Working Paper 1 - Nommon · Working Paper 1 Performance of the ... MAIN SIMILARITIES BETWEEN KPAS...

93

Working Paper 1 Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report January 2014

Transcript of Working Paper 1 - Nommon · Working Paper 1 Performance of the ... MAIN SIMILARITIES BETWEEN KPAS...

Working Paper 1

Performance of the Current Airport Slot

Allocation Process and Stakeholder Analysis

Report

January 2014

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 2 of 93

Authors

Advanced Logistics Group, Indra-Europraxis

Andrea Ranieri

Núria Alsina

Università degli Studi di Trieste

Tatjana Bolic

Lorenzo Castelli

Nommon Solutions and Technologies

Ricardo Herranz

This work is co-financed by EUROCONTROL acting on behalf of the SESAR Joint Undertaking (the

SJU) and the European Union as part of Work Package E in the SESAR Programme. Opinions

expressed in this work reflect the authors' views only and EUROCONTROL and/or the SJU shall not

be considered liable for them or for any use that may be made of the information contained herein.

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 3 of 93

Table of contents

EXECUTIVE SUMMARY ............................................................................................................................. 5

1. INTRODUCTION ................................................................................................................................... 6

1.1 SCOPE AND OBJECTIVES ..............................................................................................................................6

1.2 STRUCTURE OF THE DOCUMENT ...................................................................................................................6

1.3 ACRONYMS AND TERMINOLOGY ...................................................................................................................7

2. THE CURRENT AIRPORT SLOT ALLOCATION MECHANISM ...................................................................... 8

2.1 BACKGROUND ...........................................................................................................................................8

2.1 ANALYSIS OF THE CURRENT REGULATION ........................................................................................................9

2.2.1 Definition of Slot ........................................................................................................................................... 10

2.2.2 Conditions for airport coordination .............................................................................................................. 11

2.2.3 Appointment of slot coordinator .................................................................................................................. 12

2.2.4 Determination of capacity and associated coordination parameters .......................................................... 12

2.2.5 Primary airport slot allocation according to grandfathering and use-it-or-lose-it rules ............................... 13

2.2.6 Slot Returns ................................................................................................................................................... 17

2.2.7 Slot exchanges and transfers ........................................................................................................................ 17

2.2.8 Slot trading .................................................................................................................................................... 19

2.3 COORDINATION AT EUROPEAN AND WORLDWIDE LEVEL ................................................................................ 20

2.3.1 Airport coordinators associations ................................................................................................................. 21

2.3.2 The IATA airport slot allocation activities ..................................................................................................... 23

2.4 CURRENT SLOT EXCHANGES: EXPERIENCES OF SECONDARY TRADING ................................................................ 24

2.4.1 Slot mobility .................................................................................................................................................. 24

2.4.2 Experiences of secondary trading ................................................................................................................. 24

2.5 SYSTEMS ADOPTED IN OTHER REGIONS ....................................................................................................... 26

2.5.1 USA ................................................................................................................................................................ 26

2.5.2 Australia ........................................................................................................................................................ 28

3. PERFORMANCE OF THE CURRENT SYSTEM AND PERSPECTIVES FOR REFORM ...................................... 30

3.1 PERSPECTIVES FOR THE REFORM OF THE SLOT SYSTEM. MARKET-BASED APPROACHES ........................................ 30

3.1.1 Market-based mechanisms for primary allocation of capacity .................................................................... 30

3.1.2 Secondary slot trading .................................................................................................................................. 32

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 4 of 93

3.2 THE WAY FORWARD PROPOSED BY THE EC .................................................................................................. 33

3.3 TOWARDS A COMPREHENSIVE PERFORMANCE FRAMEWORK FOR THE ASSESSMENT OF AIRPORT SLOT ALLOCATION

MECHANISMS ......................................................................................................................................... 35

3.3.1 Concepts and definitions .............................................................................................................................. 35

3.3.2 Required Properties ...................................................................................................................................... 36

3.3.3 Preliminary proposal for a comprehensive performance framework .......................................................... 36

4. ANALYSIS OF STAKEHOLDERS............................................................................................................. 45

4.1 ROLE OF STAKEHOLDERS .......................................................................................................................... 45

4.1.1 Regulators ..................................................................................................................................................... 48

4.1.2 Coordinators ................................................................................................................................................. 51

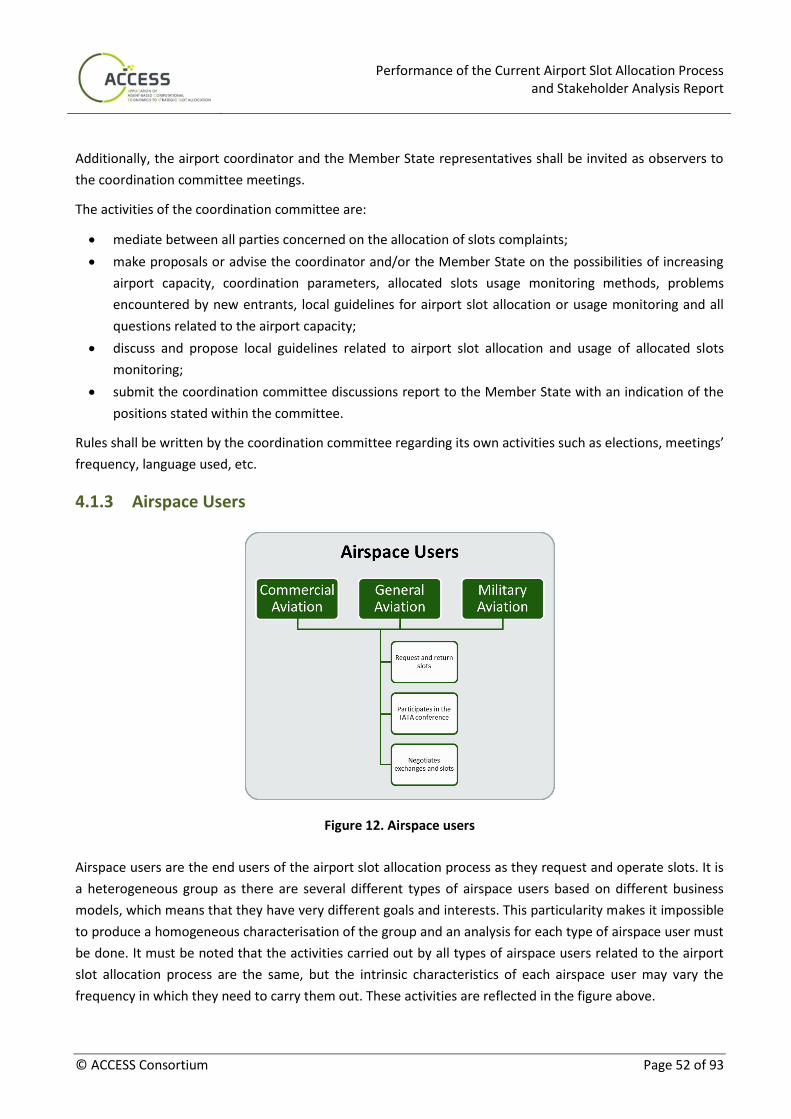

4.1.3 Airspace Users ............................................................................................................................................... 52

4.1.4 Airport Operators.......................................................................................................................................... 58

4.1.5 Passengers .................................................................................................................................................... 59

4.2 STAKEHOLDERS' PREFERENCE AND POSITION REGARDING MARKED-BASED MECHANISMS ..................................... 60

4.2.1 Airspace Users ............................................................................................................................................... 60

4.2.2 Airport Operators.......................................................................................................................................... 63

4.2.3 Coordinators ................................................................................................................................................. 65

4.2.4 Regulators ..................................................................................................................................................... 66

5. CONCLUSIONS ................................................................................................................................... 67

ANNEX I. REFERENCES ............................................................................................................................ 70

ANNEX II. EUROPEAN AIRPORT COORDINATORS ..................................................................................... 73

