![No Detriment Policy [V70 Published 9 June 2020] · No Detriment Policy [V7.0 Published 9 June 2020] Overview No Detriment Policy: to be applied in place of standard regulations on](https://static.fdocuments.in/doc/165x107/5f0b6ef87e708231d4307efd/no-detriment-policy-v70-published-9-june-2020-no-detriment-policy-v70-published.jpg)

Who gets the money? Troy Smith Financial dependency Nomination of beneficiaries Insurance in super...

37

-

Upload

nigel-leonard -

Category

Documents

-

view

214 -

download

0

Transcript of Who gets the money? Troy Smith Financial dependency Nomination of beneficiaries Insurance in super...

Who gets the money?

Troy Smith

Financial dependency

Nomination of beneficiaries

Insurance in super strategy

Anti-detriment vs recycle strategy

Agenda

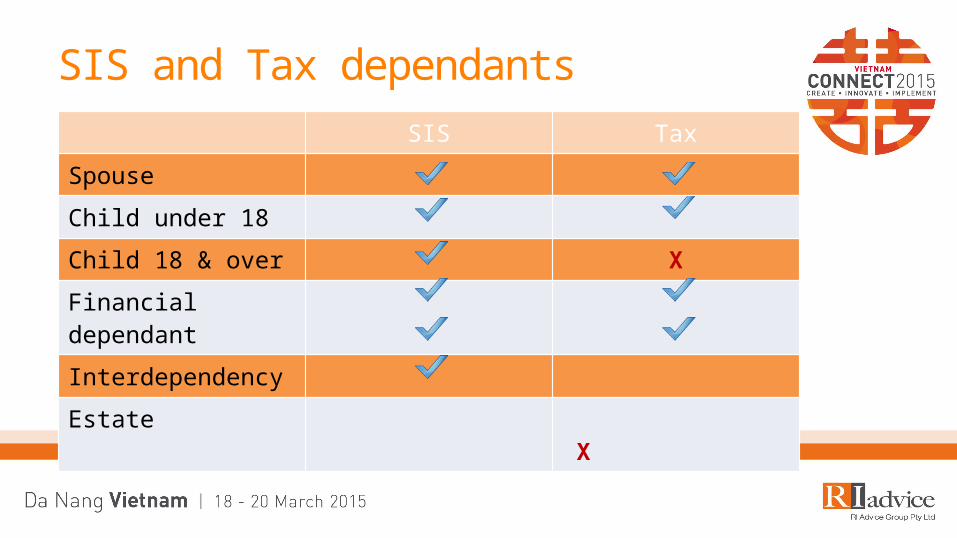

SIS and Tax dependantsSIS Tax

Spouse

Child under 18

Child 18 & over X

Financial dependant

Interdependency

Estate X

What is it?

Real time voting system

Provides direct feedback

How does it work?

Vote by pressing button

Voting is open for a limited time

Able to alter vote, whilst voting is open

CLiKAPA

• Financial dependency (ATO ID 2014/22)• Client is caring for their terminally ill parent• Client is able 18 years of age• Client gave up work, and doesn’t receive any financial

