What is valuation?

61

What is valuation? 1

-

Upload

vernon-reese -

Category

Documents

-

view

34 -

download

0

description

What is valuation?. The need for valuations. Reasons for valuations. Types of property to be valued. Types of property to be valued. Legal estates in property. Concepts of price, value and worth. Market Price Price paid, exchange price - PowerPoint PPT Presentation

Transcript of What is valuation?

What is valuation?

1

THE NEED FOR VALUATIONS

Reasons for valuations

Development appraisal

Transfer of ownership

Monitoring of property investment performance

Reporting the value of property assets held by companiesLoan security

For taxation purposes

Insurance risk assessment

Compensation claims

Types of property to be valuedStandard Property Types

Offices Shops Factories & WarehousesStandard office Kiosk Factory

Business park Standard unitWorks (e.g. quarry, pit, mine, tip)

Post Office, bank Workshop

ShowroomLight industrial business unit

Supermarket / Superstore WarehouseRetail Warehouse Builders yardRetail Park (collection of retail warehouses)

Store

Shopping centre (collection of standard units)

Storage land

Department / Variety store Storage depotMarket stall

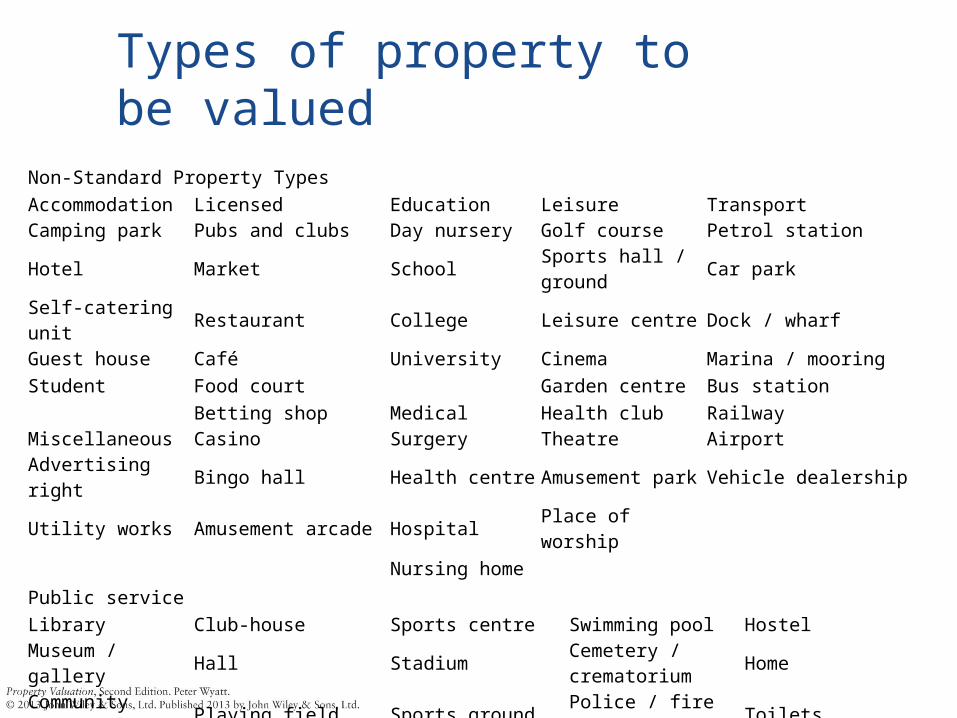

Types of property to be valuedNon-Standard Property Types

Accommodation Licensed Education Leisure TransportCamping park Pubs and clubs Day nursery Golf course Petrol station

Hotel Market SchoolSports hall / ground

Car park

Self-catering unit Restaurant College Leisure centre Dock / wharfGuest house Café University Cinema Marina / mooring

Student Food court Garden centre Bus station

Betting shop Medical Health club RailwayMiscellaneous Casino Surgery Theatre AirportAdvertising right Bingo hall Health centre Amusement park Vehicle dealership

Utility works Amusement arcade Hospital Place of worship

Nursing home

Public service

Library Club-house Sports centre Swimming pool Hostel

Museum / gallery Hall StadiumCemetery / crematorium

Home

Community centre

Playing field Sports groundPolice / fire station

Toilets

Prison Allotments Sporting right Law court Park

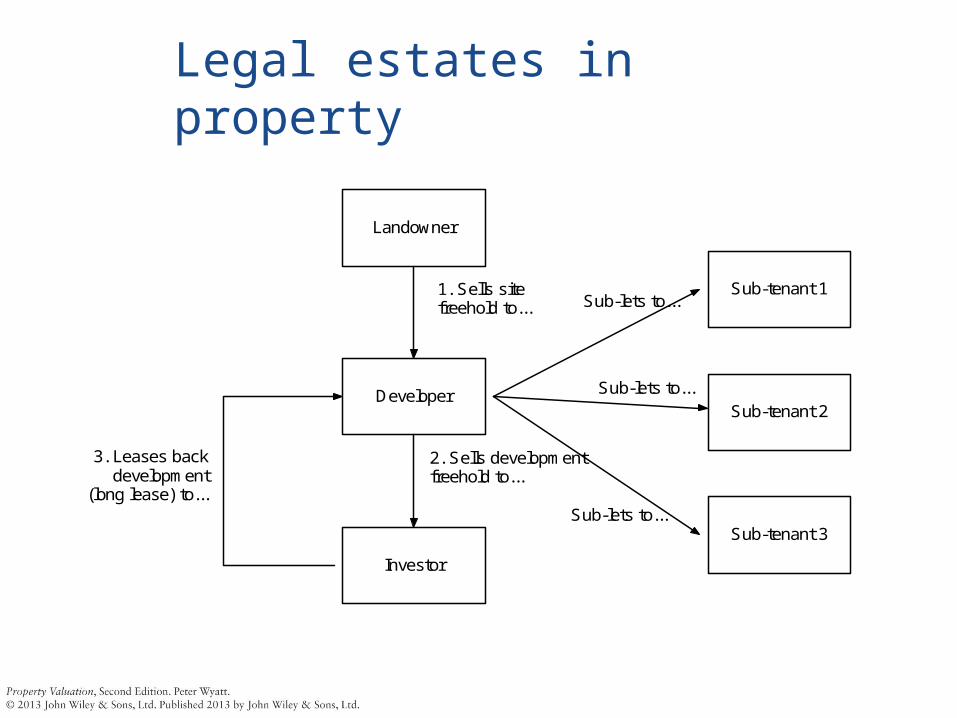

Legal estates in property

Landowner

Developer

Sub-tenant 1

Sub-tenant 3

Sub-tenant 2

3. Leases backdevelopment

(long lease) to...

