World Bank Documentdocuments.worldbank.org/curated/en/999141468059332347/pdf/multi0... · -i - for...

53

Report No. 2538 FILE COPY PROJECT PERFORMANCE AUDIT REPORT PANAMA - TOCUMEN INTERNATIONAL AIRPORT PROJECT (LOAN 783-PAN) June 11, 1979 Operations Evaluation Department Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized Public Disclosure Authorized

Transcript of World Bank Documentdocuments.worldbank.org/curated/en/999141468059332347/pdf/multi0... · -i - for...

Report No. 2538

FILE COPY

PROJECT PERFORMANCE AUDIT REPORT

PANAMA - TOCUMEN INTERNATIONAL AIRPORT PROJECT(LOAN 783-PAN)

June 11, 1979

Operations Evaluation Department

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

- i - FOR OFFICIAL USE ONLY

PROJECT PERFORMANCE AUDIT REPORT

PANAMA - TOCUMEN INTERNATIONAL AIRPORT PROJECT(LOAN 783-PAN)

Table of Contents

Page No.

PREFACE ii

PROJECT PERFORMANCE AUDIT BASIC DATA SHEET iii

HIGHLIGHTS iv

PROJECT PERFORMANCE AUDIT MEMORANDUM

I. Background 1II. The Project 2III. Main Points of Interest 7IV. Conclusions 11

Annexes

I. The Overall Concept of the New Tocumen Airport 13

II. Direccion de Aeronautica Civil - AnticipatedReturn on Net Operating Assets (1979-1985) 15

ATTACHMENT: PROJECT COMPLETION REPORT

I. Introduction 16II. Project Preparation and Appraisal 16

III. Project Implementation and Cost 18IV. Traffic and Operating Performance 23V. Financial Performance of the Borrower 23

VI. Institutional Performance and Development 27

VII. Economic Reevaluation 29

VIII. Bank Performance 32

IX. Conclusions 33

Tables

1. Actual and Appraisal Estimates of Project Cost 35

2. Schedule of Disbursements as of 31 December 1977 36

3. Actual and Appraisal Airport Traffic Projections 37

4. Actual and Projected Income Statements of DAC,1971-1977 (Figures in Balboas '000) 38

5. Actual and Projected Balance Sheets of the AirportAuthority, 1971-1977 (Figures in Balboas '000) 39

6. Actual and Appraisal Expectation of Project Financing 407. Summary Status of Principal Covenants 41

Map

This document has a restricted distribution and may be used by recipients only in the performanceof their official duties. Its contents may not otherwise be disclosed without World Bank authorization.

- ii -

PROJECT PERFORMANCE AUDIT REPORT

PANAMA - TOCUMEN INTERNATIONAL AIRPORT PROJECT(LOAN 783-PAN)

Preface

This report presents a performance audit of the Panama - TocumenInternational Airport Project for which Loan 783-PAN in the amount ofUS$20 million was closed fully disbursed in July 1977. It consists ofa memorandum prepared by the Operations Evaluation Department (OED) and aProject Completion Report (PCR) prepared by the Bank's Latin America andCaribbean Regional Office.

An OED mission visited Panama in January 1979 to review the re-sults of the project and carry out discussions with the Government, espe-cially the Direccion de Aeronautica Civil (DAC). The assistance providedto the mission by the Government is gratefully acknowledged.

The memorandum is based on the attached PCR, discussions withGovernment officials and Bank staff, review of project files and the min-utes of the Board of Executive Directors' meeting which considered theproject. The draft audit was sent to the Government for comments in thenormal course; however, no comments were received.

On the basis described above, the audit accepts the principalconclusions of the PCR. However, it expands on the reasons for the costoverrun and delays in project execution, the need for improved managementof DAC, the experience in project supervision by the Bank and on the PCR'sre-estimated economic rate of return.

- iWi -

PROJECT PERFORM}ANCE AUDIT BASIC DATA SHEET

PANAMA - TQCUMEN INTERNATIONAL AIRPORT PROJECT(LOAN 783-PAN)

KEY PROJECT DATA

Original Actual or

Item Plan Current Estimate

Total Project Coat (US$ Million) 34.8 77.0

Overrun (X) - 121

Loan Amount (US$ Million) - 20.0

Disbursed ) - 17.34

Cancelled )- 0Repaid as of 1/31/79 - 2.67

Outstanding ) - 20.38B

Date Physical Componenta Completed 6/75 6/78

Proportion Completed by Above Date (Z) 36/2 100

Proportion of Time Overrun (%) - 78

Economic Rate of Return (X) 18-20 13-14

Financial Performance - good

Institutional Performance _ less than satisfactory

Cumulative Estimated and Actual Disbursements(USS Million)

FY72 FY73 Fy74 FY75 FY76 FY77 FY78

(i) Estimated 2.5 8.4 15.8 20.0 20.0 20.0 20.0

(ii) Actual 1.1 1.1 3.6 7.2 13.9 18.8 20.0

% of (ii) to Ci) 44.0 13.1 22.8 36.0 69.5 94.0 100.0

OTHER PROJECT DATA

Original Actual or

Item Plan Current Estimate

First Mention in Files - 02/24/69

Government's Application - 05/28/69

Negotiations - 06/ /71

Board Approval - 07/27/71

Loan Agreement - 08/02/71

Effectiveness 11/01/71 01/18/72

Closing Date 10/31/75 03/31/78

Borrower Direccion de Aeronautica Civil (OAC)

Executing Agency Direccion de Aeronautica Civil (DAC)

Fiscal Year of Borrower Calendar Year

Follow-on Project Name None Scheduled

MISSION DATA

Month/ No. of No. of Date of

Item Year Days Persons Man-days Report

Identifica-ion 3/70 3 1 3 03/12/70

Preparation 6/70 2 3 6 07/08/70

Preappraisal 8/70 4 1 4 08/10/70

Appraisal 9/70 24 4 96 07/13/71

Supervision I 9/71 3 1 3 09/14/71

Supervision II 1/72 3 2 6 01/28/72

Supervision III 4/72 2 1 2 04/17/72

Supervision IV 6/72 8 1 8 06/16/72

Supervision V 10/72 5 2 10 10/04/72

Supervision VI 11/72 4 1 4 11/17/72

Supervision VII 1/73 5 1 5 02/16/73

Supervision VIII 4/73 3 1 3 05/09/73

Supervision IX 7/73 5 2 10 08/06/73

Supervision X 11/73 4 1 4 12/18/73

Supervision XI 1/74 5 1 5 01/24/74

Supervision XII 5/74 5 1 5 06/28/74

Supervision XIII 5/75 5 1 5 07/07/75

Supervision XIV 1/76 5 3 15 02/11/76

Supervision XV 9/76 2 1 2 09/22/76

Supervision XVI 1/77 3 3 9 02/09/77

Supervision XVII 11/77 2 2 6 12/07/77

COUNTRY EXCHANGE RATES

Name of Currency (Abbreviation) Balboa (B)

Appraisal Year Average (1970 Exchange Rate: US01 28 1

Intervening Years Average USl ==B 1

Completion Year Average (1978) US$l - B 1

/1 Includes US$3.04 million for exchange adjustment.TJ Actual accomplishment estimated based on loan disbursement.

- iv -

PROJECT PERFORMANCE AUDIT REPORT

PANAMA - TOCUMEN INTERNATIONAL AIRPORT PROJECT(LOAN 783-PAN)

Highlights

The Panama Tocumen International Airport Project helped

finance the construction of an air terminal building and a runwayto accommodate the increasing volumes of jet aircraft operation(especially the wide-body jets) at the nation's main civil airport.The basic objective of the. project was to assure continued development ofPanama's national economy which is particularly sensitive to touristflows and variations in air traffic volumes. The project also included

consultants' services to the Government's civil aviation agency formanagement, accounting, data services, and planning.

The project was implemented with a three-year delay and 120%cost increase. The delay and cost increase were due to many changes inproject design which were introduced after the loan was made (para. 16).

These changes, in retrospect, represented considerable improvement on theoriginal project design (para. 28). The re-estimated economic rate ofreturn is in the range of 13%-14%, which is satisfactory although lowerthan the appraisal estimate of 18%-20%. Cost increase and some shortfallin traffic development over the appraisal projection explain the currentlower estimate (para. 23). The airport is expected to make financialprofits beginning in 1980 and, by 1985, the return on net assets isprojected at 9.6% (para. 24).

The following points may be of particular interest:

- the planned closure of the downtown airfield atPaitilla, and moving its general aviation opera-tion to Tocumen, may require reconsideration(para. 15);

- poor timing and excessively sophisticated approachcontributed to lack of success in the managementconsultants' work (para. 19);

- training needs for management improvement(paras 36-37);

- need for a covenant limiting non-project invest-ments (para. 21) and for better designed financialcovenants (para. 24 and PCR, para. 5.14);

- lack of coordinated action on charges in differentairports and the resulting cross-subsidization(para. 25);

- inadequate project supervision (paras 31-34);

- complementary measures and investments neces-sary to realize the full benefits of the invest-ment in the airport (paras 40-44).

PROJECT PERFORMANCE AUDIT MEMORANDUM

PANAMA - TOCUMEN INTERNATIONAL AIRPORT PROJECT

(LOAN 783-PAN)

I. Background

1. In the mid-1960s, it had become clear that the principal air-port for Panama, located at Tocumen about 25 km outside the capital city,was inadequate for the growing needs for international air traffic ofthe country. The site, acquired by the Government in 1946, was in agood location for civil air operations, but the terminal facilities hadbecome outmoded and cramped, having been extended in stages since theoriginal terminal building was erected in 1953. The runways and taxiwayswere also becoming in serious need of repair following patching and ex-tension over 20 years.

