What to Expect When an IRS or DOL 401(k) Auditor Comes ...€¦ · 401(k) Auditor Comes Knocking...

30

The opinions expressed in this presentation are those of the speaker. The International Society and International Foundation disclaim responsibility for views expressed and statements made by the program speakers. What to Expect When an IRS or DOL 401(k) Auditor Comes Knocking Kim Schultz, CPA Managing Director Compensation & Benefit Solutions Greenwood Village, Colorado Patrick Blanchard, JD, LLM Managing Director Compensation & Benefit Solutions Greenwood Village, Colorado 6B-1

Transcript of What to Expect When an IRS or DOL 401(k) Auditor Comes ...€¦ · 401(k) Auditor Comes Knocking...

The opinions expressed in this presentation are those of the speaker. The International Society and International Foundation disclaim responsibility for views expressed and statements made by the program speakers.

What to Expect When an IRS or DOL 401(k) Auditor Comes Knocking

Kim Schultz, CPAManaging Director

Compensation & Benefit SolutionsGreenwood Village, Colorado

Patrick Blanchard, JD, LLMManaging Director

Compensation & Benefit SolutionsGreenwood Village, Colorado

6B-1

• ExaminationStatistics

• ExaminationStepsandTipsforManagingtheExaminationProcess

• TopIssuesDiscoveredDuringtheExaminationProcess

• Questions

Agenda

6B-2

Examination—Whatisit?

6B-3

• Todate,theEmployeePlansComplianceUnit(“EPCU”)hasconductedover41,000compliancechecks1

• Affectedsome$105millionincorrections

• Assessedover$16millionintaxassessments

• Estimatedtohavehad9,100examinationsin2014

IRSExaminationStatistics

Source: Tax Exempt & Government Entities: Employee Plans, “EPCU Updates August 2016.1 This represent EPCU contacts and does not represent IRS audits as a whole.

