WHAT’S TRENDING IN BEVERAGE ALCOHOL - ECRM- A … · WHAT’S TRENDING IN BEVERAGE ALCOHOL....

58

1 Copyright © 2017 The Nielsen Company. Confidential and proprietary. Copyright © 2017 The Nielsen Company. Confidential and proprietary. Chateau Elan Winery & Resort Braselton, GA August 27, 2017 WHAT’S TRENDING IN BEVERAGE ALCOHOL Global Wine, Beer, & Spirits EPPS

Transcript of WHAT’S TRENDING IN BEVERAGE ALCOHOL - ECRM- A … · WHAT’S TRENDING IN BEVERAGE ALCOHOL....

1Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

Chateau Elan Winery & ResortBraselton, GAAugust 27, 2017

WHAT’S TRENDING IN BEVERAGE ALCOHOL

Global Wine, Beer, & Spirits EPPS

2Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

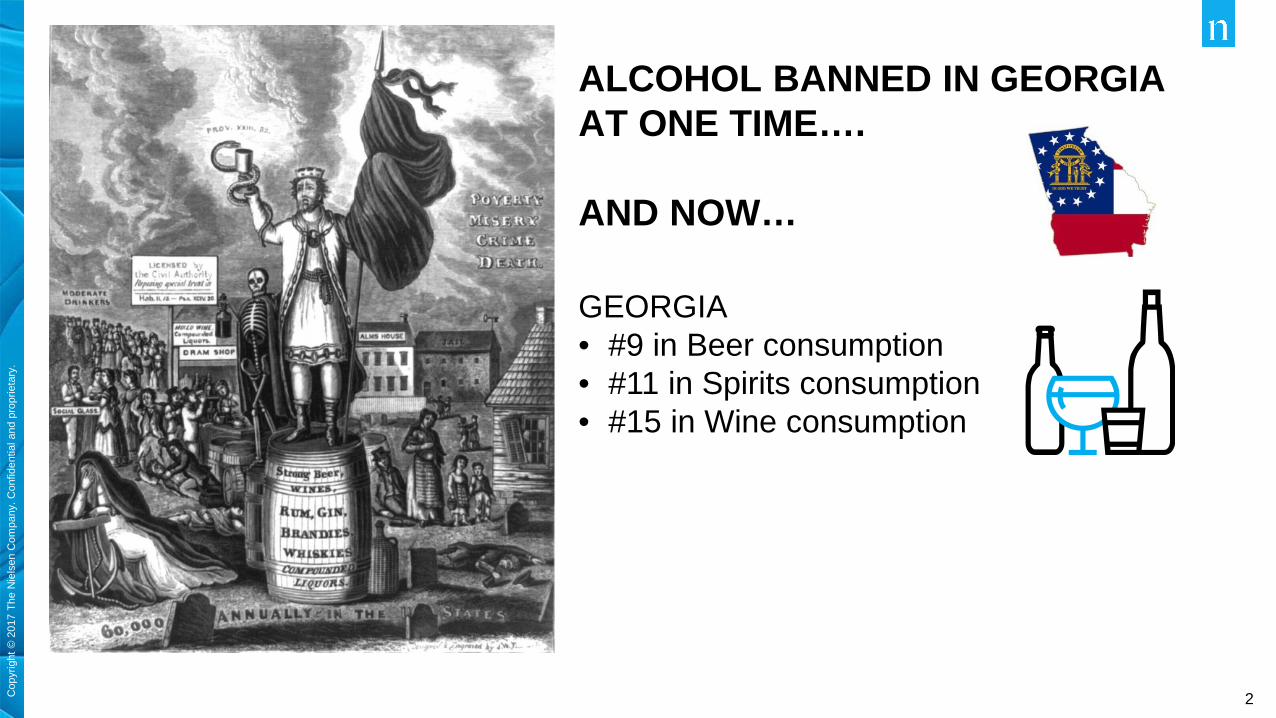

ALCOHOL BANNED IN GEORGIA AT ONE TIME….

AND NOW…

GEORGIA• #9 in Beer consumption• #11 in Spirits consumption• #15 in Wine consumption

3Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

AGENDA TODAY

Danny BragerSenior Vice President - Bev Al Practice LeaderOrange County, CA

• Overall industry landscape

• Beer• Wine• Spirits

4Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

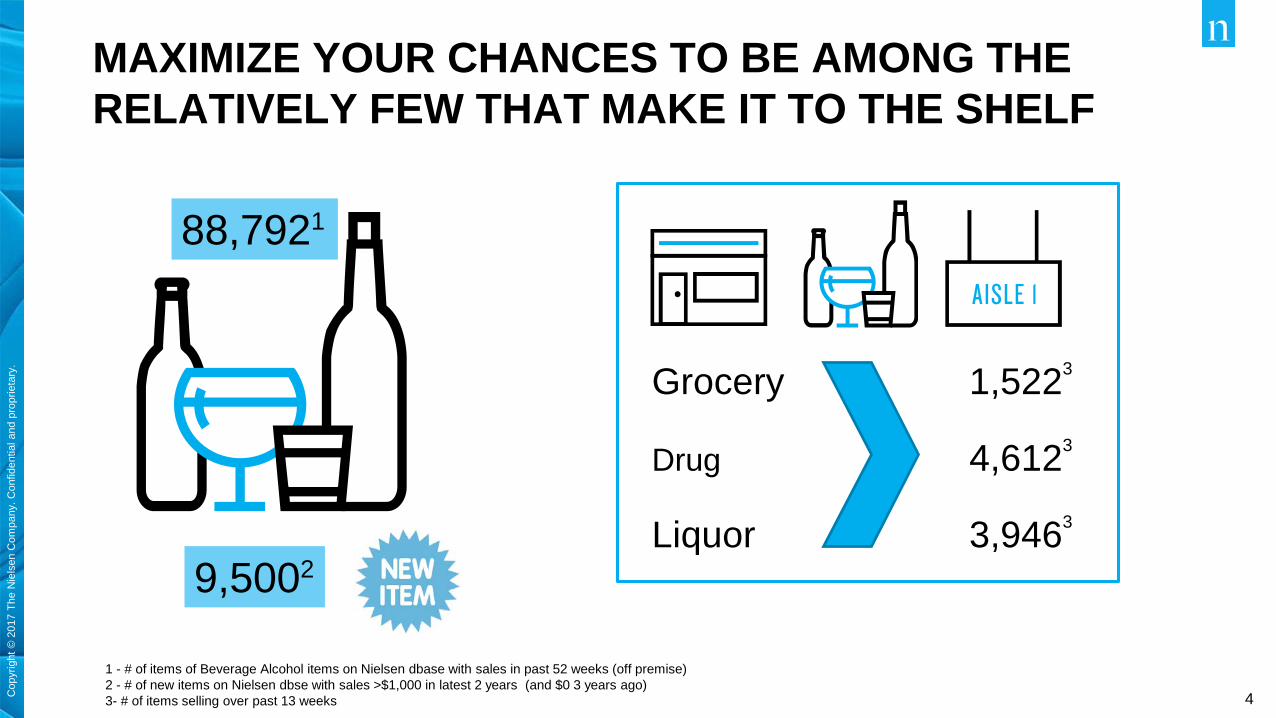

MAXIMIZE YOUR CHANCES TO BE AMONG THE RELATIVELY FEW THAT MAKE IT TO THE SHELF

1 - # of items of Beverage Alcohol items on Nielsen dbase with sales in past 52 weeks (off premise)2 - # of new items on Nielsen dbse with sales >$1,000 in latest 2 years (and $0 3 years ago)3- # of items selling over past 13 weeks

88,7921

9,5002

Grocery 1,5223

Drug 4,6123

Liquor 3,9463

5Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

TREND OR FAD?

GET IN? GET OUT? STAY OUT!

6Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

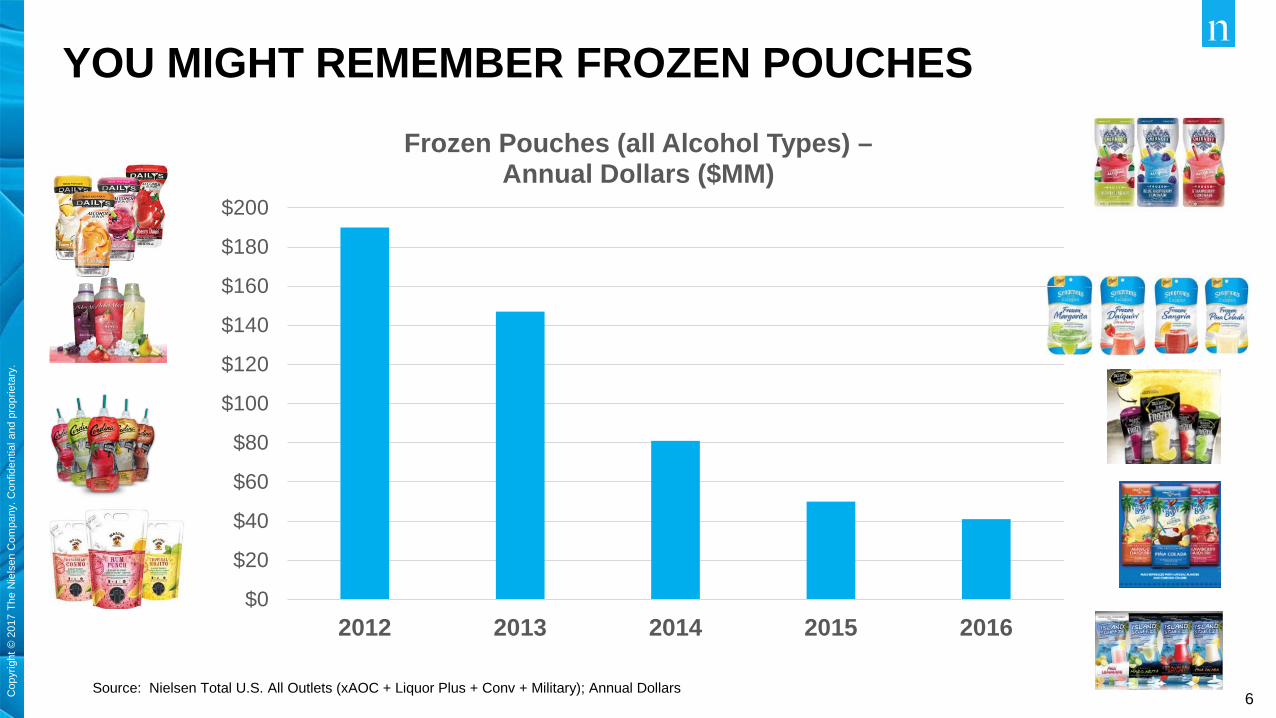

YOU MIGHT REMEMBER FROZEN POUCHES

Source: Nielsen Total U.S. All Outlets (xAOC + Liquor Plus + Conv + Military); Annual Dollars

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

2012 2013 2014 2015 2016

Frozen Pouches (all Alcohol Types) –Annual Dollars ($MM)

7Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

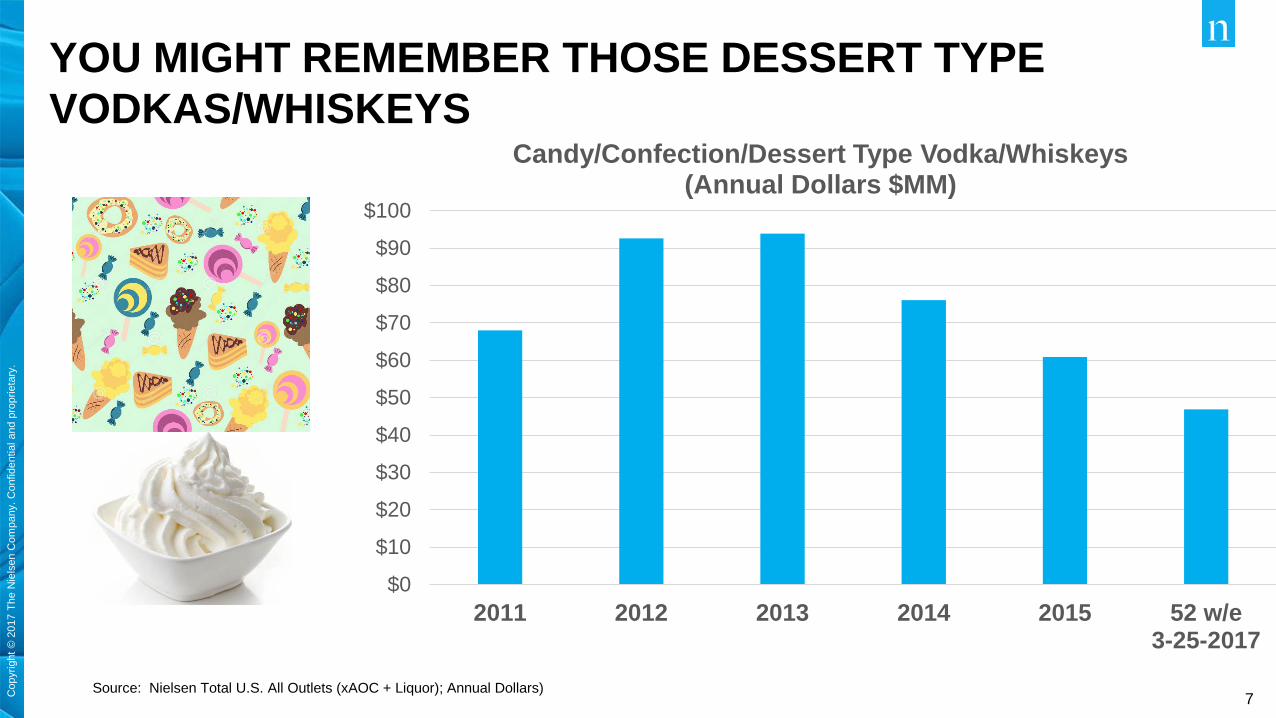

YOU MIGHT REMEMBER THOSE DESSERT TYPE VODKAS/WHISKEYS

Source: Nielsen Total U.S. All Outlets (xAOC + Liquor); Annual Dollars)

$0

$10

$20

$30

$40

$50

$60

$70

$80

$90

$100

2011 2012 2013 2014 2015 52 w/e3-25-2017

Candy/Confection/Dessert Type Vodka/Whiskeys (Annual Dollars $MM)

8Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

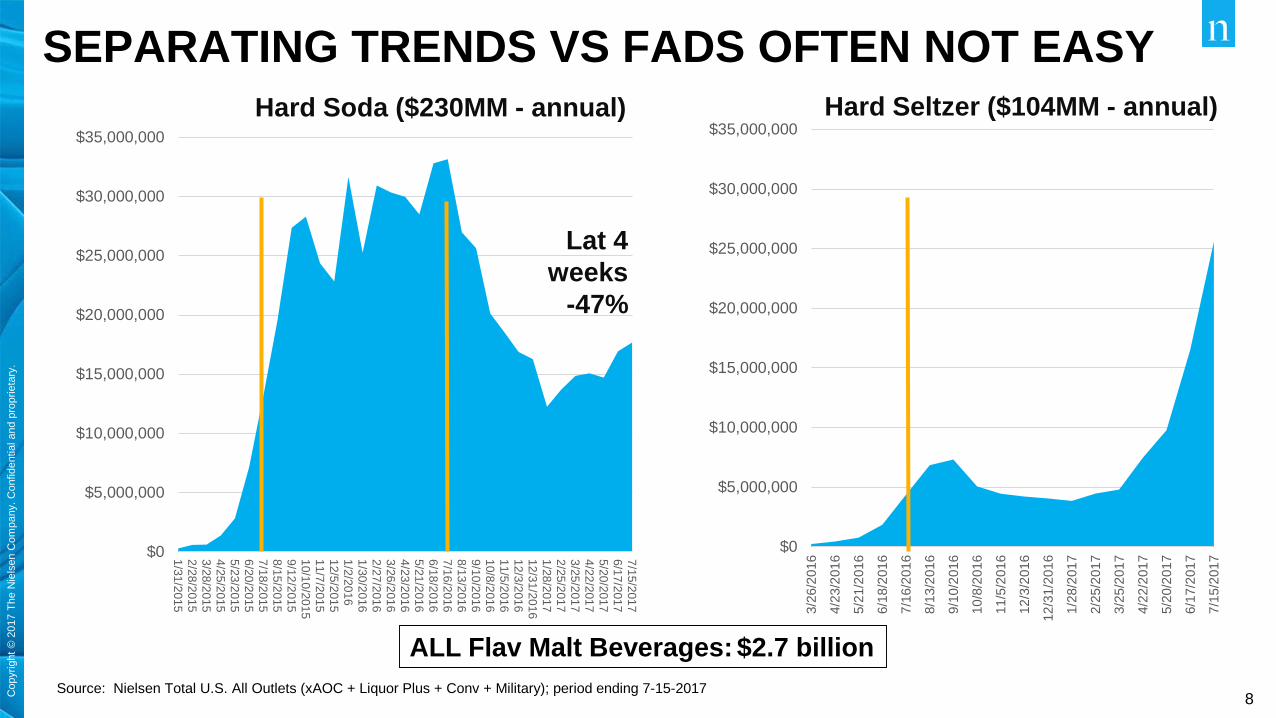

SEPARATING TRENDS VS FADS OFTEN NOT EASY

Source: Nielsen Total U.S. All Outlets (xAOC + Liquor Plus + Conv + Military); period ending 7-15-2017

