World Bank Conference on New Technologies for SME Finance: Differentiating Markets for SME Finance...

21

World Bank Conference on New Technologies for SME Finance: Differentiating Markets for SME Finance December 4, 2002 Copyright © 2002 by Monitor Company Group, L.P. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means — electronic, mechanical, photocopying, recording, or otherwise — without the permission of Monitor Company Group, L.P. This document provides an outline of a presentation and is incomplete without the accompanying oral commentary and discussion. COMPANY CONFIDENTIAL Melbourne Amsterdam Athens Cambridge Chicago Frankfurt Hong Kong Istanbul Johannesburg London Los Angeles Madrid Manila Milan Moscow Mumbai Munich New York Paris San Francisco São Paulo Seoul Singapore Stockholm Tel Aviv Tokyo Toronto Zurich

-

Upload

stephen-matthews -

Category

Documents

-

view

224 -

download

1

Transcript of World Bank Conference on New Technologies for SME Finance: Differentiating Markets for SME Finance...

World Bank Conference on New Technologies for SME Finance:

Differentiating Markets for SME Finance

December 4, 2002

Copyright © 2002 by Monitor Company Group, L.P.

No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means — electronic, mechanical, photocopying, recording, or otherwise — without the permission of Monitor Company Group, L.P.

This document provides an outline of a presentation and is incomplete without the accompanying oral commentary and discussion.

COMPANY CONFIDENTIAL

Melbourne

Amsterdam Athens Cambridge Chicago Frankfurt Hong Kong Istanbul Johannesburg London

Los Angeles Madrid Manila Milan Moscow Mumbai Munich New York Paris

San Francisco São Paulo Seoul Singapore Stockholm Tel Aviv Tokyo Toronto Zurich

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 2

Decisions & ActionsDecisions & ActionsDecisions & ActionsDecisions & ActionsMarket ResearchMarket ResearchMarket ResearchMarket Research

Market Research Can Tell Us A Great Deal About Our Customers

Understanding Who, What, and Why Informs Key Decisions and Actions

Action Segmentation™ Customer Portrait®

Middle to upper income households Kitchen is important part of her home and her life

– Where she plays a large part of her role asprovider and caregiver for her family

– Entertaining often occurs in or includes the kitchen Remodeling to build her dream kitchen is a very

exciting project– Redoing the cabinets and countertops is the most

exciting part as they have the greatest impact onthe look / feel of the kitchen

– Not as excited about the new appliances Shops at several nearby stores

– Husband may go along to endorse selection– Each store has a reasonably wide selection of

brands and price ranges– Cabinet depth product is displayed alongside

regular product with no explanation of benefits tojustify price

– Dishwashers look quite similar across brands

Wants to build her dream kitchen in this house– This may be their home for a long time– Wants to feel good in her kitchen and have others

complement her More than someone who is replacing a broken unit, wants her

dishwasher to also look attractive and to complement orenhance the look of her kitchen

– Shouldn’t stick out in kitchen– Usually wants a more energy-efficient dishwasher than

she currently has– Her husband wants one that makes less noise– Price, within a broad range, is not a big factor

Must be able to physically see and touch it before buying it– Wants to imagine the dishwasher in her beautiful, new

kitchen Wants to feel she is getting a good deal on whatever she

selects (though all things considered, price is not thatimportant)

Dishwasher is an important part of theattractiveness of the kitchen

Has a sense of some brands being acceptableand others being too “cheap” and unreliable

– Believes that some brands are better atmaking some appliances than others

May have a view (based on prior experience)that a particular store will give her a better priceor will have more helpful staff

Price is usually within the range she expects The best value is a style that is right for her and

her husband and a brand they think is good Dishwashers that “stick out” destroy the “look” of

the kitchen Believes that client’s brand is ‘old-fashioned’ Believes that most major manufacturers offer

similar quality

DesiredExperience

DesiredExperience

Product / ServiceBeliefs and

Associations

Product / ServiceBeliefs and

Associations

Purchaseand Usage

Environment

Purchaseand Usage

Environment

Purchase andUsage Behavior

Purchase andUsage Behavior

Female head of household is primary shopper because appliance has tolook good based on her tastes