6B-4

• 2,335examinationsclosedinFY16

• 1,431examinationsclosedwithresultsinFY16

• $777.5millionintotalrecoveriesinFY16

DOLExaminationStatistics

6B-5

• Participantquestionsorcomplaint• OftenbasedonForm5500information

– Specificresponse

– FocusedprogrambyIRS/DOL

– Random

• Referralsfromotheragencies• Media• Other

BasisforExamination

6B-6

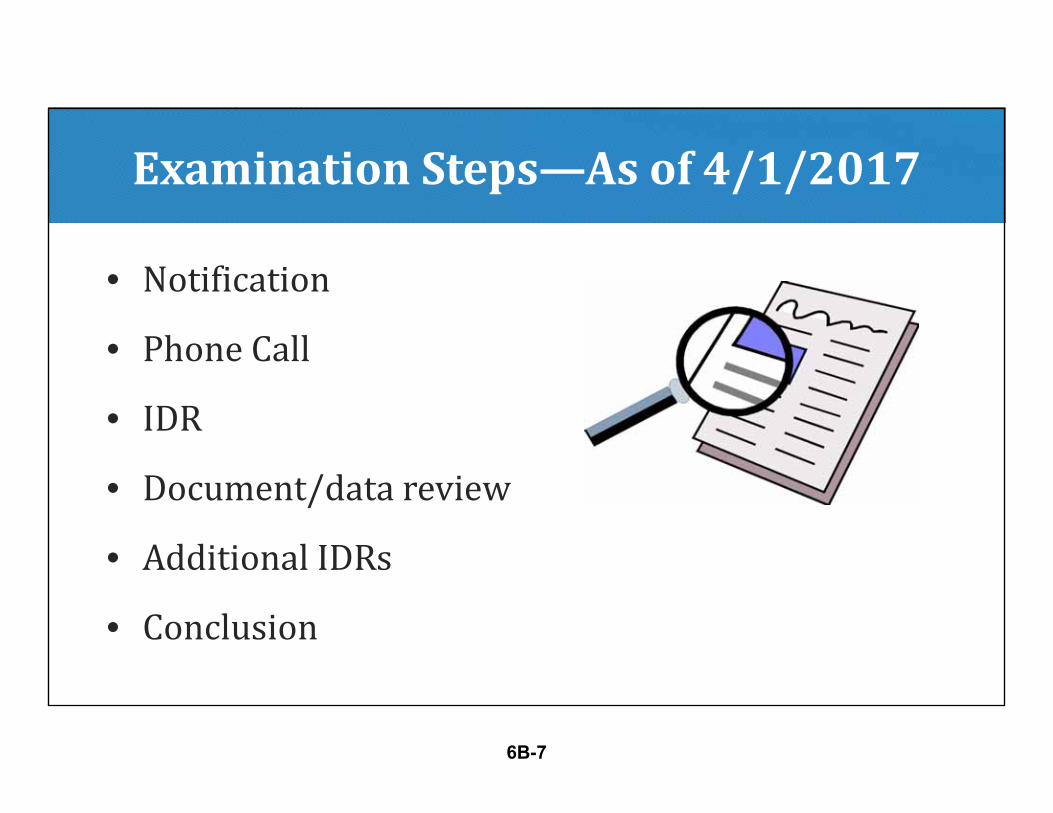

• Notification

• PhoneCall

• IDR

• Document/datareview

• AdditionalIDRs

• Conclusion

ExaminationSteps—Asof4/1/2017

6B-7

• Designateaclear“chainofcommand”forrespondingtoauditnoticesandothercommunications

• Retainexpertadvisors

• Closelymanagetheaudittimeline

• Setspecificmilestonestoensuremutualaccountability

ManagingtheExaminationProcess

6B-8

• WaittoreceiveanIDRbeforeprovidingplanmaterials– Onlyprovidedocumentationthatisspecificallyrequested

– DonotvolunteeranydocumentationthatisNOTrequested

• Establishacooperativeapproach– RespondtoIDRsinatimelymanner

– Itisabalancingact

ManagingtheExaminationProcess(continued)

6B-9

TopIssuesDiscoveredDuringtheAuditProcess

6B-10

FailuretoFollowPlanTerms

Operationofyourplanmustconformtothetermsoftheplandocument

6B-11

AccordingtotheIRS,moremistakesaremadewithcompensationthananyotherarea

Compensation

6B-12

• Failuretoincludeand/orexcludecertaincompensationtypes:– Imputedcompensationelements(e.g.,grouptermlife)

– Equitycompensationandothernon‐cashelements

– Bonuses

– Overtime

• Compensationfromentrydates

• 401(a)(17)CompensationLimit

CommonCompensationErrors

6B-13

• Planprovidesforemployermatchingcontributionof50%ofdeferralsof6%ofcompensationin2016,withatrue‐up

• Benmade$100,000inregularsalaryfor2016andreceiveda$10,000bonus

• Bendeferredatarateof10%theentireyear

Example

6B-14

• Iftheemployerexcludedbonusesfromcompensation,Ben’sdeferralsandmatchwouldbeasfollows:– Deferrals=$100,000*10%=$10,000

– Match=$100,000*6%*50%=$3,000

• Iftheemployerincludedbonusesincompensation,Ben’sdeferralsandmatchwouldbeasfollows:– Deferrals=$110,000*10%=$11,000

– Match=$110,000*6%*50%=$3,300

Example(continued)