2. In a period of increasing volumes of jet aircraft operation(especially the wide-body jets), with mounting congestion in the terminalbuilding and with an economy sensitive to the variations of internationaltraffic volumes, of which over 70%1/ arrived by air, the Government thoughtit necessary to undertake an extensive development of the airport. Thus,the US firm of Parsons, Inc. was retained as consultants in the late 1960sto carry out feasibility studies, including assessment of the availableoptions.

3. At this time, a reorganization of the civil aviation responsi-bilities within the Government took place, and an autonomous body - theDireccion de Aeronautica Civil (DAC) - was created in January 1969.

4. A Master Plan for the airport prepared by the consultants wassubmitted in December 1969 to this body and, following discussions withthe Bank which had been requested by DAC to consider financing the proj-ect, further studies were undertaken by the consultants to explore morefully certain technical features and the economic justification for theproject. These studies, which included investigations of time saving,the value of time and cost-benefit analysis, were completed by the con-sultants in October 1970.

5. The consultants' recommendations, as put forward in the MasterPlan, and supported by the extended studies, were generally acceptedby the Bank's appraisal mission which visited Panama in September/October1970. However, some changes in specifications were made during appraisaland the project cost was increased by 27% over the consultants' originalestimate, to US$34.8 million, including a contingency allowance of US$7million.

6. The immediate objective of the project was to improve and ex-pand the country's main international transport hub to cope with thegrowing traffic volume. The growth of air passenger movements, which

1/ 73% in 1978.

- 2 -

had in recent years reached an annual rate of 10%, would, in the absenceof the project, further aggravate the then unsatisfactory conditions of theairport operations. To the airlines, the facilities at Tocumen were inurgent need of improvement. A longer runway and approach aids includingInstrumental Landing System (ILS) and lighting, no less than the passengerand baggage handling facilities, were required if business was not to belost to Bogota, Caracas, Guatemala, and/or Mexico City where air traffichad been growing far more rapidly at that time.

7. The more basic objective of the project was to assure continueddevelopment of the national economy. Thus, the project was considered asan investment providing local employment on an increasing scale over awide spectrum as air traffic developed, also offering industry improvedair freight facilities and, perhaps most important of all, throughbusiness and tourist developments spreading social and economic benefitsthroughout Panama.

8. The project was presented to the Board in July 1971 with a re-commendation for a 20-year loan of US$20 million (57% of the estimatedtotal project cost), with a grace period of 4 years, to DAC with the gua-rantee of the Government of Panama.

II. The Project

Description - the Plan and the Actual

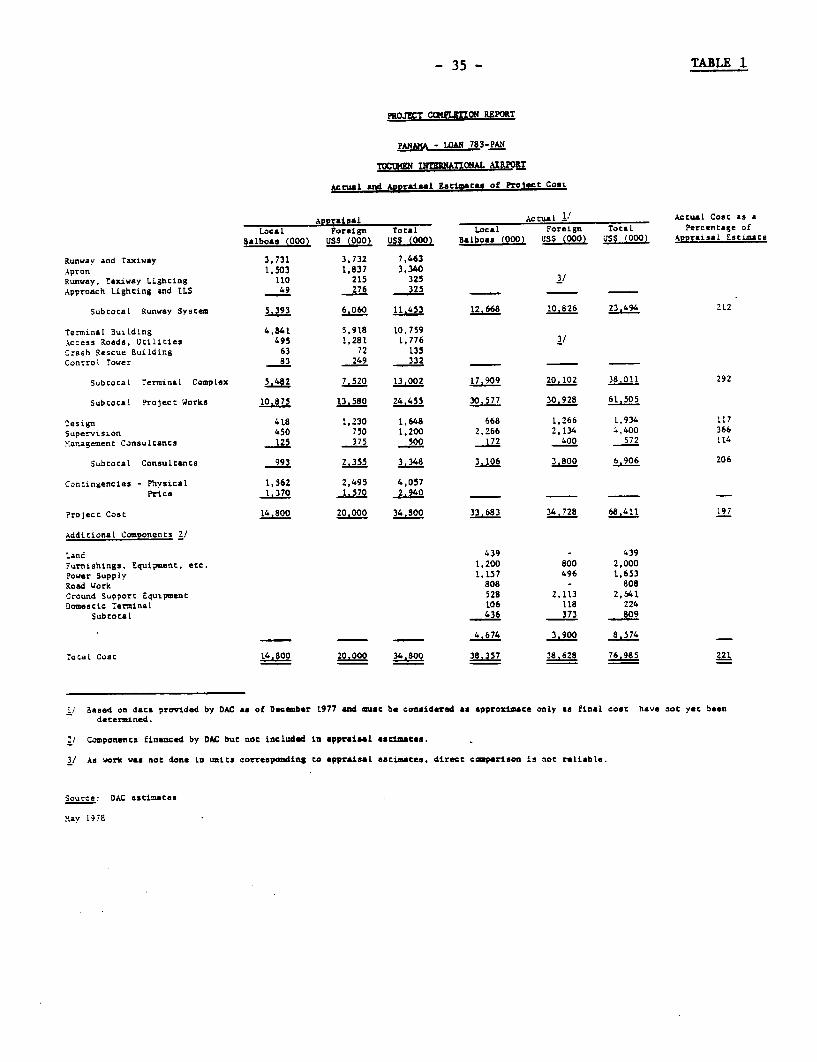

9. The project included construction of a new terminal buildingand a new parallel runway on land adjacent to the existing facility soas to provide a combined twin parallel but staggered runway and taxiwaysystem, with a centralized passenger terminal designed to handle thelevels of international and domestic air traffic forecast for 1980. Asappraised by the Bank, the project consisted of (see PCR, Table 1 forcost estimates):

(a) a new international passenger terminal withcontrol tower: 22,000 sq meter overall floorarea;

(b) a new parallel (3,350 meter) runway (03R-21L);

(c) a parallel taxiway for the new runway;

(d) approach aids including ILS with localizer andglide slope transmitter;

(e) high intensity approach and runway/taxiway lighting;

(f) ancillary buildings (fire and rescue, meteorology)and equipment; and

(g) provision of consultants' services to DAC formanagement, accounting, data services, andplanning.

- 3 -

10. A striking feature of the design of the new terminal building wasthe passenger-aircraft interface at satellite terminals, two being ini-tially required, allowing passenger access by air bridge to five aircraftof Boeing 727/707 capacity (or a mix including the largest wide-body jets)from each satellite. Two more satellites can be added as required byfuture growth of air traffic. With modifications during execution,the project furnished a 3-floor terminal with over 38,000 sq meters,which has considerably improved the layout, and extended the spaceavailable. At a later stage of the design work, the control tower,which had been conceived by the consultants, in line with the currentpractice, as a separate structure, was incorporated, following instruc-tions from the DAC, into the body of the terminal building.

11. A major decision in project design was the construction ofa new runway, rather than improvement of the existing one, which re-sulted in the efficient handling of aircraft traffic, at present usingboth runways, landing towards the terminal and taking off away from theterminal to save taxi time and cost, this being possible in all windconditions because of the central terminal location. A high intensity(HI) lighting system for approach and landing in the ILS(03) directionon the new runway, with runway and taxiway lights, was installed.

12. The building of bridges and a channel to divert the TocumenRiver was constructed as part of the Master Plan. A new fuel farm wasalso established with underground pipe delivery to apron hydrants. Thiswas financed and is now owned by the airlines, but will revert to DAC in20 years time. Separate buildings were provided for fire and rescue ve-hicles, equipment and men.

13. At present, the old terminal area is in use as a cargo and main-tenance base. As was foreseen by. the consultants, this area is the mostsuitable for air cargo. Investment was, however, excluded from the proj-ect until a later stage. While DAC had hoped that the airlines wouldprovide the finance necessary for new cargo terminal investment, this isnot yet forthcoming. Thus, an uncertain situation exists at present, andDAC seeks funds for a cargo scheme which is compatible with their new pas-senger facility.

14. The new airport was to be linked to an improved highway toPanama City, as part of the Pan-American Highway. This was to be doneoutside the project and was, in the event, completed before the airportitself. Access was to have been achieved also from the opposite side ofthe airfield by improvement to an existing road. This was to be anintegral part of the project and would have tunnelled under the maintaxiway between the new and the existing air terminals. This latterscheme was frustrated by the water level (water table) which raisedproblems of engineering and cost in tunnel drainage. Thus, an existingperipheral road was improved in lieu of a tunnel.

15. It was projected by the Bank's appraisal mission that the opera-tion of light transport and general aviation traffic would be moved fromthe downtown airfield at Paitilla to the vacated old terminal and runwayat Tocumen. Indeed, the Loan Agreement (Section 4.04) required the

- 4 -

Borrower to close the Paitilla field one year after the completion of

the project. Revenue from land sales on this airfield was one factor in

the economic justification for the Tocumen project. Even though Paitilla

does not meet an adequate level of operating safety in all flying condi-

tions because of adjacent high-rise buildings, the Government now is

reluctant to move general aviation away from this airfield. The question

whether or not the original agreement that the Paitilla field would be

closed was a correct course of action could not be adequately investi-

gated by the resources available to this audit, nor is it considered to

form part of the primary functions of this audit. It seems, however,

that the various aspects of the problems arising from this decision may

not have been fully considered at the time of appraisal. Therefore,

it seems desirable that the Regional Projects review this question afresh

with the Borrower.

