WIND Telecomunicazioni - Windgroup · WIND Telecomunicazioni First Half 2015 Results Delivering...

20

WIND Telecomunicazioni First Half 2015 Results Delivering Solid Performance August 7, 2015

Transcript of WIND Telecomunicazioni - Windgroup · WIND Telecomunicazioni First Half 2015 Results Delivering...

WIND Telecomunicazioni First Half 2015 Results

Delivering Solid Performance

August 7, 2015

2

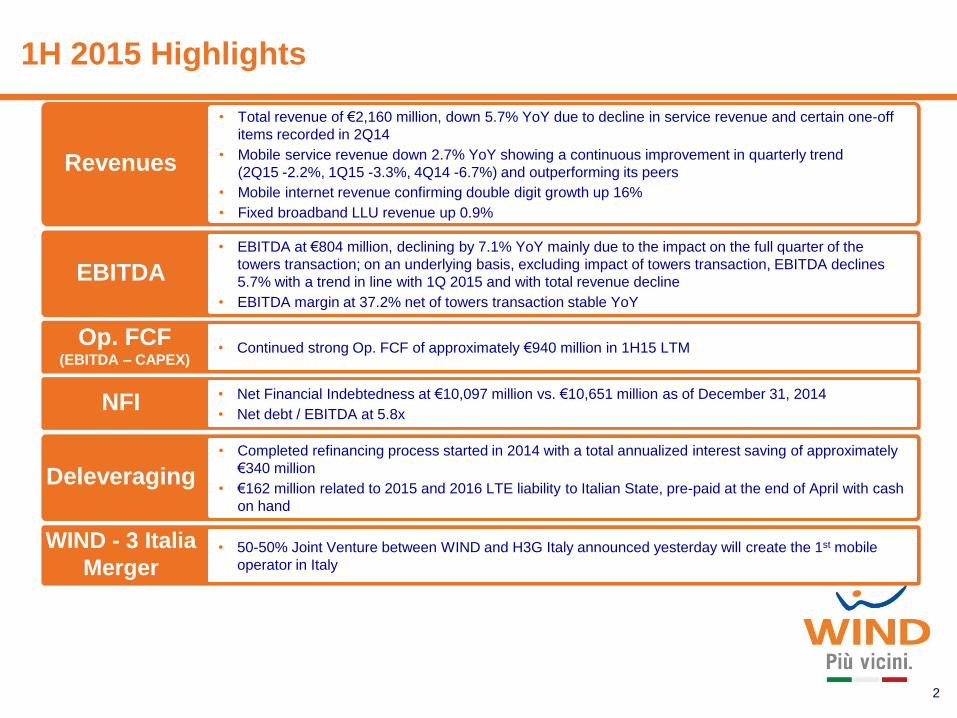

1H 2015 Highlights

Revenues

• Total revenue of €2,160 million, down 5.7% YoY due to decline in service revenue and certain one-off

items recorded in 2Q14

• Mobile service revenue down 2.7% YoY showing a continuous improvement in quarterly trend

(2Q15 -2.2%, 1Q15 -3.3%, 4Q14 -6.7%) and outperforming its peers

• Mobile internet revenue confirming double digit growth up 16%

• Fixed broadband LLU revenue up 0.9%

EBITDA

• EBITDA at €804 million, declining by 7.1% YoY mainly due to the impact on the full quarter of the

towers transaction; on an underlying basis, excluding impact of towers transaction, EBITDA declines

5.7% with a trend in line with 1Q 2015 and with total revenue decline

• EBITDA margin at 37.2% net of towers transaction stable YoY

Op. FCF (EBITDA – CAPEX)

• Continued strong Op. FCF of approximately €940 million in 1H15 LTM

NFI • Net Financial Indebtedness at €10,097 million vs. €10,651 million as of December 31, 2014

• Net debt / EBITDA at 5.8x

Deleveraging

• Completed refinancing process started in 2014 with a total annualized interest saving of approximately

