Woven and Knit Fabrics - InfoHouseinfohouse.p2ric.org/ref/27/26112.pdf · Woven and Knit Fabrics...

6

Woven and Knit Fabrics The woven and knit fabrics industry consists of establishments engaged in the production of a variety of fabrics from yarn (see Table 1). Woven and knit fabrics are used in apparel, industrial and home furnishing applications, including clothing, drapery, upholstery, towels, sheeting, belts, typewriter ribbons and hosiery. Shipments of all textile products slowed in 1988, but the effecton domestic fabric producers was reduced by a slight shift to sourcing fabrics domestically. The slack demand for textile end products was especially evident in the market for unfinished, undyed fabrics (greige goods). By mid-1988, the inventories of fabric producers began to climb, as fabric users saw little need to purchase in excess of current requirements until clear-cut signals of strengthened consumer demand was evident. Shipments of manmade fiber broadwoven fabric rose sharply in 1987and climbed another 8.2 percent, to $10 billion, in 1988. This sector benefitted from the increased use of manmade fibers in blends with natural fibers for apparel, as well as continued growth in the industrial fabric market in which manmade fibers dominate. Ship- ments of woven cotton declined 4.5 percent in constant dollars in 1988 after two successive years of growth. problems facing U. S. textile mills. In the first quarter of 1990, textile and apparel imports alone repre- sented over 30 percent of the US. trade deficit. Textile and apparel imports for 1989 showed a 13 percent gain over 1987's record- breaking figure. Fabric imports alone were up 26 percent in 1989 (see Figure 1). This double-digit import growth is occurring at a time when the textile market is expecting sluggish growth in 1990 (about 1 percent). Technological developments and market forces are causing structural changes in this industry. Vertical integration is becoming common- place, as major fabric producers acquire interests in yarn production facilities and/or apparel companies. Horizontal integration is also taking place with increasing frequency. Mergers, acquisitions, restructurings and consolidations have become common. Recently, Burlington Industries went private and sold off several divisions. Also, West Point- Imports are still one of the major SIC 221-225 Pepperell acquired much of J. P. Stevens, but was then acquired by the Farley Group. In knitting, the major change has been the rapid growth of Sara Lee, which has purchased L'eggs, Hanes, Stedman and Pannill. The ongoing structural changes make it difficult to provide an up- to-date, accurate listing of the leading companies. Nevertheless, some of the major players can be

-

Upload

dangnguyet -

Category

Documents

-

view

229 -

download

2

Transcript of Woven and Knit Fabrics - InfoHouseinfohouse.p2ric.org/ref/27/26112.pdf · Woven and Knit Fabrics...

Woven and Knit Fabrics

The woven and knit fabrics industry consists of establishments engaged in the production of a variety of fabrics from yarn (see Table 1). Woven and knit fabrics are used in apparel, industrial and home furnishing applications, including clothing, drapery, upholstery, towels, sheeting, belts, typewriter ribbons and hosiery.

0

Shipments of all textile products slowed in 1988, but the effect on domestic fabric producers was reduced by a slight shift to sourcing fabrics domestically. The slack demand for textile end products was especially evident in the market for unfinished, undyed fabrics (greige goods). By mid-1988, the inventories of fabric producers began to climb, as fabric users saw little need to purchase in excess of current requirements until clear-cut signals of strengthened consumer demand was evident.

Shipments of manmade fiber broadwoven fabric rose sharply in 1987 and climbed another 8.2 percent, to $10 billion, in 1988. This sector benefitted from the increased use of manmade fibers in blends

with natural fibers for apparel, as well as continued growth in the industrial fabric market in which manmade fibers dominate. Ship- ments of woven cotton declined 4.5 percent in constant dollars in 1988 after two successive years of growth.

problems facing U. S. textile mills. In the first quarter of 1990, textile and apparel imports alone repre- sented over 30 percent of the US. trade deficit. Textile and apparel imports for 1989 showed a 13 percent gain over 1987's record- breaking figure. Fabric imports alone were up 26 percent in 1989 (see Figure 1). This double-digit import growth is occurring at a time when the textile market is expecting sluggish growth in 1990 (about 1 percent).

Technological developments and market forces are causing structural changes in this industry. Vertical integration is becoming common- place, as major fabric producers acquire interests in yarn production facilities and/or apparel companies. Horizontal integration is also taking place with increasing frequency. Mergers, acquisitions, restructurings and consolidations have become common. Recently, Burlington Industries went private and sold off several divisions. Also, West Point-

Imports are still one of the major

SIC 221-225

Pepperell acquired much of J. P. Stevens, but was then acquired by the Farley Group. In knitting, the major change has been the rapid growth of Sara Lee, which has purchased L'eggs, Hanes, Stedman and Pannill.

