Worldwide Economic Situation 2015

17

SECOND QUARTER | 2015

-

Upload

maher-meftah -

Category

Business

-

view

50 -

download

1

Transcript of Worldwide Economic Situation 2015

SECOND QUARTER | 2015

CONTENTS

3 Global Economic Situation

6 Global Labour Market Update• Americas• EMEA• APAC• Global Labour Market Spotlight• Legislative Update

12 Workforce Solutions Industry Insight• The Ideal Workplace• Freelance Management Systems• Next-Generation RPO• The Talent Project

SECOND QUARTER | 2015

GLOBAL ECONOMIC OUTLOOK

Softer first quarter growth in key countries, including the U.S. and China, and recessions in Russia and South America are moderating the outlook for the global economy in 2015. Global growth is expected to remain essentially flat from its 2014 level, with a gradual acceleration predicted in the following years.

Source: IHS Global Insight (April 2015)4

AMERICASWhile the outlook for North American markets is modestly healthy in 2015, recessionary conditions are projected for large South American economies including Brazil, Argentina, and Venezuela.

EMEAGrowth will be supported by the Eurozone recovery and ongoing strength in the UK/Ireland, but lower oil prices along with military and political turmoil are causing significant economic challenges in Russia and the Middle East.

APACChina’s decelerating growth is being offset by an economic revival in India, keeping regional performance high. Growth in other key APAC economies, including Japan and Australia, is expected to be somewhat subdued but still healthy.

2.8% 2.8%

3.3%3.5%

2.1% 2.2%

2.5%2.7%

1.7% 1.6%

2.4%2.7%

4.8% 4.8%

5.1% 5.1%

0%

1%

2%

3%

4%

5%

6%

2014 (e) 2015 (p) 2016 (p) 2017 (p)

REAL GDP GROWTH BY REGION, 2014-2017(p)

World Americas EMEA Asia-Pacific

ECONOMIC BRIEFINGS

Growth prospects across markets are highly divergent, particularly among emerging markets. Robust expansion has pushed India past China in growth, while Brazil and Russia have fallen into recession. The developed economies show a more graduated growth pattern, led by the U.S. and the U.K., with most Eurozone markets in a gradual recovery.

-6%-5%-4%-3%-2%-1% 0% 1% 2% 3% 4% 5% 6% 7% 8% 9%10%

Russia

Brazil

Italy

Japan

France

Canada

Germany

Australia

U.K.

U.S.

China

India

REAL GDP GROWTH RATES, SELECTED MARKETS

Ranked by 2015(p) growth

2014(e)

2015(p)

2016(p)

5

Global GDP Growth2015(p): 2.8%

Sources: IHS Global Insight (April 2015)

EMERGING MARKETS The economy in INDIA continues to steadily improve, driven by ongoing policy

reforms, lower commodity prices and business and infrastructure investments.

CHINA’s GDP growth is forecast to decelerate to 6.5% in 2015, in response to overloads in areas including the housing market, industrial capacity and debt.

BRAZIL faces a recession in 2015, with business and consumer sentiment at record lows; the Petrobras corruption scandal has also had major negative repercussions.

The RUSSIAN economy will see a steep decline in 2015, with GDP contraction of -5%, driven by falling oil prices, sanctions and capital flight.

DEVELOPED ECONOMIES The U.S. economy had a slow start to 2015, but data (particularly in consumer

spending and housing) points to a recovery in the last three quarters of the year.

The outlook for the U.K. is similarly healthy, as economic fundamentals remain positive and wage growth is supporting consumer spending and confidence levels.

Economies in CANADA and AUSTRALIA will need to adjust to changes in the natural resources sector, causing growth to moderate somewhat in 2015.

EUROZONE economic activity is slowly gaining momentum, aided by stimulus measures and a depreciating euro; however, the risk of a Greek exit is rising.

JAPAN is also expected to rebound in 2015, led by an improvement in exports, rising consumer activity, a weaker yen and monetary stimulus.

SECOND QUARTER | 2015

GLOBAL LABOUR MARKET UPDATE: AMERICAS

Labour market developments across the region reflect the markets’ varied economic climates, with a positive outlook for North America and more challenging conditions in the larger South American countries.