2. Sells development freehold to...

Sub-lets to...

Sub-lets to...

Sub-lets to...

Investor

1. Sells sitefreehold to...

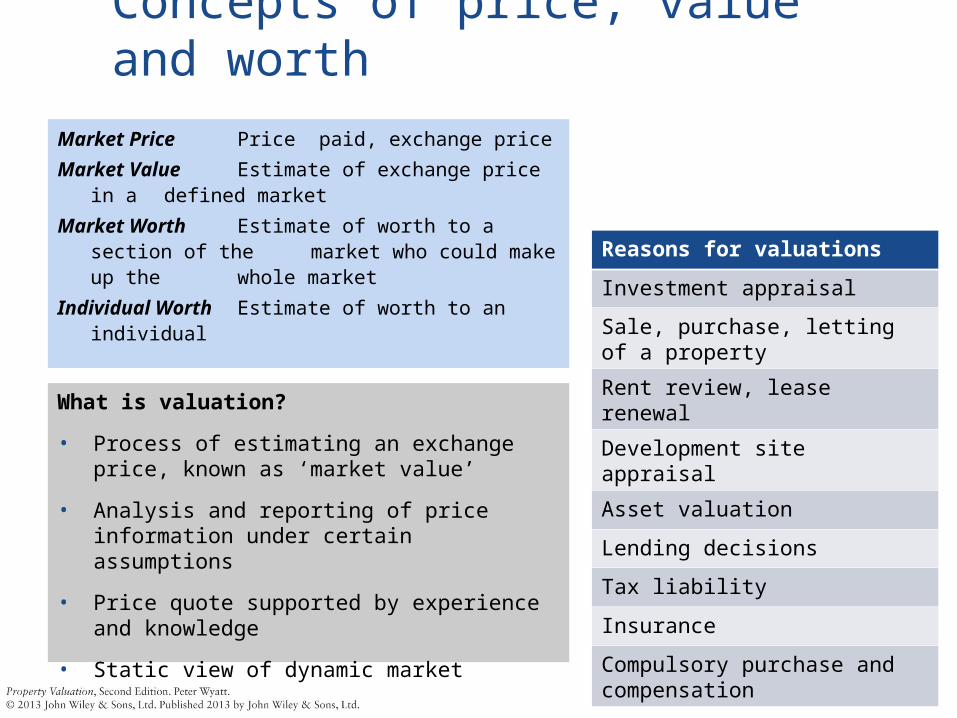

Concepts of price, value and worthMarket Price Price paid, exchange price

Market Value Estimate of exchange price in a defined market

Market Worth Estimate of worth to a section of the market who could make up the

whole market

Individual Worth Estimate of worth to an individual

What is valuation?

• Process of estimating an exchange price, known as ‘market value’

• Analysis and reporting of price information under certain assumptions

• Price quote supported by experience and knowledge

• Static view of dynamic market

Reasons for valuations

Investment appraisal

Sale, purchase, letting of a property

Rent review, lease renewal

Development site appraisal

Asset valuation

Lending decisions

Tax liability

Insurance

Compulsory purchase and compensation

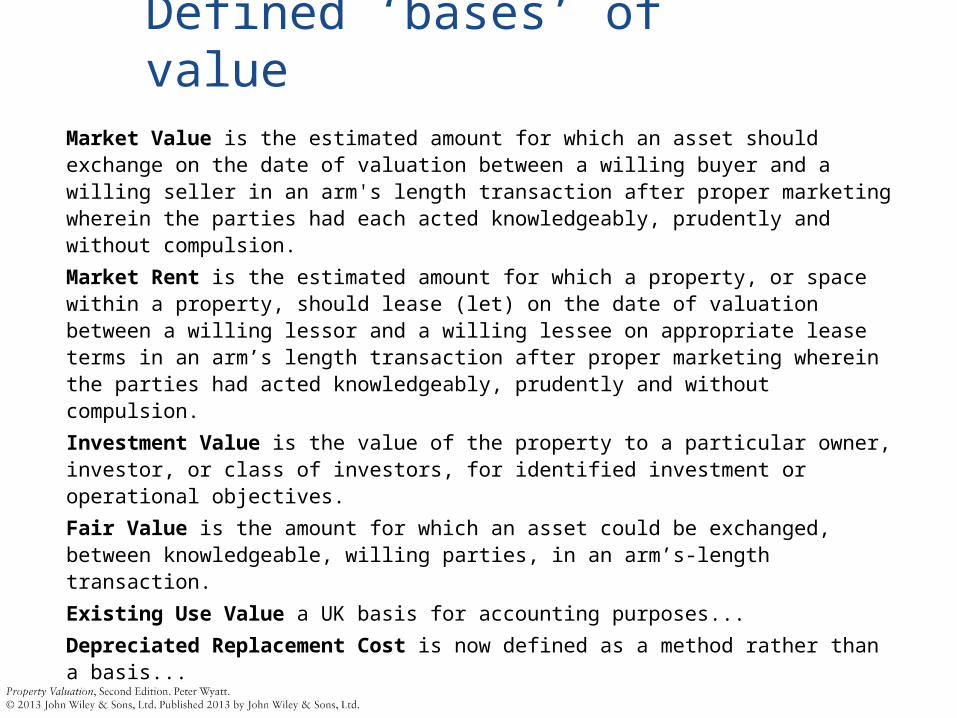

Defined ‘bases’ of valueMarket Value is the estimated amount for which an asset should exchange on the date of valuation between a willing buyer and a willing seller in an arm's length transaction after proper marketing wherein the parties had each acted knowledgeably, prudently and without compulsion.

Market Rent is the estimated amount for which a property, or space within a property, should lease (let) on the date of valuation between a willing lessor and a willing lessee on appropriate lease terms in an arm’s length transaction after proper marketing wherein the parties had acted knowledgeably, prudently and without compulsion.

Investment Value is the value of the property to a particular owner, investor, or class of investors, for identified investment or operational objectives.

Fair Value is the amount for which an asset could be exchanged, between knowledgeable, willing parties, in an arm’s-length transaction.

Existing Use Value a UK basis for accounting purposes...

Depreciated Replacement Cost is now defined as a method rather than a basis...

