World Bank Documentdocuments.worldbank.org/curated/en/889281468146694547/pdf/multi... · SNGPL -...

75

Dewiness lt The WorldBank FOR OFFCLAL USE ONLY Report No. 6020-PAK STAFF APPRAISAL REPORT PAKISTAN KOTADDU COMBINED CYCLEPOWER PROJECT April 28, 1986 Energy Division South Asia Projects Department This document has a restricted distribution andmay be used by recipients only in the performance of their official duties. Its contents may not otherwise bedisclosed without WorldBank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of World Bank Documentdocuments.worldbank.org/curated/en/889281468146694547/pdf/multi... · SNGPL -...

Dewiness lt

The World Bank

FOR OFFCLAL USE ONLY

Report No. 6020-PAK

STAFF APPRAISAL REPORT

PAKISTAN

KOT ADDU COMBINED CYCLE POWER PROJECT

April 28, 1986

Energy DivisionSouth Asia Projects Department

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENT

Currency Unit Pakistan Rupees (PRs)Rupee 1 = Paisa 100Rupee I - US$0.0625kupees 1,000,000 US$62,500US$1 5 PRs 16.0US$1,000,000 - PRs 16,000,000

MEASURES AND EQUIVALENTS

1 Kilometer (km) - 0.6214 miles (mi)I Ton (t) - 1,000 kilograms (kg)=2,200 pounds (lbs)1 Kilovolt (kV) - 1,000 volts (V)1 Megawatt (MW) - 1,000 kilowatts (kW)1 Megavolt-ampere (MVA) 1,000 kilovolt-amperes (kVA)1 Kilowatt hour (kWh) = 1,000 watt-hours (Wh)1 Gigawatt hour (GWh) = 1,000,000 kilowatt hours (kWh)1 Kilocalorie (Kcal) = 3.97 British Thermal Units (BTe)I Ton of oil equivalent (toe) = 10,200 Kcal/kg

ABBREVIATIONS AND ACRONYMS

ADB - Asian Development BankADP - Annual Development PlanAEB - Area Electricity BoardAG - Auditor GeneralCIDA - Canadian International Development AgencyCIP - Core Investment ProgramCDWP - Central Development Working PartyECC - Economic Coordination CommitteeECNEC - Executive Committee of the National Economic CouncilERWG - Energy Review Working GroupESL - Energy Sector LoanGOP - Government of PakistanHSD - High Speed DieselICB - International Competitive BiddingIERR - Internal Economic Rate of ReturnKESC - Karachi Electric Supply Corporation, Ltd.LCB - Local Competitive BiddingLRMC - Long-Run Marginal CostMPD - Ministry of Planning and DevelopmentMPNR - Ministry of Petroleua. and Natural ResourcesNEPC - National Energy Policy CommitteeOGDC - Oil and Gas Development CorporationPARCO - Pakistan Arab CompanyPMDC - Pakistan Mineral Development CorporationPSO - Pakistan Sate Oil CompanySGC - Southern Gas CompanySNGPL - Sui Northern Gas Pipeline Ltd.USAID - United States Agency for International DevelopmentUNDP - United Nations Development ProgramWAP!A - Water and Power Development Authority

GOP AND WAPDA'S FISCAL YEAR (FY)

July 1 - June 30

FOR OFFICIAL USE ONLY

PAKISTAN

KOT ADDU COMBINED CYCLE POWER PROJECT

STAFF APPRAISAL REPORT

Table of Contents

Page No.

Is THE ENERGY SECTOR .............. 1........................... 1

A. Strategy for the Development of the Energy Sector ..... 1B. The Bank Group Strategy and Involvement ................ 5

II. THE BORROWER * ............................................. 7

A. Organization of WAPDA 7................ ...... 7B. Existing Facilities *...e.........*.... 8C. Power Planning ....... ............ .... 8

III. THE PROJECT ................... 12.....................

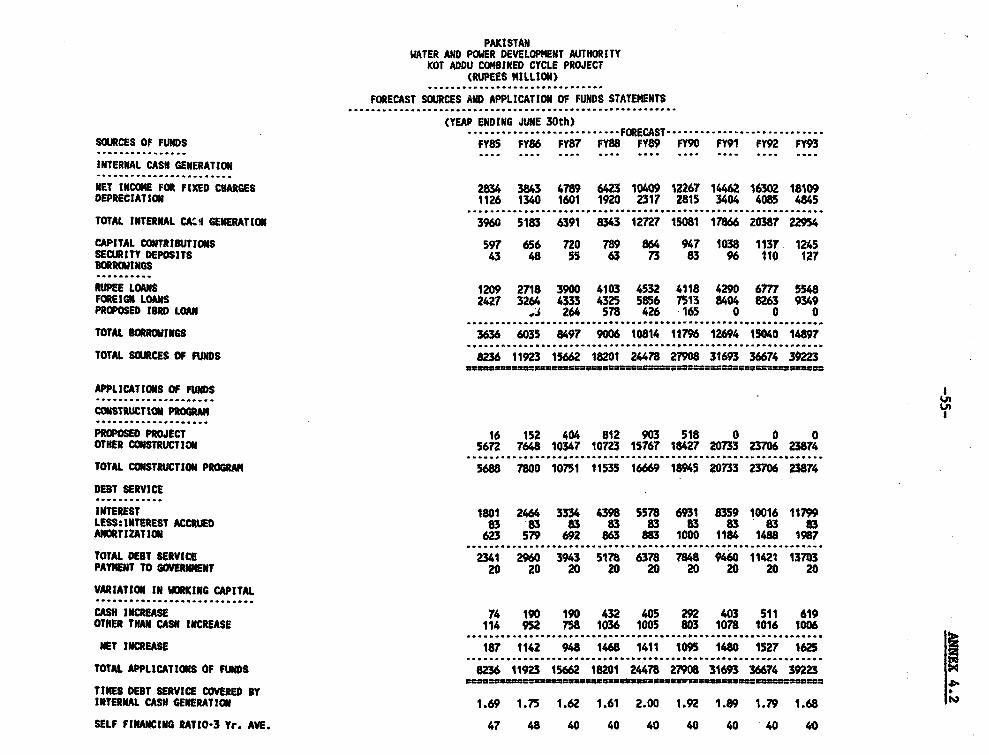

IV. FINANCES ............................................ 19

V. ECONOMIC JUSTIFICATION .................................... 30

A. Forecast of Electricity Sales by WAPDA ................. 30B. Least Cost Alternative ............................ * 31C. Return on Investment ...................... *...*. 31

VI. AGREEMENTS AND RECOMMENDATION .................. *......* 33

This report was prepared by Messrs. E. Linard de Guertechin (Engineer),M. Sharma (Consultant), S. Babbar (Engineer), J. Vance (Senior Financial Analyst),R. Sharma (Financial Analyst), and Gauhar Ali (Energy Advisor, PakistanResident Mission).

This document has a sttid distibuton nd may be ued by cipients only in the peneof thek officl dutie Its contents may not otherwis be dickad without World Bank authodrnion.

'-ii-

Page No.

ANNEXES

1.1 - Strategy for the Development of the Energy Sector .... 351.2 - Organization Chart - Energy Sector ................... 422.1 - Organization Chart - WAPDA ........................... 432.2 - Organization Chart - Power Wing ...................... 442.3 - WAPDA Thermal Generation Statistics .................. 452.4 - Forecast of Energy Balances .......................... 473.1 - Project Description ........................... 483.2 - Project Costs ..................... 493.3 - Project Implementation Schedule ...................... 523.4 - Schedule of Disbursements ............................ 534.1 - WAPDA Balance Sheets ................................. 544.2 - WAPDA Income Statements .............................. 554.3 - WAPDA Sources and Application of Funds Statements .... 564.4 - Notes and Assumptions for Financial Forecasts ........4.5 - WAPDA Investment Program for PY85-FY93 ............... 604.6 - Summary of Status and Plans for strengthening WAPDA's

Financial and Commercial Operations under the WAPDA/USAID Power Distribution Project ...................... 62

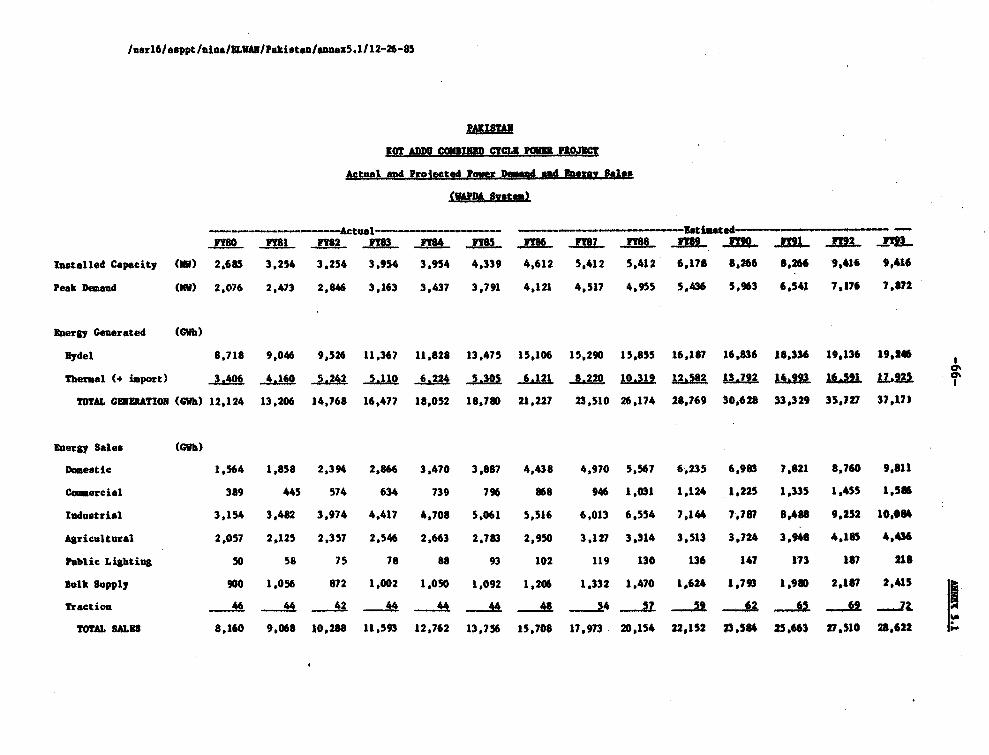

5.1 - Actual and Projected Power Demand and Energy Sales ... 665.2 - Assumption for Rate of Return on Project ...... ,...... 676.1 - Documents and Information in the Project File * ....... 69

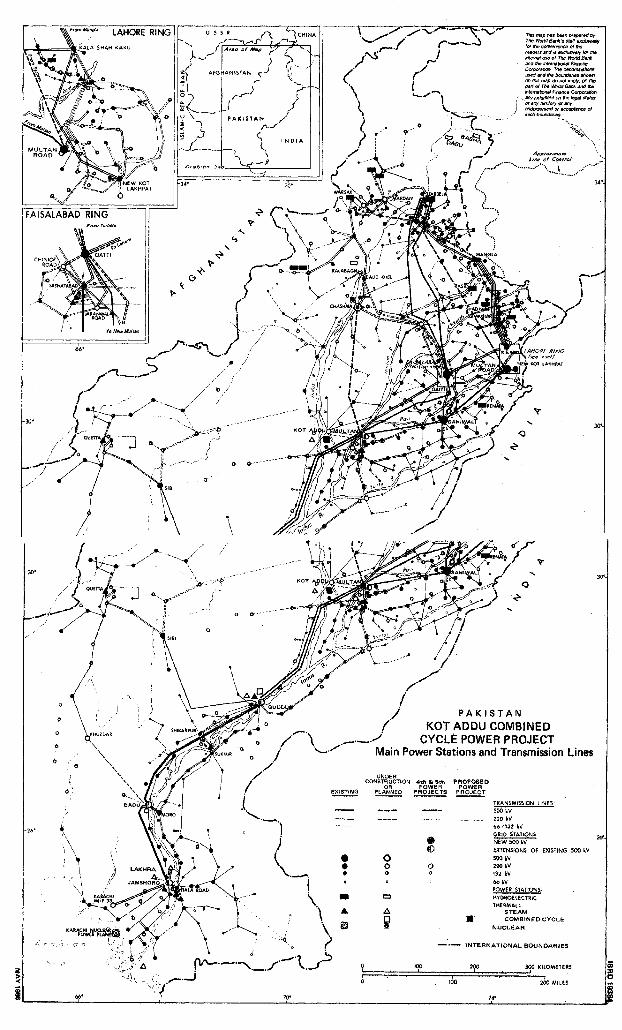

MAP

IBRD 19384

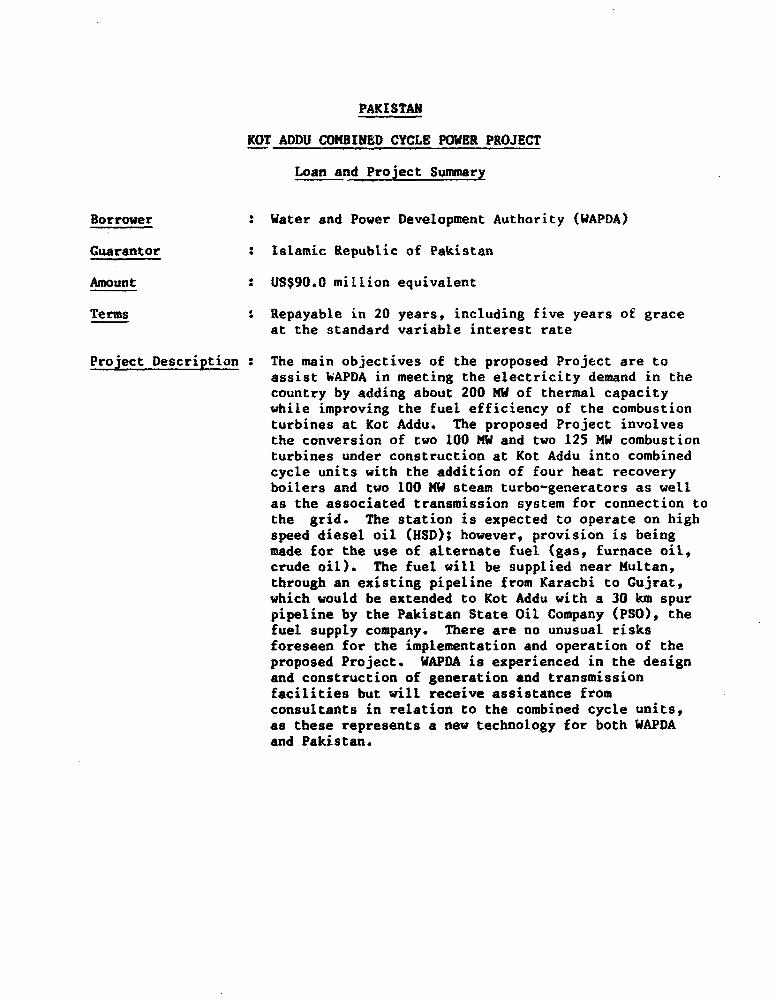

PAKISTAN

KOT ADDU COMBINED CYCLE POWER PROJECT

Loan and Project Summary

Borrower : Water and Power Development Authority (WAPDA)