Sources: IHS Global Insight (April 2015); Reuters, 04.23.15; Dow Jones, 04.27.15

7

UNITED STATESAfter a relatively slow start to 2015, the pace of hiring is expected to pick up over the rest of the year—but employment gains may not match the robust 260,000 new jobs per month trend seen in 2014.

BRAZILThe Brazilian labour market snapped a three-month string of employment declines in March 2015, but manufacturers, retailers and construction firms continued to shed jobs. Unemployment is expected to rise to 5.5% in 2015.

CANADACanada’s employment picture remains relatively stable, with somewhat surprisingly healthy job creation and level unemployment. One concern is the growth of part-time employment at the expense of full-time positions.

MEXICOThe unemployment rate fell significantly in March, reflecting a positive economic climate. Further large declines in unemployment are unlikely in the near term, however, as more people are expected to join the labour force.

6.2%

5.5%

5.2% 5.2%

4.8% 5.5%

5.4% 5.4%

6.9% 7.0%6.8%

6.6%

4.8% 4.8%4.5%

4.3%

3%

4%

5%

6%

7%

8%

9%

2014 (e) 2015 (p) 2016 (p) 2017 (p)

AVERAGE ANNUAL UNEMPLOYMENT RATE

U.S. Brazil Canada Mexico

GLOBAL LABOUR MARKET UPDATE: EMEA

Although the Eurozone economy is gradually recovering, labour market improvements have been slower to develop. The region does have some standout labour market performers, including the U.K. and Germany.

Sources: IHS Global Insight (April 2015); EIU, 04.23.15

8

FRANCEDespite an improving economy, France’s employment situation remains precarious. Unemployment will remain high and job creation will be limited due to the slow recovery, rigid labour market conditions and high labourcosts.

GERMANYThe labour market showed significant signs of improvement in the first part of 2015, with healthy employment gains and a falling jobless rate. The positive momentum is expected to continue as the economy remains strong.

RUSSIAUnemployment began to rise in the first quarter of 2015 as the economy contracted. Although the jobless rate is expected to continue to climb, many companies may prefer to institute wage cuts over job cuts if possible.

UNITED KINGDOMEmployment growth accelerated in the first part of 2015 and the jobless rate continued on its steady downward trend. Healthy economic activity is expected to keep the demand for labour robust, driving skills shortages.

10.2% 10.2% 9.9%9.6%

6.7%

6.3%6.1% 5.9%

5.2%

6.6% 6.7%

5.8%

6.2%

5.4%5.0% 4.9%

3%

4%

5%

6%

7%

8%

9%

10%

11%

12%

2014 (e) 2015 (p) 2016 (p) 2017 (p)

AVERAGE ANNUAL UNEMPLOYMENT RATE

France Germany Russia U.K.

GLOBAL LABOUR MARKET UPDATE: APAC

The outlook across APAC labour markets is largely positive, with steady job creation and relatively low unemployment expected to persist. Skills shortages are increasing along with the ongoing and rising demand for higher skilled workers.

Sources: IHS Global Insight (April 2015); EIU, 04.17.15; Reuters, 04.24.15

9

AUSTRALIAThe Australian economy added more than 75,000 jobs in February and March combined and the unemployment rate fell to 6.1%. These gains, however, may not be sustained as labour market conditions remain volatile.

CHINADespite a slowing economy, employment remained relatively steady in Q1 2015. Still, the labour ministry said that the pace of urban job creation is slowing and it aims to implement policies that will help spur employment.

INDIACompetition for higher-level talent—particularly technology professionals—continues to increase. As a result, recruitment and retention strategies that target professional workers are becoming much more important.

JAPANJob cuts are decreasing and hiring trends are healthy, driving up job availability rates. Employment demand will keep the unemployment rate low, as well as fuel shortages of high-skilled labour.

