Where in the world are “permanently reinvested”...

44

Where in the world are “permanently reinvested” foreign earnings? Jennifer Blouin University of Pennsylvania Linda Krull † University of Oregon Leslie Robinson Dartmouth College January 2012 Abstract: This study uses permanently reinvested earnings (PRE) reported in U.S. multinational corporations (MNCs) financial statements, combined with detailed information on foreign affiliate assets to estimate the location and composition of PRE. We use these estimates to gain an understanding of the motivations for PRE designations, and thus implications of reported PRE for firms’ growth and liquidity, as well as the potential effects of U.S. tax reform. Our analysis suggests that PRE designations are driven by earnings incentives and growth – 94 percent of PRE is located in affiliates that would require recognition of an expected repatriation tax expense, and 60 percent of PRE is in high growth affiliates. While our estimates suggest that most PRE are associated with unrecognized repatriation tax obligations, the existence of some PRE in high tax jurisdictions reduces the potential tax revenue associated with PRE. We also find that, for firms in overall non-binding foreign tax credit positions, a significantly greater proportion of PRE in low-tax jurisdictions is held in cash, relative to high-tax jurisdictions, suggesting liquidity implications arising from the current tax system. † Corresponding Author: Lundquist College of Business, 1208 University of Oregon, Eugene, OR 97403 Phone: (541) 346-3252; email: [email protected] ________________________________________________________________________ The statistical analysis of firm-level data on U.S. multinational companies were conducted at the Bureau of Economic Analysis, Department of Commerce under arrangements that maintain legal confidentiality requirements. The views expressed in this study are those of the authors and do not reflect official positions of the U.S. Department of Commerce. The authors thank Dave Guenther, Mihir Desai (discussant), Allison Koester, Jake Thornock, members of the International Tax Policy Forum, and workshop participants at the National University of Singapore and the 2011 UBCOW conference, for helpful comments. For helpful discussions in the development of this paper, the authors thank eight partners in the national offices of Deloitte & Touche, Ernst & Young, PricewaterhouseCoopers, and KPMG. For financial support, the authors thank the International Tax Policy Forum, and Linda Krull thanks the Lundquist College of Business Finance and Securities Analysis Center.

-

Upload

doannguyet -

Category

Documents

-

view

217 -

download

1

Transcript of Where in the world are “permanently reinvested”...

Where in the world are “permanently reinvested” foreign earnings?

Jennifer Blouin University of Pennsylvania

Linda Krull†

University of Oregon

Leslie Robinson Dartmouth College

January 2012

Abstract: This study uses permanently reinvested earnings (PRE) reported in U.S. multinational corporations (MNCs) financial statements, combined with detailed information on foreign affiliate assets to estimate the location and composition of PRE. We use these estimates to gain an understanding of the motivations for PRE designations, and thus implications of reported PRE for firms’ growth and liquidity, as well as the potential effects of U.S. tax reform. Our analysis suggests that PRE designations are driven by earnings incentives and growth – 94 percent of PRE is located in affiliates that would require recognition of an expected repatriation tax expense, and 60 percent of PRE is in high growth affiliates. While our estimates suggest that most PRE are associated with unrecognized repatriation tax obligations, the existence of some PRE in high tax jurisdictions reduces the potential tax revenue associated with PRE. We also find that, for firms in overall non-binding foreign tax credit positions, a significantly greater proportion of PRE in low-tax jurisdictions is held in cash, relative to high-tax jurisdictions, suggesting liquidity implications arising from the current tax system.

† Corresponding Author:

Lundquist College of Business, 1208 University of Oregon, Eugene, OR 97403 Phone: (541) 346-3252; email: [email protected] ________________________________________________________________________ The statistical analysis of firm-level data on U.S. multinational companies were conducted at the Bureau of Economic Analysis, Department of Commerce under arrangements that maintain legal confidentiality requirements. The views expressed in this study are those of the authors and do not reflect official positions of the U.S. Department of Commerce. The authors thank Dave Guenther, Mihir Desai (discussant), Allison Koester, Jake Thornock, members of the International Tax Policy Forum, and workshop participants at the National University of Singapore and the 2011 UBCOW conference, for helpful comments. For helpful discussions in the development of this paper, the authors thank eight partners in the national offices of Deloitte & Touche, Ernst & Young, PricewaterhouseCoopers, and KPMG. For financial support, the authors thank the International Tax Policy Forum, and Linda Krull thanks the Lundquist College of Business Finance and Securities Analysis Center.

1

1. Introduction

The foreign operations of U.S. multinational corporations (MNCs) continue to generate

interest among investors and policymakers as these firms expand internationally. Investors’

interest arises from the need to assess the value and liquidity of these complex conglomerates.

Policymakers’ interest stems from the ongoing debate about changes to the U.S. international tax

system. However, current accounting standards require MNCs to report remarkably little detail

about their foreign operations. This lack of information presents a striking paradox: 89 percent of

S&P 500 firms operate outside the U.S. and, on average, report material subsidiaries in 19

countries and pre-tax foreign earnings equal to 31 percent of consolidated pre-tax earnings; yet

the only required information about foreign operations is aggregated pre-tax income, tax

expense, sales, long-lived assets, material subsidiary locations, and permanently reinvested

earnings (PRE).1,2

Much of the recent attention directed at MNCs’ overseas operations has focused on the

amount of PRE these firms report in their financial statements. PRE are foreign affiliate earnings

for which a firm has not recognized, in its consolidated financial statements, a residual U.S. tax

expense, if any, due upon repatriation of those earnings.3 MNCs must report the amount of PRE,

along with an estimate of the expected tax liability, in their financial statement footnotes. In

1 We determine that 89 percent of S&P 500 firms have foreign operations at the end of fiscal 2010 by examining whether these firms report foreign sales, foreign pre-tax earnings, or a material foreign subsidiary. Firms with profitable domestic, foreign, and total pre-tax earnings (60 percent of firms) report, on average, 31 percent and 49 percent foreign sales and pre-tax earnings, respectively. Securities and Exchange Commission (SEC) Regulation §210.4-08(h) requires firms to report total domestic and foreign pretax earnings. Financial Accounting Standards Board (FASB) ASC 280 – Segment Reporting (formerly SFAS 131) requires firms to report sales by geographic area. SEC Regulation S-K §229.601 requires firms to list material subsidiaries in Exhibit 21 of the 10-K. 2 MNCs are required to report sales and long-lived assets by geographic segment from a management perspective (i.e., how management organizes segments within the enterprise for making decisions and assessing performance). Hence, segment information is rarely reported by country but instead reported by region, which results in the financial information being difficult to compare across MNCs. 3 We use the terms ‘affiliate’ and ‘subsidiary’ interchangeably throughout the paper. If MNCs defer U.S. cash taxes on foreign affiliate earnings by reinvesting them abroad, they can also defer tax expense recognition for financial reporting if the earnings will remain outside the U.S. indefinitely. We discuss the PRE designation in Section 2.

2

2010, Credit Suisse began a series of reports on corporate taxes (Zion, Varshney, and Cornett

2010; Zion, Varshney, and Burnap 2011), documenting aggregate PRE for S&P 500 firms in the

amount of $1.3 trillion at the end of 2010. The authors describe PRE as “earnings parked

overseas that have so far avoided U.S. taxation” and speculate that high levels of PRE indicate a

less flexible balance sheet because it represents assets that cannot be deployed in the U.S.

without taking a tax hit. They estimate that these earnings are associated with a $360 billion

unrecognized tax liability.4

The Securities and Exchange Commission (SEC) has also begun scrutinizing firms’ PRE

assertions. Mark Shannon, an associate chief accountant in the SEC’s division of Corporate

Finance, reports that the SEC seeks to ensure “that companies are telling consistent stories about

offshore versus domestic liquidity” (Whitehouse 2011). In the context of a U.S. MNC’s liquidity

needs, the SEC is concerned that the disclosures lack details regarding what proportion of a

MNC’s cash is located overseas and the extent of the tax obligation that would be incurred upon

repatriation. Shannon notes that the SEC inquiries have yielded “a lot of revised disclosures.”

In light of the recent attention focused on PRE and foreign operations, the objective of our

study is to provide insight about what PRE represent. Using firms’ SEC 10-K disclosures of PRE

and confidential financial and operating data on MNCs’ foreign affiliates, we estimate the

motivations for designating foreign affiliate earnings as permanently reinvested, in what type of

assets PRE are held, and where they are located.5

First, we analyze attributes of affiliates that are associated with firms’ PRE assertions to

identify motivations for designating earnings as PRE. Existing studies conjecture that MNCs’

4 The authors estimate that the $1.3 trillion of PRE will be subject to a 28 percent repatriation tax rate in the U.S. using the median repatriation tax rate disclosed by 60 firms that provided such an estimate. 5 Confidential data are from legally mandated surveys of U.S. MNCs conducted by the U.S. Bureau of Economic Analysis. See Mataloni (2003) for a detailed discussion of BEA data.

