Wilshire Metro Times - January 2011

9

Discover Publications , 6797 N. High St., #213, Worthington, OH 43085 6 Inside • JANUARY/FEBRUAR Y 2011 PRESORTED STANDARD U.S. POSTAGE PAID DISCOVER PUBLICATIONS UPS STORE RUSSELL CHAN DRE# 01326223 EVAN FUJII DRE# 01370718 Coming Soon Promenade West Third Quarter Metro Area Home Prices Hold During Post-Credit Sales Decline ully half of metropolitan areas tracked in the third quarter continued to show modest home price increases from a year ago, despite a sharp decline in home sales after the deadline for the home buyer tax credit, according to the latest surv ey by the National Association of Realtors ® . In the third quar ter, 77 out of 155 metropolitan statis- tical areas1 (MSAs) had higher median existing single- family home prices in comparison with the third quarter of 2009, including 11 with double-digit increases; two were unchanged and 76 metros showed price declines. In the third quarter of 2009 only 30 MSAs experienced annual price gains. The national median existing single-family price was little changed at $177,900 in the third quarter, down 0.2 percent from $178,200 in the third quarter of 2009. The median is where half sold for more and half sold for less. Distre ssed home s, typica lly sold at discoun t, accou nted for 34 percent of third qu arter sales, up from 30 percent a year ago. Lawre nce Y un, NAR chief eco nomis t, said relati vely flat home prices have been the hallmark of the 2010 housing market. “Ev en with swings in ho me sales, prices this year have been changing very little from year-ago readings. Areas with some larger swings in home price reflect the degree of distressed sales in those markets,” he said. “Home sales through the first three quarters of this year are virtually the same as year-to-date sales at this time last year, and therefore b roadly support home val- ues. Howe ver, there are large local market dif ferences with prices rising in job-creating regions like the Washington, D.C. area, the Dakotas and T exas; and also in markets recovering from over-correction such as California coastal cities,” Y un said. As expected , total state existing -home sales, includ ing single-family and condo , fell 25.3 percent to a seasonal- ly adjusted annual rate2 of 4.16 million in the third quar- ter from a surge of 5.57 million in the second quarter driven by the home buyer tax credit; they were 21.2 per- cent below the 5.28 million-unit pace in the third quarter of 2009. Y ear-to-date, there were 3.79 million existing- home sales, essentially unchanged from 3.77 million at this point in 2009. NAR Pr esident Ron Phipps, broker-president of Phipps Realty in Warwick, R.I., said the outstanding fac- tor in the current market is housing affordability. “The great news for home buyers in today’s market is histori- cally low mortgage interest rates and affordable home prices in much of the coun try, along with a great selec- tion of properties, ” he said. According to F reddie Mac, the national averag e com- mitment rate on a 30-year conventional fixed-rate mort- gage was a record low 4.45 percent in the third quarter, down from 4.91 percent in the second quarter; it was 5.16 percent in the third quarter of 2009. “Given the relationship between mortgage interest rates, home pr ices and medi an family in come, the buy els we’ve seen dating all the way back to 1970. Although credit is still tight, a REALTOR® can guide you to ward responsible, sustainable home ownership in today ’s mar- ket by helping you find both the right home and a mort- gage that meets your need s,” Phipps said. Y un added that there are additional indicators for home price stabilization. “A recent surge in commodity prices, along with the fact that the cost of constructing a new home exceeds the value of existing homes in many mar- kets, bode well for continu ing home price stabilization, ” he said. In the condo secto r, metro area con domin ium and cooperative prices—covering changes in 56 metro areas—showed the national median existi ng-condo price was $171,400 in the third quarter , down 3.9 percent from the third quarter of 2009. Twenty-nine metros showed increases in the median condo price from a year ago and 27 areas had declines; only four metros saw annual price gains in third quarter of 2009. Regionally, the med ian existing single-family h ome price in the Northeast rose 2.5 percent to $253,400 in the third quarter from a year earlier. Existing-home sales in the Northeast fell 27.3 percent in the third quarter to a pace of 693,000 and are 24.4 percent below the third quarter of 2009. Year-to-date sales in the Northeast totaled 638,000, essentially unchanged from 637,000 at this time last year. In the Midwes t, the median ex isting sin gle-f amily home price declined 3.0 percent t o $145,600 in the third quarter from the third quarter of 2009. Existing-home sales in the Midwest dropped 33.7 percent in the third quarter to a level of 860,000 and are 28.9 percent below a year ago. Year-to-date there were 849,000 sales in the Midwest, compared with 860,000 in 2009. In the South, the median existing single-family home price slipped 1.9 percent to $157,000 in the third quarter from the same period in 2009. Existing-home sales in the region fell 21.8 percent in the third quarter to an annual rate of 1.64 million and are 16.4 percent below the third quarter of last year. There were 1.43 million sales year- to-date in the South, in contrast with 1.39 million last year. The median existing single-family home price in the West dipped 0.4 percent to $224,800 in the third quarter from a year ago. Existing-home sales in the West fell 20.7 percent in the third quarter to a pace of 973,000 and are 18.2 percent bel ow the third quarter of 2009. Y ear-to- date sales in the W est totaled 876,000, vs. 889,000 in 2009. The National Association of Realtors ® , “The V oice for Real Estate, ” is Americ a’s larg est trade associatio n, rep- resenting 1.1 million members involved in all aspects of F SI MPLY HELP B UNK E R HILL FI RS T & HO PE PRIME GRIND PHYSICAL THERAPY Listings • Market Stats • Sold Properties • Buyer/Seller Tips & More! AXIS

