World Nuclear Fuel - JAIF Nuclear Fuel ... Enrichment 7 SWU $150 per SWU 1050 Fabrication 1 kg $300...

92

Pick a title, any title will do… This is a sample of how our PowerPoint presentation s could look in the future WNU Summer Institute Oxford 13 July 2009 Steve Kidd Director of Strategy & Research World Nuclear Association World Nuclear Fuel Market

Transcript of World Nuclear Fuel - JAIF Nuclear Fuel ... Enrichment 7 SWU $150 per SWU 1050 Fabrication 1 kg $300...

Pick a title, any title

will do…

This is a

sample of

how our

PowerPoint

presentation

s could look

in the future

WNU

Summer

Institute

Oxford

13 July 2009

Steve KiddDirector of Strategy & ResearchWorld Nuclear Association

World Nuclear Fuel

Market

Daejeon – July 09

Beijing – June/July 09

South Africa – June 09

OUTLINE

Outline of today‟s presentation

• Overview of the fuel cycle

• What determines the demand for nuclear fuel?

• Uranium

• Uranium market

• Conversion

• Enrichment

• Fuel fabrication

• Trade in nuclear fuel

• Summary & outlook

nb. This presentation covers the commercial side of nuclear –the technical side is a huge but different area!

WNA Market Report 2007

Why is nuclear fuel important?

• Without it the reactor will not operate!

• Yet if it is so insignificant in nuclear economics,

why are we bothering devoting 90 minutes to it?

• But without cheap fuel, nuclear is dead!

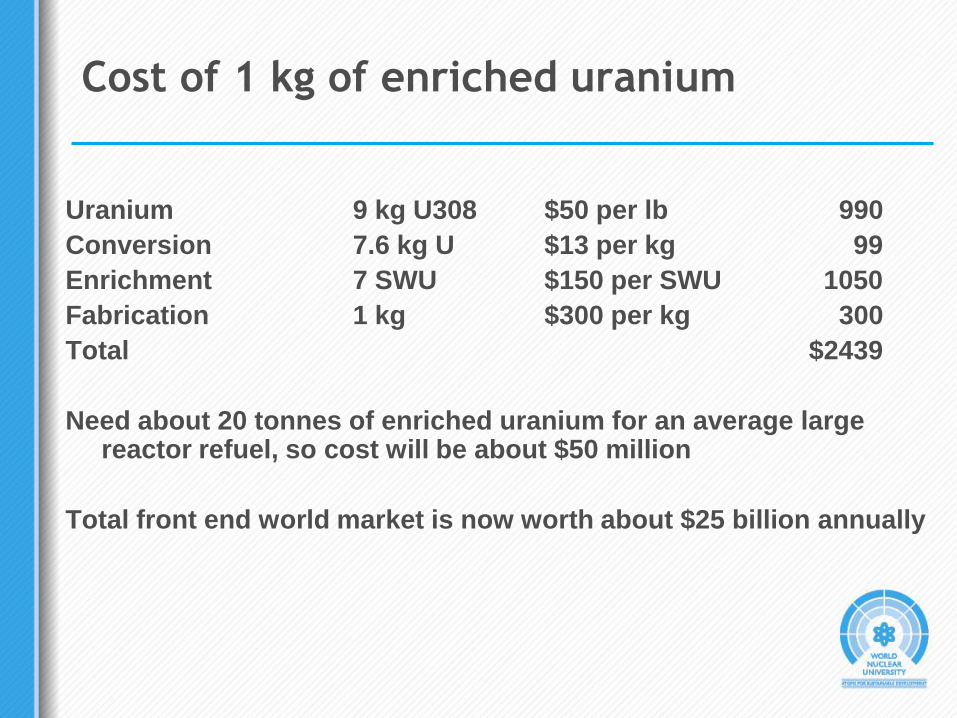

Cost of 1 kg of enriched uranium

Uranium 9 kg U308 $50 per lb 990

Conversion 7.6 kg U $13 per kg 99

Enrichment 7 SWU $150 per SWU 1050

Fabrication 1 kg $300 per kg 300

Total $2439

Need about 20 tonnes of enriched uranium for an average large reactor refuel, so cost will be about $50 million

Total front end world market is now worth about $25 billion annually

OVERVIEW OF THE

FUEL CYCLE

The Nuclear Fuel Cycle - Closed

MiningConversion

Enrichment

Fuel

fabrication

Nuclear Power Plant

Reprocessing

Waste

UraniumPlutonium

Key aspects of fuel cycle

• Complexity!