€340 million

• €162 million related to 2015 and 2016 LTE liability to Italian State, pre-paid at the end of April with cash

on hand

WIND - 3 Italia

Merger • 50-50% Joint Venture between WIND and H3G Italy announced yesterday will create the 1st mobile

operator in Italy

3

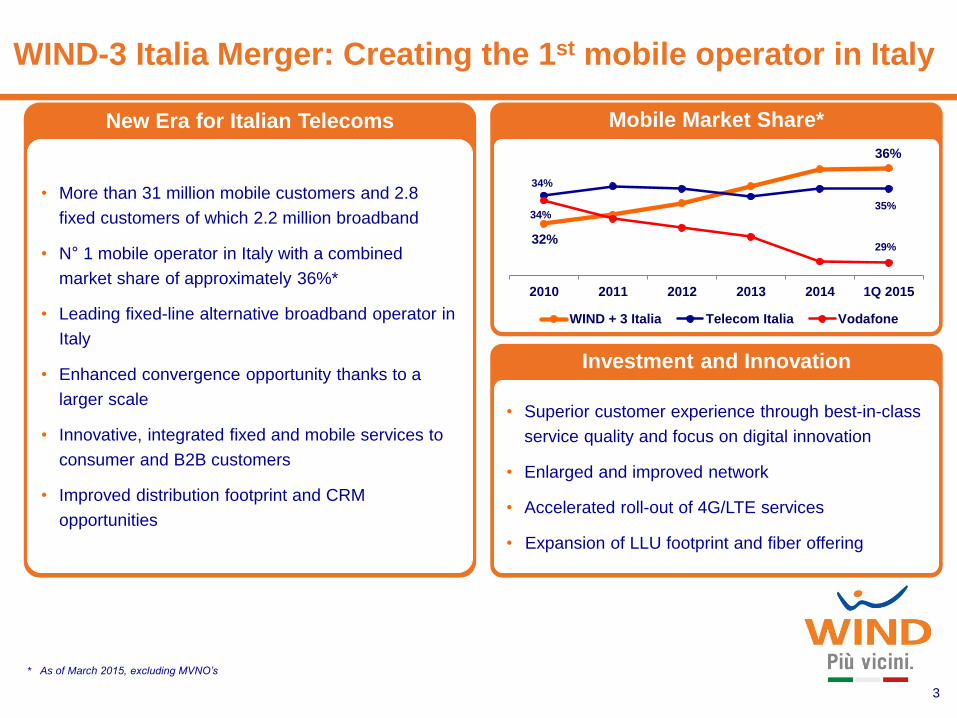

Mobile Market Share* New Era for Italian Telecoms

WIND-3 Italia Merger: Creating the 1st mobile operator in Italy

• More than 31 million mobile customers and 2.8

fixed customers of which 2.2 million broadband

• N° 1 mobile operator in Italy with a combined

market share of approximately 36%*

• Leading fixed-line alternative broadband operator in

Italy

• Enhanced convergence opportunity thanks to a

larger scale

• Innovative, integrated fixed and mobile services to

consumer and B2B customers

• Improved distribution footprint and CRM

opportunities

* As of March 2015, excluding MVNO’s

32%

36%

34%

35% 34%

29%

2010 2011 2012 2013 2014 1Q 2015

WIND + 3 Italia Telecom Italia Vodafone

Investment and Innovation

• Superior customer experience through best-in-class

service quality and focus on digital innovation

• Enlarged and improved network

• Accelerated roll-out of 4G/LTE services

• Expansion of LLU footprint and fiber offering

4

* Source: CSC (Sep ‘14), ISTAT (Nov ‘14)