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

$30,000,000

$35,000,000

1/31/20152/28/20153/28/20154/25/20155/23/20156/20/20157/18/20158/15/20159/12/201510/10/201511/7/201512/5/20151/2/20161/30/20162/27/20163/26/20164/23/20165/21/20166/18/20167/16/20168/13/20169/10/201610/8/201611/5/201612/3/201612/31/20161/28/20172/25/20173/25/20174/22/20175/20/20176/17/20177/15/2017

Hard Soda ($230MM - annual)

Lat 4 weeks

-47%

ALL Flav Malt Beverages: $2.7 billion

$0

$5,000,000

$10,000,000

$15,000,000

$20,000,000

$25,000,000

$30,000,000

$35,000,000

3/26

/201

6

4/23

/201

6

5/21

/201

6

6/18

/201

6

7/16

/201

6

8/13

/201

6

9/10

/201

6

10/8

/201

6

11/5

/201

6

12/3

/201

6

12/3

1/20

16

1/28

/201

7

2/25

/201

7

3/25

/201

7

4/22

/201

7

5/20

/201

7

6/17

/201

7

7/15

/201

7

Hard Seltzer ($104MM - annual)

9Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

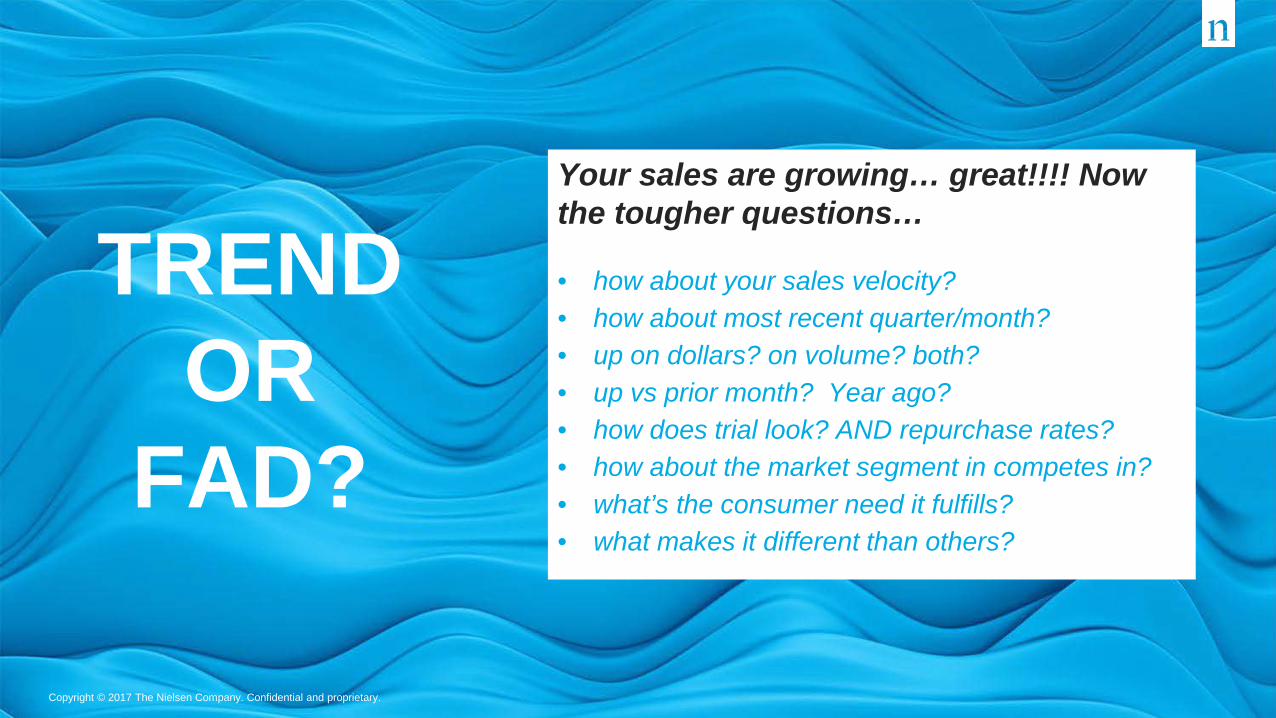

TREND OR

FAD?

Your sales are growing… great!!!! Now the tougher questions…

• how about your sales velocity?• how about most recent quarter/month?• up on dollars? on volume? both?• up vs prior month? Year ago? • how does trial look? AND repurchase rates?• how about the market segment in competes in? • what’s the consumer need it fulfills?• what makes it different than others?

10Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

NIELSEN MEASURES WHAT PEOPLE WATCH AND BUY

WATCH

Who - What - Where - When - Why

BUY

11Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

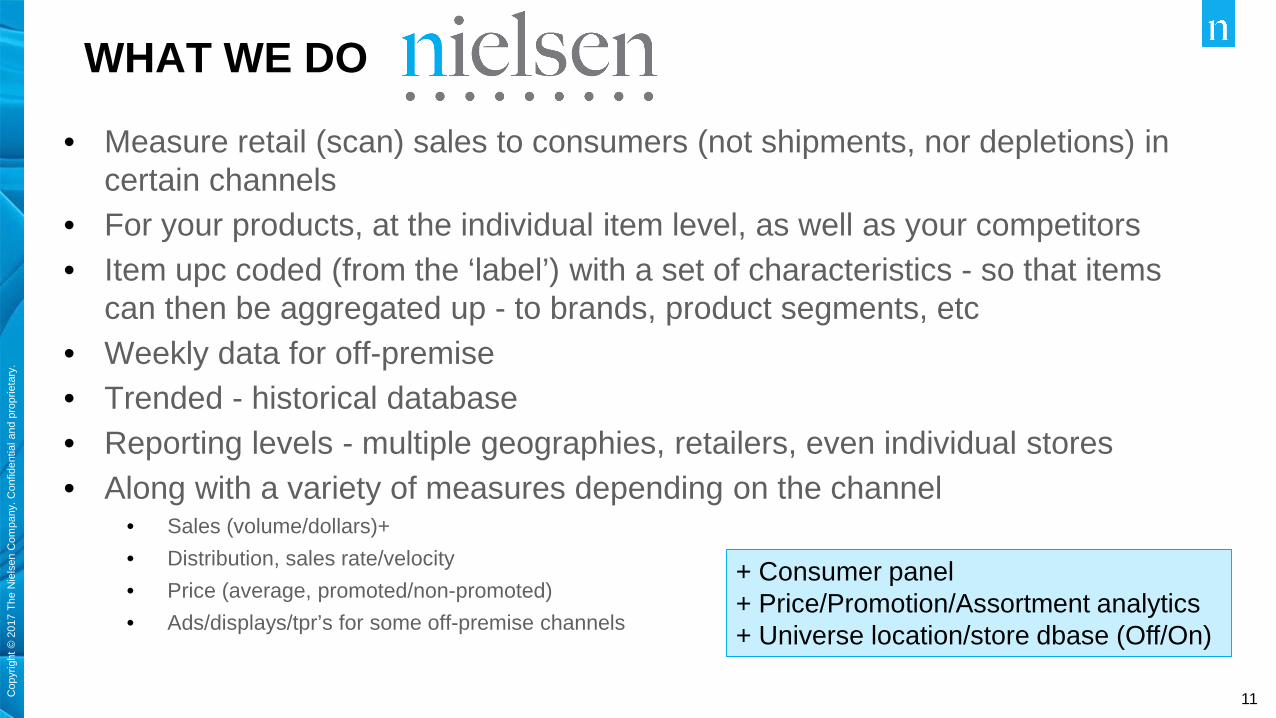

WHAT WE DO

• Measure retail (scan) sales to consumers (not shipments, nor depletions) in certain channels

• For your products, at the individual item level, as well as your competitors • Item upc coded (from the ‘label’) with a set of characteristics - so that items

can then be aggregated up - to brands, product segments, etc• Weekly data for off-premise• Trended - historical database• Reporting levels - multiple geographies, retailers, even individual stores• Along with a variety of measures depending on the channel

• Sales (volume/dollars)+ • Distribution, sales rate/velocity• Price (average, promoted/non-promoted)• Ads/displays/tpr’s for some off-premise channels

+ Consumer panel+ Price/Promotion/Assortment analytics+ Universe location/store dbase (Off/On)

12Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

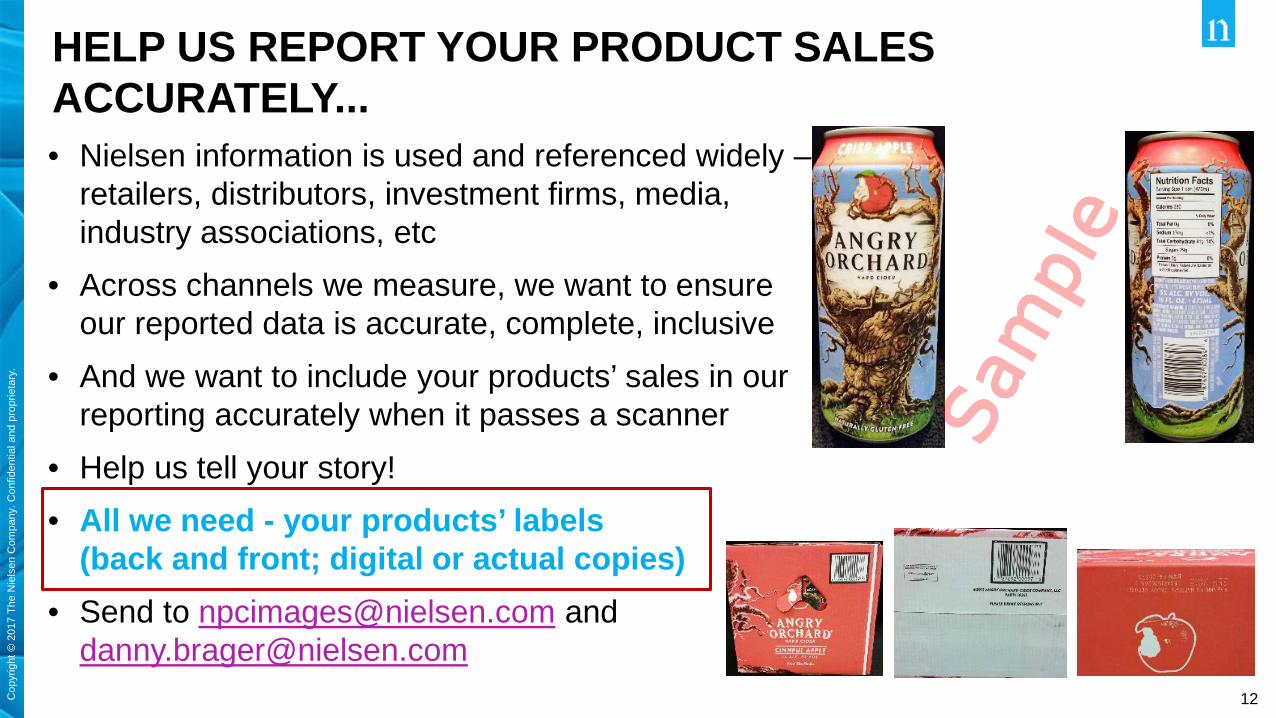

HELP US REPORT YOUR PRODUCT SALES ACCURATELY...• Nielsen information is used and referenced widely –

retailers, distributors, investment firms, media, industry associations, etc

• Across channels we measure, we want to ensure our reported data is accurate, complete, inclusive

• And we want to include your products’ sales in our reporting accurately when it passes a scanner

• Help us tell your story!• All we need - your products’ labels

(back and front; digital or actual copies)• Send to [email protected] and

13Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

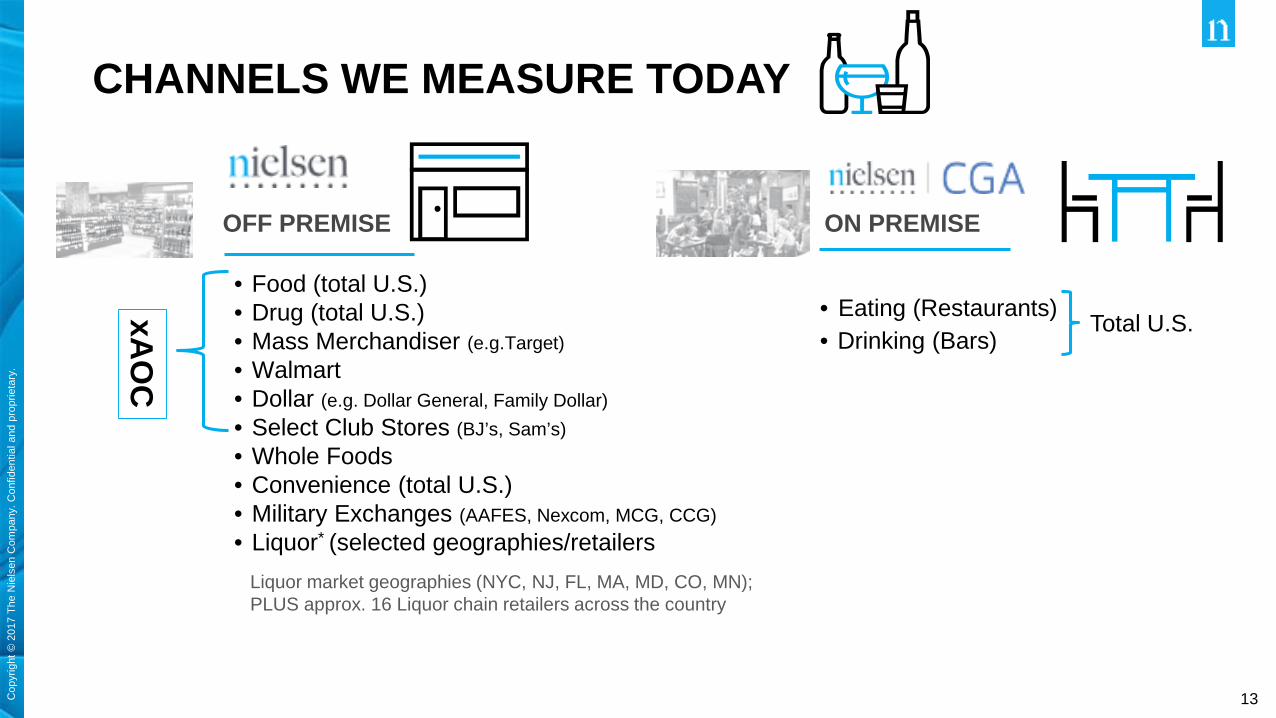

CHANNELS WE MEASURE TODAY

OFF PREMISE

• Food (total U.S.)• Drug (total U.S.)• Mass Merchandiser (e.g.Target)• Walmart• Dollar (e.g. Dollar General, Family Dollar)• Select Club Stores (BJ’s, Sam’s)• Whole Foods• Convenience (total U.S.)• Military Exchanges (AAFES, Nexcom, MCG, CCG)• Liquor* (selected geographies/retailers

ON PREMISE

• Eating (Restaurants)• Drinking (Bars)

Liquor market geographies (NYC, NJ, FL, MA, MD, CO, MN); PLUS approx. 16 Liquor chain retailers across the country

xAO

C

Total U.S.

14Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

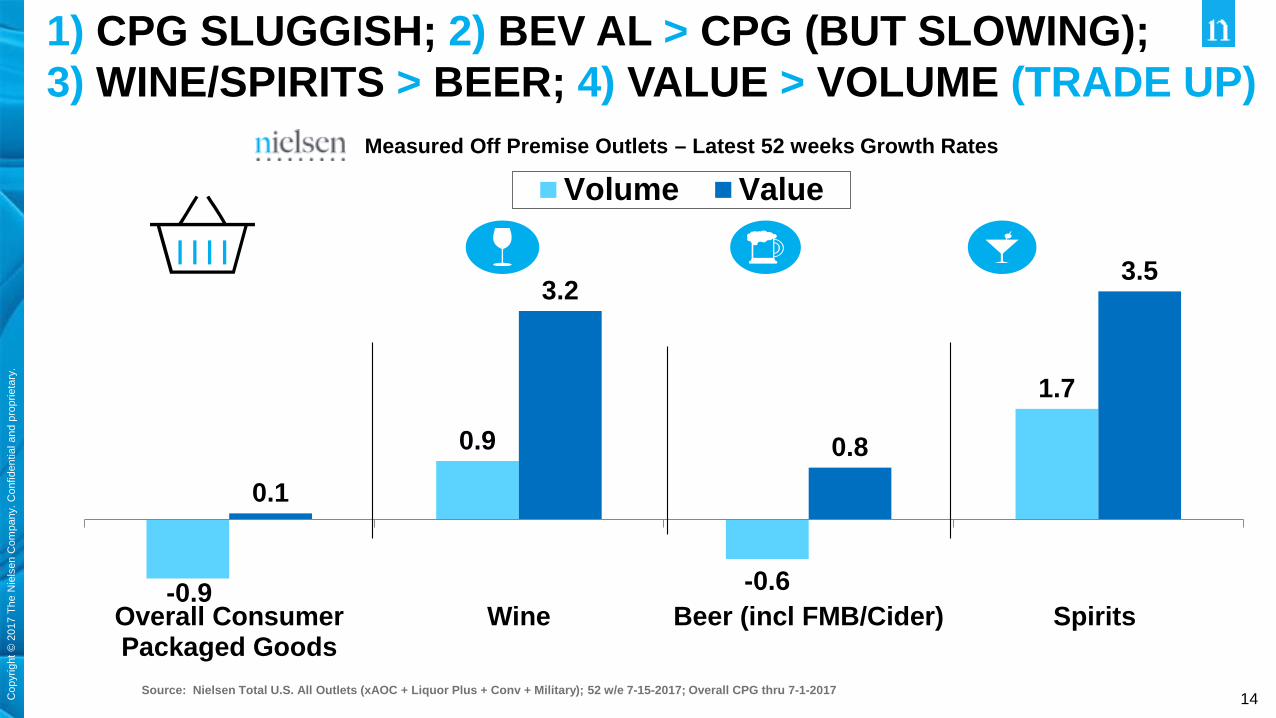

-0.9

0.9

-0.6

1.7

0.1

3.2

0.8

3.5

Overall ConsumerPackaged Goods

Wine Beer (incl FMB/Cider) Spirits

Measured Off Premise Outlets – Latest 52 weeks Growth Rates

Volume Value

1) CPG SLUGGISH; 2) BEV AL > CPG (BUT SLOWING); 3) WINE/SPIRITS > BEER; 4) VALUE > VOLUME (TRADE UP)

Source: Nielsen Total U.S. All Outlets (xAOC + Liquor Plus + Conv + Military); 52 w/e 7-15-2017; Overall CPG thru 7-1-2017

15Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

15

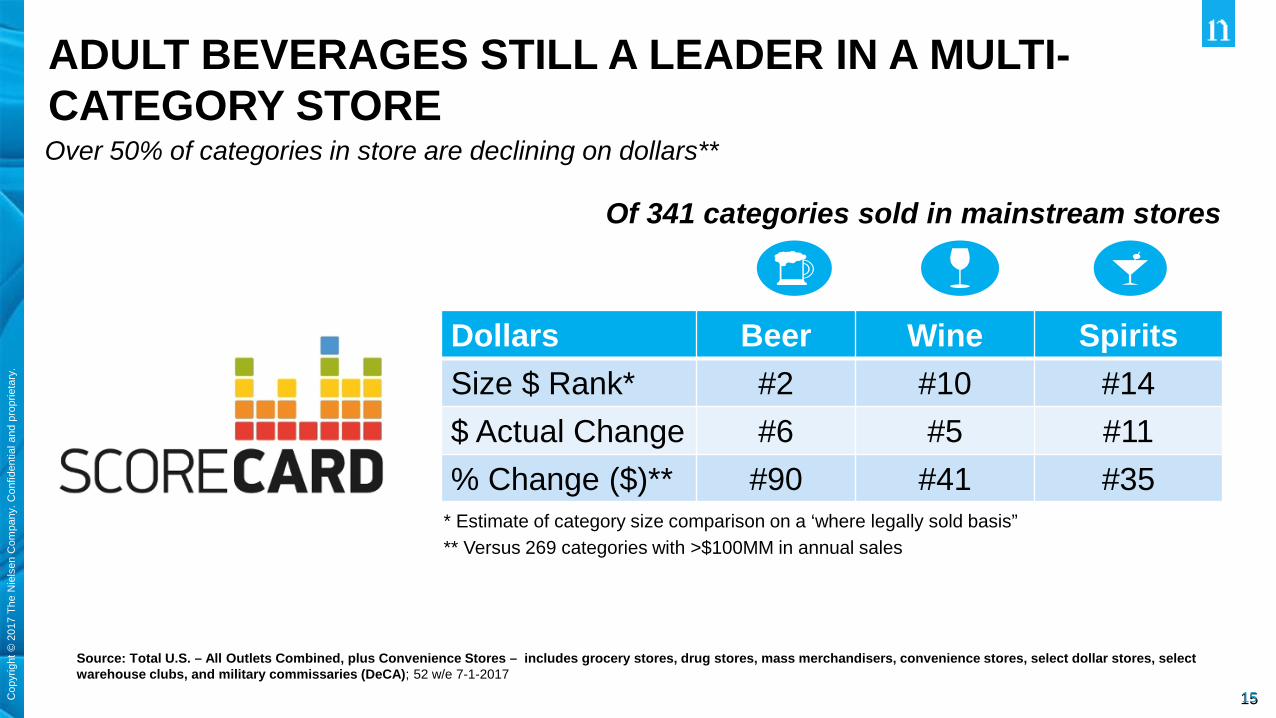

ADULT BEVERAGES STILL A LEADER IN A MULTI-CATEGORY STORE

Source: Total U.S. – All Outlets Combined, plus Convenience Stores – includes grocery stores, drug stores, mass merchandisers, convenience stores, select dollar stores, select warehouse clubs, and military commissaries (DeCA); 52 w/e 7-1-2017

Over 50% of categories in store are declining on dollars**

Dollars Beer Wine SpiritsSize $ Rank* #2 #10 #14$ Actual Change #6 #5 #11% Change ($)** #90 #41 #35

Of 341 categories sold in mainstream stores

* Estimate of category size comparison on a ‘where legally sold basis”** Versus 269 categories with >$100MM in annual sales

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

17Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

FRAGMENTATION

Versus just 5 years ago…

• 2/3 of the top 25 brands from then are smaller today

• Today’s top 25 brands – in aggregate – are about 3.5 share points lower

• Source: (2017 Advance Handbook)

18Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

RETAIL POLARIZATION TO SERVE DISTINCT CONSUMER GROUPSSome of the fastest growing channels - based on Store Count

Limited Assortment (no frills)

Nielsen TDLinx – December of each year

Upscale/FreshHispanic/Asian

19Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

FRAGMENTATION

Versus just 5 years ago…•2/3 of the top 25 brands from then are smaller now•Today’s top 25 brands – in aggregate – are about 3.5 share points lower•Retailer/retailing polarization to distinct consumer groups

LEADING TO CONSOLIDATION (across all 3 tiers)

Source: Nielsen Answers on Demand, Total U.S., 52 weeks ending December 31, 2016, UPC-coded

• In 2006, 76 retailers accounted for 80% of CPG retailers; now it’s 52 retailers

20Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

SOME KEY CONSUMER GROUPS…•Millennials now largest generation; but VERY, VERY diverse within…

–Broad age, and lifestage range; 21-39–Disparate incomes: from… 28%<$25K, and ….27%>$75K

–44% Multi-cultural (& growing) – Hispanic, African American, Asian

•Senior/Older group – only age group with significant population growth (>1%)

•Females - Gender balance a huge asset

21Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

WHAT ARE CONSUMERS – ESPECIALLY YOUNGER ONES - LOOKING FOR…

•Product transparency, authenticity, emotional connection •Health/wellness (but must also taste GOOD); along with an appetite for indulgences and social enjoyment

•Values the ‘experience’, sometimes even more than the brand•Diverse choice/looking for something different, unbound by past

–e.g. alternative packaging; styles/flavors (but must discern trends vs fads – know when to get in, get out, or just stay out)

•Wordly/global connections – food/drinks, travel, entertainment•Choosing across B/W/S – occasion by occasion (dwindling exclusive category drinkers)

22Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

BEER

23Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

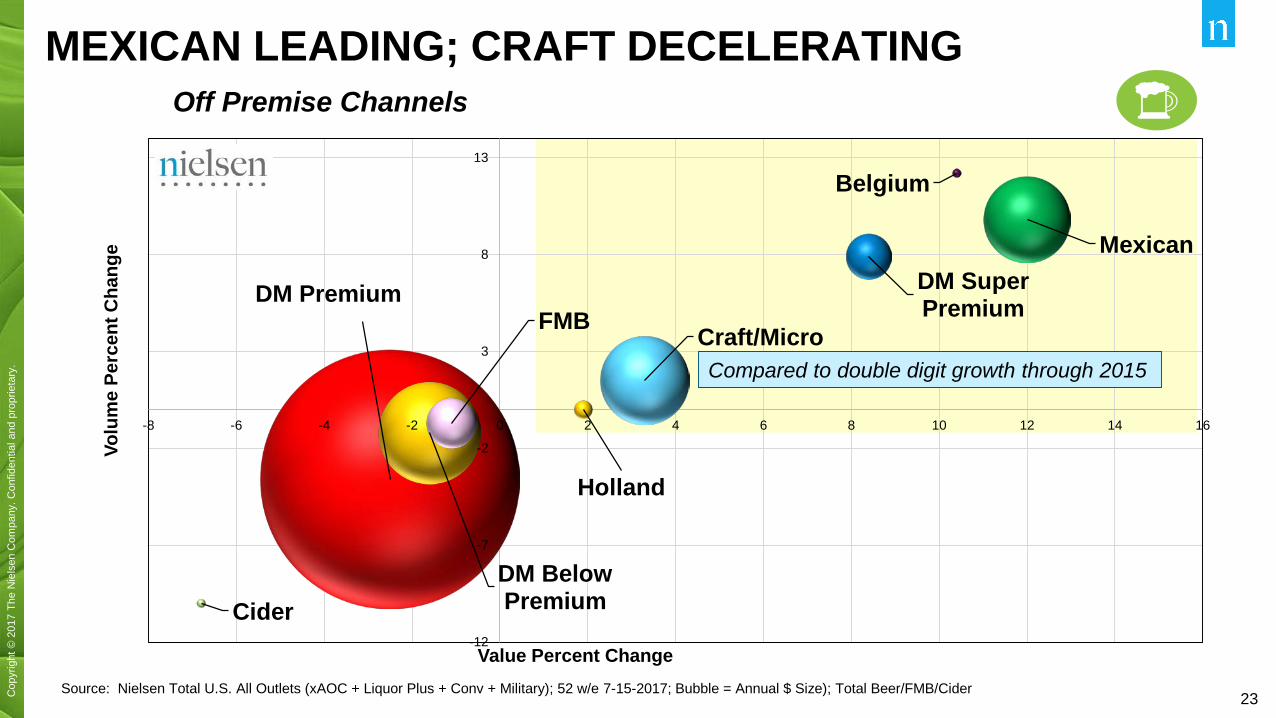

DM Premium

DM Below Premium

DM Super Premium

Mexican

Craft/MicroFMB

Holland

Belgium

Cider-12

-7

-2

3

8

13

-8 -6 -4 -2 0 2 4 6 8 10 12 14 16

Volu

me

Perc

ent C

hang

e

Value Percent Change

MEXICAN LEADING; CRAFT DECELERATINGOff Premise Channels

Source: Nielsen Total U.S. All Outlets (xAOC + Liquor Plus + Conv + Military); 52 w/e 7-15-2017; Bubble = Annual $ Size); Total Beer/FMB/Cider

Compared to double digit growth through 2015

24Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

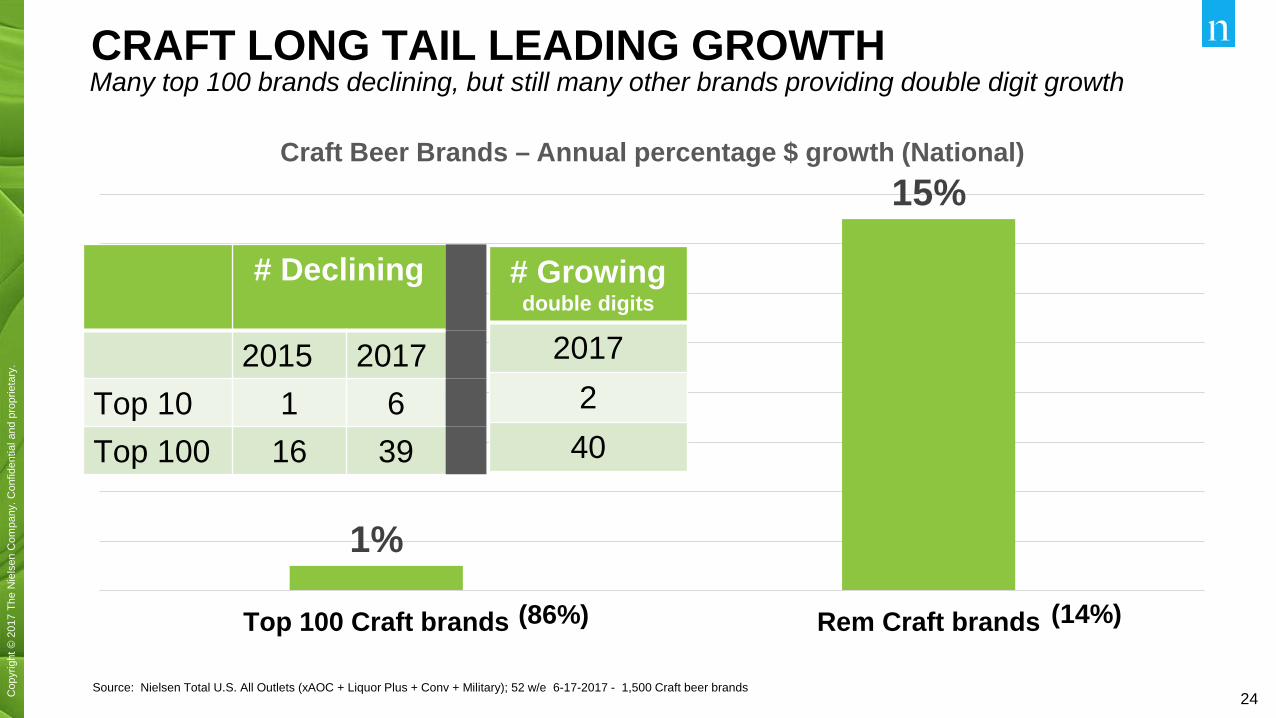

1%

15%

Top 100 Craft brands Rem Craft brands

Craft Beer Brands – Annual percentage $ growth (National)

CRAFT LONG TAIL LEADING GROWTH Many top 100 brands declining, but still many other brands providing double digit growth

Source: Nielsen Total U.S. All Outlets (xAOC + Liquor Plus + Conv + Military); 52 w/e 6-17-2017 - 1,500 Craft beer brands

(86%) (14%)

# Declining

2015 2017Top 10 1 6Top 100 16 39

# Growingdouble digits

2017240

25Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

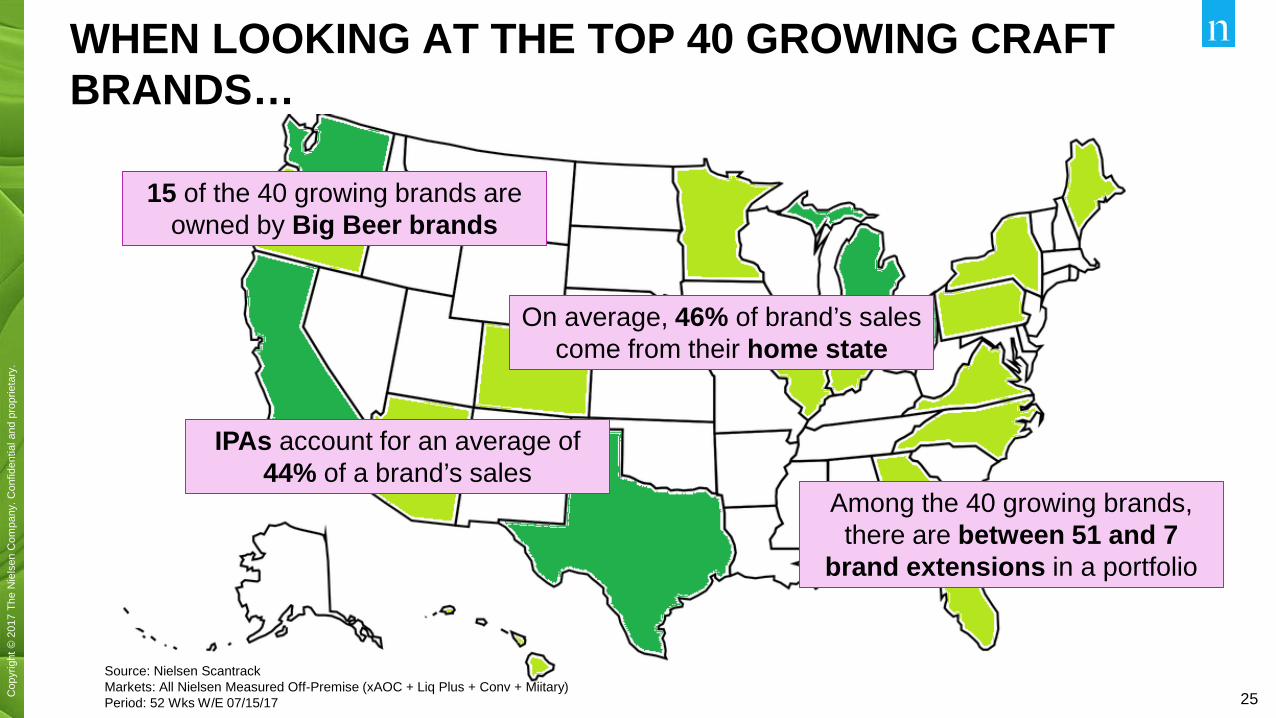

WHEN LOOKING AT THE TOP 40 GROWING CRAFT BRANDS…

Source: Nielsen ScantrackMarkets: All Nielsen Measured Off-Premise (xAOC + Liq Plus + Conv + Miitary)Period: 52 Wks W/E 07/15/17