6.1%6.4%

6.1%

5.6%

4.1% 4.2% 4.3% 4.2%

8.8%8.4%

7.8%7.4%

3.6% 3.6% 3.5% 3.9%

3%

4%

5%

6%

7%

8%

9%

10%

2014 (e) 2015 (p) 2016 (p) 2017 (p)

AVERAGE ANNUAL UNEMPLOYMENT RATE

Australia China India Japan

LABOUR MARKET SPOTLIGHT: GLOBAL SKILLS SHIFTS

Source: World Employment and Social Outlook 2015, ILO

10

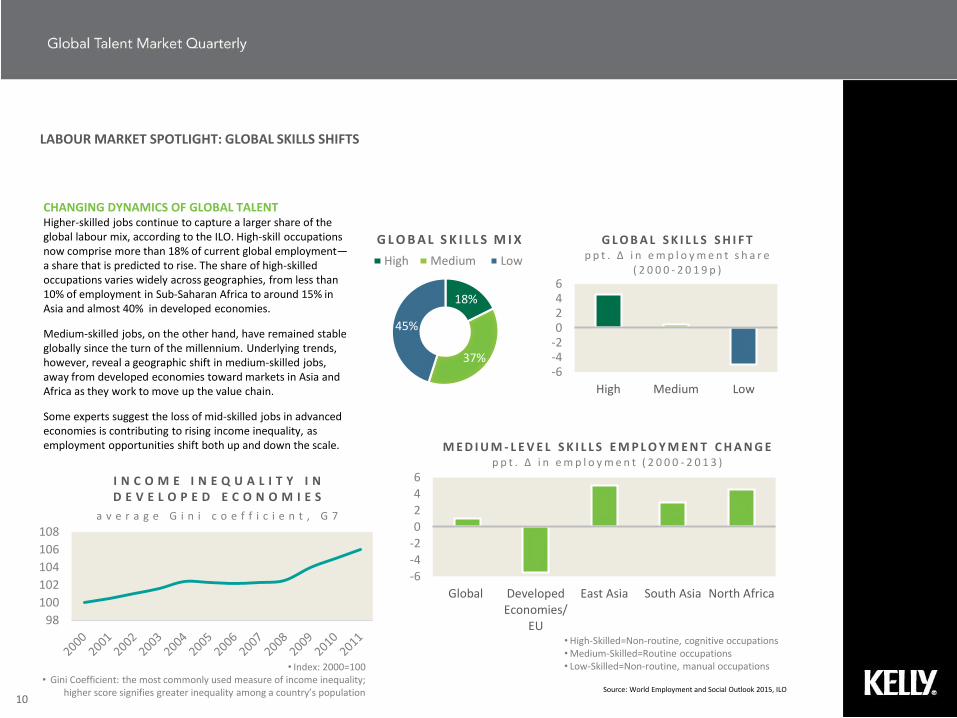

CHANGING DYNAMICS OF GLOBAL TALENT Higher-skilled jobs continue to capture a larger share of the global labour mix, according to the ILO. High-skill occupations now comprise more than 18% of current global employment—a share that is predicted to rise. The share of high-skilled occupations varies widely across geographies, from less than 10% of employment in Sub-Saharan Africa to around 15% in Asia and almost 40% in developed economies.

Medium-skilled jobs, on the other hand, have remained stable globally since the turn of the millennium. Underlying trends, however, reveal a geographic shift in medium-skilled jobs, away from developed economies toward markets in Asia and Africa as they work to move up the value chain.

Some experts suggest the loss of mid-skilled jobs in advanced economies is contributing to rising income inequality, as employment opportunities shift both up and down the scale.

18%

37%

45%

G L O B A L S K I L L S M I X

High Medium Low

-6-4-20246

High Medium Low

G L O B A L S K I L L S S H I F T p p t . ∆ i n e m p l o y m e n t s h a r e

( 2 0 0 0 - 2 0 1 9 p )

-6-4-20246

Global DevelopedEconomies/

EU

East Asia South Asia North Africa

M E D I U M - L E V E L S K I L L S E M P L O Y M E N T C H A N G Ep p t . ∆ i n e m p l o y m e n t ( 2 0 0 0 - 2 0 1 3 )

•High-Skilled=Non-routine, cognitive occupations•Medium-Skilled=Routine occupations• Low-Skilled=Non-routine, manual occupations

98

100

102

104

106

108

I N C O M E I N E Q U A L I T Y I N D E V E L O P E D E C O N O M I E S

a v e r a g e G i n i c o e f f i c i e n t , G 7

• Index: 2000=100• Gini Coefficient: the most commonly used measure of income inequality;

higher score signifies greater inequality among a country’s population

GLOBAL LEGISLATIVE UPDATE

Several markets have seen new regulations that seek to more clearly define the use of temporary workers; those in Slovakia, Poland and South Africa place limits on the length of temporary work contracts. In Australia, Mexico and Puerto Rico, recent court rulings help clarify those countries’ laws surrounding discrimination and sexual harassment.

