Winning Friends and Infliencing Expectations: The … and...• The perfect storm, with a tipping...

33

Building Credibility and Influencing Expectations: The Evolution of Central Bank Communication Monique Reid, Stellenbosch Pierre Siklos, WLU & BSIA 1

Transcript of Winning Friends and Infliencing Expectations: The … and...• The perfect storm, with a tipping...

Building Credibility and Influencing Expectations: The Evolution of Central

Bank CommunicationMonique Reid, StellenboschPierre Siklos, WLU & BSIA

1

What is a Central Banker to Do? 2019 Edition

• Qualities desirable in central bank communication?Consider goals:

• "[O]penness is an obligation of a central bank in a free and democratic society.” (Greenspan 2002)

• “For not only do expectations about policy matter, but, at least under current conditions, very little else matters.” (Woodford 2003, pg. 3; italics in original)

• The ‘quiet revolution’ (Blinder, 2008) is a ‘one way street’ (Blinder, 2017 and Siklos, 2018), despite …

• Lack acceptable theoretical framework • Existing theory has not performed well against the data

2

‘the concept of inflation expectations is quite undertheorised’ Tarullo (2017: 13)

Canada ECB South Africa

Expectations but Communication NOT explicitly mentioned. WHY? Whose expectations never clearly spelled out

THE MONETARY TRANSMISSION MECHANISM: THREE EXAMPLES

3

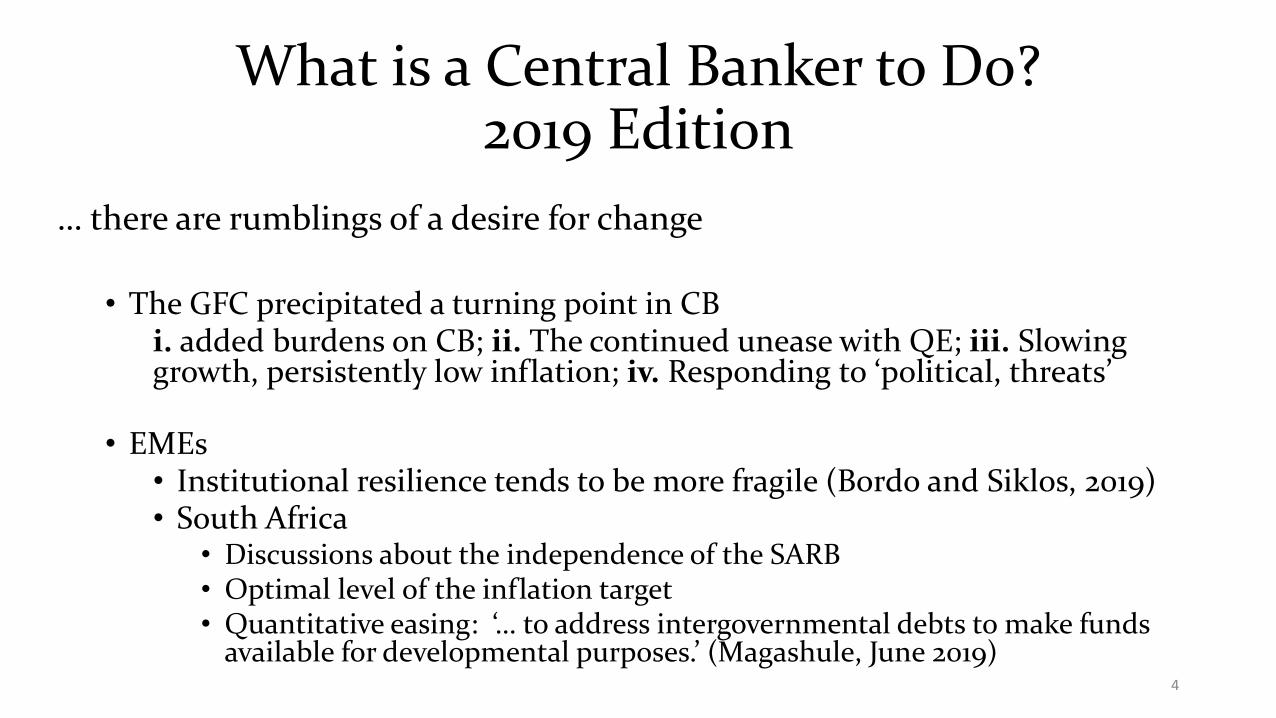

What is a Central Banker to Do? 2019 Edition

… there are rumblings of a desire for change

• The GFC precipitated a turning point in CB i. added burdens on CB; ii. The continued unease with QE; iii. Slowing growth, persistently low inflation; iv. Responding to ‘political, threats’

• EMEs• Institutional resilience tends to be more fragile (Bordo and Siklos, 2019)• South Africa

• Discussions about the independence of the SARB • Optimal level of the inflation target• Quantitative easing: ‘… to address intergovernmental debts to make funds

available for developmental purposes.’ (Magashule, June 2019)4

The Strategy of CB Communication

• Flourishing empirical literature is offering insights• Improve theory through the insights of how expectations are formed

• What the paper seeks to do?• Explore the evolution of CBC globally• Provide some evidence (direct & indirect) on the scope and impact of

CBC globally with an EME and South African flavour…drawing on our current research (Reid, Siklos, Du Plessis, and others)

• CBC today: where do we go from here?

