World insurance in 2015 - Türkiye Sigorta Birliği insurance in 2015: steady growth amid regional...

52

No 3 /2016 World insurance in 2015: steady growth amid regional disparities 01 Executive summary 03 The global economy and financial markets in 2015 08 Insurance premium growth steady 16 Global trade and insurance market growth 22 Advanced market premiums grow faster than GDP 28 Emerging markets continue to gain global share 35 Methodology and data 37 Statistical appendix

Transcript of World insurance in 2015 - Türkiye Sigorta Birliği insurance in 2015: steady growth amid regional...

No 3 /2016

World insurance in 2015: steady growth amid regional disparities

01 Executive summary

03 The global economy and financial markets in 2015

08 Insurance premium growth steady

16 Global trade and insurance market growth

22 Advanced market premiums grow faster than GDP

28 Emerging markets continue to gain global share

35 Methodology and data

37 Statistical appendix

Swiss Re sigma No 3/2016 1

No data < –10.0%

–10.0% to –5.0%–5.0% to –2.5%–2.5% to 0.0%

0.0% to 2.5%2.5% to 5.0%5.0% to 10.0%

> 10.0%

Executive summary

The re/insurance industry faced another year of moderate global economic growth in 2015. Global real gross domestic product (GDP)1 grew by 2.5%. The advanced economies improved, but there was slowdown in the emerging markets with many major countries impacted by political instability and low commodity prices. The investment environment remained challenging globally, with uncertainty around policy tightening in the US and very low interest rates prevailing in advanced economies for another year. With the exception of some emerging markets, inflation was low in most countries, driven by the low commodity prices.

Despite the challenging environment, real global direct life and non-life insurance premiums written grew by 3.8% in 2015, up from 3.5% in the previous year.2 However, in nominal US dollar terms, premiums were down by 4.2% due to wide-spread currency depreciation against the USD. In real terms, life premium growth slowed to 4% from a 4.3%-gain in 2014 (2015: USD 2 534 billion). In advanced markets life premiums grew 2.5%, down from 3.8% growth the previous year. North America returned to positive growth after two years of decline. Life premium growth was also stronger in advanced Asia, driven by Japan and Korea. In Western Europe, however, growth slowed significantly. In the emerging markets, overall life premium growth almost doubled to near 12%, supported by strong sector performance in emerging Asia. Growth also improved in Latin America but was slower in the Middle East and Central Asia, and Africa. In Central and Eastern Europe (CEE), premiums contracted. Last year, life premium growth fell short of the pre-crisis3 average in advanced markets yet again, but it was slightly higher in the emerging markets.

Source: Swiss Re Economic Research & Consulting.

1 The aggregation of the individual economies that make up the global economy is weighted using US dollar GDP based on market exchange rates. International statistics using purchasing-power parity place more weight on fast-growing countries like China and India and so show higher world GDP growth rates.

2 Unless otherwise stated, all premium growth rates indicate changes in real terms (ie, adjusted for local consumer price inflation).

3 Pre-crisis: 2003–2007; post-crisis: 2009–2014.

The insurance industry faced another challenging year in 2015, with moderate economic growth and low interest rates.

Global life insurance premium growth remained steady in 2015, but the trend varied across regions.

Figure 1 Global real premium growth rates, 2015

Life Non-life Total

Advanced markets 2.5% 2.6% 2.5%Emerging markets 12% 7.8% 9.8%World 4.0% 3.6% 3.8%

2 Swiss Re sigma No 3/2016

Executive summary

Global non-life premium growth improved to 3.6% in 2015 from 2.4% the previous year (2015: 2 020 billion USD). The advanced markets were the main drivers, with all regions other than Oceania experiencing higher growth rates. Advanced Asia (+4.1%) registered the highest growth among the advanced regions, and there was a considerable gain in North America (+3.2%) also. Growth was moderate in Western Europe (+1.5%), but that was nevertheless an improvement on previous years of stagnation. Emerging markets continued their robust premium growth trend (+7.8%), primarily driven by China. Other markets in emerging Asia were solid also, as were the Middle East and Central Asia (+9.0%). In CEE, non-life premiums contracted, due to a sharp fall in Russia.

Profitability in life and non-life remained under pressure in 2015. In life, moderate premium growth in many markets and the prolonged low interest rates dragged on profits. In non-life, both the underwriting and investment result was weaker than in 2014. The underwriting result was impacted by lower reserve releases and investment results were hit by low interest rates. However, the insurance industry overall remains well capitalised.

Life premium growth is expected to accelerate slightly in the advanced economies in 2016, mainly driven by a modest improvement in Western Europe and a recovery in Oceania. In the emerging markets, the life sector is forecast to decelerate since premium growth in China is expected to slow from the high levels of 2015. The out-look for the non-life industry in advanced markets is more muted than for life, given expectations of a moderate economic recovery and pricing weakness. The outlook for non-life in the emerging markets is mixed. Premium growth will likely be strong in emerging Asia, mainly supported by China. In other emerging regions, however, premium growth is expected to weaken or even contract.

Trade flows have slowed in recent years. Global trade grew about twice as fast as world GDP between the early 1990s and mid-2000s, but has grown at the same pace as GDP in more recent years. The slowdown has in part been cyclical due to sluggish economic growth, and trade should pick up again once economic activity accelerates. However, the slowdown also reflects deeper, structural factors, such as a limit in the further dispersion of global supply chains, protectionism and the transitioning of the Chinese economy from export- and investment-led growth to domestic services and consumption. The negative impact of the trade slowdown on global growth reduces sector-wide premium growth generally. A persistent slowdown in global trade will affect marine and credit insurance growth in particular.

This sigma study contains the latest market data available at the time of going to press. The final figures for 2015 are not available for most insurance markets. As such, the sigma also contains Swiss Re Economic Research & Consulting estimates and provisional data released by supervisory authorities and insurance associations.

Non-life premium growth improved in 2015, mainly driven by the advanced markets.

Profitability was under pressure in both life and non-life, but both sectors are well capitalised.

Life premium growth in the advanced markets will improve slightly, but non-life premium growth will moderate.

The special chapter of this sigma focuses on slower trade growth and its implications for related lines of insurance.

The data in this study are the latest available at the time of going to press.

Swiss Re sigma No 3/2016 3

The global economy and financial markets in 2015

Global economic growth uneven across regions

The global re/insurance industry faced another year of moderate economic growth in 2015. Global real gross domestic product (GDP) was up 2.5%, above the post-crisis annual average of 2.2%. Growth in advanced markets continued to improve, to 1.9% from 1.8% in 2014. This was still below the pre-crisis but exceeded the post-crisis average by 1 percentage point (ppt). Emerging markets’ aggregate growth was disappointing at 3.5%, less than half the pre-financial crisis average growth levels of 7.4%, and below the post-crisis average of 4.7%.

Among the advanced markets, the US economy expanded by 2.4%, while growth in Canada fell to 1.2% from 2.5% in 2014. Total GDP growth in North America fell to 2.3%, slightly short of the pre-crisis but 1 ppt more than the post-crisis annual average growth rate. Japan’s economy grew slightly after a shallow recession in 2014. In Western Europe, growth improved to 1.8% in 2015 (2014: 1.4%), supported by low interest rates, low oil prices and a relatively weak euro. The UK outperformed its continental peers again while within the Euro area, Germany and Spain grew faster than France and Italy, where structural reforms are still much needed.

Aggregate emerging market growth was weak at 3.5%, with some countries struggling with low commodity prices and political instability. Growth in other markets, however, most notably China, CEE EU member countries and African non-commodity exporters, remained solid. Deep recessions in Brazil and Venezuela dragged on overall performance in Latin America. Brazil’s economy contracted by 3.8%, suffering from low commodity prices, high inflation and political uncertainty. In Mexico, industrial activity was low while private consumption remained healthy. Economic growth in most CEE countries was solid but recession in Russia (GDP fell 3.7%), due to low oil prices and sanctions because of the Ukraine conflict, weighed on the region’s aggregate growth (–1.2%).

The emerging Asian economies expanded unevenly last year. China’s economy continued its transition from manufacturing to services, and growth slowed to 6.9%, just below the government’s target of 7%. India was the world’s fastest-expanding large economy (+7.3%) in 2015, with business and consumer sentiment improving significantly on expectations of a strong push towards economic reform and liberalization by the Narendra Modi government.