3

designate foreign earnings as PRE when the incremental repatriation tax has a greater impact on

earnings (Graham, Hanlon, and Shevlin 2011; Blouin, Krull, and Robinson 2012). Therefore, we

investigate whether the presence of affiliates in tax havens and low foreign income tax or high

withholding tax jurisdictions is associated with higher levels of PRE. In addition, we consider

whether fluctuating currency exchange rates, which could lead to earnings volatility, and high

growth, which could increase the investment horizon, are associated with MNCs’ PRE levels.

Second, we examine the types of assets in which PRE are held. In particular, we investigate

the conjecture, illustrated in the Credit Suisse study, that PRE is held primarily in foreign cash

rather than investments in long-lived assets. This distinction is important because, if PRE is held

in non-liquid assets, then a repeal of tax laws that allow MNCs to defer U.S. tax on foreign

affiliate earnings until repatriation could cause firms to either sell productive assets or borrow to

avoid such a sale. Third, we study the location of PRE by estimating how much PRE is located in

specific countries. This analysis also allows us to estimate the tax cost of repatriating PRE held

in the form of liquid assets to the United States.

We note two important observations from our analysis. First, we find that a greater

proportion of PRE are located in affiliates operating in countries with either low income tax or

high withholding tax rates (94 percent), relative to affiliates in other countries (6 percent). Nearly

20 percent of PRE is located in ‘Big 7’ tax haven affiliates – those operating in Hong Kong,

Ireland, Lebanon, Liberia, Panama, Singapore and Switzerland. These results are concentrated in

firms that will owe U.S. tax on repatriations and suggest that most, but not all, PRE represent

foreign earnings that have a significant tax cost associated with repatriation to the United States.6

Second, we find that a non-trivial proportion of PRE appears to be held in cash; this proportion is

6 Note that we find a substantial proportion of PRE located in low income tax or high withholding tax jurisdictions even when controlling for growth and/or investment expectations.

4

particularly high in affiliates operating in low income tax or high withholding tax countries (38

percent), relative to those operating in other countries (1 percent). This result implies that U.S.

tax policy has a significant impact on the liquidity of MNCs. However, it also implies that over

half of PRE is held in non-liquid assets.

Our detailed examination of the location and composition of PRE makes two significant

contributions. First, our study helps investors identify and assess the relative importance of

various motivations for designating earnings as PRE, and thus better understand the implications

of PRE for firm value. In practice, a firm may designate earnings as PRE because a) it has no

intention of repatriating the foreign earnings to the U.S. in the foreseeable future, b) it does not

want to induce an undesirable financial statement effect, or c) it is too difficult to estimate the

residual tax liability. Each motivation has a different implication for the earnings potential of

those reinvested earnings, the size of the unrecognized tax cost associated with the repatriation of

those earnings, and/or the agency costs of underinvestment associated with those earnings.

Second, we help policy-makers better estimate the potential revenue impact of changes in

international tax policy. Press reports argue that PRE represents large pools of cash “parked” in

haven countries which represents a significant untapped source of tax revenue. This conjecture

assumes that deferral can be repealed without requiring firms to sell productive assets to pay

their tax obligations. Although some PRE is located in haven jurisdictions or in affiliates with

high levels of cash, our estimates also suggest that some PRE is located in affiliates with

significant operating assets and/or high-tax jurisdictions. By documenting the proportion of PRE

in these locations, we illustrate the need to be cautious when interpreting the effect of PRE on

firm liquidity and tax revenue. It is also important to note that undistributed earnings that are not

PRE also represent a potential source of tax revenue. Because PRE is an accounting construct,

5

firms’ actual tax cost associated with undistributed foreign earnings is not directly related to the

use, or lack thereof, of the PRE designation..

Section 2 provides a background and develops our hypotheses. Section 3 describes our data.

Section 4 describes our empirical specification. Section 5 discusses our main results and Section

6 concludes.

2. Background

The U.S. taxes MNCs’ foreign affiliate earnings when they repatriate the earnings to the U.S.

parent. The amount of tax due at the time of repatriation equals the dividend grossed-up for

foreign taxes paid times the U.S. statutory tax rate minus a foreign tax credit. Generally, the

foreign tax credit equals the amount of foreign income and withholding taxes paid on the

repatriated earnings up to the amount of the U.S. tax liability. If the foreign tax credit is greater

than the U.S. tax liability, the MNC owes no incremental tax on repatriation.7

Financial accounting rules require MNCs to recognize the expected U.S. income and foreign

withholding tax expense related to future repatriation of undistributed foreign earnings in the

period those earnings are generated (FAS 109). However, quantifying the expected U.S. tax on

undistributed earnings abroad is complex and requires estimates and assumptions that are

susceptible to error or manipulation.8

In light of this complexity, Accounting Principles Board Opinion No. 23 (hereafter APB 23)

creates an exception to the general rule described above. This exception (the Indefinite Reversal

Exception) is now defined in FASB ASC 740 - Income Taxes (ASC 740 and formerly FAS 109)

and allows firms to defer recognizing an expense for the expected tax consequences of

7 For simplicity, we ignore the anti-abuse rules generally referred to as Subpart F, which would result in incremental U.S. tax without actual repatriation. 8 http://www2.financialexecutives.org/news/finrep/letters/Dfdtax_Jun14.pdf (last accessed January 7, 2012)

6

repatriation if “sufficient evidence shows that the subsidiary has invested or will invest the

undistributed earnings indefinitely or that the earnings will be remitted in a tax-free liquidation”

(ASC 740-30-25-17).

The Indefinite Reversal Exception operates at the subsidiary level; i.e., a parent firm need not

assert that the undistributed earnings of all foreign affiliates are permanently reinvested to avoid

income tax expense recognition. It can apply the exception to some affiliates and not others. The

exception can also be applied to an affiliate using a year-by-year, or a dollar-by-dollar approach

(BNA 948).9

In addition, the Indefinite Reversal Exception is not an ‘election’ per se, but rather applies if

specific facts and circumstances suggest that the earnings will be reinvested outside the U.S.

indefinitely. The exception further states that:

“A parent entity shall have evidence of specific plans for reinvestment of undistributed earnings of a subsidiary which demonstrate that remittance of the earnings will be postponed indefinitely…Experience of the entities and definite future programs of operations and remittances are examples of the types of evidence required to substantiate the parent entity's representation of indefinite postponement of remittances from a subsidiary.” (ASC 740-30-25-17)

These criteria are sufficiently ambiguous such that identical facts and circumstances could

ultimately lead to different designations of PRE. Krull (2004) documents that PRE reflects

investment and tax incentives but, most notably, finds that amounts reported as PRE are also

used to manage earnings. Thus, an important unanswered question is the extent to which PRE

disclosures communicate relevant tax and investment information that can help investors

evaluate firm performance and liquidity given that firms designate PRE to manage financial

reporting outcomes.

9 The year-by-year approach means that a firm can change its PRE assertion related to undistributed subsidiary earnings from a prior period to the extent that facts change over time. The dollar-by-dollar approach means that a firm can assert a portion of a undistributed subsidiary earnings as PRE, while at the same time anticipating a future distribution of the remaining portion.

7

The facts and circumstances that underlie PRE designations are important to understand as

researchers and policymakers scrutinize PRE in the context of proposals on international tax

reform. Blouin et al. (2012) uses PRE to test whether unrecognized tax consequences of

repatriation in accounting earnings are an important factor in the repatriation decision on MNCs.

The authors’ approach makes an implicit assumption that PRE are primarily located in low tax

jurisdictions and that financial reporting outcomes are the primary factor considered when firms

designate PRE.10 Similar to Zion et al. (2011), Graham et al. (2011) uses PRE as a proxy for

foreign cash to examine the importance of expense deferral in explaining foreign cash.

Somewhat implicit these studies is the notion that PRE represents untaxed earnings, held in the

form of liquid assets, that are available to be immediately repatriated to the U.S.

However, the ability of PRE to aid in evaluating either micro- or macro-level effects of

proposed tax reform depends on the underlying reasons that firms designate PRE. Mott and

Schmidt (2011) scrutinizes recent disclosures of foreign cash and PRE in a sample of 258 firms,

noting that foreign cash balances are, on average, 68 percent of the amount disclosed as PRE and

that there is significant variation across firms. Noting high levels of PRE in recent years,

Graham, Raedy, and Shackelford (2011) conjecture that, conditional on another anticipated tax

holiday, this build-up of PRE may reflect the fact that the American Jobs Creation Act of 2004

(AJCA) used PRE as a factor in determining the amount of dividends that were eligible for the

reduced tax rate. Our study strives to better understand the underlying motivations for

designating PRE to help researchers and policymakers better interpret this accounting figure.

