Tarif forfaitaire de responsabilité: quels impacts sur le ...

Document of

The World Bank

FOR OFFICIAL USE ONLY

Report No. P-6855-AL

REPORT AND RECOMMENDATION

OF THE

PRESIDENT OF THE

INTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT

TO THE

E CUTIVE DIRECTORS

ON A

PROPOSED STRUCTURAL ADJUSTMENT LOAN

IN AN AMOUNT EQUIVALENT TO US$300 MILLION

TO THE

DEMOCRATIC AND POPULAR REPUBLIC OF ALGERIA

APRIL 4, 1996

This document has a restricted distribution and may be used by recipients only in the perfornance oftheir official duties. Its contents may not otherwise be disclosed without World Bank authorization.

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

Pub

lic D

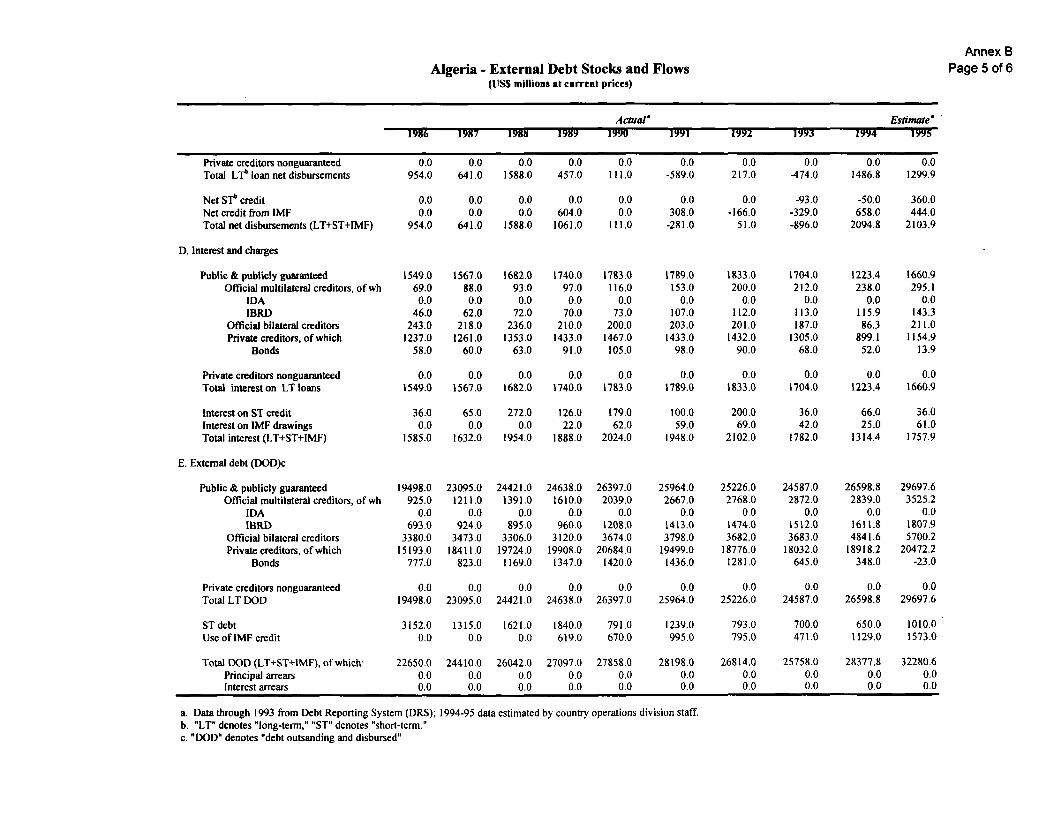

iscl

osur

e A

utho

rized

Pub

lic D

iscl

osur

e A

utho

rized

CURRENCY EQUIVALENTS

Unit of Currency = Algerian Dinar (DA)

1992 1993 1994 1995 JAN 1996

DA per US$, period average 21.84 23.34 35.06 47.66 53.00

DA per US$, end of period 22.78 24.12 42.89 52.17 53.77

FISCAL YEAR

January 1 - December 31

WEIGHTS AND MEASURES

Metric System

ACRONYMS AND ABBREVIATIONS

AFS Allocation Forfaitaire de Solidarite (public assistance payments to the elderlyand handicapped)

ASAL AgricuJture Sector Adjustment LoanBOP Balance of PaymentsCAS Country Assistance StrategyCNEP Caisse Nationale d'Epargne et de Prevoyance (National Housing Finance

Institution)CNPE Conseil Nationale de Participation de l'Etat (governing body for the state

holding companies)COSOB Commission d'Organisation et de Surveillance des Operations de Bourse

(Exchange Commission)EFF Extended Fund FacilityEPE Entreprise Publique Economique (Autonomous Public Enterprise)EPL Entreprise Publique Locale (Local Public Enterprise)EPS Entreprise Publique Socialiste (Non-autonomous Public Enterprise)ERL Economic Rehabilitation Support LoanEU European UnionFA Fonds d'assainissement (Restructuring Fund)ICOR Incremental Capital Output RatioIMF International Monetary FundLSMS Living Standards Measurement SurveyONS Office National des Statistiques (National Statistical Office)PAIG Programme d'Activites d'Interet General (self-targeted public assistance

program)PE Public EnterprisePER Public Expenditure ReviewPSA Private Sector AssessmentSAL Structural Adjustment LoanVAT Value Added Tax

FOR OFFICIAL USE ONLY

DEMOCRATIC AND POPULAR REPUBLIC OF ALGERIA

STRUCTURAI, ADJUSTMENT LOAN

TABLE OF CONTENTS

Page No.

Loan and Program Summary .................... i

PART I: Recent Developments and Prospects .1A. Background .1B. Performance under the Renewed Reform Program .2C. Medium-term Prospects and Financing Plan. 8

PART II: The Government's Adjustment Strategy .. 10A. Macroeconomic Program .IIB. Major Elements of the Adjustment Program .12

PART III: Algeria's Social Safety Net Strategy .18

PART IV: The Proposed Loan ........................................ 19A. Program to be Supported and Link to the Country

Assistance Strategy ................................... 19B. Poverty Impact .......... ........................... 20C. Negotiations, Effectiveness, and Proposed Tranche Conditionality ..... 20D. Procurement, Disbursement, Financial Management, and Auditing ..... 22E. Cofinancing . ....................................... 23F. Environmental Assessment .............................. 23G. Program Benefits and Risks ............................. 23

PART V: Recommendation ........... 24

ANNEXESA. Social Indicators of DevelopmentB. Key Economic Indicators, 1986-95C. Status of Bank Group OperationsD. Government Letter of Development Policy

Attachment 1 -- List of Monitorable IndicatorsAttachment 2-- Matrix of ActionsAttachment 3 -- Restructuring Fund

MAP: IBRD No. 21836

This document has a restricted distribution and may be used by recipients only in the performance of theirofficial duties. Its contents may not otherwise be disclosed without World Bank authorization.

Democratic and Popular Republic of Algeria

Structural Adjustment Loan

Summary of Proposed Loan and Program

Borrower: Democratic and Popular Republic of Algeria.

Amount: US$300 million equivalent.

Terms: Repayment in 17 years, including 5 years of grace, at the Bank'sstandard variable interest rate.

Loan Objectives: The proposed Structural Adjustment Loan (SAL) is the centralelement in the Bank's assistance strategy for Algeria. Thisstrategy aims to support the Algerian authorities in: (i)stimulating private-sector-led growth; (ii) protecting the poorduring the transition to a market-based economy; and (iii)enhancing the country's ability to mobilize external resources.The SAL builds on progress made under the recent EconomicRehabilitation Support Loan, under which the Algerianauthorities made tangible progress in adjustment and met manyof the agreed objectives, including the adoption of a privatizationlaw, sooner than anticipated.

Loan Description: The loan supports an adjustment program that is moving Algeriacloser to its goal of an open, market-based economy in thecontext of growth and increased employment. The keycomponents of the program include: (i) macroeconomicstabilization and rationalization of public expenditures; (ii)support for public enterprise reform and private sectordevelopment, including: large-scale privatization of small publicenterprises, where local demand exists; further reforms designedto limit the losses of large public enterprises and ready them forprivatization; increased private-sector participation insubcontracting and in the provision of municipal services; andfinancial sector reform designed to increase competition andcreate needed new financial instruments; and (iii) support for thealready successfully implemented new social protection system,including some measures to improve its performance. All of thespecific measures to be supported by the SAL are outlined in thegovernment's Letter of Development Policy and are listed in theattached policy matrix.

