What Retail Apocalypse-Reviewing Trends in US … Retail Apocalypse? Reviewing Trends in US...

18

1 January 24, 2018 Deborah Weinswig, Managing Director, FGRT [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016 Copyright © 2018 The Fung Group. All rights reserved. 1) Total US store numbers fell in 2017 for the first time since 2009. The decline was driven by apparel retailers and regional malls, which are more skewed toward apparel. 2) Open-air shopping centers are benefiting from the growth of off-price, dollar and grocery stores. These shopping centers showed resilient occupancy rates in 2017. 3) Superregional malls, which are leisure destinations as well as retail destinations, registered solid occupancy rates across 2017 despite the impact of retail bankruptcies. 4) A number of major shopping center owners are pivoting away from apparel specialist stores. Some are focusing on bringing in grocery and other everyday-goods retailers, while others are moving toward mixed-use spaces that incorporate leisure and entertainment venues. What Retail Apocalypse? Reviewing Trends in US Brick-and-Mortar Retail Deborah Weinswig Managing Director FGRT [email protected] US: 917.655.6790 HK: 852.6119.1779 CN: 86.186.1420.3016

Transcript of What Retail Apocalypse-Reviewing Trends in US … Retail Apocalypse? Reviewing Trends in US...

1

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

1) TotalUSstorenumbersfellin2017forthefirsttimesince2009.Thedeclinewasdrivenbyapparelretailersandregionalmalls,whicharemoreskewedtowardapparel.

2) Open-airshoppingcentersarebenefitingfromthegrowthofoff-price,dollarandgrocerystores.Theseshoppingcentersshowedresilientoccupancyratesin2017.

3) Superregionalmalls,whichareleisuredestinationsaswellasretaildestinations,registeredsolidoccupancyratesacross2017despitetheimpactofretailbankruptcies.

4) Anumberofmajorshoppingcenterownersarepivotingawayfromapparelspecialiststores.Somearefocusingonbringingingroceryandothereveryday-goodsretailers,whileothersaremovingtowardmixed-usespacesthatincorporateleisureandentertainmentvenues.

What Retail Apocalypse? Reviewing Trends in US Brick-and-Mortar Retail

Deborah Weinswig

Managing Director

FGRT

US: 917.655.6790

HK: 852.6119.1779

CN: 86.186.1420.3016

2

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

Contents

ExecutiveSummary..................................................................................................................................................3

Introduction..............................................................................................................................................................4

TheBadNews...........................................................................................................................................................4TotalStoreNumbersDeclinedin2017fortheFirstTimeSince2009...................................................................4ShopperTrafficFellbyNearly8%in2017.............................................................................................................7

TheGoodNews........................................................................................................................................................7In-StoreRetailSalesContinuetoGrow..................................................................................................................7SalesperStoreandSalesDensitiesAreGrowing,Too..........................................................................................8Open-AirCentersandSuperregionalMallsSeeSolidOccupancyRates................................................................9TopRetailRealEstateOwnersMaintain95%OccupancyRates.........................................................................11

KeyTakeaways........................................................................................................................................................12

Appendix:RealEstateManagementCommentary.................................................................................................13

3

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

ExecutiveSummaryThe“retailapocalypse”narrativeintheUShasbeendrivenbyclosuresofapparelspecialtystoresandapparel-focuseddepartmentstores.Theseclosureshaveheavilyimpactedregionalmalls,whichtendtoskewtowardappareland,so,havebeenwheremanyclosureshavebeenconcentrated.Buttoseethefullerpictureofbrick-and-mortarperformance,wemustlookbeyondapparelandregionalmalls,asitrevealsthattheretaillandscapeismoreresilientthanrecentcoveragehassuggested.

Intermsofoccupancyrates,open-airshoppingcentersandsuperregionalmallsfaroutperformedregionalmallsintheUSin2017.Manyoftheretailersthatareactivelyopeningstores—fromAlditoT.J.Maxx—areopeninginoff-malllocationssuchasstripmalls.Open-aircentersalsotendtobenefitfromhavingastrongpresenceofeveryday-goodsretailers,suchasgrocerystores,whichsupportshoppertraffic.Larger,well-invested,destinationmallshavetendedtooutperformunremarkableregionalmallsbymixingtraffic-drawingleisurevenueswithretail.

Shopping-centerownerssuchasGGPhavebeenreducingtheirexposuretoapparelspecialiststoresandanumberofretailrealestateownershavesoughttobringinmoregrocerytenantsorcreatemoremixed-usespacesattheirproperties.

Below,wesummarizekeymetricsthatreflectthediversityofUSbrick-and-mortarperformance.

Figure1.USBrick-and-MortarRetail:PositiveandNegativeMetricsin2017

Totalphysicalstoresaleswereupbyabout2.5%in2017,wecalculate,basedonUSCensusBureaudata.Wethinkthataveragein-storesalesgrowthislikelytoacceleratein2018.

AveragesalesperstoreandaveragesalespersquarefootacrossUSretailalsoincreasedin2017,weestimate.

Thegroceryanddollarstoresectorsexpandedsignificantlyin2017,withmajorretailersopeninganet1,785stores.Thisboostedoff-malllocationssuchasstripmalls.

Shopping-centerownerGGPnotedsustainedtrafficgrowthinitspremium,classAmallsduringtheyear.

Mall-basedsalesdensitieswereflatinfurnitureandwereupmeaningfullyinelectronicsyearoveryearinthefirst10monthsof2017(latest),accordingtodatafromtheInternationalCouncilofShoppingCenters(ICSC).