support from anyone, other than the parent• A death benefit is paid

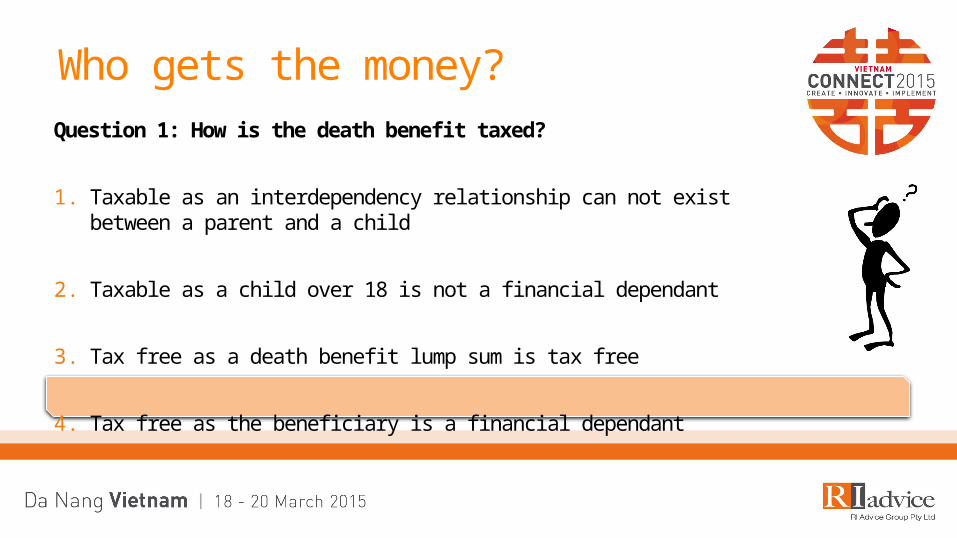

Who gets the money?

Question 1: How is the death benefit taxed?

1. Taxable as an interdependency relationship can not exist between a parent and a child

2. Taxable as a child over 18 is not a financial dependant

3. Tax free as a death benefit lump sum is tax free

4. Tax free as the beneficiary is a financial dependant

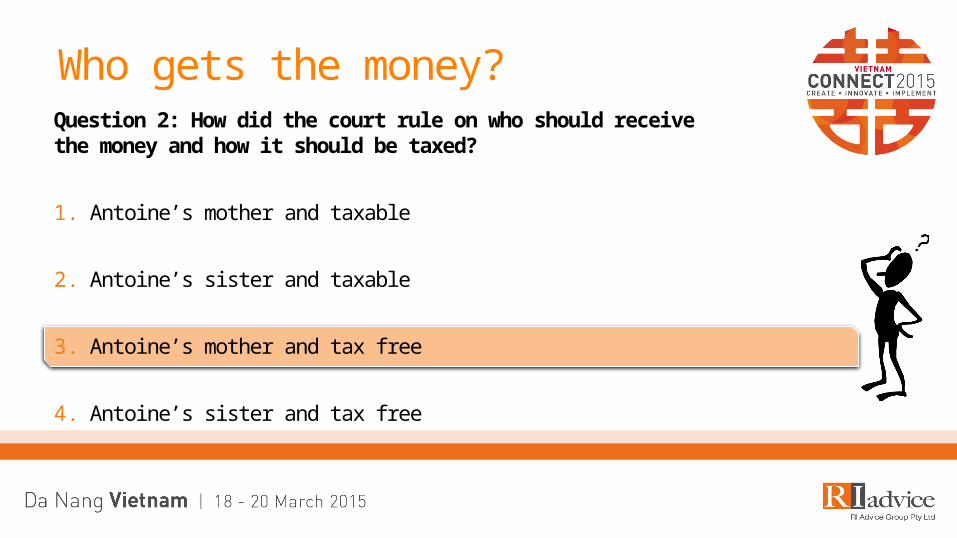

Who gets the money?

Who is a financial dependant?• Malek v FC of T 99ATC 2294

• Son, Antoine Malek (age 25) and mother Mary (widowed) lived together

• Antoine had a sister who did not live with them

• Mary suffered from a number of illnesses

• Antoine contributed towards the household bills

• Antoine passed away leaving a death benefit of $157,384

Who gets the money?

Question 2: How did the court rule on who should receive the money and how it should be taxed?

1. Antoine’s mother and taxable

2. Antoine’s sister and taxable

3. Antoine’s mother and tax free

4. Antoine’s sister and tax free

Who gets the money?

