Why is Brazilian FDI so low? Victor Prochnik Institute of Economics/UFRJ.

25

Why is Brazilian FDI so low? Victor Prochnik Victor Prochnik Institute of Economics/UFRJ Institute of Economics/UFRJ

-

Upload

hillary-may -

Category

Documents

-

view

219 -

download

2

Transcript of Why is Brazilian FDI so low? Victor Prochnik Institute of Economics/UFRJ.

Why is Brazilian FDI so low?

Victor ProchnikVictor Prochnik

Institute of Economics/UFRJ Institute of Economics/UFRJ

Presentation items

•1 Statistics on Brazilian outward foreign direct investment (FDI)

•2 Home country effects of FDI

•3 Why is Brazilian FDI so low?

•4 Characteristics of Brazilian industrial firms

•5 Opportunity for comparative research

1 Statistics on Brazilian outward foreign direct

investment (FDI)

Participation (%) of FDI in the total investment (average 2001-

2003)

• Sweden 27.4

• France 22.0

• United Kingdom 19.0

• United States 6.6

• Germany 4.1

• Japan 3.2

•

• Singapore 36.3

• Hong Kong 28.2

• Taiwan 10.5

• Chile 7.4

• Malaysia 5.3

• India 1.0

• China 0.8

• Brazil 0.2

Outward FDI (UNCTAD data)1980

1990

1995 2000 2005 Annual

growth rate00/05

World (US $ bi) 571 1,791

2,949 6,471 10,672

10.5

BRICS (US $ bi) 44 72 167 521 748 7.5

Brazil (US $ bi) 39 41 44 52 72 6.7

LDCs (%) 12.5 8.2 11.3 13.2 11.9

BRICS/world (%)

7.8 4.0 5.7 8.0 7.0

Brazil/world (%) 6.7 2.3 1.5 0.8 0.7

Brazil/LDCs (%) 7.7 2.5 1.7 0.9 0.8

Brazil/BRICS (%)

87.0 56.7 26.7 10.0 9.6

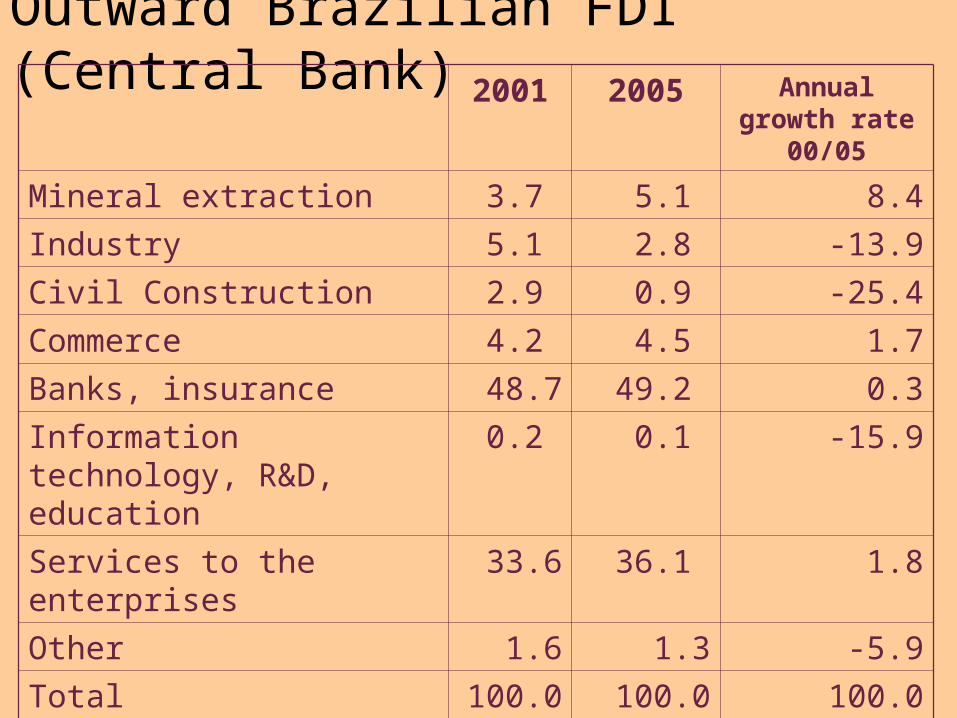

Outward Brazilian FDI (Central Bank) 2001 2005 Annual

growth rate 00/05

Mineral extraction 3.7 5.1 8.4

Industry 5.1 2.8 -13.9

Civil Construction 2.9 0.9 -25.4

Commerce 4.2 4.5 1.7

Banks, insurance 48.7 49.2 0.3

Information technology, R&D, education

0.2 0.1 -15.9

Services to the enterprises

33.6 36.1 1.8

Other 1.6 1.3 -5.9

Total 100.0 100.0 100.0

Total (US $ bi) 42,6 65,4 11,3

2 Home country effects of FDI

(a survey of the international literature)

2.1 The effect of FDI on home output and employment:

•EXPORTS: an increase in foreign affiliate sales is tipically associated with na increase in export by the home operations.