Major economies in Africa developed unevenly, driven largely by political developments and lower oil and commodity prices. Growth in South Africa was sluggish with companies there having to contend with lower commodity prices, weak domestic demand, electrical outages, worker strikes and rising input costs. Nigeria and Angola suffered from low oil prices and infrastructure bottlenecks, while many oil-importing countries grew solidly (eg, Morocco, Kenya and Côte d’Ivoire). In the Middle East and Central Asia, Saudi Arabia experienced solid growth, supported by greater public spending, despite collapsing government revenues from oil. Growth in Turkey was robust, despite civil disturbance and political turmoil.

The global economy grew moderately in 2015.

Growth in the advanced markets continued to improve slightly …

… but emerging market growth was weak, with some countries impacted by low commodity prices and political instability.

India overtook China as the world’s fastest growing large economy.

Major economies in Africa developed unevenly due to political uncertainties and dependency on commodities.

4 Swiss Re sigma No 3/2016

The global economy and financial markets in 2015

Remarks: Countries’ GDP weighted with market exchange rates. Source: Oxford Economics, WIIW, Swiss Re Economic Research & Consulting.

Interest rates and headline inflation approach zero

Central bank intervention, policy divergence and uncertainty drove the financial markets in 2015, and interest rates were at record lows. The European Central Bank (ECB) and the Bank of Japan (BoJ) continued their expansionary and unconventional monetary policies as the Euro area and Japanese economies remained fragile with deflation an ongoing risk. In contrast, the US Federal Reserve Board made a small move towards monetary policy normalisation with an interest rate hike in December.

–1.0%

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

US Germany France

Apr

20

16

Aug

20

11

Apr

20

11

Dec

20

10

Dec

20

11

Aug

20

12

Apr

20

12

Dec

20

12

Aug

20

13

Apr

20

13

Dec

20

13

Aug

20

14

Apr

20

14

Dec

20

14

Aug

20

15

Apr

20

15

Dec

20

15

Aug

20

10

Apr

20

10

Dec

20

09

Aug

20

09

Apr

20

09

Dec

20

08

Aug

20

08

Apr

20

08

Dec

20

07

Aug

20

07

Apr

20

07

Dec

20

06

Aug

20

06

Apr

20

06

Dec

20

05

Japan UK

Source: Datastream.

Figure 2 Real GDP growth by region in 2015, and pre- and post-financial crisis average

–2% 0% 2% 4% 6% 8% 10%

Middle East and Central Asia

Latin America and the Caribbean

Emerging AsiaEmerging Asia excl. China

Emerging markets excl. ChinaEmerging markets

OceaniaAdvanced Asia

Western EuropeNorth America

Advanced markets

World

Central and Eastern Europe

Post-crisis average growth 2009–2014Pre-crisis average growth 2003–2007Growth rate 2015

Africa

The ECB continued quantitative easing, but the US Fed raised rates once.

Figure 3 Long-term interest rates, December 2005 to April 2016

Swiss Re sigma No 3/2016 5

Anticipation of a US interest rate hike kept yields on US and UK 10-year government bonds about 1.5 ppt above the German and Japanese equivalents (Figure 3). The US took a first step to monetary policy normalisation in 2015, but interest rates in the advanced economies remain historically low (see Box: Low interest rates forever?). Even so, inflation in the US, the Euro area and the UK dropped close to zero last year, based largely on low commodity prices. In the US, core inflation, which excludes food and energy, was essentially unchanged at 1.8%. Inflation in Japan fell below 1% after rising to 2.9% in 2014 due to the sales tax increase in April 2014. Crisis-hit Brazil and Russia increased policy rates in an attempt to counter capital outflows and inflation. In contrast, China and India both reduced their policy rates.

Stock market performance in advanced markets was mixed. The S&P 500 in the US was down 0.7%, and the MSCI UK index was down 5.9%. By contrast, the Japanese Nikkei 225 was up 9.1% and the German DAX 30 by 9.6% (Figure 4). The mixed performance reflects the diverging paths of monetary policy. After three consecutive years of ending in positive territory, the world’s major equity markets slowed due to increased uncertainty, weak profit growth and investor caution.

US (S&P 500): –0.7% MSCI UK: –5.9%MSCI Emerging Markets: –17%Germany (DAX 30): 9.6%Japan (Nikkei 225): 9.1%

May

20

16

Apr

20

15

Mar

20

15

Feb

20

15

Jan

20

15

Dec

20

14

Nov

20

14

Oct

20

14

Sep

20

14

Aug

20

14

Jul 2

01

4Ju

n 2

01

4M

ay 2

01

4

Apr

20

16

Mar

20

16

Feb

20

16

Jan

20

16

Dec

20

15

Nov

20

15

Oct

20

15

Sep

20

15

Aug

20

15

Jul 2

01

5Ju

n 2

01

5M

ay 2

01

5

Apr

20

14

Mar

20

14

Feb

20

14

Jan

20

14

70

80

90

100

110

120

130

Note: percent values indicate year-on-year change of respective indices in 2015.

Source: Datastream.

Stock markets in the emerging markets suffered substantial losses driven by falling commodity prices, heightened political instability in many regions and uncertainty around US monetary policy. The MSCI Emerging Markets index fell by 17% in 2015, but recovered partially in the first quarter of 2016.

In the emerging markets, policy rates diverged.

It was a mixed year for stocks in the advanced markets.

Figure 4 Stock market performance, 2014–2016 (December 2014 = 100)

Emerging market stock indices fell substantially.

6 Swiss Re sigma No 3/2016

The global economy and financial markets in 2015

Outlook: improving, but interest rates to rise only moderately

The global economy faces four major headwinds that will produce periods of market volatility alongside moderate growth in 2016 and 2017: the US Federal Reserve will continue to raise interest rates; China continues to open its capital account; commodity prices have stabilized at low levels and are unlikely to increase substantially; and global political developments continue to create uncertainty. Nevertheless, in advanced markets economic fundamentals remain strong. In the US, real GDP is expected to continue to grow steadily this year and next, and employment and income growth are expected to remain strong. The Euro area is benefiting from a weak euro and low oil prices, and growth is forecast to improve in each of the next two years. Stable growth is likely in the UK, where consumer spending and housing construction have sustained momentum in the first half of 2016, in spite of the uncertainty created by the Brexit referendum which has dampened business investment and hiring.4

Economic growth in emerging markets is forecast to improve in 2016, reflecting reduced recessionary pressures in key markets in Latin America and CEE. However, weak growth in trade is likely to continue and financial volatility, currency depreciation and capital outflows will remain key challenges for many emerging economies. Growth in China is expected to slow in 2016, while Brazil and Russia will likely remain stuck in recession. In Brazil challenges to governability will remain following the recent impeachment of President Rousseff, given the heavily charged and polarized political atmosphere. In Russia low oil prices and the continuation of sanctions are holding back growth. Risk of an emerging market financial crisis continues, as indicated by wide emerging market bond spreads. However, the threat of contagion is limited due to stronger financial buffers in individual markets and also enforcement of precautionary macro-prudential measures.

Global monetary policy divergence will continue in 2016 after the BoJ surprised markets with negative interest rates in January and the ECB, in March, announced further extension of its unconventional policy measures. Inflation in the US is forecast to rise, and the Fed is expected to raise its policy rate two times in 2016. The slow pace of monetary tightening has increased the risk of inflation. The Bank of England (BoE) will likely follow suit, with two rate hikes starting in August after the Brexit referendum. In contrast, the ECB and BoJ are more likely to ease monetary policy further. In such an environment, yields on the US and UK 10-year government bonds are likely to rise modestly, to 2.2% and 2.0%, respectively, by end-2016. German and Japanese 10-year yields will also rise, but by less (to 0.8% and 0%). Their low value is essentially pulling down US and UK yields. If volatility subsides, equity markets could improve and credit spreads could narrow further this year.

Many downside risks to the global economy remain. In the US, the risk is inflation followed by more-rapid-than-expected monetary tightening. In the Euro area, a “Grexit” could become a problem again as implementation of reforms is lagging. However, contagion risk has declined over the last few years and the ECB has become a credible lender of last resort. Immigration will remain an issue in Europe and could compromise pro-reform governments and/or delay implementation of structural reforms. In China economic and financial risks remain high. The country is pursuing contradictory policies as it attempts to simultaneously liberalise its capital account, lower interest rates to support growth and maintain a stable exchange rate. A string of unfavourable events, such as defaults by property developers or local governments, or a sharp renminbi depreciation and capital outflows, would increase the likelihood of a hard-landing.

