working capital and corporate strategy patterns in working capital of ...

Upload

deepika-pandeyCategory

view

79download

2

MANUAL

ON

WORKING CAPITAL FINANCE

For Internal Circulation only

2032032032032032032 2

2 of 203

PREFACE We have pleasure in presenting the manual on working capital financing. The manual

contains various procedural guidelines on working capital. It starts with the introduction

of working capital and gradually proceeds towards classification of assets, methods of

assessment, fixing various limits and finally broad guidelines on obtaining the

documentation for the limits.

It may please be noted that working capital advances are dynamic in nature and utilised

for building up of current assets. These assets being floating in nature depletes rapidly

in value if rotation of working capital cycle is not maintained. Therefore an effective

monitoring mechanism is pre-requisite to ensure rotation of working capital cycle as

envisaged for the specific purpose. Effective supervision and surveillance of the credit

portfolio is an essential requirement for working capital financing. Therefore, for easy

reference of the branches/offices, a whole chapter in the manual has been dedicated to

monitoring of working capital financing.

Given the dynamic nature of the financing, the branches/offices are, requested to also

refer the following documents/circulars issued from time to time:

Credit Policy of the bank

RBI Circulars

FEMA guidelines

Delegation of Power, issued by the bank

Credmin Guidelines

Any other internal guidelines issued by the management.

All endeavours have been made to make this manual comprehensive and up to date. At

the same time due care has been taken that the manual does not become bulky.

We hope that this manual will be handy and useful to all the branches/offices in the day to day management of working capital finance.

Jitender Balakrishnan Dy. Managing Director

Mumbai, September 18, 2007

*****

2032032032032032033 3

3 of 203

INDEX

Chapter No.

Particulars Page Nos.

1 Basic Principles of Lending 7 - 8 – Objectives of Lending – Basic Principles

2 Introduction to Working Capital 9 – 11 – What is Working Capital – Operating Cycle or Working Capital Cycle

3 Management of Working Capital 12 – 15 – Management of Working capital – Current Assets – Current Liabilities – Working Capital Gap – Net Working Capital – Current Ratio

4 Methods of Assessment 16 – 45 – Turnover Method – MPBF System – Classification of Current Assets and Current Liabilities – Cash Budget System – Structure of Cash Flow Statement

Operating Activities Investing Activities Financing Activities

– Appendix I – Working capital assessment based on MPBF Method

26

– Appendix II - Cash Flow Statement 27 – Appendix III - Profitability Statement & Projected Balance

Sheet

Profitability Statement (Form II – Part A of CMA) Analysis of Balance Sheet (Form III – Part A of CMA) Analytical & Comparative Ratio (Form III – Part B of

CMA)

31

– Appendix IV - Credit Monitoring Arrangement (CMA) Data 40 Annexure I (Form I) Existing & proposed Working

Capital limits

Annexure II (Form II - Part B of CMA) Comparative Statement of Current Assets & Current Liability

Annexure III (Form IV of CMA) - Funds Flow Statement

2032032032032032034 4

4 of 203

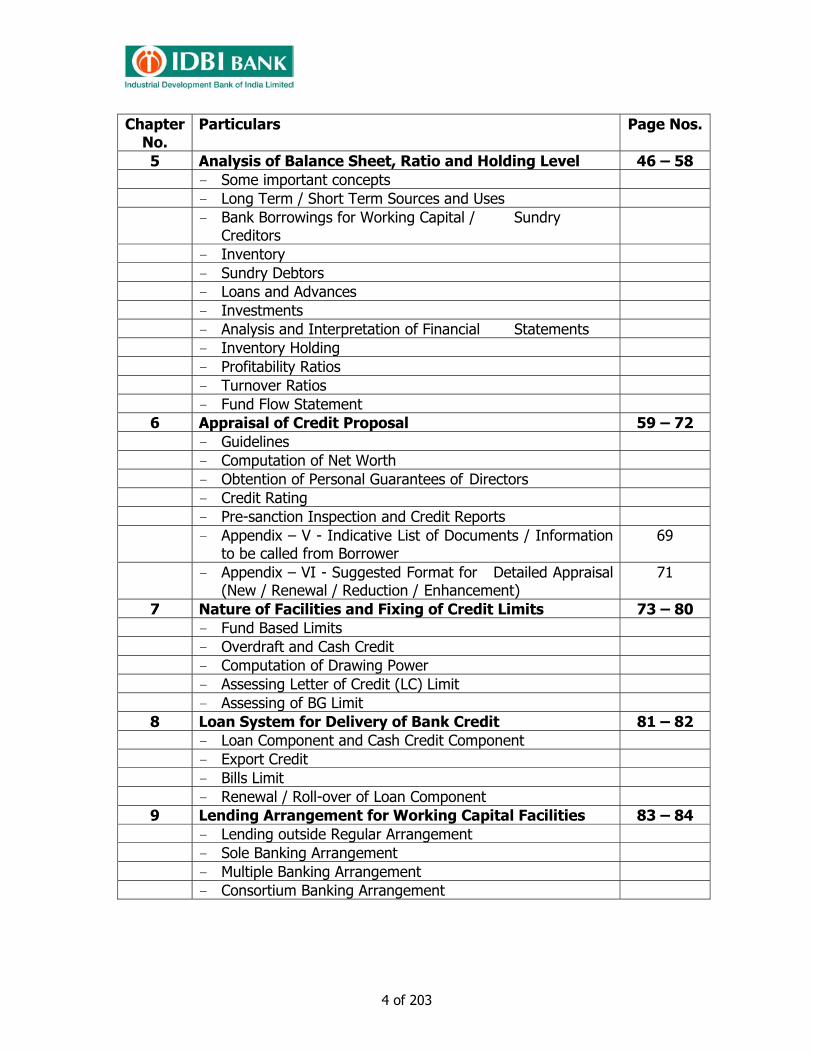

Chapter No.

Particulars Page Nos.

5 Analysis of Balance Sheet, Ratio and Holding Level 46 – 58 – Some important concepts – Long Term / Short Term Sources and Uses – Bank Borrowings for Working Capital / Sundry

Creditors

– Inventory – Sundry Debtors – Loans and Advances – Investments – Analysis and Interpretation of Financial Statements – Inventory Holding – Profitability Ratios – Turnover Ratios – Fund Flow Statement

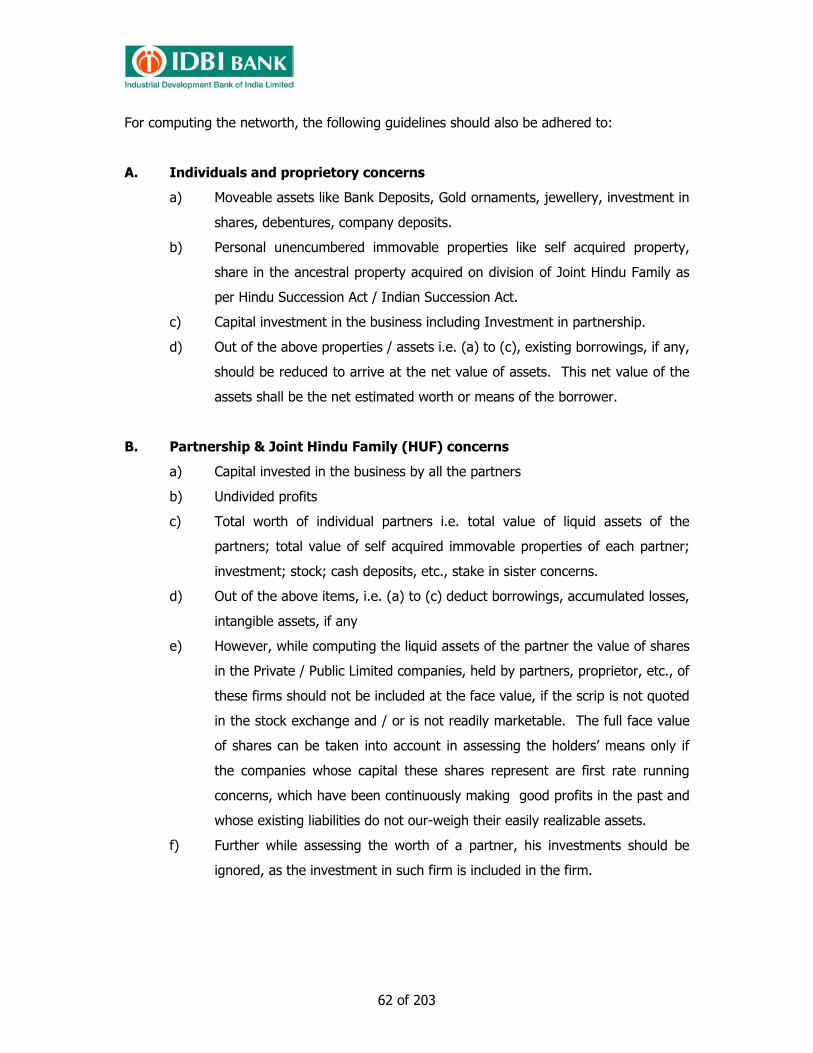

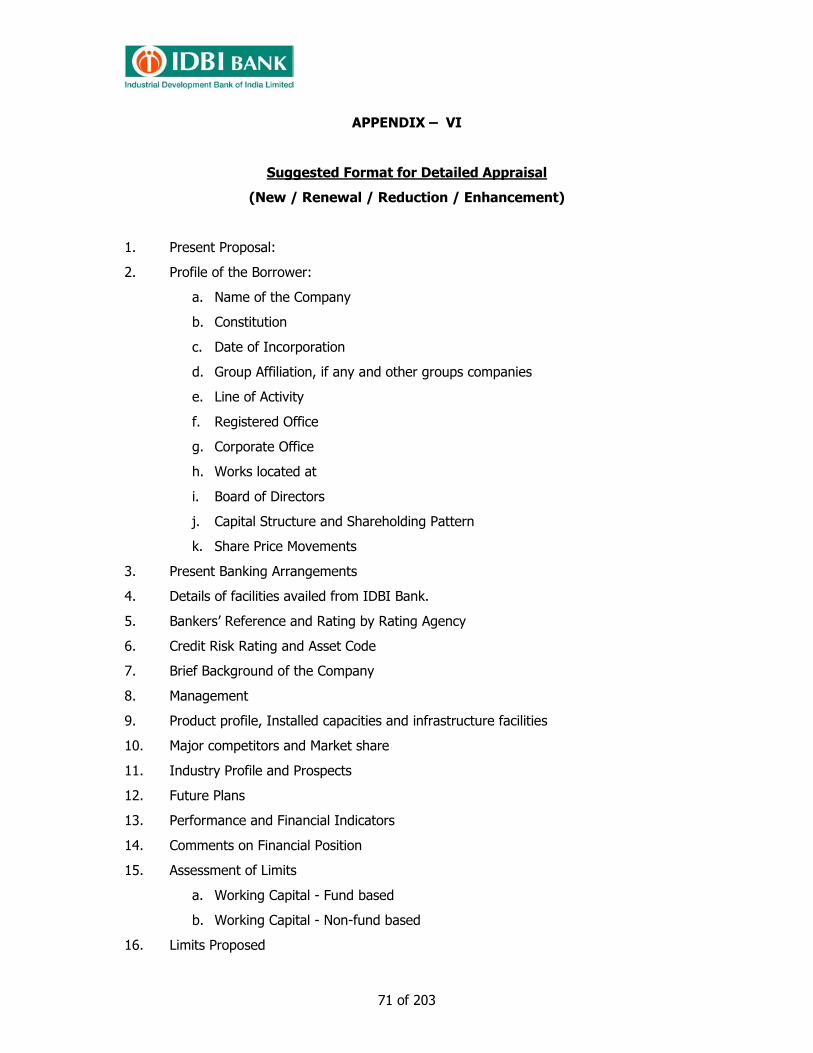

6 Appraisal of Credit Proposal 59 – 72 – Guidelines – Computation of Net Worth – Obtention of Personal Guarantees of Directors – Credit Rating – Pre-sanction Inspection and Credit Reports – Appendix – V - Indicative List of Documents / Information

to be called from Borrower 69

– Appendix – VI - Suggested Format for Detailed Appraisal (New / Renewal / Reduction / Enhancement)

71

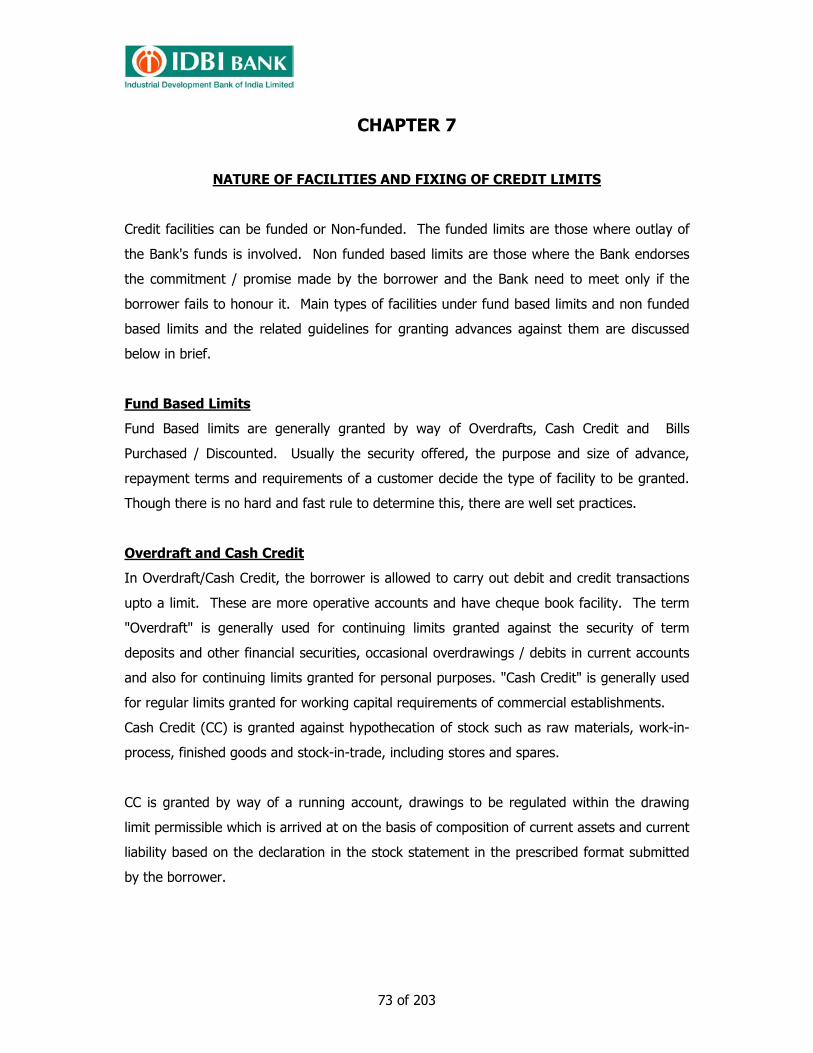

7 Nature of Facilities and Fixing of Credit Limits 73 – 80 – Fund Based Limits – Overdraft and Cash Credit – Computation of Drawing Power – Assessing Letter of Credit (LC) Limit – Assessing of BG Limit

8 Loan System for Delivery of Bank Credit 81 – 82 – Loan Component and Cash Credit Component – Export Credit – Bills Limit – Renewal / Roll-over of Loan Component

9 Lending Arrangement for Working Capital Facilities 83 – 84 – Lending outside Regular Arrangement – Sole Banking Arrangement – Multiple Banking Arrangement – Consortium Banking Arrangement

2032032032032032035 5

5 of 203

Chapter No.

Particulars Page Nos.

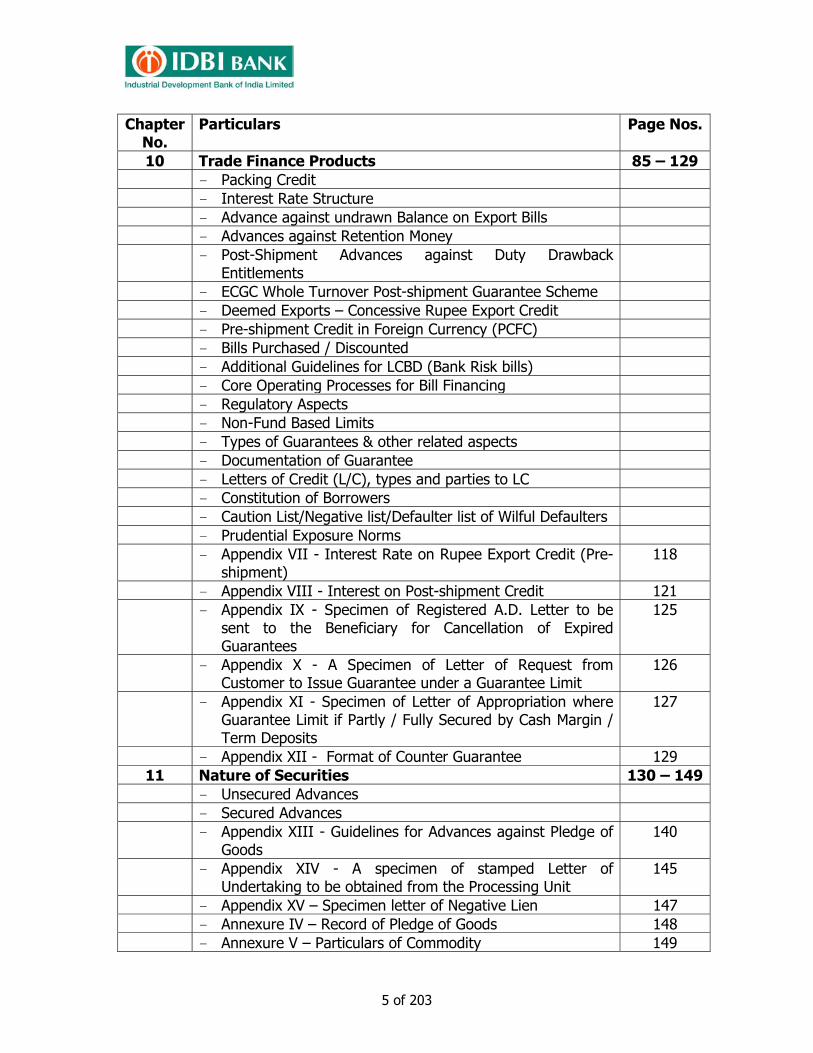

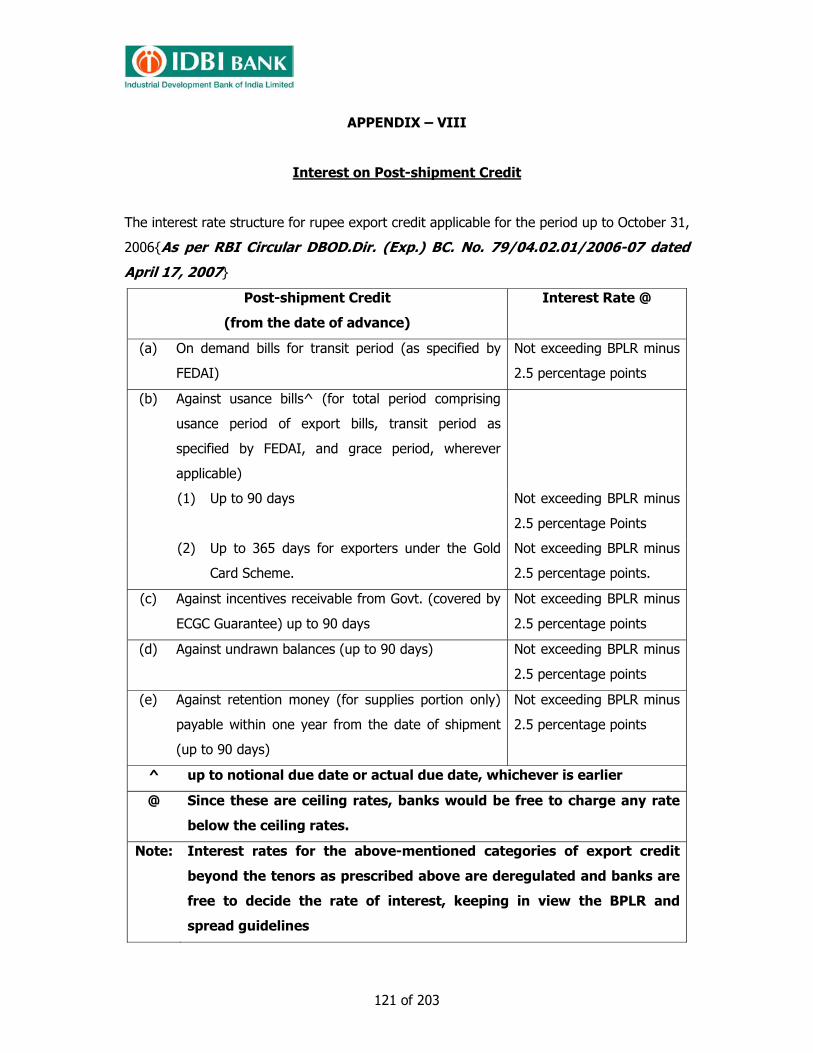

10 Trade Finance Products 85 – 129 – Packing Credit – Interest Rate Structure – Advance against undrawn Balance on Export Bills – Advances against Retention Money – Post-Shipment Advances against Duty Drawback