- ii -

Benefits: The key benefit would be to contribute, in conjunction with theIMF's ongoing EFF program, to the reversal of ten years ofeconomic decline in Algeria through a more efficient use ofeconomic resources. The actions to be supported by this loanwould clearly demonstrate the authorities' commitment to movequickly in establishing the necessary conditions for a market-based economy.

Risks: The risks are great, most notably the security-related risks. Thedifficult security situation complicates the process of structuraladjustment and reform. These risks cannot be totally offset.However, the fact that the authorities have taken most of themajor actions required under the loan before Board presentationminimizes, to the extent possible, the risk of policy reversal.Many of these actions, including privatization of small-scaleenterprises, will create a constituency for further reform and arelikely to keep Algeria on the path toward a market-basedeconomy.

Disbursements: The Structural Adjustment Loan will disburse in two tranches ofUS$150 million each. The first will be available upon loaneffectiveness. The release of the second tranche will beconditional on satisfactory macroeconomic performance (notablycompliance with EFF conditionality) and satisfactory progress onadjustment, including the fulfillment of a limited number ofspecific measures. The expected date for second tranche releaseis 12 months after loan effectiveness.

Poverty Category: Poverty focused; the loan acknowledges the efforts of theAlgerian authorities in successfully implementing their newsocial safety net programs, designed to minimize possiblenegative impacts of adjustment on the poor, notably as a resultof the removal of inefficient and costly generalized pricesubsidies. The two new programs, targeted payments to theelderly and handicapped without other income and a self-targetedlabor-based income transfer program for those able to work arein operation. The loan supports further improvements in thesocial safety net, including actions to improve the functioning ofthe above two programs.

REPORT AND RECOMMENDATION OF THE PRESIDENT OF THEINTERNATIONAL BANK FOR RECONSTRUCTION AND DEVELOPMENT TO THEEXECUTIVE DIRECTORS ON A PROPOSED STRUCTURAL ADJUSTMENT LOAN

TO THE DEMOCRATIC AND POPULAR REPUBLIC OF ALGERIA

1. I submit for your approval the following report and recommendation on a proposedStructural Adjustment Loan (SAL) to the Government of the Democratic and Popular Republic of Algeriafor the equivalent of US$300 million in support of a program of structural reform and privatization. TheLoan would be at the Bank's standard variable interest rate, with a maturity of 17 years, including fiveyears of grace. The Bank's Country Assistance Strategy was presented to the Board on February 27,1996 (Report No. 15316-AL).

I. Recent Economic Developments and Prospects

A. Background

2. After independence in 1962, Algeria followed a central planning model of growthcharacterized by heavy industrialization and extensive social infrastructure development. Thedevelopment program relied heavily on hydrocarbon revenues. During this period, Algeria achievedimportant social progress. Illiteracy was reduced, life expectancy increased, and primary schoolenrollment reached close to 100 percent. By the end of the 1970s, however, there were clear signs thatthe model followed had resulted in an inefficient allocation of resources and presented poor growthprospects. Productivity was low in spite of investment/output ratios from 40 to more than 50 percent,on a par with the high-growth East Asian countries. Shortages were common and a flourishing informalsector had emerged.

3. The sharp fall in oil prices in 1986 triggered the crisis. Hydrocarbon exports fell fromUS$12.7 billion in 1985 to an average of US$7.7 billion in 1986-88. The authorities initially usedexternal borrowing to maintain consumption. In two years, the total stock of external debt rose fromUS$18 billion to more than US$24 billion; most of this new borrowing fell at the short end of thematurity spectrum. Realizing that the situation was unsustainable, the Algerian Government took initialsteps to liberalize the system, both on the political and the economic front. A wide number of policymeasures were undertaken, ranging from the dismantling of state farms to the removal of barriers toforeign investment, increasing the private sector's access to credit and foreign exchange, and the abolitionof state import monopolies. In addition, most public enterprises (PEs) became autonomous, collectivebargaining was decentralized, and the central bank was given much greater autonomy in monetary policy.The IMF and the World Bank actively supported these reforms. The Bank's support included twoadjustment operations, an Economic Reform Support Loan approved in 1989 and an Economic andFinancial Sector Adjustment Loan approved in 1991.

4. However, the institutional reforms failed to reverse the economic decline. The mainreasons for the lack of a supply response were: (i) little change in incentives for public sector managers;(ii) a financial sector not equipped to cope with the new demands placed on it; and (iii) a publicbureaucracy that maintained its orientation of control, rather than facilitation, of private sectordevelopment. For example, private sector access to foreign exchange improved but was limited anderratic, as demonstrated by the large gap, as much as 300 percent, between the official and parallelmarket rates from 1990 to 1993. Unemployment increased from 17 percent in 1986 to 21 percent in

- 2 -

1991. An already serious housing shortage worsened to the point that the average occupancy rate perunit is now more than eight.

5. The period 1992-1993 was marked by increasing civil strife and some important reversalsof economic policy. Import controls were implemented in order to ration foreign exchange -- the privatesector was virtually excluded from access -- and to generate resources to cope with the service of theexternal debt; the debt service ratio reached 73 percent in 1993. However, arrears began to appeardespite these efforts and despite the government's attempt to restructure debt on a bilateral basis with keycreditors. Access to foreign credit became more and more difficult. Planned adjustment and structuralreform measures were delayed. Subsidies and wage expenditures soared, culminating in a fiscal deficitof 8.7 percent of GDP in 1993. In spite of these outlays, private consumption per capita fell by 4 percentand per capita output dropped 5 percent. The authorities faced an untenable economic situation.

B. Performance under the Renewed Reform Program

6. The initiation of the current reform process. In 1994, in response to the emergingnational consensus on the need for major structural reform, the authorities implemented an intensifiedstabilization and adjustment program. The program was based on 3 pillars: (i) stabilization of theeconomy; (ii) relaunching and deepening the postponed structural reform needed in order to acceleratethe transition to a market economy; while at the same time, (iii) taking actions to reverse the debilitatingdecline in living standards and to protect the poor during the transition. These actions included anincrease in the current account deficit to make room for imports necessary to stimulate growth. TheAlgerian Government needed and received the support of the international community. In March 1994,the IMF Executive Board approved a one year stand-by arrangement and a request for a purchase underthe Compensatory and Contingency Financing Facility totaling SDR731.5 million (about US$1 billion).This agreement was followed in early June by a rescheduling of Algeria's official bilateral debt at theParis Club. World Bank assistance for structural reform came in the form of an Economic RehabilitationSupport Loan (ERL) of US$150 million, approved on January 12, 1995.

7. The stabilization program for 1994/95 backed by the IMF and World Bank focused onreducing macroeconomic imbalances and, at the same time, establishing the basis for a sound and credibleprogram of transition to a market economy. Its main objectives were: moderation of the inflation rate;fiscal restraint; exchange rate realignment; and further domestic price liberalization. The policy packageincluded, among others measures: an important devaluation (80 percent and a further devaluation sincethen to 100 percent) of the exchange value of the dinar; elimination of most non-tariff trade and exchangerestrictions; the reduction of subsidies on energy and food products; freeing the prices on agriculturalinputs; imposing a ceiling on the central government wage bill; limits on bank credit to the non-autonomous PEs; and removal of the ceiling on bank lending rates. Special provisions in the programaimed at reducing the impact of the adjustment on the poorest segment of the population. Under theERL, reform measures agreed with the government included private sector development measures, a verysmall pilot privatization program, restructuring of the largest public enterprises, public expenditurereform, financial sector reform, and strengthening of the social protection system.

8. The Algerian authorities have clearly demonstrated that they are serious in the pursuit ofmeaningful adjustment. They met all the conditions of the Fund stand-by arrangement. They alsoundertook the measures foreseen under the ERL, in several cases ahead of schedule (notably the passageof a privatization law). When unexpected expenditure pressures arose at midyear, the authoritiesundertook corrective action to raise revenues (advancing cuts in subsidies) and to reduce expenditures

- 3 -

(delaying wage increases) to keep the program on track. In spite of good policy performance, growthwas a disappointing -1.2 percent of GDP in 1994. Two key factors contributed to the poor outcome:a drought reduced agricultural output, and the expected increase in imports came too late in the year tocontribute to growth. The delay was in part the result of the difficulties faced by Algerian banks inmaintaining access to short-term credit after the Paris Club rescheduling.