5

The Strategy of CB Communication

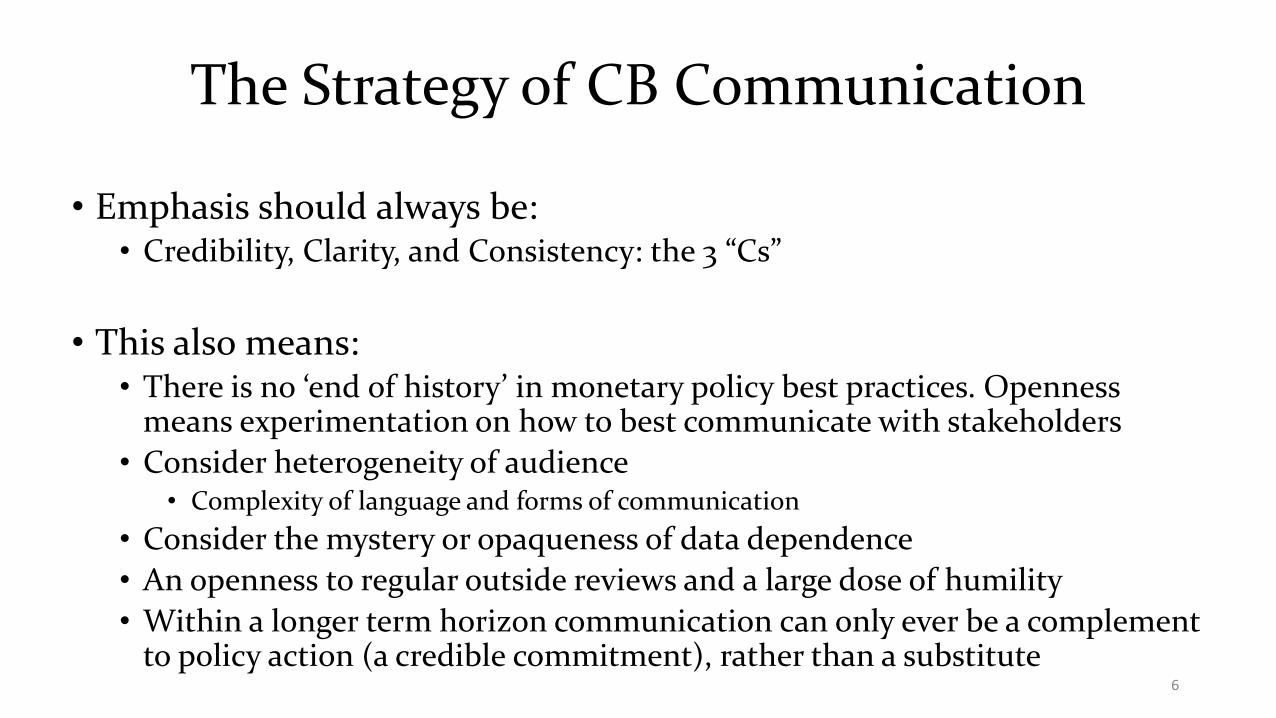

• Emphasis should always be:• Credibility, Clarity, and Consistency: the 3 “Cs”

• This also means:• There is no ‘end of history’ in monetary policy best practices. Openness

means experimentation on how to best communicate with stakeholders• Consider heterogeneity of audience

• Complexity of language and forms of communication • Consider the mystery or opaqueness of data dependence• An openness to regular outside reviews and a large dose of humility• Within a longer term horizon communication can only ever be a complement

to policy action (a credible commitment), rather than a substitute6

The Sparks that Kindled Interest in CBC: Why and How It became Critical for the Conduct of Monetary Policy

7

Why and How It became Critical for the Conduct of Monetary Policy

WHEN? • The perfect storm, with a tipping point in the 1990s: stagflation, search for a new anchor,

passive fiscal policy led to primacy of MP in economic stabilization. Pressure to provide autonomy but democratic accountability also required greater transparency.

WHY?• Improve and maintain credibility and trust as by-products • A forward-looking MP requires inflation expectations management

HOW?• By increasing transparency …if not always, clarity• “Only with explicit performance targets will accountability arrangements be truly

effective…helpful in providing a more stable and predictable environment” (Thiessen 2001, pp. 24, 39)

Many EMEs adopted similar strategies (Bordo and Siklos, 2019) 8

CBC: ImpactHigh Frequency Impact• CBC may ‘create news’, and • If successful, reduce ‘noise’ (volatility?)

• Examples: short-run exchange rate movements, interest rate movements but not inflation expectations

Low Frequency Impact• CBC helps manage/anchor inflation expectations

• “For not only do expectations about policy matter, but, at least under current conditions, very little else matters.” (Woodford 2003, pg. 3; italics in original)

• Whose expectations?• Takes as given credibility and the existence of a clear mandate• Determined by the MP strategy (i.e., IT versus alternatives)

• NOTE: POTENTIAL TENSION WITH A CB’S MANDATE (“inflation nutter” syndrome)9

The Tactics of Central Bank Communications

• It is only recently (relative to CB’s “long” history) that CB have begun to treat “communication” as an additional channel

• Often communication strategies are not clear

• Complement? Substitute?

“monetary policy is 98% talk and 2% action.” (Bernanke, 2015)

• Just as there are constraints on the use of MP tools (conventional or unconventional) there are similar constraints on CBC

• Scope; Timing; Audiences (receptiveness and comprehension); Monetary policy strategy … and others

• Available discretion in communications may differ between EME and AE• In both cases, there could be too little or too much activism 10

Forms of Central Bank Communication

11

Tacticsof CBC: Traditional; 4 Case Studies

BANK OF CANADA BOARD OF GOVERNORS BANCO CENTRAL DE CHILE SOUTH AFRICAN RESERVE BANK

SURVEYS (2) Surveys (18) SURVEYS (4) SURVEYS (12)

PRESS RELEASE PRESS RELEASE PRESS RELEASE PRESS RELEASE

BRIEFING BRIEFING BRIEFING BRIEFING

MINUTES (15) MINUTES (15) (16)

SPEECHESTESTIMONY

SPEECHESTESTIMONY

SPEECHES(17)

SPEECHESTESTIMONY

CONSULTATIONS(5) CONSULTATIONS(5) (13)