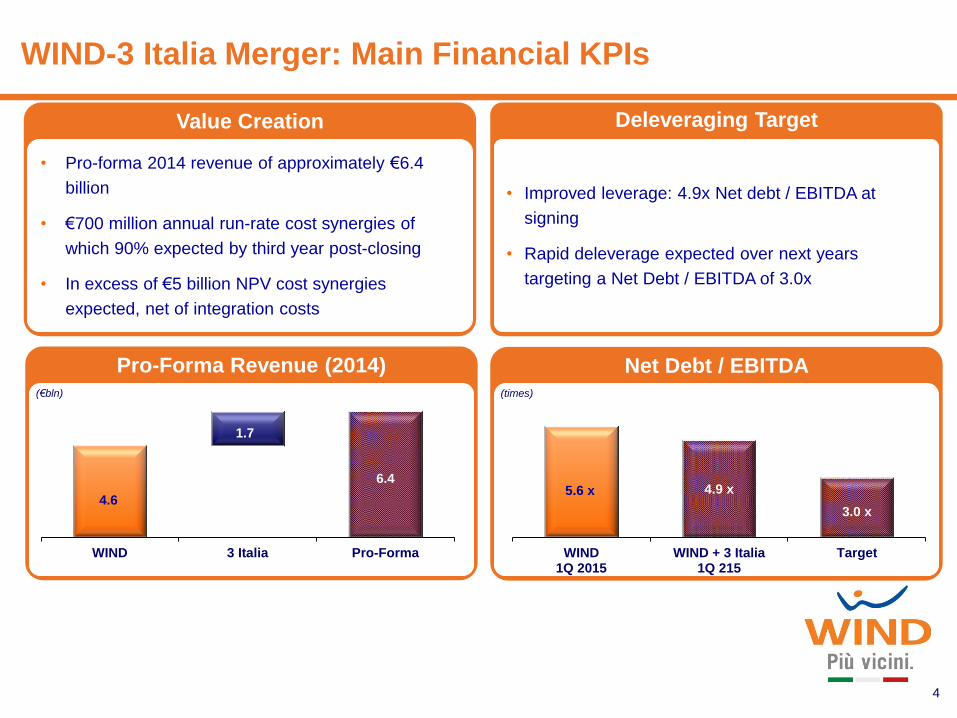

Deleveraging Target

Pro-Forma Revenue (2014) Net Debt / EBITDA

Value Creation

• Pro-forma 2014 revenue of approximately €6.4

billion

• €700 million annual run-rate cost synergies of

which 90% expected by third year post-closing

• In excess of €5 billion NPV cost synergies

expected, net of integration costs

• Improved leverage: 4.9x Net debt / EBITDA at

signing

• Rapid deleverage expected over next years

targeting a Net Debt / EBITDA of 3.0x

4.6

6.4

1.7

WIND 3 Italia Pro-Forma

5.6 x 4.9 x

3.0 x

WIND1Q 2015

WIND + 3 Italia1Q 215

Target

(€bln) (times)

WIND-3 Italia Merger: Main Financial KPIs

Highlights

Transaction Structure

• 50-50% JV of VimpelCom (VIP) and CK Hutchison Holdings (CKHH)

• VIP to contribute WIND with its existing debt

• CKHH to contribute 3 Italia on a cash and debt free basis

• No further cash contributions expected from VIP or CKHH

• Transaction conditional on parties being satisfied with regulatory approvals

Timing

• Expected closing within next 12 months subject to receiving clearance from relevant authorities

• Filing with European and Italian authorities

Management

• Company to be led by Maximo Ibarra, with an experienced combined management team

Governance

• Substantive shareholder agreement to ensure successful JV

• Board consisting of 6 directors (3 nominated by VIP, 3 by CKHH)

• Chairman rotating every 18 months, with casting vote to ensure no grid lock, first appointed by

CKHH

5

VIP CKHH

50% 50%

Holdco

WIND 3 Italia

WIND-3 Italia Merger: Key Transaction Highlights

6

* Source: CSC (Sep ‘14), ISTAT (Nov ‘14)