•EMPLOYMENT: in the short run, there is evidence of substitution between home and foreign labour. But in the long run they are complementary.

2.2 The effect of FDI on home skills:

•Headquarters activities are more skill intensive than production

•The rellocation of activities contributes to skill upgrading of home activities

2.3 Technological sourcing

•Findings: a coutry’s productivity is increased by outward investments when it invests in R&D-intensive countries

2.4 Productivity

• Investing abroad enhances the productivity path of investing firms, which gets steeper after the investment, compared with the path of non-investing firms.

3 Why is Brazilian FDI so low? – a survey of the literature

Export structure (intensive in commodities)

•Export products are homogeneous and do not need producers’ support on target markets.

•Differentiated products are exported primarily by subsidiaries of multinationals, whose external logistics make foreign investment unnecessary.

The targeted markets

•The size of the national market, as long as it ‘fulfills the company’s objectives’ (stronger for smaller companies).

• Insufficient scale to compete evenly with international players.

•Low share of exports in national firms’ overall sales

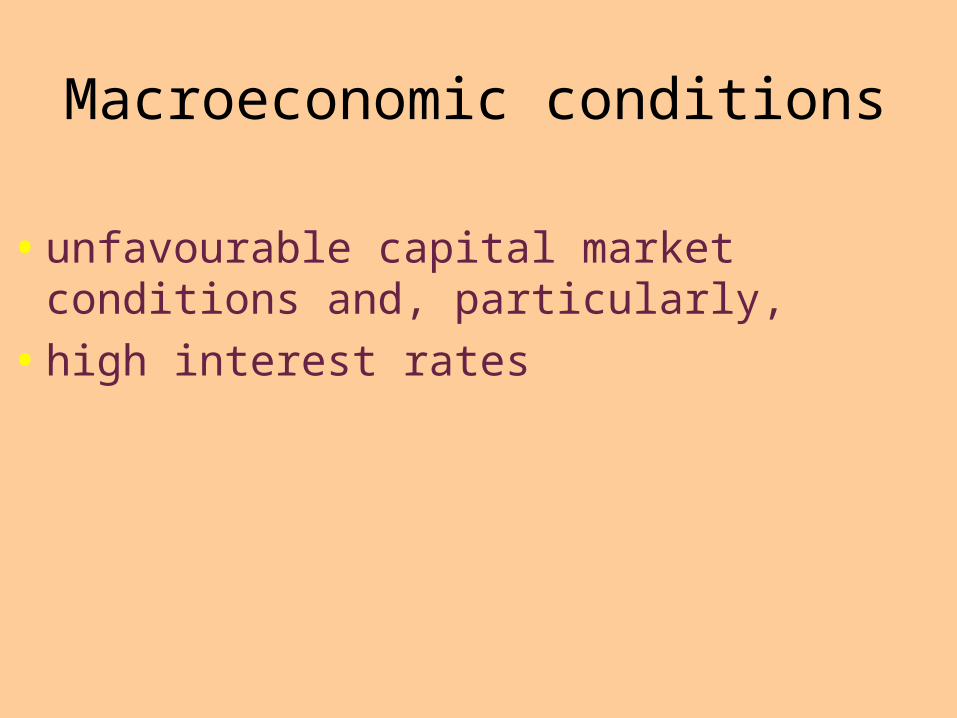

Macroeconomic conditions

•unfavourable capital market conditions and, particularly,

•high interest rates

Geographic and cultural factors

•Brazil is distant from the areas in which the main trade flows occur,

•There is a widespread perception of cultural distance (less important in relation to the other South America countries),

•Portuguese is spoken by a relatively small part of world population.

