World Nondestructive Test Inspection Services Market

88

World Nondestructive Test Inspection Services Market N94C-30 June 2011 An Indestructible Future

description

NDT Market

Transcript of World Nondestructive Test Inspection Services Market

World Nondestructive Test Inspection Services Market

N94C-30June 2011

An Indestructible Future

2N94C-30

Disclaimer

• Frost & Sullivan takes no responsibility for any incorrect information supplied to us by manufacturers orusers

• Quantitative market information is based primarily on interviews and therefore, is subject to fluctuation.

• Frost & Sullivan Research Services are limited publications containing valuable market information providedto a select group of customers in response to orders. Our customers acknowledge, when ordering, thatFrost & Sullivan Research Services are for customers’ internal use and not for general publication ordisclosure to third parties.

• No part of this Research Service may be given, lent, resold or disclosed to non-customers without writtenpermission.

• Furthermore, no part may be reproduced, stored in a retrieval system, or transmitted in any form or by anymeans, electronic, mechanical, photocopying, recording or otherwise, without the permission of thepublisher.

• For information regarding permission, write to:

Frost & Sullivan

7550 IH 10 West, Suite 400

San Antonio, TX 78229 – 5616

USA

© 2011 Frost & Sullivan. All rights reserved. This document contains highly confidential information and is the sole property of Frost & Sullivan. No part of it may be circulated, quoted, copied or otherwise reproduced without the written approval of Frost & Sullivan.

3N94C-30

Certification

• We hereby certify that the views expressed in this research service accurately reflect our views based onprimary and secondary research with industry participants, industry experts, end users, regulatoryorganisations, financial and investment community, and other related sources.

• In addition to the above, our robust in-house forecast & benchmarking models along with theFrost & Sullivan Decision Support Databases have been instrumental in the completion and publishing ofthis research service.

• We also certify that no part of our analyst compensation was, is or will be, directly or indirectly, related tothe specific recommendations or views expressed in this service.

4N94C-30

Table of Contents

Executive Summary

• Definitions and Scope of research

• Growth Opportunities and Total Forecasts

• Key Market Drivers Summary

• Trends

• Key Market Participants

Total World NDT Inspection Services Market

• Market Overview and Definitions

• Market Engineering Measurements

• Industry Challenges

• Market Drivers and Restraints

• Market Trends

• Technology Trends

• Revenue Forecasts

• Trends by End User

• Trends by Geography

• Competitive Environment

• Market Share Analysis

Slide number

10

11

12

13

14

15

17

18

21

22

29

38

40

41

43

46

47

48

5N94C-30

Table of Contents (Contd…)

North American NDT Inspection Services Market

• Market Engineering Measurements

• Revenue Forecast

• Trends by End User

• Competitive Environment

European NDT Inspection Services Market

• Market Engineering Measurements

• Revenue Forecast

• Trends by End User

• Competitive Environment

Asia Pacific NDT Inspection Services Market

• Market Engineering Measurements

• Revenue Forecast

• Trends by End User

• Competitive Environment

Slides number

49

50

51

53

55

57

58

59

61

63

65

66

67

69

71

6N94C-30

Table of Contents (Contd…)

Rest-of-World NDT Inspection Services Market

• Market Engineering Measurements

• Revenue Forecast

• Trends by End User

• Competitive Environment

Strategic Observations and Conclusion

Which Way is the NDT Inspection Services Market Headed?

About Frost & Sullivan

Slides number

73

74

75

77

79

81

82

84

7N94C-30

List of Figures

Total NDT Inspection Services Market: Impact of Top Five Industry Challenges (World), 2011-2017

NDT Inspection Services Market: Certification Requirements for Level I and Level II (World), 2010

Total NDT Inspection Services Market: Market Drivers Ranked in Order of Impact (World), 2011-2017

Total NDT Inspection Services Market: Market Restraints Ranked in Order of Impact (World), 2011-2017

NDT Inspection Services Market: Significant Mergers and Acquisitions (World), 2010

Total NDT Inspection Services Market: Revenue Forecast (World), 2007-2017

Total NDT Inspection Services Market: Revenue Forecast by End User (World), 2007-2017

Total NDT Inspection Services Market: Competitive Structure (World), 2010

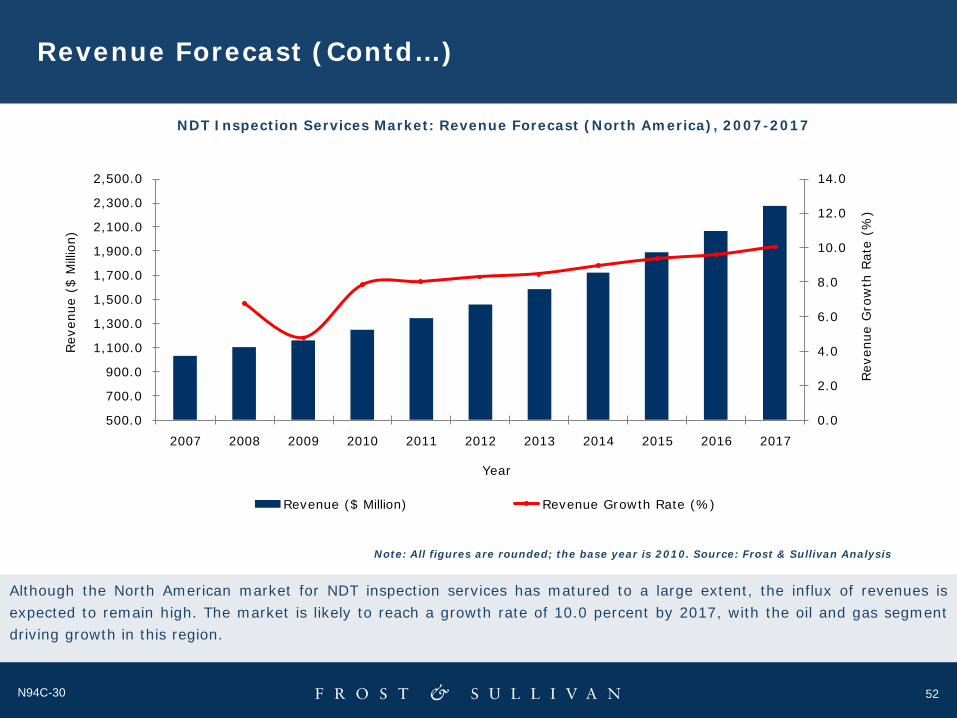

NDT Inspection Services Market: Revenue Forecast (North America), 2007-2017

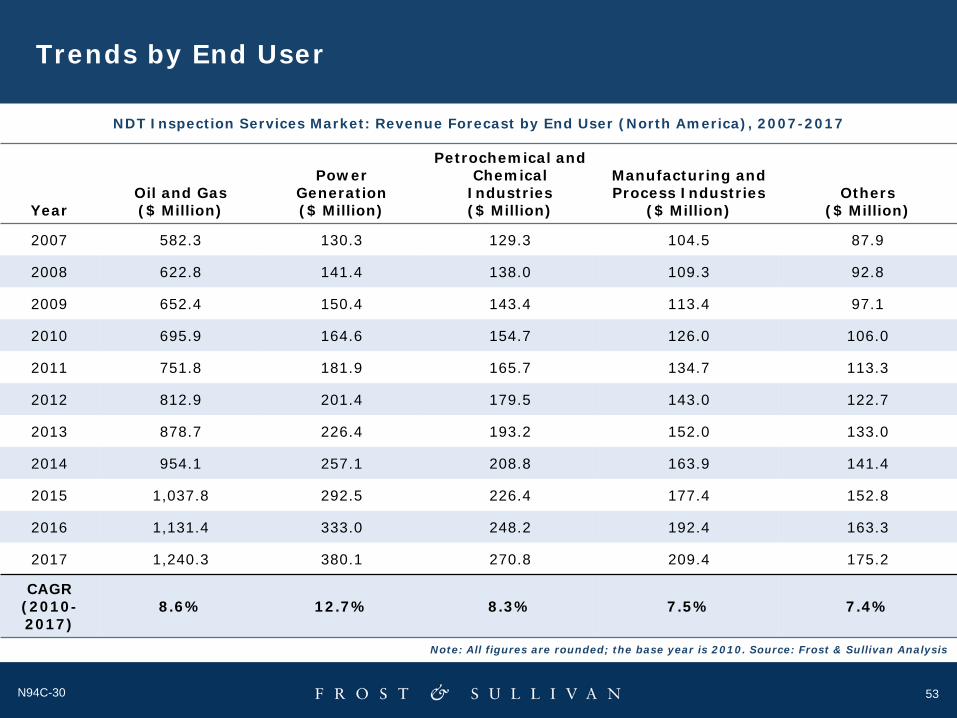

NDT Inspection Services Market: Revenue Forecast by End User (North America), 2007-2017

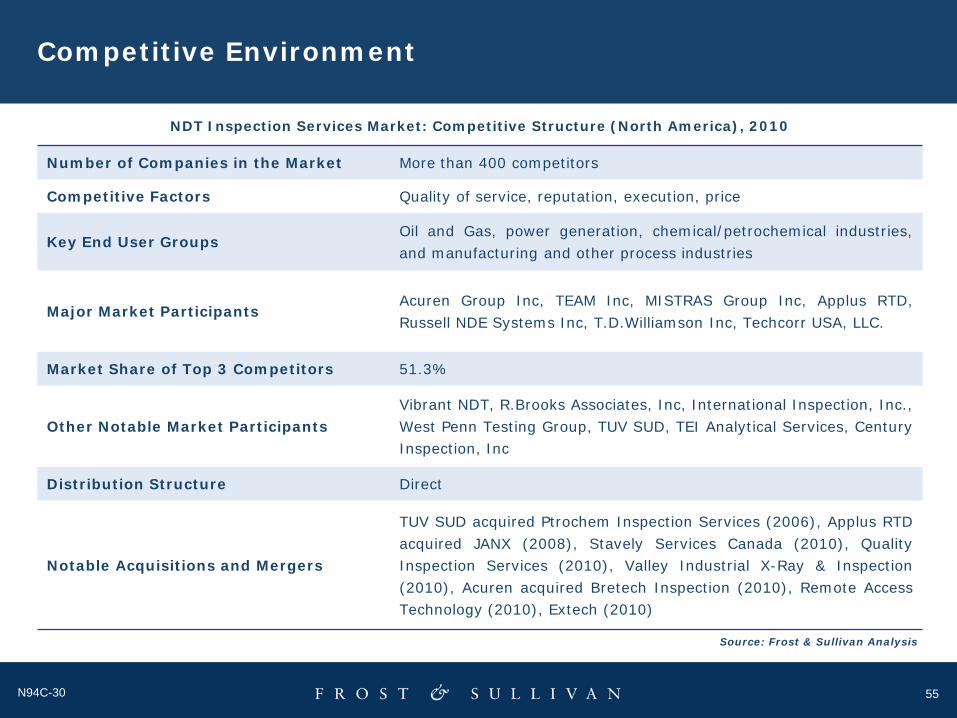

NDT Inspection Services Market: Competitive Structure (North America), 2010

NDT Inspection Services Market: Revenue Forecast (Europe), 2007-2017

NDT Inspection Services Market: Revenue Forecast by End User (Europe), 2007-2017

NDT Inspection Services Market: Competitive Structure (Europe), 2010

NDT Inspection Services Market: Revenue Forecast (Asia Pacific), 2007-2017

23

26

30

35

38

41

44

47

51

53

55

59

61

63

67

8N94C-30

List of Figures (Contd…)

NDT Inspection Services Market: Revenue Forecast by End User (Asia Pacific), 2007-2017

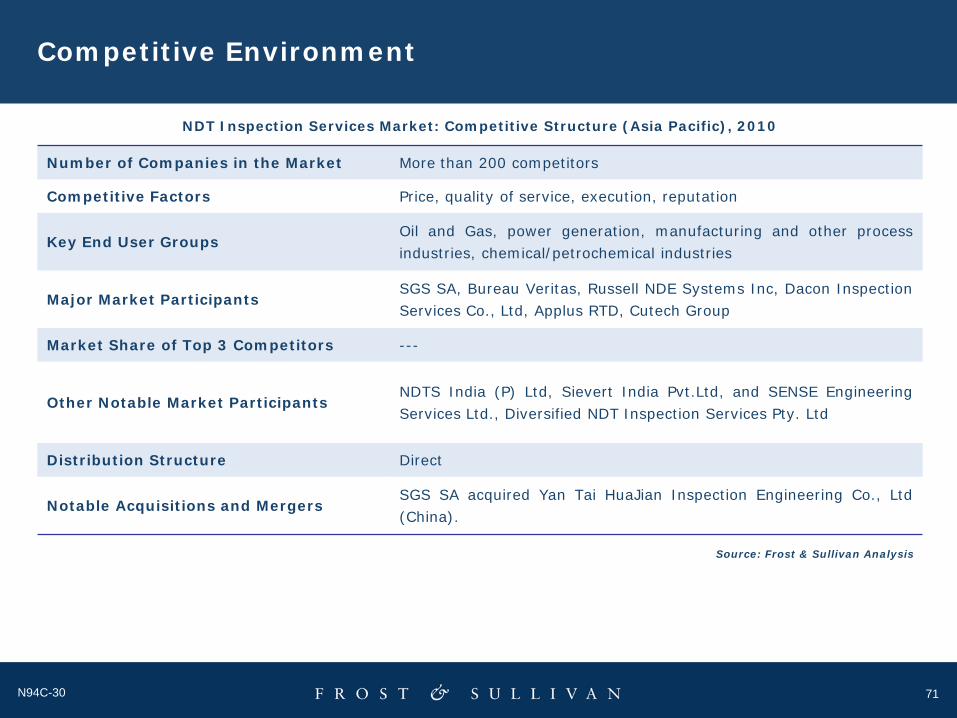

NDT Inspection Services Market: Competitive Structure (Asia Pacific), 2010

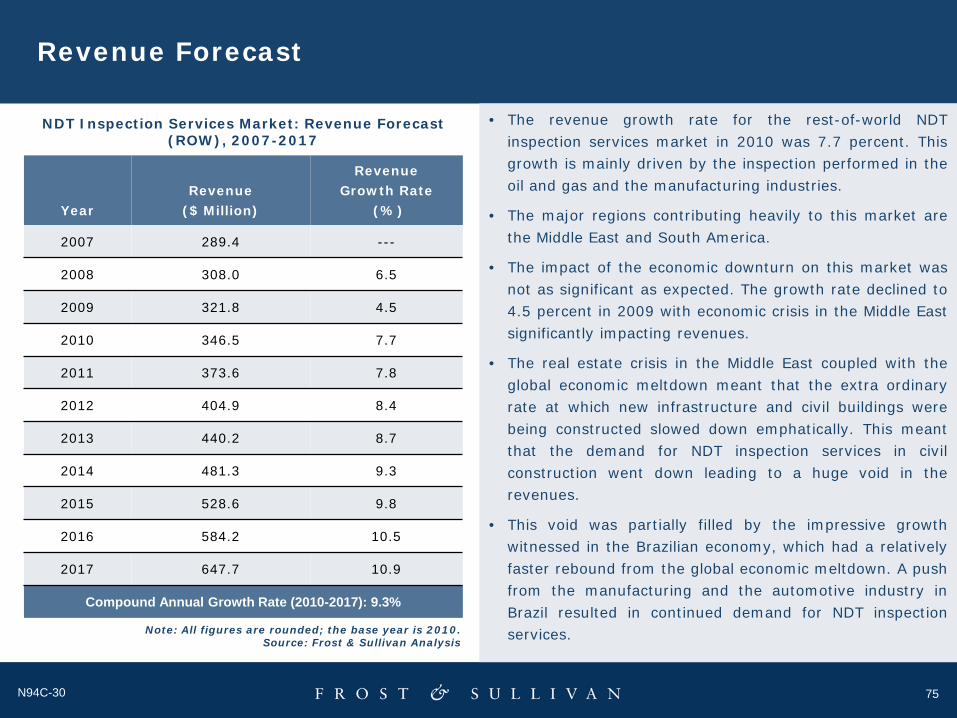

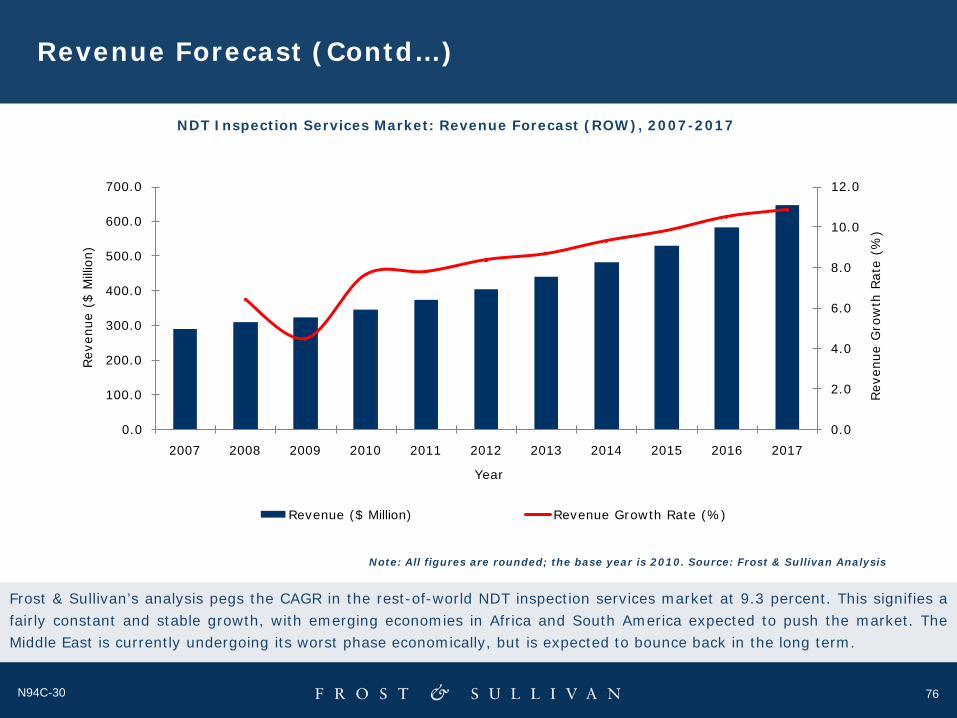

NDT Inspection Services Market: Revenue Forecast (ROW), 2007-2017

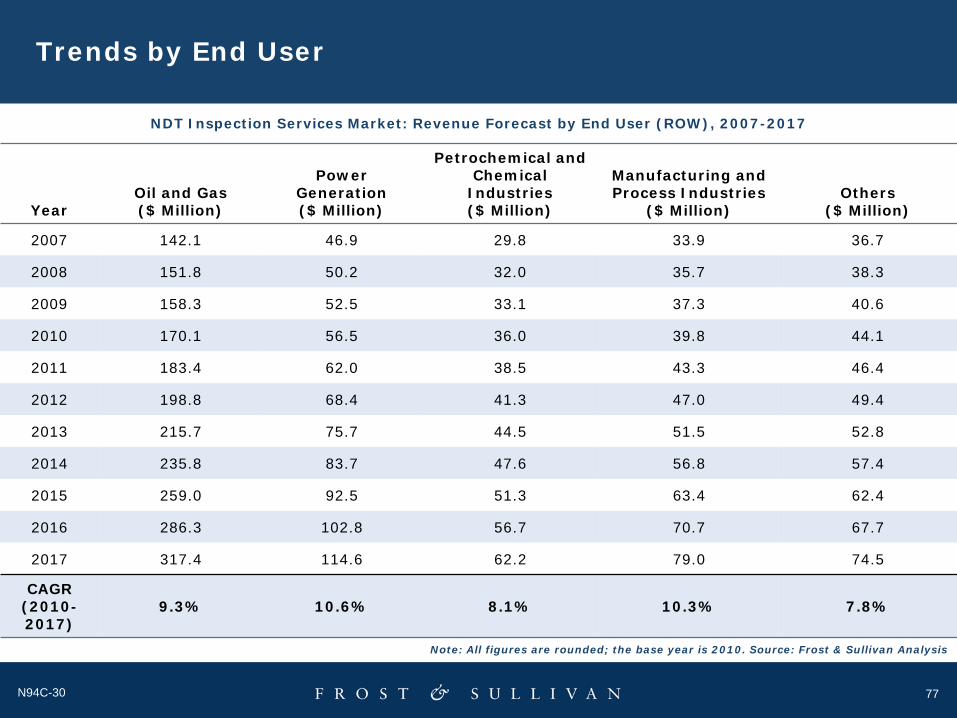

NDT Inspection Services Market: Revenue Forecast by End User (ROW), 2007-2017

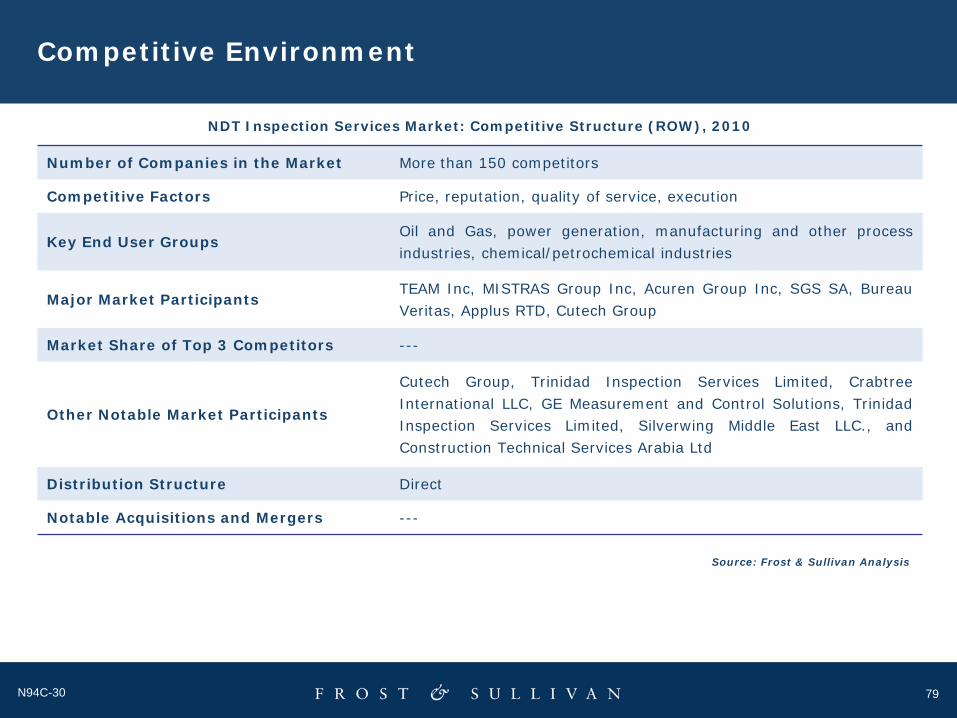

NDT Inspection Services Market: Competitive Structure (ROW), 2010

69

71

75

77

79

9N94C-30

List of Charts

Total NDT Inspection Services Market: Revenue Forecast by Geographic Region (World), 2007-2017