-

Upload

wilshiremetro -

Category

Documents

-

view

217 -

download

0

Transcript of Wilshire Metro Times - January 2011

8/7/2019 Wilshire Metro Times - January 2011

http://slidepdf.com/reader/full/wilshire-metro-times-january-2011 1/8

Discover Publications, 6797 N. High St., #213, Worthington, OH 43085

D P

# 1 1 1 3 6

Inside • JANUARY/FEBRUARY 2011 PRESORTED

STANDARD

U.S.POSTAGE

PAID

DISCOVER

PUBLICATIONS

UPS STORE

RUSSELL CHANDRE# 01326223

EVAN FUJIIDRE# 01370718

Coming SoonPromenade West

Rare, south facing 2+2 • $370,000

Third Quarter Metro Area Home PricesHold During Post-Credit Sales Decline

ully half of metropolitan areas tracked in the thirdquarter continued to show modest home priceincreases from a year ago, despite a sharp decline

in home sales after the deadline for the home buyer taxcredit, according to the latest survey by the NationalAssociation of Realtors®.

In the third quarter, 77 out of 155 metropolitan statis-tical areas1 (MSAs) had higher median existing single-family home prices in comparison with the third quarterof 2009, including 11 with double-digit increases; twowere unchanged and 76 metros showed price declines. Inthe third quarter of 2009 only 30 MSAs experiencedannual price gains.

The national median existing single-family price waslittle changed at $177,900 in the third quarter, down 0.2percent from $178,200 in the third quarter of 2009. Themedian is where half sold for more and half sold for less.Distressed homes, typically sold at discount, accountedfor 34 percent of third quarter sales, up from 30 percenta year ago.

Lawrence Yun, NAR chief economist, said relativelyflat home prices have been the hallmark of the 2010housing market. “Even with swings in home sales, pricesthis year have been changing very little from year-agoreadings. Areas with some larger swings in home pricereflect the degree of distressed sales in those markets,”he said.

“Home sales through the first three quarters of thisyear are virtually the same as year-to-date sales at this

time last year, and therefore broadly support home val-ues. However, there are large local market differenceswith prices rising in job-creating regions like theWashington, D.C. area, the Dakotas and Texas; and alsoin markets recovering from over-correction such asCalifornia coastal cities,” Yun said.

As expected, total state existing-home sales, includingsingle-family and condo, fell 25.3 percent to a seasonal-ly adjusted annual rate2 of 4.16 million in the third quar-ter from a surge of 5.57 million in the second quarterdriven by the home buyer tax credit; they were 21.2 per-cent below the 5.28 million-unit pace in the third quarterof 2009. Year-to-date, there were 3.79 million existing-home sales, essentially unchanged from 3.77 million atthis point in 2009.

NAR President Ron Phipps, broker-president of Phipps Realty in Warwick, R.I., said the outstanding fac-tor in the current market is housing affordability. “Thegreat news for home buyers in today’s market is histori-cally low mortgage interest rates and affordable homeprices in much of the country, along with a great selec-tion of properties,” he said.

According to Freddie Mac, the national average com-mitment rate on a 30-year conventional fixed-rate mort-gage was a record low 4.45 percent in the third quarter,down from 4.91 percent in the second quarter; it was5.16 percent in the third quarter of 2009.

“Given the relationship between mortgage interestrates, home prices and median family income, the buy-ing power in today’s market is matching the highest lev-

els we’ve seen dating all the way back to 1970. Although

credit is still tight, a REALTOR® can guide you toward

responsible, sustainable home ownership in today’s mar-

ket by helping you find both the right home and a mort-

gage that meets your needs,” Phipps said.

Yun added that there are additional indicators for home

price stabilization. “A recent surge in commodity prices,

along with the fact that the cost of constructing a new

home exceeds the value of existing homes in many mar-

kets, bode well for continuing home price stabilization,”

he said.

In the condo sector, metro area condominium and

cooperative prices—covering changes in 56 metro

areas—showed the national median existing-condo price

was $171,400 in the third quarter, down 3.9 percent from

the third quarter of 2009. Twenty-nine metros showed

increases in the median condo price from a year ago and

27 areas had declines; only four metros saw annual price

gains in third quarter of 2009.

Regionally, the median existing single-family home

price in the Northeast rose 2.5 percent to $253,400 in the

third quarter from a year earlier. Existing-home sales in

the Northeast fell 27.3 percent in the third quarter to a

pace of 693,000 and are 24.4 percent below the third

quarter of 2009. Year-to-date sales in the Northeast

totaled 638,000, essentially unchanged from 637,000 at

this time last year.In the Midwest, the median existing single-family

home price declined 3.0 percent to $145,600 in the third

quarter from the third quarter of 2009. Existing-home

sales in the Midwest dropped 33.7 percent in the third

quarter to a level of 860,000 and are 28.9 percent below

a year ago. Year-to-date there were 849,000 sales in the

Midwest, compared with 860,000 in 2009.

In the South, the median existing single-family home

price slipped 1.9 percent to $157,000 in the third quarter

from the same period in 2009. Existing-home sales in the

region fell 21.8 percent in the third quarter to an annual

rate of 1.64 million and are 16.4 percent below the third

quarter of last year. There were 1.43 million sales year-

to-date in the South, in contrast with 1.39 million last

year.The median existing single-family home price in the

West dipped 0.4 percent to $224,800 in the third quarter

from a year ago. Existing-home sales in the West fell

20.7 percent in the third quarter to a pace of 973,000 and

are 18.2 percent below the third quarter of 2009. Year-to-

date sales in the West totaled 876,000, vs. 889,000 in

2009.