4 The result of the 23 June 2016 vote in the UK on whether to stay in the EU was not known at the time of going to print.

There will likely be heightened market volatility alongside moderate global growth in the next two years.

Economic growth in the emerging markets is forecast to pick up, but challenges remain.

Monetary policy divergence will continue, and inflation is expected to accelerate, particularly in the US.

The global economy will likely muddle through in 2016, but downside risks remain.

Swiss Re sigma No 3/2016 7

Low interest rates forever?After the financial crisis, major central banks kept policy rates at close to zero for about seven years to support economic recovery and put upward pressure on prices. In this context, the consequences of the interest rate hike by the US Fed in December 2015 and the direction of long-term interest rates raise key questions for insurers. This is because income from financial assets is an important part of earnings, although not all lines of business are affected to the same degree. Will interest rates finally rise and go back to pre-crisis levels?

During the last three decades, yields for 10-year government bonds have decreased steadily. However, inflation expectations, calculated by the difference in yields from inflation-protected and unprotected bonds, remained relatively stable, reflecting the credibility of central banks’ inflation targets. A recently published Geneva Report on the world economy therefore associates the fall in yields during the last two decades with lower real interest rates, rather than with a decline in inflation expectations.5

The financial crisis and the subsequent reaction of central banks caused just a small dip in the long-term down trend of real interest rates. Hence, other drivers need to be at work. The Geneva report focuses on different explanations: An ageing population in most parts of the world led to an increase in the

aggregate propensity to save, some of which went into fixed income assets, lowering real interest rates.

Another contributing factor has been the increase in savings in China. The higher savings coupled with China’s increased financial integration, led to large capital outflows into global financial markets.

A shift in investor preferences away from risky assets towards safe bonds is another likely driver for lowering real interest rates.

These factors may persist for some time, and re/insurers need to be prepared to cope with low interest rates for a while yet. However, the report also mentions that with time, interest rates could increase as the causes of the downward trend reverse: First, aggregate savings levels could decrease as the cohort of current savers

continues to move towards retirement; Second, with the shift in China from investment and exportled growth to a more

consumption-driven economy, the Chinese outflow of capital into global financial markets may also stabilise; and

Finally, a gradual return of investors into more risky assets could alleviate pressure on interest rates.

5 Low for Long? Causes and Consequences of Persistently Low Interest Rates, October 2015, International Center for Monetary and Banking Studies (ICMB) and Centre for Economic Policy Research (CEPR).

Interest rates remain very low after the financial crisis.

A Geneva Report finds that long-term government bond yields have fallen for three decades, but inflation expectations have remained stable.

Other factors could be at play in the long-term downtrend in interest rates.

According to the report, interest rates could eventually rise again.

8 Swiss Re sigma No 3/2016

Global insurance premiums continued to grow in 2015

Total direct premiums written grew by 3.8% in real terms in 2015, up from 3.5% growth in 2014.6 Global premium volumes were USD 4 554 billion, which in nominal terms was 4.2% less than the previous year, due to significant currency depreciation against the US dollar (USD). The euro lost significant value against the USD (–20%), and UK sterling (GBP) and the Japanese yen (JPY) were also impacted, as were advanced-market commodity exporters (Australia, Canada). Many emerging market (Russia, Brazil, South Africa, others) currencies depreciated strongly also.

Total Non-life Life

–10%

–5%

0%

5%

10%

15%

20%

2015

2013

2011

200

9

2007

200

5

200

3

2001

199

9

1997

199

5

1993

1991

198

9

1987

198

5

198

3

1981

Source: Swiss Re Economic Research & Consulting.

Source: Swiss Re Economic Research & Consulting.

6 Unless otherwise stated, all premium growth rates indicate changes in real terms (ie, adjusted for local consumer price inflation).

Global premiums grew by a real 3.8% in 2015, but declined by 4.2% to USD 4 554 billion in nominal terms.

Figure 5 Global real direct premium growth, 1980 –2015

Figure 6 Global real premium growth rates, 2015

Insurance premium growth steady

No data < –10.0%

–10.0% to –5.0%–5.0% to –2.5%–2.5% to 0.0%

0.0% to 2.5%2.5% to 5.0%5.0% to 10.0%

> 10.0%

Swiss Re sigma No 3/2016 9

Life insurance: positive overall growth masks regional disparities

Premium developmentGlobal direct life premiums written totalled USD 2 534 billion in 2015, down 4.6% in nominal terms but up 4.0% in real terms after a 4.3%-real gain in 2014. In the last two years, global life premium growth has exceeded both the pre- and post-crisis averages (see Figure 7). However, the overall growth masks considerable variation across regions and countries. Last year premium growth in the advanced markets slowed, but accelerated in the emerging markets.

Middle East and Central Asia

Latin America and the Caribbean

Emerging AsiaEmerging Asia excl. China

Emerging markets excl. ChinaEmerging markets

OceaniaAdvanced Asia

Western EuropeNorth America

Advanced markets

World

Central and Eastern Europe

Post-crisis average growth 2009–2014Pre-crisis average growth 2003–2007Growth rate 2015

Africa

–10% –5% 0% 5% 10% 15% 20%

Source: Swiss Re Economic Research & Consulting.

In the advanced markets, premiums recovered in North America following two years of contraction. There was also renewed momentum in Japan. In Oceania, however, markets declined sharply, mainly due to base effects after very solid growth in Australia in 2014. There was minimal growth in Western Europe, mainly due to a contraction in Germany. Among the emerging markets, growth was particularly strong in emerging Asia, supported by solid gains in a number of countries including China, India, Indonesia and the Philippines. Life premium growth also strengthened in Latin America and remained on a positive track in Africa, the Middle East and Central Asia. The improvement in Latin America reflects robust growth in Brazil and a strong rebound in Chile. By contrast, premiums in CEE were down for a third year running, mainly because of the two largest markets, Poland and the Czech Republic (see page 32).

Despite the above-average growth rates in 2014 and 2015, life insurance premiums have been sluggish since the financial crisis in 2008. On average, advanced-market premiums have stagnated since then, with very little and even negative life premium growth in Western Europe and North America. The emerging markets have also slowed markedly, with premium growth less than half pre-crisis levels.

Global life insurance premiums rose by 4.0% in 2015, slightly slower than in the previous year.

Figure 7 Life premium growth in the advanced and emerging markets in 2015, and pre- and post-financial crisis averages

Premium growth in the advanced markets slowed; it accelerated in the emerging markets.

Despite signs of recovery of late, overall life premium growth has been sluggish since the financial crisis.

10 Swiss Re sigma No 3/2016

Insurance premium growth steady

Source: Swiss Re Economic Research & Consulting.

Life insurers’ profitability and capital positionGlobal life industry profitability remained under pressure in 2015, with return on equity (ROE) at about 12% (see Figure 9). ROE is expected to remain below pre-crisis levels in the near- and medium term. Ongoing headwinds are the moderate premium growth in many markets and prolonged low interest rates. In some countries bond yields are even negative. Insurers from Canada and Western Europe in particular contributed to the weak year-on-year (yoy) ROE outcome in the fourth quarter of 2015. Among US insurers, most of the improvement in average ROE was because of an increase in the net income of one company due to positive forex developments. From an accounting perspective, the life sector reported stronger capitalization at the end of 2015 than in 2014, reflecting solid results in China. However, the improvement was also partly driven by decreasing interest rates, leading to a higher mark-to-market value of fixed-income and derivative investments.

Figure 8 Life real premium growth, 2015

Profitability in the life sector remains under pressure. However, the industry is well capitalised.

No data < –10.0%

–10.0% to –5.0%–5.0% to –2.5%–2.5% to 0.0%

0.0% to 2.5%2.5% to 5.0%5.0% to 10.0%

> 10.0%

Swiss Re sigma No 3/2016 11

5075

100

150125

175200

250225

300275

325 (4Q07 = 100)

Market cap weighted average2 Chinese companies10 US companies 6 UK companies7 European Globals3 Canadian companies

4Q

15

2Q

14

4Q

13

2Q

13

2Q

15

4Q

14

4Q

12

2Q

12

4Q

11

2Q

11

4Q

10

2Q

10

4Q

09

2Q

09

4Q

08

2Q

08

4Q

07

2Q

14

4Q

13

2Q

13

2Q

15

4Q

14

4Q

12

2Q

12

4Q

11

2Q

11

4Q

10

2Q

10

4Q

09

2Q

09

4Q

08

2Q

08

4Q

07

4Q

15–10%

–5%

0%

5%

10%

15%

20%

25%

Note: Based on a sample of companies7, missing 1Q/3Q values are interpolated.