Total NDT Inspection Services Market: Key Market Drivers (World), 2011-2017

Total NDT Inspection Services Market: Market Engineering Measurements (World), 2010

Total NDT Inspection Services Market: Industry Challenges (World), 2011-2017

Total NDT Inspection Services Market: Market Drivers and Restraints (World), 2011-2017

NDT Inspection Services Market: GDP Growth Rate in Major Economies (World), Q1 2008-Q1 2011

Total NDT Inspection Services Market: Revenue Forecast (World), 2007-2017

Total NDT Inspection Services Market: Percent of Revenues by End user (World), 2010

Total NDT Inspection Services Market: Percent of Revenues by Geographic Region (World), 2010

Total NDT Inspection Services Market: Company Market Share by Revenues (World), 2010

NDT Inspection Services Market: Market Engineering Measurements (North America), 2010

NDT Inspection Services Market: Revenue Forecast (North America), 2007-2017

NDT Inspection Services Market: Market Engineering Measurements (Europe), 2010

NDT Inspection Services Market: Revenue Forecast (Europe), 2007-2017

NDT Inspection Services Market: Market Engineering Measurements (Asia Pacific), 2010

NDT Inspection Services Market: Revenue Forecast (Asia Pacific), 2007-2017

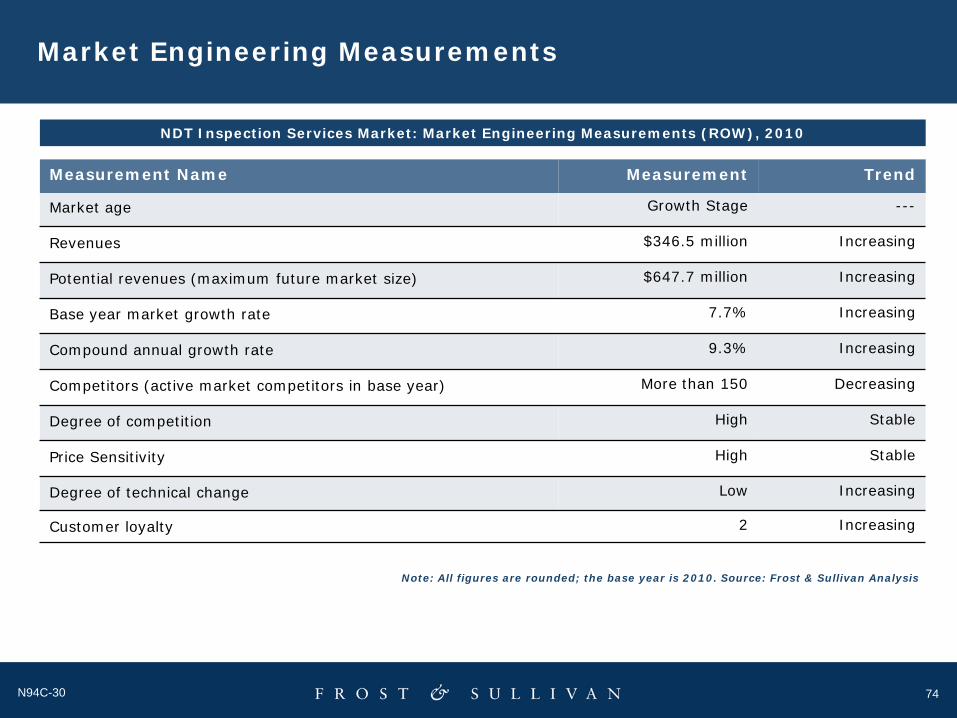

NDT Inspection Services Market: Market Engineering Measurements (ROW), 2010

NDT Inspection Services Market: Revenue Forecast (ROW), 2007-2017

12

13

21

22

29

33

42

43

46

48

50

52

58

60

66

68

74

76

10N94C-30

Executive Summary

10

11N94C-30

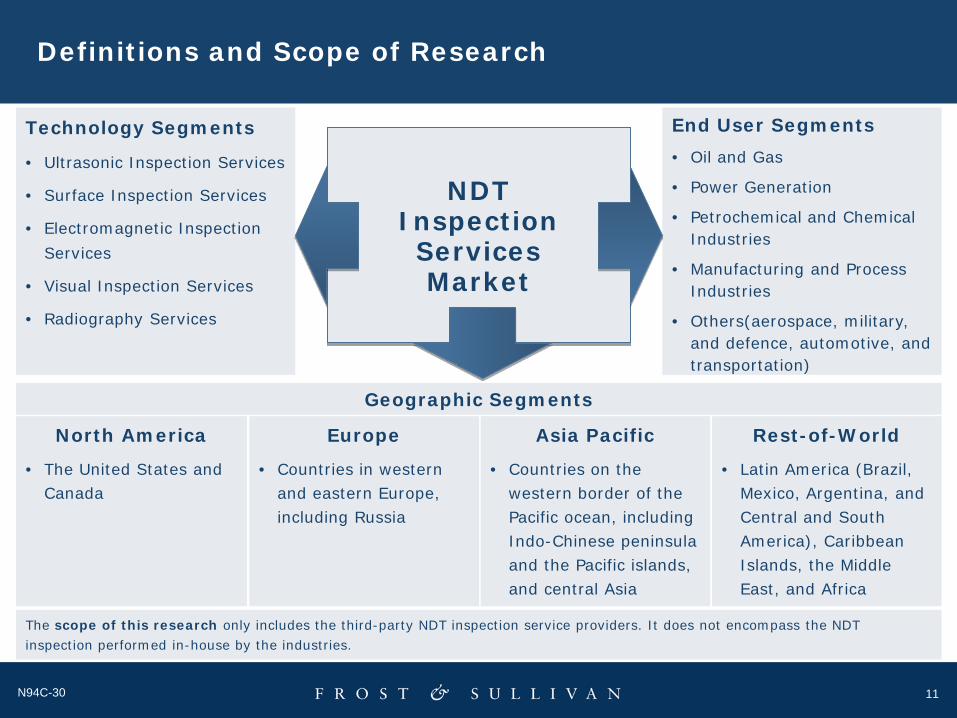

Definitions and Scope of Research

Technology Segments

• Ultrasonic Inspection Services

• Surface Inspection Services

• Electromagnetic Inspection Services

• Visual Inspection Services

• Radiography Services

End User Segments• Oil and Gas

• Power Generation

• Petrochemical and Chemical Industries

• Manufacturing and Process Industries

• Others(aerospace, military, and defence, automotive, and transportation)

Geographic Segments

North America

• The United States and Canada

Rest-of-World

• Latin America (Brazil, Mexico, Argentina, and Central and South America), Caribbean Islands, the Middle East, and Africa

Asia Pacific

• Countries on the western border of the Pacific ocean, including Indo-Chinese peninsula and the Pacific islands, and central Asia

Europe

• Countries in western and eastern Europe, including Russia

NDT Inspection Services Market

The scope of this research only includes the third-party NDT inspection service providers. It does not encompass the NDT inspection performed in-house by the industries.

12N94C-30

Growth Opportunities and Total Forecasts

600.0

1,600.0

2,600.0

3,600.0

4,600.0

5,600.0

6,600.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Rev

enue

s ($

Millio

n)

North America Europe Asia Pacif ic Rest-of-World

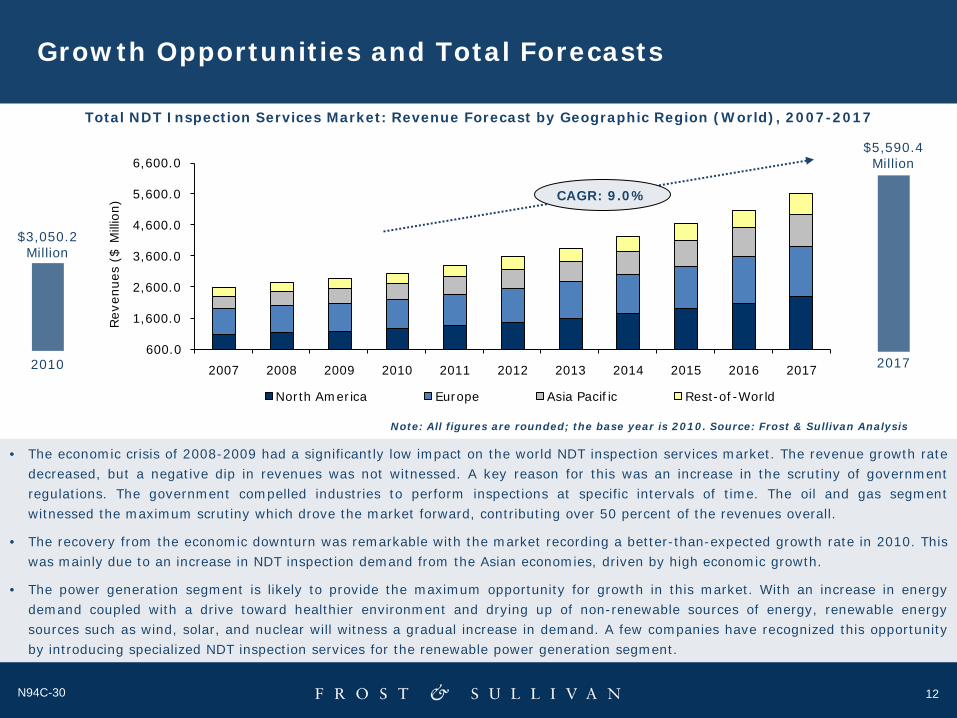

Total NDT Inspection Services Market: Revenue Forecast by Geographic Region (World), 2007-2017

• The economic crisis of 2008-2009 had a significantly low impact on the world NDT inspection services market. The revenue growth ratedecreased, but a negative dip in revenues was not witnessed. A key reason for this was an increase in the scrutiny of governmentregulations. The government compelled industries to perform inspections at specific intervals of time. The oil and gas segmentwitnessed the maximum scrutiny which drove the market forward, contributing over 50 percent of the revenues overall.

• The recovery from the economic downturn was remarkable with the market recording a better-than-expected growth rate in 2010. Thiswas mainly due to an increase in NDT inspection demand from the Asian economies, driven by high economic growth.

• The power generation segment is likely to provide the maximum opportunity for growth in this market. With an increase in energydemand coupled with a drive toward healthier environment and drying up of non-renewable sources of energy, renewable energysources such as wind, solar, and nuclear will witness a gradual increase in demand. A few companies have recognized this opportunityby introducing specialized NDT inspection services for the renewable power generation segment.

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan Analysis

$3,050.2 Million

2010 2017

$5,590.4 Million

CAGR: 9.0%

13N94C-30

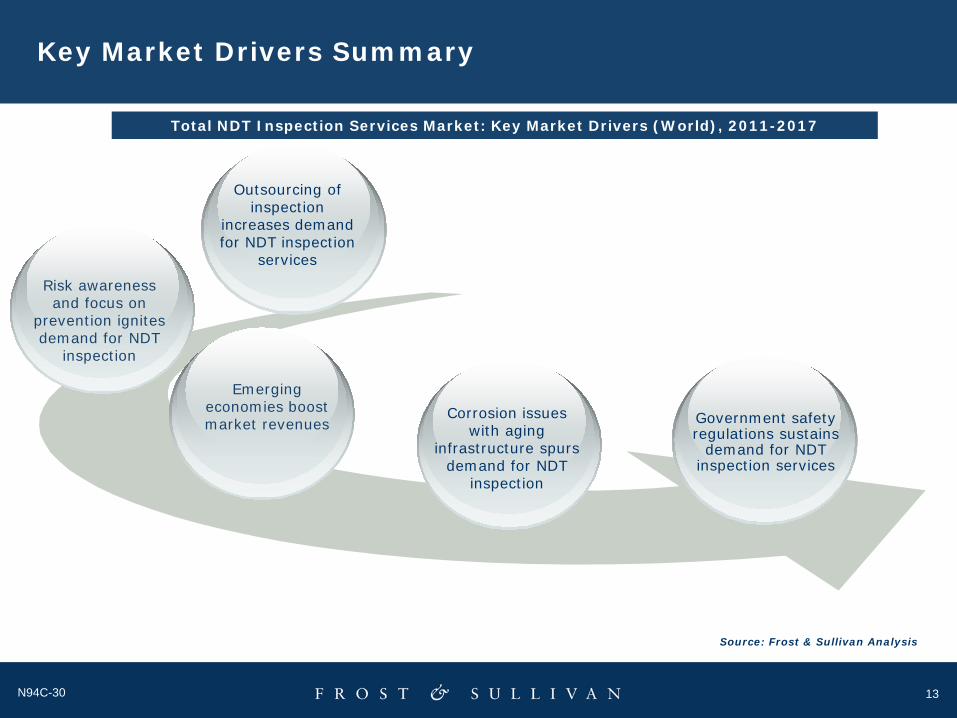

Key Market Drivers Summary

Source: Frost & Sullivan Analysis

Outsourcing of inspection

increases demand for NDT inspection

services

Corrosion issues with aging

infrastructure spurs demand for NDT

inspection

Emerging economies boost market revenues Government safety

regulations sustains demand for NDT

inspection services

Risk awareness and focus on

prevention ignites demand for NDT

inspection

Total NDT Inspection Services Market: Key Market Drivers (World), 2011-2017

14N94C-30

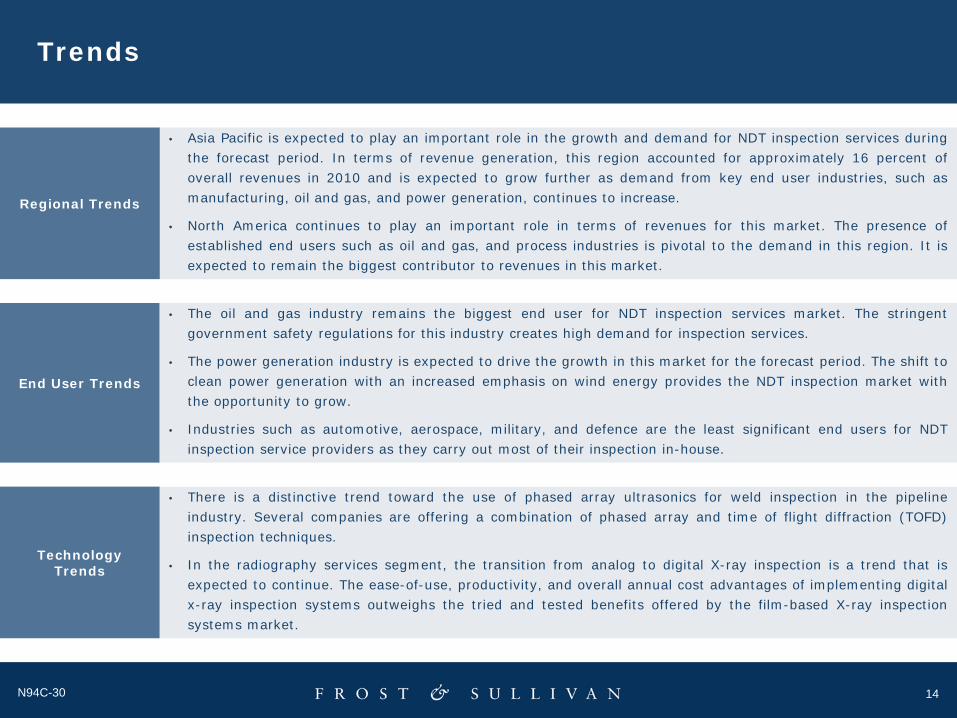

Trends

• Asia Pacific is expected to play an important role in the growth and demand for NDT inspection services duringthe forecast period. In terms of revenue generation, this region accounted for approximately 16 percent ofoverall revenues in 2010 and is expected to grow further as demand from key end user industries, such asmanufacturing, oil and gas, and power generation, continues to increase.

• North America continues to play an important role in terms of revenues for this market. The presence ofestablished end users such as oil and gas, and process industries is pivotal to the demand in this region. It isexpected to remain the biggest contributor to revenues in this market.

Regional Trends

End User Trends

• The oil and gas industry remains the biggest end user for NDT inspection services market. The stringentgovernment safety regulations for this industry creates high demand for inspection services.

• The power generation industry is expected to drive the growth in this market for the forecast period. The shift toclean power generation with an increased emphasis on wind energy provides the NDT inspection market withthe opportunity to grow.

• Industries such as automotive, aerospace, military, and defence are the least significant end users for NDTinspection service providers as they carry out most of their inspection in-house.

• There is a distinctive trend toward the use of phased array ultrasonics for weld inspection in the pipelineindustry. Several companies are offering a combination of phased array and time of flight diffraction (TOFD)inspection techniques.

• In the radiography services segment, the transition from analog to digital X-ray inspection is a trend that isexpected to continue. The ease-of-use, productivity, and overall annual cost advantages of implementing digitalx-ray inspection systems outweighs the tried and tested benefits offered by the film-based X-ray inspectionsystems market.

Technology Trends

15N94C-30

Key Market Participants

• Acuren Group Inc

• TEAM Inc

• Bureau Veritas

• TWI Ltd

• TUV SUD

• GE measurement and control solutions

• Vibrant NDT

• Intron Plus Ltd.

• TEI Analytical Services

• Century Inspection, Inc

• Hi-Tech NDT Inspection Services (S) Pte Ltd

• Sonovation B.V.

• VOGT Ultrasonics GambH

• Applus RTD

• Techcorr USA, LLC

• Intertek Group PLC

• NDT Services Ltd

• NDT Systems and Services AG

• MISTRAS Group Inc

• Russell NDE Systems Inc

• Dacon Inspection Services Co., Ltd.

• SGS SA

• Dekra Industrial AB

• NDTS India (P) Ltd.

• T.D.Williamson, Inc.

• Cutech Group

• Hi-Tech Testing Service, Inc

• R.Brooks Associates, Inc

• International Inspection, Inc.