It is important to emphasize that PRE is an accounting, not a tax construct. Specifically, PRE

only affects the timing of expense recognition in the financial statements. It does not affect the

10 Recognizing that other interpretations of PRE, and thus their results, are possible, the authors use alternative measures that do not rely on PRE disclosures and find consistent results.

8

amount or timing of actual tax payments. Moreover, PRE represents more than just undistributed

foreign earnings. The Indefinite Reversal Exception applies broadly to temporary differences

between the tax basis and the financial reporting basis of an investment in the stock of a foreign

affiliate (i.e., an outside basis difference).11 Undistributed earnings of a foreign affiliate increase

the book basis of the shares of the affiliate in the hands of the domestic parent and is the most

common item giving rise to outside basis differences. Other items can give rise to outside basis

differences. For example, the book and tax basis of shares in a newly acquired foreign target

often differ, creating an outside basis difference.12 Because undistributed earnings is the most

common item giving rise to outside basis differences, we refer to amounts for which the firm has

invoked the Indefinite Reversal Exception as permanently reinvested earnings, or PRE.

3. Sample selection and data

We select our sample of U.S. incorporated firms with publicly traded equity from among all

firms appearing in Compustat at any point from 1997 through 2010 (excluding REITs, banks,

and insurance companies). To remain in our sample we require significant foreign operations,

defined as any firm reporting foreign income tax expense (TXTO) exceeding $1 million (in

absolute value) in any single year during that time period. When a firm avails itself of the

Indefinite Reversal Exception, it is required to report in its financial statements the dollar amount

of outside basis differences for which no expected tax consequences of repatriation are

recognized, as well as an estimate of the unrecognized tax liability. The amount of PRE reported

in a firm’s SEC 10-K is cumulative over time and aggregated across all foreign affiliates. We use

11 APB 23 was issued in 1972 and was significantly modified by paragraph 31 of FAS 109. Specifically, FAS 109 expanded the scope of the exception under APB 23. While APB 23 provided an exception only for undistributed foreign earnings of subsidies, FAS 109 provides an exception for all outside basis differences that a domestic parent may have with respect to is shares of a foreign subsidiary. 12 Other transactions that create outside basis differences include share issuances to unrelated investors, subpart F inclusions, stock options, and cumulative translation adjustments (BNA 948, PWC 2010).

9

a text search program to scan 10-K filings of 1,309 firms (13,177 firm-years) that meet our

criteria for disclosures of PRE, using variations on the following search terms: “permanently

reinvested”, “indefinitely reinvested”, “undistributed”, and “unremitted” foreign earnings.13

We combine our PRE data described above with affiliate-level data obtained from the Annual

(Benchmark) Survey of U.S. Direct Investment Abroad conducted by the Bureau of Economic

Analysis (BEA) each year since 1982. Federal law obligates U.S. MNCs to report certain

financial and operating data for both domestic and foreign operations to the BEA. A U.S. MNC

is the combination of a single U.S. entity, called the U.S. parent, and at least one foreign affiliate

in which the U.S. parent holds, directly or indirectly, a 10 percent interest. The amount of data

collected by the BEA varies by year and depends on whether the affiliate meets the applicable

reporting threshold; reporting thresholds in benchmark years (i.e., 1999, 2004) are lower so more

affiliates are required to report.14

In some instances, U.S. MNCs’ ownership structures include tiered ownership (i.e., where

affiliates are owned by other affiliates either instead of, or in conjunction with, the U.S. parent).

To study the location and composition of PRE, we focus on the financial position of the lower-

tier entities and do not attribute the financial positions of a lower-tier entity to its owner. For

instance, when an affiliate is directly (partially or wholly) owned by another affiliate, the assets

of the lower-tier entity are considered in our analysis and the proportion of the upper-tier entity’s

assets attributable to the lower-tier entity are removed from the upper-tier. The BEA data

13 We confirm the accuracy of our dataset constructed using a text search by comparing the PRE amounts to a hand-collected dataset of PRE (from a prior study) consisting of 475 MNCs (3,376 firm-years). There are no differences in PRE across the two datasets. 14 In order to reduce the reporting burden, the BEA requires affiliates to participate if its assets, sales, or net income (loss) exceed $7 million in 1999, $30 million in 2000-2003, $10 million in 2004, and $40 million in 2005-2008. During 2000-2003, and 2005-2008 (i.e., non-benchmark years), most of the financial and operating data that we observe for smaller affiliates not required to participate in the survey is estimated by the BEA.

10

provides information on ownership structures, as well as investment in and income from

affiliates that allow us to make these adjustments.

To conduct our analyses, we also aggregate affiliate-level BEA data to the firm-level. U.S.

MNCs report to the BEA on a fiscal year basis and follow U.S. Generally Accepted Accounting

Principles (GAAP), with the exception of consolidation rules. The BEA requires that the U.S.

MNC use the equity method of accounting for equity investments of more than 50 percent,

whereas GAAP requires consolidation. Thus, to avoid double-counting assets in the

consolidation process, we eliminate intercompany assets in computing worldwide assets.15

When we match our Compustat data with BEA data, this yields a final sample of 917 firms

(5,992 firm-years). In this sample, we find no disclosure regarding PRE in 1,337 firm-years and

thus, do not include these firm-years in our multivariate analysis. The final sample for our study

is an unbalanced panel of 4,655 firm-years (748 firms) from 1998 through 2008. Our 748 MNCs

represent 100,003 affiliate-years.

4. Empirical design

We test for evidence of various motivations for declaring undistributed earnings as PRE by

estimating the following empirical equation at the firm level for our sample of 4,655 firm-years

from 1998 to 2008:

PREi,t = α0 + α1Total Foreign Assetsi,t + α2Characteristic Foreign Assetsi,t + ΣαkYeark + εi,t (1)

15 For example, under the equity method of accounting used for BEA reporting, the total assets of the domestic operation will include the ‘net assets’ or equity investment in all foreign affiliates. Thus, a measure of worldwide assets necessitates that we remove the investment in foreign affiliates from domestic assets, and instead include aggregate total assets of foreign affiliates with domestic assets. This mimics the result that would be achieved if the U.S. MNCs assets were consolidated under GAAP. Total assets computed using BEA data and total assets in Compustat are highly correlated (p = 0.998).

11

Where PRE equals the amount of permanently reinvested earnings reported in a firm’s SEC

10-K filing, Total Foreign Assets equals a firm’s total assets in all foreign affiliates,

Characteristic Foreign Assets equals a firm’s total assets in foreign affiliates with the

characteristic of interest, Year represents year fixed effects, and i and t represent firm and year

subscripts, respectively.16 All continuous variables are scaled by worldwide assets.17

We examine four affiliate characteristics which we describe in more detail in Sections 4.1 to

4.4: tax status, haven status, currency volatility, and growth. The coefficients in Equation (1)

estimate the increase in PRE as assets in affiliates with these characteristics increase. For

example, when we examine tax status, Characteristic Foreign Assets equals a firm’s total assets

in foreign affiliates that would generate a tax liability upon repatriation of earnings (i.e., affiliates

with tax due), either in the form of a residual U.S. income tax, a foreign withholding tax, or both.

In this case, α1 in Equation (1) represents the change in PRE as assets in affiliates with no tax

due increases by one dollar, and α2 represents the change in PRE per dollar of assets in affiliates

with tax due, incremental to the change per dollar of assets in affiliates with no tax due. The total

change in PRE per dollar of assets in affiliates with tax due is represented by α1 + α2.

As noted above, we cannot observe the amount of PRE in each affiliate. Therefore, we

interpret these coefficients as the average amount of PRE associated with assets in affiliates with

and without the characteristic of interest. 18

4.1. Affiliates anticipated having tax due upon repatriation

Several existing studies that investigate PRE focus on its earnings implications because

designating foreign subsidiary earnings as PRE will, in many cases, increase financial statement

16 Results of estimating Equation (1) are similar when we also include a control for size and indicator variables that correspond to parent industry. 17 Unless otherwise noted, all variables are computed using BEA data. 18 We also estimate the association between PRE and foreign equity and find consistent results.

12

earnings (Krull 2004; Blouin et al. 2012; Graham et al. 2011). However, the decision to

designate undistributed foreign earnings as PRE has financial reporting consequences only when,

in expectation, there is a tax consequence of repatriation. Said another way, a firm cannot

influence financial reporting outcomes with PRE designations unless the firm expects to pay

U.S. income taxes, foreign withholding taxes, or both, upon repatriation of foreign earnings.

