World Bank Documentdocuments.worldbank.org/curated/en/639131468333839199/...Power 56 V. Education 61...

165

DOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT INTERNATIONAL DEVELOPMENT ASSOCIATION Not For Public Use Report No. 74-PAK ECONOMIC SITUATION AND PROSPECTS OF PAKISTAN (in four volumes) VOLUME I THE MAIN REPORT February 16, 1973 Asia Region - Country Programs 2A This report was prepared for official use only by the Bank Group. It may not be published, quoted or cited without Bank Group authorization. The Bank Group does not accept responsibility for the accuracy or completeness of the report. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of World Bank Documentdocuments.worldbank.org/curated/en/639131468333839199/...Power 56 V. Education 61...

DOCUMENT OF INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENTINTERNATIONAL DEVELOPMENT ASSOCIATION

Not For Public Use

Report No. 74-PAK

ECONOMIC SITUATION AND PROSPECTS

OF PAKISTAN

(in four volumes)

VOLUME I

THE MAIN REPORT

February 16, 1973

Asia Region - Country Programs 2A

This report was prepared for official use only by the Bank Group. It may not be published, quotedor cited without Bank Group authorization. The Bank Group does not accept responsibility for theaccuracy or completeness of the report.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

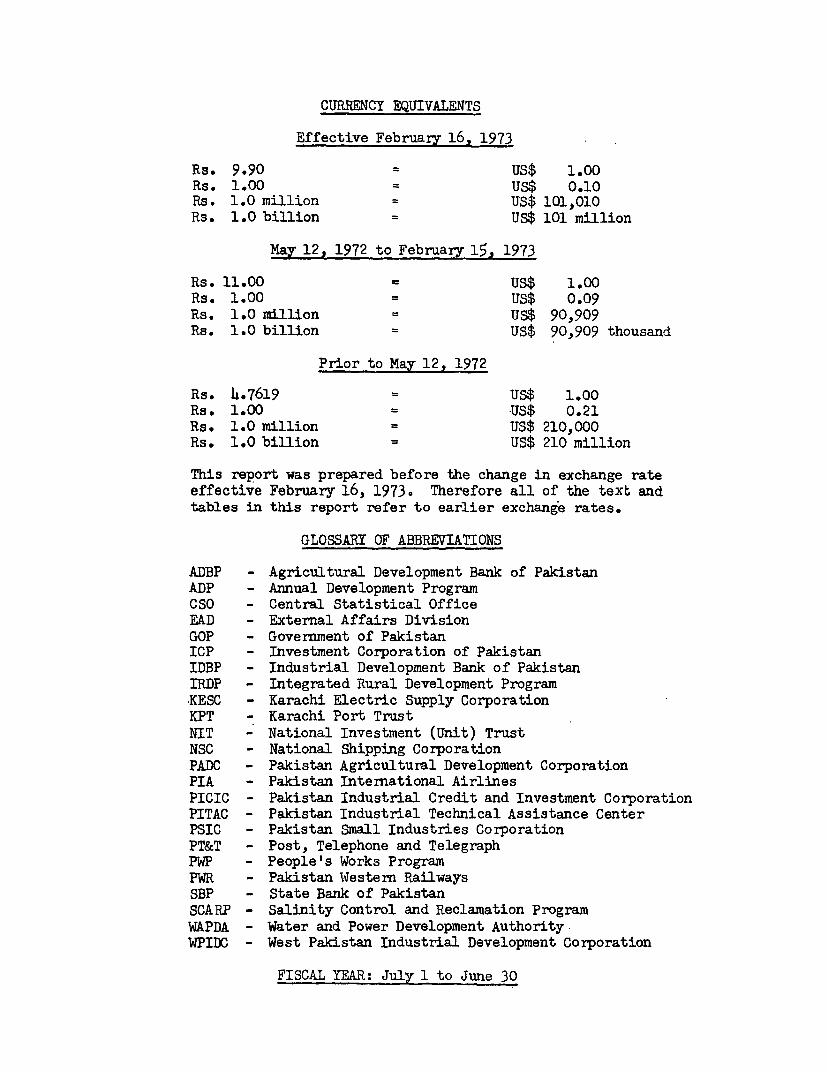

CURRENCY EQUIVALENTS

Effective February 16, 1973

Rs. 9.90 US$ 1.00Rs. 1.00 US$ 0.10Rs. 1.0 million US$ 101,010Rs. 1.0 billion US$ 101 million

May 12, 1972 to February 15, 1973

Rs. 11.00 TUS$ 1.00Rs. 1.00 US$ 0.09Rs. 1.0 million US$ 90,909Rs. 1.0 billion US$ 90,909 thousand

Prior to May 12, 1972

Rs. 4.7619 = US$ 1.00Rs. 1.00 = US$ 0.21Rs. 1.0 million US$ 210,000Rs. 1.0 billion US$ 210 million

This report was prepared before the change in exchange rateeffective February 16, 1973. Therefore all of the text andtables in this report refer to earlier exchange rates.

GLOSSARY OF ABBREVIATIONS

ADBP - Agricultural Development Bank of PakistanADP - Annual Development ProgramCSO - Central Statistical OfficeEAD - External Affairs DivisionGOP - Government of PakistanICP - Investment Corporation of PakistanIDBP - Industrial Development Bank of PakistanIRDP - Integrated Rural Development ProgramKESC - Karachi Electric Supply CorporationKPT - Karachi Port TrustNIT - National Investment (Unit) TrustNSC - National Shipping CorporationPADC - Pakistan Agricultural Development CorporationPIA - Pakistan Intermational AirlinesPICIC - Pakistan Industrial Credit and Investment CorporationPITAC - Pakistan Industrial Technical Assistance CenterPSIC - Pakistan Small Industries CorporationPT&T - Post, Telephone and TelegraphPWP - People's Works ProgramPWR - Pakistan Western RailwaysSBP - State Bank of PakistanSCARP - Salinity Control and Reclamation ProgramWAPDA - Water and Power Development Authority-WPIDC - West Pakistan Industrial Development Corporation

FISCAL YEAR:-July 1 to June 30

This report is based on the findings of an economicmission which visited Pakistan in October-November 1972. Itsmembers were:

Gilbert T. Brown Chief of MissionSalah El Serafy Deputy Chief of Mission and Trade

and Balance of Payments EconomistBijaya B. Pradhan General EconomistMarinus van der Mel Fiscal and Monetary EconomistRalph H. Hofmeister Employment and Education EconomistWilliam H. Edwards Agriculture SpecialistJulian Blackwood Agriculture/Water Economist

(Consultant)John Schnittker Agriculture Economist

(Consultant)Richard C. Taylor Agriculture EconomistBernard Decaux Industrial Economist

(Consultant)Toshikazu Nasu Industrial EconomistTillman H. Neuner Transportation EconomistMahfouz E. Tadros General EconomistJoseph E. Gholl Population and Family Planning

SpecialistElizabeth M. McLeod Secretary

In addition, J. Hanns Pichler, Resident Representative,participated very activily in arranging for and in the work ofthe mission, and carefully reviewed the draft report.

ECONCaIC SITUATION AND PROSPECTSOF PAKISTAN

Table of Contents

Page No.

COUNTRY DATA

SUMMARY AND CONCLUSIONS i - vii

I. Recent Developments and Prospects 1

Introduction 1Economic Performance 4Saving and Investment 6Short and Medium Term Outlook 8

II. Employment, Unemployment and Income Distribution 12

Size and Strmeture of the Labor Force 12Unemployment and Underemployment 13Prospects for Employment and Unemployment 15Towards an Employment Strategy 18Income Distribution 24

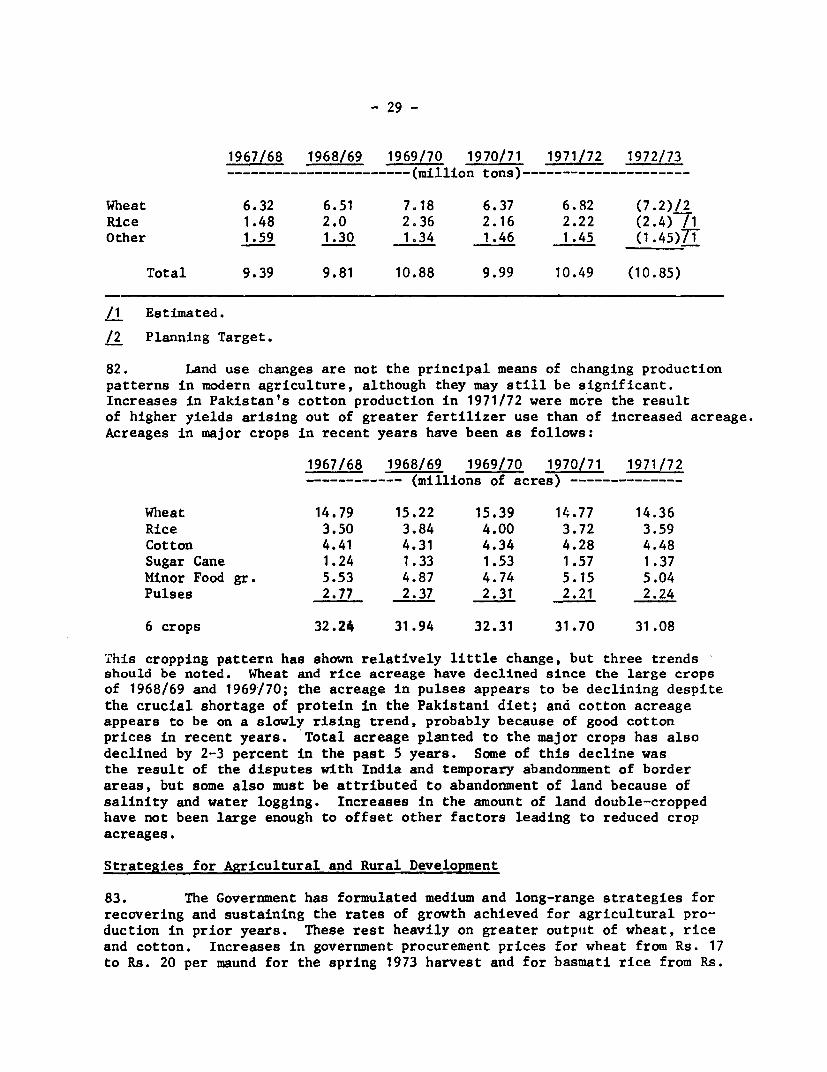

III. Agriculture: Strategy and Problems 28

Introduction 28Strategies for Agricultural and Rural

Development 29Pricing Inputs and Outputs 30Fertilizers 32Seeds 33Water 34The Salinity Control and ReclamationProgram (SCARP) 35

Rainfed Agriculture 37Farm Mechanization 39Agricultural Credit 40Land Reform and Protection of the

Rights of Tenants 41People's Works Program 42Integrated Rural Development Program 43

IV. Industry, Transport and Power 46

Industrialization of Pakistan - an overallview 46

Page No.