Guarantor : Islamic Republic of Pakistan

Amount : US$90.0 million equivalent

Terms : Repayable in 20 years, including five years of graceat the standard variable interest rate

Project Description : The main objectives of the proposed Project are toassist WAPDA in meeting the electricity demand in thecountry by adding about 200 MW of thermal capacitywhile improving the fuel efficiency of the combustionturbines at Kot Addu. The proposed Project involvesthe conversion of two 100 MW and two 125 MW combustionturbines under construction at Kot Addu into combinedcycle units with the addition of four heat recoveryboilers and two 100 MW steam turbo-generators as wellas the associated transmission system for connection tothe grid. The station is expected to operate on highspeed diesel oil (HSD); however, provision is beingmade for the use of alternate fuel (gas, furnace oil,crude oil). The fuel will be supplied near Multan,through an existing pipeline from Karachi to Gujrat,which would be extended to Kot Addu with a 30 km spurpipeline by the Pakistan State Oil Company (PSO), thefuel supply company. There are no unusual risksforeseen for the implementation and operation of theproposed Project. WAPDA is experienced in the designand construction of generation and transmissionfacilities but will receive assistance fromconsultants in relation to the combined cycle units,as these represents a new technology for both WAPDAand Pakistan.

Local Foreign Total------- US$ million-

Estimated Costs:l/

Preliminary and Civil Works 12.5 - 12.5Power Station Equipment 28.4 56.1 84.5Transmission Equipment 1.6 3.8 5.4Erection 9.7 4.4 14.1Consultancy 1.4 1.4Engineering and Administration 4.8 - 4.8Total Base Cost 57.0 65.7 122.7

Physical Contingencies 7.6 5.5 13.1Price Contingencies 20.8 18.8 39.6Total Project Cost 85.4 90.0 175.4

Interest During ConstructionBank - 12.4 12.4Other _ _ --

Total Financing Required 85.4 102.4 187.8

Financing Plan:

IBRD Loan - 90.0 90.0WAPDA 75.1 - 75.1GOP 10.3 12.4 22.7Total 85.4 102.4 187.8

Estimated Disbursements:

IBRD FY87 FY88 FY89 FY90 FY91--- US$ million------------

Annual 3.2 16.0 35.0 25.8 10.0Cumulative 3.2 19.2 54.2 80.0 90.0

Rate of Return: 15.2Z

Map : IBRD 19384

1/ Including local duties and taxes of US$36.0 million.

PAKISTAN

KOT ADDU COMBINED CYCLE POWER PROJECT

STAFF APPRAISAL REPORT

I. THE ENERGY SECTOR

A. Strategy for the Development of the Energy Sector

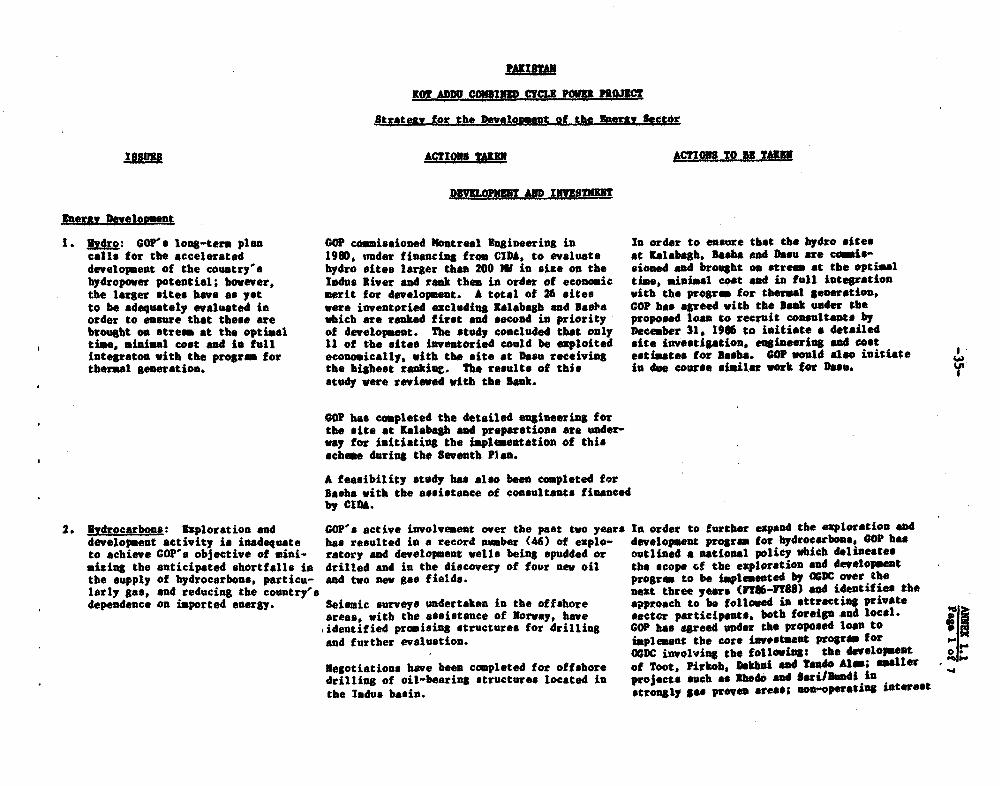

1.01 Pakistan's commercially exploitable domestic energy resources consistin order of importance of hydropower, natural gas, oil and coal. In addi-tion, the country has a large base of renewable energy in the form ofagriculture and animal wastes, and solar and wind energy. The hydropowerpotential is estimated at about 30,000 MW, of which only 2,897 MW has beendeveloped and 1,928 MW is under construction or at an advanced stage ofpreparation. In addition, 3,600 MW will be added when the site at Kalabaghis fully developed. Natural gas is Pakistan's main commercially exploitablehydrocarbon resource, with proven and probable reserves estimated at about340 million tons of oil equivalent (toe). Proven and probable reserves ofoil are estimated at about 58 million toe. Consequently, the prospects aregood for increasing the supply of domestic hydrocarbons; however, this wouldonly be achieved by increasing the private sector's participation in explora-tion to reduce the risk :orne by the Government of Pakistan (GOP)(para 1.04).Coal and lignite reserves are estimated at about 900 million tons, of whichonly 175 million tons are proven. GOP has outlined a systematic program forthe formulation of a comprehensive coal exploration strategy to determine thereserves where further assessment is justified. The first phase of theprogram would be carried out in 1987 and 1988. GOP is also assessing, underfinancing from the United States Agency for International Development (USAID)the potential for stimulating increased private sector involvement in coalproduction using the reserves at Lakhra as a model. If the results at Lakhraare favorable, the same model could be applied to other promising areas. Byand large, the development of Pakistan's domestic energy resources hasprogressed at a substantially slower pace than is warranted by the size ofreserves mainly because of financial constraints. As a result, the country'sdependence on imported energy increased which contributed to the rapid growthof imports and external payments deficits.

1.02 In recognition of the possible adverse impact on the economy of thesustained growth in the demand for energy and increased dependence onimported energy, the Fifth Five-Year Plan (FY79-FY83) emphasized theaccelerated development of domestic energy resources and rationalization ofconsumption. However, the plan targets were not achieved. In addressing theset-backs experienced in achieving the energy targets of the Fifth Plan, GOPincluded the energy sector among the high priority sectors in the SixthFive-Year Plan (FY84-FY88) by increasing its share of the resources and

-2-

taking several important policy initiatives. Despite these actions, itbecame evident during the first two years of the Plan that supply targetswere not likely to be achieved fully. The shortfall in achieving the targetsof the Fifth and Sixth Plans was mainly due to: (a) the shortages of finan-cial resources, precipitated by the underpricing of natural gas and elec-tricity which, in turn, stimulated consumption and resulted in severe andfrequent supply interruptions; and (b) the absence of a system for settingpriorities in investment and for mobilizing resources for their implementa-tion. As a result, the development of primary and secondary energyprogressed in a piecemeal fashion, dictated primarily by the availability offinancial resources, causing persistent gaps between actual and plannedinvestments.

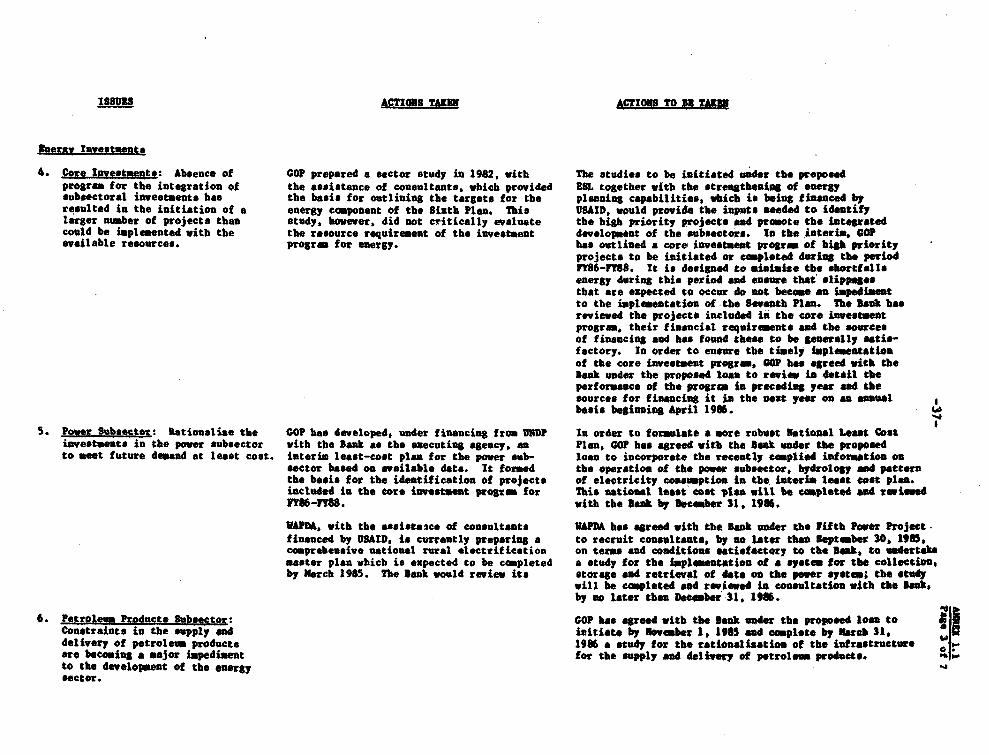

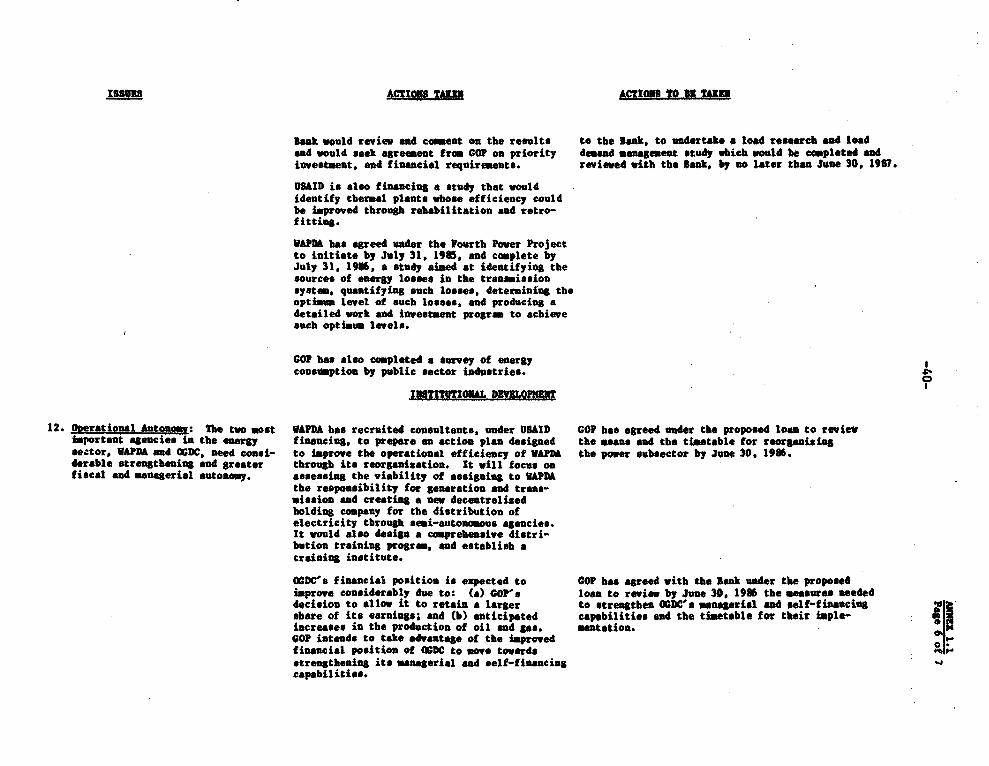

1.03 The lack of progress under the Fifth Plan, the setbacks experiencedin the implementation of the investment program for the energy sector duringthe first two years of the Sixth Plan and the likelihood that resource con-straints would continue into the immediate future prompted GOP to formulate acomprehensive development strategy to address the major sectoral issues. Thestrategy was formulated in 1985 in collaboration with the Bank, under theEnergy Sector Loan (ESL) (Ln. 2552-PAK). It invoived a two-pronged approach.The first focuses on minimizing the shortfalls in energy during the remainingthree years (FY86-FY88) of the current Plan period and on ensuring thatinvestments needed for the Seventh Five-Year Plan are identified and imple-mented. The second calls for studies to outline the framework for theintegrated development of the sector during the Seventh and Eighth Planperiods. The actions and studies under the energy development strategy arecategorized under three headings: (i) investment and development;(ii) pricing and demand management; and (iii) institutional development. Asummary of the issues identified, the plan of action outlined to address themand the target dates for achieving them is summarized in Annex 1.