• West Penn Testing Group

• Sievert India Pvt.Ltd

• Trinidad Inspection Services Limited

• Coastal Inspection Services, Inc

• Bonded Inspections Inc.

• RNDT, Inc.

• Alloyweld Inspection Company, Inc.

• Magnachek, Inс.

• Silverwing (UK) Ltd.

• ABEN Technical Services

• Sinclair X-ray Inspection Services

• NDT EXPERT

• HMT Inc

• IRISNDT

• Westech Inspection, Inc.

• James Fisher Inspection and Measurement Services

• SENSE Engineering Services Ltd.

16N94C-30

Key Market Participants (Contd…)

• Focus NDT

• ANKO AS

• Diversified NDT Inspection Services Pty. Ltd

• Independent Integrity Inspection Limited

• Trinity NDT

• DJA Inspection Services, Inc.

• Construction Technical Services Arabia Ltd

• Centurion NDT

• Axiom NDT and Offshore Services

• Wavelength NDT Ltd

• Advanced Quality Group, Inc.

• Applied Inspection Ltd

• Baker Testing Services, Inc.

17N94C-30

Total World NDT Inspection Services Market

17

18N94C-30

Market Overview and Definitions

The NDT inspection services market is very fragmented as there are no significant barriers to entry. Also, the initialinvestment required is considerably low. In 2010, the estimated number of active competitors in the world NDT inspectionservices market was over 1,000, with several companies set up regionally, catering to the needs of industries in theirrespective regions.

According to the United States Energy Information Administration (EIA), total world marketed energy consumption contractedby approximately 1.0 percent in 2008 and by an estimated 2.0 percent in 2009. Many new projects, especially for pipelineconstruction, were postponed or cancelled due to a lack of capital. Despite these short-term restraints, growth drivers such asageing infrastructure, safety, and compliance have offset the decline with the market showing slow but positive growth duringthe economic downturn.

Frost & Sullivan’s research indicates that the total world market for NDT inspection services in 2010 was $3,050.2 million witha positive growth rate of 7.0 percent. This market is expected to be valued at $5,590.4 million by 2017.

Introduction

Nondestructive testing (NDT) involves examination of an objectwithout impacting its current or future usefulness. The ability of NDTto inspect an object without affecting its operating performanceprovides an excellent balance between quality control and costeffectiveness. The NDT equipment market is well researched withproducts and technologies well defined. As a result, often, thecontribution of the inspection services industry and technicians getsoverlooked. Although the advancement of NDT technologies providesan undeniable boost to the industry, the importance of actuallyimplementing these technologies and analyzing data to provideactionable intelligence is of equal importance to the industrial world.

Source: Olympus NDT

19N94C-30

Market Overview and Definitions (Contd…)

Definitions

For the purpose of this study, the global nondestructive test (NDT) inspection services market has been segmented as:

• Ultrasonic inspection services

• Surface inspection services

• Electromagnetic inspection services

• Visual inspection services

• Radiography services

Ultrasonic inspection Services - Ultrasonic nondestructive testing has been used for over 50 years for a wide range of enduser applications ranging from evaluation of joints, weld inspection, and crack detection. For the purpose of this study, thescope of ultrasonic inspection methods encompasses ultrasonic testing and acoustic emission monitoring (AE).

Surface Inspection Services - For the purpose of this study, the scope of surface inspection methods encompasses liquidpenetrant inspection (LPI), dye penetrant inspection (DPI), and magnetic particle inspection (MPI).

Electromagnetic Inspection Services – For the purpose of this study, the scope of electromagnetic inspection comprises ofeddy current testing (ECT), remote field testing (RFT), magnetic flux leakage (MFL), and alternating current fieldmeasurement (ACFM).

Visual Inspection Services - Visual inspection is by far the most common and simplest NDT technique. For the purpose ofthis study, visual inspection is defined as the examination of surfaces using direct viewing or low magnification techniques.

Radiography Services - It is a method of inspecting materials for hidden flaws by using the ability of short X-rays andgamma rays to penetrate various materials. For the purpose of this study, radiography inspection market includes X-ray,gamma ray, real-time radiography, digital radiography, computed radiography (CR), and computed tomography (CT)inspection services.

20N94C-30

Market Overview and Definitions (Contd…)

This research service provides a global analysis of the NDT inspection services market. In addition, it also provides the totalmarket as well as a breakdown of revenues by four major geographic segments, including:

• North America – The United States and Canada.

• Europe – Countries in western and eastern Europe, including Russia.

• Asia Pacific – Countries on the western border of the Pacific ocean, including those on the Indo-Chinese peninsula and thePacific islands, and central Asia.

• Rest-of-World – Latin America (Brazil, Mexico, Argentina, and Central and South America) and regions not mentionedabove, particularly the Caribbean Islands, the Middle East, and Africa.

This research service also analyzes the total market and each of the segments from an end user perspective. The major endusers of NDT inspection services include:

• Oil and Gas – Includes refineries, both on-shore ad off-shore, and pipelines, both oil and gas.

• Power generation – Energy, utilities, co-generation, renewable and non-renewable power plants.

• Petrochemical and Chemical Industries– Includes ammonium plants, sodium, and other chemical plants.

• Manufacturing and Process Industries – Includes pulp and paper, pharmaceutical, rubber, cement, foundries, and other manufacturing plants.

• Others – Aerospace, military and defence, automotive, civil construction and transportation including railways and roadways.

Frost & Sullivan has not analyzed and broken down the world NDT inspection services market by technologiesbecause in any inspection procedure there is a combination of technologies used for inspection. As a result, theNDT inspection services providers generally provide all the NDT inspection service technologies.

21N94C-30

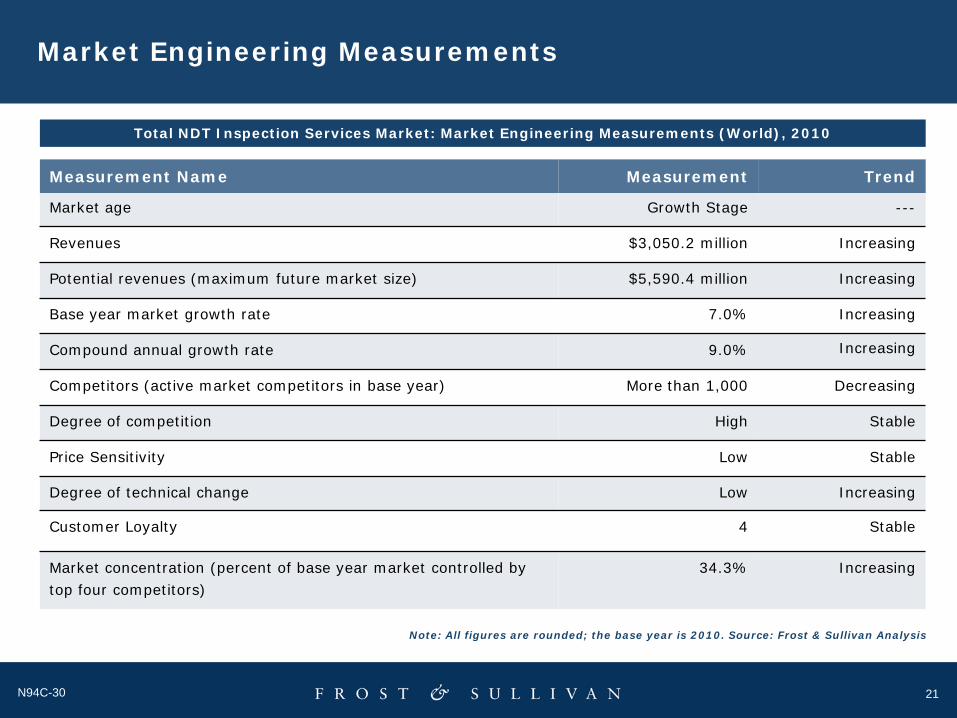

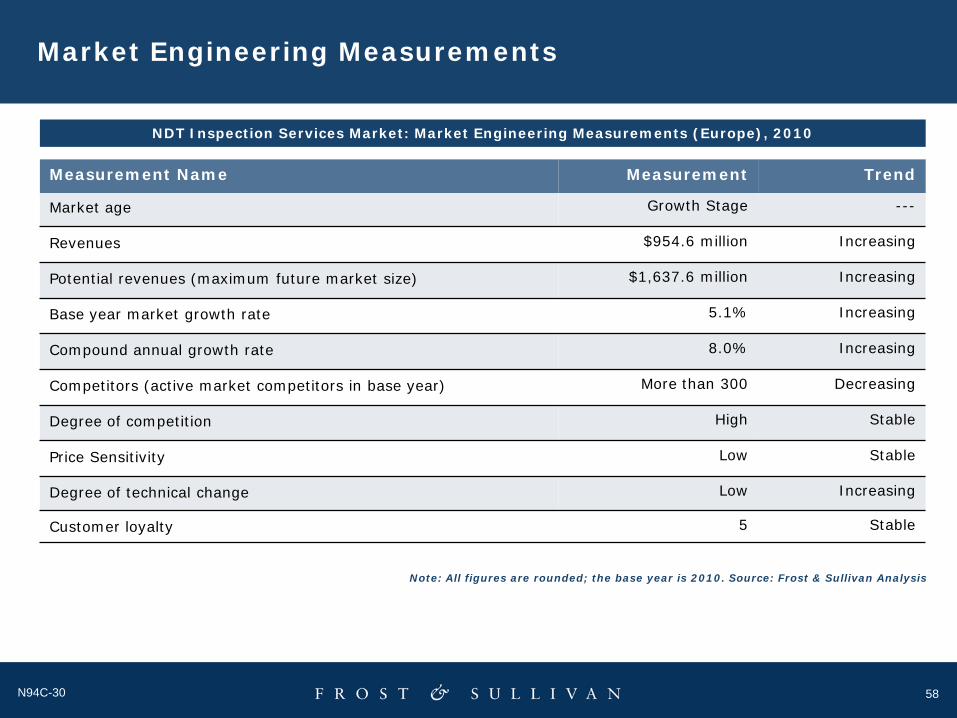

Market Engineering Measurements

Market age Growth Stage ---

Revenues $3,050.2 million Increasing

Potential revenues (maximum future market size) $5,590.4 million Increasing

Base year market growth rate 7.0% Increasing

Compound annual growth rate 9.0% Increasing

Competitors (active market competitors in base year) More than 1,000 Decreasing

Degree of competition High Stable

Price Sensitivity Low Stable

Degree of technical change Low Increasing

Customer Loyalty 4 Stable

Market concentration (percent of base year market controlled by top four competitors)

34.3% Increasing

Measurement Name Measurement Trend

Total NDT Inspection Services Market: Market Engineering Measurements (World), 2010

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan Analysis

22N94C-30

NDT Inspection ServicesMarket

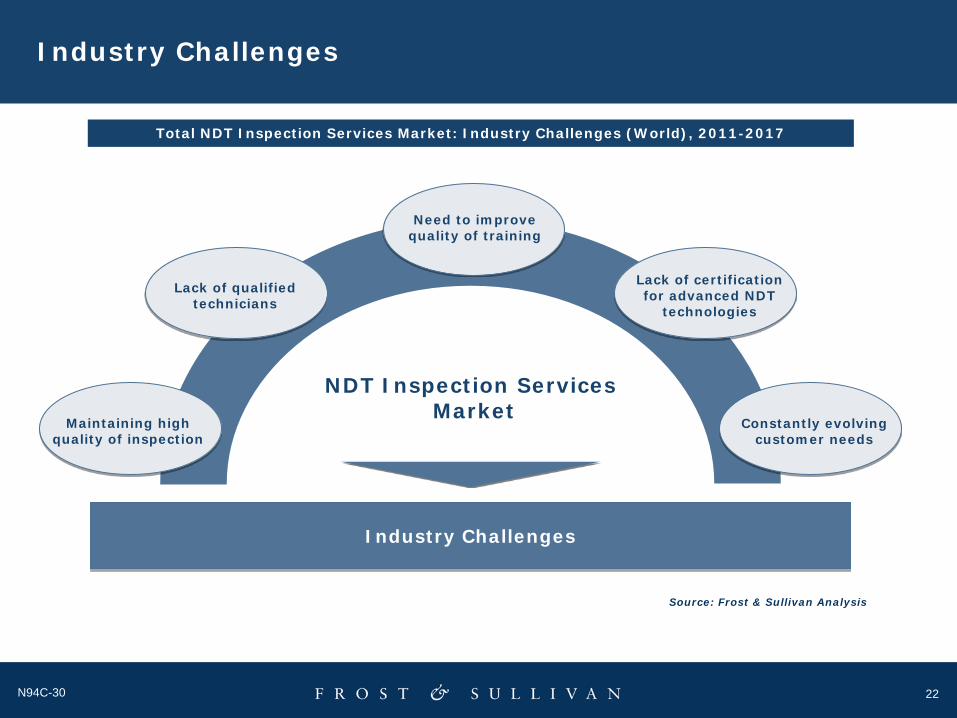

Industry Challenges

Constantly evolving customer needs

Industry Challenges

Source: Frost & Sullivan Analysis

Total NDT Inspection Services Market: Industry Challenges (World), 2011-2017

Maintaining high quality of inspection

Lack of qualified technicians

Need to improve quality of training

Lack of certification for advanced NDT

technologies

23N94C-30

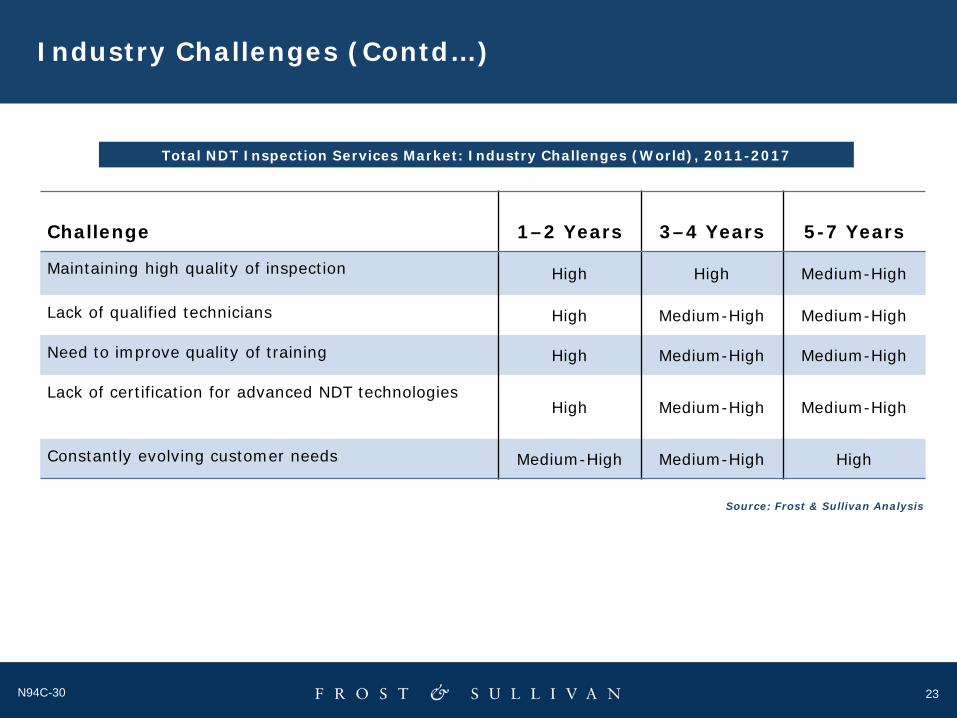

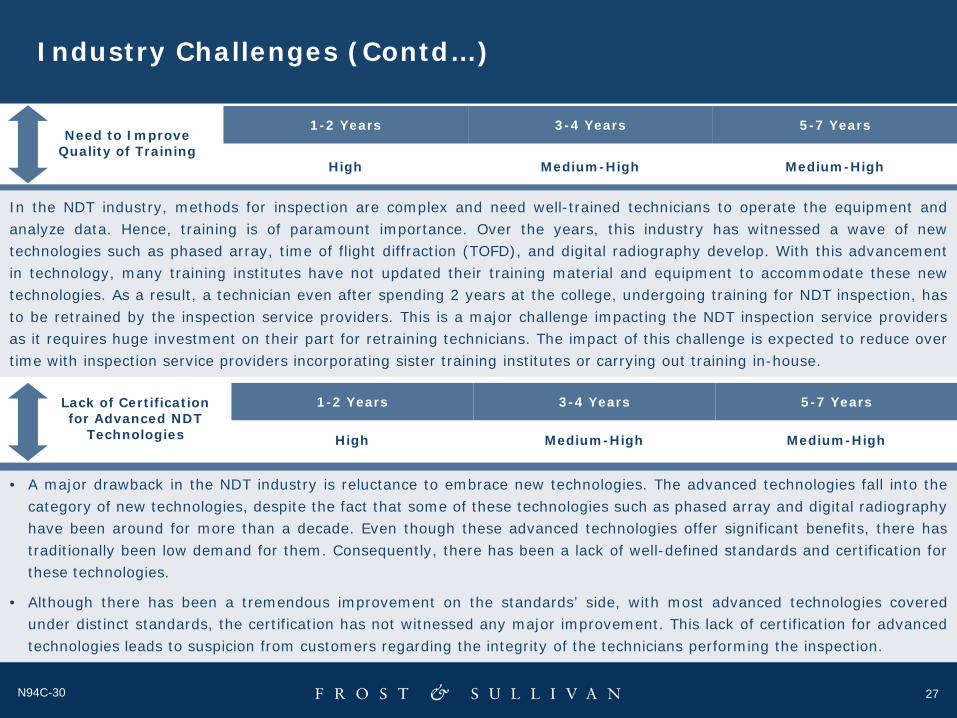

Industry Challenges (Contd…)

Challenge 1–2 Years 3–4 Years 5-7 Years

Maintaining high quality of inspection High High Medium-High

Lack of qualified technicians High Medium-High Medium-High

Need to improve quality of training High Medium-High Medium-High

Lack of certification for advanced NDT technologiesHigh Medium-High Medium-High

Constantly evolving customer needs Medium-High Medium-High High

Total NDT Inspection Services Market: Industry Challenges (World), 2011-2017

Source: Frost & Sullivan Analysis

24N94C-30

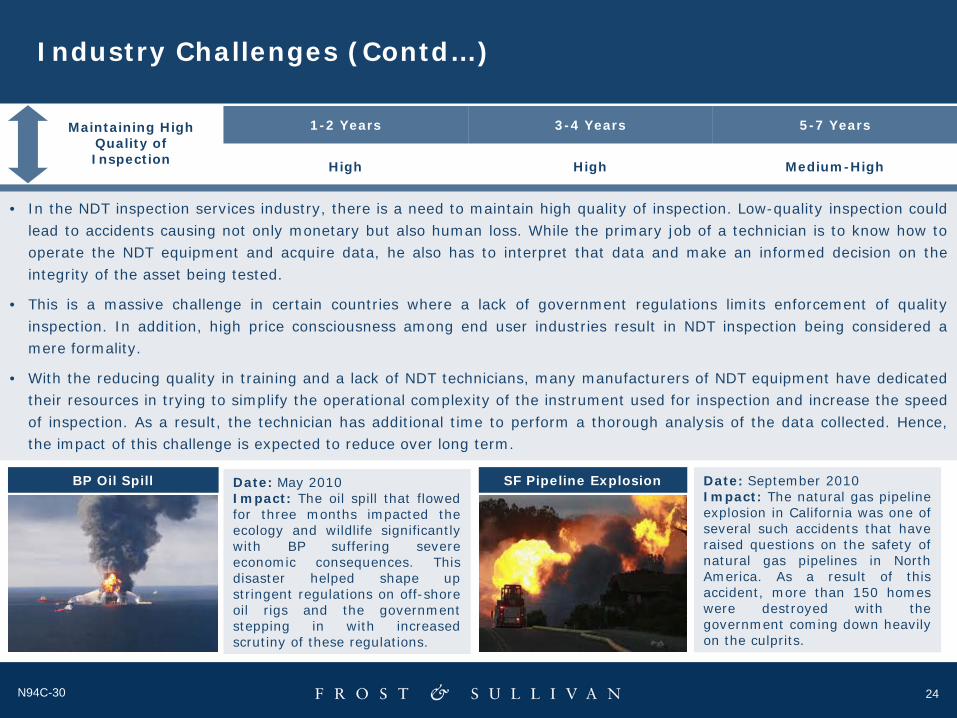

Industry Challenges (Contd…)

1-2 Years 3-4 Years 5-7 Years

High High Medium-High

• In the NDT inspection services industry, there is a need to maintain high quality of inspection. Low-quality inspection couldlead to accidents causing not only monetary but also human loss. While the primary job of a technician is to know how tooperate the NDT equipment and acquire data, he also has to interpret that data and make an informed decision on theintegrity of the asset being tested.