Strategy for Industrialization 47Industrial Finance 51Public Sector Enterprise Effectiveness 52Transport 53Power 56

V. Education 61

Targeted Expansion 61Past Budgetary Support 64Financial Implications of the New Policy 66Comments on the Educational Policy 70Institutional Means for Policy-Making n1

VI. Population, Family Planning and Health 73

Population 73Family Planning 74Health 75

VII. Public Finance 77

Introduction 77Budget Structure 781972/73 Budget 79Current Revenues 79Non-Development Expenditures 81Annual Development Programs 811972/73 Budget Prospects 84Longer-term Budget Prospects and Problems 85

VIII. Money, Banking and Credit 97

Introduction 97Monetary and Credit Trends 97Banking Reforms 99Interest Rates 101Term Lending Institutions and Capital Market 101

IX. External Debt 1iO

External Public Sector Debt 104Terms and Sources of Loans 104Unilateral Moratorium and Short-term Debt Relief 105Effect of the 1972 Debt Rescheduling 107Debt Service Ratios 107Need for Debt Relief 108

Page No.

X. The Balance of Payments and Growth Requirements 110

Introduction 110Recent Developments 110Balance of Trade 112The Effect of Devaluation 113Prospects for Trade 116Invisibles 118Aid Inflow 118

XI. Growth Potential and Foreign Financing Requirements 119

Growth Potential 119Financing Requirements 122

MAP

* * *

VOLUME II STATISTICAL APPENDIX

VOLUME III AGRICULTURE

VOLUME IV INDUSTRY

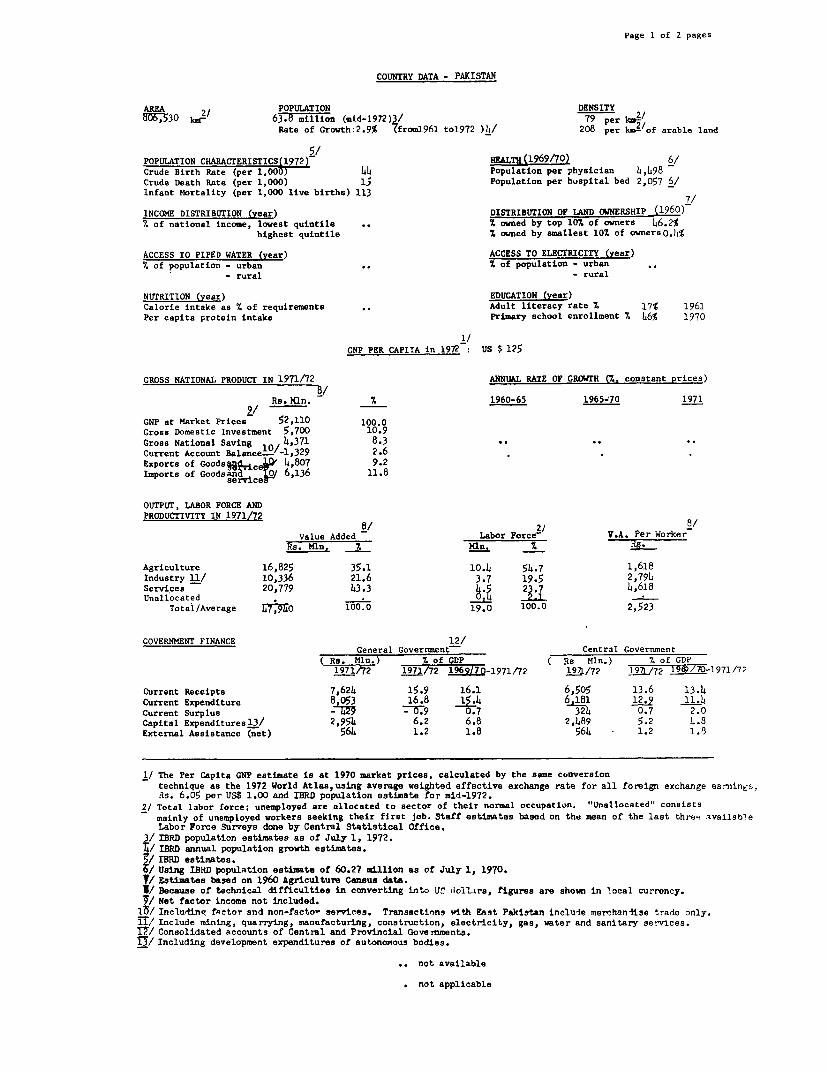

Page I of 2 pageS

COUNTRY DATA - PAKISTAN

AREA 2/ POPULATION DENSITY85F,53O k- 63.8 million (mid-1972)3/ 79 per kmIo

Rate of Growth:2.9% Tfroml961 to1972 )4/ 208 per kin-/of arable land

5/POPULATION CHARACTERISTICS(1972) HEALTH(1969t70) 6/Crude Birth Rate (per 1,000) 44 Population per physician 4,498Crude Death Rate (per 1,000) is Population per hospital bed 2,057 6/Infant Mortality (per 1,000 live births) 113 7/

INCOME DISTRIBUTION (year) DISTRIBUTION OF LAND OWNERSHIP (1960)% of national income, lowest quintile .. % owned by top 10% of owners 46.2%

highest quintile % owned by smallest 10% of ownerso.4%

ACCESS TO PIPED WATER (year) ACCESS TO ELECTRICITY (year)% of population - urban .% of population - urban

- rural - rural

NUTRITION (year) EDUCATION (year)Calorie intake as % of requirements .. Adult literacy rate % 173 1961Per capita protein intake Primary school enrollment % 46% 1970

_ /CNP PER CAPITA in 1972 US $ 125

GROSS NATIONAL PRODUCT IN 1971/72 ANNUAL RATE OF GROWrH (%. constant prices)8/

Re.Mln. I 1960-65 1965-70 1971Z/ - __

GNP at Market Prices 52,110 100.0Gross Domestic Investment 5,700 10.9Gross National Saving 4,371 8.3Current Account Balance1

O/-1 329 2.6Exports of Goods : 1 0ie i 4,807 9.2Imports of Goodsana i 6,136 11.8

OUTPUT, LABOR FORCE ANDPRODUCTIVITY IN 1971/72

8/ 2/ 8/Value Added Labor Force- V.A. Per Worker

Rs. Mln. % Mlm. % 7..

Agriculture 16,825 35.1 10.4 54.7 1,618Industry 11/ 10,336 21.6 3.7 19.5 2,794Services 20,779 43.3 4.5 23.7 4,618Unallocated . 04 I.2.1 .

Total/Average T MO 100.0 19.0 100.0 2,523

GOVERNMENT FINANCE 12/General Government Central Government

Rs. Mln.) % of GDP ( Re Mln.) /. of GDP1971 2 1971/72 1969/70-1971 72 !27/72 i271/72 l969/7-1971/72

Current Receipts 7,624 15.9 16.1 6,505 13.6 13.4Current Expenditure 8 053 16.8 15.4 6 181 12.9 11.4Current Surplus - 4 - 9 0.7 32L4 0.7 2.0Capital Expendituresl3/ 2,954 6.2 6.8 2,489 5.2 8.8External Assistance (net) 5644 1.2 1.8 564 1.2 1.6

1/ The Per Capita GNP estimate is at 1970 market prices, calculated by the same conversiontechnique as the 1972 World Atlas,using average weighted effective exchange rate for all foreign exchange earnings.Rs. 6.05 per US$ 1.00 and IBRO population estimate for mid-1972.

2/ Total labor force; unemployed are allocated to sector of their normal occupation. "Unallocated" consistsmainly of unemployed workers seeking their first job. Staff estimates based on the mean of the last thre" availableLabor Force Surveys done by Central Statistical Office.

3/ IBRD population estimates as of July 1, 1972.14/ IBRD annual population growth estimates./ IBRD estimates./ Using IBND population estimate of 60.27 m3llion as of July 1, 1970./ Estimates based on 1960 Agriculture Censua data.1/ Because of technical difficulties in converting into 'JS dollars, figures are shown in local currency.§/ Net factor income not included.