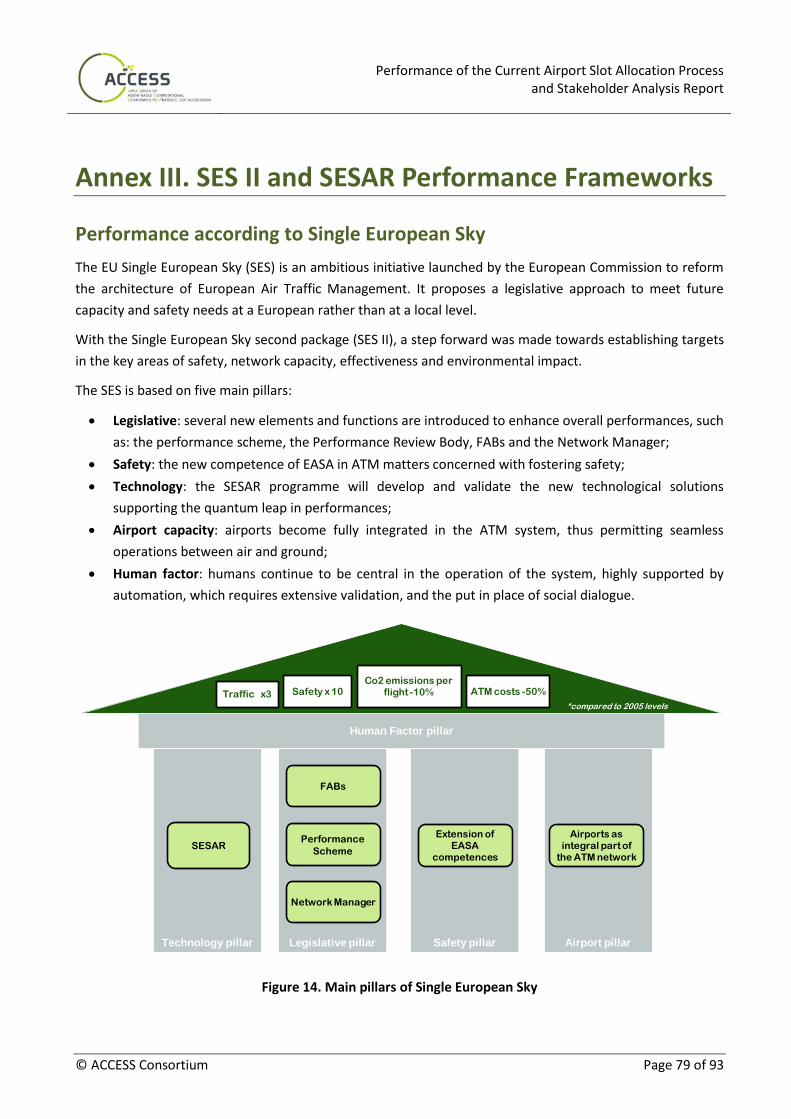

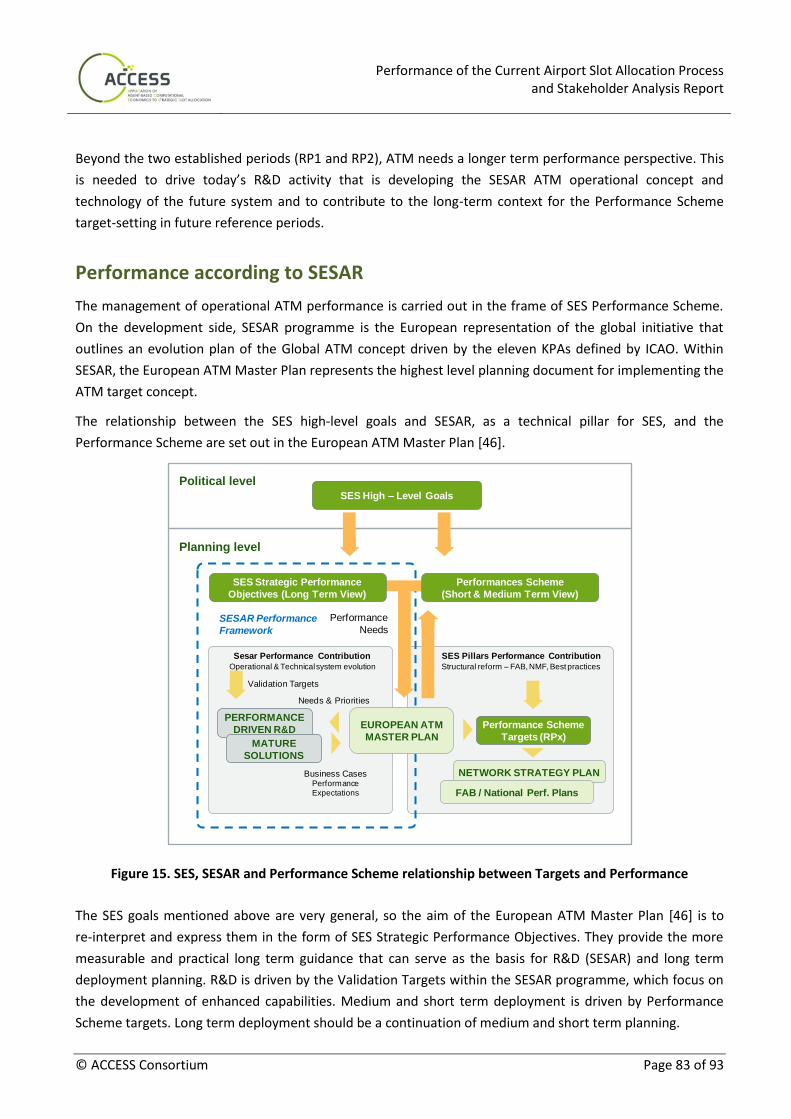

ANNEX III. SES II AND SESAR PERFORMANCE FRAMEWORKS ................................................................... 79

PERFORMANCE ACCORDING TO SINGLE EUROPEAN SKY ............................................................................................ 79

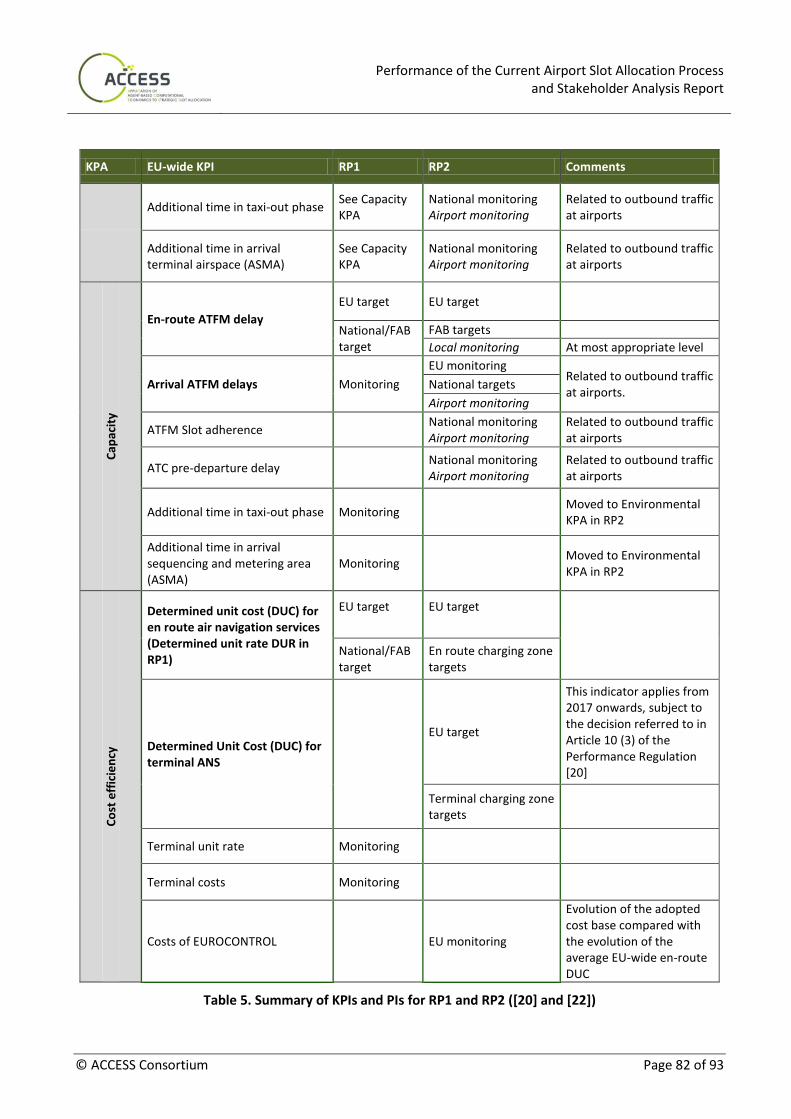

THE SES II PERFORMANCE SCHEME ...................................................................................................................... 80

PERFORMANCE ACCORDING TO SESAR .................................................................................................................. 83

MAIN SIMILARITIES BETWEEN KPAS AND KPIS ........................................................................................................ 86

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 5 of 93

Executive summary

Among the different modes of transport, air transport has experienced the fastest growth over the last

years. Most major airports in Europe suffer of capacity shortage due to several reasons. As building new

facilities is not always possible, the expansion of air service relies upon improvements in ATC technology and

implementation of new procedures. These improvements have provided great increases in capacity, but this

is still insufficient to cope with air traffic demand at the most congested airports, and it thus has to be

accompanied by other measures for the management of scarce capacity. The European approach to the

strategic allocation of airport capacity is an administrative slot allocation system inspired by IATA Guidelines.

Airport slot allocation at EU airports is governed globally by the IATA Worldwide Slot Guidelines and within

the European Union by Regulation 95/93 and its respective amendments Regulation 894/2002, Regulation

1554/2003, Regulation 793/2004 and Regulation 545/2009. A “slot” is defined as “the permission given by a

coordinator in accordance with this Regulation to use the full range of airport infrastructure necessary to

operate an air service at a coordinated airport on a specific date and time for the purpose of landing or

take-off as allocated by a coordinator in accordance with this Regulation”. The coordinators are responsible

for assigning slots applying the regulation. Coordinators and airspace users meet at biannual IATA

conferences, where bilateral negotiations are carried out and slot assignment is negotiated. The main

criteria applied for airport slot allocation is historical precedence: airlines can earn historic rights (the

so-called grandfather rights) to a series of slots, provided they operate the slots as allocated by the

coordinator at least 80% of the time during a season (use-it-or-lose-it rule, also called 80-20 rule).

The European Commission proposed a way forward with regulation proposal COM 2011/827. This proposal

introduces deep changes in the current system: secondary trading is explicitly accepted, use-it-or-lose-it rule

is tightened, rules are reformed to help new entrants access the market at congested airports and rules on

the independence of the coordinator are also tightened.

The stakeholders involved in airport slot allocation can be classified into four groups: regulators, airport

coordinators, airspace users and airport operators. Each of them plays a role in the system and has its own

interests. Airspace users group is quite heterogeneous, since it is composed by several types of stakeholders,

with different strategies. Stakeholder’s preference and positioning regarding market-based mechanisms

depend on their interests and business strategies. Their positioning ranges from being satisfied with the

current regulation and thus not supporting any changes, to favouring the change of several principles

(e.g. increase the use-it-or-lose-it rule). The proposal that arouses more consensus is the regulation of

secondary slot trading.