Open-airshoppingcentersanddestinationsuperregionalmallssawrelativelyresilientoccupancylevelsin2017amidarashofretailbankruptcies.

In2017,thetotalnumberofretailoutletsfellforthefirsttimesince2009,accordingtoEuromonitorInternational.Totalretailspacedeclined,too.

FGRTdatarevealedthatsoftlineretailers,whichincludeapparelspecialists,closedthehighestnumberofstoresamongmajorretailersin2017,with3,411netclosures.

Shoppertrafficwasdownsharplyatspecialtyandlarge-storeretailerslastyear,accordingtoRetailNext.

Totalmalloccupancyratesdeclinedslightlyin2017,accordingtoICSCdata,drivenbyaslumpinregionalmalls,whichtendtohaveahigherproportionofappareltenants.

FourofthetopfiveretailrealestateownersintheUSreportedmildyear-over-yeardeclinesinoccupancyattheendofthethirdquarterof2017(latest),astheycontinuedtofeeltheeffectsofretailbankruptcies.

The“retailapocalypse”narrativehasbeendrivenbyclosuresofapparelspecialtystoresandapparel-focuseddepartmentstoresinregionalmalls.

4

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

IntroductionAsmoreandmoreretailersenteredbankruptcyorshutteredstoresin2017,thenarrativethatUSretailwasundergoinganapocalypsetookhold.Inthisreport,webringtogetheranumberofdatapointsonbrick-and-mortarretailandretailrealestatetoanalyzewhatactuallyhappenedlastyear.Ourfocusisonthephysicalstorelandscaperatherthanonindividualretailers.

Storeclosuresbyapparelanddepartmentstoreretailersfueledthenegativeheadlinesin2017andearly2018,althoughtherewerecasualtiesinothersectors,too,suchasRadioShackinelectronics.Theseclosuresimpactedregionalshoppingmallsmostheavily.Inthisreport,wearguethatwemustlookbeyondapparelandregionalmallstoseethefullerpictureofbrick-and-mortarperformance.Thiswiderviewrevealsabrick-and-mortarlandscapethatismoreresilientthanrecentcoveragehassuggested.

• ReadersmayalsobeinterestedinourMallIsNotDeadreports.

TheBadNewsFirst,weroundupsomeofthebadnewsregardingstoreclosuresandtraffic,muchofwhichislikelyfamiliartoreaders.Weexaminemorepositiveindicatorslaterinthereport.

TotalStoreNumbersDeclinedin2017fortheFirstTimeSince2009Storeclosuresgrabbedtheheadlinesanddrovetheretailapocalypsenarrativein2017andinto2018.Accordingtoourownresearch,majorUSchainsannouncedatotalof6,955storeclosuresin2017.AccordingtoEuromonitorInternational,whosestoreclosurefiguresincludesmallandindependentretailers,totalUSstorenumbersfellin2017forthefirsttimesince2009.However,inthecontextofallretailstores,thedeclineswereslight:

• ThetotalnumberofUSstoresfellbyjust0.1%yearoveryearin2017,to965,148,accordingtoEuromonitorInternational.

• Becausemanyofthelocationsthatwereclosedin2017werelarge-formatstores,suchasdepartmentstores,theyear-over-yeardeclineintotalretailnetsellingspaceequatedtoamoresizeable0.6%.Asofyear-end,theUShad8.52billionsquarefeetofretailsellingspace,accordingtoEuromonitor.

USstorenumbersfellin2017forthefirsttimesince2009.

5

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

Figure2.USRetail:TotalNumberofStores(Thous.,LeftAxis)andNetSquareFootage(Mil.Sq.Ft.,RightAxis)atYear-End

Source:EuromonitorInternational

OuranalysisofEuromonitorselling-spacedataandourowntallyofstoreclosureandopeningannouncementsrevealedthefollowingsectortrends:

• Apparelandfootwearspecialiststores’totalsellingspacedeclinedby2.2%yearoveryearin2017.PaylessShoeSource,Rue21,AscenaRetail,GymboreeandTheLimitedannouncedacombined2,080storeclosuresin2017.However,apparelretailisfragmented,sotheseclosuresresultedinonlyalow-single-digitdeclineintotalsectorspace.

• Departmentstores’totalsellingspacefellby3.5%in2017.Sears,Kmart,JCPenneyandMacy’sannouncedacombined566storeclosuresduringtheyear.

• Sellingspaceinelectronicsandappliancestoresfellsharplyin2017.RadioShackaloneclosedalmost1,500stores,whileHHGreggclosed220stores.

• Varietystoreandgroceryretailersgrewtotalsellingspacein2017.DollarGeneral,DollarTree,Aldi,FiveBelowandLidlannouncedacombinedtotalof2,535storeopeningsintheyear.

• Warehouseclubsgrewsellingspace,too.

955.5 962.6 966.4 965.1

8,506

8,539

8,575

8,521

8,460

8,480

8,500

8,520

8,540

8,560

8,580

8,600

0

200

400

600

800

1,000

2014 2015 2016 2017

Stores(Thous.) Sq.Ft.(Mil.)

DollarGeneral,DollarTree,Aldi,FiveBelowandLidlannouncedacombined2,535storeopeningsin2017.