1.04 Investment and Development. The first element of the strategy formu-lated was to revise the supply targets of the Sixth Plan and outline a CoreInvestment Program that covers the remaining three years (FY86-FY88) of thePlan. The core program for power covers ongoing projects needed to achievethe revised supply targets and projects to be initiated during the remainderof the Sixth Plan to ensure smooth transition to the Seventh Plan. Moreover,it calls for predetermined yearly financial allocations between generation,transmission and distribution to balance the development of the power subsec-tor. In the oil and gas subsector, the core program covers the Oil and GasDevelopment Corporation's (OGDC) annual program of exploration and develop-ment of specific low risk gas and oil prone areas, and the allocation of ayearly budget by GOP to implement the program. In addition, a program paral-lel to that of OGDC was outlined involving the development of fields suitablefor attracting risk capital through joint venture. A new gas producer priceformula was introduced under ESL (Ln. 2552-PAK) to stimulate the interest ofthe international oil firms in undertaking exploration drilling in Pakistan(para 1.06).

-3-

1.05 The financial requirements of the core investment program amounts toabout Rs 50 billion (US$3.2) of which Rs 36.5 billion (US$2.3 billion) wouldbe absorbed by the power subsector; Rs 12.8 billion (US$0.8 billion) by thepetroleum subsector; Rs 0.4 billion (US$24 million) by the coal subsector;and Rs 0.25 billion (US$17 million) by energy planning and conservationactivities. To finance the core investment program, the Government wouldcontribute Rs 8.7 billion (US$0.6 billion) from the Annual Development Plan(ADP) and the contribution of the entities from their internally-generatedfunds would amount to Rs 14.7 billion (US$0.9 billion). The remainingRs 26.4 billion (US$1.7 billion) would be in the form of loans, grants andsuppliers' credits, the bulk of which have been secured.

1.06 Pricing and Demand Management. The petroleum products subsectorcontinues to be a net contrit.tor to the resources of COP. In December 1985,the weighted average domestic price of petroleum products was at 148% of theborder price, US$287/toe compared to US$194/toe. Under the prevailing pricestructure, prices of all petroleum products are above their respective borderprices, with the exception of fuel oil which is below its border price byabout US$39/toe. The price of natural gas, by contrast, was maintained atlevels substantially below those of competing petroleum products, reflecting(?OP's decision to buffer the economy from the adverse impact of the highercost of imported energy. This stimulated demand and by 1981, supply con-straints started to emerge. Accordingly, under SAL I (1981), COP decided toincrease the price of gas to reach two-thirds the border price of fuel oil byFY88. The same policy was reiterated under ESL (Ln. 2552-PAK). In implement-ing the gas pricing policy, the weighted average domestic price of gas hasbeen increased since 1981 at an average annual rate of about 30%. As aresult, in December 1985, the weighted average price of gas was about 65% ofthe border price of fuel oil, that is, US$96/toe compared to US$147/toe. Inaddition, a new producer price for natural gas was introduced in 1985, whichlinks the price of new gas to the border price of fuel oil less a discount tobe determined on a field by field basis. This formula would provide addedincentives for the international petroleum firms to increase their explora-tion activities in high risks gas prone areas (para 1.04).

1.07 As regards electricity, the averige revenue, including fuel sur-charge, in FY85 was 61 paisa/kWh for WAPDA, representing about 60% of theaverage long-run marginal cost (LRMC) of 110 paisa/kWh. Despite the diver-gence between the average revenue and LRMC, WAPDA has been able to financemore than 40% of its investment program from internally generated revenuesbecause actual investments in the past have amounted to only about 50% of theplanned investment. In order to ensure that actual and planned investmentsdo not diverge, GOP and WAPDA agreed under ESL (Ln. 2552-PAK) to undertakeall necessary measures including tariff increases and annual allocations fromthe budget to ensure that the core investment program is financed(paras 4.09, 4.10 and 4.11). Electricity tariffs which had changed verylittle since November 1981 were increased, effective July 1, 1985, by 10%

-4-

across the board for all consumers. Based on the Bank's forecast, theimplementation of WAPDA's investment program for the period FY87-FY94 wouldrequire annual real increases in tariffs of about 8% for the next eightyears. The forecasts further show that for FY87, tariffs will need to beincreased by about 11% on July 1, 1986, in order for WAPDA to cover 40% ofits core investment program for FY87 from internal sources (para 4.11). Inaddition, WAPDA has recruited Argonne Laboratories in the USA, under financ-ing from United Nations Development Program (UNDP). to design a system forthe collection, storage and retrieval of data on the power system(para 2.05). Concurrently, WAPDA, assisted by consultants, EBASCO Services,a US firm, under financing from USAID, has initiated a load research andmanagement study to compile detailed information on the pattern (extent,duration, load factors, etc.) of electricity consumption by the varioujconsumer categories (paras 4.04 and 5.02). The data base study is expectedto be completed by December 1986 (para 2.05), and the load management bySeptember 1987. These would provide the necessary inputs needed for restruc-turing electricity tariffs in Pakistan. In the interim WAPDA is assessingthe impact on consumers of introducing a fuel surcharge in the tariff for thelow voltage consumers. Current plans call for this change to be introducedin FY87.

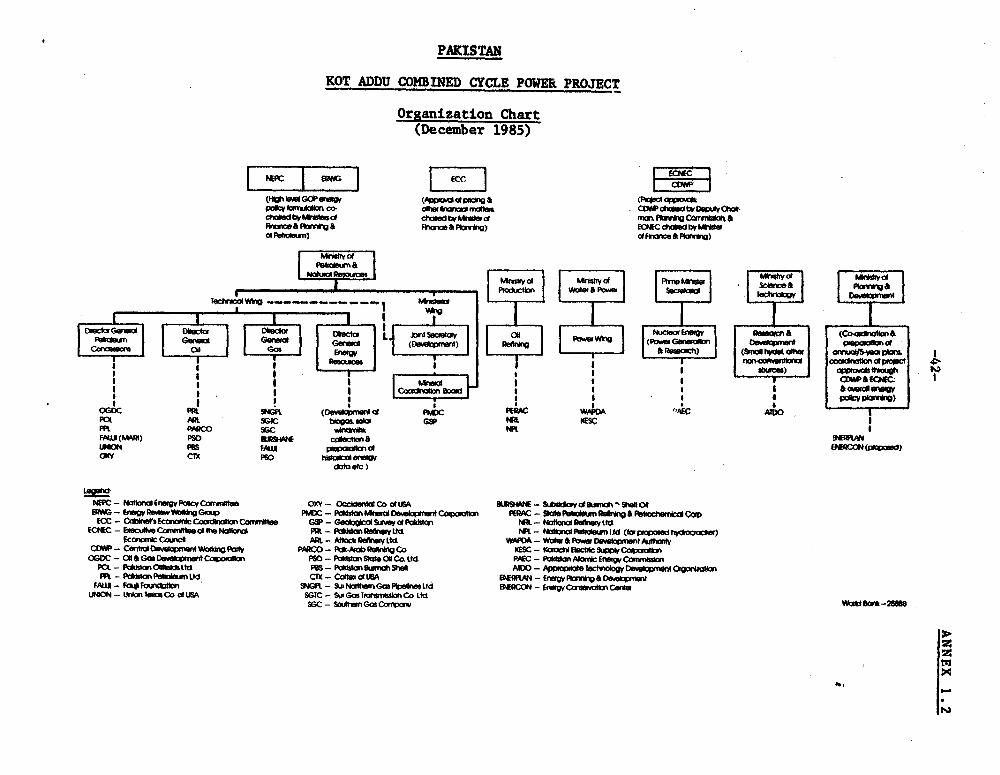

1.08 Institutional Responsibilities and Development. Three ministriesshare the responsibility for supervising the operational entities and agen-cies involved in the energy sector. These are the Ministry of Petrolevm, andNatural Resources (MPNR), the Ministry of Water and Power, and the Ministryof Production. In addition, the Energy Division of the Ministry of Planningand Development (MPD) has responsibility for energy planning. Operationalresponsibilities in the sector are vested in a large number of entities andagencies in both the public and the private sectors. As shown in theorganization chart in Annex 1.2, all these entities and agencies, come underthe jurisdiction of HPNR, except for three state organizations engaged in oilrefining or petrochemicals, the two electricity supply organizations and theAppropriate Technology Development Corporation. Nuclear energy comes underthe office of the Prime Minister. Coordination between the ministries onenergy matters is secured through a number of committees, namely the NationalEnergy Policy Committee (NEPC), Energy Review Working Group (ERWC), theEconomic Coordination Committee (ECC), the Executive Committee of theNational Economic Council (ECNEC), and the Central Development Working Party(CDWP). NEPC is responsible for the formulation of GOP's overall energypolicy. ERWG performs the functions of inter-ministerial coordination aswell as monitors the status of on-going projects in the public sector andendeavors to remove the operational bottlenecks. The review of the financialplans of the sector and the approval of energy pricing proposals is under thejurisdiction of ECC. ECNEC and CDWP review and approve major proposals andprojects in the energy sector, as in other sectors.

1.09 The main issue concerning the organization of the energy sector isthe multiplicity of ministries and committees responsible for planning,

-5-

coordinating and monitoring the performance of the public and privateenterprises involved in the production, transport and delivery of energyproducts. This division of responsibility spreads the scarce human resour-ces, particularty at the techiical level, among a large number of publicagencies resulting in reduced effectiveness of each agency. Recently, GOPunder ESL (Ln. 2552-PAK) created in MPD an energy planning cell (ENERPLnN)with USAID financing, and an energy conservation unit (ENERCON) with jointUSAID and Bank financing. ENERPLAN is mandated to collect, compile andanalyze, on an on-going basis, alL relevant data on the energy sector andintegrate them with the country's annual, five-year and long-term developmentplans, to enable GOP to identify priorities and evaluate resource require-ments to support effective policy formulation and investment planning.ENERPLAN would be staffed by Pakistani personnel who will be assisted duringthe first four years by consultants financed by USAID. CNERCON would serveas the focal point for all conservation activities and its main respon-sibilities will be to plan energy conservation actions, formulate policyguidelines, develop a data-base, support training activities and privateresearch, undertake development and demonstration as well as public informa-tion activities, and monitor the implementation of conservation program ofvarious public and private entities. It would formulate a c.nprehensivenational energy conservation program by the end of 1986. The long-termconsultants for the ENERCON project are expected to start work in mid-1986.

B. The Bank Group Strategy and Involvement

1.10 The Bank's broad objectives in the sector involve the support of thepolicies initiated under ESL (Ln. 2552-PAK), and the allocation of resourcesfor specific projects included in the core investment program (para 1.03).In the area of primary energy production, the Bank would support theimplementation of a comprehensive plan for the exploration and development ofhydrocarbons and coal. In addition, it would support an investment programaimed at the substitution of lower-value products, particula.ly imported coalfor gas in power generation and the release of gas for use by industry andhouseholds as a substitute for imported petroleum products. As for hydropotential, emphasis would be on providing technical and financial support forthe development of high priority schemes. Efforts would also be directedtoward retrofitting and restructuring the refinery subsector, as well as therationalization of the infrastructure for the transport of liquid hydrocar-bons and gas. The Bank would also support the formulation of plans forbringing domestic prices of energy products to parity with their respectivecost to the economy to rationalize consumption and mobilize resources forGOP, and for investing in rehabilitation and retrofitting in major energyconsuming industries, such as oil refineries, fertilizers, cement, etc. Inthe power subsector, the Bank has directed its efforts to strengtheningWAPDA's management and technical capabilities. WAPDA has improved its over-all financial operations by developing modern accounting and commercialsystems (para 4.02). The Bank would continue supporting the institutionbuilding measures already undertaken by WAPDA, including the strengthening of

-6-

technical capability in formulating an integrated least cost plan for thedevelopment of generation, transmission and distribution facilities.

1.11 The Bank Group involvement in Pakistan's energy sector started in1955, with a loan to KESC for the construction of a thermal power station.Since then, it has assisted in financing projects in all energy subsectors.In the power subsector, the Bank has participated in the Indus Basin Develop-ment Projects, which include the hydrogeneration development at Mangla andTarbela. A series of four credits/loans were made to KESC between 1955 and1967 for the development of its generation capacity. Since 1970, the Bankhas been more directly involved in COP's program for strengthening the powertransmission and distribution networks, for which five credits/loans weremade to WAPDA. The first (Cr. 213-PAK) of US$23 milLion, made in 1970,covered the cost of upgrading the transmission network. A second operation,a Third Window loan (Ln. 1208T-PAK) of US$50 million, subsequently reduced bvUS$15 million due to savings achieved under international competitive bid-ding, was made in 1975 to finance the development of part of the 500-kVtransmission system to connect the hydra resources of the north with thethermal generation in the center and south to provide the most economic meansof supplying power throughout the country. A third operation (Cr. 968-PAK)in the amount of US$45 million was made to cover four years of WAPDA'sprogram for the development of the secondary transmission (FY79-FY83),involving the erection of about 4,345 km of single and double circuit linesand the construction, expansion and conversion of 216 substations. Thisproject was completed in December 1985.