Entitlements

– ECGC Whole Turnover Post-shipment Guarantee Scheme – Deemed Exports – Concessive Rupee Export Credit – Pre-shipment Credit in Foreign Currency (PCFC) – Bills Purchased / Discounted – Additional Guidelines for LCBD (Bank Risk bills) – Core Operating Processes for Bill Financing – Regulatory Aspects – Non-Fund Based Limits – Types of Guarantees & other related aspects – Documentation of Guarantee – Letters of Credit (L/C), types and parties to LC – Constitution of Borrowers – Caution List/Negative list/Defaulter list of Wilful Defaulters – Prudential Exposure Norms – Appendix VII - Interest Rate on Rupee Export Credit (Pre-

shipment) 118

– Appendix VIII - Interest on Post-shipment Credit 121 – Appendix IX - Specimen of Registered A.D. Letter to be

sent to the Beneficiary for Cancellation of Expired Guarantees

125

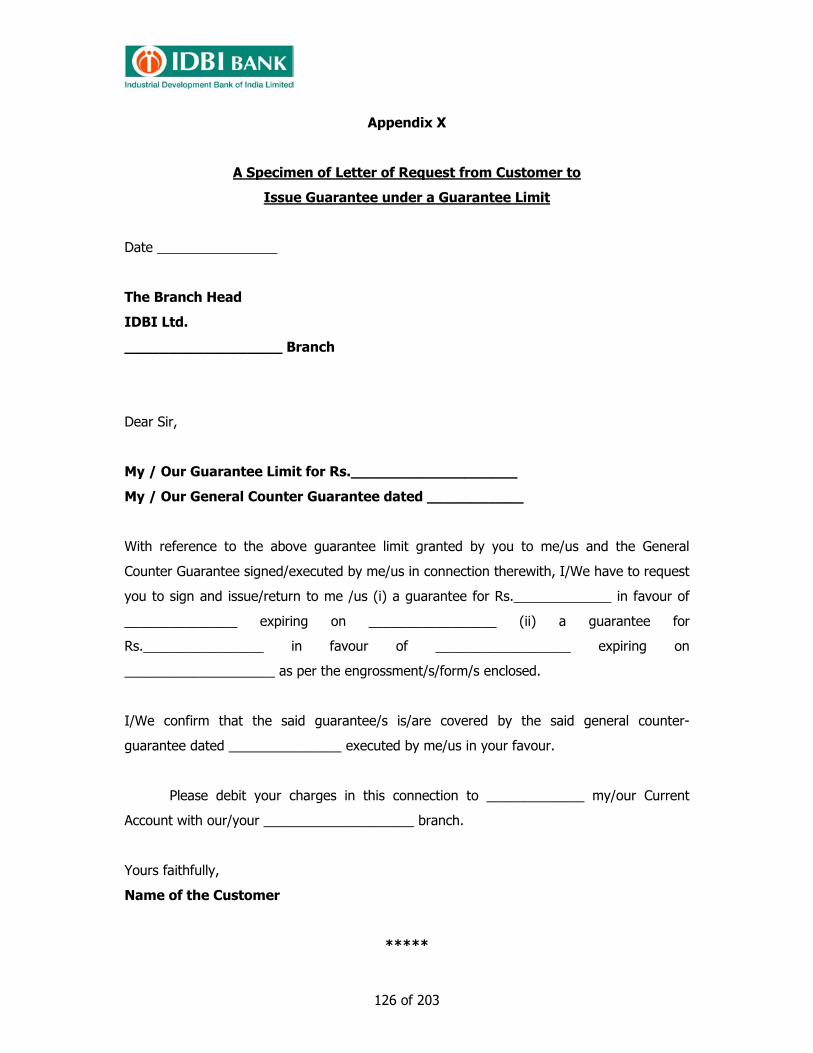

– Appendix X - A Specimen of Letter of Request from Customer to Issue Guarantee under a Guarantee Limit

126

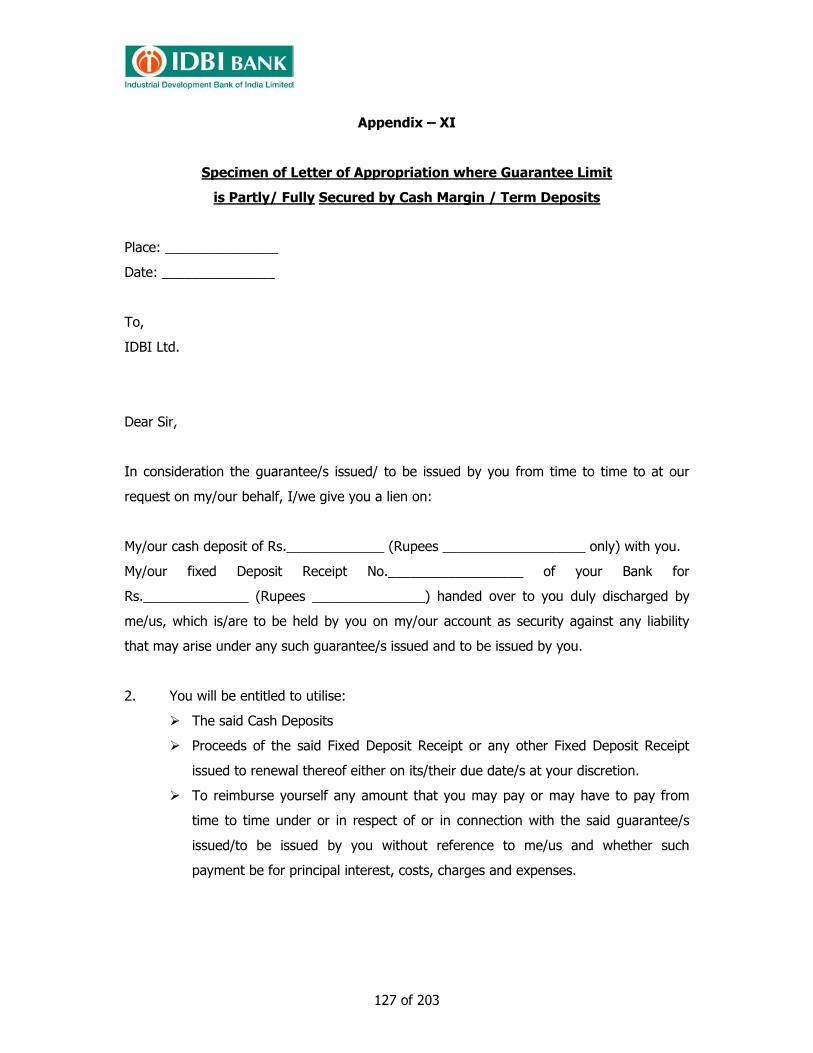

– Appendix XI - Specimen of Letter of Appropriation where Guarantee Limit if Partly / Fully Secured by Cash Margin / Term Deposits

127

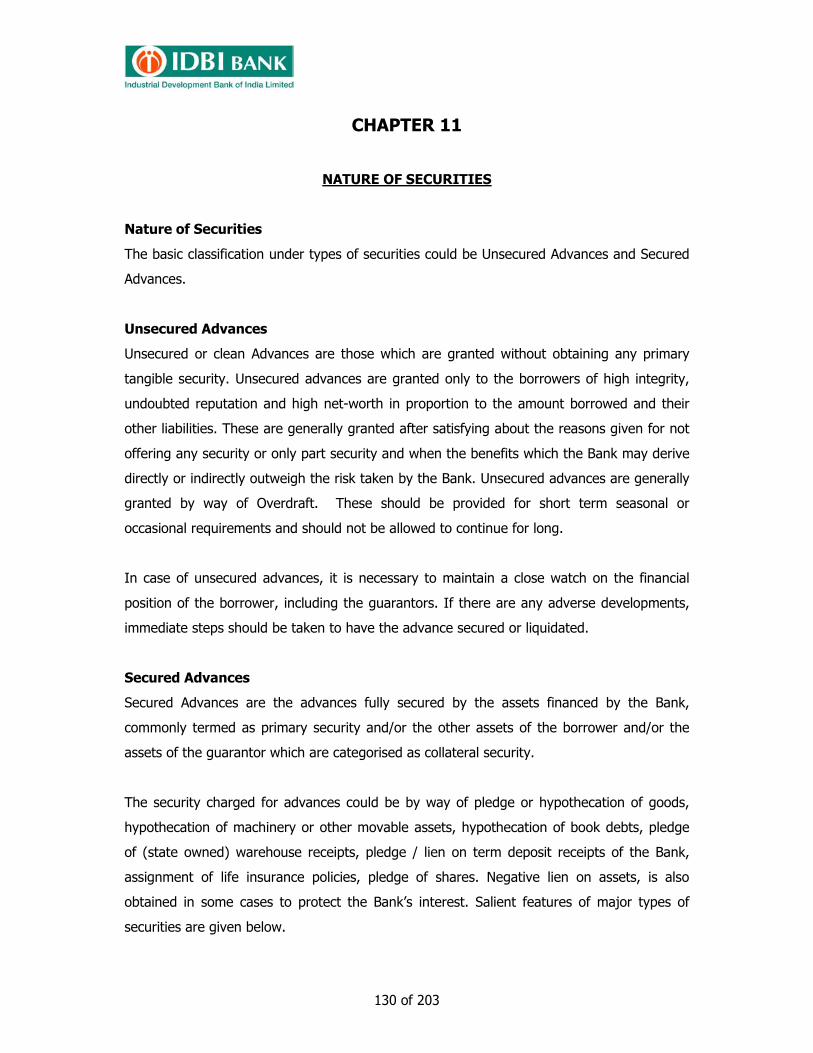

– Appendix XII - Format of Counter Guarantee 129 11 Nature of Securities 130 – 149

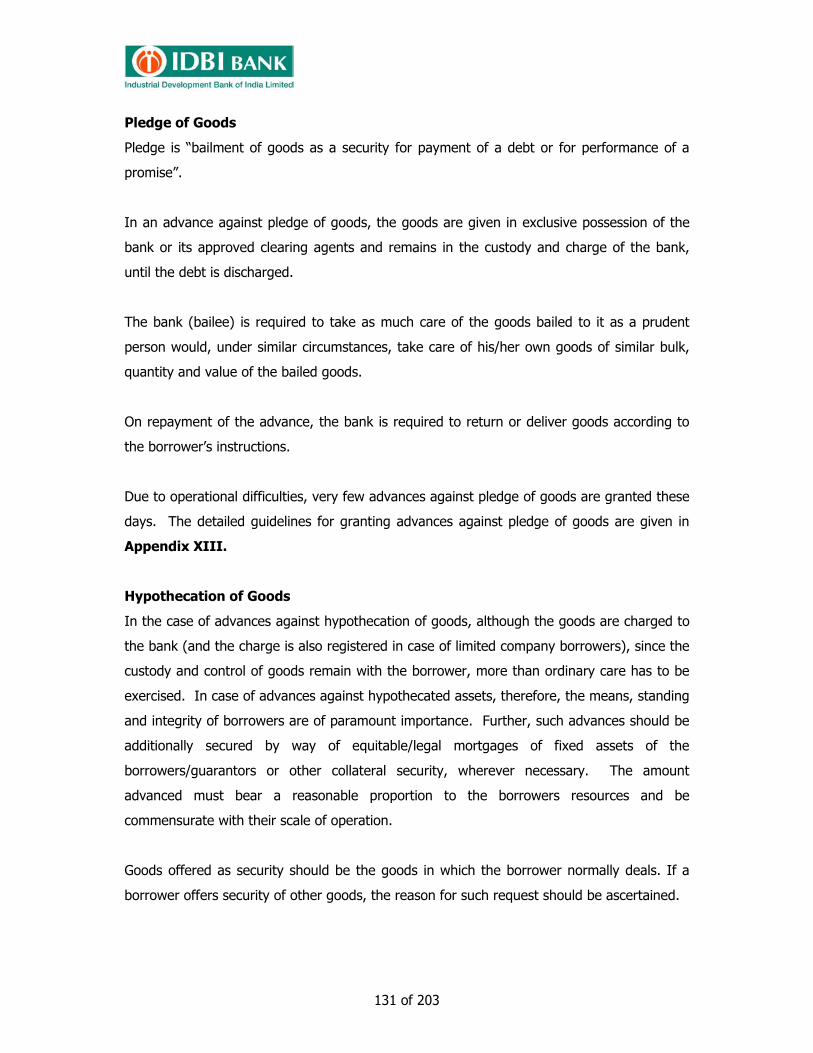

– Unsecured Advances – Secured Advances – Appendix XIII - Guidelines for Advances against Pledge of

Goods 140

– Appendix XIV - A specimen of stamped Letter of Undertaking to be obtained from the Processing Unit

145

– Appendix XV – Specimen letter of Negative Lien 147 – Annexure IV – Record of Pledge of Goods 148 – Annexure V – Particulars of Commodity 149

2032032032032032036 6

6 of 203

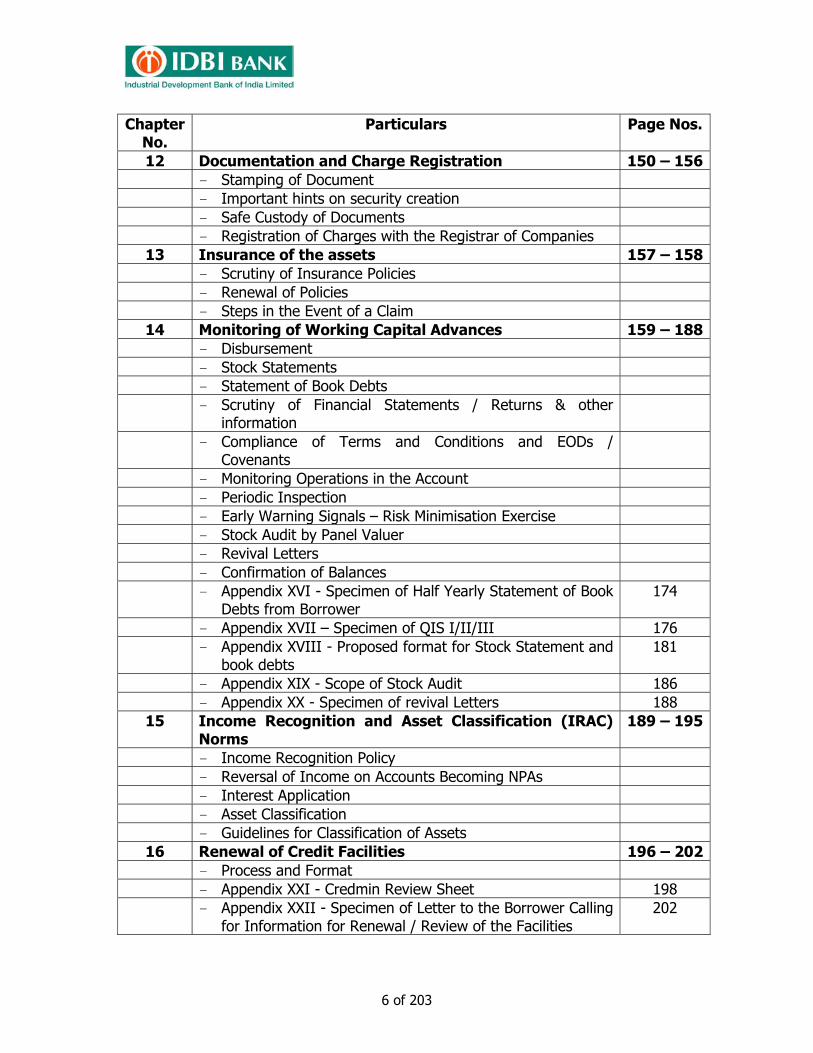

Chapter No.

Particulars Page Nos.

