World Bank Documentdocuments.worldbank.org/curated/en/... · TEXTILE IN71DUSTRY STUDY August 16,...

85

o lh FALECOPY Document of J S 0 The World Bank FOR OFFICIAL USE ONLY COA/P/DEA/7;A PL Report No. 4346-PAK PAKISTAN TEXTILE IN71DUSTRY STUDY August 16, 1983 South Asia Projects Department Industrial Development and Finance Division This document has a restricted distribution and may be used by recipients only in the performance of their official duties. Its contents may not otherwise be disclosed without World Bank authorization. Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of World Bank Documentdocuments.worldbank.org/curated/en/... · TEXTILE IN71DUSTRY STUDY August 16,...

o lh FALECOPYDocument of J S 0

The World Bank

FOR OFFICIAL USE ONLY

COA/P/DEA/7;A PL

Report No. 4346-PAK

PAKISTAN

TEXTILE IN71DUSTRY STUDY

August 16, 1983

South Asia Projects DepartmentIndustrial Development and Finance Division

This document has a restricted distribution and may be used by recipients only in the performance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

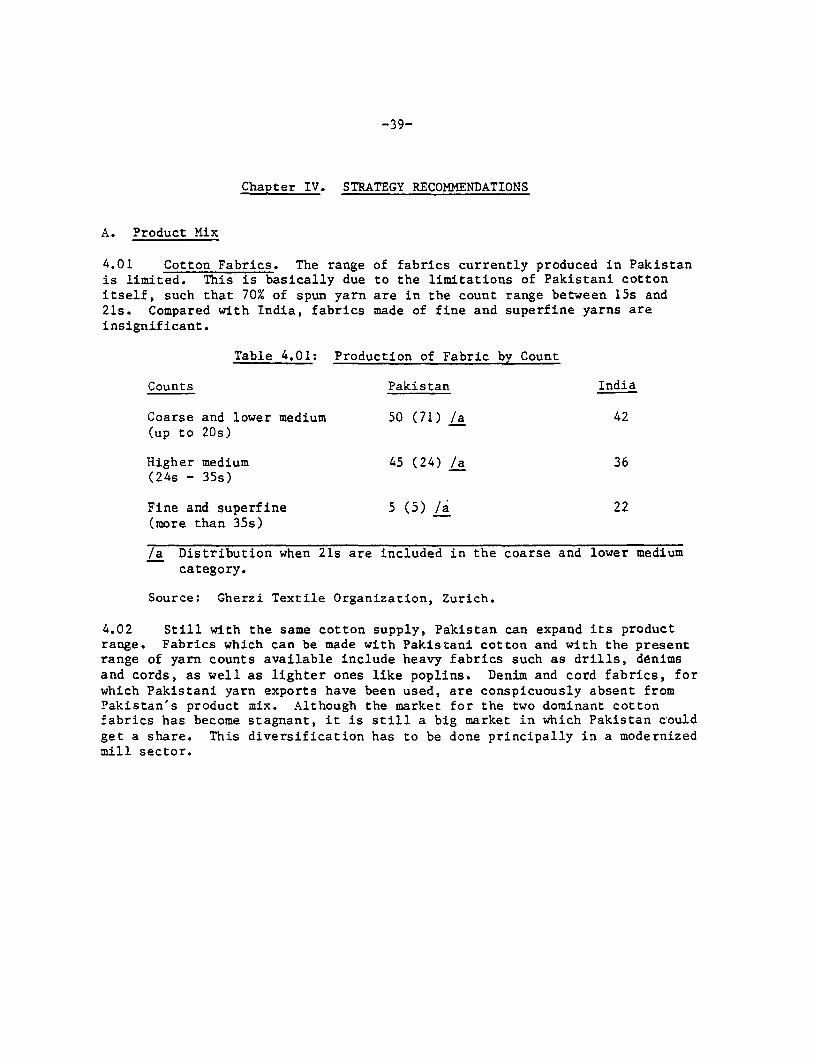

PAKISTAN: TEXTILE INDUSTRY STUDY

Table of Contents

Page No.

SUMMARY AND CONCLUSIONS .......... i...... ............ i

I. RECENT PERFORMANCE AND CURRENT STATUS ....................... 1

A. Profile and Structure ........... ....... 1B. Output and Capacity Utilization ......................... 3C. Export Performance ..................... 8D. Financial Performance ................................... 18

II. MAIN PROBLEMS ...................... ..... 20

A. Product Quality .......................................... 20

B. Labor Productivity ...................................... ... 23

C. Cost Competitiveness ..................... ........ 24D. Plant Efficiency ........................................ 28

E. Structural Problems ...................................... 29

III. MAJOR PROSPECTS ............ . ........ 32

A. Domestic Market ......... . ........... 32

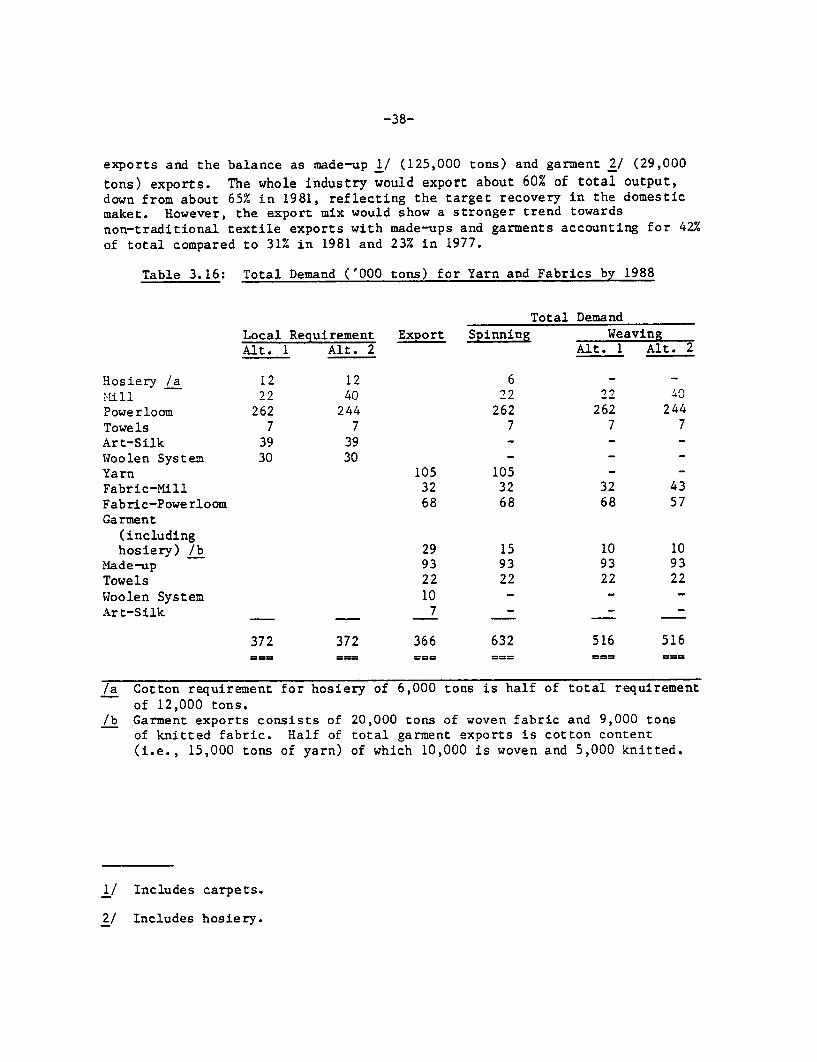

B. Export Market ........... ............... . ........... 33C. Total Requirement -. .................................. 37

IV. STRATEGY RECOMMENDATIONS ........ ................. 39

A. Product Mix ................................... ... ..... 39B. Overall Strategy - Mill and Powerloom Sectors ........... 44

V. DIRECT ASSISTANCE AND POLICY SUPPORT o..................... . 46

A. Technical Requirements .................................. 46

B. Financial Requirements .................................. 48C. Policy Support .......................................... 49

ANNEXES ..... . 54

This study was prepared following a sector mission in October 1982,consisting of Mr. J. Pernia, ASPID (Mission Chief), Mr. U. Hartmann andMr. E. Burger (Consultants).

ABBREVIATIONS USED

APTMA - All Pakistan Textile Mills Association

CSO - Central Statistics OfficeEPB - Export Promotion BureauGOP - Government of Pakistan

ITMF - International Textile Mills Federation

HB - Men's & Boys'MFA - Multi-Fiber ArrangementOE - Open-endPIDE - Pakistan Institute of Development EconomicsSYE - Square yards equivalentWGI - Women's, Girls' and Infants

CURRENCY EQUIVALENTS

Rs 9.90 - US$1.00

Rs 1.00 - US$0.10

These were the currency equivalents from

February 1973 to January 1982

GOVERNMENT OF PAKISTAN

FISCAL YEAR

July 1 - June 30

SUMMARY AND CONCLUSIONS

1. A comprehensive study on the textile industry was undertaken in 1978

with Bank assistance by Werner International 1/ to assist the Government ofPakistan (GOP) in formulating a long-term strategy for this industry. Thepresent study is intended primarily to assist GOP in preparing the sixthFive-Year Plan (1984-1988). It reviews industry's performance in the past

five years (1977-1981), and in this sense is an update of the Werner Report,identifies major problems and prospects, and presents an overall approach for

the next five years. By concentrating on main issues and providing an overallpicture, it complements the Werner Report which went into detailed recommen-dations, many of which are still valid today.

2. In the past five years (1977-1981), 2/ performance of Pakistan'stextile industry was generally poor. Output declined overall and in allsubsectors, except jute goods and towel manufacturing, reaching its lowestlevel in 1981. Domestic supply of textile products of all fibers dropped tohalf the peak level in 1978 from 3.72 kg/capita to 1.93 kg/capita in 1981.Capacity increase was negated by capacity idling and capacity utilizationstagnated at 70% for spinning and deteriorated from 69% to 54% for millweaving. Due to the low overall capacity utilization Government declared itpolicy not to allow new spinning and weaving capacity except in composite

mills (spinning and weaving).

3. Most mills continued to experience operating losses. While some

profits were realized these were due to non-operating revenues, principallyfiscal incentives, and were too small to attract additional investments.Dividends could not be paid and arrears with financial institutionsincreased. With declining networth and increasing indebtedness, the millsfinancial structure further deteriorated from already poor levels. Therewere not enough funds for reinvestment to upgrade the condition of the mills.Marginal operations, in turn, aggravated their financial position. Textilestocks continued to trade much below par.

4. The only bright spot in the overall picture was exports. Exportvolume grew by 54% in this period. Moreover, the product mix improved withthe share of traditional textile exports (yarn and grey goods) declining andthat of higher value-added goods (made-ups and garments) increasing. Theindustry became more export-oriented as output declined and exports increasedsuch that exports, as a percentage of total output, increased from 41% to

1/ Completed in October 1978 and known as the Werner Report.

2/ All references are to fiscal years except when otherwise specified.

-ii-

65%. However, the market structure remained unchanged. Markets for yarnremained concentrated in Hong Kong and Japan. For fabrics, there was somediversification with two new markets, Australia and Singapore, emerging.However, the EEC, USA and Iran continued to dominate. Prices of Pakistanitextile exports also declined by 20% in real terms, indicating deterioratingproduct quality. For yarn and grey goods prices were among the lowest in theworld, except for those of China. With escalating costs of labor, power andimported spares and accessories, low prices squeezed profit margins andbrought operating losses to most mills. Only the export rebates, initiatedin 1978, kept some mills profitable, though at a very marginal level.

5. Major problems of the textile industry stem from the general struc-ture of the industry. The mill sector continued to compete directly with thepowerloom sector, producing practically the same product mix and selling tothe same market segments for end-uses for which no quality premium is paid.Clearly, the mill sector could not compete since the powerloom sector haslower operating costs, partly due to exemption from excise tax, but prin-cipally because, being too fragmented, it could stay, in practice, outsidethe scope of tax and labor legislation and sometimes, power bill collection.Moreover, powerloom units do not require licensing and can be organizedquickly with little capital and readily available locally made equipment.Thus, the powerloom sector continued to displace weaving activity in the millsector for local as well as export markets. However, product quality ispoor, again due to fragmentation, since while the weaving process itself isof acceptable standard, crucial pre- and post-weaving processes and methods,as well as other quality control systems hardly can be implemented at anacceptable level in small powerloom units.