A comprehensive assessment of different potential reforms of the slot system should develop a better

understanding of the economic value of each slot, evaluate the effects of such reforms along different

dimensions (economic efficiency; equity; access and competition; flexibility; resilience and adaptability;

interoperability; capacity and delay) and analyse their impact on the different stakeholders involved.

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 6 of 93

1. Introduction

1.1 Scope and objectives

The main objective of this document is to establish a solid baseline regarding the performance of the current

airport slot allocation system and the characterisation of the stakeholders involved.

The document is expected to meet a number of lower level objectives:

1. To perform a review of the current slot allocation process, including the observed practices and

legislative framework set by the Regulation (EEC) 95/93, as amended by Regulation (EC) 793/2004.

2. To identify the potential for improvement offered by the EC legislative proposal COM/2011/0827:

- slot trading among airlines anywhere in the EU in a transparent way;

- access of new entrants to congested airports;

- rules requiring airlines to demonstrate slot usage;

- independence of the coordinator and transparency on slots transactions;

- information flows between stakeholders in order to inform decision making;

3. To provide a framework for the design and development of market-based mechanisms for airport slot

allocation, in terms of:

- roles and responsibilities;

- rules, principles and challenges;

- expectations and positions from stakeholders.

1.2 Structure of the document

The document is structured as follows:

Section 2 describes the current airport slot allocation mechanism. It first describes and analyses the

applicable European regulation within the framework of the universally applicable IATA guidelines,

evaluates the worldwide scope of the problem, compiles and analyses examples of current slot

exchanges, and analyses airport slot allocation systems adopted in other regions of the world.

Section 3 evaluates the performance of the current system, based on the description of its advantages

and drawbacks in relevant performance areas: economic efficiency; equity and distributional issues;

access and competition, flexibility, resilience and adaptability; interoperability; and capacity and delay.

It also describes the way forward proposed by the European Commission on airport slot allocation.

Section 4 analyses the stakeholders involved in the airport slot allocation process, describing their

roles and responsibilities as well as their preferences and position regarding the implementation of

market-based mechanisms.

Section 5 includes a synthesis of the main findings and the conclusions.

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 7 of 93

1.3 Acronyms and terminology

Term Definition

AENA Aeropuertos Españoles y Navegación Aérea

ACI Airports Council International

AEA Association of European Airlines

AER Assembly of European Regions

ALG Advanced Logistic Group

ATC Air Traffic Control

ATM Air Traffic Management

ATMs Air Transport Movements

CFMU Central Flow Management Unit

E-ATMS European Air Traffic Management System

EBAA European Business Aviation Association

EC European Commission

EEC European Economic Community

ERA European Regions Airline Association

EU European Union

EUACA European Union of Airport Coordinators Association

FAA Federal Aviation Association

GFR Grandfather rights

IATA International Air Transport Association

IBAC International Business Aviation Council

IFR Instrument Flight Rules

IMC Instrument Meteorological Conditions

KPA Key Performance Area

NOTAM Notice to Airmen

PSO Public Service Obligation

SARS Severe Acute Respiratory Syndrome

SC Slot Conference

SESAR Single European Sky ATM Research Programme

SJU SESAR Joint Undertaking (Agency of the European Commission)

UK United Kingdom

VFR Visual Flight Rules

WSG IATA Worldwide Slot Guidelines

Table 1. Acronyms and terminology

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 8 of 93

2. The current airport slot allocation mechanism

Over the past decades, the overwhelming increase in air transport demand, in conjunction with severe

political, physical and institutional constraints for providing sufficient airport capacity, have resulted in a

serious gap between the demand and the available capacity at certain airports. A recent EUROCONTROL

study [18] foresees around 1.9 million of un-accommodated flights in Europe in 2035, accounting for 12% of

the demand.

Many major airports in Europe suffer from capacity shortage due to several reasons. Most European airports

are still publicly controlled, which means they are dependent on political decisions and tight budgets. But

even where such constraints apply less (as in the UK), expansion is restricted due to environmental

limitations and other planning controls. Building new facilities, such as runways, is not an easy task. As a

consequence, the expansion of air services relies mainly upon improvements in ATC technology and the

development and implementation of new procedures to increase traffic in the already existing facilities. In

the last decades, these improvements have provided great increases in capacity but, nevertheless, major

airports are operating at, or close to, declared capacity for much of the day.

To respond to these needs, two main solutions can be adopted: to apply demand/congestion management

or to implement capacity enhancement programs. Due to the complications for expanding existing airport

capacity, demand management solutions have recently received much attention from researchers, operators

and policy makers.

Airport demand management includes a wide spectrum of measures, ranging from pure administrative

procedures, such as slot control according to regulations, to economic, market-based and hybrid

instruments, such as congestion-based pricing, slot trading and auctions. Even though different studies have

shown that administrative slot controls lead to inefficiencies and hinder competition [11], [40], slot control

and schedule coordination have been so far the dominant approach in Europe.

2.1 Background

Two approaches predominate for the allocation of this capacity:

Airport slot allocation: all the airlines that intend to schedule a flight movement to and from a

coordinated airport need to be assigned an airport slot for this purpose. Most of the world outside the

US allocates capacity according to a set of rules based on the guidelines set down by IATA. These

guidelines are based on the recognition of the historical use of slots; an airline has the right to a slot if

it has already made use of that slot during the preceding equivalent season. This historical precedence

is commonly known as grandfather rights.

Congestion: in the US, in contrast, the IATA-based system is not applied for most of the airports.

Schedules are allocated on a first-come, first-served basis, and expected delays are calculated and

taken into account by airlines in order to operate at the busiest airports. Aircraft wait to land or

take-off in queues, rationing the overall demand. Although this is the general picture of the US

airports, there are four which are an exception: Ronald Reagan Washington National airport and three

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 9 of 93

New York area airports (JFK, Newark, and La Guardia). At these airports the FAA prescribes the hourly

number of flight operations and departure and arrival slots are assigned, loosely applying the IATA

guidelines: the grandfather rule applies, but there is much that the national regulation imposes on the

airport slot allocation process that is different. Slots can be bought and sold only at one airport; at the

other three, only slot transfers between airlines are allowed.

A third possible rationing mechanism suggested in the literature, but with limited real application, is

congestion pricing. Most proposals in this sense have involved setting an additional per-flight surcharge for

operations at certain times of day. However, congestion charging is of difficult to implementation in practice.

First, there are legal obstacles to such surcharges, since according to ICAO, aeronautical charges by airport

operators must be set on a cost recovery basis. Conceptually one should get congestion charges to bring the

level of scheduled operations in line with capacity, but this would require the calculation ex-ante of the

relationship between prices and level of operations, which is a very difficult problem. Furthermore,

surcharges would have the effect of shifting demand from one time window to another, making the price

setting problem multi-dimensional.

2.1 Analysis of the current regulation

Airport slot allocation at EU airports is governed by Regulation 95/93 [12] and its respective amendments

Regulation 894/2002, Regulation 1554/2003, Regulation 793/2004 and Regulation 545/2009 [23], [24], [25],

[26], which retain and develop the principles of the IATA slot allocation process. There are also national or

local laws in some countries imposing the rules that are sometimes more stringent.

From the four amendments of Regulation 95/93, only one of them (Regulation 793/2004) is a full revision of

the regulation intended as a first step in a comprehensive revision process and focusing on a number of

technical issues, notably:

keep abreast of developments, in particular with respect to new entrants and market access issues;

strengthen the Regulation 95/93 to ensure the fullest and most flexible use of limited capacity at

congested airports;

clarify a number of its provisions;

follow the international terminology using the terms ‘schedules facilitated airport’ and ‘coordinated

airport’ instead of ‘coordinated airport’ and ‘fully-coordinated airport’ respectively;

specify in detail the role of the schedules facilitator and the coordination committee; and

encourage regular operations at coordinated airports relating grandfather rights to series of slots.

The three other amendments to the regulation refer to mitigation actions taken due to specific events that

impacted air transport operations:

Regulation 894/2002: the terrorist attacks of 11th September 2001 in the United States and the

political developments that followed those events seriously affected the operations of air carriers and

resulted in a significant drop in demand during the remainder of the summer 2001 and winter

2001/2002 scheduling seasons. The decision taken to mitigate the impact of these events on the air

carriers was to constrain coordinators to accept that air carriers were entitled to the same series of

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 10 of 93

slots during the summer scheduling season 2002 and the winter scheduling season 2002/2003 as the

ones allocated to them on the date of 11 September 2001 for the summer scheduling season 2001

and the winter scheduling season 2001/2002 respectively, without considering the utilisation rate.

Regulation 1554/2003: the war launched in March 2003 against Iraq and the political developments

that followed, as well as the outbreak of the Severe Acute Respiratory Syndrome (SARS), seriously

affected the operations of air carriers and triggered a significant reduction in demand in the beginning

of the summer 2003 scheduling season. The decision taken to mitigate the impact of these events was

to constrain coordinators to accept that air carriers were entitled to the same series of slots during the

summer 2004 scheduling season as the ones allocated to them during the summer 2003 scheduling

season without considering the utilisation rate.

Regulation 545/2009: the global economic and financial crisis was seriously affecting the activities of

air carriers and led to a significant reduction in air traffic over the winter 2008/2009 scheduling period

and the summer 2009 scheduling period. The decision taken to mitigate the impact of these events on

the air carriers’ activities was to constrain coordinators to accept that air carriers were entitled to the

same series of slots for the summer 2010 scheduling period as the ones allocated to them at the start

of the summer 2009 scheduling period without considering the utilisation rate.

Although the European Regulation is broadly based on the IATA guidelines, the EC Slot Regulation contains

some specific measures to promote non-discriminatory behaviour, support protection for routes serving

Public Service Obligations (PSO) and encourage new entrants.