Anecdotally, MNCs strongly favor the Indefinite Reversal Exception because it avails them of

the ability to consistently report higher earnings and lower effective tax rates, all else equal. A

tax director of a Fortune 500 firm described the Indefinite Reversal Exception like “crack, once

you start using it, it’s hard to stop.”

Because PRE designations only affect earnings when there is an expected repatriation tax

obligation, MNCs may implement a simple rule whereby they designate earnings as PRE when

there is an expected tax consequence to repatriation and do not designate earnings as PRE

otherwise.19 If this is the case, we would expect that PRE is located primarily in subsidiaries that

will generate a tax (income and/or withholding) obligation upon repatriation.

However, a lack of earnings implications does not preclude MNCs from designating earnings

in affiliates without a repatriation tax obligation as PRE. In fact, firms may designate earnings in

these affiliates as PRE for at least two reasons. First, MNCs often operate multiple affiliates as a

coordinated business because they operate in the same geographic region or product line; these

affiliates can be located in different countries and face a wide range of different foreign income

and withholding tax rates. In this case, firms will often reinvest earnings of affiliates without

19 This would be possible in a world where audit firms were not particularly stringent in their documentation requirements for firms invoking the Exception. Although there is no evidence on this, anecdotally, permanent reinvestment assertions are a top review issue for the PCAOB. AU Section 9326 was revised for audits of fiscal years beginning after December 15, 2010 to require that audit documentation include “support for applying the indefinite reversal criteria, including specific plans for reinvestment of undistributed foreign earnings.”

13

repatriation tax obligations concurrently with the earnings of affiliates with repatriation tax

obligations and make the permanent reinvestment assertion jointly for a group of affiliates.

Second, if a firm does not have intentions to repatriate the earnings of an affiliate with no

repatriation tax obligation, it incurs no financial reporting cost by designating its earnings as

PRE. While firms with multiple subsidiaries do have the ability to cross-credit; i.e. use high

taxed foreign earnings to offset low-taxed foreign earnings, cross-crediting does not necessarily

change the financial reporting outcome associated with the PRE designation.20 The expected tax

obligation generated upon repatriation of low taxed earnings requires recognition of a deferred

tax expense/liability, while the expected tax credit generated upon repatriation of high-taxed

earnings can only be recognized as a deferred tax benefit/asset if the firm has plans to repatriate

the earnings in the foreseeable future.21 Thus, the role of each affiliate’s tax status in the PRE

decision is unclear.

To investigate the role of affiliate tax status on PRE designations, we identify affiliates that

will owe taxes upon repatriation by estimating both U.S. repatriation taxes and foreign

withholding taxes. If an affiliate’s average income tax rate is less than 0.35, it will generate a

U.S. tax obligation upon repatriation. If an affiliate’s average income tax rate is greater than 0.35

and it has a positive withholding tax rate, it will generate a withholding tax obligation with no

corresponding foreign tax credit. For each firm, we sum assets in affiliates that face either an

20 If a MNC repatriates earnings from more than one country, it can use tax credits generated in high tax countries to offset taxes on repatriations from low-tax countries. Therefore, the incremental tax rate on repatriation can be thought of as the difference between the U.S. income tax rate and the average foreign income tax rate and withholding rate paid on repatriated earnings. 21 We thank our accounting firm contacts for discussing this issue with us at length. As outlined in paragraph 34 of FAS 109, a deferred tax asset (DTA) cannot be recognized on outside basis differences (e.g., undistributed earnings) unless the temporary difference will reverse in the “foreseeable future” (often interpreted in practice to mean within 12 months). Tax credits expected to be generated upon repatriation are often referred to in practice as ‘unborn foreign tax credits’ and this guidance is applied. Based on our discussions, the requirement to recognize a DTA is much more stringent than the requirement to recognize a deferred tax liability (DTL). A firm with both a high tax and low tax subsidiary that does not designate earnings as PRE would be required to recognize a DTL but not able to recognize a DTA unless it had specific plans to repatriate the high tax earnings within 12 months.

14

average income tax rate less than the U.S. statutory tax rate of 35 percent or an average income

tax rate greater than the U.S. statutory tax rate of 35 percent and a positive withholding tax rate.

We label this sum TaxDue Foreign Assets.22

4.2. Use of havens

Existing research documents that MNCs use tax planning strategies, such as tiered ownership

in low and high tax jurisdictions (Altshuler and Grubert, 2003) and investment in tax havens

(Dyreng and Lindsay, 2009 and Hines and Rice, 1994), to avoid or defer U.S. tax on foreign

affiliate earnings. Tax haven countries are a subset of low tax countries that provide companies

opportunities for tax avoidance. Therefore, investments in tax havens result in low-taxed foreign

earnings which will generally result in a U.S. tax liability when repatriated, and require an

estimate of the repatriation tax expense on the financial statements unless the firm invokes the

Indefinite Reversal Exception.

In addition, foreign affiliate earnings invested in tax havens to avoid or defer U.S. tax can

meet the technical definition of PRE under the Indefinite Reversal Exception, i.e. if based on past

experience funds invested in these strategies are not repatriated, the firm can justifiably make a

PRE assertion. Thus, we expect that tax planning strategies are another motivation for

designating foreign earnings as permanently reinvested and investigate the importance of tax

haven presence in PRE decisions.

We focus on what Hines and Rice (1994) distinguish as large tax havens termed the ‘Big 7’

havens.23 To study the effect of Big 7 haven subsidiaries on PRE designations we calculate the

22 We use the withholding rate that would be applicable between the affiliate and its direct owner. 23 Hines and Rice (1994) highlight that economies of tax havens differ considerably noting that the Big 7 havens – Hong Kong, Ireland, Lebanon, Liberia, Panama, Singapore and Switzerland – account for 80 percent of the tax haven population, 89 percent of tax haven GDP, and are the “locus of most physical activity undertaken by U.S. haven affiliates” (pg. 153). In Section 6.1, we consider ‘Dot’ havens – havens that have smaller economies.

15

sum of each firm’s assets in affiliates located in Big 7 tax havens and label this variable B7

Foreign Assets.

4.3. Currency volatility

Another factor that can affect PRE is foreign currency translation of the foreign tax credit.

Since many foreign affiliates of U.S. firms operate in foreign currencies, it is necessary to

translate dividend payments and foreign taxes paid into U.S. dollars to calculate U.S. repatriation

taxes. However, the dividend and the foreign tax credit are translated into U.S. dollars at

different points in time. The foreign tax credit is translated based on the exchange rate in effect

when the foreign taxes were paid (see Moore 2011). The dividend, however, is translated based

on spot rates in effect at the time of the repatriation. Therefore, fluctuation in currency rates

generates variation in repatriation tax obligations and any associated accounting expense

recognition. By designating undistributed foreign earnings as PRE, MNCs are able to mitigate

potential volatility in earnings attributable to the repatriation tax accrual.

However, Dodonova and Khoroshilov (2007) develop a model showing that firms facing

exchange rate volatility have incentives to repatriate income sooner. The authors model the

foreign currency translation of foreign tax credits as the U.S. government de facto holding

foreign currency put options against U.S. firms with foreign affiliates that, when combined with

exchange rate volatility, reduces their foreign after-tax rate of return.

To investigate the role of currency volatility on PRE designations, we define affiliates with

high currency volatility as those whose local (real) exchange rate volatility against the U.S.

dollar over the previous 12 months is greater than the median for all affiliates.24 We define FX

Foreign Assets as total assets in affiliates with high foreign currency volatility.

4.4. Growth opportunities 24 We obtain exchange rate data from Global Financial Data at https://www.globalfinancialdata.com .

16

The criteria for designating earnings as PRE state that MNCs must have sufficient evidence

“that the subsidiary has invested or will invest the undistributed earnings indefinitely or that the

earnings will be remitted in a tax-free liquidation.” MNCs can use their past experience,

forecasted future operations, and repatriation patterns as evidence to support a PRE assertion

with respect to foreign earnings. In addition, existing research finds that U.S. investment abroad

is increasing in expected growth (e.g., Desai, Foley, and Hines 2007), and that firms will reinvest

abroad, rather than repatriate to the U.S., when the foreign after-tax return is greater than the

domestic after-tax return (Hartman 1985). This research suggests that MNCs will reinvest more

in affiliates with higher growth. As growth increases, the expected length of their investment

likely increases as well, improving the MNCs ability to make a PRE assertion. Thus, we

investigate whether growth opportunities are an important motivation for designating foreign

affiliate earnings as PRE.