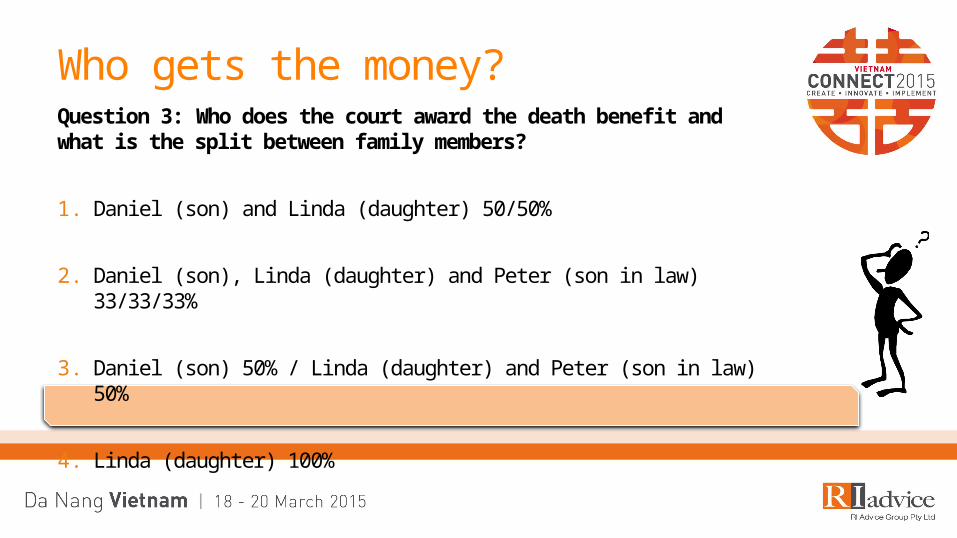

Katz vs Grossman [2005] NSWSC 934

Who gets the money?

SMSF

Katz vs Grossman [2005] NSWSC 934

Who gets the money?

SMSF

Katz vs Grossman [2005] NSWSC 934

Who gets the money?

SMSF

Question 3: Who does the court award the death benefit and what is the split between family members?

1. Daniel (son) and Linda (daughter) 50/50%

2. Daniel (son), Linda (daughter) and Peter (son in law) 33/33/33%

3. Daniel (son) 50% / Linda (daughter) and Peter (son in law) 50%

4. Linda (daughter) 100%

Who gets the money?

Who gets the money?

Super fund(Billy)

Super fund(Wendy)

Question 4: Who receives the death benefit lump sum payment? Billy is 43 years old and Wendy is 39 years old.

1. Billy receives Wendy’s super. Wendy receives Billy’s super.

2. Billy’s estate receives Wendy’s super. Wendy’s estate receives Billy’s super

3. Billy’s estate retains Billy’s super, as it can’t be paid to Wendy. Billy’s estate receives Wendy’s super.

4. Wendy’s estate receives Billy’s super. Wendy’s estate retains Wendy’s super as it can’t be paid to Billy.

5. Billy’s estate retains Billy’s super, as it can’t be paid to Wendy. Wendy’s estate retains Wendy’s super as it can’t be paid to Billy.

Who gets the money?

• Non-lapsing binding nominations

• Binding nominations only to SIS dependants

• Outside SIS dependant – binding nomination to the estate

• Reversionary pension

• Continuation of existing pension

• Lapsing binding nominations

• Renewed every 3 years

Death benefit nominations

Two questions to ask:

1. Who is receiving the lump sum death benefit?• - Definition of a tax dependant

2. What are the taxation components?- Underlying components- Effect of insurance proceeds

Taxation of a lump sum benefit

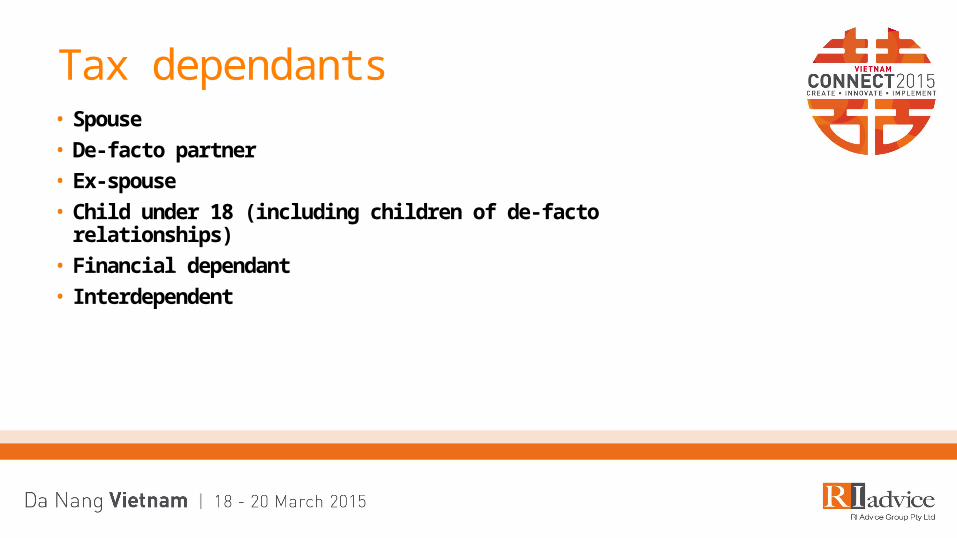

• Spouse

• De-facto partner

• Ex-spouse

• Child under 18 (including children of de-facto relationships)

• Financial dependant

• Interdependent

Tax dependants

• Tax dependent

• Tax free component: Tax free

• Taxable component (element taxed): Tax free

• Taxable component (element untaxed): Tax free

• Non-dependent for tax

• Tax free component: Tax free

• Taxable component (element taxed): 17%

• Taxable component (element untaxed): 32%

Taxation of a lump sum death benefit

Death benefit (with insurance)

Super fund uses formula:

Untaxed element = (super balance – taxed element)

Superannuation balance

service days x--------------------------------------------

service days + days to retirement

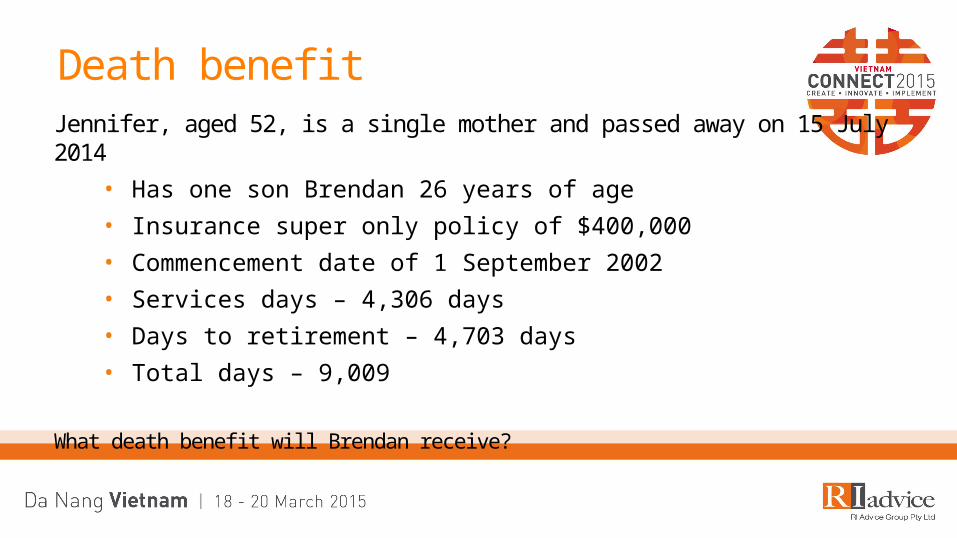

Jennifer, aged 52, is a single mother and passed away on 15 July 2014

• Has one son Brendan 26 years of age

• Insurance super only policy of $400,000

• Commencement date of 1 September 2002

• Services days – 4,306 days

• Days to retirement – 4,703 days

• Total days – 9,009

What death benefit will Brendan receive?