2.2.1 Definition of ‘slot’

The first approach followed by the European Commission in Regulation 95/93 regarding the definition of

slot, following the IATA guidelines at the time, was “the scheduled time of arrival or departure available or

allocated to an aircraft movement on a specific date at an airport coordinated under the terms of this

Regulation”. This definition opened issues regarding the ownership of slots, as three separate parties laid

claim to these property rights: the state, the airport operators and the airlines. These issues ended up with a

modification of the slot definition in the amendment of Regulation 95/93 in 2004, Regulation 793/2004.

‘Slot’ is defined in the current EC Regulation as “the permission given by a coordinator in accordance with

this Regulation to use the full range of airport infrastructure necessary to operate an air service at a

coordinated airport on a specific date and time for the purpose of landing or take-off as allocated by a

coordinator in accordance with this Regulation”.

Such definition is fully in line with the one provided by IATA in [34]: “a permission given by a coordinator for

a planned operation to use the full range of airport infrastructure necessary to arrive or depart at a Level 3

airport on a specific date and time”.

It must be noted that, according to these two definitions, the runway does not constitute the only

capacity-constrained resource: the definitions include the full range of airport infrastructure, i.e. runway,

terminal, apron, gates, night quota, etc. Practically a slot is a temporal permit to perform operations: the slot

time defines the moment of leaving or arriving at the aircraft stand (in-block, off-block) and is usually equal

to the layover based on the published flight times.

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 11 of 93

2.2.2 Conditions for airport coordination

Both the EC Slot Regulation and the IATA Worldwide Slot Guidance (WSG) define different levels of airport

coordination. According to the EC Slot regulation, the levels of airport coordination are:

Coordinated airport: any airport where, in order to land or take off, it is necessary for an air carrier or

any other aircraft operator to have been allocated a slot by a coordinator, with the exception of State

flights, emergency landings and humanitarian flights;

Schedules facilitated airport: an airport where there is potential for congestion at some periods of the

day, week or year which is amenable to resolution by voluntary cooperation between air carriers and

where a schedules facilitator has been appointed to facilitate the operations of air carriers operating

services or intending to operate services at that airport.

In the IATA WSG, the different categories of airport coordination are identified with 3 levels, which are

aligned with the two ones mentioned above, level 3 being coordinated airports and level 2 facilitated

airports. IATA WSG also adds the category of non-coordinated airports (Level 1) for completeness.

According to the EC Slot Regulation, the Member States are responsible for designating airports as schedules

facilitated or coordinated. The only conditions Member States have to meet in order to indicate one airport

as schedules facilitated or coordinated is to guarantee the principles of transparency, neutrality and

non-discrimination in the discussions conducted between the schedules facilitator and the aircraft operators.

The designation of an airport as coordinated or schedules facilitated shall be preceded by a capacity analysis

and a consultation on the capacity situation with the airport managing body, the air carriers using the airport

regularly, their representative organisations, representatives of general aviation using the airport regularly,

and the air traffic control authorities. A thorough capacity analysis shall be carried out at any airport by the

airport managing body or any other competent body in order to determine any shortfall in capacity, taking

into account environmental constraints, when one of the following situations occur:

the Member State considers it necessary;

within 6 months following a request from air carriers representing more than 50% of the operations at

the airport considering that the airport capacity is insufficient;

within 6 months following a request from the airport managing body considering that the airport

capacity is insufficient;

within 6 months upon request from the Commission, especially where an airport is only accessible for

air carriers that have been allocated slots or where air carriers (in particular new entrants) have

serious problems in securing landing and take-off possibilities.

This analysis shall consider the possibility of overcoming such shortfall through new or modified

infrastructure, operational changes or any other change.

An airport may also be designated as coordinated in exceptional circumstances where capacity problems

occur for at least one scheduling period, such that significant delays cannot be avoided and it is impossible to

resolve the shortfall in the short term.

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 12 of 93

2.2.3 Appointment of slot coordinator

According to the EC Slot regulation, a schedules facilitator or a coordinator must be a qualified natural or

legal person, acting in an independent, neutral, non-discriminatory and transparent manner. Each country

has an appointed responsible member with the airport coordination role. The Member State responsible for

a schedules facilitated or coordinated airport shall ensure the independence of the coordinator at a

coordinated airport by separating the coordinator functionally from any single interested party. The system

of financing the coordinators’ activities shall be such as to guarantee the coordinator’s independent status.

Both coordinators and schedules facilitators shall participate in international scheduling conferences of air

carries permitted by the Community law.

The Airport Slot Coordinator’s role is three-fold:

to prepare the allocation of airport slots to aircraft operators wanting to operate from/to a fully

coordinated airport on a seasonal basis, in a neutral, non-discriminatory and transparent way;

to facilitate the operations of aircraft operators at schedules facilitated airports. The corresponding

responsibility (Airport Slot Negotiation) is to negotiate the allocation of airport slots with the aircraft

operators in accordance with the rules and regulations and to define the airport slot allocation plan;

to monitor the use of airport slots and adherence of Aircraft Operators to allocated schedules. The

corresponding responsibility (Airport Slot Monitoring) is to monitor that the utilisation of airport slots

by the aircraft operators is in accordance with the airport slot allocation plan.

The schedules facilitator shall advise air carriers and recommend alternative arrival and/or departure times

when congestion is likely to occur.

In addition to its own tasks, the coordinator shall on request and within a reasonable time make available

free of charge for review to interested parties, in particular to members or observers of the coordination

committee, the following information:

historical slots by airline, chronologically, for all air carriers at the airport;

requested slots (initial submissions), by air carriers and chronologically, for all air carriers;

all allocated slots, and outstanding slot requests, listed individually and in chronological order by air

carriers, for all air carriers;

remaining available slots;

full details on the criteria being used in the allocation.

2.2.4 Determination of capacity and associated coordination parameters

Regulation 95/93 defines coordination parameters as the “expression in operational terms of all the capacity

available for airport slot allocation at an airport during each coordination period, reflecting all technical,

operational and environmental factors that affect the performance of the airport infrastructure and its

different sub-systems”.

Member States shall ensure that a thorough capacity analysis is carried out at an airport before declaring it

as coordinated. The analysis, based on commonly recognised methods, shall determine any shortfall in

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 13 of 93

capacity, taking into account environmental constraints at the airport in question. The analysis shall consider

the possibilities of overcoming such shortfall through new or modified infrastructure, operational changes,

or any other change, and the time frame envisaged to resolve the problems.

The number of air transport movements (ATMs) at Level 3 airports is specified in detail according to the time

of day; Regulation 95/93 assumes that all air services are operated under Instrument Flight Rules in IMC.

When adverse weather conditions are experienced, this enables the flow rates to be maintained and delays

to be minimised.

Declared capacity values may differentiate between arrival, departure and total movements. This results in a

capacity declaration profile, which may vary throughout the airport opening hours to reflect the historical

traffic mix and permit the possibility of recovery from demand peaks by incorporating a “fire-break” in the

schedule.

Declared capacity is underpinned by assumptions on a seasonal weather norm, operational practices

designed to maximise the productivity of the airport infrastructure and recognition of external constraints.

Typically these might embrace:

noise and emission constraints;

ground handling and capacity of terminal facilities;

runway capacities;

taxiway capacities;

stand allocation/planning;

de-icing positions.

For example, taxiway usage rules are defined for all traffic and depend on the runway configurations in use

and the weather conditions. Meanwhile, stand allocation usage rules are defined for each type of aircraft

and priority criteria could be established depending on the airline or type of cargo.

The duration of blocks can vary and multiple constraints in terms of capacity per blocks of different duration

can exist. Usually 60-mins blocks are used to determine the maximum number of slots, while blocks of 30

and 10 minutes are optionally used to control the concentration of flights [53].

A coordination committee at each coordinated airport is responsible for the timely provision of the

coordination parameters to the coordinator. The committee includes amongst others air carriers, the

managing body of the airport, the relevant air traffic control authorities as well as the regulatory authority.

2.2.5 Primary airport slot allocation according to grandfathering and

use-it-or-lose-it rules

The primary allocation of slots is an administrative process: Member States designate congested airports as

coordinated, and slot coordinators at each of these airports seek to balance the demand for slots with the

supply.

Each coordinated airport must specify a declared capacity (in number of aircraft movements per unit of

time) taking into account all the constraints affecting availability of resources.

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 14 of 93

Users interested in scheduling operations at these airports must send a formal request for each desired slot.

The submission of planned schedules from airlines to the responsible coordinator must be done about five

months in advance of the upcoming season. Slots are allocated in series, i.e. sequences of at least five slots

at the same time on the same day of the week, distributed regularly in the same scheduling season, e.g., a

series of 09:15 departure slots over at least five consecutive Mondays.

In Figure 1 below there is an example of a series of slots depicted together with examples of what is not

considered a series of slots.