Implementation

16. Considerable delays occurred in the implementation of this

project which was completed in October 1978, as compared to the original

target of July 1975. The cost of the project increased by more than 120%

from the appraisal estimate of US$34.8 million to US$77 million. A large

part of the cost increase was met by a US$25 million loan from the

Venezuelan Government, making it the largest outside source of financing

of the project. However, the Venezuelan Government did not participate

in project supervision. In part, both the delays and cost increases were

due to the changes in the project design which have been noted above,

but the other factors, which became significant during project execution,

affected the time scale no less than the cost. There have been three

successive Directors General of Civil Aviation since 1969. The second

appointee (in office between 1972-78), who had an extensive experience in

major building projects, contributed to considerable improvement in the

project but this necessitated the increasing costs and delays. He took

exception to a number of major features in the plans, and conflicts arose

with the engineering consultants who had by then reached an advanced

stage of detailed design. The DAC required changes in the location of the

control tower, which involved considerable redesign of the terminal, and

expressed concern at the results of soil tests done by US and Panamanian

specialist consultants. This led to a change in engineering consultants,

in spite of efforts by Bank staff to avert this, and a consortium of a

Panamanian firm (Planos y Supervisiones Tecnicas (PISTSA)) and a major US

consulting firm (Greiner Engineering Services, Inc.) took over the

project, finalized design and supervised construction. Weather condi-

tions, inadequate equipment, poor labor planning, and local labor pro-

blems augmented these difficulties. The additional soil testing required

by DAC turned out to be very beneficial as without this, there would have

been a serious structural problem to the terminal building.

17. Not only were the delays and the introduction of a new consult-

ing team a source of cost increase in themselves, but further work was

called for such as soil tests, roads, runway grooving and terminal modi-

fications, and power supply; this inevitably increased costs. Moreover,

- 5 -

items not included in the original estimates of project costs had to

be provided for, some of which might reasonably have been foreseen (see

more details in para. 29). Such were ground support equipment, and

furnishings. Finally, inflation created a serious impact upon the level

of costs, with the price increase in Panama between 1971 and 1978 having

been 74%.

18. When inspected by the audit mission in January 1979, the

completed project is, with some exceptions, operating reasonably effec-

tively. Despite the delays and cost increases, the outcome is gen-

erally a successful project, approved of in most respects by airlines

and by the public (see the discussion on the overall concept of the

project in Annex I). A remarkably high standard of finish is noted in

the buildings and installed equipment both in the public and business

areas. As yet outstanding are the Instrument Landing System (ILS),

already installed but not accepted by the US Federal Aviation Adminis-

tration (FAA) which is the approval authority, and the cargo area, which

urgently awaits capital investment (para. 13).

19. While implementation of the physical project has been achieved

to a high specification, and some items were provided perhaps to a

standard above what is required,l/ other aspects of the project have not

been completed satisfactorily. The management consultant, who reported

early during the project, prepared manuals which appear to have been too

elaborate and sophisticated for DAC's immediate needs. Because of delay

in the project, the work was undertaken too soon to be useful to the

airport management and it was provided in a form which was unsuitable forthe small number of trained staff who were available at the time. To

help remedy this, a new management advisor is to be retained on a 2-year

assignment beginning in March 1979.

Covenants

20. No major problems arose over the loan covenants but there were

delays in fulfilling some of these obligations. The minimum cash genera-

tion requirement, the minimum rate of return on project completion, and

the overall debt limitation were not in the event applicable in a given

year because of the delay in the project. The dating would have been

better related to the actual completion time rather than the estimated

completion year (c.f., PCR, para. 5.11).

21. The provision of a National Aviation Plan for Panama has also

not yet been completed as required by the covenants. However, this has

been in preparation for some months with the help of an ICAO specialist

and is expected to be completed by July 1979. Pending preparation of this

plan, no limitation was placed upon other investments by DAC (PCR, para.

5.10); because of the absence of such a covenant, it was not possible to

closely monitor DAC's other investments, such as the extension and improve-

ment of the Paitilla field, which another loan covenant (Section 4.04)

specified to be closed (c.f., para. 15).

1/ Such as the electronic and electrical systems which DAC does not

have personnel to maintain, and the furnishings on the terminal.n- 1u#-F- *.nQ nnt financed bv the loan.

-6-

Disbursements

22. The Key Data Sheet includes information on the disbursements

achieved in each year from 1971 to 1977. It will be noted that owing

to delay in the construction, only about 35% of this loan had been dis-

bursed by the original closing date and full disbursement was delayed

by two years.

Economic Return

23. At appraisal, the project was estimated to yield an economic

rate of return of 18%-20%. Some shortfall on the appraisal traffic

estimates occurred; the 1978 volume of passenger traffic, for example, is

86% of that forecast at appraisal. The lower traffic volume, together

with the increased cost, reduced the re-estimated economic rate of return

to 13%-14%. Some qualification to this re-estimate is made under Main

Points of Interest (paras 39-44).

Financial Conditions of DAC

24. Loan covenants include the undertaking by the Borrower that

it will take all necessary measures to achieve a financial rate of

return for DAC of at least 1.5% in 1976, increasing to 6.5% by 1980. The

year 1976 was taken, at appraisal, as the first year of operation of the

new airport. As mentioned above, this covenant was superseded by events.

Based on information provided by DAC, the audit estimates that the

positive return will first be reached in 1981, the third full year of

operation of the project airport, and it will increase to 6.6% in 1985

(see Annex II). However, the Tocumen Airport itself (viz., excluding

other airfields under DAC) will start to make profits in 1980 and by 1985

the return on net assets would be 9.6%. It would have been desirable

that, in addition to the financial covenants for DAC as a whole, separate

covenants for the Tocumen Airport only have been agreed so that the

project's financial results are not needlessly encumbered by the deficits

produced by DAC's other operations (c.f., PCR, para. 5.14).

25. The financial projection in the Appraisal Report was based

on the assumption that the various airport charges, including the passen-

ger exit tax, aircraft landing, and leasing charges, would be increased

by reasonable steps so as to raise the net revenues as required without

restraining demand. This action has already been taken. However,

charges at other airports under DAC have not been increased with the

result that they are presently producing larger financial deficits, and

the Tocumen Airport, in effect, will cross-subsidize these other air-

fields in Panama from 1980 on.

26. The airlines accepted increases in landing and other charges,

which in some cases were steep, because of the marked improvement in the

facilities. Some criticism of the lack of option to the airlines to use

all the services provided is heard, however. A US$8 passenger exit tax

is now in force and this is expected to rise to US$10 in 1980. These

-7 -

taxes are high but not exceptional. The same is true for ground rents

for concessions which reach US$500 per sq meter per annum for the duty

free shops; the fact that there is a waiting list of potential leasees

appears to be an indication that the expected commercial profits justify

the levels of rents. A schedule of increments has been planned for other

airport services at Tocumen.

III. Main Points of Interest

Cost Increases and Delay in Completion

27. The audit is in broad agreement with the PCR as to the causes

of delay and of the allocation of the increases in cost which arose. The

effect of inflation has been fairly assessed in the PCR (para. 3.20), and

it is clear that about US$9.5 million is the cost of the residual work

and equipment at inflated prices, which should have been identified in

the Master Planning or appraisal stage (para. 17).

28. It appears that the appraisal considerably underestimated the

cost, especially for the terminal and may have failed to take fully into

account some of the potential problems of execution, such as the power

and water supplies, and communication facilities which were assumed to

be provided by others, but in the end DAC had to provide them by itself.

29. Much of the cost increases therefore is something that could

have been either anticipated or measures taken to minimize them during

the project appraisal and execution. They could be grouped into three

categories:

1. Omissions in the Master Plan or appraisal stage.

Examples are: fencing and passenger handling equip-

ment omitted by the consultants.

2. Unforeseen work found to be mandatory as the proj-ect proceeded. Examples are: power supplies, land

surveys, and additional road work not initially

foreseen to be required on the scale found necessary.

3. Underestimation in the planning stage. The founda-

tion and erection of the terminal and, to some ex-

tent, runway/taxiway as well as furnishings and equip-

ment of the terminal were seriously underestimated.

30. Execution delays arose from the causes which have also been

well spelt out in the PCR. Such were changes in leadership in DAC,

uneven performance of consultancy services by the original design team,

and conflicts in the views taken of significant features in the basic

design and of the engineering works between DAC and the original consul-

tants, leading to the decision to change consultants (para. 16). It is

clear that other factors, including the labor problems and shortage of

the equipment of earth moving contractors, and misjudgment of supplies

provision to avoid seasonal bad weather, aggravated the problems.

-8-

Project Supervision

31. The supervision of this project was put under considerable

strain because of the numerous problems described above and because

of the lack of experience on the part of the newly established DAC,

especially with a project of this magnitude. The problem was com-

pounded by the Borrower's lack of confidence in his consultants; ra-

ther than working with his consultant to solve terminal design problems,

he frequently turned to the Bank for advice.