• Specialisation of producers

• International aspects

• Trade rules & regulations

• Transport difficulties

• Recycling possibilities

• Historical production levels still relevant

DEMAND FOR

NUCLEAR FUEL

Demand for nuclear fuel

Depends on two factors

• Number and size of reactors in operation

• How they are run – load/capacity factors,

enrichment level, burn-up and tails assay

WNA scenario approach

Three scenarios approach to demand –

• Reference case

• Upper case

• Lower case

Generic assumptions underlie each scenario –

on nuclear economics, public acceptance,

impact of climate change debate and

electricity market structure

Scenarios to 2030

• Country-level judgements.

• Existing reactors – consideration of operating lives

(technical, licensing and policy issues) – also power up-

rates.

• New reactors - a) under construction

b) already within planning & licensing

c) proposed without firm commitment

Key countries

• United States

• Europe – United Kingdom, Germany

• China

• India

• Russia

• Other developing countries

Nuclear generating capacity

to 2030, MWe net

0

100000

200000

300000

400000

500000

600000

700000

800000

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

MW

e n

et

Reference Scenario Upper Scenario Lower Scenario

Forecasting reactor requirements

• Nuclear generating capacity

• Fuel cycle and reactor operating factors – load/capacity

factors, tails assay, enrichment level, fuel burn-up

• MS Excel-based spreadsheet model computes uranium,

conversion and enrichment requirements by year to

2030

• WNA revises forecasts every two years, published in

biennial Market Report

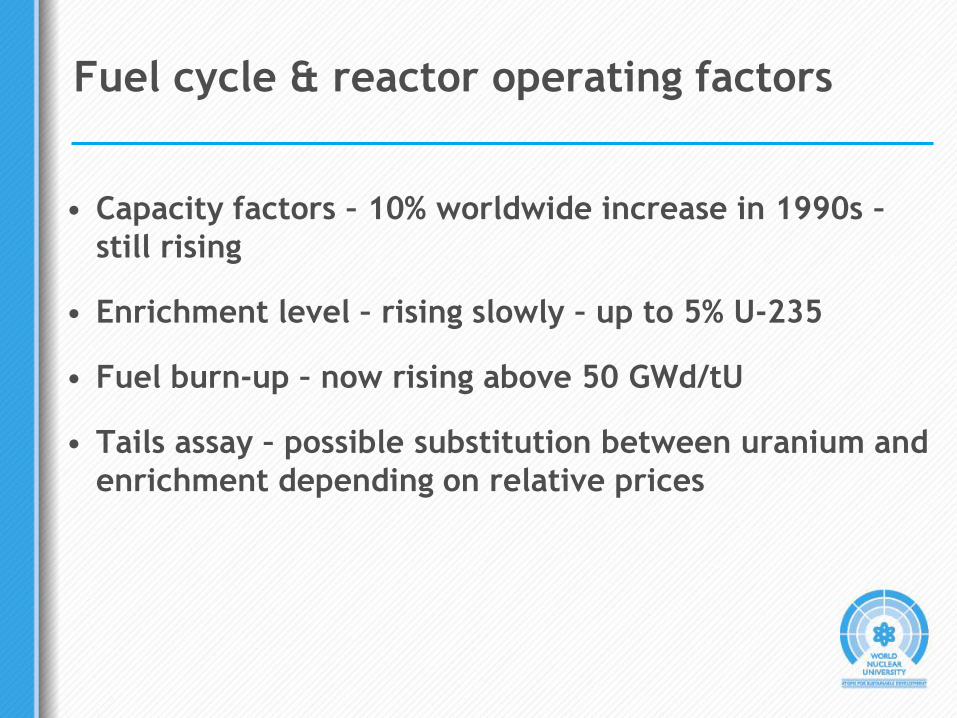

Fuel cycle & reactor operating factors

• Capacity factors – 10% worldwide increase in 1990s –

still rising

• Enrichment level – rising slowly – up to 5% U-235

• Fuel burn-up – now rising above 50 GWd/tU

• Tails assay – possible substitution between uranium and

enrichment depending on relative prices

Uranium requirements to 2030

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

180,000

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

2007 Lower Scenario 2007 Reference Scenario 2007 Upper Scenario

2005 Lower Scenario 2005 Reference Scenario 2005 Upper Scenario

URANIUM

Uranium geology

• Uranium is by no means scarce

• Found in several different types of deposits

• 0.1% grade can be enough for mining today

• Average concentration in Earth‟s crust 2.8

ppm – similar to tin

• Phosphates

• Trace amounts in sea water

Low cost (<$80/kg) uranium reserves,

thousand tonnes U

Australia 714

Kazakhstan 344

Canada 329

South Africa 206

Russia 172

Brazil 157

Namibia 145

Ukraine 127

USA 99

Others 155

Total 2438

Key Lake(Cameco, Cogema)