ANNUAL REPORT ANNUAL REPORT ANNUAL REPORT ANNUAL REPORT

FINANCIAL STABILITY REPORT FINANCIAL STABILITY REPORT FINANCIAL STABILITY REPORT FINANCIAL STABILITY REPORT

MPR(7) MPR(7) MPR(7) MPR(7)

CONFERENCESCALENDARWORKING PAPERSAWARDS

CONFERENCESCALENDARWORKING PAPERSAWARDS

CONFERENCESCALENDARWORKING PAPERSAWARDS

CONFERENCESCALENDARWORKING PAPERSAWARD

ECONOMIC REVIEW(8) ECONOMIC REVIEW(8) ECONOMIC REVIEW(8)

COMMUNICATIONS POLICY COMMUNICATIONS POLICY

(9) MODELPOLICY RULE (14)

STRATEGIC PLAN(10)

(10) STRATEGIC PLAN STRATEGIC PLAN I11)

GOVERNANCE DOCUMENTS GOVERNANCE DOCUMENTS GOVERNANCE DOCUMENTS GOVERNANCE DOCUMENTS12

Forms of CBC: New and Emerging

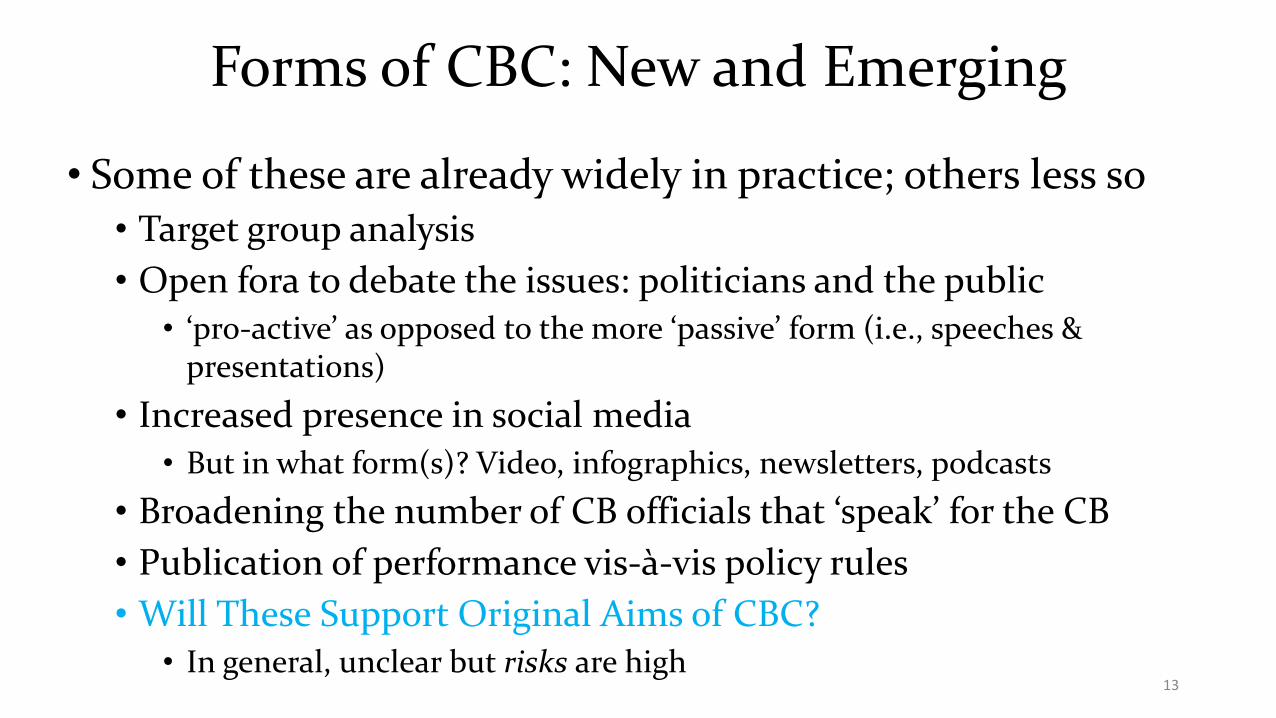

• Some of these are already widely in practice; others less so• Target group analysis• Open fora to debate the issues: politicians and the public

• ‘pro-active’ as opposed to the more ‘passive’ form (i.e., speeches & presentations)

• Increased presence in social media• But in what form(s)? Video, infographics, newsletters, podcasts

• Broadening the number of CB officials that ‘speak’ for the CB• Publication of performance vis-à-vis policy rules• Will These Support Original Aims of CBC?

• In general, unclear but risks are high13

Challenges in CBCA. A (Partial) List of CBC ChallengesB. Identifying the challenges: Outline of a FrameworkC. Who Listens to What?D. The Qualitative Dimension of CBC: The Promise and Perils of Content AnalysisE. Inflation Expectations and CBC: International and South African EvidenceF. Communicating With a Diverse Audience: the example of Non-Financial ExpertsG. CBC and the Stance of Monetary Policy

14

CBC Challenges: What Have We Learned?There are quite a number of challenges, including:

• ‘Excessive’ reliance on unobserved variables distorts effectiveness of CBC and can be misleading (e.g., r* is an AE problem not a global one)

• Treating MP ‘surprises’ in normal and crisis times contradicts what CB say and evidence (differences in volatility; overreaction of financial markets)

• Reliance on models ignores the need to develop a communications strategy to explain the results to the public, and downplays the role of judgment in delivering MP (e.g., what we can learn from weather forecasting; Haldane 2014). Tunnel vision and myopia risks (Siklos 1998) remain

• There is too little emphasis on the role of monetary-fiscal cooperation/coordination (an old lesson that needs reminding; Laidler et. al. 1997). The central bank may be left feeling overburdened as mandates become less clear

We will focus in this presentation on a limited number of them15

D. The Qualitative Dimension of CBC: The Promise and Perils of Language

16

Contrasting Algorithms: What to Make of Them?