15 of the 40 growing brands are owned by Big Beer brands

IPAs account for an average of 44% of a brand’s sales

On average, 46% of brand’s sales come from their home state

Among the 40 growing brands, there are between 51 and 7

brand extensions in a portfolio

26Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

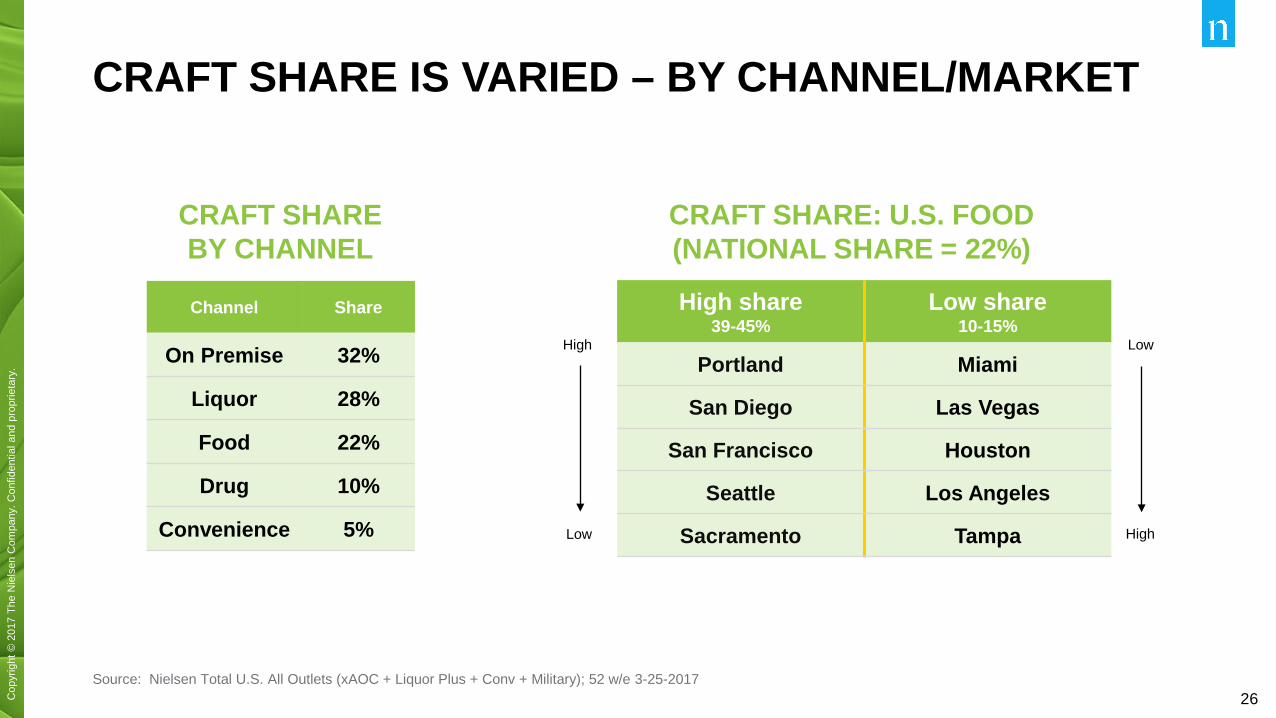

CRAFT SHARE IS VARIED – BY CHANNEL/MARKET

Source: Nielsen Total U.S. All Outlets (xAOC + Liquor Plus + Conv + Military); 52 w/e 3-25-2017

High

Low

CRAFT SHARE: U.S. FOOD(NATIONAL SHARE = 22%)

High share39-45%

Low share10-15%

Portland Miami

San Diego Las Vegas

San Francisco Houston

Seattle Los Angeles

Sacramento Tampa

Low

High

CRAFT SHARE BY CHANNEL

Channel Share

On Premise 32%

Liquor 28%

Food 22%

Drug 10%

Convenience 5%

27Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

CRAFT BEER LANDSCAPE • # of breweries still expanding fast – 2 per day• And brewer product portfolios expanding too

• Yet, meager Craft beer sales growth overall• Very little incremental space

More critical than ever to…

1. Know what the consumer is looking for2. Focus on what you do best and do it better

than everyone else

…rather than trying to be all things to all people

28Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

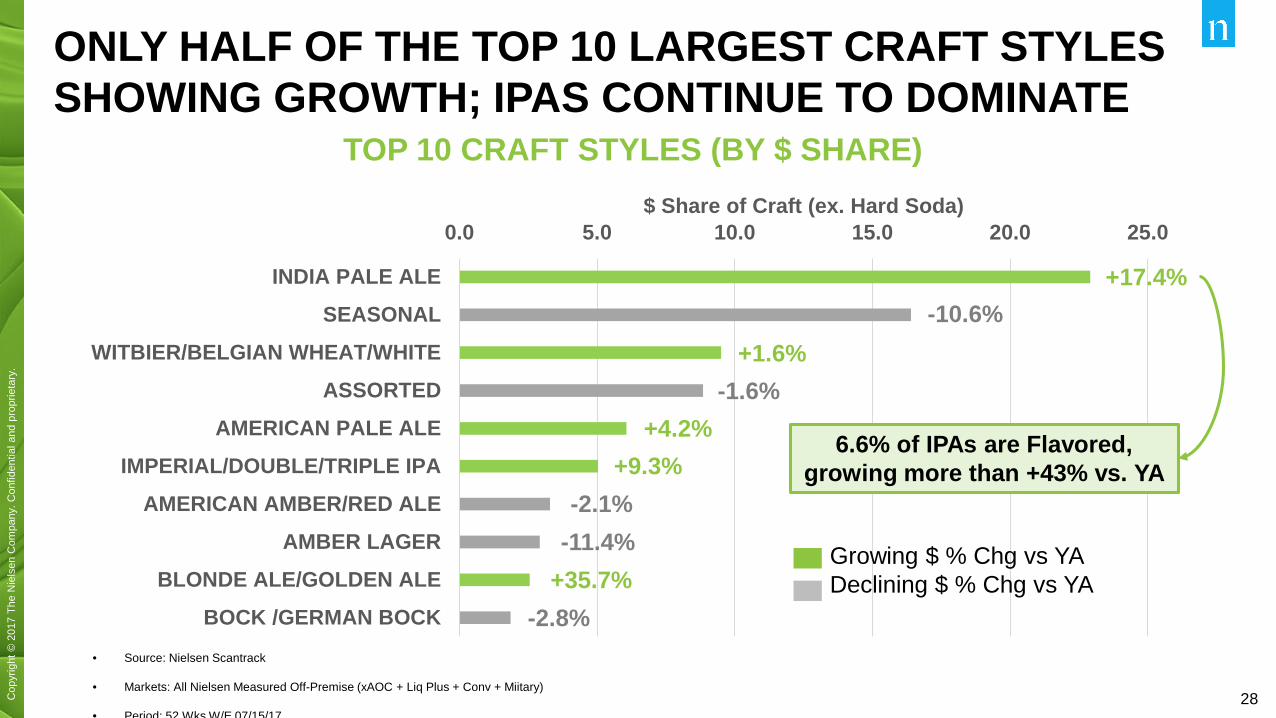

TOP 10 CRAFT STYLES (BY $ SHARE)

0.0 5.0 10.0 15.0 20.0 25.0

INDIA PALE ALESEASONAL

WITBIER/BELGIAN WHEAT/WHITEASSORTED

AMERICAN PALE ALEIMPERIAL/DOUBLE/TRIPLE IPA

AMERICAN AMBER/RED ALEAMBER LAGER

BLONDE ALE/GOLDEN ALEBOCK /GERMAN BOCK

$ Share of Craft (ex. Hard Soda)

ONLY HALF OF THE TOP 10 LARGEST CRAFT STYLES SHOWING GROWTH; IPAS CONTINUE TO DOMINATE

• Source: Nielsen Scantrack

• Markets: All Nielsen Measured Off-Premise (xAOC + Liq Plus + Conv + Miitary)

• Period: 52 Wks W/E 07/15/17

+17.4%

+1.6%

+4.2%+9.3%

+35.7%

-10.6%

-1.6%

-2.1%-11.4%

-2.8%

6.6% of IPAs are Flavored, growing more than +43% vs. YA

Growing $ % Chg vs YADeclining $ % Chg vs YA

29Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

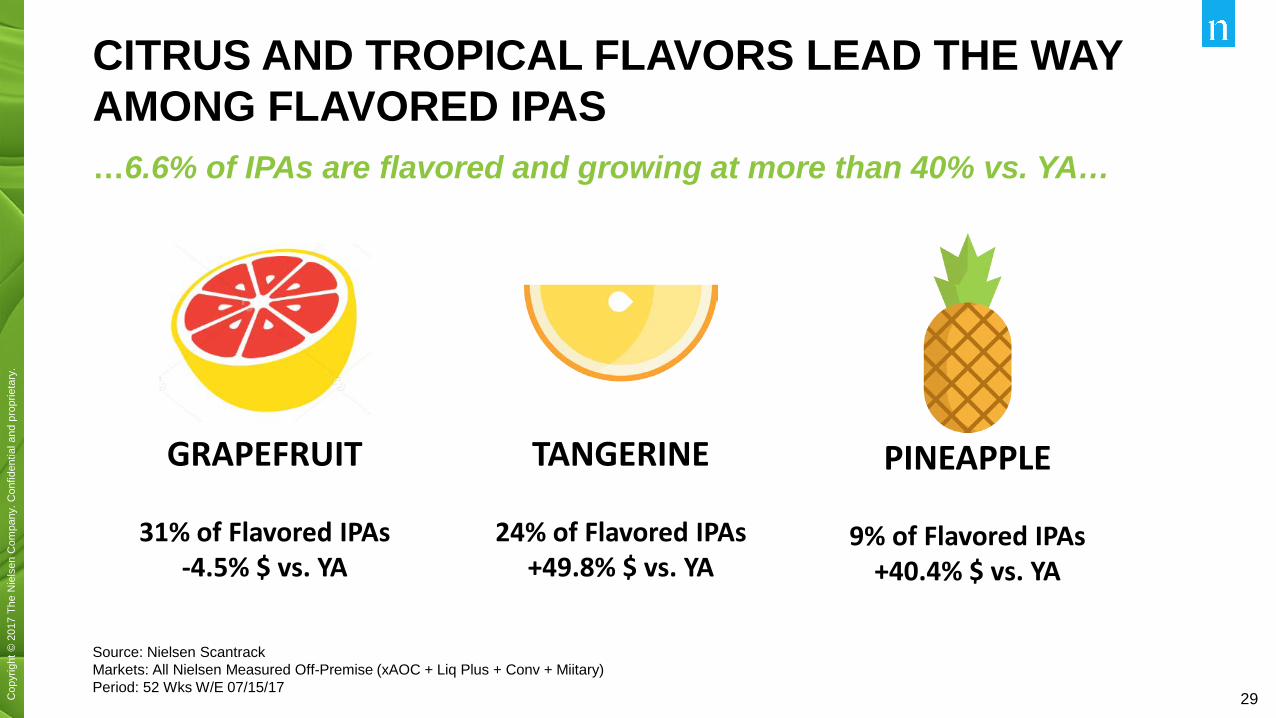

CITRUS AND TROPICAL FLAVORS LEAD THE WAY AMONG FLAVORED IPAS

Source: Nielsen ScantrackMarkets: All Nielsen Measured Off-Premise (xAOC + Liq Plus + Conv + Miitary)Period: 52 Wks W/E 07/15/17

…6.6% of IPAs are flavored and growing at more than 40% vs. YA…

GRAPEFRUIT

31% of Flavored IPAs-4.5% $ vs. YA

TANGERINE

24% of Flavored IPAs+49.8% $ vs. YA

PINEAPPLE

9% of Flavored IPAs+40.4% $ vs. YA

30Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

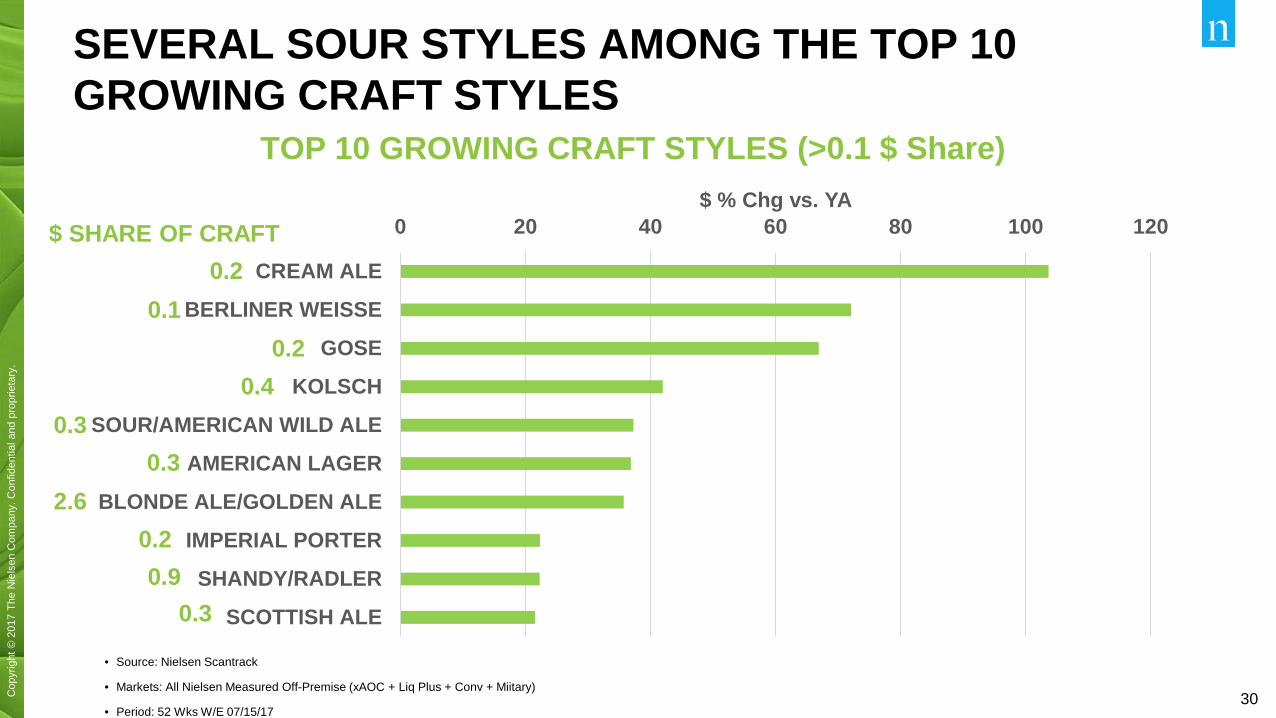

TOP 10 GROWING CRAFT STYLES (>0.1 $ Share)

0 20 40 60 80 100 120

CREAM ALE

BERLINER WEISSE

GOSE

KOLSCH

SOUR/AMERICAN WILD ALE

AMERICAN LAGER

BLONDE ALE/GOLDEN ALE

IMPERIAL PORTER

SHANDY/RADLER

SCOTTISH ALE

$ % Chg vs. YA

SEVERAL SOUR STYLES AMONG THE TOP 10 GROWING CRAFT STYLES

• Source: Nielsen Scantrack

• Markets: All Nielsen Measured Off-Premise (xAOC + Liq Plus + Conv + Miitary)

• Period: 52 Wks W/E 07/15/17

0.20.1

0.20.4

0.30.3

2.60.20.9

0.3

$ SHARE OF CRAFT

31Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

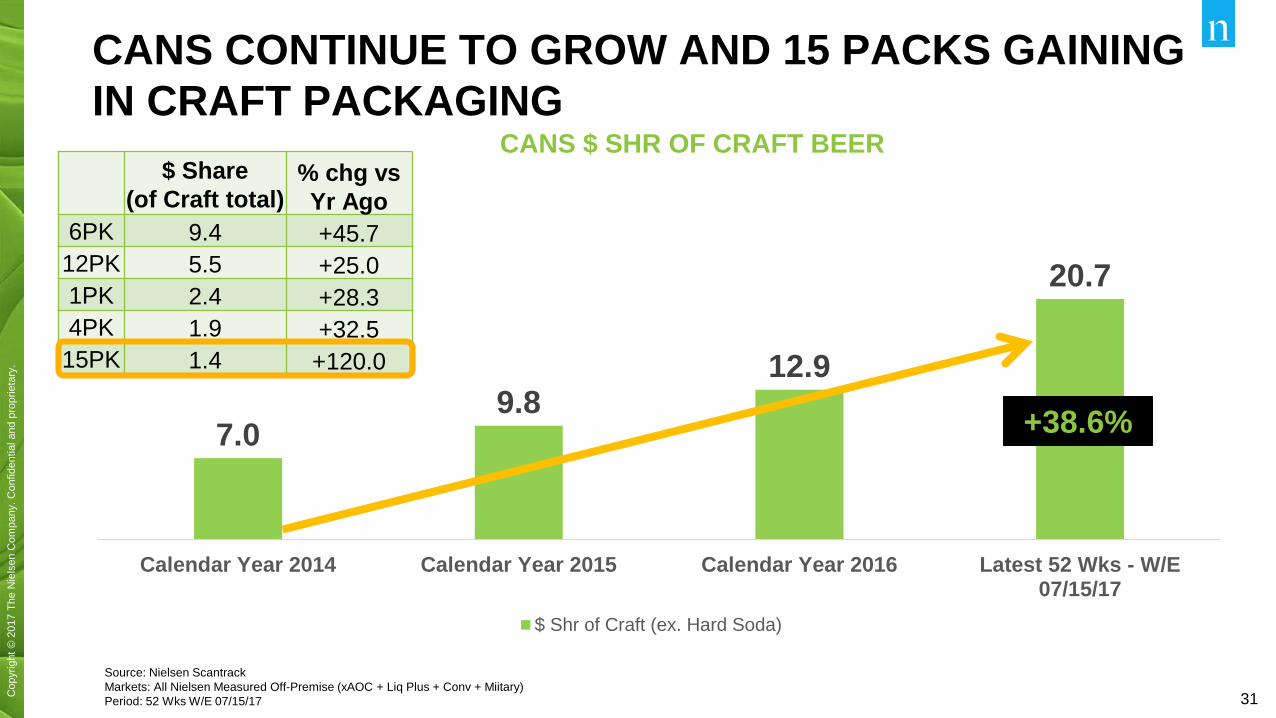

CANS $ SHR OF CRAFT BEER

7.09.8

12.9

20.7

Calendar Year 2014 Calendar Year 2015 Calendar Year 2016 Latest 52 Wks - W/E07/15/17