6. The overall strategy should center on promoting product and marketspecialization by the mill and powerloom sectors. In order that the millsector can revive, it has to concentrate on products and markets in which ithas comparative advantage in the long-term. It should start differentiatingits production and exports from those of the powerloom sector not only inquality levels, but also in constructions, widths, counts and fibers. Thereis evidently a growing local demand for blend fabrics which appear currentlyto be filled mainly by legal and illegal imports due to the inability of themills to respond adequately to this demand shift. Within the constraints ofPakistani cotton there are diversification possibilities for cotton fabricsoutside of the standard grey sheeting, 21s x 21s, 60 x 60. Differentiationand diversification are happening already in leading mills and should bepromoted in the entire mill sector if it is to survive.

7. Mills which take this reorientation seriously should be provided withthe necessary1means for rehabilitation. This means providing them not onlywith investment capital, but also easier access to imported spares, acces-sories and modernizing attachments as well as more modern looms at reasonablecosts by reducing import duties on them. Capacity licensing should berelaxed to allow mills to match market requirements for quality and blendedgoods with appropriate machinery and equipment. With a modernized and/or

-iii-

modern capacity the mill sector should develop new market orientations,moving out of the traditional grey fabric exports into higher-priced fabricexports, catering to the local market for blended as well as other cottonfabrics and providing quality fabrics to the garment and made-up exportsectors. Such a program would require about US$330 million for 11,000 newlooms and US$10 million annually for spares and attachments. "Sick" millsshould be individually evaluated. Nonviable mills should be closed, liqui-dated and sold either as entire units or as machinery pieces. This willprovide working mills with a choice of retooling and expanding with cheapused equipment which can be modernized or through importation of new modernlooms. Policy should encourage consolidation into larger, more economicunits through acquisitions and mergers or expansion. A benchmark mill size

could be 25,000 spindles and 500 looms. More rigid subproject appraisal ofre-equipping proposals for individual mills, covering areas such as productquality assurance, marketing channels, economic sizes, training, etc., wouldbe required to help assure this re-orientation program.

8. Since the powerloom sector appears to be an efficient provider ofcheap quality fabrics, it should be allowed to continue to produce for thelocal rural market and for low-priced exports. Even without additionalexplicit assistance, but assuming that the implicit incentives would continuein practice, it still would expand in the next five years, especially to meetthe growing local requirement. Investments would come mainly from the unor-ganized capital market and should not strain the limited resources of theorganized capital and credit markets. While overall quality levels wouldremain essentially the same, there are specific measures which can improvequality to some degree even in the same fragmented structure. However, asignificant improvement in product quality and mix for the industry as awhole can come only from a revitalized mill sector.

9. In encouraging a strong and efficient mill sector, appropriatepolicies would be needed. An across-the-board operating subsidy such as thepresent system of compensatory rebates should be avoided, since this wouldencourage the continuation of marginal operations that produce low-pricedexports which the powerloom sector can produce more economically. Aside fromprovision of investment capital and imported capital equipment, capitalinvestment incentives would be required to encourage mill owners and inves-tors to get involved in re-orienting their production and marketing programsinto areas which are more risky than the traditional grey goods sector.

10. To be competitive in the export market, the cost -disadvantage of thePakistani industry has to be tackled. First, the problem of low laborproductivity should be addressed directly. Labor legislation, which preventstreating and paying workers on the basis of productivity, needs to berevised. Also, the issue of appropriate level of fringe benefits needs to bereviewed. Moreover, a more appropriate and strong in-plant training programis needed. In the short run, this should be done by the mills' managementsthemselves and this could be encouraged through a training incentive package.Second, appropriate pricing of inputs is crucial for the mill sector to

-iv-

compete internationally. The price of cotton for the Pakistan industry hasusually been,lower than-world prices. However, the-costs of man-made fibersand of imported spares in Pakistan are still among the highest.

11. Finally, there is a need to encourage the further diversification ofexports towards higher value-added products. The new textile agreementssignificantly improve the market entry of made-ups and garments; in contrastthere is little scope for expanding cotton fabric exports, except throughtrading-up, as quotas have been almost fully utilized in the past andincreases provided in the new agreements are marginal. While an incentivesystem which provides higher effective protection for higher value-addedproducts, appears to be already in place, the base level might be too highencouraging continuation of inefficient operations and the differentialsmight be insufficient to encourage industry to be more involved in theexports of more processed exports which are clearly more risky.

Chapter I: RECENT PERFORMANCE AND CURRENT STATUS

A. Profile and Structure

1.01 Textiles 1/ is the most important industrial subsector of Pakistanaccounting for 30% of industrial value-added and 75% of manufactured exports,utilizing 25% of industrial fixed assets and employing 35% of the industriallabor force. The industry is dominated by the cotton system (72%) whichdepends principally on locally grown cotton. Pakistan produces about700,000 MT 2/ of cotton annually of which between 400-440,000 MT is consumedby the textile industry and the surplus exported. 3/ There are 142 spinning

mills with 2.4 million spindles and 69 composite mills with 1.8 millionspindles. Weaving is done by 69 composite mills with 25,000 automatic loomsand by small cottage-type weaving units (the powerloom sector) which operateanywhere between 40,000 to 75,000 looms. About half of cotton fabric produc-tion is finished by 165 finishing plants with total capacity of 1.15 billion

sq. meters. Most are small commission finishing units, with only about 30integrated with spinning and weaving plants and another 10 large units.

1.02 There are some activities in other fibers, such as jute manufacturing(12%), filament yarn (polyester and polyamide) weaving, the so-called

art-silk sector (7%), blending with synthetic fibers (5%) and wool spinningand carpet manufacturing (4%). The jute sector which spins and weaves

imported jute fibers consists of seven units with a total capacity of 31,592spindles and 1,739 looms. With a highly protected domestic market, output of

this sector in the past five years expanded at an annual compound rate of14%, reaching 56,000 MT in 1982. As a result, imports of jute goods declinedfrom 53% of total supply in 1978 to 40% in 1982. With two more units

expected to be operational within the next plan period, imports are expectedto decline further to about 15% of total projected demand of 110,000 MT by1987.

1.03 The art-silk sector which is composed mainly of small units with less

than 10 looms, weaves imported and local filament yarn. Although output ofthis sector increased in the past three years it could not recover from the

1/ In this study, the term "textiles" is used to refer to all categories

of textile products: yarns, fabrics (piecegoods), made-ups and garments(clothing).

2/ In the 1982 crop year, cotton produced on 5.3 million acres reached anall-time high of 731,000 MT at an average yield of 331 lbs/acre. Pakis-tan has a 5% share in world cotton production and ranks fifth behind USA,USSR, China, and India.

3/ Pakistan is the third largest exporter of cotton after the USA and USSRwith a market share of 7.5%.

-2-

peak of 33,600 tons achieved in 1977 due to shortfall of yarn supply. Fila-ment yarn is subject to quantitative import restrictions (500 kg per loom)and high duties and taxes. While importation of fabrics of man-made fibersis banned providing the industry with a monopoly in the local market, it isclaimed that competition from illegal imports has increased considerably.Thus, a good portion of the decrease in per capita consumption from 0.4 kg in1977 to 0.2 kg in 1981 is attributed to illegal imports. The industry ishighly domestic market oriented with exports constituting only 3% of output,except in 1981 when exports to the Middle East suddenly increased due to thepolitical situation. However, considering its cost structure and productquality it is doubtful whether this sector can compete regularly in theexport market.

1.04 There are 109 mills in the wool spinning sector with about 135,000spindles producing worsted, semi-worsted and woolen yarn. Output, which inthe past five years had stagnated at about 30,000 MT, is used mainly by thecarpet sector (45%) and other cottage industry units producing blankets, bagsand other woolen and wool blend goods (35%). The carpet sector is made-upmainly of small hand-knotting operations estimated to be about 13,000 unitswith 110,000 looms and employing about 330,000 people. Exports ofhand-knotted carpets grew steadily from 4,800 MT to 7,500 MT from 1977 to1981 at a compound rate of 12% p.a.

1.05 The major product groups of the made-up sector are towels,tents/canvas and cotton bags. Towel manufacturing expanded in this periodwith output and exports increasing at 11% p.a. and at 22% p.a. respectively.There are about 2,800 looms with capacity of about 15,000 MT. Most towelunits are small with between 5-15 looms. About 80% of output is exported butthe market is mainly institutional since quality is poor. Exports of theother made-up goods also grew rapidly with cotton bags increasing four timesand tents/canvas almost doubling. Overall, made-up goods were the biggestcontributor to textile export growth.

1.06 The garment sector is the most recent segment of the textile industryto develop and consists of three distinct groups: hosiery, local wovenfabric garment manufacture 1/ and garment manufacture from imported wovenfabric for re-export. 2/ There are about 9,500 knitting machines withcapacity of about 14,500 MT. Most units are small and half of the machinesare manual (for sock-making). Hosiery and knitwear output in this perioddeclined while its exports were the slowest growing among textile products,increasing even slower than fabric and yarn exports. In contrast, woven

1/ Represented by the Pakistan Cotton Fashion Apparel Manufacturers andExporters Association.

2/ Represented by the Pakistan Ready-Made Garment Manufacturers andExporters Association.

-3-

fabric garment manufacture and exports expanded quite well in the past fiveyears. Exports of both subgroups reached 10,300 tons in 1981 and were thesecond biggest contributor to overall textile export growth.

B. Output and Capacity Utilization

1.07 In 1981, the Pakistan textile industry produced 396,000 tons ofyarn 1/ equivalent and 333,800 tons of fabric equivalent; these were thelowest output levels in the past five years during which peak production

occurred in 1978. The 1981 yarn and fabric output were 13% and 22% lowerthan the 1978 output respectively. With declining production, increasingexports (Section C) and increasing population, domestic supply of textile

products declined by 48% to 1.93 kg/capita from the peak of 3.72 kg/capita in1978. Production dropped by 0.91 kg/capita while exports increased by0.88 kg/capita. The picture of overall decline was true in all subsectors ofthe industry, except towel and jute goods manufacturing which increased by11% p.a. and 14% p.a. respectively from 1977-81. All other subsectors, i.e.hosiery, art-silk, carpets and other made-ups, followed the overall decliningtrend of yarn and fabric production.

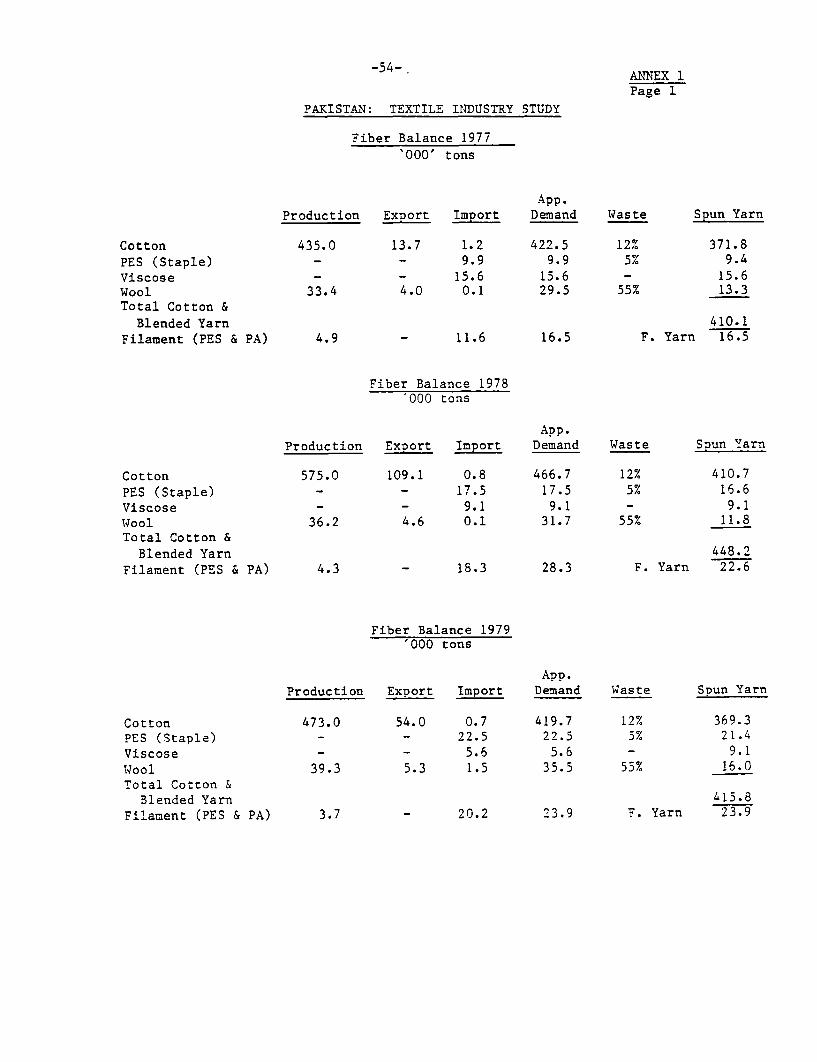

1/ Supporting data for Table 1.07 are found in Annex 1.