Rejects brands that she is unfamiliar with Talks to friends and family, browses stores and reads shelter magazines

to learn about what is available and figure out style options When shopping for her dishwasher, she tries to imagine how it will look

in her kitchen, how it will blend-in, how it will enhance it

Visits several stores to find the dishwasher that best fits her desired style– May price shop once she has identified a specific SKU

Asks her husband to endorse her choice — he may have input on price anddurability

Shows off kitchen to friends and family once remodeling is complete and newappliance is in place

Note: Hypothesis in italics

<50K 50K+

Casual

LightHiking

Back -packing /Mountain-

eering

18-29 30-44 45 and Older

MaleMale Female Female <50K 50K+

AA

CC

EE

D

IB

F

H

G

L

JJ K

Collapsed becauseindividual segmentswere too small

Do not target

Developing Products and Services

Developing Products and Services

Strengthening Delivery Channels

Strengthening Delivery Channels

Improving Information

Infrastructure

Improving Information

Infrastructure

Addressing Policy and Strategic Challenges

Addressing Policy and Strategic Challenges

Through focused market research, we can develop an actionable segmentation of the SME financing market to more effectively target, understand and serve SME customers.

Who, What, and Why

Not All SME Customers Are the Same

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 3

Action SegmentationWhat Is It and What Do You Get From It?

Extensive Facilitated Sessions with Managers & Market “Experts”

Extensive Facilitated Sessions with Managers & Market “Experts”

Leveraging of Existing Organizational Data

Leveraging of Existing Organizational Data

Selective Primary ResearchSelective Primary Research

Multi-functional group develops hypothesized market definition and desired behavioral change

Qualitative and quantitative research to capture relevant market data and test hypotheses

Market experience to understand customer behavior

Focused qualitative and quantitative research to validate segmentation and test hypotheses

Action Segmentation™ is a tool used to create a base of knowledge and insight about customers and the market to enable better decision-making.

Determine the target customer segments and/or what occasions to target

Determine which customer segments not to address

Understand key differences between customer segments and determine allocation of resources

Develop foundation for creating– Segment specific strategies– Products, brands, customer

experience for different segments– Integrated marketing strategy

Structured Process Output

Target SegmentsTarget Segments Target SegmentsTarget Segments

Key Differences Between Key Differences Between SegmentsSegments

Key Differences Between Key Differences Between SegmentsSegments

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 4

Action SegmentationDefining the Market & Behavioral Objectives For SME Finance

The first step is to hypothesize a definition of the market . . .

. . . And then identify the desired behavioral change.

Primary business owners of small and medium-sized enterprises, in country, in need of loans and other financial products and services

Move away from using family, local money lenders and/or consumer credit and look to formal financial institutions for business financing

Secure loans, and ultimately a full range of financial products and services via our organization

