Wiley CPA Exam Review Quizg-ecx.images-amazon.com/.../WileyCPAExamReviewQuiz.pdf · 2009-10-13 ·...

27

Wiley CPA Exam Review Amazon Exclusive Quiz The CPA exam is considered to be one of the most challenging professional exams. If there is any constant with the exam, it is that the passing rate hovers a bit below 50%. Candidates must cope with the fact that their efforts are likely to be met with failure. But, pass rates for candidates who use effective tools, proven over years, to prepare for the exam tend to be significantly higher. This only makes sense. There is much to master for the exam. Without guidance and most importantly, practice, the exam is impossibly difficult. The Wiley CPA Test Preparation books have been successfully preparing candidates for the exam for over 35 years. The series includes over 3,600 practice questions - including numerous actual exam questions. We’ve taken some time to select several relevant questions from each of the exam parts. Take a moment to see how well prepared you are. Don’t be discouraged by the results. Be encouraged by the excellent guidance provided with the answer, and the instructional material in the books. You will pass - Wiley will show you how.

Transcript of Wiley CPA Exam Review Quizg-ecx.images-amazon.com/.../WileyCPAExamReviewQuiz.pdf · 2009-10-13 ·...

Wiley CPA Exam Review

Amazon Exclusive Quiz The CPA exam is considered to be one of the most challenging professional exams. If there is any constant with the exam, it is that the passing rate hovers a bit below 50%. Candidates must cope with the fact that their efforts are likely to be met with failure. But, pass rates for candidates who use effective tools, proven over years, to prepare for the exam tend to be significantly higher. This only makes sense. There is much to master for the exam. Without guidance and most importantly, practice, the exam is impossibly difficult. The Wiley CPA Test Preparation books have been successfully preparing candidates for the exam for over 35 years. The series includes over 3,600 practice questions - including numerous actual exam questions. We’ve taken some time to select several relevant questions from each of the exam parts. Take a moment to see how well prepared you are. Don’t be discouraged by the results. Be encouraged by the excellent guidance provided with the answer, and the instructional material in the books. You will pass - Wiley will show you how.

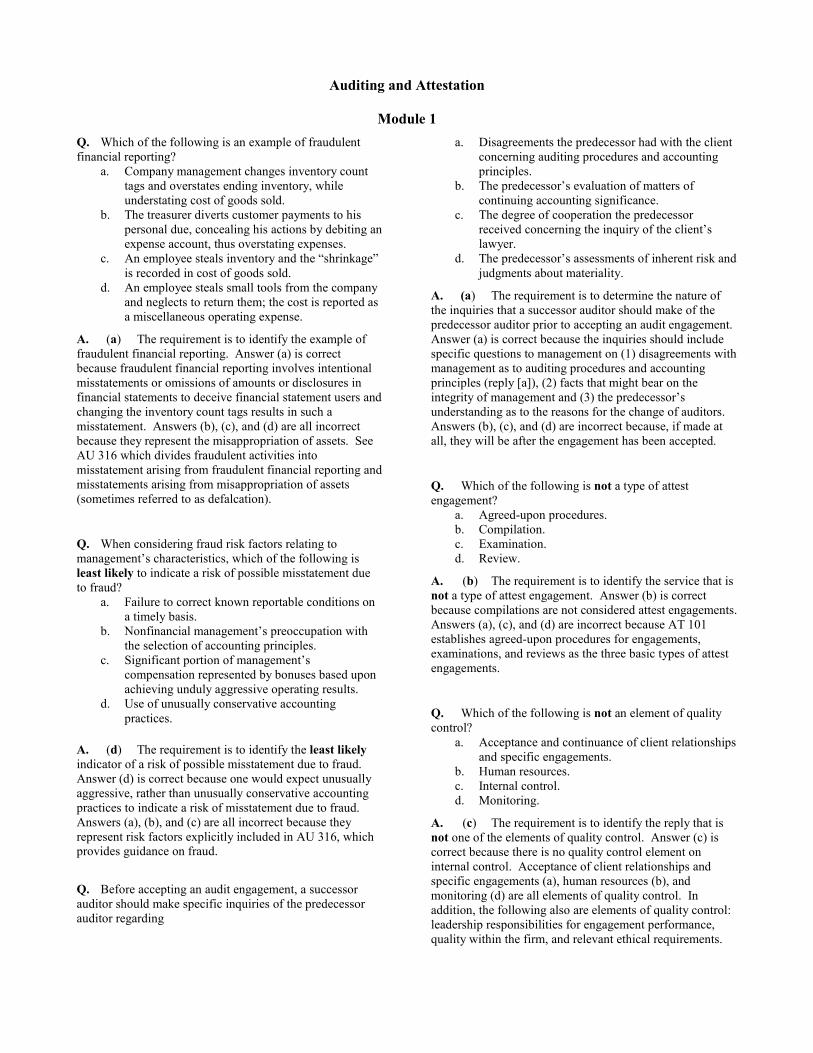

Auditing and Attestation

Module 1

Q. Which of the following is an example of fraudulent financial reporting?

a. Company management changes inventory count tags and overstates ending inventory, while understating cost of goods sold.

b. The treasurer diverts customer payments to his personal due, concealing his actions by debiting an expense account, thus overstating expenses.

c. An employee steals inventory and the “shrinkage” is recorded in cost of goods sold.

d. An employee steals small tools from the company and neglects to return them; the cost is reported as a miscellaneous operating expense.

A. (a) The requirement is to identify the example of fraudulent financial reporting. Answer (a) is correct because fraudulent financial reporting involves intentional misstatements or omissions of amounts or disclosures in financial statements to deceive financial statement users and changing the inventory count tags results in such a misstatement. Answers (b), (c), and (d) are all incorrect because they represent the misappropriation of assets. See AU 316 which divides fraudulent activities into misstatement arising from fraudulent financial reporting and misstatements arising from misappropriation of assets (sometimes referred to as defalcation).

Q. When considering fraud risk factors relating to management’s characteristics, which of the following is least likely to indicate a risk of possible misstatement due to fraud?

a. Failure to correct known reportable conditions on a timely basis.

b. Nonfinancial management’s preoccupation with the selection of accounting principles.

c. Significant portion of management’s compensation represented by bonuses based upon achieving unduly aggressive operating results.

d. Use of unusually conservative accounting practices.

A. (d) The requirement is to identify the least likely indicator of a risk of possible misstatement due to fraud. Answer (d) is correct because one would expect unusually aggressive, rather than unusually conservative accounting practices to indicate a risk of misstatement due to fraud. Answers (a), (b), and (c) are all incorrect because they represent risk factors explicitly included in AU 316, which provides guidance on fraud.

Q. Before accepting an audit engagement, a successor auditor should make specific inquiries of the predecessor auditor regarding

a. Disagreements the predecessor had with the client concerning auditing procedures and accounting principles.

b. The predecessor’s evaluation of matters of continuing accounting significance.

c. The degree of cooperation the predecessor received concerning the inquiry of the client’s lawyer.

d. The predecessor’s assessments of inherent risk and judgments about materiality.

A. (a) The requirement is to determine the nature of the inquiries that a successor auditor should make of the predecessor auditor prior to accepting an audit engagement. Answer (a) is correct because the inquiries should include specific questions to management on (1) disagreements with management as to auditing procedures and accounting principles (reply [a]), (2) facts that might bear on the integrity of management and (3) the predecessor’s understanding as to the reasons for the change of auditors. Answers (b), (c), and (d) are incorrect because, if made at all, they will be after the engagement has been accepted.

Q. Which of the following is not a type of attest engagement?

a. Agreed-upon procedures. b. Compilation. c. Examination. d. Review.

A. (b) The requirement is to identify the service that is not a type of attest engagement. Answer (b) is correct because compilations are not considered attest engagements. Answers (a), (c), and (d) are incorrect because AT 101 establishes agreed-upon procedures for engagements, examinations, and reviews as the three basic types of attest engagements.

Q. Which of the following is not an element of quality control?

a. Acceptance and continuance of client relationships and specific engagements.

b. Human resources. c. Internal control. d. Monitoring.

A. (c) The requirement is to identify the reply that is not one of the elements of quality control. Answer (c) is correct because there is no quality control element on internal control. Acceptance of client relationships and specific engagements (a), human resources (b), and monitoring (d) are all elements of quality control. In addition, the following also are elements of quality control: leadership responsibilities for engagement performance, quality within the firm, and relevant ethical requirements.

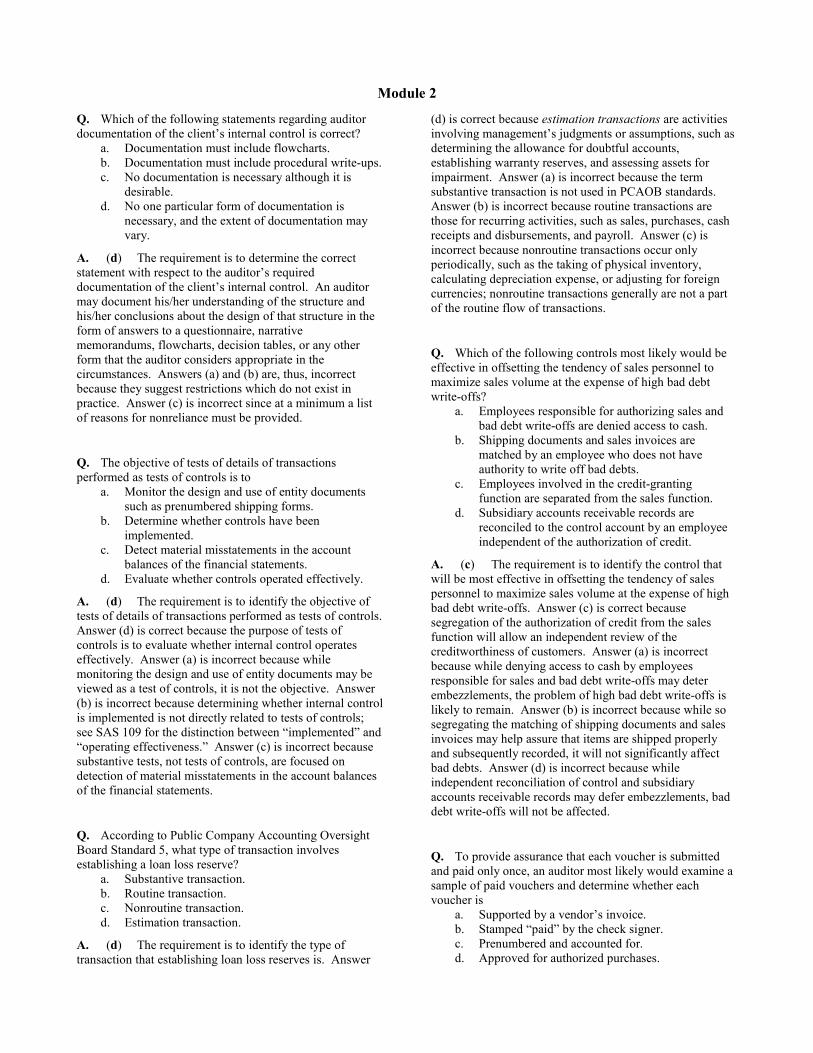

Module 2

Q. Which of the following statements regarding auditor documentation of the client’s internal control is correct?

a. Documentation must include flowcharts. b. Documentation must include procedural write-ups. c. No documentation is necessary although it is

desirable. d. No one particular form of documentation is

necessary, and the extent of documentation may vary.