15/ Includine Netor end non-factor servi"es. Transactions with EAst Pakistan include merchandise trade only.iT/ Include mining, quarrying, manufacturing, construction, electricity, gas, water and sanitary services.T1/ Consolidated accounts of Central and Provincial Dovernments.13/ Including development expenditures of autonomous bodies.

not available

not applicable

Page 2 of 2 pages

COUNTRY DATA - PAKTSTAI

June June1964/65 1968/69 1969/70 1970/71 1971/72 1971 1972MONEY. CREDIT and PRICES

(Million rupesoutstanding end period)

Money and Quasi Money 18,9773Bank Credit to Public Sector 12 607-Bank Credit to Private Sector 13,8333/

(Percentages or Index Numbers)

Money and Quasi Money as % of GDP 4/ .. .. 5/ 36.4l 6/General Price Index (1962/63 * 100) 109.8 125.4 1?8.8 136.2 144.4 Sept 1971- Sept 1972 -Annual percentage changes in: 141.6 162.6General Price Index 4/ +4.2 -0.4 .2.7 +5.7 +6.0 +4.0 + 12.6Bank credit to Public SectorBank credit to Private Sector

7/BAEAfC: OF PAYMEN';

9/MERCHANDISE EXPORTS (AVERAGE1969/7O-197i/72)

t9 ')/70 1970/71 197:tMillions of US $) US $ Mln %Receipts 525 584 772 Raw Cotton 89.7 19.9Merchandise Exports 3m0 T7 07 Cotton yarn 74.7 16.5Invisibles 175 141 165 Cotton Cloth 6J.9 211.?Payments 1,131 1 176 1,009 Rice 33.7 7.2Merchandise Imports 690 :75 646 Leather and leather goods 32.7 7.2Invisibles 229 229 234 Fish 17.7 3.RPublic Sector (158) (155) (152) All other conmodities 140.0 31.0Private Sector ( 71) ( 74) ( 82) Total 45l.4 TOO 0Debt Service (after debt 212 191 129

relief) EXTERNAL DEBT, DECEMBER 31. 1971Overall Deficit 606 592 237Financed by:

US $ MlnForeign Aid 347 416 186Use of Official Reserve3 51 83 14 Public Debt, incl. guaranteed 3,636Errors and Omissions 208 93 37 Non-Guaranteed Private Debt -

Total outstanding & Disbursed 3,6J 10/

DEBT SERVICE RATIO for 1_971/72

June June June1970 1971 1972 Public Debt, incl. guaranteed 16.7

Nan-Guaranteed Private Debt -Gross Reserves (end year)8/ 230 176 183 Total outstanding & Disbursed T 7Tl1/Net Reserves (end year)

RATE OF EXCHANGEIBR/ID LEDIN.Deemner 1. 972Million US$Through _May 1921-

121/US $ 1.00 = Re. 4.7619 IBRD IDARs. 1.00 = US $0.21Prom May 12 572 to February 15, 1973 Outstanding & Disbursed 327 264S$1.0-R.1.UU Undihbursed 62 go

Rs. 1.00 = US $ 0.09 Outstanding incl. Undisbursed 389 363Since - Feb 16 1973US $ 1.00 t R 15 9.9Rs. 1.00 = US $ 0.10

1/ Ratio of Debt Service to Exports of Goods and Factor and Non-Factor Services.2/ Rough estimate for present Pakistan.7/ Figures need downward adjustment because of separation of Sast Wing.1/ Implicit GDP deflator; for September 1971 and 1972 iinkei with changes in wholesale price index.:/ Change between FY 1970/71 average and September 1971, using wholesale price index./ Change between FY 1971/72 average and September 1972, usinG wholesale price index.7/ Excluding merchandise and service transactions with East Pakistan.

e/ Goli and fbreign exchange reserve held by the State Bank of Pakistan and net IMF position.7/ Excluding exports to East Pakistan.l:/ Total external debt outstanding (disbursed only) relate to combinei West and East wings of former Pakistan.11/ Actual debt service papments (inclusive of East Pakistan) related to West Pakistan's foreign exchange earninpsonly. Payments due exclusive of debt moratoriun and vhort-tern -escheduling were 32%.1I/ Those loans and credits which were intended for disbLrsen3nt in both Wings are treatet as fo. ':ost Padi-i,nonly.

not. ava_:ablenot applic:able

SUMMARY AND CONCLUSIONS

Introduction

i. The period since the last Bank Economic Report (SA-15a dated July17, 1970) has been one of profound change for Pakistan. Fourteen years ofmilitary rule came to an end in December 1971 after the conflict with Indiaand the separation of East Pakistan. There was a morale crisis, and uncer-tainty about both Pakistan's international position and the change from aconservative military to a progressive parliamentary government. The popula-tion is now about 65 million rather than 130 million; 1/ members of theNational and Provincial Assemblies were popularly elected in December, 1970(one year before assuming power); the former West Pakistan now consists offour provinces; and the new government is emphasizing social justice andimprovement in the position of lower income groups (such as urban workersand small farmers) more than economic growth for its own sake.

ii. The Pakistan economy underwent considerable strains during theyears 1970/71 and 1971/72, reflecting political events, foreign exchangeshortages and a prolonged drought. Separation meant severing of the unifiedmarket and economic relations. Markets, sources of supply and assets werelost. The drought was primarily responsible for the failure of agriculturalproduction to increase by more than one percent over the two year period.Industrial production declined by about one percent as a result of powershortages, labor troubles and increasingly tight import restrictions. Withpopulation growing at perhaps 2.9 percent annually, the decline in per capitaproduction of physical goods has been about 6 percent, though the decline inper capita GDP is estimated at less than 3 percent because of increaseddefense and other current government egpenditures. Reduced per capita out-put, budget deficits, repatriation of money from East Pakistan, and risingwage rates contributed to wholesale price increases of about 18 percent inthe year ended last September. Inflationary pressures appear to have lessened,but there is still concern about food prices and the budget deficit.

iii. Numerous economic and social reform measures have been adopted inresponse to these pressures. The government has taken over management (butnot ownership) of the 31 largest firms in 10 "basic" industries, managingagency agreements have been declared invalid, life insurance companies havebeen nationalized, and legislative and administration actions taken to increasecontrol over commercial banks. Land reform legislation, strengthening thelegal and economic position of tenant farmers, has been enacted. Many laborlaw changes have been made to guarantee the right to collective bargainingand give job security and welfare benefits to workers. Integrated RuralDevelopment and People's Works Programs have been started, along with newinitiatives in education and health.

1/ The term Pakistan is used in this report, unless otherwise specificallynoted, to refer to the present nation of Pakistan, i.e., the formerWest Pakistan. GDP, balance of payments and other data have beencalculated for former West Pakistan.

- ii -

iv. In May 1972, the government took a long over-due action whichprevious governments had considered but not acted on by devaluing the rupeeand liberalizing import restrictions. The official exchange rate was changedfrom Rs. 4.76 per dollar to Rs. 11. Actual average increases, compared withprevious multiple exchange rates and including adjustments in import dutiesand sales taxes and the introduction of export duties, were 24 percent inthe rupee price of major agricultural exports, 23 percent in the rupee priceof industrial exports, and 40 percent in the average rupee price of imports.Import prices of capital equipment were approximately doubled, and the costof servicing foreign debt rose by 131 percent. Except for banned goods andgoods tied to particular foreign aid or barter sources, most quantitativeimport restrictions were also dropped at the time of devaluation. While"temporary" export duties on 17 commodities and heavy subsidies of the retailprices of wheat, fertilizer and insecticides have not yet allowed prices onthese commodities to fully reflect devaluation, exports and imports haveboth reacted favorably to devaluation. Pakistan's trade deficit for 1972/73is expected to be about $200 million, and then rise to $250 million to $300million annually over the next several years. These correspond with tradedeficits for West Pakistan from 1965 to 1971 of about $250 million per year,but with tighter import restrictions.

Development Strategy

v. Pakistan's most urgent requirement is for increased levels ofoutput and employment. The most promising sources of demand to sparkrevival are from increased agricultural output and incomes, growth of exports,increased government spending on development and a renewal of private invest-ment to meet growing demand and capacity limitations. It is also necessarythat future growth be labor-intensive and export-oriented to make moreefficient use of abundant supplies of labor and to increase the supply offoreign exchange. Devaluation has been a major step in this direction.Aggressive promotion of exports through technical and marketing assistance(including quality control) to those exporters requiring it, and removal ofthe disincentives of export duties, and the constraints imposed by inadequatecredit, power, storage, port and transportation facilities, will also helpgenerate sustained export and production increases. Other measures that needto be taken include the generation of substantially more non-inflationaryrupee financing for both current and capital account government expendituresfor development purposes, greater credit and other resource availabilitiesto increase productivity in medium and small scale farming and industry,technical assistance to small farmers and manufacturers, and increased privatesaving and investment. Unemployment and underemployment are sufficientlyserious that in agriculture particularly it will be important to preventlarge-scale displacement of labor by over-mechanization. Present tax andother incentives encouraging capital good investment in industry need to bere-examined and perhaps replaced by incentives to employ labor.

Employment

vi. While there are no satisfactory measurements of unemployment andunderemployment, best estimates are that this figure is between 20 percentand 30 percent. Open unemployment is much higher among the educated than

- Lii -

among the uneducated, partly reflecting the higher faiiily incomes of theformet. One-third of recent engineering graduates have been estimated tobe unemployed.

vii. Harsh demographic realities dominate employment prospects inPakistan. Most of the labor force of the 1980's is here already, and familyplanning efforts cannot substantially affect growth of the labor force untilafter 1990. It appears that annual growth of the labor force will rise froma present rate of 2.8 percent to a peak of 3.2 percent in the late 1980'sand early 1990's. Optimism about quickly reducing unemployment and under-employment must be tempered by realization of the rapid growth of productionthis would also require.

viii. Special employment generating programs such as the People'sWorks Program (PWP) can directly provide only a small fraction of the addi-tional employment needed. If these programs provide productive infrastructure(e.g. irrigation or feeder road projects), increase the productivity ofhuman beings (e.g. safe drinking water and education), or mobilize additionalprivate resources (e.g. use of public resources to mobilize much greaterprivate saving for housing), however, their total contribution to employ-ment and output may be much greater than provided directly by their ownbudgets.

ix. Income distribution data for Pakistan are scanty, but there isconsiderable evidence to support the judgement that the income distributionbecame increasingly skewed during the 1960's. Rapid growth of productiveemployment would reduce present income disparities, as would increased avail-abilities of education, public transport, agricultural extension and otherpublic services to lower income groups. Adequate production and suppliesof basic consumption goods will also be important to this objective.