Sources: Company reports, Bloomberg, Swiss Re Economic Research & Consulting.

Life insurance industry outlookLife premiums are expected to grow in both the advanced and emerging markets in 2016. Growth is forecast to accelerate slightly in the advanced but decelerate in the emerging countries. The small improvement in the advanced markets will come from an expected recovery in Oceania and modest acceleration in Western Europe. In North America, growth will remain roughly stable. In the emerging markets, the pace of growth reflects sustained strong performance in emerging Asia. Premium growth in China, though slowing, is expected to remain strong in 2016. The fast-growing sharia compliant/takaful business in Indonesia and Malaysia is expected to further benefit the life sector. In contrast, growth in Latin America will remain below recent trend levels due to price competition, demand weakness and heightened financial and economic volatility. Life premiums will also remain under pressure in most CEE EU countries, and are expected to decline in Russia due to the ongoing economic difficulties there. In Africa, life insurance penetration is still very low, so there is ample potential for growth.

Interest rates and the macroeconomic and financial market environment will continue to shape the outlook for the primary life insurance industry. Downside risks from just modest global economic growth, persistently low interest rates, volatility in the financial markets and regulatory changes remain significant in the short- and medium-term. With profitability under pressure, life insurers will continue to focus on improving capital management, lowering expenses and enhancing investment yields.

7 AFLAC; Allianz; Assurant Inc; Aviva; AXA; China Life; CNP; Generali; Genworth Financial; Great-West Lifeco; Hartford; Legal & General; Lincoln National; Manulife; MetLife Group; Old Mutual; Ping An; Prudential (UK); Prudential (US); St. James Place ; StanCorp Financial Group; Standard Life; Storebrand ASA; Sun Life; Swiss Life; Torchmark; UNUM Group; Zurich.

Figure 9 Return on equity (left panel) and shareholder equity (right) of large life insurers and globals with life business

Life premiums will likely grow in the advanced and emerging markets in 2016 …

… although the overall environment will remain challenging.

12 Swiss Re sigma No 3/2016

Insurance premium growth steady

Non-life: higher premium growth, driven by advanced markets

Non-life insurance premium developmentGlobal non-life insurance sector improved further in 2015, with premiums up 3.6% in real terms to USD 2 020 billion, higher than the 2.4%-gain registered in 2014 and also better than pre-crisis average growth (see Figure 10). However, in nominal USD terms, premiums fell 3.8% due to currency depreciations against the dollar. The advanced markets were the main drivers, with higher growth registered in all regions except Oceania (flat at +0.1%). Advanced Asia (+4.1%) registered the highest growth among the advanced regions and premiums in North America were also solid (+3.2%). Western Europe premiums showed moderate growth (+1.5%) after several years of stagnation.

Source: Swiss Re Economic Research & Consulting.

In the emerging markets, premium growth slowed to a still-robust 7.8% in 2015 from 8.6% in 2014, but was below the pre-crisis average of 10%. Growth trends among regions were mixed. China was the main driver, with premiums there increasing by 17%. In the Middle East and Central Asia, growth remained solid at 9%, and likewise in emerging Asia excluding China at 5.9%. However, in most regions the level of premium growth was lower than in 2014. Growth was slow in Africa (+1.3%) and Latin America (+2.3%). This was still higher than in CEE where premiums were down 4.9%, with sharp contractions in Russia and the Ukraine offsetting more positive results in other countries.

Global non-life premium growth improved further in 2015, mainly driven by advanced markets.

Figure 10 Non-life premiums growth in the advanced and emerging markets in 2015, pre- and post-financial crisis averages

Middle East and Central Asia

Latin America and the Caribbean

Emerging AsiaEmerging Asia excl. China

Emerging markets excl. ChinaEmerging markets

OceaniaAdvanced Asia

Western EuropeNorth America

Advanced markets

World

Central and Eastern Europe

Africa

Post-crisis average growth 2009–2014Pre-crisis average growth 2003–2007Growth rate 2015

–6% –3% 0% 3% 6% 9% 12% 15%

Emerging market premiums growth slowed but remained solid.

Swiss Re sigma No 3/2016 13

Source: Swiss Re Economic Research & Consulting.

Catastrophe losses8

There were 353 disaster events in 2015, of which a record 198 were natural catastrophes, the highest number ever recorded in a single year. Total economic losses caused by all disasters were estimated at USD 92 billion in 2015, down from USD 113 billion in 2014 and below the inflation-adjusted average of USD 192 billion for the previous 10 years. Asia was hardest hit with total losses of USD 38 billion. An earthquake in Nepal was the biggest disaster of the year, with total losses estimated at USD 6 billion, including damage reported in India, China and Bangladesh. The biggest insured-loss event of the year was the two explosions at the Port of Tianjin in China in August, with an estimated property loss of USD 2.5 billion to USD 3.5 billion, making it also Asia’s largest man-made insured loss event ever.

Overall, the insurance sector covered USD 28 billion of losses from natural catastrophes and USD 9 billion from man-made disasters in 2015. However, there was a large difference of USD 55 billion between total and insured losses, highlighting the lack of insurance protection globally against catastrophe events.

8 sigma 1/2016 – Natural catastrophes and man-made disasters in 2015: Asia suffers substantial losses, Swiss Re.

Figure 11 Non-life real premium growth, 2015

Losses from disaster events in 2015 were below the previous 10-year average.

Irrespective, there was still a large global catastrophe protection gap of USD 55 billion.

No data < –10.0%

–10.0% to –5.0%–5.0% to –2.5%–2.5% to 0.0%

0.0% to 2.5%2.5% to 5.0%5.0% to 10.0%

> 10.0%

14 Swiss Re sigma No 3/2016

Non-life insurers’ profitability and capital positionThe overall profitability of non-life insurance, measured by ROE, declined from 9.0% in 2014 to 7.2% in 2015. Underwriting and investment results both declined. Investment income as a percentage of net premiums earned in eight major markets fell by 0.7 ppt to 9.2% in 2015 (see Figure 12) due to the low interest rate environment. Underwriting results were also down as the pace of reserve releases slowed. Overall, underwriting profitability in the eight markets deteriorated with the combined ratio moving up to 98.9% in 2015 from 97.6% in 2014. In the US, the industry combined ratio worsened due to rising claims in motor and general liability insurance. In the UK and continental Europe, motor underwriting results started to deteriorate again after some improvements previously. In Japan, overall underwriting results improved across all lines, but the combined ratio in the compulsory motor line remained high. Underwriting performance in Australia, however, deteriorated due largely to poor results in property offsetting improvements in compulsory motor. The overall negative trend in profitability is expected to continue in 2016.

Source: Swiss Re Economic Research & Consulting.

The non-life sector remains well capitalised with solvency at a record high of 130% in 2015, up from 124% in 2014. Nevertheless, shareholder equity in the eight markets declined marginally in USD terms due to negative currency effects as the USD strengthened. On a local currency basis, shareholder equity increased. Although capitalisation is expected to remain strong, the support from higher unrealised gains due to ultra-low interest rates will disappear once rates begin to rise (in the US and UK mainly).

Non-life profitability weakened in 2015 due to low investment returns and weaker underwriting results.

Figure 12 Composition of profits as a % of net premiums earned and ROE, aggregate of eight major markets, 1999–2016

–15%

–10%

–5%

0%

5%

10%

15%

Aggregate of the US, Canada, the UK, Germany, France, Italy, Japan and Australia

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

E

20

16

F

20%

After-tax return on equity (%)Capital gains/losses as a % of net premiums earnedCurrent investment income as a % of net premiums earnedUnderwriting result as a % of net premiums earned E = estimate

F = forecast

The non-life industry is well capitalized.

Insurance premium growth steady

Swiss Re sigma No 3/2016 15

Source: Swiss Re Economic Research & Consulting.

Non-life insurance industry outlookGlobal non-life sector growth is expected to weaken due to moderate economic activity and soft pricing, mainly in the advanced markets. In North America, premium growth is expected to slow slightly in 2016 because of price declines in most commercial lines. In Western Europe, non-life premium growth will remain subdued due to moderate economic recovery. In advanced Asia, a weakening economic environment will pose challenges to most of the non-life sector, but some lines are expected to grow (eg, accident & health, due to increasing awareness and product re-pricing). The non-life sector in Oceania will likely be affected by pricing pressures and also regulatory changes (see page 27).