To investigate the effect of growth on PRE designations, we define high growth affiliates as

those with total investment in R&D and capital expenditures greater than the median for all

subsidiaries in year t. For each firm, we calculate GR Assets as total assets in high growth

affiliates.

5. Results

5.1 Descriptive statistics

In Table 1 Panel A we present descriptive statistics on the sample that we use in our analysis

as well as the 1,337 zero-PRE MNC observations noted in Section 3. MNCs that report PRE

greater than zero are significantly larger, and have significantly greater foreign assets as a

fraction of total assets than firms with no PRE. The estimated repatriation tax rate (which is the

estimated cash outflow firms would incur upon repatriation) for firms with PRE is significantly

17

lower than the rate on zero-PRE firms, which suggests the existence of some reason for using the

Indefinite Reversal Exception beyond simply minimizing MNCs’ reported tax expense. The

mean withholding taxes on repatriations is 3.7 percent for the PRE firms, which suggests that

withholding taxes are a non-trivial component of firms’ repatriation tax obligations. In addition,

Panel A reports that mean PRE is about $1.0 billion and that PRE represents 11% of worldwide

assets.

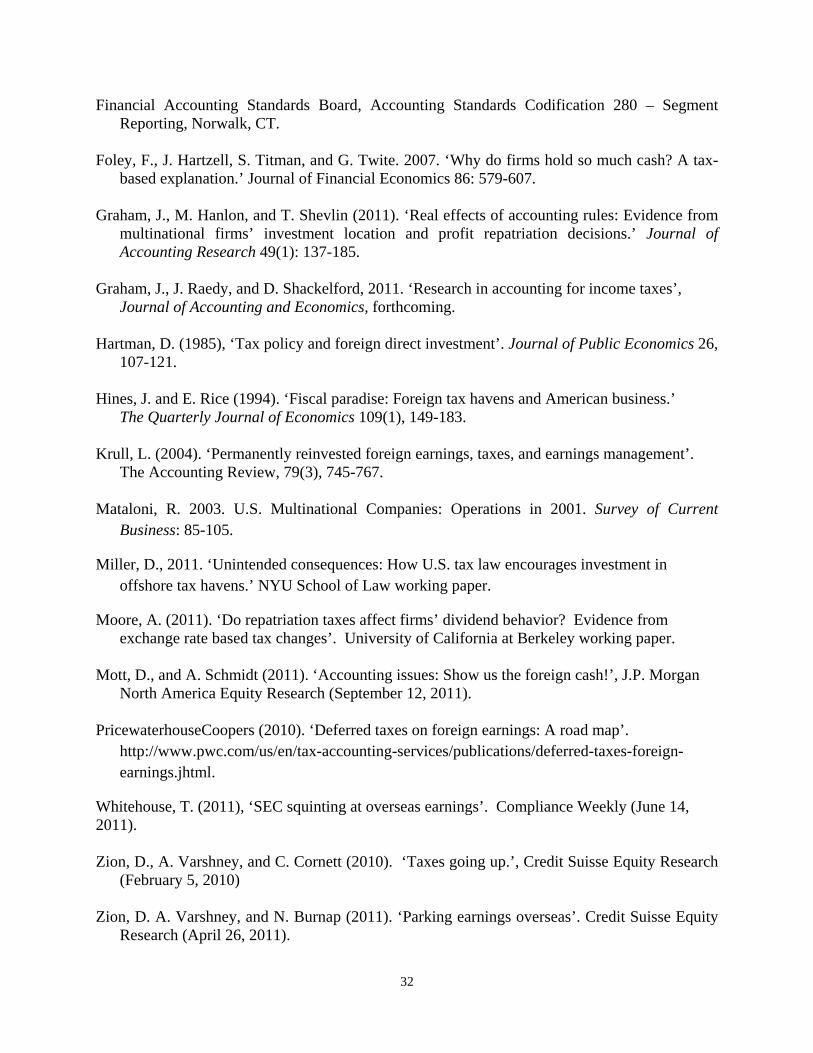

In Table 1 Panel B, we report several measures of PRE over our sample period. Aggregate

PRE for our sample grows from $180 billion in 1998 to $777 billion in 2008. The only drop in

aggregate PRE occurs in 2005, from $500 billion to $419 billion, which is likely attributable to

the AJCA, which permitted firms a temporarily reduced tax cost associated with the repatriation

of foreign earnings. Although aggregate PRE has not grown as quickly as aggregate foreign

assets, mean PRE appears to have increased precipitously in the post-AJCA period. Finally,

consistent with declining foreign income tax rates, the Repatriation Tax Rate has increased over

our sample period.

5.2. Analysis of motivations for PRE designations

Table 2 reports the results of estimating the effect of affiliate characteristics on the proportion

of foreign assets designated as permanently reinvested. Specifically, Panels A through D report

the results of estimating Equation (1) for the four affiliate characteristics of interest (tax status,

haven status, currency volatility, and growth).

Panel A reports the results of estimating Equation (1) using TaxDue Foreign Assets (as

Characteristic Foreign Assets). The coefficient on Total Foreign Assets is 0.1815 which suggests

that 18 percent of assets in affiliates with no tax due are designated as PRE. The coefficient on

TaxDue Foreign Assets suggests that 29 percent (0.1815 + 0.1059) of assets in affiliates with tax

18

due are designated as PRE. This proportion is not significantly different than the proportion for

affiliates with no tax due (t=-1.00). However, the mean foreign assets in affiliates with tax due

represents 90 percent of total foreign assets (mean foreign assets in affiliates with tax due as a

percentage of worldwide assets is 0.3014 and mean foreign assets as a percentage of worldwide

assets is 0.3344). When we use these respective means to estimate the amount of PRE in

affiliates with and without tax due, we find that PRE in affiliates with tax due is 8.66 percent of

worldwide assets [0.3014*(0.1815+0.1059)] and PRE in affiliates with no tax due is 0.6 percent

of worldwide assets. These estimates suggest that 94 percent of PRE is located in affiliates with

tax due [8.66/(0.60+8.66)] and 6 percent of PRE is located in affiliates with no tax due

[0.60/(0.60+8.66)]. This result provides evidence that a large proportion of PRE are located in or

associated with earnings in low income tax or high withholding tax affiliates, and would likely

trigger a U.S. repatriation tax or foreign withholding tax upon repatriation.25

Panel B reports results of estimating Equation (1) using B7 Foreign Assets. This test

estimates the effect of assets in Big 7 haven affiliates on PRE relative to assets in non-Big 7

haven affiliates. If assets invested in Big 7 affiliates are tied up in complex tax planning

strategies, then assets in Big 7 haven affiliates should have a more positive effect on PRE than

assets in other affiliates. Consistent with this expectation, the coefficient on B7 Foreign Assets is

0.1222 and is significantly different from zero. This result suggests that a higher proportion of

assets in Big 7 haven affiliates is designated as PRE than in non-Big 7 haven affiliates. Using the

mean foreign assets in all affiliates and Big 7 haven affiliates to interpret these coefficients, we

find that PRE located in non-Big 7 haven affiliates equals 7.65 percent of worldwide assets

25 We also estimate Equation (1) defining Characteristic Foreign assets as the sum of assets in affiliates with an average tax rate less than 0.35 (LT Foreign Assets). We find that the coefficient on LT Foreign Assets is -0.0525 (t=-0.97) and 74 percent of PRE is located in low tax affiliates. When we define Characteristic Foreign Assets as the sum of assets in affiliates with a positive withholding tax rate (WH Foreign Assets) the coefficient on WH Foreign Assets is 0.1087 (t=2.44) and 54 percent of PRE is located in positive withholding tax affiliates.

19

[(0.3344 - 0.0424)*0.2620], and PRE located in Big 7 haven affiliates equals 1.63 percent of

worldwide assets [0.0424*(0.2620 + 0.1222)]. Thus, our estimates suggest that about 18 percent

of PRE is located in Big 7 tax havens. Yet, only 5 percent of our sample’s worldwide assets are

located in Big 7 tax haven countries (untabulated). This latter observation is consistent with

firms making the PRE designation for tax and/or earnings purposes.

We repeat these analyses in Panels C and D, using FX Foreign Assets and GR Foreign Assets

respectively, to test the significance of the association between assets in high currency volatility

and high growth affiliates. In Panel C, we report the effect of assets in high currency volatility

affiliates on PRE designations. Although earnings incentives would predict a positive association

between currency volatility and PRE designations, we find that the coefficient on FX Foreign

Assets is negative and significant. Consistent with Dodonova and Khoroshilov (2007), this result

suggests that firms are less likely to designate foreign earnings as PRE if they are in an affiliate

with high currency volatility, because the firm is more likely to repatriate the income sooner.

