WORLD MONEY ANALYST - Mauldin · PDF filestraight from the “envy politics”...

33

• Southeast Asia A major telecom company with solid cash flow and a nice dividend ...............................................Page 10 IN THIS ISSUE: Dear reader, C alifornia is back in the news, announcing that the state’s budget deficit has grown to a $16 billion steaming caldera. Exactly when the tax heavy/spend big/borrow bigger budget shenanigans fail is anyone’s guess. But while we wait, the announced remedy is straight from the “envy politics” playbook: tax the rich. Maybe it’s just me, but I’m starting to see a greater than usual number of articles covering the rise in the number of Americans leaving the country. This seems in line with the numbers released by the US Treasury that show those renouncing their US citizenship is growing. Just for kicks, I plotted the number of US renunciations since 1998 against the gold price. Except for the “everybody feels good about America” bubble that burst in 2008, the slope of both lines is rather similar. If one believes that gold is a crisis barometer, this makes sense. As the fiscal crises in the US persist, the higher taxes are likely to climb, adding more incentive for the wealth creators to leave… and take their wealth with them. The IRS seems to be losing one taxpayer for every dollar rise in the gold price. Kevin Brekke WORLD MONEY ANALYST INTERNATIONALIZE YOUR MONEY. YOUR LIFE. A MAULDIN ECONOMICS PUBLICATION ISSUE 4 • May 2012 International Overview Political pandering to anti-austerity backlash threatens the euro union ............................................... Page 3 • • A cyclical play in a little known segment of the agriculture sector ................................................Page 7 Scandinavia • Currency Watch A look at interest rate differentials of select global currencies ........ Page 14 • Cattle and groceries: two high-yield corporate bond opportunities ............................................. Page 20 Latin America • Russia Growing credit card demand points to attractive returns. ............. Page 17 • Commodities A unique option strategy to squeeze “yield” out of gold and silver bullion ............................................. Page 23 • International Investors Toolkit Update on reporting requirements for US tax filers .................... Page 27

Transcript of WORLD MONEY ANALYST - Mauldin · PDF filestraight from the “envy politics”...

• Southeast AsiaA major telecom company with solid cash flow and a nice dividend ...............................................Page 10

IN THIS ISSUE:Dear reader,

California is back in the news, announcing that the state’s budget deficit has grown to a $16 billion steaming caldera. Exactly

when the tax heavy/spend big/borrow bigger budget shenanigans fail is anyone’s guess. But while we wait, the announced remedy is

straight from the “envy politics” playbook: tax the rich.

Maybe it’s just me, but I’m starting to see a greater than usual number of articles covering the rise in the number of Americans leaving the country. This seems in line with the numbers released by the US Treasury that show those renouncing their US citizenship is growing.

Just for kicks, I plotted the number of US renunciations since 1998 against the gold price. Except for the “everybody feels good about America” bubble that burst in 2008, the slope of both lines is rather similar. If one believes that gold is a crisis barometer, this makes sense. As the fiscal crises in the US persist, the higher taxes are likely to climb, adding more incentive for the wealth creators to leave… and take their wealth with them. The IRS seems to be losing one taxpayer for every dollar rise in the gold price.

Kevin Brekke

WORLD MONEY ANALYSTINTERNATIONALIZE YOUR MONEY. YOUR LIFE.

A MAULDIN ECONOMICS PUBLICATION ISSUE 4 • May 2012

International Overview

Political pandering to anti-austerity backlash threatens the euro union ............................................... Page 3

•

•A cyclical play in a little known segment of the agriculture sector ................................................Page 7

Scandinavia

• Currency WatchA look at interest rate differentials of select global currencies ........Page 14

•Cattle and groceries: two high-yield corporate bond opportunities .............................................Page 20

Latin America

• Russia

Growing credit card demand points to attractive returns. .............Page 17

• Commodities

A unique option strategy to squeeze “yield” out of gold and silver bullion .............................................Page 23

• International Investors Toolkit

Update on reporting requirements for US tax filers ....................Page 27

WORLD MONEY ANALYST ISSUE 4 • May 20122

Keeping our promise: new analysts join WMAOf course, sending assets beyond one’s national border doesn’t require such a drastic step

as renouncing citizenship. A foreign brokerage and bank account is all that is required to get started. Then it’s a matter of finding great opportunities in which to invest. And that, of course, is what World Money Analyst is all about.

To assist in that endeavour, I am very pleased to introduce two new analysts that have joined the team here at WMA: Dirk Steinhoff and Ankur Shah.

Dirk Steinhoff is Managing Director, Portfolio Management, at the BFI Capital Group, Zurich. Dirk brings over 15 years of asset management experience to bear on his investment analysis. At the top of this month’s issue, he takes a look at a Norwegian company operating in aquaculture, an agriculture niche that few investors are aware of. Dirk brings added insight to our coverage of Europe, Eastern Europe, and Scandinavia, and we are excited to have him on board.

Ankur Shah has many years experience as an analyst in global equity, covering emerging markets, with a focus on southeast Asia, and is a graduate of Harvard Business School. Coming up, he applies his value-investing methodology to take a look at a Singapore telecom company selling at a discount with a 5% dividend yield. Ankur joins WMA as our Singapore and SE Asia analyst, and we are very glad he did.

Good yield huntingThis month, I tasked our analysts to uncover great opportunities in the equity and bond

arenas that also offer the investor higher yields. The demographics in the developed world are becoming ever heavier with seniors, and this segment of investors is looking to allocate more of their wealth into investments with a decent yield.

To that end, Claudio Maulhardt shows us two Central American corporate bonds paying double-digit yields; Alexei Medved takes a look at a Russian “What’s in your wallet?” company that offers a great yield; Chuck Butler spins the globe and singles out some of the best higher-yield currencies; and Steve Belmont shows us how to wring some yield out of those barbarous precious metals.

So to get started, I will hand the baton to Grant Williams, our globe-trotting global macro guy, who just returned to Singapore after rubbing elbows with some of the brightest investment minds at a conference in California. Dedicated analyst that he is, Grant found the time on his 15-hour flight home to pen his thoughts on what’s happening in that perennial political hot bed, Europe.

I think this month’s issue is loaded with actionable investment research, and I hope you agree.

Thank you for subscribing to the World Money Analyst!

Kevin Brekke

Managing Editor

Fribourg, Switzerland

WORLD MONEY ANALYST ISSUE 4 • May 20123

I recently attended a conference in Carlsbad, CA, where some of the very brightest minds in the investment business shared their insight with those of us lucky enough to attend. I don’t think I'd be speaking out of turn to share with you that one of the common themes was the future

of Europe and whether the European Union in general, and the euro specifically, could be held together in the coming months.

The consensus seemed to be that they would successfully manage to keep this multi-faceted political construct together. But to achieve that noble aim, Germany would have to concede the fact that they would have to pay their share of the costs of doing so - costs which would reach many tens of billions of euros.

That last paragraph contains three words that hold the key to the fate of both the euro and the European Union: "they," "Germany" and "they."

Whenever the future of the Eurozone and/or the euro is discussed, it takes place against a backdrop of "they," meaning the government of the respective nation whose current foibles represent the crisis du jour, or the governments of the other members of the Eurozone who are attempting to impose conditions around bailouts.

Reminder: a country is the sum of its votersWhen commentators talk about "Germany doing the right thing," or "Greece refusing to agree

to terms imposed upon them by the Troika," or "Spain making draconian cuts in public spending," what they are actually talking about is a small group of officials in government who represent the real "Greece," the real "Germany," and the real "Spain" (to name but three). Of course, the reality of all those countries is the citizens who vote for their elected officials, and, more importantly right now, vote them out.

The last six months have seen the fall of governments in Spain, Greece and France as a backlash against imposed austerity begins to creep across Europe. As we approach Southern Europe's hottest months, the situation is ripe for a summer of discontent that could lead to a seismic change in the political landscape before we usher in 2013.

Spain’s soaring unemployment levels have been the recent focus of hundreds of column inches, and with good reason; 24% headline unemployment allied with a 50% rate amongst 16-24 year-olds is a toxic mix that could explode at any moment. The first move that Spain’s newly-elected Prime Minister, Mariano Rajoy, made after displacing the previous administration was to inform the EU that Spain would be unable to meet the budget deficit targets imposed upon them by the Fiscal Compact, and that Spain would unilaterally lower their own target. The new "they" had markedly different ideas than the old "them."

EU Election Trends Confound Efforts to Sustain UnionBy Grant Williams

International Overview

WORLD MONEY ANALYST ISSUE 4 • May 20124

As March gave way to April, all eyes turned to France and the Presidential elections that would determine the political fate of one half of the Franco-German “Merkozy” alliance that had been at the core of all attempts to instill a sense of fiscal discipline amongst Europe’s prodigal peripheral countries.

The first round of the French elections was eye-opening in the extreme, for both its citizens and the world-at-large, as the far-right National Front party of Marine Le Pen captured almost 1 in 5 votes, sending a shiver up the spines of Sarkozy’s more centrist-right supporters.