6

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

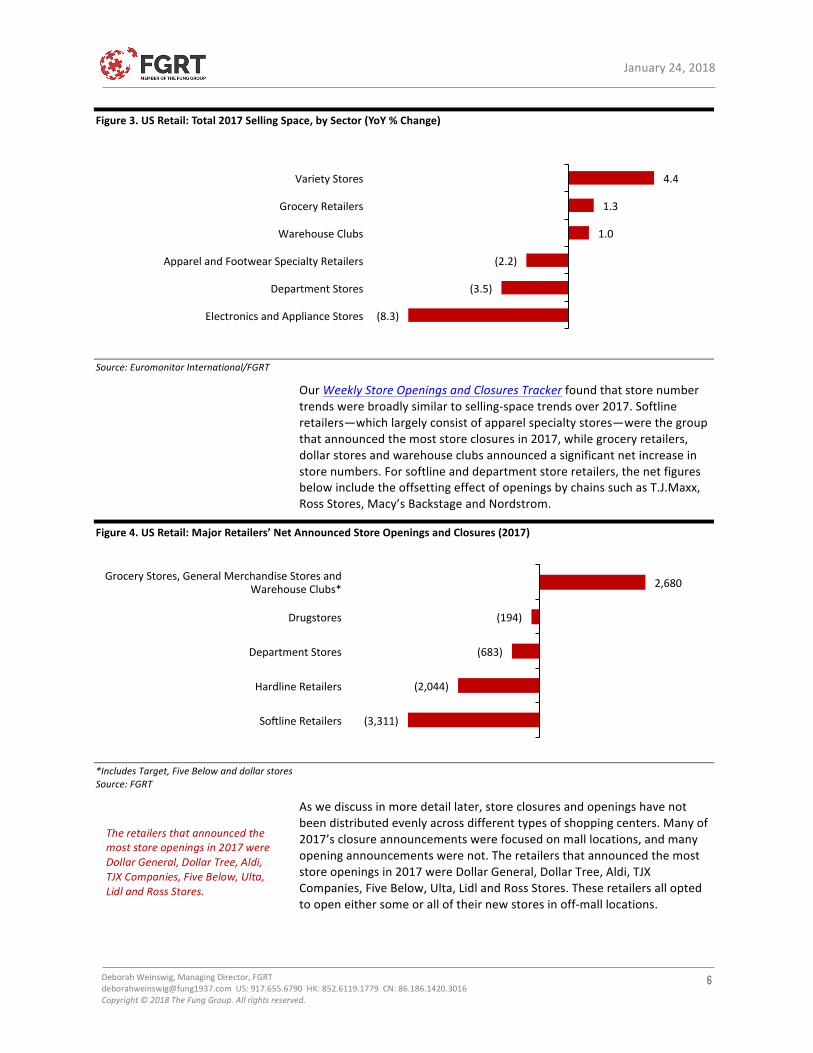

Figure3.USRetail:Total2017SellingSpace,bySector(YoY%Change)

Source:EuromonitorInternational/FGRT

OurWeeklyStoreOpeningsandClosuresTrackerfoundthatstorenumbertrendswerebroadlysimilartoselling-spacetrendsover2017.Softlineretailers—whichlargelyconsistofapparelspecialtystores—werethegroupthatannouncedthemoststoreclosuresin2017,whilegroceryretailers,dollarstoresandwarehouseclubsannouncedasignificantnetincreaseinstorenumbers.Forsoftlineanddepartmentstoreretailers,thenetfiguresbelowincludetheoffsettingeffectofopeningsbychainssuchasT.J.Maxx,RossStores,Macy’sBackstageandNordstrom.

Figure4.USRetail:MajorRetailers’NetAnnouncedStoreOpeningsandClosures(2017)

*IncludesTarget,FiveBelowanddollarstoresSource:FGRT

Aswediscussinmoredetaillater,storeclosuresandopeningshavenotbeendistributedevenlyacrossdifferenttypesofshoppingcenters.Manyof2017’sclosureannouncementswerefocusedonmalllocations,andmanyopeningannouncementswerenot.Theretailersthatannouncedthemoststoreopeningsin2017wereDollarGeneral,DollarTree,Aldi,TJXCompanies,FiveBelow,Ulta,LidlandRossStores.Theseretailersalloptedtoopeneithersomeoralloftheirnewstoresinoff-malllocations.

(8.3)

(3.5)

(2.2)

1.0

1.3

4.4

ElectronicsandApplianceStores

DepartmentStores

ApparelandFootwearSpecialtyRetailers

WarehouseClubs

GroceryRetailers

VarietyStores

(3,311)

(2,044)

(683)

(194)

2,680

SoilineRetailers

HardlineRetailers

DepartmentStores

Drugstores

GroceryStores,GeneralMerchandiseStoresandWarehouseClubs*

Theretailersthatannouncedthemoststoreopeningsin2017wereDollarGeneral,DollarTree,Aldi,TJXCompanies,FiveBelow,Ulta,LidlandRossStores.

7

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

ShopperTrafficFellbyNearly8%in2017Shoppertrafficdeclinedsharplyacrossspecialtyandlarger-formatstoresin2017,accordingtodatafromRetailNext.Thesetypesofstoressawtrafficfallbyanaverageof7.9%overtheyear,slightlybelowthe8.3%averagedeclineseenacross2016.

Meanwhile,traffictrendsatcertainpremiummallsintheUSwerestrongin2017.Onitsmidyearconferencecall,shopping-centerownerGGPpointedtoa1.4%year-over-yearincreaseintrafficatitstop-tier,classAmalls.ThefirmalsonotedthatitsB+mallshadseenpositivetraffictrendsandthatitsBmallshadseenflattraffictrends.

Figure5.USShopperTrafficinSpecialtyandLarger-FormatStores(YoY%Change)

Source:RetailNext/FGRT

TheGoodNewsDespitethechallengesretailersfacedin2017,totalin-storesalescontinuedtogrow,yieldinganupliftinsalesdensitiesacrossUSretail.Moreover,occupancyratesinopen-airshoppingcentersandsuperregionalmallsprovedresilient.