The National Association of Realtors®, “The Voice for

Real Estate,” is America’s largest trade association, rep-

resenting 1.1 million members involved in all aspects of

the residential and commercial real estate industries. ■

F

If your property is listed with another broker, this is not intended as a solicitation. The information available on this publication is not intended to be legal advice.

The reader is advised to consult with a qualified attorney on any legal matters. Information herein deemed realiable but not guaranteed.

SIMPLY HELP BUNKER HILL FIRST & HOPE PRIME GRIND PHYSICAL THERAPY

Listings • Market Stats • Sold Properties • Buyer/Seller Tips & More!

AXIS

8/7/2019 Wilshire Metro Times - January 2011

http://slidepdf.com/reader/full/wilshire-metro-times-january-2011 2/8

2

Current State of theHousing Market in Downtown

by Evan Fujii DRE #01370718

nlike anywhere else in LosAngeles, the Downtown areahas been improved and

expanded over the last decade, withmore growth yet to come. Thenumber of residential unitsDowntown grew from less than 900to over 3000 between 2000 and2010. The opening of the RalphsFresh Fare on 9th and Flowerbrought pedestrian traffic to SouthPark overnight. LA Live is com-plete, and the newly constructed,affordable lofts at Barker Block andEvo are nearly sold out. There arenew units still available for pur-chase at the Ritz-Carlton, 655 Hopeand Concerto. Feel free to contactWilshire Metro for more details.

There are currently about 180

resale condos and lofts inDowntown on the market. Of thoseunits, there are about 90 shortsales, 70 regular sales, and 20bank-owned units. The data graphsshown are from the MLS.Developers cannot list all new loftson the MLS, only a small portionare listed. The graph shows thatprices have stayed steady for thelast 2 years. Graphs are forDowntown Los Angeles with zipcodes 90012, 90013, 90015,90017, and 90021.

Downtown is still expanding.The Target Store at 7th and Fig will

open in 2012. The Grand Ave Park next to City Hall is presently underconstruction. The Eli Broad ArtMuseum just south of the DisneyConcert Hall is in the planningstages. The Grand Ave Project,which was planned to include anentertainment and residential com-plex, hotel, and mall, is awaitingconstruction. The Subway to theSea, which will run fromDowntown to Santa Monica, isunder construction, and a new ligh-trail station on Bunker Hill is alsoin the planning stages. Even inthese tough economic times,

Downtown continues to draw innew residents and businesses, cre-ating a more vibrant environmentto Live, Work, and Play. ■

U

© 2009-2010 Terradatum and its suppliers and licensors

Avoiding Foreclosure:

Short Sales vs.Loan Modifications

THE TOP CHOICE FOR DOWNTOWNREAL ESTATE WILSHIRE METRO REALTY, INC.

DRE 01090146IF YOU ARE LOOKING FOR SALES OR

LEASING SERVICES, CONTACT US TODAY!

by Jack Simon

Are you falling victim to the predatory lending of years past? Do you find yourself in foreclosure, ordrawing near foreclosure? For many people, there isa solution to these nightmares. Whether you seek ahome mortgage modification, a refinance or a shortsale, identifying where you are is the first steptowards a recovery.

In the event of a mortgage refinance, the keys torecovery begin with identifying any remaining equi-ty within your home, calculating your bottom linehousehold income, and knowing where you stand with your credit score. Successful refinancing begins

with your ability to show you can pay the mortgage,and whether you are a worthwhile credit risk.Financial institutions interested in these qualifica-tions, who more often have your best interest atheart, reside on the local level. You will find localbanks and credit unions willing to invest in individ-uals with a stable financial position.

For individuals who find themselves looking formortgage modification, all of the above still apply,but it is important to understand that there is a key criteria that many individuals are not aware of, which may or may not qualify a person for a loanmodification program. Usually, very few individualsqualify for a mortgage modification, because realisti-cally, it pays significantly better for a financial insti-tution to foreclose or short sell your home. Whilethis may seem rather shocking that your better inter-est is not at stake, you will find that their corporatefinancial interest is greater than your financial inter-

est.Individuals looking for short sale opportunities

have an advantage over other options mentionedabove. It is true that financial institutions earn largeamounts of income on foreclosures and short sales,but short sale transactions allow the homeowner tomove ahead, or at least level the playing field in anestablished, yet unfair industry. Walking away froman underwater mortgage via a short sale can be ablessing in disguise, if done properly. To be executedcorrectly, an individual must request that the mort-gage holder waive all debt beyond the resale amount.This is critical to prevent unwanted liens or judg-ments from coming back to the seller, to secure thatloss in future years when a lender may deem a seller’ssituation improved. Failure to enact this requestgrants lenders five years to seek a judgment, and 20years to collect upon that judgment. Debt should be

displayed as settled in full, and no longer collectable.Before you get any further under water, contact a

real estate agent or attorney to help you with yourproceedings. ■

If your property is listed with another broker, this is not intended as a solicitation. The information available on this publication is not intended to be legal advice.

The reader is advised to consult with a qualified attorney on any legal matters. Information herein deemed realiable but not guaranteed.

8/7/2019 Wilshire Metro Times - January 2011

http://slidepdf.com/reader/full/wilshire-metro-times-january-2011 3/8

3

If your property is listed with another broker, this is not intended as a solicitation. The information available on this publication is not intended to be legal advice.

The reader is advised to consult with a qualified attorney on any legal matters. Information herein deemed realiable but not guaranteed.