9. Algeria's achievements through this first year of renewed adjustment were important (seecolumn 1 of Table 1). Prices are substantially free. The external trading system is open; for the firsttime, the private sector has access to foreign exchange on a market basis for trade transactions. The taxsystem has been reformed. Public enterprises face hard budget constraints -- no access to the Treasuryexcept for a handful of key enterprises on a very limited basis and access to the banking system on moreor less equal terms with the private sector. The commercial and investment codes have been modernizedand no longer favor the public sector. For example, investments no longer require government approvaland investment incentives apply equally to foreign and domestic investors, public or private. For the firsttime, the sale or dissolution of public enterprises is legally possible -- and has happened. The bankingand insurance sectors are open to private investment, in existing institutions or through the creation ofnew ones (one new private bank and a cooperative agricultural finance institution have opened). At leastas important, a vital and significant new social safety net has been put in place, comprising a self-targetedpublic works program for the able-bodied poor, a means-tested program for the elderly and handicapped,and a program of unemployment insurance for those laid off in the context of firm restructuring orclosure. To date, almost one million Algerians have benefitted directly from the three new programs;the number reaches approximately 4 million counting dependents.

10. The authorities realize that their ambition of achieving significant and sustainableeconomic growth depends on continued implementation of a strong stabilization and adjustment program.In that context, they sought the support of the IMF (and are seeking the support of the World Bank inthe form of the proposed SAL) for a medium-term reform program. On May 22, 1995 the IMF Boardapproved a three-year (April 1995-March 1998) SDR1.17 billion extended arrangement under theExtended Fund Facility (EFF). The program supported by the EFF, discussed below, targets fourobjectives: (i) ensuring high and sustainable growth; (ii) rapidly establishing a low level of inflation; (iii)strengthening the social safety net; and (iv) restoring balance of payments viability by 1998.

11. Performance under the EFF. The IMF has conducted its first review under the EFF.All the performance criteria for end-June 1995 were met, and all structural measures envisaged under theprogram have been implemented as scheduled, a few of them ahead of their target dates. Performancecriteria for end-September were met, except, however, for those relating to foreign exchange reservesand the Bank of Algeria's net domestic assets. The non-observation of these two criteria was due toexogenous factors which are temporary in nature, namely: (i) a large rise in grain prices: (ii) a shortfallof capital inflows; and (iii) a depreciation of the dollar relative to other major currencies (Algeria'sexternal debt and imports are heavily non-dollar denominated while petroleum exports are priced indollars.) In response to these shocks, the authorities have allowed the dinar to depreciate well beyondprogramn projections, maintained a tight fiscal stance, including an acceleration of the scheduled subsidyelimination, and allowed interest rates to increase. Given the policy actions taken by the authorities inresponse to these exogenous shocks, as well as their continued commitment to the macroeconomicobjectives of the three-year program, the Fund Executive Board granted a waiver for non-observance ofthe end-September 1995 performance criteria for the Bank of Algeria's net domestic assets and for foreignexchange reserves. The recent pressure on foreign exchange reserves is clear evidence of Algeria's needfor timely balance of payments support; the SAL will be a critical element of that support.

- 4 -

Table 1: Algeria - Structural Reform Program

Policy Achievements prior to EFF Current Program Supported by the EFF Remaining Adjustment Agendaand Proposed Structural Adjustment I

Loan __

Trade and Exchange Reform

- Substantial exchange rate adjustment. - Establishment of an interbank foreign - Move to capital account convertibility.exchange market (end-1995, EFF) and

- Introduction of a managed float for the expansion of the interbank market to non- - Establish hedging mechanisms fordinar through fixing sessions. bank participants (1996, EFF). foreign exchange risk.

- Elimination of most exchange rate - Elimination of minimum maturity - Pursue negotiation of a Free Traderestrictions for trade transactions. requirement on external borrowing for Agreement with the European Union,

imports of capital goods, achieving full accompanied by parallel- Elimination of a broad range of convertibility for trade in goods nondiscriminatory reduction in tradeproducts from the list of products subject (completed, EFF). protection.to professional criteria requirements forimporters. - Progressive liberalization of invisible - Program of trade facilitation.

transactions, culminating in current- Elimination of negative lists for account convertibility (1997, EFF).imports.

- Elimination of export prohibitions and - Elimination of professional criteriathe adoption of a uniform export proceeds requirements for importers (completed,surrender requirement of 50 percent. EFF)

- Revise tariff rates progressivelydownward, based on the results of aneffective protection study now underwaywith Bank support (1996-1998; EFF).

Prce Liberalization

- Freeing of prices of goods accounting - Elimination of the global subsidy on (Price liberalization program is foreseenfor 80 percent of CPI basket, not energy products (domestic energy prices to be virtually complete at the end of theincluding further price liberalization noted now globally at or above world market EFF program.)below and in column 2. prices, completed. EFF).

- 98 percent increase in the weighted - Removal of subsidies on all productsaverage price of subsidized food and except wheat products and pasteurizedenergy products in the year ending in milk (completed, EFF).May 1995.

- Removal of last remaining global- Adoption of a competition law (ERL). subsidies -- wheat products (completed,

EFF) and pasteurized milk (end-1996,- Transfer of several products from the EFF).administered price category to thecontrolled profit margin category. - Elimination of profit margin controls on

sugar, all grains except wheat, edible oils- Quarterly revisions in the price of and school supplies (done, EFF).electricity and gas in line with inflationtrends. - Removal of last remaining profit margin

controls, those on medicines (1998, EFF).- Freeing of agriculture input prices.

- Freeing of construction prices for socialhousing.

Policy Achievements prior to EFF | Current Program Supported by the EFF Remaining Adjustment Agendaand Proposed Structural Adjustment

Loan

Government Budget

- Expansion of the VAT base and an - Further VAT reforms (ongoing through - Adoption of a fonmal mechanism toincrease in rates for several products. January 1997, EFF). institutionalize budget surpluses.

- Excise duty of 50 percent introduced for - Public expenditure program revisions in - Further reduction of marginal incomecars and increase in duties on luxury the context of a Public Expenditure tax rates.products and consumer appliances. Review (ongoing through 1997, SAL).

- Further reduction and rationalization of- Reduction in the maximum effective tax - Civil service reform designed to corporate income tax rates.rate for personal income from 79 percent gradually reduce overstaffing, whileto 65 percent. meeting priority needs more effectively - Continue civil service reform process

and generating savings on the wage bill started under EFF and SAL.- Increase in the tax rate on reinvested (1996-1998 in the context of the publicprofits from 5 to 33 percent as a step expenditure review, EFF/SAL). - Continued reform of budget formulationtoward a uniform corporate tax rate. and control processes started under the

- Achievement of significant budget EFF and SAL.- Elimination of tax exemptions for surplus (1998, EFF).interest earnings on treasury bonds.

- Ceiling on central government wage billand limitation of the minimum wageincrease to 12.5 percent.

- Withdrawal of the Treasury from thefinancing of new investments inautonomous public enterprises, withexceptions limited to the frameworkadopted under the ERL and establishmentof a timetable to phase out theRestructuring Fund (ERL).

Public Enterprise Reform and PrivateSector Development _________________

- Passage to financial autonomy of 5 of - Passage of a privatization law (drafted - Privatization of remaining public23 large non-autonomous public under ERL, passage -- SAL) enterprises in competitive sectors, exceptenterprises. (Almost 400 national public for a small number deemed strategic.enterprises are already autonomous.) - Implementation of a large-scale program

of privatization and private provision of - Reform, including possible- Creation of a Ministry charged with the municipal services. privatization, of public monopolies,development of a privatization program, including the national airline, railway,adoption of a privatization policy, - Adoption of a holding company and telecommunications companies.drafting of a privatization law. framework for autonomous public

enterprises, designed to isolate them from - Labor market reform; reduction in- Enactment of a revised commercial code political influence and prepare most for payroll tax rate,applying the same regulations to public privatization (SAL).and private enterprises. - Abolish public land developers; future

- Preparation of legal texts permitting the sales of public lands by auction.- Adoption of a new investment code that privatization of state agricultural landgives foreign investors rights equal to or (SAL). - Adoption of regulatory framework forsurpassing domestic investors. private pinmary, secondary, and higher

education.- Creation of a national investmentagency and a one-stop informationwindow to help cut through red tape.

- 6 -

Policy Achievements prior to EFF Current Programn Supported by the EFF | Remaining Adjustment Agendaand Proposed Structural Adjustment

Loan

Pubhc Enterprise Reformn and PrivateSector Development (continued)

- Removal of the obligation to maintain - Program for the regularization of land - Development of institutions for a better-one price for a product throughout the titles or leases for commercial and functioning real estate market.country (pan-territorial pricing). industrial enterprises (SAL.

- Dissolution of 88 local publicenterpnses.

- Putting up for bids of five public hotels(one has been sold to date).

Financial Sector

- Introduction of a minimum reserve - Removal of the ceiling on bank interest - Privatization of remaining state-ownedrequirement of 3 percent on bank rate spreads (EFF). banks.deposits, remunerated at I I percent.