DETERMINANTS OF VALUE

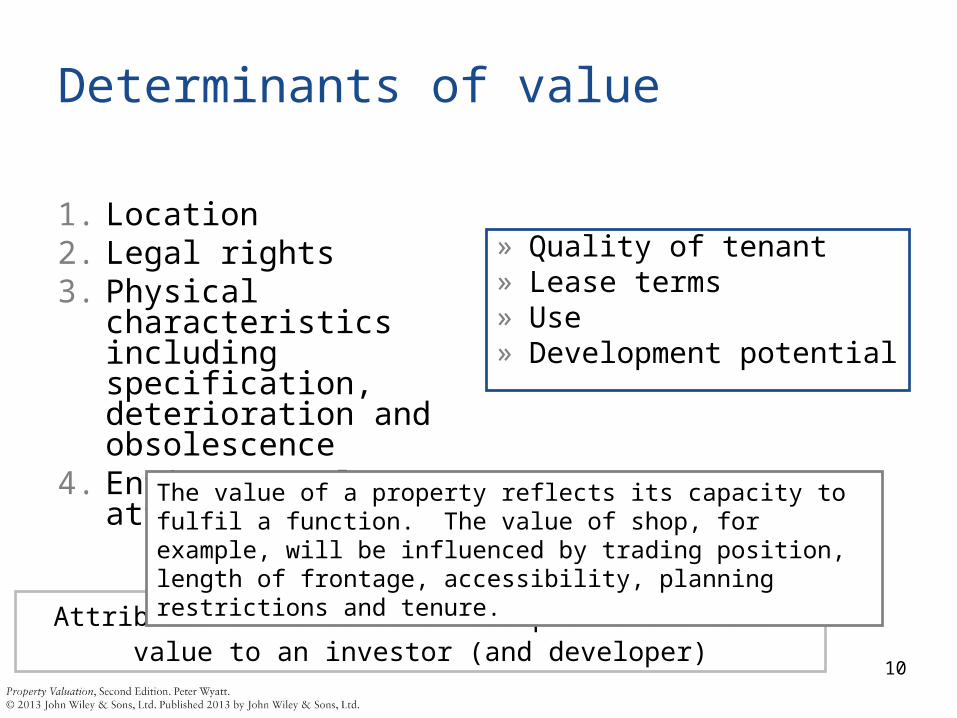

Determinants of value

1. Location2. Legal rights3. Physical characteristics

including specification, deterioration and obsolescence

4. Environmental attributes

» Quality of tenant» Lease terms» Use» Development potential

10

Attributes of value to an occupier are also of value to an investor (and developer)

The value of a property reflects its capacity to fulfil a function. The value of shop, for example, will be influenced by trading position, length of frontage, accessibility, planning restrictions and tenure.

Average house prices in London in the third quarter of 2000

1. Location

2. Legal rights• Type of lease

– Head-lease, sub-lease• Incentives

– Rent-free periods, financial contributions, works• Length of lease term• Break rights

– Fixed, rolling, benefit, notice, conditions

• Security of tenure• Rent reviews

– Upward-only, index-linked, turnover

12

Two main methods of leasing offices; whole building to single tenant (best) or suites to several tenants (service charges)Industrial voids due to economic conditions, changes in manufacturing practice

Warehouse voids as demand varies with economic activity, changing technological factors and ‘just-in-time’ production

2. Legal rights• Alienation

– Assignment, sub-letting, sharing

• Service charge obligations• Repairing obligations• Alterations• Use restrictions• Insurance

13

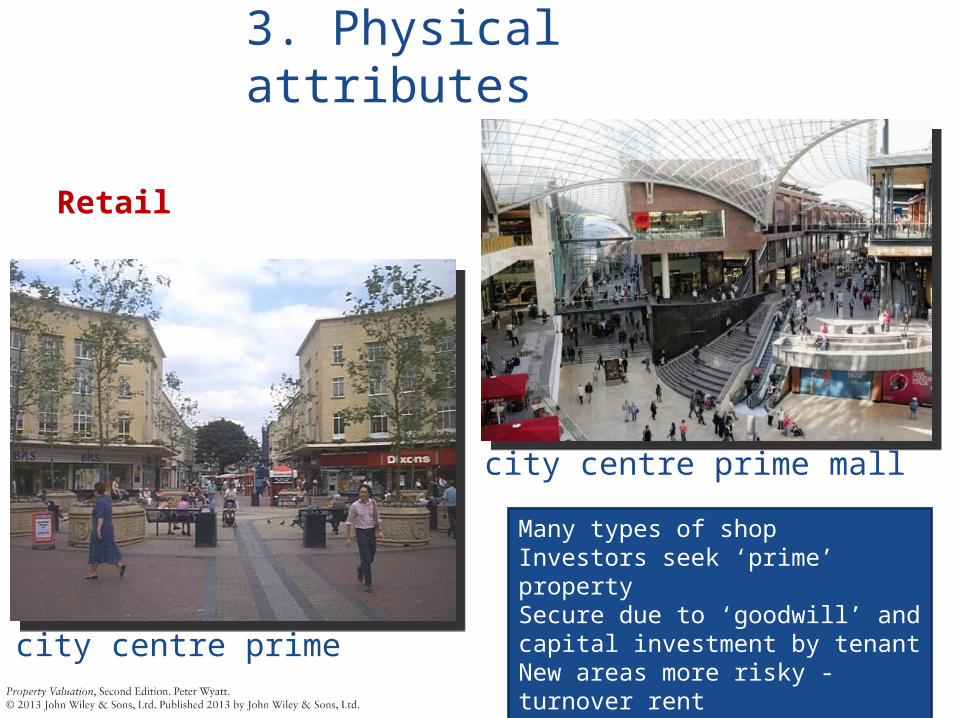

3. Physical attributes

city centre prime

city centre prime mall

Retail

Many types of shopInvestors seek ‘prime’ propertySecure due to ‘goodwill’ and capital investment by tenantNew areas more risky - turnover rent