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 5

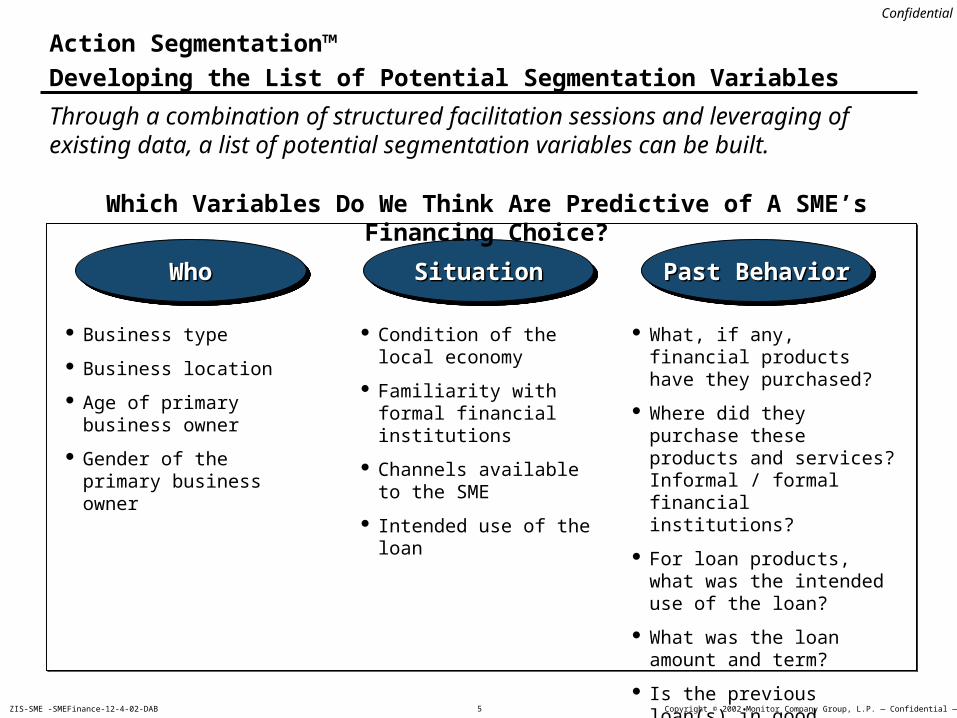

Action Segmentation™

Developing the List of Potential Segmentation Variables

Through a combination of structured facilitation sessions and leveraging of existing data, a list of potential segmentation variables can be built.

WhoWhoWhoWho SituationSituationSituationSituation Past BehaviorPast BehaviorPast BehaviorPast Behavior

Business type

Business location

Age of primary business owner

Gender of the primary business owner

Condition of the local economy

Familiarity with formal financial institutions

Channels available to the SME

Intended use of the loan

What, if any, financial products have they purchased?

Where did they purchase these products and services? Informal / formal financial institutions?

For loan products, what was the intended use of the loan?

What was the loan amount and term?

Is the previous loan(s) in good standing?

Which Variables Do We Think Are Predictive of A SME’s Financing Choice?

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 6

Urban Setting Rural Setting

<500K INR >500K INR

Men Women Men Women <500K

INR >500K

INR

Lending

Lending Plus (Savings, Insurance, etc.)

Full Service Banking (Lending, Savings, Insurance, Payment Transfer, other services)

Action Segmentation™

Creating the Market Map and Selecting Target Segments

Business Information

Product Requirements

These variables are then used to create a map that can be populated with the market data that has been collected. This allows us to prioritize segments based on relative size / attractiveness and our ability to execute.

Want more than local lender can offer in terms of product flexibility and/or breadth Women are more likely than men to look beyond local financing alternatives Our organization has facilities / representatives in densely populated urban areas where these

businesses are located

Want more than local lender can offer in terms of product flexibility and/or breadth Women are more likely than men to look beyond local financing alternatives Our organization has facilities / representatives in densely populated urban areas where these

businesses are located

Urban Women

Illustrative Market Data

Note: INR indicates Indian rupees.

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 7

Customer Portrait®

What Is It and What Do You Get from It?

The Customer Portrait® is an integrated process which results in a detailed understanding of a target customer’s behaviors and motivations.

Who?Who? Who?Who?

What?What? What?What?

Why?Why? Why?Why?

Integrated Process

Organizes and synthesizes existing organizational data

– Market research

– Market experience

Identifies critical data gaps to guide in-depth primary research on target customers

Output

Who are these customers?

What are they like?What do they do?

Why do they behave the way they do?

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 8

Desired Experience

Desired Experience

Product/Service

Beliefs & Associations

Product/Service

Beliefs & Associations

Purchaseand Usage

Environment

Purchaseand Usage

Environment

Purchase andUsage

Behavior

Purchase andUsage

Behavior

What the Customer WantsOut of the Experience

The Customer’s Mental Model of Purchase and

Consumption

The Setting

What the Customer Does

Customer Portrait®

Framework

The Customer Portrait® framework captures key influencers of customers’ decisions as well as critical beliefs and behaviors.