A. (d) The requirement is to determine the correct statement with respect to the auditor’s required documentation of the client’s internal control. An auditor may document his/her understanding of the structure and his/her conclusions about the design of that structure in the form of answers to a questionnaire, narrative memorandums, flowcharts, decision tables, or any other form that the auditor considers appropriate in the circumstances. Answers (a) and (b) are, thus, incorrect because they suggest restrictions which do not exist in practice. Answer (c) is incorrect since at a minimum a list of reasons for nonreliance must be provided.

Q. The objective of tests of details of transactions performed as tests of controls is to

a. Monitor the design and use of entity documents such as prenumbered shipping forms.

b. Determine whether controls have been implemented.

c. Detect material misstatements in the account balances of the financial statements.

d. Evaluate whether controls operated effectively.

A. (d) The requirement is to identify the objective of tests of details of transactions performed as tests of controls. Answer (d) is correct because the purpose of tests of controls is to evaluate whether internal control operates effectively. Answer (a) is incorrect because while monitoring the design and use of entity documents may be viewed as a test of controls, it is not the objective. Answer (b) is incorrect because determining whether internal control is implemented is not directly related to tests of controls; see SAS 109 for the distinction between “implemented” and “operating effectiveness.” Answer (c) is incorrect because substantive tests, not tests of controls, are focused on detection of material misstatements in the account balances of the financial statements.

Q. According to Public Company Accounting Oversight Board Standard 5, what type of transaction involves establishing a loan loss reserve?

a. Substantive transaction. b. Routine transaction. c. Nonroutine transaction. d. Estimation transaction.

A. (d) The requirement is to identify the type of transaction that establishing loan loss reserves is. Answer

(d) is correct because estimation transactions are activities involving management’s judgments or assumptions, such as determining the allowance for doubtful accounts, establishing warranty reserves, and assessing assets for impairment. Answer (a) is incorrect because the term substantive transaction is not used in PCAOB standards. Answer (b) is incorrect because routine transactions are those for recurring activities, such as sales, purchases, cash receipts and disbursements, and payroll. Answer (c) is incorrect because nonroutine transactions occur only periodically, such as the taking of physical inventory, calculating depreciation expense, or adjusting for foreign currencies; nonroutine transactions generally are not a part of the routine flow of transactions.

Q. Which of the following controls most likely would be effective in offsetting the tendency of sales personnel to maximize sales volume at the expense of high bad debt write-offs?

a. Employees responsible for authorizing sales and bad debt write-offs are denied access to cash.

b. Shipping documents and sales invoices are matched by an employee who does not have authority to write off bad debts.

c. Employees involved in the credit-granting function are separated from the sales function.

d. Subsidiary accounts receivable records are reconciled to the control account by an employee independent of the authorization of credit.

A. (c) The requirement is to identify the control that will be most effective in offsetting the tendency of sales personnel to maximize sales volume at the expense of high bad debt write-offs. Answer (c) is correct because segregation of the authorization of credit from the sales function will allow an independent review of the creditworthiness of customers. Answer (a) is incorrect because while denying access to cash by employees responsible for sales and bad debt write-offs may deter embezzlements, the problem of high bad debt write-offs is likely to remain. Answer (b) is incorrect because while so segregating the matching of shipping documents and sales invoices may help assure that items are shipped properly and subsequently recorded, it will not significantly affect bad debts. Answer (d) is incorrect because while independent reconciliation of control and subsidiary accounts receivable records may defer embezzlements, bad debt write-offs will not be affected.

Q. To provide assurance that each voucher is submitted and paid only once, an auditor most likely would examine a sample of paid vouchers and determine whether each voucher is

a. Supported by a vendor’s invoice. b. Stamped “paid” by the check signer. c. Prenumbered and accounted for. d. Approved for authorized purchases.

A. (b) The requirement is to identify the audit procedure relating to paid vouchers that will provide assurance that each voucher is submitted and paid only once. Answer (b) is correct because when the check signer

stamps vouchers “paid” it is unlikely to be paid a second time since that individual will notice the stamp on the voucher the second time it is submitted for payment.

Module 3

Q. The objective of tests of details of transactions performed as substantive tests is to

a. Comply with generally accepted auditing standards.

b. Attain assurance about the reliability of the accounting system.

c. Detect material misstatements in the financial statements.

d. Evaluate whether management’s policies and procedures operated effectively.

A. (c) The requirement is to identify the objective of tests of details of transactions performed as substantive tests. Answer (c) is correct because SAS 110 states that the objective of tests of details of transactions performed as substantive tests is to detect material misstatements in the financial statements. Answer (a) is incorrect because while performing tests of details of transactions as substantive tests complies with generally accepted auditing standards, this is not their objective. Answers (b) and (d) are incorrect because neither attaining assurance about the reliability of the accounting system nor the evaluation of the operating effectiveness of management’s policies and procedures are the objective of tests of details of transactions performed as substantive tests.

Q. Audit documentation for audits performed under the requirements of the Public Company Accounting Oversight Board should be retained for

a. The shorter of five years, or the period required by law.

b. Seven years. c. The longer of seven years, or the period required

by law. d. Indefinitely.

A. (c) The requirement is to identify the period for which audit documentation should be retained for issuer (public) company audits. Answer (c) is correct because PCAOB Standard 3 requires that audit documentation be retained for the longer of seven years or the period required by law. Answer (a) is incorrect both because of the seven-year requirement, and because it is the longer of seven years or the period required by law. Answer (b) is incorrect because while seven years is the general requirement, a longer period may be required by law. Answer (d) is incorrect because audit documentation need not be retained indefinitely.

Q. In auditing accounts receivable, the negative form of confirmation request most likely would be used when

a. The total recorded amount of accounts receivable is immaterial to the financial statements taken as a whole.

b. Response rates in prior years to properly designed positive confirmation requests were inadequate.

c. Recipients are likely to return positive confirmation requests without verifying the accuracy of the information.

d. The combined assessed level of inherent risk and control risk relative to accounts receivable is low.

A. (d) The requirement is to identify the circumstance in which the negative form of confirmation request most likely would be used. Answer (d) is correct because AU 330 states that negative confirmations may be used when (1) the combined assessed level of inherent and control risk is low [answer (d)], (2) a large number of small balances is involved, and (3) the auditor has no reason to believe that the recipients of the requests are unlikely to give them consideration. Answer (a) is incorrect because when the accounts receivable are immaterial, a decision may be made to send no confirmations. Answer (b) is incorrect because an inadequate rate is not an acceptable reason to send negative confirmations. Answer (c) is incorrect because negative confirmations are only of value when the auditor has no reason to believe that the recipients of the requests are unlikely to give them consideration.

Q. The most likely risk involved with a bill and hold transaction at year-end is a(n)

a. Accrued liability may be overstated as of year-end.

b. Buyer may have made an absolute purchase commitment.

c. Sale may inappropriately have been recorded as of year-end.

d. Buyer may have assumed the risk and reward of the purchased product.

A. (c) The requirement is to identify the most likely risk involved with a bill and hold transaction at year-end. Answer (c) is correct because a bill and hold transaction results in the recording of a sale prior to delivery of the goods—accordingly, sales may be inappropriately recorded. Answer (a) is incorrect because accrued liabilities are not ordinarily affected by bill and hold transactions. Answers (b) and (d) are incorrect because an absolute purchase commitment and the assuming of risk and reward relating to the product represent conditions which increase the likelihood that recording of a sale for such a transaction is appropriate.

Q. Which of the following procedures should an accountant perform during an engagement to review the financial statements of a nonissuer?

a. Communicating significant deficiencies discovered during the assessment of control risk.

b. Obtaining a client representation letter from members of management.

c. Sending bank confirmation letters to the entity’s financial institutions.

d. Examining cash disbursements in the subsequent period for unrecorded liabilities.

A. (b) The requirement is to identify the procedures that an accountant would perform during an engagement to review the financial statements of a nonissuer. Answer (b) is correct because AR100 requires that the CPA obtain a representation letter. Answers (a), (c), and (d) are incorrect because they are not included in AR100 which presents a list of procedures performed during a review.

Module 4

Q. Under which of the following circumstances would a disclaimer of opinion not be appropriate?

a. The auditor is unable to determine the amounts associated with an employee fraud scheme.

b. Management does not provide reasonable justification for a change in accounting principles.

c. The client refuses to permit the auditor to confirm certain accounts receivable or apply alternative procedures to verify their balances.

d. The chief executive officer is unwilling to sign the management representation letter.

A. (b) The requirement is to identify the circumstance in which a disclaimer of opinion is not appropriate. Answer (b) is correct because when management does not provide reasonable justification of a change in accounting principles either a qualified or an adverse opinion is appropriate, not a disclaimer. Answers (a), (c), and (d) are all incorrect because they represent scope limitations that lead to either a qualified opinion or a disclaimer of opinion.