Figure 1. Example of Series of Slots and what is not considered a Series of Slots

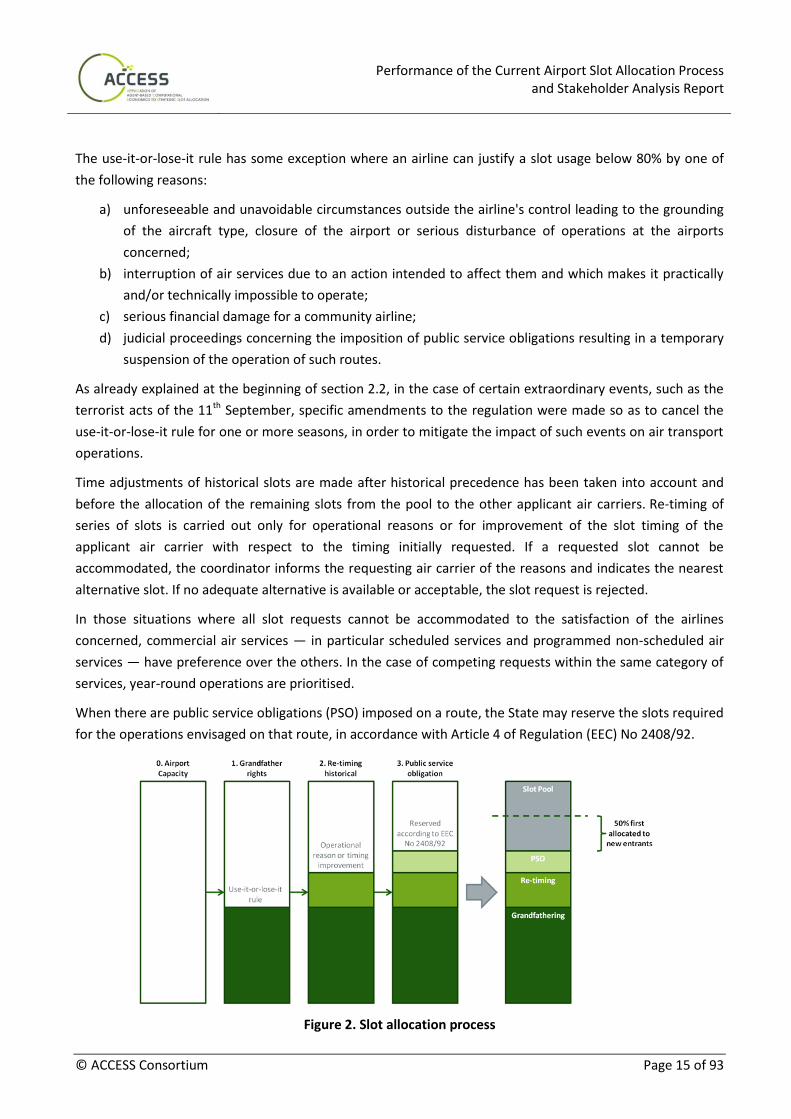

Two fundamental criteria are applied when allocating the available capacity: historical precedence (the

so-called grandfather rights) and time adjustments of historical slots.

Airlines can earn historic rights or grandfather rights to a series of slots, provided they operate the slots as

allocated by the coordinator at least 80% of the time during a season (use-it-or-lose-it rule, also called 80-20

rule). Airlines can lose historic rights due to repeated and intentional slot misuse. Grandfather rights only

apply to series of slots, never to single slots or other ways of grouping slots. Single slots and other groups of

slots will return to the slot pool the following season.

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 15 of 93

The use-it-or-lose-it rule has some exception where an airline can justify a slot usage below 80% by one of

the following reasons:

a) unforeseeable and unavoidable circumstances outside the airline's control leading to the grounding

of the aircraft type, closure of the airport or serious disturbance of operations at the airports

concerned;

b) interruption of air services due to an action intended to affect them and which makes it practically

and/or technically impossible to operate;

c) serious financial damage for a community airline;

d) judicial proceedings concerning the imposition of public service obligations resulting in a temporary

suspension of the operation of such routes.

As already explained at the beginning of section 2.2, in the case of certain extraordinary events, such as the

terrorist acts of the 11th September, specific amendments to the regulation were made so as to cancel the

use-it-or-lose-it rule for one or more seasons, in order to mitigate the impact of such events on air transport

operations.

Time adjustments of historical slots are made after historical precedence has been taken into account and

before the allocation of the remaining slots from the pool to the other applicant air carriers. Re-timing of

series of slots is carried out only for operational reasons or for improvement of the slot timing of the

applicant air carrier with respect to the timing initially requested. If a requested slot cannot be

accommodated, the coordinator informs the requesting air carrier of the reasons and indicates the nearest

alternative slot. If no adequate alternative is available or acceptable, the slot request is rejected.

In those situations where all slot requests cannot be accommodated to the satisfaction of the airlines

concerned, commercial air services — in particular scheduled services and programmed non-scheduled air

services — have preference over the others. In the case of competing requests within the same category of

services, year-round operations are prioritised.

When there are public service obligations (PSO) imposed on a route, the State may reserve the slots required

for the operations envisaged on that route, in accordance with Article 4 of Regulation (EEC) No 2408/92.

Figure 2. Slot allocation process

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 16 of 93

After this first assignment to incumbent airlines and the slot reservation for PSOs, a slot pool is created with

the remaining slots. Fifty percent of this slot pool is allocated free of charge by the slot coordinator to new

entrant airlines. An airline is considered a new entrant at an airport on a particular day if, upon allocation,

a) it would hold fewer than five slots in total on that day; or

b) for an intra-EU route with less than three competitors, it would hold fewer than five slots for that

route on that day.

The remaining slots in the pool are allocated giving priority to year-round commercial air services.

Within each category (changes to historic slots, allocations to new entrants and other allocations from the

slot pool), a request to extend an existing operation to operate on a year round basis should have priority

over a new slot request.

Coordinators allocate the available capacity based on the following broad priority order:

a) a series of scheduled services;

b) ad hoc services;

c) other operations.

Other criteria to be applied when slots cannot be allocated based on the above mentioned rules are:

d) Effective Period of Operation: the schedule that will be effective for a longer period of operation in

the same season should have priority;

e) Type of Service and Market: the balance of the different types of services (scheduled, charter and

cargo) and markets (domestic, regional and long haul), and the development of the airport route

network should be considered.

f) Competition: coordinators should try to ensure that due account is taken of competitive factors in

the allocation of available slots;

g) Curfews: when a curfew at one airport creates a slot problem elsewhere, priority should be given to

the airline whose schedule is constrained by the curfew;

h) Requirements of the Travelling Public and Other Users: coordinators should try to ensure that the

needs of the travelling public and shippers are met as far as possible;

i) Frequency of Operation: higher frequency such as more flights per week should not in itself imply

higher priority for airport slot allocation;

j) Local Guidelines: the coordinator must take local guidelines into account should they exist. Such

guidelines should be approved by the Coordination Committee or its equivalent.

Slots are allocated in scheduling seasons ― summer starting in late March and winter starting in late

October. The initial allocation of slots occurs in advance of the biannual IATA Slot Conferences held each

November (summer) and June (winter).

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 17 of 93

2.2.6 Slot Returns

Airlines shall return slots that are allocated to them but they do not intend to use. Returns shall take place

before the slot return date to allow better opportunities for a successful reallocation by the coordinators

and to provide available capacity for schedules adjustments as described above. The slot return date of each

schedule season is dated about 2 months before its start: January 31st for summer scheduling season, and

August 31st for winter season.

Late slot returns are considered as unused slots and thus will diminish an airline’s opportunity to achieve

historical status for certain slots or series of slots. This procedure features characteristics of a slight

penalisation for late slot returns.

Figure 3. Theoretical slot return timings (Source: RTWH Aachen)

2.2.7 Slot exchanges and transfers

Description of the current IATA system

Under the IATA Guidelines, following primary allocation, slot exchange is expressly encouraged (provided

that, in the case of newly allocated slots, the coordinator is satisfied that the exchange improves the

operating position of the airline to which the slots were originally allocated). Slots may be freely exchanged

on a one for one basis at a coordinated airport by any number of airlines; and indeed, to encourage and

facilitate multilateral slot exchanges, the IATA website [33] is available for airlines to inform other airlines

about their needs and any current slot holdings available for exchange.

Slot transfers (i.e. without an exchange) may only take place where the laws of the relevant country permit

it, and only to airlines serving or planning to serve the same airport. However, transfers of new slots are not

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 18 of 93

permitted until such slots have been operated for two equivalent scheduling periods, in order to prevent

airlines from taking advantage of an enhanced priority, such as new entrant status, simply by transferring

them to another airline.

Shared operations are also allowed, so that slots held by one airline are used by another airline. Shared

operations may only take place where not prohibited by the laws of the relevant country. The original slot

holder retains historic precedence.

An airline that ceases operations at an airport must immediately return all the slots allocated to it for the

remainder of the season and for the next season (if already allocated), and inform the coordinator whether it

will use the slots in the future.

In the IATA Guidelines there is no bar to monetary consideration being involved in secondary trading. A

system of secondary trading would therefore not appear to be inconsistent with the IATA system.

Description of the current EC system

Under the EC Slot Regulation, following primary allocation, slots may be exchanged or transferred between

airlines in certain specified circumstances (and then subject to certain exceptions). Slots may be:

1. transferred by an air carrier from one route or type of service to another route or type of service

operated by the same air carrier;

2. transferred:

i) between parent and subsidiary companies, and between subsidiaries of the same company;

ii) as part of the acquisition of control over the capital of an air carrier;

iii) in the case of a total or partial take-over, when the slots are directly related to the air carrier

taken over;

3. exchanged one for one, between air carriers.

Exchanges and transfers are always subject to the express confirmation of the coordinator. The coordinator

must not confirm a transfer or exchange unless it is in conformity with the Regulation and it is satisfied that

airport operations will not be prejudiced. The coordinator must also be satisfied that the slots are not the

ones which are reserved for a PSO route and that slots allocated from the pool to those qualifying for them

as “new entrants” may not be exchanged or transferred by them for a period of two equivalent scheduling

periods.

Even if not explicitly specified by the Regulation, it is assumed that an exchange of slots “one for one” refers

to slots at the same airport.

Regarding shared operations, the EC Slot Regulation provides that “slots allocated to one air carrier may be

used by (an) other carrier(s) participating in a joint operation (...)” and “in the case of services operated by a

group of air carriers, such carriers can use each other’s’ slots”. “Group of air carriers” is defined (Article 2 (f)

(ii)) as “two or more air carriers which together perform joint operations, franchise operations or code-

sharing for the purpose of operating a specific air service”. This allows, for example, carriers in the same

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 19 of 93

alliance to use each other’s slots when performing joint operations or code sharing, although any actual

exchange or transfer is still subject to Article 8a.