1.12 In FY85, four loans amounting to a total of US$433 million wereapproved by the Bank. The Fourth WAPDA Power Project (Ln. 2499-PAK) for anamount of US$100 million is a continuation of the Third WAPDA Power Project(Cr. 968-PAK) and covers the construction of a total of about 3,890 km oftransmission lines and 227 substations, including expansion of 86 substa-tions, ot the subtransmission system over the period FY86-FY90. The FifthWAPDA Power Project (Ln. 2556-PAK) for an amount of US$100 million wasapproved in order to assist WAPDA in the installation of about 1,100 km of500-kV transmission line between Lahore and Jamshoro via Sahiwal, Multan,Guddu and Dadu, and of new 500-kY substations at Lahore and Sahiwal and theextension and reinforcement of existing 500-kV substations at Multan, Guddu,Dadu and Jamshoro (para 2.09). In the area of petroleum exploration anddevelopment, the Bank approved a Petroleum Resources Joint Venture Project(Ln. 2553-PAK) with a view to financing the Government's and OGDC's share offoreign exchange commitments under the existing joint ventures with privatesector as the operator in Badin and North Potwar blocks and the new jointventures yet to be firmed up during the next three years (para 1.04).

-7-

II. THE BORROWER

A. Organization of WAPDA

2.01 WAPDA, the beneficiary of the loan, was established in 1958 to coor-dinate the development of Pakistan's water and power resources. It is asemi-autonomous agency whose capital investment program and tariffs areapproved by GOP. WAPDA is divided into two largely independent 'wings' onefor power and the other for water (Annex 2.1). The Power Wing is responsiblefor the construction and operation of power generation, transmission anddistribution facilities throughout the country, except the Karachi area whichis served by KESC. The Water Wing is responsible for the overall planningand investigation of water resources, and the design and construction ofsurface and groundwater development projects for the federal and provincialgovernments. WAPDA's governing body, referred to as the "Authority", con-sists of a chairman and three members who are in charge of power, water, andfinance, and are designated Member (Power), Member (Water) and Member(Finance) respectively. The members are appointed by the Government andfunction as chief executives of their respective groups.

2.02 Member (Power) is assisted by a Deputy Managing Director (distribu-tion) and seven general managers in charge of generation (thermal), gener-ation (hydel), transmission and grid stations, finance, coordination andplanning, system operation and load dispatch, and inventory control. Theorganization of the Power Wing which, for convenience, is herein referred toas WAPDA, is shown in Annex 2.2. Although WAPDA is highly centralized withrespect to decision-making, its distribution department is divided into eightArea Electricity Boards (AEBs), which were established in 1981 to take overthe responsibility for local electricity service. Each AEB has a chairman,who is the chief engineer for the area, appointed by WAPDA for a five-yearterm; three full-time members, who are also directors in charge of depart-ments; and three part-time members representing local interests, one of whomis normally a representative of the Provincial Government. The members ofAEBs are appointed for a period of three years.

2.03 In January 1985, WAPDA had about 88,000 employees, 2,100 engineers,700 other professionals, 9,200 technical and other staff, 15,000 administra-tive and accounts staff, 44,000 skilled workers and 17,000 general staff.The number of consumers served by WAPDA in that same year was about 4.5million, representing about 51 consumers per employee. The relatively highconsumer-employee ratio, reflecting the overstaffing of the distributiondepartment, 1/ has induced WAPDA to initiate a program, with the assistance

1/ The distribution department accounts for about 70% of WAPDA's staff.

-8-

of consultants, EBASCO Services, a U.S. firm financed by USAID, for stream-lining the operations of the distribution department and for updating itspolicies, procedures and methods (paras 4.02 and 4.14). These same consult-ants are also assessing the viability of creating a Power DistributionAuthority. In addition, in order to promote the integrated development ofthe power subsector, GOP has agreed under ESL (Ln. 2552-PAK) to review themeans for reorganizing the subsector. COP is presently examining the legalimplications of assigning to WAPDA the responsibility of generation and highvoltage transmission of electricity for the entire country and restrictingKESC's operation to the bulk purchase of power from WAPDA for distribution inthe Karachi area. Consideration is also being given by GOP to private sectorinvolvement in the power subsector. Toward that end, GOP appointed in August1985 a National Deregulation Commission headed by the Governor of the StateBank of Pakistan. One of its objectives is to outline a strategy forincreasing private sector involvement in power distribution. Moreover, ECCapproved in September 1985 a charter of terms and conditions under which theprivate sector would be invited to participate in power generation, in thecontext of the agreed medium and long-term plans. A detailed framework forcompensating potential private firms involved in the supply of power inPakistan is currently being formulated. The Bank would review tne means andthe timetable for reorganizing the subsector.

B. Existing Facilities

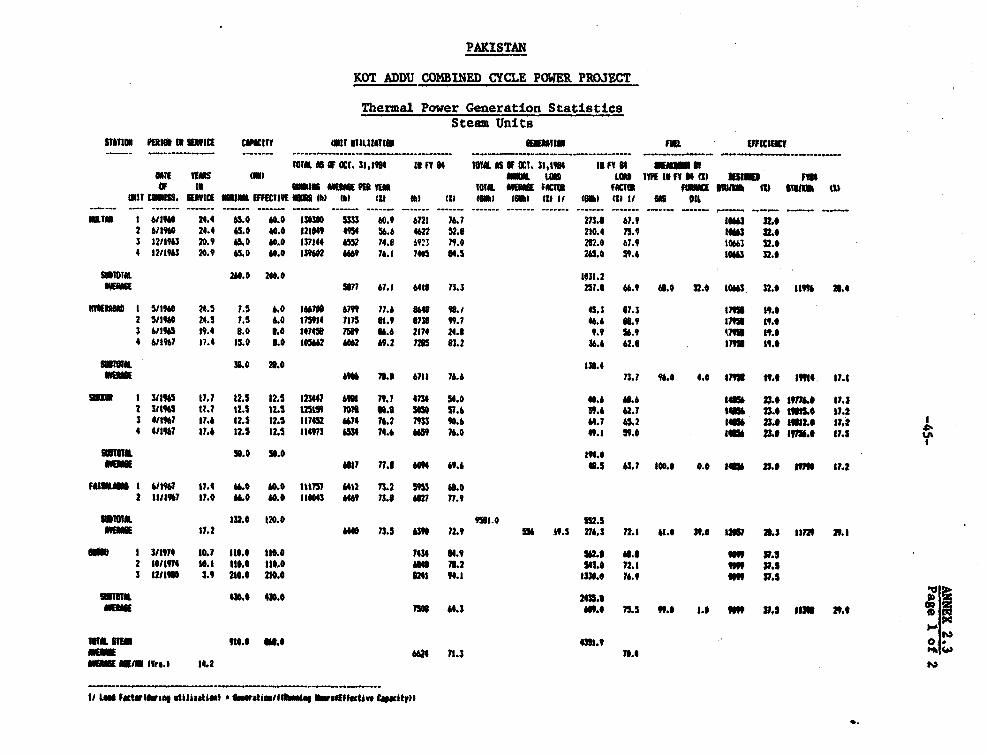

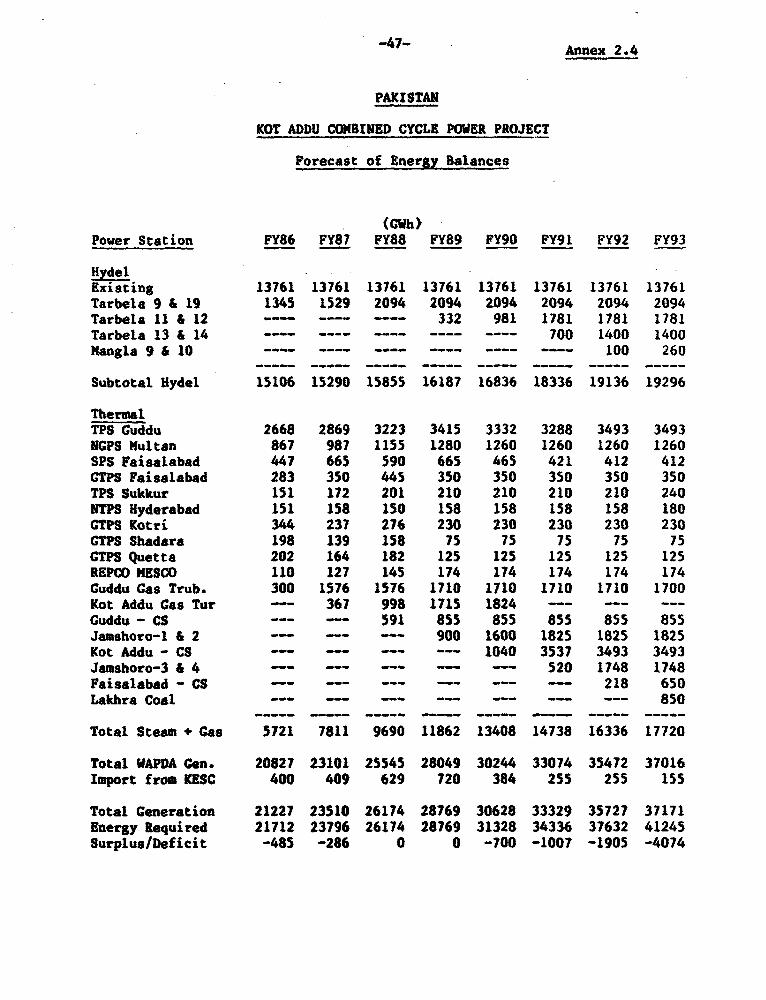

2.04 In June 1985, WAPDA's total installed generating capacity was4,339 MW, comprising 2,897 MW (67%) of hydro and 1,442 MW (33%) of thermalcapacity. The maximum potential output of the existing hydro stationsamounts to about 3,100 MW when all the reservoirs are full. This potentialdrops to about 1,000 MW during the dry seasons, and has to be offset bythermal generation, including the more extensive use of combustion turbinesthan for the normal peak load, because of the overall shortage of generatingcapacity (Annex 2.3). According to WAPDA, the shortfall between demand andthe generation capability of its system, estimated at about 1,000 MW inJanuary 1985 and about 1,200 MW in June 1985, is expected to continue intothe mid-1990s (paras 4.07 and 5.02).

C. Power Planning

2.05 The slippages in the implementation of investment program,precipita:ed by both resource constraints (paras 1.07, 4.01 and 4.06) and theabsence of a mechanism that would identify priority projects and the scaleand timir.g of investments (para 1.02), prompted WAPDA to formulate, with theassistance of Argonne Laboratories, under financing fromi UNDP, with the Bankas the executing agency, an interim least-cost program for the development ofgeneration facilities. A revised national long-term least cost plan whichincorporates the more recent developments in the subsector is expected to becompLeted by December 31, 1986. In addition, in order to strengthen WAPDA'sin-house power system planning capability, Argonne, under the auspices of the

-9-

International Atomic Energy Agency, has trained its staff in the use of theWien Automatic System Planning (WASP III) computer model and has successfullyinstalled that model on WAPDA's computer in early 1985. This would enableWAPDA to revise the national least-cost plan, as and when needed, incorporat-ing the updated information on the operation of the subsector, includinghydrology, water management and pattern of electricity consumption. ArgonneNational Laboratory, under financing from UNDP, is presently assisting WAPDAin outlining a system for collection, storage and retrieval of data on thepower system. The consultants are expected to complete this work by the endof 1986 (para 1.07).

Ceneration Program

2.06 Based on the interim long-term least cost development plan, WAPDA'sinstalled generating capacity is forecast to increase from 4,339 MW in June1985 to 9,416 MW in 1993. This would involve the commissioning of Projectsunder construction including: the extension at Tarbela (Units 11-14,4x432 MW), a steam unit (Unit No. 4, 210 MW) and a combined cycle station(450 MW) at Cuddu, a steam unit (Unit No. 1, 250 MW) at Jamshoro, and a setof combustion turbines at Kot Addu (4x10 MW). Financing for the aboveprojects has been secured. All of these units, except the ones at Tarbela,are expected to be commissioned during the Sixth Five-vear Plan. Units 11and 12 at Tarbela are expected to be commissioned in December 1989, and units13 and 14 in June 1990. In addition, the interim plan calls for the develop-ment of: a Large hydropower scheme at Kalabagh with a total capacity of3,200 MW when fully developed and a number of low-head hydro schemes inves-tigated by consultants under financing from Federal Republic of Germany; animported coal complex at Karachi; and thermal capacities at Lakhra based ondomestic coal and at Jamshoro based on fuel oil. Project implementationschedule for Kalabagh provides for construction over an eight-year periodwith civil works beginning end-1987.