The outlook for emerging markets is mixed. Emerging Asia is forecast to grow robustly, mainly driven by China because of government support for insurance. Further backing will come from rate hikes in motor third-party liability (MTPL) insurance in India and infrastructure investments in other Asian markets. However, detariffication of motor in China and Malaysia could offset some of the positive momentum in the region. Non-life premiums in Africa and the Middle East and Central Asia will continue to grow but at a lower rate than before. In Latin America, growth is expected to be flat due to contraction in Brazil and Venezuela, and slower growth in Argentina. In CEE, non-life premiums are expected to decline further due to contraction in Russia, where the economy remains stuck in recession.

Non-life insurers’ profitability is expected to continue to be under pressure as investment returns remain depressed and soft market conditions continue.

Figure 13 Non-life insurers’ solvency, 1999–2016

USD bn Aggregate of the US, Canada, the UK, Germany, France, Italy, Japan and Australia

0

200

400

600

800

1000

1200

1400

2015

E

2016

F

2014

2013

2012

2011

2010

200

9

200

8

2007

200

6

200

5

200

4

200

3

200

2

2001

200

0

199

9

0%

20%

40%

60%

80%

100%

120%

140%

Shareholders' equityPremiums earned E = estimate

F = forecast

Solvency (equity/premiums – RHS)

Lower premium rates and weak economic growth will drag on non-life premium development in advanced markets.

Growth in Emerging Asia will remain strong, mainly driven by China.

Overall non-life sector profitability will remain subdued.

16 Swiss Re sigma No 3/2016

Introduction

Trade data of the last 150 years tell a straightforward story: excluding periods of recession, and during and between World Wars I and II, growth in global trade volumes mostly exceeded growth in global real GDP.9 The outperformance was most pronounced from the late 1980s to mid-2000s, with trade volumes growing about twice as fast as real GDP.10 This was reflected by an increase in exports as a share of GDP from below 15% to more than 30% during that time (Figure 14).

The gains were based on a series of major geo-political and economic events: the end of the Cold War and reintegration of the CEE countries into the world economy; the adoption of an export-led growth model in China and its integration into global business; the Uruguay Round trade negotiations between 1986 and 1994, leading to the creation of the World Trade Organisation (WTO) and a reduction in average tariffs; rapid innovation in information and communications technology; and ongoing improvements in transport efficiency. Optimisation of production processes with more outsourcing of specific functions over time led to a rise in global supply chains.

Grey bars indicate global recessions, equalized with global real GDP growth below 1%; the dashed line shows the pre-crisis trends according to the average growth rates between 1990 and 2007.

Source: World Bank, Swiss Re Economic Research & Consulting.

There has been a slowdown in global trade in more recent years. This appears more pronounced in nominal terms than in real terms because: USD appreciation: national values need to be converted to a common currency,

typically the USD. A stronger USD reduces the value of exports denominated in other currencies, even if prices in local currency terms and volumes increase. The same applies to world GDP. However, as the US accounts for a smaller share of world trade than it does for world GDP, converting local currencies to USD to aggregate nominal trade and GDP causes the ratio between the two variables to decline as the USD appreciates.

Falling commodity and manufacturing prices in recent years have led to lower export prices (see Figure 15). Commodities and manufactured goods account for a larger share of trade than they do for global output. Decreasing commodity and manufacturing prices therefore have a larger negative effect on nominal exports than on nominal GDP, causing the ratio between the two variables to decline.

9 D. Irwin, “Long-run trends in world trade and income”, World Trade Review, 1(1) 2002, pp. 89–100.10 C. Constantinescu, A. Mattoo and M. Ruta, “The Global Trade Slowdown; Cyclical or Structural?”,

IMF Working Papers, 15(6), 2015.

Trade volumes grew about twice as fast as global output in the two decades prior to 2007 …

… driven by major geo-political and economic events.

Figure 14 Development of global exports relative to global GDP

0.10

0.15

0.20

0.25

0.30

0.35

0.40

Exports to GDP (nominal)

Exports to GDP (real)

2015

2010

200

5

200

0

199

5

199

0

198

5

198

0

1975

1970

Pre-crisis trend (real) RecessionsExports to GDP (real) Exports to GDP (nominal)

However, trade has grown in line with GDP in more recent years.

Global trade and insurance market growth

Swiss Re sigma No 3/2016 17

Source: CPB Netherlands Bureau for Economic Policy Analysis, Swiss Re Economic Research & Consulting.

USD aggregation effects overstate the magnitude of the recent slowdown in trade, but it is also visible in real terms. This raises the question of whether the trade slowdown is cyclical or reflects a structural change in the world economy. And, if the latter, how will the decrease in the trade-to-GDP growth ratio impact global economic growth?

Determinants of the slowdown

Cyclical factorsTrade volumes normally respond more than proportionally to movements in real GDP. Irwin11 explains this by citing that demand for investment and durable consumer goods is cyclical, growing rapidly in times of strong economic performance. As these goods represent a large share of global trade volumes, recent weakness in global growth is likely having a negative impact on the trade-to-GDP ratio.

The regional composition of world growth is also important. In particular, sluggish growth in the EU in recent years has had a disproportionally large impact on global trade volumes: the EU accounts for less than one quarter of global output, but for more than one third of global trade. The substantial trade flows between EU member states are included as part of global trade statistics. However, trade within large countries (eg, the US or China) is not included.

Another cyclical factor in the trade-volume slowdown since 2007 is that economic growth in many emerging markets has been weak relative to the previous two decades. Geopolitical tensions, exchange rate fluctuations, and the holding off of investments because of an uncertain outlook has also contributed to lower flows.

11 Irwin, op. cit.

Figure 15 Global manufacturing and export price indices (2005=100)

Export price index

Manufacturing price index

2016

2014

2012

2010

200

8

200

6

200

4

200

2

200

0

199

8

199

6

199

4

1992

Manufacturing price indexExport price index

70

80

90

100

110

120

130

140

This raises questions regarding the outlook of the global trade-to-GDP ratio.

During recession, the purchase of traded goods is often postponed, resulting in high sensitivity of trade volumes to GDP moves.

Intra-EU trade matters disproportionally for global trade, and EU GDP growth has been weak for the last several years.

Cyclical factors explain some of the recent slowdown.

18 Swiss Re sigma No 3/2016

Source: WTO, Swiss Re Economic Research & Consulting.

Structural factorsThe recent slowdown in trade relative to GDP growth results from sluggishness in trade of goods, in particular in manufacturing, fuel and mining products. By contrast trade in services is still growing at a much higher rate than global GDP. However, as Figure 16 shows, services still account only for about one fifth of global trade. The slowdown in global trade, therefore, is about structural changes in the production and trade of goods rather than services.

The rapid expansion of international production networks/supply chains is an important factor in explaining the outperformance of trade relative to income growth in the two decades prior to 2007.12 Trade is measured on a gross value basis. If a good which consists to a large part of imported intermediate goods is exported, the imported intermediate goods are recorded again in a country’s exports. In contrast, GDP only measures the value added in the exporter country. Hence, in the years before 2007, the rise of global value chains led to a large increase in the trade-to-GDP ratio.

According to theory, the fundamental trade-off in supply chain dispersion is between specialisation gains and coordination costs.13 The revolution in information and communication technology radically lowered coordination costs in the 1990s and early 2000s. However, the recent slowdown in offshore activities indicates that a further substantial reduction in communication costs might be hard to achieve. In addition, narrowing wage gaps between countries like China and advanced economies could lower specialisation gains. Constantinescu et al.14 find evidence that the slowing pace of international vertical specialization might be another structural change affecting the trade-to-income relationship. The ECB supports this finding by presenting evidence from the World Input-Output Database. The share of foreign value added in gross exports increased until 2008, and has remained broadly unchanged since 2009. High wages in some emerging markets appear to be reducing dependence on foreign supply chains as manufacturers shift production back to their home country.

12 G. Gaulier, G. Santoni, D. Taglioni et al., “The power of a few in determining trade acceleration and slowdowns” in B. Hoekman (ed). The Global Trade Slowdown: A New Normal?, VoxEU Book, 2015.

13 R. Baldwin, “Global supply chains: Why they emerged, why they matter, and where they are going”, CEPR Discussion Papers, vol 9103, 2012.