The current EC Regulation is silent on the monetary compensation accompanying slot exchanges and

transfers. In Heathrow airport, there are cases of exchanges of slots in which an airline has exchanged a

highly valuable slot against a so called “junk” slot, which is a slot with no commercial value; the air carrier

receiving the highly valuable slot at peak time pays a monetary compensation to the “seller”, and the “junk”

slot usually ends up returning to the pool.

On 30 April 2008, the European Commission issued a clarification of the Slot Regulation. In his press release,

Jacques Barrot, Vice-President of the European Commission, said:

“At crowded airports, we need to make sure that slots are used as efficiently as possible and that airlines

have a fair chance to develop their operations. Slots at airports must be distributed in a fair and

non-discriminatory way. Today we are recognising for the first time that secondary trading is an acceptable

way of allowing slots to be swapped among airlines. We will keep a close eye on the situation across Europe

and ensure that secondary trading works to the advantage of consumers, but this system has already shown

its value in London, where it has allowed a range of airlines to take advantage of the opportunities provided

by the EU-US aviation agreement and to create new levels of competition”.

2.2.8 Slot trading

When Regulation 95/93 was drafted, the EC followed the principles of IATA WSG. Art. 8(4) of the Regulation

95/93 stated that “slots may be freely exchanged between air carriers or transferred by an air carrier from

one route or type of service to another, by mutual agreement or as a result of a total or partial takeover or

unilaterally”. Though different EU officials reiterated that the Commission's position was that slot trading

was in principle illegal, the text of the Regulation gave rise to much discussion as to whether it indeed

prohibited any form of slot trading. In Regulation 793/2004, slot trading was in principle refused due to the

risk that it would reinforce the dominant position of incumbent carriers at congested European airports, but

the political discussion led to a Regulation that was still ambiguous: neither is secondary trading explicitly

allowed nor is it explicitly forbidden. In practice, secondary slot trading has been in operation at UK airports

for some time, as the EC recognised in 2008 [19].

Within the EU, slot trading is therefore not specifically regulated at the time being. The ground rules for slot

trading have evolved from the general principles of airport slot allocation contained within the EU Slot

Regulation and the IATA Worldwide Slot Guidelines. These ground rules are:

willing buyers and willing sellers: airlines are free to choose whether to trade slots and with whom.

There is no compulsion to sell slots or to accept the highest bid;

only airlines can hold and trade slots: a slot holder must be an airline with a valid operating licence.

Non-airline entities cannot hold slots, and if an airline loses its operating licence its slots are forfeited

to the pool – they cannot be considered assets for liquidation;

slots are subject to use-it-or-lose-it rules: airlines must operate slots as allocated by the coordinator at

least 80% of the time during a season to earn or retain historic rights to the slots. Airlines can lose

historic rights to slots for repeated and intentional slot misuse;

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 20 of 93

slots are permissions to use a bundle of airport infrastructure: slots are not just a runway time, but

include access to all scarce components of airport capacity (terminal, apron, gates, night quota, etc.).

Typically slots are traded as a bundle, but it is possible to construct trades for individual components

of capacity;

slots are traded by way of a one-for-one slot exchange: to overcome this rule, the slot exchange often

involves swapping historic peak time slots for newly allocated off peak slots. The off peak slots is then

returned to the pool after the exchange, so that the net effect of the exchange is the transfer of peak

time slots from Airline A to Airline B;

the coordinator must confirm the feasibility of any slot trade: in confirming feasibility, the coordinator

must ensure that airport operations would not be prejudiced (e.g., that there is sufficient terminal

capacity available if the slots are operated with a larger aircraft). There are additional restrictions on

trading new entrant slots and slots used on PSO routes. The coordinator shall undertake his role in an

independent, transparent and non-discriminatory way;

slots are traded in seasons: in order to complete a year-round slot trade, two separate transactions

are required to exchange slots for the summer and winter seasons. Slots can be exchanged at any time

after the initial allocation of slots in November for a summer season and June for a winter season;

only slots in the future can be exchanged: slots can be exchanged for the next season (after the initial

allocation of slots) and for the remainder of the current season. In the case of a mid-season exchange,

slots for the beginning part of the season must be either (a) exchanged separately, or (b) requested by

the new slot holder as “fill in” slots from the pool, in the next equivalent season;

only slots with historic rights can be traded: in order to prevent abuse of the free primary allocation of

slots by the coordinator, slots must be operated during at least one season and historic rights earned

before they may be traded in the next equivalent season. Slots allocated on the basis of a new entrant

priority cannot be traded until they have been operated for two equivalent seasons;

slot trade transactions are transparent but price disclosure is not mandated: the coordinator has a

duty of transparency, so the details of slots traded between airlines may be disclosed to interested

parties. It is currently not mandatory for airlines to disclose other details of the trade, such as any

monetary or other compensation accompanying a trade.

2.3 Coordination at European and worldwide level

Airport slots are not independent time permissions which can be easily modified, as a schedule change at

one airport can affect one or more other airports. The structure and organisation at international level is a

key element in the airport slot allocation process and for that purpose different associations intervene. In

the following sub-sections, we describe the airport coordination associations and the activities related to

airport slot allocation conducted by IATA.

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 21 of 93

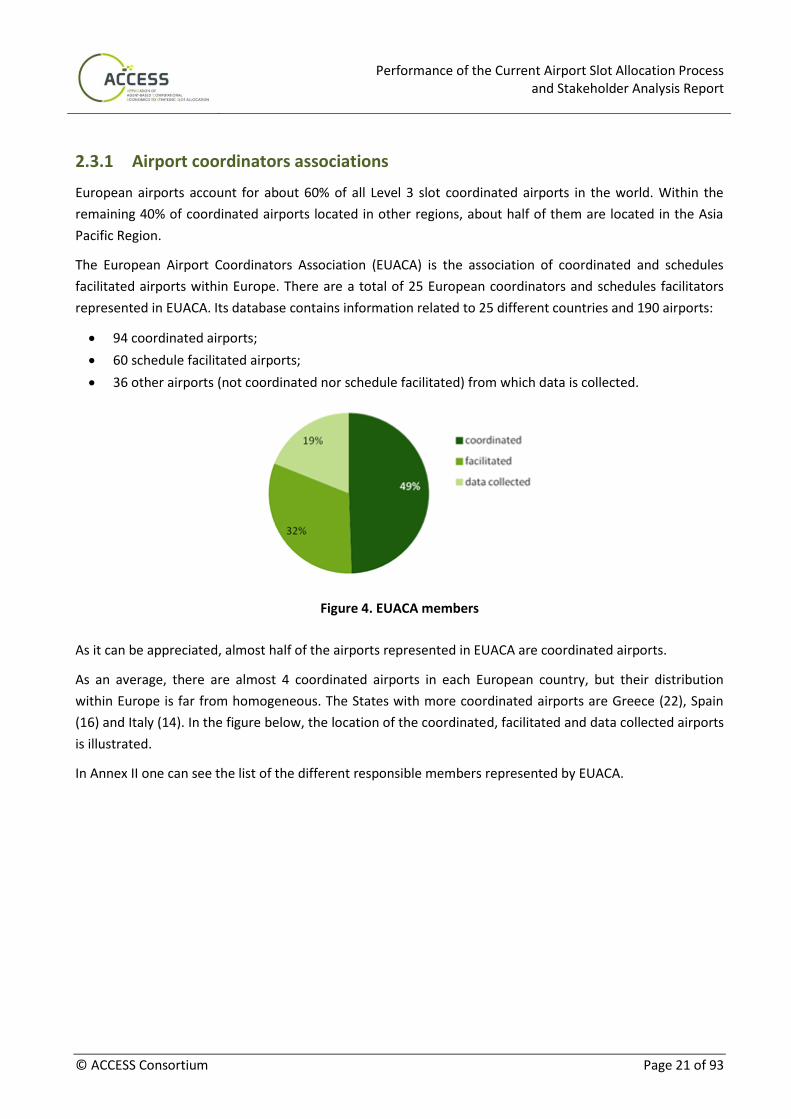

2.3.1 Airport coordinators associations

European airports account for about 60% of all Level 3 slot coordinated airports in the world. Within the

remaining 40% of coordinated airports located in other regions, about half of them are located in the Asia

Pacific Region.

The European Airport Coordinators Association (EUACA) is the association of coordinated and schedules

facilitated airports within Europe. There are a total of 25 European coordinators and schedules facilitators

represented in EUACA. Its database contains information related to 25 different countries and 190 airports:

94 coordinated airports;

60 schedule facilitated airports;

36 other airports (not coordinated nor schedule facilitated) from which data is collected.

Figure 4. EUACA members

As it can be appreciated, almost half of the airports represented in EUACA are coordinated airports.

As an average, there are almost 4 coordinated airports in each European country, but their distribution

within Europe is far from homogeneous. The States with more coordinated airports are Greece (22), Spain

(16) and Italy (14). In the figure below, the location of the coordinated, facilitated and data collected airports

is illustrated.