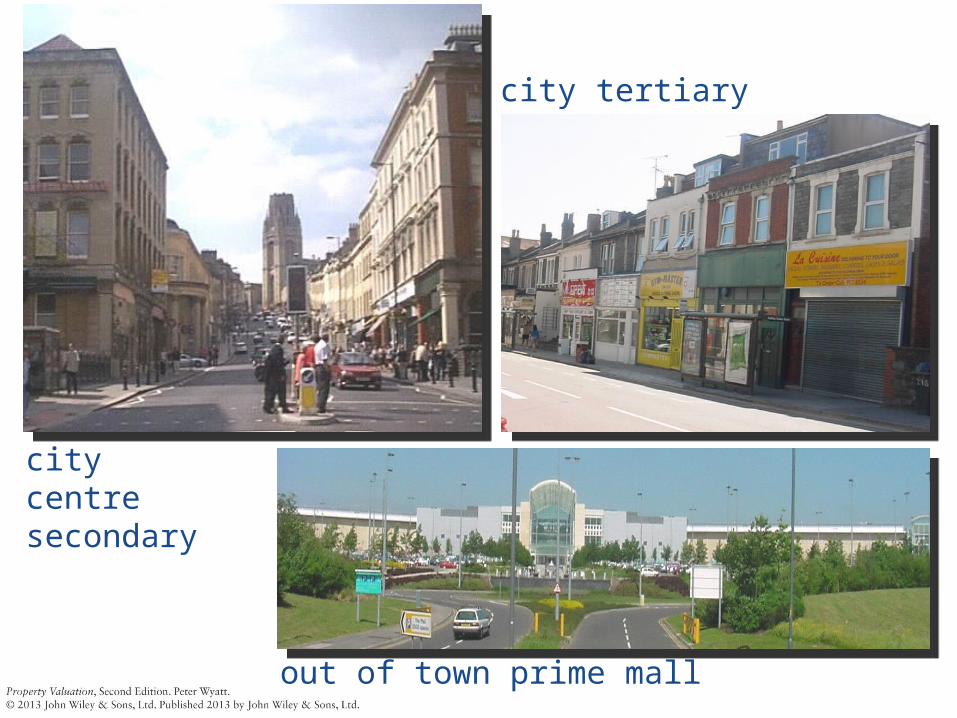

city tertiary

citycentresecondary

out of town prime mall

city centre prime…

…and

co

nvers

ion

s-p

rim

e/s

eco

nd

ary

wide range of types

Offices

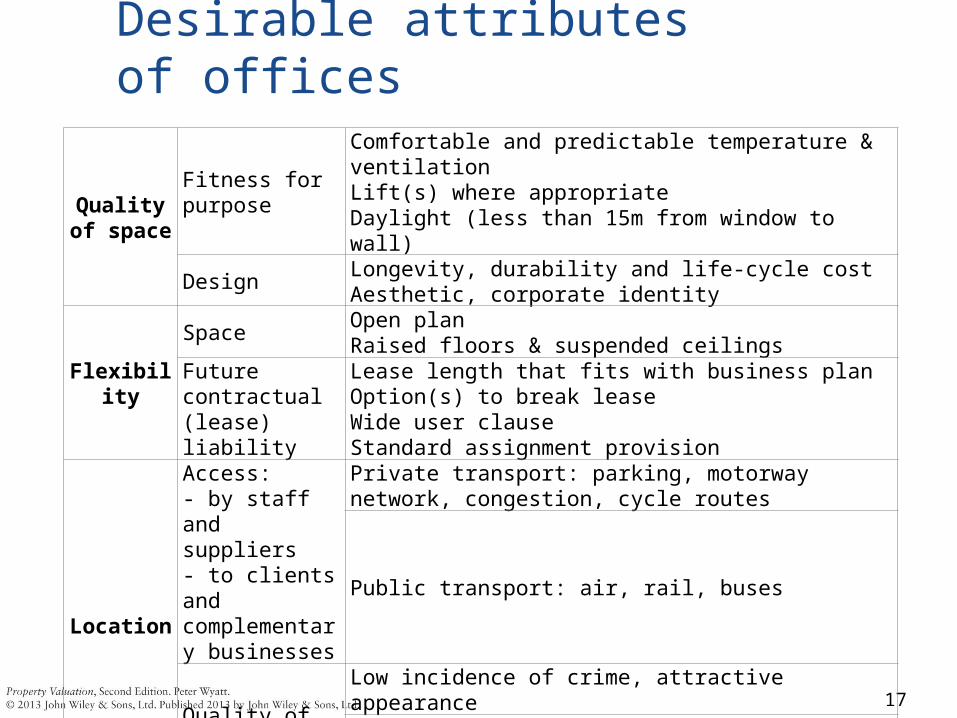

Desirable attributes of offices

17

Quality of space

Fitness for purpose

Comfortable and predictable temperature & ventilationLift(s) where appropriateDaylight (less than 15m from window to wall)

DesignLongevity, durability and life-cycle costAesthetic, corporate identity

Flexibility

SpaceOpen planRaised floors & suspended ceilings

Future contractual (lease) liability

Lease length that fits with business planOption(s) to break leaseWide user clauseStandard assignment provision

Location

Access:- by staff and suppliers- to clients and complementary businesses

Private transport: parking, motorway network, congestion, cycle routes

Public transport: air, rail, buses

Quality of surroundings

Low incidence of crime, attractive appearanceAccess to: open space, retail, leisure, amenities (post office, doctors, schools, opticians, dentists, pharmacists, etc.)

Offi

ces

– ou

t of

tow

n p

urp

ose

bu

ilt

pri

me a

nd

ou

t of

tow

n s

pecu

lati

ve

pri

me /

seco

nd

ary

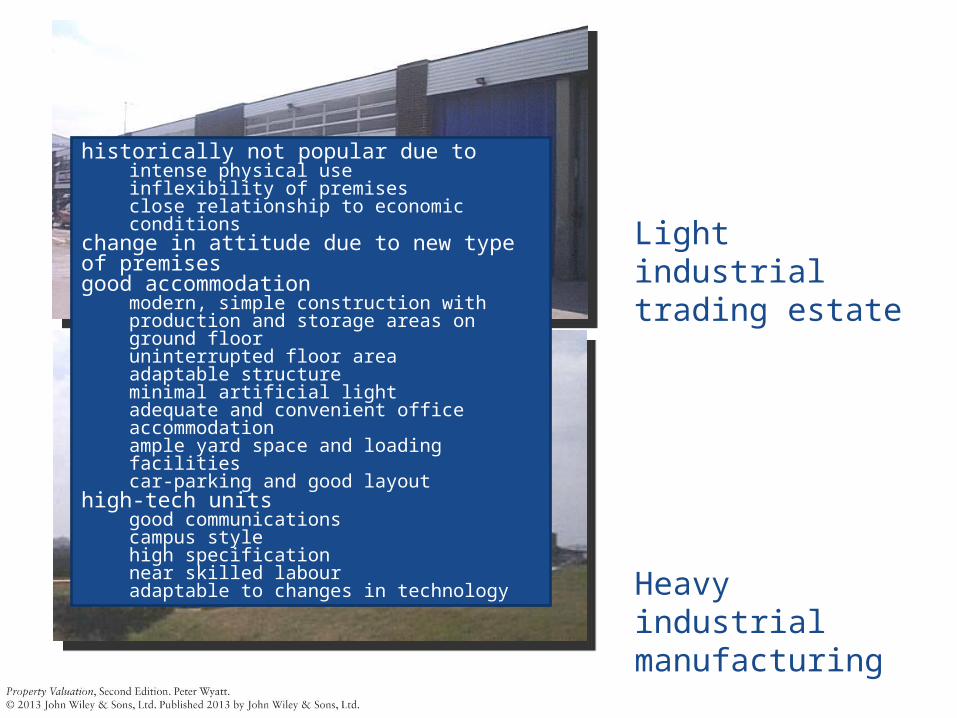

Heavyindustrialmanufacturing

Lightindustrialtrading estate

historically not popular due tointense physical useinflexibility of premisesclose relationship to economic conditions

change in attitude due to new type of premisesgood accommodation

modern, simple construction with production and storage areas on ground flooruninterrupted floor areaadaptable structureminimal artificial lightadequate and convenient office accommodationample yard space and loading facilitiescar-parking and good layout

high-tech unitsgood communicationscampus stylehigh specificationnear skilled labouradaptable to changes in technology