Agriculture and Water

x. Both employment and income distribution prospects hinge importantlyon the agricultural sector. Projected economic growth, increased exportsand employment are expected to result in increased demand for the produce ofagriculture, including foodstuffs and fibers, by at least 5 percent perannum. A sustained rate of agricultural growth of this order could beachieved, and substantial growth of employment provided, but this will bemore difficult to accomplish than were the "green revolution" increases ofthe late 1960's, which reflected primarily increased output from the largerfarms. Both employment and production goals require that the new technologybe extended to medium and small scale farms; this requires face-to-facetechnical assistance, credit for (and adequate supplies of) purchased inputs,research on non-cereal crops and non-irrigated farming, a policy to achievelabor-intensive mechanization, and improved marketing opportunities forsmaller farmers. The type of mechanization that accompanies increasedagricultural production will be an important determinant of the growth ofagricultural employment and perhaps of income distribution also.

xi. The most immediate increases in agricultural output (in a yearor less) can be achieved through ample supplies of productive inputs and

- iv -

through higher (closer to free market) prices for those products of whichprices are directly or indirectly regulated by the government. The benefitsderived from fertilizer, pesticide and other agricultural input subsidies arealso questionable. The cost-benefit ratios are such that even the smallfarmers need primarily more credit and available supplies - not subsidies -to increase their use of fertilizer. Thus the production benefits of thissubsidy may well be negative (through reduced supplies). The doubling offertilizer application to cotton when the price of the crop was raised in1971/72 suggests that fair market prices for crops may do more to increaseuse of fertilizer than will direct input subsidies. Cost-benefit ratiosare also high on insecticides, but many farmers still need to be convinced.

xii. The availability of water (in some cases over-availability resultingin salinity and water logging) is a critical, limiting factor in agriculturalproduction in Pakistan, and the efficient use of water and avoidance ofunnecessary wastage is crucial. Maximum benefits require integrated nationalplanning for use of all 8surface and groundwater. Public tubewells have afundamental role to play in salinity control and reclamation program (SCARP)projects, and may have important advantages in fresh groundwater area develop-ment as well.

Industry

xiii. Industrial development patterns will also be an important deter-minant of economic and employment growth. In manufacturing, the predominantindustrial sector, registered enterprises (employing more than 10 workers)are believed to account for about three-fourths of ouput but only aboutone-fourth of employment. Very little is known about unregistered manufac-turing. Most of it is in household scale units, with only family memberworkers. In order to avoid substantial product and labor displacementby large scale manufacturing (with seriously adverse effects on the growthof total employment), credit, marketing and technical assistance should beprovided to as many small producers as possible.

xiv. Employment growth in registered manufacturing will depend uponthe speed with which higher rates of utilization of existing capacity areachieved, and the degree to which new investment is in labor intensivesectors and uses labor-intensive techniques. Restoration of private sectorconfidence, modernization and balancing investment to equalize capacity ofsuccessive stages of production, promotion of exports and further liberaliza-tion of imports will all facilitate increased use of existing capacity. Muchof this unused capacity exists because of past exchange rate distortions anderratic availability of imported materials. Export growth is particularlyattractive since Pakistan's comparative advantage appears to lie primarilyin labor-intensive products, thus meeting the twin goals of employment andexchange earning. Forward integration of the textile industry into finishedgoods and apparel production, and development of leather goods production,are two of the most promising export areas. Increased output of capitalequipment is a labor-intensive activity that should find an increaseddomestic market and might become an important export, particularly to theextent that it is designed to take advantage of low labor costs and isadjusted to maintenance and other problems common in developing countries.

Domestic Resource Mobilization and Use

xv. Now that the exchange rate has been adjusted (though some relatedprice adjustments have yet to be made), increased mobilization of domesticrescurces has become the key economic issue. Greater government revenuesare needed for developmental programs, and to reduce the inflationarypressure from the budget deficit. Increased public and private savings arealso needed for investment in economic infrastructure and in agriculturaland industrial production capacity. It will be necessary to mobilize therequired resources by non-inflationary methods since, because of the inelasticnature of Pakistan's budget revenues, inflation would reduce rather than in-crease public saving, as well as have other undesirable effects. Between1969/70 and 1971/72 national saving estimates declined from 13.3 percent toonly 8.4 percent of GDP, with public saving declining by 2.3 percent of GDP(to minus one percent) and private saving declining by 2.6 percent of GDP(to 9.4 percent). Gross private fixed investment in 1971/72 is estimatedat only 4.2 percent of GDP, or less than enough to offset depreciation.Public sector investment of 5.4 percent was financed entirely (along withthe current account budget deficit) by domestic borrowing and foreign savings.

xvi. Increased private saving is closely tied to economic revival,the restoration of private confidence, and increased nominal and real ratesof return on fixed-income financial assets. The decline in public savingsreflects rising current expenditures (defense, debt service, price subsidyincreases following devaluation and government salaries) and the inelasticnature of tax revenues. Sharp increases in defense spending (from 6.2 per-cent to 7.3 percent of GDP) and a more than doubling of foreign debt service(as a result of devaluation plus rising debt) have absorbed nearly 90 percentof the projected increase in central government current expenditures in the1972/73 budget compared with 1970/71 actual expenditures. MIost of the growthin money incomes has escaped taxation because of failure to tax the growthof agricultural incomes, personal and business income tax exemptions intendedto encourage private saving, investment and exports, and tax evasion. Recentlegislation reducing some tax exemptions and eliminating others, plus self-assessment of income and other administrative improvements, may help solvethe government revenue and saving problems. The failure to earn any significantrate of return on the large investment in public enterprises also continuesto limit public sector saving.

xvii. Improvement of resource use is also possible by correcting theremaining price distortions, increasing domestic saving and exports andredirecting some government expenditures. Devaluation has helped by improvingprivate sector price incentives. A little explored but relevant question isthe efficiency of government expenditures. That substantially greaterbenefits can be achieved within existing levels of government expendituresis suggested by such facts as that over half of public educational expendi-tures are at secondary and higher levels, that urban services have beenprovided much more generously to high income rather than low income neighbor-hoods, and that most agricultural subsidies and government services havegone only to large scale farmers.

- vi -

Balance of Payments and Aid Requirements

xviii. The rapid growth of exports suggests considerable underlyingstrength in Pakistan's balance of payments. Exports from then West Pakistanto foreign countries (excluding East Pakistan) grew by 12 percent annuallybetween 1965/66 and 1970/71, though total exports (i.e. including those tothe East Wing) were growing only by 6.6 percent. In 1971/72 exports toforeign countries rose by nearly 40 percent, and for the first 5 months of1972/73 (through November) are running about 23 percent above last year,but much greater raw cotton exports and diversion to foreign markets of goodspreviously sold in East Pakistan have accounted for the larger part of theseincreases. Nevertheless, devaluation has sufficiently increased the attrac-tiveness of exporting that annual growth of perhaps 12 percent seems possiblefor the next several years.

xix. Import licensing and arrivals suggest an import level of about$850 million for 1972/73, or just slightly above annual 1966-71 levels.In addition to projected annual trade deficits of $250 million to $300 mil-lion for the next several years, the deficit on invisibles plus privatetransfers, after this year, may be only moderately above $100 million.Since the latter amount is also approximately the annual interest chargeon Pakistan's foreign debt, it is useful to think of Pakistan's totalforeign financing requirements for the next several years as equal to thetrade deficit plus both the interest and principal burden of foreign debtservice. Without any relief from present debt obligations through eithera division of the debt with Bangladesh or a rescheduling with creditors,that debt burden is expected to rise to $370 million in 1974/75 solely toservice debt outstanding at the end of 1971, or to nearly $400 million, ifaccount is taken of probable new debt obligations. This gross financingrequirement within two years of $650 million to $700 million, of which only$250 million to $300 million would represent net receipts, and the factthat debt service would constitute nearly 40 percent of expected exchangeearnings, indicate the size and importance of the external debt issue.

xx. If foreign financing of this amount is forthcoming, it seemsreasonable to expect that Pakistan's gross domestic product may grow about7 percent per year. This would require some improvement in past ratios ofthe growth of output to new investment, but no more than seems reasonableto expect as the result of devaluation and import liberalization, whichhave removed incentives to build idle industrial capacity. It will alsorequire a marginal saving rate of at least 20 percent, which is substantiallyabove the estimated rate since 1965. Achievement of such a marginal savingrate will depend upon both measures to increase public saving and anattractive environment for private saving. To achieve a relatively lowinvestment to growth of output ratio (and reduce Pakistan's serious un-employment) will probably require a primarily labor-intensive and perhapsexport-led growth pattern.

xxi. This analysis of growth requirements has two important implicationsfor foreign creditors. One is that annual net foreign financial inflows of$250 million to $300 million may be difficult to achieve unless and until avery substantial reduction can be made in Pakistan's prospective interest

- vii -

and p-irr pal-4ehA-service burden of nearly $400 mi-llior-by-1974/75.-'heother is that the desirable growth pattern forseen for Pakistan, with fullerutilization of existing capacity, labor-intensive new investment andincreased productivity of small and medium scale manufacturers and farmers,will require a substantial portion of foreign assistance to be providedeither as program aid or as local currency project financing. If most aidwere to finance capital good imports, there would be severe shortages offoreign exchange to maintain the present degree of import liberalization,and of local currency to carry out new and expanded developmental and socialservice programs.