Despite his attempts to win over Le Pen’s bloc in the run-off with the socialist candidate, Francois Hollande, Sarkozy lost fairly handily - making his the first one-term presidency since the 1980s.

And what was Hollande’s first initiative as President? Fulfilling his primary campaign plank by renegotiating the fiscal compact at the heart of Europe; the same fiscal compact Rajoy openly defied but that Angela Merkel had declared “non-negotiable,” adding for good measure that it would “last forever.”

And then there’s GreeceLike an indestructible demon that continues to rise up and terrorize the EU, Greece has once

again put itself back in the frame as a likely reason why the Eurozone may yet confound many, and disintegrate - perhaps within the year.

Source: Mike Shedlock

WORLD MONEY ANALYST ISSUE 4 • May 20125

The recent chaos following inconclusive elections in Greece is testament to the fact that finding a coherent government that will toe the line and carry out the measures demanded of it by the core European countries is going to be no easy task.

The timeline of upcoming events in Greece (Table, below) shows just how difficult killing the Greek beast will be.

After the May 6 elections, several parties have made desperate attempts to form a coalition government, but as I write, none have been successful.

The most telling part of this post-election process has been the enormous surge in popularity of the left-wing Syriza Party as it continues to vehemently oppose the fiscal compact and the conditional austerity of the bailouts.

A rather bizarre Greek election rule gives the winning party (assuming they can form a government) 50 “bonus seats” in parliament (you really can’t make this stuff up).

So, with Syriza’s post-election, anti-Europe rhetoric sending their share of the vote soaring to 27.7% (making them the largest party by quite a distance), the dynamics of a second election on June 6 could be markedly different.

2012 Event

May 10 PASOK Venizelos attempts to form coalition government

May 11 Greek T-bill redemption for €1.6 billion

May 14 Eurogroup meeting

May 15 EcoFin meeting

May 15 Greek T-Bill auction

May 15 Greek Q1 Provisional GDP Data

May 15 Greek foreign law bond redemption for €435.9 million

May 16 Greek President appoints caretaker government if coalition not formed

May 18 Greek bond redemption for 5.25% May 2012 GGB for €3.334 billion

May 18 Greek T-bill redemption for €1.6 billion

May 25 EU Head of State Summit on growth compact

June 6 ECB Governing Council meeting, Draghi to give staff forecasts

June 10 Earliest date for Greek elections if parties fail to form government

June 15 Greek T-bill redemption for €2.0 billion

June 25 Greek foreign law bond redemption for €1.172 billion

Source: BTIG

WORLD MONEY ANALYST ISSUE 4 • May 20126

The latest polls show Syriza with 128 seats (up from 52 in the last vote) and its nearest rivals, New Democracy, with a mere 57 (down from 108) giving Alexis Tsipras’ left-wing party an extremely strong hand.

Economic ills encourage pandering politiciansIt hardly helps the situation when, in the middle of trying to form a government, the Hellenic

Statistical Authority reports that unemployment has risen again, to 21.3%, youth unemployment has reached 53.8%, and industrial output has slumped by 8.5% y-o-y.

In Europe, campaigning against the fiscal compact and ever-increasing austerity is a vote-winning strategy that politicians were quick to figure out.

Given the choice between cuts in public sector compensation levels, rising retirement ages, and reduced state services, or freshly-printed money that papers over the cracks for just a little longer, it’s no surprise that the vox populi - conditioned as they have been by their elected officials to believe that printing money can solve all the economic problems facing them - are far more inclined to vote “growth,” even if that growth will be largely in their money supply and their national debt levels.

This is a trend you can bet will continue in the coming months.

It is getting harder by the day to somehow find a way to hold the euro together. I find it extremely difficult to see ultimately how countries like Greece, Portugal and Spain can possibly stay a part of the project once each of them crosses their own individual threshold.

But if you want the real answer to a question, there is only one truly reliable source to consult: a bookie.

In the UK this week, Ladbrokes has stopped taking bets on a Greek exit from the euro after seeing a flood of money pouring in over the past several days.

“They” face an almighty struggle. •

Grant Williams is portfolio manager and strategist for the Testudo Fund in Singapore, part of the Vulpes Investment Management group of funds. He has 26 years of experience in finance on the Asian, Australian, European and US markets, including senior positions at several international investment houses. Vulpes is a multi-strategy hedge fund with $200 million AUM. www.vulpesinvest.com. Grant also writes the popular investment blog Things That Make You Go Hmmm..... which is open to subscribers.

WORLD MONEY ANALYST ISSUE 4 • May 20127

Historically, investments in the agriculture arena have largely been the domain of a few professional investors and futures traders. But this has slowly started to change over the past few years, particularly with the current secular bull market in commodities. Interest

in agriculture has not only spread to a broader investment community, but today you also see all facets of agriculture well represented in the political, economic and investment media.

However, whereas many investors tend to be familiar with corn, wheat, sugar and pork bellies, and possibly read investment recommendations about farm land, there is one sector rarely in the news: Aquaculture. Aquaculture, also known as aqua-farming, is defined as the farming of aquatic organisms including fish, mollusks, crustaceans and aquatic plants.

For centuries, humanity’s need for fish was supplied by capture fisheries, where aquatic life is not controlled and thus the fish must be “captured” or fished. Of course, the resources seemed unlimited. The global spread of modern commercial fishing since the 1970’s – through a combination of technological advances in sonar and satellites, nets that can stretch for miles, and some increasingly reckless fishing practices — has substantially cut the population of edible fish. The depletion of ocean capture fisheries continues at an alarming pace. To a certain degree, you can compare the depletion in seafood with developments in the energy sector. Countries formerly self-sufficient and exporters of fish are now becoming net importers.

Figure 1: World capture fishing production has been flat for years

A Little Known Agricultural NicheEurope & Scandinavia

By Dirk Steinhoff

WORLD MONEY ANALYST ISSUE 4 • May 20128

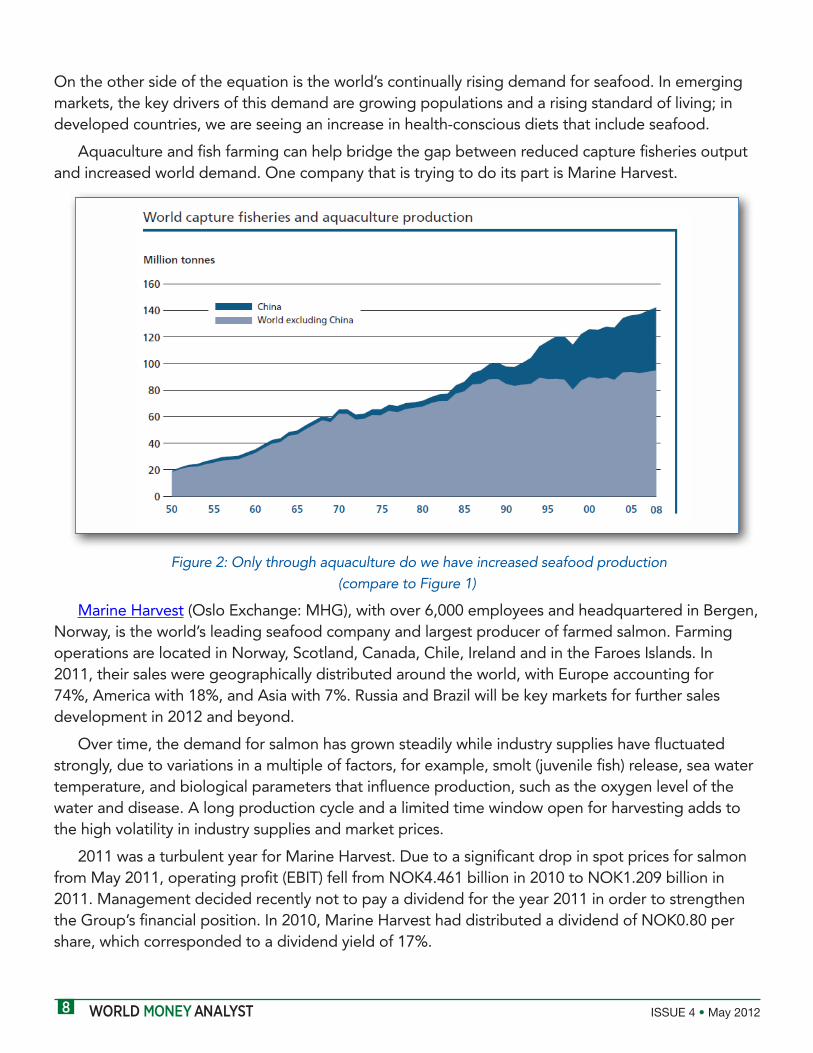

On the other side of the equation is the world’s continually rising demand for seafood. In emerging markets, the key drivers of this demand are growing populations and a rising standard of living; in developed countries, we are seeing an increase in health-conscious diets that include seafood.

Aquaculture and fish farming can help bridge the gap between reduced capture fisheries output and increased world demand. One company that is trying to do its part is Marine Harvest.