• This is a massive challenge in certain countries where a lack of government regulations limits enforcement of qualityinspection. In addition, high price consciousness among end user industries result in NDT inspection being considered amere formality.

• With the reducing quality in training and a lack of NDT technicians, many manufacturers of NDT equipment have dedicatedtheir resources in trying to simplify the operational complexity of the instrument used for inspection and increase the speedof inspection. As a result, the technician has additional time to perform a thorough analysis of the data collected. Hence,the impact of this challenge is expected to reduce over long term.

Maintaining High Quality of Inspection

BP Oil Spill Date: May 2010Impact: The oil spill that flowedfor three months impacted theecology and wildlife significantlywith BP suffering severeeconomic consequences. Thisdisaster helped shape upstringent regulations on off-shoreoil rigs and the governmentstepping in with increasedscrutiny of these regulations.

Date: September 2010Impact: The natural gas pipelineexplosion in California was one ofseveral such accidents that haveraised questions on the safety ofnatural gas pipelines in NorthAmerica. As a result of thisaccident, more than 150 homeswere destroyed with thegovernment coming down heavilyon the culprits.

SF Pipeline Explosion

25N94C-30

Industry Challenges (Contd…)

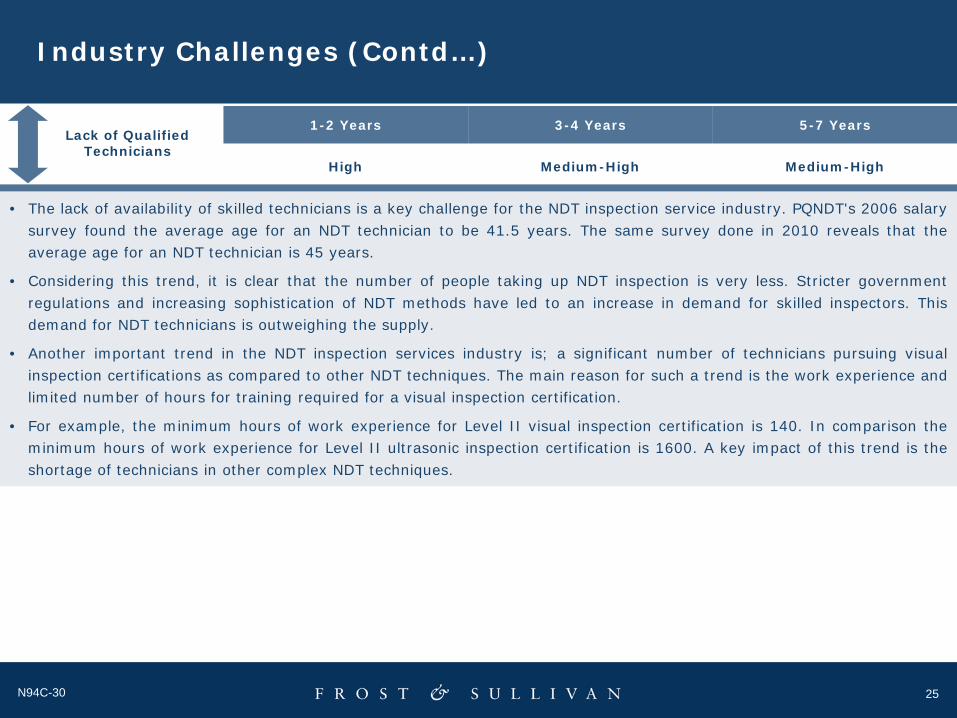

1-2 Years 3-4 Years 5-7 Years

High Medium-High Medium-High

Lack of Qualified Technicians

• The lack of availability of skilled technicians is a key challenge for the NDT inspection service industry. PQNDT's 2006 salarysurvey found the average age for an NDT technician to be 41.5 years. The same survey done in 2010 reveals that theaverage age for an NDT technician is 45 years.

• Considering this trend, it is clear that the number of people taking up NDT inspection is very less. Stricter governmentregulations and increasing sophistication of NDT methods have led to an increase in demand for skilled inspectors. Thisdemand for NDT technicians is outweighing the supply.

• Another important trend in the NDT inspection services industry is; a significant number of technicians pursuing visualinspection certifications as compared to other NDT techniques. The main reason for such a trend is the work experience andlimited number of hours for training required for a visual inspection certification.

• For example, the minimum hours of work experience for Level II visual inspection certification is 140. In comparison theminimum hours of work experience for Level II ultrasonic inspection certification is 1600. A key impact of this trend is theshortage of technicians in other complex NDT techniques.

26N94C-30

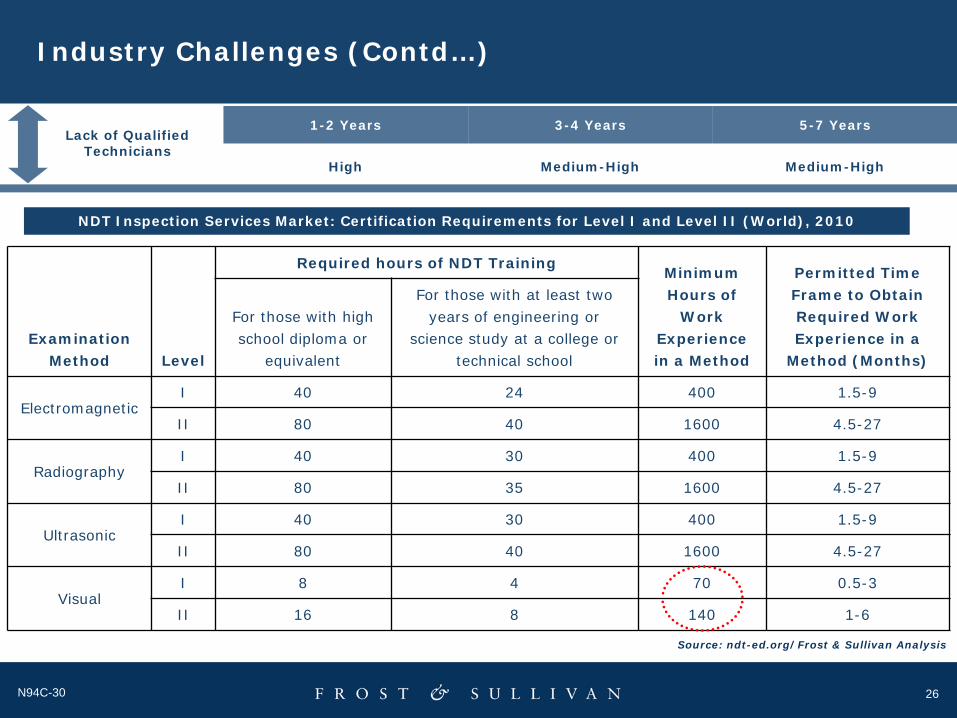

Industry Challenges (Contd…)

1-2 Years 3-4 Years 5-7 Years

High Medium-High Medium-High

Lack of Qualified Technicians

Examination Method Level

Required hours of NDT Training Minimum Hours of

Work Experience in a Method

Permitted Time Frame to Obtain Required Work Experience in a

Method (Months)

For those with high school diploma or

equivalent

For those with at least two years of engineering or

science study at a college or technical school

ElectromagneticI 40 24 400 1.5-9

II 80 40 1600 4.5-27

RadiographyI 40 30 400 1.5-9

II 80 35 1600 4.5-27

UltrasonicI 40 30 400 1.5-9

II 80 40 1600 4.5-27

VisualI 8 4 70 0.5-3

II 16 8 140 1-6

NDT Inspection Services Market: Certification Requirements for Level I and Level II (World), 2010

Source: ndt-ed.org/Frost & Sullivan Analysis

27N94C-30

Industry Challenges (Contd…)

1-2 Years 3-4 Years 5-7 Years

High Medium-High Medium-High

In the NDT industry, methods for inspection are complex and need well-trained technicians to operate the equipment andanalyze data. Hence, training is of paramount importance. Over the years, this industry has witnessed a wave of newtechnologies such as phased array, time of flight diffraction (TOFD), and digital radiography develop. With this advancementin technology, many training institutes have not updated their training material and equipment to accommodate these newtechnologies. As a result, a technician even after spending 2 years at the college, undergoing training for NDT inspection, hasto be retrained by the inspection service providers. This is a major challenge impacting the NDT inspection service providersas it requires huge investment on their part for retraining technicians. The impact of this challenge is expected to reduce overtime with inspection service providers incorporating sister training institutes or carrying out training in-house.

• A major drawback in the NDT industry is reluctance to embrace new technologies. The advanced technologies fall into thecategory of new technologies, despite the fact that some of these technologies such as phased array and digital radiographyhave been around for more than a decade. Even though these advanced technologies offer significant benefits, there hastraditionally been low demand for them. Consequently, there has been a lack of well-defined standards and certification forthese technologies.

• Although there has been a tremendous improvement on the standards’ side, with most advanced technologies coveredunder distinct standards, the certification has not witnessed any major improvement. This lack of certification for advancedtechnologies leads to suspicion from customers regarding the integrity of the technicians performing the inspection.

High Medium-High Medium-High

1-2 Years 3-4 Years 5-7 YearsLack of Certification for Advanced NDT

Technologies

Need to Improve Quality of Training

28N94C-30

Industry Challenges (Contd…)

1-2 Years 3-4 Years 5-7 Years

Medium-High Medium-High High

• Around the world, there have been questions raised regarding the future of energy supplies. These questions ariseespecially due to the concerns surrounding impact of global warming. Global warming is caused by excessive greenhousegas emission. The largest producers of these gases are thermal power plants. According to the EIA International EnergyOutlook 2010, the world marketed energy consumption is likely to increase by 49.0 percent from 2007 to 2035. Thereneeds to be a balance between addressing this demand for energy and trying to decrease the emission of greenhousegases. As a result, there has been a major push towards power generation from renewable energy sources such as wind,solar, and hydroelectric.

• Wind energy has witnessed rapid development in Europe, especially in Germany, Spain, and Denmark. Wind energy poses alot of difficulties toward NDT inspection as there is a lack of standardized methods for testing turbine blades and turbinetowers. On the solar side, photovoltaics have huge potential to generate power in sunnier countries. NDT on PV materials iscarried out on a micro-scale.

• With the advent of power generation from renewable sources of energy, technologies, methods and standards have alsohad to evolve, which poses a challenge for NDT inspection industry in trying to keep pace with ever-changing consumerneeds.

Constantly Evolving Customer

Needs

29N94C-30

Mar

ket D

river

sM

arke

t Res

trai

nts

Low

High

Low

High

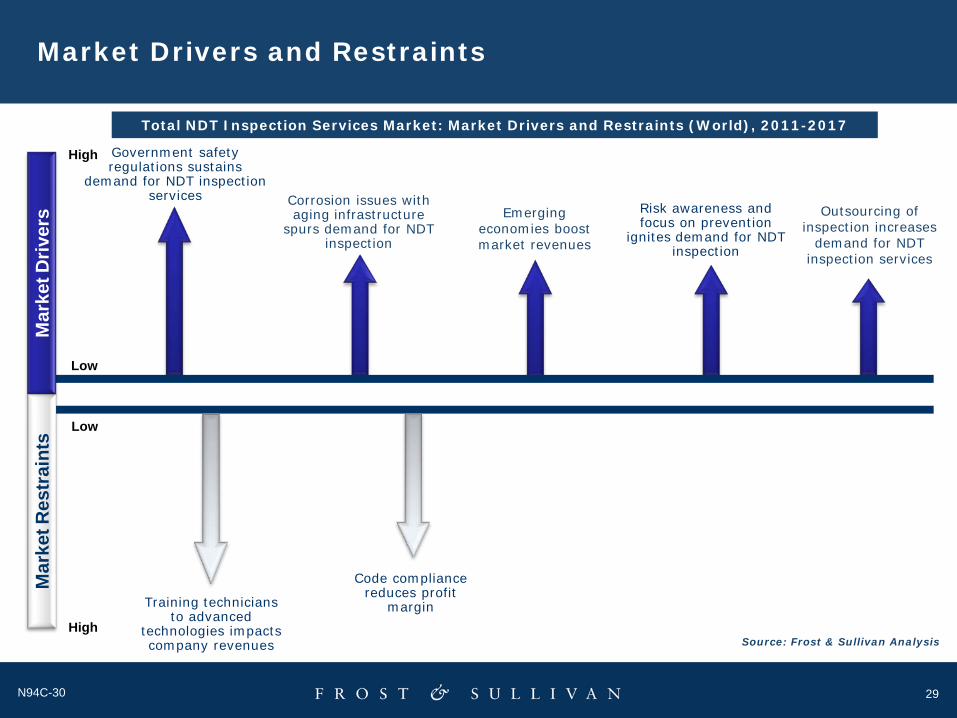

Market Drivers and Restraints

Source: Frost & Sullivan Analysis

Corrosion issues with aging infrastructure

spurs demand for NDT inspection

Government safety regulations sustains

demand for NDT inspection services

Risk awareness and focus on prevention

ignites demand for NDT inspection

Outsourcing of inspection increases

demand for NDT inspection services

Emerging economies boost market revenues

Code compliance reduces profit

marginTraining technicians to advanced

technologies impacts company revenues

Total NDT Inspection Services Market: Market Drivers and Restraints (World), 2011-2017

30N94C-30

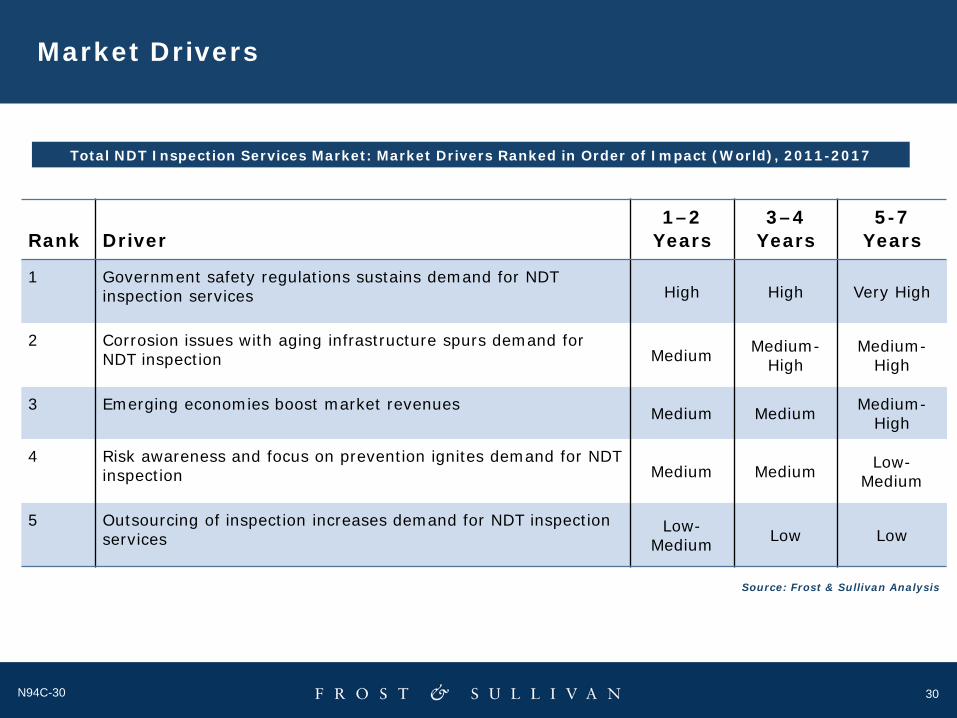

Market Drivers

Rank Driver1–2

Years3–4

Years5-7

Years

1 Government safety regulations sustains demand for NDT inspection services High High Very High

2 Corrosion issues with aging infrastructure spurs demand for NDT inspection Medium Medium-

HighMedium-

High

3 Emerging economies boost market revenues Medium Medium Medium-High

4 Risk awareness and focus on prevention ignites demand for NDT inspection Medium Medium Low-

Medium

5 Outsourcing of inspection increases demand for NDT inspection services

Low-Medium Low Low

Source: Frost & Sullivan Analysis

Total NDT Inspection Services Market: Market Drivers Ranked in Order of Impact (World), 2011-2017

31N94C-30

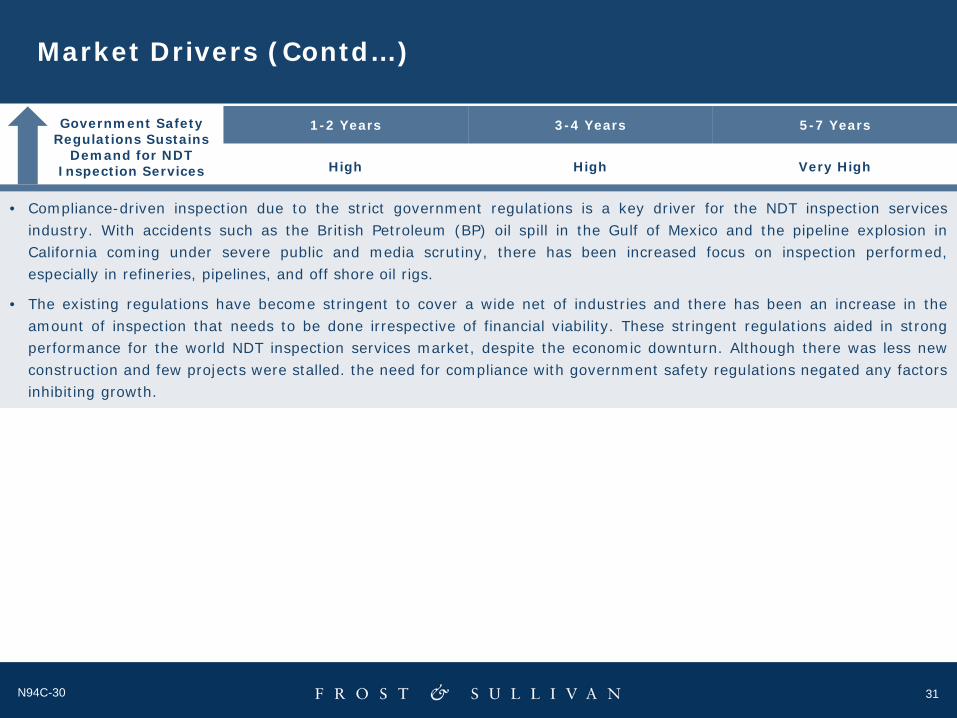

Market Drivers (Contd…)

1-2 Years 3-4 Years 5-7 Years

High High Very High

Government Safety Regulations Sustains

Demand for NDT Inspection Services

• Compliance-driven inspection due to the strict government regulations is a key driver for the NDT inspection servicesindustry. With accidents such as the British Petroleum (BP) oil spill in the Gulf of Mexico and the pipeline explosion inCalifornia coming under severe public and media scrutiny, there has been increased focus on inspection performed,especially in refineries, pipelines, and off shore oil rigs.

• The existing regulations have become stringent to cover a wide net of industries and there has been an increase in theamount of inspection that needs to be done irrespective of financial viability. These stringent regulations aided in strongperformance for the world NDT inspection services market, despite the economic downturn. Although there was less newconstruction and few projects were stalled. the need for compliance with government safety regulations negated any factorsinhibiting growth.