$ Shr of Craft (ex. Hard Soda)

CANS CONTINUE TO GROW AND 15 PACKS GAINING IN CRAFT PACKAGING

Source: Nielsen ScantrackMarkets: All Nielsen Measured Off-Premise (xAOC + Liq Plus + Conv + Miitary)Period: 52 Wks W/E 07/15/17

+38.6%

$ Share (of Craft total)

% chg vs Yr Ago

6PK 9.4 +45.712PK 5.5 +25.01PK 2.4 +28.34PK 1.9 +32.5

15PK 1.4 +120.0

32Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

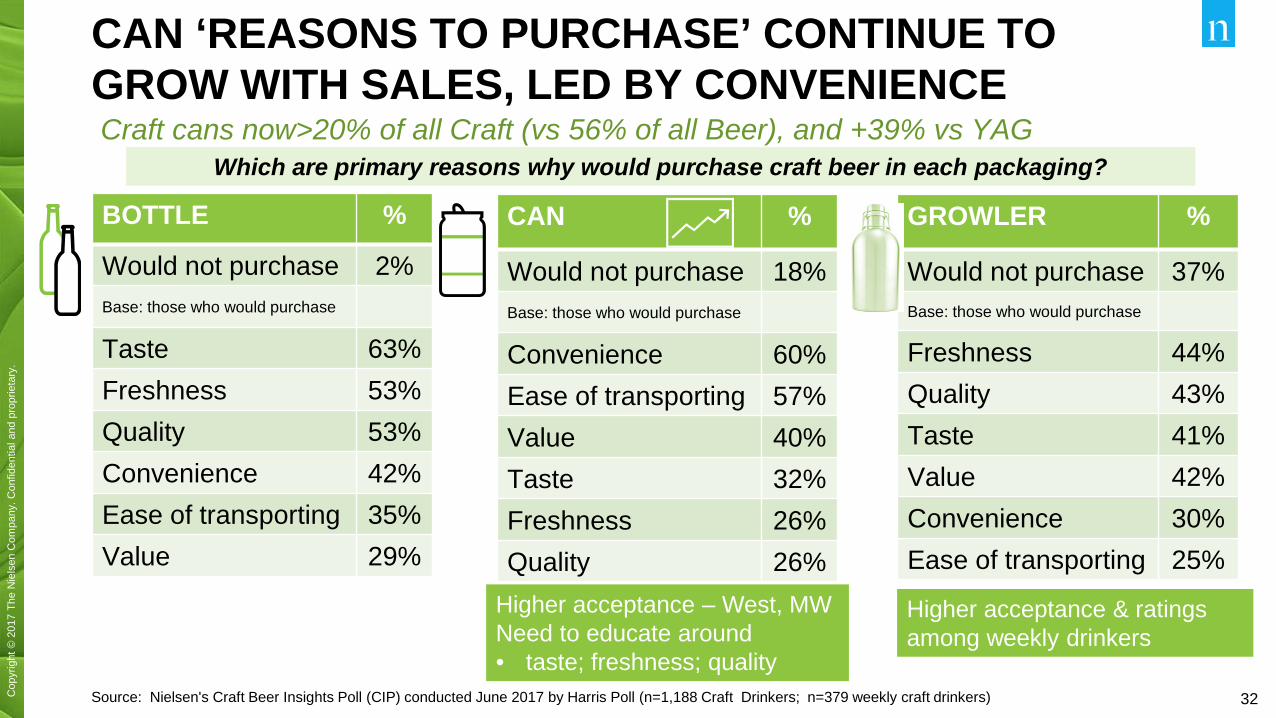

CAN ‘REASONS TO PURCHASE’ CONTINUE TO GROW WITH SALES, LED BY CONVENIENCE Craft cans now>20% of all Craft (vs 56% of all Beer), and +39% vs YAG

Source: Nielsen's Craft Beer Insights Poll (CIP) conducted June 2017 by Harris Poll (n=1,188 Craft Drinkers; n=379 weekly craft drinkers)

BOTTLE %

Would not purchase 2%Base: those who would purchase

Taste 63%Freshness 53%Quality 53%Convenience 42%Ease of transporting 35%Value 29%

CAN %

Would not purchase 18%Base: those who would purchase

Convenience 60%Ease of transporting 57%Value 40%Taste 32%Freshness 26%Quality 26%

GROWLER %

Would not purchase 37%Base: those who would purchase

Freshness 44%Quality 43%Taste 41%Value 42%Convenience 30%Ease of transporting 25%

Which are primary reasons why would purchase craft beer in each packaging?

Higher acceptance – West, MWNeed to educate around• taste; freshness; quality

Higher acceptance & ratings among weekly drinkers

33Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

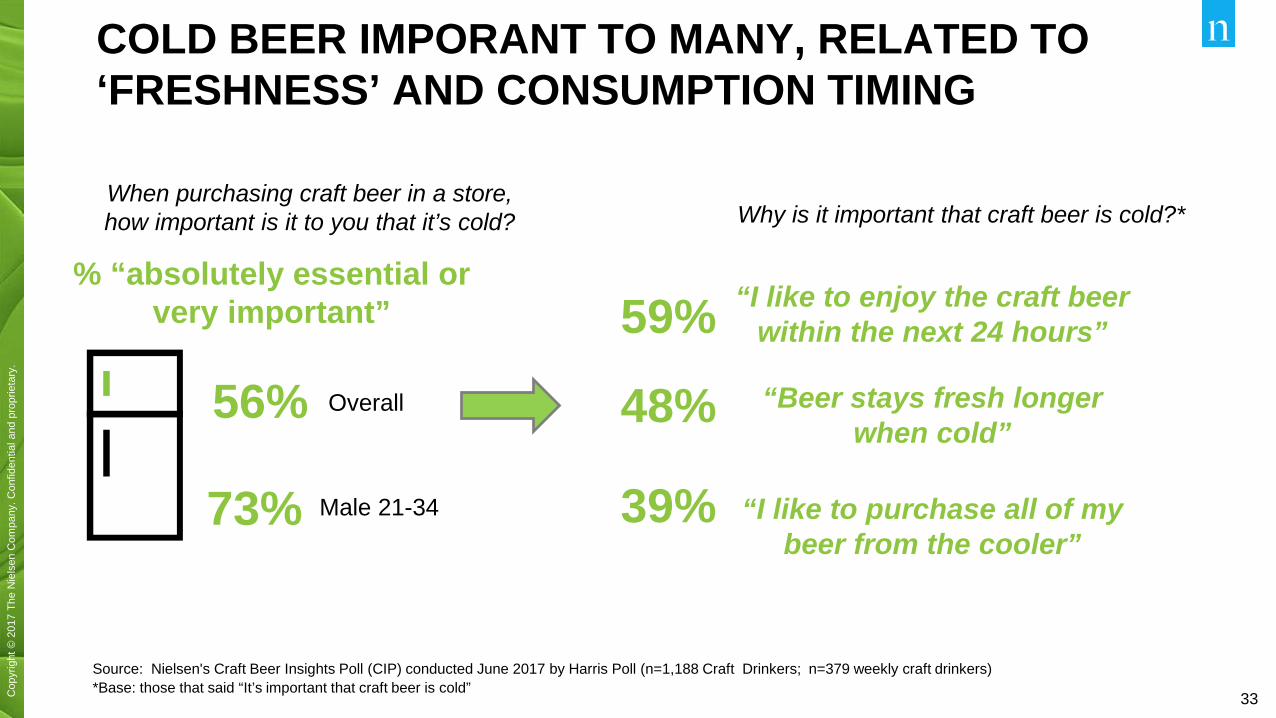

COLD BEER IMPORANT TO MANY, RELATED TO‘FRESHNESS’ AND CONSUMPTION TIMING

Source: Nielsen's Craft Beer Insights Poll (CIP) conducted June 2017 by Harris Poll (n=1,188 Craft Drinkers; n=379 weekly craft drinkers)*Base: those that said “It’s important that craft beer is cold”

56%

When purchasing craft beer in a store, how important is it to you that it’s cold?

73%

% “absolutely essential or very important”

Male 21-34

Overall

Why is it important that craft beer is cold?*

“I like to enjoy the craft beer within the next 24 hours”59%

48% “Beer stays fresh longer when cold”

39% “I like to purchase all of my beer from the cooler”

34Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

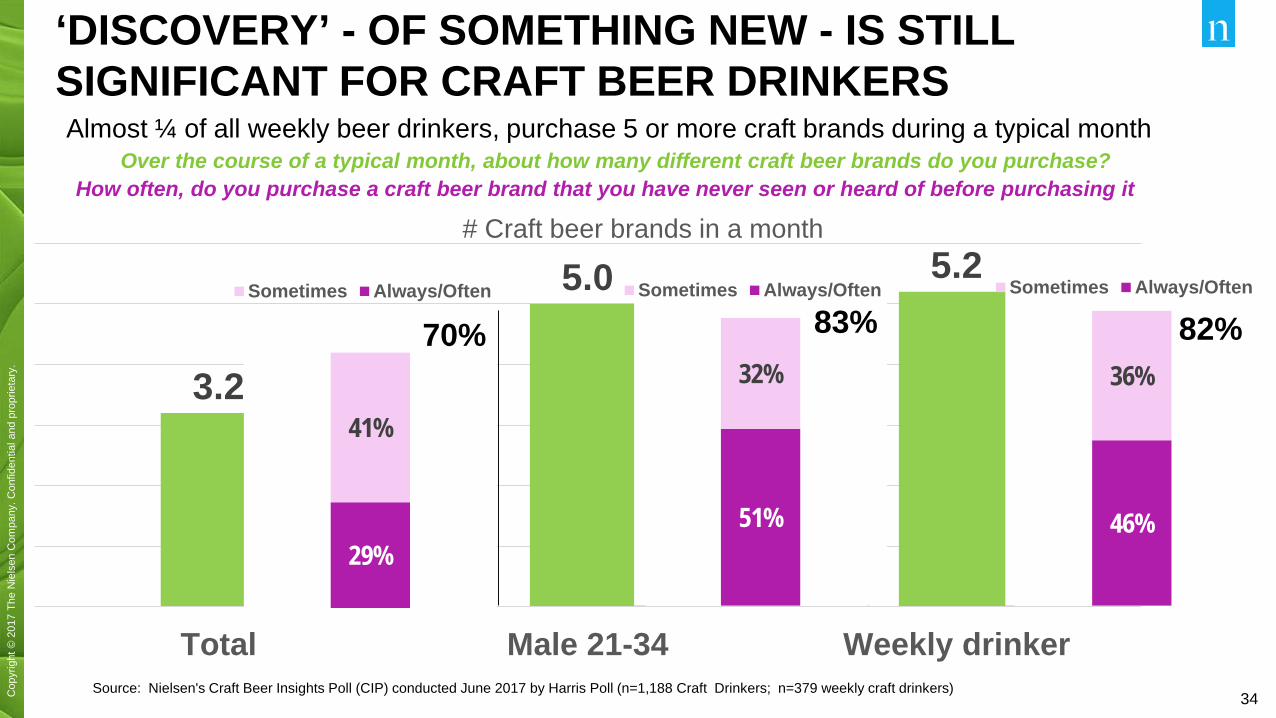

‘DISCOVERY’ - OF SOMETHING NEW - IS STILL SIGNIFICANT FOR CRAFT BEER DRINKERS

Source: Nielsen's Craft Beer Insights Poll (CIP) conducted June 2017 by Harris Poll (n=1,188 Craft Drinkers; n=379 weekly craft drinkers)

3.2

5.0 5.2

Total Male 21-34 Weekly drinker

# Craft beer brands in a month

Over the course of a typical month, about how many different craft beer brands do you purchase?Almost ¼ of all weekly beer drinkers, purchase 5 or more craft brands during a typical month

29%

41%

Sometimes Always/Often

51%

32%

Sometimes Always/Often

46%

36%

Sometimes Always/Often

How often, do you purchase a craft beer brand that you have never seen or heard of before purchasing it

70% 83% 82%

35Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

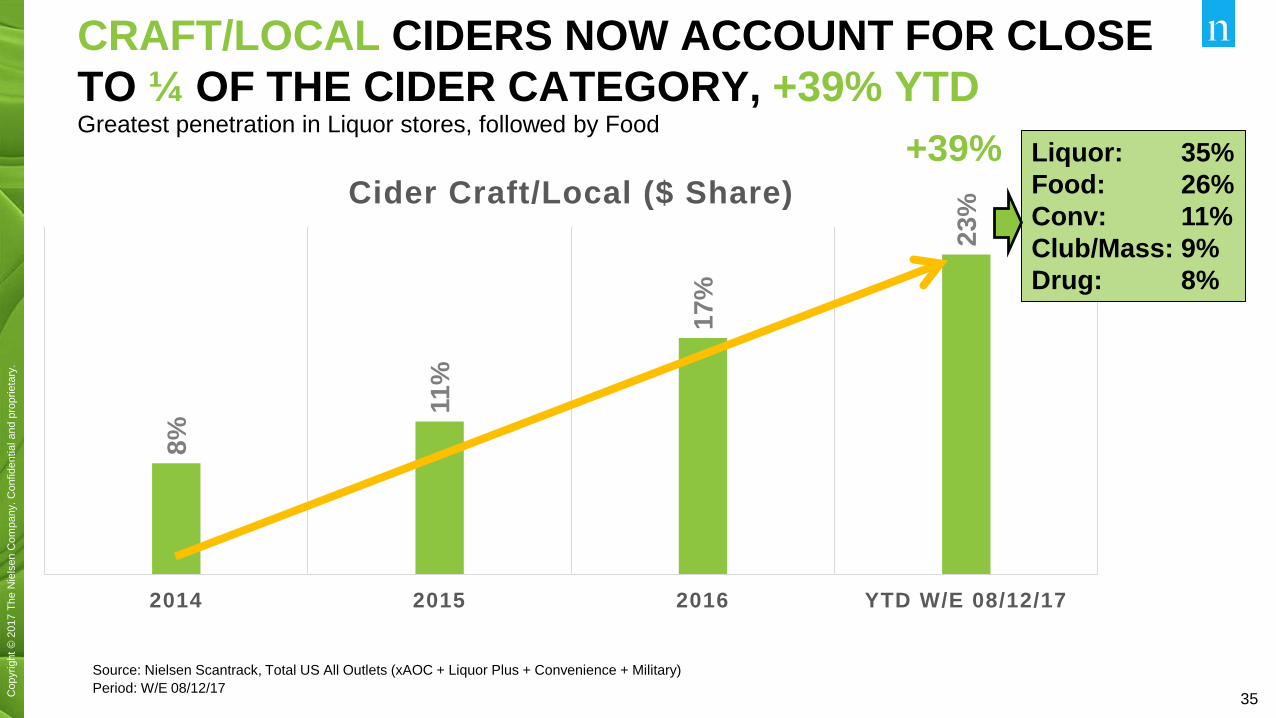

CRAFT/LOCAL CIDERS NOW ACCOUNT FOR CLOSE TO ¼ OF THE CIDER CATEGORY, +39% YTD

Source: Nielsen Scantrack, Total US All Outlets (xAOC + Liquor Plus + Convenience + Military)Period: W/E 08/12/17

8%

11%

17%

23%

2014 2015 2016 YTD W/E 08/12/17

Cider Craft/Local ($ Share)Liquor: 35%Food: 26%Conv: 11%Club/Mass: 9%Drug: 8%

Greatest penetration in Liquor stores, followed by Food+39%

36Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

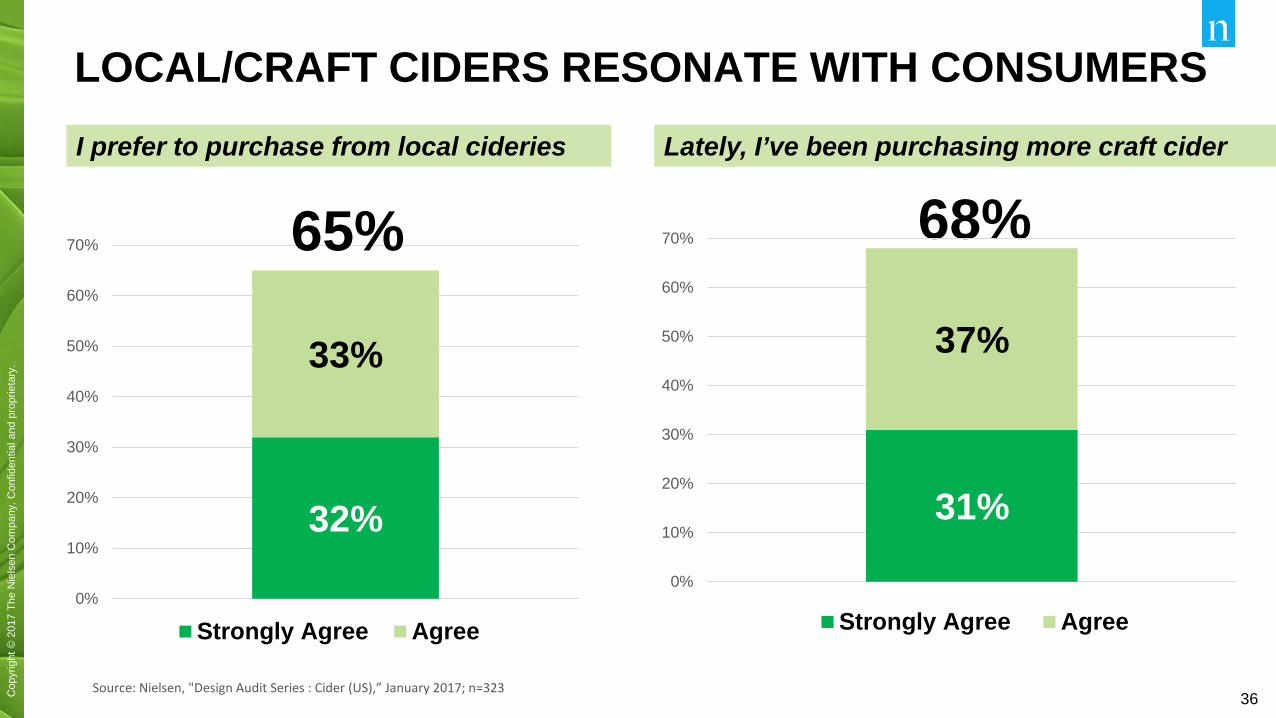

LOCAL/CRAFT CIDERS RESONATE WITH CONSUMERS

Source: Nielsen, "Design Audit Series : Cider (US),” January 2017; n=323

32%

33%

0%

10%

20%

30%

40%

50%

60%

70%

Strongly Agree Agree

I prefer to purchase from local cideries Lately, I’ve been purchasing more craft cider