12 Documentation and Charge Registration 150 – 156 – Stamping of Document – Important hints on security creation – Safe Custody of Documents – Registration of Charges with the Registrar of Companies

13 Insurance of the assets 157 – 158 – Scrutiny of Insurance Policies – Renewal of Policies – Steps in the Event of a Claim

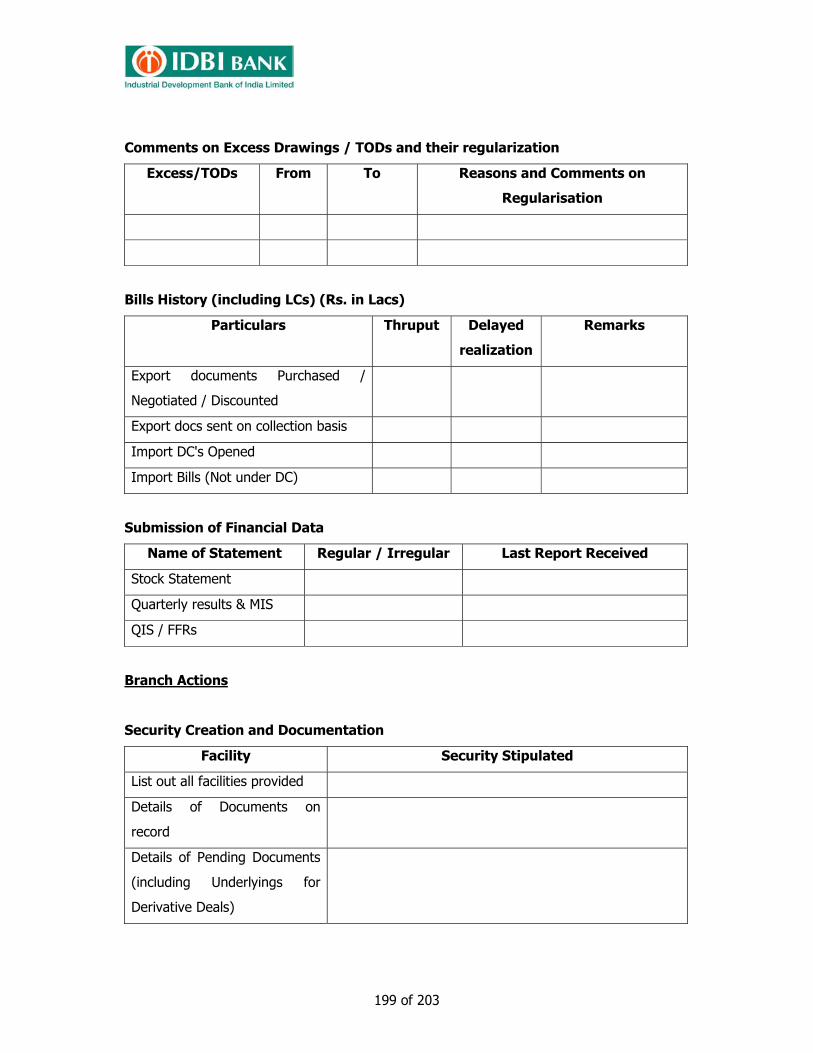

14 Monitoring of Working Capital Advances 159 – 188 – Disbursement – Stock Statements – Statement of Book Debts – Scrutiny of Financial Statements / Returns & other

information

– Compliance of Terms and Conditions and EODs / Covenants

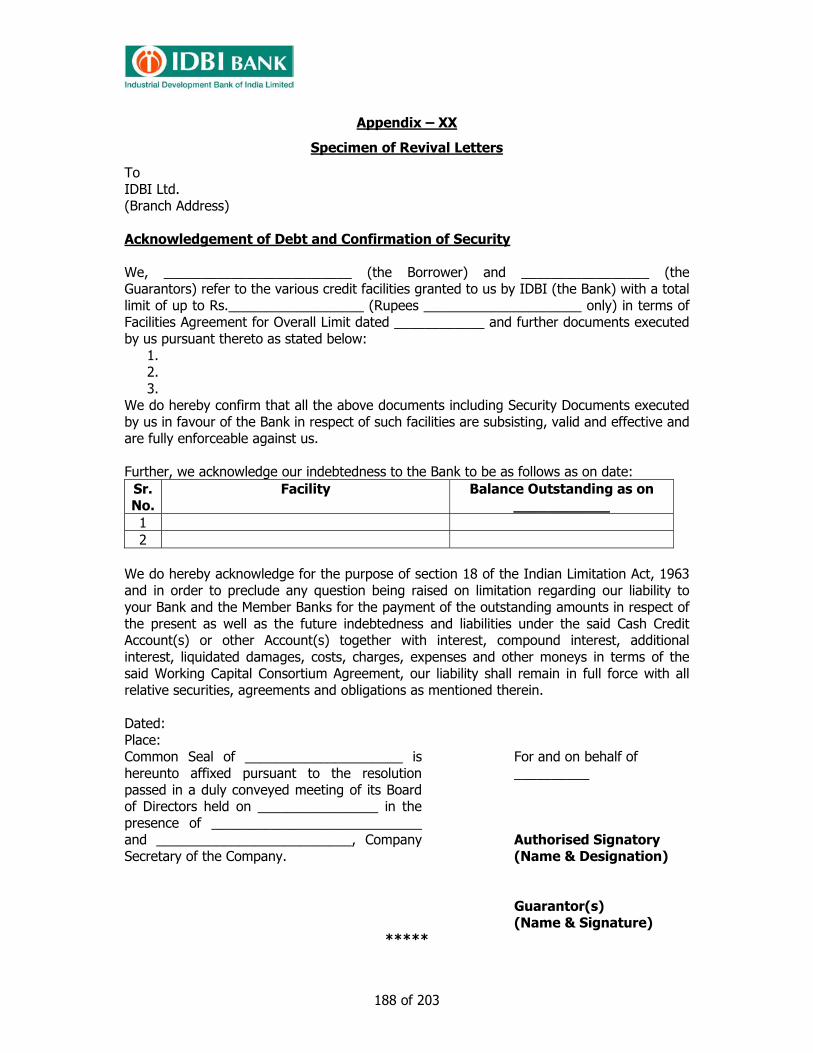

– Monitoring Operations in the Account – Periodic Inspection – Early Warning Signals – Risk Minimisation Exercise – Stock Audit by Panel Valuer – Revival Letters – Confirmation of Balances – Appendix XVI - Specimen of Half Yearly Statement of Book