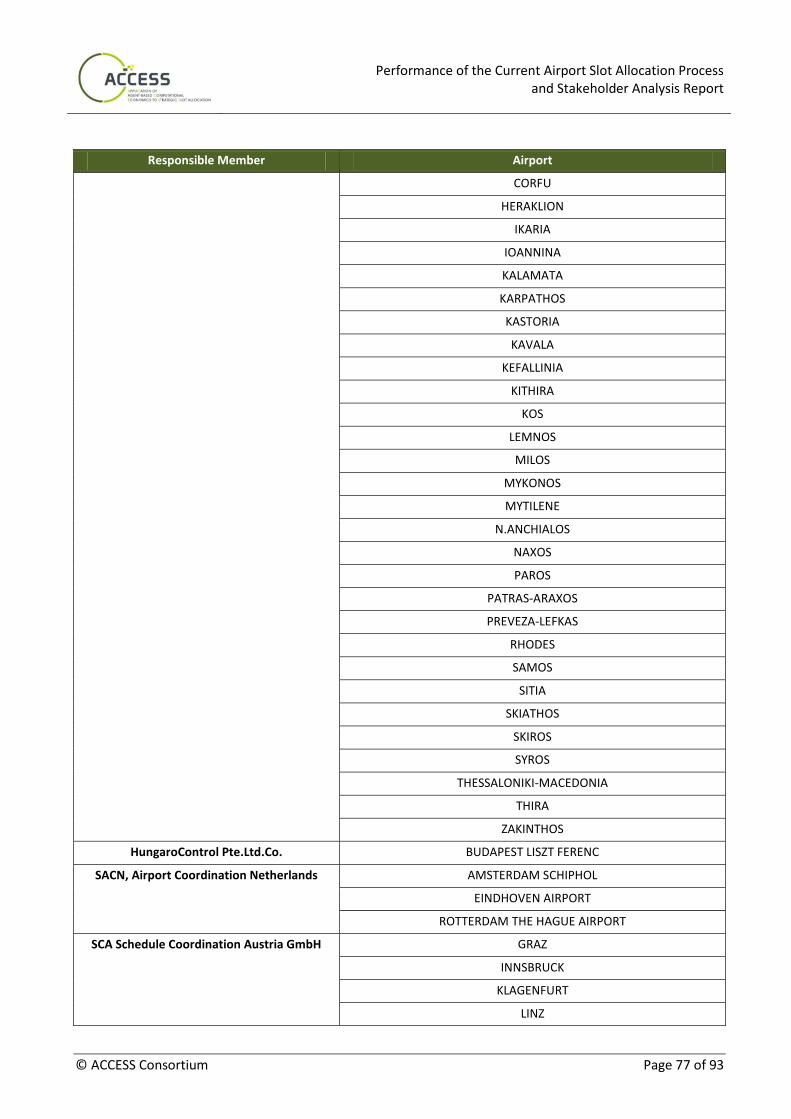

In Annex II one can see the list of the different responsible members represented by EUACA.

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 22 of 93

Figure 5. Geographic distribution of EUACA members

In the same way that the European coordinators are associated through EUACA, there is a similar association

worldwide called Worldwide Airport Coordinators Group (WWACG). The WWACG represents a total of 87

coordinators, which concerns 313 airports and 69 different countries. The distribution of the type of airports

is very similar to the one in Europe:

158 coordinated airports (51%);

118 facilitated airports (38%);

35 other airports from which data is collected (11%).

Figure 6. WWACG members distribution

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 23 of 93

2.3.2 The IATA airport slot allocation activities

The International Air Transport Association (IATA) is an international association representing some 240

airlines. Among its activities, IATA manages and publishes the Worldwide Slot Guidelines (WSG), which are

intended to provide guidance on the allocation of airport slots and set the baseline for most of the airport

slot allocation regulations worldwide.

The main instrument of the IATA slot allocation system is the organisation of biannual, international

scheduling conferences with the participation of slot coordinators, airport representatives, and airline

delegates. The IATA Slot Conferences (SC) are organised the Thursday after the second Saturday in

November, for the summer scheduling season, and June, for the winter scheduling season.

The worldwide IATA Schedules Conference takes place after the initial allocation, involving airline

representatives and airport coordinators into negotiation, arrangement of slot amendment, slot alternatives

and slot exchange (between airlines). Schedule adjustments are carried out through bilateral discussions

between airlines and coordinators. Schedules adjustments may continue until the day of operations, mainly

following first-come-first-served criteria, i.e. by using waiting lists.

As a schedule change at one airport could affect one or more other airports, the conference provides the

best forum in which all such interdependent changes can be quickly and efficiently processed and all airlines

can leave the conference with schedules which they consider are the best compromise between what is

wanted and what is available.

The IATA Slot Conference is convened solely for the purpose of allocating and managing slots. Discussions

about pooling of flights, pricing, market entry or any other competitively sensitive activities beyond the

scope of the SC are not permitted. For that reason, delegates at the SC must be the accredited

representatives of their airlines or coordination organisation. IATA maintains a directory of companies

participating in the SC and the individuals designated by their companies as Heads of Delegation.

This directory lists the names and contact details of coordinators and facilitators, and those authorised to

trade, exchange or make slot requests on behalf of a participant airline.

The baseline of the IATA SC is the entitlement of airlines to historic slots. For that reason, information must

be provided by airport coordinators to airlines and vice versa regarding the slots with grandfather rights. At

the biannual conferences, airlines seek to modify their schedules by exchanging or transferring between

themselves their existing slot holdings and trying to obtain additional slots that occasionally become

available.

The after conference activity involves bilateral negotiations among airlines with the aim to establish mutually

beneficial exchanges of slots.

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 24 of 93

2.4 Current slot exchanges: experiences of secondary trading

2.4.1 Slot mobility

‘Slot mobility’ can be defined as the extent to which the airlines that held slots at the start of one period still

held the slots by the end, [48]. SDG analysed slot mobility at some of the major European airports during the

period 2007-2010. At the most congested airports, there was limited change in the allocation of slots during

this period (e.g. 6.6% at Heathrow or 9.5% at Frankfurt), with the exceptions of Dusseldorf (27.6%) and

Gatwick (39%).

2.4.2 Experiences of secondary trading

In the US air carriers are allowed to trade slots since the adoption of the so-called ‘Buy-Sell Rule’ in 1985,

and there are well-known cases of carriers like US Airways or Delta engaging in major slot transactions.

Secondary slot trading appears in some cases to have been a useful tool that has led to increased slot

mobility. There are many slot swaps for timing adjustments, but relatively few permanent or long-term

transfers, most of them taking place between large carriers. Most of the secondary trading activity has taken

the form of leasing, as opposed to outright sales. It is worth noticing that not all the opinions concur.

According to the US Government accounting office the trading just solidified the dominant carriers and they

continued to lease slots as a way of babysitting them (see section 0). A detailed analysis of the US secondary

market can be found e.g. in [39].

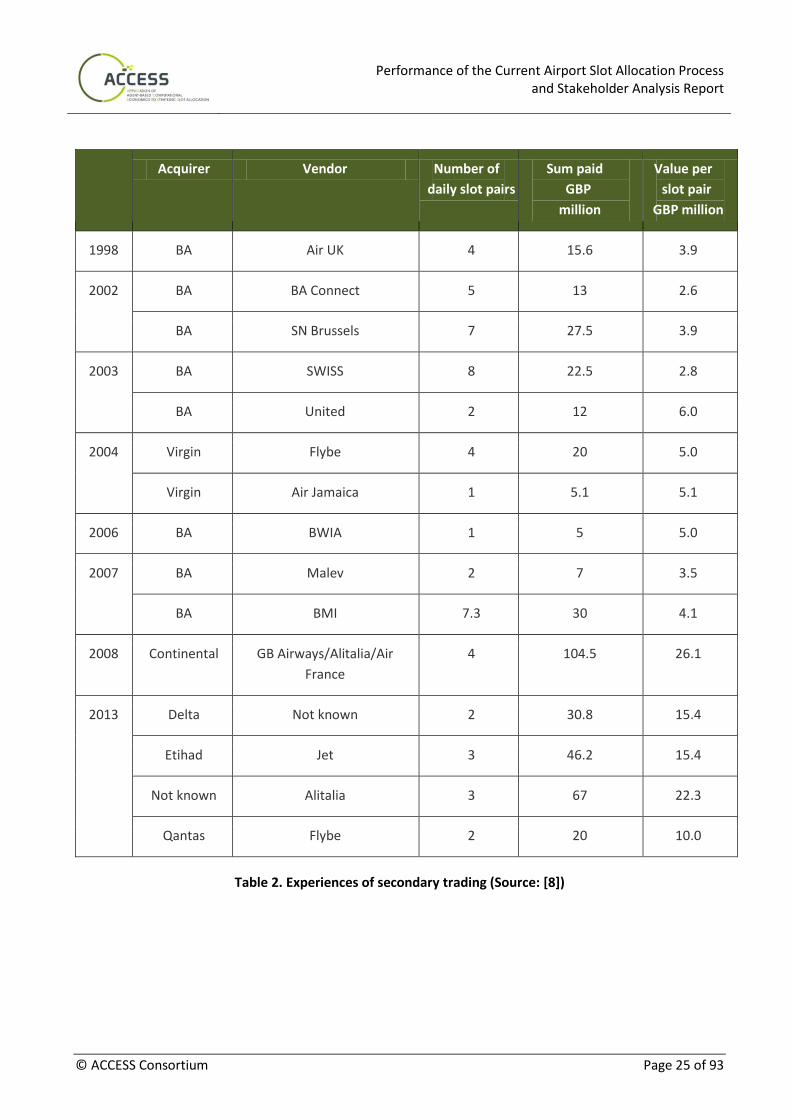

In Europe, an official market for slots does not exist. However, a grey market has developed at certain

airports, with buying, selling and leasing of slots occurring through “fake” or “artificial” exchanges.