Crow Butte(Cameco, Kepco Res.)

Rabbit Lake(Cameco)

Ranger(Rio, Cameco,Cogema, JAURDC)

Olympic Dam(WMC)

Arlit + Akouta(Cogema, State of Niger, OURD)

Christensen Ranch(Cogema, Fuel Internat.)

Highland(Cameco)

Rossing (Rio, State of Iran,

State of Sth Africa)

Vaal Reefs(Anglo)

Russia

Uzbekistan

Kazakhstan

Converters

Jouac (Cogema)

Blind River

(Cameco)

Metropolis

(Honywell)

Pierrelatte

(Areva)

Springfields

(BNF)

Angarsk

(Russian Govt)

Beverley(General Atomics)

McLean(Cameco)

Uranium operations & conversion facilities

World uranium production 2008, tU

Canada 9000

Kazakhstan 8521

Australia 8430

Namibia 4366

Russia 3521

Niger 3032

Uzbekistan 2338

USA 1430

Others 3292

Total 43930

Top 10 uranium mines 2008 tonnes U

McArthur River 6383

Ranger 4527

Rossing 3449

Olympic Dam 3344

Priargunsky 3050

Arlit 1743

Rabbit Lake 1368

Akouta 1289

McLean Lake 1249

Akdala 1034

Top 10 companies producing uranium,

2008, tU

Rio Tinto 7975

Cameco 6659

Areva 6318

KazAtomProm 5328

ARMZ 3688

BHP Billiton 3344

Navoi 2338

Uranium One 1107

Paladin 917

General Atomics 636

Others 5620

Total 43930

Uranium production by mining method,

2008

Conventional 62%

In situ leaching (ISL) 28%

By-product 10%

Total 100%

“Western” uranium demand & supply, tU

0

10000

20000

30000

40000

50000

60000

70000

1945

1948

1951

1954

1957

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

Australia Canada France

Gabon Namibia Niger

South Africa USA Others

Reactor Requirements

Four ages of uranium

• Military, 1945-1967

• Booming civil demand, 1967-1985

• Secondary supply overhang, 1985-2003

• Renewed production growth, 2003 +

“Eastern” uranium supply

0

5000

10000

15000

20000

25000

30000

1945

1948

1951

1954

1957

1960

1963

1966

1969

1972

1975

1978

1981

1984

1987

1990

1993

1996

1999

2002

2005

Former DDR Czechoslovakia Bulgaria Romania Hungary Russia

Ukraine Kazakhstan Tajikistan Uzbekistan Others

Secondary supplies

• Can be regarded as previous uranium production,

held off the market for an extended period

• An important element in nuclear fuel supply

• Ex-military materials

• Commercial inventories

• MOX and RepU fuel

Ex-military materials

• Disarmament treaties have made much military

fissile material surplus to requirements and available

for use in the civil market

• Russian HEU – 500 tonnes to be down-blended

• US HEU – for later

• Plutonium in both US and Russia – use in MOX fuel

Civil inventories

• Utility inventory – pipeline, strategic and excess

• Producer inventory

• Smaller quantities owned by converters, enrichers,

traders & brokers

• Now some speculative uranium holdings by financial

companies

• Depleted uranium – can be economic to re-enrich

this to create fresh fuel

The Nuclear Fuel Cycle - Closed

MiningConversion

Enrichment

Fuel

fabrication

Nuclear Power Plant

Reprocessing

Waste

Uranium Plutonium

MOX and RepU

• Reprocessing plants separate uranium and

plutonium from used fuel

• RepU is re-enriched by centrifuges or blending to

produce fresh fuel

• Extracted plutonium is introduced as the primary

fissile element in MOX fuel

• Major reprocessing plants in France and UK with

one nearing completion in Japan

Future of secondary supplies

• Future of down-blended HEU – the big question?