I. RECENT DEVELOPMENTS AND PROSPECTS

A. Introduction

1. The period since the last Bank Economic Report (SA-15a datedJuly 17, 1970) has been one of profound change for Pakistan. Fourteenyears of military rule came to an end in December 1971 after the conflictwith India and the separation of East Pakistan, when the leader of WestPakistan's majority political party assumed the Presidency. Thus thePakistan of this Report is geographically the former West Pakistan only,and there are many other differences. 1/ The population is now about 65million rather than 130 million;, members of the National and ProvincialAssemblies have been popularly elected, the former single province ofWest Pakistan has been divided into four provinces, and the new governmentis emphasizing social justice and improving the position of lower incomegroups (such as urban workers and small farmers) rather than economic growthfor its own sake.

2. The consequences of the separation of the former East and Westwings into two separate countries have been very great. Some of theobvious economic consequences have been the complete severing of alleconomic ties between two areas which, by virtue of having been a singlecountry, were also largely an integrated economic unit sharing the samecurrency, and the free flow of goods, persons and capital. The integrationwas not quite complete because of their physical separation and somedifferences in taxes and tariffs intended to encourage investment in theEast rather than the West wing. Thus the West found itself cut off fromthe market for more than one third of its exports and the source of one-sixth of its imports. Assets invested in commercial and industrial facili-ties in the East were suddenly beyond the control or reach of owners in theWest. Monetary and fiscal affairs were greatly disturbed.

3. On a deeper level there was stunned disbelief about eventsleading up to and including military defeat and the separation of theEast Wing. The loss of life and continuing detention of 90,000 prisonersof war affected many families. Future relations with India and Bangladeshand the future nature of West Pakistan itself were also in doubt. Thegovernment that took over in December 1971 had been elected on a programof "Islamic Socialism"; calling for fundamental social, economic andpolitical reforms. Opposition parties had won the 1970 elections in twoof the four provinces that were in the process of being established priorto December 1971, however, and questions of national unity were thereforeraised.

1/ The term Pakistan is used in this report, unless otherwise specificallynoted, to refer to the present nation of Pakistan, i.e,, the formerWest Pakistan. GDP, balance of payments and other data have beencalculated for former West Pakistan.

- 2 -

4. Thus the problems facing the restructured nation and economy havebeen many. These have included restoring national morale, unity and senseof direction, negotiating a border agreement with India, seeking to gain therelease of the prisoners of war, and finding a new basis of relation-ship with India and Bangladesh. Issues of social and economic justice, suchas had embittered relations between the East and West wings, had also beensensitized within the West. In general the poor felt exploited by the rich:laborers by mill owners, farmers by industry, small farmers and businessmenby the large, and less developed regions by the more developed.

5. A number of eccnomic and social reform measures have been adoptedin response to these pressures. In January 1972, the government announcedthat it was taking over management (but not ownership) of the 31 largest firmsin 10 "basic" industries. 1/ The "managing agency" system was prohibitedand all existing agreements declared invalid. 2/ All life insurance companieswere nationalized. Legislative and administrative actions were taken toincrease taxation of commercial banks and to make credit more accessible tosmall farmers and businessmen. A land reform was announced that reducedthe amount of land that could be held by an individual (though only very largefarms were affected), and also gave tenants certain rights to their land andrequired owners rather than tenants to bear certain taxes and cultivationexpenses. A very large number of labor legislation measures were passed toguarantee workers the right to collective bargaining, to give employees jobsecurity, to provide certain welfare benefits such as post-Drimary leveleducation for one child, and health, severance and retirement benefits, andgenerally to change the nature of labor-management relations toward greater

equality. An integrated rural development program (IRDP) has been started,and this is intended within a few years to bring adequate credit, know-how andmarketing opportunities to all farmers. A People's Works Program (PWP) isalso getting underway to provide employment plus useful economic and socialinfrastructure and in some cases new production capacity as a result of jointlocal and provincial-central government cooperation. Other actions includea program to provide medicines to all on a low-cost basis and nationalizationof most private educational institutions in order to improve quality standards.

6. The Fourth Plan has been scrapped as no longer relevant, dealingas it does with both wings. An Annual Development Plan for 1972/73, completedin October 1972, tries to capture the present direction and short-run budgetimplications of government policies. Work on a new five year plan, totake effect from july 1974, is just beginning.

7. In May 1972, the government took a long over-due action whichprevious governments had considered but not acted on by devaluing the rupee

1/ Iron and steel, basic metals, heavy engineering, heavy chemicals,motor vehicle assembly and manufacture, tractor assembly and manufac-ture, heavy and basic chemicals, petro-chemicals, cement and publicutilities. See Chapter V.

2/ Managing agency contracts gave full control over company affairs toa minority ownership group of insiders.

-3-

and liberalizing import restrictions. The official exchange rate was changedfrom Rs. 4.76 per dollar to Rs. 11, with actual average increases, comparedwith previous multiple exchange rates, of about 24 percent in the rupee priceof major agricultural exports, 23 percent in the rupee price of industrialexports, and 40 percent in the rupee price of imports. 1/

8. Despite the changes, there is still much that is the same inthe new Pakistan. The war caused minor physical damage in the West - someships sunk, damage to Karachi port and to a fertilizer factory and loss of200,000 acres of farmland not evacuated by India until December, 1972. Thebasic infrastructure of power, water and transportation is little changed,except that new construction has been greatly reduced in the last two yearsand the systems are working closer to capacity. Power will be in seriouslyshort supply until at least 1975/76. The nature of political power andeconomic relationships between the Central Government and the Provinces isstill at issue, although this is a less serious problem since it now concernsonly the four provinces in the former West Wing. Agreement in October, 1972by leaders of all political parties represented in the National Assembly onthe outline of a draft national constitution further defused this issue,though several major issues have subsequently arisen.

9. While devaluation and liberalization have reduced many pricedistortions, others remain because of the imposition of export duties andincreased subsidization of the retail price of wheat to prevent the priceeffects that otherwise would have followed from devaluation. Subsidies onsuch agricultural inputs as fertilizer, pesticides and water are alsocontributing to the serious shortage of domestic resources. Many otherformer problems also continue. There have been improvements in tax law andadministration, but the long standing needs to meaningfully tax agriculturalincome and to increase urban real estate taxes still remain. Governmententerprises continue to generate extremely small surpluses and remain abudgetary burden, while shortages of funds are severely limiting the govern-ment's ability to carry through on pledges of expanded education, health,rural development and other social and development projects. Unemploymentand underemployment are massive and growing problems, and along with risingfood prices and the lack of urban facilities have continued to foster urbanunrest. The "Green Revolution" has by and large, reached only the largerfarmers. There is still much underutilization of industrial capacity.

10. Pakistan still faces many difficult questions in its relations withBangladesh and India. Major internal political and economic issues remain.In comparison with December 1971, however, much progress has been made inat least establishing a basis for solution to these problems. Progress onfundamental political issues should now make it possible for national energiesto be focused increasingly on economic problems. Devaluation has brightenedeconomic growth prospects. Pakistan's immediate problem is that of recoveringfrom an economic recession that has continued since 1970. Agriculturalproduction during 1972/73 is expected to be well above levels of the past

1/ These percentages include adjustments to export duties and importand sales taxes.

two years, and the beginnings of industrial recovery also seem to beoccurring. Longer run prospects suggest the possibility of substantialfurther growth in agricultural productivity in conjunction with rapid export -

led industrial growth if major remaining economic policy problems are solved.Solution of Pakistan's severe unemployment and underemployment problems anddevelopment of national health, education and rural development programs,however, will take time.

B. Economic Performance

11. The present Pakistan economy (i.e. former West Pakistan) grewrapidly during the first half of the 1960's with GDP increasing at 6.7percent per annum. This high growth rate was spearheaded by an industrialgrowth rate of 11.6 percent per annum; large-scale industries grew at aneven higher rate of 13.8 percent. However, the agricultural sector grewat a modest annual rate of 3.7 percent. Pakistan's overall economicperformance slowed down somewhat in the second half of the decade to 6.2percent, as the rate of industrial growth fell to 8 percent, but theagricultural sector grew 5.6 percent annually with the aid of new high-yieldingwheat and rice varieties, bringing the country to the threshold of self-suffi-ciency in food. Following the 1965 War with India, however, both public andprivate saving declined. The level of net foreign aid also declined overthe same period as increasingly larger portions of aid were utilized in EastPakistan and as debt service charges rose rather rapidly. As a consequence,gross investment is estimated to have fallen from about 22 percent of GDPin 1964/65 to about 17 percent in 1969/70 and only 11 percent in 1971/72(Table I.2).

12. The Pakistan economy underwent severe strains during the years1970/71 and 1971/72, reflecting both political events and a prolonged droughtwhich reduced the total increase in agricultural output for these two yearsto about one percent (Table I.1). As agriculture accounts for one-thirdof GDP, and is the major source of industrial raw materials, this contributedto a general economic recession, made worse after 1970 by the loss of markets,assets and sources of supply in East Pakistan. Industry also experiencedincreasing difficulties in getting foreign raw material and spare part importsas foreign exchange difficulties forced the government to tighten importrestrictions and to declare a unilateral moratorium on a large portion of itsexternal debt payments from MIay 1, 1971. Power shortages and mounting laborunrest further curtailed industrial production. Reduced aid, the diversionof resources to defense and rising debt service forced the Government to curtaildevelopment expenditures. The uncertain economic and political situation alsoreduced private investment.

13. During these two years overall GDP grew by only 3.3 percent, whilepopulation increased by about 5.8 percent so that per capita income declined.Furthermore, the GDP increase came largely in defense, public administrationand other service sectors.