Alternatively, high currency volatility may be correlated with politically or economically

unstable economies in which U.S. multinationals have little expectation of making long-term

investment commitments. Our interpretation of these coefficients suggests that about 27 percent

of PRE is located in affiliates with high currency volatility.26

Panel D reports the results of using GR Foreign Assets to estimate Equation (1). A positive

coefficient on GR Foreign Assets is consistent with firms’ designating more subsidiary earnings

as PRE when the firm has profitable investment opportunities abroad. Consistent with this

assertion, we find that the coefficient on GR Foreign Assets is significantly greater than the

26 As sensitivity tests we define FX Foreign Assets as assets in affiliates with a change in the exchange rate over the last three years and five years greater than the median change for sample and find similar results.

20

coefficient on Total Foreign Assets. Further, this coefficient suggests that 60 percent of PRE is

located in affiliates with high growth.

5.3. Binding versus non-binding foreign tax credit positions

The tests in Table 2 investigate whether affiliate characteristics affect firms’ decisions to

designate foreign affiliate earnings as PRE. However, we measure PRE at the firm level. While

an individual affiliate characteristic can affect PRE decisions, affiliate earnings often travel

through chains of ownership before they reach the ultimate U.S. parent. In addition, in

calculating the overall U.S. tax liability, firms can use foreign tax credits from high taxed entities

to offset the U.S. tax liability on low-taxed entities and can carry forward unused foreign tax

credits.

As a result, some MNCs face foreign tax rates that, on average, are higher than the U.S. rate.

These firms effectively have “extra” U.S. credit for their foreign tax payments (binding MNCs)

and thus, the foreign tax credit (FTC) generally eliminates the repatriation tax. In contrast, other

MNCs face foreign tax rates that, on average, are lower than the U.S. rate and these firms are

said to be in a non-binding FTC position. The parent firm’s overall tax status can affect the

ultimate U.S. tax liability on foreign affiliate earnings and the financial statement effect of the

tax liability.

Thus, MNCs’ in different FTC positions – binding versus non-binding – may place

differential focus on the motivations for designating PRE outlined above. To study the role of

firms’ FTC positions on PRE motivations, we partition our sample based on whether it is in a

binding FTC position or not and then re-estimate Equation (1) for each affiliate characteristic.

Table 3 reports the results of partitioning our estimation of Equation (1) by the firms’ FTC

positions. Consistent with MNCs making PRE assertions for earnings incentives, we find that the

21

association between TaxDue Foreign Assets and B7 Foreign Assets and PRE levels, reported in

Panels A and B, respectively, is concentrated in the sample of MNCs facing non-binding FTC

constraints.27 This result is consistent with firms facing non-binding FTC positions placing more

weight on earnings and tax motivations for designating PRE because they likely have a greater

unrecognized repatriation tax expense.

Results in Panel C suggest that the role of currency volatility in PRE designations is not

associated with the MNC’s FTC position. In Panel D, while growth appears to affect PRE

designations of firms in both binding and non-binding FTC positions, the coefficient on GR

Foreign Assets is 0.1356 for binding firms and 0.0624 for nonbinding firms. The results in

Panels A, B, and D suggest that growth plays a larger role and taxes play a lesser role in PRE

designations for binding FTC firms, relative to non-binding FTC firms.

5.4. Competing motivations

As we are curious as to whether there is any dominant characteristic that explains PRE, we

further explore firms’ motivations for designating earnings as PRE using the following equation:

PREi,t = α0 + α1Total Foreign Assetsi,t + α2TaxDue Foreign Assetsi,t + α3B7 Foreign

Assetsi,t + α4FX Foreign Assetsi,t + α5GR Foreign Assetsi,t + ΣαkYeark + εi,t (2)

All variables in Equation (2) are defined as in Equation (1). Equation (2) differs in that it allows

each motivation to compete, thus testing whether each motivation is significant, after controlling

for the other.

27 When we define Characteristic Foreign Assets using LT Foreign Assets (assets in affiliates with an average tax rate less than 0.35) the coefficient on LT Foreign Assets is 0.0699 (t=1.49) for non-binding FTC firms and -0.2445 (t=-2.92) for binding FTC firms. These results suggest that 88 (32) percent of PRE is in low tax affiliates for non-binding (binding) firms. When we define Characteristic Foreign Assets using WH Foreign Assets (assets in affiliates with a positive withholding tax rate) the coefficient on WH Foreign Assets is 0.0879 (t=1.88) for non-binding FTC firms and 0.1923 (t=2.04) for binding FTC firms. These results suggest that 51 (66) percent of PRE is in positive withholding tax affiliates for non-binding (binding) firms.

22

Table 4 reports the results of tests of estimating Equation (2) that allow us to test whether

each motivation is important after controlling for other motivations. In Panel A, we report results

using the full sample. The results suggest that, after controlling for other motivations to designate

earnings as PRE, only the coefficient on TaxDue Foreign Assets is insignificant. The results for

all of the motivations are similar to those presented in Table 2. These tests also allow us to

compare the relative magnitudes of each effect. Comparing the magnitude of each coefficient

indicates that haven affiliates have the highest proportion of assets designated as PRE with a

coefficient of 0.1390, and affiliates with high currency volatility have the lowest proportion of

assets associated with PRE with a coefficient of -0.1805.

The Estimate of PRE/Assets column provides an estimate of the amount of PRE located in

affiliates with each motivation, after controlling for other motivations. This column takes the

sum of the coefficient on Total Foreign Assets and the respective motivation and multiplies this

total by the mean assets for each motivation. For example, the estimate of PRE/Assets for GR

Foreign Assets equals the coefficient on Total Foreign Assets plus the coefficient on GR Foreign

Assets times the mean GR Foreign Assets [(0.2190 + 0.0959)*0.1794 = 0.0565]. The results in

this column suggest that PRE is largely located in high growth affiliates and affiliates with

repatriation tax obligations, consistent with motivations to designate PRE for growth reasons and

to defer recognition of the anticipated future repatriation tax expense.

Table 4 Panels B and C reports the results of estimating Equation (2) by the MNC’s FTC

position (binding or non-binding). Similar to results in Table 3, PRE designations are more

prevalent in affiliates with repatriation tax obligations and haven affiliates for MNCs facing a

non-binding FTC constraint, but more prevalent in high growth affiliates for firms in binding

23

FTC positions. Once again, PRE assertions are not disparately affected by the MNC’s FTC

position in highly volatile currency jurisdictions.

6. Additional analyses

6.1 Types of tax havens

Next, we examine the effect of tax status and haven status in more detail. This analysis is

motivated by interest in PRE in the context of discussions about corporate tax reform (see

Section 1). A common perception in the business press and policy debates is that U.S. tax law

encourages investment in offshore tax havens (Miller 2011), and that PRE signals the extent to

which this conjecture may be true by conveying information about the undistributed earnings

that have not yet been taxed by the U.S. (Zion et al. 2011). We target the role of anticipated

repatriation tax costs and tax planning strategies involving offshore tax havens in PRE

designations by estimating Equation (1) using alternative definitions of a tax haven.

Table 5 Panel A defines affiliates’ tax haven status based on the 34 tax haven countries

defined in Hines and Rice (1994). Panel B separates these 34 havens into Big 7 tax havens and

all other havens which we label DOT havens. DOT havens are those with relatively small

economies (many of them island communities), whereas Big 7 havens are those with more

significant economies in terms of population, land area, and GDP. Overall, the results indicate

that affiliate assets in DOT havens and Big 7 havens exhibit very different proportions and levels

of PRE. In fact, on average, a presence in DOT havens decreases a firm’s level of PRE. We

conjecture that MNCs find it difficult to substantiate PRE designations in DOT havens because

there is very little active business in these locations to support such an assertion.

6.2 Asset composition

24

Undistributed foreign earnings can be reinvested in either operating assets or financial assets.

The distinction is important for two reasons. First, the tax revenue implications of PRE depend

on the extent to which firms with significant amounts of PRE hold liquid assets (i.e., cash and

cash equivalents) that can be repatriated without the need to sell productive assets used in an

active trade or business. Second, PRE’s asset composition has implications for firm value. De

Waegenaere and Sansing (2008) derives the valuation implications of future repatriation tax

consequences and infers that firm value should only impound repatriation tax liabilities when

PRE is invested in financial assets. Bryant-Kutcher, Eiler and Guenther. (2008) finds empirical

support for the predictions of the De Waegenaere and Sansing (2008) model.28

We are interested in understanding the decision to hold operating versus financial assets

because of the implications for international tax policy and MNC liquidity. If a significant

proportion of PRE is in non-financial assets, then these earnings are likely to remain reinvested

in perpetuity. Should policymakers consider the repeal of deferral, transition rules requiring the

immediate taxation of reinvested earnings could have adverse consequences to MNCs if the

MNCs must either sell productive assets or borrow to pay any resulting tax obligation. However,

if PRE is in liquid assets, then as illustrated by the recent SEC inquiries into the location of

MNCs’ cash balances, investors may be concerned about the cost firms must incur to access their

cash.