Debts from Borrower 174

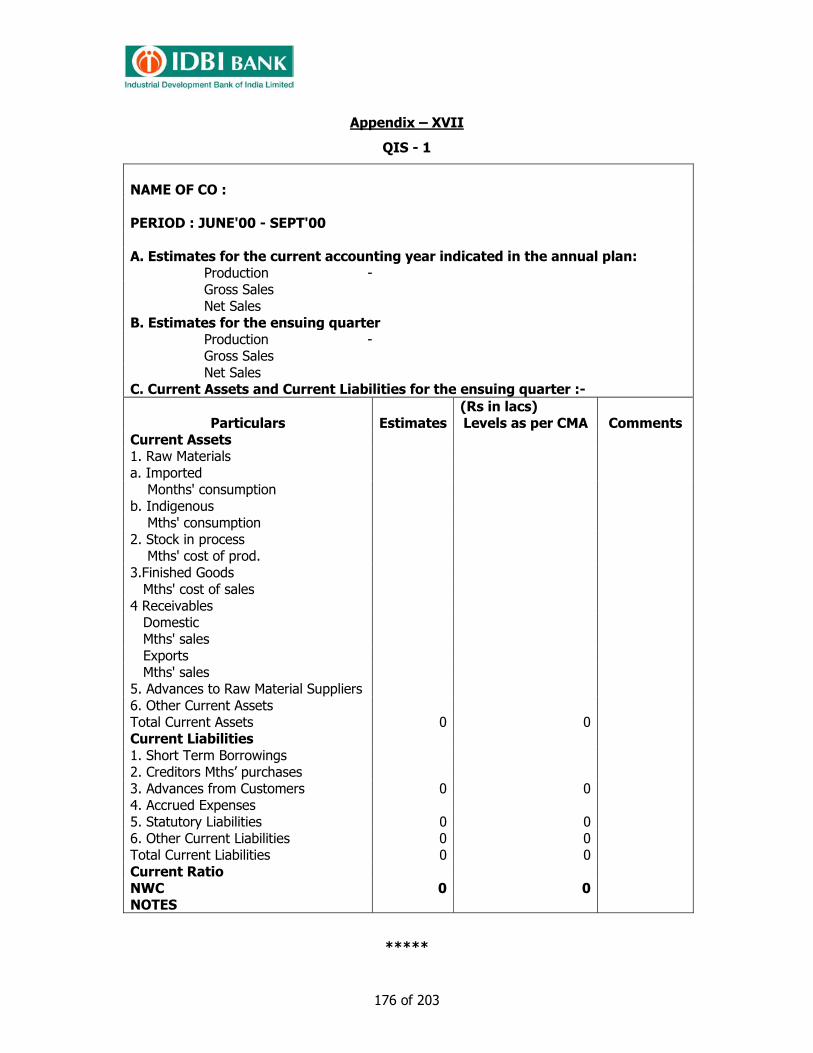

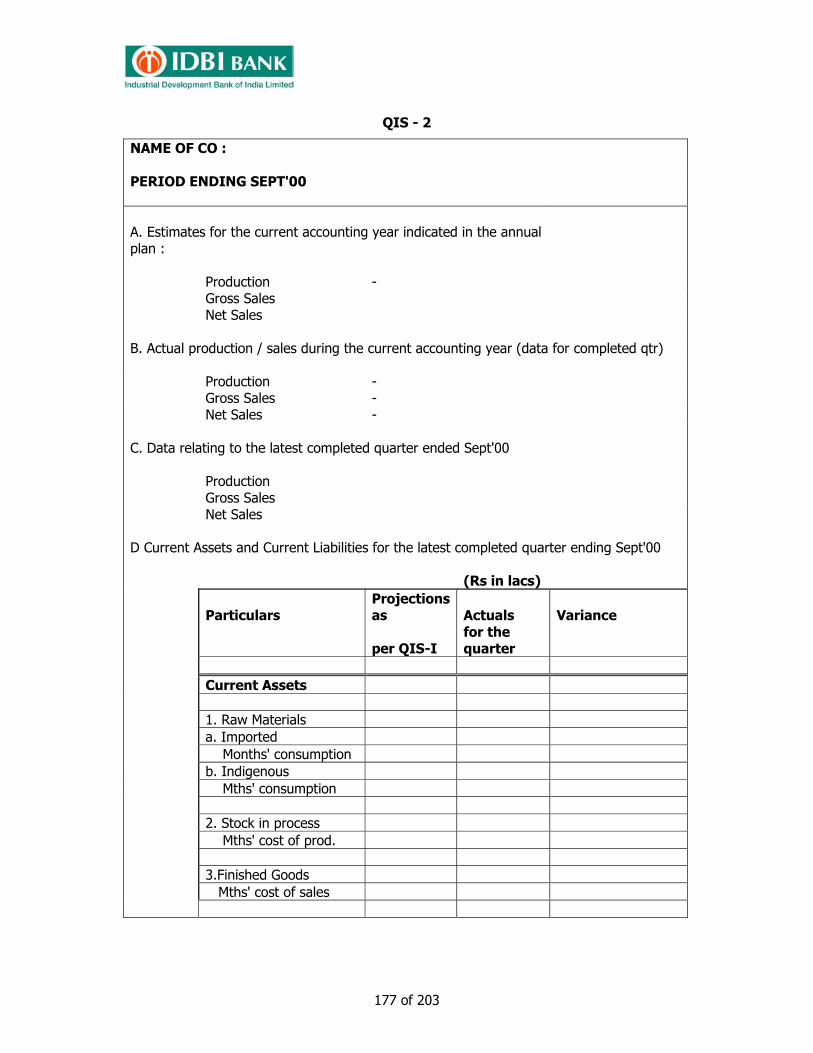

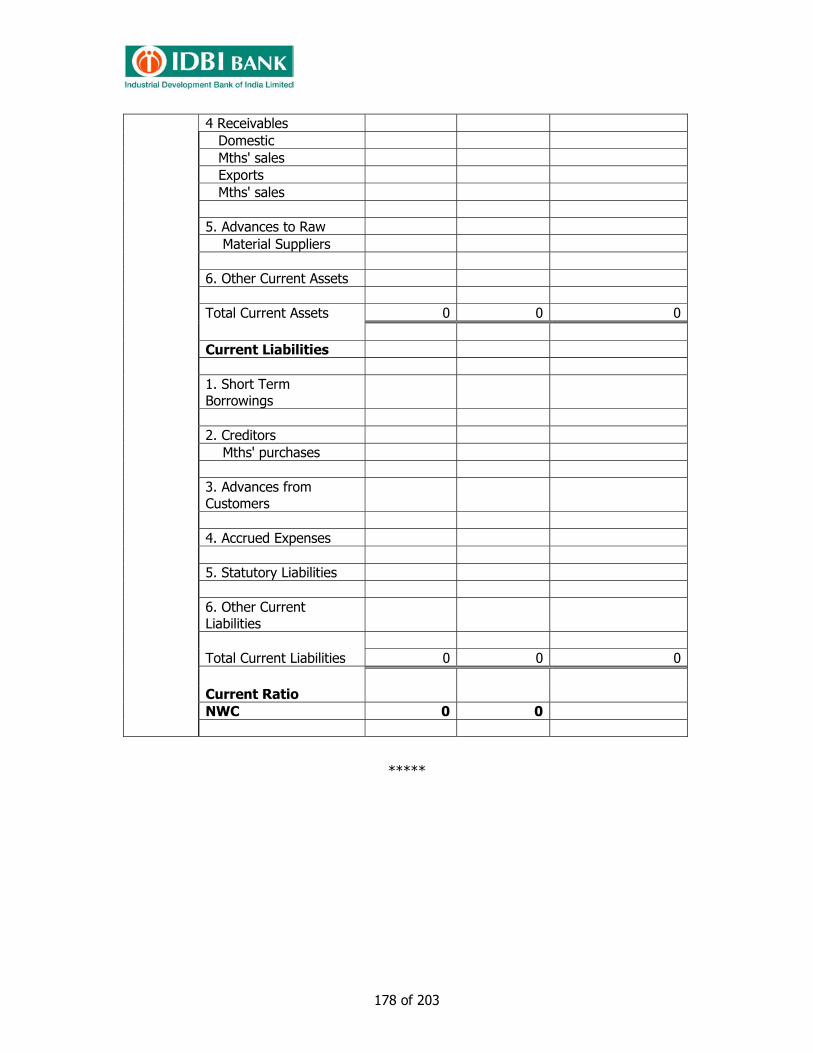

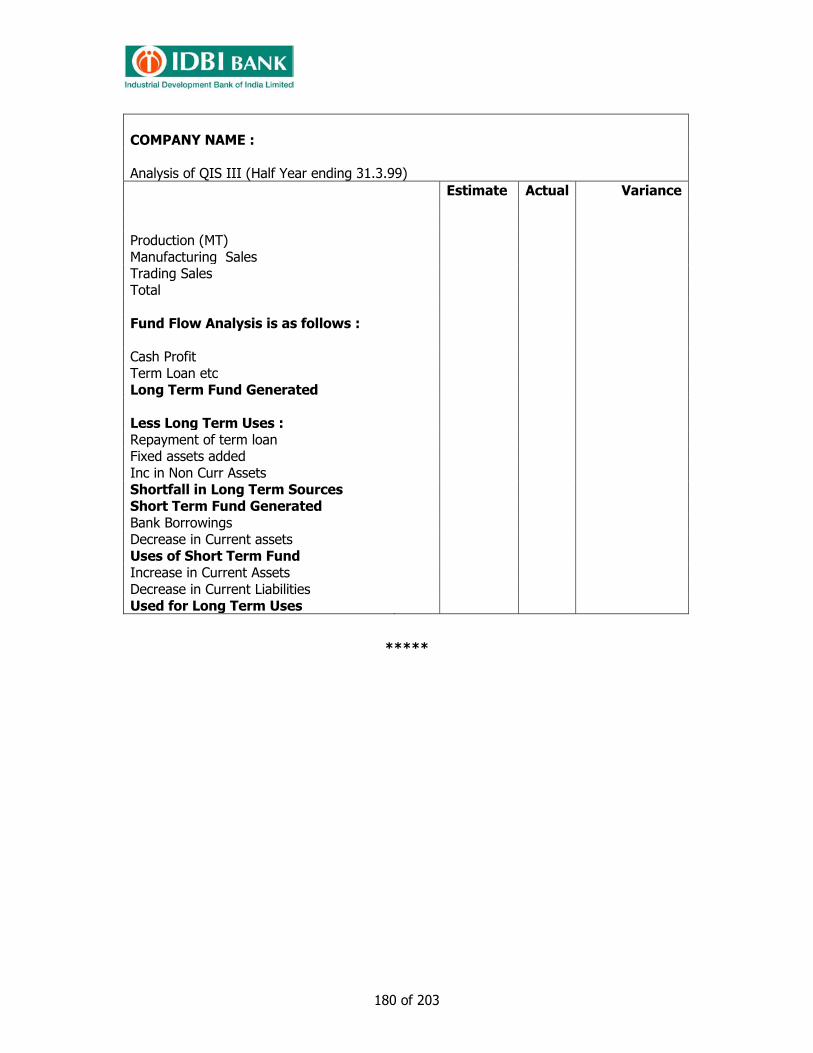

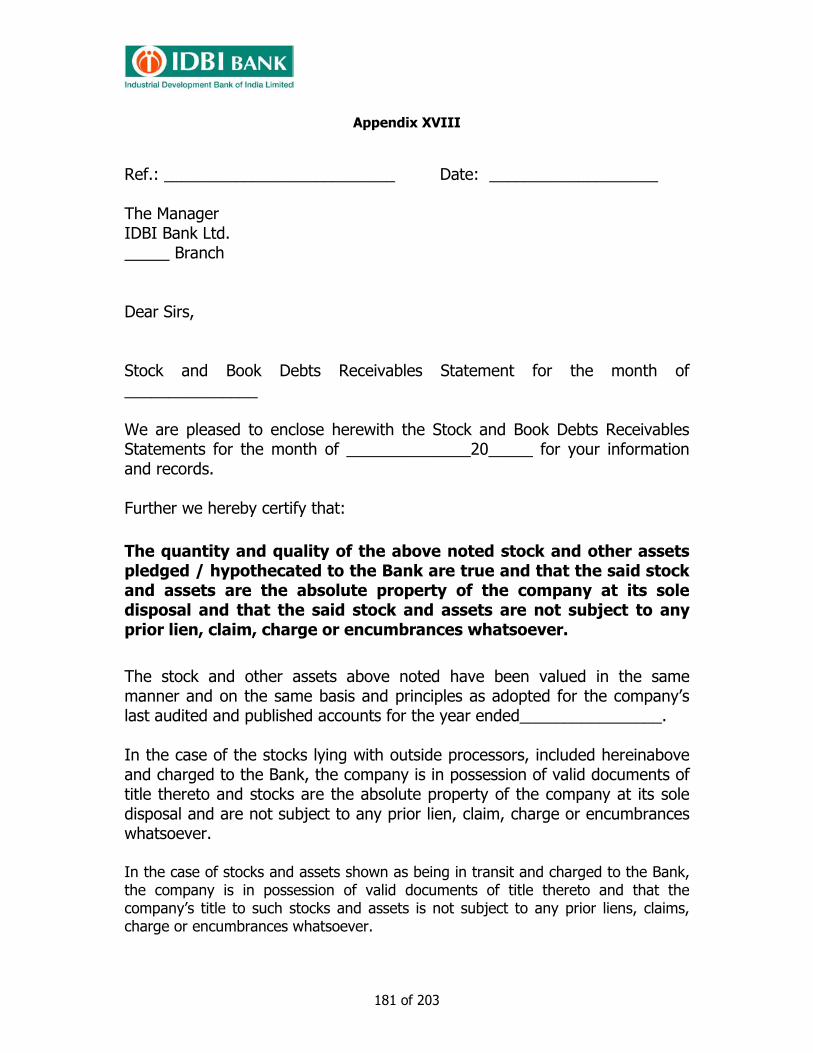

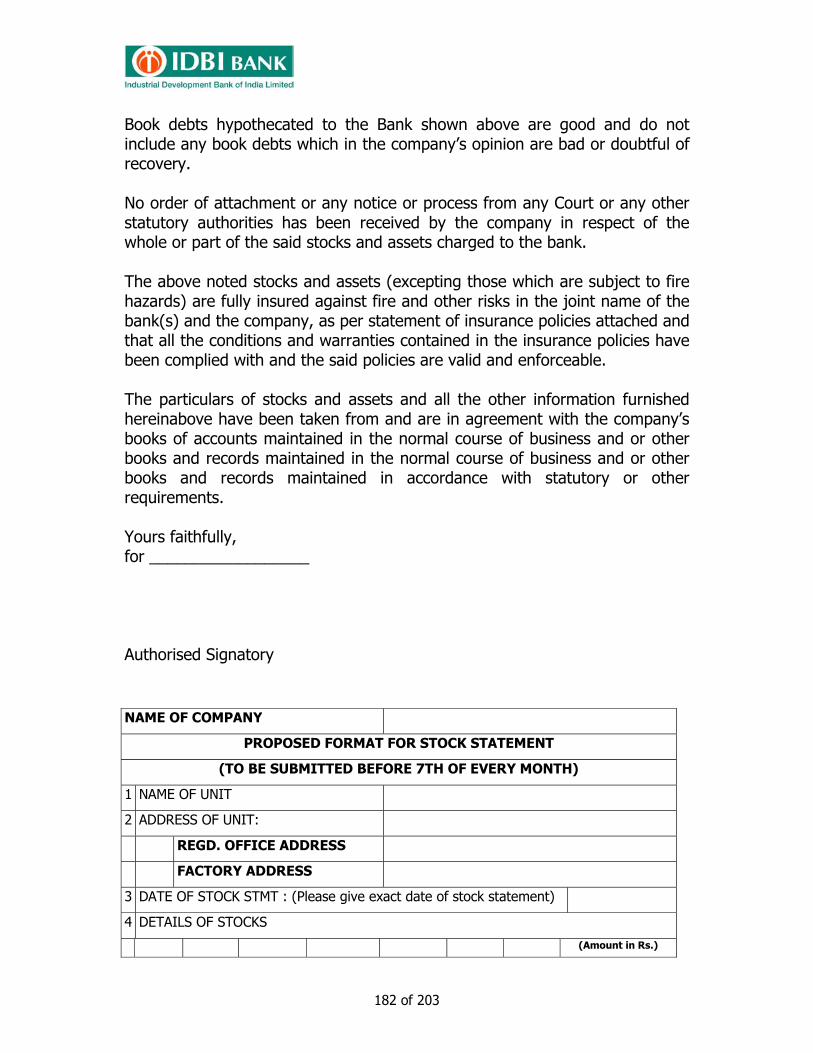

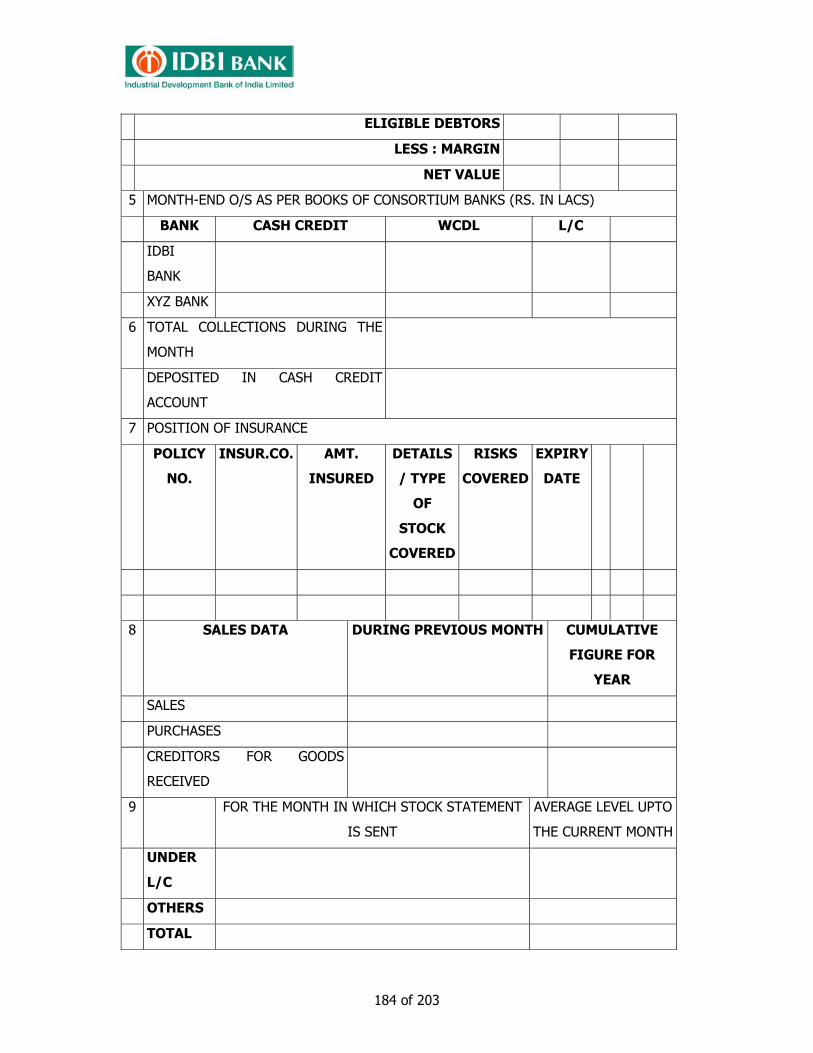

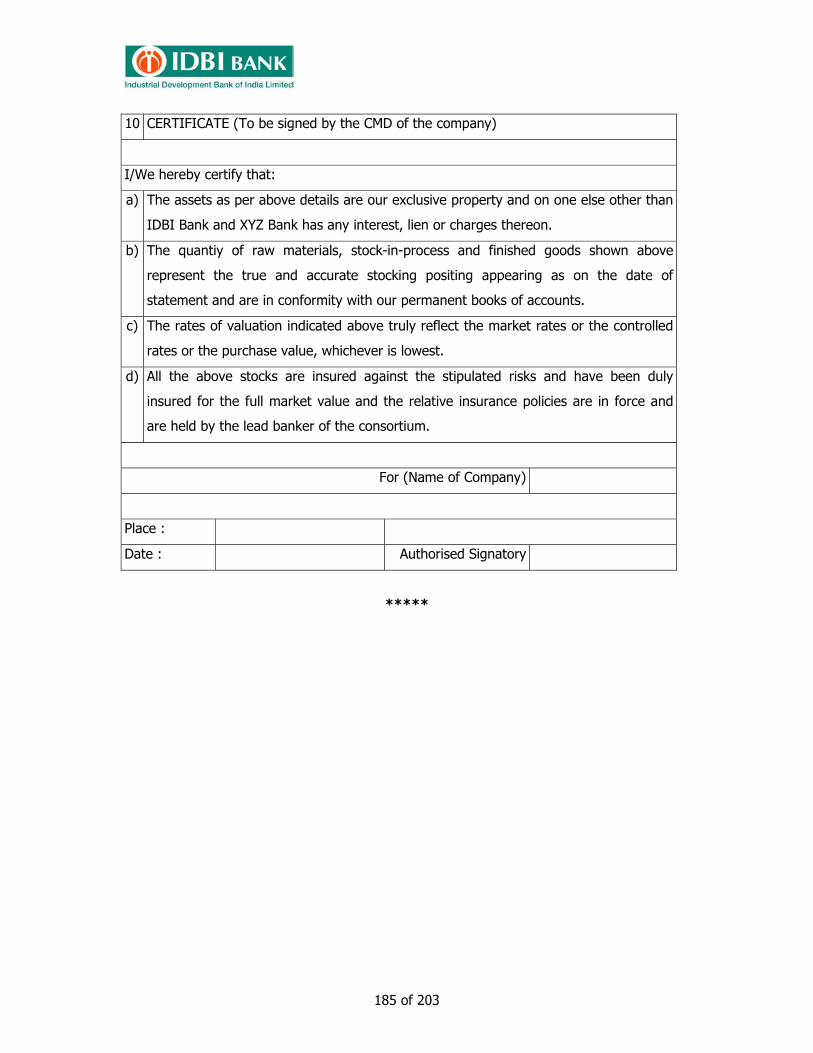

– Appendix XVII – Specimen of QIS I/II/III 176 – Appendix XVIII - Proposed format for Stock Statement and

book debts 181

– Appendix XIX - Scope of Stock Audit 186 – Appendix XX - Specimen of revival Letters 188

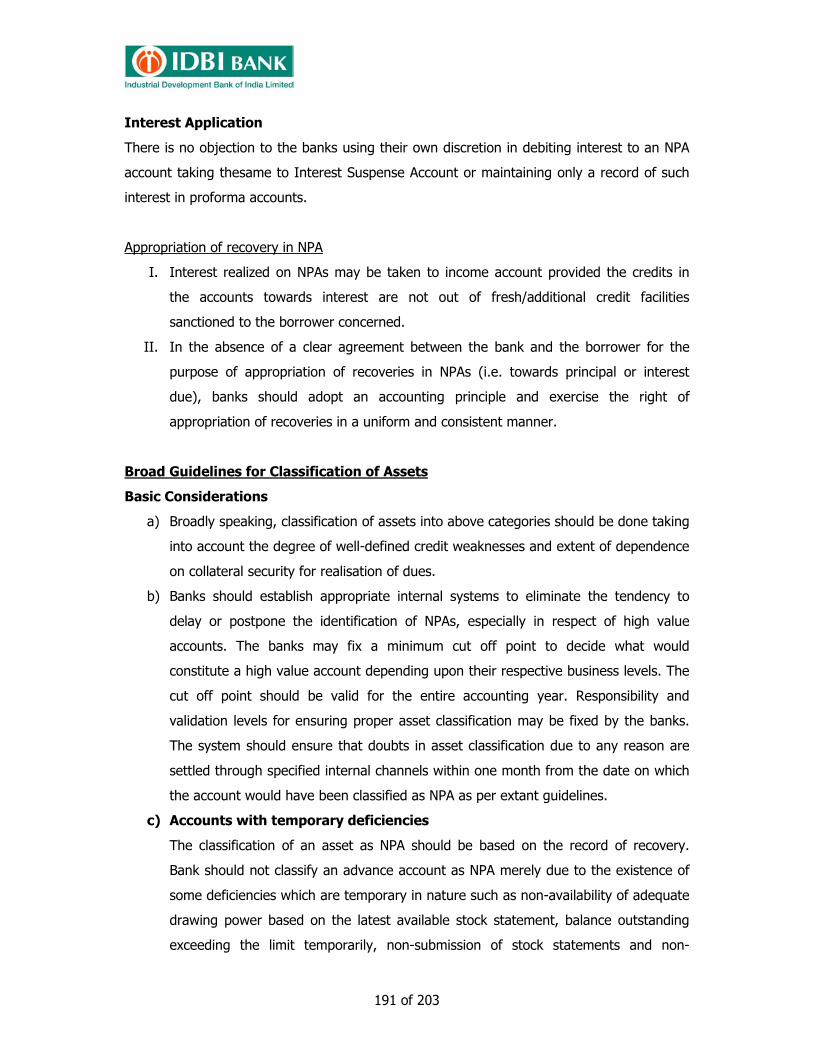

15 Income Recognition and Asset Classification (IRAC) Norms

189 – 195

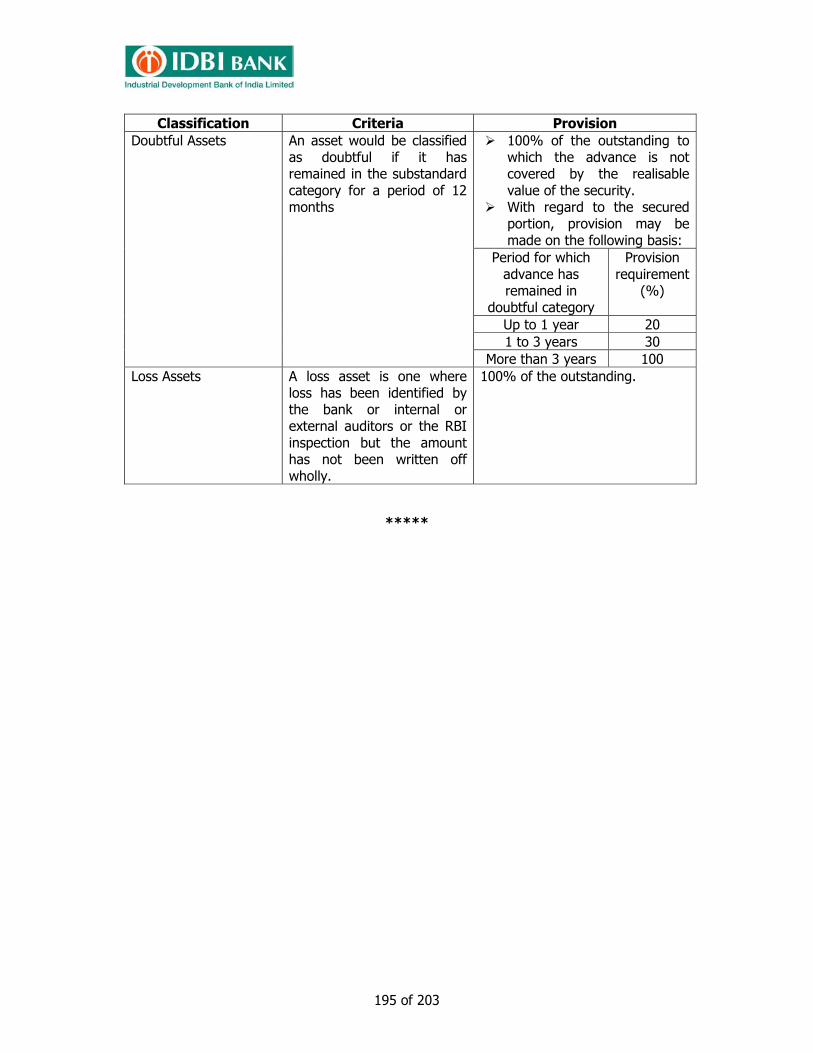

– Income Recognition Policy – Reversal of Income on Accounts Becoming NPAs – Interest Application – Asset Classification – Guidelines for Classification of Assets

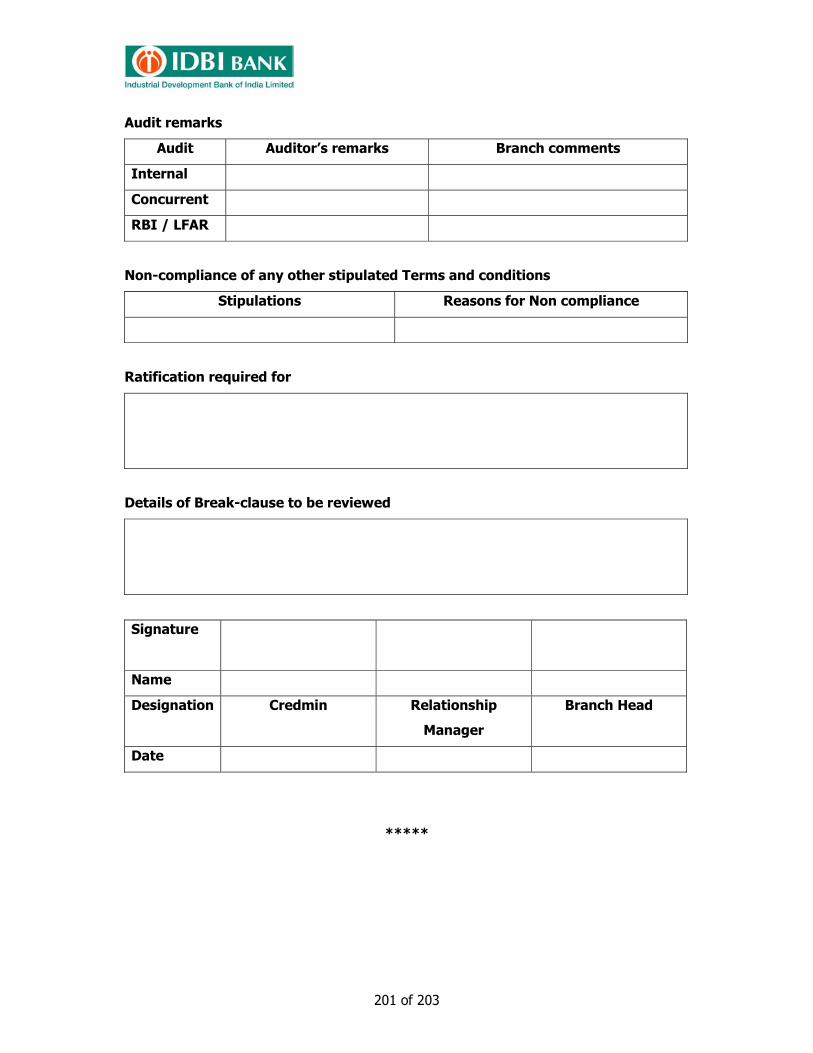

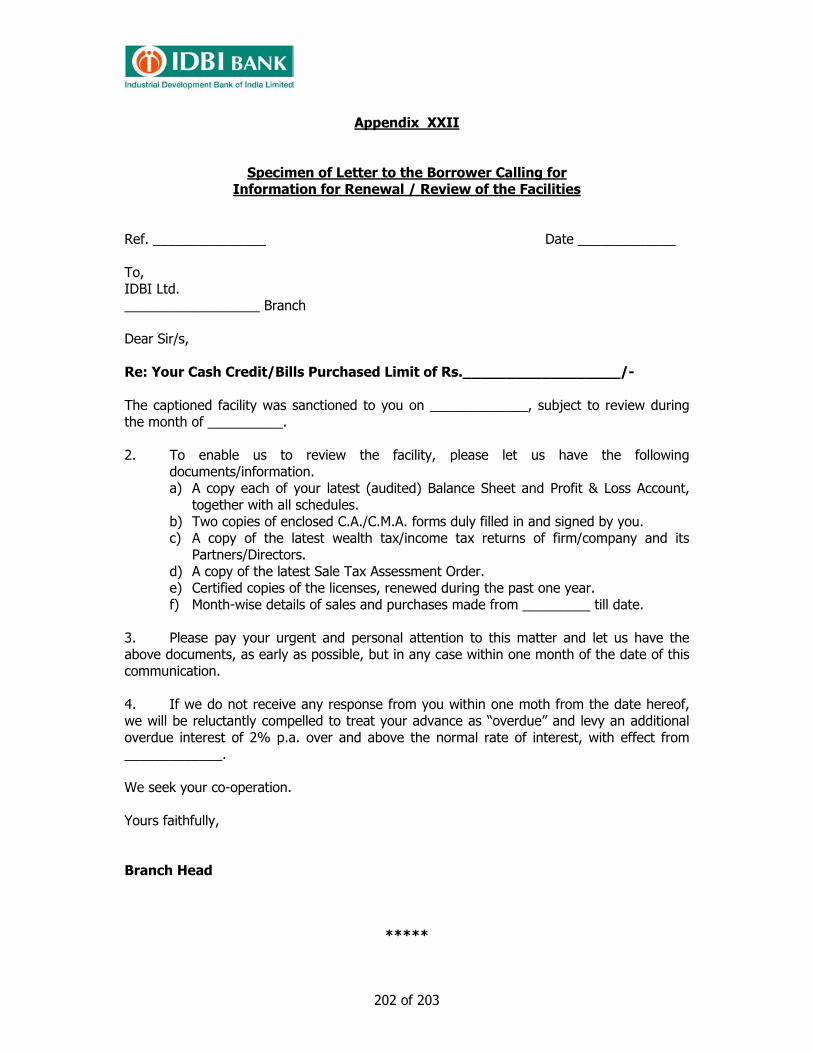

16 Renewal of Credit Facilities 196 – 202 – Process and Format – Appendix XXI - Credmin Review Sheet 198 – Appendix XXII - Specimen of Letter to the Borrower Calling

for Information for Renewal / Review of the Facilities 202

2032032032032032037 7

7 of 203

CHAPTER 1

BASIC PRINCIPLES OF LENDING

Objectives of Lending

The basic objectives of lending are to grant credit facilities to the entities:

i. For a defined purpose.

ii. To deploy the Bank’s resources in a profitable manner and to achieve the statutory

and regulatory norms.

Basic Principles

To achieve these objectives, the Bank has to follow a prudent policy and conduct the

business on the basis of sound principles of lending namely, Safety, Liquidity and

Profitability. These aspects are further elaborated below.

Safety

Safety of the funds lent has to be ensured with respect to:

i. Borrower

The Borrower should have the means, ability and willingness to repay the advance

along with interest as per the terms of finance. These depend on factors like tangible

assets, income generating potential, operational efficiency and integrity of the

borrower. It is therefore imperative to make a thorough investigation into the means,

character, antecedents, respectability and capacity of the borrower before allowing

them any credit facilities and by keeping a close watch on their dealings and on the

operations in their accounts during the period of advance. Character - Indicating the

borrower’s honesty, integrity, business ethics, regularity, dependability, reputation

and promptness to keep promise.

ii. Profitability

Notwithstanding the socio-economic objectives of lending, the fact remains that

banks are profit making institutions. They have to be run on commercial

considerations to meet the expectations of the shareholders and ensure their healthy

growth. The Bank should, therefore, have a proper mix of credit portfolio which

would earn sufficient income to enable it to defray the cost of funds, meet

2032032032032032038 8

8 of 203

establishment and other expenses, provide for contingencies and risky assets, build

reserves and pay dividend to the shareholders.

iii. Liquidity

As the funds lent mostly belong to the depositors and as the Bank should always be

in a position to meet the demands of the depositors, it is essential that the loans and

advances are recoverable in full on demand or within a reasonable period. It is,

therefore, necessary to ensure that the funds lent are backed by securities that are

easily marketable and realisable. Matching of Assets and Liabilities is very critical

from this point of view.

iv. Security

Though repayment in the ordinary course must come out of the surplus from

business of the borrower, the security aspect cannot be neglected. Security serves as

a cushion or comfort to fall back upon in the event on the borrower’s failure or

default in the repayment of advance. Adequate tangible security ensures safety of

advance. The assets purchased out of the credit facilities are obviously the first to be

taken. It is a safeguard against disposal/alienation of such securities. Wherever

necessary, the advances could also be secured by obtaining collateral securities.