32N94C-30

Market Drivers (Contd…)

1-2 Years 3-4 Years 5-7 Years

Medium Medium-High Medium-High

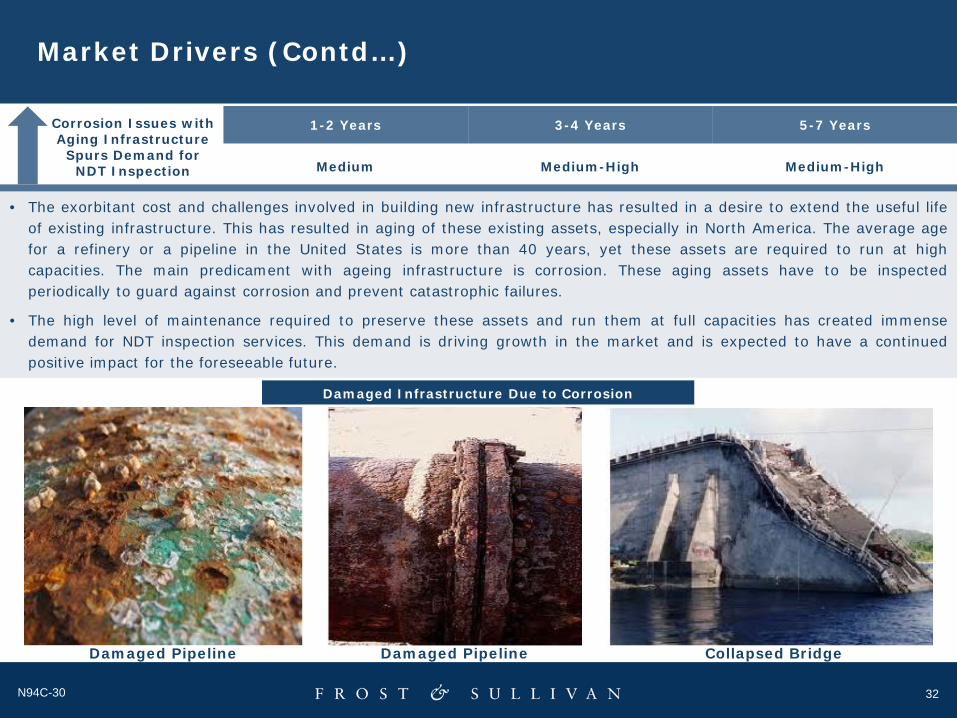

Corrosion Issues with Aging Infrastructure

Spurs Demand for NDT Inspection

• The exorbitant cost and challenges involved in building new infrastructure has resulted in a desire to extend the useful lifeof existing infrastructure. This has resulted in aging of these existing assets, especially in North America. The average agefor a refinery or a pipeline in the United States is more than 40 years, yet these assets are required to run at highcapacities. The main predicament with ageing infrastructure is corrosion. These aging assets have to be inspectedperiodically to guard against corrosion and prevent catastrophic failures.

• The high level of maintenance required to preserve these assets and run them at full capacities has created immensedemand for NDT inspection services. This demand is driving growth in the market and is expected to have a continuedpositive impact for the foreseeable future.

Damaged Infrastructure Due to Corrosion

Damaged Pipeline Damaged Pipeline Collapsed Bridge

33N94C-30

Market Drivers (Contd…)

1-2 Years 3-4 Years 5-7 Years

Medium Medium Medium-High

Emerging Economies Boost Market Revenues

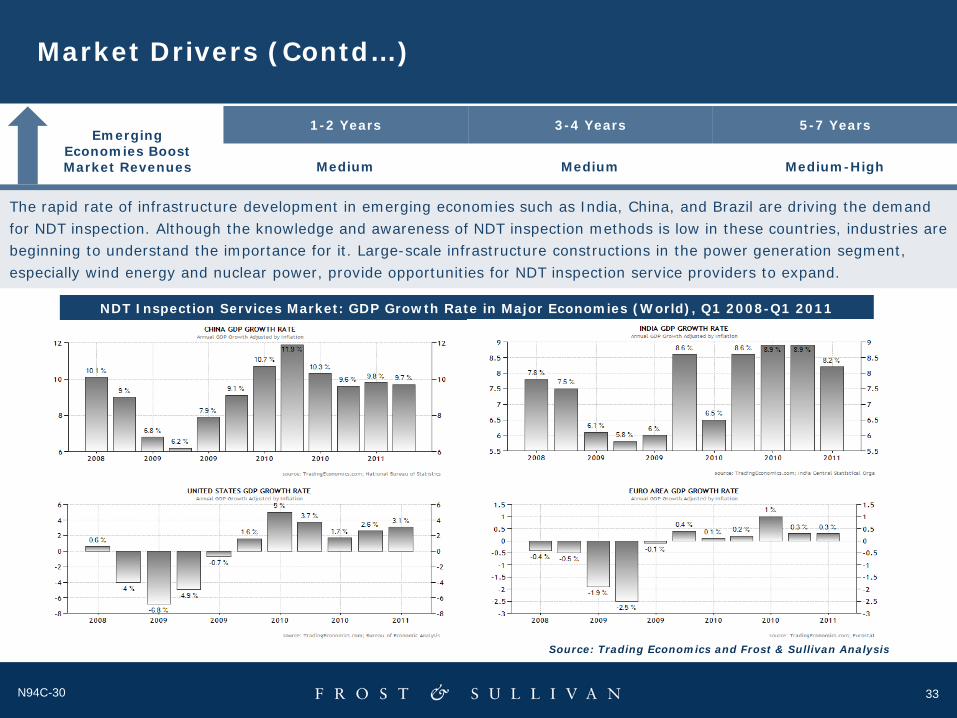

The rapid rate of infrastructure development in emerging economies such as India, China, and Brazil are driving the demand for NDT inspection. Although the knowledge and awareness of NDT inspection methods is low in these countries, industries are beginning to understand the importance for it. Large-scale infrastructure constructions in the power generation segment, especially wind energy and nuclear power, provide opportunities for NDT inspection service providers to expand.

Source: Trading Economics and Frost & Sullivan Analysis

NDT Inspection Services Market: GDP Growth Rate in Major Economies (World), Q1 2008-Q1 2011

34N94C-30

Market Drivers (Contd…)

1-2 Years 3-4 Years 5-7 Years

Medium Medium Low-Medium

• In the present highly competitive world, shutting down operations even for a few minutes has high cost implications. Theeconomic downturn during 2008 and 2009 also emphasized the importance of maintaining asset integrity. These stepshelped end users to guard against severe impacts that malfunctioning assets would have on the already low profitability.

• In some of the more critical applications where failure of assets would result in not only monetary loss but also loss to theenvironment or people, prevention is of paramount importance. In addition, end users of NDT inspection services arerapidly realizing the importance of prevention as failures can incur severe financial penalties.

• This is a key driver for the market in geographic regions such as Asia Pacific, the Middle East, and Africa where traditionallya lack of awareness has inhibited demand. But with a drive towards safety from end users and an improved understandingof the importance of NDT, demand for NDT inspection services has increased.

• Traditionally, NDT inspection in industries such as oil and gas, power generation, and process industries were done in-house. But with the increased sophistication of the methods for inspection, these end users are turning to NDT inspectionservice providers for all there inspection needs.

• In addition, the amount of training required for certain advanced techniques and increased scrutiny of inspection and safetyaspects, have made it financially viable for these industries to get their inspection outsourced. This trend has resulted in anincrease in the availability of work for NDT inspection service providers and has hence helped drive this market.

Low-Medium Low Low

1-2 Years 3-4 Years 5-7 YearsOutsourcing of

Inspection Increases Demand for NDT

Inspection Services

Risk Awareness and Focus on Prevention Ignites Demand for

NDT Inspection

35N94C-30

Market Restraints

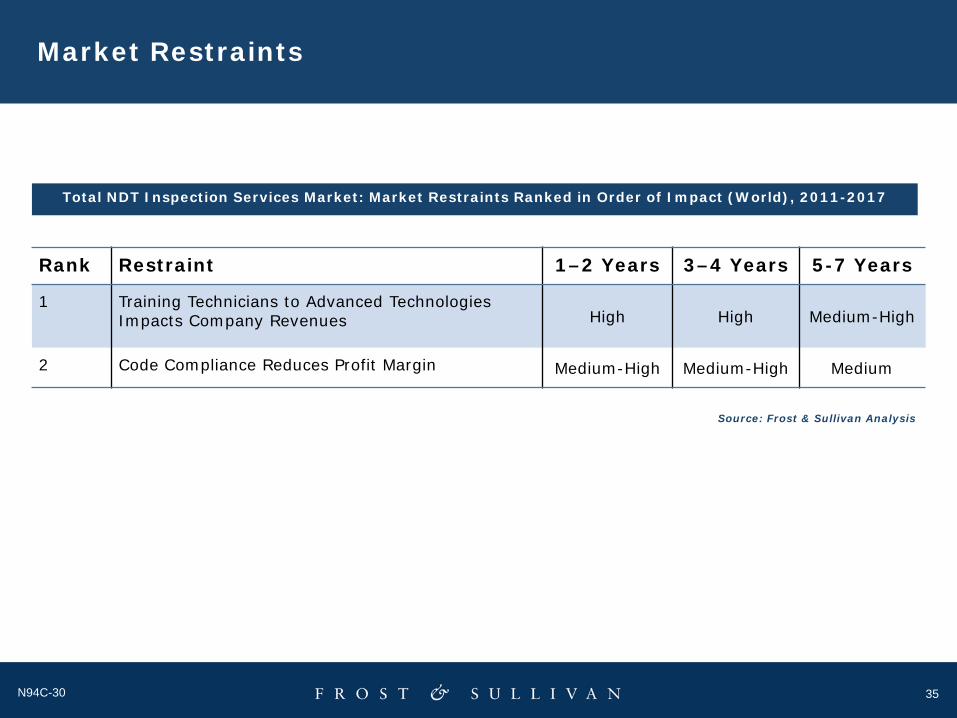

Rank Restraint 1–2 Years 3–4 Years 5-7 Years

1 Training Technicians to Advanced Technologies Impacts Company Revenues High High Medium-High

2 Code Compliance Reduces Profit Margin Medium-High Medium-High Medium

Source: Frost & Sullivan Analysis

Total NDT Inspection Services Market: Market Restraints Ranked in Order of Impact (World), 2011-2017

36N94C-30

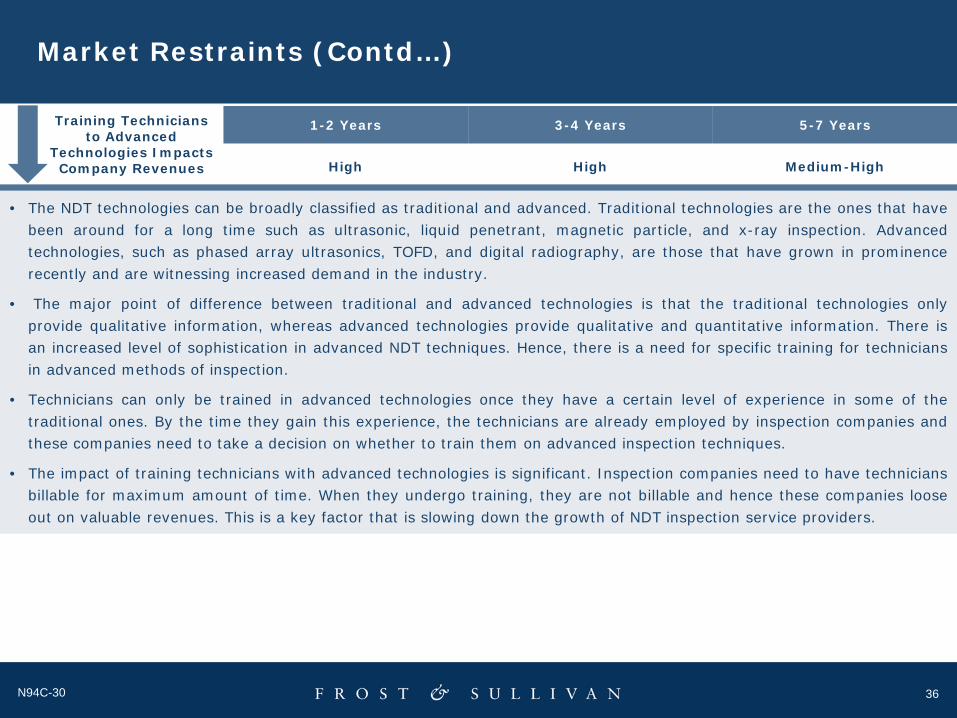

Market Restraints (Contd…)

1-2 Years 3-4 Years 5-7 Years

High High Medium-High

Training Technicians to Advanced

Technologies Impacts Company Revenues

• The NDT technologies can be broadly classified as traditional and advanced. Traditional technologies are the ones that havebeen around for a long time such as ultrasonic, liquid penetrant, magnetic particle, and x-ray inspection. Advancedtechnologies, such as phased array ultrasonics, TOFD, and digital radiography, are those that have grown in prominencerecently and are witnessing increased demand in the industry.

• The major point of difference between traditional and advanced technologies is that the traditional technologies onlyprovide qualitative information, whereas advanced technologies provide qualitative and quantitative information. There isan increased level of sophistication in advanced NDT techniques. Hence, there is a need for specific training for techniciansin advanced methods of inspection.

• Technicians can only be trained in advanced technologies once they have a certain level of experience in some of thetraditional ones. By the time they gain this experience, the technicians are already employed by inspection companies andthese companies need to take a decision on whether to train them on advanced inspection techniques.

• The impact of training technicians with advanced technologies is significant. Inspection companies need to have techniciansbillable for maximum amount of time. When they undergo training, they are not billable and hence these companies looseout on valuable revenues. This is a key factor that is slowing down the growth of NDT inspection service providers.

37N94C-30

Market Restraints (Contd…)

1-2 Years 3-4 Years 5-7 Years

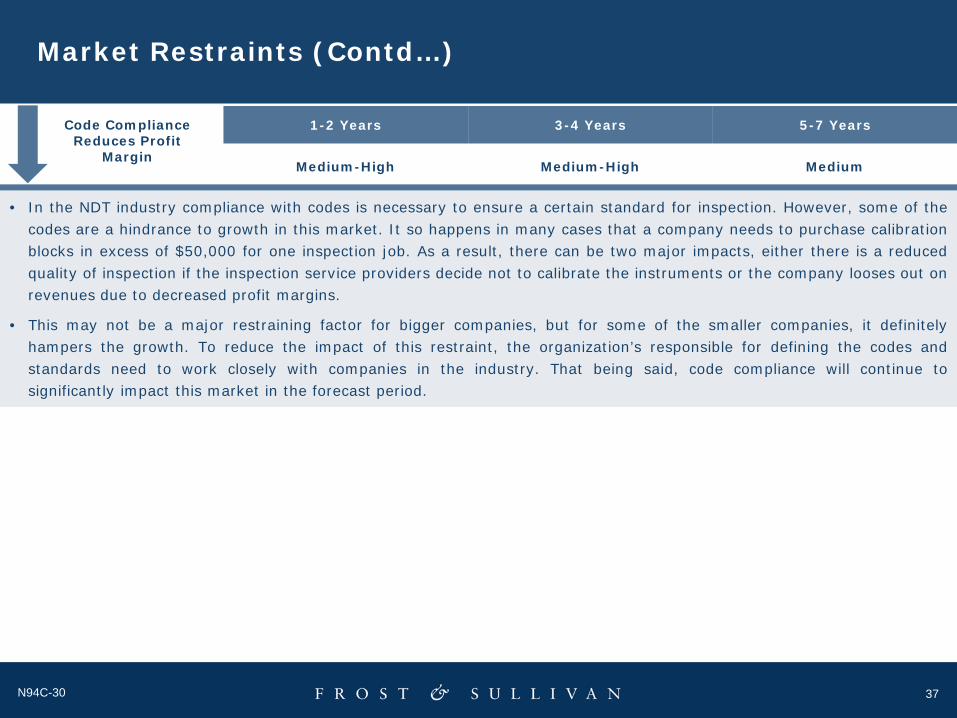

Medium-High Medium-High Medium

Code Compliance Reduces Profit

Margin

• In the NDT industry compliance with codes is necessary to ensure a certain standard for inspection. However, some of thecodes are a hindrance to growth in this market. It so happens in many cases that a company needs to purchase calibrationblocks in excess of $50,000 for one inspection job. As a result, there can be two major impacts, either there is a reducedquality of inspection if the inspection service providers decide not to calibrate the instruments or the company looses out onrevenues due to decreased profit margins.

• This may not be a major restraining factor for bigger companies, but for some of the smaller companies, it definitelyhampers the growth. To reduce the impact of this restraint, the organization’s responsible for defining the codes andstandards need to work closely with companies in the industry. That being said, code compliance will continue tosignificantly impact this market in the forecast period.

38N94C-30

Market Trends

1-2 Years 3-4 Years 5-7 Years

High Medium-High High

Mergers and Acquisitions

• Consolidation has been a key trend in the NDT industry, especially over the past few years. In the NDT inspection servicesmarket, there have been some important mergers and acquisitions. A major reason for this is the impact of economicdownturn, which affected some of the smaller companies significantly. Companies struggled to survive in such a challengingand dampening economic conditions and, as a result were acquired by some of the bigger market participants.Globalization was another factor, which fuelled mergers and acquisitions activity in this market.

• Many companies recognize the importance of expanding geographically and acquiring middle-market companies in regionswhere they have minimal presence, giving them greater global reach. It is also used as an effective strategy to accelerategrowth in such a fragmented market.

Acquirer Acquired*

Acuren Extech, Bretech Inspection, Remote Access Technologies

Applus RTD Valley Industrial X-ray & Inspection, Staveley Services,Quality Inspection Services, Technicio (2009), JanX (2008)

SGS Yan Tai Hua Jian Inspection Engineering Ltd, FTS (2007)

TUV SUD Mechanical Integrity, Rail Sciences, NDT group (2008),Petrochem Inspection (2006)

NDT Inspection Services Market: Significant Mergers and Acquisitions (World), 2010

Source: Frost & Sullivan Analysis*Note: 2010 unless mentioned

39N94C-30

Market Trends (Contd…)

• Traditionally, the NDT industry has been slow in accepting advanced technologies. Techniques such as phased arrayultrasonics, TOFD, and digital radiography have been around for decades but have not witnessed huge acceptance. This isdue to the fact that there is reluctance from end users in shifting from traditional methods which have been around formore than 100 years.

• The first industrial phased array system was introduced in the 1980s, but it has only been in the last few years that it hasseen acceptance. There has been improved demand for these systems from end users as technology awareness hasimproved. Another factor that has aided this demand has been the increase in availability of equipment and training foradvanced technologies.

Drive Towards Advanced Technologies

High Medium-High Medium-High

1-2 Years 3-4 Years 5-7 Years

Phased Array Ultrasonics TOFD Digital Radiography

Some Advanced NDT Technologies

40N94C-30

Technology Trends

• The NDT technologies can be broadly categorized as:-

1. Traditional NDT techniques

2. Advanced NDT techniques

• Traditional NDT Techniques – These are basic techniques that have been in use for a long time. The main techniquesunder traditional NDT are ultrasonic, visual, surface, and radiography. These services are generally offered by all the NDTinspection service providers as they form the base of any inspection. As these techniques are around for a large period oftime, they have well-defined standards and training certification courses.

• Advanced NDT Techniques – These are derived from traditional NDT techniques but are more complex in nature. Theyhave been developed and improved quite recently and hence are not in demand heavily. As a result, all of these techniquesare not offered by NDT inspection service providers. It depends on the availability of highly trained technicians and thedemand from the customers. Some of the main techniques covered under this category are remote field testing, phasedarray ultrasonics, time of flight diffraction (TOFD), alternating current field measurement, guided wave ultrasonics, andmagnetic flux leakage. These are some of the more popular advanced techniques.

• There are many niche technologies as well provided by specialized NDT inspection service providers. One such technologyis process compensated resonance testing. This technique is offered by Vibrant NDT, mainly to the aerospace andautomotive segments.

• Most end users of NDT inspection services use a combination of technologies to meet their inspection needs. The structureor the unit under test is assessed and then a technology or a combination of technologies is recommended for NDTinspection.