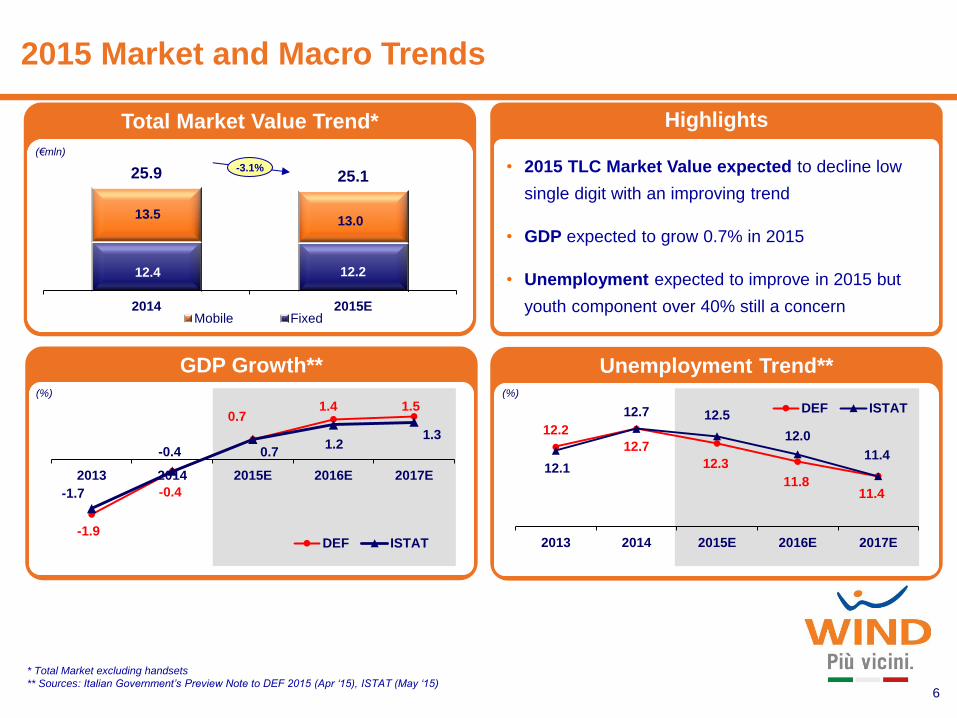

2015 Market and Macro Trends

Highlights

GDP Growth** Unemployment Trend**

12.2

12.7

12.3

11.8 11.4

12.1

12.7 12.5

12.0

11.4

2013 2014 2015E 2016E 2017E

DEF ISTAT

-1.9

-0.4

0.7 1.4 1.5

-1.7

-0.4 0.7 1.2

1.3

2013 2014 2015E 2016E 2017E

DEF ISTAT

• 2015 TLC Market Value expected to decline low

single digit with an improving trend

• GDP expected to grow 0.7% in 2015

• Unemployment expected to improve in 2015 but

youth component over 40% still a concern

Total Market Value Trend*

(€bln)

* Total Market excluding handsets

** Sources: Italian Government’s Preview Note to DEF 2015 (Apr ‘15), ISTAT (May ‘15)

(%) (%)

12.4 12.2

13.5 13.0

25.9 25.1

2014 2015EMobile Fixed

-3.1%

(€mln)

7

* Mobile Internet includes customers that have performed at least one mobile Internet event in the previous month

** Mobile average data usage measured on mobile Internet users

Outperforming in Mobile Data

Highlights

• Strong performance in data revenue with double digit

growth YoY

• Mobile internet customer base continues to increase

+13.5%

• 1.4 GB average monthly usage of active customers: 4G

data customers monthly data usage 1.5 times the

average data user

•

Mobile Internet Revenue

Mobile Internet CB*

269 312

1H 2014 1H 2015

9.7 11.0

1H 2014 1H 2015

(€mln)

(mln)

+13.5%

+16.0%

Upselling Growing Data Demand**

1.1 1.2

1.3 1.2

1.4 1.4

1Q 14 2Q 14 3Q 14 4Q 14 1Q 15 2Q 15

(GB month)

Basic

bundle

allowance

1 GB

8

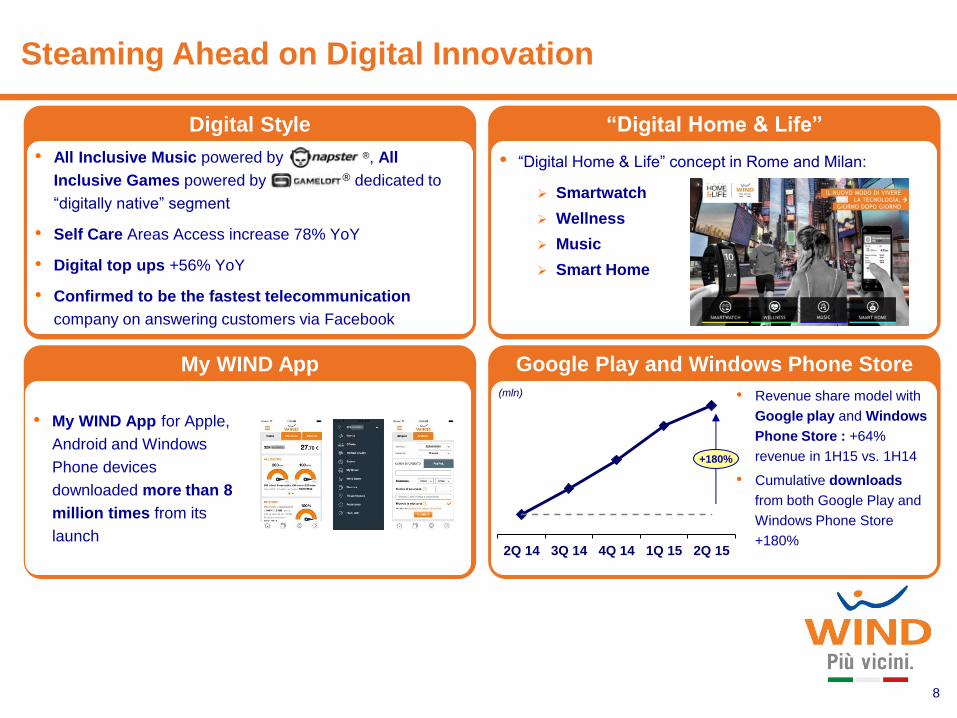

Steaming Ahead on Digital Innovation

Digital Style

• All Inclusive Music powered by ®, All

Inclusive Games powered by ® dedicated to

“digitally native” segment

• Self Care Areas Access increase 78% YoY

• Digital top ups +56% YoY

• Confirmed to be the fastest telecommunication

company on answering customers via Facebook

My WIND App

• My WIND App for Apple,

Android and Windows

Phone devices

downloaded more than 8

million times from its

launch

“Digital Home & Life”