- Introduction of auctions for central bank - Development of a functioning stock- Elimination of the ceiling on bank credit to banks (EFF). market.lending rates and the introduction of a 5percent limit on spreads. - Achievement of positive real deposit - Further development of bond market.

interest rates (except on deposits related to- Issuance of government bonds carrying housing), in relation to underlying - Development of new privatean interest rate of 16.5 percent. inflation trend (EFF, end-1996). institutional savers and reform of existing

official institutional savers (pension- Auditing of state-owned banks and - Recapitalization of state-owned banks to funds, mutual funds, and insuranceagreement on a plan for their achieve capital adequacy ratios of 4 companies).recapitalization (ERL). percent and signing of management

contracts obliging managers to maintain - Development of an active and- Introduction of a management fee of 3.5 and increase capital adequacy ratios (to 8 competitive pnmary and secondarypercent on Bank of Algeria credit to the percent by end-1999 - SAL). mortgage market.government.

-Seek private sector participation in at - Development of financial institutions- Opening the bank and insurance least one state-owned bank (SAL). designed to service the demand for creditindustries to the private sector (latter-- from micro-enterprises.ERL). - Strengthening of prudential regulations

dealing with foreign exchange andgovernment bond transactions (SAL).

- Restructure the state housing bank (end-1996. SAL and housing loans).

- Creation of a functioning treasury billand bond market (1996; EFF and SAL).

Housing Sector

- Ongoing land registration program. - Adoption of a new housing strategy, - Shift housing fuiance from treasury-emphasizing the role of the private sector managed resources to household and

- A mechanism has been put in place for (SAL; the implementation of the strategy institutional savings, managed by aautomatic adjustment of rent on public would be supported by a Housing Sector private banking sector.rental housing. Adjustment Loan -- see CAS).

- Shift to transparent and targeted- Consolidation of some public sector housing subsidies.housing companies and liquidation ofothers. - Private sector land development in the

context of municipal plans.

Policy Achievements prior to EFF Current Program Supported by the EFF Remaining Adjustment Agendaand Proposed Structural Adjustment

Loan

Agriculture l

- Distribution of state lands held by - Preparation of laws establishing the - Carry out state agricultural landsocialist state farms to individuals and mechanisms for the privatization of state- privatization program, in the context ofcollective farms, with long-term usufruct owned agriculture land (SAL). an ASAL (see CAS).rights.

- Privatization of public agricultural - Elimination of state monopolies in- Elimination of input subsidies except for enterprises (SAL). cereal commerce, stocking, andseed potatoes and irrigation water. distribution.

- Resolve financial problems of privatizedcooperatives arising from debtsaccumulated before privatization.

- Development of modem, private sectorbased agricultural finance and riskmanagement systems.

Social Safety Net

- Elimination of system of poorly targeted - Strengthen the targeting and improve the - Carry out social protection programcash allowances for non-income-earning functioning of the PAIG, AFS, improvements, based on LSMS andfamilies. unemployment insurance schemes (SAL). poverty study results.

- Transfer of responsibility of family - Creation and implementation of a social - Overhaul of social security system.allowances from payroll taxes to the fund (1996-1998; proposed Social Safetygovernment budget. Net Loan). - Further public expenditure reform in

favor of expenditures targeted toward- Introduction of a self-targeted public - Program of public works designed to basic education and basic preventiveworks scheme (PAIG) designed to benefit unemployed workers (separate medicine.transfer income to the very poor. from the PAIG, which targets the very

poor -- 1996; proposed Social Safety Net- Introduction of a targeted transfer Loan.)scheme (AFS) for the elderly andhandicapped not benefitting from existing - Carry out LSMS to gain information forpension and benefit system. better targeting of social protection

programs (ongoing; ERL and SAL).- Introduction of an unemploymentinsurance scheme. - Revise social protection programs, based

on LSMS data and Poverty Assessment(1996; SAL).

- Reform of housing subsidy program,retargeted toward the poor (1996; housingloans).

- 8 -

C. Medium-term Prospects and Financing Plan

12. Algeria's medium-term growth and balance of payments prospects are promising,provided that the authorities can maintain the momentum of adjustment (Table 2). Non-hydrocarbonoutput is projected to grow at a real rate of more than four percent between 1995 and 1998. The sourcesof non-hydrocarbon growth, as noted above, will be mainly in the construction, service, and agriculturesectors. Growth in these sectors will generate the jobs needed to blunt the growth in unemployment.Construction will benefit from the housing sector reforms, the availability of key imported inputs, theincreased use of private contractors for public works, and the privatization program. That program willput construction equipment in the hands of private operators. In addition, former public sectorconstruction workers are likely to start their own private businesses or find employment with emergingor expanding private firms. Expanded private sector activity will contribute enormously to meeting thecritical housing needs of the Algerian population. The agriculture sector will benefit from landprivatization and from the break-up of inefficient monopoly suppliers in the privatization process. Inorder to generate employment quickly, these reforms will be accompanied by labor-intensive public worksprograms aimed at unemployed youth. As explained in the Country Assistance Strategy (CAS) discussedat the Board on February 27, 1996, the public works program will be supported by the Bank.

13. While non-petroleum sectors will generate internal growth, Algeria will remain dependenton petroleum exports for a quick return to balance of payments viability, expected before the end of1998. Non-petroleum exports are projected to rise almost 300 percent between 1994 and 1998, but theirinitial level is low (US$280 million in 1994). Investments currently underway would double natural gasexports and reverse the decline in oil exports, resulting in an increase in hydrocarbon export revenuesof more than US$2 billion between 1995 and 1998 and a further sizeable increase thereafter. (Severalforeign petroleum companies, including BP, Total, REPSOL, and ARCO, have recently signed contractsto invest a total of almost US$6 billion in Algeria.) As noted in the CAS, the Bank strategy for Algeriaincludes support for policies that would further increase hydrocarbon exports.

14. The largest element in the medium-term financing plan is the rescheduling of officialbilateral debt through the Paris Club (Table 3). The rescheduling of private debt on the basis of anagreement reached with a consortium of banks and leasing companies will make a smaller but importantcontribution. These reschedulings, which provide a total of US$16 billion of debt service relief between1994 and 1998, would not have been possible without the support of the IMF, first through the 1994Stand-by and now under the EFF. The first Paris Club rescheduling, shortly after the approval of theStand-by, provided Algeria with favorable terms: a one-year consolidation period (the period in whichdebt service is reduced); a maturity of 15 years with three years of grace and a graduated principalrepayment period; a contract cut-off date of September 1993; and, importantly, rescheduling of interestbetween January and October 1994. The second Paris Club rescheduling took place shortly after theapproval of the EFF. It covered maturities falling due between June 1, 1995 and May 31, 1998; inaddition, to close the financing gap -- which widened, as noted above, between the negotiation of the EFFand the Paris Club meeting -- official creditors rescheduled US$750 million of interest payments fallingdue between June 1, 1995 and May 31, 1996. The repayment terms were the same as those for the firstParis Club rescheduling. The private debt rescheduling will cover US$3.3 billion of principal maturitiesfalling due between March 1, 1994 and December 31, 1997. Maturities vary between 10'h and 16 years(counting from March 1994), with creditors who had previously reprofiled their claims benefitting fromshorter maturities.

- 9 -

Table 2: Selected Macroeconomic Indicators

1987-92 1993 1994 1995 1996 1997 1998

(In percent)

Real GDP Growth 0.4 -2.2 -1.2 3.5 5.8 4.2 3.5

-Hydrocarbons 2.4 -0.8 -2.5 1.0 13.6 4.0 0.1

-Non Hydrocarbons -0.6 -2.9 -0.5 4.0 3.4 4.4 4.6

(In percent of GDP)

Gross Investment 29.5 29.2 31.5 33.0 31.5 30.7 29.9

-Central Government 9.5 10.4 10.1 9.6 8.5 7.5 7.2& Public Enterp. 1/

- Other PE and Priv. 20.0 18.8 21.5 23.4 23.0 23.2 22.6

Budget Deficit (-) -2.8 -8.7 -4.4 -1.6 0.3 0.9 2.4

Current Account Deficit 0.7 1.6 -4.3 -7.2 4.4 -3.4 -2.8(-)

Imports 19.8 23.2 28.6 31.1 29.8 28.7 28.3

Exports 21.1 21.9 23.7 25.7 26.9 27.1 27.3

-Hydrocarbons 18.6 19.6 20.5 22.8 23.8 23.8 23.7

Foreign Debt 49.3 51.8 67.7 78.5 78.7 77.6 76.8

(In US$ billions)

Foreign Debt 26.7 25.8 28.4 32.3 34.9 36.5 38.2

(In percent of exports)

Foreign Debt Service 60.2 73.4 41.4 37.2 28.5 32.6 40.9

(In months of imports)

Foreign Rserves 1.2 1.5 2.5 1.8 2.1 2.4 2.4(excluding gold)

I lncludes only public enterpnse uiveslments fmanced through the budget or through thC Restructuring Fund (FA).