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 9

Desired Experience

Desired Experience

Product / Service Beliefs and

Associations

Product / Service Beliefs and

Associations

Purchase and Usage

Environment

Purchase and Usage

Environment

Invest in growing business Desire flexibility in loan terms due to

exposure to business fluctuations Want “lending plus” or full service

banking relationship

Women 25-35 years old Live and work in urban areas Varied education levels Fluctuating income, dependent on

business performance Expect to continue running the

business during lifetime Household has young children, not old

enough to run business, but in case of death, expect other family members to continue running the business

Borrows money from local lender when necessary, limited exposure to financial institutions

Customer Portrait®

SME Example: Small Businesswomen in Urban Areas

Purchase andUsage Behavior

Purchase andUsage Behavior

Welcome products offering them greater flexibility in managing their cash flows

Believe financial institutions will not provide loans

Local lender is preferred source of financing– Easily accessible for loan

initiation and repayment

Usually purchased one prior loan from local lender– 5-year term is common Prefer monthly payment schedule as it

helps them manage short-term fluctuations in business income

Prefer option to vary monthly payments subject to business fluctuation

This businesswoman owns a small baked goods business in an urban area. She distributes her products through a couple of small stores in her neighborhood and has a handful of employees, and relatives who help out during the busy holiday season. The country’s recent economic downturn has impacted her sales and made her question whether she can afford her plans to expand her business by buying a new oven to keep pace with upcoming holiday demand.

She is an established, if small, business owner and takes pride in her ability to support her children through her business efforts. In the past, she has taken small loans from a local credit union, which she has always paid back on schedule.

However, to pay for the new oven, she would need to resort to taking multiple loans from sources other than the credit union. In addition, she would like a secure place to keep the profit she generates during the holiday season so she can access it during the slower parts of the year. While she is concerned about taking on additional loans, she does not believe a formal financial institution would lend money to a small woman-owned business, so she makes plans to approach a local money-lender for the rest of the capital required to purchase the new oven.

This businesswoman owns a small baked goods business in an urban area. She distributes her products through a couple of small stores in her neighborhood and has a handful of employees, and relatives who help out during the busy holiday season. The country’s recent economic downturn has impacted her sales and made her question whether she can afford her plans to expand her business by buying a new oven to keep pace with upcoming holiday demand.

She is an established, if small, business owner and takes pride in her ability to support her children through her business efforts. In the past, she has taken small loans from a local credit union, which she has always paid back on schedule.

However, to pay for the new oven, she would need to resort to taking multiple loans from sources other than the credit union. In addition, she would like a secure place to keep the profit she generates during the holiday season so she can access it during the slower parts of the year. While she is concerned about taking on additional loans, she does not believe a formal financial institution would lend money to a small woman-owned business, so she makes plans to approach a local money-lender for the rest of the capital required to purchase the new oven.

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 10

Decisions & ActionsDecisions & ActionsDecisions & ActionsDecisions & ActionsMarket ResearchMarket ResearchMarket ResearchMarket Research