8/7/2019 Wilshire Metro Times - January 2011

http://slidepdf.com/reader/full/wilshire-metro-times-january-2011 4/8

4

6797 N. High Street, Suite 213

Worthington, Ohio 43085(614) 785-1111 • www.DiscoverPublications.com

KidNews, distributed by Knight Ridder/Tribune.Sudoku, Scrabble, Pet World, Rita St. Clair,

Wolfgang Puck’s Kitchen distributed by Tribune Media Service.

© Copyright 2010 by Discover Publications, Inc.

All rights reserved.

PublisherEvan Fujii, Russell Chan,

Joseph Kang

800 W 1st Street, Suite 400

Los Angeles, CA 90012

213.629.2530 Office

213.617.0384 Fax

www.wilshiremetro.com

r e a l e s t a t e h e a d l i n e s

Realtors® Cautiously Optimistic About Future of Housing Market

Real estate experts were cautiously opti-mistic about the current and future state of the industry at the recent State of the RealEstate Industry forum during the 2010Realtors® Conference & Expo.

Panelist Margaret Kelly, chief executiveofficer of RE/MAX, said today’s marketshouldn’t be called the new normal becausethe old market was abnormal. “The spike upand down in the housing market wasn’t nor-mal so we shouldn’t be measuring ourselvesagainst it,” she said.

Kelly said that despite some challengesthere are plenty of opportunities in the hous-ing market, adding that low mortgage inter-est rates, abundant inventory and stableprices are attracting buyers to the marketright now.

Steady Improvement Predicted forCommercial Property Market

While still experiencing challenges, thecommercial real estate market could see signsof steady improvement in the near future, specifically concerninglending. This is according to two economists at the Economic Issuesand Commercial Real Estate Business Trends Forum at the 2010Realtors® Conference & Expo in New Orleans.

National Association of Realtors® Chief Economist Lawrence Yunand Hugh Kelly, clinical professor of real estate at New York University Schack Institute of Real Estate, shared their predictionssurrounding the commercial market, indicating a slight improve-ment in commercial lending.

“Banks’ profits have returned to healthy levels. As a result, it isinevitable they will return to the business they were created for,

which is lending,” said Yun. “Commercial real estate has experienceda sharp price correction, but there is still a shortage of buyers becauseof lack of adequate capital resources.”NAR Survey Shows Value of Home Ownership

Home buyers today have affirmed a long-term view of homeownership, the typical seller is experiencing positive returns and the

vast majority of home owners see their property as a good invest-ment, according to the latest consumer survey of home buyers andsellers. The study was released here today at the 2010 Realtors®

Conference & Expo.The 2010 National Association of Realtors® Profile of Home

Buyers and Sellers is the latest in a series of large national NAR sur-veys evaluating demographics, preferences, marketing and experi-ences of recent home buyers and sellers.

Although typical sellers had been in their previous home foreight years, up from seven years in the 2009 study, first-time buy-ers plan to stay for 10 years and repeat buyers plan to hold theirproperty for 15 years.

NAR 2010 President Vicki Cox Golder, owner of Vicki L. Cox & Associates in Tucson, Ariz., said the pattern of home buyers takinga long-term view has solidified over the past few years. “This under-scores two simple facts—home ownership encourages stability, andthe longer you own, the better your investment.” ■

Buying a Home Still a Good Investment for 2011

If your property is listed with another broker, this is not intended as a solicitation. The information available on this publication is not intended to be legal advice.

The reader is advised to consult with a qualified attorney on any legal matters. Information herein deemed realiable but not guaranteed.

Downtown L.A.’s Neighborhood Market.Wide selection of Beer & Liquor

Import & Domestic WinesCome in for our lunchtime specials

(213) 624 - 1245 - Open Late800 W 1st Street

(Near 1st & Hope, Park in the rear of 800 W 1st Street Building)

BUNKER HILL MARKET DELI

8/7/2019 Wilshire Metro Times - January 2011

http://slidepdf.com/reader/full/wilshire-metro-times-january-2011 5/8

5

PHYSICAL THERAPY IN DOWNTOWN

• Personalized One on One Care with Physical Therapist • Scheduled One Hour Treatment Sessions • Pre & Post-Surgical Rehabilitation• Spine (Neck & Back) Rehabilitation & Stabilization• General Musculoskeletal & Sports Rehabilitation• Migraine & Headache Relief

• Postural Dysfunction & Overuse Injury Rehab.• Orthotic Assessment & Evaluation• Biomechanical Sport Specific Analysis (ie: Golf)• Ergonomic Assessment • 30’ Physical Therapy Screens • Personal Training also available

Located in Downtown Los Angeles, across the street from the Walt Disney Concert Hall

708 West 1st Street • Downtown Los Angeles, CA • Phone (213) 617-2947 • Fax: (213) 617-2903

NOTARY

LIVE SCAN-

FINGERPRINTING

SHIPPING

PACKING

BANNERS

MAIL BOX RENTALS

TM

The UPS Store®

645 West 9th Street, Ste. 110(on FLOWER before 9th Street)

213.620.0081www.theupsstore.com/4977.htm

AXISPTOrthopedic, Manual

& Sports Physical Therapy www.axispt.net

s e l l e r ’ s c o r n e r

by Martin Cantu

In an odd twist to the old adage, “Buyer beware,”this real estate market adds additional problems toalready burdened real estate sellers.

The scenario: A homeowner is behind on theirmortgage payments. The house has just enough value

to payoff the mortgage and the closing costs, if they get the price they are after. The house sits on the mar-ket for months, stressing the homeowners even more.