-5

-4

-3

-2

-1

0

1

2

3

4

1955 1960 1965 1970 1975 1980 1985 1990 1995 2000 2005

change in FFR WS

Cha

nge

in fe

d fu

nds

rate

and

WS

equa

tion

(2)

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

12%

-1.6

-1.2

-0.8

-0.4

0.0

0.4

0.8

1.2

1.6

2.0

2.4

55 60 65 70 75 80 85 90 95 00 05 10

change in FFR DICTION indicator

chan

ge in

fed

fund

s ra

te (%

)

DIC

TION

indicator from factor m

odel

The DICTION indicator is based on a (factor) model that includes activity, certainty, optimism, and commonality.

Bars indicate bias towards Hawkish (+)/Dovish (-)

Benchmark No Benchmark

Dot.com

Oil price shocks

Volcker

Minutes of FOMC Meetings; Siklos (2019)

The Influence of a benchmarkUS

17

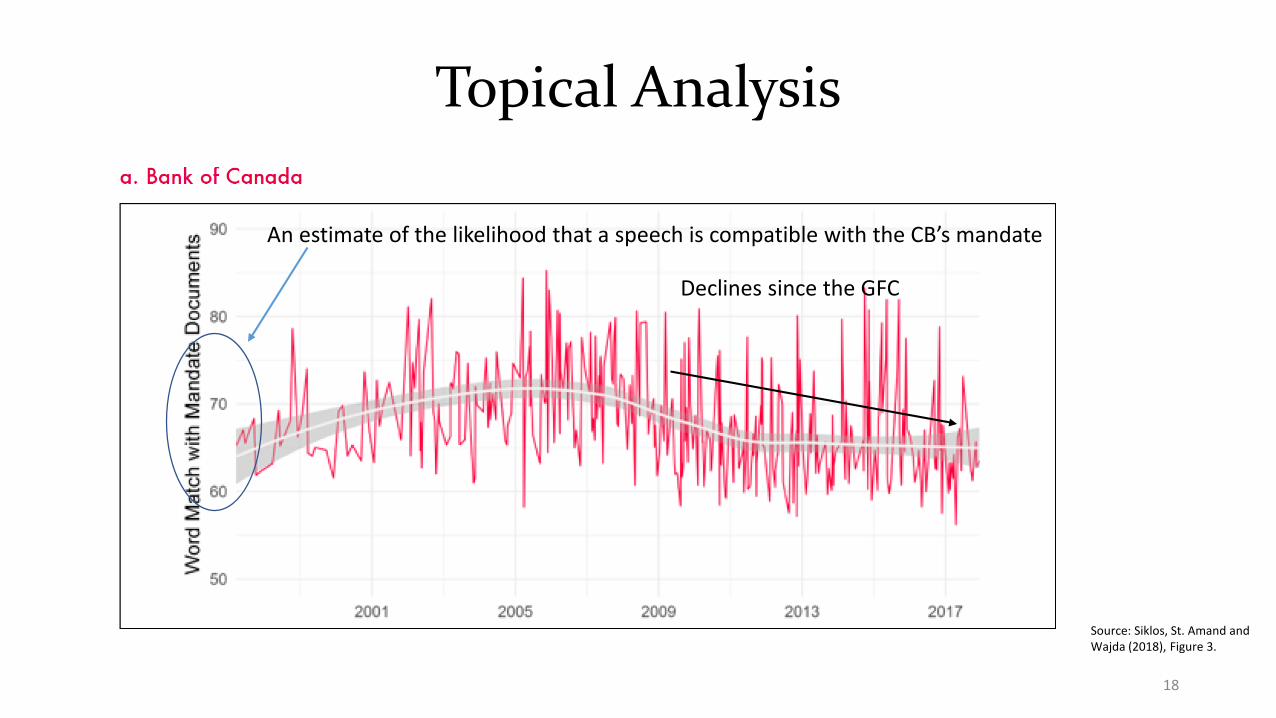

Topical Analysis

Declines since the GFC

Source: Siklos, St. Amand andWajda (2018), Figure 3.