Figure 2: Only through aquaculture do we have increased seafood production (compare to Figure 1)

Marine Harvest (Oslo Exchange: MHG), with over 6,000 employees and headquartered in Bergen, Norway, is the world’s leading seafood company and largest producer of farmed salmon. Farming operations are located in Norway, Scotland, Canada, Chile, Ireland and in the Faroes Islands. In 2011, their sales were geographically distributed around the world, with Europe accounting for 74%, America with 18%, and Asia with 7%. Russia and Brazil will be key markets for further sales development in 2012 and beyond.

Over time, the demand for salmon has grown steadily while industry supplies have fluctuated strongly, due to variations in a multiple of factors, for example, smolt (juvenile fish) release, sea water temperature, and biological parameters that influence production, such as the oxygen level of the water and disease. A long production cycle and a limited time window open for harvesting adds to the high volatility in industry supplies and market prices.

2011 was a turbulent year for Marine Harvest. Due to a significant drop in spot prices for salmon from May 2011, operating profit (EBIT) fell from NOK4.461 billion in 2010 to NOK1.209 billion in 2011. Management decided recently not to pay a dividend for the year 2011 in order to strengthen the Group’s financial position. In 2010, Marine Harvest had distributed a dividend of NOK0.80 per share, which corresponded to a dividend yield of 17%.

WORLD MONEY ANALYST ISSUE 4 • May 20129

Figure 3: Marine Harvest share performance

As salmon prices have traditionally been subject to large price fluctuations, the current price decline should be viewed as a cyclical event rather than a permanent change. Marine Harvest management seems to have undertaken all the necessary steps necessary to navigate the company through this cyclical downturn. Any price recovery in salmon will have a substantial impact on profitability and cash flows.

In our view, the long-term outlook for Marine Harvest is positive. It has taken measures to protect its cash flow and the financial strength of the company in current volatile times by the implementation of a global cost reduction program and other significant changes. And its globally diversified production and sales is supported by growing worldwide demand for salmon that should continue into the future.

In our opinion, at the current share price of approx. NOK2.90 (≈USD0.50) Marine Harvest is undervalued and represents a good buying opportunity for the long-term investor. In the short- to mid-term (12 to 18 months) we expect a continued consolidation. Once this consolidation phase is complete, Marine Harvest should be strengthened and we expect the share price to recover as well. Further, we expect that the company will resume its dividend-paying policy. In this case, the investor should not only be rewarded for investing in a turnaround situation by receiving a nice dividend, but the dividend will be paid in NOK, one of the world’s strongest currencies. (See April issue of WMA for a review of the Norwegian krone.) •

[Ed. Note: buying Marine Harvest on its home exchange is recommended. If access to the Oslo market is not an option, the security is cross-listed on the Frankfurt Exchange (symbol: PND) and the Stockholm Exchange (symbol: MHGO).]

Dirk Steinhoff is Managing Director, Portfolio Management (US clients), at the BFI Capital Group, Zurich. Prior to joining BFI in 2007, Mr Steinhoff had acted as an independent asset manager for over 15 years. He successfully founded and built two companies in the realm of infrastructure and real estate management. Mr Steinhoff is German by background. He holds a Bachelor´s and Master´s degree in Civil Engineering and Business Administration, magna cum laude, from the University of Technology in Berlin, Germany. Contact: [email protected].

WORLD MONEY ANALYST ISSUE 4 • May 201210

Why You Should be Investing in SingaporeBy Ankur Shah

Singapore & Southeast Asia

As Facebook kicks off its official IPO road show, one of its original co-founders will be conspicuously absent. If you saw the movie “The Social Network,” you know that Eduardo Saverin provided the initial seed capital to start Facebook. Although his stake has been

diluted from 34% to only 2%, the company currently has a pre-IPO valuation of $96 billion. Now that he’s a billionaire, Eduardo is currently living it up in Singapore and is better known for his nocturnal club going adventures than his business ventures.

Less known is that, as an undergraduate, he had made $300,000 via strategic investments in Brazil’s oil and gas industry and was president of the Harvard Investment Association. Despite his recent burst of “Kardashian”-like publicity, he undoubtedly has a knack for identifying trends and investment themes early. Interestingly, he relocated to Singapore in 2009. Why would a Brazilian-born tech entrepreneur with strong ties to Latin America and the US choose to live in Singapore, when he could’ve chosen any major city in the world?

Elections in France and Greece doom austerity in EuropeBefore I get to the answer, I must discuss the recent French elections where François Hollande

was elected president. Hollande achieved victory on an anti-austerity platform, making it clear that the French electorate rejects the deflationary impact of reduced deficit spending. Europe has entered the next stage of its crisis. With a large swath of Europe in recession and a slowing US economy based on weak job growth, the likelihood of further doses of monetary stimulus by both the ECB and FED has materially risen.

WORLD MONEY ANALYST ISSUE 4 • May 201211

The election in Greece sent a similar anti-austerity message. The outcome is that the ECB will be increasingly pressured to monetize government debt. More uncertainty, volatility, and further deterioration in government finances across the developed world lie ahead. Thus, investors should be thinking about capital preservation and reducing risk as market sentiment continues to turn negative. Traditionally, that meant seeking the safety of government debt.

However, as David Rosenberg of Gluskin Sheff has pointed out, “since the time the Great Recession took hold in 2008, we have seen the total value of government debt backed with AAA-ratings decline from over a 50% share of total outstanding sovereign credit to less than 10%.” With US 10-year treasury yields at historic lows under 2%, the tail end of the bull market in US treasuries that began in 1982 is at hand.

Given the current US fiscal outlook and Federal Reserve balance sheet debauchment, US treasuries represent perhaps one of the worst investments imaginable. Yet, short-term yields can still head lower as the US economy weakens – we are clearly closer to the “great reset” on US yields than many investors and foreign central bankers currently believe…

Investors fleeing developed markets will find a home in SingaporeInvestors seeking safe harbor from the brewing storm in developed markets should move

capital to countries with small government debt, current account surpluses and a well-capitalized banking sector. Which brings us back to Eduardo Saverin, who has a knack for being at the right place at the right time and chose to relocate to Singapore – a country that meets all three of my criteria. And Singapore is currently rated AAA by all three ratings agencies, an increasingly rare feat.

As western governments pursue larger budget deficits combined with quantitative easing, exposure to the Singapore dollar should provide positive real returns for developed market investors. As a contributor to the World Money Analyst, my goal will be to identify attractive investment opportunities in South East Asia – and Singapore in particular – that provide limited downside risk and significant upside potential based on a value investing framework.

WORLD MONEY ANALYST ISSUE 4 • May 201212

The art of valuation and the one Singapore stock you should ownGiven my investing criteria, I believe that Singapore Telecommunications (SingTel; Singapore

Exchange: Z74) is an attractive candidate given its free cash flow generation, stable revenue model, and reasonable upside potential at current price levels. SingTel is the largest fixed-line and mobile communications provider in Singapore.

The company’s primary markets are Singapore and Australia, where the company operates through its wholly-owned subsidiary SingTel Optus.

SingTel also has a presence across Asia and Africa with more than 434 million mobile subscribers in 25 countries including Bangladesh, India, Indonesia, Pakistan, the Philippines and Thailand through equity stakes in the following mobile communications companies:

• 32.3% stake in Bharti Airtel (India)

• 35% stake in Telkomsel (Indonesia)

• 23.3% stake in AIS (Thailand)

• 47.3% stake in Globe (Philippines)

• 30% stake in Warid (Pakistan)

• 45% stake in PBTL (Bangladesh)

The basic intent of any valuation exercise is to determine how much a security is worth. A stock is the sum of its discounted cash flows plus shareholders’ equity. Shareholders’ equity essentially measures the current value of the firm if it were to shut down today. By paying off total liabilities with total assets, it represents the value left over for equity shareholders.

Give yourself a safety marginAfter we’ve calculated the intrinsic value of a security, the next step is to determine an

adequate margin of safety, something that will vary for each investor. For SingTel, I use a 25% margin of safety due to its consistent cash flows. For a more speculative investment such as Facebook, I would likely use a margin closer to 40%.

We apply a safety margin to account for the large potential for errors when using forecasts. We know that a twenty-year cash flow projection will not be exact and the margin of safety compensates for the inherent uncertainty in our intrinsic value calculation.

By analyzing a company’s past cash flows, we have a reasonable base upon which to build our forecast. It’s likely that a company producing solid cash flow growth over the past 10 years will continue to do so in the future, regardless of the macroeconomic environment.

Based on a Discounted Cash Flow (DCF) analysis, I calculate the intrinsic value for SingTel at S$4.00. Using a 25% margin of safety, we get a target entry price of S$3.00. With the stock currently trading near our entry target price (S$3.25 on 5/11/12), we believe the shares provide adequate upside potential with limited downside risk.

WORLD MONEY ANALYST ISSUE 4 • May 201213

Dividend yield plus currency diversificationThe company reported respectable FY12 (year ending March 31, 2012) results, with 4Q12

net income of S$1.29 billion, up 30% y-o-y (including an exceptional net tax credit of S$270 million). Free cash flow for FY12 declined to S$3.46 billion, a 14% y-o-y decrease. The decline on a y-o-y basis, however, was due primarily to a special dividend paid by its Advanced Info Service subsidiary in FY11, which was not repeated in FY12.