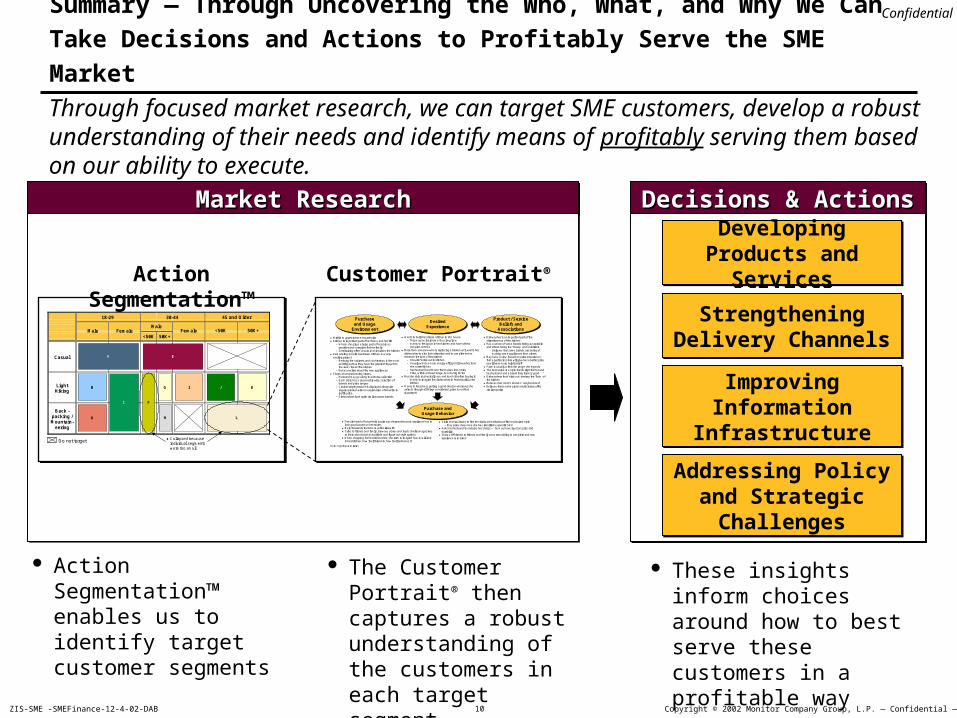

Summary — Through Uncovering the Who, What, and Why We Can Take

Decisions and Actions to Profitably Serve the SME Market

Action Segmentation™ Customer Portrait®

Middle to upper income households Kitchen is important part of her home and her life

– Where she plays a large part of her role asprovider and caregiver for her family

– Entertaining often occurs in or includes the kitchen Remodeling to build her dream kitchen is a very

exciting project– Redoing the cabinets and countertops is the most

exciting part as they have the greatest impact onthe look / feel of the kitchen

– Not as excited about the new appliances Shops at several nearby stores

– Husband may go along to endorse selection– Each store has a reasonably wide selection of

brands and price ranges– Cabinet depth product is displayed alongside

regular product with no explanation of benefits tojustify price

– Dishwashers look quite similar across brands

Wants to build her dream kitchen in this house– This may be their home for a long time– Wants to feel good in her kitchen and have others

complement her More than someone who is replacing a broken unit, wants her

dishwasher to also look attractive and to complement orenhance the look of her kitchen

– Shouldn’t stick out in kitchen– Usually wants a more energy-efficient dishwasher than

she currently has– Her husband wants one that makes less noise– Price, within a broad range, is not a big factor

Must be able to physically see and touch it before buying it– Wants to imagine the dishwasher in her beautiful, new

kitchen Wants to feel she is getting a good deal on whatever she

selects (though all things considered, price is not thatimportant)

Dishwasher is an important part of theattractiveness of the kitchen

Has a sense of some brands being acceptableand others being too “cheap” and unreliable

– Believes that some brands are better atmaking some appliances than others

May have a view (based on prior experience)that a particular store will give her a better priceor will have more helpful staff

Price is usually within the range she expects The best value is a style that is right for her and

her husband and a brand they think is good Dishwashers that “stick out” destroy the “look” of

the kitchen Believes that client’s brand is ‘old-fashioned’ Believes that most major manufacturers offer

similar quality

DesiredExperience

DesiredExperience

Product / ServiceBeliefs and

Associations

Product / ServiceBeliefs and

Associations

Purchaseand Usage

Environment

Purchaseand Usage

Environment

Purchase andUsage Behavior

Purchase andUsage Behavior

Female head of household is primary shopper because appliance has tolook good based on her tastes

Rejects brands that she is unfamiliar with Talks to friends and family, browses stores and reads shelter magazines

to learn about what is available and figure out style options When shopping for her dishwasher, she tries to imagine how it will look

in her kitchen, how it will blend-in, how it will enhance it

Visits several stores to find the dishwasher that best fits her desired style– May price shop once she has identified a specific SKU

Asks her husband to endorse her choice — he may have input on price anddurability

Shows off kitchen to friends and family once remodeling is complete and newappliance is in place

Note: Hypothesis in italics

<50K 50K+

Casual

LightHiking

Back -packing /Mountain-

eering

18-29 30-44 45 and Older

MaleMale Female Female <50K 50K+

AA

CC

EE

D

IB

F

H

G

L

JJ K

Collapsed becauseindividual segmentswere too small

Do not target

Developing Products and Services

Developing Products and Services

Strengthening Delivery Channels

Strengthening Delivery Channels

Improving Information

Infrastructure

Improving Information

Infrastructure

Addressing Policy and Strategic Challenges

Addressing Policy and Strategic Challenges

Through focused market research, we can target SME customers, develop a robust understanding of their needs and identify means of profitably serving them based on our ability to execute.