Table I.Ot Fiber 84lance

1977 5978 1979 1980 1981onn' 1000'

tona Unit _uos __ tUni- _tos Unit tons Unit tona Unit

Spun Yarn 410.1 448,2 415.8 421.1 396.0

Fila-ent (Tas 4 Fiat) (6.5 22.6 21.9 36.4 31.0

Total Yarn Avaliable 426.6 4711.8 439.7 451.5 429.0

Total Y,rn E.xportø <C 6 PES/C) 68.1 62.2 99.5 102.3 98.4of WhIh Thread Export 1.5 2.2 1.6 2.5 3.2

Total Yarn Avatlable forCurcther Proceaing 358. 4.6 140.2 355.2 333.8

- il,siery (Cotton) 12.5 84.2 mil[ pieces 12.5 84.4 mill piece* 12.5 84.0 mill pieces: 12.1 M mill piece@ 12.1 81 Mill pi.r- Mill Sector 58.3 408.3 mill m 2 55.9 191.3 mill n 2 46.1 319.4 Gitt a 2 4.9 342.3 Dilt n 2 43.5 307.9 mit a 2- lorgir d Sector 1/ 211.4 1493.8 mill m 2 267.n 1869.0 mill a 2 211.6 1521.2 mill a 2 211.5 1624 mill a 2 209.2 1464.4 mill a I- Tow-lå 10.7 10.0 8.8 8.5 14.1- Art Slik 31.6 498 mitt m 2 31.2 492 mill a 2 22.8 338.0 mill a 2 24.2 158 mill m 2 26.1 386.6 mill m 2- Wo,- Sectar 2/ 30.0 30.0 10.0 30.0 28.8

Total Fabric and (kher Products 358.5 408.6 140.2 351.2 333.85% Waste 17.9 20.4 17.0 11.9 16.1Pabricg Imported 31 -

Total Fabrica Av.ailble 140.6 388.2 321.2 337.4 117.1

1/ locludet cotton basa, tente, canvan, ete.; 2/ Fat.imje. Uncludlag cotrt and# acryllr yarn;1/ T1.ære ale no offIcial ImporEa of fabriL.. vc"ept for 1011 export as garment6 (banded warehouse system).

vern_on, Factore Ilsed:

1. 11,,alery: 149 g/plece (Average from C.ATT)2. C0ttna Fabri: 142.85 g/aquare meter or 7 sq.m. - I kg. (20s x 2

0s. 60 n 60)

1, Art Silk Fabrie: 0.675 g/squar. meter ur 14.81 aq.m. - I kg. (Art Silk Assocition>4. land-knaotted Carpets 4.8 kg./square meter (tarpet Anseciation)1. Hachine-made Carpet*, 1.92 kg/aquare meter (Wa.en Hills Association)

Table 1.01: Fiber Balance ((on't)

1977 1998 1979

------ *'o000otons Unit nn Unit tns Unit tns - Unit Total Fabrics Available 340.6 388.2 121.2 111.4 317.1

fxjtrt (Fnbric & Other Products) 98.3 106.6 120.5 11.9 157.5- Hill Sector 27.2 190.7 mill I 2 27.6 391.6 illi e 2 22.0 15).8 mill m 2 23.7 166.2 mill a 2 22.7 159.1 mis 2- Unorganized Sector 32.3 226.1 miII m 2 37.2 259.9 mllt a 2 J4.0 311.7 bill a 2 54.2 379.6 mill a2 48.8 341.4 .1 a 2- Art Silk 0.6 9.3 mill a 2 2.1 11.3 million a 2 0.1 10.1 mll m 2 0.2 2.8 milt " 2 5.5 8.2 milm 2

Total Fabrica 60.1 66.9 76.1 78.1 77.0- Towels 5.1 4.2 6.1 1.1 11.*- Cotton Baga 3.8 R.1 4.1

23.6- Tente. Canvas 12.8 12.6 12.5 34.6 8.1- Made-uop (Bedsheets, 2.2 2.2 1*4 4.1cover curtain, napkin,

etc)

Total Made-upe 23.9 271 11.1 34.1 58.5hoslery 1.5 21.1 mill pieces 2.1 10.0 Bill pieces 1.3 20.9 mill psee 3.9 25.9 mill pieces 4.2 28.1 mlp .rmnuGarments 6.0 31.6 mill pieces 1.9 24.3 mill pieces 6.2 32.11 mill pieree .6 45.4 mili pieces 0.5 2.3 mil on 2C.rpeta 4.8 1.6 mill a 2 6.0 1.9 .1l a 2 1.2 2.4 ail aZ 7 .2 2.4 mill I 2 7.5 2.5 ill a 2

Apparent Consumption 242.3 283.6 202.7 2(5.5 159.6- Mill Sector - contribution 1 I1 in 13 12- Power Loom - contribution I 61 11 it 73 116 Li'- Other@ - contribution 2 20 I 16 1I

Population (milion) 73.43 15.61 11.911 80.23 82.60Apparent Consumption, p.c.

In kg. 3.30 3.12 2.61 1.93

In eq.. 23.1 26.0 18.2 2.5617.9 3.5

Conversion Factor' Used (con't)

6. Carmenta (Sources CA'r)

Product SoMeter/Piece Sj Heter/Kg. Product Soerer/Place Sq. Meter/Xg.Clothing Accessories 0.O 7 Outer Garoments 2.511Pants 2.50 5 Shirta 2.00 1Arab Romaes 3.01) 7 Scarves 0.90 2Shawls 1.50 7 Under Carments 11.10 1Costs 2.50 5 iank,erchiefs 0.20 7Gloves 0.04 5

1. Made-Up. Redeheets: Estimated from value (interview with Exporters)

1971 R. 4.5/sq.m. 7 sq.m./kg 1980 Re. 1.5/sq.m. 7 sq.m./kg1978 Re. 5.0/sq.a. I sq.m./kg 1981 As. 5.5/sq... 1 eq.m./kg1979 Ra. 5.5/sq... 7 sq.m./kg

Sources Misaton estimates based on various official sources.

-6-

1.08 This decline in production occurred in a period of expandingcapacity. Installed capacity in spinning increased by 439,000 spindles or12% and though weaving capacity in the mill sector declined by 5,000 loomsthere was reportedly a more than offsetting increase of weaving capacity inthe powerloom sector which is estimated to be currently between 40,000 -75,000 looms. In 1981, only 70% of installed spinning capacity and 54% ofweaving capacity (mill sector) were operating. This was the general picturein the past five years for the spinning subsector with average utilization of70%. The picture in the mill weaving subsector was worse, deteriorating froma utilization rate of 69% at the beginning to 54% at the end of the period.

1.09 Moreover, productivity of capacity which was operative was also low.Average output per spindle year was 121.9 kg which was 86% of the five-yearplan target of 141.7 kg. Effective capacity utilization at target produc-tivity was thus only 60%. Loom productivity in the mill sector was24,300 sq. meters per year which is slightly higher than the target of23,000 sq. meters, raising effective capacity utilization a little to 57%.Still loom efficiency is only 65% compared to 85-90% in Europe and 92-95%in the USA. Productivity in the powerloom sector is difficult to estimatesince the exact number of looms is not known, but it appears to be about thesame as the mill sector, probably around 24,000 sq meters p.a.

1.10 Spinning Capacity. The installed cotton spinning capacity increasedbetween 1975 and 1982 by about 990,000 spindles and 21,600 open-end (OE)rotors. Pakistan's main competitors in the yarn export market showed thefollowing development:

Table 1.10: Increase in Spinning Capacity from 1975 to 1982

Total Spindles Increase Total Rotors Increaseas of 1982 1975-82 as of 1982 1975-82

(million spindles)

Italy 3.3 1.17 93,000 91,800Brazil 4.6 1.60 47,000 47,000Egypt 2.5 0.81 N.A. 39,800Pakistan 4.2 0.99 29,800 21,600Taiwan 3.5 0.71 N.A. 101,000India 21.8 3.83 N.A. 41,500

Source: International Textile Mills Federation, Zurich.

Nominally, the development of Pakistan's spinning industry is comparable.However, with about I million spindles currently idle, of which at least halfcannot be rehabilitated, the effective increase is marginal. Also, with only19,000 operating, open-end rotors account for only 1.9% of the operatingspinning capacity and is below world average even though both the cotton of

-7-

Pakistan and the count ranges spun are ideal for OE-spinning. 1/ Theopen-end spindleage in other areas are: Japan 5.5%; Western Europe 5.3%;East Asia 3.6%; Africa 3.3%; USA 2.7%; and Latin America 1.7%.

1.11 Weaving Capacity. Out of 25,000 looms installed in the mill sector,an average 14,000 were idle during this period. It is believed that mostidle looms have been removed from the mill sector and are now operating inthe powerloom sector. Moreover, over 75% of the looms are more than 28 yearsold. Practically no modern shuttle or shuttleless looms is operating in theindustry. While Pakistan's competitors have invested heavily in modernshuttleless looms as well as high speed shuttle looms, Pakistan's mill sectorremained with conventional technology as the following comparison shows:

Table 1.12: Increase in Weaving Capacity 1974-80

Shuttle Looms Increaseas of 1980 1974-80

Korea 30,000 21,300Taiwan 73,000 13,000Brazil 72,000 8,300Italy 38,000 3,400Indonesia 41,000 15,400India 209,000 16,400Pakistan 26,000 (13,000)

Shuttleless Looms Increaseas of 1980 1974-80

Italy 21,000 16,000USA 36,000 25,800Korea 7,300 2,000Hong Kong 3,700 2,900Turkey 2,700 2,000Taiwan 8,800 3,600Pakistan 400 400

Source: International Textile Mills Federation, Zurich.

1.12 The situation with regard to powerloom weaving is not clear. It isuncertain whether looms are cop-changing automatic looms or non-automaticlooms. Also, the number of looms'quoted ranges from 40,000 to 75,000. Basedon the total output of this subsector in 1981 of 1,526.10 million m2 andassuming annual output per loom of 24,000 m2 there could be over 60,000looms. It is clear, however, that the powerloom sector has continued to

1/ Subject, however, to removal of the high trash content in the blow-room.

-8-

displace weaving in the mill sector. Output share of the powerloom sectorincreased ,from 75% in 1978 to-83% in 1981 despite ,the overall decline.Capacity in the powerloom sector increased not only from looms transferredfrom the mills, but also from new locally manufactured looms.