The ongoing structural changes make it difficult to provide an up- to-date, accurate listing of the leading companies. Nevertheless, some of the major players can be

Table 1

Woven and Knit Fabrics Industry: Basic Statistics (1987)

EMPLOYMENT DATA (1,000)

Prod. SIC Industry Employees Wkers.

2211 2221 2231 2241 2251 2252 2253 2254 2257 2258 2259

Cotton Manmade Fibers/Silk Wool Narrow Woven Women's Hosiery, Hosiery, N.E.C.** Knit Outerwear Knit Underwear Weft Knits Warp Knits Knitting, N.E.C.**

Total *Excluding socks **N.E.C = NoI Elsewhem Classified

72.5 89.1 15.0 19.0 29.3 36.5 59.6 20.0 34.6 20.1 3.2

398.9

65.0 77.6 13.0 16.1 25.9 32.5 51 .O 18.1 29.1 16.5 2.7

347.5

OPERATING STATISTICS (MILLION DOLLARS)

Ship- Value New Cap. Cost of ments Added Expend. Materials Payroll

5,516.1 8,136.6 1,086.7 1,179.7 1,496.7 1,952.3 3,199.7 1,086.1 3,548.3 1,953.9

168.3

29,324.4

2,607.7 3,646.2

507.1 609.9 769.0 960.1

1,641.3 534.9

1,408.2 7,64.1

82.5

13,531.0

199.0 315.9 39.8 33.8 32.3 64.6 95.2 32.1 94.2 65.6 5.3

977.8

2,922.6 4,541.9

593.5 572.5 715.2

1,009.0 1,603.9

557.9 2,169.5 1,168.5

86.9

15,941.4

1,262.7 1,610.4

243.9 304.4 385.7 467.8 848.6 288.3 573.1 379.2 43.3

6,407.4

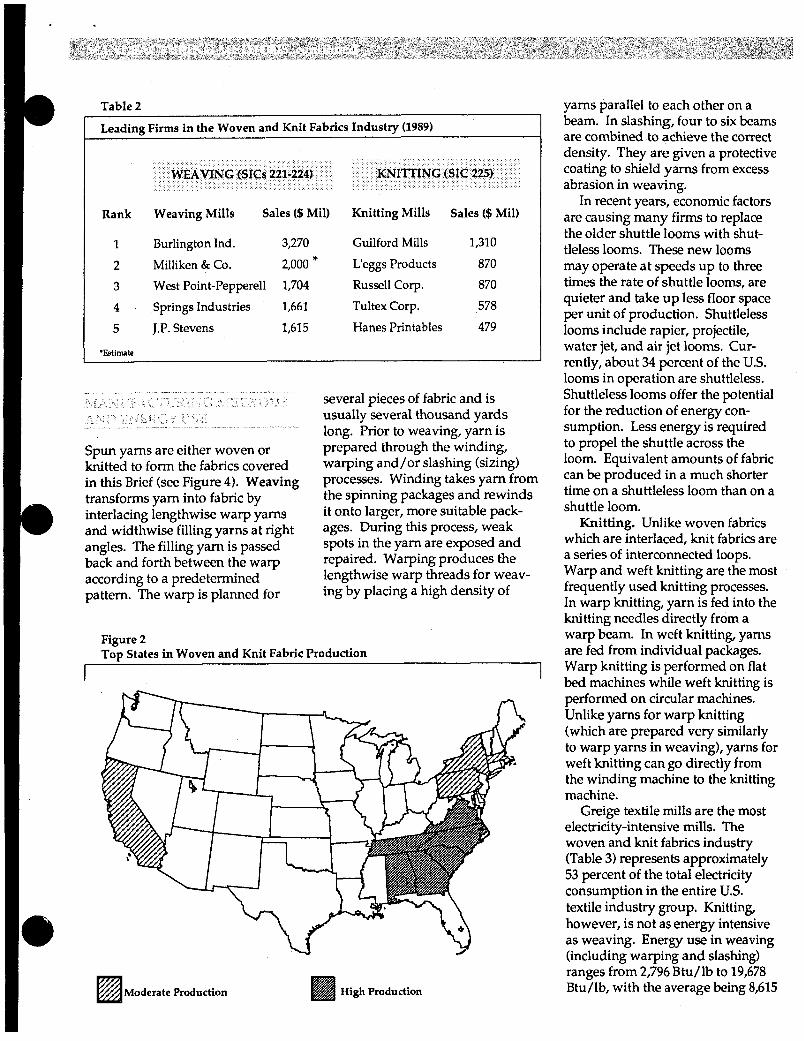

identified (see Table 2). Despite the presence of large, dominant firms such as Burlington and Milliken, the industry remains fairly diverse, with hundreds of small companies.