*****

2032032032032032039 9

9 of 203

CHAPTER 2

INTRODUCTION TO WORKING CAPITAL

What is Working Capital

For running an industry or a Concern, two types of capital are required viz., fixed capital and

working capital. Fixed Capital is utilized for acquiring the fixed assets such as land, building,

plant & machinery, etc., and to meet capital expenditure connected with the setting to keep

the wheels moving up of the industry or Concern. But by themselves, these fixed assets

would not produce / earn anything. They have to be run / worked for production. This

requires enough liquid sources, viz., working capital

Working Capital represents the money that is required for purchase / stocking of raw

materials, payment of salary, wages, power charges etc, and also for financing the gap

between the supply of goods and the receipt of payment thereafter.

In other words, Working Capital Finance is the fund required to meet the cost involved

during the working capital cycle or operating cycle.

Operating Cycle or Working Capital Cycle

Working capital cycle of a manufacturing activity starts with the acquisition of the raw

materials / stores & spares and ends with realisation of cash for finished goods. The cycle is

long in some cases and short in other cases depending upon the nature of business. In

manufacturing units, Working capital cycle comprises of purchase of raw materials either in

cash or credit basis, converting raw materials into stock in process and then into finished

goods and transformation of finished goods into book debts / cash.

In respect of trading concerns, operating cycle represents the period involved from the time

the goods and services are procured and the same are sold and realized. The working

capital cycle is illustrated as follows:

20320320320320320310 10

10 of 203

The total working capital requirements for Industrial Units will depend upon the holding

period of assets and the operation of the cycle. Thus, the stocking of raw materials may be

equivalent to one or three months’ raw materials consumption for most industries, but say

nil for a sugar mill.

As regards the operating cycle, the duration of each stage of process cycle is first decided

upon having regard to the function it is supposed to perform. The conversion of raw

materials into finished goods depends upon the technical requirements and manufacturing

facilities available. Similarly, the turnover of finished products and their transformation into

book debts, bills or cash could be related to factors like delivery schedule, business customs

and competition. Thus, the working capital cycle of a manufacturing activity starts with the

acquisition of raw materials and ends with realization of cash for finished goods.

The cycle is long in some cases and short in others, depending upon the nature of business.

Cycle is fast in consumer goods industries and slow in capital goods industries. Cycle is

short in case of perishables such as food articles, beverages, fruits, fish, eggs, etc. Cycle is

long in the case of tobacco, distilling, timber, steel, etc. Seasonal industries like

Cash/Sundry Creditors

Raw Materials / Stores & Spares

Sundry Debtors

Sales

Stock-in-Process

Finished Goods

20320320320320320311 11

11 of 203

manufacturers of umbrella, woollen fabrics, fans, refrigerators, etc., require higher stocks in

some months and bare minimum in remaining months.

During the cycle, funds are blocked in various stages of current assets, viz., cash itself,

inventory (consisting of raw materials, stock in process, finished goods) and receivables.

These require finance. Finance involves costs. Quicker the cycle more is the turnover

normally and longer the cycle, the less is the turnover. Stagnation in any area effects

turnover and profitability.

Working capital cycle vary from industry to industry depending upon its nature of business.

Factors which affect working capital cycle are:

1) Policy of the management on production and sales

2) Inventory management/ Receivables management

3) Nature of manufacturing activity/process

4) Policy of extending credit for purchases as well as sales

5) Government policy

6) Type of product

The above factors are only illustrative and not exhaustive.

*****

20320320320320320312 12

12 of 203

CHAPTER 3

MANAGEMENT OF WORKING CAPITAL

Management of working capital

Management of working capital involves management of current assets, current liabilities

and Net working capital.

Current Assets

Current Assets are convertible assets, liquid assets or floating assets. They change their

form every now and then and ultimately are converted into cash. Current assets are such

assets which are reasonably expected to be realised into cash within a period of 12 months.

They indicate short-term deployment of funds and form Gross Working Capital.

Current Assets mainly consist of:

1) Cash and bank balance

2) Stock in trade consisting of raw materials, stock in process, finished goods, stores,

packing materials'

3) Book debts: including bills purchased & discounting (only upto 180 days)

4) Investments (Short term)

5) Cash margin from non fund based limit (L/C / guarantee) may be treated as a part of

current assets. and

6) Other loans and advances, etc.

The quantum and period, for which each current asset is held, should be reasonable and

related to the requirement. Any asset held in excess, burdens the business with

unnecessary interest and costs on such borrowings.

Cash and Bank Balance tied to or earmarked for long term use, for example for a future

expansion / diversification programme or investment outside business, should be excluded

from Current Assets. Such part of the Cash and Bank Balances should be shown under

Other Non-Current Assets.

20320320320320320313 13

13 of 203

Holding of Cash or Bank Balances (or marketable securities / investments) beyond the

normal needs of business necessitates critical evaluation. It is a common banking practice

that a business can not be granted bank credit, if it has surplus / idle cash lying with it.

Book Debts, including Bills Purchased and Discounted outstanding within the normal credit

period allowed by the firm or six months, whichever is lower, should be treated as Current

Assets – Receivables.

A break-up of the Receivables age-wise and party-wise may be quite informative. Overdue

debts, which are considered realizable, should be classified into Other Non-Current Assets.

Debts which have doubtful realisability because of quality control disputes, depressed

market conditions, or because the debtors are not financially sound and can not pay in the

foreseeable future etc. should be shown under Intangible Assets, unless full provision has

been made for them in the accounts.

The basis of valuation of each item of inventory should be the invoice value / cost or market

value, whichever is lower. The period of holding of each item should conform to its demand

and supply position in the market, production requirements and ordering time. The quality

of stocks should satisfy the requirements of a good security. "Dead Inventory" i.e. slow

moving or obsolete items should be excluded. Only those stores and spares, which are of

consumable nature and are linked to the operating cycle, should be considered as Current

Assets. Machinery stores (with exception of certain items like consumable injection moulds

etc. in some industries) should be a part of Other Non-Current Assets, since these items are

included in the capital cost.

The following items should not be treated as Current Assets and the same may be classified

as Non-Current Assets.

1) Investments / loans to subsidiaries / associates (non-trade investments)

2) Other Investments (not marketable)

3) Overdue book debts (generally those more than six months old)

4) Deferred Receivables (maturity exceeding one year)

5) Others – fixed deposits with Government Departments, loans to directors /

employees / partners, advances (machinery suppliers), machinery stores, tools etc.

6) Cash margin held for deferred payment guarantee

20320320320320320314 14

14 of 203

Current Liabilities

Current liabilities are short term liabilities which are repayable within a year. They are

normally raised for meeting the working capital needs and to acquire current assets.

Current liabilities are the main source of finance for working capital and are normally

identified with the operating cycle of the business. Current Liabilities normally consists of:

1) Bank Borrowings for working capital

2) Other short term borrowings like Unsecured Loans, Inter Corporate Deposits etc.

3) Sundry Creditors (for goods, expenses and others including advance payment against

orders)

4) Term Loan / Debentures / Deferred Payments and Lease Rental instalments

repayable within a period of one year

5) Statutory Liabilities (due within one year)

6) Other current liabilities and provisions (accrued expenses of wages, interest,

unclaimed dividend and provision for taxation etc.)

Working Capital Gap

This represents excess of current assets over current liabilities excluding bank borrowings.

A part of the Current Assets are financed by Current Liabilities (other than bank borrowings).

The remaining portion of current assets which requires financing is called as working capital

gap. Banks do not grant advance to the full extent of working capital gap. It is always

desirable rule that the borrower has to finance a part of working capital gap out of either

capital or long term sources which reflects his continued commitment to the business that is

necessary for the survival of the unit.

Net Working Capital

This represents excess of current assets over current liabilities (including bank finance). It

indicates the margin or long term sources provided by the borrower for financing a part of

the current assets. For successful operation of a business, Current Assets should be more

than the Current Liabilities. It ensures continuous liquidity (current assets are prone to price

fluctuations and should, therefore, have an in-built margin to absorb changes) and owner's

stake in the current business operations.

20320320320320320315 15

15 of 203

Current Ratio

The ratio of current assets to current liabilities is known as Current Ratio. It indicates the

liquidity position whereby the capacity of unit to pay the creditors and short-term liabilities is

determined. It is generally expected that the customer should meet about 25% of its

Working Capital requirements or Current Asset from long term sources. Thus, normally, the

current ratio should be minimum 1.33.

The current ratio indicates only the quantitative coverage and by itself does not give any

indication as to quality of current assets and current liabilities. The adequacy of the ratio

should, therefore be judged by examining the quality of the components of current assets

and current liabilities.

Consideration of factors such as valuation of stocks and guidelines on inventory, sundry

debtors, borrowing and marketability of investments would substantially assist in

determining the quality of the ratio. If a scrutiny of current assets reveals that they contain

slow moving/non moving stock of raw materials, work in process, finished goods and non

recoverable debtors, and if there are current liabilities requiring urgent attention/payment,

even a high current ratio cannot be deemed adequate as liquidity may be affected.

Similarly, a certain fall in the price of materials would shrink the value of stocks thereby

narrowing the margin of safety to creditors/banks. It is therefore always necessary to make

an in depth study of the current ratio of the unit and not to take it at is face value. It is also

essential that proper classification of current assets and current liabilities is ensured to arrive

at need based permissible bank finance.

*****

20320320320320320316 16

16 of 203

CHAPTER 4

METHODS OF ASSESMENT

Consistent with the policy of liberalization, in April 1997, RBI withdrew the prescription in

regard to assessment of working capital needs, based on MPBF, enunciated by Tandon

Committee. Thus banks are given greater operational freedom for dispensation of credit.

Banks are also free to evolve their own method of assessing working capital requirements of

the borrowers within the prudential guidelines and exposure norms already prescribed.

However the banks continue to adhere to various guidelines under Credit Monitoring

Arrangement (CMA) for sanction of credit proposals and classification of current assets and

liabilities as they still hold good and valid.

Working capital to business/industry is what blood is to human body. Short supply and

excess supply will have adverse effects on the business.

Effects of short supply: It shall bring crunch in the working of the unit and thereby failure

to utilize the created capacities which result in short fall in production, short fall in sales,

business failure, under utilization of men, materials, machinery and management, frustration

of the objective of enterprise, inability to accept attractive opportunities etc.

Effects of excess supply - Builds up huge inventory, book debts, which is not required for

their normal operations. Complacency and deteriorating management efficiency,

extravagance, unhealthy speculation unwarranted expansion, Liberal Dividend Policy,

Diversion of funds, etc.

The level of investment in an operating cycle depends upon changes in:

1) Terms of production and sales other factors remaining constant

2) The price of raw materials

3) Lead time for producing raw materials

4) The pattern of manufacturing expenses

5) The process time

6) Policy of extending credit (both on purchase as well as sales) etc.

20320320320320320317 17

17 of 203

Assessment of working capital shall normally based on the following:

1) Production / Processing cycle of the industry

2) Size of the business and quantum of working capital requirements

3) Financial and managerial capability of the borrower and the various parameters

relating to the borrower.

4) Prevailing mandatory instructions of RBI

5) The trade and industry practice prevailing and other objective factors

Assessment of the Working Capital requirement of a borrower shall generally be made under

any one of the following three methods:

1) Turnover method (P R Nayak Committee recommendation)

2) Maximum Permissible Bank Finance (MPBF) System (Tandon/Chore Committee

recommendation)

3) Cash Budget System

Turnover Method

Under this method working capital limit shall be computed at 20% of the projected gross

sales turnover accepted by the bank. This system is normally applicable to traders,

merchants, exporters who are not having a pre determined manufacturing / trading cycle.

Under the turnover method bank should ensure that maintenance of minimum margin on

the projected annual sales turnover. Normally 25% of the estimated gross sales turnover

value shall be computed as working capital requirements, of which 20% shall be provided

by the bank and the balance 5% by way of promoter contribution towards margin money.

However if the available net working capital (NWC) is more, the same shall be reckoned for

assessing the extent of bank finance and lower limit/s can be considered. The turnover

method may be applied for sanction of fund based working capital to the borrowers

requiring working capital facility upto Rs 500 lakhs from the banking system for SSI units. In

case of a traders, while bank finance could be assessed at 20% of the projected turnover,

the actual drawals should be allowed on the basis of drawing power determined after

deducting unpaid stocks. Under this method current ratio would be 1.25.

20320320320320320318 18

18 of 203

Example

Projected accepted annual Gross Sales Turnover - Rs.10.00 lacs

25% of the above - Rs. 2.50 lacs

Minimum margin to be provided by the borrower - Rs. 0.50 lacs

(or NWC, whichever is higher)

Bank finance - Rs. 2.00 lacs

(or lesser, in case NWC is higher)

As the working capital requirement are linked to projected turnover, reasonableness of the

projected annual turnover of the applicant company should be analysed by keeping in view

of past performance of the unit, the orders on hand, installed capacity of the units, power,

availability of raw materials and other infrastructural facilities . In respect of a new unit

projected turnover should be analysed with regard to installed capacity, marketability of the

products, performance of the similar unit in the industry, background of the promoters etc.

The projected turnover / output value is the gross sales which include excise duty. The

assessment of working capital credit limits should be done both as per projected turnover

basis and traditional methods based on production/processing cycle (MPBF). If the credit

requirement based on MPBF method is higher than the one assessed on projected turnover

basis, the same may be sanctioned. On the other hand, if the assessed credit requirement

is lower than the one assessed on projected turnover basis, while the credit limit can be

sanctioned at 20% of the projected turnover, drawals may be allowed basing on actual

drawing power after excluding unpaid stocks.

In addition to the above, any other short term / adhoc Working Capital facilities to meet the

emergent needs of the borrowers and other seasonal imperfections can be considered by

the sanctioning authority, subject to the borrower submitting the required details in support

of the need/justification and the sanctioning authority is convinced / satisfied with the

borrower requirements. Such short term finance / adhoc facilities shall be permitted for

short term, say upto 3-4 months.

20320320320320320319 19

19 of 203

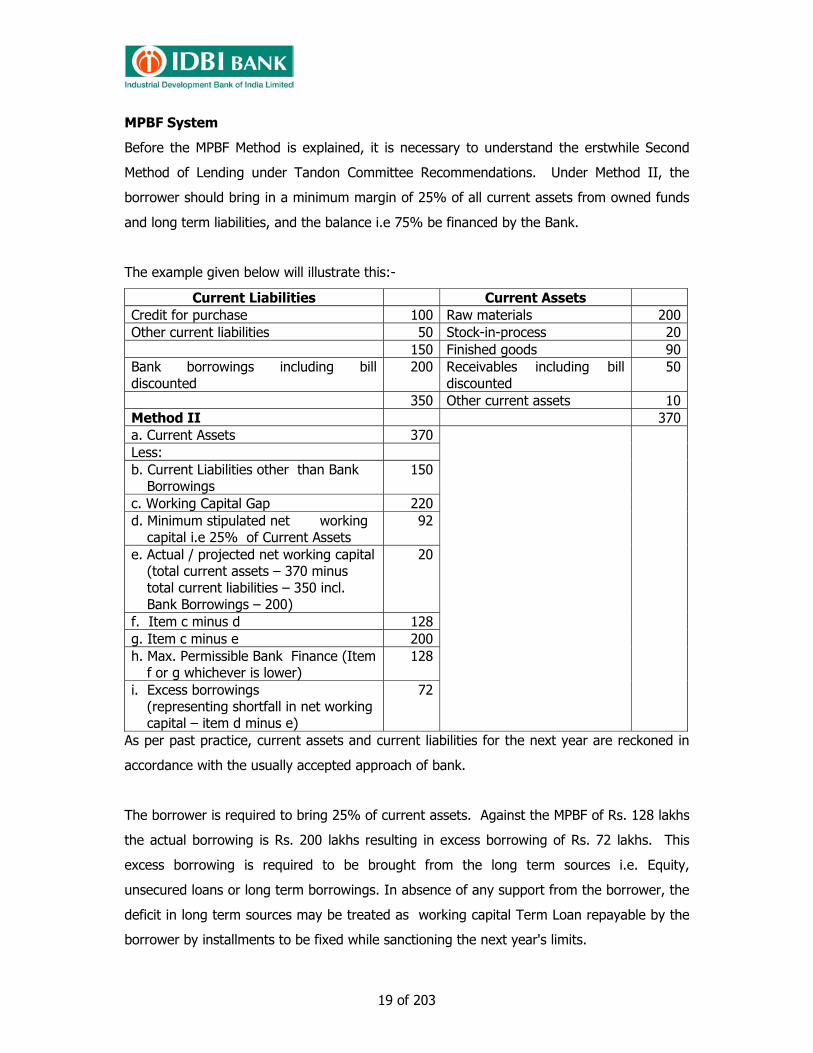

MPBF System

Before the MPBF Method is explained, it is necessary to understand the erstwhile Second

Method of Lending under Tandon Committee Recommendations. Under Method II, the

borrower should bring in a minimum margin of 25% of all current assets from owned funds

and long term liabilities, and the balance i.e 75% be financed by the Bank.

The example given below will illustrate this:-

Current Liabilities Current Assets Credit for purchase 100 Raw materials 200Other current liabilities 50 Stock-in-process 20 150 Finished goods 90Bank borrowings including bill discounted

200 Receivables including bill discounted

50

350 Other current assets 10Method II 370a. Current Assets 370 Less: b. Current Liabilities other than Bank

Borrowings 150

c. Working Capital Gap 220 d. Minimum stipulated net working

capital i.e 25% of Current Assets92

e. Actual / projected net working capital (total current assets – 370 minus total current liabilities – 350 incl. Bank Borrowings – 200)

20

f. Item c minus d 128 g. Item c minus e 200 h. Max. Permissible Bank Finance (Item

f or g whichever is lower) 128

i. Excess borrowings (representing shortfall in net working capital – item d minus e)

72

As per past practice, current assets and current liabilities for the next year are reckoned in

accordance with the usually accepted approach of bank.

The borrower is required to bring 25% of current assets. Against the MPBF of Rs. 128 lakhs

the actual borrowing is Rs. 200 lakhs resulting in excess borrowing of Rs. 72 lakhs. This

excess borrowing is required to be brought from the long term sources i.e. Equity,

unsecured loans or long term borrowings. In absence of any support from the borrower, the

deficit in long term sources may be treated as working capital Term Loan repayable by the

borrower by installments to be fixed while sanctioning the next year's limits.

20320320320320320320 20

20 of 203

The assessment of credit requirement of the borrower shall be made based on the total

study of the borrower's business operations vis-à-vis the production/processing cycle of the

industry, which shall represent a reasonable build up of current assets for being supported

by bank finance.

Based on Kannan Committee recommendations, RBI has allowed freedom to the banks to

decide the holding levels of various components of current assets for financial support to

ensure efficient functioning of the unit.

The levels of inventory and receivables shall be based on industry trend and closely related

market developments. Projected level of inventory and receivables shall be examined in

relation to the past trend and based on inter firm comparisons. The existing norms are only

indicative level of inventory and borrower specific operational needs to hold projected level

of inventory and reasonable thereof, ability to absorb the cost of carrying such inventory

and comparison of the other similar units in the industry shall be relied upon to decide the

required and acceptable level for being supported by the bank.

Classification of Current Assets and Current Liabilities

(A few important classifications are furnished hereunder)

1) All Short Term / Temporary investments in money market instruments like

Commercial Paper, Certificate of Deposits can be considered as Current Assets.

However, other investments like ICDs (inter Corporate Deposits), investment in listed

Shares & Debentures including investment in subsidiaries and associates are to be

considered as Non-Current Assets.

2) Cash margin for Non-Fund Based limits (like LCs / Guarantees) may be treated as

part of current assets for the purpose of MPBF and Current Ratio. However, such

margin held for Deferred Payment Guarantees should be considered as Non Current

Assets.

3) All Term Loan instalments, Fixed Deposits, Debentures etc., repayable within next 12

months should be considered as Current Liabilities for computation of Current Ratio

and MPBF.

4) Inter Corporate Deposits (ICDs) taken are to be treated as Current Liabilities.