SingTel maintained its 15.8 Singapore-cents per share dividend, equaling a 68% payout ratio. In addition to generating significant positive free cash flow, the shares offer an attractive 5% dividend yield.

The real dividend yield for investors from developed markets could be higher, assuming a devaluation of your domestic currency relative to the Singapore dollar. Additionally, management provided a stable outlook for FY13, with revenue growth expected in the low single digits and a stable EBITDA. Singapore Telecommunications represents a defensive investment opportunity with a reasonable margin of safety, combined with an attractive dividend yield.

Overall, our investing philosophy requires a strict adherence to a value investing methodology. If we are correct about our negative market outlook for the developed world, emerging markets in Asia will not be spared. However, we are confident that a correction in emerging market equities will also bring opportunities for value-oriented investors who are ready to take positions in high quality, strong cash flow companies located in jurisdictions with positive demographics, underleveraged consumers, and strong banking systems. •

Ankur Shah is the founder of the Value Investing India Report, a leading independent, value oriented journal of the Indian financial markets. Ankur has more than eight years of equity research experience covering emerging markets, with a focus on South East Asia. He has worked as both a buy-side investment analyst for a global long/short equity hedge fund and a sell-side analyst for an emerging markets investment bank. Ankur is a graduate of Harvard Business School. You can learn more about his latest views on global markets and sign-up for his subscription service at http://www.valueinvestingindiareport.com/subscribe-3/.

WORLD MONEY ANALYST ISSUE 4 • May 201214

A year ago, the challenge of this month’s “finding yield” theme would have been pretty easy, as interest rates in some of the commodity currency countries enjoyed some very wide rate differentials to the major currencies of the world.

But all that changed as we headed into the last quarter of 2011. The “blame finger” gets pointed at the Eurozone’s debt debacle. But in reality, the U.S. economy has also slowed down, enough to have people like PIMCO’s Bill Gross state that he believes QE3 will be implemented soon.

So as the two major contributors to global GDP – the Eurozone and the U.S. – deal with economic slowdowns, global growth is taking a beating. That means commodity currency countries like Australia, Norway, and Canada had to reverse course on previously raised interest rates.

That, unfortunately, doesn’t leave me with much to talk about…

However, when you deal with currencies from around the world, there’s always a bull market somewhere! And where there’s a bull market in currencies, there’s a positive rate differential or at least one that is coming.

The warning label that gets applied to yield hunting is that there are various reasons for countries to have positive rate/yield differentials. Things like: A country has a different economic cycle than other countries. A country determines that they are in need of foreign investment to fund infrastructure projects. Or, an emerging nation might need to pay investors a higher interest rate as a “risk premium” to attract foreign investment.

And then there’s the rogue country that allows inflation to get out of control, and then races to raise interest rates to combat that inflation. These are countries we want to avoid.

So, with the ground rules understood, let’s go yield hunting!

AustraliaWe’ll start with the highest yield in the industrialized world… Australia, where the economic

cycle jumped ahead of most countries due to demand for its raw materials. In Australia, you can still find yields that beat the U.S., Eurozone or Japan by 200 basis points (2%) in the 5-year maturity area.

The Reserve Bank of Australia recently cut interest rates in response to the global slowdown, and will look to cut rates again later this year. So an investor still has time to look at the 5 year, or longer, Aussie government bond and lock in a yield.

Currency Watch

Interest Rate Differentials Around the GlobeBy Chuck Butler

Remember that when buying a foreign bond, the foreign currency that denominates the bond must be purchased to settle the bond trade. Therefore, you own the foreign currency through the bond.

The Currency Component

“

”

WORLD MONEY ANALYST ISSUE 4 • May 201215

BrazilAs recently as last year, this emerging nation held double-digit interest rates/yields. Brazil is a

hybrid country in that it qualifies as a commodity currency country that has seen very high inflation … and an Emerging Market that is in need of foreign investment to fund infrastructure projects for their hosting of the upcoming World Cup and Olympics.

Brazilian bonds are not readily available for the individual investor, so investors are left with deposit accounts that are denominated in Brazilian real.

Brazilian 3-month deposit yields are over 350 basis points (3.5%) better than rates found in the U.S.

The Brazilian government, through its Central Bank, has been on a mission to weaken the Brazilian real to promote growth, and they have gone about achieving this mission by cutting interest rates by very large chunks in the past year.

However, if the Brazilian government continues its efforts to weaken the currency with further rate cuts, one needs to understand that they might achieve a debasement of the real and loss of value against the US dollar. But if the Brazilian government is finished cutting rates, then you may have found a positive interest rate/yield that you can live with.

South AfricaSouth Africa, another of the BRICS (Brazil, Russia, India, China, S. Africa) countries, has always

maintained a higher interest rate structure than most of the world. As an Emerging Nation currency, the South African rand is very volatile.

However, since 2002 the rand has appreciated 34% against the US dollar. When you add in the higher interest rate that S. Africa offered during this period, the overall gains versus the dollar would be even higher.

As with Brazil, South African government bonds are not readily available for individual investors, so an investor needs to look at deposit rates only. S. African 3-month deposit rates/yields carry a positive rate differential to the U.S. of 300 basis points, or 3%.

TurkeyAnother Emerging Nation currency, the Turkish lira, is one that I currently have my eye on. (For

people that know me, that’s funny because I only have one eye that works!) Turkey’s economy has really taken off in the right direction after years of muddling through.

However, with economic growth has come rising inflation. In fact, Turkish inflation just printed for April, and showed that it was rising at the fastest pace in over 3 years.

This report suggests to me that we will see moderate rate hikes in Turkey in the coming year. This will add to the already-positive rate differential that Turkey employs – more than 300 basis points for 3-month deposits.

WORLD MONEY ANALYST ISSUE 4 • May 201216

South KoreaAnd the last Emerging Nation currency I’ll talk about this month is the South Korean won.

The won currently has a positive differential in the 3-month deposits of around 200 basis points. This isn’t as good as the others we talked about, and with steady economic growth forecast for S. Korea this year, interest rates should remain unchanged (thus no potential increase in rate differential).

Conclusion: enter these markets with cautionOf course, we all hear about the rising bond yields in Greece, Spain, and Italy. But keep in

mind that these bonds are denominated in euros. So, unless you want to own euros, these bonds should not be on your list.

When dealing with or holding currencies from Emerging Nations, they should be part of the speculative allocation of your investment portfolio. The Emerging Nations get thrown in the same barrel by the markets, which means that if something bad happens in one, all the others feel the pinch. This is a huge contributor to the wilds swings in value in the Emerging Nation currencies.

This is why I’m a true believer that currencies should be held as a diversification asset over long periods. Historically, currencies trade in trends, which are moved by fundamentals. These trends are not one-way streets, and can see volatility for short periods of time, which is why I prefer holding currencies to take advantage of the long sweeping moves they make, when the fundamentals are their friend. •

Chuck Butler is President of EverBank World Markets. Everbank is an FDIC insured US-based bank specializing in WorldCurrency® Certificates of Deposit and deposit accounts denominated in select global currencies. Contact: www.EverBank.com.

WORLD MONEY ANALYST ISSUE 4 • May 201217

Attractive Returns from Growth in Credit Card UseBy Alexei Medved

Russia

I will again start with an old Soviet joke from the time of Brezhnev in the 1970’s:

Nixon, Pompidou and Brezhnev meet God, and God says they can each ask Him a question.

“When will Americans have everything?” Nixon says.

God replies: “In five years’ time.”

“So, sadly, not within my term of office,” says Nixon shaking his head.

“When will the French become rich?” asks the French president.

God answers: “In fifteen years.”

“So, sadly, not within my term of office,” says Pompidou.

“When will everything be all right in the Soviet Union?” asks Brezhnev.

“Oh, sadly, not within my term of office” replied God.

This joke rings the bell even 40 years later, particularly in these precarious economic times.

Reforms set to show resultsNow that Vladimir Putin was officially inaugurated as President on 7 May, and the former

President Dmitry Medvedev is the new Prime Minister, the government can get down to work. Putin’s margin of victory was sufficient to give a mandate for new reforms. Also, earlier announced reforms are likely to show results later in 2012. The most important among those is Russia’s official entry into the WTO (due in June), which will push Russian companies to become more efficient to compete with foreign imports.

Other important reforms include the shift to increasing the dividend payouts by Russian companies, and the privatisation of more state-owned assets. Russia’s drive to create an international financial centre is encouraging a number of financial market friendly reforms, and this contrasts with a trend in the opposite direction in major Western economies.

Later this year, it is expected that trades in rouble-denominated securities could be settled through Euroclear, thereby allowing investors to buy Russian securities through their Western broker.

The Russian market, being high beta, is now trading at the very low P/E multiple of 5. With the medium- and long-term forecast for the crude price trending up and various reforms in the pipeline, Russia has a chance to shed its “high beta” label and significantly increase its multiples.