It is in this environment that the vultures come out.Desperate sellers turn to the bottom feeders, who trotout schemes that appear to “sell” the property, but inreality, do nothing more than shift title to theunscrupulous buyer, who pockets cash from rentals without paying the underlying mortgage.

Experts will tell you that there are no new congames, just new twists. The scenario described aboveplayed out frequently in the 1980s at a time whenbanks and savings and loans institutions were failingon a daily basis. At this time, local institutions heldmost mortgages and collection actions were swifterand more concentrated. Foreclosure usually took place within 90 days of the first default, and rollinglate payments were not allowed. More importantly,any deficiency on the foreclosure—that is, theamount by which the debt and foreclosure expenses

exceeded the amount of debt—were subject to collec-tion by the mortgage holder. Lenders routinely pur-sued foreclosed borrowers for the deficiency judg-ment.

This led to so called “wrap notes” where buyers would assume the mortgage note, usually with littleor no cash to sellers. The sellers move out, thinkingtheir problems are behind them. The buyers collectrent payments for a couple of months plus a deposit,do not pay the underlying mortgage and put off fore-closure for as long as they can. Multiply this by 10 ormore properties and they make a tidy sum beforemoving to another city and starting again.

This time the scam has new twists. National com-panies and servicers, who can take as long as a year toforeclose, now hold mortgages. These same lendersand servicers, also desperate to reduce foreclosureinventory and comply with government mandates,are open to idea of a short sale, a process by which theseller receives no compensation for the sale and the

lender accepts a payoff amount less than what it isentitled to receive.

As is the case, the process has been abused. Lendersoften engage real estate companies to administer theshort sales. Recently, lenders discovered that agents of these companies, armed with inside information, aredirecting desperate homeowner/sellers to their associ-ates. The sale amount is usually way below any shortsale value. The company attests to the value of thenegotiated contract, inducing the parties into the con-tract. Once the sale closes, the associate flips the prop-erty at the true value, sharing the profits with thereferring agent. Here are some tips sellers can follow to get through this situation:

1. Investigate your Realtor®. How active are they inthe market? Does he or she have listings, as well asrepresent buyers? Drive by other listings, maybeyou can catch one of the property owners of theirother listings and visit with them about their per-formance.Realize that this market is difficult. You do not needan agent who says yes all the time. You need anagent who will discuss your price point in an hon-est and frank discussion. If you need to pursue ashort sale, do not shy away from it.

2. Monitor property values in your area so you canspot someone trying to take advantage of you.

3. If the deal sounds too good to be true, it probably is.

4. You are not released from liability on your mort-gage until the mortgage is paid full, or the lenderaccepts a short sale, and you have a release in hand.Most mortgages cannot be assumed under theseterms—assumption does not equal release. ■

SELLER BEWARE:

Tips to Escaping Foreclosure Scamsby Tom Kraeutler

Fully half of metropolitan areas tracked in the third quarter continued to show modest home price increases from a year ago, despite a sharp decline in homesales after the deadline for the home buyer tax credit, according to the latest sur-vey by the National Association of Realtors®.

In the third quarter, 77 out of 155 metropolitan statistical areas (MSAs) had

higher median existing single-family home prices in comparison with the thirdquarter of 2009, including 11 with double-digit increases; two were unchangedand 76 metros showed price declines. In the third quarter of 2009 only 30 MSAsexperienced annual price gains.

The national median existing single-family price was little changed at$177,900 in the third quarter, down 0.2 percent from $178,200 in the thirdquarter of 2009. The median is where half sold for more and half sold for less.Distressed homes, typically sold at discount, accounted for 34 percent of thirdquarter sales, up from 30 percent a year ago.

Lawrence Yun, NAR chief economist, said relatively flat home prices havebeen the hallmark of the 2010 housing market. “Even with swings in home sales,prices this year have been changing very little from year-ago readings. Areas withsome larger swings in home price reflect the degree of distressed sales in thosemarkets,” he said.

“Home sales through the first three quarters of this year are virtually the same asyear-to-date sales at this time last year, and therefore broadly support home values.However, there are large local market differences with prices rising in job-creatingregions like the Washington, D.C. area, the Dakotas and Texas; and also in mar-kets recovering from over-correction such as California coastal cities,” Yun said.

As expected, total state existing-home sales, including single-family andcondo, fell 25.3 percent to a seasonally adjusted annual rate2 of 4.16 million inthe third quarter from a surge of 5.57 million in the second quarter driven by the home buyer tax credit; they were 21.2 percent below the 5.28 million-unitpace in the third quarter of 2009. Year-to-date, there were 3.79 million existing-home sales, essentially unchanged from 3.77 million at this point in 2009.

NAR President Ron Phipps, broker-president of Phipps Realty in Warwick,R.I., said the outstanding factor in the current market is housing affordability.“The great news for home buyers in today’s market is historically low mortgageinterest rates and affordable home prices in much of the country, along with agreat selection of properties,” he said.

According to Freddie Mac, the national average commitment rate on a 30-yearconventional fixed-rate mortgage was a record low 4.45 percent in the thirdquarter, down from 4.91 percent in the second quarter; it was 5.16 percent inthe third quarter of 2009.

“Given the relationship between mortgage interest rates, home prices andmedian family income, the buying power in today’s market is matching the high-est levels we’ve seen dating all the way back to 1970. Although credit is still tight,a Realtor® can guide you toward responsible, sustainable home ownership intoday’s market by helping you find both the right home and a mortgage thatmeets your needs,” Phipps said. ■

Third Quarter Prices HoldDuring Sales Decline

If your property is listed with another broker, this is not intended as a solicitation. The information available on this publication is not intended to be legal advice.