• “Digital Home & Life” concept in Rome and Milan:

Smartwatch

Wellness

Music

Smart Home

Google Play and Windows Phone Store

• Revenue share model with

Google play and Windows

Phone Store : +64%

revenue in 1H15 vs. 1H14

• Cumulative downloads

from both Google Play and

Windows Phone Store

+180% 2Q 14 3Q 14 4Q 14 1Q 15 2Q 15

+180%

(mln)

CAPEX

9

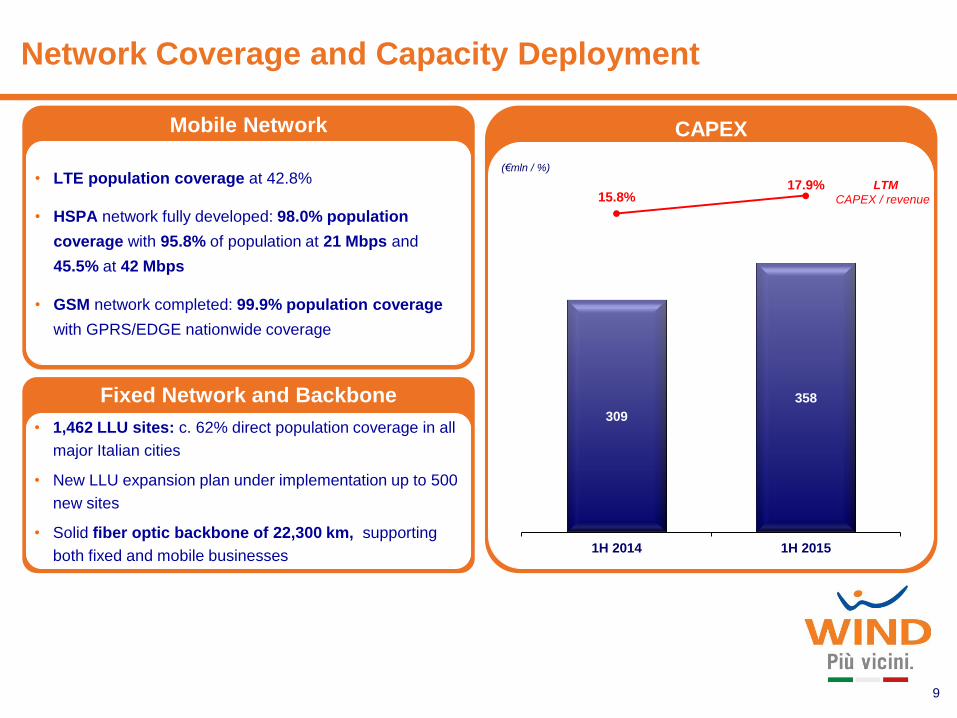

Network Coverage and Capacity Deployment

309

358

1H 2014 1H 2015

LTM

CAPEX / revenue

(€mln / %)

15.8% 17.9%

Mobile Network

• LTE population coverage at 42.8%

• HSPA network fully developed: 98.0% population

coverage with 95.8% of population at 21 Mbps and

45.5% at 42 Mbps

• GSM network completed: 99.9% population coverage

with GPRS/EDGE nationwide coverage

Fixed Network and Backbone

• 1,462 LLU sites: c. 62% direct population coverage in all

major Italian cities

• New LLU expansion plan under implementation up to 500

new sites

• Solid fiber optic backbone of 22,300 km, supporting

both fixed and mobile businesses

10

Solid Mobile Commercial Performance

Highlights

• Mobile customer base at 21.4 million declining

2.3% YoY

• Stable market share

• Total ARPU stable YoY at €11.0 increasing

versus previous quarter after more than 5 years

trend of decline in the overall market, confirming

WIND’s expectation of market recovery

• Data ARPU accounting 42% of total ARPU

increasing 8% completely offsetting the decline in

voice ARPU

Customer Base

ARPU

21.9 21.4

1H 2014 1H 2015

11.0 11.0

1H 2014 1H 2015

-2.3%

stable

% Data

on Total

(mln)