2.0? A prefeasibility study for the imported coal complex has been com-pleted by consultants, Shawinigan Integ, a Canadidli firm, under financingfrom the Canadian International Development Agency (CIDA) and the Bank. Theconsultants have identified three possible sites - two near the existing PortQasim and the third, in the area west of Karachi. The feasibility study anddetailed engineering and preparation of bidding documents for the first phaseof the imported coal power complex are expected to be completed by Decem-ber 31, 1987. The feasibility studies for the Lakhra mine and power stationare under preparation by consultants, Gilbert Commonwealth, J.T. Boyd andICF, U.S. firms, under USAID financing. The results of these studies wouldbe reviewed by the Bank. The prefeasibility study for the plants at Jamshorohas been completed by consultants, Bechtel International, Inc., a U.S. firm,under financing from USAID who are also expected to finance the detailedengineering. The study shows that the expansion of the installed capacityfrom 670 MW to about 1,600 MW and the construction of a pipeline to transportfuel oil for the operation of the plants would be economic. In view of the

-10-

need to diversify the fuel used for power generation and expand the gener-ating capacity to reduce power shortages, WAPDA agreed to recruit consult-ant3 with qualifications, experience and terms of reference satisfactory tothe Bank, to undertake a feasibility study and detailed engineering, andprepare the bidding documents for the second stage of the power generationcomplex at Jamshoro; the work should be completed and reviewed in consult-ation with the Bank by no later than March 31, 1987 (para 6.02(a)).

2.08 In addition, in order to improve the efficiency of the existingthermal power plants WAPDA with the assistance of consultants, Stone andWebster, a U.S. firm, financed by USAID, has prepared a program for theirrehabilitation and retrofitting. The principal eiements of the recommendedprogram, which would increase WAPDA's generating capacity by about 200 MW,would form the basis of a project suitable for possible Bank financing inFY87.

Transmission Program

2.09 Major hydro resources are located in the north of the country andthermal facilities and load centers are concentrated in the center and thesouth, which requires the bulk transmission of electricity over long distan-ces. In order to ensure the efficient evacuation of power, WAPDA's long-termplan calls for the development of extra high voltage (500-kV) transmissionlines between Tarbela and Karachi by 1990. The Tarbela-Faisalabad section(about 300 kn) of the first 500-kV transmission line is already in service;the section from Faisalabad to Jamshoro via Multan and Guddu, presentlyoperated at 220-kV, is being upgraded for 500-kV operation. A double circuit220-kV transmission link between Jamshoro and Karachi (about 130 km) wascompleted in December 1984. The second 500-kV line from Tarbela toFaisalabad was commissioned in August 1985 with financial assistance fromCIDA. The transmission system will be further reinforced with the completionby 1990 of a third 500-kV line. The section between Tarbela and Lahore isfinanced by the Asian Development Bank (ADB), and section between Lahore andJamshoro via Multan and Guddu is financed by the Bank (Ln. 2556-PAK)(para 1.12). The 220-kV network and subtransmission system would also beexpanded during the period FY85-FY89 under the Fourth WAPDA Power Project(Ln. 2499-PAK) (para 1.12) whose development would be integrated and coor-dinated with the expansion of the high voltage transmission and distributionsystems. As losses in the network are relatively high, about 27X of grossgeneration, WAPDA has also initiated a study, with the assistance of consult-ants, EBASCO Services, a US firm, financed by USAID, to prepare a detailedwork and inviestment programs needed to reduce losses to economically accept-able levels. The study, which is expected to be completed by June 30, 1986,will serve as a basis for a possible loss reduction project suitable for Bankfinancing.

-11-

Distribution and Rural Electrification Program

2.10 EBASCO Services, a US firm, financed by USAID, is assisting WAPDA inthe design and preparation of a comprehensive Master Plan for Power Distribu-tion System which would identify the changes required to expand as well asimprove the efficiency of WAPDA's service. The objective of this program isto reduce losses at the distribution level and provide for the economicexpansion of the distribution network in rural as well as urban areas. Thestudy, to be completed by mid-1986, has focussed specifically on: the dis-tribution organization, energy loss analysis, establishing criteria forselection of feeders for rehabilitation, plans for efficient distributionexpansion and practices, load management, voltage regulation and servicereliability. The Bank, together with WAPDA and USAID, will review the MasterPlan prepared by the consultants. This Master Plan, along with the study ontransmission losses (para 2.09), would serve as a basis for identifying thetransmission and distribution components of the Core Investment Program andset a framework for selecting projects suitable for external financing.

-12-

III. THE PROJECT

Project Setting

3.01 In order to rationalize investments, GOP's energy sector strategycalls for the implementation of a core investment program which covers theongoing projects and those to be initiated during the remaining three yearsof the plan (para 1.04). One of the ongoing projects included in the coreinvestment program is the power plant at Kot Addu (400 MW), located in thecentral part of the country (Map IBRD 19384). The Kot Addu power plant,comprising four combustion turbine, was designed to ensure system stabilityand provide peaking capacity at Multan, one of the main load centers in thecountry. However, the forecast energy requirements indicate that these unitswill be operated for at least the first ten years during off-peak periods.Accordingly, priority has been accorded to the conversion of combustionturbines to combined cycle operation which would allow WAPDA to make use ofthe waste heat from the turbines and improve the overall efficiency of thepower plant. The conversion of combustion turbines to combined cycle opera-tion is consistent with GOP's overall objectives for the energy sector whichcall for rationalizing consumption, improving efficiency and meeting futuredemands at least cost to the economy.

Objective of the Project

3.02 The -primary objective of the Project is to improve the efficiency ofthe Kot Addu power station by providing 50X more power per unit of fuelconsumed. Moreover, it would also assist in reducing the forecast shortfallin generating capacity, expected to continue until the mid-1990s, by addingan additional 200 KW of capacity in a relatively short time.

Description of the Project

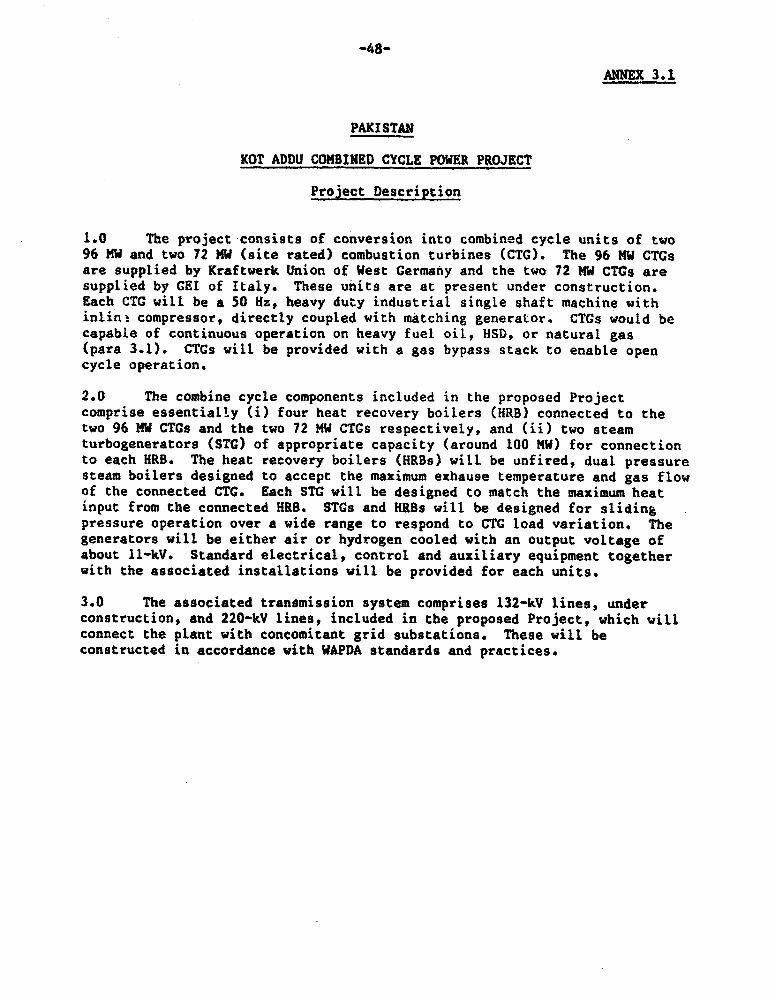

3.03 The Project, which is described in detail in Annex 3.1, consists ofthe following components:

(a) the installation of four heat recovery boilers to be connected totwo 125 MW and two 100 MW combustion turbines currently underconstruction, two steam turbo-generators of about 100 MW, togetherwith associated high voltage transformers, cooling water supply,and auxiliary facilities3

(b) the construction of about 104 km of 220-kV transmission lines fromNot Addu to Multan and the addition of connecting bays at thesegrid substations; and

-13-

(c) consulting services for the preparation of specification of equip-ment, bidding documents, evaluation of bids, finalization ofdesigns and supervision of erection and testing of the combinedcycle units.

Project Cost

3.04 The estimated cost of the Project, including price and physicalcontingencies and customs duties is about US$175 million. The total financ-ing required, inclusive of interest during construction, is US$188 million.Of the total financing required, US$102 million would be in foreign exchangeand the remaining US$86 million would be in local costs. These estimates arebased on quotations for similar ongoing works, updated to December 1985prices. Physical contingencies were assumed at 7% for equipment andmaterial, and 14% for erection services. These amount to 10.7% of the basecost of the Project. Escalation of foreign costs is assumed at 3.25% forFY86, 7% for FY87, and 7.25% for FY88, 7.6% for FY89 and FY90, and 6% forFY91. Escalation of local costs is assumed at 10% for FY86, 8.5% for FY87,and 7.5% per annum thereafter. The total price escalation amounts to 29.2%of the base cost plus physical contingencies. Estimates of duties and taxesamount to US$36.0 million, resulting in total cost of the Project of US$139.4million net of taxes and duties. Summary of project cost is presented inTable 3.1 below and details are given in Annex 3.2.

Table 3.1: Project Estimated Cost 1/

Local Foreign Total Local Foreign TotalRs Millioi ----- -----US$ Million-----

Preliminary and Civil Works 200 - 200 12.5 - 12.5Power Station Equipment 454 899 1,353 28.4 56.1 84.5Transmission Equipment 26 60 86 1.6 3.8 5.4Erection 156 70 226 9.7 4.4 14.1Consultancy - 23 23 - 1.4 1.4Engineering and Administration 77 - 77 4.8 - 4.8Total Base Cost 913 1,052 1,965 57.0 65.7 122.7

Physical Contingencies 122 83 205 7.6 5.5 13.1Price Contingencies 333 301 634 20.8 18.8 39.6Total Project Cost 1,368 1,436 2,804 85.4 90.0 175.4Interest during Construction

Bank - 199 199 - 12.4 12.4Total Financing Required 1,368 1,635 3,003 85.4 102.4 187.8

1/ Figures may not add due to rounding.

-14-

Project Financing

3.05 The foreign exchange cost of the Project would be covered by a Bankloan of US$90.0 million, and a loan of about US$12.4 million by GOP towardsinterest during construction, which would be capitalized. The Bank loanwould be made to WAPDA with GOP as guarantor. GOP and WAPDA would providethe local financing, amounting to US$85.4 million of which US$10.3 millionwould be in the form of Rupee loan from GOP and US$75.1 million from WAPDA'sinternal sources. WAPDA would bear the interest rate risk and cost overrunsand GOP would bear the foreign exchange risk. The following table summarize-the financing plan:

Table 3.2: Project Financing Plan

Local Forjein Total(US$ Million)

IBRD Loan - 90.0 90.0WAPDA 75.1 - 75.1GOP 10.3 12.4 22.7

Total 85.4 102.4 187.8

Engineering and Construction

3.06 WAPDA has acquired extensive experience in the installation andoperation of thermal power stations, both steam units and combustion tur-bines, and associated high voltage transmission systems. This experience,however, does not cover the installation of combined cycle units. The firstcombined cycle station of 450 MW is currently under construction at Gudduwith ADB and USAID financing. The Project would be the second such stationin the country. WAPDA is in the process of recruiting consultants, on termsand conditions satisfactory to the Bank, to assist in: (i) the preparation ofthe specifications for the equipment and bidding documents; (ii) the evalua-tion of bids; (iii) the finalization of the design proposed by the selectedbidder; and (iv) the supervision of the manufacture, erection, testing andcommissioning of the equipment. The cost of consulting services required forthe Project would be financed under the loan.

3.07 The proposed power station "4ill be located in the outskirts of thetown of Kot Addu close to major roads and railways, which will facilitatetransport of equipment, materials and fuel (para 3.12). Cooling water willbe supplied from tubewells because the quality of groundwater is better thanthat of the water from nearby irrigation canals. Moreover, the station wouldbe equipped with cooling towers in order to reduce water requirement. Theassociated transmission system would consist of 132-kV lines being con-structed under the Fourth WAPDA Power Project (Ln. 2499-PAK) connecting the

-15-

station to the regional load centers. In addition, 220-kV lines to Mu'Ltanwill connect the station with WAPDA's national grid. WAPDA has alreadyestablished a specific unit responsible for the implementation of the Projectto ensure prompt decision-making and effective coordination. Constructionwould be supervised and conducted by resident engineers with the assistanceof consultants (para 3.06). In the context of the ongoing installation ofthe combustion turDines, WAPDA has already started a training program for theoperation of similar facilities, using a simulator at WAPDA's training centerat Faisalabad. Specific training for the operation and maintenance of thecombined cycLe equipment included in the Project would be provided by theequipment contractors.

Project Preparation and Implementation Schedule

3.08 WAPDA is currently installing the four combustion turbines to whichthe equipment incLuded under the Project would be connected (para 3.01).These turbines are scheduled to be commissioned by the end of 1986. Land hasalready been acquired by WAPDA to accommodate the installation of the combus-tion turbines and combined cycle facilities and allow for possible extensionin the future. All basic infrastructure facilities (e.g. access roads, watersupply, fuel treatment plant and storage reservoirs, accommodation for con-tractors and WAPDA personnel) are under construction. The equipment includedin the Project is standard and preparation of tender document is straightfor-ward and is expected to be completed before September 30, 1986. Major con-tracts, in particular the combined package for the heat recovery boilers andsteam turbo-generators, would be awarded by June 30, 1987. Project comple-tion is expected in mid-1990. The detailed implementation schedule for theProject is shown in Annex 3.3. The approval by ECNEC of the PC-1 documentwith respect to the Project would be a condition of effectiveness for theloan (para 6.03(a)).