Q. An auditor who qualifies an opinion because of an insufficiency of evidential matter should describe the limitations in an explanatory paragraph. The auditor should also refer to the limitation in the

Scope Opinion Notes to the

paragraph paragraph financial statements

a. Yes No Yes b. No Yes No c. Yes Yes No d. Yes Yes Yes

A. (c) The requirement is to determine whether the scope paragraph, opinion paragraph, and/or notes to the financial statements should refer to an audit scope limitation. Answer (c) is correct because the suggested report presented for a scope limitation includes modification of both the scope and opinion paragraphs. In addition, it is not appropriate for the scope of the audit to be explained in a note to the financial statements.

Q. Financial statements of a nonissuer that have been reviewed by an accountant should be accompanied by a report stating that

a. The scope of the inquiry and analytical procedures performed by the accountant has not been restricted.

b. All information included in the financial statements is the representation of the management of the entity.

c. A review includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements.

d. A review is greater in scope than a compilation, the objective of which is to present financial statements that are free of material misstatements.

A. (b) The requirement is to identify the information presented in a review report of financial statements of a nonissuer. Answer (b) is correct because the report indicates that all information included in the financial statements is the representation of the management of the entity.

Q. An accountant’s compilation report on a financial forecast should include a statement that

a. The forecast should be read only in conjunction with the audited historical financial statements.

b. The accountant expresses only limited assurance on the forecasted statements and their assumptions.

c. There will usually be differences between the forecasted and actual results.

d. The hypothetical assumptions used in the forecast are reasonable in the circumstances.

A. (c) The requirement is to identify the statement which should be included in an accountant’s compilation report on financial forecasts. Answer (c) is correct because when the accountant is preparing a standard compilation report on prospective financial statements, AT 301 requires that the accountant include a statement indicating that the prospective results may not be achieved.

Module 5

Q. An advantage of statistical sampling over nonstatistical sampling is that statistical sampling helps an auditor to

a. Eliminate the risk of nonsampling errors. b. Reduce the level of audit risk and materiality to a

relatively low amount.

c. Measure the sufficiency of the evidential matter obtained.

d. Minimize the failure to detect errors and fraud.

A. (c) The requirement is to identify an advantage of statistical sampling over nonstatistical sampling. Answer (c) is correct because statistical sampling helps the auditor to (1) design an efficient sample, (2) measure the sufficiency of the evidential matter obtained, and (3) evaluate the sample results (AICPA Audit Sampling Guide). Answer (a) is incorrect because the risk of nonsampling errors is not directly affected by whether statistical or nonstatistical sampling is used. Answer (b) is incorrect because either statistical or nonstatistical sampling can be used to reduce the level of audit risk to a low level; the materiality level should not be affected by the type of sampling used. Answer (d) is incorrect because either statistical or nonstatistical sampling may be used to minimize the failure to detect errors and fraud.

Q. Which of the following factors is(are) considered in determining the sample size for a test of controls?

Expected

deviation rate Tolerable

deviation rate a. Yes Yes b. No No c. No Yes d. Yes No

A. (a) The requirement is to determine whether the expected deviation rate, the tolerable deviation rate, or both affect the sample size for a test of controls. Answer (a) is correct because attribute sampling formulas and tables used in auditing generally require the auditor to specify an expected deviation rate, a tolerable deviation rate and the

risk of assessing control risk too low. See AICPA Audit Sampling Guide and AU 350 for more information on audit sampling.

Q. A number of factors influence the sample size for a substantive test of details of an account balance. All other factors being equal, which of the following would lead to a larger sample size?

a. Greater reliance on internal control. b. Greater reliance on analytical procedures. c. Smaller expected frequency of errors. d. Smaller measure of tolerable misstatement.

A. (d) The requirement is to determine the factor that would lead to larger sample size in a substantive test of details. Answer (d) is correct because the sample size required to achieve the auditor’s objective at a given risk of incorrect acceptance increases as the auditor’s assessment of tolerable misstatement for the balance or class decreases. Answer (a) is incorrect because a greater reliance on internal control will lead to a smaller sample size in a substantive test of details. Answer (b) is incorrect because greater reliance upon analytical procedures will result in a need for less reliance on substantive tests of details and therefore will result in a smaller sample. Answer (c) is incorrect because a smaller expected frequency of errors will generally include properly functioning internal control and will therefore result in a smaller sample for substantive tests of details.

Module 6

Q. An auditor would most likely be concerned with which of the following controls in a distributed data processing system?

a. Hardware controls. b. Systems documentation controls. c. Access controls. d. Disaster recovery controls.

A. (c) The requirement is to identify the types of controls with which an auditor would be most likely to be concerned in a distributed data processing system. A distributed data processing system is one in which there is a network of remote computer sites, each having a computer connected to the main computer system, thus allowing access to the computers by various levels of users. Accordingly, answer (c) is correct because numerous individuals may access the system, thereby making such controls of extreme importance. Answers (a), (b), and (d), while requiring concern, are normally considered less critical than proper access controls for this situation.

Q. Which of the following computer-assisted auditing techniques allows fictitious and real transactions to be processed together without client operating personnel being aware of the testing process?

a. Integrated test facility. b. Input controls matrix.

c. Parallel simulation. d. Data entry monitor.

A. (a) The requirement is to identify the computer-assisted auditing technique which allows fictitious and real transactions to be processed together without client operating personnel being aware of the testing process. Answer (a) is correct because the integrated test facility approach introduces dummy transactions into a system in the midst of live transactions. Accordingly, client operating personnel may not be aware of the testing process. Answer (b) is incorrect because an input control matrix would simply indicate various controls in the form of a matrix. Answer (c) is incorrect because the parallel simulation technique requires the processing of actual client data through an auditor’s software program. In this case, the client would be aware of the testing process since the auditor would need to request copies of data run on the actual system so that the data could then be run on the auditor’s software program. Additionally, only valid transactions would be tested under parallel simulation. Answer (d) is incorrect because the client would generally be aware of an auditor using a data entry monitor (screen) to input transactions.

Q. An auditor most likely would test for the presence of unauthorized computer program changes by running a

a. Program with test data. b. Check digit verification program. c. Source code comparison program. d. Program that computes control totals.

A. (c) The requirement is to identify how an auditor would test for the presence of unauthorized computer program changes. Answer (c) is correct because comparing source code of the program with a correct version of the program will disclose unauthorized computer program

changes. Answer (a) is incorrect because test data is generally used to test specific controls and it will generally be less effective for detecting unauthorized changes than will source code comparison. Answer (b) is incorrect because check digits are primarily used as an input control to determine that input data is proper. Answer (d) is incorrect because properly computing control totals is only one possible unauthorized change that might be made to a program.

Financial Accounting and Reporting

Module 7A

Q. What is the underlying concept governing the generally accepted accounting principles pertaining to recording gain contingencies?

a. Conservatism. b. Relevance. c. Consistency. d. Reliability.

A. (a) Conservatism means that when in doubt, accountants should choose the procedure that will be least likely to overstate assets and income. This concept underlies the GAAP pertaining to recording gain contingencies. In an effort to not overstate assets or income, gain contingencies are not recorded until they are no longer contingencies, and are disclosed only when probabilities are high that a gain contingency will become reality.

Module 7B

Q. On December 31, 2009, special insurance costs were incurred and unpaid, but were not recorded. If these insurance costs were related to a particular job order in work in process that was not completed during the period, what is the effect of the omission on accrued liabilities and retained earnings in the December 31, 2009 balance sheet?

Accrued liabilities Retained earnings

a. No effect No effect b. No effect Overstated c. Understated No effect d. Understated Overstated

A. (c) A liability is accrued when an obligation to pay or perform services has been incurred. This is the case even if the liability will not be satisfied until a future date. Therefore, accrued liabilities will be understated on the December 31, 2009 balance sheet because the special insurance costs were not recorded. However, there will be no effect on the December 31, 2009 balance of retained earnings because these costs relate to work in process, and work in process does not affect net income currently. Please note that if the special insurance costs related to goods that were sold, cost of goods sold would have been understated that would have caused both net income and retained earnings to be overstated.

Module 7C

Q. The effect of a change in accounting principle that is inseparable from the effect of a change in accounting estimate should be reported

a. By restating the financial statements of all prior periods presented.

b. As a correction of an error. c. As a component of income from continuing

operations, in the period of change and future periods if the change affects both.

d. As a separate disclosure after income from continuing operations, in the period of change and future periods if the change affects both.

A. (c) Per ASC Topic 250, the effect of a change in accounting principle which is inseparable from the effect of a change in accounting estimate should be accounted for as a change in accounting estimate. Changes in estimate should be accounted for in the period of change and also in any affected future periods as a component of income from continuing operations. Financial statements are only restated for changes due to an error. Errors include mathematical mistakes, mistakes in applying accounting principles, oversights or misuse of available facts, and changes from unacceptable accounting principles to GAAP. The situation described in this question does not meet the description of an error.

Module 7D

Q. Which of the following changes during a period is not a component of other comprehensive income?

a. Pension liability adjustment for funded status of plan.

b. Treasury stock, at cost. c. Foreign currency translation adjustment. d. Reclassification adjustment, for securities gain

included in net income.

Q. (b) SFAS 130 requires disclosure of changes during a period of the following components of other comprehensive income: unrealized gains and losses on available-for-sale investments and foreign currency items, including any reclassification adjustments, and the pension liability adjustment required to recognize the funded status of the plan. Treasury stock is deducted from stockholders’ equity and not a component of other comprehensive income.

Module 8

Q. The following information pertained to Azur Co. for the year:

Purchases $102,800 Purchase discounts 10,280 Freight in 15,420 Freight out 5,140 Beginning inventory 30,840 Ending inventory 20,560

What amount should Azur report as cost of goods sold for the year?

a. $102,800 b. $118,220 c. $123,360 d. $128,500

A. (b) Azur should report cost of goods sold calculated as

Cost of goods sold (CGS) = Beg. Inventory + Net purchases* + Freight in – Ending Inventory

CGS = $ 30,840 + $92,520** + $15,420 – $20,560

CGS = $118,220

Freight out is a selling expense and does not enter the calculation of cost of goods sold.