In-StoreRetailSalesContinuetoGrowTherapidgrowthofe-commerceiswelldocumented,buttotalstore-basedretailsaleshavecontinuedtogrow,too.OuranalysisofUSCensusBureaudatafoundthat,in2017:

• Totalofflineretailsalesgrewbyapproximately2.5%.

• Totalofflinenonfoodsalesgrewmorestrongly,byabout2.8%.

• Totalofflinefoodandbeveragesalesgrewbyabout1.8%.

Meanwhile,totalUSretailsalesgrewby4.0%overtheyear.

Wethinkthatstore-basedsalesgrowthislikelytostrengthenin2018amidacceleratingtotalretailsalesgrowth.Offlinesalesaremadelargelythroughphysicalstores,buttheyalsoincludemoreminorchannels,suchasdirectselling.

(15.0)

(13.0)

(11.0)

(9.0)

(7.0)

(5.0)

(3.0)

(1.0)

1.02016 2017

2017Average:(7.9)%2016Average:(8.3)%

8

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

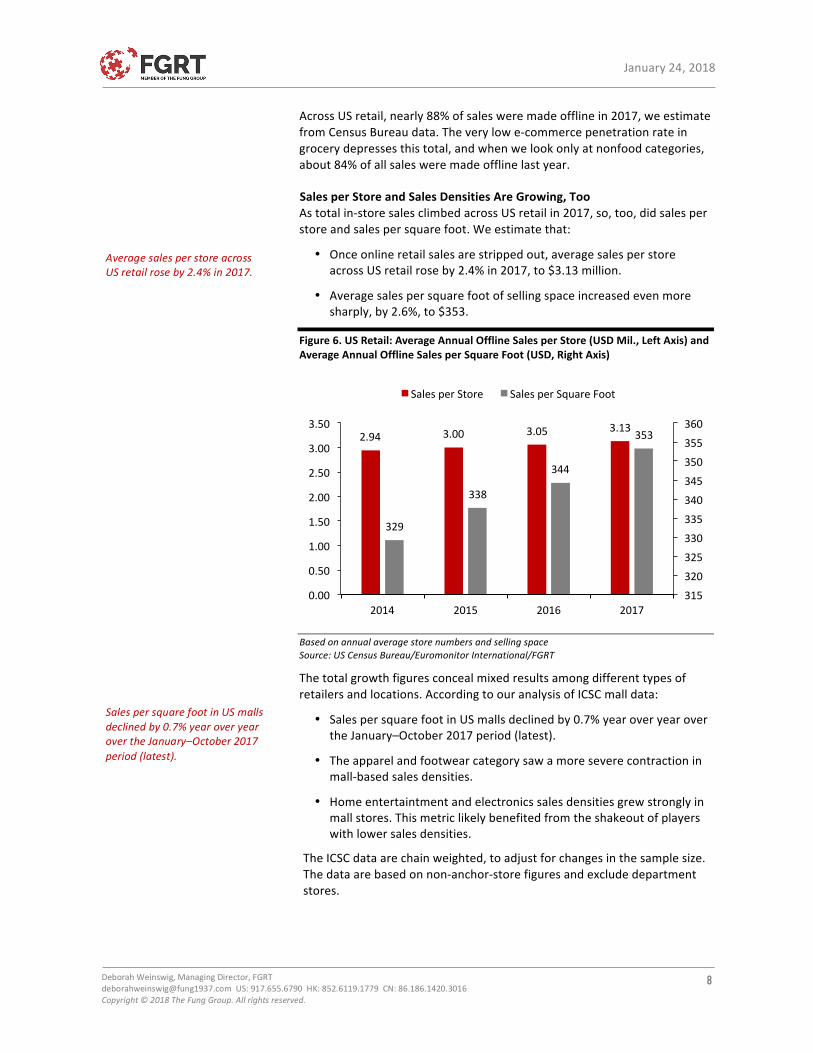

AcrossUSretail,nearly88%ofsalesweremadeofflinein2017,weestimatefromCensusBureaudata.Theverylowe-commercepenetrationrateingrocerydepressesthistotal,andwhenwelookonlyatnonfoodcategories,about84%ofallsalesweremadeofflinelastyear.

SalesperStoreandSalesDensitiesAreGrowing,TooAstotalin-storesalesclimbedacrossUSretailin2017,so,too,didsalesperstoreandsalespersquarefoot.Weestimatethat:

• Onceonlineretailsalesarestrippedout,averagesalesperstoreacrossUSretailroseby2.4%in2017,to$3.13million.

• Averagesalespersquarefootofsellingspaceincreasedevenmoresharply,by2.6%,to$353.

Figure6.USRetail:AverageAnnualOfflineSalesperStore(USDMil.,LeftAxis)andAverageAnnualOfflineSalesperSquareFoot(USD,RightAxis)

BasedonannualaveragestorenumbersandsellingspaceSource:USCensusBureau/EuromonitorInternational/FGRT

Thetotalgrowthfiguresconcealmixedresultsamongdifferenttypesofretailersandlocations.AccordingtoouranalysisofICSCmalldata:

• SalespersquarefootinUSmallsdeclinedby0.7%yearoveryearovertheJanuary–October2017period(latest).

• Theapparelandfootwearcategorysawamoreseverecontractioninmall-basedsalesdensities.

• Homeentertaintmentandelectronicssalesdensitiesgrewstronglyinmallstores.Thismetriclikelybenefitedfromtheshakeoutofplayerswithlowersalesdensities.