WORLD MONEY ANALYST ISSUE 4 • May 201218

A well respected market analyst projects that the RTS index (a major Russian equity index) will advance from its current level of 1489 to 1900 by the end of 2012 – a 27% rise in less than 8 months.

All this information is unlikely to find its way into the mainstream Western media that usually reports only “exciting” news.

This leaves the typical Western investor, including money managers, with scarce knowledge of investment opportunities in Russia. For the intrepid few Westerners that venture to invest in Russia, there are many assets available at reasonable valuations that are likely to offer attractive returns.

Finding high yields in Russian bondsFor the last few years, due to the policies of the Fed and other major central banks to keep

interest rates very low, Western investors are “starved for yield.” Investing in short-term Treasuries offers almost no return. And shifting fixed income investments into longer maturities seeking a better return, investors run the risk of incurring capital losses, as their bonds are likely to fall in price if inflation runs up in a few years.

We think that such a scenario is a distinct possibility and are keeping our fixed income investments only in short-term bonds (under 5 years; average portfolio maturity about 2 years).

One of the bonds we like on a risk-return basis (our clients have positions in it) is the US dollar denominated Eurobond issued by Tinkoff Credit System (TCS; ISIN: XS0619845349). This issue has a coupon of 11.5%, matures in April 2014, and is governed by English law.

TCS is a medium-size Russian bank that, for Russia, has an unusual business model: they concentrate on issuing credit cards to carefully pre-screened customers. This taps directly into the fast growing consumer finance market.

Unlike in the US, Western Europe or major emerging markets, the credit card penetration rates in Russia remain very low (0.1 cards per person compared with 1.7 in the USA), but the demand is very high. Unlike the situation in the West, consumer debt levels in Russia are very low. There is a lot of potential to grow this business, and TCS will be one of the main beneficiaries. Their assets quadrupled during 2010-2011, and the bank now has the 4th largest credit card portfolio in Russia (US$710 million), and is well diversified geographically across the country. The FY2011 NPL (non-performing loan) rate was only 3.7%.

TCS does not have a branch network in Russia and uses the Internet, telephone and postal services to interact with their customers. This keeps operating expenses low and profit margins high. Because the market for credit cards in Russia is less competitive than in the West, in FY2011 TCS achieved a Net Interest Margin of 43.6% and Return on Equity of 85%. These levels of profitability are rarely seen in the developed countries. The bank is well capitalised, with a Tier 1 capital ratio of 15.6% as of FY 2011 (under Basel II).

To stay prepared for the unexpected, the bank maintains a high liquidity position. Its FY2011 ratio of cash + cash equivalents to total assets was 17.8%.

WORLD MONEY ANALYST ISSUE 4 • May 201219

Alexei Medved was born and raised in Russia and later moved to the West. He received an MBA from Wharton Business School and worked for a major global investment bank, where from 1989, he developed the East European investment banking business. Since 1992, he has been running an independent business which concentrates on investments in Russia and the CIS. Contact: [email protected]

A strong track recordTCS has a history of accurately repaying its bonds on schedule (both domestic bonds and

Eurobonds). They have a number of different bonds outstanding, denominated in roubles, US$ and Swedish krona. The US$ bond described here is recommended, because it is the easiest for a Western investor to buy.

The bank is a private company, majority owned (69%) by a well-known Russian entrepreneur Oleg Tinkov, who has a track record of creating successful businesses. The main minority investors are Goldman Sachs (14%) and a well-respected Swedish investment vehicle (16%).

This combination of high profitability, strong capital position, high liquidity, good repayment history, and reputable shareholders allows us to be comfortable with TCS’ risk. At the current price of about 100.50, the yield to maturity is 11.2%.

If another financial crisis (a-la 2008) hits, the bond price will also take a hit. But if one is content to hold this bond to its maturity, this risk should not cause much worry. Even though the bank is rated as B and B2 by Fitch and Moody, respectively, well below the “investment grade,” we think that the high yield and above mentioned positive fundamentals more than adequately compensate for the risks, which we consider acceptable.

Throughout our long experience with investing in Russian assets, we found that one must go beyond the formal rating from a credit agency and look deeper for attractive returns. For 19 years, we have advised our clients on navigating this market without a single bond default in our portfolio.

An investor who considers TCS too risky can always invest in “First Tier” Russian bonds, as I described in the April issue of WMA. These will provide low credit risk, but also lower but still very attractive returns. •

WORLD MONEY ANALYST ISSUE 4 • May 201220

The FOMC looks determined to keep the Zero Interest Rate Policy (ZIRP) in place for some time. Holding cash or short-term US Treasuries has stopped being fun. Nor is it much fun buying equities when two-thirds of global GDP is close to stagnation.

In Latin America, the story is not very different. Equities have sustained a huge rally following the Lehman debacle, and sovereign debt now trades at the narrowest spreads ever to US Treasuries. Returns improve when we move into high-yield corporate bonds or high-yielding dividend stocks. In equities, there are a number of solid companies in stable sectors, such as telecommunications, food and beverages or tobacco, which offer dividend yields in the 3-4% area. Ambev (NYSE: ABV) and Telefonica do Brasil (NYSE: VIV) come to mind.

However, in Latin America we see a better risk-return profile in high-yield corporate debt, which, despite having gained liquidity in the last few years, remains a laggard relative to the region’s sovereign debt and equities. That explains why there are good opportunities left.

When we move out the risk spectrum into high-yield debt, the risk of principal loss increases. In-depth analysis is needed to find out where the best risk/reward lies, because high-yield debt typically comprises companies with either high levels of debt, or in a country or industry that is undergoing a negative cycle. Country-wise, Brazil and Mexico offer the best value and the most liquidity for non-resident investors. Chile, Colombia and Peru have a number of liquid corporate issues, but in general they trade too narrow to the sovereign debt and have limited liquidity. Argentina, on the other hand, is on its way to creating a once-in-a decade opportunity. But we are not there yet, as the government may still inflict more damage before things turn around.

Our two favorite corporate bonds in the region are the Mexican retailer Comerci’s (COMMEX 7% 2018; ISIN: USP3097WBP43) and Brazilian beef producer Minerva’s (MINERV 12.25% 2022; ISIN: USL6401PAA14).

COMMEX 7% 2018

Controladora Comercial Mexicana, or Comerci, is one of the largest self-service retail chains in Mexico. Historically run as a conservative company in a stable business (food represents a majority of sales), then-investment-grade-rated Comerci ran into financial trouble when the 2008 financial crisis hit Mexico. The peso/USD ratio, which had traded in a narrow range between 2000 and August 2008, depreciated from 10 in August to 13 in October, and later to 15 in March 2009. This sharp move led to a US$1.6 billion derivatives loss that became immediately due and payable, leading the company into default.

Latin America

Opportunities in Latin American Corporate DebtBy Claudio Maulhardt

WORLD MONEY ANALYST ISSUE 4 • May 201221

Comerci reached an agreement with its creditors in May 2010, coming out of the restructuring with a substantially lower amount of debt. The new debt is heavily collateralized by hard assets (Comerci owns 83% of its stores). Our recommended USD-denominated COMMEX 7% 2018 Notes share a collateral package made up of 78 stores and a trust with the shares of 100%-owned subsidiaries with other peso-denominated debt.

Since the day after the restructuring concluded, Comerci has been working hard to release collateral and get rid of restrictive covenants on the new debt. Indeed, Comerci made voluntary prepayments with the cash raised through the sale of non-core, non-productive assets. Net debt stood at 4.0x EBITDA by the end of 2011 (vs. 6.5x required by covenants), and the company is on a clear path to reach 2.5x by the end of 2012 through asset sales and voluntary prepayments. It is likely that if Comerci reaches that goal, yields will decline, adding potential capital gains to the yield.

COMMEX 7% 2018 Notes yield 6.5% at the ask price of 102.5 (close on May 7), for a duration of 5 years. On the basis of sector stability, company reliability, credit metrics and duration, our investment case calls for the Notes to trade at 6% yield within one year, which would result in a price of 102.40, for a total return of 8.8% on the Notes.

MINERVA 12.25% 2022

Minerva is a different story. It is a leading Brazilian protein producer and the third-largest beef exporter in the country. Over the last decade, the protein producing industry in Brazil has boomed with the support of the country’s development bank (BNDES). Minerva competitors JBS and Marfrig have been involved in an acquisition spree that saw them become global giants with diversified interests in beef, pork and chicken. On the other hand, Minerva has pursued a more conservative growth strategy focused exclusively on beef, with a preference for organic growth (internally generated) and smaller acquisitions.

This has helped its results be far less volatile than those of its competitors. Minerva enjoys a lower cost structure and higher capacity utilization than its peers. Its margins have been improving, thanks to a mix of international dynamics (growing demand for protein), market share gains, and, as of late, a much improved cattle cycle in Brazil (which reduced the price of livestock).

In September 2011, Minerva started to improve its debt maturity profile, which was heavily front-loaded. The first step of the process included the issue of mandatory convertibles for BRL200 million (about US$110 million). That was followed in early 2012 by the issue of US$450 million in 2022 Notes. Although as of the end of 2011, Minerva was still highly leveraged at 6x debt/EBITDA, these two issues have cleared its maturity profile completely – there is no significant debt coming due until 2019.