6B-15

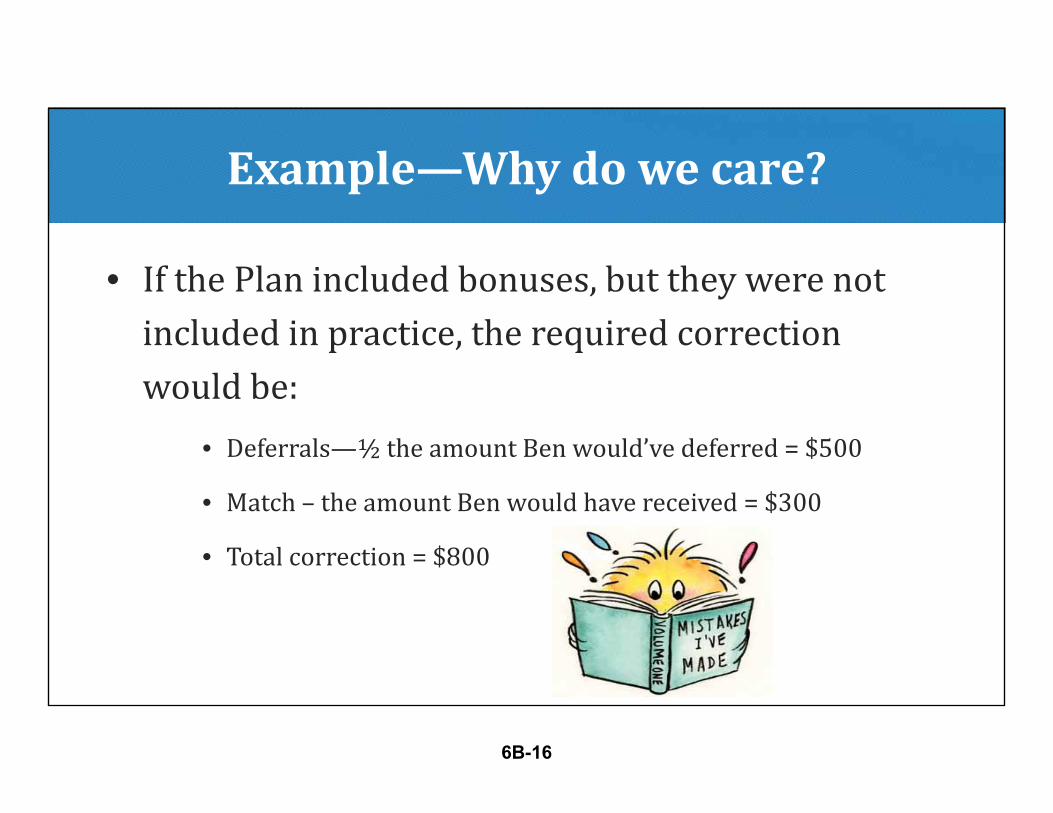

• IfthePlanincludedbonuses,buttheywerenotincludedinpractice,therequiredcorrectionwouldbe:

• Deferrals—½theamountBenwould’vedeferred=$500

• Match– theamountBenwouldhavereceived=$300

• Totalcorrection=$800

Example—Whydowecare?