32. The Bank's supervision efforts to expedite the design revision

(paras 16 and 17) did not appear to have been fully effective. The re-

vision began in the second half of 1972 but was not completed much be-

fore the end of 1975. During this three-year period, eight supervision

visits took place but they were all brief visits - 3 to 5 days - during

which it would have been difficult to deal with the details of the en-

gineering problems as well as other usual supervision tasks.

33. There are several other unsatisfactory features of supervision

missions. All these visits during the three-year period were one-man

missions, with one exception in which a Young Professional joined.

Four different individuals carried out these eight missions, although

five have been done by one individual. This staff member, who was the

project engineer but belonged to the Bank's Central Projects Staff and

not the Regional Projects, could not carry out field supervision between

July 1973 and May 1974 during which period two supervision missions were

carried out by two different non-aviation engineers. Most of the super-

vision missions were carried out during trips which included visits to

one or more other projects in Panama or other Latin American countries,

some of them within a week's time. Between October 1972 and January

1976, no financial analyst joined supervision missions, while financial

review and the check on the progress of the accounting consultants' work

should have been an important part of supervision. There was only one

supervision mission in which an aviation economist participated, while

the preparation of a National Aviation Plan, which is a loan condition,

should have been closely supervised.

34. The impression that one gains from the above is that much of

the supervision efforts represented reactions to "crises" in the field,

although it is to be recognized that these missions tried to make DAC

do proper programming and planning of project workflow. A number of

visits made by DAC staff to Washington was also generally for resolving

urgent engineering problems, rather than consultation on overall project

implementation. The fact that little or no supervision inputs were made

by financial analysts or economists appears to suggest that these fairly

frequent supervision missions did not adequately cover the entire range

of problems which arose during the execution of the project. Indeed,

many of the non-engineering aspects, e.g., financial conditions of DAC or

preparation of the National Aviation Plan, of the discussions in super-

vision reports were generally less informative than they should have been.

- 9 -

Some opportunities for the Bank to learn useful lessons from its first

major airport project therefore appeared to have been lost due to the

inability to carry out well planned and more comprehensive supervision.

35. The new Director General felt that the Bank's supervision of

the project could have been more systematic and comprehensive. At the

same time, however, gratitude was expressed by him and other DAC officers

for the assistance given by Bank staff in the various stages of supervision.

Need for Improved Management

36. The change in the leadership of the DAC during the execution of

the project not only increased the problems in implementing the project

but also adversely affected sound and continuous institutional develop-

ment of DAC. The supervision reports during 1975-1977 pointed out

the need for management planning and efforts were made by the Regional

Projects staff to encourage the DAC to engage in the training of its

staff in management and in key engineering areas, but DAC's effortsappear to have been made more toward solving problems arising in the

construction part of the project. DAC management now recognizes these

institutional problems, but action is yet to be taken.

37. The problem is to establish a firm structure of experience

at several levels. Critical also is the provision of trained engineers

for plant maintenance, and especially electro-mechanical technicians in

preparation for plant operation in a large and multi-faceted project.

Again in this area, a first-class advisor is required, followed rapidly

by the establishment of a training program. One of the conditionsfor achieving this is the establishment of a realistic pay scale in

the Government's civil aeronautics service, since the best men can getwork in private industry. As a partial attempt to deal with this pro-

blem, the Chief of the Plant Maintenance Engineering has been engaged, on

a temporary basis, on loan from private industry.

38. The physical investment alone in the airport cannot be expected

to assure the benefits envisaged from it, unless airport management is

improved as planned. The recently appointed Director General is very

much aware of this problem and is convinced of the need for a competent

professional management backed up by plant operators and technicians in

DAC. This is shown by his successful negotiation with ICAO recently forthe appointment of a suitably qualified airport management advisor for

two years (para. 19). But much more than this needs to be done.

Qualifications to the Re-estimated Economic Return

39. The re-estimated return of 13% to 14%, as shown in the PCR, was

calculated on the assumption that the flow of annual project benefits

would be realized throughout the life of the project. Also, the estima-

tion supposes, although not specifically mentioned, that other investments

necessary to accommodate international visitors to Panama, such as hotels,

would be made.

- 10 -

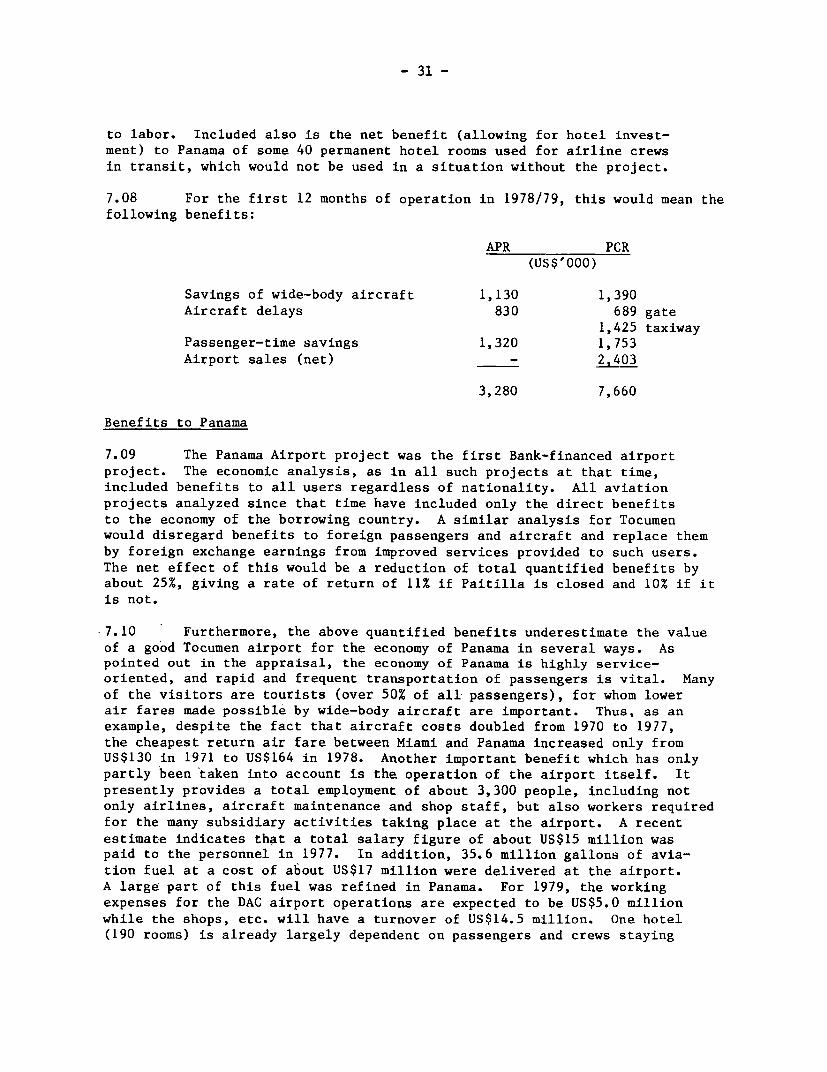

40. As of now, the benefits of the project are not fully realizedbecause, although the facilities to handle traffic efficiently are nowin place, there has been insufficient expediting of the passenger trafficflow within the new terminal due to the fact that no steps have beentaken to improve the immigration and customs procedures. For example,arriving passengers are required to wait for anything up to 45 minutes atpassport control. This is an unacceptable feature of any airport in thejet era, and especially so for an airport in which a large investment wasmade for the very purpose of facilitating the traffic flow. The esti-mates of benefits given in the PCR (para. 7.08) are not being achievedfully during the first year of operation; in the medium term (say1985), however, they are achievable if measures are taken to eliminatedelays at those Government check points, thereby fully realizing theadvantages of the new facilities.

41. The real challenge to realizing a maximum benefit of the projectis the drive to maintain the projected rate of growth of the air trafficat Tocumen over future years. This audit identified some of the key areaswhich should be probed further, and where assistance would now be welcomedby DAC and by other Government agencies so that this essential air trafficgrowth both in passengers and cargo can be maintained through the 1980s.

42. The success of the project depends upon the growth of interna-tional traffic, and two aspects of this are most significant. Firstly,the promotion and provision of facilities for business and recreationalactivities and, secondly, investments in hotels. While the Ministry ofPlanning and Political Economy, and even more so the Government's TouristBureau, are well aware of those factors and two hotels are currentlybeing built, the present scale of activity and investments may not beadequate to maintain the growth required.

43. Forecasts of a 6.5% p.a. growth rate, which reflects currenttrends in international (non-resident) arrivals in Panama, indicate anexpected 605,000 international visitors in 1990. This represents morethan doubling of the number which arrived in 1978, requiring a consider-able increase in hotel capacity. Panama has the advantage of a relativelyuniform international air traffic throughout the year, the peak month ofDecember generating only 29% above the average month. Even so, over5,500 additional hotel beds are estimated to be required over this timescale, and present building plans reach no more than 12%-15% of thatfigure. The increasing domestic demand within Panama is not includedin these figures. Hotel building therefore would have to be encouragedto retain tourists for a longer visit.

44. The maintenance of this rate of growth in international airpassenger traffic is dependent also upon other non-aviation investmentin convention centers, tourist attractions, and surface transport facil-ities, and forward planning for these is necessary. Stepped-up touristpromotional activities are also necessary. On a Tourist Bureau promo-tional budget of US$912,000 in 1979, an adequate level of overseas

- 11 -

publicity for Panama may not be possible. Inquiries indicate thatequivalent expenditures in Singapore and Hong Kong are US$7.45 million

and US$6.06 million, respectively, in the current year.