14 C. Constantinescu, A. Mattoo and M. Ruta, op. cit.

Figure 16 Global exports in USD trillion

19

80

19

82

19

84

19

86

19

88

19

90

19

92

19

94

19

96

19

98

20

00

20

02

20

04

20

06

20

08

20

10

20

12

20

14

ManufacturesFuels and miningAgricultureServices exports

0

5

10

15

20

25

The slowdown in global trade is based on sluggishness in trade of goods. Trade in services continues to exceed income growth.

The expansion of international supply chains was an important driver of global trade in the two decades prior to the mid-2000s.

Offshoring is a trade-off between specialisation gains and coordination costs.

Global trade and insurance market growth

Swiss Re sigma No 3/2016 19

There is a general consensus that developments in China have contributed to both the large increase in the trade-to-income ratio in the high-trade growth period prior to 2007, and also to the ratio’s decline during the trade slowdown of more recent years.15 Prior to the mid-2000s, China’s export-led growth model was a main driver of global trade volumes. Moreover, Gaulier et al.16 argue that China’s economic integration also had a “juggernaut effect” on trade liberalisation in Southeast Asian countries – ie, a virtuous cycle in which trade liberalisation strengthens the export sector, which in turn lobbies for further trade liberalisation. With China’s transition from an export- and investment-led to a more consumption and service-based growth model, a large driver of global trade growth has diminished. The rebalanced Chinese economy with a higher emphasis on growth in the less trade-intensive service sector and domestic consumption will contribute less to global trade. Further, Constantinescu et al.17 state that the share of Chinese imports of parts and components in its total exports has declined from a peak of 55% in the mid-1990s to around 35% currently. China’s increasing ability to source from itself has contributed to the sluggish development of the global trade-to-GDP ratio in recent years.

Source: World Bank, Swiss Re Economic Research & Consulting.

The ECB claims that protectionism may be playing “a small but non-negligible role” in the most recent trade slowdown.18 However, even a stagnating level of trade liberalisation would not drive the trade-to-GDP ratio higher. Figure 17 shows the average import tariffs in percentage points for different regions since the early 1990s. During this period in which global trade volumes grew twice as fast as output, average tariffs across the world fell significantly. Average tariffs levelled off at low levels in the years after the financial crisis, and any further declines may only have a marginal impact. The stagnation in liberalization initiatives since the mid-2000s may have also slowed trade growth relative to output.

Future prospects and implications for growth

There is no agreement on the relative importance of cyclical versus structural factors in trade growth, but there is strong evidence that both are at play. Among others, Boz et al.19 argue that on balance, cyclical forces have been more important. However, Gaulier et al.20 and others argue that structural changes were responsible for a significant part of the recent slowdown. Global trade should pick up again once global economic activity accelerates, but is unlikely to return to double-GDP-growth

15 Ibid.16 G. Gaulier, G. Santoni, D. Taglioni, op. cit.17 C. Constantinescu, A. Mattoo and M. Ruta, op. cit.18 “Understanding the weakness in world trade”, ECB Economic Bulletin, vol 3, 2015.19 E. Boz, M. Bussière and C. Marsilli, “Recent slowdown in global trade: Cyclical or structural?”,

in B. Hoekman (ed.) The Global Trade Slowdown: A New Normal?, VoxEU Book, 2015.20 G. Gaulier, G. Santoni, D. Taglioni, op. cit.

An important structural factor is China’s transition from an export-led to a consumption driven growth model, and the declining import content of its exports.

Figure 17 Average import tariffs for different regions, in %

2011

200

9

2007

200

5

200

3

2001

199

9

1997

199

5

1993

1991

2013

Middle East AsiaNorth America EuropeWorld

0

2

4

6

8

10

12

16

14

Large trade liberalization deals supported the increase in the trade-to-income ratio during the 1990s and early 2000s, but there have been few notable agreements recently.

In coming years, trade will most likely not increase twice as fast as GDP.

20 Swiss Re sigma No 3/2016

Global trade and insurance market growth

rates. Changes in underlying factors causing the recent decline of the trade-to-GDP ratio are likely to persist: China’s transition to a more consumption and service-driven growth model will proceed, and gains from further international dispersion of production networks may have peaked.

It is unclear whether protectionism or trade liberalization measures will gain the upper hand in the years to come. The Trans-Pacific Partnership (TPP) reached agreement in October 2015, but the accord still needs to be signed and ratified by participating countries. It should positively affect the trade-to-GDP ratio, although estimates on the potential impact on trade volumes and economic growth vary greatly. A proposed Transatlantic Trade and Investment Partnership (TTIP) between the US and the EU is still being negotiated. When and in what form the agreement will come into force is uncertain.

No current academic literature explicitly investigates the impact of the recent global trade slowdown on global growth. But there is a large body of literature linking increases in productivity to trade in general, and to various aspects of dispersing the global value chain in particular.21 This material says a stagnating or decreasing trade-to-GDP ratio may have a negative effect on global growth as trade is a channel for knowledge transfer and diffusion of technologies, as well as for specialization and resource allocation according to the theory of comparative advantage.

Implications for insurance

Premium rates tend to be cyclical, and are the most important determinant of marine and credit insurance premiums in the short run. However, over the longer term, premiums are mostly determined by the level of insurance exposure. A persistent slowdown in global exports would directly lower exposure growth and would therefore have a negative impact on marine and credit insurance premiums.

Source: IMF World Economic Outlook, Swiss Re Economic Research & Consulting.

Marine insurance22 Data from the last two decades reveals that an increase of trade activity by 1% eventually leads to an increase in cargo premiums of slightly below 0.9%, and to an increase in hull premiums of about 0.8%. Over the last 20 years, this long-run response of premiums to the value of traded goods has tended to be below 1.0. The reason might be found by commercial pressures in the shipping industry. Credit availability and overly optimistic trade growth projections led to substantially increased orders for new ships from 2004 to 2008. The overhang of shipping capacity and resulting weak prices in maritime freight markets put pressure on premium rates. Also, safety may be rising, lowering the risk and the premium rates.

While cargo premiums can be directly linked to the value of traded goods, trade only indirectly affects hull premiums through the assumption that the global value of ships is connected to the total value of its cargo. The excess supply of shipping capacity

21 See M. Amiti and J. Konings, “Trade Liberalization, Intermediate Inputs, and Productivity: Evidence from Indonesia”, American Economic Review, vol 97, no 5 2007, pp 1611–1638. Also P. K. Goldberg, A. K. Khandelwal, N. Pavcnik et al., “Imported Intermediate Inputs and Domestic Product Growth: Evidence from India”, Quarterly Journal of Economics, vol 125, no 4 2010, pp 1727–1767, and G. M. Grossman and E. Rossi-Hansberg, “Trading Tasks: A Simple Theory of Offshoring.” American Economic Review, vol 98, no 5 2008, pp 1978–97.

22 The econometric analyses in this chapter follows the methodology used in sigma 4/2013: Navigating recent developments in marine and airline insurance, Swiss Re.

TPP and TTIP might be a source for a renewed boost to the trade-to-GDP ratio.

Weak global trade growth will likely dampen global economic growth.

Rates determine marine insurance premiums in the short run. Trade activities are the main determinant of premiums in the long run.

Table 1 Scenarios for the development of marine premiums over the next 10 years

Long-run response of premiums to trade

Average real GDP growth forecast over the next 10 years

Projected average real premium growth if trade:

grows in tandem with real GDP

grows twice as fast as real GDP

Cargo 0.892.8%

2.5% 5.0%Hull 0.80 2.2% 4.4%

Rising trade activity increases cargo and hull premiums, but not by as much as the increase in trade.

A trend towards larger ships has kept average hull premium below cargo premium growth rates.

Swiss Re sigma No 3/2016 21

led to a decrease in ships’ market value. This and a trend towards larger ships, carrying more cargo for less cost, might also explain the lower long-run response of hull premiums to trade relative to cargo premiums.

Using an external forecast for global real GDP growth, Table 1 presents two scenarios for average real growth rates of cargo and hull premiums over the next 10 years: an upside scenario in which trade is assumed to grow twice as fast as GDP as during the period between 1990 and 2007; and a downside scenario in which trade is assumed to grow at the same pace as global GDP. From these scenarios, cargo premiums are forecast to grow on average by between 2.5% and 5%, and hull premiums by between 2.2% and 4.4%. While short-run prospects of marine premiums are mainly driven by the development of premium rates, long run prospects are highly dependent on the future development of the trade-to-GDP ratio.