15. The World Bank will provide important direct and indirect contributions to the financingplan in 1996 and 1997. As outlined in the CAS, it is proposed that the World Bank increase adjustmentlending to three quarters of total lending in FYs 1996 and 1997, in order to provide quick-disbursingresources appropriate to Algeria's current circumstances and needs. Gross World Bank disbursementsare projected at US$410 million in 1996, of which about half would be direct balance of paymentssupport toward filling the financing gap (assuming one more adjustment loan before the end of calendaryear 1996 -- see the CAS). World Bank support through the SAL also provides comfort to other lenders,

- 10-

including potential SAL parallel financiers such as the EU (see "Cofinancing" below). These otherlenders are also key to filling the financing gap.

Table 3: Financing Plan(US$ billion)

1994 1995 1996 1997 1998

Extraordinary Financing 5.72 6.00 4.78 3.42 0.99Needs

Financing Sources: 5.72 6.00 4.78 3.42 0.99

Rescheduling 4.49 4.78 3.73 2.38 0.56

Paris Club 3.70 3.77 2.81 1.74 0.56

London Club 0.79 1.01 0.92 0.64 0.00

IMF 0.85 0.61 0.53 0.52 0.13

IBRD (BOP) 0.08 0.26 0.20 0.20 0.20

Other Multilateral (BOP) 0.30 0.35 0.32 0.33 0.10

U1. The Government's Adjustment Strategy

16. While the Algerian economy has made important progress since the introduction of theaccelerated reform program in early 1994, full macroeconomic stability has not been achieved and majorstructural impediments remain. Inflation remains high, and the economy remains dependent onhydrocarbon exports. Most notably, an inefficient and monopolistic public sector dominates in industryand finance and accounts for almost half of non-agriculture non-government employment. One in fourworkers in the formal sector is in government service. Property rights remain poorly defined for privatesector operators in agriculture and industry. To address these problems, the Algerian authorities arecommitted to a strong and sustained adjustment effort over several years. The goals of the programremain basically the same as in 1994: (i) achieving and maintaining a stable macroeconomy; (ii)deepening the structural reforms needed in order to accelerate and complete the transition to a marketeconomy; while at the same time, (iii) taking actions to reduce the unacceptably high level ofunemployment (see the CAS) and protect the poor during the transition. The stabilization and adjustmentprogramn supported by the EFF and to be supported by the proposed SAL is outlined above (see Column2 of Table 1). The EFF, the proposed SAL, and other proposed Bank adjustment lending supportcomplementary parts of a coherent program of adjustment. Discussions on the adjustment program haveproceeded in close collaboration with the IMF. (As always, the authorities cannot take on the wholeadjustment agenda under this program. Some measures must logically follow those currently under

- 11 -

implementation; others may not yet have the necessary consensus for successful implementation. Column3 of Table 1 indicates key measures that should be tackled in the next phase of adjustment.)

A. Macroeconomic Program

17. The goals of Algeria's macroeconomic program are ambitious: the achievement of 5percent annual real growth in non-hydrocarbon output over the next three years; and a reduction ofinflation to the rate of its trading partners, achievement of a budget surplus equal to about 2½h percentof GDP (a sensible policy for a country dependent on non-renewable hydrocarbon resources for more thanhalf of budgetary expenditures), and a current account deficit of about 2½h percent of GDP by mid-1998.In addition to the adjustment program outlined below, a range of macroeconomic policies will be usedto achieve these goals. (Macroeconomic conditionality is listed in the policy matrix in Annex D.)

18. Exchange Rate Policy. The Algerian authorities plan to introduce current accountconvertibility of the dinar by end-1997. To this end, virtually all controls on foreign exchange purchasesfor merchandise imports have been lifted. Restrictions on payments for invisibles will be lifted graduallyduring the next two years. In addition, the dinar rate will be more heavily influenced by market forces.An interbank foreign exchange market was introduced at the end of 1995. The receipts of Sonatrach, thenational oil company, in excess of official needs will be sold through this market.

19. Trade Liberalization. Under the stand-by and ERL, imports were substantiallyliberalized. The removal of impediments to access to foreign exchange was the most important action.Algeria did not have an explicit quantitative trade restriction regime, relying instead on foreign exchangeallocation to achieve high rates of protection for domestic producers. Since the beginning of 1995,further trade liberalization measures include the removal of the minimum maturity requirement onextemal borrowing for imports of capital goods (a measure seen as important by the private sector) andthe elimination of professional criteria requirements for importers of medicines, milk, semolina, flour,and wheat. The maximum tariff rate is now 60 percent. Further tariff reductions are envisaged, inaccordance with the results of a study of effective protection now underway in collaboration with theBank. The phased reduction in tariff rates is necessary in the Algerian context in which domesticproducers currently face intense competition from imports as a result of the lifting of exchange controlsthat provided a much higher level of protection than that afforded by tariffs.

20. Price Liberalization. Price controls have been eliminated, except for a limited numberof energy products and pasteurized milk. The global subsidy on energy products has been completelyeliminated, although some cross-subsidization exists among products and among consumer classes.Controls on profit margins have been eliminated, except for medicines and powdered milk. The onlyremaining generalized subsidy (pasteurized milk) will be removed by the end of 1996. The authoritiesare aware of the potential negative impact on the poor of the price increases for basic commodities. Asa result, they plan to further strengthen the social safety net with measures targeting the poor.

21. Fiscal Policy. Much progress has already been achieved on the revenue side, but becauserates are high and because import tariffs will be reduced, further progress will depend on widening thetax base. To that end, some VAT exemptions have been removed this year, and interest income is nowtaxed. The authorities have agreed to review the possibility of reducing the number of VAT rates fromthree to two in consultation with the Fund. However, expenditure measures will be more important inachieving the targeted fiscal surplus. The key tool for expenditure decisions is the ongoing publicexpenditure review (PER). The authorities have used the PER as a guide in the process of expenditure

- 12 -

reallocation, under the overall budget limits set in the context of the EFF. The government investmentprogram for 1996 is in compliance with the recommendations of that report, notably concerningexpenditures on basic health and education. In education, net recruitment will be zero (the educationsystem is overstaffed); and reallocation toward important non-wage expenditures was achieved.(Worldwide experience demonstrates the importance of these expenditures in education outcomes.) Inhealth, total expenditures as a share of GDP were not only protected but slightly increased, with areallocation toward preventive medicine. The authorities have agreed to a 130 percent increase inpreventive medicine expenditures, a 75 percent increase in pharmaceutical expenditures, and will launchpilot subcontracts with the private sector for food and cleaning services in government-run healthfacilities. In addition, adjustments have been made in transportation expenditures, including shelving theconstruction of the Algiers metro and a postponement of lower-priority infrastructure investments witha reallocation to housing. The PER also reviewed personnel expenditures; the recommendations of thereport were taken into account in the measures foreseen in the 1996 budget for reaching the agreedreduction of these expenditures as a share of GDP, in the context of the EFF. Specifically, recruitmentwill be stabilized. By 1998, personnel expenditures are to decline to 8.8 percent of GDP, from 10.5percent in 1993 and about 10 percent currently. The PER, which is an on-going exercise, will be thebasis for a review of the proposed 1997 investment and personnel budgets before release of the secondtranche of the SAL. In all, government expenditures are to fall from about 32 percent of GDP currentlyto about 28½/2 percent by 1998, all in recurrent expenditures. Government investment expenditures willremain roughly constant at about 7'½ percent of GDP.

22. Monetary and Interest Rate Policy. A strict monetary policy is an important componentof the Government's stabilization program, contributing to demand management and a reduction ininflation. At the same time, crowding out by the Government will be reduced, as it makes net paymentsto the banking system, allowing banks to increase non-government credit by 20 to 30 percent per year.Monetary growth is programmed at 13 percent in 1996. Interest rates have been freed. A five percentlimit on the margin between deposit and lending rates of banks was eliminated in December 1995. Mostlending rates are now in the 19-24 percent range.