Warehousing

trading estateO

ffice

/ ware

hou

seou

t of to

wn

purpose-built or conversions

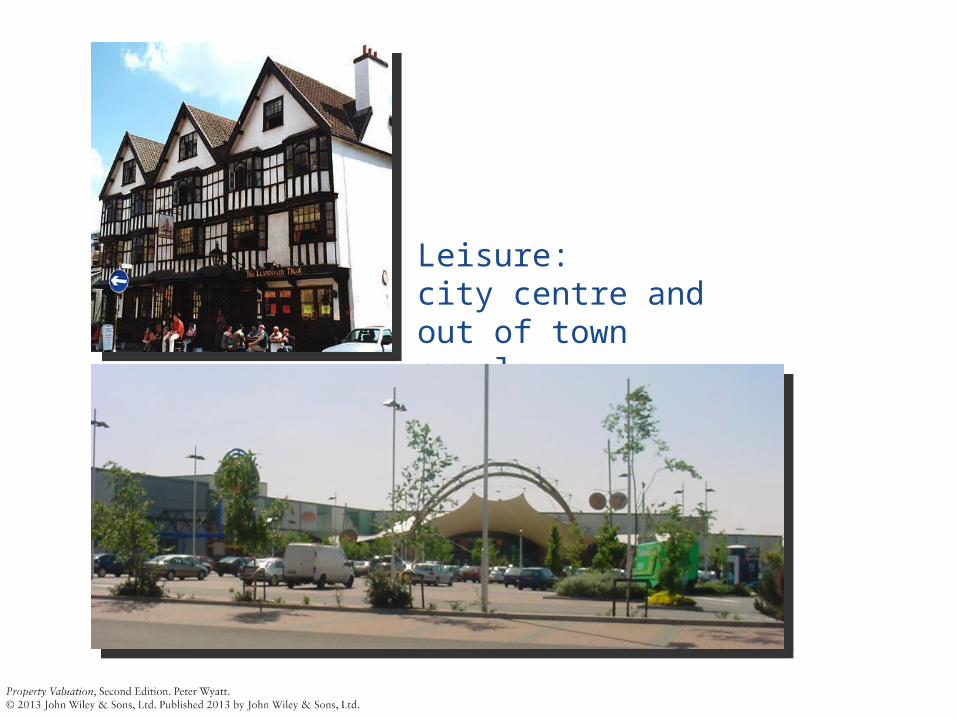

Leisure:city centre andout of town complex

4. Environmental considerations• Energy efficient• Good environmental rating

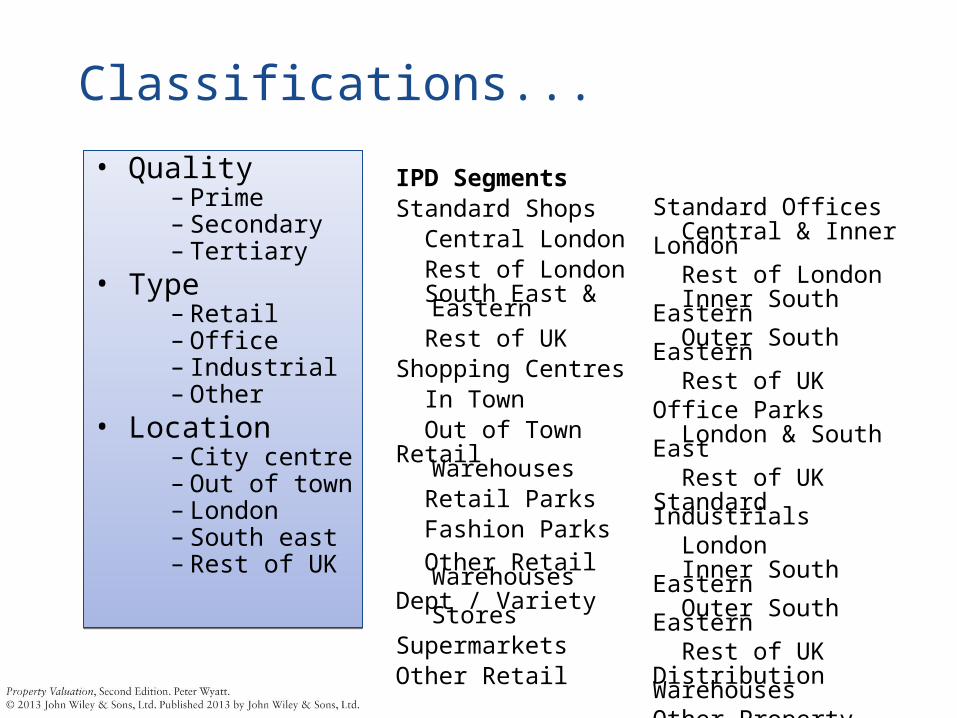

Classifications...

• Quality– Prime– Secondary– Tertiary

• Type– Retail– Office– Industrial– Other

• Location– City centre– Out of town– London– South east– Rest of UK

• Quality– Prime– Secondary– Tertiary

• Type– Retail– Office– Industrial– Other

• Location– City centre– Out of town– London– South east– Rest of UK

IPD SegmentsStandard Shops Central London Rest of London South East &

Eastern Rest of UKShopping Centres In Town Out of TownRetail Warehouses Retail Parks Fashion Parks Other Retail