- 5 -

Table I.1: ECONOMIC GROWTH RATES(Percent Per Annum at Constant Factor Cost)

Second Third AnnualPlan Period Plan Period (Provi- Plan

Annual Annual sional) Target1960-1965 1965-1970 1969-70 1970-71 1971-72 1972-73

Agriculture 3.7 5.6 6.4 -1.7 2.8 5.1Major Crops (4.7) (7.5) (9.8) (-5.6) (3.0) (7.0)Others (2.7) (3.3) (2.1) (3.7) (2.5) (3.0)

Manufacturing 11.6 8.0 11.2 2.8 -3.8 12.6Larlge Scale (13.8) (9.9) (13.9) (2.8) (-5.6) (15.6)Small Scale (2.6) (2.6) (2.6) (2.7) (2.6) (2.6)

Construction 22.0 5.7 3.0 2.4 -5.5 10.0Trade 8.5 6.6 8.6 -0.1 -1.2 5.2The Rest /1 6.8 6.1 4.8 6.4 6.0 5.4Gross DomesticProduct 6.7 6.2 6.9 1.6 1.7 6.6

/1 Including estimates of unallocable GDP originating from PIA (Transportand Communications), Central Public Administration, Defense andBanking and Insurance.

Source: CSO, Planning Commission and Staff estimates.

The production of goods in Pakistan was almost unchanged between 1969/70 and1971/72. 1/ At constant factor prices, value added in agriculture roseabout one percent during these two years, while value added in manufActuringfell in the same proportion. The resulting decline in per capita availabilityof goods has been accentuated by a decline of imports and a rise in exports.Since there has also been a substantial increase in money supply since early1971, and cost increases from devaluation and rising wages, it is notsurprising that the wholesale price index rose about 18 percent and theconsumer price index about 10 percent from September 1971 to September 1972.There is considerable official optimism that inflation has now largelyspent itself, but concern continues over food prices and the budget deficit.

14. The decline in agricultural production between 1969/70 and 1971/72reflected primarily a lack of adequate river and canal water supplies becauseof less tharn normal rainfalls in the Himalayas and the batani (rainfed)areas. The war also played a part the second year in disrupting fertilizersupplies and driving farmers off valuable farmlands on the Indian border.Agricultural production during 1971/72 would have slumped markedly except forthe increase in cotton production.

1/ As previously noted, data given here and elsewhere refer to the presentnation of Pakistan, i.e., the former West Pakistan only, unless other-wise specifically noted.

- 6 -

15. Industrial production has been much depressed during 1972 withlittle recovery evident through October, the latest month for which data areavailable. The two key factors holding down production have been strikesand labor unrest on the one hand, and the hesitancy of businessmen to investor undertake long-term commitments on the other. The sympathy of the newgovernment for labor encouraged workers to organize and to resort to strikes.The fact that Pakistan has not previously had strong unions has meant lack ofestablished union organization and discipline, and competition between thosevying for union leadership. On the job discipline declined in some casesbecause workers felt less likely to be laid off. However, after numerousstrikes between June and October, centered in the Karachi textile industry area,labor management relations seem to have entered a more peaceful phase. Majorlabor legislation changes seem to be complete, and the government is pointingout the many benefits that workers have obtained this year through legislationand fringe benefits as well as wage increases, and calling on workers to increaseproductivity and to resort to strikes only after legal procedures have beencomplied with and bargaining has failed.

16. Private sector lack of confidence and unwillingness to invest hasalso reflected uncertainties about governmental intentions to further nation-alize or otherwise control the private sector. While private sector fearshave not been fully put to rest, they have been lessened. The President hasrepeatedly stated that achievement of the socialist goals of his party's platformwill be an evolutionary process spread over a number of years rather than arevolutionary one, and that he plans no further nationalization of industryduring his present five-year term of office. Criticism of past businesspractices has also diminished in recent months, and businessmen have beenincreasingly urged to assist in expanding national output. The government isalso showing more concern for the problems of business, including effortsto provide adequate credit to firms whose financial positions were temporarilyweakened by devaluation (because of the 131 percent increase in foreign debtservice charges) or substantial losses of assets, markets or sources ofsupply in the former East Wing.

D. Saving and Investment

17. The seriousness of Pakistan's 1/ domestic resource mobilizationproblem is indicated by the steady decline in rates of savings and invest-ment since 1964/65, the last year of the Second Plan, when domestic savingreached 13.5 percent of GDP and gross investment, 22.5 percent (and grossfixed investment 21.1 percent). Domestic savings fell from 13.3 percent in1969/70 to 8.4 percent in 1971/72, and foreign saving from 9.0 percent in1964/65 to 3.3 percent in 1969/70 (Table I.2).

1/ These data, as others in the report, refer only to the economy offormer West Pakistan.

Table I.2: INVESTMENT AND SAVINGS RATES(Percent of GDP)

(Target)1964/65 1969/70 1970/71 1971/72 1972/73

Gross Investment(Including changesin stocks) 22.5 16.6 15.0 10.9 15.1

FinancingForeign Savings(Current AccountBalance) 9.0 3.3 3.4 2.5 7.3Domestic Savings 13.5 13.3 11.6 8.4 7.8Private Savings .. (12.0) (10.5) (9.4) (8.2)Public Savings .. (1.3) (1.1) (-1.0) (-0.4)

Gross FixedInvestment 21.1 15.1 13.6 9.6 13.4Private Sector 11.4 7.7 7.2 4.2 5.6Public Sector 9.7 7.3 6.4 5.4 7.8Indus (3.7) (2.3) (1.5) (1.9) (2.0)Others (6.0) (5.0) (4.9) (3.5) (5.8)

Source: 1964/65, staff estimates from West Pakistan data; 1969/70 andlater data from Planning Commission.

l

18. The larger part of the domestic decline was in private saving, forreasons of political and economic uncertainty already discussed. The lowlevel of public saving throughout this period reflects partly the inelasticnature of tax revenues. Because there is no significant agricultural incometax, the very substantial growth of larger farmer income in the second halfof the sixties went untapped. Much of the growth in urban personal andbusiness income has also been tax-exempt or taxed only lightly because ofconcessions intended to encourage private saving, investment and exports aswell as because of tax evasion. As a result, the Government has steadilyincreased tax rates and coverage with but little increase in revenues asa percent of GDP. (Recent tax reforms lowering or abolishing many suchexemptions, however, should increase tax revenues in 1973/74). The declinein public saving has also reflected rapid growth of current expenditures fordefense, debt service, subsidies and civil service salaries. The low rateof return on the huge capital investment in public enterprises has alsocontributed to low public revenues and savings.

19. Gross investment fell sharply during the 1965-70 Third Planperiod. The largest part of the drop reflected the decline in aid followingthe outbreak of war with India, the increasing proportion of aid used inEast Pakistan, and the rising level of debt service. The inflow of foreignsavings to West Pakistan fell from 9 percent of GDP in 1964/65 to 3.3 percentin 1969/70, and gross fixed investment fell by about the same absolute

- 8 -

amount, from 21 percent of GDP to 15 percent. Public sector investmentfell from 9.7 percent of GDP in 1964/65 to 6.4 percent in 1970/71, and huge

demands of the Indus/Tarbela project required other public investment programs

to be cut back even more sharply. Gross private fixed investment in agricul-

ture is estimated to have grown by only 4.2 percent annually in current prices

between 1964/65 and 1970/71, or very little, if at all, in constant prices.

Gross private fixed investment in large-scale manufacturing industry remainedalmost unchanged in current prices. Private investment declined after the1965 war, then rose in 1967-69, after which it declined again following the

ouster of Ayub Khan and increased political and economic uncertainty. The

decline of fixed investment to only 9.6 percent in 1971/72 reflected, of

course, the sharp decline in domestic savings and investment following the

outbreak of war in East Pakistan.

20. The share of GDP going to both private and public consumptionhas increased since 1969/70. As a percent of estimated West Pakistan GDP,

total defense expealditures rose from 4.4 percent in 1964/65 to 6.1 percent

in 1969/70 and 8.2 percent in 1971/72; they are being cut to about 7.3 percent

in 1972/73.

CONSUMPTION RATES(Percent of GDP)

1964/65 1969/70 1970/71 1971/72 1972/73(Target)

Consumption 86.5 86.7 88.4 91.6 92.2Private Consumption 76.2 77.8 79.3 79.4

Public Consumption 10.5 10.6 12.3 12.8

Short and Medium Term Outlook

21. Production levels have failed to show much improvement over the

preceding year through October-November 1972. Nevertheless, good agricultural

production prospects, strong export demand, and profitable import substitution

production possibilities, particularly in capital goods, are reasons to

believe that economic activity has already or will shortly pick up, and that

the latter part of 1972/73 could be the beginning of a period of verysubstantial growth. Increased public investment and development - typecurrent expenditures should provide further momentum to the economy, provided

additional domestic and foreign resources are available for their finance.The biggest question marks appear to be whether adequate domestic andforeign savings will be available to finance public development expenditures

and public and private investment, and whether private sector confidencewill be sufficiently great to make the long-term investment necessary to

take full advantage of growth opportunities.

22. Rains in October-December 1972 have relieved much of dhe drought

condition of the past two years. Canal and river water supplies haverisen and Mangla dam reservoir is now full. Rain created excellent planting

conditions for wheat and other winter crops in most rain-fed areas. A

-9-

shortage of fertilizer in late summer and early fall reduced yields on latercotton pickings (as did also poor-weather conditions) and will adverselyaffect yields on next spring's wheat crop. Nevertheless cotton productionis estimated to be down by less than 5 percent from last year's record levels,and the fall harvest of rice and other crops such as sugar and tobacco wasgenerally better than a year ago. Spring wheat yields in 1973 are expectedto increase by perhaps 10 percent. Massive fertilizer imports arrivals atthe end of 1972 suggest that ample future supplies can be maintained ifdiligent efforts are made to procure inputs in a timely fashion.