Future trends:

• It is expected a sharp growth in the internationalization of Brazilian firms

•Motives for internationalization (results of a recent study – 2006):

1 Profit and growth opportunities in the international markets2 To reduce dependence on domestic market

Characteristics of Brazilian industrial firms according to the internationalization

index

1 Internationalization index

• ‘DOM firms’ – Brazilian capital firms that sell only to the national market

• ‘EXP firms’ - Brazilian capital firms that only export

• ‘INV firms’ - Brazilian capital firms that export and engage in foreign direct investment (FDI)

Brazilian capital industrial firms 1

DOM firms2000

EXPFirms2000

INVFirms2000

DOM firms2003

EXPFirms2003

INVFirms2003

# of firms 66,735

2,862 19171,12

510,92

9213

Employees40.9

351.3

1,946

33.4204.6

2,184

Productivity 0.06 0.09 0.32 0.06 0.14 0.48

Sales2.3 31.8

613.4

2.1 28.01,037

Brazilian capital industrial firms 2DOM firms2000

EXPFirms2000

INVFirms2000

DOM firms2003

EXPFirms2003

INVFirms2003

Mean em-ployment time

34.7 43.2 67.8 35.6 45.2 69.6

Mean years schooling 7.0 7.5 9.1 7.6 8.1 9.6

Age of the firm 32.0 32.1 33.2 13.7 23.7 34.7

Brazilian capital industrial firms 3

DOM firms2000

EXPFirms2000

INVfirms2000

DOM firms2003

EXPFirms2003

INVFirms2003

R&D expen-ditures

7.9 155 5,694 76.3 354 12,339

Employees R&D

0.3 3.5 46.1 0.1 1.3 44.1

No. Masters and PhDs

0.009

0.1 5.20.00

70.08

04.1

% Employees in R&D

0.007

0.01 0.020.00

30.00

60.02

% of Braz. Cap. industrial firms 4

DOM firms2000

EXPFirms2000

INVfirms2000

DOM firms2003

EXPFirms2003

INVFirms2003

new to the firm product innovation

12.5128.2

420.4

213.18 17.1 23.8

new to the market product innovation

2.7814.6

139.2

73.37 1.9 6.7

new to the firm product innovation

21.4940.8

234.0

322.32 24.7 34.7

new to the market process innovation

1.76 9.9636.13

2.19 0.7 2.8

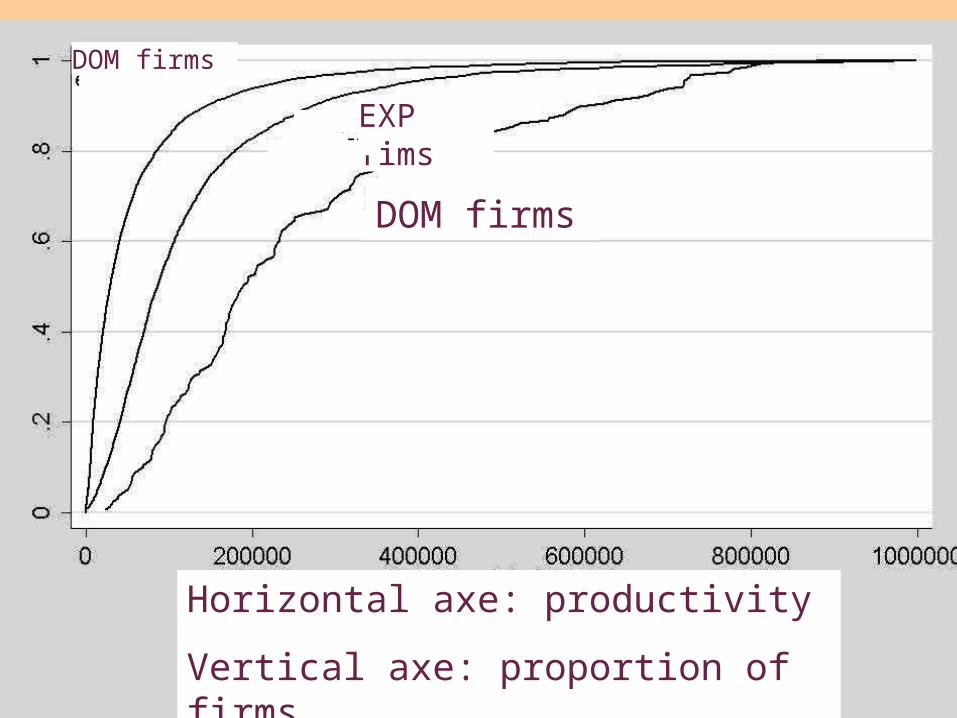

DOM firms

EXP fims

DOM firms

Horizontal axe: productivity

Vertical axe: proportion of firms

5 Opportunity for comparative research

•Study of a small sample of leader firms from the same economic sectors,

•Emphasis on comparability.•Main topics:

Growth dynamicsCompetitiveness, organizational structureGeographical diversificationProduct diversification