To examine the asset composition of PRE, we estimate the following regression equation:

PREi,t = β0 + β1Total Foreign Assetsi,t + β2Foreign Cashi,t + ΣβkYeark + εi,t (3)

Foreign Cash equals total foreign cash and cash equivalents (i.e., financial assets). All other

variables are defined in Equation (1).

28 Bryant-Kutcher et al. (2008) confirms the Collins, Hand and Shackelford (2000) finding that firms’ value is affected when the firm discloses the estimated tax liability on PRE.

25

We also examine the asset composition of PRE in affiliates with the various characteristics

described in Sections 4.1 to 4.4 to further understand motivations for PRE. In particular, we are

interested in understanding whether the asset composition of PRE varies by the extent of MNCs’

expected repatriation obligations. Similarly, investigating the association between asset

composition and growth aids in our understanding of whether high growth affiliates build up

cash or operating assets. To investigate the asset composition of PRE jointly with affiliate

characteristics, we estimate the following regression equation:29

PREi,t = β0 + β1Non-Cash Foreign Assetsi,t + β2Foreign Cashi,t

+ β3 Characteristic Non-Cash Foreign Assetsi,t

+ β4 Characteristic Foreign Cashi,t + ΣβkYeark + εi,t (4)

Characteristic Foreign Cash (Characteristic Non-Cash Foreign Assets) equals Foreign Cash

(Non-Cash Foreign Assets) assets summed across a firm’s affiliates with the characteristic of

interest.

We study the same four characteristics we examine in Equation (1): affiliates with

repatriation tax obligations (TaxDue), Big 7 tax haven affiliates (B7), affiliates with high

currency volatility (FX), and high growth affiliates (GR). When Characteristic Foreign Cash

equals TaxDue Foreign Cash, β2 in Equation (4) represents the change in PRE as cash assets in

affiliates with no tax due increase by one dollar, and β4 represents the change in PRE per dollar

of cash assets in affiliates with tax due, incremental to the change per dollar of cash assets in

affiliates with no tax due. The total change in PRE per dollar of cash assets in affiliates with tax

due is represented by β2 + β4. This equation allows us to test whether cash (non-cash) assets in

affiliates with tax due have a significantly different effect on PRE than cash (non-cash) assets in

29 We disaggregate Total Foreign Assets into Non-Cash Foreign Assets and Foreign Cash in Equation (4) to facilitate the interpretation of the coefficients.

26

affiliates with no tax due, and also allows us to observe the relative magnitudes of the effects of

cash versus non-cash assets.

Table 6 reports the results of estimating Equations (3) and (4) that investigate the types of

assets in which firms invest PRE. We compare cash versus non-cash assets. For each

comparison, we also estimate whether the proportion of PRE invested in each asset category

varies along our four affiliate characteristics. The results generally suggest that a higher

proportion of cash is designated as PRE than non-cash assets. For example, in Panel A, the

coefficient on Total Foreign Assets is 0.2492 and the coefficient on Foreign Cash is 0.3419

(0.2492 + 0.0927). However, the % of PRE column suggests that 58% of PRE is held in the form

of non-cash assets, and 42% of PRE is held in cash. Thus, our estimates suggest that over half of

PRE is held in non-cash assets.

Panels B and C suggest that the proportion of PRE held in cash does not vary with the tax

attributes of the affiliate. However, in Panel E the coefficient on non-cash assets in high growth

affiliates is 0.2531 (0.2471 + 0.0060) and the coefficient on cash in high growth affiliates is

0.5327 (0.2500 + 0.2827). This result is consistent with high growth affiliates holding more cash

to have available for investments.

In Table 7 we estimate Equations (3) and (4) for the non-binding and binding FTC partitions.

In Panel A we find that non-binding firms designate a significantly higher proportion of foreign

cash as PRE than non-cash foreign assets whereas binding firms do not. Foley et al. (2007) find

that firms with higher repatriation taxes hold more cash. Consistent with this notion, our result

further suggests that this cash is designated as PRE. This same pattern is apparent in Panel B.

Non-binding FTC firms designate a significantly higher proportion of cash as PRE in tax due

27

affiliates than in no tax due affiliates, whereas as binding FTC firms do not. However, Panels C,

D, and E do not exhibit any notable differences across binding and non-binding FTC firms.

6.3 Country and industry location

A natural extension from the previous analyses is to investigate the specific countries and

industries in which PRE are located. As mentioned above, investors are clearly interested in

understanding the potential tax liabilities associated with cash abroad. Furthermore, information

regarding country and industry location of PRE could inform policymakers about the revenue

consequences of any change in U.S. international tax policy as well as the impact of changes in

other countries’ tax policy. Although admittedly descriptive, we believe that our analysis

provides information regarding PRE that has never been revealed.

In order to provide descriptive evidence on the countries where PRE is located, we estimate

the following regression:

PREi,t = ΣδnCountryn Assetsi,t + εi,t (5)

Where Country Assets equal a firm’s total foreign assets in each individual country in which the

firm’s affiliates operate. All other variables are defined in Equation (1).

We also provide descriptive evidence on how the use of PRE varies across industries by

estimating the following regression:

PREi,t = ΣδnIndustryn Assetsi,t + εi,t (6)

Where Industry Assets reflect a firm’s total foreign assets in various industries represented by the

firm’s affiliates. Note that our industry summations use the industry membership of the affiliate,

so our industry analysis captures variation in PRE across industries regardless of the extent of

28

firms’ industrial diversification.30 The coefficient δn in Equations (5) and (6) represents the

change in PRE as assets in country n and industry n, respectively, increase by one dollar.

In Table 8, we present the results of estimating Equations (5) and (6). In Panel A, we report

the estimated country location of PRE. We separately tabulate the coefficients and estimates of

PRE in 17 countries where U.S. MNCs have significant foreign assets, and combine all other

countries into ‘Other’. The coefficient on Country Assets estimates the change in PRE for each

dollar of assets in each country. Since PRE is a component of assets, these coefficients can be

interpreted as the proportion of assets in each location designated as PRE and allow us to

estimate the amount of PRE in each jurisdiction.

Panel A reports that the UK and Canada have the highest percent of PRE. It is interesting to

note that both countries have historically had high statutory income tax rates, but yet the

Indefinite Reversal Exception is asserted in these countries.

We also estimate how much PRE is held in cash in each country and the tax obligation that

would be necessary to repatriate cash designated as PRE.31 These estimates are also reported in

Panel A. As suggested by the estimates of PRE held in cash, the greatest average repatriation tax

obligation is in the UK followed by Ireland and the Netherlands.

In Table 8 Panel B, we investigate the industry location of PRE. The largest industry for PRE

is “Wholesale trade” followed by “Services”. The former industry group includes firms that sell

any type of good, but whose role is to simplify flows of products, payments, and information by

acting as intermediaries between a manufacturer and the final customer whereas services

30 The BEA surveys capture 4-digit NAICS codes for each affiliate and our industry groups align with those that the BEA uses to report international statistics. 31 We estimate PRE held in cash in each country using the following regression: PREi,t = ΣδnCountryn Cash Assetsi,t + ΣγnCountryn Non-Cash Assetsi,t where Countryn Cash Assets equals the sum of cash held in Country n and Countryn Non-Cash Assets equals the sum of non-cash assets held in country n. We interpret the coefficients on Countryn Cash Assets to estimate the amount of PRE held in cash in each country.

29

includes software business. Finally, Other Manufacturing (which primarily includes textile

manufacturers) and Chemical (which includes pharmaceutical companies), and Other are the

next largest industries for PRE. Note that Chemical companies were among the largest

repatriating firms under the AJCA.

7. Conclusion

U.S. firms continue to expand their operations abroad at a rapid pace – at the end of 2010, 89

percent of S&P 500 firms conducted business outside the U.S. – yet the only required

information in firms’ publicly available financial statements are foreign pre-tax earnings, taxes,

PRE in aggregate, sales and long-lived assets by geographic area, and a list of material

subsidiaries and their locations. The value relevance of the information contained in many of

these reported amounts has been studied extensively. One particular disclosure about foreign

operations is receiving significant interest in current debates on corporate tax reform – aggregate

permanently reinvested earnings (PRE). Motivated by the potential importance of PRE in tax

policy debates, and the fact that we know very little about its meaning and implications for firm

value, we conduct a detailed study of the location and composition of PRE.