* Net purchase = Purchases – Purchase returns and allowances –

Purchase discounts

** ($102,800 – $10,280)

Module 9

Q. A nonmonetary exchange is recognized at fair value of the assets exchanged unless

a. Exchange has commercial substance. b. Fair value is not determinable. c. The assets are similar in nature. d. The assets are dissimilar.

A. (b) Per ASC Topic 845, a nonmonetary exchange is recognized at fair value unless the fair value is not determinable, the exchange transaction is to facilitate sales to customers, or the exchange transactions lacks commercial substance. Answer (a) is incorrect, because the exchange must lack commercial substance. Answers (c) and (d) are incorrect because there is no longer the distinction of similar or dissimilar assets in nonmonetary exchanges.

Q. Turtle Co. purchased equipment on January 2, 2007, for $50,000. The equipment had an estimated five-year service life. Turtle’s policy for five-year assets is to use the 200% double-declining depreciation method for the first two years of the asset’s life, and then switch to the straight-line depreciation method. In its December 31, 2009 balance sheet, what amount should Turtle report as accumulated depreciation for equipment?

a. $30,000 b. $38,000 c. $39,200 d. $42,000

A. (b) The formula for 200% double-declining balance (DDB) depreciation is

(Beginning-of-year book value) × DDB rate = Depreciation expense

The DDB rate is two times the straight-line rate (in this case, 1/5 × 2 = 2/5 or 40%). Therefore, depreciation for the first two years is

2007: $50,000 × 40% = $20,000 2008: ($50,000 – $20,000) × 40% = 12,000 $32,000

In 2009, Turtle switches to the straight-line method. The book value ($50,000 – $32,000 = $18,000) would be depreciated over the remaining three years (five years less two gone by). Therefore, 2009 depreciation is $6,000 ($18,000 × 1/3) and 12/31/09 accumulated depreciation is $38,000 ($32,000 + $6,000).

Module 10

Q. The following information pertains to Tara Co.’s accounts receivable at December 31, 2008:

Days outstanding Amount Estimated % uncollectible 0 – 60 $120,000 1% 61 – 120 90,000 2% Over 120 100,000 6% $310,000

During 2008, Tara wrote off $7,000 in receivables and recovered $4,000 that had been written off in prior years. Tara’s December 31, 2007 allowance for uncollectible accounts was $22,000. Under the aging method, what amount of allowance for uncollectible accounts should Tara report at December 31, 2008?

a. $ 9,000 b. $10,000 c. $13,000

d. $19,000

A. (a) When an aging schedule is used to estimate uncollectibles, the total uncollectibles computed is the amount used for the ending balance in the allowance account. As computed below, the 12/31/08 allowance for uncollectible accounts should be $9,000.

$120,000 × 1% = $1,200 90,000 × 2% = 1,800 100,000 × 6% = 6,000

$9,000

The other information given (12/31/07 allowance, write-offs, and recoveries) would be used to determine the bad debt expense adjustment, not the allowance balance. In this case, apparently due to a change in estimate, the bad debt

expense adjustment would actually be a credit (to offset the necessary debit to the allowance account).

Allowance for U.A.

22,000 12/31/07 Write-offs 7,000 4,000 Recoveries

19,000 Adjustment 10,000

9,000 12/31/08

Q. Cobb Company sells appliance service contracts agreeing to repair appliances for a two-year period. Cobb’s past experience is that, of the total dollars spent for repairs on service contracts, 40% is incurred evenly during the first contract year and 60% evenly during the second contract year. Receipts from service contract sales for the two years ended December 31, 2008, are as follows:

2007 $500,000 2008 600,000

Receipts from contracts are credited to unearned service contract revenue. Assume that all contract sales are made evenly during the year. What amount should Cobb report as unearned service contract revenue at December 31, 2008?

a. $360,000 b. $470,000 c. $480,000

d. $630,000

A. (d) All contract sales are made evenly during the year. Therefore, the 2007 contracts range from one year expired (if sold on 12/31/07) to two years expired (if sold on 1/1/07), for an average of one and one-half years expired [(2+1)/2]. Similarly, the 2008 contracts range from zero years expired to one year expired, for an average of one-half year expired [(0+1)/2]. The average unearned portion of the 2007 contracts is one-half year (two years – one and one-half years), the last half of the second contract year. The amount of unearned revenue related to 2007 contracts is computed as follows:

$500,000 × 60% × 1/2 = $150,000

The average unearned portion of the 2008 contracts is one and one-half years (two years – one-half year), the last half of the first contract year and all of the second contract year. The amount of unearned revenue related to the 2008 contracts is computed as follows:

2008: $600,000 × 40% × ½ = $120,000 $600,000 × 60% = 360,000

$480,000

Therefore, the total unearned revenue is $630,000 ($150,000 + $480,000).

Module 11A

Q. On July 1, 2008, James Rago signed an agreement to operate as a franchisee of Fast Foods, Inc. for an initial franchise fee of $60,000. Of this amount, $20,000 was paid when the agreement was signed and the balance is payable in four equal annual payments of $10,000 beginning July 1, 2009. The agreement provides that the down payment is not refundable and no future services are required of the franchisor. Rago’s credit rating indicates that he can borrow money at 14% for a loan of this type. Information on present and future value factors is as follows:

Present value of $1 at 14% for four periods 0.59 Future amount of $1 at 14% for four periods 1.69 Present value of an ordinary annuity of $1 at 14% for four periods 2.91

Rago should record the acquisition cost of the franchise on July1, 2008 at

a. $43,600

b. $49,100 c. $60,000 d. $67,600

A. (b) The requirement is to determine the acquisition cost of a franchise. The cost of this franchise is the down payment of $20,000 plus the present value of the four equal annual payments of $10,000. The annual payments represent an annuity, so the $10,000 annual payment is multiplied by the present value factor of 2.91. Therefore, the franchise cost is $49,100 ($20,000 + $29,100). The journal entry is

Franchise 49,100 Discount on notes payable 10,900

Notes payable 40,000 Cash 20,000

Module 11B

Q. The market price of a bond issued at a discount is the present value of its principal amount at the market (effective) rate of interest

a. Less the present value of all future interest payments at the market (effective) rate of interest.

b. Less the present value of all future interest payments at the rate of interest stated on the bond.

c. Plus the present value of all future interest payments at the market (effective) rate of interest.

d. Plus the present value of all future interest payments at the rate of interest stated on the bond.

A. (c) The market price of a bond issued at any amount (par, premium, or discount) is equal to the present value of all of its future cash flows, discounted at the current market (effective) interest rate. The market price of a bond issued at a discount is equal to the present value of both its principal and periodic future cash interest payments at the stated (cash) rate of interest, discounted at the current market (effective) rate.

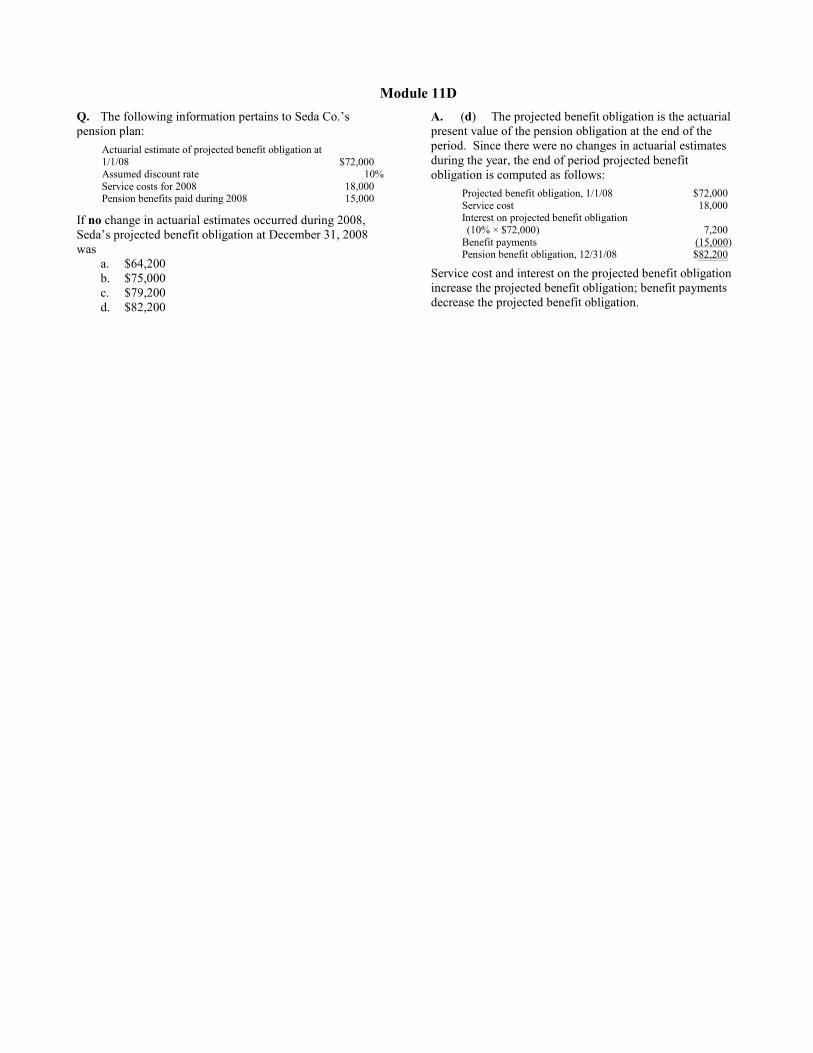

Module 11D

Q. The following information pertains to Seda Co.’s pension plan:

Actuarial estimate of projected benefit obligation at 1/1/08 $72,000 Assumed discount rate 10% Service costs for 2008 18,000 Pension benefits paid during 2008 15,000

If no change in actuarial estimates occurred during 2008, Seda’s projected benefit obligation at December 31, 2008 was

a. $64,200 b. $75,000 c. $79,200 d. $82,200

A. (d) The projected benefit obligation is the actuarial present value of the pension obligation at the end of the period. Since there were no changes in actuarial estimates during the year, the end of period projected benefit obligation is computed as follows:

Projected benefit obligation, 1/1/08 $72,000 Service cost 18,000 Interest on projected benefit obligation (10% × $72,000) 7,200 Benefit payments (15,000) Pension benefit obligation, 12/31/08 $82,200

Service cost and interest on the projected benefit obligation increase the projected benefit obligation; benefit payments decrease the projected benefit obligation.