An estimate of the likelihood that a speech is compatible with the CB’s mandate

18

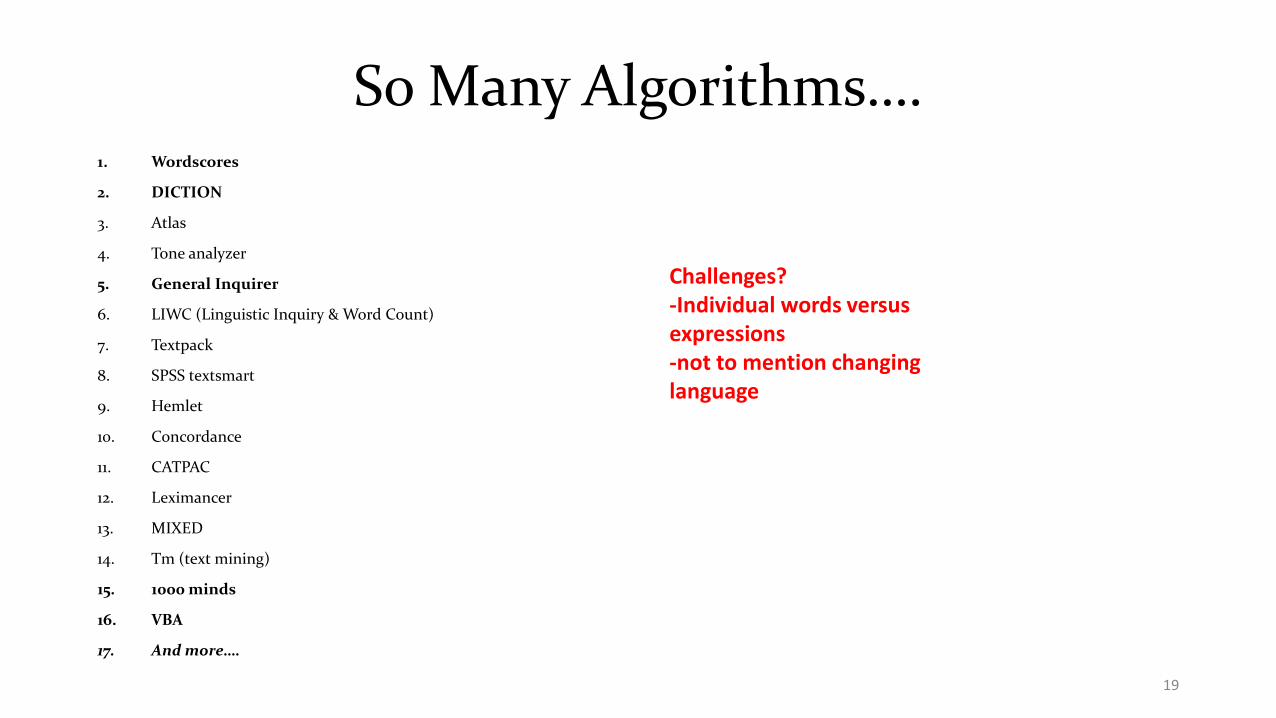

So Many Algorithms….1. Wordscores

2. DICTION

3. Atlas

4. Tone analyzer

5. General Inquirer

6. LIWC (Linguistic Inquiry & Word Count)

7. Textpack

8. SPSS textsmart

9. Hemlet

10. Concordance

11. CATPAC

12. Leximancer

13. MIXED

14. Tm (text mining)

15. 1000 minds

16. VBA

17. And more….

Challenges? -Individual words versus expressions-not to mention changing language

19

The SARB’s CBC and Its Mandate

20

Real GDP growth Inflation

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

-4

-2

0

2

4

6

8

10

1/19

/01

11/1

5/01

11/2

8/02

12/1

1/03

12/9

/04

12/8

/05

12/7

/06

12/6

/07

12/1

1/08

8/13

/09

5/13

/10

5/12

/11

5/24

/12

5/23

/13

5/22

/14

5/21

/15

5/19

/16

5/25

/17

5/24

/18

5/23

/19

NEGATIVE_SARB_WORDS za_rgdpg

Wor

d Co

unt

Real GDP G

rowth (%

)

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

0

2

4

6

8

10

12

14

1/19

/01

11/1

5/01

11/2

8/02

12/1

1/03

12/9

/04

12/8

/05

12/7

/06

12/6

/07

12/1

1/08

8/13

/09

5/13

/10

5/12

/11

5/24

/12

5/23

/13

5/22

/14

5/21

/15

5/19

/16

5/25

/17

5/24

/18

5/23

/19

FORWARD_LOOKING_SARB_WORDSza_inf

Annualized %

SARB’s MPC Communication: Drawing Some General Lessons

• Unlike other CB no trends in # words used in MPC Statements• Forward-looking inflation language playing a more prominent

role in MPC communication in recent years: a role in anchoring?• MPC communication on exchange rate steady but not prominent:

a contrast with communication by media• Like many other CB the SARB displays a concern for asset prices

but this takes a back seat to inflation and real economic concerns• There are some asymmetries in SARB communication: Rand

depreciations vs. appreciations; positive vs. negative outlook

21

E. Inflation Expectations and CBCSome South African Evidence

22

Some Simple Specifications

• How the past and “MR” inflation expectations influence “SR” inflation expectations