Action Segmentation™ enables us to identify target customer segments

The Customer Portrait® then captures a robust understanding of the customers in each target segment

These insights inform choices around how to best serve these customers in a profitable way

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 11

Summary

Benefits of Better Understanding the SME Customer

Increased ability to “mass-customize” products and services

– Targeted product and service design to better meet the needs of attractive SME customer segments

Ability to capitalize on SME opportunities that were previously “invisible”

– Lower the risk of “unknowns” in the SME financing market by truly understanding customers and capturing risk profile data more accurately

– Gain a better understanding of SME customers’ abilities to access technologies that could lower transaction costs and improve access

Better, more efficient use of resources to target new opportunities

– Improved credit approval capabilities by adding meaningful, qualitative data to existing credit-scoring approaches

– Effectively bridging the gap between relationship-driven corporate lending and consumer credit-scoring

This approach to truly getting to know the SME customer results in an increased ability to identify and activate this segment of the financial services market.

Benefits of Better Understanding the SME Customer

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 12

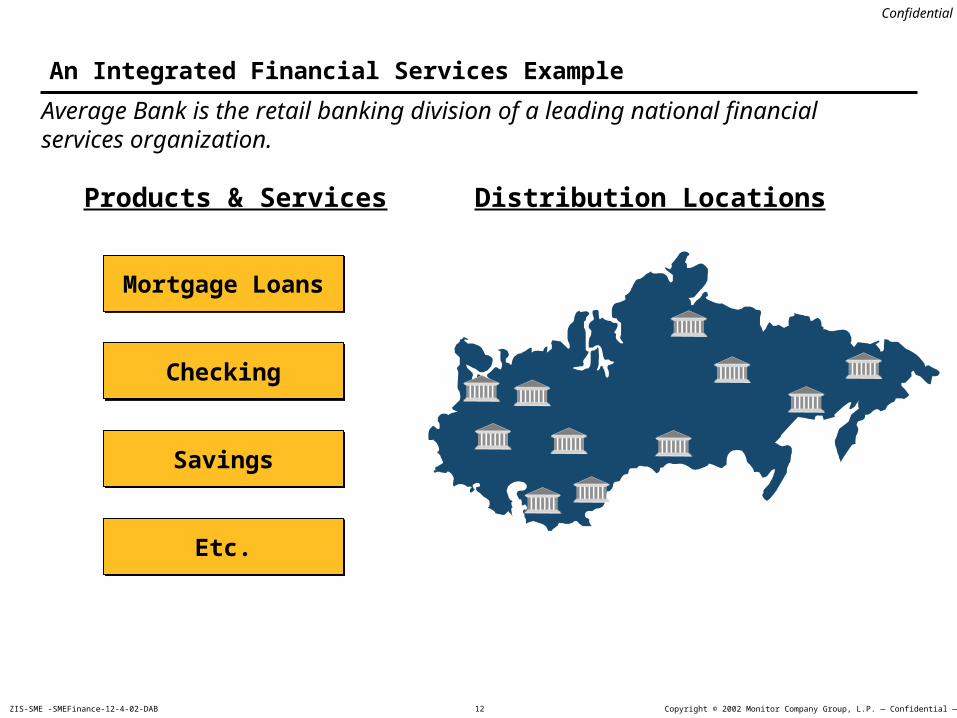

An Integrated Financial Services Example

Average Bank is the retail banking division of a leading national financial services organization.

Mortgage LoansMortgage Loans

CheckingChecking

SavingsSavings

Etc.Etc.

Distribution LocationsProducts & Services

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 13

Asset Retention: A Serious Problem

Average Bank had difficulty retaining its customers’ assets as they accumulated more and more money.