23. Longer-term agricultural growth prospects are also bright. Muchhigher yields can be obtained on most farms of less than 12.5 acres (whichcomprise about three-fourths of all farms and nearly one-third of thepresent cultivated area), if improved seed and adequate fertilizer andpesticides are made available to these farmers on credit, and if they aretaught basic improvements in their husbandry practices. In some instances,low-cost plows and other implements will also need to be supplied on credit.Foodgrain self-sufficiency seems a likely possibility (though one to beweighed against the relative profitability of alternative nongrain crops),as does also substantial expansion of exports of cotton, fruit, and perhapsmeat and leather. Increased agricultural production will also increasedomestic supplies for cotton textiles, leather products arnd other agro-basedindustries. The ultimate ceiling on Pakistan's agricultural production willbe imposed by water supplies and control of salinity, so that efficientwater use on an integrated national basis is also of the highest priority.

24. Devaluation has also greatly increased the attractiveness ofexploiting domestic mineral resources. New discoveries indicate thatPakistan may be richer in mineral resources than previously thought, althoughfurther studies are needed to determine the commercial feasibility of manyof the known deposits, some of which are in remote areas.

25. There are a number of factors in addition to more stable laborrelations and increased government support to indicate that industrial outputwill rise substantially during 1973. For one, the excess capacity in mostindustrial sectors creates the possibility of rapid increases in output inresponse to greater demand. This capacity was built up partly to qualifyfor higher raw material import quotas under the previous regime of tightimport controls and multiple exchange rates. 1/ Import liberalization in May1972 led to very large orders for spare parts to restore some of this "excess"capacity to working order, and also removed quantitative restrictions fromimports of most raw materials and intermediate products.

1/ Most capital equipment came in at or near the official exchange rateof Rs. 4.76 per dollar, as did certain raw materials provided under aidand barter agreements. While most raw materials came in at higher rates,their processing and sale as finished goods in either the protecteddomestic market or abroad was often very profitable.

- 10 -

26. Increases in demand for industrial output seem likely to come fromseveral quarters. One is the steady expansion of exports. Piecemeal devalua-tion under the export-bonus system during most of 1971/72, followed by thedevaluation of May 1972, has increased the competitiveness of Pakistaniproducts. Exports to foreign countries grew by 42 percent during 1971/72,although most of the increase was accounted for by a more than 150 percentincrease in raw cotton exports (following adoption of a more favorableexchange rate for cotton), plus the sale in third markets of goods that werepreviously sold in East Pakistan. The cotton textile industry, which accountsfor nearly 30 percent of exports and a little more than one-third of industrialproduction, is experiencing strong export demand. Cotton yarn mills arehard put to fill both export and domestic orders. 1/ Gray cloth exportsare also rising, but are bumping up against import quota restrictions inthe U. S. and some European markets. Since most textiles are now exportedas gray yarn and cloth, however, there appears to be a large untapped potentialfor dyeing and finishing and for apparel and other finished good exports,although industrial country import quotas may also limit this growth. Leatherand leather products is another area where it appears the export potentialhas only begun to be tapped, although problems of improving the quality ofhides may limit the speed of export growth. Raw cotton, rice, fish, fruit,vegetables and meat are primary products with good export prospects.

27. Devaluation has also expanded the domestic market potential forcapital equipment and other goods previously imported at very favorableexchange rates. Even after a halving of tariffs on capital equipment, thecost of their importation has nearly doubled. Some types of domestictextile machinery, for example, can now be produced locally for one-thirdthe cost of comparable imports. Enough of a base already exists in thecapital equipment and other engineering industries that output could berapidly expanded.

28. A number of other investment opportunities exist in processingagriculture products, meeting growing consumer demand and replacing goodspreviously imported from East Pakistan. Rising agricultural productionlevels both generate supplies for, and create demand for the output of,agro-based industries. Oilseed and vegetable ghee production as well astextile production have risen in response to strong demand and the largercotton crop. Refined sugar production is expected to rise by 25 percentor more this year due to a larger crop and higher cane prices to attractmore of the crop into sugar mills. Rice milling will also increase. Paperand match production is rising to replace supplies formerly imported fromEast Pakistan. New capacity in fertilizer and in engineering goods isalso expected to lead to substantial increases in output in these industries.Pakistan's trade deficit now expected to be about $200 million in thecurrent fiscal year, and then rise to perhaps $250 million to $300 millionin each of the following several years. This corresponds with trade

1/ In December the export duty on yarn was raised to increase suppliesavailable to the domestic market and moderate the rise in its domesticprice.

- 11 -

deficits of just under $250 million annually during 1965-1971 for formerWest Pakistnm when account is taken of interwing trade, and of $400 millionto $500 million for both wings. A marked rise in private transfer receipts,primarily homeward remittances, has also reduced the expected deficit oninvisibles plus private transfers. Consequently, Pakist;an is expected toneed foreign financing of about $250 million to $300 million annually tocover its trade deficit, plus additional capital receipts and/or debt reliefequal to the full interest and principal service charges on its externaldebt. If there is no settlement of outstanding debt issues with Bangladeshand/or other debt relief, then total debt service charges would reachnearly $400 million by 1974/75, and equal 37 percent of projected foreignexchange earnings. Thus there is a total gap of $650 million to $700million per year to be filled by some combination of fresh capital inflow,debt settlement and debt renegotiation.

29. The many potential sources of increased demand and output suggestthat the limiting factor in Pakistan's growth may be the availability ofresources and the ability to use them to exploit these potentials. Ifforeign financing can be found to permit Pakistan to have a trade deficitof $250 million to $300 million per year, then it appears reasonable toexpect GDP growth rates of about 7 percent annually, with higher ratespossible if domestic resource mobilization and productivity of resource useimprove substantially (Chapter XI). Growth rates of 7 percent and aboveoffer hope for reducing the rate of unemployment and making progress onother economic and social problems, including the generation of neededbudget resources to carry out proposed government developmental and socialprograms, while growth rates much below 6 percent do not.

30. Concern for employment and other social aspects of developmentwill mean more rapid rather than less rapid growth if it is translated intopolicies to make more efficient use of all resources, including labor.Increasing use of labor-intensive production techniques as a result ofdevaluation and of explicit employment and mechanization policies cansimultaneously meet high employment and high output growth goals. Ruraldevelopment, increased small farm and small industry productivity, and ex-pansion of exports can all be labor intensive activities that also generatea high rate of growth relative to the level of new investment (i.e. createa low incremental capital-output ratio). Such a growth pattern would notmake any less urgent the necessity to increase domestic resource mobilization(taxation and saving) for both public and private investment and development-related purposes, but rather would increase the benefits generated by givenlevels of resources (including foreign capital) and expenditures. Sincedomestic and foreign savings are complements as well as substitutes, increaseddomestic resources will also create potentials for investment and development,which will increase the attractive opportunities for use of foreign resources.

- 12 -

II. EMPLOYMENT, UNEMPLOYMENT AND INCOME DISTRIBUTION

A. Size and Structure of the Labor Force

31. Until the new census results are available the size of the laborforce can be estimated only from age specific population projections andfrom past participation rates. The more reliable estimates of the laborforce closely approximate 19 million as of January 1, 1973. 1/ Currentadditions to the labor force are about 540,000 per year.

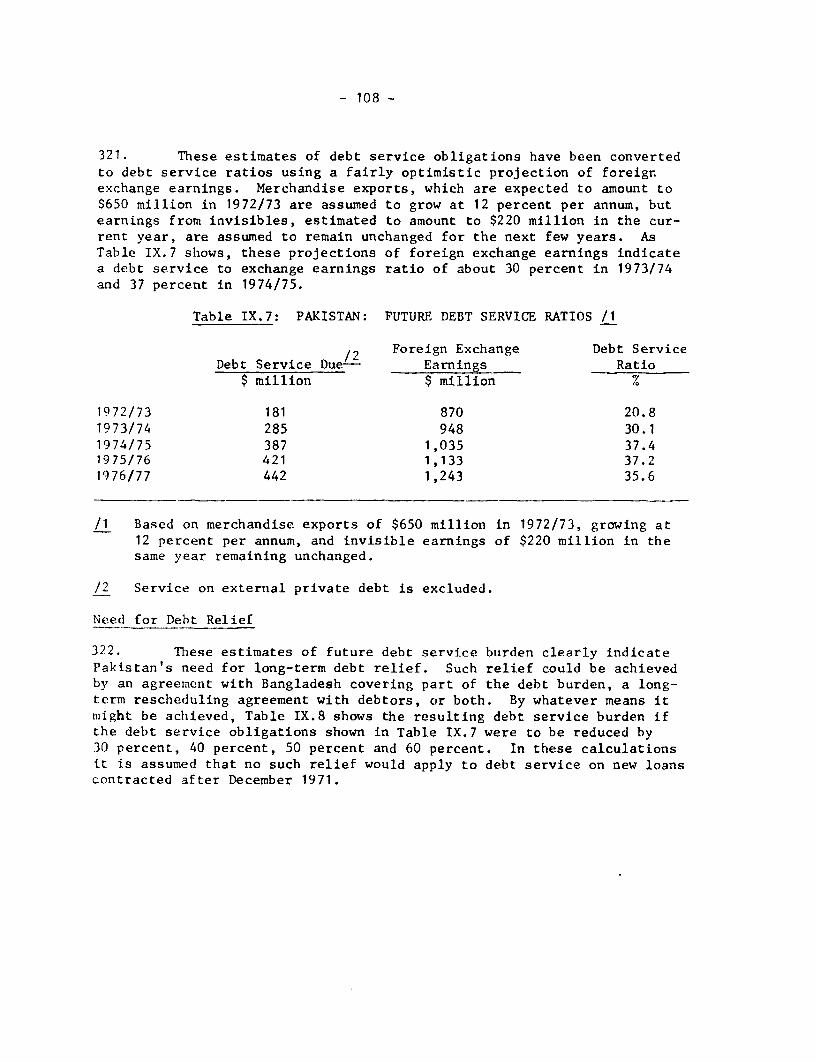

32. The size of the labor force is dependent on definitions which atthe margin are arbitrary: e.g., in Pakistan the lower age limit is 10 yearsof age. 2/ The overall low labor force participation rate in Pakistan arisesfrom the very low female participation rate; age - specific male participa-tion rates are high by comparison with other countries. Hence, thereappears to be little disguised unemployment of the "discouraged job seeker"category among men. Among women, there may be considerable numbers whowould seek employment outside the home (and thereby enter the definitionallabor force) if openings were available.