Comerci’s Total Debt $bn

WORLD MONEY ANALYST ISSUE 4 • May 201222

Minerva is in a volatile industry and is highly indebted, but it is an improving credit whose cash earnings doubled in the last three years. It has built a solid cash position worth more than US$400 million and faces virtually no maturities in the next seven years.

At the ask price of 107 (close on May 7), MINERV 12.25% 2022 Notes yield 10.9% for a duration of 5.3 years. Our financial model suggests that Minerva’s leverage could fall to 3.0x by the end of 2013.

At that stage, we would expect the Notes to trade at a 9% yield (a price of 113), for a total return of 24% in 19 months.

Conclusion

Zero yields are not an acceptable return on cash that loses purchasing power against inflation. US Treasuries and high-grade corporates offer little reward for taking the duration risk while the money-printing machines are working full hours.

The opportunities are to be sought in the high-yield spectrum. This could be tricky in turbulent times, but the way to get around the problems is an in-depth analysis of target credits.

Within Latin America, two of our preferred credits are Comerci and Minerva. With different levels of risk and return, both present a clear alternative for the investor undertaking an intelligent risk to avoid the ZIRP world. •

Claudio Maulhardt is a partner and portfolio manager at Copernico Capital Partners, a hedge fund manager headquartered in Buenos Aires, Argentina, with a Latin America geographic focus. Claudio joined Copernico in 2003 following ten years as a senior equity research analyst for Latin America at ABN AMRO in Buenos Aires and New York, and at Banco Republica in Buenos Aires. Claudio graduated from the Universidad de Buenos Aires in economics. Contact: [email protected].

Minerva’s debt maturity profile $M

WORLD MONEY ANALYST ISSUE 4 • May 201223

Gold and silver have been taking it on the chin lately – and not just in terms of price. Financial luminaries Warren Buffett and Bill Gates trashed precious metals earlier this month, calling them “unproductive assets.” While we suspect Warren may be “talking his

book”—rumor is he has a fairly substantial short position in gold—he is also correct in the classic sense: gold and silver, by themselves, generate no return.

Precious metal holdings don’t generate earnings, throw off dividends or pay interest. They may be stores of value, but unless the world returns to the gold standard—a possibility that we believe is slim at best—their ultimate worth is based solely on what other people think they are worth. This makes them highly susceptible to swings in trader psychology, as demonstrated by their recent pummeling.

But what if there was a way to turn precious metal holdings into investments that produced an income stream? Not only is this possible, it is the way many professional metals traders enhance the income-generating potential of their positions. Individual investors can do the same thing. All it takes is a simple plan coupled with a rudimentary, working knowledge of options.

A Short Course in Options When you trade options, you are not buying and selling the underlying market. You are

trading rights and obligations connected with that market. Option buyers pay money for the right to engage in a specific action. Option sellers receive money in exchange for the obligation to engage in a specific action. Understand this and all options—even complex strategies—will make sense to you. Think of it this way: your employer pays you money, and, in exchange, he has a right to expect you to perform. You’ve taken his money, so you have an obligation to perform. Options work the same way.

• Buyers of precious metal call options pay money for the right, but not the obligation, to be long metal at a specific price (known as the “strike” or “striking” price) for a limited amount of time.

• Sellers of precious metal call options receive money for the obligation to sell metal at a specific price (known as the “strike” or “striking” price) for a limited amount of time.

Notice that nowhere are we buying and/or selling actual metal. Instead, we are buying and selling rights and obligations related to that metal.

Call option buyers do not buy metal; they buy the right to be long. Call option sellers do not sell metal; they get paid for the obligation to sell. They may never have to make good on that obligation and get to keep the money they receive no matter what.

Generating Yield in Unyielding Markets

Commodities

By Stephen Belmont

WORLD MONEY ANALYST ISSUE 4 • May 201224

It’s the same with put options.

• Buyers of precious metal put options pay money for the right, but not the obligation, to sell (or short) metal at a specific price (known as the “strike” or “striking” price) for a limited amount of time.

• Sellers of precious metal put options receive money in exchange for the obligation to buy metal. Put options buyers don’t short metal; they buy the right to be short.

Put option sellers do not buy metal, they get paid for the obligation to buy. Like call sellers, they may never have to make good on that obligation. They get to keep the money they receive no matter what.

Selling Covered Calls to Generate Yield in GoldBefore I can structure a yield-generating investment strategy, I need to have a market outlook

that includes a price at which I would be willing to sell the portion of my gold holdings I wish to earn an income stream on. As the chart below indicates, the Midas metal is firmly ensconced in a 10-month trading range and looks to be approaching support around the $1,500 level.

Let’s assume I am a long-term bull and I want to use this dip as an opportunity to buy, but also want to “earn interest” on my gold. In the example below, I am going to exchange the obligation to sell gold at the top of its recent trading range for the opportunity to earn a “yield” on my holdings.

As an options broker and trader, I am going to use the options I know best – the gold and silver futures options traded on the COMEX in New York. The COMEX is the most liquid precious metals option market in the world and gets a favorable tax treatment. Liquid markets are essential to making these strategies work. That said, one could probably take the same concepts I will outline in the two examples below and apply them to any underlying security with a liquid options market, including the ETFs SLV, GLD or GDX.

WORLD MONEY ANALYST ISSUE 4 • May 201225

On the COMEX close May 8 (actual prices), I buy gold at $1,604 per ounce and then sell a December 2012 $1,900 call for $21 per ounce. I receive $21 in exchange for my obligation to sell the gold I just purchased for $1,604 per ounce at a price of $1,900, almost $300 per ounce higher. This obligation is good until the December option expiration on November 27 – 202 days from my trade date. (The COMEX gold contract size is 100 ounces.)

The $1,900 strike price of my call is roughly 18.5% higher than my $1604 buy price, so in essence, I am “getting paid” an additional $21 per ounce for the obligation to sell my gold if it rallies 18.5% prior to option expiration. I get to keep that $21 as long as I maintain my short option position. Since $21 is 1.3% of the $1,604 per ounce I paid for my gold, this is the “yield” on my gold holdings over the next 202 days.

Divide 1.3% by 202 and multiply the result times 365 and my annualized rate of return on my gold works out to 2.4% -- roughly a half a percentage point better than 10-year Treasuries.

Let’s say gold stays below $1,900 through option expiration on November 27. My short call will expire with no value and my effective buy price will be reduced by $21 per ounce from $1,604 to $1,583. I could then resell another call 18.5% away from the market—or more—to generate a new income stream. I could keep doing this as long as gold stayed below the strike price of my short option.

Now let’s assume gold is above $1,900 per ounce on option expiration. I will be forced to sell at $1,900 an ounce, but I will still get to keep the $21 I received for this obligation. That makes my net selling price $1,921 ($1,900 plus $21). Subtract from the $1921 the $1,604 that I paid and my gain is $317 per ounce – not a bad consolation prize for being forced to sell my gold. If I wanted to maintain my position, I could simply buy another 100 ounces and look to sell options with a higher strike price on it as well.

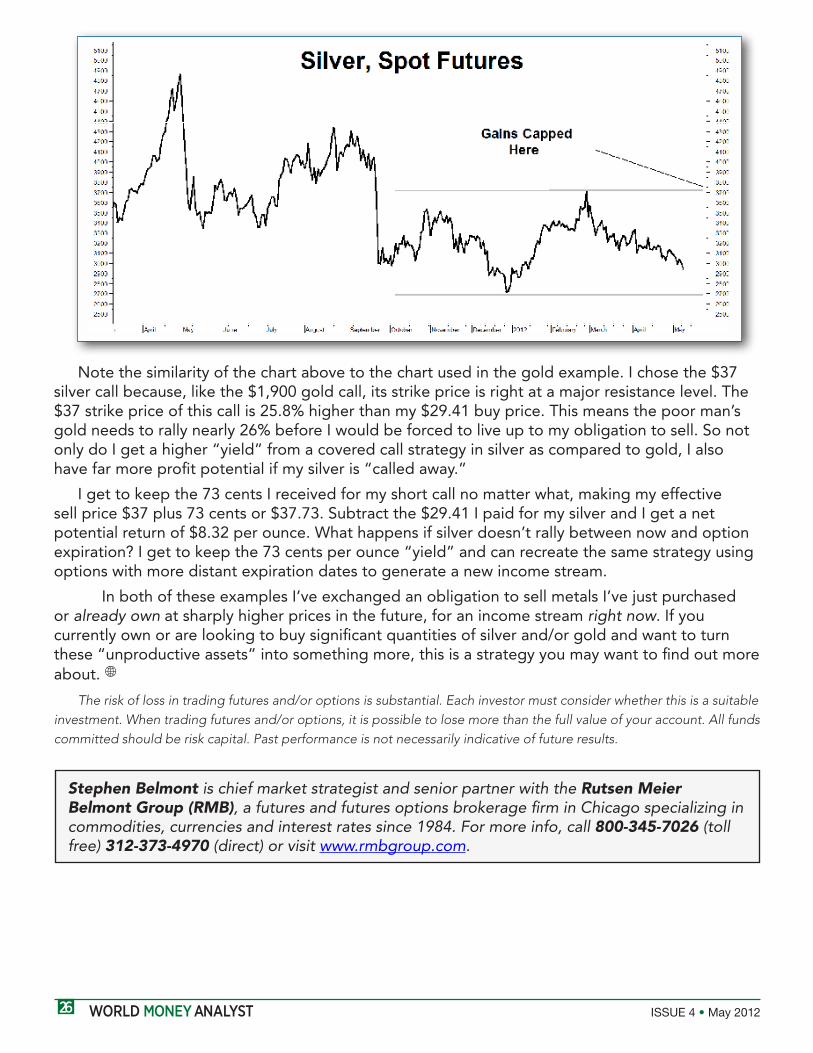

Silver “Yields” Are Even Higher Because of its relatively small size, the silver market is typically far more volatile than gold.