Sources: SIA ROW and EU Legs and Regs Advisors, January 2015; SIA Daily News, 02.23.15, 04.02.15; IHS Global Insight 04.30.15; globalemploymentlaw.com

11

PUERTO RICOThe Puerto Rico Supreme Court ruled that employers may adopt their own regulations that go beyond the requirements of the national law that prohibits sexual harassment in the workplace.

SLOVAKIAAmendments to the labour code that affect temporary employment took effect in March 2015. Among the provisions are equal pay for temporary workers, changes to the rules about paying travel expenses for temporary work, a ban on temporary assignments for hazardous work and a 24-month cap on assignments.

SOUTH AFRICANew provisions that clarify the meaning of temporary work took effect in January 2015. Under the new rules, temporary work should not exceed three months; and may be used either as a substitute for an employee who is temporarily absent or to perform work that is determined to be a temporary service by a collective agreement.

POLANDThe government approved a 36-month cap on temporary employment contracts. This limit applies to all work completed by a temporary worker for a single employer, even if there are gaps in the employment. After 36 months the contract will automatically become indefinite.

ITALYThe cabinet approved certain key labour market reforms that: ease firing restrictions for large private sector firms; introduce a new type of permanent contract that aims to reduce the use of temporary contracts; and extend unemployment benefits for temporary workers.

BRAZILThe lower house of Congress approved a bill that would allow companies to use contract workers for most of their business functions (rather than just ancillary activities currently). The controversial bill, which is strongly opposed by labour unions and the leftist ruling party, will now go to the Senate for approval.

MEXICOThe Supreme Court has ruled that employers cannot discriminate in recruiting staff on the basis of gender, age or disability. The consequences of violation include fines, compensatory damages and even criminal penalties.

AUSTRALIAA recent court ruling reaffirmed that requesting personal data—such as age or gender—from job applicants may breach the country’s discrimination law.

SECOND QUARTER | 2015

THE IDEAL WORKPLACE

Employees across the globe are looking for a variety of non-traditional, collaborative and technology-based approaches as they think about the optimal setting in which to work. The Kelly Global Workforce Index shows that organizations that integrate these features into their work environments may have greater success in attracting and retaining the best talent.

13 Source: Kelly Global Workforce Index 2014

UNDERSTANDING EMPLOYEES’ PREFERENCESWorkers across the globe were asked to identify what their ideal work environment would look like as part of the 2014 Kelly Global Workforce Index. Employees said that they most prefer a workplace that offers collaboration and cross-functional teams (57%), followed by flexible work arrangements (54%). Other top features include being able to use cutting-edge technology, a creative/innovative culture, and virtual teams.

Among generations, older workers are less likely to prefer collaborative environments, but slightly more likely to want flexible work styles. Differences appear among regions as well, with those in EMEA less interested in both flexible work and virtual teams. Workers in STEM occupations show a greater preference for a culture of innovation and the ability to work with high-level equipment compared to the average professional/technical worker. 37%

39%

44%

54%

57%

Virtual teams

Culture of innovation and creativity

Exposure to the latesttechnologies/top-notch equipment

Flexible work arrangements

Highly collaborative environment(cross-functional teams)

T O P F E A T U R E S O F I D E A L W O R K E N V I R O N M E N T

40%

53%58% 58%57% 58% 56%

51%

SilentGeneration

BabyBoomers

Gen X Gen Y

Highly collaborative environment

Flexible work arrangements

D I F F E R E N C E S B Y G E N E R A T I O N

58%

43%

60%

38%32%

47%

Americas EMEA APAC

Flexible work arrangements

Virtual teams

D I F F E R E N C E S B Y R E G I O N

51% 48% 48%44%

56% 55%63%

46%

Science Engineering IT All P/T

Culture of innovation/creativity

Exposure to latest technologies/equipment

D I F F E R E N C E S B Y O C C U P A T I O N

FREELANCE MANAGEMENT SYSTEMS

The online staffing space is now rapidly evolving with the emergence of Freelance Management Systems (FMS), which target the needs of large enterprise clients seeking solutions to control risk and better manage their growing independent worker community.