The reader is advised to consult with a qualified attorney on any legal matters. Information herein deemed realiable but not guaranteed.

8/7/2019 Wilshire Metro Times - January 2011

http://slidepdf.com/reader/full/wilshire-metro-times-january-2011 6/8

6

Introduction toShort Salesby Evan Fujii DRE #01370718

ith the assistance of an excellent third party negotiator,

Wilshire Metro Realty has a high success rate with short

sales. Helping numerous homeowners avoid foreclosure and

in one short sale transaction obtaining approval for short sale in less

than two weeks. The California association of Realtors estimated that

only 20% of short sales were successful. In comparison, Wilshire

Metro Realty has a 95% short sale success rate.

What is a short sale?

Short sales are becoming more common throughout the country due

to lower home prices. Homeowners who wish to sell their properties

but owe more on them than they are worth on the market may choose

to negotiate with their lenders in what is called a “short sale,” selling

their property for less than market value in order to avoid forclosure

and damaging their credit. Lenders may benefit by avoiding a long

foreclosure and re-sale process. However, short sales are not always

easy or successful.

What if I am a seller interested in selling a short sale property?

Please note that not all lenders will offer a short sale option, and not

all sellers will qualify for one. If you’re a seller thinking about a short

sale, our third party negotiator can contact your lender, find out if ashort sale is right for you, and help negotiate the selling price and defi-

ciency judgement. Wilshire Metro Realty can list your property and

help find you a buyer. Contact us today for more information.

What if I am a buyer interested in purchasing a short sale property?

Buyers need to be careful too, since getting a deal on a short sale is

not as easy as it may sound. Short sales may require doing some addi-

tional homework and assembling the right paperwork. Wilshire Metro

Realty can help you successfully complete the purchase of a short sale

property.

Wilshire Metro Realty represents buyers and sellers for short sales,

new home sales, re-sales, and bank-owned properties. Contact us

today for all of your new home and investment property needs. ■

W

Wilshire Metro Realty, Inc. is a top-producing realestate team proudly serving Los Angeles County and

specializing in Downtown Los Angeles.Wilshire Metro was founded in 1987 to serve the needs of theDowntown residential community. In that year there were rough-

ly 850 condo units within the Downtown business district.

Today, it is estimated that more than 40,000 residents reside inthe Downtown Los Angeles area. Our years of experience andknowledge of the existing and up-incoming developments in

Downtown and Southern California will help you find the place you have wanted in or outside the city.

Call us today for your Real Estate Needs!

ABOUT WILSHIRE METRO REALTY

by Ilyce Glink

Q: I am a 68-year-old retiree and my income isonly $860 per month. I am planning to buy a

condo for $68,000 and to use $35,000 from my IRA as a down payment. Is this a wise move? Therental rates right now are about $695 per month.

A: Good question. The first thing you have toconsider is the significant amount of federalincome taxes you may have to pay if you with-draw $35,000 from your IRA. If you’re in a low federal tax bracket and don’t pay much in federalincome taxes, the withdrawal may bump you up,as the $35,000 will be considered additionalincome. You may end up paying $5,000 or morein taxes as a result of the withdrawal.

If you plan to obtain a loan for the balance of the cost of the condominium, you may find thatyou won’t benefit much from the low loan bal-ance left. You may wind up having to pay several

thousand dollars to get that loan.If you have to pay $3,000 for the loan and end

up paying $5,000 in additional federal incometaxes due to the withdrawal from the IRA, willthose payments have a negative impact on you?Do you have the cash available to manage thosepayments? Would the purchase still make sensefor you?

In order to compare the cost of renting with thecost of owning this condominium, you will needto know what the monthly condominium assess-ments and the annual property taxes will be. Let’ssay you find out that the assessments will be $250per month and the real estate taxes on a monthly basis will end up being about $150. Your month-ly mortgage payment may be about $125.

Altogether, those payments will cost you about$525 per month, saving you about $170 permonth over the cost of renting.

While there are some savings, you also have

some additional costs associated with the pur-chase, including the move and any other costsrelating to owning a condominium. When thedishwasher breaks, for example, repairing it willcome out of your pocket.

You also need to determine whether you willneed the IRA money in the future for yourexpenses. If that money is now earning dividendsor interest, or if it’s invested in stock that’s notlikely to lose value, your IRA money may contin-ue to grow.

If you decide to buy the condominium, youhad better review the finances of the condomini-um association before you sign on the dotted line.If the association’s finances are weak and it endsup having to spend money on building improve-ments, those costs may come back to haunt you

in the form of a special assessment.If those costs are significant, the low purchase

price of the condominium may not outweigh theadditional expenses you end up paying to keep upthe building. Remember, if you rent in a building,you usually aren’t responsible for repairs or capitalimprovements. The landlord can raise your rent,but you can always move to another building.

You’ll have to review all of these costs and deter-mine if the move is right for you. You may decidethe new place is what you want and need, and thatyou can go ahead and do it. Please tell us what youdecide to do and how it turns out. ■

© 2010 Ilyce R. Glink. Distributed By Tribune Media Services, Inc.