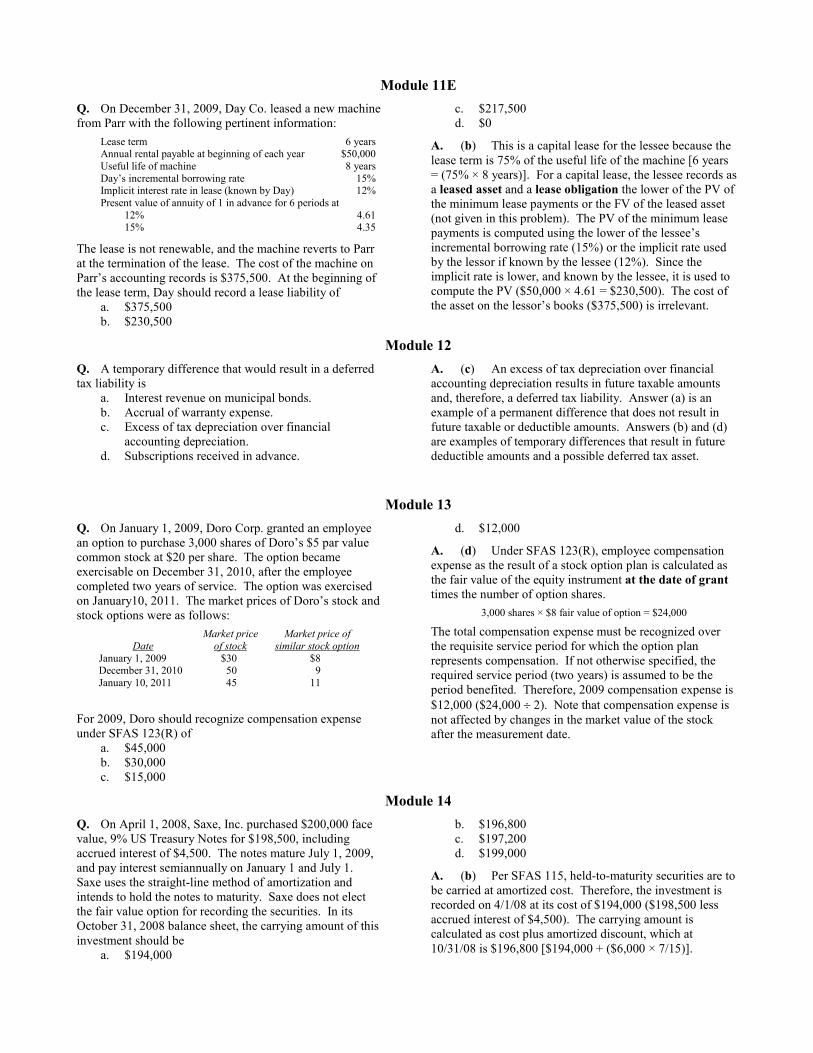

Module 11E

Q. On December 31, 2009, Day Co. leased a new machine from Parr with the following pertinent information:

Lease term 6 years Annual rental payable at beginning of each year $50,000 Useful life of machine 8 years Day’s incremental borrowing rate 15% Implicit interest rate in lease (known by Day) 12% Present value of annuity of 1 in advance for 6 periods at

12% 4.61 15% 4.35

The lease is not renewable, and the machine reverts to Parr at the termination of the lease. The cost of the machine on Parr’s accounting records is $375,500. At the beginning of the lease term, Day should record a lease liability of

a. $375,500 b. $230,500

c. $217,500 d. $0

A. (b) This is a capital lease for the lessee because the lease term is 75% of the useful life of the machine [6 years = (75% × 8 years)]. For a capital lease, the lessee records as a leased asset and a lease obligation the lower of the PV of the minimum lease payments or the FV of the leased asset (not given in this problem). The PV of the minimum lease payments is computed using the lower of the lessee’s incremental borrowing rate (15%) or the implicit rate used by the lessor if known by the lessee (12%). Since the implicit rate is lower, and known by the lessee, it is used to compute the PV ($50,000 × 4.61 = $230,500). The cost of the asset on the lessor’s books ($375,500) is irrelevant.

Module 12

Q. A temporary difference that would result in a deferred tax liability is

a. Interest revenue on municipal bonds. b. Accrual of warranty expense. c. Excess of tax depreciation over financial

accounting depreciation. d. Subscriptions received in advance.

A. (c) An excess of tax depreciation over financial accounting depreciation results in future taxable amounts and, therefore, a deferred tax liability. Answer (a) is an example of a permanent difference that does not result in future taxable or deductible amounts. Answers (b) and (d) are examples of temporary differences that result in future deductible amounts and a possible deferred tax asset.

Module 13

Q. On January 1, 2009, Doro Corp. granted an employee an option to purchase 3,000 shares of Doro’s $5 par value common stock at $20 per share. The option became exercisable on December 31, 2010, after the employee completed two years of service. The option was exercised on January10, 2011. The market prices of Doro’s stock and stock options were as follows:

Date

Market price

of stock

Market price of

similar stock option

January 1, 2009 $30 $8 December 31, 2010 50 9 January 10, 2011 45 11

For 2009, Doro should recognize compensation expense under SFAS 123(R) of

a. $45,000 b. $30,000 c. $15,000

d. $12,000

A. (d) Under SFAS 123(R), employee compensation expense as the result of a stock option plan is calculated as the fair value of the equity instrument at the date of grant times the number of option shares.

3,000 shares × $8 fair value of option = $24,000

The total compensation expense must be recognized over the requisite service period for which the option plan represents compensation. If not otherwise specified, the required service period (two years) is assumed to be the period benefited. Therefore, 2009 compensation expense is

$12,000 ($24,000 ÷ 2). Note that compensation expense is not affected by changes in the market value of the stock after the measurement date.

Module 14

Q. On April 1, 2008, Saxe, Inc. purchased $200,000 face value, 9% US Treasury Notes for $198,500, including accrued interest of $4,500. The notes mature July 1, 2009, and pay interest semiannually on January 1 and July 1. Saxe uses the straight-line method of amortization and intends to hold the notes to maturity. Saxe does not elect the fair value option for recording the securities. In its October 31, 2008 balance sheet, the carrying amount of this investment should be

a. $194,000

b. $196,800 c. $197,200 d. $199,000

A. (b) Per SFAS 115, held-to-maturity securities are to be carried at amortized cost. Therefore, the investment is recorded on 4/1/08 at its cost of $194,000 ($198,500 less accrued interest of $4,500). The carrying amount is calculated as cost plus amortized discount, which at 10/31/08 is $196,800 [$194,000 + ($6,000 × 7/15)].

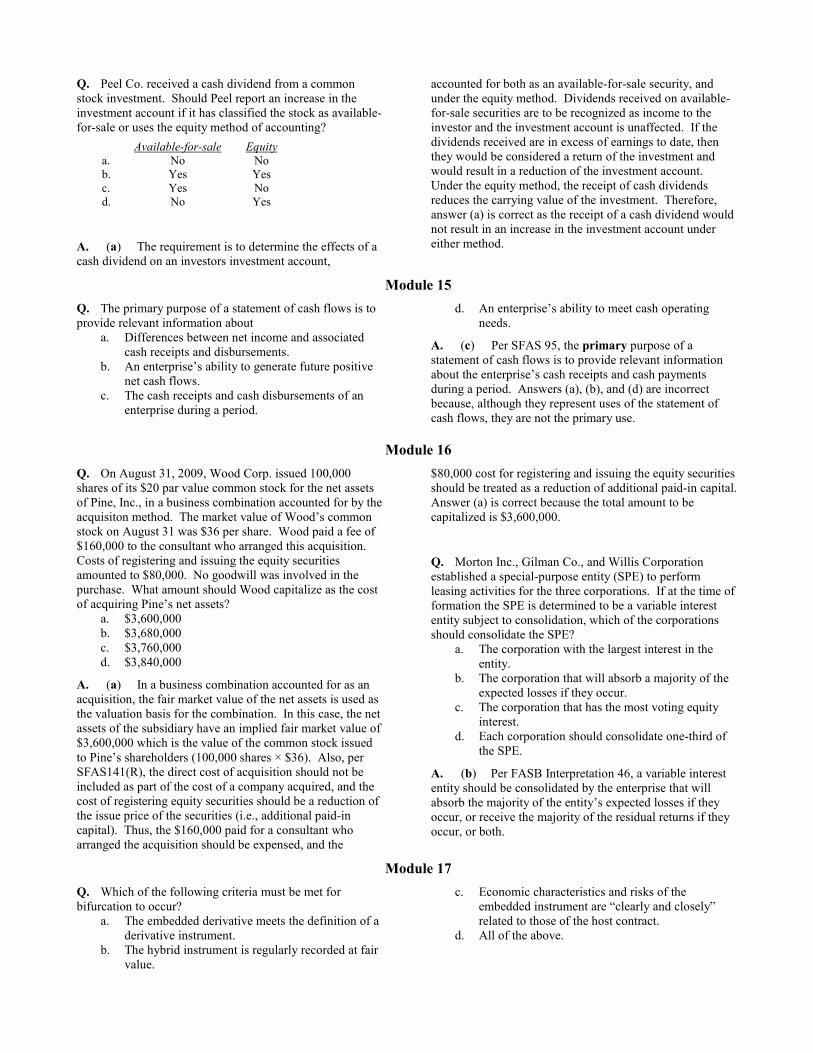

Q. Peel Co. received a cash dividend from a common stock investment. Should Peel report an increase in the investment account if it has classified the stock as available-for-sale or uses the equity method of accounting?

Available-for-sale Equity

a. No No b. Yes Yes c. Yes No d. No Yes

A. (a) The requirement is to determine the effects of a cash dividend on an investors investment account,

accounted for both as an available-for-sale security, and under the equity method. Dividends received on available-for-sale securities are to be recognized as income to the investor and the investment account is unaffected. If the dividends received are in excess of earnings to date, then they would be considered a return of the investment and would result in a reduction of the investment account. Under the equity method, the receipt of cash dividends reduces the carrying value of the investment. Therefore, answer (a) is correct as the receipt of a cash dividend would not result in an increase in the investment account under either method.