14 Source: Staffing Industry Analysts

GREATER SUPPORT OF THE INDEPENDENT WORKFORCETraditional online staffing platforms got their start serving the needs of small-to-mid-sized clients who were seeking a marketplace for bringing together buyers and suppliers of independent worker (IW) talent.

Freelance management systems (FMS) go beyond just talent matching; they function as workforce management platforms with tools to support all aspects of IW engagement, from compliance and screening to payment and performance measurement.

Online Staffing

FMS

IW MARKETPLACE IW MANAGEMENT

MORE

LESS

RIS

K L

EVEL

BUSINESS OBJECTIVE

FMS platforms are also integrating with VMS systems to support the needs of their most sophisticated managed solutions clients. An FMS offers end-to-end service and support to both enterprise users and independent workers, whereas a VMS is primarily used to manage vendors with limited value for independent workers.

Although online staffing platforms were originally geared towards the SME market, FMS solutions are beginning to gain traction within larger clients. On average, more than half of all FMS revenues are coming from companies with at least $500M in revenue.

F M S S U P P O R T I N D E P E N D E N T W O R K E R E N G A G E M E N T A N D R E D U C E R I S K S

VMS

Client

Vendors

Temporary Agency

Workers

SOW Consultants

FMS

Client

Independent Workers

F M S + V M S A S P A R T O F A C O M P R E H E N S I V E C O N T I N G E N T

W O R K F O R C E M A N A G E M E N T P R O G R A M

NEXT-GENERATION RPO

RPO clients have traditionally looked to providers to deliver cost savings and efficiencies in their core recruitment processes. As the market matures, the focus is turning towards more value-added processes that provide greater impact across the client’s organization.

15 Source: Nelson Hall; Everest

RPO MOVING UP THE VALUE CHAINRPO contracts are becoming more than just agreements to provide core recruitment services in the most efficient and cost-effective way possible. RPO is evolving to include higher-level solutions that help to make HR more meaningful and integrated with strategy at an enterprise level.

These value-added services include functions that address the critical issue of candidate attraction and retention, such as developing employer branding strategies and creating talent communities. Other services like workforce planning and analytics functions provide clients with the ability to elevate and optimize their talent management processes using internal and external market data and insights.

PAST FUTURE

• Cost Reduction

• Scalability

• Efficiency

• Effectiveness

• Business Impact

• Strategic Alignment

Core Recruitment Services

• Sourcing

• Screening

• Interviewing

• Applicant Tracking

Core Recruitment PLUSValue-Added Services

• Employer Branding

• Talent Communities

• Labour Market Data/ Analytics

• Workforce Planning

FOC

US

SCO

PE

INCREASING VALUE TO CLIENT

R P O M A R K E T E V O L U T I O N

70% of RPO providers say they will increase investments in analytics in next 12 months

30% of RPO providers are developing a portal to increase visibility of labour market data

0%

50%

100%

2007 2009 2014

RPO PROVIDERS OFFERING EMPLOYER BRANDING SERVICES

Kelly offers a complete content library that advances the discussion and thinking around current trends, strategies and issues impacting global talent management.

To register for webcasts or for more information, visit www.kellyocg.comDownload The Talent Project, a free iPad ® app by Kelly Services.

TITLE PRESENTED BY: DESCRIPTION

Propelling InnovationChris Jock, VP & Global BPO Practice Lead, KellyOCG

In leading organizations, innovation is both an investment and a state of mind that is essential to success. Read this report to discover the vital components of innovation and the qualities that innovators possess.

Five Factors of the Candidate Experience

Anne Marie Ryan, President, Employee Research Group and Professor, Michigan State University

This e-book provides an evidence-based look at what matters most to candidates and what really impacts their attraction to an organization, satisfaction with the hiring process and their decisions to accept offers and recommend the organization to others.

Outsourcing Rigor

Juan Luevano, Director & Supply Chain & Administrative Practice Lead, BPO, KellyOCG

Mike Koper, Manufacturing Solutions Architect - BPO, KellyOCG

Regulation adds complexity to the outsourcing process. In this paper, Kelly presents elements you can put in place to help you make sure your outsourced business functions meet regulatory expectations in the long term.

16

Kelly Services Inc. makes no representation or warranty with respect to the material contained within this report.