• Remaining commercial inventories

• Further governmental inventories

• Future of MOX and RepU fuel

• Re-enrichment of depleted uranium (“tails”)

Will the future look like this?

Sorry,

we are out

of material.

Help,

we need

more!

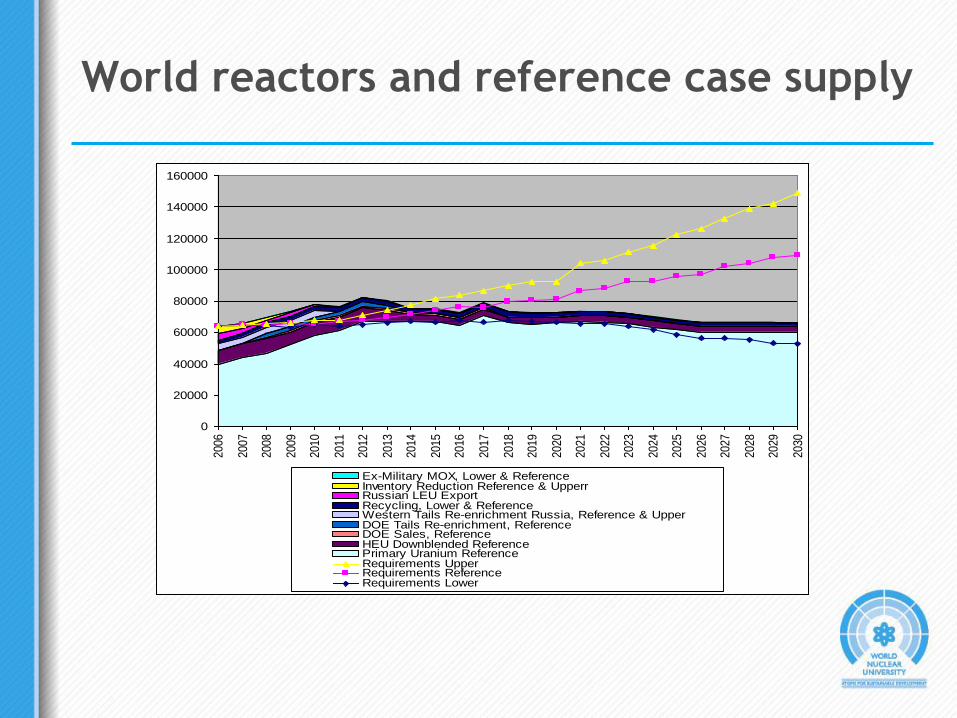

World reactors and reference case supply

0

20000

40000

60000

80000

100000

120000

140000

160000

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

2020

2021

2022

2023

2024

2025

2026

2027

2028

2029

2030

Ex-Military MOX, Lower & ReferenceInventory Reduction Reference & UpperrRussian LEU ExportRecycling, Lower & ReferenceWestern Tails Re-enrichment Russia, Reference & UpperDOE Tails Re-enrichment, Reference DOE Sales, ReferenceHEU Downblended ReferencePrimary Uranium ReferenceRequirements UpperRequirements ReferenceRequirements Lower

Future uranium production

• Must now increase sharply to (a) cover rising

demand and (b) diminishing secondary supplies

• Recent trend has been for increased dominance by a

small number of major producing companies and

countries

• Canada, Australia, Kazakhstan, Africa

• More exploration now taking place – stimulated by

higher prices

• Over 400 “junior” uranium companies have

suddenly appeared

• Some will eventually produce but how many?

Uranium production plans of Kazakhstan

2007 6,637 tU

2008 8,521 tU

2009 11,900 tU

2010 14,000 tU

2011 17,000 tU

2015 onwards 25,000 tU per annum

Implied requirement for primary uranium

production

0

20000

40000

60000

80000

100000

120000

140000

160000

20062007

20082009

20102011

20122013

20142015

20162017

20182019

20202021

20222023

20242025

20262027

20282029

2030

ton

nes

U

Requirements Lower minus Secondary UpperRequirements Reference minus Secondary UpperRequirements Upper minus Secondary Upper