PRE are foreign affiliate earnings for which a firm has not recognized a residual U.S. tax

expense, if any, due upon repatriation of those earnings. In practice, firms only report the

aggregate amount of PRE across all foreign affiliates and seldom report the expected tax liability

associated with its repatriation to the United States. This aggregate number makes it difficult, if

not impossible, for investors to understand the implications of PRE for firm value and liquidity,

or for policy-makers to understand the implications of PRE regarding the effects of corporate tax

reform. The common perception in the business press and policy debates is that PRE is

informative about all undistributed earnings that have not yet been taxed by the U.S., suggesting

30

that PRE are located primarily in low-tax and haven jurisdictions. However, there is no evidence

of this to date.

Our study combines amounts reported as PRE with confidential affiliate-level data collected

on legally mandated federal surveys of U.S. MNCs to learn the location and composition of PRE.

We make two key observations. First, we find that most (approximately 94 percent) but not all

PRE is located in low tax jurisdictions. Second, we find that a significantly higher proportion of

PRE is held in the form of cash in low-tax, relative to high-tax jurisdictions. Overall, our analysis

suggests that PRE has multiple implications for firm value. Some portion of PRE appears to

represent high levels of cash held by affiliates in low-tax jurisdictions, while other portions

represent non-cash assets in high growth affiliates. Thus, we urge researchers and policymakers

to exercise caution when using PRE to assess implications of corporate tax reform.

31

References Altshuler, R. and H. Grubert (2003), ‘Repatriation taxes, repatriation strategies, and

multinational financial policy’. Journal of Public Economics 87, 73-107. Blouin, J. and L. Krull (2009), ‘Bringing it home: A study of the Incentives Surrounding the

Repatriation of Foreign Earnings Under the American Jobs Creation Act of 2004’. Journal of Accounting Research 47, 1027-1059.

Blouin, J., L. Krull and L. Robinson (2012), ‘Is U.S. multinational repatriation policy influenced

by reporting incentives?’ The Accounting Review, forthcoming. Bryant-Kutcher, L. L. Eiler and D. Guenther (2008). ‘Taxes and financial assets: Valuing

permanently reinvested earnings’. National Tax Journal 61(4): 699-721. Bureau of National Affairs (BNA) Tax Management Foreign Income Portfolio No. 948, U.S.

Tax-Related Accounting Issues of Multinational Corporations. Collins, J., J.R.M. Hand and D. Shackelford (2000). ‘Valuing deferral: The effect of permanently

reinvested earnings on stock prices.’ In: J. Hines (ed): International Taxation and Multinational Activity, University of Chicago Press, 143-172.

Desai, M., F. Foley and J. Hines (2003). ‘Chains of ownership, regional tax competition, and

foreign direct investment.’ In Foreign Direct Investment in the Real and Financial Sector of Industrial Countries, edited by Heinz Herrmann and Robert Lipsey, Heidelberg: Springer Verlag, pp. 61-98.

Desai, M., F. Foley and J. Hines (2007), ‘Dividend policy inside the multinational firm’.

Financial Management 36(1): 5-26. De Waegenaere, A., and R. Sansing, 2008. Taxation of international investment and accounting

valuation.’, Contemporary Accounting Research 25(4): 1045-66. Dodonova, A., and Y. Khoroshilov, 2007. Income repatriation decision for multinational

corporations: Tax issues. Journal of Accounting and Public Policy, 26(3): 376-384. Dyreng, S. and B. Lindsey (2009), ‘Using financial accounting data to examine the effect of

foreign operations located in tax havens and other countries on U.S. multinational firms’ tax rates’. Journal of Accounting Research 47, 1283-1316.

Dyreng, S., B. Lindsey, K. Markle and D. Shackelford (2011). Taxes and the clustering of

foreign subsidiaries. Duke University working paper. Financial Accounting Standards Board, Accounting Standards Codification 740 – Income Taxes,

Norwalk, CT.

32

Financial Accounting Standards Board, Accounting Standards Codification 280 – Segment Reporting, Norwalk, CT.

Foley, F., J. Hartzell, S. Titman, and G. Twite. 2007. ‘Why do firms hold so much cash? A tax-

based explanation.’ Journal of Financial Economics 86: 579-607. Graham, J., M. Hanlon, and T. Shevlin (2011). ‘Real effects of accounting rules: Evidence from

multinational firms’ investment location and profit repatriation decisions.’ Journal of Accounting Research 49(1): 137-185.

Graham, J., J. Raedy, and D. Shackelford, 2011. ‘Research in accounting for income taxes’,

Journal of Accounting and Economics, forthcoming. Hartman, D. (1985), ‘Tax policy and foreign direct investment’. Journal of Public Economics 26,

107-121. Hines, J. and E. Rice (1994). ‘Fiscal paradise: Foreign tax havens and American business.’

The Quarterly Journal of Economics 109(1), 149-183. Krull, L. (2004). ‘Permanently reinvested foreign earnings, taxes, and earnings management’.

The Accounting Review, 79(3), 745-767. Mataloni, R. 2003. U.S. Multinational Companies: Operations in 2001. Survey of Current

Business: 85-105.

Miller, D., 2011. ‘Unintended consequences: How U.S. tax law encourages investment in offshore tax havens.’ NYU School of Law working paper.

Moore, A. (2011). ‘Do repatriation taxes affect firms’ dividend behavior? Evidence from exchange rate based tax changes’. University of California at Berkeley working paper.

Mott, D., and A. Schmidt (2011). ‘Accounting issues: Show us the foreign cash!’, J.P. Morgan

North America Equity Research (September 12, 2011). PricewaterhouseCoopers (2010). ‘Deferred taxes on foreign earnings: A road map’.

http://www.pwc.com/us/en/tax-accounting-services/publications/deferred-taxes-foreign-earnings.jhtml.

Whitehouse, T. (2011), ‘SEC squinting at overseas earnings’. Compliance Weekly (June 14, 2011). Zion, D., A. Varshney, and C. Cornett (2010). ‘Taxes going up.’, Credit Suisse Equity Research

(February 5, 2010) Zion, D. A. Varshney, and N. Burnap (2011). ‘Parking earnings overseas’. Credit Suisse Equity

Research (April 26, 2011).

33

TABLE 1 Descriptive Statistics

Panel A: Descriptive Statistics for Firms with and without PRE PRE > 0; N=4,655 PRE = 0; N=1,337

Variable Mean Std Deviation Mean Std Deviation PRE 997.6904*** 3,292.3700 N/A N/A PRE/Assets 0.1095*** 0.1320 N/A N/A Worldwide Assets 12926.8109*** 626909.6070 7049.3700 278744.0310 Domestic Net Income 476.8669*** 2775.9284 188.3550 2016.5783 Foreign Net Income 227.1819*** 862.0576 44.3259 123.2746 Foreign Assets 5060.6161*** 21447.7079 1040.0418 2524.8760 Foreign Assets/Assets 0.3348*** 0.2575 0.2487 0.3212 Foreign Cash/Foreign Assets 0.1145*** 0.1192 0.0704 0.1109 Repatriation Tax Rate 0.1839*** 0.0774 0.1927 0.0999 Withholding Tax Rate 0.0371*** 0.0210 0.0415 0.0249 ETR 0.3652 0.2857 0.3595 0.2730

34

TABLE 1 Continued Panel B: Measures of Aggregate PRE, Retained Earnings, and Assets by Year

Year

N

Aggregate PRE ($)

Mean PRE ($)

Aggregate For Assets

($)

Aggregate For Ret Earn

($)

Mean PRE/Assets

(%)

Mean PRE/For Assets

(%)

Repatriation Tax Rate

(%) 1998 303 179,851 594 899,739 202,533 8.0 32.1 16.1 1999 363 218,609 602 1,133,365 253,052 9.4 31.4 17.8 2000 372 261,143 702 1,285,392 309,490 10.3 35.6 16.8 2001 378 294,569 779 1,332,270 345,624 15.0 38.2 17.2 2002 423 350,651 829 1,782,083 473,525 10.5 37.6 17.8 2003 451 429,429 952 2,149,159 555,796 11.0 41.2 18.7 2004 505 500,115 992 2,341,874 547,721 14.7 50.2 18.5 2005 496 418,901 843 2,741,243 644,560 10.3 38.5 18.8 2006 481 527,359 1,096 3,054,793 837,409 8.9 35.9 19.5 2007 446 688,571 1,543 3,468,212 982,046 11.3 47.9 19.8 2008 439 777,047 1,770 3,379,117 1,003,683 13.5 60.6 19.7