38.6% 41.6%

(€ / %)

11

Stable Performance in Fixed-Line

Voice Subscribers

Dual-play Subscribers

487 422

2,415 2,391

1H 2014 1H 2015

Indirect

Direct -1.0%

2,902 (‘000)

2,814

Broadband Subscribers

Highlights

• Fixed customer base decline mainly due to contraction of

indirect segment as a consequence of the company focus

on the direct CB

• Direct customer base marginal decline (-1.0%)

• Fixed Broadband customers up 1.5% with solid LLU

performance

• Higher value dual play customers increasing 3.9% to

almost 2 million customers

(‘000)

2,180 2,212

1H 2014 1H 2015

+1.5%

1,881 1,954

1H 2014 1H 2015

+3.9%

(‘000)

1H 2015 Financial

Performance

13

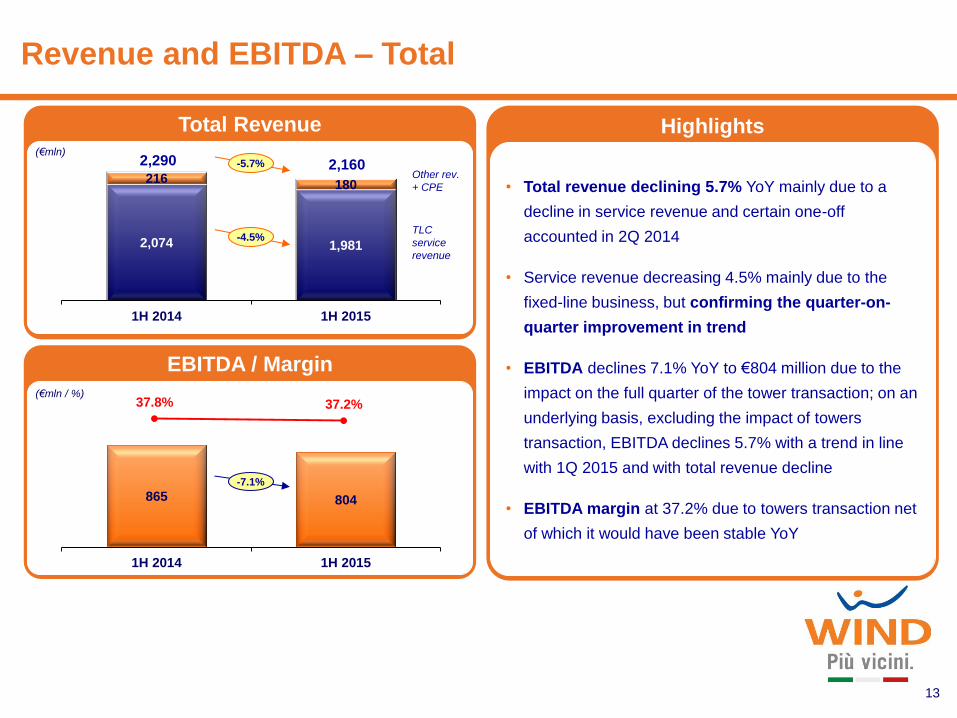

Revenue and EBITDA – Total

Highlights

• Total revenue declining 5.7% YoY mainly due to a

decline in service revenue and certain one-off

accounted in 2Q 2014

• Service revenue decreasing 4.5% mainly due to the

fixed-line business, but confirming the quarter-on-

quarter improvement in trend

• EBITDA declines 7.1% YoY to €804 million due to the

impact on the full quarter of the tower transaction; on an

underlying basis, excluding the impact of towers

transaction, EBITDA declines 5.7% with a trend in line

with 1Q 2015 and with total revenue decline

• EBITDA margin at 37.2% due to towers transaction net

of which it would have been stable YoY

Total Revenue

EBITDA / Margin

2,074 1,981

216 180

1H 2014 1H 2015

(€mln / %)

2,290 (€mln)

Other rev.

+ CPE

TLC

service

revenue

865 804

1H 2014 1H 2015

37.8% 37.2%

-5.7%

-4.5%

-7.1%

2,160

14

Revenue and EBITDA – Mobile

Highlights

• Total mobile revenue declining 4.8% with a further

improvement in service revenue trend

• Service revenue down 2.7%YoY showing a significant

improvement in trend QoQ (2Q15 -2.2%, 1Q15 -3.3%,

4Q14 -6.7%)

• Strong performance in mobile Internet with revenue up

16.0%

• EBITDA decreasing 7.8% due to the impact on the full

quarter of the tower transaction

• EBITDA Margin at 40.4% due to the towers transaction

impact net of which it would have been almost stable

Total Revenue

EBITDA / Margin

(€mln / %)

(€mln)

692 639

1H 2014 1H 2015

41.7% 40.4%

-7.8%

1,465 1,425

194 155

1H 2014 1H 2015

1,660 -4.8% 1,580

-2.7%

Other rev.