Conclusions

• Uranium market has sound supply to 2015 but meeting

demand becomes more challenging thereafter, unless

the lower scenario is accurate

• Primary uranium supply needs to rise sharply to meet

rising market demand

• Secondary supplies will remain important

URANIUM MARKET

Features of nuclear fuel market

• Fuel is not generally bought in its fabricated form –rather the reactor operator buys uranium and conversion, enrichment and fuel fabrication services separately

• Many contracts are very long term

• Reactors are only refuelled once per year – buyers don‟t need to be in the market all the time

• Fuel can be easily stored – inventories can play an important part in the market

• Spot market is largely an outlet for smoothing out unforeseen blips in supply and demand

• Spot market prices relevant to many longer term contracts

Market structure

• Few participants

• Small number of transactions – illiquid

• Not transparent – most deals highly confidential

• Data on prices limited – spot market quotations,

estimates of contract prices and historic series

Spot uranium prices – current

Reasons for uranium price rise 2003-now

• Perception that secondary supplies are beginning to

run out

• Lack of investment in new production facilities from

1980s onwards – supply fixed in short run

• Production disruptions in 2003 -emphasized that

supply was fragile

• Expectation that demand will rise from “rebirth” of

nuclear power

• Change in Russian strategy in the market

• Weakening US dollar

CONVERSION

The Nuclear Fuel Cycle - Closed

MiningConversion

Enrichment

Fuel

fabrication

Nuclear Power Plant

Reprocessing

Waste

UraniumPlutonium

Reactors by type

GCR 1%

FBR 1%

PHWR 6%

LWGR 3%

AGR 2%

BWR 22%

PWR 65%

Conversion - basics

• Enrichment for light water reactors requires

conversion of uranium to UF6

• CANDU reactors require direct conversion to UO2

• 4 major UF6 conversion suppliers – Cameco,

Comurhex (Areva), ConverDyn and Rosatom

• UO2 conversion by Cameco and domestic suppliers

in Argentina, China, India and Romania

Key Lake(Cameco, Cogema)

Crow Butte(Cameco, Kepco Res.)

Rabbit Lake(Cameco)

Ranger(Rio, Cameco,Cogema, JAURDC)

Olympic Dam(WMC)

Arlit + Akouta(Cogema, State of Niger, OURD)

Christensen Ranch(Cogema, Fuel Internat.)

Highland(Cameco)

Rossing (Rio, State of Iran,

State of Sth Africa)

Vaal Reefs(Anglo)

Russia

Uzbekistan

Kazakhstan

Converters

Jouac (Cogema)

Blind River

(Cameco)

Metropolis

(Honywell)

Pierrelatte

(Areva)

Springfields

(BNF)

Angarsk

(Russian Govt)

Beverley(General Atomics)

McLean(Cameco)