• How “MR” inflation expectations are linked to the past or the CB’s goal

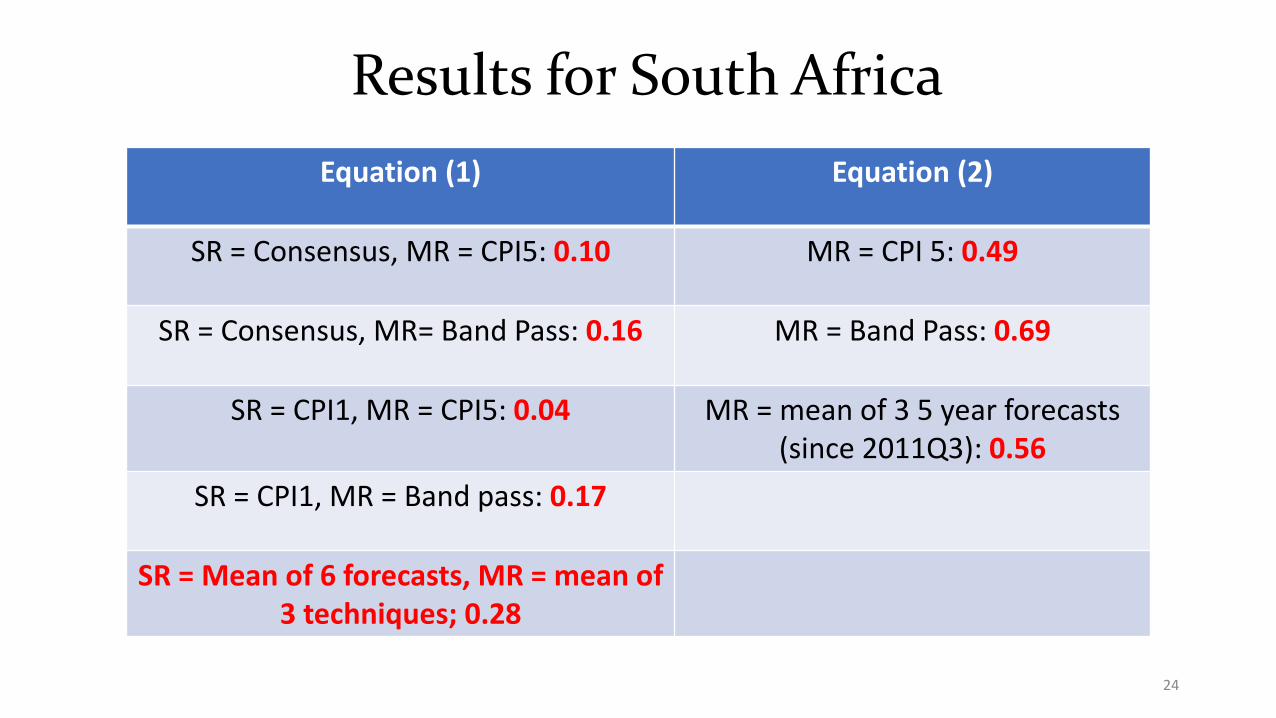

𝜋𝜋𝑡𝑡+1𝑒𝑒 = 𝜆𝜆𝜋𝜋𝑡𝑡−1 + (1 − 𝜆𝜆)𝜋𝜋𝑡𝑡+5𝑒𝑒 (1)

23

Results for South AfricaEquation (1) Equation (2)

SR = Consensus, MR = CPI5: 0.10 MR = CPI 5: 0.49

SR = Consensus, MR= Band Pass: 0.16 MR = Band Pass: 0.69

SR = CPI1, MR = CPI5: 0.04 MR = mean of 3 5 year forecasts (since 2011Q3): 0.56

SR = CPI1, MR = Band pass: 0.17

SR = Mean of 6 forecasts, MR = mean of 3 techniques; 0.28

24

Main Conclusions

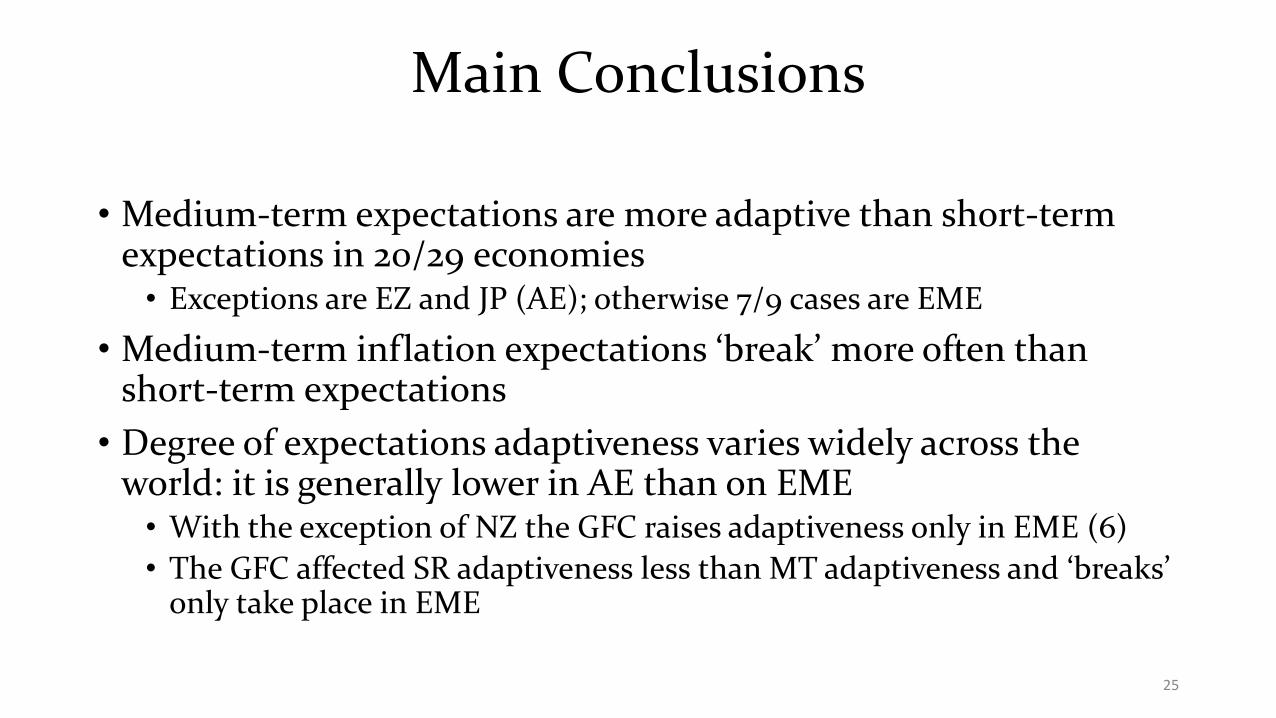

• Medium-term expectations are more adaptive than short-term expectations in 20/29 economies

• Exceptions are EZ and JP (AE); otherwise 7/9 cases are EME

• Medium-term inflation expectations ‘break’ more often than short-term expectations

• Degree of expectations adaptiveness varies widely across the world: it is generally lower in AE than on EME

• With the exception of NZ the GFC raises adaptiveness only in EME (6)• The GFC affected SR adaptiveness less than MT adaptiveness and ‘breaks’

only take place in EME

25

Varieties of Inflation Expectations in South Africa: 3 Views

26

0%

1%

2%

3%

4%

5%

6%

7%

8%

9%

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018

HHOLD_ALL_FH HHOLD_MALE_FH HHOLD_FEMALE_FHHHOLD_14K_FH HHOLD_1K3K_FH HHOLD_50_FH

HHOLD_1624_FH

2

4

6

8

10

12

00 01 02 03 04 05 06 07 08 09 10

HHOLD_ALL HHOLD_FEMALE HHOLD_MALEHHOLD_14K HHOLD_1K3K HHOLD_50

HHOLD_1624

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

2011 2012 2013 2014 2015 2016 2017 2018 2019

HHOLD_ALL_FH HHOLD_MALE_FH HHOLD_FEMALE_FHHHOLD_14K_FH HHOLD_1K3K_FH HHOLD_50_FH

HHOLD_1624_FH

Fixed Horizon forecasts throughout Pre-2011: Fixed Event Post-2010: Fixed Horizon