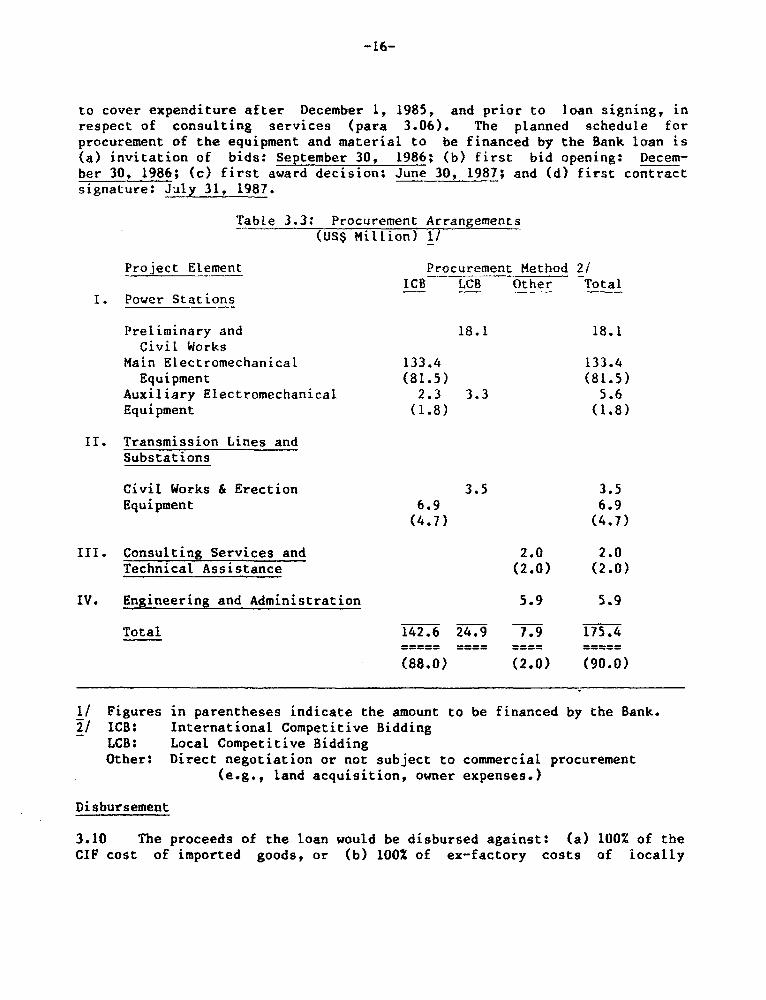

Procurement

3.09 Procurement arrangements for the Project are summarized in Table 3.3.The major equipment for the combined cycle units, estimated to cost aboutUS$133.5 million, would be tendered as a turnkey package, subject to interna-tional competitive bidding (ICB) in accordance with Bank guidelines.Auxiliary equipment for the power station and equipment associated with thetransmission facilities, estimated to cost about US$9.0 million, would begrouped in packages and will be subject to ICB in accordance with Bankguidelines. About 81% of works, goods and services for the Project would beprocured through ICB. Documents for individual contracts above US$1,000,000equivalent would be subject to prior review by the Bank. Local suppliers andmanufacturers competing for the supply of goods under ICB would have a 15%preference or the applicable duty, whichever is less. Consultants forproject engineering, training and technical assistance would be selected andemployed in accordance with Bank guidelines. WAPDA has requested the Bank toauthorize advance procurement and retroactive financing of up to US$500,000

-16-

to cover expenditure after December 1, 1985, and prior to loan signing, inrespect of consulting services (para 3.06). The planned schedule forprocurement of the equipment and material to be financed by the Bank loan is(a) invitation of bids: September 30, 1986; (b) first bid opening: Decem-ber 30, 1986; (c) first award decision: June 30, 1987; and (d) first contractsignature: July 31, 1987.

Table 3.3: Procurement Arrangements(US$ Million) 1/

Project Element Procurement Method 2/ICB LCB Other Total

I. Power Stations

Preliminary and 18.1 18.1Civil Works

Main Electromechanical 133.4 133.4Equipment (81.5) (81.5)

Auxiliary Electromechanical 2.3 3.3 5.6Equipment (1.8) (1.8)

II. Transmission Lines andSubstations

Civil Works & Erection 3.5 3.5Equipment 6.9 6.9

(4.7) (4.7)

III. Consulting Services and 2.0 2.0Technical Assistance (2.0) (2.0)

IV. Engineering and Administration 5.9 5.9

Total 142.6 24.9 7.9 175.4

(88.0) (2.0) (90.0)

1/ Figures in parentheses indicate the amount to be financed by the Bank.2/ ICB: International Competitive Bidding

LCB: Local Competitive BiddingOther: Direct negotiation or not subject to commercial procurement

(e.g., land acquisition, owner expenses.)

Disbursement

3.10 The proceeds of the loan would be disbursed against: (a) 100% of theCIF cost of imported goods, or (b) 100% of ex-factory costs of locally

-17-

manufactured goods, aoth being subject to ICB. Disbursement of the loanwould also be made against 100% of the foreign cost of consultancy. Aschedule of disbursements is given in Annex 3.4 and relates to the projectimplementation schedule (Annex 3.3). The disbursement schedule is fasterthan the Bank's standard profile for thermal generation projects, five yearsas against eight. This is reasonable given: (a) the shorter time requiredfor the manufacture and installation of equipment for the conversion tocombined cycle operation compared to Large coal-fired power stations whichfeature significantly in the standard profile; and (b) the conversion tocombined cycle in this project basically involves retrofitting a stationwhere all infrastructural facilities are nearly complete. The Bank is satis-fied that the proposed profile reflects worldwide experience in combinedcycle conctruction, WAPDA's implementation capabilities, and the advancedstage of project preparation.

Fuel Supply

3.11 The Kot Addu combustion turbines which are at an advanced stage ofinstallation would operate on 1iquid fuel to be transported from Karachi toGujarat, near Multan, through an existing pipeline. 1/ The pipeline has beendesigned to transport crude oil to a refinery that GOP had planned toinstall at Multan. However, under ESL (Ln. 2552-PAK), the Government agreedto undertake a study for the rationalization of the infrastructure for supplyand delivery of petroleum products throughout the country. Accordingly, thestatus of the proposed Multan refinery is being reviewed. In the interim,the Karachi-Cujarat pipeline is being used to transport batches of kerosene(30%) and high speed diesel oil (HSD) (70%) for distribution to mid-countryconsumers. Although diesel oil would be used to operate the Kot Addu sta-tion, the combustion turbines have been designed to use a mix of furnace oilor crude oil (80%) and HSD (20%), in the event that these fuels become avail-able in the area, through the pipeline or the refinery. An alternative fuelto be considered would be gas, which is Pakistan's main commnrciallyexpl,ited hydrocarbon resource (para 1.01). However, the nearest known gasfields, Nandpur and Panjpir, are located about 200 km from Kot Addu and havelimited reserves. According to OGDC, these fields could only supply smallunits of about 25 KW each. In addition, because of recent shortages in gasproduction, GOP has decided, for the time being, to release the gas from thepower subsector for higher value uses, and has agreed under ESL(Ln. 2552-PAK) to undertake a study to revise the Gas Development Plan todetermine the optimal supply and utilization pattern for the next five years.Therefore, in the absence of gas or crude oil, the operation of the Kot Addustation with HSD would be the only economic option (para 5.03).

lf Diameter 16 inches, length 864 km.

-18-

3.12 The Karachi-Gujarat pipeline is operated by the Pakistan Arab Company(PARCO) which delivers the fuel to the oil depot at Mahmood Kot, nearGujarat. PSO would deliver the fuel to the Kot Addu power station which islocated about 30 km from Mahmood Kot. PSO has decided to construct a 11 inchdiameter pipeline for the transport of fuel between the two stations. Afeasibility study has demonstrated that the transport of fuel by pipeline isthe least cost alernative, particularly in view of the fact that for atleast ten years after its commissioning, the station is expected to operateat a high load factor. Therefore, in order to ensure the coordinateddevelopment of the Mahmood Kot - Kot Addu fuel pipeline and the proposedpower station, confirmation by GOP that a contract for the_pipeline construc-tion has been signed, would be a condition of effectiveness of the loan(para 6.03(b)).

Ecology

3.13 The operation of the station at full capacity should present noenvironmental problems because the fuel has a low sulphur content. Theemission levels are expected to meet the requirements specified in the Bankguidelines. Owing to the relatively small size of the steam units and theinstallation of cooling towers, the water requirement can easily be drawnfrom the underground without affecting the aquifer level. Safety regulationsfor power stations, to which all operating personnel must conform, will bestrictly enforced, as they are in existing WAPDA stations which all have agood safety record. The combustion turbines are being equipped with adequatesilencing equipment and the turbine halls of the steam turbo-generator com-ponents will have a sound pressure level of less than the maximum acceptablethreshold of 90 decibels. Transmission lines will be designed to keep radiointerference within acceptable limits.

Project Risks

3.14 No unusual risks are foreseen. Combined cycle units are a standardtype of installation which require limited civil works and relatively littleassembly on site. Risk of damage due to fire, explosion, etc. would becovered by the respective contractors during the construction phase, and,after commissioning, by WAPDA, through its insurance policies which aresatisfactory (para 4.22).

Project Monitoring

3.15 WAPDA will submit quarterly reports covering the works of the con-sultants, physical progress, costs, disbursements and administrative aspectsof the Project. In addition, there will be annual financial and administra-tive reports.

-19-

IV. FINANCES 1/

Introduction

4.01 WAPDA's financial affairs are governed by the WAPDA Act whichrequires the utility to generate sufficient revenues from electricity salesto cover operating costs including depreciation, debt service and achieve areasonable return on investment. Under the First WAPDA Power Project(Cr. 213-PAK), WAPDA agreed to achieve a rate of return of 8% on revaluedaverage net fixed assets in use. However, because of GOP's reluctance torevalue assets, this covenant was replaced in FY80 under the Third WAPDAPower Project (Cr. 968-PAK) by an internal cash generation covenant whichrequires WAPDA to generate annually from internal sources 40% of the invest-ment, averaged over the previous two years and the current year withouttaking into account the net changes in working capital. WAPDA was able tocomply with this covenant until FY85 with minimal tariff increases(para 4.04), but only because of substantial slippages in its investmentprogram. It was in the context of these slippages and the accompanyingshortfalls in generating capacity that agreement was reached with WAPDA underthe Fourth WAPDA Power Project (Ln. 2499-PAK) on a Rs 30 billion Core Invest-ment Program (CIP) for the period FY86-FY88 (para 4.06).

Accounting Systems and Organization

4.02 Under previous Bank Group operations (Ln. 1208T-PAK and Cr. 968-PAK),WAPDA engaged Peat, Marwick, Mitchell and Co. (PMM) of UK as consultants tostudy the financial organization and make recommendations to improve theutility's financial management, particularly in the areas of accountingsystems and procedures, and organization and staffing. The study, which wascompleted in FY82, recommended the introduction of a modern accruals basedaccounting system with a code of accounts, the updating of inventory manage-ment methods and the streamlining of financial reporting procedures. Theserecommendations were implemented by PMM in FY83 and FY84 and as a result,WAPDA's revenue billing and collection, and control over its finances haveimproved significantly. In addition, the appointment of General Manager andDeputy General Manager for Finance has strengthened the overall financialfunction and enhanced its role within WAPDA. In order to sustain this momen-tum, WAPDA, under financing from USAID, has engaged EBASCO Services, AmericanElectric Power Energy Services and International Training and EducationCompany, US firms, is consultants to carry out additional work in the areas

1/ WAPDA maintains complete and separate accounts for the Power Wing. Thefinancial analysis and discussions in this chapter are confined to theoperations of WAPDA's Power Wing, which for ease of reference is referredto as WAPDA.

-20-

of Fixed Asset Accounting (para 4.08), Internal Audit (para 4.15) and train-ing of staff (paras 2.03 and 4.14).