WarehousesDept / Variety

StoresSupermarketsOther Retail

Standard Offices Central & Inner London Rest of London Inner South Eastern Outer South Eastern Rest of UKOffice Parks London & South East Rest of UKStandard Industrials London Inner South Eastern Outer South Eastern Rest of UKDistribution WarehousesOther Property Leisure

requires market knowledge

Asset market:Bad property investment attributes

illiquid

few transactions

decentralised market

stepped income growth

external influences

high transaction costs

depreciatesheterogeneous

lumpy

high management costs

useful portfolio diversifier

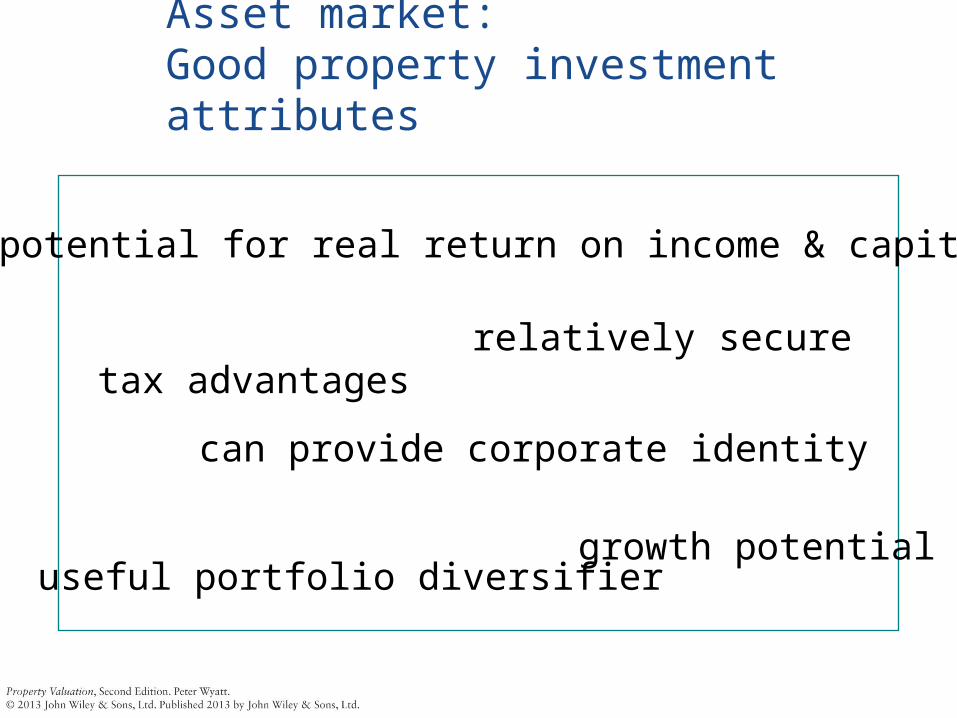

Asset market:Good property investment attributes

potential for real return on income & capital

tax advantagesrelatively secure

can provide corporate identity

growth potential

VALUATION PROCEDURES

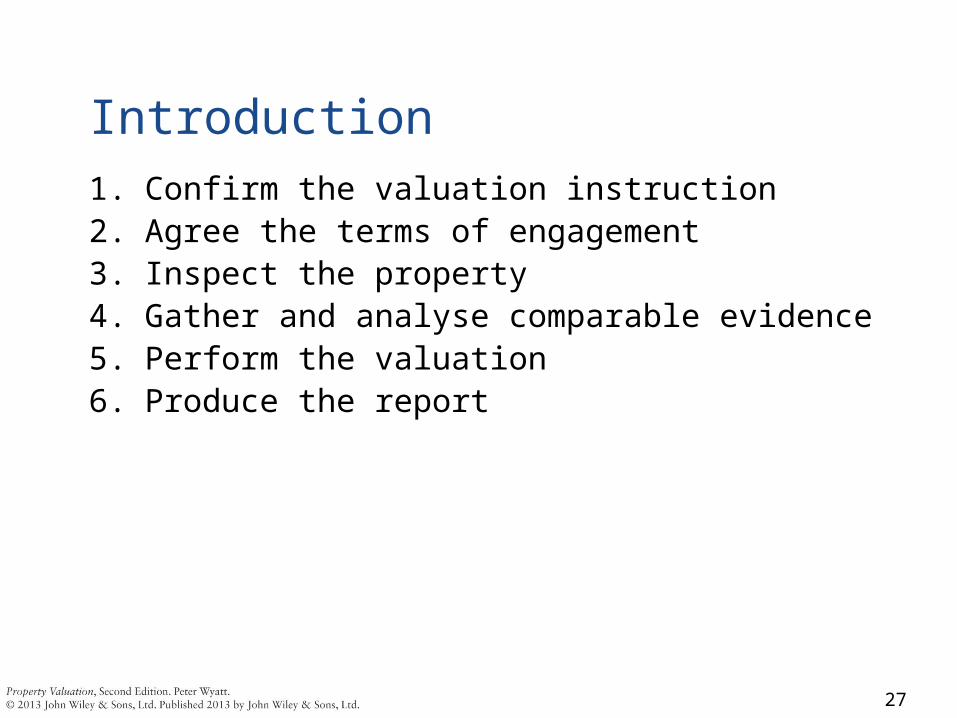

Introduction1. Confirm the valuation instruction2. Agree the terms of engagement3. Inspect the property4. Gather and analyse comparable evidence5. Perform the valuation6. Produce the report

27

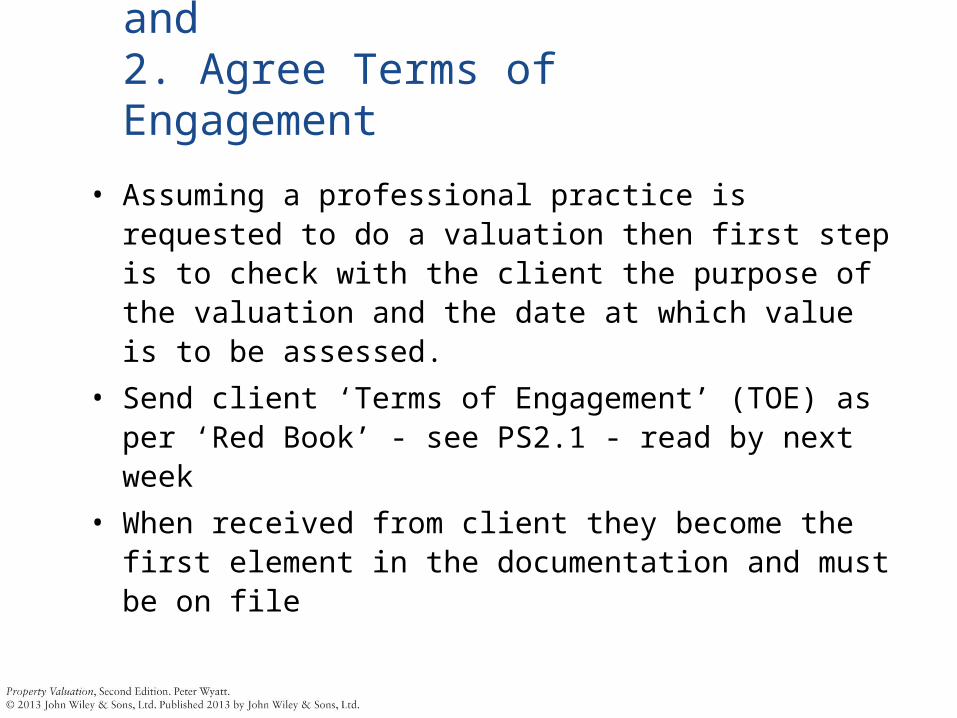

1. Confirm Instruction and2. Agree Terms of Engagement

• Assuming a professional practice is requested to do a valuation then first step is to check with the client the purpose of the valuation and the date at which value is to be assessed.