TheICSCdataarechainweighted,toadjustforchangesinthesamplesize.Thedataarebasedonnon-anchor-storefiguresandexcludedepartmentstores.

2.94 3.00 3.05 3.13

329

338

344

353

315

320

325

330

335

340

345

350

355

360

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

2014 2015 2016 2017

SalesperStore SalesperSquareFoot

AveragesalesperstoreacrossUSretailroseby2.4%in2017.

SalespersquarefootinUSmallsdeclinedby0.7%yearoveryearovertheJanuary–October2017period(latest).

9

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

Figure7.USShoppingMalls:Chain-WeightedAverageAnnualSalesperSquareFoot,bySelectedRetailCategory,January–October2017(YoY%Change)

Source:ICSC/FGRT

Open-AirCentersandSuperregionalMallsSeeSolidOccupancyRatesBankruptcyfilingsfromretailerssuchasSportsAuthority,PaylessShoeSourceandRue21impactedoccupancyratesatshoppingcentersin2017.However,theimpactsoftheseclosureswerenotevenlydistributed,asoccupancyratesatopen-aircentersandsuperregionalmallsoutperformedthoseofregionalmallsovertheyear.

In2017,superregionalmallsweretheonlymajorshopping-centersegmenttogrowoccupancyrates.Onatwo-yearstack,open-aircentersperformedbestintermsofoccupancyrates.Powercenters,whicharefocusedonafewanchortenants,sawasecondyearofdeepdeclinesinoccupancyin2017.

Figure8.USShoppingCenters:Basis-PointChangeinOccupancyRates(asofSeptember2017)

Open-aircentersaregeneralpurposecentersandincludestripmalls,neighborhoodcentersandcommunitycenters.Powercentershavecategory-dominantanchorsandonlyafewsmalltenants;theyarenotincludedwithintheopen-aircenterscategory.*Regionalmallsandsuperregionalmallsaresubsetsoftotalmalls.Source:ICSC/FGRT

(0.7)

(3.8)

0.0

4.7

Total ApparelandFootwear

FurnitureandFurnishings

HomeEntertainmentand

Electronics

(13)

(102)

(208)

(143)

76

(83)

(36) (31)

(216) (210)

OneYear TwoYears

TotalMalls RegionalMalls* SuperregionalMalls*

Open-AirCenters PowerCenters

Onatwo-yearstack,open-aircentersperformedbestintermsofoccupancyrates.

10

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

Open-aircentersareoneofthemostresilientretailrealestatesegments.Thereareanumberofreasonsforthestrengthoftheseproperties:

• Manyoftheretailersthatareactivelyopeningstores—fromAlditoDollarGeneraltoT.J.MaxxtoUlta—areopeningtheminoff-malllocationssuchasstripmalls.

• Open-aircenterstendtohavelessexposuretoapparelspecialtyretailers,whereretailbankruptcieshavebeenmostconcentrated.

• Thecenterstendtohaveastrongpresenceofeverydayretailerssuchasgrocerystores.Grocery,inparticular,continuestoseeaverylargemajorityofsalestransactedinphysicalstoresratherthanonline,whichsupportsshoppertrafficatopen-aircenters.

Superregionalmalls,whichtheICSCdefinesasthoseof800,000squarefeetormore,wereresilientin2017.Thesemallsgrewoccupancyratesby76basispointsovertheyearandoutperformedtotalmallsonatwo-yearstack.Somemallownershavechosentocatertoconsumerdemandforqualityexperiencesbyinvestinginsuperregionalmallstoensuretheyprovideshopperswithwiderchoiceandleisurefacilities.

Regionalmalls,whicharetypicallyenclosedmallsof400,000–800,000squarefeet,havebeenthehardesthitofthelargershopping-centerformats.Thesemallsincludealongtailofshoppingcentersthatfocusonapparelretailers,andsomeofthemhavesufferedfromanegativecycleofpoortraffictrendsandstoreclosures.

In2017,managementatretailrealestatefirmDDRnotedanaveragewindowof12–18monthsbetweenthetimeananchorstoreinashoppingcenterclosesandthetimethespacereopens.

Aschartedbelow,occupancyrateshavetendedtoholdupwellatsuperregionalmallsandopen-aircenters.Powercentershaveseensteepdeclinesinoccupancy,butfromaverystrongposition.Regionalmallshaveexperiencedsevereattritioninoccupancyratessincemid-2016asaresultofbankruptciesandstoreclosureprograms.

Figure9.USShoppingCenters:OccupancyRates(%)

Source:ICSC

93.0

91.0

93.993.3

92.8

90.0

91.0

92.0

93.0

94.0

95.0

Sep15 Dec15 Mar16 Jun16 Sep16 Dec16 Mar17 Jun17 Sep17

TotalMalls RegionalMalls

SuperregionalMalls Open-AirCenters

PowerCenters

Regionalmallshaveexperiencedsevereattritioninoccupancyratessincemid-2016.

11

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

Asaresultofthesetrends,anumberofmallownershavebeendiversifyingtheirportfoliostoincorporatemorepremium,classAmalls,wheresalesdensitiesarehigherandwheretenantsmayincludedestinationstoressuchasAppleorTeslastores.TheseAmallsaccountforonly20%ofallUSmalls,buttheygenerate72%oftotalmallsales,accordingtoGreenStreetAdvisors.ThestrugglingmallstendtoberegionalclassCandDmallsaswellassomeBmalls.Combined,thesemakeupthe300orsomallsthatdominatethenegativecommentaryonthestateofphysicalretailintheUS.