Death benefit

Death benefitFormula Component

Taxed element $400,000 x (4,306 / 9,009)

$191,187

Untaxed element $400,000 - $191,187 $208,813

Tax payable

Taxed element $191,187 x 17% $32,502

Untaxed element $208,813 x 32% $66,820

Total tax $32,502 + $66,820 $99,322

Net benefit $400,000 - $99,322 $300,678

Jennifer also had an accumulation super account

• Taxable $150,000

• Plus insurance policy of $400,000

Two options:

• 1. Accumulation fund inclusive of insurance

• 2. Separate accumulation fund and super based insurance

Jennifer’s Options

Option 1: Accumulation + InsuranceFormula Component

Taxed element $550,000 x (4,306 / 9,009) $262,882

Untaxed element $550,000 - $262,882 $287,118

Tax payable

Taxed element $262,882 x 17% $44,690

Untaxed element $287,118 x 32% $91,878

Total tax $44,690 + $91,878 $136,568

Net benefit $550,000 - $136,568 $413,432

Option 2: Accumulation and Insurance

Accumulation account

Component Tax payable Net benefit

Taxable component $150,000 x 17% $25,500

Net proceeds $150,000 - $25,500 $124,500

Accumulation account

$124,500

Insurance only super fund $300,678

Combined benefit

$425,178

The outcome: Option 1 vs Option 2

Option 1 – Accumulation +

insurance$413,432

Option 2 – Accumulation and

insurance separate $425,178

Difference $11,746 Option 2 gives a better

result

Question 5: In 1988 Paul Keating revolutionises the super system and introduces tax on contributions going into super. Realising this might impact politician's super he allows the tax to be reimbursed upon death. Who can receive an anti-detriment payment?

1. Spouse

2. Child of any age

3. Grandparent

4. A and B

Who gets the money?

What is it?

• Refund of contributions tax

• Death benefits should not be disadvantaged

• Fund can claim a tax deduction

Who qualifies?

• Spouse (including former spouse)

• Child (any age)• Payable to an estate if end beneficiary is spouse or child

• Only payable on lump sums

Anti-detriment

How is an anti-detriment calculated?

• An approved formula (most funds use)

• R – service period after 30 June 1983• P – no of days in R after 30 June 1988• C – taxable component

Question 6: What is the maximum percentage that a super death benefit will increase when the anti-detriment is added?

1. 12.53%

2. 15%

3. 17.647%

4. 21.56%

Anti-detriment payments

Sally passed away on 1 October 2014, super balance of $100,000 and service period start date is 01/01/2002

Calculating anti-detriment payment

Spouse

Super benefit $100,000

Anti-detriment $17,647

Total payment $117,647

Tax $0

Net benefit $117,647

Adult child

$100,000

$17,647

$117,647

$20,000

$97,647

Via Estate

$100,000

$17,647

$117,647

$17,647

$100,000

• Recycle strategy?

• Client who has met a condition of release

• Withdraws a lump sum

• Use low rate cap - $185,000 (2014/15)

• Recontribute as non-concessional within cap

• Forms part of tax free component

• Estate planning purposes and people aged 55 – 59 drawing an account based pension

• Reduces taxable component and increases tax free

Anti-detriment vs recycle strategy

• Sally passed away on 1 October 2014

• Superannuation balance of $100,000 (all taxable)

• Service period start date is 01/01/2002

• Death benefit going to only adult child, Jessica

• Benefit payable with an anti-detriment payment is $97,647

• Benefit payable with a re-contribution strategy is $100,000

Remember Sally?

Remember Sally?Super balance

Anti-detriment

Recycle strategy

$100,000 $97,647 $100,000

$200,000 $195,294 $197,450

$300,000 $292,941 $280,450

$400,000 $390,588 $363,450

$500,000 $488,235 $446,450

• Who can receive super death benefits?

• Tax treatment of death benefits

• Implication of insurance in super

• Anti-detriment payments v recycle strategy

Wrap-up