+ CPE

TLC

service

revenue

15

Revenue and EBITDA – Fixed-Line

Highlights

• Total fixed-line revenue declining 8.1% YoY with

service revenue decrease of 8.8% due to the decline in

voice volumes as a result of the decrease in pay per

use traffic coming from the increased penetration of

bundles

• EBITDA at €165 million decreasing 4.5% YoY mainly

due to the decline in revenue

• EBITDA margin increasing 1.1 p.p. to 28.4%

Total Revenue

EBITDA / Margin

609 556

22 24

1H 2014 1H 2015

(€mln / %)

(€mln)

173 165

1H 2014 1H 2015

27.4% 28.4%

-8.1%

-8.8%

-4.5%

631

Other rev.

+ CPE

TLC

service

revenue

580

16

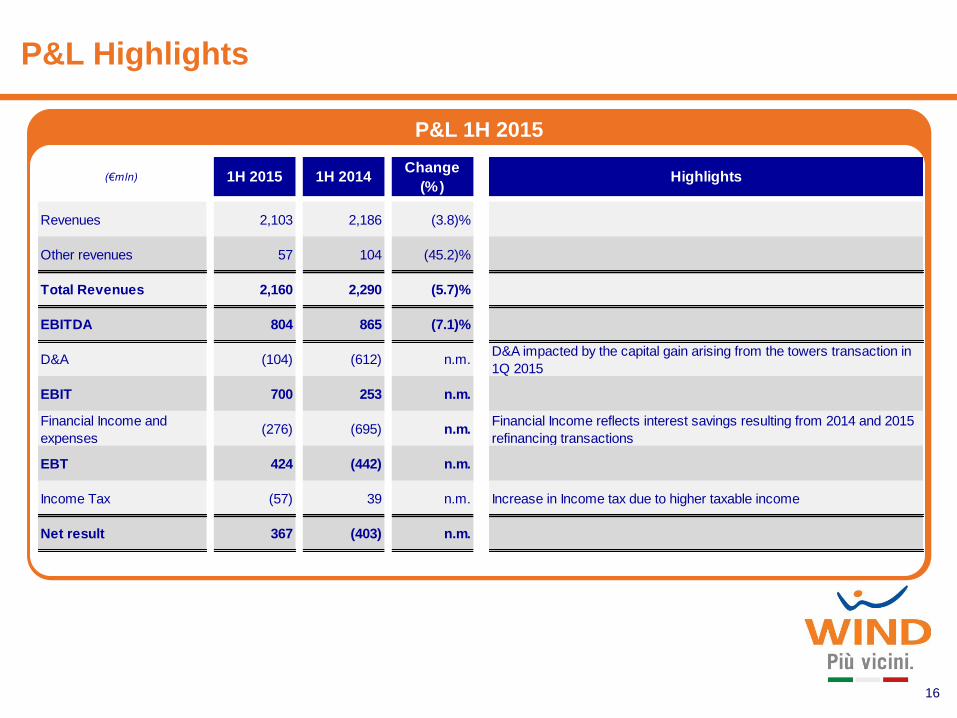

P&L Highlights

P&L 1H 2015

(€mln) 1H 2015 1H 2014Change

(%)Highlights

Revenues 2,103 2,186 (3.8)%

Other revenues 57 104 (45.2)%

Total Revenues 2,160 2,290 (5.7)%

EBITDA 804 865 (7.1)%

D&A (104) (612) n.m.D&A impacted by the capital gain arising from the towers transaction in

1Q 2015

EBIT 700 253 n.m.

Financial Income and

expenses(276) (695) n.m.

Financial Income reflects interest savings resulting from 2014 and 2015

refinancing transactions

EBT 424 (442) n.m.

Income Tax (57) 39 n.m. Increase in Income tax due to higher taxable income

Net result 367 (403) n.m.