35%

30%

20%

10%

0%

10%

20%

30%

40%

Competitor A Competitor B Competitor C Average Bank

Percent of Bank

Customer Base

Retention Rates

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 14

18–54 Years 55+ Years

Home Owners Renters

<$50K $50K–$250K $250K–$500K >$500K

Management

Equity

Mutual Funds

Savings

Selecting Target Segments

Life Stage

BankNeeds

We developed a deeper understanding of the customer landscape . . .

Young Families

Established Families

Wealthy Individuals

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 15

Identifying Segment Opportunities

. . . And worked with Average Bank to identify and quantify segment opportunities…

Improve Customer Experience to

Attract Customers and Build Loyalty

Cross-sell Borrowing Products

Retain through Customized Wealth

Management

$350

$150$75

0

250

500

Young Families Established Families Wealthy Individuals

$ / Opportunity

(MM)

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 16

Understanding the Customer

‘Young Families’ Segment

Busy balancing work withspending time with family

Prefer to conduct transactions by telephone

Some of these customers have mortgages(most of which are with Average Bank)

Enough income to pay mortgage and daily expenses

Starting to save small amounts

…Resulting in the development of an in-depth understanding of the “Young Families” segment.

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 17

0

25

50

75

100

Understanding the Customer

‘Young Families’ Segment (cont.)

Believe other banks have better investment products

Think Average Bank offers only basic products

Unsure whether they will continue investing with Average Bank as they accumulate assets ?

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 18

Then…

The same product for everyone

– Broadcast advertising

– No segmentation

– Product focus

– Marketing / sales at the end of the process

– Focus on new customers

Percent

Performance Before

0%

10%

0%

10%

20%

MortgageMargins

AssetRetention

Strategy Results

Average Bank’s previous strategy had focused on products instead of customers, resulting in poor performance.

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 19

Now… A Marketing Turnaround with Results

Improved profitability and customer retention

Repositioned from a ‘mortgage’ to a ‘home ownership’ bank

Designed unique products to attract new ‘Young Families’ consumers

– Launched no-payment down mortgage loan (first in its market)

Improved customer experience to build loyalty

– Embedded customer mindset and understanding of the ‘Young Families’ segment across company

– Redesigned telephone support and sales to be convenient for ‘Young Families’

– Created life cycle products appropriate for ‘Young Families’ as they grow

Strategy Results

Average Bank has completed a strategic turnaround which improved retention of assets and increased margins.