Early IRA Withdrawal CostsMay Outweigh Benefits of Using Funds to Buy Condo

SOLD PROPERTIES

15115 Del Prado - $520,000

880 W 1st Street - $345,000

100 S Alameda - $295,000

880 W 1st Street - $275,000

1111 S Grand - $390,000

800 W 1st Street - $210,000121 S Hope Street - $365,000

600 W 9th Street - $455,000

800 W 1st Street - $180,000

800 W 1st Street - $247,000

880 W 1st Street - $375,000

1410 Estepona - $260,000

1111 S Grand - $368,000

100 S Alameda - $325,000

1234 S Wilshire - $290,000

1111 S Grand - $450,000

222 S Central - $290,000

800 W 1st Street - $265,000

1100 S Hope - $450,000

RUSSELL CHANDRE# 01326223

EVAN FUJIIDRE# 01370718

If your property is listed with another broker, this is not intended as a solicitation. The information available on this publication is not intended to be legal advice.

The reader is advised to consult with a qualified attorney on any legal matters. Information herein deemed realiable but not guaranteed.

8/7/2019 Wilshire Metro Times - January 2011

http://slidepdf.com/reader/full/wilshire-metro-times-january-2011 7/8

7

645 W 9th Street, 2nd Floor

$2,500

nter a posh hotel and one of the firstthings you notice is the way itsparkles. From the crystal chandeliers

to the brass stair railings, a truly great hotelgleams. You can bring the same sparkle toyour home. Here are some cleaning tips tomake your home glitter—and you shimmer with pride.

1. Make your windows shine. Clean,sparkling windows make the whole houselook clean. To wash windows super-fast, addtwo tablespoons of sudsy ammonia to a gal-lon of warm water. Use a sponge to spreadthe solution onto windows and a squeegee to wipe it off. Remove any streaks with amicrofiber towel. For extra sparkle, follow with a wipe of a microfiber polishing cloth.

2. Clean the oven. The fall’s warm applepies are less appealing when you pull themout of a grimy oven. Set your oven to the

“clean” setting when you’re at home. Onceit’s cooled, wipe down with paper towels andclear water. Clean grates with a commercialoven-cleaning product and scour with asoap-filled scouring pad to make them shine.

3. Give your wood furniture a shine withfurniture oil. Lemon or orange oil products will protect wood and give it a nice sheen. Usesparingly and be sure to polish thoroughly, wiping off any excess so that the wood has anice patina but doesn’t look oily.

4. Make your china cabinet sparklelike a jewelry box. Although it’s closedup, china cabinets still attract dust. And with the holidays coming up, a china cab-inet that’s cleaned, dust-free, and full of

gleaming china and crystal will be ready for use when holiday parties and dinnersroll around. Start by putting a waterproof pad on your table and emptying out yourchina cabinet. Wash and polish china andcrystal. Clean cabinet shelves and polishany glass or mirror in your cabinet, andthen replace with the clean service pieces.

5. Make your chandelier shimmer.If your chandelier is very high or very intricate, your best bet might be to find a

lighting company that offers cleaning service.If you want to clean your chandelier yourself,first move the dining table out from under-neath the light. Then, turn off the electricity atthe panel. Make a solution of distilled waterand ammonia; distilled water won’t leaveresidue on delicate crystals. Wipe the crystals with a wet cloth and follow with a polish froma dry cloth. Let dry for two or three daysbefore turning the electricity back on.

6. Polish metal fittings. If you have brassor other hardware on furniture, doors, rail-ings or switch plates, give them a polish witha brass polishing liquid to clean the fittings. Wipe them clean, and then using a polishingcloth to buff and make the metal shine.

7. Get a jump on holiday dinners withsparkling silver. Before you start your holi-day menu planning, get your silver servingpieces out and polish them. Then, when it’s

time to set your table, the silver will be ready, waiting and sparkling. Store in zipperedplastic bags with the air removed to keep sil-ver completely tarnish free. ■

For more information, contact Kathryn Weber through her Web site, www.redlotusletter.com.

© 2010 Kathryn Weber.Distributed By Tribune Media Services, Inc.

Seven Ways to MakeYour Home Sparkle by Kathryn

Weber

E

A Laundry Room to Loveby Kathryn Weber

Do you dread facingpiles of laundry, or are youone of those people who finddeep satisfaction in all thatfolding, sorting and stainremoval? Regardless of where

you fall on the laundry love-hate continuum, the factremains that the job has to getdone. And the task is going tobe a lot more pleasant if youmake the space where you doit more efficient and attractive.

Crying for Style

Most laundry rooms are,frankly, way more institutionalthan they need to be. Tacklingthis lack of style should beagenda item No. 1 in yourredesign. Rather than merely focusing onthe requisite cabinets, counters and col-ors, start with a design that appeals to

you. Pick a decorating theme to help youstay focused: British Colonial, say, or an

ultra-contemporary laboratory look -- any-thing to add a little fun or pleasure to thehumdrum task at hand. By selecting adecor theme, you’ll stay on track whenchoosing colors and accents.

Details Count

Once you’ve decided on a themeand the colors that support your style, it’stime to attend to the little details that makedoing laundry more comfortable, easyand attractive. Art objects are often over-looked in the laundry room. Find decora-tive items, especially prints and acces-sories that can be hung on the walls, thatsupport your design theme.

Laundry detergent is the product usedmore than any other in the laundry room,so it should be convenient and easy to use

-- and stored attractively. If you’re a fan ofpowdered soap, select a large, stylishcanister to store and display your deter-gent. If you’re a fan of liquid soaps, use asmart looking beverage dispenser thatwill look great on the counter. Plus, it willbe much easier to dispense the soap thanpouring from a large, heavy bottle into asmall plastic cup. Another plus: Seeing

your soap in these pretty containers mightmake you want to do laundry.