Uranium operations & conversion facilities

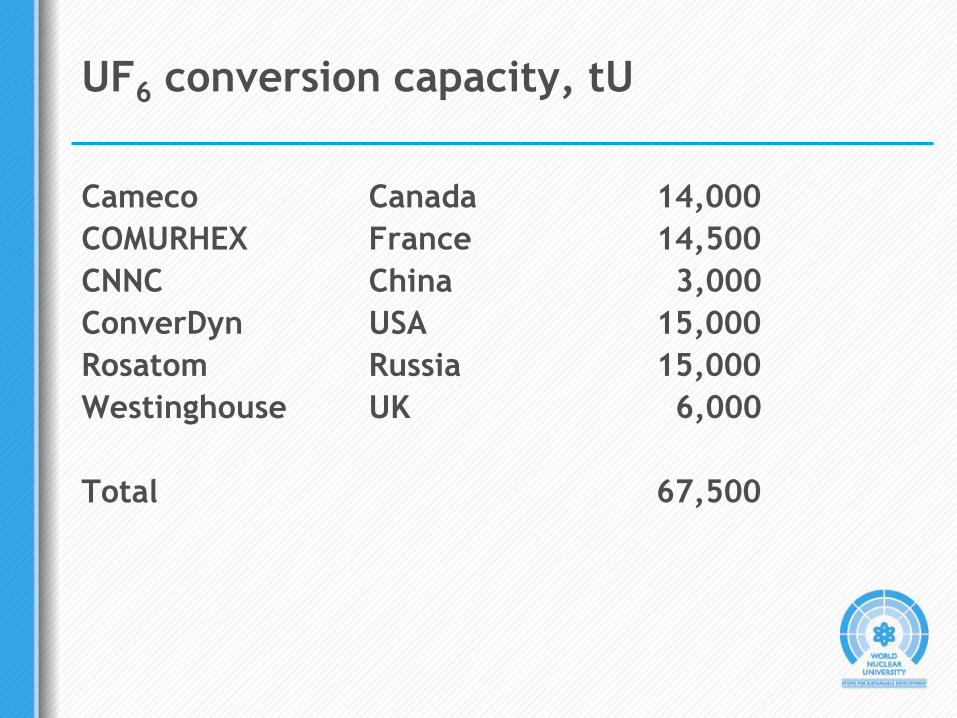

UF6 conversion capacity, tU

Cameco Canada 14,000

COMURHEX France 14,500

CNNC China 3,000

ConverDyn USA 15,000

Rosatom Russia 15,000

Westinghouse UK 6,000

Total 67,500

UO2 conversion capacity, tU

Argentina 160

Canada 2700

China 200

India 435

Korea 400

Romania 150

Total 4045

Conversion – now and future

• Market for conversion to UF6 has been quite tight

• Clear shortfalls when plants have been “down”

• Regional imbalance in supply – need for transport

• BNFL facility in UK didn‟t close as originally scheduled in 2006 – some relief to supply

• Investment in expanded and new facilities

• Possible increased access to surplus Russia capacity

• Continued need for secondary supplies –particularly from down-blended Russian HEU

ENRICHMENT

Enrichment - basics

• 90% of current power reactors need fuel where the U-235 isotope is above the natural 0.71% (typically 3-5%)

• Two main technologies – gaseous diffusion and centrifuges

• Investment in laser enrichment so far unrewarded by commercial application

• Large front-end expense for utilities

• Effort expended is measured in separative work units (SWUs)

Centrifuges

What is a SWU?

• A unit unique to the nuclear industry

• A measure of the quantity of work or effort

necessary to create a quantity of enriched uranium

from natural uranium

• A complex unit – detailed mathematical formulae

• Given the huge electricity input in gas diffusion

enrichment plants, the SWU could effectively be

taken as the electricity required to separate the two

isotopes

Enrichment – supply

• Four large suppliers of primary enrichment services

– USEC, Eurodif (Areva), Urenco and Rosatom

• USEC and Eurodif use gas diffusion

• Urenco and Rosatom use centrifuges

• JNFL and CNNC also primary suppliers

• Heavy current investment in new centrifuge plants

by USEC and Urenco in US and by Eurodif in France

(and eventually US too)

• Will SILEX prove commercially viable?