20320320320320320321 21

21 of 203

In order to have flexibility in inventory and receivable norms and ensure adequate finance

for industrial and other activities, MPBF method has been revised. In order to rectify the

deficiency of rigidity of the norms in the erstwhile MPBF, the projected levels of inventory

and receivables would now be based on actual level in the past 2-3 years.

Combined limits against stocks/book debts may be fixed to have flexibility with suitable sub-

limits for book debts/inventory etc. The level of the book debts for drawing limits/bills limits

should correspond to the level of receivables accepted for MPBF. However, the level of book

debts/receivables should be uniform for computation of both MPBF and drawing power. In

other words, if the level of book debts accepted is 3 months for MPBF, quantum of said level

of book debts minus stipulated margin should be the sub-limit for drawing limit purposes.

Assessment of working capital limits of over Rs. 5 cr. but upto Rs. 25 crore shall be assessed

based on the MPBF system.

The Bench mark current ratio for borrowers whose working capital limit is assessed under

MPBF system shall be 1.33.

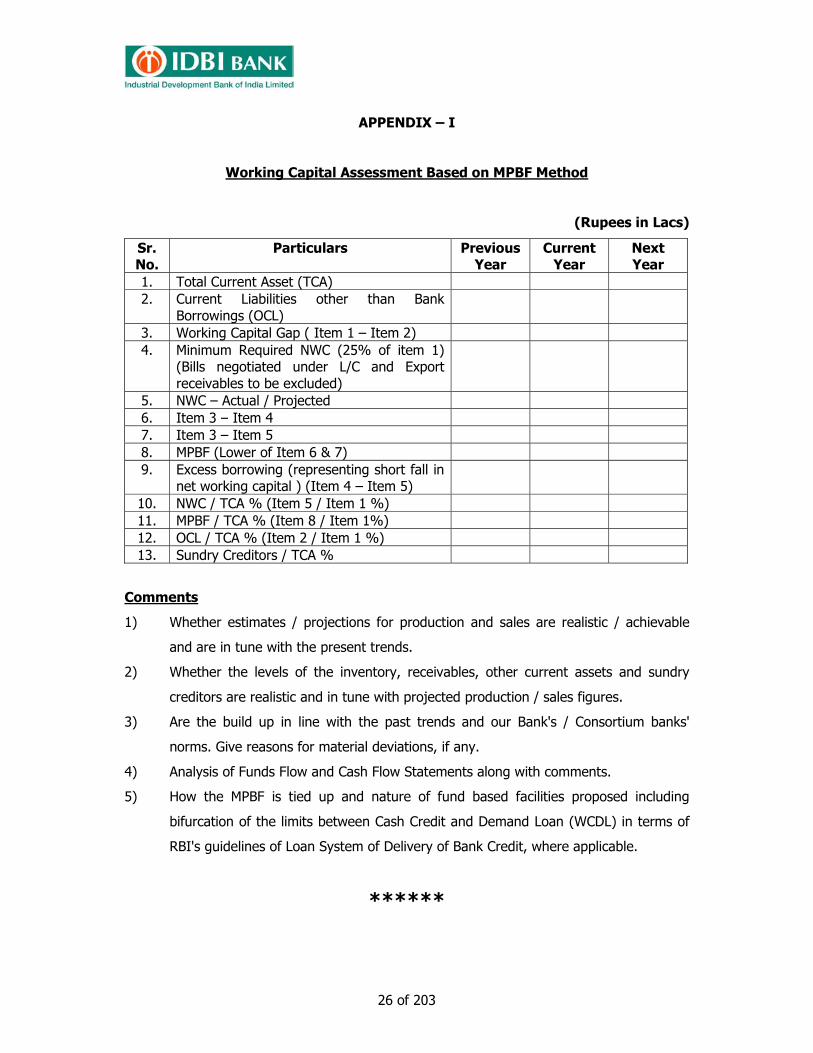

Summary of assessment of working capital on the basis of MPBF System is indicated at

Appendix – I.

Cash Budget System

In the case of borrowers enjoying /requiring credit facilities of over Rs. 25 cr., the same can

be assessed on the basis of Cash Budget system or MPBF system, at the option of the

borrowers. However conservative approach has to be followed. However, in the case of

specific industries / seasonal activities such as software export, construction activity, tea and

sugar, normally, the system of assessment based on the cash budget may be adopted.

Further, in the case of specific industries like tea, wherever for specific reasons, the

borrower opts to avail the Working Capital facility under MPBF system, the same may be

permitted by the respective sanctioning authority after necessary evaluation and

justification.

20320320320320320322 22

22 of 203

Structure of Cash Flow Statement

The cash flow statement shows the movement of cash and bank balances during a certain

period, the reasons for increase (+) or decrease (-) in the bank borrowings, the level of cash

holding between 2 intervals of time. The cash flow statement is a historical statement that

depicts the flow of cash in the system. A cash budget statement depicts the projected

movement of cash and bank balances at a future period. It shows the expected inflow and

outflow of cash and deficit and surplus in generation of cash.

The statement covers most of the details needed for assessment of the financial needs of

the borrower.

The statement of cash flow is made more meaningful and useful for assessment of working

capital by grouping the cash flows under three heads viz., Operating, Investing and

Financing. The principal cash flows arising out of the above three main groups are

described below:

i) Operating Activities

These activities involve producing and delivering goods and providing services. Cash

inflows from operating activities include receipts from customers for sale of goods

and services, including receipts from collection of debtors. Cash outflows from

operating activities include payments to employees for services, payment to suppliers

of goods, payments to Governments for taxes and duties and services etc.

ii) Investing Activities

These activities involve extending and recovering loans and acquiring and disposing

of debt and equity instruments and fixed assets. Cash inflow from investing activities

include receipts from loan collections, receipts from sales of debt and equity

instruments of other enterprises and receipts from sale of fixed assets. Cash

outflows from investing activities include disbursements of loans, payments to

acquire debt and equity instruments of other enterprises and payments (including

advances or down payments) to acquire fixed assets.

iii) Financing Activities

These activities involve obtaining resources from owners and providing them with a

return on and return of their investment, borrowing and repaying amounts borrowed,

and obtaining and paying for other resources obtained from creditors on long term

20320320320320320323 23

23 of 203

credit. Cash inflows from financing activities include proceeds from issuing equity

instruments, debentures, mortgages, bills and from other long and short term

borrowings. Cash outflows from financing activities are payments of dividends,

repayments of amounts borrowed and principal payments to creditors who have

extended long term credit.

Assessment of the limit under the cash budget system is done by arriving at the deficit

between cash inflow and cash outflow during a period of time. The various segments of

cash budget are as under:

1. Cash inflow

(a) Realisation from debtors

(b) Cash Sales

(c) Receipt by way of trade advances

(d) Miscellaneous receipts

(e) Long term sources in the form of TL, equity induction

TOTAL CASH INFLOW

2. Cash Outflow

(a) Payment to Sundry Creditors (Trade Creditors)

(b) Payment of Sundry Creditors (expenses)

(c) Cash expenses

(d) Cash purchases

(e) Deposits and Investments

(f) Advances to suppliers

(g) Other outflows like repayment of TL, Debentures, ICDs, CPs and other

obligations.

TOTAL CASH OUTFLOW

3. Deficit (-) Surplus (+) (1 -2) (3)

4. Add Opening Balance (Deficit/Surplus) (4)

5. Amount of Deficit to be Financed (5)

(NET OF 3 + 4 or 3-4)

20320320320320320324 24

24 of 203

In the case of borrowers whose credit limits are to be assessed on the basis of cash budget

system, the bank shall obtain the following data from the borrower along with applications.

(a) Cash Flow Statement

(b) Projected Balance Sheet and Profitability Statement

(c) Credit Monitoring Arrangement (CMA) data

In addition to the cash budget statement, the bank shall obtain following additional

information to scrutinise the cash budget statement.

(a) Credit sales during the quarter

(b) Credit purchase during the quarter

(c) Opening Stock of the finished goods

(d) Closing Stock of the finished goods

(e) Receivables outstanding at the beginning

(f) Receivables outstanding at the end

(g) Creditors outstanding at the beginning

(h) Creditors outstanding at the end.

In the case of seasonal industries / industries having peak/non peak level operations, cash

budget indicating the peak level/non peak level cash flows shall be obtained separately.

Based on such peak level/non peak level cash deficit, peak level limits shall be arrived at.

The quantum of bank finance for working capital to the borrower shall be the peak level of

the annual cash deficit projected as per the projected cash flow statement. However, the

working capital limits shall be in tune with the quarterly cash deficit of the borrower as

revealed in the quarterly cash budget. To ensure sufficient liquidity, the projected balance

sheet should reveal the minimum current ratio acceptable to the bank.

The bank shall obtain the quarterly cash flow projections one month in advance before the

commencement of the quarter for stipulating the operative limit.

While fixing the limits based on the cash budget, the following points shall be borne in mind:

(a) The cash budget is realistic and based on the operations in the business / similar

business

20320320320320320325 25

25 of 203

(b) The cash budget statement tallies with the underlying financial statements viz.,

projected balance sheet and profit and loss account.

(c) Outstanding bank borrowings figured in the projected balance sheet tally with the

deficit as shown in the cash budget statement.

(d) The closing balance of the debtors is correctly arrived at by summing up, opening

balance of debtors + credit sales minus (-) realization of debtors.

(e) The expenses as indicated in the cash budget tallies with the expenses as reflected

in the project profit and loss account.

In the case of existing borrowers, the branches shall be in a position to scrutinize the

projected cash flow statement with the actuals for the previous period and if necessary,

obtain other explanation from the borrowers for variations. In the case of new clients, the

projected cash flow statement shall be analysed based on the operating cycle / activities of

the borrower / other similar borrowers.

The bank shall obtain on a quarterly basis, the actuals of cash flow within a fortnight of the

completion of the quarter and scrutinise the variations with reference to the projected cash

flow obtained earlier, in the same format.

During the review of the cash flow statement, if there are major variations between the

projected and actuals, the same may be analysed. The reasons therefore should also be

indicated and evaluated critically.

Apart from the above, the bank should also obtain half yearly balance sheet and funds flow

statement.

Format of cash flow statement, projected balance sheet and profitability statement and data

in respect of CMA are at Appendix II, III and IV respectively. CMA data comprises

particulars of existing and proposed limits from the banking system, projected profitability

and balance sheet statement, comparative statement of current assets and current liabilities,

computation MPBF for working capital and fund flow statement. Computation of MPBF for

working capital and Projected profitability and balance sheet statement are already

furnished at Appendix I & III respectively. Hence rest of the statements are only included in

Appendix – IV.

20320320320320320326 26

26 of 203

APPENDIX – I

Working Capital Assessment Based on MPBF Method

(Rupees in Lacs)

Sr. No.

Particulars Previous Year

Current Year

Next Year

1. Total Current Asset (TCA) 2. Current Liabilities other than Bank

Borrowings (OCL)

3. Working Capital Gap ( Item 1 – Item 2) 4. Minimum Required NWC (25% of item 1)

(Bills negotiated under L/C and Export receivables to be excluded)

5. NWC – Actual / Projected 6. Item 3 – Item 4 7. Item 3 – Item 5 8. MPBF (Lower of Item 6 & 7) 9. Excess borrowing (representing short fall in

net working capital ) (Item 4 – Item 5)

10. NWC / TCA % (Item 5 / Item 1 %) 11. MPBF / TCA % (Item 8 / Item 1%) 12. OCL / TCA % (Item 2 / Item 1 %) 13. Sundry Creditors / TCA %

Comments

1) Whether estimates / projections for production and sales are realistic / achievable

and are in tune with the present trends.

2) Whether the levels of the inventory, receivables, other current assets and sundry

creditors are realistic and in tune with projected production / sales figures.

3) Are the build up in line with the past trends and our Bank's / Consortium banks'

norms. Give reasons for material deviations, if any.

4) Analysis of Funds Flow and Cash Flow Statements along with comments.

5) How the MPBF is tied up and nature of fund based facilities proposed including

bifurcation of the limits between Cash Credit and Demand Loan (WCDL) in terms of

RBI's guidelines of Loan System of Delivery of Bank Credit, where applicable.

******

20320320320320320327 27

27 of 203

APPENDIX – II

Cash Flow Statement

(Rupees in Lacs)

P a r t i

c u

l a r s

Quarter 1 Quarter 2 Quarter 3 Quarter 4 Total for the year

Projec-

tions

Actuals Projec-

tions

Actuals Projec-

tions

Actuals Projec-

tions

Actuals Projec-

tions

Actuals

1. Cash Flow from Operating Activities

A. Receipts

→ Cash Sales

→ Collection from trade debtors

→ Other receipts relating to operations (specify)

→ Total receipts from operations

B. Payments

→ Cash purchases – inventories only

→ Payment made to trade Creditors.

→ Payment towards other

Manufacturing expenses

→ Power and fuel

→ Wages and Salaries

→ Other Factory expenses

→ Administration expenses

→ Payments towards selling & distribution expenses

→ Excise duty

→ Other Selling and distribution on

→ Expenses including ST

→ Payment of direct taxes

→ Deposits towards LC and Guarantee margin

→ Deposits made with Government departments

→ Other deposits (specify)

→ Loans to employees

→ Other payment relating to Operating activities

20320320320320320328 28

28 of 203

Total cash outflow from operating activities (B)

Net cash flow from Operating activities (A-B)

2. Cash Flows from Investing Activities

A. Receipts

→ Dividends on investments

→ Interest on investments

→ Proceeds from sale of investments other than fixed assets

→ Collection from Loans (other than employees)

→ Others (specify)

Total cash inflow from Investing activities (A)

B. Payments

→ Acquisition of fixed assets

→ Advances to capital goods

• Shares

• Debentures

• Others (specify)

→ Loans made to parties other than employees

→ Others (specify)

Total cash outflow from Investing activities (B)

Net Cash flow from Investing activities (A-B)

3. Cash flows from Financing Activities

A. Receipts

→ Proceeds from issue of shares capital

→ Proceeds from long term borrowing

→ Term loan from institution

→ Term loan from banks

20320320320320320329 29

29 of 203

→ Debentures

→ Others

→ Proceeds from short term borrowings other than bank borrowings including CPS

→ CDs

→ Others specify

→ Margin money loan (specify)

Total cash inflow from financing activities (A)

B. Payments

→ Interest paid

→ Dividend paid

→ Repayments of term borrowings:

• from Institutions

• from Banks

• from Others

→ Redemption of Debentures/Share capital

→ Lease and HP payments

Total cash outflow from Financing activities (B)

Net cash flow from financing Activities (A-B)

STATEMENT OF BANK FINANCE FOR WORKING CAPITAL

I Net cash flow from operating activities

II Net cash flow from investing activities

III Net cash flow from Financing activities

Total (I + II + III) ___________________________________

20320320320320320330 30

30 of 203

Opening cash ___________________________________

Add: Net cash inflow (I + II + III) ___________________________________

Less: Closing cash ___________________________________

Net Deficit ___________________________________

All non-cash transactions will form part of cash flow statement as notes:

Other information:

1) Credit Sales during the quarter

2) Credit Purchase

3) Opening stock of Processed Goods

4) Closing stock of Finished Goods

5) Receivables outstanding in the beginning

6) Receivables outstanding at the end

7) Creditors outstanding in the beginning

8) Creditors outstanding at the end

*****

20320320320320320331 31

31 of 203

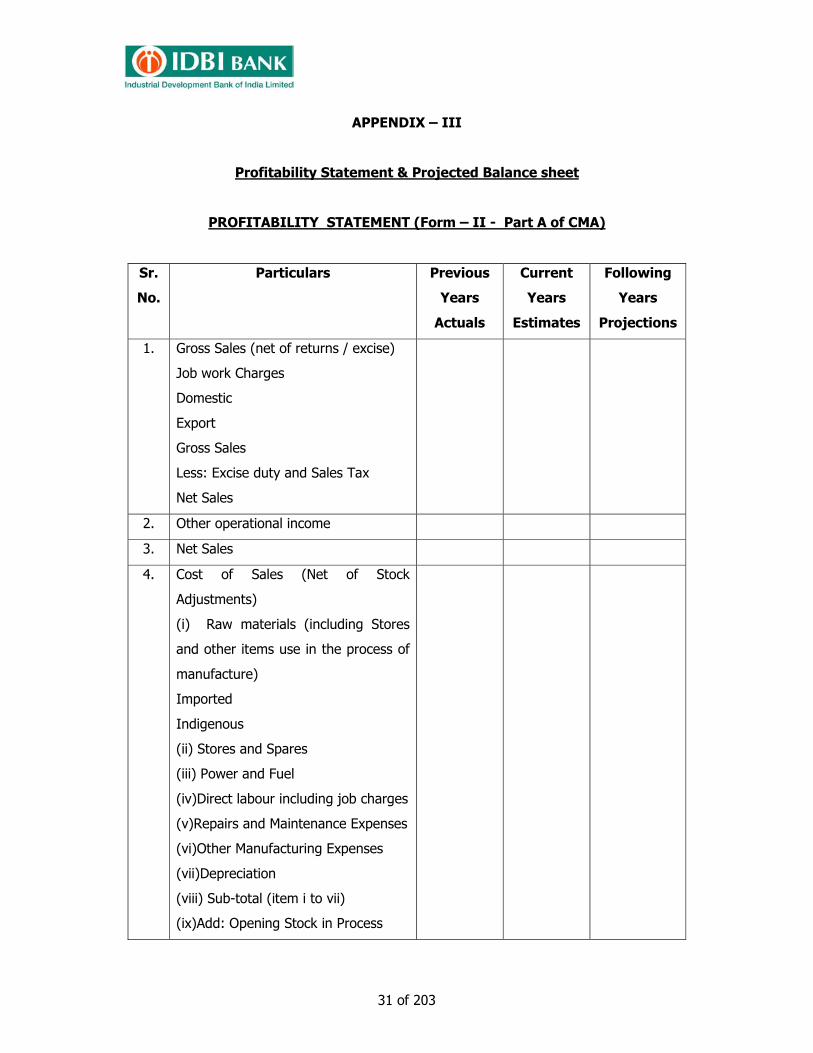

APPENDIX – III

Profitability Statement & Projected Balance sheet

PROFITABILITY STATEMENT (Form – II - Part A of CMA)

Sr.

No.

Particulars Previous

Years

Actuals

Current

Years

Estimates

Following

Years

Projections

1. Gross Sales (net of returns / excise)

Job work Charges

Domestic

Export

Gross Sales

Less: Excise duty and Sales Tax

Net Sales

2. Other operational income

3. Net Sales

4. Cost of Sales (Net of Stock

Adjustments)

(i) Raw materials (including Stores

and other items use in the process of

manufacture)

Imported

Indigenous

(ii) Stores and Spares

(iii) Power and Fuel

(iv)Direct labour including job charges

(v)Repairs and Maintenance Expenses

(vi)Other Manufacturing Expenses

(vii)Depreciation

(viii) Sub-total (item i to vii)

(ix)Add: Opening Stock in Process

20320320320320320332 32

32 of 203

Sub-total

(x)Deduct: Closing Stock in process

(xi) Sub-total

(xii)Add: Opening Stock of Finished

Goods

Sub-total

(xiii)Deduct: Closing stock of finished

goods

(xiv) Sub-total (Total cost of sales)

5. Gross Profit (Item 3 minus item 4 )

6. Interest

7. Selling: General and Administrative

Expenses

Sub-total (item 6 plus item 7 )

8. Operating profit (item 5 minus total of

items 6 and item 7 )

9. Other income/expenses

Add: Income

Discount

Interest

Exchange Difference

Others

Sub-total (+)

Deduct expenses

Prior Period adjustments

Preliminary Exp. Written off.