Module 15

Q. The primary purpose of a statement of cash flows is to provide relevant information about

a. Differences between net income and associated cash receipts and disbursements.

b. An enterprise’s ability to generate future positive net cash flows.

c. The cash receipts and cash disbursements of an enterprise during a period.

d. An enterprise’s ability to meet cash operating needs.

A. (c) Per SFAS 95, the primary purpose of a statement of cash flows is to provide relevant information about the enterprise’s cash receipts and cash payments during a period. Answers (a), (b), and (d) are incorrect because, although they represent uses of the statement of cash flows, they are not the primary use.

Module 16

Q. On August 31, 2009, Wood Corp. issued 100,000 shares of its $20 par value common stock for the net assets of Pine, Inc., in a business combination accounted for by the acquisiton method. The market value of Wood’s common stock on August 31 was $36 per share. Wood paid a fee of $160,000 to the consultant who arranged this acquisition. Costs of registering and issuing the equity securities amounted to $80,000. No goodwill was involved in the purchase. What amount should Wood capitalize as the cost of acquiring Pine’s net assets?

a. $3,600,000 b. $3,680,000 c. $3,760,000 d. $3,840,000

A. (a) In a business combination accounted for as an acquisition, the fair market value of the net assets is used as the valuation basis for the combination. In this case, the net assets of the subsidiary have an implied fair market value of $3,600,000 which is the value of the common stock issued to Pine’s shareholders (100,000 shares × $36). Also, per SFAS141(R), the direct cost of acquisition should not be included as part of the cost of a company acquired, and the cost of registering equity securities should be a reduction of the issue price of the securities (i.e., additional paid-in capital). Thus, the $160,000 paid for a consultant who arranged the acquisition should be expensed, and the

$80,000 cost for registering and issuing the equity securities should be treated as a reduction of additional paid-in capital. Answer (a) is correct because the total amount to be capitalized is $3,600,000.

Q. Morton Inc., Gilman Co., and Willis Corporation established a special-purpose entity (SPE) to perform leasing activities for the three corporations. If at the time of formation the SPE is determined to be a variable interest entity subject to consolidation, which of the corporations should consolidate the SPE?

a. The corporation with the largest interest in the entity.

b. The corporation that will absorb a majority of the expected losses if they occur.

c. The corporation that has the most voting equity interest.

d. Each corporation should consolidate one-third of the SPE.

A. (b) Per FASB Interpretation 46, a variable interest entity should be consolidated by the enterprise that will absorb the majority of the entity’s expected losses if they occur, or receive the majority of the residual returns if they occur, or both.

Module 17

Q. Which of the following criteria must be met for bifurcation to occur?

a. The embedded derivative meets the definition of a derivative instrument.

b. The hybrid instrument is regularly recorded at fair value.

c. Economic characteristics and risks of the embedded instrument are “clearly and closely” related to those of the host contract.

d. All of the above.

A. (a) The hybrid instrument is not recorded at fair value. Economic characteristics and risks of the embedded instrument are not “clearly and closely” related to those of

the host contract. For purposes of applying SFAS 133, the embedded derivative must meet the definition of a derivative instrument.

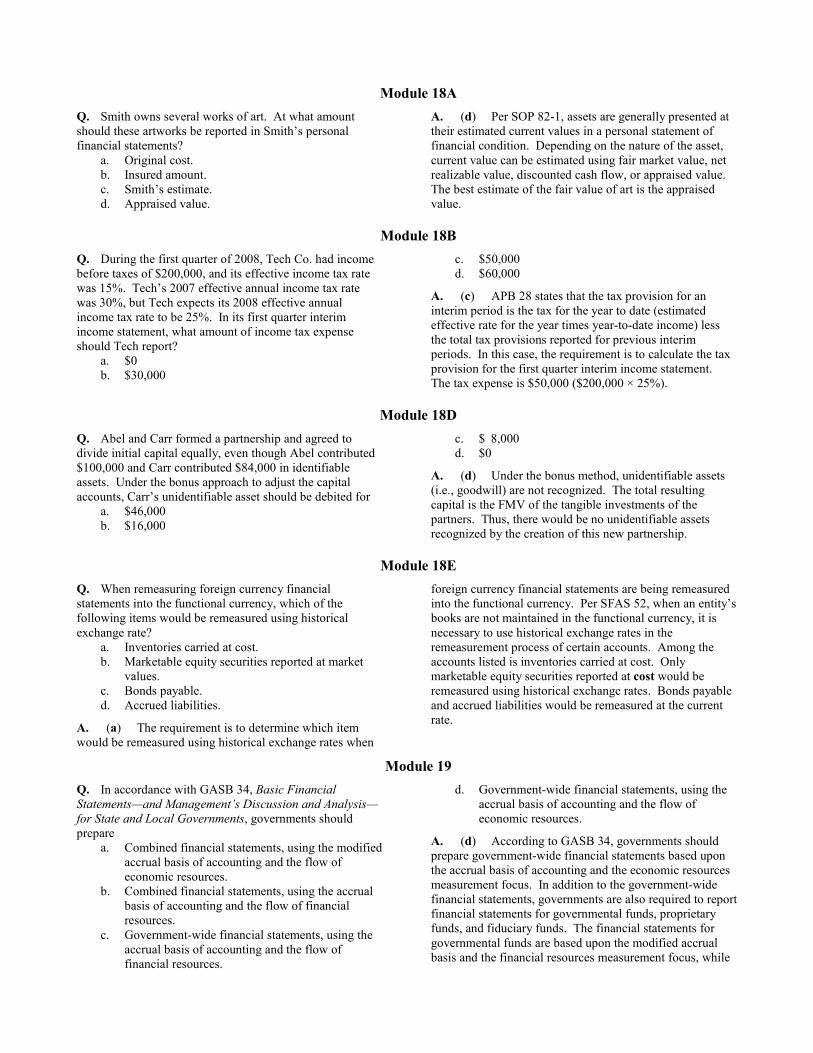

Module 18A

Q. Smith owns several works of art. At what amount should these artworks be reported in Smith’s personal financial statements?

a. Original cost. b. Insured amount. c. Smith’s estimate. d. Appraised value.

A. (d) Per SOP 82-1, assets are generally presented at their estimated current values in a personal statement of financial condition. Depending on the nature of the asset, current value can be estimated using fair market value, net realizable value, discounted cash flow, or appraised value. The best estimate of the fair value of art is the appraised value.

Module 18B

Q. During the first quarter of 2008, Tech Co. had income before taxes of $200,000, and its effective income tax rate was 15%. Tech’s 2007 effective annual income tax rate was 30%, but Tech expects its 2008 effective annual income tax rate to be 25%. In its first quarter interim income statement, what amount of income tax expense should Tech report?

a. $0 b. $30,000

c. $50,000 d. $60,000

A. (c) APB 28 states that the tax provision for an interim period is the tax for the year to date (estimated effective rate for the year times year-to-date income) less the total tax provisions reported for previous interim periods. In this case, the requirement is to calculate the tax provision for the first quarter interim income statement. The tax expense is $50,000 ($200,000 × 25%).

Module 18D

Q. Abel and Carr formed a partnership and agreed to divide initial capital equally, even though Abel contributed $100,000 and Carr contributed $84,000 in identifiable assets. Under the bonus approach to adjust the capital accounts, Carr’s unidentifiable asset should be debited for

a. $46,000 b. $16,000

c. $ 8,000 d. $0

A. (d) Under the bonus method, unidentifiable assets (i.e., goodwill) are not recognized. The total resulting capital is the FMV of the tangible investments of the partners. Thus, there would be no unidentifiable assets recognized by the creation of this new partnership.

Module 18E

Q. When remeasuring foreign currency financial statements into the functional currency, which of the following items would be remeasured using historical exchange rate?

a. Inventories carried at cost. b. Marketable equity securities reported at market

values. c. Bonds payable. d. Accrued liabilities.

A. (a) The requirement is to determine which item would be remeasured using historical exchange rates when

foreign currency financial statements are being remeasured into the functional currency. Per SFAS 52, when an entity’s books are not maintained in the functional currency, it is necessary to use historical exchange rates in the remeasurement process of certain accounts. Among the accounts listed is inventories carried at cost. Only marketable equity securities reported at cost would be remeasured using historical exchange rates. Bonds payable and accrued liabilities would be remeasured at the current rate.

Module 19

Q. In accordance with GASB 34, Basic Financial Statements—and Management’s Discussion and Analysis—

for State and Local Governments, governments should prepare

a. Combined financial statements, using the modified accrual basis of accounting and the flow of economic resources.

b. Combined financial statements, using the accrual basis of accounting and the flow of financial resources.

c. Government-wide financial statements, using the accrual basis of accounting and the flow of financial resources.

d. Government-wide financial statements, using the accrual basis of accounting and the flow of economic resources.

A. (d) According to GASB 34, governments should prepare government-wide financial statements based upon the accrual basis of accounting and the economic resources measurement focus. In addition to the government-wide financial statements, governments are also required to report financial statements for governmental funds, proprietary funds, and fiduciary funds. The financial statements for governmental funds are based upon the modified accrual basis and the financial resources measurement focus, while

the financial statements for proprietary and fiduciary funds are based upon the accrual basis of accounting and the flow of economic resources measurement focus.

Module 20

Q. If the Pel Museum, a not-for-profit organization, received a contribution of historical artifacts, it need not recognize the contribution if the artifacts are to be sold and the proceeds used to

a. Support general museum activities. b. Acquire other items for collections. c. Repair existing collections.

d. Purchase buildings to house collections.

A. (b) Per SFAS 116, an entity need not recognize the contributions of works of art and historical artifacts if the collection is held for public exhibition rather than financial profit, cared for and preserved, and, if sold, the proceeds are used to acquire other items for collections.

Regulation

Module 21

Q. According to the ethical standards of the profession, which of the following acts is generally prohibited?

a. Issuing a modified report explaining a failure to follow a governmental regulatory agency’s standards when conducting an attest service for a client.

b. Revealing confidential client information during a quality review of a professional practice by a team from the state CPA society.

c. Accepting a contingent fee for representing a client in an examination of the client’s federal tax return by an IRS agent.

d. Retaining client records after an engagement is terminated prior to completion and the client has demanded their return.