41N94C-30

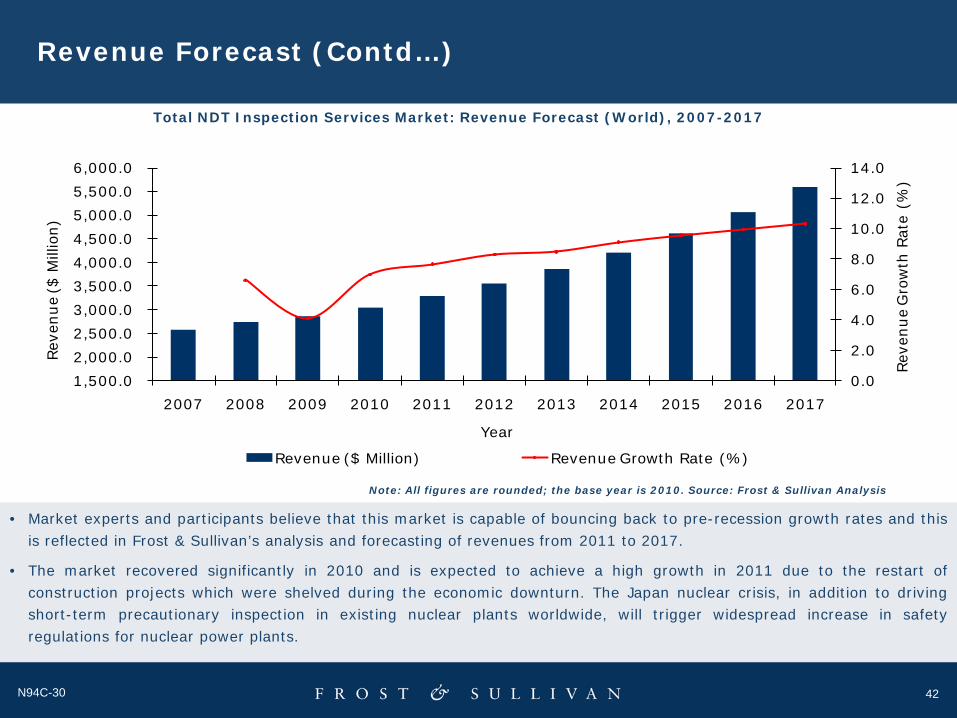

Revenue Forecast

YearRevenue

($ Million)

RevenueGrowth Rate

(%)

2007 2,568.5 ---

2008 2,738.4 6.6

2009 2,850.7 4.1

2010 3,050.2 7.0

2011 3,283.7 7.7

2012 3,555.4 8.3

2013 3,856.9 8.5

2014 4,208.2 9.1

2015 4,609.8 9.5

2016 5,067.4 9.9

2017 5,590.4 10.3

Compound Annual Growth Rate (2010-2017): 9.0%

Total NDT Inspection Services Market: Revenue Forecast (World), 2007-2017

Note: All figures are rounded; the base year is 2010.Source: Frost & Sullivan Analysis

• The global economic downturn that hit in late 2008impacted the revenue growth rate of this market. Capitalexpenditure cuts and review of inspection budgetsadversely affected the growth of third-party NDT inspectionservice providers. In 2008, the market witnessed a badending to a possibly good year in terms of revenues. Frost& Sullivan’s analysis shows that the market grew by 6.6percent in 2008.

• 2009 witnessed economic uncertainty affecting capitalexpenditure, and as a result, many new constructionprojects were postponed. This impacted the revenues to acertain extent but the operational expenditure was highdue to compliance-driven inspection of refineries, pipelinesetc despite financial constraints.

• This was one of the key reasons why the market did notdecline in revenues but witnessed a slower revenue growthrate as compared to the previous year.

• Another key reason for significantly low impact of theeconomic downturn in 2009 was increased scrutiny ofinspection by safety regulatory bodies due to high-profileinfrastructure failures and accidents such as the BritishPetroleum (BP) oil spill, California pipeline explosion, andMississippi river bridge collapse.

42N94C-30

Revenue Forecast (Contd…)

Total NDT Inspection Services Market: Revenue Forecast (World), 2007-2017

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

1,500.0 2,000.0 2,500.0 3,000.0 3,500.0 4,000.0 4,500.0 5,000.0 5,500.0 6,000.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Reve

nue

Gro

wth

Rat

e (%

)

Reve

nue

($ M

illio

n)

Year

Revenue ($ Million) Revenue Growth Rate (%)

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan Analysis

• Market experts and participants believe that this market is capable of bouncing back to pre-recession growth rates and thisis reflected in Frost & Sullivan’s analysis and forecasting of revenues from 2011 to 2017.

• The market recovered significantly in 2010 and is expected to achieve a high growth in 2011 due to the restart ofconstruction projects which were shelved during the economic downturn. The Japan nuclear crisis, in addition to drivingshort-term precautionary inspection in existing nuclear plants worldwide, will trigger widespread increase in safetyregulations for nuclear power plants.

43N94C-30

Trends by End User

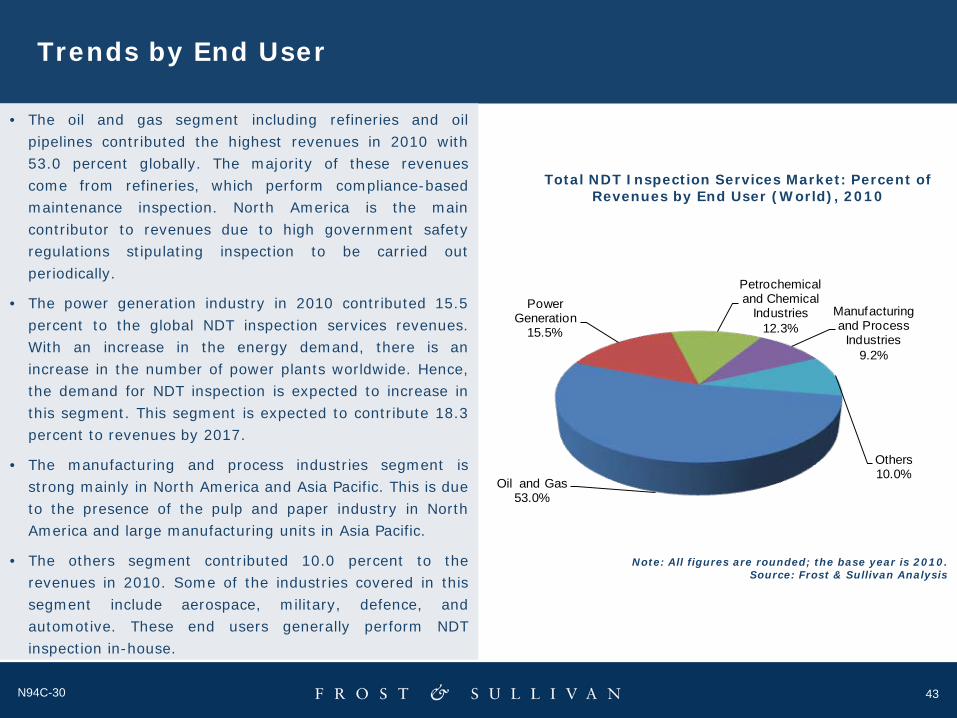

• The oil and gas segment including refineries and oilpipelines contributed the highest revenues in 2010 with53.0 percent globally. The majority of these revenuescome from refineries, which perform compliance-basedmaintenance inspection. North America is the maincontributor to revenues due to high government safetyregulations stipulating inspection to be carried outperiodically.

• The power generation industry in 2010 contributed 15.5percent to the global NDT inspection services revenues.With an increase in the energy demand, there is anincrease in the number of power plants worldwide. Hence,the demand for NDT inspection is expected to increase inthis segment. This segment is expected to contribute 18.3percent to revenues by 2017.

• The manufacturing and process industries segment isstrong mainly in North America and Asia Pacific. This is dueto the presence of the pulp and paper industry in NorthAmerica and large manufacturing units in Asia Pacific.

• The others segment contributed 10.0 percent to therevenues in 2010. Some of the industries covered in thissegment include aerospace, military, defence, andautomotive. These end users generally perform NDTinspection in-house.

Total NDT Inspection Services Market: Percent of Revenues by End User (World), 2010

Note: All figures are rounded; the base year is 2010.Source: Frost & Sullivan Analysis

Oil and Gas53.0%

Power Generation

15.5%

Petrochemical and Chemical

Industries12.3%

Manufacturing and Process

Industries9.2%

Others10.0%

44N94C-30

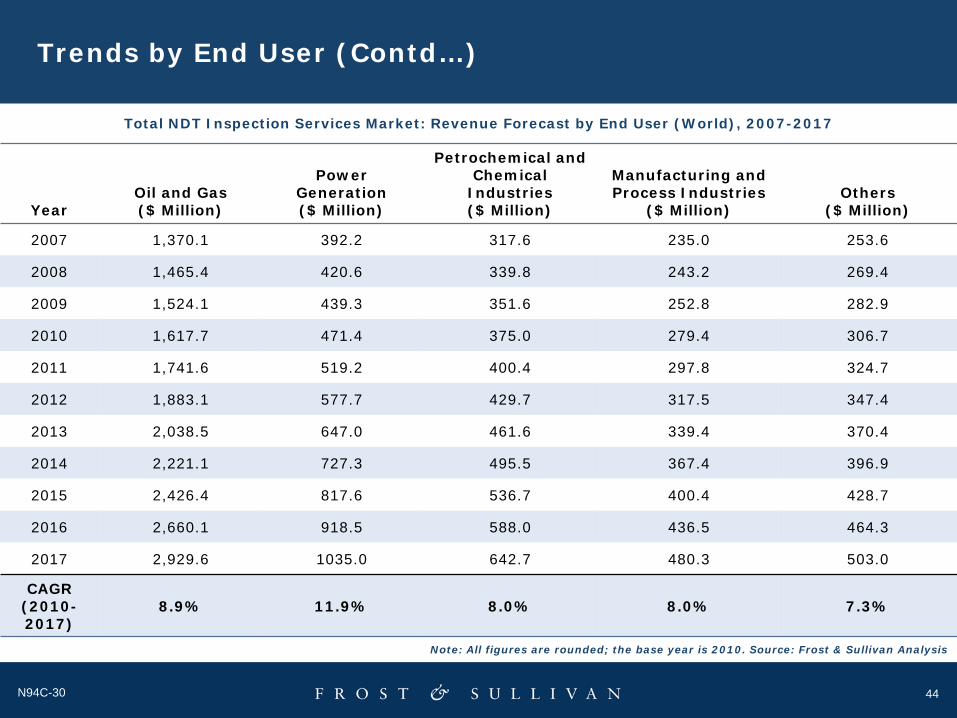

Trends by End User (Contd…)

YearOil and Gas($ Million)

Power Generation($ Million)

Petrochemical and Chemical

Industries($ Million)

Manufacturing and Process Industries

($ Million)Others

($ Million)

2007 1,370.1 392.2 317.6 235.0 253.6

2008 1,465.4 420.6 339.8 243.2 269.4

2009 1,524.1 439.3 351.6 252.8 282.9

2010 1,617.7 471.4 375.0 279.4 306.7

2011 1,741.6 519.2 400.4 297.8 324.7

2012 1,883.1 577.7 429.7 317.5 347.4

2013 2,038.5 647.0 461.6 339.4 370.4

2014 2,221.1 727.3 495.5 367.4 396.9

2015 2,426.4 817.6 536.7 400.4 428.7

2016 2,660.1 918.5 588.0 436.5 464.3

2017 2,929.6 1035.0 642.7 480.3 503.0

CAGR (2010-2017)

8.9% 11.9% 8.0% 8.0% 7.3%

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan Analysis

Total NDT Inspection Services Market: Revenue Forecast by End User (World), 2007-2017

45N94C-30

Trends by End User (Contd…)

• In terms of revenue contribution, the oil and gas segment remains the highest and is expected to continue that way till2017. In this segment, maintenance-driven inspection in refineries plays a pivotal role in driving revenues.

• The other segment, oil pipelines, contributes in a small but significant way. With the recent pipeline explosions in NorthAmerica, the inspection in this sector is at an all-time high.

• The power generation industry is expected to witness the highest growth in the NDT inspection services market with CAGRof 11.7 percent. The catalyst for such high growth is the increased importance given to renewable energy.

• The nuclear industry is one of the key users of NDT inspection due to the importance of safety in hazardous surroundings.With more than 60 nuclear power plants under construction worldwide and many more in the pipeline, power generation isexpected to drive this market in the future.

• Manufacturing and process industries are expected to witness slow growth with respect to NDT inspection. The maincontributor in this segment, pulp and paper, has been on a steady decline over the past few years. This has impacted theinvestment in NDT inspection services. As a result, the demand for NDT inspection services has suffered and this trend isexpected to continue over the forecast period.

• That being said, the manufacturing industry is likely to shed its sluggish growth exhibited over the last 2 years due toeconomic downturn and bounce back in a significant way. Hence, demand for NDT inspection in the manufacturing industryis expected to grow.

46N94C-30

Trends by Geography

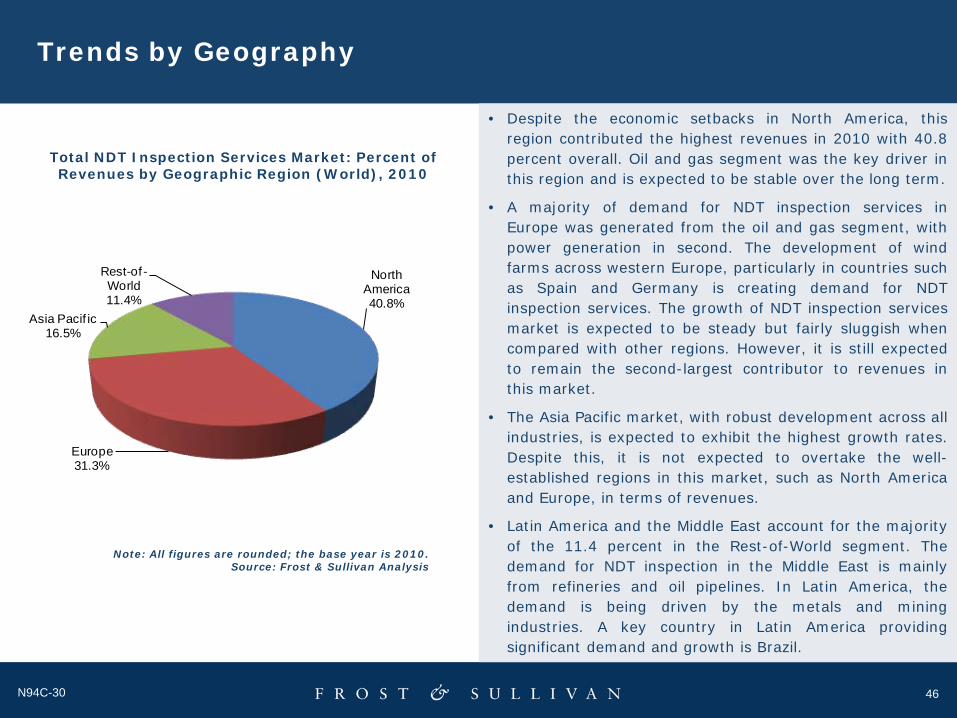

• Despite the economic setbacks in North America, thisregion contributed the highest revenues in 2010 with 40.8percent overall. Oil and gas segment was the key driver inthis region and is expected to be stable over the long term.

• A majority of demand for NDT inspection services inEurope was generated from the oil and gas segment, withpower generation in second. The development of windfarms across western Europe, particularly in countries suchas Spain and Germany is creating demand for NDTinspection services. The growth of NDT inspection servicesmarket is expected to be steady but fairly sluggish whencompared with other regions. However, it is still expectedto remain the second-largest contributor to revenues inthis market.

• The Asia Pacific market, with robust development across allindustries, is expected to exhibit the highest growth rates.Despite this, it is not expected to overtake the well-established regions in this market, such as North Americaand Europe, in terms of revenues.

• Latin America and the Middle East account for the majorityof the 11.4 percent in the Rest-of-World segment. Thedemand for NDT inspection in the Middle East is mainlyfrom refineries and oil pipelines. In Latin America, thedemand is being driven by the metals and miningindustries. A key country in Latin America providingsignificant demand and growth is Brazil.

Total NDT Inspection Services Market: Percent of Revenues by Geographic Region (World), 2010

Note: All figures are rounded; the base year is 2010.Source: Frost & Sullivan Analysis

North America40.8%

Europe31.3%

Asia Pacif ic16.5%

Rest-of -World11.4%

47N94C-30

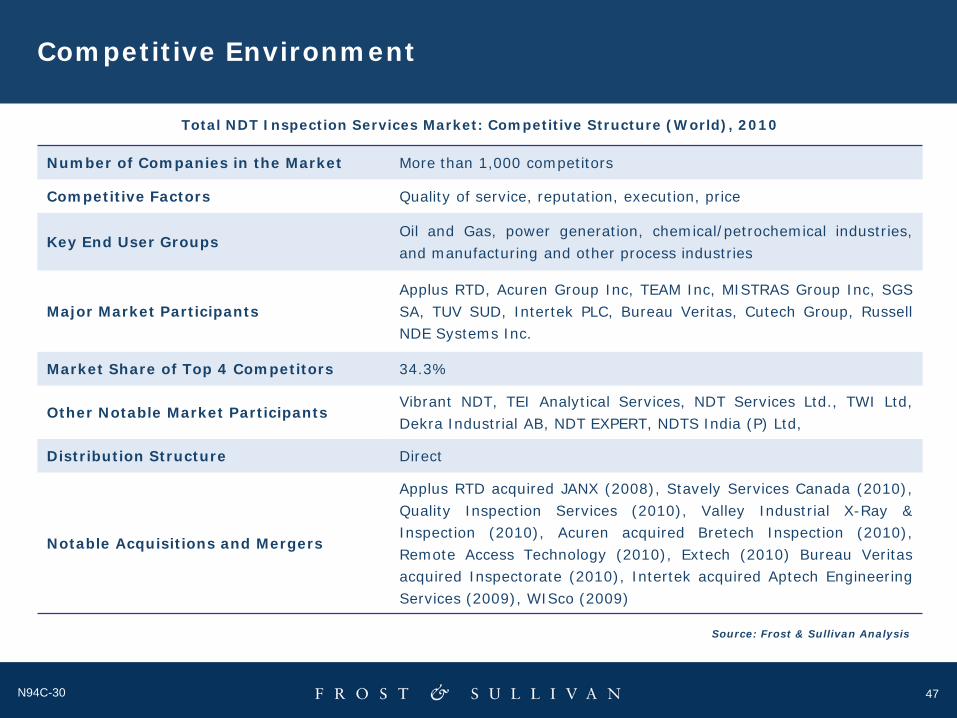

Competitive Environment

Total NDT Inspection Services Market: Competitive Structure (World), 2010

Number of Companies in the Market More than 1,000 competitors

Competitive Factors Quality of service, reputation, execution, price

Key End User GroupsOil and Gas, power generation, chemical/petrochemical industries,and manufacturing and other process industries

Major Market ParticipantsApplus RTD, Acuren Group Inc, TEAM Inc, MISTRAS Group Inc, SGSSA, TUV SUD, Intertek PLC, Bureau Veritas, Cutech Group, RussellNDE Systems Inc.

Market Share of Top 4 Competitors 34.3%

Other Notable Market ParticipantsVibrant NDT, TEI Analytical Services, NDT Services Ltd., TWI Ltd,Dekra Industrial AB, NDT EXPERT, NDTS India (P) Ltd,

Distribution Structure Direct

Notable Acquisitions and Mergers

Applus RTD acquired JANX (2008), Stavely Services Canada (2010),Quality Inspection Services (2010), Valley Industrial X-Ray &Inspection (2010), Acuren acquired Bretech Inspection (2010),Remote Access Technology (2010), Extech (2010) Bureau Veritasacquired Inspectorate (2010), Intertek acquired Aptech EngineeringServices (2009), WISco (2009)

Source: Frost & Sullivan Analysis

48N94C-30

Market Share Analysis

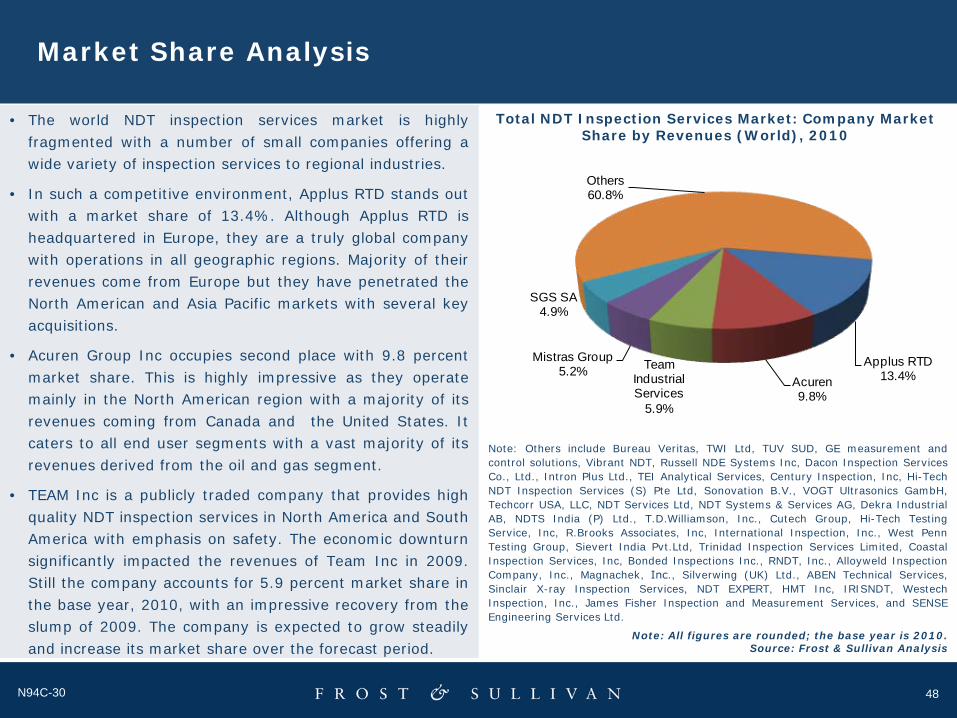

• The world NDT inspection services market is highlyfragmented with a number of small companies offering awide variety of inspection services to regional industries.