65% 68%

31%

37%

0%

10%

20%

30%

40%

50%

60%

70%

Strongly Agree Agree

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

WINE

38Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

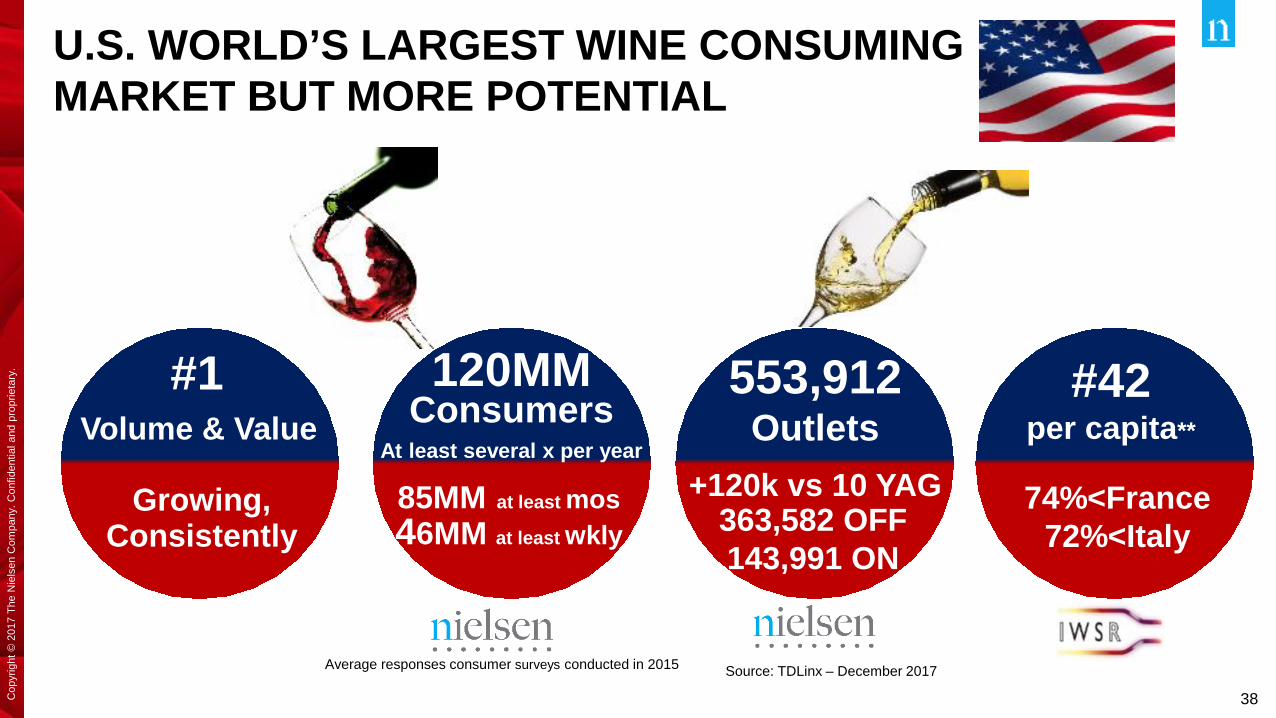

U.S. WORLD’S LARGEST WINE CONSUMING MARKET BUT MORE POTENTIAL

Average responses consumer surveys conducted in 2015

#1

Growing, Consistently

Volume & Value120MM

ConsumersAt least several x per year

85MM at least mos46MM at least wkly

Source: TDLinx – December 2017

553,912Outlets

+120k vs 10 YAG363,582 OFF143,991 ON

#42 per capita**

74%<France72%<Italy

39Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

40Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

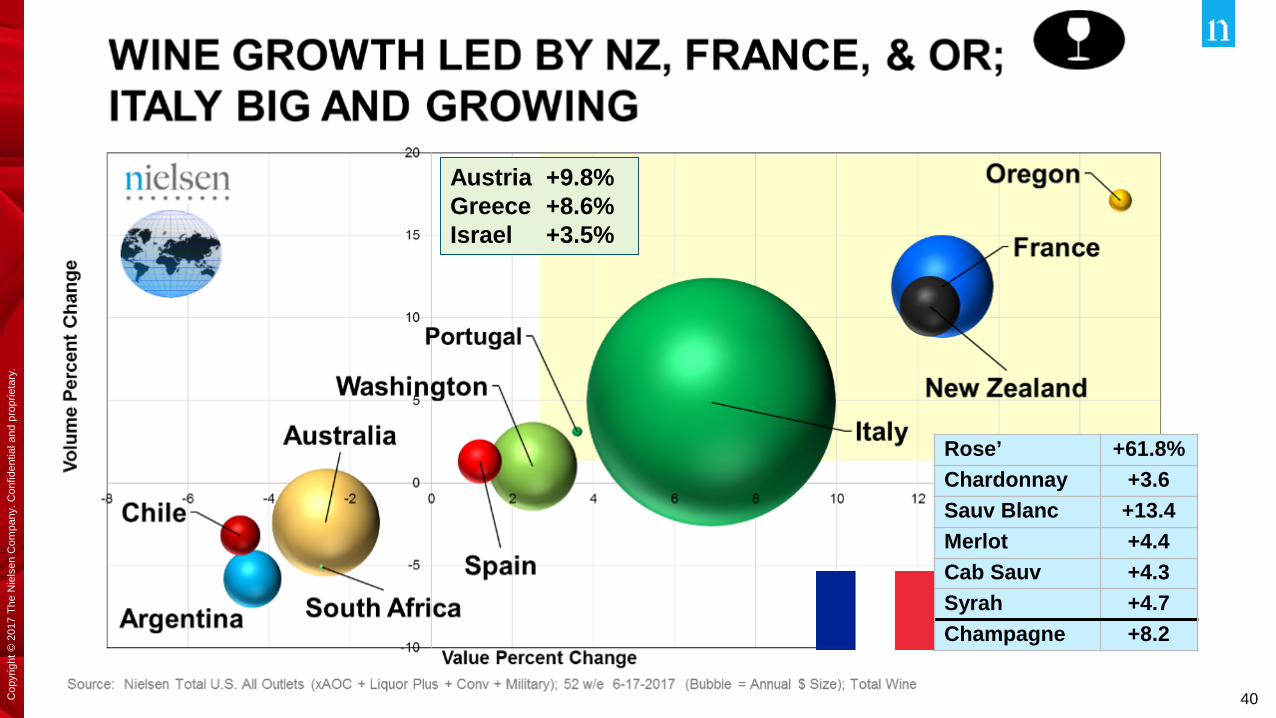

Austria +9.8%Greece +8.6%Israel +3.5%

Rose’ +61.8%Chardonnay +3.6Sauv Blanc +13.4Merlot +4.4Cab Sauv +4.3Syrah +4.7Champagne +8.2

41Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

42Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

$-

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

$300,000,000

$350,000,000

$400,000,0006/

15/2

013

7/15

/201

38/

15/2

013

9/15

/201

310

/15/

2013

11/1

5/20

1312

/15/

2013

1/15

/201

42/

15/2

014

3/15

/201

44/

15/2

014

5/15

/201

46/

15/2

014

7/15

/201

48/

15/2

014

9/15

/201

410

/15/

2014

11/1

5/20

1412

/15/

2014

1/15

/201

52/

15/2

015

3/15

/201

54/

15/2

015

5/15

/201

56/

15/2

015

7/15

/201

58/

15/2

015

9/15

/201

510

/15/

2015

11/1

5/20

1512

/15/

2015

1/15

/201

62/

15/2

016

3/15

/201

64/

15/2

016

5/15

/201

66/

15/2

016

7/15

/201

68/

15/2

016

9/15

/201

610

/15/

2016

11/1

5/20

1612

/15/

2016

1/15

/201

72/

15/2

017

3/15

/201

74/

15/2

017

5/15

/201

76/

15/2

017

7/15

/201

7

Rose’ (Table + Sparkling) – rolling 52 week dollars

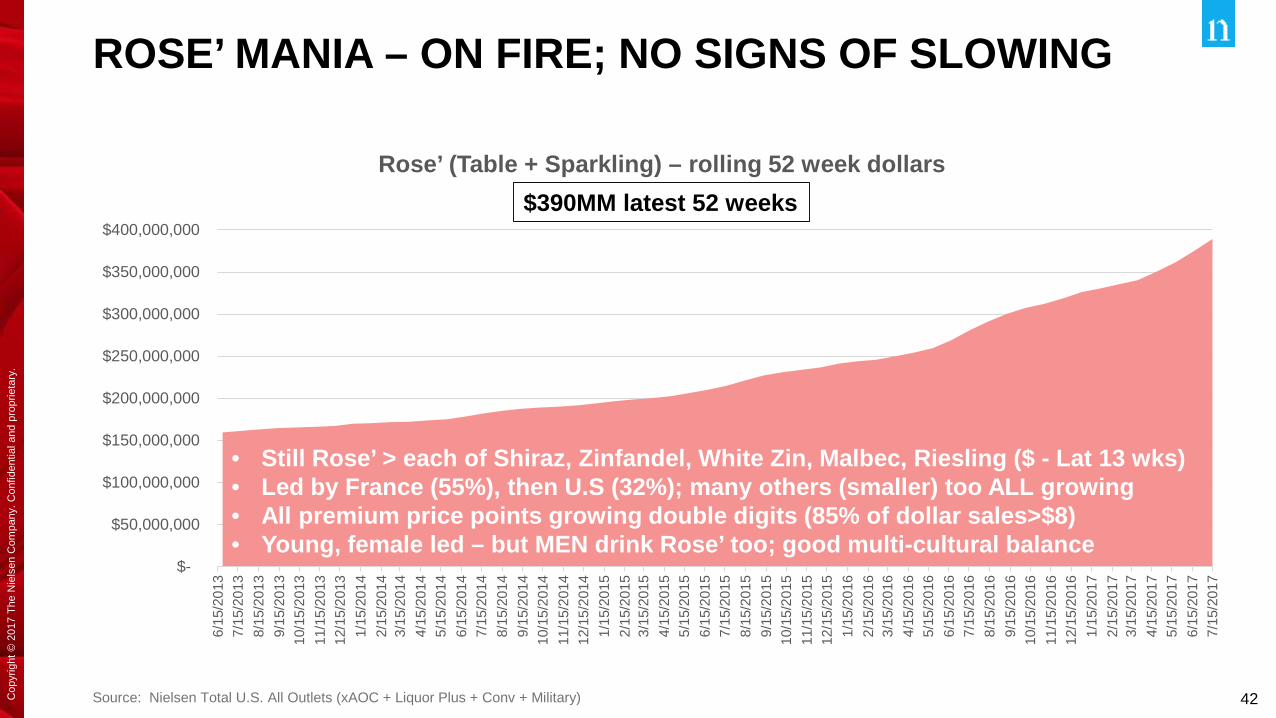

ROSE’ MANIA – ON FIRE; NO SIGNS OF SLOWING

Source: Nielsen Total U.S. All Outlets (xAOC + Liquor Plus + Conv + Military)

$390MM latest 52 weeks

• Still Rose’ > each of Shiraz, Zinfandel, White Zin, Malbec, Riesling ($ - Lat 13 wks)• Led by France (55%), then U.S (32%); many others (smaller) too ALL growing• All premium price points growing double digits (85% of dollar sales>$8)• Young, female led – but MEN drink Rose’ too; good multi-cultural balance

43Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

ROSE’ MANIA – ON FIRE; NO SIGNS OF SLOWINGFrom the pink walls/displays to Rose’ extensions beyond Wine

44Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

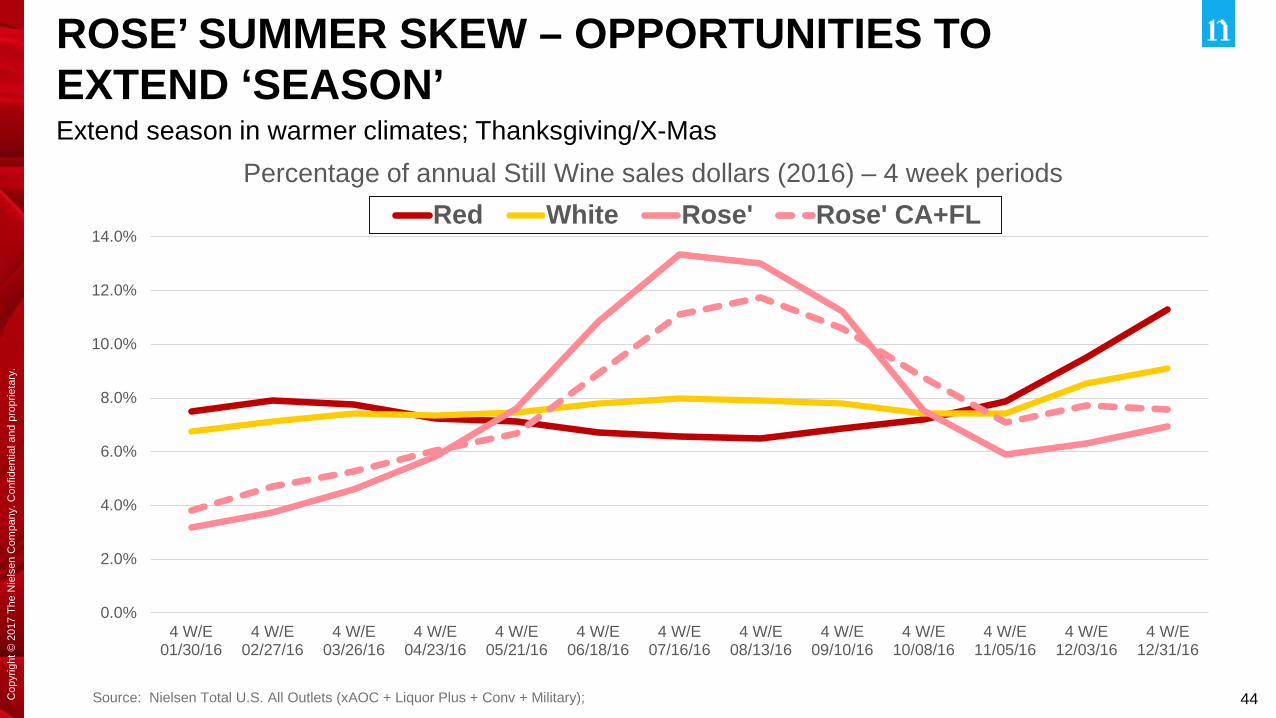

ROSE’ SUMMER SKEW – OPPORTUNITIES TO EXTEND ‘SEASON’

Source: Nielsen Total U.S. All Outlets (xAOC + Liquor Plus + Conv + Military);

0.0%

2.0%

4.0%

6.0%

8.0%

10.0%

12.0%

14.0%

4 W/E01/30/16

4 W/E02/27/16

4 W/E03/26/16

4 W/E04/23/16

4 W/E05/21/16

4 W/E06/18/16

4 W/E07/16/16

4 W/E08/13/16

4 W/E09/10/16

4 W/E10/08/16

4 W/E11/05/16

4 W/E12/03/16

4 W/E12/31/16

Percentage of annual Still Wine sales dollars (2016) – 4 week periodsRed White Rose' Rose' CA+FL