Enrichment capacities, 000 SWUs

CNNC China 1,000

Eurodif France 10,800

JNFL Japan 1,050

Rosatom Russia 25,000

Urenco Germany 1,800

Netherlands 3,500

UK 3,700

USEC USA 11,300

Total 58,150

Enrichment requirements to 2030

0

20000

40000

60000

80000

100000

1200002

00

3

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

20

20

20

21

20

22

20

23

20

24

20

25

20

26

20

27

20

28

20

29

20

30

tho

us

an

d S

WU

Lower Scenario Reference Scenario Upper Scenario

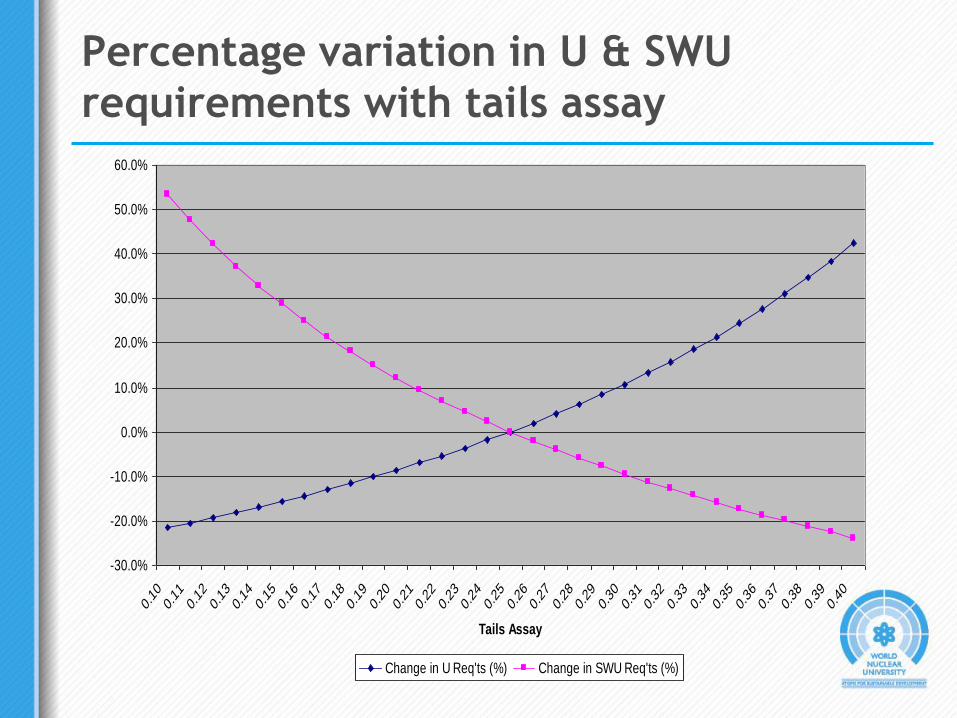

Importance of the tails assay

• Reactor operators require enriched uranium and can achieve this by many combinations of uranium and enrichment

• Relatively high enrichment input means lower tails assay (waste stream from the enrichment plant)

• Essentially an economic decision – relative price of U and SWU

• Optimal tails assay – 0.30%-0.35% until 2003-4

below 0.25% now

Percentage variation in U & SWU

requirements with tails assay

-30.0%

-20.0%

-10.0%

0.0%

10.0%

20.0%

30.0%

40.0%

50.0%

60.0%

0.10

0.11

0.12

0.13

0.14

0.15

0.16

0.17

0.18

0.19

0.20

0.21

0.22

0.23

0.24

0.25

0.26

0.27

0.28

0.29

0.30

0.31

0.32

0.33

0.34

0.35

0.36

0.37

0.38

0.39

0.40

Tails Assay

Change in U Req'ts (%) Change in SWU Req'ts (%)

Depleted uranium

• Over 1.5 million tonnes in storage throughout the

world

• Volume increasing by 50,000 tonnes per annum

• Use in diluting HEU

• Possibility of re-enrichment to form new reactor

fuel

• Very minor non-nuclear uses owing to density

Enrichment – current issues

• Acute proliferation issues surround this area of the

fuel cycle – similar to reprocessing of used fuel

• Proposals for “regional fuel cycle centres” and fuel

banks?

• Significant dependence on down-blended Russian

HEU – half of SWUs supplied in US in recent years

• Difficulties of access to large Russia capacity for

Western reactor operators

• Significant capacity has been devoted to re-

enrichment of depleted uranium (“tails”)

FUEL FABRICATION

Fuel fabrication - basics

• Reactor fuel is generally in the form of ceramic

pellets

• These are formed from pressed uranium oxide which

is sintered (baked) at high temperature

• Pellets are then encased in metal tubes to form fuel

rods

• Rods are then arranged in fuel assemblies (or

bundles) for introduction into the reactor

• Fundamentally a different process to uranium,

conversion and enrichment – not a bulk commodity

item – but “high tech”

Fuel fabrication

Fuel fabrication – capacities etc

• Annual requirements for LWR fuel fabrication is

about 7,000 tonnes of heavy metal (enriched U)

• Annual requirements for CANDUS and other reactor

types are 2,000-3,000 tU per annum

• Capacity for LWRs is around 11,500 tU per annum

• Production much more “localised” than other areas

of fuel cycle

• “Big boys are Areva NP, Toshiba-Westinghouse, GE-

Hitachi and TVEL

• Important smaller suppliers – CNNC, JNFL, KNFC,

ENUSA

Fuel fabrication – current trends

• PWR fuel market very competitive

• BWR fuel market becoming more competitive

• Now some competition for fuelling Russian-origin

reactors

• Non-LWR fuel requirements tend to be met by

domestic suppliers – for CANDUs, AGRs etc

• Consolidation of suppliers apparent within the sector

– BNFL with Westinghouse/ABB (then Toshiba

acquired it), Framatome-Siemens merger (Areva NP)

and Global Nuclear Fuels (GE and Japanese)