Make It Easy

Doing laundry is a time-consumingchore. Time spent on your feet on tilefloors can create an aching back andlegs. To make ironing and folding morecomfortable, buy a gel floor mat (thesecan be found in the kitchen area at homecenters or in restaurant supply stores). Tomake air drying easier, install a wall-mounted accordion drying rack that canbe pushed back under a small shelf whennot in use. A telescoping valet rod mount-ed to a cabinet can hold garments youwant to hang or repair, or it can be a con-venient spot to hold dry cleaning. Add apretty basket on a wall next to the dryer tostore dryer sheets so they’re at the readyand not in the box.

If you’re giving your laundry room acomplete overhaul, consider installingextra deep cabinets that have openshelves to hold laundry baskets. The bas-kets will be out of sight, and the deepercountertops will give you more folding

and workspace.Another fun thought? Pick a washer

and dryer in a stylish colo r. We’ve movedway past white, and a garnet-coloredwasher and dryer would look incrediblewith cabinets painted ■

© 2010 Kathryn Weber. Distributed by Tribune Media Services, Inc.

h o m e s p a c e

PROPERTIES FOR LEASE

L E A S E

D

1100 S Hope Street, 2nd Floor

$2,400

L O F T

100 S Alameda Street, 4th Floor

$2,500

2 + 2

490 N. Garfield, Montebello

$1.06/SF/MONTH

RETAIL/COMMERCIAL/OFFICE

100 S Alameda Street, 2nd Floor

$1,650

1 + 1

15904 Annellen, Hacienda Heights

$2,600

DOWNTOWN BUNKER HILL OFFICE800 W 1ST STREET (NEAR 1ST & HOPE)

WILSHIRE METRO REALTY, INC.

Free Parking • Centrally LocatedYour Downtown Neighborhood Real Estate Team

If your property is listed with another broker, this is not intended as a solicitation. The information available on this publication is not intended to be legal advice.

The reader is advised to consult with a qualified attorney on any legal matters. Information herein deemed realiable but not guaranteed.

8/7/2019 Wilshire Metro Times - January 2011

http://slidepdf.com/reader/full/wilshire-metro-times-january-2011 8/8

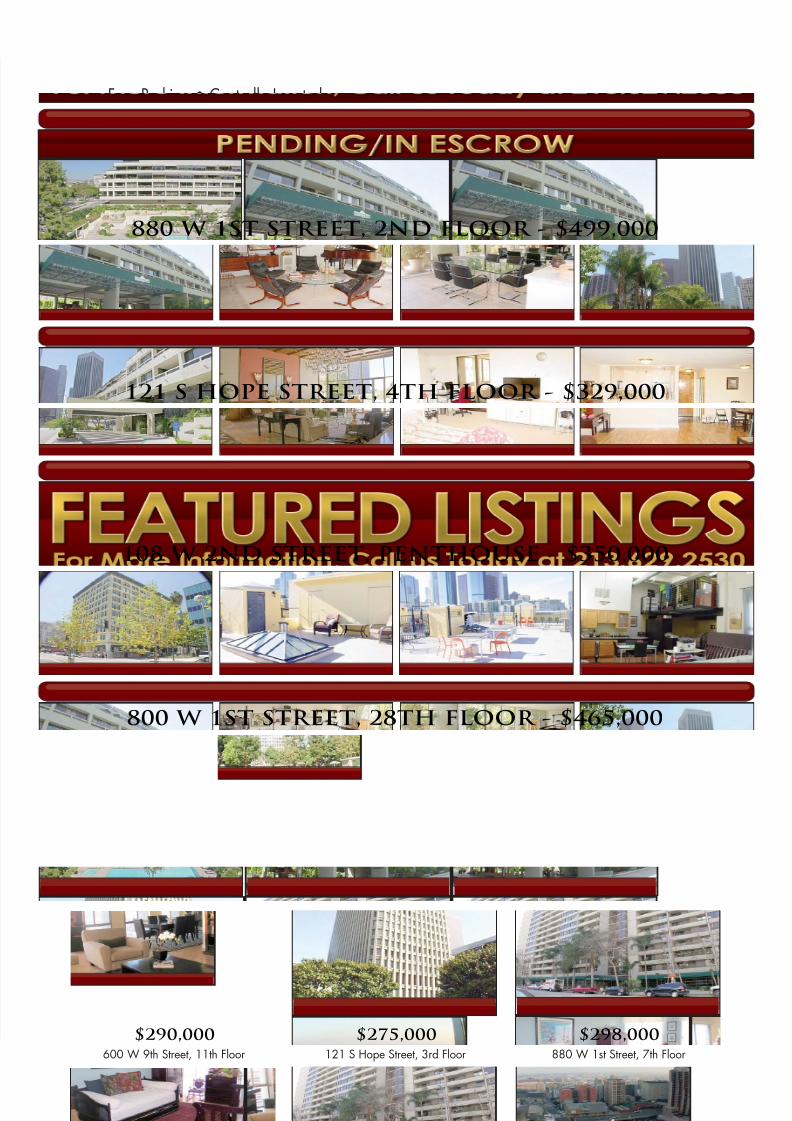

880 W 1ST STREET, 2ND FLOOR - $499,000

600 W 9th Street, 11th Floor$290,000 121 S Hope Street, 3rd Floor$275,000

121 S HOPE STREET, 4TH FLOOR - $329,000

108 W 2ND STREET, PENTHOUSE - $350,000

800 W 1ST STREET, 28TH FLOOR - $465,000

880 W 1st Street, 7th Floor$298,000

600 W 9th Street, 8th Floor

$478,000880 W 1st Street, 2nd Floor

$485,000800 W 1st Street, 7th Floor

$169,000

If your property is listed with another broker, this is not intended as a solicitation. The information available on this publication is not intended to be legal advice.