Sub-total (-)

10. Profit before tax/loss

(Item 8 plus item 9 )

11. Provision for taxes/tax paid (Including

tax on Dividend)

Normal Tax

Deferred Tax

20320320320320320333 33

33 of 203

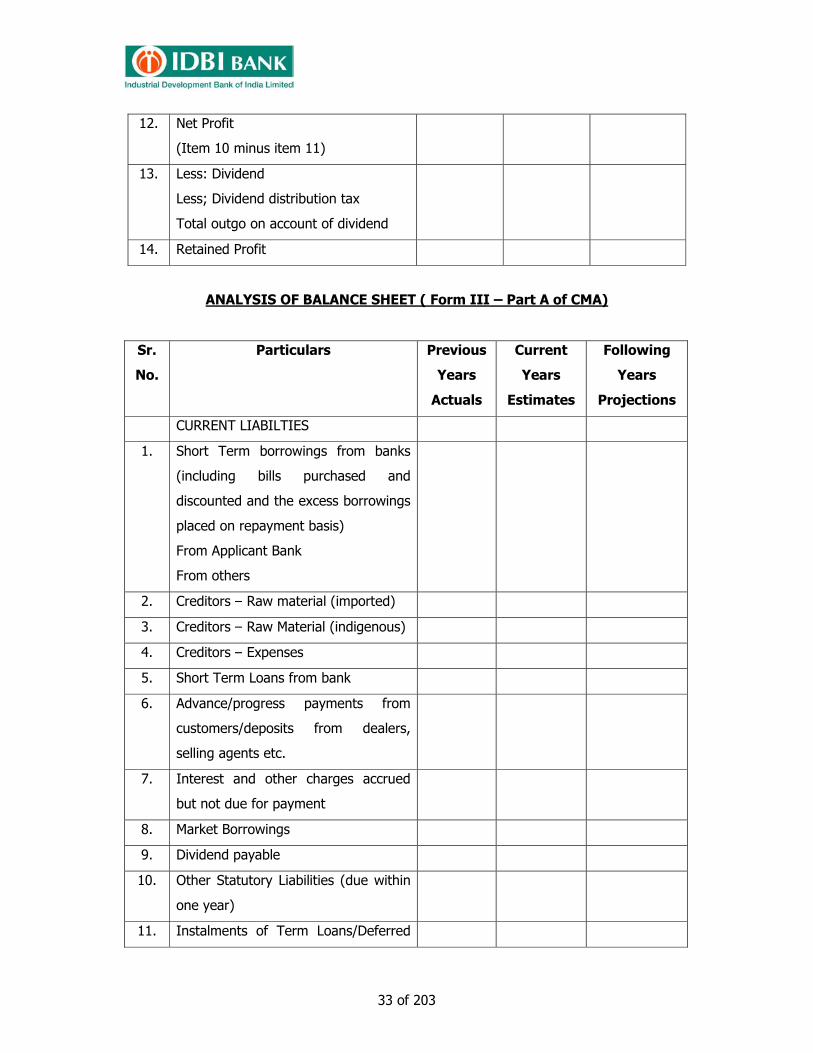

12. Net Profit

(Item 10 minus item 11)

13. Less: Dividend

Less; Dividend distribution tax

Total outgo on account of dividend

14. Retained Profit

ANALYSIS OF BALANCE SHEET ( Form III – Part A of CMA)

Sr.

No.

Particulars Previous

Years

Actuals

Current

Years

Estimates

Following

Years

Projections

CURRENT LIABILTIES

1. Short Term borrowings from banks

(including bills purchased and

discounted and the excess borrowings

placed on repayment basis)

From Applicant Bank

From others

2. Creditors – Raw material (imported)

3. Creditors – Raw Material (indigenous)

4. Creditors – Expenses

5. Short Term Loans from bank

6. Advance/progress payments from

customers/deposits from dealers,

selling agents etc.

7. Interest and other charges accrued

but not due for payment

8. Market Borrowings

9. Dividend payable

10. Other Statutory Liabilities (due within

one year)

11. Instalments of Term Loans/Deferred

20320320320320320334 34

34 of 203

Payment Credit/Debentures

redeemable preference shares (due

within one year)

12. Other Current Liabilities and

provisions (due within one year)

major items to be specified

individually.

Total Current Liabilities

13. Total current liabilities (Total of items

to 1 to 12 )

TERM LIABILITIES

14. Unsecured Loans from a bank

15. Redeemable preference shares (not

maturing within one year but of

maturity not exceeding 12 years)

16. Term Loan (exclusive of instalments

payable within one year )

17. Advance against sale of land

18. Term Deposits

19. Other term liabilities

20. Total term liabilities

21. Total outside liabilities

Deferred Tax Liability

NETWORTH

22. Equity Share Capital

23. General Reserve

24. Development rebate reserve

(investment allowance)

25. Other reserves (excluding provisions)

26. Surplus (+) or deficit (-) in Profit &

Loss Account

27. Net Worth

28. Total Liabilities (item 21 plus item 27)

20320320320320320335 35

35 of 203

CURRENT ASSETS

29. Cash and Bank Balance

30. Investments (other than long term

investment e.g sinking fund. Gratuity

Fund etc.)

(i)Government and other Trustees

Securities

(ii) Fixed Deposits with banks

31. Receivable other than deferred and

export receivable (including bills

purchased and discounted by

bankers)

Export receivables (including bills

purchased and discounted by

bankers)

32. Instalments of deferred receivables

(due within one year)

33. Inventory

Raw materials (including stores and

other items used in the process of

manufacture)

Imported

Indigenous

Stock in process

Finished Goods

(iv) Other consumable spares

34. Advance to suppliers of raw materials

and stores/spares consumable and for

expenses

35. Advance and Loans

36. Other current assets/major items to

be specified individually

37. Total Current Assets

20320320320320320336 36

36 of 203

FIXED ASSETS

38. Gross Block (Land and Building,

Machinery construction in progress

etc.) (Including additions during the

year)

39. Depreciation to date

40. Net Block (item 38 minus 39)

OTHER NON CURRENT ASSETS

41. Investments/Book

Debts/Advances/Deposits, which are

not current assets

i) a) Investment in subsidiary

companies/affiliates

b) Others

ii) Advances to suppliers of capital

goods/spares and contractors for

capital expenditure

iii) Deferred Receivables (other than

those maturing within one year )

iv) Others

42. Non consumable stores and spares

43. Other Miscellaneous assets including

dues from directors

44. Total other non current assets

45. Intangible assets (patents, goodwill,

preliminary and formation expenses,

bad/doubtful debts not provided for

etc. share issue expenses

46. Total Assets (Total of items 37,40,44

and 45)

47. Tangible Net Worth (item 28 minus

item 45)

48. Net working capital (item 37 minus

20320320320320320337 37

37 of 203

item 13)

Additional Information

Arrears of depreciation:

Contingent Liabilities:

Arrears of cumulative dividends

Gratuity Scheme of Staff

Other liabilities not provided for

Notes:

a) If the company is subsidiary, the

extent and nature of interest of the

holding company and its name.

b) If the company is a holding

company, extent and nature of

interest in subsidiary company and

their names.

ANALYTICAL AND COMPARATIVE RATIO (Form III - Part B of CMA)

Sr.

No.

Particulars Previous

Years

Actuals

Current

Years

Estimates

Following

Years

Projections

1. Net Sales

(Item 3 in Form IIA)

2. %rise (+) or fall (-) in net sales

during the year as compared to

previous year

3. Profit before Tax (+) or Loss (-) (item

10 in Form IIA)

4. Net Profit i.e after tax (+) or Loss (-)

5. Net profit/(Loss) appropriated

6. Retained Profit as % of Net Profit

7. Retained Profit as % of Net Profit

8. Raw materials (including stores and

20320320320320320338 38

38 of 203

other items used in the process of

manufacture

Imported (Item 33(i) (a) in the Form

III) How many months' consumption

do these represent?

Indigenous (item 33(i)(b) in Form

IIIA) How many months' consumption

do these represent?

Months

9. Stock-in-process (item 33(ii) in Form

IIIA) How many months' cost of

production do these represent?

Months

10. Finished Goods (item 33(iii) in Form

IIIA) How many months' cost of sales

do these represent?

Months

11. Other Consumable spares (item 33(iv)

in Form IIA) What is the % of total

inventory & how many months'

normal consumption do these

represent

12. Receivables other than Deferred

receivables and Export receivables

(incl. Bills purchased and discounted

by bankers item 31(i) in Form IIIA)

Export receivables (item 31(ii) in Form

IIIA) How many months' export sales

do these represent?

13. Sundry Creditors (Trade item 2 in

Form IIIA)

Indigenous

How many months' purchase do these

20320320320320320339 39

39 of 203

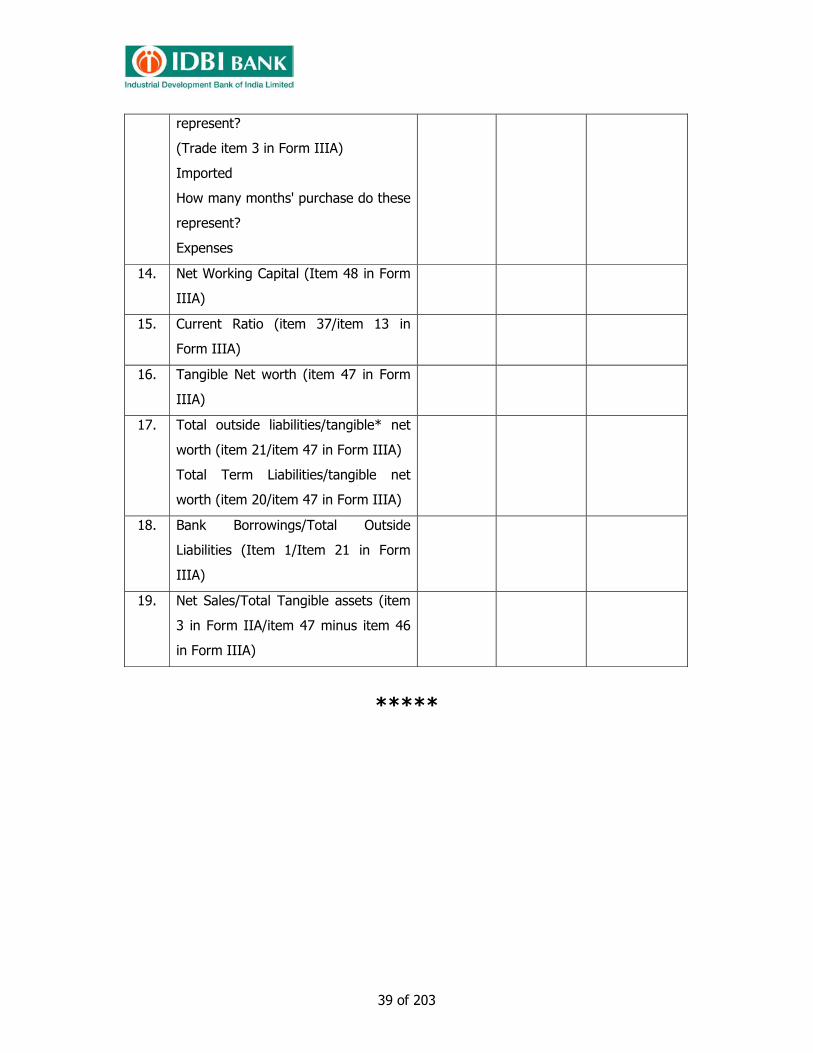

represent?

(Trade item 3 in Form IIIA)

Imported

How many months' purchase do these

represent?

Expenses

14. Net Working Capital (Item 48 in Form

IIIA)

15. Current Ratio (item 37/item 13 in

Form IIIA)

16. Tangible Net worth (item 47 in Form

IIIA)

17. Total outside liabilities/tangible* net

worth (item 21/item 47 in Form IIIA)

Total Term Liabilities/tangible net

worth (item 20/item 47 in Form IIIA)

18. Bank Borrowings/Total Outside

Liabilities (Item 1/Item 21 in Form

IIIA)

19. Net Sales/Total Tangible assets (item

3 in Form IIA/item 47 minus item 46

in Form IIIA)

*****

20320320320320320340 40

40 of 203

Appendix – IV

Credit Monitoring Arrangement (CMA) Data

(Other than Computation of Maximum Permissible Bank Finance for Working Capital

and Projected Profitability and Balance-sheet Statement,

which are at Appendix I & III respectively)

Annexure – I (Form I)

Existing and proposed working capital limits

Particulars of the existing / proposed limits from the banking system. (Limits from all Banks

and Financial Institutions, NBFCs, Term Lending Institutions for WC Limit, Associates and

subsidiary for inter corporate deposits taken and leasing finance from Leasing Companies as

on date.)

(Rupees in Lacs)

Sr. No. Name of

Bank /

Financial

Institution

Nature

of

facility

Existing

Limits

Extent to

which

limits

were

utilised

during the

last 12

months

Balance

outstanding

as on

Limits

now

requested

Max. Min.

1 2 3 4 5 6 7 8

A.

Working

Capital

Limits

Sr. No. Name of

the Bank/

Financial

Institutions

Sanction

Limit

Outstanding

as on

Overdues, if

any

Remarks

20320320320320320341 41

41 of 203

B.

TERM

LOANS /

DPGs

(Excluding

working

capital

terms

loans)

Annexure – II (Form II – Part B of CMA)

Comparative statement of current assets and current liability

(Rupees in Lacs)

Sr.

No. Particulars

Last

year

Actuals

Current

year

Estimates

Following

years

projections

1 Current Assets

i) Raw materials (including stores and other

items used in the process of manufacture)

a) Imported [Month’s consumption]

b] Indigenous [Month’s consumption]

ii) Other consumable spares [excluding those

included under item (i) above] [% of total

inventory and month's consumption]

iii) Stock-in-process [month's cost of production]

iv) Finished goods [Month's cost of sales]

v) Receivables other than export and deferred

receivables [including bills purchased and

discounted by bankers] [Month’s domestic

sales excluding deferred payment sales]

vi) Export receivables [including bills purchased

and discounted by bankers] [Month’s export

sales]

20320320320320320342 42

42 of 203

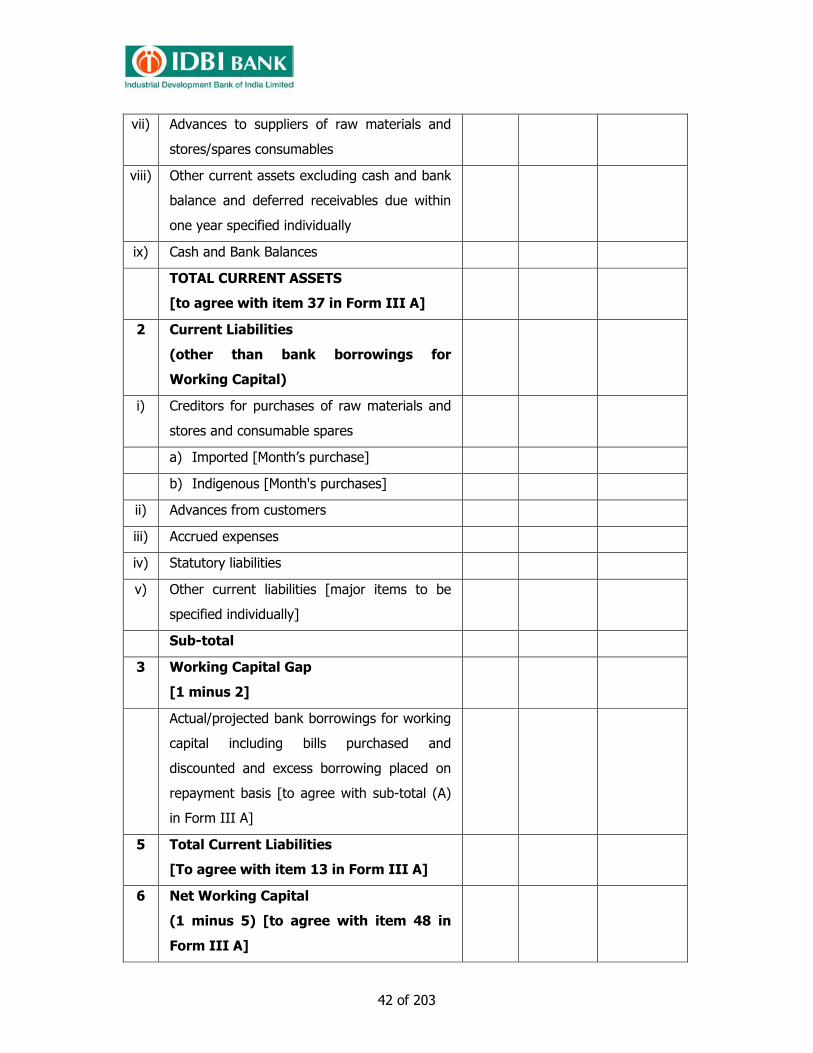

vii) Advances to suppliers of raw materials and

stores/spares consumables

viii) Other current assets excluding cash and bank

balance and deferred receivables due within

one year specified individually

ix) Cash and Bank Balances

TOTAL CURRENT ASSETS

[to agree with item 37 in Form III A]

2 Current Liabilities

(other than bank borrowings for

Working Capital)

i) Creditors for purchases of raw materials and

stores and consumable spares

a) Imported [Month’s purchase]

b) Indigenous [Month's purchases]

ii) Advances from customers

iii) Accrued expenses

iv) Statutory liabilities

v) Other current liabilities [major items to be

specified individually]

Sub-total

3 Working Capital Gap

[1 minus 2]

Actual/projected bank borrowings for working

capital including bills purchased and

discounted and excess borrowing placed on

repayment basis [to agree with sub-total (A)

in Form III A]

5 Total Current Liabilities

[To agree with item 13 in Form III A]

6 Net Working Capital

(1 minus 5) [to agree with item 48 in

Form III A]