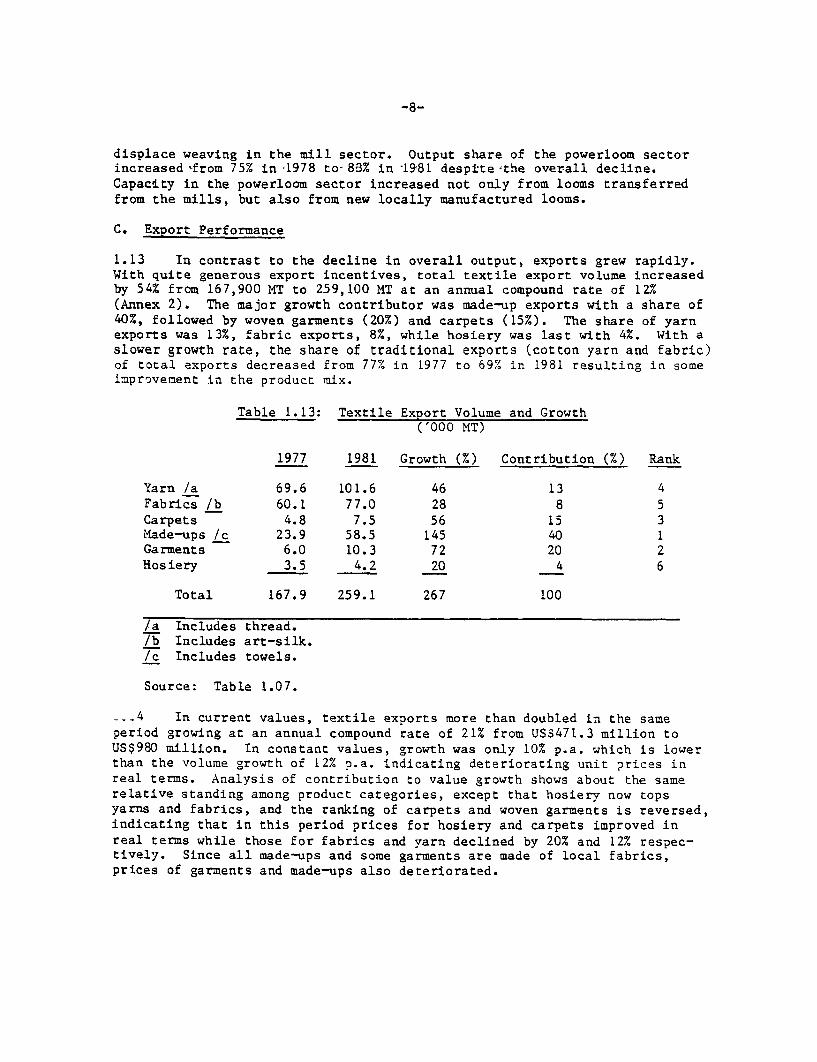

C. Export Performance

1.13 In contrast to the decline in overall output, exports grew rapidly.With quite generous export incentives, total textile export volume increasedby 54% from 167,900 MT to 259,100 MT at an annual compound rate of 12%(Annex 2). The major growth contributor was made-up exports with a share of40%, followed by woven garments (20%) and carpets (15%). The share of yarnexports was 13%, fabric exports, 8%, while hosiery was last with 4%. With aslower growth rate, the share of traditional exports (cotton yarn and fabric)of total exports decreased from 77% in 1977 to 69% in 1981 resulting in someimprovement in the product mix.

Table 1.13: Textile Export Volume and Growth('000 MT)

1977 1981 Growth (%) Contribution (%) Rank

Yarn /a 69.6 101.6 46 13 4Fabrics /b 60.1 77.0 28 8 5Carpets 4.8 7.5 56 15 3Made-ups /c 23.9 58.5 145 40 1Garments 6.0 10.3 72 20 2Hosiery 3.5 4.2 20 4 6

Total 167.9 259.1 267 100

/a Includes thread./b Includes art-silk./c Includes towels.

Source: Table 1.07.

__.4 In current values, textile exports more than doubled in the sameperiod growing at an annual compound rate of 21% from US$471.3 million toUS$980 million. In constant values, growth was only 10% p.a. which is lowerthan the volume growth of 12% p.a. indicating deteriorating unit prices inreal terms. Analysis of contribution to value growth shows about the samerelative standing among product categories, except that hosiery now topsyarns and fabrics, and the ranking of carpets and woven garments is reversed,indicating that in this period prices for hosiery and carpets improved inreal terms while those for fabrics and yarn declined by 20% and 12% respec-tively. Since all made-ups and some garments are made of local fabrics,prices of garments and made-ups also deteriorated.

-9-

Table 1.14: Textile Export Value and Growth(in million 1977 USDollars)

Ratio of UnitValue 1981 to

1977 1981 /a Growth (%) Contribution (%) Rank Unit Value 1977

Yarn 112.9 150.1 33 10 5 0.88Fabrics 162.0 166.9 3 1 6 0.80Carpets 87.7 151.7 73 22 2 1.11Made-ups 54.6 124.9 129 39 1 0.94Garments 42.2 68.0 61 18 3 0.94Hosiery 11.9 16.0 34 10 4 1.12

TOTAL 471.3 677.6 333 100

/a Deflated using the International Price Index of the World Bank.

Source: Central Statistics Office, Government of Pakistan.

1.15 Pakistan ranks first in yarn and seventh in fabric exports with amarket share of 13% and 8%, respectively. Pakistan's yarn market share,however, decreased as its exports remained practically stagnant while worldtrade increased by 20%. 1/ In contrast, her fabric market share increased asexports grew in a stagnant world market.

Table 1.15: Share in World Textile Trade

(in metric tons)

Cotton Yarn Cotton ClothShare in Share in

World Pakistan World World Pakistan WorldCY /a Exports Exports Exports Exports Exports Exports

1976 600,834 95,914 16% 887,501 48,812 5%1977 526,106 46,716 9% 822,138 36,986 4%1978 589,600 74,883 13% 861,867 51,646 6%1979 637,591 88,759 14% 956,637 58,707 6%1980 719,045 95,221 13% 891,800 68,400 8%

/a Pakistan export figures in this table differ from the official GOPfigures due to use of calendar years.

Source: Cotton World Statistics.

1/ In the early 1970s when Pakistan was exporting almost half of totalproduction, its market share was 30%. Currently only about 25-30% ofproduction is exported, despite lower output.

-10-

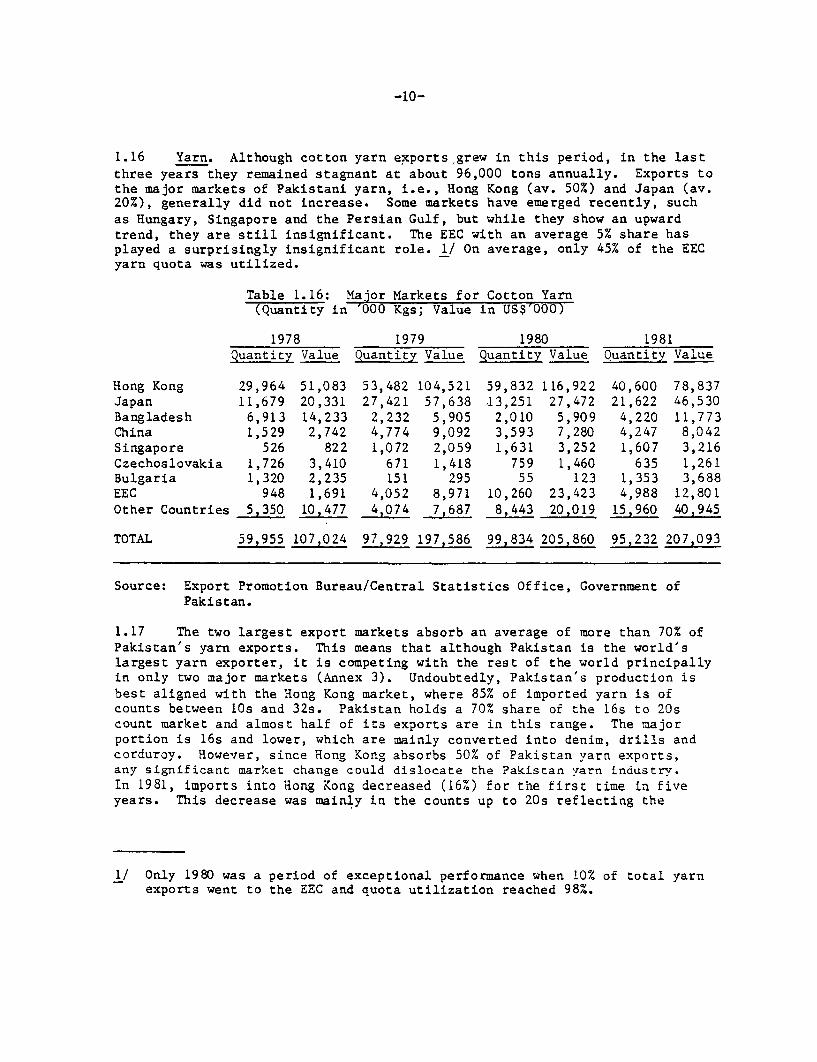

1.16 Yarn. Although cotton yarn exports grew in this period, in the lastthree years they remained stagnant at about 96,000 tons annually. Exports tothe major markets of Pakistani yarn, i.e., Hong Kong (av. 50%) and Japan (av.20%), generally did not increase. Some markets have emerged recently, suchas Hungary, Singapore and the Persian Gulf, but while they show an upwardtrend, they are still insignificant. The EEC with an average 5% share hasplayed a surprisingly insignificant role. 1/ On average, only 45% of the EECyarn quota was utilized.

Table 1.16: Major Markets for Cotton Yarn(Quantity in '000 Kgs; Value in US$'000)

1978 1979 1980 1981Quantity Value Quantity Value Quantity Value Quantity Value

Hong Kong 29,964 51,083 53,482 104,521 59,832 116,922 40,600 78,837Japan 11,679 20,331 27,421 57,638 .13,251 27,472 21,622 46,530Bangladesh 6,913 14,233 2,232 5,905 2,010 5,909 4,220 11,773China 1,529 2,742 4,774 9,092 3,593 7,280 4,247 8,042Singapore 526 822 1,072 2,059 1,631 3,252 1,607 3,216Czechoslovakia 1,726 3,410 671 1,418 759 1,460 635 1,261Bulgaria 1,320 2,235 151 295 55 123 1,353 3,688EEC 948 1,691 4,052 8,971 10,260 23,423 4,988 12,801Other Countries 5,350 10,47 7 _4074 7,687 _8443 20,019 15 960 40,945

TOTAL 59,955 107,024 97,929 197,586 99, 834 205,860 95,232 207,093

Source: Export Promotion Bureau/Central Statistics Office, Government ofPakistan.

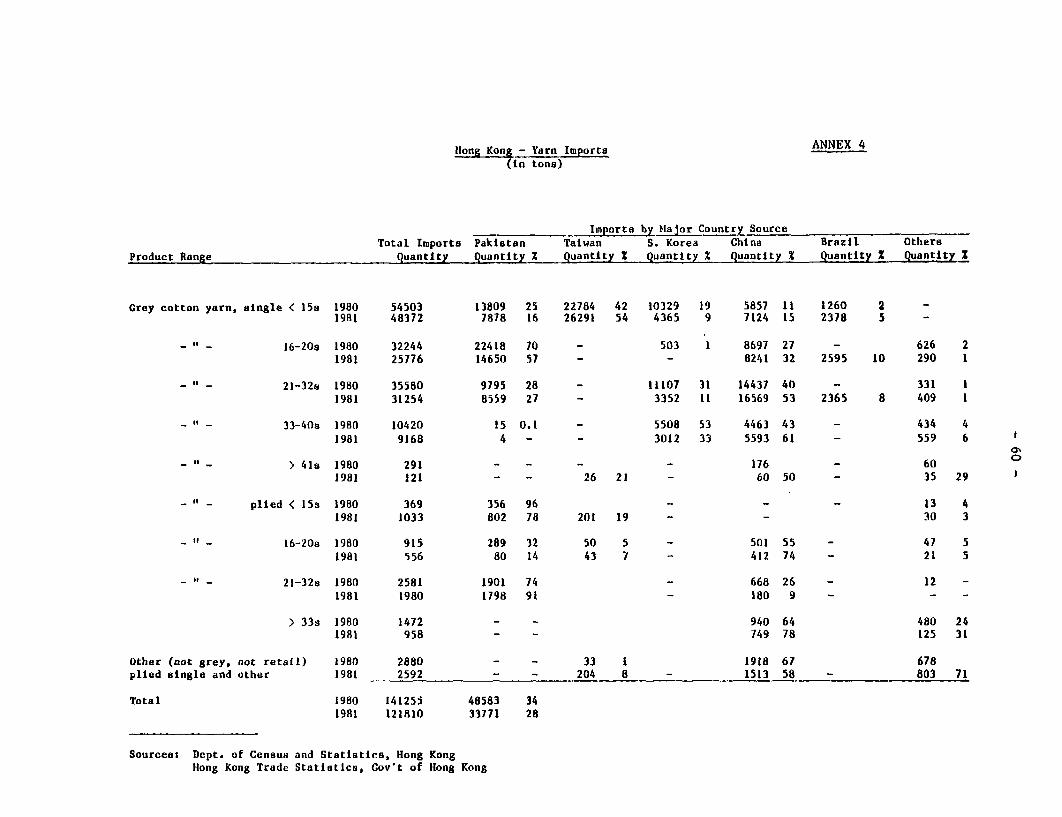

1.17 The two largest export markets absorb an average of more than 70% ofPakistan's yarn exports. This means that although Pakistan is the world'slargest yarn exporter, it is competing with the rest of the world principallyin only two major markets (Annex 3). Undoubtedly, Pakistan's production isbest aligned with the Hong Kong market, where 85% of imported yarn is ofcounts between 10s and 32s. Pakistan holds a 70% share of the 16s to 20scount market and almost half of its exports are in this range. The majorportion is 16s and lower, which are mainly converted into denim, drills andcorduroy. However, since Hong Kong absorbs 50% of Pakistan yarn exports,any significant market change could dislocate the Pakistan yarn industry.In 1981, imports into Hong Kong decreased (16%) for the first time in fiveyears. This decrease was mainly in the counts up to 20s reflecting the

1/ Only 1980 was a period of exceptional performance when 10% of total yarnexports went to the EEC and quota utilization reached 98%.