A. (d) The requirement is to determine which act is generally prohibited. Answer (d) is correct because “If an engagement is terminated prior to completion, the member is required to return only client records” (ET 501). Answer (a) is incorrect because issuing a modified report explaining a failure to follow a governmental regulatory agency’s standards when conducting an attest service is not prohibited. Answer (c) is incorrect because accepting a contingent fee is allowable when representing a client in an examination by a revenue agent of the client’s federal or state income tax return (ET 302). Answer (b) is incorrect because revealing confidential client information during a

quality review of a professional practice by a team from the state CPA society is not prohibited (ET 301).

Q. Which of the following statements is(are) correct regarding a CPA employee of a CPA firm taking copies of information contained in client files when the CPA leaves the firm?

I. A CPA leaving a firm may take copies of information contained in client files to assist another firm in serving that client.

II. A CPA leaving a firm may take copies of information contained in client files as a method of gaining technical expertise.

a. I only. b. II only. c. Both I and II. d. Neither I nor II.

A. (d) Both of the statements are incorrect; either would violate Rule 301 on confidential client information. Answer (a) is incorrect because statement I also is incorrect. Answer (b) is incorrect because statement II also is incorrect. Answer (c) is incorrect because statements I and II are both incorrect.

Module 22

Q. Which of the following securities would be regulated by the provisions of the Securities Act of 1933?

a. Securities issued by not-for-profit, charitable organizations.

b. Securities guaranteed by domestic governmental organizations.

c. Securities issued by savings and loan associations. d. Securities issued by insurance companies.

A. (d) Under the 1933 Act, certain securities are exempt. Although insurance and annuity contracts are exempt, securities issued by the insurance companies are not. Answer (a) is incorrect because securities of nonprofit organizations are exempt. Answer (b) is incorrect because

securities issued by or guaranteed by domestic government organizations are exempt. Answer (c) is incorrect because securities issued by savings and loan associations are exempt.

Module 23

Q. Under the UCC Sales Article, a plaintiff who proves fraud in the formation of a contract may

a. Elect to rescind the contract and need not return the consideration received from the other party.

b. Be entitled to rescind the contract and sue for damages resulting from the fraud.

c. Be entitled to punitive damages provided physical injuries resulted from the fraud.

d. Rescind the contract even if there was no reliance on the fraudulent statement.

A. (b) There are two remedies for fraud under the UCC Sales Article: (1) the plaintiff may affirm the agreement and sue for damages under the tort of deceit, or (2) the plaintiff may rescind the contract and sue for damages resulting from the fraud. Answer (a) is incorrect because the plaintiff must return any consideration received from the other party when the contract is rescinded. Answer (c) is incorrect because although punitive damages are allowed in fraud actions because they are intentional torts, they do not require physical injuries. Answer (d) is incorrect because without reliance by the plaintiff on the

misrepresentation, there is no fraud, and therefore, the plaintiff may not rescind the contract.

Module 24

Q. Under the Sales Article of the UCC, most goods sold by merchants are covered by certain warranties. An example of an express warranty would be a warranty of

a. Usage of trade. b. Fitness for a particular purpose. c. Merchantability. d. Conformity of goods to sample.

A. (d) In the Sales Article of the UCC, express warranties include warranties that the goods will conform to any description used or any sample or model shown. Answer (a) is incorrect because although usage of trade can help interpret terms used in contracts, it is not a warranty. Answers (b) and (c) are incorrect because the warranty of fitness for a particular purpose and the warranty of merchantability are both implied warranties.

Q. High sues the manufacturer, wholesaler, and retailer for bodily injuries caused by a power saw High purchased. Which of the following statements is correct under strict liability theory?

a. Contributory negligence on High’s part will always be a bar to recovery.

b. The manufacturer will avoid liability if it can show it followed the custom of the industry.

c. Privity will be a bar to recovery insofar as the wholesaler is concerned if the wholesaler did not have a reasonable opportunity to inspect.

d. High may recover even if he cannot show any negligence was involved.

A. (d) Under the theory of strict liability, the plaintiff must establish the following: (1) the seller was engaged in the business of selling the product, (2) the product was defective, (3) the defect was unreasonably dangerous to the plaintiff, and (4) the defect caused injury to the plaintiff. If the plaintiff can prove these elements, then the seller will be liable regardless of whether the seller was negligent or at fault for the defect. Thus, High can recover even if he cannot show any negligence was involved. Answer (a) is incorrect because contributory negligence is not an available defense in a strict liability case. Answer (b) is incorrect because the manufacturer’s only defenses are misuse and assumption of risk by the buyer. The fact that the manufacturer followed the custom of the industry is irrelevant under strict liability. Answer (c) is incorrect because privity of contract is not a defense under strict liability since the suit is not based on contract law.

Module 25

Q. A check is postdated to November 20 even though the check was written out on November 3 of the same year. Which of the following is correct under the Revised Article 3 of the Uniform Commercial Code?

a. The check is payable on demand on or after November 3 because part of the definition of a check is that it be payable on demand.

b. The check ceases to be demand paper and is payable on November 20.

c. The postdating destroys negotiability.

d. A bank that pays the check is automatically liable for early payment.

A. (b) Under the Revised Article 3, postdating a check does not destroy negotiability but makes the check properly payable on or after the date written on the check. Although the postdated check is not properly payable before the date on the instrument, if a bank pays it earlier, it is not liable unless the drawer had notified the bank that the check was postdated.

Module 26Q. Under the Revised UCC Secured Transaction Article, which of the following after-acquired property may be attached to a security agreement given to a secured lender?

Inventory Equipment

a. Yes Yes b. Yes No c. No Yes d. No No

A. (a) An after-acquired property clause in a security agreement allows the secured party’s interest in such property to attach once the debtor acquires the property, without the need to make a new security agreement. These clauses are typically used for inventory and accounts receivable, and can also be used for equipment.

Module 27

Q. Under the liquidation provisions of Chapter 7 of the Federal Bankruptcy Code, a debtor will be denied a discharge in bankruptcy if the debtor

a. Fails to list a creditor. b. Owes alimony and support payments. c. Cannot pay administration expenses. d. Refuses to satisfactorily explain a loss of assets.

A. (d) Improper actions during a bankruptcy that bar a discharge of all of the debts include concealing property and refusing to explain a loss of assets. Answer (a) is incorrect because this action means that this particular creditor’s claim will not be discharged but does not bar a general discharge of the other debts. Answer (b) is incorrect because although alimony and support payments are not

discharged themselves, their existence does not bar a general discharge. Answer (c) is incorrect because the

inability to pay does not bar a general discharge.

Module 28

Q. Under the law of suretyship, which are generally among the rights that the surety may use?

I. Subrogation. II. Exoneration. III. Reimbursement from debtor.

a. I only. b. III only. c. I and II only. d. I, II, and III.

A. (d) Upon payment, the surety obtains the right of subrogation which is the ability to use the same rights the creditor had. Also, the surety may resort to the right of exoneration by requiring the debtor to pay when s/he is able if the creditor has not demanded immediate payment directly from the surety. If the surety has paid the debtor’s obligation, the surety may attempt reimbursement from the debtor.

Module 29

Q. Able, as agent for Baker, an undisclosed principal, contracted with Safe to purchase an antique car. In payment, Able issued his personal check to Safe. Able could not cover the check but expected Baker to give him cash to deposit before the check was presented for payment. Baker did not do so and the check was dishonored. Baker’s identity became known to Safe. Safe may not recover from

a. Baker individually on the contract. b. Able individually on the contract. c. Baker individually on the check.

d. Able individually on the check.

A. (c) One who issues a personal check is liable on it; however, any party or principal who is not disclosed on the check is not liable on the negotiable instrument. Answers (a) and (b) are incorrect because the third party can elect to hold either the agent or the principal liable when the agent makes a contract for an undisclosed principal. Answer (d) is incorrect because the party who signs a check is liable on it.

Module 30

Q. The National Environmental Policy Act was passed to enhance and preserve the environment. Which of the following is not true?

a. The Act applies to all federal agencies. b. The Act requires that an environmental impact

statement be provided if any proposed federal legislation may significantly affect the environment.

c. Enforcement of the Act is primarily accomplished by litigation of persons who decide to challenge federal government decisions.

d. The Act provides generous tax breaks to those companies that help accomplish national environmental policy.

A. (d) The National Environmental Policy Act is centered around requiring the federal government and its agencies to consider the effects of its actions on the

environment. It does not provide tax breaks to companies to accomplish environmental goals. Answer (a) is not chosen because it correctly states that the Act applies to all federal agencies. Answer (b) is not chosen because it is also correct. The Act does require an environmental impact statement if the environment may be significantly hurt. Answer (c) is not chosen because private litigation is the main way this Act is enforced.

Module 31

Q. A method of transferring ownership of real property that most likely would be considered an arm’s-length transaction is transfer by

a. Inheritance. b. Eminent domain. c. Adverse possession. d. Sale.

A. (d) An arm’s-length transaction is a negotiation between unrelated parties acting in his/her interest. A way to test an arm’s-length transaction is to consider what a disinterested third party would pay for the property.

Answer (d) is correct because a sale involves the transfer of property for consideration in which a third party would generally negotiate and act in his/her interest. Answer (a) is incorrect because the property passes to a party as the decedent directs, subject to certain state limitations. Answer (b) is incorrect because eminent domain is the power of the government to take, with just compensation, private property for public use. Answer (c) is incorrect because adverse possession allows a person to gain title to real property if the person has continuously and openly occupied the land of another for a statutory period of time.

Module 33

Q. Under a “cafeteria plan” maintained by an employer, a. Participation must be restricted to employees, and

their spouses and minor children. b. At least three years of service are required before

an employee can participate in the plan. c. Participants may select their own menu of

benefits. d. Provision may be made for deferred compensation

other than 401(k) plans.