Thesesameregionalmallsarelikelytobetheonesimpactedwhenanchordepartmentstoresclose,andsuchclosuresaredrivingmallownerstorethinkhowtheyareusingtheirspaces.Today,anumberofmallownersareusingtheseclosuresasopportunitiestoreshapetheirretailofferingandarefillingtheirmallswithtrafficdriversthatincludegrocerystores,discountstores(suchasT.J.Maxx)andhigher-growthfashionretailers(suchasH&MandZara).Insomecases,mallownersaredividingtheirspacesintosmallersectionstohouseboutiquesthatofferacuratedselectionofgoods.

TopRetailRealEstateOwnersMaintain95%OccupancyRatesAccordingtoNationalRealEstateInvestor,thetopfiveownersofUSretailrealestate(asmeasuredbygrossleasablearea)in2016were,indescendingorder,SimonPropertyGroup,GGP,KimcoRealty,BrixmorPropertyGroupandDDR.

Attheendofthethirdquarterof2017(latest),fourofthesefivecompanieshadseenayear-over-yeardeclineinoccupancyrate,asweshowinthetablebelow.However,thedeclinesweremarginal,especiallyinthecontextofretailbankruptcies.Thenonweightedaverageoccupancyratesacrossthesecompanieswas94.5%attheendofthethirdquarterof2017,versus95.2%oneyearearlier.

• SimonPropertyGroupoperatesregionalmalls,premiumoutletcentersandmallsundertheMillsbanner,thelatterofwhichblendconventionalretail,outletstoresandentertainment.

• GGPoperatespremiumretailpropertiesacrossopen-aircentersandcoveredmalls.

• Kimco,BrixmorandDDRconcentrateonopen-aircenters.Manyoftheseincludeeverydayretailerssuchasgrocerystoresandvalueretailers:BrixmorshoppingcenterstendtohavegroceryanchorswhileDDRcharacterizesitscentersas“value-oriented.”

Figure10.MajorUSRetailRealEstateOwners:OccupancyRate(%)

Simon GGP Kimco Brixmor DDR

1Q16 95.6 95.9 95.8 92.4 96.12Q16 95.9 96.1 96.0 92.8 96.13Q16 96.3 96.7 95.1 92.6 95.44Q16 96.8 97.2 95.4 92.8 95.01Q17 95.6 95.9 95.3 92.5 94.32Q17 95.2 95.7 95.5 92.0 93.73Q17 95.3 96.5 95.8 91.6 93.4YoYbasis-pointchangeat3Q17 (100) (20) 70 (100) (200)

Figuresareasofquarter-end.Source:Companyreports/FGRT

Attheendofthethirdquarterof2017(latest),fourofthetopfiveownersofretailrealestatehadseenayear-over-yeardeclineinoccupancyrate.

12

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

GGPandothershavebeendialingdowntheirexposuretoapparelspecialtystores,andanumberofthesecompanieshavefocusedongrocery-anchoredcentersorsoughttobringinmoregrocerytenantstotheirexistingcenters.Somehavealsobeenaddingleisureservicessuchasfitnesscentersandentertainmentvenuestotheirproperties.

Inaddition,SimonPropertyGroupandGGPareembarkingonmixed-useconceptsthatincluderesidences,hotels,restaurants,grocerystores,bowlingalleysandfoodhalls.

• Wefeaturecommentaryfrommanagementatthesefivefirmsinanappendixtothisreport.

KeyTakeaways• 2017sawajumpinstoreclosureannouncementsbymajorretailers,

whichpromptedadeclineintotalUSstorenumbersforthefirsttimesince2009.Negativeheadlinesweredrivenbyapparelretailandtheregionalmallsthataremorereliantonthatsector.

• Open-aircentersarebenefitingfromthegrowthofoff-price,dollarandgroceryretailers.Theopen-airsegmentsawresilientoccupancyratesin2017despitetheimpactofretailbankruptices.

• Similarly,superregionalmalls,whichareleisureaswellasretaildestinations,registeredsolidoccupancyratesacross2017.Reflectingthestrengthofpremiumcenters,GGPrecordedpositivetraffictrendsinitsAmallsovertheyear.

• Anumberofmajorshopping-centerownersarepivotingawayfromapparelspecialiststores.Somearefocusingonbringingingroceryandeveryday-goodsretailers,whicharelessvulnerabletoe-commercemigrationthanapparelretailersare.Othersaremovingtowardmixed-usespacesthatincorporateleisureandentertainmentvenuesaswellasofficeandresidentialunits.

Lastyear’snegativeheadlinesweredrivenbyapparelretailandtheregionalmallsthataremorereliantonthatsector.

13

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

Appendix:RealEstateManagementCommentaryFinally,toaddcoloranddetail,wewrapupkeycommentaryfromthemanagementofSimonPropertyGroup,GGP,KimcoRealty,BrixmorPropertyGroupandDDR,asstatedonconferencecallsacrossthefirstthreequartersof2017(latestattimeofwriting).

SimonPropertyGroupSimonPropertyGroupisdiversifyingthemixofspaceatitspropertiestoincludelesiure,officeandresidentialspace.

3Q17DavidE.Simon,ChairmanandCEO:

Wehaveasignificantopportunitytocontinuetoimproveourportfoliothroughthedensificationofourcenterswiththeadditionofmixed-usecomponents:hotels,multifamily,officeandothers.…WerecentlyopenedTheShopsatClearfork,agreatnewcenter.Thisopen-aircenterisanexcellentexampleofthetypeofvibrantmixed-use,community-centricenvironmentwecreate,alongwithourpartners.Wehavecarefullycuratedamixofshopping,dining,entertainment[and]office[space].