Trade credit insurance23 Using historical data from 40 countries, an evaluation was conducted of the effect of exports on trade credit insurance premiums. The analysis estimates that a 1% increase in exports is accompanied by a 0.67% increase in trade credit insurance premiums. Trade credit insurance protects sellers of products and services against the risk of non-payment by the buyer. Since this also includes domestic buyers, export data only capture a part of the exposure to non-payment. The rest of the exposure depends on the development of the economic activity within a country, which in turn also affects trade. After controlling for these effects (ie, keeping the level of global economic activity constant), the analysis shows that a 1% increase of trade results in a just 0.32% increase in trade credit insurance premiums. However, that is still significant. Moreover, as with the analysis on the impact of trade on marine lines, the estimates do not account for a possible negative impact of a global trade slowdown on economic activity.

ConclusionThe long-run prospects of marine and trade credit insurance lines are significantly affected by the development of the trade-to-GDP ratio. This ratio should pick up in the coming years as the global economy recovers. However, the recent slowdown in trade growth also reflects, to a certain extent, permanent structural changes in the global economy. Most of the mentioned factors are likely to persist, pointing to more modest development of marine and trade credit insurance premiums than would have been expected several years ago using only real GDP growth rates.

23 For an economic analysis of the trade credit insurance market, see Trade credit insurance & surety: taking stock after the financial crisis, October 2014, Swiss Re.

Long-run premium growth forecasts are highly dependent on the future path of trade-to-GDP ratio.

Higher exports typically lead to an increase in trade credit insurance premiums.

Over the next decade, marine and trade credit insurance premiums are likely to develop more modestly than previously.

22 Swiss Re sigma No 3/2016

Global share of advanced markets declined to 81.3% in 2015

Total premiums in the advanced markets grew by 2.5% in 2015, little changed from the previous year. In nominal USD terms, however, premiums declined by 5.7% to USD 3 704 billion due to widespread exchange rate depreciation, particularly in the euro zone, Australia and Canada. Exchange rate weakness against a resilient Chinese renminbi also contributed to the decline in the advanced markets’ share of global insurance premiums to 81.3% (2014: 82.6%).

Life insuranceTotal life premiums in the advanced markets grew by 2.5% in 2015, outpacing GDP growth slightly and increasing insurance penetration marginally (premiums/GDP). In 17 of the 28 markets for which data are available (see Figure 18 in which the blue dots above the line indicate premium growth above GDP growth), life premiums growth outpaced economic growth.

Source: Swiss Re Economic Research & Consulting.

Non-life insuranceIn non-life, total premiums in the advanced markets grew by 2.6% in 2015, also more than the overall economy. Premium growth was stronger than GDP growth in 16 of the 28 markets with data.

Advanced countries continued to lose global insurance market share in 2015 due to exchange rate depreciation.

Life insurance premiums grew slightly faster than the economy, …

Figure 18 Life and non-life premium growth versus GDP growth in the advanced markets, 2015

Rea

l pre

miu

m g

row

th 2

015

Real GDP growth 2015

Non-life insuranceLife insurance

Netherlands

Portugal

Portugal

Greece

Finland

Singapore

Luxembourg

Hong Kong Sweden

Spain

Australia

GDP growth equal to premium growth

–20%

–15%

–10%

–5%

5%

0%

10%

15%

20%

–0.5% 0% 0.5% 1.5% 2.5% 3.5% 4.5%

… as did non-life premiums.

Advanced market premiums grow faster than GDP

Swiss Re sigma No 3/2016 23

Insurance penetration and densityIn 2015, average per capita spending on insurance in advanced markets was USD 3440, down almost 6% from the previous year due primarily to exchange rate movements. Per capita spending on life insurance was USD 1954 and in non-life it was USD 1486. Penetration remained at the same level since it is unaffected by exchange rate movements.

GreeceCyprus

MaltaIceland

SpainPortugal

IsraelNew Zealand

AustriaGermany

ItalyBelgium

EU, 15 countriesAustralia

South KoreaCanadaFrance

SwedenAverage

JapanNorway

G7Singapore

IrelandTaiwan

United StatesUnited Kingdom

NetherlandsDenmark

FinlandLuxembourg

Hong KongSwitzerland

0 1000 2000 3000 8000

0% 20%15%10%5%

700050004000 6000

Premiums as a % of GDP

Total insurance penetration (lower axis)Non-life premiums per capita

Premiums in USD

Life premiums per capita

Source: Swiss Re Economic Research & Consulting.

Per capita spending on insurance in advanced markets decreased in 2015.

Figure 19 Insurance density and penetration in advanced markets, 2015

24 Swiss Re sigma No 3/2016

North America: life premiums rebound, non-life growth strengthens

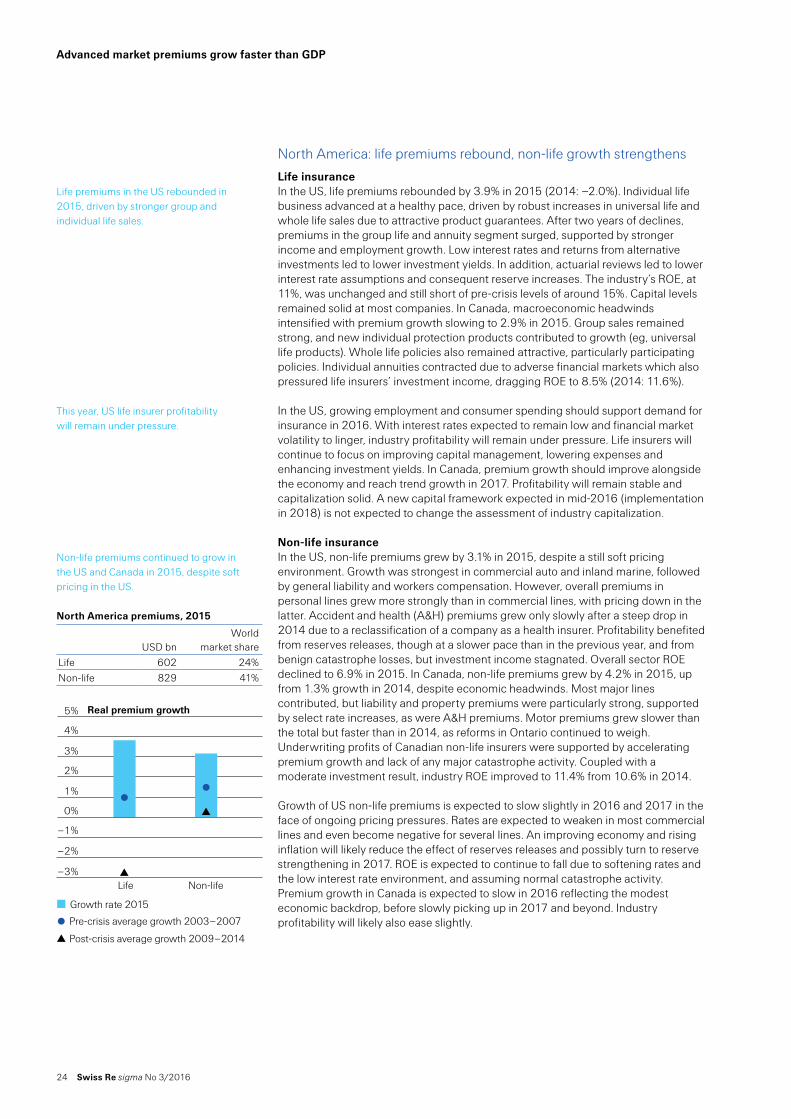

Life insuranceIn the US, life premiums rebounded by 3.9% in 2015 (2014: –2.0%). Individual life business advanced at a healthy pace, driven by robust increases in universal life and whole life sales due to attractive product guarantees. After two years of declines, premiums in the group life and annuity segment surged, supported by stronger income and employment growth. Low interest rates and returns from alternative investments led to lower investment yields. In addition, actuarial reviews led to lower interest rate assumptions and consequent reserve increases. The industry’s ROE, at 11%, was unchanged and still short of pre-crisis levels of around 15%. Capital levels remained solid at most companies. In Canada, macroeconomic headwinds intensified with premium growth slowing to 2.9% in 2015. Group sales remained strong, and new individual protection products contributed to growth (eg, universal life products). Whole life policies also remained attractive, particularly participating policies. Individual annuities contracted due to adverse financial markets which also pressured life insurers’ investment income, dragging ROE to 8.5% (2014: 11.6%).