• In such a competitive environment, Applus RTD stands outwith a market share of 13.4%. Although Applus RTD isheadquartered in Europe, they are a truly global companywith operations in all geographic regions. Majority of theirrevenues come from Europe but they have penetrated theNorth American and Asia Pacific markets with several keyacquisitions.

• Acuren Group Inc occupies second place with 9.8 percentmarket share. This is highly impressive as they operatemainly in the North American region with a majority of itsrevenues coming from Canada and the United States. Itcaters to all end user segments with a vast majority of itsrevenues derived from the oil and gas segment.

• TEAM Inc is a publicly traded company that provides highquality NDT inspection services in North America and SouthAmerica with emphasis on safety. The economic downturnsignificantly impacted the revenues of Team Inc in 2009.Still the company accounts for 5.9 percent market share inthe base year, 2010, with an impressive recovery from theslump of 2009. The company is expected to grow steadilyand increase its market share over the forecast period.

Total NDT Inspection Services Market: Company Market Share by Revenues (World), 2010

Note: All figures are rounded; the base year is 2010.Source: Frost & Sullivan Analysis

Note: Others include Bureau Veritas, TWI Ltd, TUV SUD, GE measurement andcontrol solutions, Vibrant NDT, Russell NDE Systems Inc, Dacon Inspection ServicesCo., Ltd., Intron Plus Ltd., TEI Analytical Services, Century Inspection, Inc, Hi-TechNDT Inspection Services (S) Pte Ltd, Sonovation B.V., VOGT Ultrasonics GambH,Techcorr USA, LLC, NDT Services Ltd, NDT Systems & Services AG, Dekra IndustrialAB, NDTS India (P) Ltd., T.D.Williamson, Inc., Cutech Group, Hi-Tech TestingService, Inc, R.Brooks Associates, Inc, International Inspection, Inc., West PennTesting Group, Sievert India Pvt.Ltd, Trinidad Inspection Services Limited, CoastalInspection Services, Inc, Bonded Inspections Inc., RNDT, Inc., Alloyweld InspectionCompany, Inc., Magnachek, Inс., Silverwing (UK) Ltd., ABEN Technical Services,Sinclair X-ray Inspection Services, NDT EXPERT, HMT Inc, IRISNDT, WestechInspection, Inc., James Fisher Inspection and Measurement Services, and SENSEEngineering Services Ltd.

Applus RTD13.4%Acuren

9.8%

Team Industrial Services

5.9%

Mistras Group5.2%

SGS SA4.9%

Others60.8%

49N94C-30

North American NDT Inspection Services Market

49

50N94C-30

Market Engineering Measurements

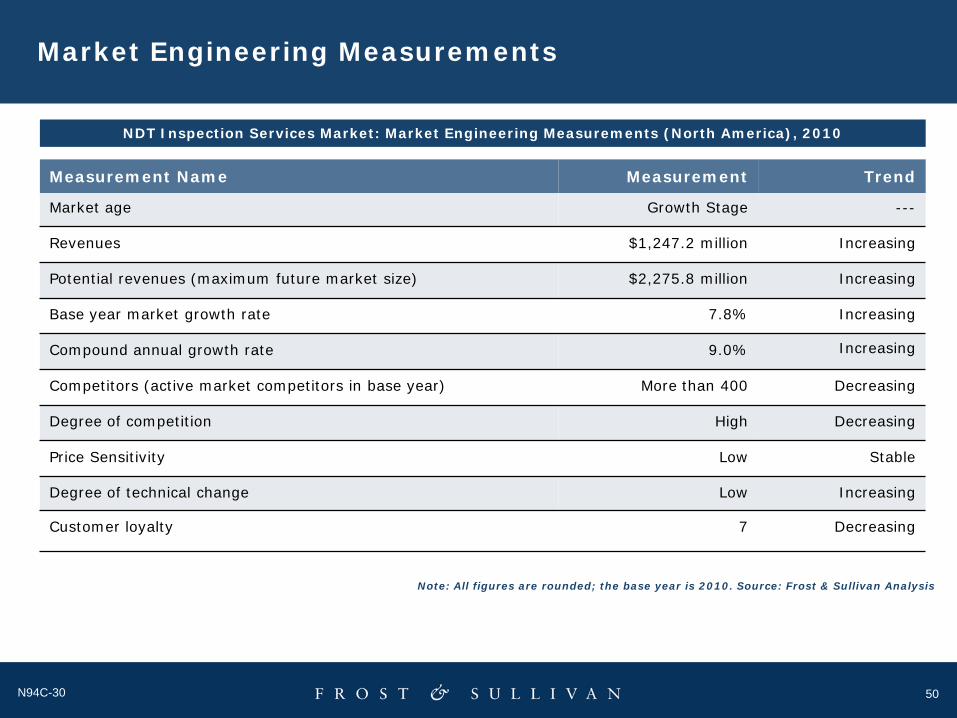

Market age Growth Stage ---

Revenues $1,247.2 million Increasing

Potential revenues (maximum future market size) $2,275.8 million Increasing

Base year market growth rate 7.8% Increasing

Compound annual growth rate 9.0% Increasing

Competitors (active market competitors in base year) More than 400 Decreasing

Degree of competition High Decreasing

Price Sensitivity Low Stable

Degree of technical change Low Increasing

Customer loyalty 7 Decreasing

Measurement Name Measurement Trend

NDT Inspection Services Market: Market Engineering Measurements (North America), 2010

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan Analysis

51N94C-30

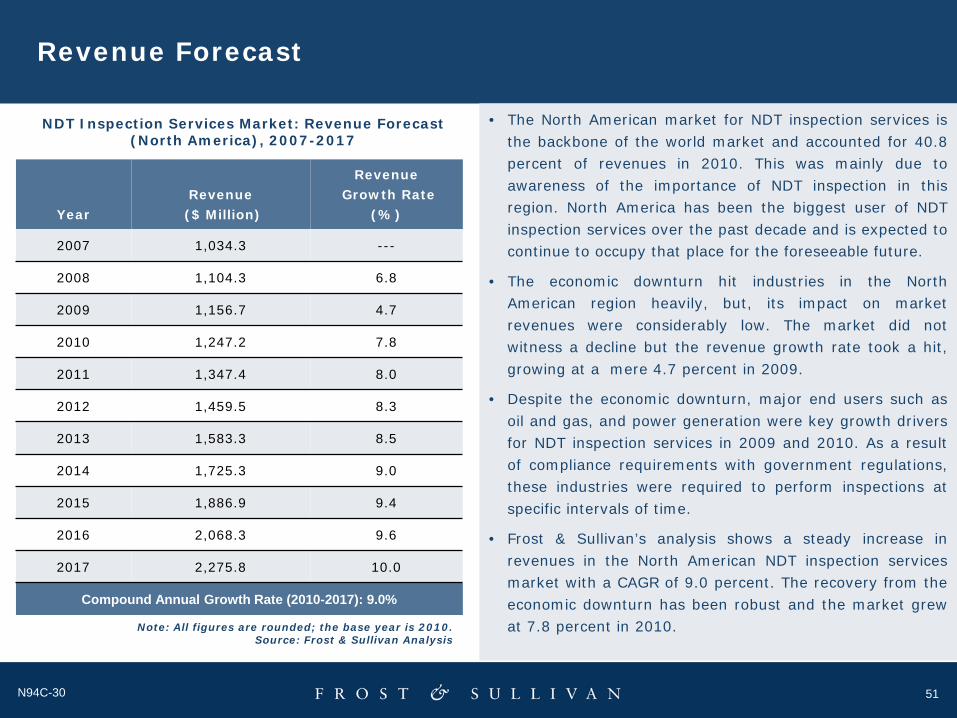

Revenue Forecast

YearRevenue($ Million)

RevenueGrowth Rate

(%)

2007 1,034.3 ---

2008 1,104.3 6.8

2009 1,156.7 4.7

2010 1,247.2 7.8

2011 1,347.4 8.0

2012 1,459.5 8.3

2013 1,583.3 8.5

2014 1,725.3 9.0

2015 1,886.9 9.4

2016 2,068.3 9.6

2017 2,275.8 10.0

Compound Annual Growth Rate (2010-2017): 9.0%

NDT Inspection Services Market: Revenue Forecast (North America), 2007-2017

Note: All figures are rounded; the base year is 2010.Source: Frost & Sullivan Analysis

• The North American market for NDT inspection services isthe backbone of the world market and accounted for 40.8percent of revenues in 2010. This was mainly due toawareness of the importance of NDT inspection in thisregion. North America has been the biggest user of NDTinspection services over the past decade and is expected tocontinue to occupy that place for the foreseeable future.

• The economic downturn hit industries in the NorthAmerican region heavily, but, its impact on marketrevenues were considerably low. The market did notwitness a decline but the revenue growth rate took a hit,growing at a mere 4.7 percent in 2009.

• Despite the economic downturn, major end users such asoil and gas, and power generation were key growth driversfor NDT inspection services in 2009 and 2010. As a resultof compliance requirements with government regulations,these industries were required to perform inspections atspecific intervals of time.

• Frost & Sullivan’s analysis shows a steady increase inrevenues in the North American NDT inspection servicesmarket with a CAGR of 9.0 percent. The recovery from theeconomic downturn has been robust and the market grewat 7.8 percent in 2010.

52N94C-30

Revenue Forecast (Contd…)

NDT Inspection Services Market: Revenue Forecast (North America), 2007-2017

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan Analysis

Although the North American market for NDT inspection services has matured to a large extent, the influx of revenues isexpected to remain high. The market is likely to reach a growth rate of 10.0 percent by 2017, with the oil and gas segmentdriving growth in this region.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

500.0

700.0

900.0

1,100.0

1,300.0

1,500.0

1,700.0

1,900.0

2,100.0

2,300.0

2,500.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Rev

enue

Gro

wth

Rat

e (%

)

Rev

enue

($

Millio

n)

Year

Revenue ($ Million) Revenue Growth Rate (%)

53N94C-30

Trends by End User

YearOil and Gas($ Million)

Power Generation($ Million)

Petrochemical and Chemical

Industries($ Million)

Manufacturing and Process Industries

($ Million)Others

($ Million)

2007 582.3 130.3 129.3 104.5 87.9

2008 622.8 141.4 138.0 109.3 92.8

2009 652.4 150.4 143.4 113.4 97.1

2010 695.9 164.6 154.7 126.0 106.0

2011 751.8 181.9 165.7 134.7 113.3

2012 812.9 201.4 179.5 143.0 122.7

2013 878.7 226.4 193.2 152.0 133.0

2014 954.1 257.1 208.8 163.9 141.4

2015 1,037.8 292.5 226.4 177.4 152.8

2016 1,131.4 333.0 248.2 192.4 163.3

2017 1,240.3 380.1 270.8 209.4 175.2

CAGR (2010-2017)

8.6% 12.7% 8.3% 7.5% 7.4%

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan Analysis

NDT Inspection Services Market: Revenue Forecast by End User (North America), 2007-2017

54N94C-30

Trends by End User (Contd…)

The major end user for NDT inspection services in the North American market is oil and gas, which contributed 55.8 percentto revenues in 2010. One of the main reasons for oil and gas being a key end user is the number of governmentregulations, which stipulate heavy inspection in this segment.

The oil and gas segment is expected to grow at a CAGR of 8.6 percent, which makes it a focal point of revenues. In theUnited States, even though a new refinery has not been constructed for over 30 years, the oil and gas segment is thelargest contributor to revenues. Hence, a significant percentage of revenues in this segment is derived from maintenance-based inspection.

With a CAGR of 12.7 percent, power generation is expected to become a prominent end user for NDT inspection services.The main reason for this is the development being witnessed in the renewable energy sector. A large number of windfarms, and nuclear power plants are being constructed in North America to meet the growing energy demand. This isexpected to contribute significantly to the growth in power generation segment.

The process industry in North America is noteworthy, with pulp and paper being one of the major segments. With a CAGRof 7.5 percent, growth in this segment is likely to be the slowest. A key reason for this is the maturity of the pulp and papermarket in the United States.

55N94C-30

Competitive Environment

NDT Inspection Services Market: Competitive Structure (North America), 2010

Number of Companies in the Market More than 400 competitors

Competitive Factors Quality of service, reputation, execution, price

Key End User GroupsOil and Gas, power generation, chemical/petrochemical industries,and manufacturing and other process industries

Major Market ParticipantsAcuren Group Inc, TEAM Inc, MISTRAS Group Inc, Applus RTD,Russell NDE Systems Inc, T.D.Williamson Inc, Techcorr USA, LLC.

Market Share of Top 3 Competitors 51.3%

Other Notable Market ParticipantsVibrant NDT, R.Brooks Associates, Inc, International Inspection, Inc.,West Penn Testing Group, TUV SUD, TEI Analytical Services, CenturyInspection, Inc

Distribution Structure Direct

Notable Acquisitions and Mergers

TUV SUD acquired Ptrochem Inspection Services (2006), Applus RTDacquired JANX (2008), Stavely Services Canada (2010), QualityInspection Services (2010), Valley Industrial X-Ray & Inspection(2010), Acuren acquired Bretech Inspection (2010), Remote AccessTechnology (2010), Extech (2010)

Source: Frost & Sullivan Analysis

56N94C-30

Competitive Environment (Contd…)

• The North American NDT inspection services market is highly fragmented with more than 400 competitors active in thebase year, 2010. A major reason for such high competition is the low barriers to entry in this market. This challenges thetop market participants to constantly review their growth strategies for maintaining their position in the market.

• Despite the large number of competitors, ACUREN, Team Inc, and MISTRAS Group Inc have emerged as the top threecompetitors occupying 51.3 percent market share by revenues in 2010. Of these three market participants, ACUREN leadsthe way with 24.1 percent market share, followed by Team Inc with 14.4 percent and MISTRAS Group Inc with 12.8 percentmarket share in 2010.

• The economic downturn impacted these companies differently, TEAM Inc recorded a negative growth rate in FY 2010 withlower revenues. However, ACUREN and MISTRAS Group Inc recorded positive growth.

• Market share for the major participants is expected to increase over the short term. MISTRAS Group is expected to growsignificantly with a continued focus on expansion through mergers and acquisitions. Over the last two years, the companyhas acquired more than 10 NDT inspection businesses in a bid to boost revenues and enhance its market position.

• TEAM Inc. endured a torrid time through the economic downturn and is expected to bounce back with improved results inFY 2011. The company is expected to continue growing as it revises growth strategies and targets newer markets.

• Some of the key competitive factors in this market are quality of service, reputation, execution, and price. In the NorthAmerican NDT inspection services market, quality of service is most important and price is the least important factor. Thisis evident from the fact that ACUREN is the top market participant as it differentiates itself by providing highest qualityinspection services.

• TEAM Inc is also recognized as one of the more reputable NDT inspection services company providing high standards forquality and safety.

• Some of the other market participants in this market are Applus RTD, Russell NDE Systems, and TUV SUD – Petrochem,T.D.Williamson, Inc.

57N94C-30

European NDT Inspection Services Market

57

58N94C-30

Market Engineering Measurements

Market age Growth Stage ---

Revenues $954.6 million Increasing

Potential revenues (maximum future market size) $1,637.6 million Increasing

Base year market growth rate 5.1% Increasing

Compound annual growth rate 8.0% Increasing

Competitors (active market competitors in base year) More than 300 Decreasing

Degree of competition High Stable

Price Sensitivity Low Stable

Degree of technical change Low Increasing

Customer loyalty 5 Stable

Measurement Name Measurement Trend

NDT Inspection Services Market: Market Engineering Measurements (Europe), 2010

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan Analysis

59N94C-30

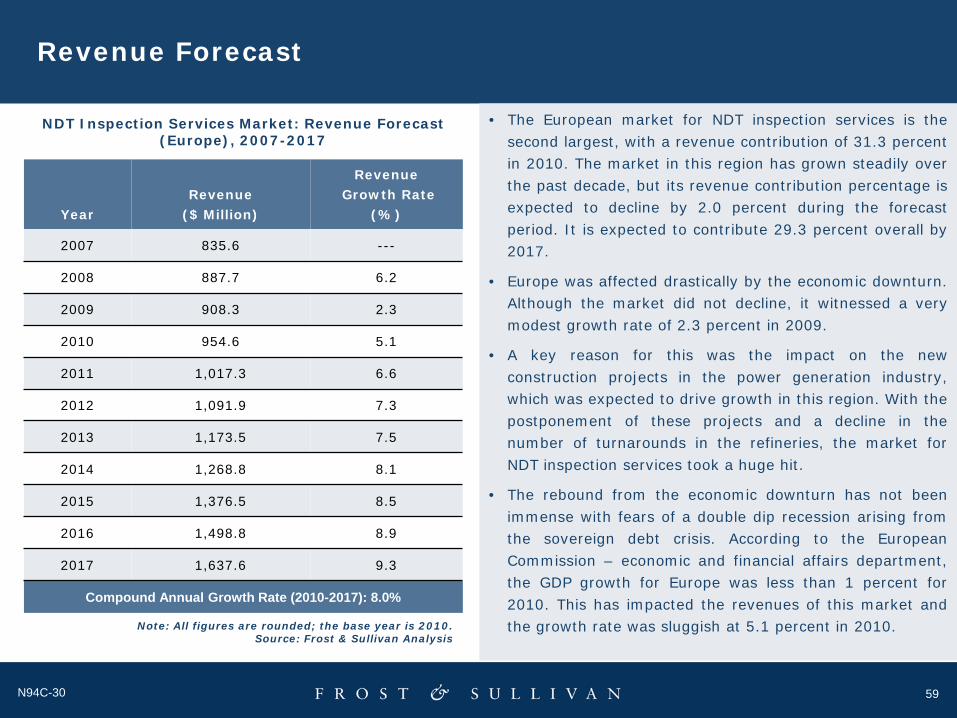

Revenue Forecast

YearRevenue

($ Million)

RevenueGrowth Rate

(%)

2007 835.6 ---

2008 887.7 6.2

2009 908.3 2.3

2010 954.6 5.1

2011 1,017.3 6.6

2012 1,091.9 7.3

2013 1,173.5 7.5

2014 1,268.8 8.1

2015 1,376.5 8.5

2016 1,498.8 8.9

2017 1,637.6 9.3

Compound Annual Growth Rate (2010-2017): 8.0%

NDT Inspection Services Market: Revenue Forecast (Europe), 2007-2017

Note: All figures are rounded; the base year is 2010.Source: Frost & Sullivan Analysis

• The European market for NDT inspection services is thesecond largest, with a revenue contribution of 31.3 percentin 2010. The market in this region has grown steadily overthe past decade, but its revenue contribution percentage isexpected to decline by 2.0 percent during the forecastperiod. It is expected to contribute 29.3 percent overall by2017.

• Europe was affected drastically by the economic downturn.Although the market did not decline, it witnessed a verymodest growth rate of 2.3 percent in 2009.

• A key reason for this was the impact on the newconstruction projects in the power generation industry,which was expected to drive growth in this region. With thepostponement of these projects and a decline in thenumber of turnarounds in the refineries, the market forNDT inspection services took a huge hit.

• The rebound from the economic downturn has not beenimmense with fears of a double dip recession arising fromthe sovereign debt crisis. According to the EuropeanCommission – economic and financial affairs department,the GDP growth for Europe was less than 1 percent for2010. This has impacted the revenues of this market andthe growth rate was sluggish at 5.1 percent in 2010.