-11-

slackening denim and corduroy market and Pakistan absorbed 70% of the total

decrease. Pakistan's major competitors in the Hong Kong market are China andSouth Korea but, unlike Pakistan, they also supply a large portion of finercount yarns up to 40s. Brazil has entered the market only recently, but hascaptured already 5% to 10% of the market for the count range up to 32s(Annex 4).

1.18 Since, in contrast to Hong Kong, the Japanese market trades a higherportion of finer counts (40% to 50% is above 23s), it is suprising thatPakistan increased its share from 20% to 36% between 1980 and 1981. Pakis-tan's yarn exports doubled in a market that only expanded by 8%. This isdue, however, to voluntary export restraints placed on Pakistan's competitorsand closure of low count mills in Japan, rather than an indication of achange in Pakistan's product mix. Pakistan's exports are still in thecoarse-medium count range in which South Korea is again the major competitor.

South Korea, however, covers the full range of counts and in counts above23s, South Korea provides almost all of the Japanese imports. Again, Brazilhas entered this market, but with an insignificant share as yet (Annex 5).

1.19 The EEC market has been the most difficult for the Pakistani yarnindustry to penetrate in recent years. Compared to the early 1970s, whenPakistan's share was between 8-10% of total EEC imports, Pakistan's recent

performance in this market has been generally poor and is probably due mainlyto deteriorating product quality, since prices of Pakistani yarn are _stillcompetitive and are lower than its major competitors. The EEC yarn market isdominated by three countries, Turkey, Greece and Brazil, with Turkey supply-ing the bulk of the coarser counts (8s to 23s) directly competing with Pakis-tan, while Greece dominates the finer counts between 23s to 47s (Annex 6).

1.20 Compared to other LDC yarn exporting countries, growth of Pakistan'syarn exports during the past four years is about average. Faster growthrates were experienced by Taiwan and Brazil. Exports by Greece, South Koreaand Turkey had slower growth. However, Pakistan's market and product mixwere narrower compared to competitors.

-12-

Table 1.20: Cotton Yarn Export Development - LDC Yarn Exporters('000 tons)

Annual1978 1979 1980 1981 Growth Rate

Pakistan 74.9 88.8 95.2 95.6 8.7South Korea 72.8 78.0 94.3 86.8 6.3Taiwan 17.1 23.7 30.6 30.3 /a 22.3Turkey 62.0 73.4 80.0 - 8.5Greece 59.4 51.6 62.0 54.1 -2.0Brazil 52.9 55.5 57.4 72.2 11.3

/a Estimated.

Source: Cotton World Statistics and Central Statistics Office,Government of Pakistan.

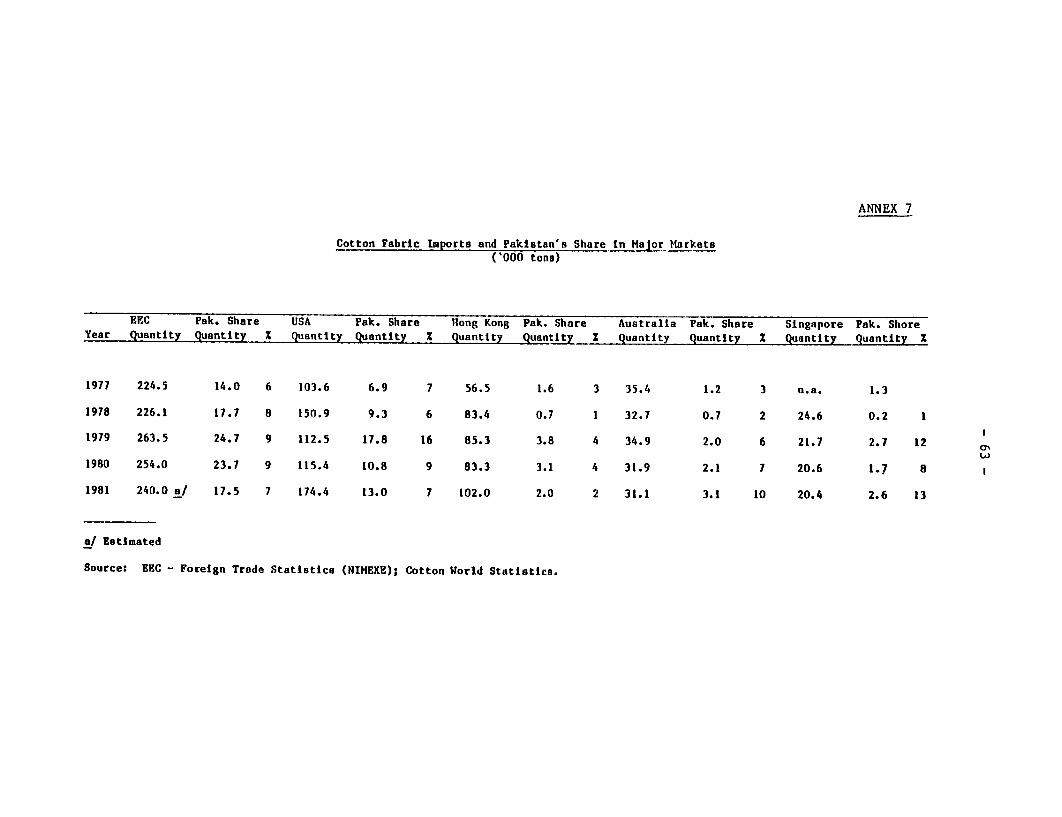

1.21 Cotton Fabric. The mill sector, which produces about one-fifth ofthe total-output, exports half its production (22,000 tons), while the power-loom sector exports about 20% of output (45,000 tons) accounting for abouttwo-thirds of exports. Practically all of fabric exports are in grey formand Pakistan is one of the world's major suppliers of cheap quality greygoods which are further processed in the importing country. From 1977 to1981, fabric export volume increased by a moderate 4.8% p.a. from 416.8 to500.9 million sq. meters. The increase in exports is accounted for solely bythe powerloom sector whose exports increased by 51% from 226.1 to 341.4million sq. meters, compensating for the decline in mill fabric export of 17%from 190.7 to 159.1 million sq. meters. The type of cloth exported is wovenfrom coarse to medium count yarn and two-thirds consist of sheeting of the20s x 20s/60 x 60 standard construction. This is a low priced, smallvalue-added item with an average export price/sq meter of between US$0.39 toUS$0.48. The major export markets for Pakistani fabrics are the EEC and theUSA, both accounting for 46% of total fabric exports. In the EEC and theUSA, Pakistan holds an average share of 8% and 9%, respectively, of the totalcotton fabric imports. Two markets have recently emerged, Singapore andAustralia where cotton is a newly developing market (Annex 7).

-13-

Table 1.21: Major Markets for Cotton Cloth(Quantity in '000 Sq. Meters)

1978 1979 1980 1981

Canada 10,275 12,584 12,519 12,017USA 65,235 124,308 75,566 91,306EEC 123,998 172,746 166,151 122,389Iran 57,417 22,590 33,765 50,422USSR 30,328 23,566 41,994 33,767Iraq 17,180 4,334 12,932 15,392Sudan 69,695 14,522 52,038 22,303Hong Kong 4,685 26,819 21,647 14,091Singapore 1,287 19,211 12,098 18,267Hungary 3,872 2,742 4,363 9,317Saudi Arabia 16,469 15,652 14,160 18,011Australia 5,110 14,283 14,681 22,000Other Countries 47,914 78,171 83,858 71,622

TOTAL 453,465 531,528 545,772 500,904

Source: Export Promotion Bureau, Government of Pakistan.

1.22 The biggest import item into the EEC market is mainly sheeting andGroup I fabrics 1/ in which Pakistan has a share of 13% to 18%. In thisgroup as well as in finer cloth, like shirting and print cloth (Group II),China is increasing her share. In the third group of heavier cloth (twill,canvas, denim), India is the biggest exporter with a share of 23% to 32% asagainst only 5% to 6% for Pakistan. One third of the EEC imports areprocessed cloth (bleached, dyed, printed or colour woven) but Pakistan'sexports in these categories of higher value-added items are practically nil.However, overall, Pakistan's quota utilization has been high averaging above

85% (Annex 8).

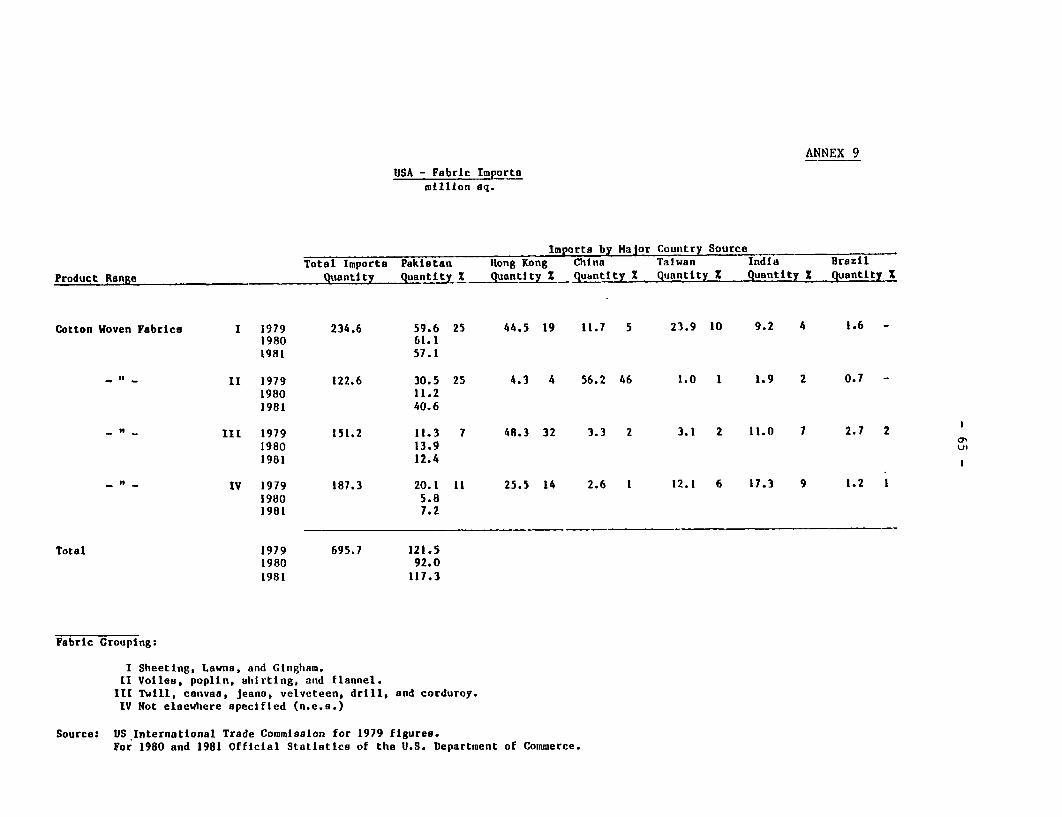

1.23 In the USA, which imports only about half of the E4C volume, Pakistan

holds the biggest share (25%) in the first group (sheeting) and is secondonly to China (46%) in the second group (printcloth) with 25% share. Like inthe EEC, Pakistan has been utilizing its quotas almost fully necessitating

use of flexibility provisions to adjust quotas upward throughout the 1978-81period (Annex 9).

1/ Fabric grouping:Group I - Sheeting, Lawns and Gingham.Group II - Voiles, Poplin, Shirting and Flannel.Group III - Twill, Canvas, Denim, Velveteen, Drills and CbrduroyGroup IV - Others.