2Q17DavidE.Simon:

Tenantbankruptciesprocessedduringthesecondquarterforretailers,including,butnotlimitedto,Rue21,Payless,BCBGandBebe,impactedouroccupancybyapproximately100basispoints.

1Q17RichardS.Sokolov,PresidentandCOO:

[Y]ou’llseenewretailers,boththee-tailersandtheinternationalretailers,andourexistingbrandsandnewdesignerbrandsthatallwanttotakeadvantageofthespacethatisbecomingavailable,eitherbecausewecreatedit,becausewetookbackspacefromunderproductiveretailers,orweconsolidatedthoseunproductiveretailersintomoreproductivespacetofreeupspace.

GGPGGPisseekingtoreducetheapparelsector’sshareofspaceonitspropertiesandisbringingingrocerytenants,includingLidl,andleisuretenantssuchasfitnesscenters.LikeatSimonPropertyGroup,managementatGGPhaspointedtoInternetretailersopeningstoresasanopportunity.

3Q17SandeepLakhmiMathrani,CEO:

Thesecondquarterofthisyearwasthetrough[inoccupancy],followingthestoreclosuresearlierthisyear.…[I]nthe[Amalls],again,whicharethetopsortof80malls…apparelisalreadydowntolike41%oftotalsquarefootage.…So,effectively,itaccounts—intotalsales—[for]about35%oftotalsales.So,we’resayingthatbasicallywe’llgettothe35%to40%markeronapparel.

14

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

2Q17SandeepLakhmiMathrani:

InJuly,weacquiredanadditionalinterestin13SearsboxeslocatedinourportfoliofromSeritageGrowthProperties.…Theselocationsaresubstantiallyleasedtonewtenantssuchasrestaurants,fitnesscenters,entertainmentvenues,supermarketsandotherlarge-formatstores.Searswillcontinuetooccupy600,000squarefeetofthe1.5millionsquarefeet.

[T]herewas1.8millionsquarefeetofbankruptcies[impactingGGP]thisyear;80%hasbeenre-leased,i.e.,1.4millionsquarefeet.…Therearenumerouse-commerceretailersplanningtoopenstores.ThesearecompaniesthathavebeenoperatingforfivetosevenyearsontheInternetandhavesalesof$25millionto$100million.

Theoverallexposure[toapparel]isstill50%.Thenewleasingfortheyearis25%.So,it’strendingdownto41%.IntheAassets,it’salreadydownintothelow40s.

1Q17SandeepLakhmiMathrani:

InMarch,PrimarkopenedatStatenIslandMall.Trafficincreasedover10%fromthepriorweekend,andthisincreasedlevelhasbeenmaintained.Also,Lidl,aGermansupermarketoperator,willopensoonintherecapturedSearsspace.Lidloperatesover10,000storesthroughoutEuropeandisbringingtheirconcepttotheUS,beginningwitheightstates.…[AtStatenIslandMall],entertainmentwillbe54%andwillincludeanAMCtheaterandDave&Buster’s.Apparelwillbe17%andincludeZara.Foodanddiningwillbeabout20%andwillincludeShakeShack.Theremainingspacewillbetakenbyavarietyofpersonalcare,homefurnishingandothertenants,suchasAppleBank,Ulta[and]ZGallerie.

Theportfoliowas95.9%leasedatquarter-endcomparedto96.1%ayearago.Thedecrease[was]primarilyduetotenantbankruptciesduringthequarter.Therelatedstoreclosuresaffected1.2millionsquarefeetwithinourportfolio.Todate,wehavere-leasednearly80%ofthespace.

KimcoRealtyInearly2017,KimcowasimpactedbytheSportsAuthoritybankruptcy.IthasnotedthatthereareopportunitieswithnascentUSchainssuchasLidlandHomeSensefromTJX.

3Q17ConorC.Flynn,CEO:

Theseresultsvalidateourongoingthesisthatopen-aircentersthatfocusongrocers,off-price,fitness,everydaygoodsandservicescontinuetobesolidinvestmentsandremainthebackboneofourstrategytocreatetheoptimalportfolioanddriveshareholdervalue.

15

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

2Q17ConorC.Flynn:

[W]henyoulookatthenamesthatarestillreorganizingandcomingout,ourstoreclosurelistisvery,verysmall…andthey’retypicallysmallshops,sotheyhaveaverymodestimpact,ifanyatall,intermsofournextyear’snumbers.Sowecontinuetolookatthegrowingretailersthatwe’redoingbusinesswith.Ithinkthatwillfaroutweightheexposurewehavetosomeofthewatchlisttenantsthatareclosingstores.

1Q17ConorC.Flynn:

Kimcoisadaptingto[the]evolvinglandscapebyworkinghardtodeliverboththeproductandanexperiencetotenantsandshopperscommensuratewiththisnewworldorder.Andthatiswhyatmanyof[our]sites,you’llseemorehealthandwellness,moreserviceproviders,morefoodandrestaurants,moreentertainmentandmoreexperientialretailing.…Ofourtop20tenants,sevenhaverecentlyhitall-timehighsintheirstockprice,andmanyhavelargenewstoreopeningplans.Forexample,TJX,RossandBurlingtoninaggregatehaveannouncedexpansionplansinexcessof300stores.Whilewearenotimmune[to]storeclosures,wecontinuetobelieveweareinthesweetspotofretailandwillcontinuetogenerateinterestfromhigh-qualitytenantsthatwilldrivemoretrafficandmoresalestothesurroundingretailstores.

GlennGaryCohen,CFO,EVPandTreasurer:

First-quarteroccupancywasimpactedbyapproximately70basispointsrelatingtotheremainingSportsAuthorityvacancies.