Past Operations

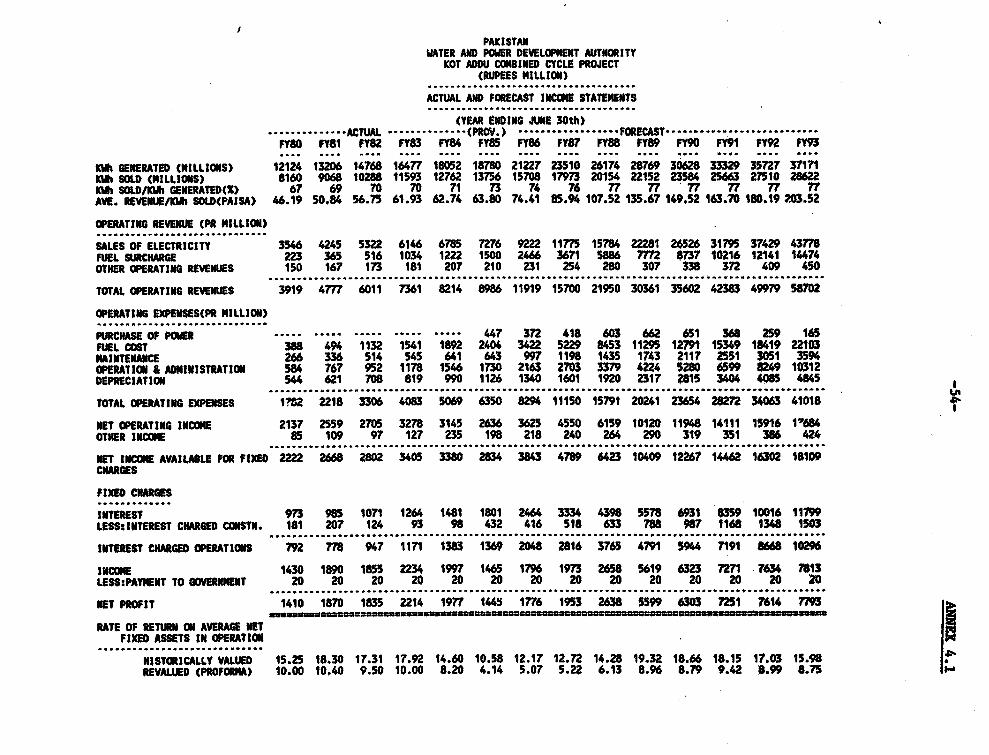

4.03 Financial statements showing WAPDA's performance during the periodFY80-FY85, are presented in Annexes 4.1, 4.2 and 4.3, and summarized inTable 4.1:

Table 4.1: Operating Results FY80-FY85

Year Ending June 30 FY80 FY81 FY 82 FY83 FY84 FY85(prov)

kWh generated (million) 12,124 13,206 14,768 16,477 18,052 18,780kWh sold (million) 8,160 9,068 10,288 11,593 12,762 13,156System losses (%) 33 31 30 30 29 27Avg. rev/kWh sold,including fuel surcharge 46 51 57 62 63 64

Operating Rev. (Rs million) 3,919 4,777 6,011 7,361 8,214 8,986Operating Exp. (Rs million) 1,782 2,218 3,306 4,083 5,069 6,350Operating Income (Rs million) 2,137 2,559 2,705 3,278 3,145 2,636Net income after int.and payment to Govt.(Rs million) 1,410 1,870 1,835 2,214 1,977 1,445

Self-financing ratio(3 yr. Avg.) (%) 56 65 82 70 47

Rate of Return:Historically valued assets (Z) 15.3 18.3 17.3 17.9 14.6 10.6Revalued assets (proforma) (X) 10.0 10.4 9.5 10.0 8.2 4.1

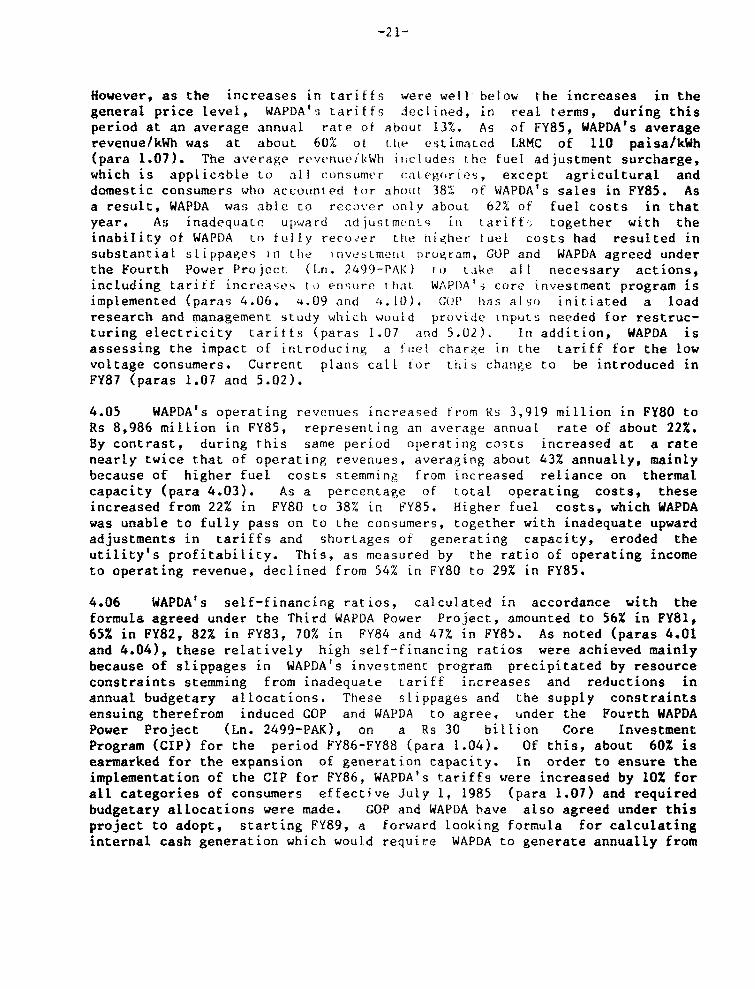

WAPDA's electricity generation increased from 12,124 GWh in PY80 to18,780 GWh in FY85; however, because of the overall shortage of generatingcapacity precipitated by resource constraints (para 1.02) and the poorhydrological conditions, particularly in FY84 and FY85, the rate of growth ofgeneration declined from an average of about 10.PZ between FY80 and FY83 toabout 6.8% between FY84 and FY85. The poor hydrological conditions alsonecessitated the increased use of thermal capacity and, as a result, itsshare in total generation increased from 28% in FY80 to 35% in FY85, whilethat of hydro declined correspondingly. As WAPDA was able to reduce systemlosses from 33% of gross generation in FY80 to 27% in FY85, by extending andupgrading the transmission network (paras 1.11 and 1.13) and by streamliningand strengthening billing/collection operations, its electricity salesincreased at a higher rate of growth than generation, averaging about 12% ayear.

4.04 WAPDA's tariffs were increased from 46 paisa/kWh in FY80 to 64paisa/kWh in FY85, representing an average annual increase of about 7Z.

-21-

However, as the increases in tariffs were well below the increases in thegeneral price level, WAPDA'S tariffs declined, in real terms, during thisperiod at an average annual rate of about 13%. As of FY85, WAPDA's averagerevenue/kWh was at about 60% of Lthe estimated LRMC of 110 paisa/kWh(para 1.07). The average rovenuei'kWh it;cludes the fuel adjustment surcharge,which is applicable toi all consumer C(ategories, except agricultural anddomestic consumers who accouttnted ttr abolut 38%r of WAPDA's sales in FY85. Asa result, WAPDA was able to recover onlv about 62% of fuel costs in thatyear. As inadequate upward adjustmentns in tariff; together with theinability of WAPDA to fully recov'er the nigher tuel costs had resulted insubstantial stippages in thle investLMenL prugram, GOP and WAPDA agreed underthe Fourth Power Proiect (L.n. 2499-PAK) t) tLake all necessary actions,including tariff increases to ensure that WAPI)A'-i core investment program isimplemented (paras 4.06. 4.09 and 4.101). GOP has also initiated a loadresearch and management study wlhich would provide inputs needed for restruc-turing electricity tariffs (paras 1.07 and 5.02). In addition, WAPDA isassessing the impact of introducing a fuel charge in the tariff for the lowvoltage consumers. Current plans call for this change to be introduced inFY87 (paras 1.07 and 5.02).

4.05 WAPDA's operating revenues increased from Rs 3,919 million in FY80 toRs 8,986 milLion in FY85, representing an average annual rate of about 22%.By contrast, during this same period operating costs increased at a ratenearly twice that of operating revenues, averaging about 43% annually, mainlybecause of higher fuel costs stemming from increased reliance on thermalcapacity (para 4.03). As a percentage of total operating costs, theseincreased from 22% in FY80 to 38% in FY85. Higher fuel costs, which WAPDAwas unable to fully pass on to the consumers, together with inadequate upwardadjustments in tariffs and shortages of generating capacity, eroded theutility's profitability. This, as measured by the ratio of operating incometo operating revenue, declined from 54% in FY80 to 29% in FY85.

4.06 WAPDA's self-financing ratios, calculated in accordance with theformula agreed under the Third WAPDA Power Project, amounted to 56% in FY81,65% in FY82, 82% in FY83, 70% in FY84 and 47% in FY85. As noted (paras 4.01and 4.04), these relatively high self-financing ratios were achieved mainlybecause of slippages in WAPDA's investment program precipitated by resourceconstraints stemming from inadequate tariff increases and reductions inannual budgetary allocations. These slippages and the supply constraintsensuing therefrom induced GOP and WAPDA to agree, under the Fourth WAPDAPower Project (Ln. 2499-PAK), on a Rs 30 billion Core InvestmentProgram (CIP) for the period FY86-FY88 (para 1.04). Of this, about 60% isearmarked for the expansion of generation capacity. In order to ensure theimplementation of the CIP for FY86, WAPDA's tariffs were increased by 10% forall categories of consumers effective July 1, 1985 (para 1.07) and requiredbudgetary allocations were made. GOP and WAPDA have also agreed under thisproject to adopt, starting FY89, a forward looking formula for calculatinginternal cash generation which would require WAPDA to generate annually from

-22-

internal sources 40% of its investment averaged over the previous, currentand succeeding years, after taking into account the changes in working capi-tal.

4.07 During the period FY80-FY83, WAPDA's revenues and net income keptpace with increases in its asset base, thereby enabling the utility toachieve an average rate of return of 17% on historically valued assets and10% on revalued assets. In FY84 and FY85, however, the rate of returndeclined to 14.6% and 10.6% on historically valued assets and 8.2% and 4.1%on revalued assets. This decline in rates of return is attributable to:(a) the commissioning of large assets during those two years, particularlyhydro capacity; and (b) the erosion of WAPDA's profitability (para 4.05).Moreover, as some of WAPDA's assets were underutilized during FY84 and FY85,particularly hydro units and the associated transmission lines, WAPDA'saverage net fixed assets in use are overstated relative to the revenue gener-ated. The rates of return -n FY84 and FY85, therefore, should be viewed asunderstated return. WAPDA's financial projections for the period FY86-FY93,in fact, show that the rates of return on revalued assets is expected toimprove, but is unlikely to exceed 8% because capacity shortages are forecastto continue into the mid-1990s (paras 2.04 and 5.02). This implies thatincreases in operating revenues will continue to increase Gver the foresee-able at a slower pace than the increases in assets.

Present Financial Position

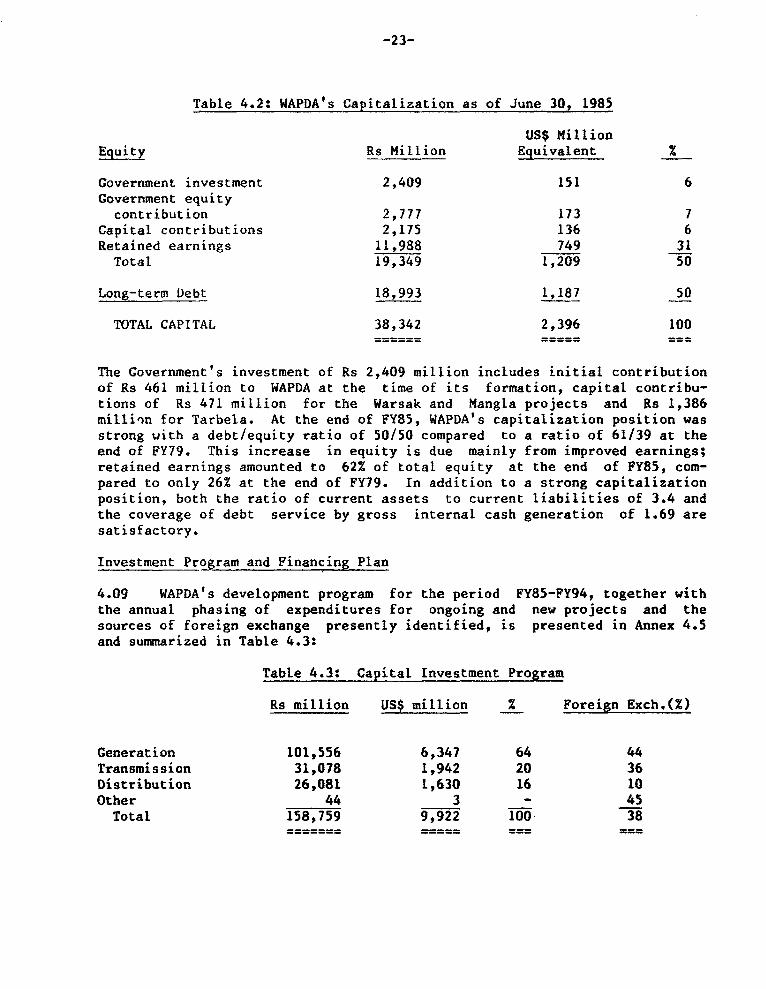

4.08 Balance sheets showing WAPDA's financial position are presented inAnnex 4.1. The book value of fixed assets is shown at historical cost, asrequired by GOP. As a large proportion of WAPDA's electricity supplyfacilities (generating plant, and transmission and distribution networks)were commissioned during the last few years, its gross fixed assets in serv-ice increased between FY80 and FY85 by about 115%, 60% of which were financedfrom WAPDA's internal sources and 40% from borrowings. WAPDA is currently inthe process of establishing a system that will classify fixed assets bycategory and form the basis for the formulation of appropriate depreciationschedules (para 4.02). This work is expected to be completed by June 30,1986. Until such time, an average rate of depreciation of about 3.5% isbeing applied, which is considered adequate by the Bank. WAPDA's capitaliza-tion as of June 30, 1985 is summarized in Table 4.2:

-23-

Table 4.2: WAPDA's Capitalization as of June 30, 1985

US$ MillionEquity Rs Million Equivalent X

Government investment 2,409 151 6Government equitycontribution 2,777 173 7

Capital contributions 2,175 136 6Retained earnings 11,988 749 31Total 19,349 1,209 50

Long-term Debt 18,993 1,187 50

TOTAL CAPITAL 38,342 2,396 100

The Government's investment of Rs 2,409 million includes initial contributionof Rs 461 million to WAPDA at the time of its formation, capital contribu-tions of Rs 471 million for the Warsak and Mangla projects and Rs 1,386millinn for Tarbela. At the end of FY85, WAPDA's capitalization position wasstrong with a debt/equity ratio of 50/50 compared to a ratio of 61/39 at theend of FY79. This increase in equity is due mainly from improved earnings;retained earnings amounted to 62% of total equity at the end of FY85, com-pared to only 26% at the end of FY79. In addition to a strong capitalizationposition, both the ratio of current assets to current liabilities of 3.4 andthe coverage of debt service by gross internal cash generation of 1.69 aresatisfactory.