SARB’s ITrange SARB’s IT

Upper range

Disagreement About Future Inflation in South Africa: Selected Socio-EconomicGroups

27

.00

.04

.08

.12

.16

.20

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

DIS1_MALE_FH

.00

.05

.10

.15

.20

.25

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

DIS1_FEMALE_FH

0

1

2

3

4

520

0020

0120

0220

0320

0420

0520

0620

0720

0820

0920

1020

1120

1220

1320

1420

1520

1620

1720

1820

19

DIS2_14K_FH

0

1

2

3

4

5

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

DIS2_1K3K_FH

0

1

2

3

4

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

DIS2_50_FH

0

1

2

3

4

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

2017

2018

2019

DIS2_1624_FH

Disagreement a la Siklos (2013)=1/(#forecasts-1) XSquared deviation from Aggregate CPI forecast(fixed horizon)

Level of Aggregation matters

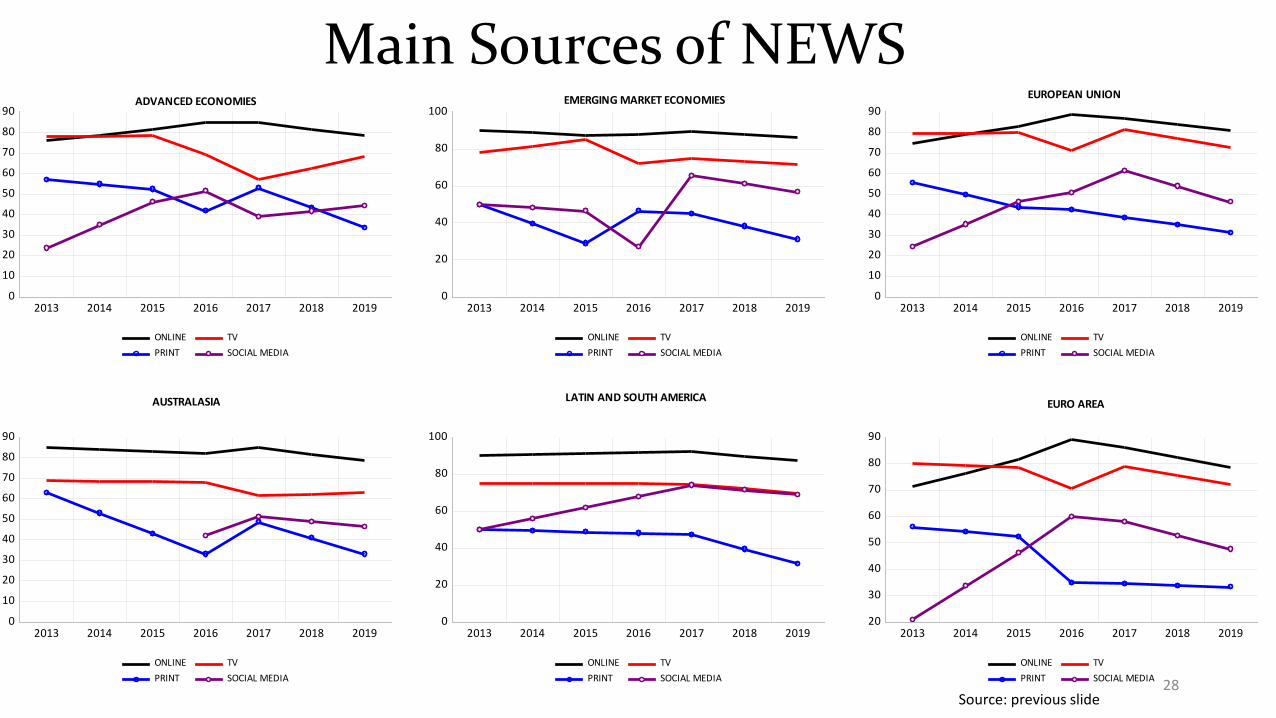

Main Sources of NEWS

0

10

20

30

40

50

60

70

80

90

2013 2014 2015 2016 2017 2018 2019

ONLINE TVPRINT SOCIAL MEDIA

0

20

40

60

80

100

2013 2014 2015 2016 2017 2018 2019

ONLINE TVPRINT SOCIAL MEDIA

0

10

20

30

40

50

60

70

80

90

2013 2014 2015 2016 2017 2018 2019

ONLINE TVPRINT SOCIAL MEDIA

0

10

20

30

40

50

60

70

80

90

2013 2014 2015 2016 2017 2018 2019

ONLINE TVPRINT SOCIAL MEDIA

0

20

40

60

80

100

2013 2014 2015 2016 2017 2018 2019

ONLINE TVPRINT SOCIAL MEDIA

20

30

40

50

60

70

80

90

2013 2014 2015 2016 2017 2018 2019

ONLINE TVPRINT SOCIAL MEDIA

ADVANCED ECONOMIES EMERGING MARKET ECONOMIES EUROPEAN UNION

AUSTRALASIA LATIN AND SOUTH AMERICA EURO AREA

Source: previous slide28

Sources of News? The South African Experience

.0

.1

.2

.3

.4

.5

TV

Newspa

per

Intern

etRad

io

Own exp

erien

ce

Family

and f

riend

s

SOURCE of INFORMATION

Perc

ent o

f ALL

Res

pond

ents

SOURCE: Survey data collected by the authors (via AC Nielsen)29

Information Sources: The Conclusions So Far

• What/Who the public listens to varies considerably around the world BUT

• Its personal: friends as a source of information is important, stable, and global

• TV and newspaper are declining in importance while the internet’s importance is rising

• Trust, in media is more comparable across economies than choice of news sources but data are mixed

• Social media is not catching up to other sources and has peaked or shows signs of declining in importance. Will it become the ‘media meteor’?