-14-

1.24 The Hong Kong import market for cotton fabrics is about the size ofthe U.S. market, but Pakistan's exports to'Hong Kong are only one-tenth ofits USA exports, i.e., about 3% of Pakistan's total fabric exports. TheHong Kong fabric market is dominated by imports from China for grey andprocessed piecegoods and only for grey sheeting (Group I) could Pakistan gaina 9% to 10% share. For processed cloth, Pakistan's contribution is negli-gible, with the main suppliers being China and Japan. High quality require-ment measured according to re-export standards is the main obstacle indeveloping the Hong Kong market for Pakistani cloth (Annex 10).

1.25 Although Pakistan's performance in finer counts and more processedfabrics was insignificant, she dominated the coarse count grey fabric market.In her main markets, the EEC and USA, quotas were fully or almost fully used.Overall, Pakistan had the highest annual growth rate (14.5%) among major LDCtextile exporters, with the exception of China which is believed to have made

significant market entry in the recent past.

Table 1.25: Cotton Fabric Export Development-LDC Fabric Exporters-('000 tons)

AnnualAverage

1977 1978 1979 1980 1981 Growth (%)

Pakistan 37.0 51.6 58.7 68.4 60.0 /a 14.5China n.a. n.a. n.a. n.a. n.a. n.a.India 56.2 51.0 69.0 65.0 62.0 3.8Taiwan 65.7 60.4 55.7 59.1 60.7 (1.8)South Korea 25.6 27.0 25.9 35.3 35.0 9.0Brazil 21.3 20.9 25.8 25.1 30.0 9.5Hong Kong 50.3 52.9 56.6 55.6 59.9 4.5

/a Estimated. These figures differ from those of the World CottonStatistics.

Source: Central Statistical Office, Government of Pakistan.International Trade Administration, Office of Textiles andApparel, U.S. Department of Commerce.

1.26 Made-up Goods. The major export articles in this category are tentsand canvas, towels, cotton bags and bedsheets. From 1977-1981 total exportsvolume of made-up goods increased by 145%, with cotton bags growing fastest.Price improvement, however, occurred only in towel exports while prices fortents/canvas, cotton bags and bedsheets deteriorated in real terms.

-15-

Table 1.26: Made-up Exports

(in '000 tons and 1977 US$ million)

Ratio of Unit1977 1981 Value 1981 to

Quantity Value Quantity Value /a Unit Value 1977

Bedsheets, napkinsand others 2.2 7.1 8.1 21.9 0.84

Towels 5.1 14.2 11.2 33.1 1.07Tents and canvas 12.8 25.0 23.6 45.2 0.95Cotton bags 3.8 8.3 15.6 24.7 0.72

/a Deflated using the International Price Index, World Bank.

Source: Export Promotion Bureau, Government of Pakistan.

1.27 Major markets for bedsheets, napkins and others are the EEC (30%),the Gulf States (26%), and the USA (11%). China is becoming an importantmarket expanding about nine times from 1977-81. The EEC, however, continuesto be the main and also the fastest growing market. Towel exports go mainlyto the USA (63%), and the EEC (12%). Saudi Arabia is emerging as a sig-nificant market, growing almost 20 times from 1978-1981 and accounting foralready 6% of total exports. The USA still continues to dominate, growingmore than 5 times in the same period. As for tents/canvas, the major marketsare the Middle East and the EEC. The Middle East accounts for three fourthsof total exports with Saudi Arabia absorbing more than half of the MiddleEastern share. While exports to the EEC increased two-and-a-half times theystill account for only 4% of total.

1.28 Readymade Garments. Garment exports increased from 1977 to 1981 by71% in volume from 31.6 to 54.1 million pieces and by 148% in value fromUS$30.4 to US$75.3 million. The product mix in this period shows that theshare of outer garments and shirts increased to 90% of the total exportvalue. Blouses and knit shirts are the main products for the USA market,while dresses, trousers, shirts and blouses go to the EEC market.

-16-

Table 1.28: Garment Export by Product Lines

1977 1978 1979 1980 1981Quantity Value Quantity Value Quantity Value Quantity Value Quantity Value

Gloves(non-knit) 416.6 7,963 635.6 15,207 1,099.1 22,604 1,808.6 43,507 1,734.7 35,600OuterGarments 1,079.5 171,010 710.9 147,987 1,099.1 231,961 1,372.7 360,642 1,544.7 441,754Shirts &Bush Shirts 436.4 63,681 161.0 25,655 153.3 29,397 294.4 58,730 946.3 227,183Scarves 24.4 1,475 28.4 1,902 26.7 2,214 72.9 6,697 107.8 8,309Under-Garments 4.9 468 Neg. Neg. 3.4 607 45.0 5,436 77.7 14,784Handkerchiefs 135.5 2,580 102.2 2,604 39.7 934 43.2 622 37.0 1,702ClothingAccessories 501.6 32,042 313.6 72,059 283.8 67,371 109.9 40,506 35.8 4,467Pants 9.8 1,792 2.5 490 2.4 624 1.7 561 14.8 2,783Arab Romals 6.4 2,597 13.2 2,711 3.3 1,685 3.1 1,148 2.0 372Shawls 16.5 16,180 36.7 29,225 20.8 20,.627 12.4 11,537 1.8 6,702Frocks &Costumes Neg. Neg. - - 0.1 23 0.2 82 0.1 35Coats 1.9 542 1.8 714 1.2 378 5.4 3,049 1.9 961Others 1.4 143 3.2 2,019 1.3 116 13.3 834 - -

TOTAL 2,634.9 300,477 2,009.1 300,575 2,734.8 378,541 3,782.8 533,351 4,504.6 744,652

Source: Export Promotion Bureau, Government of Pakistan.

1.29 The main markets for Pakistani garment exports are the EEC, with theUK and West Germany taking almost 60%, followed by the USSR, Eastern Europe,the USA, and the Middle East. The increase in garment exports was equallydistributed over the major markets during the five-year period.

-17-

Table 1.29: Major Markets for Garments

1979 1980 1981Quantity Value Quantity Value Quantity Value

EEC 14.87 100.88 20.81 182.20 23.16 184.50(45) (27) (46) (34) (43) (25)

USA 8.03 81.93 9.60 101.13 12.92 138.60(25) (22) (21) (19) (24) (19)

USSR & Eastern 3.65 83.77 3.60 107.57 4.47 165.30Europe (11) (22) (8) (20) (8) (22)

Middle East 2.91 65.97 3.61 73.36 5.54 131.50(9) (17) (8) (14) (10) (18)

Canada 0.37 3.06 1.72 10.56 2.63 17.40(1) (1) (4) (2) (5) (2)

Others 2.97 42.93 6.01 58.53 5.38 107.40(9) (11) (13) (11) (10) (14)

TOTAL 32.80 378.54 45.39 533.35 54.10 744.70(100) (100) (100) (100) (100) (100)

Source: Central Statistics Office, Government of Pakistan.

1.30 Hosiery (Knitwear). Hosiery had the weakest export performance,growing only from 23.3 to 28.1 million pieces from 1977 to 1981. This quan-tity represents about one-third of domestic production. The reasons for thepoor export performance are the difficulty of finding cotton yarn of satis-factory quality for knitting and the high price of the imported syntheticyarns. Also, there is a good home market for whatever quantities the localknitting operations can produce. In value terms, the increase from 1978 to1981 was by 137% to US$23 million, indicating improving quality of hosieryexports. The major markets in the past years have been the USA (36%), theEEC (38%), Hungary (7%), and Saudi Arabia (5%):

-18-

Table 1.30: Major Markets for Hosiery (Knitwear)(Value in US$'000)

1978 1979 1980 1981

EEC 1,721 3,564 8,046 8,836USA 5,429 6,780 7,527 8,439Hungary 1,007 500 567 1,711Sweden 65 157 722 1,119Saudi Arabia 172 92 125 1,103Other 1 1 2

TOTAL 9 12.314 19,984 23,187

Source: Export Promotion Bureau, Government of Pakistan.

D. Financial Performance

1.31 In 1981, the financial performance and status of the mill sector 1/deterioriated from the previous year. Although sales increased, the millslost money on operations due to increased operating cost. Profits came onlyfrom other sources, principally government rebates. There was practically nomovement in the mills' already precarious liquidity position and capitalstructure. Return to investment was substandard and could not attract inves-tor interest.

Table 1.31: Financial Ratios of Mill Sector

1980 1981

Current Ratio 0.77:1 0.76:1Total Debt/Equity 78:22 79:21Operating Profit/Sales 0.008 (0.003)Gross Profit/Sales 0.12 0.10Pre-Tax Profit/Sales 0.02 0.01Pre-Tax Profit/Total Assets 0.02 0.01Pre-Tax Profit/Equity 0.08 0.05Pre-Tax Profit/Investment 0.05 0.03

Source: All Pakistan Textile Mills Association, Karachi.

1/ Based on the audited financial statements of 78 mills (49 spinning and 29composite mills), which account for about 45% of spinning capacity andabout 50% of mill weaving capacity.

-19-

1.32 In general, the composite mills performed better than the spinningmills. Although performance was poorer compared to the previous year, thecomposite mills made operating profits while the spinning mills lost money onoperations. The composite mills also shows a stronger financial positionthan the spinning mills despite more capital infusion in the spinning millgroup. Reflecting poor financial performance, the stocks of most textilemills (73 out of 105) are quoted much below par. Stockholders could not bepaid dividends in the past five years by most of these mills. Arrears withfinancial institutions continued to increase. 1/

Table 1.32: Financial Ratios Comparing Spinning vs. Composite Mills

Spinning Mills Composite Mills1980 1981 1980 1981

Current Ratio 0.60:1 0.59:1 0.90:1 0.89:1Total Debt/Equity 90:10 87:13 69:31 72:28Gross Profit/Sales 0.11 0.10 0.12 0.10Operating Profit/Sales (0.008) (0.012) 0.02 0.004Pre-Tax Profit/Sales 0.001 0.002 0.03 0.013Pre-Tax'Profit/Total Assets 0.001 0.003 0.03 0.015Pre-Tax Profit/Equity 0.01 0.02 0.10 0.05Pre-Tax Profit/Investment 0.003 0.008 0.07 0.04

Source: All Pakistan Textile Mills Association, Karachi.

1.33 The overall picture of the textile industry over the most recent fiveyears is quite dim. Overall production decreased, effective capacity hasbeen reduced, and capacity utilization and productivity have declined. Thesehave caused the already poor financial position of the textile mills todeteriorate. Operating losses have aggravated their capital structure. Theonly bright spot in the overall picture is the buoyant export performance.Not only did all textile products increased in exports but the product mixhas improved reducing the share of traditional textile products and replacingthem with other products with more value-added. The major causes of thispoor performance are discussed is the next chapter.

1/ APTMA.

-20-

Chapter II. MAIN PROBLEMS

A. Product Quality

2.01 Yarn. Although the Pakistani spinning industry offers various

qualities to the export market, most exports are in the coarse to mediumcount range with 50% below 21s and 90% below 34s. 1/ Several qualityproblems are associated with Pakistani yarn: in general, technical specifica-

tions are not always met, quality is not always consistent in the same lotand is often inferior to original samples; twist factors, counts, weights andother technical specifications are uneven. Often Pakistani yarn requiresrewinding by the end-user to improve quality.

2.02 3ecause of low quality, Pakistani yarn has fetched low prices inexport markets. Even good mills suffer from the poor image of the country asa yarn supplier. In fact, unit export price declined in real terms by 12%from 1977-81. Recent price quotations in the Hong Kong market show thatPakistan prices range from 3% to 25% lower than those of competitors, withthe exception of China. 2/ From 1978-82 prices of Pakistani yarn, C&FEurope, were on average between 11% and 48% lower than those of other sup-pliers.

1/ Average yarn count produced in Pakistan increased only from 20.01 to20.81 from 1973-81, despite increased production of longer staple cotton.The share of coarse count yarn increased from 53% to 54% and that ofmedium from 42% to 46% in the same period.

2/ Origin FOB, Origin CIF, Hong Kong

(in US cents/kg)

China - 200Korea 204 248Taiwan 209 253Pakistan 210 240Brazil 220 280India 253 283Turkey 275 300Greece 305 320

Source: Cotton Outlook, October, 1982.