Extend season in warmer climates; Thanksgiving/X-Mas

45Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

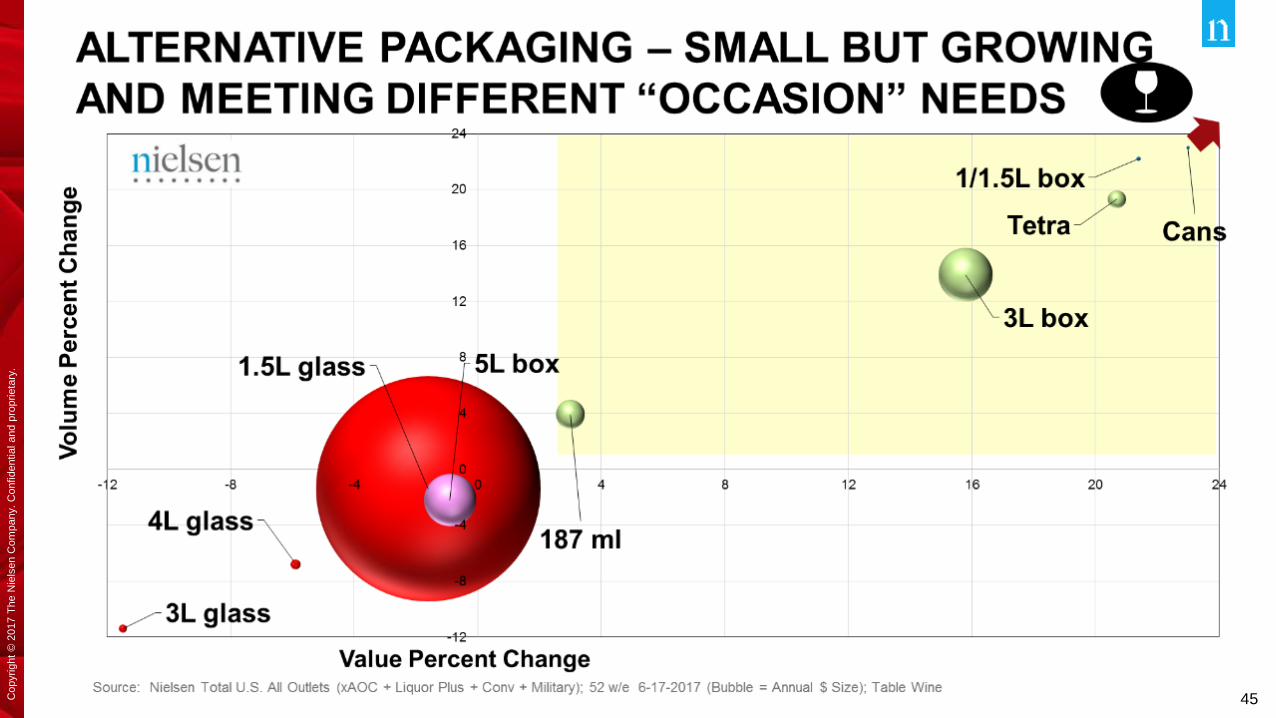

WINE PACK INNOVATION REFLECTED IN STORE MERCHANDISING

47Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

$0

$1,000,000

$2,000,000

$3,000,000

$4,000,000

$5,000,000

$6,000,0004

W/E

08/

18/1

24

W/E

09/

15/1

24

W/E

10/

13/1

24

W/E

11/

10/1

24

W/E

12/

08/1

24

W/E

01/

05/1

34

W/E

02/

02/1

34

W/E

03/

02/1

34

W/E

03/

30/1

34

W/E

04/

27/1

34

W/E

05/

25/1

34

W/E

06/

22/1

34

W/E

07/

20/1

34

W/E

08/

17/1

34

W/E

09/

14/1

34

W/E

10/

12/1

34

W/E

11/

09/1

34

W/E

12/

07/1

34

W/E

01/

04/1

44

W/E

02/

01/1

44

W/E

03/

01/1

44

W/E

03/

29/1

44

W/E

04/

26/1

44

W/E

05/

24/1

44

W/E

06/

21/1

44

W/E

07/

19/1

44

W/E

08/

16/1

44

W/E

09/

13/1

44

W/E

10/

11/1

44

W/E

11/

08/1

44

W/E

12/

06/1

44

W/E

01/

03/1

54

W/E

01/

31/1

54

W/E

02/

28/1

54

W/E

03/

28/1

54

W/E

04/

25/1

54

W/E

05/

23/1

54

W/E

06/

20/1

54

W/E

07/

18/1

54

W/E

08/

15/1

54

W/E

09/

12/1

54

W/E

10/

10/1

54

W/E

11/

07/1

54

W/E

12/

05/1

54

W/E

01/

02/1

64

W/E

01/

30/1

64

W/E

02/

27/1

64

W/E

03/

26/1

64

W/E

04/

23/1

64

W/E

05/

21/1

64

W/E

06/

18/1

64

W/E

07/

16/1

64

W/E

08/

13/1

64

W/E

09/

10/1

64

W/E

10/

08/1

64

W/E

11/

05/1

64

W/E

12/

03/1

64

W/E

12/

31/1

64

W/E

01/

28/1

74

W/E

02/

25/1

74

W/E

03/

25/1

74

W/E

04/

22/1

74

W/E

05/

20/1

74

W/E

06/

17/1

74

W/E

07/

15/1

7

4 week periods (National dollar sales) – through 7-15-2017

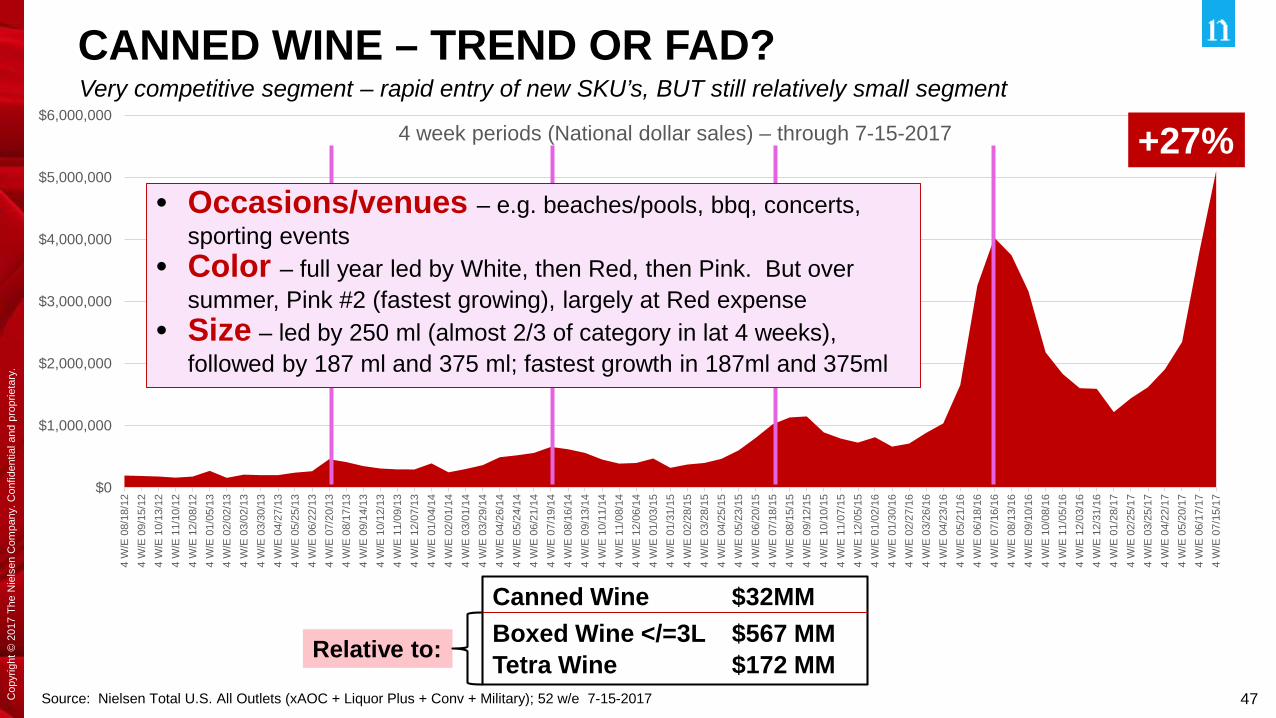

CANNED WINE – TREND OR FAD?

Source: Nielsen Total U.S. All Outlets (xAOC + Liquor Plus + Conv + Military); 52 w/e 7-15-2017

Canned Wine $32MM Boxed Wine </=3L $567 MMTetra Wine $172 MMRelative to:

+27%• Occasions/venues – e.g. beaches/pools, bbq, concerts,

sporting events• Color – full year led by White, then Red, then Pink. But over

summer, Pink #2 (fastest growing), largely at Red expense• Size – led by 250 ml (almost 2/3 of category in lat 4 weeks),

followed by 187 ml and 375 ml; fastest growth in 187ml and 375ml

Very competitive segment – rapid entry of new SKU’s, BUT still relatively small segment

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

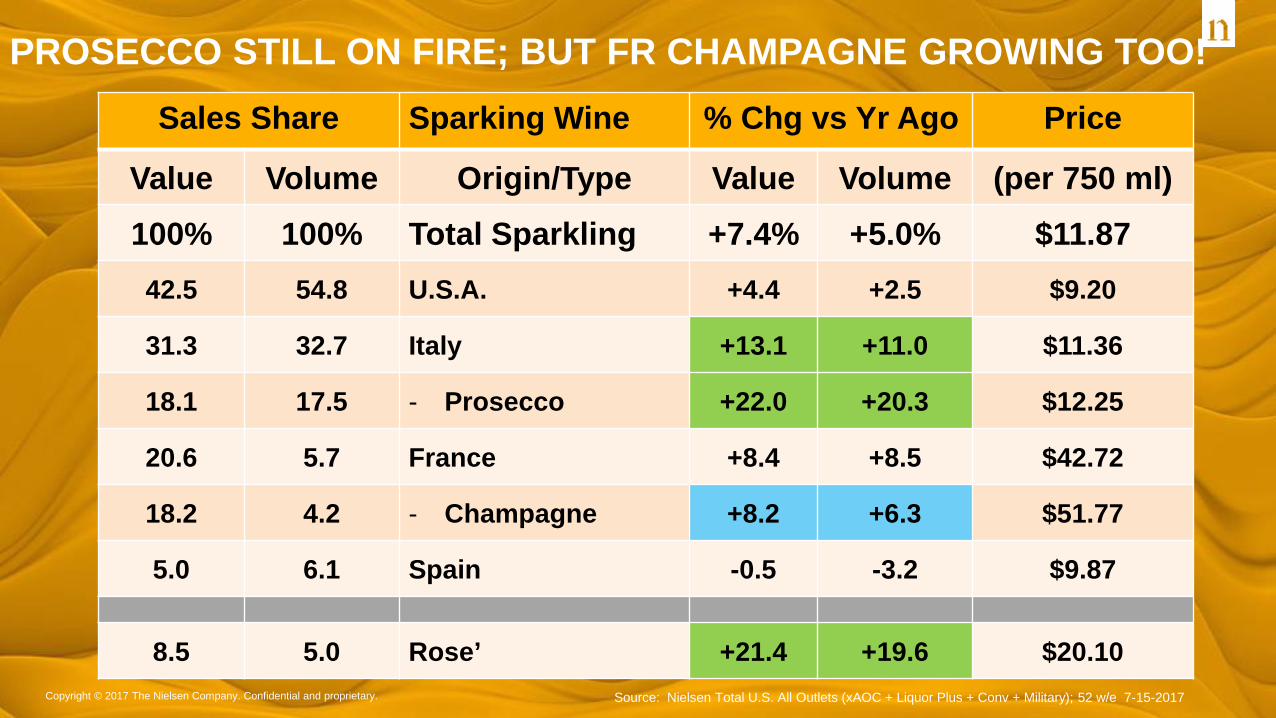

Sales Share Sparking Wine % Chg vs Yr Ago Price

Value Volume Origin/Type Value Volume (per 750 ml)100% 100% Total Sparkling +7.4% +5.0% $11.8742.5 54.8 U.S.A. +4.4 +2.5 $9.20

31.3 32.7 Italy +13.1 +11.0 $11.36

18.1 17.5 - Prosecco +22.0 +20.3 $12.25

20.6 5.7 France +8.4 +8.5 $42.72

18.2 4.2 - Champagne +8.2 +6.3 $51.77

5.0 6.1 Spain -0.5 -3.2 $9.87

8.5 5.0 Rose’ +21.4 +19.6 $20.10

PROSECCO STILL ON FIRE; BUT FR CHAMPAGNE GROWING TOO!

Source: Nielsen Total U.S. All Outlets (xAOC + Liquor Plus + Conv + Military); 52 w/e 7-15-2017

49Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

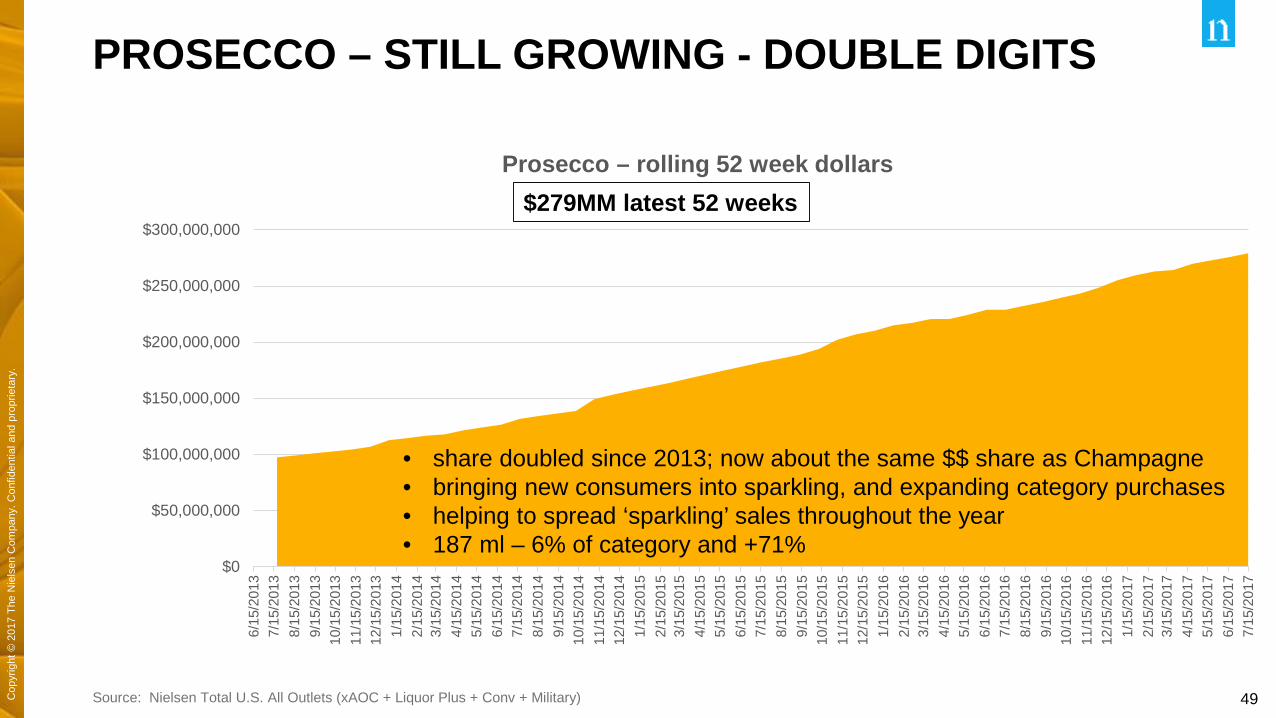

PROSECCO – STILL GROWING - DOUBLE DIGITS

Source: Nielsen Total U.S. All Outlets (xAOC + Liquor Plus + Conv + Military)

$0

$50,000,000

$100,000,000

$150,000,000

$200,000,000

$250,000,000

$300,000,0006/

15/2

013

7/15

/201

38/

15/2

013

9/15

/201

310

/15/

2013

11/1

5/20

1312

/15/

2013

1/15

/201

42/

15/2

014

3/15

/201

44/

15/2

014

5/15

/201

46/

15/2

014

7/15

/201

48/

15/2

014

9/15

/201

410

/15/

2014

11/1

5/20

1412

/15/

2014

1/15

/201

52/

15/2

015

3/15

/201

54/

15/2

015

5/15

/201

56/

15/2

015

7/15

/201

58/

15/2

015

9/15

/201

510

/15/

2015

11/1

5/20

1512

/15/

2015

1/15

/201

62/

15/2

016

3/15

/201

64/

15/2

016

5/15

/201

66/

15/2

016

7/15

/201

68/

15/2

016

9/15

/201

610

/15/

2016

11/1

5/20

1612

/15/

2016

1/15

/201

72/

15/2

017

3/15

/201

74/

15/2

017

5/15

/201

76/

15/2

017

7/15

/201

7

Prosecco – rolling 52 week dollars$279MM latest 52 weeks

• share doubled since 2013; now about the same $$ share as Champagne• bringing new consumers into sparkling, and expanding category purchases• helping to spread ‘sparkling’ sales throughout the year• 187 ml – 6% of category and +71%