Although many states have some textile mill operations, the woven and knit fabrics industry is concen- trated in the southeast. Over 60

Figure 1 US. Textile and Apparel Imports/Exports

9 $ Billions

35 I

19~~-Rev iaed ,1989-Es t imrte ,1990-Fo~t Sourcer: American Textile Mfm. 1st.; DRU McGraw-Hill Inr

percent of knitting shipments and over 75 percent of weaving ship- ments are from southeastem states. The northeastern states produce about 30 percent of knitting ship- ments (see Figure 2).

Firms in the woven and knit fabrics industry are dependent on yam suppliers for quality yarns. The price and availability of natural yams are affected by the weather and other factors. Many fabric formation firms have interests in natural, spun yam operations, but most of the woven and knit fabric firms are still largely dependent on fiber producers for manmade filament yams. Lycra, which has become popular in several apparel applications, has been an especially difficult yarn to purchase in large quantities. In recent years, the large increase in demand has surpassed the production capability of suppliers.

The U. S. depends on foreign technology for textile production machinery. The problems associ- ated with the purchase and installa- tion of foreign technology keep many small mills operating with outdated and obsolete machinery.

The importance of using the latest technology is increasing, as the U.S. struggles to gain advantages in productivity over its foreign com- petitors.

The plant closings in the mid- 1980's contributed to the decline in production workers, but much of the recent worker shrinkage has been due to increased emphasis on productivity and automation. The use of modern technology for production equipment and for process monitoring has increased efficiency and productivity. A recent estimate shows efficiency gains in the past couple of years to be in the 5 percent range, higher than the average for the entire U.S. manufacturing sector. Textile mill production efficiency is expected to rise by 3 percent a year through the end of this century.

The high capacity utilization rates shown in Figure 3 (97.7 percent capacity in 1989) are sup- ported by strong plant and equip ment spending. These capital outlays will likely rise 10 percent in 1990, and most outlays will go toward increasing productivity.

I Table 2

Leading Firms in the Woven and Knit Fabrics Industry (1989)

WEAVING (SICS 221-224) KNITTING (SIC 225)

Rank Weaving Mills Sales ($ Mil) Knitting Mills Sales ($ Mil)

1 Burlington Ind. 3,270 Guilford Mills 1,310

2 Milliken & Co. 2,000 * Leggs Products 870 3 West Point-Pepperell 1,704 Russell Corp. 870 4 Springs Industries 1,661 Tultex Corp. 578 5 J.P. Stevens 1,615 Hanes Printables 479

‘Estimate

Spun yams are either woven or knitted to form the fabrics covered in this Brief (see Figure 4). Weaving transforms yam into fabric by interlacing lengthwise warp yams and widthwise filling yarns at right angles. The filling yam is passed back and forth between the warp according to a predetermined pattem. The warp is planned for

several pieces of fabric and is usually several thousand yards long. Prior to weaving, yarn is prepared through the winding, warping and/or slashing (sizing) processes. Winding takes yam from the spinning packages and rewinds it onto larger, more suitable pack- ages. During this process, weak spots in the yarn are exposed and repaired. Warping produces the lengthwise warp threads for weav- ing by placing a high density of

Figure 2 Top States in Woven and Knit Fabric Production

Moderate Production High Production

yams parallel to each other on a beam. In slashing, four to six beams are combined to achieve the correct density. They are given a protective coating to shield yarns from excess abrasion in weaving.

In recent years, economic factors are causing many firms to replace the older shuttle looms with shut- tleless looms. These new looms may operate at speeds up to three times the rate of shuttle looms, are quieter and take up less floor space per unit of production. Shuttleless looms include rapier, projectile, water jet, and air jet looms. Cur- rently, about 34 percent of the US. looms in operation are shuttleless. Shuttleless looms offer the potential for the reduction of energy con- sumption. Less energy is required to propel the shuttle across the loom. Equivalent amounts of fabric can be produced in a much shorter time on a shuttleless loom than on a shuttle loom.