-21-

Table 2.02: Index Comparison of Average Yarn Prices by Origin(NE 20; "C&FEurope)

Origin 1978 /a 1979 1980 1981 1982 Average

Pakistan 100 100 100 100 100 100Korea 118 117 105 115 105 112India 108 107 120 125 120 116Taiwan 127 121 122 120 106 119Turkey 118 142 167 118 118 132Brazil 128 139 167 117 118 134Greece 150 187 325 180 150 198

/a Calendar Year.

Source: Cotton Outlook, 1978-82.

2.03 Fabrics. The bulk of fabric exports from Pakistan is cotton greygoods made of coarse count yarn (21s), narrow (38"), of standard construction(60 x 60) and generally of poor quality. Faulty handling (on the shop floor)in the mills and, more so, in the powerloom sheds, accentuates poor fabricappearance through dirt and oil contamination. The basic quality of the

fabric and the poor overall appearance limit Pakistan's market to end-uses,such as lining, pockets and agricultural crop cover where blemishes are notcritical, for which no quality premium is paid, and in which there could bedirect competition from cheap synthetic substitutes. As a result, prices ofPakistani fabric exports have been among the lowest in the world. Averageunit price decreased by 20% in real terms from 1977-81.

2.04 In October 1982, FOB price of 38" wide cotton grey cloth (21s x21s, 60 x 60) was US$0.28/yard for powerloom cloth and US$0.35/yard formill-made cloth. 1/ Quotations for the same fabric for October/November 1982

shipment from Pakistan's competitors reveal that prices for Pakistani fabricscould be between 4% to 38% below those of its competitors, except Brazil

1/ Pakistan Cloth Merchants Association.

-22-

which is about the same and China which is 4% lower. 1/ From 1978-82 Pakis-tani fabrics on average fetched prices between 2% and 24% below those ofcompetitors.

Table 2.04: Index Comparison of Average Fabric Prices by Origin(20 x 20, 60 x 60, grey; C&F Europe)

Origin 1978 /a 1979 1980 1981 1982 Average

Pakistan 100 100 100 100 100 100Hong Kong 119 104 97 /b 96 96 102India 126 110 101 121 134 118Brazil 139 142 121 117 121 128USA 147 120 128 136 128 132

/a Calendar Year.

/b It is significant that in the last three years Hong Kong,probably using Pakistani yarn, could sell fabrics slightlylower than Pakistan due to higher productivity at conversion.

Source: Cotton Outlook, 1978-1982.

2.05 Despite low prices, the market for Pakistani fabrics in more demand-ing markets has been declining. Many of the German importers interviewed whohad previously handled Pakistani fabrics, would not want to do it again. Theproblems with powerloom fabrics are even greater due to the inevitablepresence of many starting marks in the fabric. Moreover, quality in one lot(coming from different loomsheds) usually is not consistent. Weavers alsohave no facility for controlling the counts of yarns purchased so that coar-ser counts are passed as finer counts and different counts are bought andused in the same piece. It is not uncommon to have one piece woven of dif-ferent yarn counts. These defects do not show while the fabric is unfinishedbut inevitably appear after processing. In general, while the weaving

1/Offering Price C&F

Origin Width Europe US$ per sa meter

Pakistan 38" 0.51India 38" 0.61China (through Hong Kong) 36" 0.49Germany 120 cm 0.82USA 59" 0.53Brazil 59" 0.51Source: Cotton Outlook, October 1982 (prices have been adjusted by the

mission to arrive at C&F Europe price per sq meter).

-23-

process itself in the powerloom sector is technically good, much improvementis needed in the weaving preparation and after-weaving methods and processes.

B. Labor Productivity

2.06 Pakistan has one of the lowest wage levels among the more importanttextile producing countries of the world, ranking 39th out of 42 countries

(para. 2.07). This cost advantage, however, has been undermined by low laborproductivity. In spinning, output per operator hour is only 2.1 kg asagainst the international average of 11.5 kg and the industrial countriesaverage of 20 kg. An achievable level of 5.8 kg proposed by the WernerReport has not been attained. As a result, Pakistan's labor cost per unit ishigher than that of Korea, India, Brazil and even Japan:

Table 2.06: Labor Cost Per Unit Output in Spinning /a

Cost/Kg Yarn /b Index

1981 US Cents

Korea 6.4 0.29India 11.7 0.54Brazil 16.0 0.73Japan 18.0 0.83Pakistan 21.8 1.00USA 24.6 1.13Germany 36.8 1.69

/a Exchange rates used in arriving at US dollarequivalents in this and subsequent internationalcost comparison tables are average D1F marketrates (International Financial Statistics).

/b This is the result despite the fact that laborcost in Pakistan is based on spinning 20s whilethat of other countries, 24s.

Source: Gherzi Textile Organization, Zurich.

2.07 From 1979-81 wages for Pakistani labor has also been increasingfaster than those of competitors, except South Korea, Brazil and India.Between 1979 and 1981 wage levels in Pakistan increased by 20%, almost doublethe average increase of its competitors.

-24-

Table 2.07: Comparision of Textile Industry Wage Levels and Wage Increases

(US dollar/hour)

Average Annual % Increase from

1979 1980 1981 Increase (%) 1979 to 1981

Hong Kong 1.72 1.91 1.42 (8) (17)Germany 10.19 10.65 8.17 (9) (20)Italy 7.00 9.12 7.23 5 3Taiwan 1.16 1.26 1.32 7 14

USA 6.08 6.37 7.03 8 16Turkey 1.56 0.95 1.07 (13) (31)Greece 3.54 3.58 4.03 7 14Japan 4.53 4.35 4.90 5 8T ndia 0.53 0.60 0.69 14 30?aKistan 0.35 0.34 0.42 11 20

Brazil 1.86 1.57 2.39 18 28South Korea 0.75 0.78 1.35 39 80

Average 7 12

Source: Textile Industries, 1981.

2.08 Present labor legislation requires employers to pay several fringebenefits for workers. In the textile industry this can be as high as 80%of base pay. Aside from social security (7-8%), there are the education ces(Rs 100/worker/year), old-age benefit (7-8%), worker participation fund (5%),requirements for facilities such as transportation, canteens, bathrooms, etc.Since the textile industry pays workers higher than minimum wages and prob-ably market wage rates, the level of benefits paid to Government on behalfof workers are substantial. Moreover, current labor policy prevents paymentof wages on the basis of productivity. Mills are usually overstaffed sinceit is not allowed to fire workers, even on reasonable grounds. Inefficiencyand low morale are common among workers in the textile industry.

C. Cost Competitiveness

2.09 Spinning. Comparing Pakistan's yarn manufacturing cost with that ofits competitors, it would appear that it has the lowest cost among majorcompetitors, except India. Further analysis, however, shows that this isbecause of lower input costs rather than more efficient operations. Specifi-cally, this is due to two factors: (i) Pakistan's cotton cost is lowest,i.e., between 3% and 18% lower than that of its competitors; and (ii) in thiscomparison Pakistan's capital costs are based on data from existing millswhile those of other countries are based on new mills. Without the cottoncost advantage, and if capital costs are ignored (to make the data more

comparable), Pakistan's conversion cost becomes the highest except for Ger-many. In other words, Pakistan's competitive edge has hinged principally oncheaper cotton prices and depreciated equipment.

-25-

Table 2.09: Breakdown of Manufacturing Costs Per,Kg Yarn (24s)(1981 US$)

PakistanPakistan /a Adjusted

Cost Item Brazil Germany India Japan Korea USA 20s 24s

Cotton 1.9703 2.1978 1.9095 2.2342 2.2446 1.9688 1.4880 1.9090

Labor 0.1607 0.3680 0.1169 0.1801 0.0640 0.2461 0.2180 0.2430

Power 0.0801 0.1387 0.1183 0.2061 0.1579 0.0750 0.1090 0.1220

Auxiliary 0.0394 0.0336 0.0315 0.0435 0.0298 0.0350 0.0790 0.0860Materials

Capital 0.8548 0.5128 0.3882 0.5802 0. 3915 -0.6996 0.,2090 0.2090

ManufacturingCost 3.1053 3.2509 2.5644 3.2441 2.8878 3.0245 2.1030 2.5690

Index 1.21 1.27 0.99 1.26 1.12 1.18 - 1.00

ConversionCost 1.1350 1.0531 0.6549 1.0099 0.6432 1.0557 0.6150 0.6600

Index 1.72 1.60 0.99 1.53 0.97 1.60 - 1.00

ConversionCost WithoutCapital Cost 0.2802 0.5403 0.2667 0.4297 0.2517 0.3561 0.4060 0.4510

Index 0.62 1.20 0.59 0.95 0.56 0.79 - 1.00/a Average of eight largest exporting mills.

Sources: Pakistan: All Pakistan Textile Mills Association, Karachi.Other Countries: International Textile Mills Federation, Zurich.

2.10 Pakistan's cost disadvantages are in labor costs and costs ofauxiliary materials, spares and supplies. Labor cost is higher than that ofKorea, India, Brazil and Japan and lower only in comparison to that of theUSA and Germany due to low labor productivity (para 2.06). Cost of auxiliarymaterials, spares and supplies is highest for the Pakistani spinner (betweentwo to three times) due to high import duties and taxes and the diversity ofequipment models. There are 23 different makes of spinning machineryinstalled in the mill sector, each accounting for 0.001% to 25% of totalspindles installed, raising spares inventory-carrying cost. Moreover, sincein this comparison Pakistani data are based on the eight leading exporting

-26-

mills, it would appear that the remainder of the industry can only be con-

sidered to be extremely inefficient and in no position to compete interna-tionally.

2.11 Weaving. Comparing with the same countries, fabric conversion costis highest in Pakistan, with the exception of Germany, even when capitalcosts are included. Korea has the biggest competitive edge at 35% belowPakistan; Brazil is 5% lower. Since, as in the spinning cost comparison,existing Pakistani mills are compared with new mills in the other countries,excluding capital costs would further widen the competitive edge ofPakistan's competitors.

Table 2.11: Fabric Conversion Cost Comparison(Grey Cotton Fabric 24s x 24s, 76 x 64)

(1981 US$)

PakistanMill Sector Brazil Germany India Japan Korea

US$/sq. meter 0.311 0.294 0.312 0.221 0.267 0.201Index 1.00 0.95 1.003 0.71 0.86 0.65

Sources: Pakistan: All Pakistan Textile Mills Association, Karachi.Other Countries: International Textile Mills Federation, Zurich.

2.12 Only when the cost of yarn is included, is Pakistan's cost lower thanthat of Brazil, Japan and Germany. India's and Korea's costs, however,remain lower than Pakistan's.

Table 2.12: Fabric Manufacturing Cost Comparison(Grey Cotton Fabric 24s x 24s, 76 x 64)

(1981 US$)

PakistanMill Sector Brazil Germany India Japan Korea

Yarn 0.352 0.425 0.445 0.351, 0.444 0.396

Conversion 0.311 0.294 0.312 0.221 0.267 0.201

Total 0.663 0.719 0.757 0.572 0.711 0.597

Index 1.00 1.08 1.14 0.86 1.07 0.90

Sources: All Pakistan Textile Mills Association, Karachi.International Textile Mills Federation, Zurich.

-27-

2.13 Pakistan's powerloom sector compares better with competition sinceits conversion cost is only about a third of the mill sector (para. 2.22).Thus competitors' costs are between two to three times the costs of thePakistani powerloom sector. India, however, has also a large powerloomsector which can also produce fabrics at lower than the Indian mill sector'scosts.

Table 2.13: Fabric Conversion Cost Comparison(Grey Cotton Fabric 24s x 24s x 76 x 64)

(1981 US$)

PakistanPowerloom Brazil Germany Japan Korea

US$/H2 0.100 0.294 0.312 0.267 0.201Index 1.00 2.9-1 3.12 2.67 2.21

Sources: All Pakistan Textile Mills Association, Karachi.International Textile Mills Federation, Zurich.

2.14 These factors have caused a price-cost squeeze on Pakistani exportsof textile products. While, in general, Pakistan fetches lower prices thanits competitors, it has also higher costs. As a result, in financial terms,the mills lose on average about 24% of the cost of production for every meterexported.