In the US, growing employment and consumer spending should support demand for insurance in 2016. With interest rates expected to remain low and financial market volatility to linger, industry profitability will remain under pressure. Life insurers will continue to focus on improving capital management, lowering expenses and enhancing investment yields. In Canada, premium growth should improve alongside the economy and reach trend growth in 2017. Profitability will remain stable and capitalization solid. A new capital framework expected in mid-2016 (implementation in 2018) is not expected to change the assessment of industry capitalization.

Non-life insuranceIn the US, non-life premiums grew by 3.1% in 2015, despite a still soft pricing environment. Growth was strongest in commercial auto and inland marine, followed by general liability and workers compensation. However, overall premiums in personal lines grew more strongly than in commercial lines, with pricing down in the latter. Accident and health (A&H) premiums grew only slowly after a steep drop in 2014 due to a reclassification of a company as a health insurer. Profitability benefited from reserves releases, though at a slower pace than in the previous year, and from benign catastrophe losses, but investment income stagnated. Overall sector ROE declined to 6.9% in 2015. In Canada, non-life premiums grew by 4.2% in 2015, up from 1.3% growth in 2014, despite economic headwinds. Most major lines contributed, but liability and property premiums were particularly strong, supported by select rate increases, as were A&H premiums. Motor premiums grew slower than the total but faster than in 2014, as reforms in Ontario continued to weigh. Underwriting profits of Canadian non-life insurers were supported by accelerating premium growth and lack of any major catastrophe activity. Coupled with a moderate investment result, industry ROE improved to 11.4% from 10.6% in 2014.

Growth of US non-life premiums is expected to slow slightly in 2016 and 2017 in the face of ongoing pricing pressures. Rates are expected to weaken in most commercial lines and even become negative for several lines. An improving economy and rising inflation will likely reduce the effect of reserves releases and possibly turn to reserve strengthening in 2017. ROE is expected to continue to fall due to softening rates and the low interest rate environment, and assuming normal catastrophe activity. Premium growth in Canada is expected to slow in 2016 reflecting the modest economic backdrop, before slowly picking up in 2017 and beyond. Industry profitability will likely also ease slightly.

Life premiums in the US rebounded in 2015, driven by stronger group and individual life sales.

This year, US life insurer profitability will remain under pressure.

Non-life premiums continued to grow in the US and Canada in 2015, despite soft pricing in the US.

Advanced market premiums grow faster than GDP

North America premiums, 2015

USD bn

World market share

Life 602 24%Non-life 829 41%

Real premium growth

Growth rate 2015

Life Non-life

Pre-crisis average growth 2003–2007

Post-crisis average growth 2009–2014

5%

4%

3%

2%

1%

0%

–1%

–2%

–3%

Swiss Re sigma No 3/2016 25

Western Europe: life premiums slow, non-life returns to growth

Life insuranceIn Western Europe, growth in life insurance premiums slowed to 1.3% in 2015 from 5.8% in 2014. This was largely due to contraction in Germany (–2.5%), where new business fell in both regular (–3%) and single premiums (–8.8%). The UK life market returned to positive growth (+2.4%), after two years of premium declines. In particular, sales of investment and savings business is growing again. Premiums in France grew by 2.9%. In Italy growth flattened after two years of strong growth as sales of endowments slowed. A sharp decline (–18%) in premium income in Portugal reversed some of the strong growth of the previous two years. The market in Spain grew by +3.4%, mainly driven by traditional life and death benefit protection products. Unit-linked business continued to contract. Among the Benelux countries, the biggest premium decline (–11%) was in Luxembourg where a volatile growth pattern from the past few years continued. The confidence crisis in the Dutch market because of mis-selling continued for a fourth year running, with premiums down 8.7%. In Belgium, life premiums were down 4.9% in 2015. The Nordic markets grew by 5.9% (Sweden), 7.6% (Finland), and 2.2% (Denmark). The ROE of a sample seven European Globals24 decreased to 8.6% from 9.8% in 2014 indicating a lower profitability. ROE for a sample of 6 UK companies was 20%.25

The short-term outlook for the life industry in Western Europe is bleak, in part due to the pending UK referendum on EU membership. Given that it is the largest market in Western Europe, the outcome of the vote could have significant implications for the UK market itself. More generally, the low interest rate environment will continue to constrain demand for life insurance as well as sector profitability. On the other hand, the aging population in Western Europe should generate increased demand for protection, savings and retirement products in the longer term.

Non-life insuranceNon-life premium growth in Western Europe was a moderate 1.5% in 2015, still well below the pre-crisis average, but a big improvement on the 0.2% post-crisis average. Germany, the UK and France recorded premium volume increases of 2.0%, 1.5% and 1.5%, respectively. In Germany, motor and property lines registered solid growth, while A&H and liability premiums declined in real terms. In the UK, premium growth was up again on the back of rate improvements. The French market was mainly driven by household insurance (+3.5%). Motor insurance expanded due to strong new car registrations but a new consumer protection law (Loi Hamon) which makes switching insurance policies easier, intensified competition. The Nordic markets were mixed. Among the southern EU countries, growth was strong again in Spain and Portugal, but Greece continued to decline (–6.0%). In Italy premiums fell 2.7%, driven by a 6.8% fall in motor liability, reflecting a fall in new car sales.

Available information suggests a 1–2 ppt weakening of underwriting profitability in non-life in Western Europe in 2015. The average combined ratio of the four largest markets (France, Germany, Italy and the UK) was around 99%. Reserve releases continued, but at a reduced pace. Underwriting results deteriorated for motor (Germany, Italy) and commercial insurance (France, Germany), and due to floods in the UK. Non-life premium growth in Western Europe will remain subdued in light of the moderate economic recovery. Underwriting profitability is expected to deteriorate as a result of softer rates in commercial lines and motor insurance, while claims growth will remain moderate. Profitability will remain under pressure due to still-low investment yields.

24 Allianz, AXA, CNP, Generali, STOREBRAND ASA, Swiss Life and Zurich.25 Aviva, Legal & General, Old Mutual, Prudential (UK), St. James Place, and Standard Life.

Life premiums in Western Europe grew by 1.3% to USD 857 billion in 2015.

The near-term outlook for life insurers is subdued.

Non-life premium growth in Western Europe gained pace in 2015.

Western Europe premiums, 2015

USD bn

World market share

Life 857 34%Non-life 559 28%

Real premium growth

Growth rate 2015

Life Non-life

Pre-crisis average growth 2003–2007

Post-crisis average growth 2009–2014

7%

6%

5%

4%

3%

2%

1%

0%

26 Swiss Re sigma No 3/2016

Emerging regions continue to gain market share

Advanced Asia: steady expansion in life and non-life

Life insuranceLife insurance premiums in advanced Asia grew by 4.2% in 2015, after a 3.3%-gain in the previous year. The improvement was driven by acceleration in Japan, with premium growth up 2.8% from 1.3% in 2014. This more than compensated for a slowdown in Singapore to a still solid 9.5%. (2014: 14%) The slowdown was mostly due to slower sales of single premium linked policies, but the market continued to benefit from increased transparency and the lower distribution costs resulting from the Direct Purchase Insurance initiative. Meanwhile, sales remained robust and stable in Hong Kong, South Korea and Taiwan. In Japan, improved sales of traditional individual life products helped offset sluggish demand for annuity products. Hong Kong has continued to benefit from new business sales to visitors from mainland China, which accounted for 24% of total new premiums from individual life savings business in 2015. In Taiwan, there was a recovery in individual annuity sales and in South Korea, robust sales of protection products underpinned overall premium growth.

Prolonged low interest rates has put pressure on life insurers’ investment returns and profitability. To counter low returns at home, Japanese life insurers have increased holding of foreign securities. At the same time, insurers have sought to lower operational expenses, particularly in Japan, South Korea and Taiwan where insurers face deepening negative interest rate spreads (market interest rates are lower than the guaranteed interest rates of policies).

The near-term growth outlook for life insurance in advanced Asia remains uncertain, as low interest rates continue to threaten insurers’ ability to offer attractive returns. This is the case in South Korea and Taiwan, and even more so in Japan where the central bank has adopted a negative interest rate regime. In Hong Kong, tightening rules on overseas payments through credit cards, and regulator concerns in mainland China about currency and claims risks of mainland Chinese purchasing insurance in Hong Kong, could constrain insurance sales to China visitors.