IV. Conclusions

45. While the project experienced considerable delays and cost

increases, overall, the project has been carried out successfully.

One of the causes of the delays and cost increases was the important

modifications introduced to the terminal building design when the design

work was virtually completed and also the need to carry out more thorough

soil tests which were inadequately done preceding Bank appraisal. Many

of the modifications to the terminal design generally resulted in an

improvement of the layout. There were also certain items which were found

to be required and therefore added to the project, but had not beenidentified during appraisal. The idea envisaged at appraisal that all

international traffic movement would be handled by the new runway built

under the project, reserving the old runway for general aviation, did not

turn out to be a realistic one; today, both runways are used by inter-

national traffic with the result that the aircraft movements are made

more efficient and economical. In light of this, the question of moving

general aviation to Tocumen and closing down the Paitilla airfield

appears to warrant a careful review.

46. Some of the benefits of the project are not yet fully realizedbecause the Government still needs to further streamline its immigration

and customs procedure at the terminal.

47. The Bank's supervision of the project was not adequate.

Although frequent visits were made by the Bank staff, they were generallyof too short a duration for an adequate supervision and their emphasis

was on engineering matters, with relative neglect of management, finance

and economic matters. The impression is that the supervision took theform basically of an advisory service to the Borrower, which should havecome from his consultants in the first instance, and the main function

of supervision, i.e., the control of overall project execution, antici-

pating problems, helping to build up an institutional capability to oper-ate the airport, etc., did not receive sufficient attention.

48. The final product of the construction part of the project isan airport which is approved of in most respects by airlines and by the

public. The standard of workmanship is of a high order, and the equip-ment procured and the furnishings are of good quality. The challenge to

the DAC is to operate the facilities with high efficiency. For this, the

DAC and the Government appear to require outside assistance.

49. The audit identified four areas where assistance is required.These are: the development of a professional management and executive

structure, engineering training, especially for electro-mechanicalspecialists, development and financing of the air cargo base, and invest-ment in tourism facilities, particularly hotels. Such assistance is

- 12 -

essential to an efficient operation of the airport and therefore to themaintenance of air traffic growth upon which the viability of the project

and, for that matter, the economic growth of Panama importantly depend.

50. Some continued contact between the Borrower and the Bank's

Regional Projects staff for the next few years is desirable. This

may take the form of limited supervision of DAC operations, provided

that, in terms of priority, Bank manpower could be expended for such a

purpose. Since the completion of physical construction represents

achievement of only a part of the project objectives, the remainder being

the build-up of the institutional capability, in a case as this project

where there is no follow-up lending operation in the sector, the question

of a continued association with the Borrower until its operating capa-

bility is further improved appears to merit careful consideration.

- 13 - ANNEX IPage 1

PROJECT PERFORMANCE AUDIT MEMORANDUM

PANAMA - TOCUMEN INTERNATIONAL AIRPORT PROJECT(LOAN 783-PAN)

The Overall Concept of the New Tocumen Airport

This audit has concluded that the overall development conceptfor Tocumen Airport was sound. Given the need to expand and update facil-ities to meet a growing passenger, cargo and aircraft movement, the prin-cipal alternative option to the project as completed was the refurbishingand extension of the old terminal building and the rebuilding and length-ening of the existing runway. The old terminal (erected 1953) had reachedthe end of its useful life after several additions had been made over 25years. The old runway which had been cracking badly through poor drain-age had also an adverse slope of 0.9% towards the northern hills and of-fers take-off and landing restrictions in northerly wind conditions. Theselatter disadvantages naturally still exist on this runway.

While a convincing economic case was made in 1969 by the originalconsultants to build a new runway and terminal, it must be said that thecost overrun and delay would certainly have been less if the less ambiti-ous program of rebuilding had been chosen. The Appraisal Report detailed(in Annex 2) the features of each option and drew the conclusion that evenwith a conservative estimate of lost airport revenue, through the closingof the original runway for lengthening and strengthening in stages, theconsultants' recommendation to build a new parallel runway and new terminalwas the correct one. It would be, however, a misconception to believe, asdid the appraisal, that air transport operations with large jet aircraftwill be confined to the new runway. Now that reconditioning of the oldrunway has also been completed, the airport is operated by the airlinesusing both runways, aircraft landing towards the terminal and taking offaway from the terminal to save taxi time and cost, this being possible, be-cause of the central terminal location, in all wind conditions. Exceptionsto this will only arise when long-haul jets take off at maximum weight.

A minor conflict arises as aircraft taxi across the old roadway,on a short length of combined taxiway and road which is therefore sharedwith other airport vehicles,

There is now little doubt that the most suitable use for the oldapron is for cargo and maintenance services, replacing later the old ter-minal which would be costly to refurbish. Plans are in preparation to im-plement a scheme for this cargo area when finance is available,

The nature of the site and the constraints on location of thenew runway dictated that the layout of the main terminal should be oflinear type. This was certainly a correct decision, although it neces-sitated some restriction on the number of airline "check-in" desks. (A

- 14 - ANNEX IPage 2

limitation to the number of airline desks is already apparent in the inter-national terminal, and sharing by airlines will become necessary within afew years.) For the future, the layout of the terminal allows furtherlinear extension. More satellites can also be added when demand justifiesit. In brief, the design concept allows adequate flexibility.

- 15 - ANNEX II

PROJECT PERFORMANCE AUDIT MEMORANDUM

PANAMA - TOCUMEN INTERNATIONAL AIRPORT PROJECT(LOAN 783-PAN)

Direccion de Aeronautica Civil

Anticipated Return on Net Operating Assets (1979-1985)

1979 1981 1983 1985(US$ Millions)

NET OPERATING ASSETS

Tocumen Airport 76.98 68-.77 60.36 52.21

Other Airports 5.99 5.03 4.06 3.07

DAC Total 82.97 73.80 64.42 55.28

US$ Thousands

NET RETURN ON OPERATIONS

Tocumen Airport -261.1 1,778.8 3,579.5 5,030.4

Other Airports -1,256.7 -1,301.9 -1,267.9 -1,375.8

DAC Total -1,517.8 476.9 2,311.6 3,654.6

PERCENT RETURN (YEAR)

Tocumen Airport - 2.59- 5.93 9.63

DAC Total (All Airports) - 0.65- 3.59 6.61

1/ + 1.1% in 19802/ Loss in 1980

Source: Direccion de Aeronautica Civil

- 16 - ATTACHMENT

PANAMA

TOCUMEN INTERNATIONAL AIRPORT PROJECT (LOAN 783-PAN)

PROJECT COMPLETION REPORT

I. INTRODUCTION

1.01 In 1969 and 1970, there was strong pressure on Panama to improveits international airport facilities at Tocumen because of the economicimportance of its traditional role as a staging point between North and SouthAmerica. Thus, the leading objective of the project was to ensure that Panamawould be able to maintain this role in the face of the changes occurring inthe airline industry. The major features of the project were a new runway,taxiway and aircraft parking system, together with a new passenger terminalcomplex to provide improved service to a large and growing volume of passengerand cargo traffic and - in particular - the new, large, wide-body jets. TheGovernment attached a high priority to the project as a means of maintainingTocumen's position as an important international airport, stimulating tourismand economic diversification by capturing an increasing share of air passengerand cargo traffic and meeting the requirements of Panama's developing economy.The project was part of an airport master plan which provided for futureexpansion when required.

1.02 Because of the condition and geometry of the old runway, its rehabil-itation would have required substantial interruption to traffic and high cost.Therefore, it was decided to build a new runway to the east of, and parallelto, the existing runway, offset so that the south end of the existing runwaywas roughly in line with the north end of the new runway. The new terminalwas to be constructed between the two runways. The existing terminal building,the land adjacent to the existing terminal building and the land adjacent tothe existing runway were earmarked for air cargo and other operations. Theold runway was to be serviceable for light aircraft previously using Paitillawhile the new runway was to be used exclusively by large commercial transportaircraft.

1.03 The Borrower, Direccion de Aeronautica Civil (DAC), was a newlyestablished (1969) autonomous State agency with responsibility for handlingcivil aviation matters in Panama. Technical and financial management wereunderstandably weak; therefore, a program of technical and managementassistance was included as part of the project.

1.04 Previous Bank loans to the transportation sector in Panama hadbeen limited to two loans totaling US$13.1 million to help finance roadconstruction. Not only was this the first non-highways transportationproject in Panama but also it was the first airport project undertakenby the Bank.

II. PROJECT PREPARATION AND APPRAISAL

2.01 The project was proposed by Panama at a meeting in the Bank inFebruary 1969, at which time a loan application and prefeasibility studywere presented. Panama was then in the process of selecting a consultant tocarry out studies, and the Bank provided suggestions with respect to the termsof reference. Some 18 consultants responded to the Panamanian invitation,

and the Parsons Corporation of the USA was selected by Panama to carry out afeasibility study. This study was reviewed by the Bank in February 1970.

- 17 -

2.02 The Directorate of Civil Aeronautics (DAC) was created as an auton-

omous agency in January 1969, and its Director General, Major Patricio Janson,

acted as the guiding force in the early stages of the project, although the

formal contacts with the Bank were through the Director General of the

National Planning Department.