BrixmorPropertyGroupBrixmorhaspointedtotherelativeresilienceofopen-aircentersthatarefocusedoneverydaycategoriessuchasgroceryandthatincorporateservicessuchasfitnesscentersandrestaurants.

3Q17JamesM.Taylor,CEOandPresident:

Thesedealshighlight…ourpreviouslystatedcommitmenttoextendingourtenancywithusessuchasrestaurants,fitness,home,valueandspecialtygrocery.

[W]eexperienceda50basis[-point]impact[totheoccupancyrate]frombankruptciesthatwehighlightedlastquarter,primarilyPaylessandRue21.I’mpleasedtoreportthatwecontinuetomakestrongprogressonleasingtherecapturedspace.

2Q17JamesM.Taylor:

WetipourhatstotherecentlyreportedstrongresultsofourgoodfriendsatKimco,WeingartenandKite,whichunderscorethebroader

16

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

truththatdemandtobeinwell-locatedopen-aircentersremainedstrong.Infact,thisquarter’sanalysisbyournationalaccountsteamofover150tenantsacrossopen-airsegmentssuchasgrocery,off-price,fitness,entertainment,homegoods,restaurant,healthandbeauty,andothersindicatedplanstoopenupover12,500newstoresinthenext12months.And,importantly,thatcountdoesnotincludethethousandsofnewopeningsplannedforregionalandlocaltenants.

[W]edoexpect[theoccupancyrate]totroughinthethirdquarter.Whenyouthinkaboutthetotalimpactofbankruptciesfrom[2016]ontheyear,it’sabout60basispoints.…Andweexpectareaccelerationactuallyinthefourthquarter,giventheprogressthatwe’vemadere-leasingnotonlythatspace,but…the2016bankruptcies.

1Q17BrianT.Finnegan,EVPofLeasing:

[T]hedemandwe’reseeingforPaylessinto[the]3,000-square-footrange,aswellasforRue21in5,000to10,000squarefeet,withpetstores,withhomeaccessories,operatorslikeFiveBelow,wefeelthedemandisoverallprettygood.…[W]ealreadyaddressedroughly80%ofthebankruptcieslastyear,ourSportsAuthorityrentsatcloseto70%spread,andwefeelprettygoodaboutthedemandthatwe’reseeinginHHGreggsofar…andalsothosethatwe’restartingtoreallyhavemoreprogresswith,likeentertainment,withourfirstDave&Buster’sthatwedidattheendoftheyear.

JamesM.Taylor:

[L]ookagainatwhattheteamdidwiththose16bankruptcies,mostofwhichwerecontrolledinthelatterhalfof2016.Wewereabletoproactivelygetafteritandre-tenant—morethantherentthatwasthere,80%ofthe[grossleasablearea]and,again,bringin…muchmorerelevantconceptsacrossavarietyofuses.…Andweseefarmorenewconceptsandmanymoresegmentsbeinginterestedinmovingintotheopen-airformat,sowelikehowwe’repositioned.

DDRDDRwasimpactedbybankruptciessuchasSportsAuthority,HHGreggandGolfsmithbuthaspointedtodemandfromretailerssuchasAldi,Lidl,T.J.Maxx/HomeSenseandUlta.

3Q17MichaelMakinen,EVPandCOO:

We’reparticularlypleasedtohavethecountry’sfirsttwoHomeSensestores,TJX’snewhomefurnishingsconcept,openedatShoppersWorldinFramingham,Massachusetts,andinEastHanover,NewJersey.…[T]heleasingenvironmentcontinuestobecharacterizedbysteadydemandforspace.Tothatend,wecontinuetoexpectthatitwillbea12-monthto18-monthprocesstoachieverentcommencementsfornewtenantsfillinganchorspacesmadevacant

17

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

fromrecentbankruptcies.Wenowhave24ofthe28formerSportsAuthority,HHGreggandGolfsmithspacesre-leasedorin…negotiations.

2Q17MichaelMakinen:

[Bankruptcies]causedourquarter-endleasedratetodecline60basispointssequentially,to93.7,primarilyasaresultofHHGreggclosuresthisquarter.Wecontinuetoexpecttheleaseratetotroughinthethirdquarter.Ourleasingpipelineremainsrobust.

1Q17MichaelMakinen:

DDR’sresultsthisquarterandfortheremainderoftheyeararebeingweigheddownbysignificantanchorvacanciesresultingfromrecenttenantbankruptciesfromTheSportsAuthority,HHGreggandGolfsmith.…TheInternetandchangingconsumerpatternswillundoubtedlycausesomeweakretailerstofallintodistress,butthereisstillahealthylistofhigh-qualityreplacementanchors,includingtheTJXbrands,UltaBeauty,Dick’s,Aldi,Ross,FiveBelowandBurlington.

18

January24,2018

DeborahWeinswig,ManagingDirector,[email protected]:917.655.6790HK:852.6119.1779CN:86.186.1420.3016Copyright©2018TheFungGroup.Allrightsreserved.

DeborahWeinswig,CPAManagingDirectorFGRTNewYork:917.655.6790HongKong:852.6119.1779China:86.186.1420.3016deborahweinswig@fung1937.comJohnMercerSeniorAnalyst

ErinSchmidtResearchAssociate

HongKong:2ndFloor,HongKongSpinnersIndustrialBuildingPhase1&2800CheungShaWanRoad,KowloonHongKongTel:85223004406London:242-246MaryleboneRoadLondon,NW16JQUnitedKingdomNewYork:1359Broadway,18thFloorNewYork,NY10018Tel:6468397017

FGRT.com