• What we don’t know is: how much inattentiveness is there?• For EMEs: The missing audiences? Governments and the Press

30

F. How to Communicate With Non-Financial Experts: An Absence of Shared Objectives

• Inflation expectations continue not to be well-understood and conflict with ‘standard’ theoretical rationales

• Whose expectations matter?

• Literature (and some policy makers) appear to be moving strongly in the direction of focusing on household and firm surveys of inflation expectations. Good news?

• YES• helps identify successes & failures of CBC

• NO• There is a strong element of noise (and other biases) we have yet to understand

• “When dealing with people, let us remember we are not dealing with creatures of logic. We are dealing with creatures of emotion, creatures bristling with prejudices…” (Carnegie 1936)

• Surveys of interest (i.e., households and firms) are, in the main episodic and recent31

F. How to Communicate With Non-Financial Experts: An Absence of Shared Objectives

• The media does not attempt (nor should it be required) to further the central bank’s interests

• CB need to speak in the language of their audience(s), that is, speak in tones that are aligned with the public’s concerns

• CBC needs to better understand media bias (Gentzkow and Shapiro 2010) and the characteristics and incentives of media reporting on inflation (Reid, Bergman, Du Plessis, Bergman, and Siklos, forthcoming)

‘Although carefully crafting inflation messages are indeed important, this approach fails to recognize that the media serves multiple, incompatible interests, which ultimately may make the media an unreliable partner.’ (Reid, Bergman, Du Plessis, Bergman, and Siklos, forthcoming)

EMEs and AEs face the same challenges but some are more acute for EMEs

32

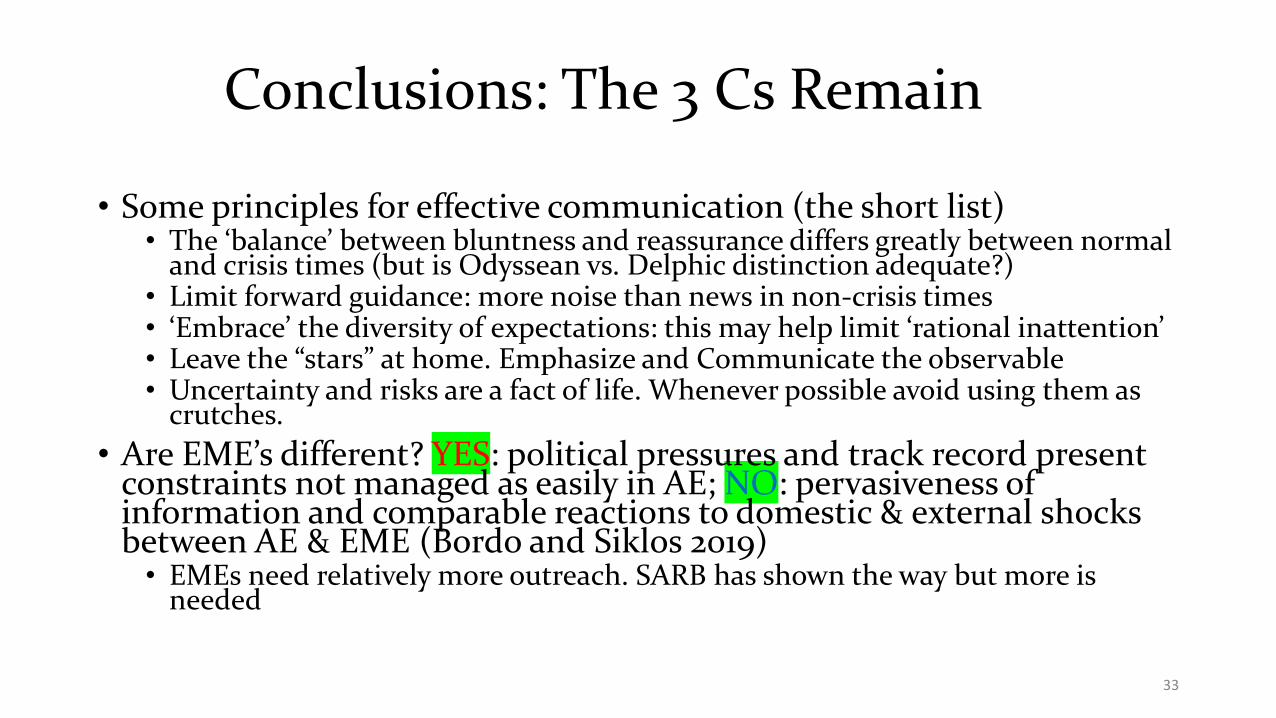

Conclusions: The 3 Cs Remain

• Some principles for effective communication (the short list)• The ‘balance’ between bluntness and reassurance differs greatly between normal

and crisis times (but is Odyssean vs. Delphic distinction adequate?)• Limit forward guidance: more noise than news in non-crisis times• ‘Embrace’ the diversity of expectations: this may help limit ‘rational inattention’ • Leave the “stars” at home. Emphasize and Communicate the observable• Uncertainty and risks are a fact of life. Whenever possible avoid using them as

crutches.• Are EME’s different? YES: political pressures and track record present

constraints not managed as easily in AE; NO: pervasiveness of information and comparable reactions to domestic & external shocks between AE & EME (Bordo and Siklos 2019)

• EMEs need relatively more outreach. SARB has shown the way but more is needed

33