60N94C-30

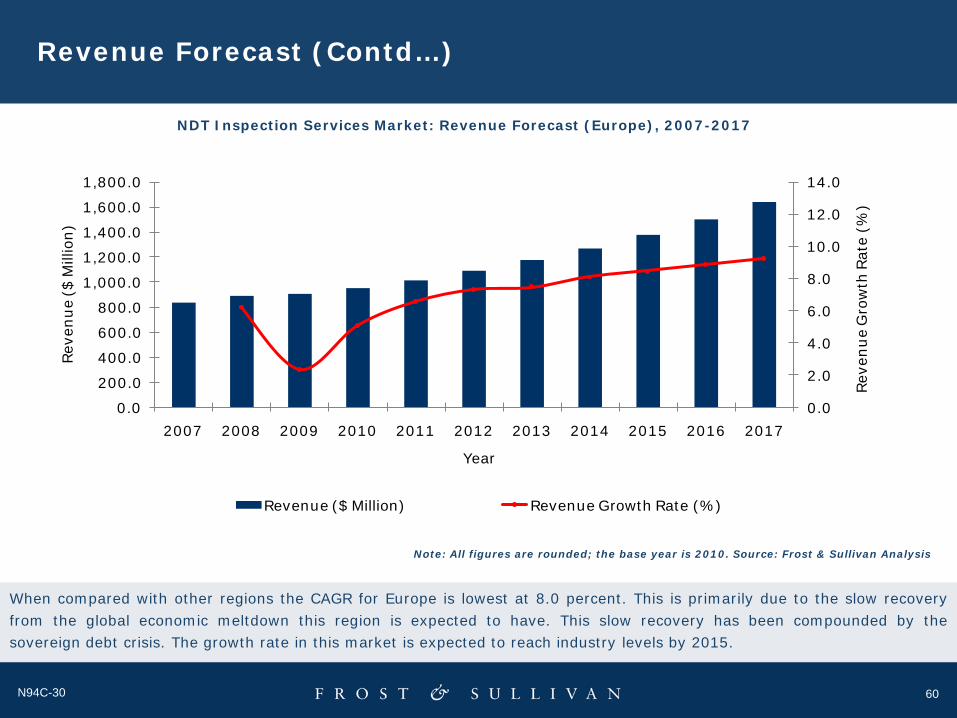

Revenue Forecast (Contd…)

NDT Inspection Services Market: Revenue Forecast (Europe), 2007-2017

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan Analysis

When compared with other regions the CAGR for Europe is lowest at 8.0 percent. This is primarily due to the slow recoveryfrom the global economic meltdown this region is expected to have. This slow recovery has been compounded by thesovereign debt crisis. The growth rate in this market is expected to reach industry levels by 2015.

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

0.0

200.0

400.0

600.0

800.0

1,000.0

1,200.0

1,400.0

1,600.0

1,800.0

2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017

Reve

nue

Gro

wth

Rat

e (%

)

Reve

nue

($ M

illio

n)

Year

Revenue ($ Million) Revenue Growth Rate (%)

61N94C-30

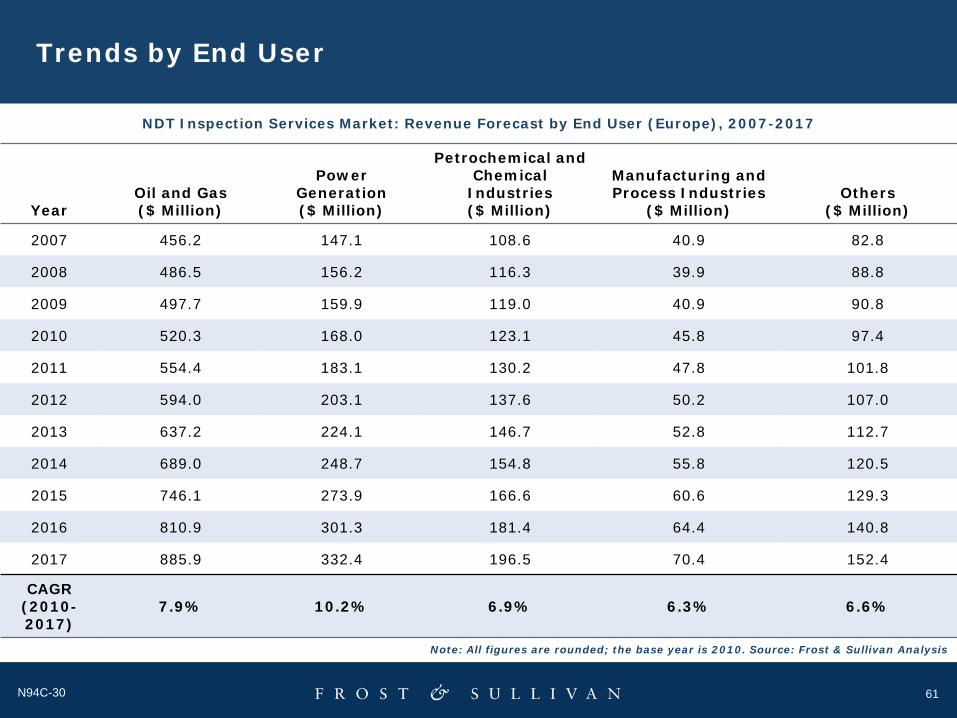

Trends by End User

YearOil and Gas($ Million)

Power Generation($ Million)

Petrochemical and Chemical

Industries($ Million)

Manufacturing and Process Industries

($ Million)Others

($ Million)

2007 456.2 147.1 108.6 40.9 82.8

2008 486.5 156.2 116.3 39.9 88.8

2009 497.7 159.9 119.0 40.9 90.8

2010 520.3 168.0 123.1 45.8 97.4

2011 554.4 183.1 130.2 47.8 101.8

2012 594.0 203.1 137.6 50.2 107.0

2013 637.2 224.1 146.7 52.8 112.7

2014 689.0 248.7 154.8 55.8 120.5

2015 746.1 273.9 166.6 60.6 129.3

2016 810.9 301.3 181.4 64.4 140.8

2017 885.9 332.4 196.5 70.4 152.4

CAGR (2010-2017)

7.9% 10.2% 6.9% 6.3% 6.6%

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan Analysis

NDT Inspection Services Market: Revenue Forecast by End User (Europe), 2007-2017

62N94C-30

Trends by End User (Contd…)

As seen in the North American NDT inspection services market, oil and gas contributed to more than 50 percent of therevenues for 2010 in the European market. It is one of the major sources of revenues for this market because of thenumber of refineries in Eastern Europe. With the number of refineries increasing each year, this end user segment isexpected to remain strong over the forecast period.

The power generation segment is the second-largest user of NDT inspection services with a share of 17.6 percent to theoverall revenues in 2010. With the construction of wind farms, especially in Spain, Germany, and France, the demand forNDT inspection services from this segment is projected to increase. This is shown by the highest CAGR of 10.2 percent,outlining immense growth in this segment.

The manufacturing and process industry segment contributes the least to overall revenues for this region. The percentagerevenue contribution for 2010 is 4.8 percent, and this is expected to decrease further. One of the key reasons for this hasbeen the continuing trend of shifting manufacturing plants to Asia Pacific and Latin America, where the labor is cheap.

With the lowest CAGR of 6.3 percent, this shift has impacted the revenues in this segment and there is no significantchange expected to this trend.

63N94C-30

Competitive Environment

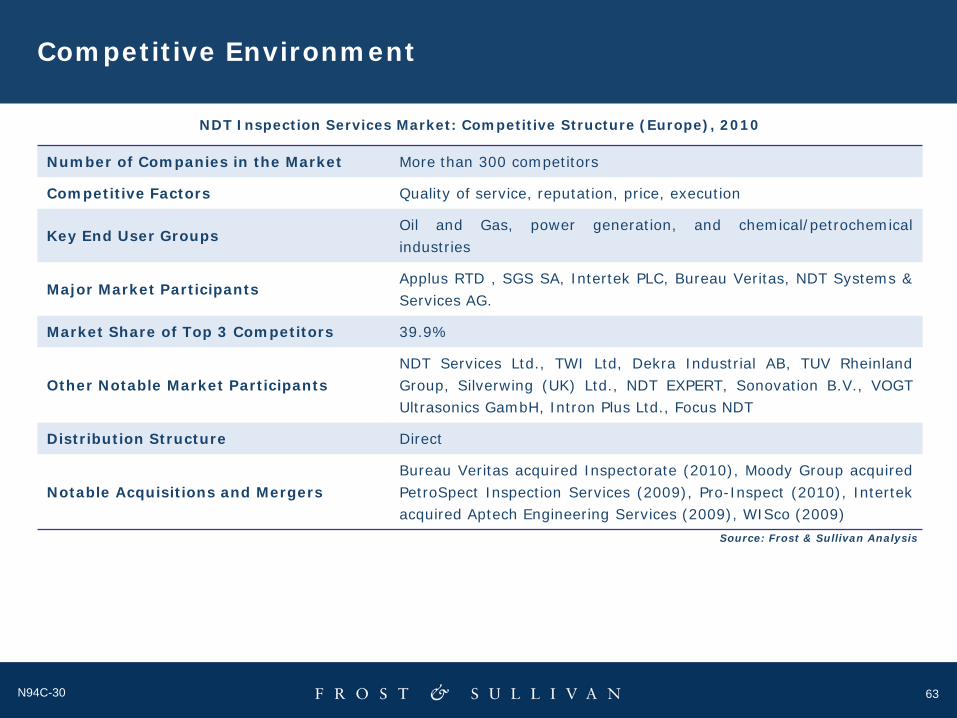

NDT Inspection Services Market: Competitive Structure (Europe), 2010

Number of Companies in the Market More than 300 competitors

Competitive Factors Quality of service, reputation, price, execution

Key End User GroupsOil and Gas, power generation, and chemical/petrochemicalindustries

Major Market ParticipantsApplus RTD , SGS SA, Intertek PLC, Bureau Veritas, NDT Systems &Services AG.

Market Share of Top 3 Competitors 39.9%

Other Notable Market ParticipantsNDT Services Ltd., TWI Ltd, Dekra Industrial AB, TUV RheinlandGroup, Silverwing (UK) Ltd., NDT EXPERT, Sonovation B.V., VOGTUltrasonics GambH, Intron Plus Ltd., Focus NDT

Distribution Structure Direct

Notable Acquisitions and MergersBureau Veritas acquired Inspectorate (2010), Moody Group acquiredPetroSpect Inspection Services (2009), Pro-Inspect (2010), Intertekacquired Aptech Engineering Services (2009), WISco (2009)

Source: Frost & Sullivan Analysis

64N94C-30

Competitive Environment (Contd…)

• The European NDT inspection services market is categorized by high competition with more than 300 active marketparticipants in the base year. As is the nature of the NDT inspection services industry, the barriers to entry are low enablinghigh degree of competition.

• The clear market leader in this region is Applus RTD. In spite of fierce competition, the company occupies 21.5 percent ofthe market in the European region. They have also made a number of key acquisitions in North America to compete withthe top market participants and increase their market presence in in this region.

• SGS SA occupies the second place in this region with a 12.2 percent market share. SGS SA is mainly known for theirtraining and certification in the NDT industry but are growing immensely in the NDT inspection services market throughstrategic mergers and acquisitions.

• Bureau Veritas and Intertek Group PLC are the other major market participants in this region. Intertek has recentlyannounced the acquisition of the inspection division of Moody group in a deal worth $730 million and are expected toexpand significantly in the medium term.

• The impact of the economic downturn on the NDT inspection services market in this region was considerable with many newconstruction projects being put on hold. In a market where majority of the revenues are derived from inspection of theseconstruction projects, profit margins of the NDT inspection service providers suffered immensely. The recovery from thedownturn has been gradual and uneven with the Eastern European countries leading the way.

• This economic uncertainty has led a majority of the market participants to look for growth through other avenues, mainlymergers and acquisitions. In the past year alone, SGS SA has completed 13 acquisitions with a majority of them being inthe NDT inspection services industry. Another company trying to expand significantly through mergers and acquisitions isIntertek Group PLC with 9 acquisitions in the NDT inspection services market.

• Some of the other significant market participants in the European NDT inspection services market are NDT Services Ltd,NDT Systems & Services AG, TWI Ltd, Dekra Industrial AB, and TUV Rheinland Group.

65N94C-30

Asia Pacific NDT Inspection Services Market

65

66N94C-30

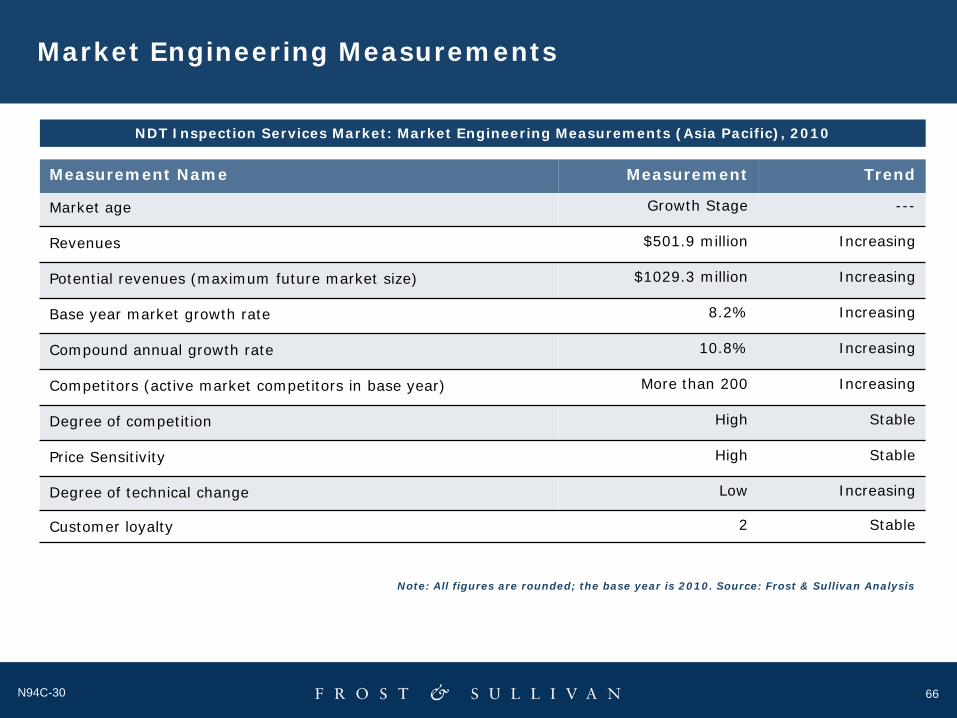

Market Engineering Measurements

Market age Growth Stage ---

Revenues $501.9 million Increasing

Potential revenues (maximum future market size) $1029.3 million Increasing

Base year market growth rate 8.2% Increasing

Compound annual growth rate 10.8% Increasing

Competitors (active market competitors in base year) More than 200 Increasing

Degree of competition High Stable

Price Sensitivity High Stable

Degree of technical change Low Increasing

Customer loyalty 2 Stable

Measurement Name Measurement Trend

NDT Inspection Services Market: Market Engineering Measurements (Asia Pacific), 2010

Note: All figures are rounded; the base year is 2010. Source: Frost & Sullivan Analysis

67N94C-30

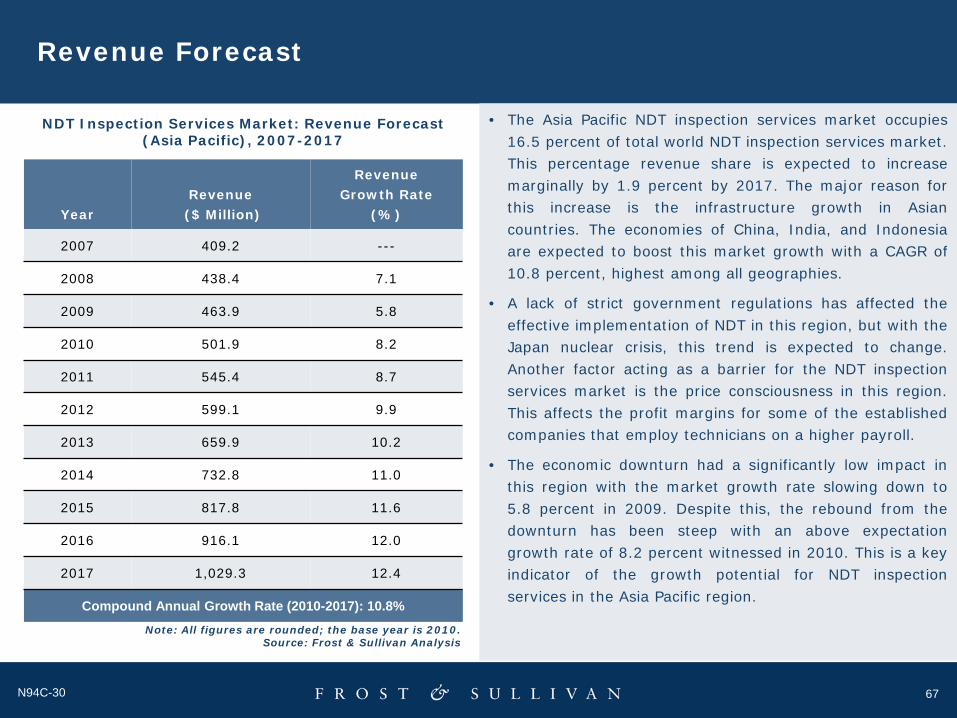

Revenue Forecast

YearRevenue($ Million)

Revenue Growth Rate

(%)

2007 409.2 ---

2008 438.4 7.1

2009 463.9 5.8

2010 501.9 8.2

2011 545.4 8.7

2012 599.1 9.9

2013 659.9 10.2

2014 732.8 11.0

2015 817.8 11.6

2016 916.1 12.0

2017 1,029.3 12.4

Compound Annual Growth Rate (2010-2017): 10.8%

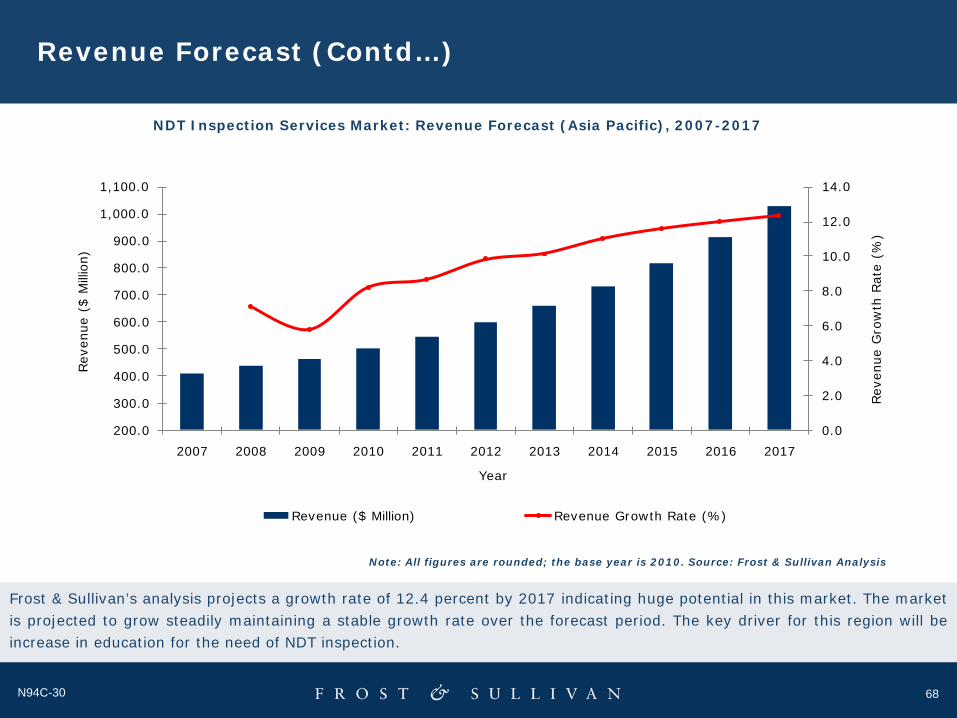

NDT Inspection Services Market: Revenue Forecast (Asia Pacific), 2007-2017

Note: All figures are rounded; the base year is 2010.Source: Frost & Sullivan Analysis

• The Asia Pacific NDT inspection services market occupies16.5 percent of total world NDT inspection services market.This percentage revenue share is expected to increasemarginally by 1.9 percent by 2017. The major reason forthis increase is the infrastructure growth in Asiancountries. The economies of China, India, and Indonesiaare expected to boost this market growth with a CAGR of10.8 percent, highest among all geographies.

• A lack of strict government regulations has affected theeffective implementation of NDT in this region, but with theJapan nuclear crisis, this trend is expected to change.Another factor acting as a barrier for the NDT inspectionservices market is the price consciousness in this region.This affects the profit margins for some of the establishedcompanies that employ technicians on a higher payroll.