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 20

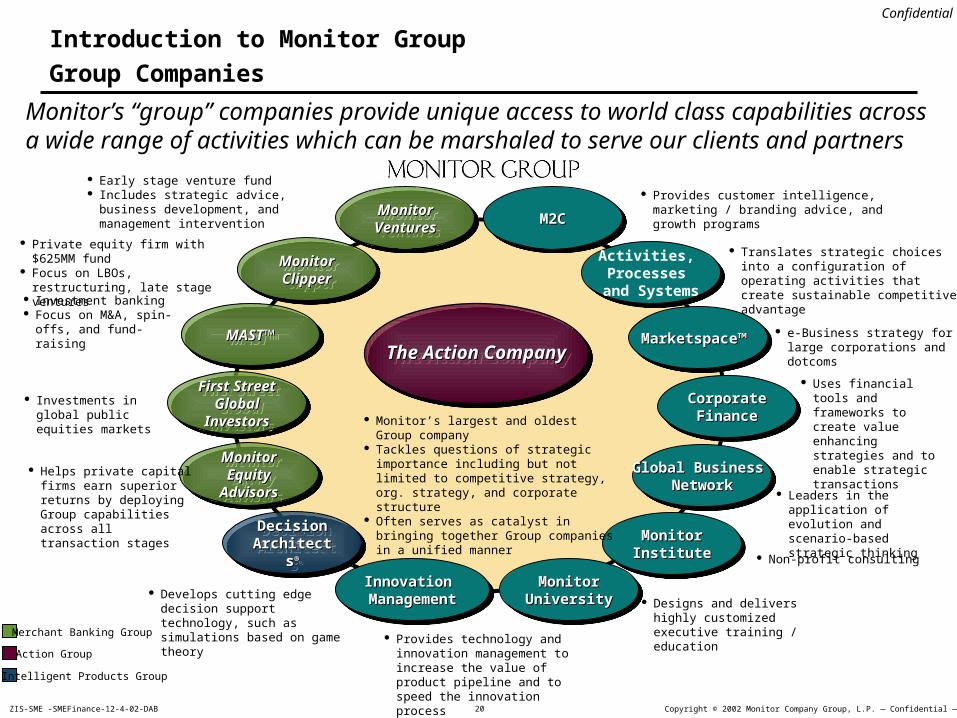

Extensive experience in consulting for telecom incumbents and new entrants

Private equity firm with $625MM fund Focus on LBOs, restructuring, late

stage ventures

Translates strategic choices into a configuration of operating activities that create sustainable competitive advantage Investment banking

Focus on M&A, spin-offs, and fund-raising

Non-profit consulting

Designs and delivers highly customized executive training / education

Develops cutting edge decision support technology, such as simulations based on game theory

Uses financial tools and frameworks to create value enhancing strategies and to enable strategic transactions

e-Business strategy for large corporations and dotcoms

Early stage venture fund Includes strategic advice, business

development, and management intervention

Investments in global public equities markets

Provides customer intelligence, marketing / branding advice, and growth programs

Monitor’s “group” companies provide unique access to world class capabilities across a wide range of activities which can be marshaled to serve our clients and partners

Introduction to Monitor Group

Group Companies

Leaders in the application of evolution and scenario-based strategic thinking

Merchant Banking Group

Action Group

Intelligent Products Group

The Action CompanyThe Action CompanyThe Action CompanyThe Action Company

M2CM2CM2CM2C

Marketspace™ Marketspace™ Marketspace™ Marketspace™ MAST™MAST™MAST™MAST™

MonitorMonitorUniversityUniversity

MonitorMonitorUniversityUniversity

Activities, Processes

and Systems

Activities, Processes

and Systems

Monitor Monitor ClipperClipper

Monitor Monitor ClipperClipper

Decision Decision ArchitectsArchitects®®

Decision Decision ArchitectsArchitects®®

CorporateCorporateFinanceFinance

CorporateCorporateFinanceFinance

MonitorMonitorInstituteInstitute

MonitorMonitorInstituteInstitute

Monitor Monitor VenturesVentures

Monitor Monitor VenturesVentures

First Street First Street Global Global

InvestorsInvestors

First Street First Street Global Global

InvestorsInvestors

Global Business Global Business NetworkNetwork

Global Business Global Business NetworkNetwork

Monitor Monitor Equity Equity

AdvisorsAdvisors

Monitor Monitor Equity Equity

AdvisorsAdvisors

Helps private capital firms earn superior returns by deploying Group capabilities across all transaction stages

Monitor’s largest and oldest Group company Tackles questions of strategic importance

including but not limited to competitive strategy, org. strategy, and corporate structure

Often serves as catalyst in bringing together Group companies in a unified manner

Innovation Innovation ManagementManagement

Innovation Innovation ManagementManagement

Provides technology and innovation management to increase the value of product pipeline and to speed the innovation process

Confidential

Copyright © 2002 Monitor Company Group, L.P. — Confidential — CAMZIS-SME -SMEFinance-12-4-02-DAB 21

Introduction to Monitor Group

Our Geographic Footprint

Monitor has approximately 1,050 professionals in 29 offices worldwide functioning as a single firm- we put a premium on serving our clients globally.

Los AngelesNew York

Cambridge

Toronto

LondonParis

Madrid

AmsterdamMunich

Stockholm

São Paulo

ZurichMilan

Johannesburg

AthensTel Aviv

Moscow

Singapore

Manila

Hong Kong

Tokyo

SeoulChicago

Frankfurt

Mumbai

San FranciscoEmeryvillePalo Alto

Melbourne

BeijingIstanbul