2.03 Since this was the Bank's first airport project, there was consider-

able interest in the various issues associated with it and a need to discuss

the project in detail. As a result of suggestions from the Bank at a meeting

with DAC and the consultants in July 1970, necessary revisions were made to

the feasibility and master plan study. The appraisal mission visited Panama

in September 1970 and found that additional data were required. These addi-

tional data were not provided by Parsons until May 1971. Parsons' report

provided preliminary design calculations and was the basis for final design

and the preparation of working drawings under an engineering services contract

with DAC. This, together with some revised cost data provided at the end of

May, led to completion of the appraisal. It was appreciated that the cost data

were based on preliminary engineering only, and consideration was given to

seeking an independent cost study or waiting until final design was completed.

Since a delay of up to one year could have resulted, a decision was taken by

the Bank to proceed with the project on the basis of the available data.

2.04 This decision, in retrospect, was understandable in the light of the

available information. The studies carried out were comprehensive: a number

of alternatives were considered and, in the time available, a great deal of

ground was covered. In particular, the Bank dealt with the financial and

economic aspects carefully since the consultant was not familiar with the

scope and depth of analysis required.

2.05 It must be remembered that, in 1970 and 1971, air transport was

in a period of very rapid growth, with newer and larger jet aircraft soon to

be introduced. There was, therefore, great pressure on Panama to improve its

airport facilities in order to retain its traditional position as a bridge

between North and South America and to profit from the opportunities provided

by the newer aircraft in terms of lower costs and increased capacity. The

timing and scope of the project were therefore appropriate for meeting Panama's

needs.

2.06 Two factors were recognized at the time of appraisal: first, that

DAC was a new and relatively inexperienced organization and, second, that care

would have to be exercised in controlling the project. A third factor, which

could not be recognized, was that construction costs would increase very

rapidly after the 1973 oil crisis. Even though the main thrusts of the

project covenants were to promote sound management practices in DAC and to

require good project control through the retention of suitable consultants to

design and supervise the project, costs increased rapidly. The results, in a

sense, were to be expected. For a small, inexperienced group to be faced with

a project of the size and complexity of Tocumen during a time of rapidly

rising costs meant that their slender resources were overwhelmed in the early

years of project execution.

- 18 -

III. PROJECT IMPLEMENTATION AND COST

Implementation

3.01 The implementation of this project was difficult, and a number of

factors contributed to the problem. A major point was the fact that the

design consultant proceeded with design fairly independently with the

enthusiastic support of the then Director General of DAC. The designs were

well advanced in the autumn of 1972, when a new Director General, an expe-

rienced engineer and contractor, was appointed. He and his advisers were

disturbed by some of the design features, particularly as they applied to site

conditions. The design consultants had assumed that they would supervise the

construction, but their relationship with DAC deteriorated to the point that

DAC refused to consider the firm for project supervision. As a result, there

were difficulties in coordinating the preparation and revision of the final

drawings. The new DAC staff and the newly appointed supervisory consultants,

who were unfamiliar with the design parameters, took over almost at the

tendering stage. The resolution of problems, e.g., organizing a plan of

action, checking and revising designs and generally coping with the startup

of construction, not only took time, but placed DAC in the position of having

to try to catch up with the job rather than being able to encounter problems

as they occurred and solve them before they became serious. DAC and the

consultants recovered ground, but it was a long, hard struggle. In addition,

DAC elected to carry out direct procurement of some equipment items (instead

of including these items in civil works contracts), which increased the

engineering coordination and administrative load. The net result was delay

in project execution with increased costs. The quality of the final work,

nevertheless, was very good. It is doubtful that, had DAC retained the

original consultants, the delays or costs would have been reduced materially

since the same problems plus the oil crisis inflation would have arisen.

Concerned that such a change might lead to delays, the Bank argued against

appointing new consultants until it was clear that no good working relation-

ship could be expected between DAC and the design firm. Although substantial

detailed design changes were made, the basic concept remained unchanged.

Procurement

3.02 Essentially, three types of procurement procedures were used:

international competitive bidding in accordance with Bank guidelines,

international competitive bidding on a negotiated basis (shopping) and direct

negotiation with a selected supplier. International competitive bidding was

used for the three major contracts, i.e., earthmoving, runway paving and the

terminal building. Competition was intense. In the case of the terminal

building, where the costs were far higher than the original estimates, the

final contract was the result of complex negotiation with the nominal low

bidder.

3.03 Most of the electronic, electrical and mechanical equipment was

procured by DAC using competitive bidding and direct negotiation. Since

this procurement did not meet the conditions of the Bank's guidelines,

- 19 -

none of these contracts were financed from the proceeds of the loan.

The value of this equipment was about US$8.0 million, and very good

quality material, of a type readily serviced in Panama, was obtained.

A number of other contracts were awarded to local firms by direct negotiation

for additional work such as airport fencing, improved drainage and the like.

DAC was also obliged to enter into unanticipated contracts with the utility

companies for power, water and telephone services. DAC preferred to let

individual contracts, where possible, to reduce costs but, in so doing,

increased the supervisory and coordinating workload.

3.04 Procurement procedures and results were, overall, satisfactory.

Tile, cement and cement products were the main products of domestic origin.

The work was executed by Panamanian tradesmen with only a few exceptions.

Project Schedule

3.05 The schedule for implementation adopted at the time of appraisal

envisaged invitations to bid being issued in September 1972. The major con-

tracts were expected to start in July 1973, and all works were estimated to

be complete by July 1975. The original plan was to have the earthmoving and

grading work started by December 1972 and sufficiently advanced by July

1973 to allow paving and terminal construction work to start at that time.

3.06 The actual start on the earthwork was April 1973, at the beginning

of the rainy season, and the paving contract was then scheduled to start in

August 1974. The paving contractor began producing base material in October

1974, but did not start his paving operation until April 1975. The work was

essentially completed by January 1977. The terminal building contract was

not awarded until May 1975 and was essentially completed in July 1978.

3.07 The delays in the paving operations were due to the earthmoving

contractor starting work at the beginning of the rainy season with inadequate

equipment. As a result, very little progress was made the first season. This

delay was compounded by the fact that there were long delays in the domestic

production of satisfactory concrete drainage pipe, which hampered drainage

work. A grade change to improve drainage had to be made, and DAC decided,

in addition, on the advice of the consultants, that surcharging a number of

areas on the runway was necessary. The time required for consolidation

of these areas was 12 to 18 months, which further delayed progress. The

actual paving operation was slow, but reasonably steady and of excellent

quality.

3.08 The terminal building and its related works were delayed, in the

first instance, by protracted reviews, redesign work and additional soil

borings to determine if any foundation problems existed because of geological

faults prevalent in the area. One of the satellite foundations had to be

redesigned as the result of the detection of an old water course with poor

bearing characteristics.

3.09 Foundation work started on the terminal in June 1975, and progress

was slow but steady. The scheduled date for contract completion was June

- 20 -

1977; because of revisions and the associated time required for decision-

making, however, it was anticipated that the work would not be completed

until November 1977. Unfortunately, labor slowdowns made progress very

difficult after the middle of 1977. There were few other jobs available

in Panama, and tradesmen, protected by the stringent Panamanian Labor

Laws, took every opportunity to extend the work as much as possible with

the result that the building was not completed until June 1978.

3.10 The major delay factors were design problems, the time required

for decision-making and labor problems. The original schedule did not allow

sufficient time even under normal conditions of good staff work, good design

and reasonable tradesman productivity.

Services of Consultants and Contractors

3.11 The first consultant (Parsons Corporation) engaged by DAC carried

out the feasibility study, the detailed engineering and the design, and

it expected to be engaged to carry out the supervision. The engineering and

architectural work was generally of high quality, but there were some defi-

ciencies, especially in the basic terminal building layout, the soils engineer-

ing and the earthmoving plan.

3.12 The consultants retained one of the most prestigious soil mechanics

consulting firms in the United States to carry out the basic investigations;

however, the actual field work was done by a Panamanian firm. No one really

controlled the Panamanian firm, but the soils consultants produced a report,

and the design consultants proceeded accordingly. A number of questions

were subsequently raised by Panamanian professionals to whom DAC had submitted

the soils report for comment. Another round of drilling was carried out,

and another report was issued by the soils consultants. DAC was not satisfied,

and further tests were made. Two critical points were at issue: first, there

was evidence of geologic fault lines crossing the proposed terminal building

location, which, in an earthquake zone, could be serious; and, second, the

runway was to be established in a swampy area of soft marine clays where

settlement was a potential problem. DAC elected to take a conservative

approach, which caused delay and increased costs; under the circumstances,

however, the decision was probably correct. Better results would have been

obtained if a well qualified firm had been solely and entirely responsible at

the outset for the soils investigation and had been charged with producing a

comprehensive testing program and analysis.

3.13 DAC's relations with the design consultants deteriorated to the

point that another group was selected to supervise construction and to redesign,

as required, the work of the original designer. This group, a consortium of a

Panamanian firm (Planos y Supervisiones Tecnicas, S.A. (PISTSA)), and a

large US consulting firm (Greiner Engineering Sciences, Inc.), took over

after the earthwork contract was awarded, and, consequently, they faced several

immediate problems that had to be resolved in the field. Again some delay was

inevitable; however, the consortium carried out its work conscientiously and

satisfactorily.

- 21 -

3.14 The terminal building design presented some problems, and theoriginal design consultant was requested to revise the design. This revisionwas done reluctantly and not too completely. DAC made a major decision toincorporate the control tower into the terminal, which caused additionalproblems and some basic design changes.