33. The distribution of the labor force by sectors and subsectors isshown in Table II.1. The unallocated category is mainly the openly unem-ployed. While declining, agriculture's share remains above one-half, andindustry's increasing share is approaching one-quarter. Manufacturing isgrowing more slowly than the rest of industry; these data include a largenumber of very small-scale enterprises. The share of services appears tohave been roughly constant since 1951 at a little under one-fifth of thetotal labor force.

1/ The fundamental work on projecting the labor force was done by R.A.Karwanski in the late 1960's. Current estimates are interpolationsfrom and minor adjustments of his projections which are published inKarwanski, Education and Supply of Manpower in Pakistan, PlanningCommission, 1970.

2/ From the 1961 census onwards; the 1951 census included age 12 andabove. Between the two censuses changed definitions created aspurious rise in the female participation rate. The change was largeenough to affect the intercensal growth rate of the total labor force:without adjustment 2.8 percent per year, compared with a probable2.2 percent per year, both for ages 12 and above.

- 13 -

Table II.1: DISTRIBUTION OF THE LABOR FORCE

Per Cent1951 1961 1968-70

Agriculture 65.3 59.6 54.8

Industry 13.3 18.7 24.2

Mining .1 .2 .1Manufacturing 9.7 13.5 15.3Construction )1 2.1 3.6Public Utilities .8 .2 .4Transport 1.7 2.7 4.8

Services 18.2 19.6 18.8

Commerce 6.9 7.1 10.2Other Services 11.3 12.5 8.6

Unallocated 3.2 2.2 2.2

Sources: 1951, 1961: the respective censuses, asadjusted for comparability in Ghazi M. Farooq,Dimensions and Structure of Labor Force andTheir Changes in the Process of EconomicDevelopment: A Case Study of Pakistan. Ph. D.dissertation, University of Pennsylvania, 1970.

1968-70: arithmetic mean of the labor forcesurveys, C.S.O., for 1967/68, 1968/69, and1969/70. The data for the last two surveys areprovisional.

B. Unemployment and Underemployment

34. Present limited data on unemployment and underemployment inPakistan, and its strong bias towards underestimation, make any assessmentof the overall situation at most a careful guesstimate. Measured rates offull-time unemployment in Pakistan approximate 2 percent of the laborforce, but the bulk of under-used manpower consists of underemployment ratherthan complete unemployment. As in other poor countries, extended open un-employment can be afforded by only a small fraction of the labor force. Mostof those unable to find regular employment produce whatever income they canvia self-employment such as petty trading or in family undertakings. Youngmen whose families are able to support them can await the right opening; asthese families are those which can afford the direct and opportunity costsof higher education, it is not surprising that the open unemployment rateamong educated youth is high.

- 14 -

35. The Third Five-Year Plan presented estimates of combined unem-ployment and the full-time unemployment equivalent of underemployment inundivided Pakistan ranging from 20.3 percent to 22.4 percent of the laborforce in the years 1950/51 through 1964/65. The Fourth Five-Year Plansuggested one-sixth of the labor force as total equivalent unemployment.The most authoritative recent estimate, again for undivided Pakistan, madeby the Study Group on Unemployment and Manpower Development in early 1971,placed unemployment and the full-time equivalent of under-employment at30 percent of the labor force. For none of these estimates are theunderlying assumptions, definitions, and empirical base set forth. 1/

36. Underemployment appears as shorter than normal working hours,as low intensity of work within nominal full-time hours, and as engagementin low productivity work. Survey data suggest that the full-time equivalentunemployment due to short working hours is not more than 4 percent of theemployed labor force. Direct measurement of the intensity of work is verydifficult, if feasible at all. Occupations of low productivity constitutethe major share of underemployment. The very high proportion of self-employedand unpaid family helpers in various nonagricultural pursuits suggests akind of self-help unemployment relief. Approximately seven-tenths of thoseengaged in manufacturing and construction are self-employed or unpaid familyhelpers; the share approaches nine-tenths in trade and comerce and is aboutsix-tenths in transport 2/. An unknown, but probably large, fradtiozi ofthese self-employed and family workers would accept alternative e6pldoyfbntif it were available. Distinctions between the ways in which undereiloytheretshows up are not very useful either for empirical measurement ot for temedialpolicy measures; they are all manifestations of the underuse of humanresources. The best evidence of the latter is the level of earned incomein the individual case. Unfortunately, income data are not collected withthe detailed characteristics of the labor force in the periodic laborforce surveys or in the census.

37. No quantitative evidence is available for the effects on unem-ployment of the dislocations and economic stagnation of the past se'veralyears. From the year 1969/70 to the present, however, it is a reasonableguess that the growth rate of the labor force may have been 1.5 percentper year greater than that of productive employment; this would imply anincrease in the unemployment rate of 4 to 5 percentage points in the threeyears.

38. One of the most ominous aspects of the unemployment situation isthe very high, and probably increasing, unemployment rate among educated

1/, Any estimate of unemployment and especially of underemployment dependson, definitions of Labor force participation, full-time employment,and underemployment. Differing definitions would yield substantiallydifferent quantitative estimates.

2/ From census data and C.S.O. Labor Force Surveys.

- 15 -

youth. Survey evidence is summarized in Table II.2. These numbers shouldnot be interpreted precisely: the time from graduation to survey variesamong the studies, and recent graduates are over-represented relative toall graduates and the former may be expected to have the higher rates ofunemployment. Based on informal surveys and the number of applicantsfor vacancies, one-third of recent engineering graduates have been estimatedto be unemployed. While empirical confirmation must await further studies,the general belief is that serious unemployment affects practically allcategories of graduates and that the rates of unemployment are increasing.

Table II.2: UNEMPLOYMENT RATES AMONG THE EDUCATED

PercentGroup Year Unemployed

1. Technical Trainees 1968 25

2. Technical Trainees 1971-72 33

3. Technical Training Centre,Karachi 1969 26

4. Swedish-Pakistan Instituteof Technology: Landhi,Kaptai, Gujrat 1971 39

5. Agricultural Graduates 1968 16

6. Educated Youth(Matriculates and above) 1969 29

Source: Directorate, National Manpower Council.

39. The employment of the educated has suffered more than that ofthe uneducated in recent years in Pakistan. Most of the educated areemployed in the modern enterprises of the private sector and in governmentservice. The modern enterprises are more vulnerable than the traditionalto economic stagnation. With extraordinary defense demands on the publicbudget, civilian programs and employment have grown slowly. Rapid expansionin education, agricultural extension, and social programs will yield somerelief from the high present levels of educated unemployment. Economicrecovery implies increased openings for the educated. Howe7er, entry intothe labor force of educated youth is high and increasing steadily.

C. Prospects for Employment and Unemployment

40. More precise estimates of unemployment and underemployment are lessimportant than information about the long-run trends in labor force growth andemployment creation. Harsh demographic realities dominate employment prospectsin Pakistan. Most of the labor force of the 1980's is here already; no publicefforts in family planning can affect substantially the growth of the labor

- 16 -

force until after 1990. Even if early declines in fertility rates areachieved, the growth rate of the labor force will accelerate for the nexttwo decades.

41. The major uncertainties in long-term projections of the labor forceof Pakistan are fertility rates and the participation rate of women. Thebest estimates suggest a current population growth rate of 2.9 percent peryear. The growth rates implied in two population projections are presentedin the first two columns of Table II.3. The first projection implies thatthe peak population growth rate has been reached already and that a signi-ficant decline in the rate will be evident in the 1980's 1/. The second,done more recently, implies a continuing acceleration to a peak in the early1980's. In view of the stagnation of the family planning program in therecent past and the inevitable lags in implementation should the decisionbe made to launch an aggressive program, the second projection is more likelyat this time, and perhaps even conservative. The second projection willbe exceeded if fertility rates do not decline substantially and soon, or ifthe female participation rates rise significantly.

Table II.3: PROJECTED GROWTH RATES OF POPULATIONAND LABOR FORCE

Percent per year for 5-year interval

Population Labor ForceA. B. A. B.

1960-65 2.89 - 2.06 2.1

1965-70 2.88 - 2.61 2.6

1970-75 2.87 2.92 2.86 2.8

1975-80 2.80 3.15 2.94 2.9

1980-85 2.68 3.25 2.92 3.0

1985-90 2.49 3.04 2.88 3.2

1990-95 - 2.76 - 3.2

1995-2000 - 2.47 - 3.1

Sources: A. Karwanski: Calculated from Education andSupply of Manpower in Pakistan, Tables I-31,I-34;

B. Prepared in Population and Human ResourcesDivision, Development Economics Department, IBRD.

1/ This projection, or minor modifications of it, is currently used bythe Planning Commission.

- 17 -