17

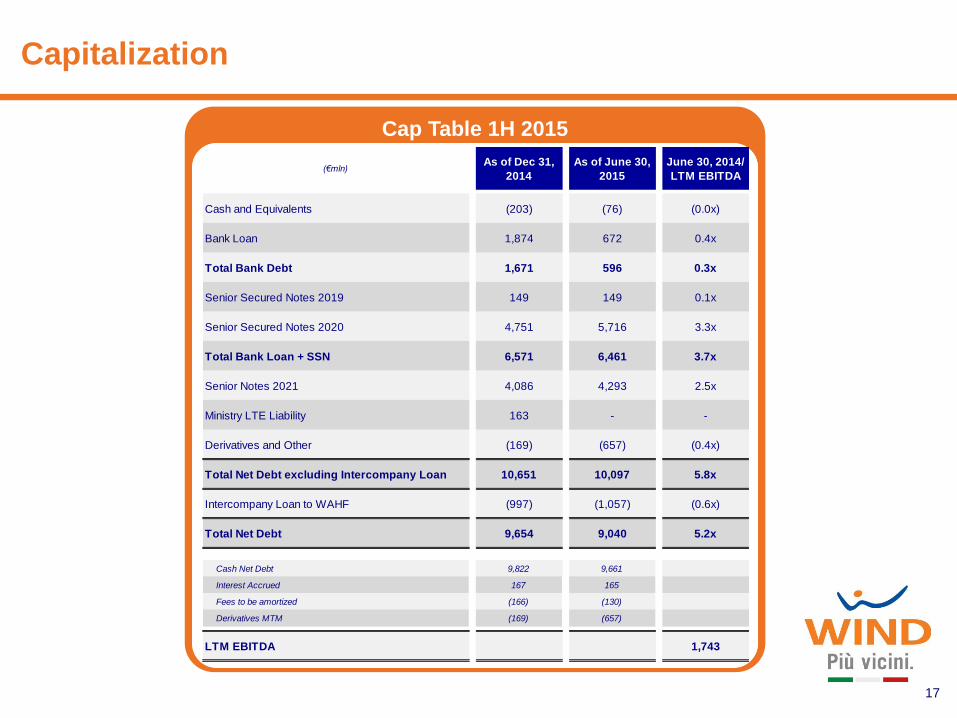

Capitalization

Cap Table 1H 2015

(€mln)As of Dec 31,

2014

As of June 30,

2015

June 30, 2014/

LTM EBITDA

Cash and Equivalents (203) (76) (0.0x)

Bank Loan 1,874 672 0.4x

Total Bank Debt 1,671 596 0.3x

Senior Secured Notes 2019 149 149 0.1x

Senior Secured Notes 2020 4,751 5,716 3.3x

Total Bank Loan + SSN 6,571 6,461 3.7x

Senior Notes 2021 4,086 4,293 2.5x

Ministry LTE Liability 163 - -

Derivatives and Other (169) (657) (0.4x)

Total Net Debt excluding Intercompany Loan 10,651 10,097 5.8x

Intercompany Loan to WAHF (997) (1,057) (0.6x)

Total Net Debt 9,654 9,040 5.2x

Cash Net Debt 9,822 9,661

Interest Accrued 167 165

Fees to be amortized (166) (130)

Derivatives MTM (169) (657)

LTM EBITDA 1,743

18 Notional amounts. USD tranche has been converted at CCS EUR/USD Exchange Rate

1H 2015

(€mln)

775 700

3,513

150

425

575

3,779

2015 2016 2017 2018 2019 2020 2021

Tap to SSN 2020 + FRN 2020 New Senior Credit Facility New Senior Secured Notes 2020 Senior Secured FRN

Senior Secured Notes 2020 New FRN 2020 New Senior Notes 2021

Highly Efficient Debt Maturity Profile

Thank You

Q&A

19

This document contains “forward-looking statements”, as the phrase is defined in Section 27A of the Securities Act of 1933, as

amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements relate to, among other things,

future market developments and trends, anticipated benefits from the Italy transaction, the ability to complete the Italy transaction and

anticipated interest cost savings. The forward-looking statements included in this presentation are based on management’s best

assessment of the Company’s strategic and financial position and of future market conditions and trends. These discussions involve

risks and uncertainties. The actual outcome may differ materially from these statements as a result of economic volatility, unforeseen

developments from competition, governmental regulation of the telecommunications industries.

20

Disclaimer

![Annual lists of contractors [2004-2013]...FM SERVIZI SCARL Operational Services for EFSA 1,216,368.25 € WIND TELECOMUNICAZIONI SPA Fixed Telephony and Data Services 204,848.61 €](https://static.fdocuments.in/doc/165x107/5fb1455ae3951a00ee4c9078/annual-lists-of-contractors-2004-2013-fm-servizi-scarl-operational-services.jpg)