Investment Program and Financing Plan

4.09 WAPDA's development program for the period FY85-FY94, together withthe annual phasing of expenditures for ongoing and new projects and thesources of foreign exchange presently identified, is presented in Annex 4.5and summarized in Table 4.3:

Table 4.3: Capital Investment Program

Rs million US$ million % Foreign Exch.(%)

Generation 101,556 6,347 64 44Transmission 31,078 1,942 20 36Distribution 26,081 1,630 16 10Other 44 3 - 45Total 158,759 9,922 100 38

-24-

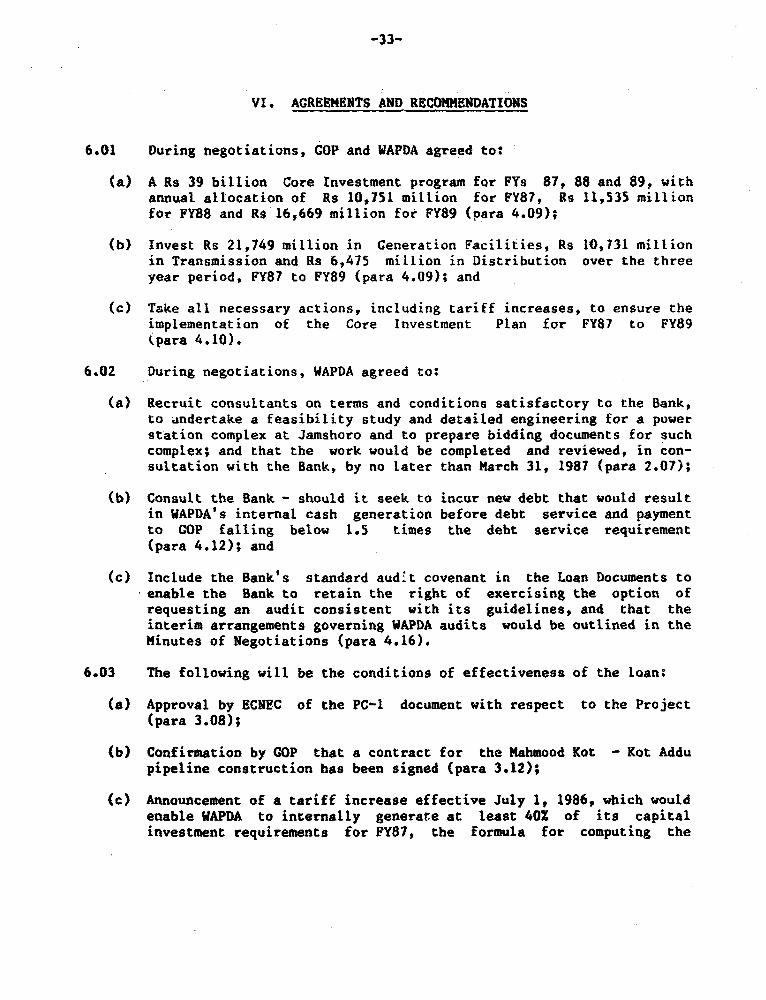

Of the total investment program, about 64% is earmarked for the expansion ofgenerating capacity, 20% for the extension and reinforcement of the transmis-sion system and 16% for the distribution system. As substantial investmentshave already been made in the development of transmission (paras 1.11 and1.13) and distribution facilities (para 2.11), and because slippages weremost acute in the commissioning of new generating capacity, a relativelylarger share of the resources are earmarked for their expansion. The Bankhas reviewed the investment plan for its content, size and allocation, andfinds it satisfactory. In order to ensure that WAPDA's system continues todevelop along the least cost path, GOP and WAPDA agreed under the Fifth WAPDAPower Project (Cr. 2556-PAK) to an annual investment review with the Bankwhich would result in a rolling three year CIP, starting with the coreprogram for FY86-FY88 (para 4.06). AccordingLy, GOP and WAPDA agreed to aCIP of Rs 39 billion for FY87, FY88 and FY89, with annual allocation ofRs 10,751 million for FY87, Rs 11,535 million for FY88 and Rs 16,669 millionfor FY89 (para 6.01(a)) and to invest over the three year period Rs 21,749million in generation, Rs 10,731 million in transmission and Rs 6,375 millionin distribution facilities (para 6.01(b)).

4.10 The purpose of the CIP is to identify high priority projects andensure that resources are made available for their implementation. Thesources of financing for the CIP covering the period FY87-FY89 are summarizedin Table 4.4:

Table 4.4: Financing Requirements and Sources During FY87-FY89

Rs million US$ million x

Requirements

Capital Investment 38,955 2,435 91Working Capital Increase 3,827 239 9Total Requirements 41,782 2,674 100

Sources

Gross Internal Sources 30,025 1,876Less: Debt Service andPayment to Government 15,560 972

Net Internal Cash Generation 14,465 904 34BorrowingsGOP Loans 11,290 706 26Foreign Loans 15,782 9&6 37Proposed Loan 1,245 78 3Total Borrowings 28,317 1,770 66

Total Sources 41,782 2,674 100

-25-

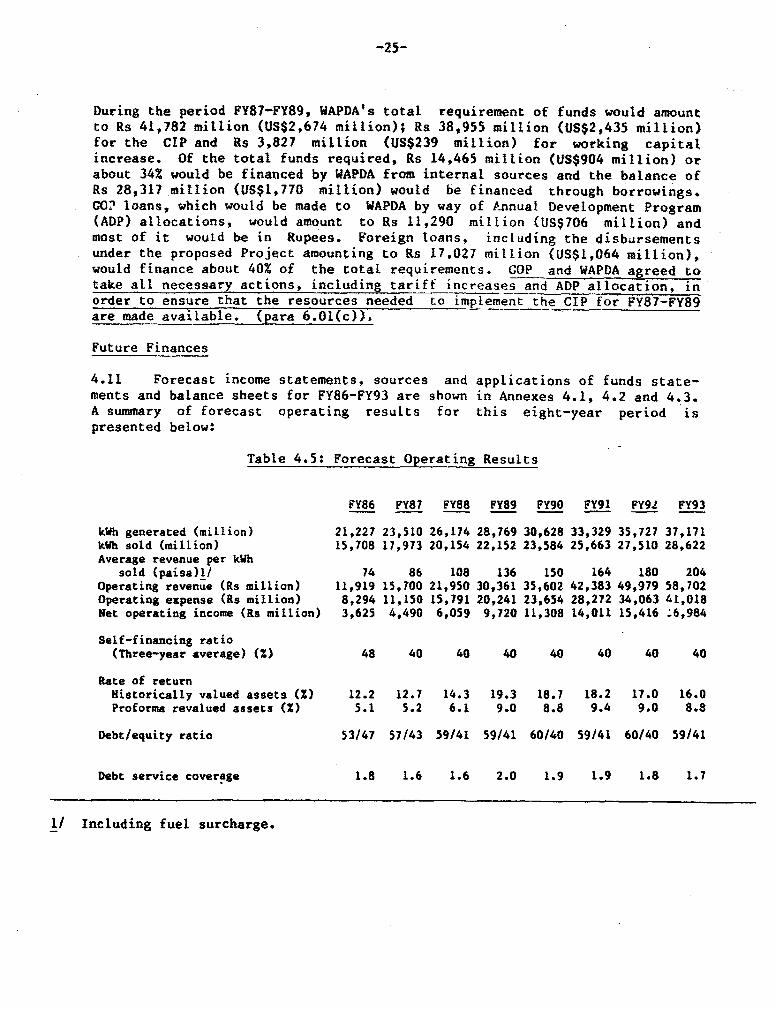

During the period PY87-FY89, WAPDA's total requirement of funds would amountto Rs 41,782 million (US$2,674 million); Rs 38,955 million (US$2,435 million)for the CIP and Rs 3,827 million (US$239 million) for working capitalincrease. Of the total funds required, Rs 14,465 million (US$904 million) orabout 342 would be financed by WAPDA from internal sources and the balance ofRs 28,317 million (US$1,770 million) would be financed through borrowings.GO! loans, which would be made to WAPDA by way of Annual Development Program(ADP) allocations, would amount to Rs 11,290 million (US$706 million) andmost of it would be in Rupees. Foreign loans, including the disbursementsunder the proposed Project amounting to Rs 17,027 million (US$1,064 million),would finance about 40% of the total requirements. COP and WAPDA agreed totake all necessary actions, including tariff increases and ADP allocation, inorder to ensure that the resources needed to implement the CIP for FY87-FY89are made available. (para 6.01(c)).

Future Finances

4.11 Forecast income statements, sources and applications of funds state-ments and balance sheets for FY86-FY93 are shown in Annexes 4.1, 4.2 and 4.3.A summary of forecast operating results for this eight-year period ispresented below:

Table 4.5: Forecast Operating Results

FY86 FY87 FY88 FY89 FY90 FY91 FY92 FY93

kWh generated (million) 21,227 23,510 26,174 28,769 30,628 33,329 35,727 37,171kWh sold (million) 15,708 17,973 20,154 22,152 23,584 25,663 27,510 28,622Average revenue per kWh

sold (paisa)l/ 74 86 108 136 150 164 180 204Operating revenue (Rs million) 11,919 15,700 21,950 30,361 35,602 42,383 49,979 58,702operating expense (Rs million) 8,294 11,150 15,791 20,241 23,654 28,272 34,063 41,018Net operating income (Rs million) 3,625 4,490 6,059 9,720 11,308 14,011 15,416 :6,984

Self-financing ratio(Three-year average) (X) 48 40 40 40 40 40 40 40

Rate of returnHistorically valued assets (X) 12.2 12.7 14.3 19.3 18.7 18.2 17.0 16.0Proforma revalued assets (Z) 5.1 5.2 6.1 9.0 8.8 9.4 9.0 8.8

Debt/equity ratio 53/47 57/43 59/41 59/41 60/40 59/41 60/40 59/41

Debt service coverage 1.8 1.6 1.6 2.0 1.9 1.9 1.8 1.7

1/ Including fuel surcharge.

-26-

WAPDA's financial projections are based on increases in electricity gener-ation and tariffs, and a reduction in system losses. Electricity generationis forecast to increase at an average annual rate of 8.9% and electricitysales by 9.6%, reflecting a sustained decrease in system losses. In orderfor WAPDA to continue to self-finance not less than 40% of its capitalinvestment program to meet the financial performance covenant, forecaststhrough FY93 show that it would need to increase tariffs at an average annualrate of about 15% in nominal terms, amounting to about 8% in real terms,assuming a forecast average annual inflation rate of 7%. The financialforecasts for FY87, in particular, show that a 11% increase in average tariffeffective July 1, 1986. is needed to satisfy the 40% self-generation covenantfor FY87. In order to ensure that adequate resources are available for theimplementation of the Rs 10,751 million Core Investment Plan for FY87, GO?and WAPDA agreed that the announcement of a tariff increase which woulienable WAPDA to finance at least 40% of its capital investment requirementsfor FY87 from internal sources, computed in accordance with the internal casheneration formula drawn up under the Third WAPDA Power Project(Cr. 968-PAK), would be a condition of loan effectiveness (para 6.03(c)).

4.12 Forecast balance sheets (Annex 4.3) show that WAPDA's gross fixedassets are expected to increase from Rs 35,019 million in FY85 to Rs 149,731million at the end of FY93. About 40% of the increase would be financed fromWAPDA's internal sources and 60% from borrowings. As a result, equity isexpected to increase by three and one-half times, from Rs 19,349 million inFY85 to Rs 67,671 million in FY93, 85% of this increase attributable toretained earnings. Long-term debt is forecast to increase fivefold, fromRs 18,992 million to Rs 99,095 million, resulting in a debt/equity ratio inFY93 of 59/41, which is reasonable for an electric utility. The coverage ofdebt service by gross internal cash generation would be satisfactory duringthis period as would the ratio of current assets to current liabilities.Nevertheless, in order to ensure that WAPDA's debt service coverage by grossinternal cash generation continues to be satisfactory, the debt limitationcovenant under the Fourth WAPDA Power Project (Ln. 2499-PAK) is repeatedunder the project, which provides that WAPDA would consult the Bank should itseek to incur new debt that would result in WAPDA's gross internal cashgeneration before debt service and payment to GOP falling below 1.5 times thedebt service requirement (para 6.02(b)).

Financial and Commercial Operations

4.13 WAPDA's distribution department is one of the largest commercialundertakings in Pakistan with annual sales in FY85 of 14 GWh to over 4.5million consumers, and billing and collections amounting to some Rs 750million each month. This magnitude of operation requires efficient finan-cial/commercial systems and capable staff to operate them. WAPDA, however,has been unable to recruit qualified mid- to high-level accounting staffbecause its current rules stipulate that such positions be filled by promot-ing individuals from within WAPDA. In order to address this constraint, new

-27-

WAPDA Accounting Service Rules have now been drafted which would permit therecruitment of mid- to high-level accounting staff from outside WAPDA, and acommittee is reviewing them before presentation to the Authority forapproval. Once these rules are approved, WAPDA will be able to recruitqualified financial staff to fill required positions at both headquarters andthe eight AEBs where the shortage of qualified staff is particularly acute.WAPDA plans to have these rules approved and put into effect, beginningJuly 1, 1986.

4.14 WAPDA continues to make progress in streamlining and strengtheningits financial/commercial operations with substantial support from USAID underits Power Distribution Project (paras 2.11 and 4.02) which includes a largetraining component. This project is timely in that it complements theinstitution-building work carried out by WAPDA under Bank-financed projects(paras 1.10 and 4.02). WAPDA, USAID and the Bank are closely coordinatingtheir institution building activities. Annex 4.6 summarizes work beingcarried out under the Power Distribution Project in the financial/commercialareas.

Internal Audit