B. Major Elements of the Adjustment Programn

23. The Algerian authorities' adjustment program supported by the ERL and to be supportedby the SAL has one key aim: to move as quickly as realistically possible to transform the Algerianeconomy into one that is market-based, efficient, and productive. The challenge is clear. The authoritiesrealize that they must use the window of opportunity presented by debt rescheduling to expand output andto reduce as much as is feasible the vulnerability of the economy to external shocks, notably oil priceshocks. By mid-1998, the economy must be ready to face the double impact of an end to reschedulingof debt service and the first principal payments on the US$16 billion of debt rescheduled during theprevious three years. The ICOR must be improved from the double-, and sometimes triple-, digit levelsof the last two decades. Efficiency will be improved through public enterprise reform, including a large-scale program of privatization of small enterprises, and the strengthening of the existing private sector.These measures are necessary if the latter is to be the engine of growth and employment creation.Experience across the world has shown the importance of an efficient and competitive financial sectorfor private sector growth. The Algerian authorities understand this and want to increase the number ofbanks and financial institutions, while strengthening supervision capabilities of the central bank. All ofthese measures will go in parallel with measures designed to improve the social safety net during thetransition (described in Section III below).

- 13 -

24. Privatization. The proposed SAL will support privatization with the following strategy.Privatization will be implemented whenever and wherever possible, while, at the same time, moving thosepublic enterprises that would not yet be candidates for privatization, because of a problem of demandunder current circumstances, to a situation in which they are no longer a drain on the budget and a threatto the integrity of the financial system.

25. Privatization is the officially stated policy of the Algerian government for public sectoractivities in competitive sectors (see the ERL Letter of Development Policy) and probably the onlyeffective means of increasing the efficiency of the Algerian economy. However, in the present securitysituation, the private market for large public enterprises is likely to be limited. Foreign investors havebecome heavily involved in oil and gas development in Algeria in recent years, and this trend is likelyto continue. However, they are not likely to move into other sectors until the security situation improves.Few local private market participants have the resources to become strategic investors in these largeenterprises, and those that do tell us that they would seek foreign expertise; hence, they face the sameproblem as potential foreign buyers. The authorities' strategy in these circumstances for the large publicenterprises is the following: (i) impose hard budget constraints and impose a new management systemto prepare enterprises for eventual privatization (see Public Enterprise Reform below); (ii) identify smallerunits of these enterprises that can be sold off under current demand conditions -- or let the enterprisesthemselves do this as a way of raising funds; (iii) seek private management or minority equityparticipation for some units; and (iv) spin off service activities of the largest public enterprises toemployees.

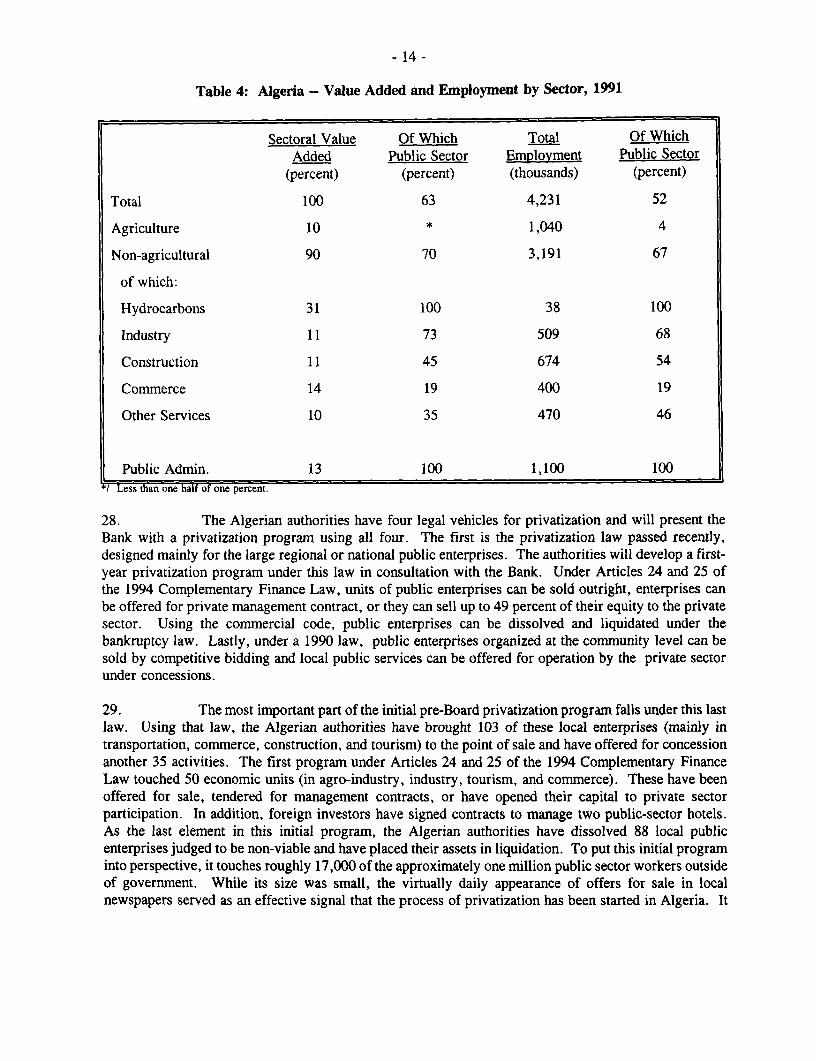

26. At the same time, the SAL will support a large-scale program of privatization of smallenterprises and the private provision of local services, concentrating on activities and sectors where thereis likely to be effective demand for the resources to be privatized, notably small-scale industry,commerce, services, construction, and transport. As shown in the table below, the latter are importantin terms of employment, accounting for more than half of public enterprise employment and 20 percentof total non-agricultural employment (see Table 4). As noted in the CAS, these are also the sectors,besides agriculture, targeted for the strategy of labor-intensive employment creation. (Large, capital-intensive PEs, mostly in industry, will be shedding labor; however, public enterprise employment inindustry accounts for only 8 percent of total employment.)

27. The sources of demand for these privatized entities are three-fold. First, privatebusinessmen in Algeria reported in the context of the recent Private Sector Assessment (PSA) that theystand ready to bid for small-scale enterprises. (A group of visiting Algerian businessmen recentlyreconfirmed their interest in buying small-scale public enterprises.) Second, Algeria has had a thrivinginformal economy, profiting from shortages created by price and exchange controls and productionshortfalls by monopoly PEs. These economic agents have seen their profits shrink with adjustment andare looking for new investments, notably in the service sector. Third, the current management of someof these small PEs is another potential source of demand.

- 14 -

Table 4: Algeria -- Value Added and Employment by Sector, 1991

Sectoral Value Of Which Total Of WhichAdded Public Sector Employment Public Sector

(percent) (percent) (thousands) (percent)

Total 100 63 4,231 52

Agriculture 10 * 1,040 4

Non-agricultural 90 70 3,191 67

of which:

Hydrocarbons 31 100 38 100

Industry 11 73 509 68

Construction 11 45 674 54

Commerce 14 19 400 19

Other Services 10 35 470 46

Public Admin. 13 100 1,100 100/ Less than one half of one percent.

28. The Algerian authorities have four legal vehicles for privatization and will present theBank with a privatization program using all four. The first is the privatization law passed recently,designed mainly for the large regional or national public enterprises. The authorities will develop a first-year privatization program under this law in consultation with the Bank. Under Articles 24 and 25 ofthe 1994 Complementary Finance Law, units of public enterprises can be sold outright, enterprises canbe offered for private management contract, or they can sell up to 49 percent of their equity to the privatesector. Using the commercial code, public enterprises can be dissolved and liquidated under thebankruptcy law. Lastly, under a 1990 law, public enterprises organized at the community level can besold by competitive bidding and local public services can be offered for operation by the private sectorunder concessions.

29. The most important part of the initial pre-Board privatization program falls under this lastlaw. Using that law, the Algerian authorities have brought 103 of these local enterprises (mainly intransportation, commerce, construction, and tourism) to the point of sale and have offered for concessionanother 35 activities. The first program under Articles 24 and 25 of the 1994 Complementary FinanceLaw touched 50 economic units (in agro-industry, industry, tourism, and commerce). These have beenoffered for sale, tendered for management contracts, or have opened their capital to private sectorparticipation. In addition, foreign investors have signed contracts to manage two public-sector hotels.As the last element in this initial program, the Algerian authorities have dissolved 88 local publicenterprises judged to be non-viable and have placed their assets in liquidation. To put this initial programinto perspective, it touches roughly 17,000 of the approximately one million public sector workers outsideof government. While its size was small, the virtually daily appearance of offers for sale in localnewspapers served as an effective signal that the process of privatization has been started in Algeria. It

- 15 -

was designed to gain adherents for the privatization process and to lock in privatization as a prioritygovernment policy.