Volatile markets generally lead to more expensive call options. Expensive call options mean bigger potential “yield” opportunities for holders of silver.

Using the same strategy as gold, let’s assume I decided to buy silver on the COMEX close on May 8 for $29.41 per ounce, and simultaneously sold a December 2012 $37.00 call and collected 73 cents in exchange for the obligation to sell silver at $37.00 per ounce. (The COMEX silver contract size is 5,000 ounces.)

Since 73 cents is roughly 2.5% of the $29.41 per ounce I just paid for my silver, the potential “yield” on this play is 2.5% over the next 202 days. (December COMEX silver options expire the same day as COMEX gold options.) I divide 2.5% by 202 and then multiply the result times 365 to get an annualized “yield” of 4.5% – over twice the current yield on 10-year Treasuries.

What I give up in exchange for this income stream is the ability to make money over $37 per ounce, should the market rally above that price prior to the expiration of my short call.

WORLD MONEY ANALYST ISSUE 4 • May 201226

Note the similarity of the chart above to the chart used in the gold example. I chose the $37 silver call because, like the $1,900 gold call, its strike price is right at a major resistance level. The $37 strike price of this call is 25.8% higher than my $29.41 buy price. This means the poor man’s gold needs to rally nearly 26% before I would be forced to live up to my obligation to sell. So not only do I get a higher “yield” from a covered call strategy in silver as compared to gold, I also have far more profit potential if my silver is “called away.”

I get to keep the 73 cents I received for my short call no matter what, making my effective sell price $37 plus 73 cents or $37.73. Subtract the $29.41 I paid for my silver and I get a net potential return of $8.32 per ounce. What happens if silver doesn’t rally between now and option expiration? I get to keep the 73 cents per ounce “yield” and can recreate the same strategy using options with more distant expiration dates to generate a new income stream.

In both of these examples I’ve exchanged an obligation to sell metals I’ve just purchased or already own at sharply higher prices in the future, for an income stream right now. If you currently own or are looking to buy significant quantities of silver and/or gold and want to turn these “unproductive assets” into something more, this is a strategy you may want to find out more about. •

The risk of loss in trading futures and/or options is substantial. Each investor must consider whether this is a suitable investment. When trading futures and/or options, it is possible to lose more than the full value of your account. All funds committed should be risk capital. Past performance is not necessarily indicative of future results.

Stephen Belmont is chief market strategist and senior partner with the Rutsen Meier Belmont Group (RMB), a futures and futures options brokerage firm in Chicago specializing in commodities, currencies and interest rates since 1984. For more info, call 800-345-7026 (toll free) 312-373-4970 (direct) or visit www.rmbgroup.com.

WORLD MONEY ANALYST ISSUE 4 • May 201227

Update on Reporting Requirements for US Tax FilersBy Kevin Brekke

International Investors Toolkit

Next month brings with it an important date: June 30, the filing deadline for Treasury Form TD F 90-22.1 (the FBAR). US persons that hold foreign financial assets or accounts are already intimately familiar with this form. Also starting this year, many also got acquainted

with the new IRS Form 8938 that greatly expanded the types of foreign assets that must now be reported to the US tax authorities.

Over the past 18 months, we have seen a series of changes to the reporting requirements for foreign assets held by US tax filers, including the release of the new form mentioned above. With each stage of change there were questions, as the instructions that accompanied the changes were not always clear and left tax filers hanging about how they should be interpreted – an unsettling situation, as the penalties for failure to file are absurdly extreme.

However, the IRS recently published guidance on reporting requirements that pretty much covers the universe of possible foreign accounts and assets in a table format, and I have reproduced it below for your reference. Much of the information it contains is not new, but to have it distilled and aggregated into a single document is a giant time saver as, previous to the table, the information was scattered across various bureaucracies, websites, circulars, notices, amendments, and final rulings.

Like thanking ones executioner for tying such a stout slipknot (in a perverse sense), we must be thankful that the bad news can now be located faster and is easier to understand.

There is some good news to reportAs shown below, the table covers everything from brokerage accounts to life insurance,

trusts to hedge funds, and precious metal bullion to real estate. For most assets, the question of whether or not it is reportable is fairly black or white. Today—considering that many WMA subscribers hold some of these foreign assets—I will cover two of them in more detail and show where we got some good news and some “gray” news.

Let’s begin with the good news: real estate. Last year, following the release of the new IRS Form 8938, real estate entered the foreign asset-reporting scheme. And lacking a clear definition, the question surfaced as to whether a personal residence and rental property are reportable.

That question has been answered as shown in the table below. The IRS uses the “failure to indicate yes means no” approach: that is, foreign real estate held directly is not reportable. “Held directly” means that the property is not held through an entity such as a trust, LLC, real estate fund, partnership, etc. So, foreign real estate such as a personal residence or rental property is not reportable if it is owned outside an entity (although any rental income from property held directly must be reported).

Also note that foreign assets such as collectibles, artwork, cars, and boats are not reportable.

WORLD MONEY ANALYST ISSUE 4 • May 201228

Foreign ownership of bullion There remains one gray area in reporting: foreign-held bullion. Some readers will recall that last

year, following amendments to the FBAR released in February, a new term was introduced under “Types of reportable accounts”: accounts with a financial agency.

The definition of “financial agency” added little clarity, as it included the phrase “transactions in gold” as part of the services that a financial agency might provide. This opened to speculation whether the word “gold” was meant as a placeholder to indicate all precious metals … or if it was meant literally and that silver, platinum, and palladium were all exempt.

That mystery was solved as IRS guidance (shown in the table) now states that all precious metals held outside the US are reportable except precious metals held directly. Well, that’s just peachy, but what the heck does “held directly” mean? Unlike for real estate, where “held directly” is defined, what it means for bullion remains unclear.

From the legal opinions that I have reviewed, “held directly” is being interpreted to mean that the owner has unencumbered access to the precious metal. But there is far from 100% consensus on that interpretation. The storage method that draws mixed opinions is the use of a bank safe box – is that “held directly”?

Private vaulting facilities, warehouse receipts, mint certificates, and companies that buy and store bullion through an account all would be reportable. But it looks like we must wait for an answer to the bank safe box question. In the meantime, I always advise that when in doubt, report it.

FATCA and final outcomesI continue to receive mail from privacy fanatics that have their jackboots laced tight and declare

that only a fool would roll over and report their personal financial information. They claim to have figured out a way around the reporting requirements and that may or may not be true. But what they haven’t figured out is the breadth and depth of the reporting tentacles of the impending Foreign Account Tax Compliance Act (FATCA).

FATCA is a topic beyond the scope of this letter. But in short, it will require all financial institutions worldwide to identify their US clients and report their assets and activity to the IRS. That is a gross simplification (the latest document on changes to FATCA is 400 pages) but just ponder the big picture for a moment.

In my mind, whether or not we parse every syllable, or hire the best attorneys, there is no escaping the fact that any US person holding assets/accounts offshore will eventually be outed. How will this happen?

Unless the intended holding period of one’s assets is “forever” (and even then, the responsibility for reporting will fall to ones heirs), when any asset that is held offshore is eventually sold, it will be converted to cash and enter the banking system. Any bank account or movement of assets through the banking system will generate a 1099 sent to the IRS. The IRS can then compare that information to the individual’s tax records and Forms 8938 or 90-22.1 that may or may not have been filed. If the required reports are missing, one can expect a call from the Criminal Investigation arm of the IRS.

WORLD MONEY ANALYST ISSUE 4 • May 201229

My personal approach is to apply a conservative interpretation and stay compliant. It simply is not worth the loss of sleep or the possible penalty – and for the FBAR, a failure to file can mean financial ruin. And for what: To maintain the appearance of keeping your financial privacy? With FATCA, financial privacy is gone. What remains is to keep your financial security, and you can only do that if you keep yourself compliant with the reporting requirements, no matter how repugnant they are. To that end, you will see a recap of the reporting thresholds for both forms at the end of the table.