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

SPIRITS• Price (least expensive per serving)• Diversity and versatility - every drink

can be a new drink• Expanding demographics

51Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

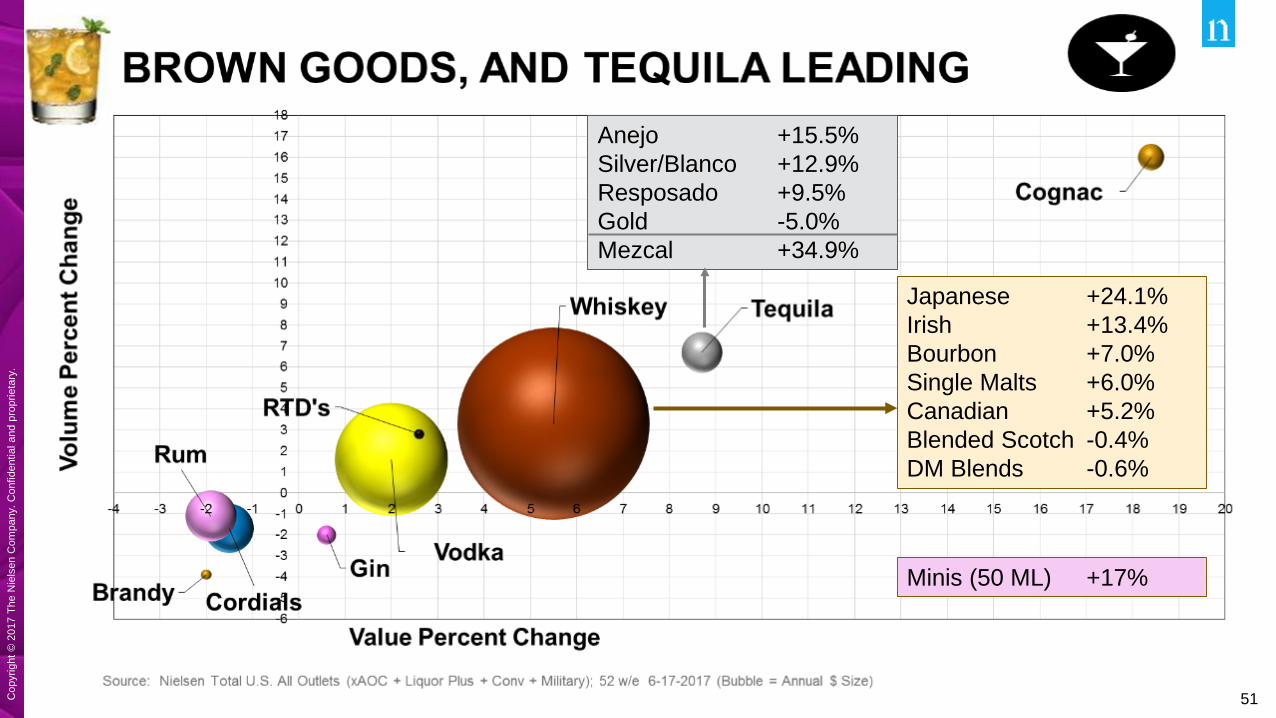

Japanese +24.1%Irish +13.4%Bourbon +7.0%Single Malts +6.0%Canadian +5.2%Blended Scotch -0.4%DM Blends -0.6%

Anejo +15.5%Silver/Blanco +12.9%Resposado +9.5%Gold -5.0%Mezcal +34.9%

Minis (50 ML) +17%

52Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

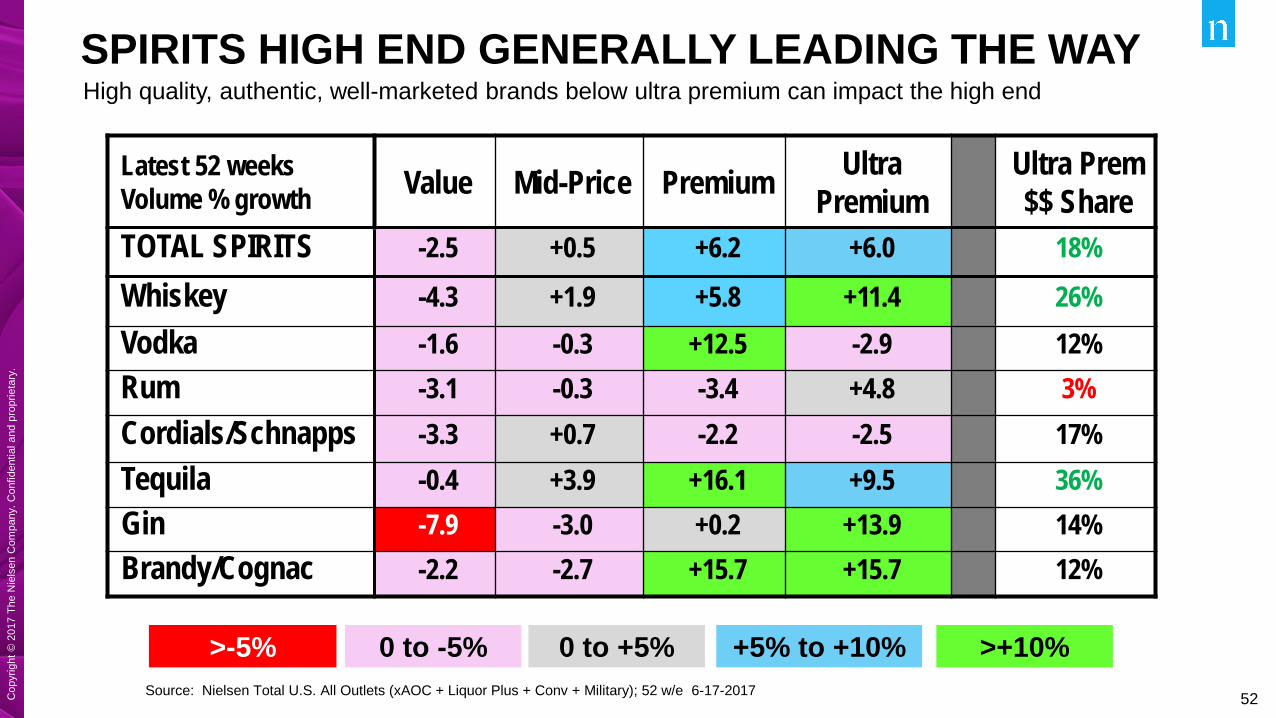

SPIRITS HIGH END GENERALLY LEADING THE WAY

Latest 52 weeksVolume % growth Value Mid-Price Premium Ultra

PremiumUltra Prem $$ Share

TOTAL SPIRITS -2.5 +0.5 +6.2 +6.0 18%Whiskey -4.3 +1.9 +5.8 +11.4 26%Vodka -1.6 -0.3 +12.5 -2.9 12%Rum -3.1 -0.3 -3.4 +4.8 3%Cordials/Schnapps -3.3 +0.7 -2.2 -2.5 17%Tequila -0.4 +3.9 +16.1 +9.5 36%Gin -7.9 -3.0 +0.2 +13.9 14%Brandy/Cognac -2.2 -2.7 +15.7 +15.7 12%

>-5% >+10%+5% to +10%0 to -5% 0 to +5%Source: Nielsen Total U.S. All Outlets (xAOC + Liquor Plus + Conv + Military); 52 w/e 6-17-2017

High quality, authentic, well-marketed brands below ultra premium can impact the high end

53Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.C

opyr

ight

© 2

017

The

Nie

lsen

Com

pany

. Con

fiden

tial a

nd p

ropr

ieta

ry.

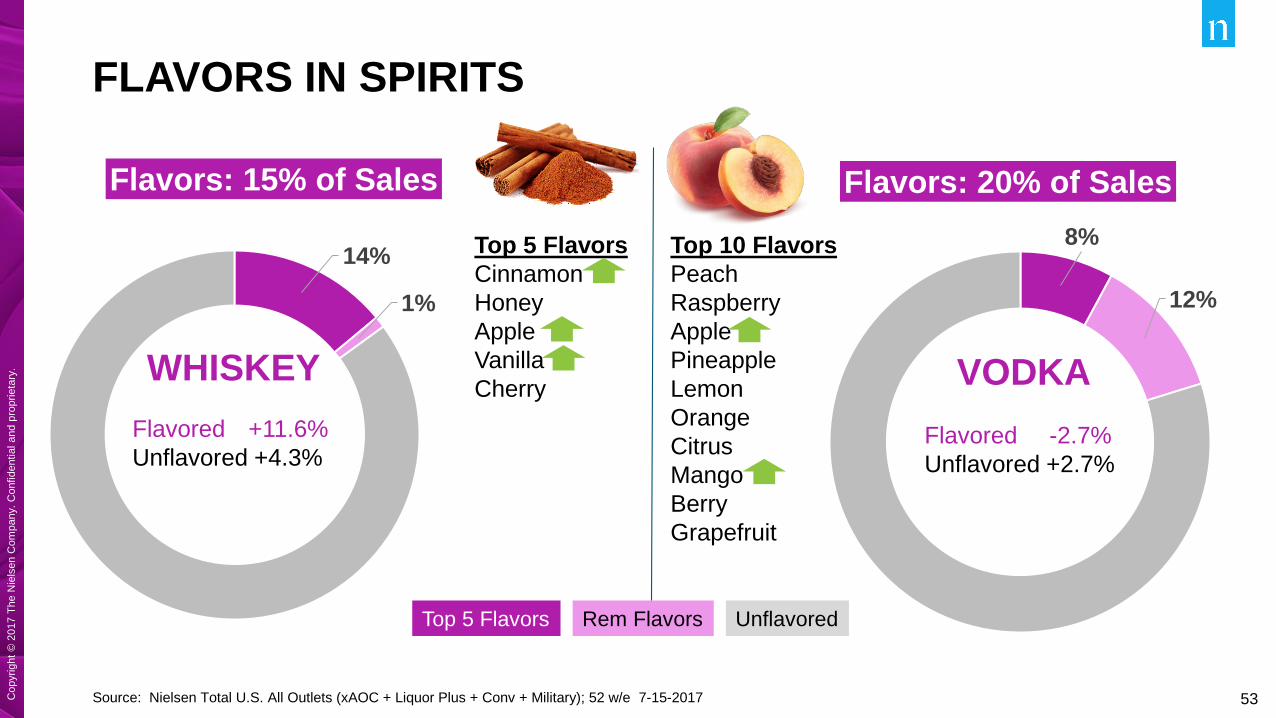

FLAVORS IN SPIRITS

Source: Nielsen Total U.S. All Outlets (xAOC + Liquor Plus + Conv + Military); 52 w/e 7-15-2017

Top 5 Flavors Rem Flavors Unflavored

Top 10 FlavorsPeachRaspberryApplePineappleLemonOrangeCitrusMangoBerryGrapefruit

Top 5 FlavorsCinnamonHoneyAppleVanillaCherry

14%

1%

Flavors: 15% of Sales

WHISKEYFlavored +11.6%Unflavored +4.3%

8%

12%

Flavors: 20% of Sales

VODKAFlavored -2.7%Unflavored +2.7%

54Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

CHANGE, CHANGE, CHANGE

55Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

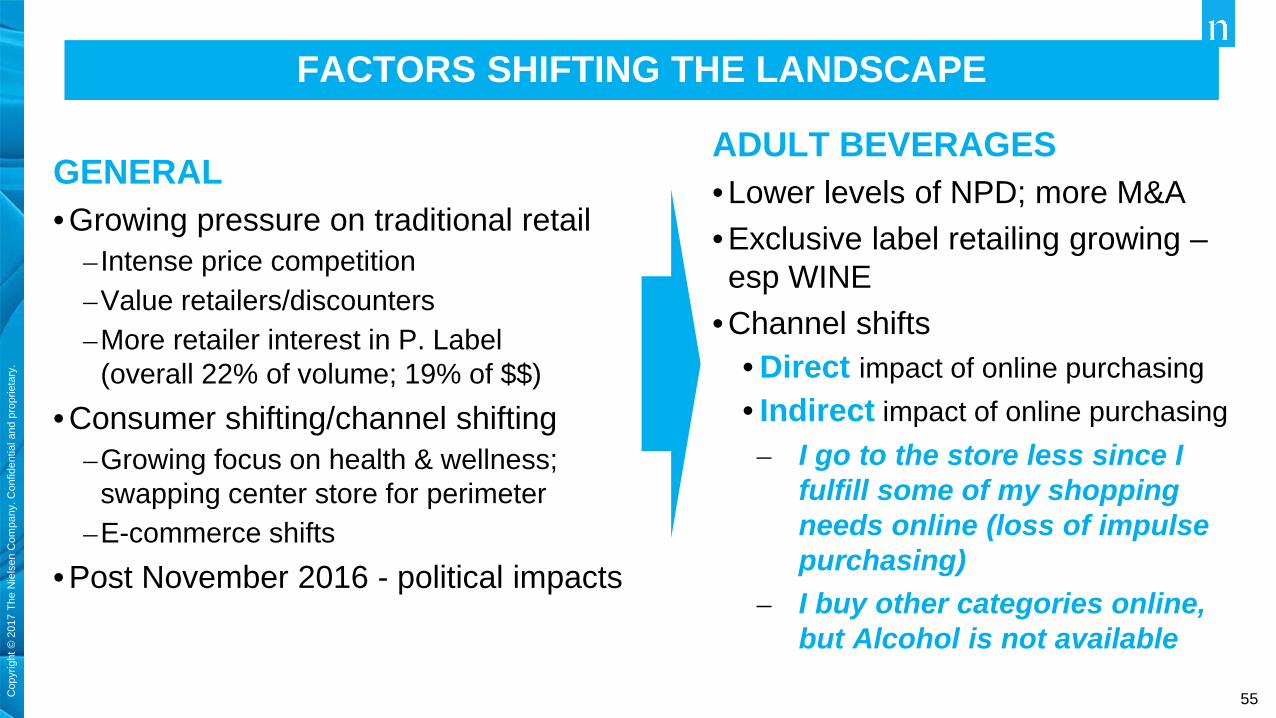

FACTORS SHIFTING THE LANDSCAPE

GENERAL• Growing pressure on traditional retail

– Intense price competition–Value retailers/discounters–More retailer interest in P. Label

(overall 22% of volume; 19% of $$) • Consumer shifting/channel shifting

–Growing focus on health & wellness; swapping center store for perimeter

–E-commerce shifts • Post November 2016 - political impacts

ADULT BEVERAGES• Lower levels of NPD; more M&A• Exclusive label retailing growing –esp WINE

• Channel shifts• Direct impact of online purchasing• Indirect impact of online purchasing– I go to the store less since I

fulfill some of my shopping needs online (loss of impulse purchasing)

– I buy other categories online, but Alcohol is not available

56Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

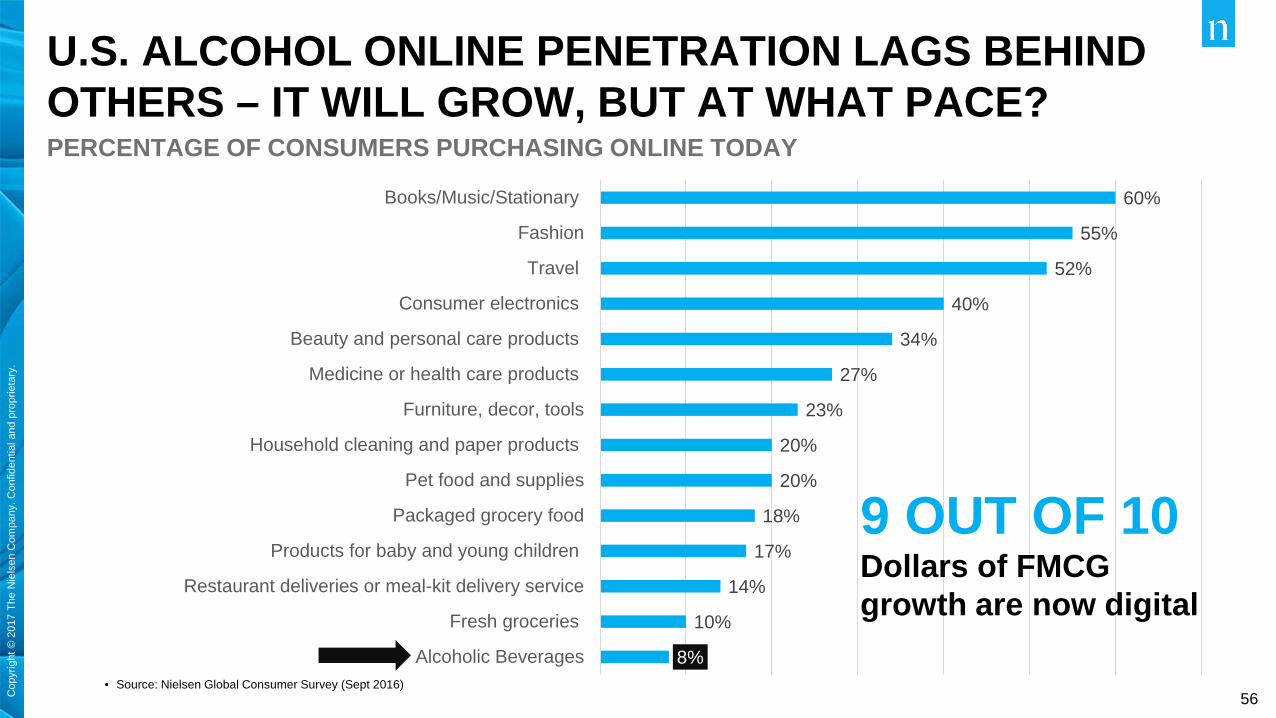

8%

10%

14%

17%

18%

20%

20%

23%

27%

34%

40%

52%

55%

60%

Alcoholic Beverages

Fresh groceries

Restaurant deliveries or meal-kit delivery service

Products for baby and young children

Packaged grocery food

Pet food and supplies

Household cleaning and paper products

Furniture, decor, tools

Medicine or health care products

Beauty and personal care products

Consumer electronics

Travel

Fashion

Books/Music/Stationary

• Source: Nielsen Global Consumer Survey (Sept 2016)

U.S. ALCOHOL ONLINE PENETRATION LAGS BEHIND OTHERS – IT WILL GROW, BUT AT WHAT PACE?PERCENTAGE OF CONSUMERS PURCHASING ONLINE TODAY

9 OUT OF 10Dollars of FMCG growth are now digital

57Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

58Cop

yrig

ht ©

201

7 Th

e N

iels

en C

ompa

ny. C

onfid

entia

l and

pro

prie

tary

.

Copyright © 2017 The Nielsen Company. Confidential and proprietary.

Danny Brager – [email protected]

Thank you – Cheers!!!