3.15 Since it was obvious that the cost of the terminal building wouldbe much higher than originally estimated, DAC sought to reduce costs by con-tracting design modifications in the package with the construction work. Thiswas negotiated with a consortium of a Panamanian firm and a U.S. design con-struction firm (Linbeck-LACA) which was awarded the contract and has carriedout the design modifications and construction of the building.

3.16 From the outset, Parsons had proposed that the work would be donein a series of contract packages with earthworks as a separate component.The major contract works were the runway, the taxiway and apron and theterminal building complex. The earthwork contractor (Energoprojekt fromYugoslavia) was responsible for general site preparation and grading. Hebegan work at the beginning of the rainy season with inadequate equipmentand personnel. The contractor had expected to use men and equipment fromthe Bayano Dam project. When this was not possible, it was necessary tosupplement his efforts by subcontracting with the paving contractor andanother Panamanian firm to provide equipment and trained operators. Thecontractor created most of his own problems, but there were extenuatingcircumstances, as explained in paragraph 3.07.

3.17 The paving contractor (ICC-Continental, a Panamanian-MexicanConsortium) was unable to start on schedule because of the slow progressof the earthwork. After initial startup problems, this contractor workedslowly but steadily and the results of his work were very good. e

3.18 The contractor for the terminal building complex (Linbeck-LACA)performed very well. Considering the major design revisions plus the usualchanges during construction due to various user decisions and the laborproblems, the work proceeded satisfactorily and the quality was good.

3.19 A contract was awarded to a management consulting firm (Arthur Young& Co.) to advise DAC on organization and administration. It produced andinstalled a sophisticated accounting and management control system that DAChas been unable and unwilling to use effectively. The system is more elaboratethan required at the moment, but, rather than scaling it down to actual needs,DAC had largely neglected it until recently. Further comments on this issueappear in paragraph 6.06.

Costs

3.20 The project costs overran the appraisal estimates by 121% asindicated in Table 1. The major factors that affected the costs were anunrealistic estimate for the cost of the terminal building at the time ofappraisal; design revisions for the earthwork, paving and terminal buildingcontracts; and additional works and compounded high inflation effects arisingfrom the delays in project execution. Based on information provided by DAC,

- 22 -

the final total cost of the project is estimated at US$77.0 million. Of this

sum, US$28.0 million is due to inflation, meaning that the cost in 1971 dollars

was US$49 million compared with US$32 million estimated in the appraisal

report. Of this difference of US$17 million, about US$5.0 million arose from

additional works not included at appraisal, US$2.5 million from additional

supervision and US$9.5 million from oversights in the cost estimates for project

items included at appraisal.

3.21 The original bid prices for the earthworks and the paving were

reasonable, but, because of oversight during design, the contracts did not

include work that had to be carried out subsequently, such as fencing the

airport, surcharging, additional drainage and grade changes on the runway and

in other areas of the airport.

3.22 In addition, in order to complete the project, DAC had to finance

works that were not contemplated at the time of appraisal, such as the con-

struction of a power line for the power authority, brought about by the power

company's decision not to relocate its main high voltage system and substation.

Additional work was done for the water and communications companies because

they were unable to finance the necessary works. DAC was also obliged to

finance, in part, a bypass road around the airport pending a major revision

of the connection to the Pan American highway at Tocumen village.

3.23 The cost of the terminal building complex was underestimated in the

first instance. As detailed engineering progressed, the cost estimates in-

creased. For example, the basic terminal complex was estimated at about US$10.0

million in 1971, US$10.6 million in 1972 and, in the consultants' final report

in 1974, US$20.7 million (including their design revisions); an independent

estimate at that time indicated that the cost would be closer to US$29.0 million.

In the interim, the terminal and apron facilities had been relocated and rotated

90 degrees, and, in 1972, both the terminal and runway locations were again

shifted. This led to more soil testing, increased costs and new engineering

problems that were fully resolved only during construction.

3.24 The appraisal estimate was based on a design engineering report

dated May 1971 which, in turn, was based on the master plan report presented in

December 1969 and on an addendum prepared in July 1970. The consultants'

final drawings for the paving were prepared in 1972, and those for the

terminal were prepared in 1974. Two points are apparent: the project had a

long gestation period, and significant design changes were made after appraisal.

The changes were beneficial, but it is unfortunate that they were not made

earlier to allow more detailed engineering and cost analysis. The appraisal

was carried out in 1971, two years prior to the oil crisis, while about 85% of

the work was carried out after the oil crisis, which led to unexpectedly high

inflation rates.

3.25 Ground support equipment was not included in the appraisal but

was installed by DAC. A hydrant refueling system, estimated to cost US$2.8

million, was installed by the airlines, and, while ownership will eventually

revert to DAC, it is not included in the costs.

- 23 -

Disbursement

3.26 Disbursement of the proceeds of the loan are as shown in Table 2.

It will be noted that, at the original closing date, only about 36% of the

loan was disbursed, and this reflected the general status of the project at

that time. The various delays that led to slow disbursement are discussed

under the project schedule part of this report.

IV. TRAFFIC AND OPERATING PERFORMANCE

4.01 Traffic projections at appraisal were made for each five-year period

until 1990. The main categories of forecast traffic were arriving and depart-

ing passengers on international flights, passengers in transit at the airport

on international flights, passengers on domestic flights and air cargo on

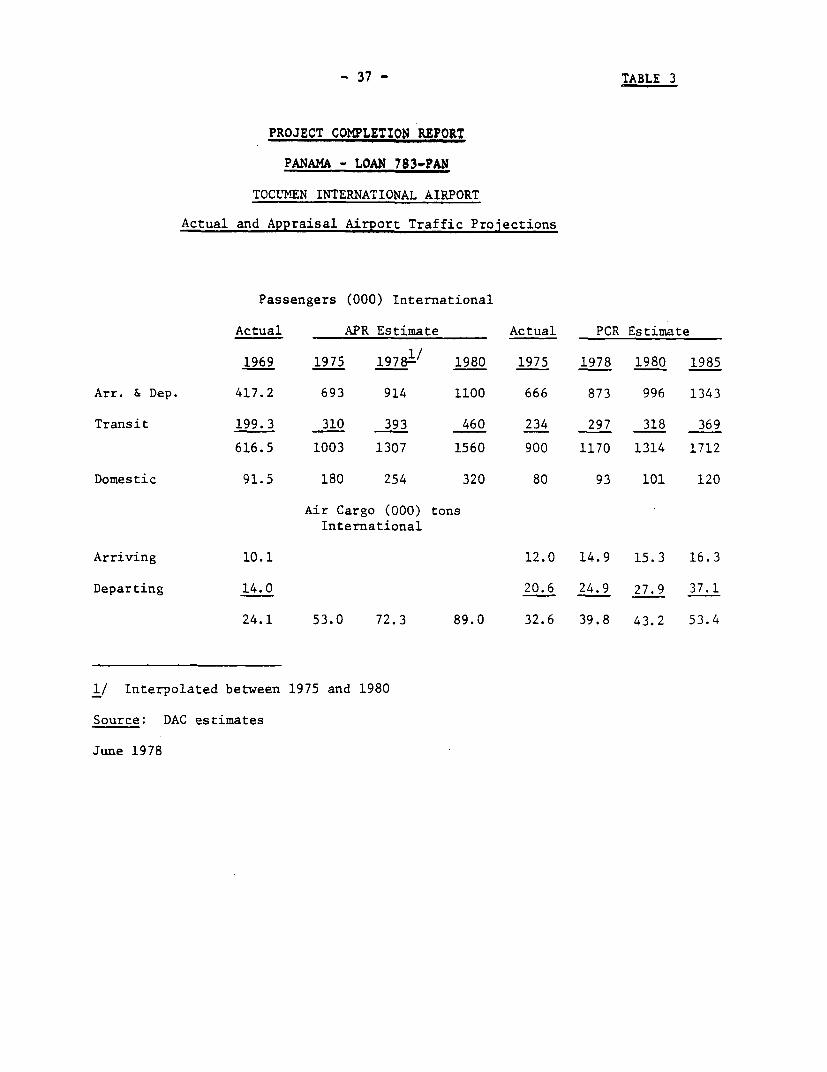

international and domestic flights. Table 3 summarizes the appraisal fore-

casts and relates these figures to actual data and the new projections. It can

be seen that expected traffic in 1978 based on traffic for 1975-1977 for the

most important category, arriving and departing passengers on international

flights, is only slightly less than that predicted in the original appraisal.

All other categories of traffic are significantly lower than expected for a

variety of reasons and particularly because of the delays of the project. The

most important consideration was the economic effect of the energy crisis,

which slowed down anticipated travel generally and air cargo growth in particular.

The fact that Paitilla, the domestic airport close to Panama City, still

operates has an effect on the traffic at Tocumen, as evidenced by the domestic

traffic figures shown in Table 3. The most important factor for Panama, how-

ever, is the very slow growth of transit traffic, which was partly caused by

the delay in the completion of the new airport investment. Despite this, a

limited transition to wide-body aircraft has already taken place and the

.proportion in 1978 (7.5%) is already almost as high as that expected for

1980. This proportion is expected to increase more rapidly as a result of

the new project. Air cargo is also expected to develop more rapidly when

former passenger aircraft loading positions can be used for cargo flights.

4.02 Day-to-day operating performance of the airport has been good

despite the delay in the project's implementation. Part of the reason for

this has been the lower than anticipated traffic volume (para 7.05). Never-

theless, for some of the relatively few large aircraft movements, long

delays for fully' 'loaded aircraft have been experienced, as anticipated at

the time of appraisal.