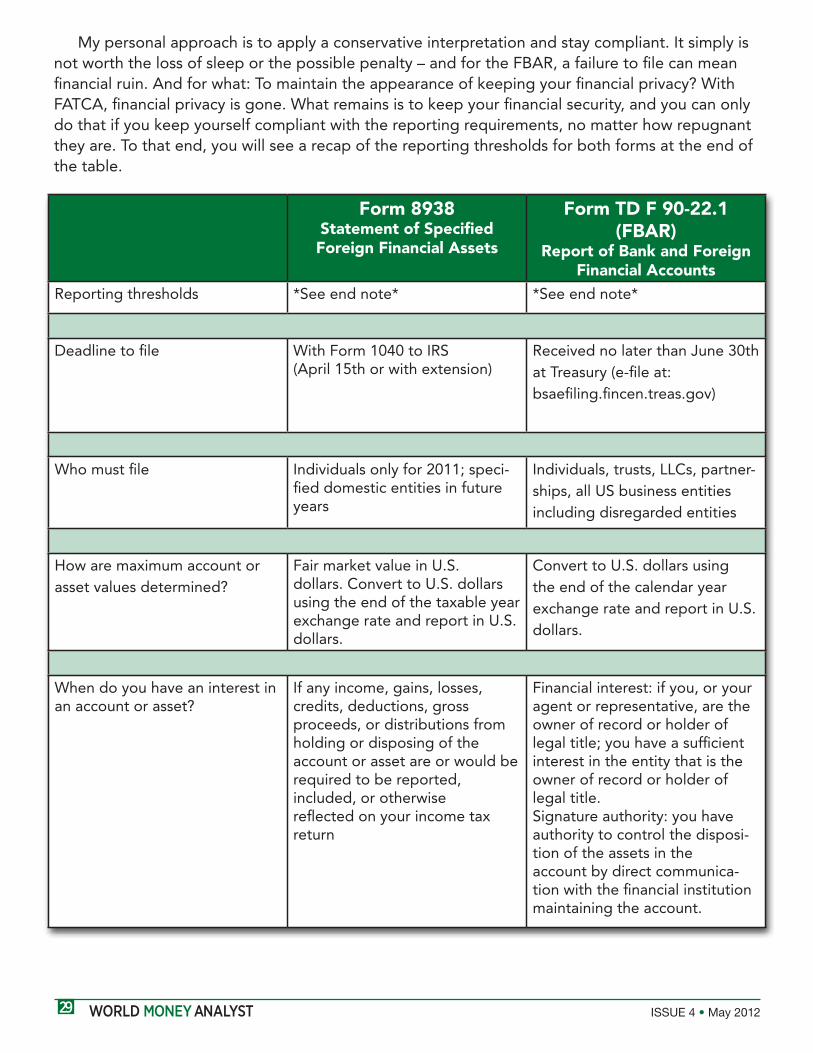

Form 8938Statement of Specified Foreign Financial Assets

Form TD F 90-22.1 (FBAR)

Report of Bank and Foreign Financial Accounts

Reporting thresholds *See end note* *See end note*

Deadline to file With Form 1040 to IRS(April 15th or with extension)

Received no later than June 30th at Treasury (e-file at:bsaefiling.fincen.treas.gov)

Who must file Individuals only for 2011; speci-fied domestic entities in future years

Individuals, trusts, LLCs, partner-ships, all US business entities including disregarded entities

How are maximum account or asset values determined?

Fair market value in U.S. dollars. Convert to U.S. dollars using the end of the taxable year exchange rate and report in U.S. dollars.

Convert to U.S. dollars using the end of the calendar year exchange rate and report in U.S. dollars.

When do you have an interest in an account or asset?

If any income, gains, losses, credits, deductions, gross proceeds, or distributions from holding or disposing of the account or asset are or would be required to be reported, included, or otherwise reflected on your income tax return

Financial interest: if you, or your agent or representative, are the owner of record or holder of legal title; you have a sufficient interest in the entity that is the owner of record or holder of legal title.Signature authority: you have authority to control the disposi-tion of the assets in the account by direct communica-tion with the financial institution maintaining the account.

WORLD MONEY ANALYST ISSUE 4 • May 201230

Form 8938Statement of Specified Foreign Financial Assets

Form TD F 90-22.1 (FBAR)

Report of Bank and Foreign

Financial AccountsDoes the U.S. include U.S. territories? No Yes. Resident aliens of U.S

territories and U.S. terri-tory entities are subject to FBAR reporting

Foreign Asset Types and Reporting Obligation

Precious metals Yes(Exception: precious metals held directly)

Yes(Exception: precious metals held directly)

Foreign real estate held directly No No

Foreign real estate held through a for-eign entity

No. But the foreign entity itself is a specified foreign financial asset and its maximum value includes the value of the real estate

No

Indirect interests in foreign financial as-sets through an entity

No Yes, if sufficient ownership or beneficial interest (i.e., a greater than 50 percent interest) in the entity. See instructions for fur-ther detail.

Foreign-issued life insurance or annuity with a cash-value

Yes Yes

Foreign stock or securities held in a financial account at a foreign financial institution

Report the account itself. Do not report the contents of the ac-count separately

Report the account itself. Do not report the contents of the account separately

Foreign stock or securities not held in a financial account

Yes No

WORLD MONEY ANALYST ISSUE 4 • May 201231

Form 8938Statement of Specified Foreign Financial Assets

Form TD F 90-22.1 (FBAR)

Report of Bank and Foreign

Financial AccountsFinancial (deposit and custodial) accounts held at foreign financial institutions

Yes Yes

Financial account held at a foreign branch of a U.S. financial institution

No Yes

Financial account held at a U.S. branch of a foreign financial institution

No No

Foreign financial account for which you have signature authority

No, unless you otherwise have an interest in the account as described above

Yes, subject to exceptions

Foreign partnership interests Yes No

Foreign mutual funds Yes Yes

Domestic mutual fund investing in foreign stocks and securities

No No

Foreign accounts and foreign non-account investment assets held by foreign or domestic grantor trust for which you are the grantor

Yes, as to both foreign accounts and foreign non-account investment assets

Yes, as to foreign accounts

Foreign hedge funds and foreign private equity funds

Yes No

"Social Security"- type program benefits provided by a foreign government

No No

WORLD MONEY ANALYST ISSUE 4 • May 201232

End Note: On Feb. 24, 2011, the Final Ruling on amendments to the FBAR were released by the Treasury Dept. and printed in the Federal Register (pg. 10234, Vol. 76, No. 37). You will find details on types of reportable accounts, exceptions, what constitutes a “financial interest,” signature authority defined, and other details in the ruling. A PDF of the ruling is available here:

http://edocket.access.gpo.gov/2011/pdf/2011-4048.pdf

Reporting threshold for the FBAR:A US person who has a financial interest in, or signature authority or other authority over,

any financial account in a foreign country, and the aggregate value of these accounts exceeds US$10,000 at any time during the calendar year must file Treasury Form TD F 90-22.1. The form must be received at the Treasury Dept. by June 30 following the year for which a reporting requirement was triggered. The FBAR can now be filed online at: http://bsaefiling.fincen.treas.gov/Enroll_Individual.html

Reporting thresholds for Form 8938:Unmarried taxpayers living in the US: if the total value of your specified foreign financial

assets is more than US$50,000 on the last day of the tax year or more than US$100,000 at any time during the tax year.

Married taxpayers filing a joint income tax return and living in the US: if the total value of your specified foreign financial assets is more than US$100,000 on the last day of the tax year or more than US$200,000 at any time during the tax year.

Married taxpayers filing separate income tax returns and living in the US: if the total value of your specified foreign financial assets is more than US$50,000 on the last day of the tax year or more than US$100,000 at any time during the tax year.

Taxpayers living abroad: Must be a bona fide resident of a foreign country or countries for an uninterrupted period that includes the entire tax year, or are present in a foreign country or countries during at least 330 full days during any period of 12 consecutive months ending in the tax year.

• Unmarried or married filing separately: if the total value of your specified foreign financial assets is more than US$200,000 on the last day of the tax year or more than US$400,000 at any time during the tax year.

• Married filing jointly: if the total value of your specified foreign financial assets is more than US$400,000 on the last day of the tax year or more than US$600,000 at any time during the tax year. •

WORLD MONEY ANALYST ISSUE 4 • May 201233

WMA Recap - May 2012

• Marine Harvest (Oslo Exchange: MHG) is the largest producer of farmed salmon. A cyclical downturn has depressed the shares of this aquaculture company. Yet, rising worldwide demand for fish will mean big profits when salmon prices rebound, and a likely return of a double-digit dividend yield. Page 7.

• Singapore Telecommunications (SingTel; Singapore Exchange: Z74) is selling at a 20% “margin of safety” based on a discounted cash flow analysis. And it pays a respectable 5% dividend yield. Page 10.

• Growing demand in Russia for credit cards makes this Eurobond an attractive investment. Tinkoff Credit Systems (TCS 11.5% 2014; ISIN: XS0619845349) is well capitalized with a Return on Equity of 85%. Page 17.

• A post-restructuring Mexican retailer (COMMEX 7% 2018; ISIN: USP3097WBP43) and a Brazilian protein producer (MINERV 12.25% 2022; ISIN: USL6401PAA14) pursuing conservative growth represent two high-yield opportunities in international corporate bonds. Page 20.