30. A second privatization program will be established and a portion of it, agreed jointlybetween the Algerian authorities and the Bank, will be brought to the point of sale before the release ofthe second tranche of the SAL. The Algerian authorities are committed to maintaining the momentumof privatization (see the attached Letter of Development Policy). In fact, the second-tranche program islikely to be significantly larger. It will have the same three components as the initial program, but, inaddition, it will include the first privatization program under the new privatization law. The privatizationinstitution was established in March 1996 and is in the process of preparing its first-year program. Inpreparing the second privatization program, the Algerian authorities will also be able to benefit from theirexperience with the initial pre-Board program and can orient sales towards sectors where demand hasbeen demonstrated to be strong.

31. Agricultural Land Tenure. The Algerian Government has announced its intention to selloff state-owned arable land. The land in question was converted from state farms to small collectivefarms or to small individual farms with usufruct rights at the beginning of the adjustment program in1987. However, some of the land went unexploited, partly because of a lack of complementaryresources; and collective operations did not work and were defacto divided into family farms. Still, landtenure is a sensitive political issue, and the process will take time. Contentious issues concerning priorproperty rights must be resolved. As a result, the authorities will work with the Bank on the preparationof legislation setting out the modalities of agricultural land privatization. (Privatization of state-ownedland is already permitted under Algerian law; the question that must be resolved is the process by whichthe land will be privatized.) This legislation will be approved by the Council of Government beforesecond tranche release. (Draft legislation, once approved by the Council of Government, is submittedto the legislative authority.) In the meantime, the Government has put into effect a law returning to theoriginal owners land voluntarily donated to the State during the period of collectivization.

32. Public Enterprise Reform. The strategy of the Algerian authorities is to limit PEs' accessto public resources, through the budget or through bad debts to the banking system made good throughbudget appropriations. Recent reforms in the banking system described below and supported under theERL effectively block access of loss-making enterprises to bank credit. As outlined in the ERL program,the last remaining 23 large non-autonomous public enterprises (EPS) were to be passed to autonomy,blocking routine access to Treasury financing and guarantees. Five were made autonomous before Boardpresentation of the ERL. Under this framework, at autonomy the authorities sign management contractswith the heads of these enterprises requiring them to implement restructuring plans that have received the"non-objection" of the authorities (approval could imply a moral obligation on the part of the governmentto provide finance.) All 23 are now autonomous. In addition, the authorities will abide by theiragreement in the ERL to close the Restructuring Fund, which was used to reduce the commercial bankdebts of PEs as the latter passed to autonomy. If this Fund were to remain operational, there would bea danger of future debt bailouts for PEs, effectively removing the hard budget constraint they wouldotherwise face and eliminating pressure to improve their financial performance.

33. The government has recently adopted a law setting up holding companies to manage PEs.Under this framework, the authorities have agreed that the holdings will: (i) set as their primaryobjective the achievement by these enterprises of positive rates of return; (ii) sanction those that do not,including requiring them to sell off assets; and (iii) prepare enterprises for eventual privatization whendemand conditions permit. In order to reduce the risk that the holdings will delay the privatization

- 16 -

process, the authorities have put in place the following safeguards: (i) the government-level authoritythat oversees the holdings has essentially the same members as the government body that approves theprivatization program; (ii) this authority is represented on the boards of the holdings; and (iii) once anenterprise has been identified as a candidate for privatization, it immediately leaves the holding and falls,by law, under the control of the privatization institution.

34. One potential short-run escape from hard budget constraints for public enterprises is arun-up in inter-enterprise debt. Under the SAL, the authorities will monitor the inter-enterprise debtsof public enterprises.

35. Incentive Framework The Algerian authorities will support the private sector indirectly,through continued improvements in the overall framework for private sector growth, and directly, throughthe enhancement of opportunities for the private sector to carry out activities previously in the publicdomain. Other than improving the overall framework for private sector growth and providingopportunities for the private sector to compete for government concessions and public works, experiencein many countries shows that it is difficult to develop specific government interventions in favor of theprivate sector that actually work. This observation is especially relevant for small and mediumenterprises, which in Algeria describes virtually the entire private sector. However, drawing on the PSAcarried out during the last 12 months, the authorities have developed a program that tries to balancemeasures to improve the general framework for private sector activity with a few major specificinterventions.

36. An important general measure consists of putting the finishing touches on the new legaland regulatory framework for economic activity. This framework has emerged with the support of theWorld Bank, starting with the development of the first adjustment operation in 1989. It includes a newcommercial code and a new investment code. One final but important element remained. Before Boardpresentation, the authorities presented to the Bank the implementing regulations for the competition lawpassed in the context of the ERL. A well-functioning competition law is important during theprivatization process in order to avoid replacing public monopolies by private monopolies. (Poorlydesigned, these regulations could be used to reduce competition.) The Bank, through the Private SectorDevelopment Department, is providing technical assistance to the Algerian authorities to help themimplement the competition monitoring and enforcement system. Other actions seek to remove what theprivate sector reported through the PSA process as important remaining legal and bureaucratic barriersto private sector growth. The authorities are implementing measures to regularize titles to industrial andcommercial land and have legalized leasing and factoring as forms of investment finance.

37. The direct measures for private sector support are mainly related to government contracts.First, in the context of the privatization program discussed above, the authorities are committed to aprogram of private provision of municipal services. Second, the authorities have adopted a series ofreforms designed to increase the participation of the private sector in the construction of public housing,notably by reducing the size of individual contracts. It is projected that, in termns of value added, morethan half of the program of 80 thousand units of public housing planned for 1996 will be produced byprivate contractors. (The use of private contractors in road construction and maintenance is supportedunder the Highways VI project, under implementation.)

38. Reform of the Financial Sector. The strategy for the financial sector is consistent withthat developed with the Algerian authorities under the ERL. As foreseen in the ERL, the next phase offinancial sector reform must include measures to increase competition. A banking system dominated by

- 17 -

five publicly-owned banks cannot generate the competition necessary to efficiently mobilize deposits orto provide the services needed by an expanding private sector. The interbank market for foreignexchange foreseen under the EFF and the bond market to be developed in collaboration with the Bankalso necessitate real competition to function well. In parallel, now is the time to start developing the basisfor new non-bank financial institutions, including a stock market.

39. Restructuring of existing banks will go on as planned under the ERL. The authoritieshave agreed with the Bank on the capital infusions necessary for the five banks in order for them to meetthe agreed interim capital-asset ratio of four percent. Recapitalization at the agreed level was a pre-Boardrequirement, as was signature and implementation of the agreed management contracts. Under themanagement contracts, the managers have the responsibility to respect the capital adequacy guidelines.As a result, they have no incentive to increase bank exposure to loss-making autonomous publicenterprises. Recapitalization was not a major drain on the government budget because the authorities hadalready cleaned up the balance sheets of these banks, using the Restructuring Fund to exchangegovernment bonds for the bad debts of PEs. More than 50 percent of the assets of the five governmentbanks consists of claims on the Algerian Treasury.

40. Increased competition in the banking sector will be encouraged under the SAL in thefollowing ways. First, the new management contracts will encourage some competition. Second, a studyis currently underway to identify the means to effectively privatize the management of one existing bank.Presentation of a draft plan to achieve this aim was a pre-Board condition. In informal contacts betweencommercial banks outside of Algeria and the IFC, many banking groups have expressed an interest inentering the Algerian market but are discouraged by the security situation. Private groups within Algeriahave explored the possibility of opening new banks but also have been discouraged by the securitysituation. They see the need to bring in foreign financial expertise, which will be difficult until thissituation improves. However, the IFC has given its assurance that it will continue to actively seek newentrants into the Algerian financial markets (see CAS). One new private bank has been approved (it plansto act mainly as an investment bank). Its entry into the Algerian market is a positive development.

41. Improvements in the supervision and regulation capabilities of the central bank willcontinue under the proposed SAL. Actions include the setting and enforcing of effective limits on bankoverdrafts and of accounting norms and regulations covering foreign exchange transactions andtransactions in governmnent securities.

42. Measures to introduce new markets concentrate in the first instance on the governmentsecurities market. The structure of new issues of government securities has been designed along the linessuggested in the Bank's study of Algerian capital markets. This design concentrates issues on a fewmaturity dates, allowing the creation of deeper secondary markets. The SAL will support the processof putting both the primary and secondary markets into operation, including the development of anauction system, the requirements for licensing of securities dealers, and the introduction of a clearingsystem. The SAL also supports the first steps toward the development of a stock market, including theadoption of key amendments to the stock market law, authorizing an over-the-counter secondary marketin Treasury securities, authorizing stock exchange members to trade other financial securities, andrelieving exchange members of the responsibility of accounting for the source of their clients' funds.Lastly, an Exchange Commission will be established and staffed.