• Send client ‘Terms of Engagement’ (TOE) as per ‘Red Book’ - see PS2.1 - read by next week

• When received from client they become the first element in the documentation and must be on file

3. Property Inspection• Inspections and investigations must always be

carried out to the extent necessary to produce a valuation which is professionally adequate for its purpose

• An essential part of the valuation process• Must be carried out in a logical and methodical manner• Must meet PS4.1 - read commentary (provides some

general guidance on the extent of the inspection)• Must be properly documented

4. Collection and Analysis of Comparables

• Central part of the valuation process• Must be evidenced on file

The documentation must include evidence of the comparables used and how they were analysed. Handwritten notes, notes of telephone calls, copies of particulars etc. NB these don’t get sent to the client.

5. Valuation CalculationsThis is what it is all about.These calculations are likely to be handwritten and these

‘working notes’ must be retained on file.Or could be done on a spreadsheet in which case a printout

should be kept on file.If valuation software is used then a printout should be put on

file.Do not send to the client.

6. Report to the Client• Could take many forms depending on the client.• Form reports - mortgages• Memos - internal• Narrative - private clients• NB must have regard to the Red Book which sets standards

for reports

A building society mortgage valuation would be on a form that they supply - may be submitted electronically.A private client would probably be sent a full narrative report that conforms to the standards set out in the Red Book.

Summary

• Valuers carry out valuations for a client• The outcome will usually be a written report• Before the report can be written a series of tasks will be

undertaken - valuation process• The tasks will be carried out to a high standard in accordance

with agreed standards and guidelines• All stages will be fully documented and held on file• Failure to meet the standards could lead to a negligence claim

and professional indemnity insurance is essential.

MEASUREMENT

Measurement

• RICS Code of Measuring Practice sets out definitions for measurement of land and property

• Defines:– Gross external area (GEA)– Gross internal area (GIA)– Net internal area (NIA)– Zoning (see next slide)– Others: clear internal height, cubic content, eaves

height, plot ratio

… and advises when and how each should be used

REGULATION OF VALUATIONS

Regulation in the UK

• Self regulation by professional body (RICS) – responsible for monitoring and ethics

• Standards published by IVS and RICS• Mandatory on all surveyors and asked for by main users of valuations• Deal with process rather than methods of valuation• Departure from Red Book procedures without good reason could be

evidence of negligence• Registered Valuer Scheme

Regulation of the valuation process

• Valuation procedures in the UK are regulated to a large extent by the Royal Institution of Chartered Surveyors (RICS)

• The RICS:– Ensures accountability– Establishes education and training requirements– Sets standards– Imposes disciplinary procedures– Publishes the Appraisal and Valuation Manual (The

Red Book)

The Red Book• Regulates valuation

procedures• Most valuation work is

covered• Includes standards for

specific-purpose valuations:– Asset valuations– Valuations for stock market

listing particulars– Valuations for mergers,

acquisitions, etc.

Why Standards?• Good technique only gets you so far.• Valuations must be:

– Credible– Cogent

• Credibility depends on trust:– Trust requires ethics

• Cogency depends on sound communication:– numerical AND– Verbal

• Standards fall into three broad groups:– Ethical– Procedural– Definitional

Ethical Standards• Relate to behaviour of individual valuer or firm• Key requirements:

– Independence– Integrity– Objectivity

• Ethical requirements distinguish a profession from a trade• Not unique to valuation• Key is not just to behave ethically but to be seen to be behaving ethically• Key components an ethical regime

– Transparency– Enforceability

• UK model is self regulation• Elsewhere professional behaviour often regulated by statute, eg licensing

Procedural Standards•Set fundamental rules for processing

•Why?– Protecting the user; they need to understand what they are

getting.

– Protecting the valuer; reputation would suffer if users did were dissatisfied with product

Rules thus needed to require valuer to clearly explain:– What is to be done

– What has been done

Definitional Standards•Needed to avoid “Tower of Babel” syndrome

•Value is an ephemeral concept; – Based on hypotheses not fact

– Mixture of science and art

– Jargon can confuse or mislead users and undermine credibility

•Need for principles and objectives to be codified and common terminology developed to clearly communicate valuation concepts

True or False?• The Red Book tells me all I need to know about

valuation• The Red Book sets out the RICS approved methods

of valuation• If I comply with the Red Book my valuation will not

be negligent• If I comply with the Red Book my valuation is more

likely to be understood by the client and anyone else relying on it

Regulates process not function• What to do, not how to do it• Minimum procedures that have to be adopted by all Chartered

Valuation Surveyors• Promote use of consistent bases and other definitions to aid

public understanding• Extends Rules of Conduct with specific requirements for valuation• Provides regulatory framework for valuation advice• Provides client and public confidence in valuation by requiring

ethical and transparent approach• Promotes consistent definitions and terminology• Assists clients in understanding what is being valued, the

assumptions made and the limitations that apply• Promulgates procedural protocols agreed with client bodies, e.g.

CML, BBA

Monitoring• Until 2005 only reactive monitoring of compliance carried

out by RICS, i.e. investigating complaints received• Now proactive monitoring regime in place• Only Regulated Purpose Valuations covered at present• Likely to be extended to all valuation work in due course