Secondary trading primarily occurs at London Heathrow and, to a lesser extent, Gatwick. It is not transparent

whether secondary trading occurs at other EU airports, but the slot coordinators have identified that “fake

exchanges” have occurred at other airports like Frankfurt, Düsseldorf and Vienna [48]. Slot trades at

Heathrow have periodically caught the attention of the public, though the transaction values that are

reported in the media are only a small proportion of the total and most likely represent the high value end of

the market. The coordinator, ACL, reports that it has facilitated about 200 Heathrow slot trades involving

over 2,300 weekly slots since 2001. ACL has recently created a website showing details of slot trades:

www.slottrade.aero. Some examples of Heathrow slot valuations from reported trades in the period 1998 to

2013 are shown in Table 2.

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 25 of 93

Acquirer Vendor Number of

daily slot pairs

Sum paid

GBP

million

Value per

slot pair

GBP million

1998 BA Air UK 4 15.6 3.9

2002 BA BA Connect 5 13 2.6

BA SN Brussels 7 27.5 3.9

2003 BA SWISS 8 22.5 2.8

BA United 2 12 6.0

2004 Virgin Flybe 4 20 5.0

Virgin Air Jamaica 1 5.1 5.1

2006 BA BWIA 1 5 5.0

2007 BA Malev 2 7 3.5

BA BMI 7.3 30 4.1

2008 Continental GB Airways/Alitalia/Air

France

4 104.5 26.1

2013 Delta Not known 2 30.8 15.4

Etihad Jet 3 46.2 15.4

Not known Alitalia 3 67 22.3

Qantas Flybe 2 20 10.0

Table 2. Experiences of secondary trading (Source: [8])

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 26 of 93

2.5 Systems adopted in other regions

2.5.1 USA

Current situation

The term slot in the USA refers to the time window assigned to the aircraft for the use of the runway: “slot

means the operational authority to conduct one IFR landing or take-off operation each day during a specific

hour or 30 minute period at one of the High Density Traffic Airports” [15]. Differently from European

situation, in the US only the use of runway is controlled; the capacity of no other airport facility is taken into

account. Only four USA airports are currently slot-controlled: Ronald Reagan Washington National airport,

and three New York area airports: JFK, Newark, and La Guardia. Slot regulation at these airports began in the

late 1960s, as an attempt to reduce congestion and ensuing delays, and was termed the High Density Rule

[16]. The regulation refers to slots as either “slots” (at Reagan National), or “operating authorization” (New

York airports).

Grandfather rules

Before 1982 the airlines needed to use 65% of their assigned slots in order to keep them. In 1982 the rule

was changed to 80%, in line with IATA slot guidelines. Although the 80 per cent usage requirement is

applicable to all four slot-controlled airports, other provisions of the rules differ between the airports,

including:

the hours when airlines are required to have a slot to operate a flight;

the time periods for which slots usage is measured and reported to FAA; and

whether airlines can buy or sell slots (see table 1- p. 10 of [51]).

Reagan National and La Guardia’s 80% usage is measured over all days over 2-month reporting periods,

while JFK and Newark’s usage is measured for each day of the week over a scheduling season.

The biggest difference with respect to the European situation is that the airlines at these four airports are

not required to schedule flights for all the slots they receive, while in Europe, airlines tend to schedule the

flights for all the slots, and return the slots they do not intend to use. US Government Accountability Office

[51] analysed this aspect for 2011, and found that the airlines in aggregate schedule between 80% and 100%

of their slots. This practice (not scheduling all slots) is widely used to provide operation flexibility for airlines

in case of unpredictable events (weather, maintenance and similar). While the airlines that have less slots

would welcome stricter rules on the use of slots (requiring scheduling all the slots), the airlines holding more

slots are against it as it would “reduce their scheduling flexibility”.

Slot usage monitoring

In the USA, FAA is in charge of “administering the slot rules, which primarily includes airport slot allocation,

transfers, and monitoring and enforcing airlines’ compliance with the 80% slot usage requirement.”

However, the GAO analysis showed that the FAA “does not calculate or know airlines’ schedule rates.” At the

time of the mentioned report, FAA did not require airlines to submit the slot usage data in one format, and

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 27 of 93

the computer systems they used were not able to compile the different data formats. Therefore, FAA was

not able to provide a reliable and accurate picture of the actual slot usage.

Trading and auctioning

Slots for Reagan National airport can be sold, traded or leased, as regulated by the FAA buy/sell rule from

1986 [15]. As the slots for the New York area airports are within the FAA temporary orders and therefore are

not considered to be the permanent solution, these slots can be only traded or leased. In 2008, the FAA

proposed congestion management rules for JFK, La Guardia, and Newark “that would have created a market

by annually auctioning a limited number of slots in each of the first 5 years of the rule, which had a 10 year

term”. However, the FAA cancelled the rule before it became effective as it was highly controversial. The

DOT and FAA started to draft the rule for the “Slot Management and Transparency for LaGuardia Airport,

John F. Kennedy International Airport, and Newark Liberty International Airport” in 2010. The aim of this

rulemaking is to replace the FAA temporary orders imposed on these airports, with the more permanent

rules. The new rules would also limit the number of operations, but would also establish a “secondary

market for U.S. and foreign air carriers to buy, sell, trade and lease slots” [28] among themselves at these

airports. Even though the original date for the rulemaking taking effect was October of 2011, the rule making

is still in the process of the review and refinement.

Brief history of slots assignment in USA

The slot control in the USA was introduced through the High Density Rule in 1969, with the aim to reduce the

congestion and delays at a few airports and delay propagation through the network stemming from airport

congestion. The airports subject to the rule were: LaGuardia, Newark, JFK, Washington National and Chicago

O'Hare. Newark was soon exempted.

Over the years the slot control management changed as a result of other changes (i.e. airline de-regulation

of 1978) or based on the assessment of the slot control process and its effects. The FAA, airlines, and the

USA government (Congress) were periodically assessing the slot control management and even more

importantly the effects of the process, mainly in terms of congestion and delays. The changes were imposed

as a result of assessments.

In the first period, the slots were allocated by the committee composed of the airlines serving the 5 (4)

airports under the High Density Rule. After the de-regulation in 1978, it became more and more difficult for

the airline scheduling committees to agree on the airport slot allocation as a consequence of increased

competition. The scheduling committees were replaces by the slot procedures in 1986. The new slot

procedures covered the withdrawal of slots used less than 65% of time, the return of slots, slot reallocation

and buy and sell rule. Buy and sell rule allowed airlines to buy, sell or lease their slots.

The review of the slot management in the 90s revealed that the High Density Rule became a barrier to

competition at slot-control airports. One of the reasons was the impossibility for new airlines to enter the

slot-controlled airports. The assessment of buy and sell rule showed that only during the first year of the

enactment of the rule about 50% of slots were bought/sold. Soon after, the percentage of actually sold slots

went down to 10%. In the process, the incumbent airlines solidified their positions at the slot controlled

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 28 of 93

airports by buying the slots. After this initial period, most of the transactions focused on short-term leases of

slots, which effectively prevented new entries. The incumbent airlines held on to their slots through the

short-term leasing, and had always the option not to renew the lease. New entrants thus did not have the

security of being able to establish a long-term market at these airports, which in turn are very important for

building efficient airline network.

In April 2000, the Congress required the phase-out of the High Density Rule at LaGuardia, JFK (by 2007), and

O’Hare. O’Hare was exempted in 2001. The rules were relaxed at the New York area airports as well.

However, after this, more and more flights got scheduled and the delays increased, especially in the summer

of 2007. In the aftermath (2007, and 2008) temporary slot control rules were imposed on Newark, JFK and

LaGuardia that are to be in effect until October 2013, or until the DOT and FAA do not issue the congestion

management rule (previously mentioned “Slot Management and Transparency” rule). The slots awarded

under the temporary rules cannot be bought or sold. Only the trade can be asked for, and needs to be

approved by FAA.

As can be seen, the airport slot allocation process in the USA went through different changes, many of them

based on the assessment of the effects of the current rules/processes. The assessments usually revolved

around congestion analysis and the ensuing delays, and around the market share and market entry analysis.

Airport efficiency

The analysis of the traffic at the slot-controlled airports and the comparison with the similar airports that do

not have slots imposed shows that at the slot-controlled airports [51]:

airlines are inclined to use smaller aircraft: because of this, FAA proposed to mandate an average

minimum aircraft size to avoid some of the inefficiencies. In general non-legacy airlines were in favour

of this rule, while the legacy airlines were opposed as, according to them, it would have a negative

impact on the service to small and medium size markets (the access to these markets needs to be

provided, by the FAA rules);

flights have, in some instances, higher daily frequencies to the same destination: the concern is that

the high frequency is the consequence of trying to preserve slots, and not of a sound business model;

overall load factors are lower: according to airports and some airline representatives, some airlines

would continue to operate the flights with the lower load factors (that would be discontinued at other

airports) in order to preserve their slots. There could be another explanation: the New York area

airports are high revenue airports, and the lower load factor flights might still be economically viable

with respect to other airports.

2.5.2 Australia

There are eight Level 3 and four Level 2 coordinated airports in Australia. The Sydney International Airport is

the only airport that is regulated by the State, under the Sydney Airport Demand Management Act from

1997. The act establishes the Slot Management Scheme, and the Compliance Scheme (established in 2012

with the most recent amendment). The concept of a slot [3] in Australia, specifically for the Sidney Airport, is

Performance of the Current Airport Slot Allocation Process and Stakeholder Analysis Report

© ACCESS Consortium Page 29 of 93

the following: “A permission for a gate movement is known as a slot. A slot allocated under the Slot

Management Scheme will permit a specified gate movement at a specified time on a specified day.”

Trading

In the case of Sydney, the slots allocated under the Slot Management Scheme are not transferable, and can

be only swapped, according to the slot swapping provisions in the same Scheme. It is not very clear if the

slots can be swapped, transferred or sold at the other slot-coordinated airports that are not subject to the