20320320320320320343 43

43 of 203

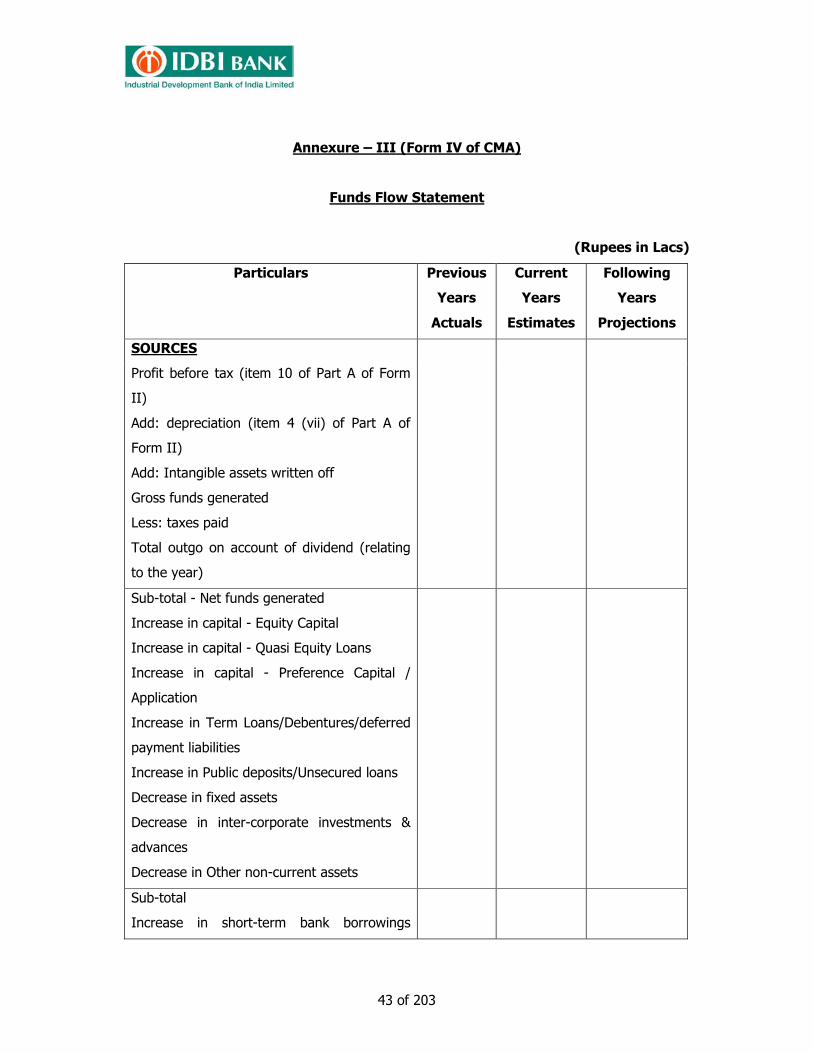

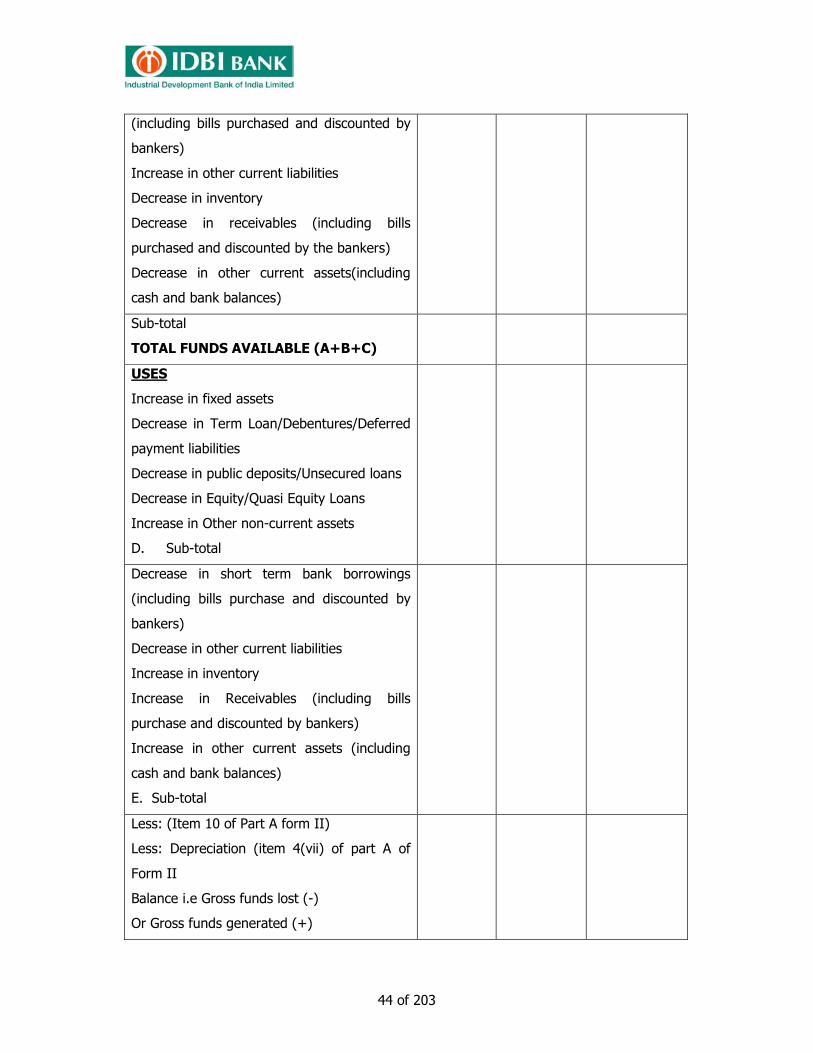

Annexure – III (Form IV of CMA)

Funds Flow Statement

(Rupees in Lacs)

Particulars Previous

Years

Actuals

Current

Years

Estimates

Following

Years

Projections

SOURCES

Profit before tax (item 10 of Part A of Form

II)

Add: depreciation (item 4 (vii) of Part A of

Form II)

Add: Intangible assets written off

Gross funds generated

Less: taxes paid

Total outgo on account of dividend (relating

to the year)

Sub-total - Net funds generated

Increase in capital - Equity Capital

Increase in capital - Quasi Equity Loans

Increase in capital - Preference Capital /

Application

Increase in Term Loans/Debentures/deferred

payment liabilities

Increase in Public deposits/Unsecured loans

Decrease in fixed assets

Decrease in inter-corporate investments &

advances

Decrease in Other non-current assets

Sub-total

Increase in short-term bank borrowings

20320320320320320344 44

44 of 203

(including bills purchased and discounted by

bankers)

Increase in other current liabilities

Decrease in inventory

Decrease in receivables (including bills

purchased and discounted by the bankers)

Decrease in other current assets(including

cash and bank balances)

Sub-total

TOTAL FUNDS AVAILABLE (A+B+C)

USES

Increase in fixed assets

Decrease in Term Loan/Debentures/Deferred

payment liabilities

Decrease in public deposits/Unsecured loans

Decrease in Equity/Quasi Equity Loans

Increase in Other non-current assets

D. Sub-total

Decrease in short term bank borrowings

(including bills purchase and discounted by

bankers)

Decrease in other current liabilities

Increase in inventory

Increase in Receivables (including bills

purchase and discounted by bankers)

Increase in other current assets (including

cash and bank balances)

E. Sub-total

Less: (Item 10 of Part A form II)

Less: Depreciation (item 4(vii) of part A of

Form II

Balance i.e Gross funds lost (-)

Or Gross funds generated (+)

20320320320320320345 45

45 of 203

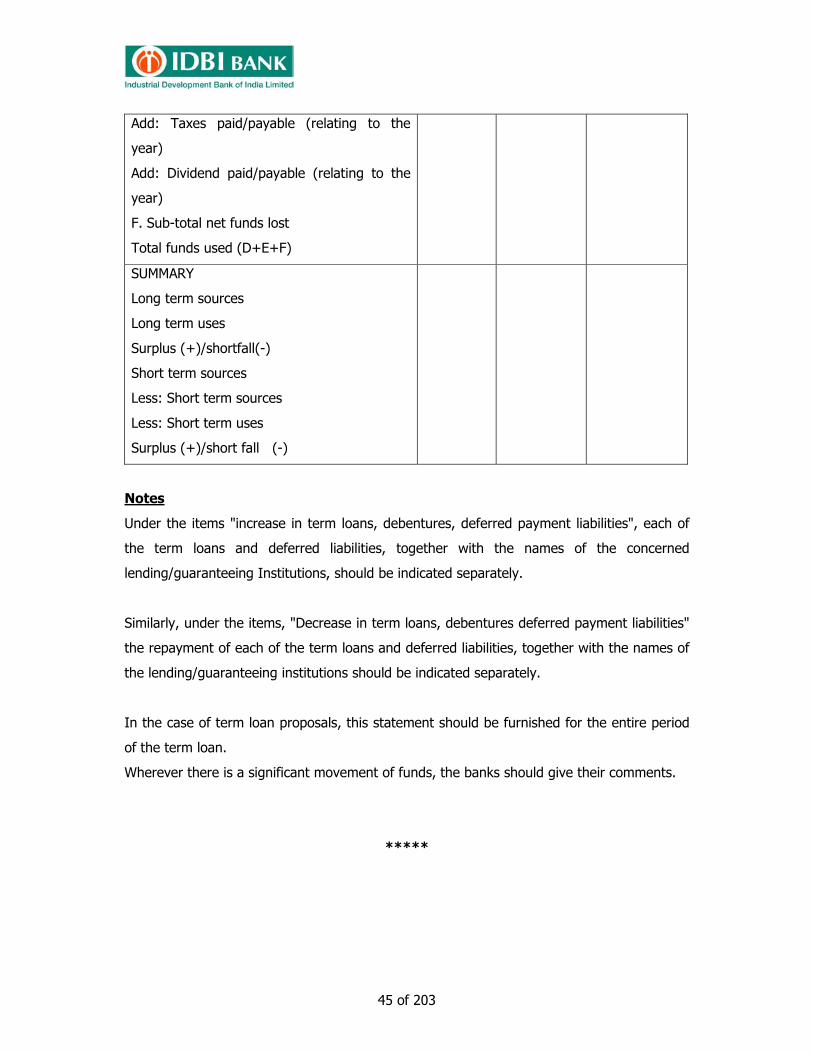

Add: Taxes paid/payable (relating to the

year)

Add: Dividend paid/payable (relating to the

year)

F. Sub-total net funds lost

Total funds used (D+E+F)

SUMMARY

Long term sources

Long term uses

Surplus (+)/shortfall(-)

Short term sources

Less: Short term sources

Less: Short term uses

Surplus (+)/short fall (-)

Notes

Under the items "increase in term loans, debentures, deferred payment liabilities", each of

the term loans and deferred liabilities, together with the names of the concerned

lending/guaranteeing Institutions, should be indicated separately.

Similarly, under the items, "Decrease in term loans, debentures deferred payment liabilities"

the repayment of each of the term loans and deferred liabilities, together with the names of

the lending/guaranteeing institutions should be indicated separately.

In the case of term loan proposals, this statement should be furnished for the entire period

of the term loan.

Wherever there is a significant movement of funds, the banks should give their comments.

*****

20320320320320320346 46

46 of 203

CHAPTER 5

ANALYSIS OF BALANCE SHEET, RATIO AND HOLDING LEVEL

Balance Sheet and Profit & Loss Account are the key financial statements of a company /

firm / organisation. The ability of those managing a business is often reflected in the

Balance Sheet. It is also indicated in the Income (Profit & Loss) Statement. The main

objective of analysis of Balance Sheet and Profit & Loss Account is to clearly find out the

present solvency and probability of continuing solvency and trend of fortunes of the

business enterprise. Study of Balance Sheet and Profit & Loss Account over a period of a

few years gives approximate idea of the financial position of the enterprise. It is, therefore,

necessary to make a comparative and comprehensive study of these statements for at least

2-3 years immediately preceding the date on which an application for an advance is made.

It is also necessary to make such study of financial estimates for the current year and

projections for the following year.

The Balance Sheet and Profit & Loss Account statements can be sourced from the borrower.

However, to enable the Bank to carry out a meaningful analysis, it is necessary that all the

items are classified properly. There may, some times, be a doubt as to the heading under

which a particular balance sheet item should be placed. The Bank has to deal with items in a

Balance Sheet from a lender’s point of view and in case of doubt, it should accordingly be

placed under appropriate heading.

For the purpose of arriving at the quantum of Current Assets and Current Liabilities and

arriving at the Working Capital gap which needs to be financed, it is necessary to analyse

the Balance Sheet. The figures furnished in a Balance Sheet are to be re-arranged to enable

an analysis as per our requirement. The following chart indicates an illustrative

classification:

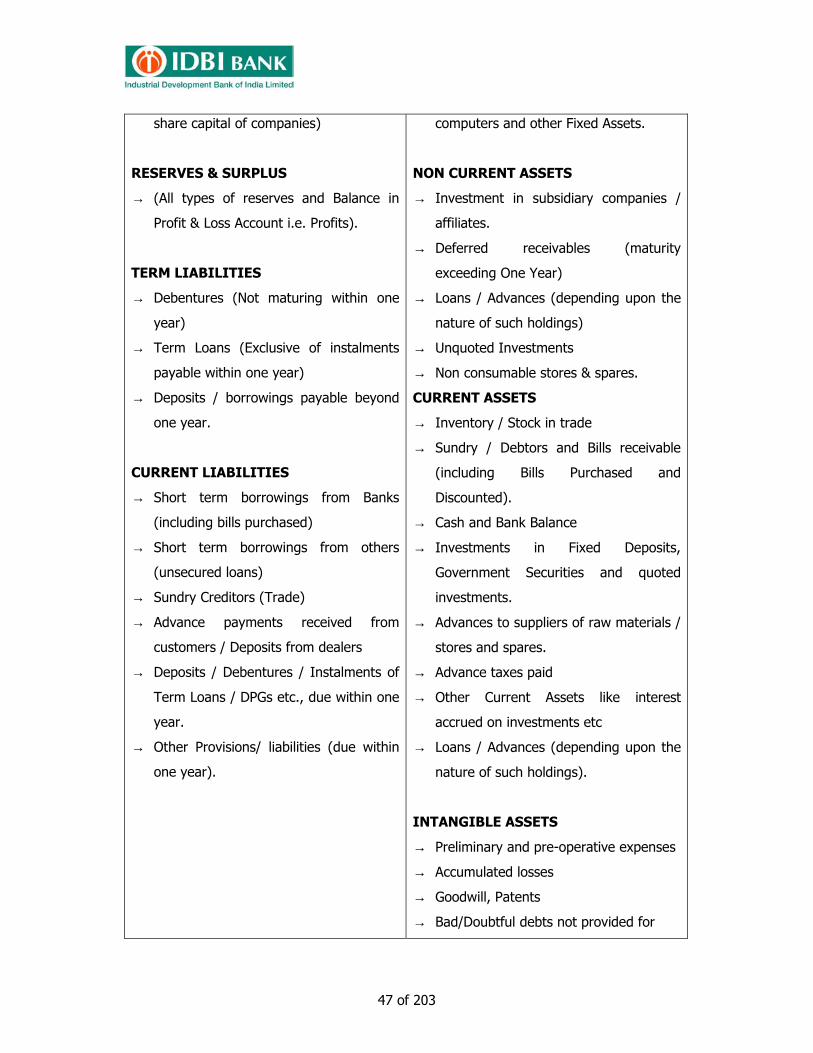

LIABILITIES ASSETS

CAPITAL

→ (includes money invested by partners,

balance in Current Accounts of Partners,

FIXED ASSETS

→ Land and Building – machinery

→ Furniture & Fixtures, vehicles,

20320320320320320347 47

47 of 203

share capital of companies)

RESERVES & SURPLUS

→ (All types of reserves and Balance in

Profit & Loss Account i.e. Profits).

TERM LIABILITIES

→ Debentures (Not maturing within one

year)

→ Term Loans (Exclusive of instalments

payable within one year)

→ Deposits / borrowings payable beyond

one year.

CURRENT LIABILITIES

→ Short term borrowings from Banks

(including bills purchased)

→ Short term borrowings from others

(unsecured loans)

→ Sundry Creditors (Trade)

→ Advance payments received from

customers / Deposits from dealers

→ Deposits / Debentures / Instalments of

Term Loans / DPGs etc., due within one

year.

→ Other Provisions/ liabilities (due within

one year).

computers and other Fixed Assets.

NON CURRENT ASSETS

→ Investment in subsidiary companies /

affiliates.

→ Deferred receivables (maturity

exceeding One Year)

→ Loans / Advances (depending upon the

nature of such holdings)

→ Unquoted Investments

→ Non consumable stores & spares.

CURRENT ASSETS

→ Inventory / Stock in trade

→ Sundry / Debtors and Bills receivable

(including Bills Purchased and

Discounted).

→ Cash and Bank Balance

→ Investments in Fixed Deposits,

Government Securities and quoted

investments.

→ Advances to suppliers of raw materials /

stores and spares.

→ Advance taxes paid

→ Other Current Assets like interest

accrued on investments etc

→ Loans / Advances (depending upon the

nature of such holdings).

INTANGIBLE ASSETS

→ Preliminary and pre-operative expenses

→ Accumulated losses

→ Goodwill, Patents

→ Bad/Doubtful debts not provided for

20320320320320320348 48

48 of 203

Some important concepts

Net Worth - Net Worth is the total of Capital and Reserves and surplus of a Company

excluding revaluation reserves. If there is a deficit in P&L Account (Loss) or any intangible

assets, the same has to be deducted for arriving at Net Worth.

Net Worth should show an increasing trend and it should be sufficient to cover the

borrower’s stake / contribution to the business.

Long Term / Short Term Sources and Uses

The total of Capital, Reserves and Surplus available and Term Liabilities represent Long

Term Sources, Bank borrowings for Working Capital and other Current Liabilities and Short

Term Sources.

Similarly, Fixed Assets are treated as long term uses and Current Assets are short term uses.

Normally, Long Term Sources are to be utilized for acquiring Fixed Assets as well as meeting

the margin on Working Capital.

Short term sources (Bank borrowing for WC) should not be diverted for long term uses like

acquiring Fixed Assets etc. Such diversion will result in deterioration of Net Working Capital

(NWC) and Current Ratio. In such cases, guidelines relating to diversion of funds are to be

enforced.

Where outside borrowings are declared, it should be ascertained whether these are taken on

long term (not repayable within one year) for considering as a long term source. Such

borrowings are to be subordinated to our advances.

Bank Borrowing for Working Capital / Sundry Creditors

As Working Capital Finance is extended against the inventories (Raw materials, work-in-

process, finished goods and stores & spares) and Receivables of the borrower, it should be

ensured that the value of inventories and receivables declared are sufficient to cover our

finance extended as well as the margin stipulated. Sundry Creditors (Trade) represent the

amount of credit available to the borrower. The level of Sundry Creditors should be

20320320320320320349 49

49 of 203

compared with the earlier accepted level. Higher level of Sundry Creditors indicates that the

borrower is getting more credit period fro the goods purchased.

Inventory

Non-moving items and slow moving items should be netted off from the total inventory and

it should be treated as non current assets or intangible assets.

Sundry Debtors

The bills discounting / book debt limits are fixed based on the level of Sundry Debtors. In

respect of bills which are not discounted and book debts, age-wise classification should be

called for to ascertain that the debtors are being realized promptly and there are not

bad/doubtful debits declared as Current Asset. Further, it should be verified from the list of

debtors to ensure that the debtors declared are on account of genuine trade transactions

and do not include accommodation bills. Bills drawn on allied / sister concerns are to be

carefully reviewed to ensure that they have been drawn on account of genuine transactions.

Doubtful, old and unrecoverable debtors to be treated as non current assets or intangible

assets.

Loans & Advances

Items outstanding under loans & advances are to be carefully reviewed and it is to be

ensured that there is no diversion and items stated under Current Assets are realizable

within a period of one year. An item on advances recoverable in cash or kind to be reviewed

critically with detailed analysis of the groupings. Particularly loans and advances to

subsidiaries/associates to be analysed along with the performance of each such companies.

In case the performance of those subsidiaries/associates companies are found to be

deteriorating or unsatisfactory, the same has to be classified as non current or intangible

assets.

Investments

The outstandings under investments in Subsidiaries/Associates to be critically reviewed and

normalcy is to be ensured. If the investment is made in the listed securities then market

value of the same is to be ascertained. If the market value is less than the book value, the

difference be treated as non current assets or intangible assets.

20320320320320320350 50

50 of 203

Analysis and Interpretation of Financial Statements

Though the method to be adopted for analysis of a Balance Sheet cannot be generalized

and each case has to be dealt with depending upon various factors, the following are some

hints:

Obtain the Audited financial statements for the last two years for the purpose of

comparison / study.

Arrive at the Net Worth (Capital + Reserves excluding revaluation reserves +-Surplus /

deficit in P&L Account – Intangible Assets if any). If it shows a declining trend, call for

the steps being taken to improve the situation.

Arrive at the Net Working Capital & Current Ratio. If the same has deteriorated,

borrower should be asked to bring in additional long term funds so that a prescribed

minimum current ratio of is achieved.

A negative Net Working Capital indicates liquidity crunch. Examine the causes –

Whether there is a diversion of short term funds to long term uses or the Net Worth has

deteriorated due to losses / withdrawal from Current Accounts by partners. Call for

corrective measures from the borrower.

Compare the levels of Current Assets over the years. Identify and ascertain the

chargeable Current Assets and exclude Non-Current Assets for the purpose of arriving at

MPBF.

If funds invested outside including in Subsidiary Companies / affiliates have resulted in

deterioration of current ratio below prescribed level, borrower should be asked to bring

back the diverted funds immediately.

Examine whether the borrower has made any other diversion by way of investments in

quoted / unquoted securities / stocks indulged in inter-corporate deposits etc., during

the year. If the current ratio is unfavourable, borrower should be asked to bring in

funds to improve the position. Performance of the subsidiaries/associates to be reviewed

critically to ensure that the investments are realizable.

Compare the Cash, Bank Balance and Deposits and ensure that the borrower is confining

the dealings with us only. If the same are kept with other banks, call for the reasons.

Analyse ‘Other Current Assets’ declared and ensure that these are of current nature only.

Particularly and item, Advances recoverable in cash or Kind necessitates thorough

scrutiny.