6B-16

AutomaticEnrollment

6B-17

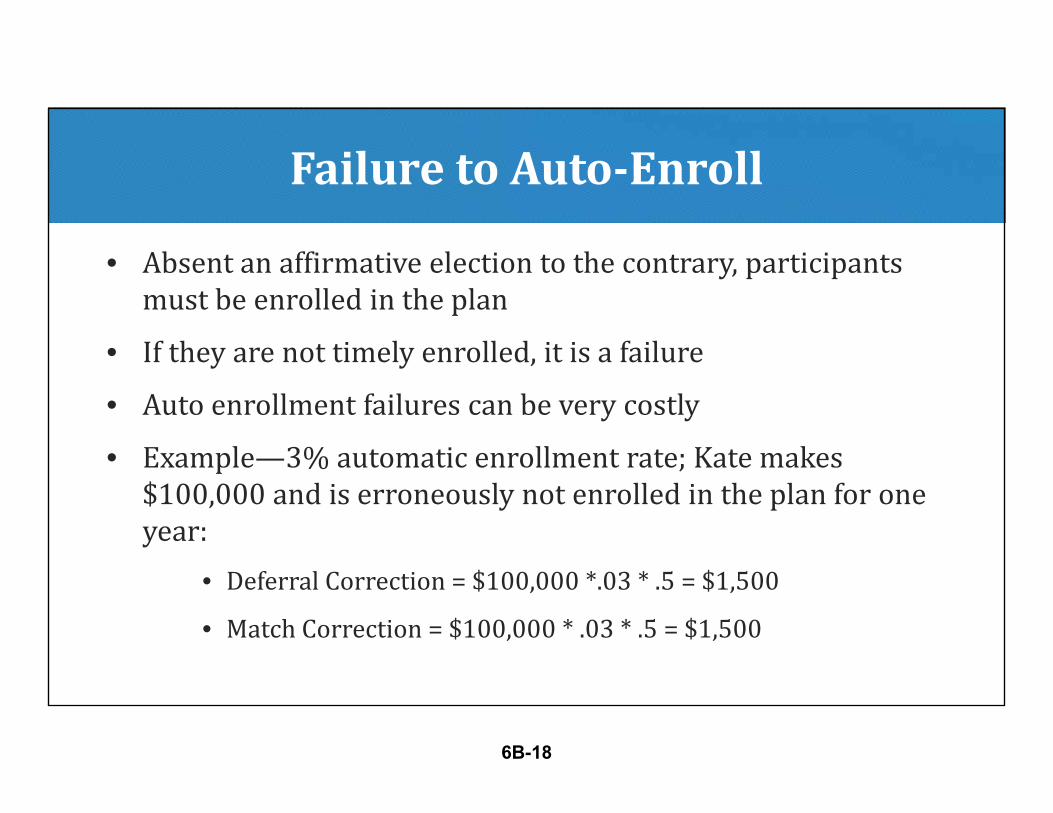

• Absentanaffirmativeelectiontothecontrary,participantsmustbeenrolledintheplan

• Iftheyarenottimelyenrolled,itisafailure

• Autoenrollmentfailurescanbeverycostly

• Example—3%automaticenrollmentrate;Katemakes$100,000andiserroneouslynotenrolledintheplanforoneyear:

• DeferralCorrection=$100,000*.03*.5=$1,500

• MatchCorrection=$100,000*.03*.5=$1,500

FailuretoAuto‐Enroll

6B-18

NondiscriminationTesting

6B-19

NondiscriminationTesting

• Thenondiscriminationtesting(NDT)rulesarecomplicatedandrequireaccuratedata

• Recordkeepersrelyonthedataprovided(almostblindlyinsomecases)

• Recordkeepersoftenusethemost conservativeapproach

6B-20

Loans

6B-21

Loans

22

• Doestheplandocumentpermitloans?• Howmanyoutstandingloansdoestheplanpermit?

• Havedelinquentloansbeenproperlydefaulted?• Loansaretypically5years...• Ifover5years,istherepropersubstantiation

6B-22

Hardships

6B-23

Hardships

• Doestheplanpermithardshipdistributions?

• Istheresufficientdocumentation?

• Weredeferralssuspendedfor6months(andreinstatedthereafter)?Forallplansoftheemployer?

• TheIRSisnotahugefanof“self‐certification”

6B-24

LateDepositof401(k)DeferralsandParticipantLoanRepayments

6B-25

LateDepositof401(k)DeferralsandParticipantLoanRepayments

• Mustbedepositedasoftheearliestdateonwhichsuchamountscanreasonably be segregated

• Haveapolicyandmakesureallpartiesinvolvedworktogethertofollowit

• Smallplansafeharbor—7businessdays

• Currentlythereisno safe harbor forlargeplans

• ExciseTaxes

6B-26

Vesting

6B-27

Vesting

• Calculatingvestingpercentages

• Permissiblevestingschedules

• Calculatingparticipantservice

6B-28

Questions

Thankyou!

6B-29

Please note that, though we believe this presentation provides accurate information, its accuracy is not guaranteed. Also, this presentation does not provide legal, accounting or tax

advice. Finally, this presentation cannot be used to avoid any tax penalty.

6B-30