• Still surplus capacity

NUCLEAR TRADE

Trade in the nuclear fuel cycle

• Worldwide nuclear fuel market worth about

US$25 billion per year

• Specialisation is essential for economic reasons

• Security of supply is essential – therefore buyers

pursue supply diversity

• Excluded from WTO, so disputes have to be solved

bilaterally

• Restrictions not necessarily more stringent than in

other energy commodities worldwide

Market segmentation

• Russia fuels all the rectors it sells around the world

• Complete fuel service in many cases

• Gradually breaking down as reactor owners seek

supply diversification

• Czech Republic and Ukraine

• But strong former Soviet Union sales to West

Trade restrictions - direct

• Import tariffs on fabricated fuel

• Australian & Canadian export monitoring

• US restrictions on supply from the former Soviet

Union

• US trade actions on enrichment from Europe

• Euratom controls in Europe

Nuclear fuel from Russia to US

• Arrived on western markets after fall of Soviet

Union

• Arguably depressed price

• US restrictions under „Suspension Agreements‟

• Highly complex…„matched sales‟, „sunset

reviews‟…blah, blah, blah!

• Now centred on enrichment

• HEU agreement only way for US utilities to get

Russian SWUs

• New provisions seem to allow gradual Russian access

to the market

SWUs from Europe to US

• US enrichment sector in poor competitive position

• Urenco and Eurodif winning increased share of US

market

• „Anti-dumping‟ action against them

• Tariffs imposed

• Is enrichment a product or service?

• Question resolved by US Supreme Court!

• Peace in the world?

Trade restrictions – political & indirect

• No direct sanctions today – in contrast to the past -

eg South Africa/Namibia

• Strategic and defence-related restrictions are also

now weaker

• Three Mines Policy in Australia

• State ownership common in the nuclear fuel

producers

• State ownership of power utilities too

• Foreign ownership restrictions

Nuclear law – trade aspects

• Important owing to proliferation concerns and trade

controls

• The concept of “origin” of nuclear materials

• “Substantial transformation”

• “Obligations” attached to materials

• “Prior consent”

• “Swaps” or “exchanges” help get around these

Non-proliferation and safeguards

Non-Proliferation Treaty (NPT)

(Signed 1970; Extended indefinitely 1995. Currently 187 Signatories)

• To stop the further spread of nuclear weapons

• To provide security for non-nuclear weapons states which have given up the nuclear option

• To encourage international cooperation in the peaceful uses of nuclear energy

• To pursue negotiations towards nuclear disarmament leading to the eventual elimination of nuclear weapons

Nuclear Suppliers Group (NSG)

“ … a group of nuclear supplier countries which seeks to contribute to the non-proliferation of nuclear weapons through the implementation of Guidelines for nuclear exports and nuclear related exports…”

1974 Creation of NSG with 7 members (currently 45 members)

1978 NSG Guidelines published as IAEA Document INFCIRC/254, covering export of items especially designed or prepared for nuclear use

1992 NSG Guidelines for “dual use” technologypublished as IAEA Document INFIRC/254, Part2

Nuclear Suppliers Group (NSG)

Impact of the NSG

• Severe limitations on nuclear trade with India and Pakistan,

neither of which has signed the NPT

• Each country has had to develop its domestic nuclear sector

without substantial recourse to outside assistance

• The lack of good quality uranium resources has forced India to

meet its ambitious NPP programme by relying on the

maximum use of recycled fuel, notably in fast reactors, and,

potentially, through the development of thorium-based

reactors

• The NSG has now approved changes to its Guidelines, after

the US/India nuclear deal was signed and approved.

SUMMARY &

OUTLOOK

Summary - 1

• Demand for nuclear fuel is rising steadily – but

different scenarios are possible

• Uranium supply is currently tight

• Secondary supplies are certainly declining

• Conversion market is also tight – needs new

investment?

• Heavy investment in enrichment facilities is taking

place

• Fuel fabrication has surplus capacity

Summary -2

• Major international market in nuclear fuel

• Not completely free trade

• A new nuclear country should get free supply – if

sticks to IAEA safeguards etc

• Are fuel banks, international fuel cycle centres an

unnecessary restriction on free trade?

• National self-sufficiency is maybe a natural reaction

• The only reactors going without fuel have been

Indian

Outlook

• Supply of nuclear fuels will be sufficient to meet

demand, even if requirements rise sharply

• But heavy investment will be needed to improve

fuel cycle infrastructure

• Over the long-term, new reactor designs, much

more efficient in their use of fuel, may

fundamentally change the nature of the fuel market

NOW

THE FUTURE