Table 2.14: Profitability of Grey Fabric Exports(Mill Sector)

Selling Price Rs 4.18Add: Rebates (10.5%) /a 0.44

Excise Duty Rebate /b 0.14 4.76

Less: Cost of Yarn 3.22Sizing 0.11Conversion 2.53Packing 0.04

0.35 6.25(Loss) (1.49)

/a Compensatory Rebate = 10%; Customs Duty Reoate = 0.37%;Sales Tax Rebate 0.11%.

/b Excise Duty is Rs 1.00/kg or Rs 0.14/sq. meter.

Source: All Pakistan Textile Mills Association, Karachi.

/usrl7/asnvp/jean/ASNID/pak.texstudy/chap2/6-14-83pm/rev

-28-

2.15 The same situation is true of yarn exports, though the loss is.much

smaller at around 1% of cost of production.

Table 2.15: Profitability of Grey Yarn Exports

Selling Price (Rs/10 lbs) 96.01

Add: Rebates (7.5%) /a 7.20 103.21

Less: Cost of Cotton 65.22

Conversion 36.43Export Packing 2.00 103.21

(Loss) (0.44)

/a Compensatory Rebate = 7.5%; there are no ocher rebates for greyyarn exports.

Source: All Pakistan Textile Mills Association, Karachi.

D. Plant Efficiency

2.16 Average output per spindle year was only 121.9 kg or 86% of the

five-year plan target output of 141.7 kg. Since only 70% of capacity was

operating, output was only 60% of installed capacity at target productivity.

This cannot be attributed to the age of equipment. The age distribution of

spindles appears favorable and compares well even with advanced countries.

In West Germany, for example, which still is considered a very efficient

producer of quality yarns (and the world's biggest exporter of textiles), 85%

of the ring spindles are more than 10 years old. Most of the machines,however, have been rebuilt and equipped with modern drafting systems, high

speed rings, spindles and pneumatic systems. Quality levels achieved on

converted machines can compare favorably with new equipment. Most of the

older ringframes in Pakistan have not been well maintained or rebuilt and

converted due to high cost of spares and accessories which are imposed duties

and taxes.

Table 2.16: Age of Spindles in Pakistan(in million spindles)

Total Spindles 1980-70 1970-60 Before 1960

4.3 1.7 1.2 1.4

Years 10 11-20 20 and more

100% 40% 28% 32%

Source: Textile Machinery Corporation of Pakistan, Ltd.

-29-

2.17 Age of equipment does not, however, tell the whole story. In thecase of ringspinning there have been considerable advances in productiontechnology in the last 10 years and machines older than 10 years, even ifrebuilt deliver, on an average, 10-15% less output and lack such labor savingdevices as automatic doffing. The replacement age has to be decided on acase by case basis and on the basis of a comparative analysis of the cost ofrebuilding a machine against the cost of a new frame. General rules, such asthe rule that only 18-year-old machines may be replaced, cause more problemsthan they can solve. Considering that ringframes in Pakistan are used mainlyfor spinning of coarse counts which places a great strain on the machine,frames older than 20 years probably should not be rebuilt but replaced.However, as a principle, mills should be allowed to replace machines at thepoint of time they consider economic.

2.13 In weaving, while target productivity was achieved, it is still muchbelow international levels, i.e., 65% loom efficiency compared to 85-90% inEurope and 92-95% in the USA. This is partly due to.age of looms .in themills where over 75% are above 28 years old. A major factor, however, ispoor maintenance of machinery brought about by high duties and taxes onspares and stores, making Pakistan the highest cost country in this regard.The financial position of most mills has aggravated the poor condition ofequipment, as the mills had little profit to plow back into operations.Moreover, disinvestment was reportedly a common phenomenon, especially in theearly and mid-1970s.

E. Structural Problems

2.19 Spinning. The spinning sector is characterized by a high degree offragmentation into small units. There are at present about 211 plants with atotal of about 4.2 million spindles. There are 142 spinning mills with 2.4million spindles giving an average plant size of 17,000 spindles. There are69 integrated mills with 1.8 million spindles or an average plant size of26,000 spindles.

2.20 Moreover, there are 62 mills with only 12,000 spindles or less. Onthe other hand, the major competitors of Pakistan in the yarn export markethave plants of much bigger size. The optimum where both flexibility andeconomies of scale are met for the present range of counts is not 12,000spindles. Conditions should be created in which spinning mills could mergeallowing the merged units to specialize in narrower ranges of counts topermit skill specialization and maximum utilization of the equipment. 1/

1/ The published plans of the Taiwan Textile Federation calls for theencouragment of mergers of smaller spinning mills into plants with50,000 spindles and of medium-sized plants into plants with 100,000spindles. The same plan calls for the merger of weaving plants tocreate plants having 500 to 1,000 looms.

-30-

2.21 Weaving. There are about 25,000 looms installed in the mill sector.With 69 mills the average plant size would be about 360 looms which could beconsidered near optimum for a medium sized plant, i.e., requiring one warppreparation. Assuming, however, that only 13,000 looms are left in the millsector, with the rest transferred to the powerloom sector, the average plantsize is reduced to 190 looms which could be sub-optional. While there aremany reasons for the idling of looms in the mill sector, it appears that themajor cause is the failure of the mill sector to stay away from direct com-petition with the powerloom sector. As a result the output share of the millsector declined from 25% in 1977 to 17% in 1981.

2.22 It is quite clear that even with the premium on mill cloth, the millsector would never be able to compete with the powerloom sector in the marketfor traditional Pakistani fabric. The main cost advantages of the powerloomsector are lower labor cost (since they can stay outside the scope of laborlegislation), lower overheads (lower capital and administrative costs andexemption, in practice, from taxation), while their only major cost disad-vantage is probably higher yarn cost since they have to purchase yarn throughthe distribution channel, i.e., after middle-men mark-ups. The onlyadvantage the powerloom sector has over the mill sector due to explicitgovernment policy is exemption from excise taxes but this is a minoradvantage. Overall, mill fabric conversion cost is about three times that ofthe powerloom sector. Since the price for mill cloth is higher than that forpowerloom cloth by about 25%, and assuming that yarn cost for the powerloomsector would include a 20% wholesale mark-up, the net disadvantage of themill sector is about 28% which is substantial.

Table 2.22: Comparison of Profitability Between Mill and Powerloom Sectors(38" wide 20 x 20, 60 x 60)

Mill Non-Mill

Selling Price/Yard Rs 4.38 Rs 3.54Cost of Yarn 2.99 3.59Conversion Cost 2.45 0.80Excise tax 0.12 /a -

Net Profit (Loss) Rs(1.18) Rs (0.85)

/a Rs 1.00/kg or 0.12/yard.

Source: Mill Sector - All Pakistan Textile Mills Association, Karachi.Non-Mill - Mission Interview

2.23 Processing. The processing sector shows also a high degree of frag-mentation. Again as in spinning, merging into bigger sized plants with ayearly capacity of 15-30 million sq meters should be encouraged. Plants ofthis size could also afford much needed effluent treatment which does not yet

-31-

exist in Pakistan. Plants should also be located in areas where there isadequate access to water, which,is a major.-r.equirement for a processingplant.

2.24 In 1981, there were about 165 finishing plants of which only 29 wereintegrated with spinning and weaving plants and of the remainder only about10 can be categorized as industrial plants. Many of the plants are closed,including about half of the integrated plants. The total installed finishingcapacity is estimated to be 1,150 million m2 . Out of the total mill sectorproduction of 307 million in 1981, 195 million were sold as grey, 35 millionas bleached and 50 million as dyed and printed. A modern bleaching range canproduce about 20 million sq meters, i.e., about 15 machines could bleach theentire production of the mill sector or only 2 modern machines would havebeen required to bleach the entire bleached fabric production in 1981.

2.25 Finally, there are the problems of insufficient infrastructure, suchas shortage of power and water, which have become more pronounced due to theheavy geographic concentration of capacity. Spinning and weaving have beenconcentrated in the Sind Province (50%), of which about 30% is in the Karachiarea, and Punjab Province (45%). For example, in the Karachi area, mills areforced to shut down one day in a week due to power shortage. This is on topof unscheduled power outages which are even more costly. While the Govern-ment has tried to disperse industry to less developed areas by incentives,the private sector's response has been understandably lukewarm due to evenpoorer facilities in those areas. Considering the general infrastructureshortage throughout the country, it appears that in the short term improvingthe supply of infrastructure to key growth areas could be the more effectivealternative than dispersal of industries. The five-year plan has to addressthe problem of inadequate infrastructure if mill productivity is to beincreased.

-32-

Chapter III. MAJOR PROSPECTS

A. Domestic Market

3.01 In 1981, domestic per capita consumption of textile products of allfibers was 1.93 kg equivalent to 13.5 sq. meters. This was the lowest con-sumption level in the five-year period and was only half of the peak level of3.72 kg (26 sq. meters equivalent) in 1978. There are several reasons givenfor this drastic drop in domestic consumption. First, there is the increas-ing volume of legal and illegal imports for which there are no records.Overseas Pakistanis are allowed to bring in 150 sq. meters of fabric per yearduty-free. There are the so-called BARA markets which sell imported fabrics(mainly blends) which have expanded phenomenally in the past years. Second,there has been an increase in consumption of locally made blend fabrics whichare two to three times more durable than all-cotton fabrics. The productionfrom man-made fibers increased from 41,500 tons in FY1977 to 55,300 tons in1981 despite the overall output decline, increasing its share from 10% to 13%of total output of yarn equivalent. Finally, there have been increasingimports of used clothing, both woven and knitted. Imported used knitwearis claimed to be the main reason for the decrease in domestic consumptionof hosiery sector from 0.12 kg to 0.10 kg per capita from 1977-81. 1/

3.02 While it is difficult to estimate how much of the drop in per capitaconsumption is attributable to offsetting factors (imports and more durableblend goods), it seems that the decline in per capita consumption of 12.5 sq.meters per capita cannot be all explained by unrecorded imports and moredurable blend fabrics. 2/ It might be useful for the Government to conduct aconsumption survey to determine the level of consumption of textile productsof all fibers. It also would seem desirable to have as a goal for the nextfive years up to 1988 recovery of domestic supply of fabrics to the 1978level of 26 sq. meters. While this target would merely provide the samelevel of textile goods as in 1978, a further shift towards blend fabricconsumption should effectively improve per capita consumption over the 1978level.

3.03 This recovery target implies that in 1988 when the population wouldreach 100 million 3/ the textile industry would have to increase production

1/ A Report on Hosiery Industry in Pakistan, PICIC, July 1982. Otherreasons proposed include the possibility of under-reporting of output toavoid taxes, and over-reporting of exports to ,avail of export incentives.

2/ Extrapolating from the 1977 per capita consumption level using an incomeelasticity of 0.4 and real income growth p.a. of 3.3%, the per capitaconsumption in 1981 would have been 3.47 kg and in 1988 would be 3.80 kg.

3/ Population growth rate of 2.8% p.a.

-33-

for the domestic market to reach 372,000 tons or 133% more than the 1981level. This would mean'an annual.compound rate of 13% p.a. Compared to thepeak supply level in 1978 of 281,600 tons the increase required is only 32%.This should be an attainable five-year target since at least already 75% ofthe capacity is in place.

3.04 What is crucial in the plan is the relative emphasis given to thecontribution to the target by the mill versus the powerloom sector. Assumingthat no special effort is placed to reviving the mill sector the expectationis that the powerloom sector would continue to dominate, probably accountingfor more than 90% of fabric output by the end of the period (Alternative I).However, if there is a significant shift in the incentive environment, whichwould allow the mill sector to restructure and revive, the contribution ofthe mill sector could increase to about 15% at the end of the five-year planperiod (Alternative II).

Table 3.04: Apparent Domestic Fibre Demand /a

1988 1988 19881978 1981 '000 tons '000 tons kg p.c.

Source kg p.c. kg p.c. (projected) (projected) (projected)Sector (actual) (actual) Alternative I /b Alternative II AI AII

Hosiery 0.12 0.09 12 12 0.12 0.12Mill Sector 0.22 0.16 22 40 0.22 0.40UnorganizedSector 2.62 1.19 262 244 2.62 2.44

Towel 0.07 0.02 7 7 0.07 0.07Art-Silk 0.39 0.23 39 39 0.39 0.39Woolen Sector 0.30 0.24 30 30 0.30 0.30

Total 3.72 1.93 372 372 3.72 3.72

Population(million)(projectedat 2.8% p.a.) 75.63 82.60 100 100

/a Not including unrecorded import of textiles./b Alternatives I and II indicate the different contributions to projected