Knitting. Unlike woven fabrics which are interlaced, knit fabrics are a series of interconnected loops. Warp and weft knitting are the most frequently used knitting processes. In warp knitting, yarn is fed into the knitting needles directly from a warp beam. In weft knitting, yams are fed from individual packages. Warp knitting is performed on flat bed machines while weft knitting is performed on circular machines. Unlike yarns for warp knitting (which are prepared very similarly to warp yarns in weaving), yarns for weft knitting can go directly from the winding machine to the knitting machine.

Greige textile mills are the most electricity-intensive mills. The woven and knit fabrics industry (Table 3) represents approximately 53 percent of the total electricity consumption in the entire U.S. textile industry group. Knitting, however, is not as energy intensive as weaving. Energy use in weaving (including warping and slashing) ranges from 2,796Bhdlb to 19,678 Btu/lb, with the average being 8,615

Table 4

Applicable Electrotechnologies in Weaving and Knitting

ELECTROTECH. ADVANTAGES

High-Efficiency Motors Machine efficiency, lower energy consumption.

Reduced drying costs and times in weaving preparation.

RF Drying in Slashing

Robotics/ Automation Reduced labor and increased efficiency in material handling, fabric inspection and process monitoring.

Strategic conservation

Strategic load growth

Strategic load growth

Cotton, Inc. P.O. Box 30067 Raleigh, NC 27612 (919) 782-6330

Industrial Fabrics Association International 345 Cedar Bldg., Suite 800 St. Paul, MN 55101 (612) 222-2508

National Association of Hosiery Manufacturers 447 South Sharon Amity Road Charlotte, NC 28211 (704) 365-0913

Applicable DSM Load Shape Objectives for SICS 221-225

I I

1 I Strategic Load Growth

Strategic Conservation

Davison's Textile Blue Book, 1989, Davison Publishing Co. Inc., Ridge- wood,NJ 07451

Electric Power Research Institute, Textile Industry ScopinE Studv, EPRIaReport, November, 1988

Market Outlook, Textile World, December, 1989

Textile Hi *lights, American Textile Manufacturers Institute, Inc., December, 1989

Textile Industry Guidebook: Profile and DSM Outions, EPRI, CU-6789, March, 1990

"Textiles in the '90s: A Decade of Change," Textile World, January, 1990

U. S. Congress, Office of Technol- ogy Assessment, U. S. Textile and Apparel Industrv: A Revolution in Prorrress, April, 1987

U.S. Dept. of Commerce, Intema- tional Trade Administration, 1989 U. S . Industrial Outlook and 1990 U. S. Industrial Outlook

U. S. Dept. of Commerce, Bureau of the Census, 1987 Census of Manu- factures

U. S. Dept. of Energy, The U. S. Textile Industrv: An Enerw Per- spective, November, 1988

Basic funding for this Brief is provided by the Electric Power Research Institute (EPRI), a nonprofit organization that conducts research and development on behalf of the electric utility industry. Industry Briefs are designed to provide the utility marketing representative with an overview of industry trends, manu- facturing methods and energy use char- acteristics of each industry. Such infor- mation will enable utilities to identify, evaluate and implement industrial demand-side management options suitable for specific process industry groups.

This Industry Brief was developed by the EPRI Textile Office, the College of Textiles, North Carolina State Univer- sity. The Resource Dynamics Corpora- tion coordinated technical review.

For ordering information, call EPRI's Affiliate Member Program

For technical information, contact EPRI Textile Office College of Textiles North Carolina State University Box 8301 Raleigh, NC 27695

1 -800-4320-A M P

1 919-737-7550 L I Copyright 0 1990 Industry Brief, Vol. 1, No 7 Electric Power Research Institute

c l o Alto, CA A

Figure 3 U.S Textile Operating Rates Percent of Capacity s

Percent

0

1985 1986 1987 1988 1989 1990

1985 - 88 - Revised 1989 - b t h t e 1990- Forecast

Btu/lb. In knitting, energy con- sumption ranges from 3,540 Btu/lb to 10,865 Btu/lb, with the average being 7,200 Btu/lb.

Warping processes are not very electricity intensive. In fact, warp- ing accounts for only about 8 percent of the energy consumed in

Table 3

weaving. Slashing and W A C each represent about 21 percent of the energy used in weaving. The remaining 50 percent of energy is actually consumed by the weaving machines. In knitting, which has less yarn preparation compared with weaving, knitting machines consume about 90 percent of process energy.