A. (c) The requirement is to determine the correct statement regarding a “cafeteria plan” maintained by an employer. Cafeteria plans are employer-sponsored benefit packages that offer employees a choice between taking cash and receiving qualified benefits (e.g., accident and health insurance, group-term life insurance, coverage under a dependent care or group legal services program). Thus, employees “may select their own menu of benefits.” If an employee chooses qualified benefits, they are excluded from the employee’s gross income to the extent allowed by law. If an employee chooses cash, it is includible in the employee’s gross income as compensation. Answer (a) is incorrect because participation is restricted to employees only. Answer (b) is incorrect because there is no minimum service requirement that must be met before an employee can participate in a plan. Answer (d) is incorrect because deferred compensation plans other than 401(k) plans are not included in the definition of a cafeteria plan.

Q. Which of the following costs is not included in inventory under the Uniform Capitalization rules for goods manufactured by the taxpayer?

a. Research. b. Warehousing costs. c. Quality control. d. Taxes excluding income taxes.

A. (a) The requirement is to determine which of the costs is not included in inventory under the Uniform Capitalization (UNICAP) rules for goods manufactured by a taxpayer. UNICAP rules require that specified overhead items must be included in inventory including factory repairs and maintenance, factory administration and officers’ salaries related to production, taxes (other than income taxes), the costs of quality control and inspection, current and past service costs of pension and profit-sharing plans, and service support such as purchasing, payroll, and warehousing costs. Nonmanufacturing costs such as selling,

advertising, and research and experimental costs are not required to be included in inventory.

Q. Under the modified accelerated cost recovery system (MACRS) of depreciation for property placed in service after 1986,

a. Used tangible depreciable property is excluded from the computation.

b. Salvage value is ignored for purposes of computing the MACRS deduction.

c. No type of straight-line depreciation is allowable. d. The recovery period for depreciable realty must be

at least 27.5 years.

A. (b) The requirement is to determine the correct statement regarding the modified accelerated cost recovery system (MACRS) of depreciation for property placed in service after 1986. Under MACRS, salvage value is completely ignored for purposes of computing the depreciation deduction, which results in the recovery of the entire cost of depreciable property. Answer (a) is incorrect because used tangible depreciable property is depreciated under MACRS. Answer (c) is incorrect because the cost of some depreciable realty must be depreciated using the straight-line method. Answer (d) is incorrect because the cost of some depreciable realty is included in the ten-year (e.g., single purpose agricultural and horticultural structures) and twenty-year (e.g., farm buildings) classes.

Q. Which one of the following is not included in determining the total support of a dependent?

a. Fair rental value of dependent’s lodging. b. Medical insurance premiums paid on behalf of the

dependent. c. Birthday presents given to the dependent. d. Nontaxable scholarship received by the depen-

dent.

A. (d) The requirement is to determine which item is not included in determining the total support of a dependent. Support includes food, clothing, FMV of lodging, medical, recreational, educational, and certain capital expenditures made on behalf of a dependent. Excluded from support is life insurance premiums, funeral expenses, nontaxable scholarships, and income and social security taxes paid from a dependent’s own income.

Module 34

Q. Murd Corporation, a domestic corporation, acquired a 90% interest in the Drum Company in 2005 for $30,000. During 2009, the stock of Drum was declared worthless. What type and amount of deduction should Murd take for 2009?

a. Long-term capital loss of $1,000. b. Long-term capital loss of $15,000. c. Ordinary loss of $30,000. d. Long-term capital loss of $30,000.

A. (c) Worthless securities generally receive capital loss treatment. However, if the loss is incurred by a corporation on its investment in an affiliated corporation (80% or more ownership), the loss is treated as an ordinary loss.

Q. Which one of the following would not be Sec. 1231 property even though held for more than twelve months?

a. Business inventory. b. Unimproved land used for business. c. Depreciable equipment used in a business. d. Depreciable real property used in a business.

A. (a) The requirement is to determine which item would not be characterized as Sec. 1231 property. Sec. 1231 property generally includes both depreciable and nondepreciable property used in a trade or business or held

for the production of income if held for more than twelve months. Specifically excluded from Sec. 1231 is inventory and property held for sale to customers, as well as accounts and notes receivable arising in the ordinary course of a trade or business.

Module 35

Q. Without obtaining prior approval from the IRS, a newly formed partnership may adopt

a. A taxable year which is the same as that used by one or more of its partners owning an aggregate interest of more than 50% in profits and capital.

b. A calendar year, only if it comprises a twelve-month period.

c. A January 31 year-end if it is a retail enterprise, and all of its principal partners are on a calendar year.

d. Any taxable year that it deems advisable to select.

A. (a) A newly formed partnership must adopt the same taxable year as is used by its partners owning a more than 50% interest in profits and capital. If partners owning more than 50% do not have the same taxable year, a partnership must adopt the same taxable year as used by all of its principal partners (i.e., partners with a 5% or more interest in capital and profits). If its principal partners have different taxable years, a partnership must adopt the tax year that results in the least aggregate deferral of income to partners.

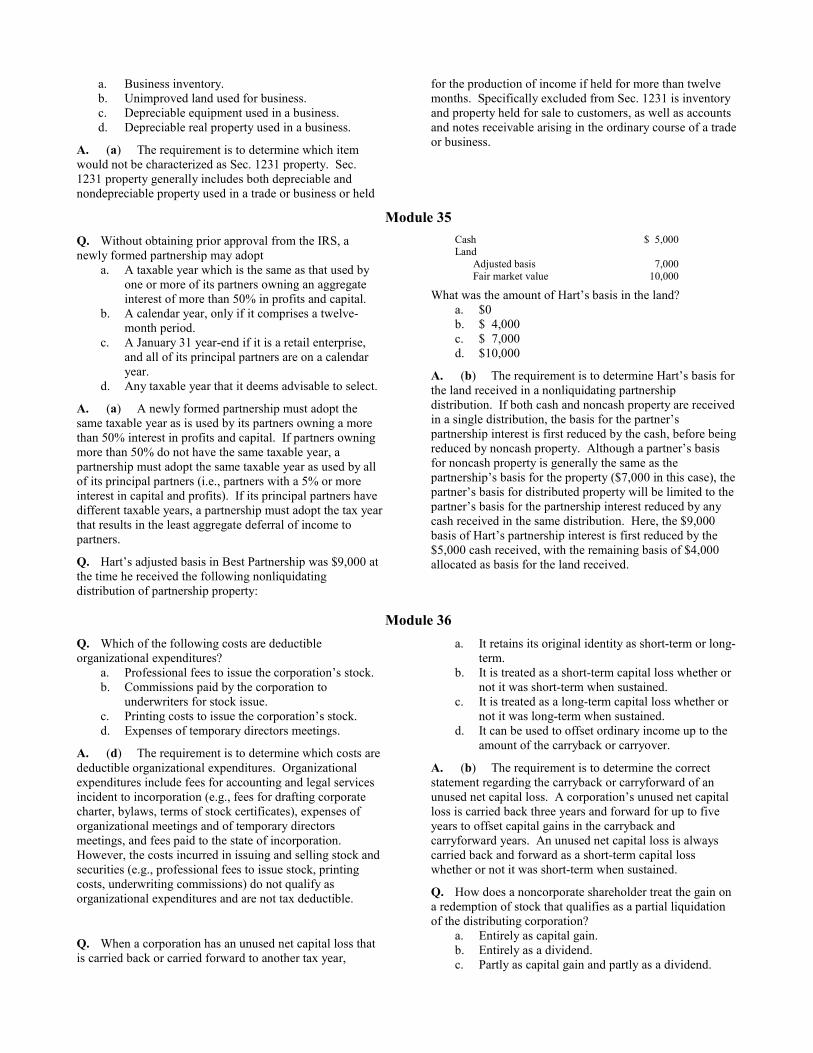

Q. Hart’s adjusted basis in Best Partnership was $9,000 at the time he received the following nonliquidating distribution of partnership property:

Cash $ 5,000 Land

Adjusted basis 7,000 Fair market value 10,000

What was the amount of Hart’s basis in the land? a. $0 b. $ 4,000 c. $ 7,000 d. $10,000

A. (b) The requirement is to determine Hart’s basis for the land received in a nonliquidating partnership distribution. If both cash and noncash property are received in a single distribution, the basis for the partner’s partnership interest is first reduced by the cash, before being reduced by noncash property. Although a partner’s basis for noncash property is generally the same as the partnership’s basis for the property ($7,000 in this case), the partner’s basis for distributed property will be limited to the partner’s basis for the partnership interest reduced by any cash received in the same distribution. Here, the $9,000 basis of Hart’s partnership interest is first reduced by the $5,000 cash received, with the remaining basis of $4,000 allocated as basis for the land received.

Module 36

Q. Which of the following costs are deductible organizational expenditures?

a. Professional fees to issue the corporation’s stock. b. Commissions paid by the corporation to

underwriters for stock issue. c. Printing costs to issue the corporation’s stock. d. Expenses of temporary directors meetings.

A. (d) The requirement is to determine which costs are deductible organizational expenditures. Organizational expenditures include fees for accounting and legal services incident to incorporation (e.g., fees for drafting corporate charter, bylaws, terms of stock certificates), expenses of organizational meetings and of temporary directors meetings, and fees paid to the state of incorporation. However, the costs incurred in issuing and selling stock and securities (e.g., professional fees to issue stock, printing costs, underwriting commissions) do not qualify as organizational expenditures and are not tax deductible.

Q. When a corporation has an unused net capital loss that is carried back or carried forward to another tax year,

a. It retains its original identity as short-term or long-term.

b. It is treated as a short-term capital loss whether or not it was short-term when sustained.

c. It is treated as a long-term capital loss whether or not it was long-term when sustained.

d. It can be used to offset ordinary income up to the amount of the carryback or carryover.

A. (b) The requirement is to determine the correct statement regarding the carryback or carryforward of an unused net capital loss. A corporation’s unused net capital loss is carried back three years and forward for up to five years to offset capital gains in the carryback and carryforward years. An unused net capital loss is always carried back and forward as a short-term capital loss whether or not it was short-term when sustained.

Q. How does a noncorporate shareholder treat the gain on a redemption of stock that qualifies as a partial liquidation of the distributing corporation?

a. Entirely as capital gain. b. Entirely as a dividend. c. Partly as capital gain and partly as a dividend.

d. As a tax-free transaction.