- 18 -

III. Algeria's Social Safety Net Strategy

43. The Algerian authorities realize that a workable social safety net is an importantaccompaniment to their adjustment program, to help the poor who might be adversely affected byadjustment and to engender popular support for the program. In late 1994, they replaced a cash paymentscheme that could not be well-targeted and had become too expensive by two new programs. (The cashpayment system itself was adopted to compensate the poor for the reduction of generalized food subsidiesas a part of past adjustment efforts.) The first program (AFS) provides assistance to the elderly andhandicapped and their dependents. It targets those who are missed by other social security programs:the elderly without pensions or other major sources of income and the handicapped who are not 100percent incapacitated (the severely handicapped already receive social assistance) but who are unable towork and have little or no savings. The second program (PAIG) provides employment, normally oflimited duration, on a self-targeted basis to those who are willing to work for half the minimum wage.

44. The other pressing social issue for the Algerian authorities is the 25 percent rate ofunemployment, mainly among youth. (While the problem must be addressed in the interest of socialcohesion, it must be noted that the link between unemployment and poverty is not clear; evidence fromother countries, including those with high unemployment rates, shows that most of those classed asunemployed come from families with incomes above the poverty line.) While the reforms underway aredesigned to generate a quick supply response, mainly in labor-intensive agriculture and construction, thereis a risk that unemployment could remain at or near its current level in the short run. To minimize thisrisk, the Algerian government, with Bank support, has put together a program of public works and isdesigning a social fund. (See the accompanying Social Safety Support Project.) In addition, the Algeriangovernment has introduced a scheme of protection for workers laid off for economic reasons.

45. The three recent programs -- the unemployment insurance scheme, the AFS, and thePAIG -- were brought to full operation in a very short period; the Algerian authorities are to becongratulated in this regard. The successful on-the-ground implementation of these social safety netprograms in a difficult security setting is -- along with (i) the public expenditure program and (ii) thepublic sector reform, privatization and private sector development components -- a key up-front policyaction justifying support under the proposed SAL. However, as with most safety net schemes, it couldbe improved. Under the SAL, the authorities will take measures to strengthen these programs. Theschemes are described below, along with potential measures to improve their effectiveness.

46. The program of aid to the elderly and handicapped (AFS) now covers 430,000 heads ofhouseholds, or about 900,000 people in all. Among the heads of benefitting households, 87 percent areelderly and 13 percent handicapped. Each beneficiary receives 600 dinars per month, plus 120 dinarsper month for each dependent up to a maximum of three. Based on a study of the program during itsinitial few months of operation, it could be improved and extended as follows. Under the SAL, theauthorities have agreed to: (i) make payments monthly, rather than quarterly; and (ii) integrate the AFSwith other existing social programs to reduce the risk of overlaps.

47. The program providing short-term emplovment (PAIG) has provided jobs of relativelyshort duration to 420,000 participants at more than 16,000 work sites. In a review undertaken by theBank, a number of areas for possible improvement were identified. The program's key feature is its self-targeting to the able-bodied poor: it is designed to benefit only those willing to work for half theminimum wage. However, some local authorities (the program is run at the local level) pay for a fullday when the participants work only half the day. As a result, the program loses its self-targeting feature

- 19 -

and could attract participants from existing or potential new jobs in the private sector. Second, the worksites do not appear to have been selected on the basis of knowledge concerning the geographical locationof the poorest groups. Third, many of the activities appear to have an unnecessarily low rate of retum.While efficiency is not the major criterion for measuring the success of this program, it appears thatefficiency could be improved at little additional cost. In the context of the SAL, the authorities haveagreed to: (i) demand (and verify) a full day's work for a full day's pay; (ii) target work sites moreclosely to geographical areas identified as having a high concentration of poor people; and (iii) setefficiency norms for the local authorities to follow and verify their use.

48. The program of protection of workers laid off for economic reasons is contributory.Employers and employees pay a combined payroll tax of four percent into a fund. In addition,enterprises that lay off workers pay an "entry fee" for each laid off worker proportional to that worker'stenure with the firm. An enterprise that would like access to the fund must prepare a restructuring planthat specifies employment compression via retrenchment or early retirement. The benefit level andduration is based on salary history and employment duration, with an upper bound equal to three timesthe minimum wage. The benefit period is a minimum of one year and a maximum of three years, andthe benefits decline over time. About 48,000 workers, mainly in construction, are eligible for financialsupport (36,000) or have taken early retirement (12,000) under the program. While the program has beensuccessfully implemented, it can be improved by: (i) the close tracking of detailed accounts of revenuesand expenditures; and (ii) the establishment of guidelines for investing the funds that accumulate as areserve. It is possible that the cost of the scheme to both firms and contributing workers can be loweredover time, if the Fund begins to accumulate large reserves.

IV. The Proposed Loan

A. Program to be Supported and Link to the Country Assistance Strategy

49. This proposal has been prepared in response to a government request, going back to early1994, for support for its intensified adjustment efforts. The proposed SAL will be a continuation of thesupport provided under ERL, recognizing the successful policy performance of the Algerian authoritiesunder that loan and the vital program of medium-term structural adjustment, described above, that theyhave already launched. The proposed SAL and the already approved EFF are complementary; both havebeen prepared in close collaboration between the Bretton Woods institutions. With regard to themacroeconomic framework, the Bank will support improvements in the composition of publicexpenditures in the context of overall ceilings established with the Fund. Privatization and other measuresto improve enterprise and financial market efficiency, supported by the Bank, will benefit frommacroeconomic stability established in the context of the EFF. Improvements in the social safety netsupported by the Bank will underpin the cuts in government expenditures, notably generalized subsidies,necessary under the EFF for the reestablishment of monetary and balance of payments equilibrium.

50. The relationship between the proposed loan and the CAS is clear. The objectives of theSAL are the three key objectives enunciated in the attached CAS. Support under the SAL will help theauthorities: (i) stimulate private sector-led growth; (ii) protect the poor during the transition to a market-based economy; and (iii) enhance the country's ability to mobilize the external resources necessary tobridge the gap to balance of payments viability. As noted in the CAS, the SAL is a central element ofthe Bank's strategy of assistance for Algeria.

- 20 -

51. The elements of Algeria's stabilization and adjustment program to be supported under theSAL are outlined in the policy matrix attached to the Letter of Development Policy (Annex D). Detailsof the specific elements to be supported under the SAL are presented above in the sections outlining theAlgerian macroeconomic, structural adjustment, and social safety net programs and are reiterated in thegovernment's Letter of Development Policy. Also annexed to the Letter of Development Policy is a setof monitorable indicators to be tracked during the life of the SAL.

B. Poverty Impact

52. While the exact impact on poverty of the Algerian program to be supported under theSAL in Algeria is difficult to quantify, its overall qualitative impact will be positive. The Algerianauthorities have already put in place a functioning social safety net designed to limit the impact ofadjustment on the poor (notably as a result of the elimination of generalized food subsidies). Theseprograms, the AFS and the PAIG, were described above. Under the SAL, the Algerian authorities willfurther improve the design and management of these programs, in consultation with the Bank. Inaddition, the program is designed to provide information to improve the targeting of future socialassistance. During the period of the SAL, the Bank will prepare, jointly with the Algerian authorities,the first Poverty Assessment for Algeria. The assessment will be based partly on data arising from aLiving Standards Measurement Survey, now underway, financed in part under a Bank technical assistanceloan. The Algerian authorities are also conscious of the need to assist those who are not poor but whomight suffer as a result of the adjustment effort, notably PE workers laid off for economic reasons. Theyhave put in place a program to provide financial assistance to these workers, described above in thediscussion of the social safety net.

53. In addition, SAL conditionality includes up-front measures to protect the level andimprove the efficiency of key social expenditures. As noted above, non-wage recurrent educationexpenditures were increased, as were expenditures on basic preventive health care.

C. Negotiations, Effectiveness, and Proposed Tranche Conditionality

54. The are no conditions of effectiveness separate from conditions for Board presentation.The program was designed, in the spirit of the CAS strategy, to require significant pre-Board actions fortwo reasons: (i) to demonstrate the authorities' commitment to the program; and (ii) to decrease to theextent possible the risk of policy reversal (see the section on risks below). Second tranche conditionsconcentrate only on major actions that require significant advance preparation.

55. The following were the key actions for Board presentation:

Macroeconomic and Public Finance Framework

o Submission to the Bank of a government investment program and plan for recurrent goverrnmentexpenditures in 1996 in the health, education, transportation, and housing sectors satisfactory tothe Bank and in accordance with the PER.

o Stabilization of recruitment for the civil service, in accordance with the EFF. (Note: the PERwas the basis for the agreement with the Fund in the context of the EFF.)

- 21 -

Support for Public Sector Reform and for Private Sector Development

o Promulgation of a privatization law.