Electricity supplies almost all of the motive power in textile mills. Motor drives account for about 80 percent of the electricity consumed. Lighting is the next largest electric- ity consumer, with process heating applications representing only about 2 percent. Weaving mills typically consume greater amounts of electricity than knitting mills due to the energy required to prepare the yarns to withstand the rigors of weaving. Also, weaving machines (especially older, shuttle looms) often consume larger amounts of electricity than knitting machines.

The woven and knit fabrics industry is often a very cyclical industry. During prosperous economic times, firms may operate 24 hours a day, 7 days a week. However, during economic downtums, companies may reduce production and scale back their operations to less than 40 hours per week. The size of a given firm plays a major role in determin- ing the extent to which operations must be scaled back during eco- nomic downturns. Larger firms, which can afford to carry high inventories, may be able to continue producing at near maximum capacity if prosperous times are forecast for the near future. Smaller firms may be greatly affected by economic downtums, and these firms may have to lower production substantially. Typical firms in this industry operate on three 8-hour or two 12-hour shift schedules. Three demand-side management strate- gies are applicable in this industry.

usually reached when plants are Peak clipping. Energy peaks are

Woven and Knit Fabrics Industry: 1986 Energy Use Statistics

ENERGY COSTS ($ MIL) ELEC. USE INTENSITY

Purch. Purch. Tot1 Purch. (Mil. (kWh Per $ of kWh) Value Added) SIC Industry Elec. Fuels Energy

221 1 2221 2231 2241 2251 2252 2253 2254 2257 2258 2259

Cotton Manmade Fibers/Silk Wool Narrow Woven Women's Hosiery, Hosiery, N.E.C.*" Knit Outerwear Knit Underwear Weft Knits Warp Knits Knitting, N.E.C.**

153.6 304.5 14.9 21.1 25.4 22.1 29.0 13.1 50.5 24.1 1.5

42.5 62.3 12.3 7.8 9.6

12.9 26.4 9.9

48.0 16.6

.6

196.1 366.8 27.2 28.9 35.0 35.0 55.4 23.0 98.5 40.7 2.1

3,392.2 7,123.9

280.3 362.4 486.6 397.0 511.6 274.4 907.1 456.1 19.4

1.60 1.89 .75 .61 .51 .54 .30 .49 .98 .77 .25

Total 659.8 248.9 908.7 14,211 .O N/A

*Excluding socks **N.E.C = Not Elsewhere Classified

Figure 4 I I I

YXll Fabric Formation: Formation

Process Flow Diagram

e3 Winding

11 Warping

operating near full capacity in hot weather conditions. Computer models are available to help firms determine what production rates and temperature combinations provide energy peaks. Monthly production, whenever possible, could be scheduled so that electric- ity consumption is spread evenly over the month rather than having several peak hours.

Strategic load growth. Electric- ity supplies about 80 percent of the total energy requirements in the greige mill. Most of the operations in greige mills are dry processes, with few opportunities for further electricity penetration. The oppor- tunities that do exist will come from automation programs, as more companies automate their plants and install computerized process control systems. Computerized process monitoring devices can be installed in present machines fairly inexpensively. These devices are currently used in a number of plants to improve efficiency. Auto-

el Dyeing

el Slashing

f i Weaving

Knitting Warping el Knitting

1 I I

c Industrial Home Apparel Uses Furnishings

mation should become more commonplace as firms seek to regain efficiency and labor cost advantages from foreign competi- tors.

tion in this industry is slashing, which involves the application of liquid chemicals to the yam. Slash- ing represents the major opportu- nity for load growth in this industry by the application of radiofrequency (RF) drying (see Table 4). The use of RF drying in slashing could lower total energy consumption, but a large capital outlay would be needed to adapt this technology to current operations.

Strategic conservation. Most woven and knit fabrics companies have not thoroughly assessed emerging electrotechnologies. Many firms do not consider energy or electricity to be an important input to their production process. However, the energy costs per dollar of value added are 3 percent higher in the woven and knit fabrics

The main wet processing applica-

industry than in the entire manufac- turing sector. The wide use of motors highlights the potential for the replacement of older motors with newer, high-efficiency ones. Electric utilities with customers in this industry could conduct plant audits as well as establish more formal lines of communication with these customers in order to deter- mine areas of possible conservation.

American Society of Knitting Technologists 386 Park Avenue, South New York, NY 10016-8897 (212) 683-7520

American Textile Manufacturers Institute, Inc. 1801 K Street, N.W., Suite 900 Washington, D.C. 20036 (202) 862-0500