014

24

What is important for the current market conditions

• Safe and efficient operations

• Solid balance sheet and financial flexibility

• Operational , Client and Driver diversity

• Strong customer base and relationships (+ 2 000 clients)

• CAPEX optimization

• Return capital to shareholders including dividends

Thank you. Questions?