V. FINANCIAL PERFORMANCE OF THE BORROWER

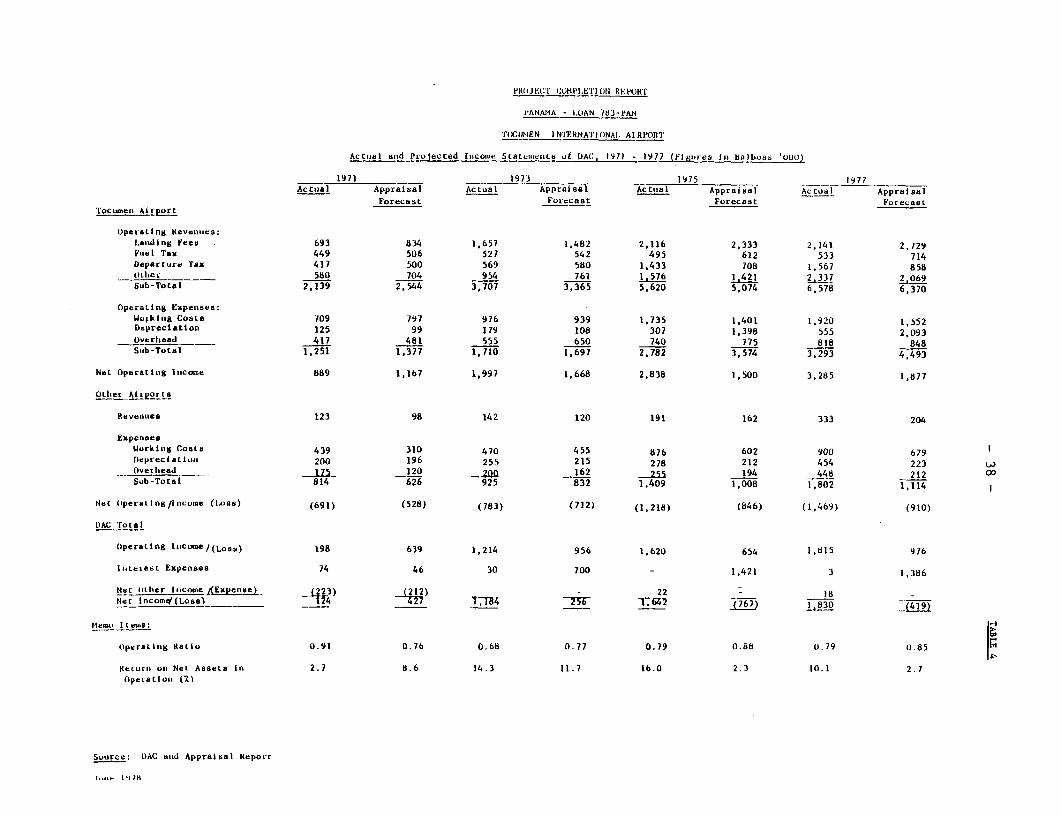

5.01 Table 4 shows that DAC's net operating income has generally

been higher than the levels forecast at appraisal and increased from 200

thousand Balboas in 1971 to 1.8 million Balboas in 1977 compared with

projected figures of 639 thousand in 1971 increasing to 976 thousand.

- 24 -

5.02 The net operating income has been higher than the appraisal pro-jections because of both higher-than-forecast revenues and lower-than-forecastexpenses (para 5.03). Total revenues increased from 2.3 million Balboas in1971 to 6.9 million Balboas in 1977, an average growth rate of 20%, comparedwith a forecast growth from 2.5 million Balboas in 1971 to 6.6 million Balboasin 1977, constituting a forecast growth rate of 17%. The reasons for thebetter-than-forecast income are:

(a) Departure fees derived from international passengers wereincreased from US$1 to US$3, then to US$5 instead of US$2 asprojected at the t:ime of appraisal. Thus, revenues from thesein 1977 were US$1,567,000 compared with US$858,000 forecast.

(b) Income received from rentals and concession fees has increasedmore rapidly than anticipated because of the great success ofthe duty-free shopping area available to both departing andin-transit passengers at,Tocumen Airport. Thus, revenues fromthese in 1977 were US$2,100,000 compared with US$1,665,000forecast at appraisal.

These factors more than offset the effect of traffic being at slightly less-than-forecast levels.

5.03 Operating costs have been lower than appraisal forecasts becauseof the later-than-forecast commencement of operations at the new airport andthe resulting lower depreciation provisions being charged. In that forecast,the new runway and terminal were scheduled to be operational during 1975;thus, depreciation of the project assets commenced in that year at a rateof about US$2 million per year. The delay in the project has meant thatthe project assets are stilL being treated as construction in progress and arenot being used. This reduction in depreciation more than offsets the increasein other operating costs over appraisal expectations. Cash operating expenseswere US$1.7 million in 1971, but increased to US$4.1 million in 1977 comparedwith US$3.3 million in the appraisal forecast. The difference principallyreflects the inflation experience of Panama in the intervening period. Itwas expected that salaries would increase by an average of 5% per year, butthe actual rate was about 10% per year. Total staff required has also beenslightly higher than anticipated. It was expected that about 600 peoplewould be employed by DAC once the new facilities were operational; however,the actual figure at the end of 1977 was 686, and some further staff areexpected to be added in order to operate the new facilities. The differencebetween the two figures arises principally from an increase in the number oflow level staff employed by DAC in the form of cleaners, attendants, etc. Thenumber of professional and management staff is, in fact, lower than wasforecast at appraisal and, to this extent, DAC has attempted to controlpersonnel costs. It does not appear that the higher figures for low levelstaff reflect underestimation at appraisal but that there may be some over-staffing in these instances.

5.04 Operating ratios were consistently lower than forecast throughoutthe period, and the return on assets can be seen to have been consistentlyhigher. Both of these differences reflect the non-inclusion of the projectassets in the asset base and depreciation provisions.

- 25 -

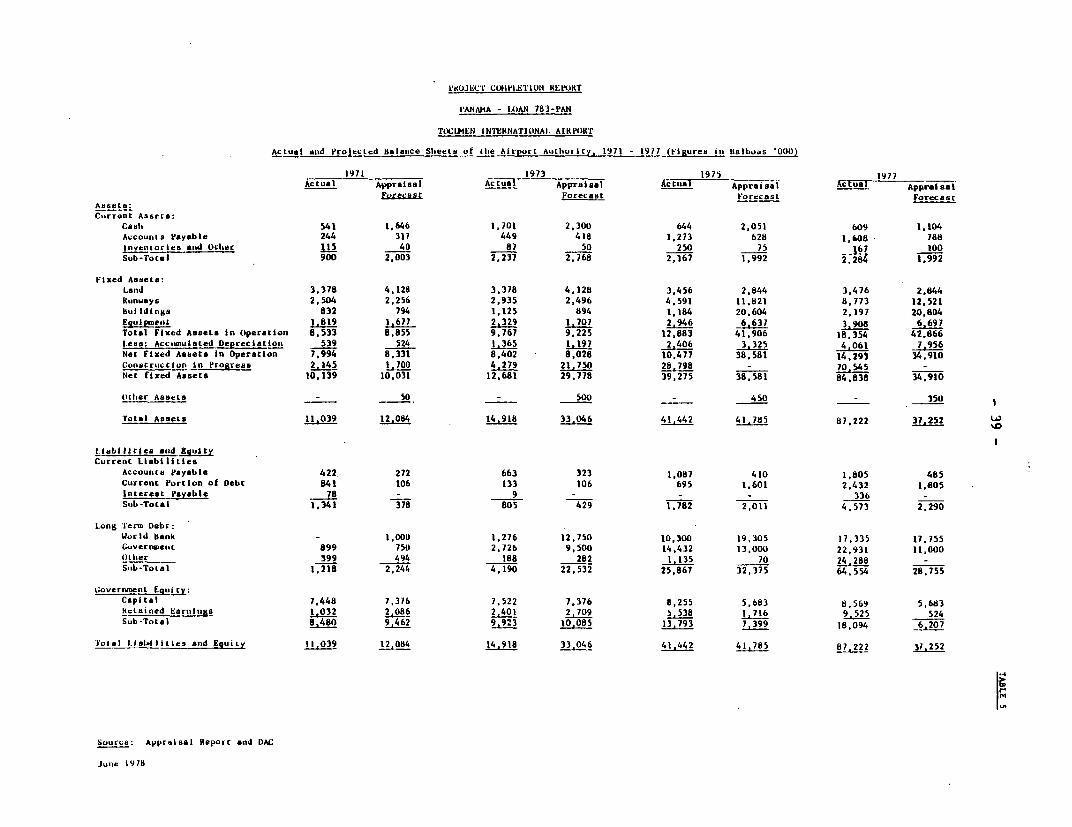

5.05 The Balance Sheet figures are shown in Table 5, which comparesthe actual figures for the period 1971-1977 with the appraisal projections.It can be seen that there was a substantial difference in total assets by1973, when forecast assets were-US$33-million and actual assets were US$15million. This difference represents the effect of delays in the project;work in progress was forecast to reach US$22 million by the end of 1973 butactually had reached only US$4 million. By 1975, total assets were roughlyequal to forecast assets of US$41.7 million. However, the bulk of the actualassets -- US$29 million -- was in work in progress rather than fixed assetsin operation as forecast.