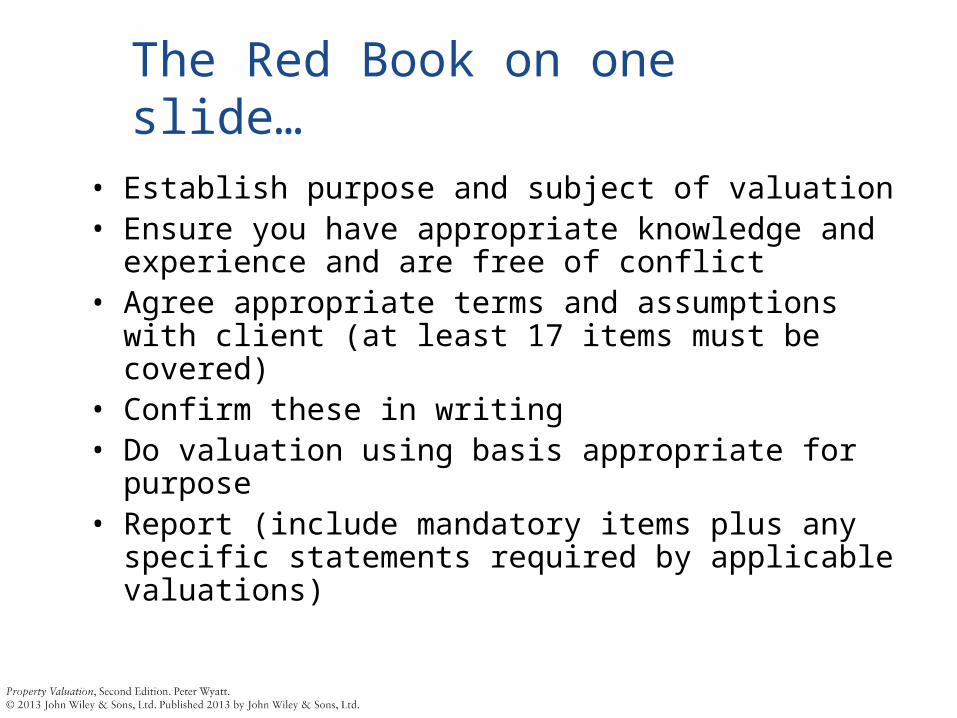

The Red Book on one slide…• Establish purpose and subject of valuation• Ensure you have appropriate knowledge and experience

and are free of conflict• Agree appropriate terms and assumptions with client (at

least 17 items must be covered)• Confirm these in writing• Do valuation using basis appropriate for purpose• Report (include mandatory items plus any specific

statements required by applicable valuations)

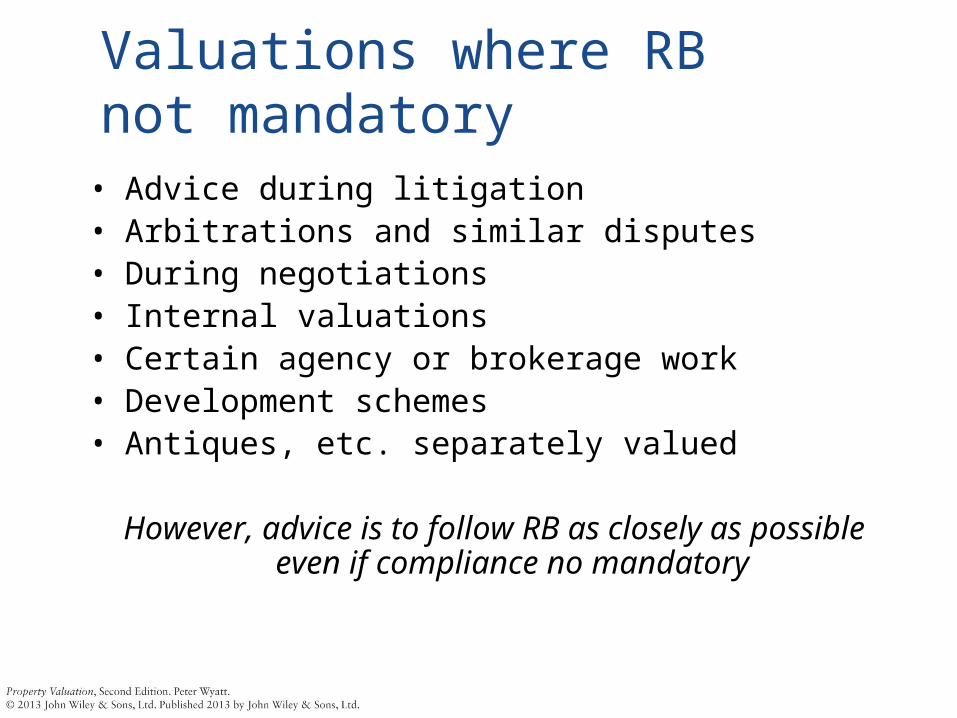

Valuations where RB not mandatory

• Advice during litigation• Arbitrations and similar disputes• During negotiations• Internal valuations• Certain agency or brokerage work• Development schemes• Antiques, etc. separately valued

However, advice is to follow RB as closely as possible even if compliance no mandatory

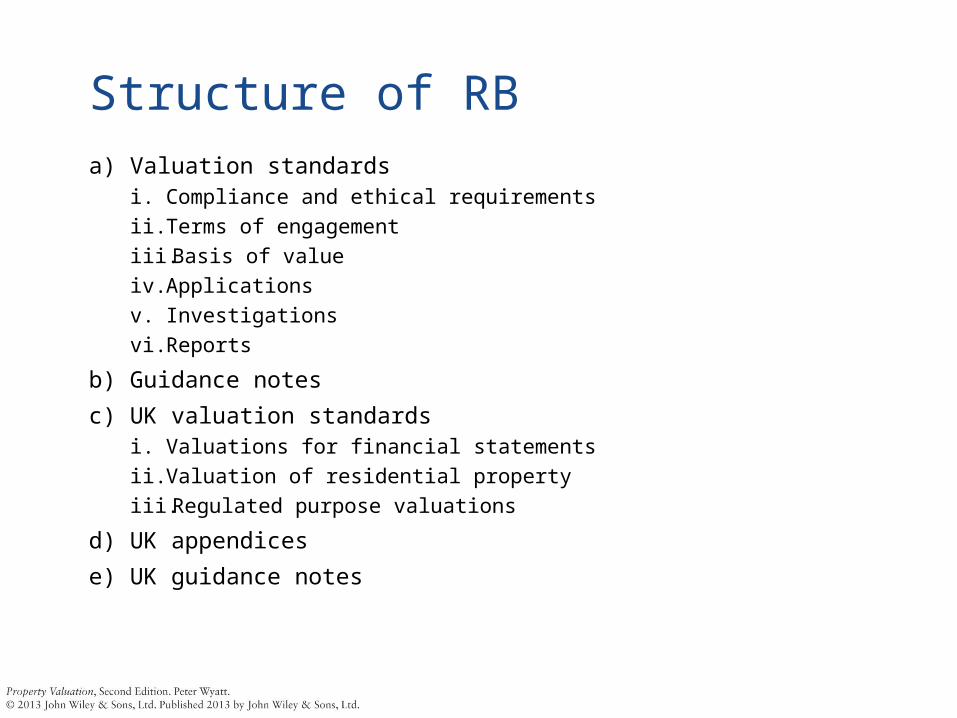

Structure of RBa) Valuation standards

i. Compliance and ethical requirementsii. Terms of engagementiii. Basis of valueiv. Applicationsv. Investigationsvi. Reports

b) Guidance notes

c) UK valuation standardsi. Valuations for financial statementsii. Valuation of residential propertyiii. Regulated purpose valuations

d) UK appendices

e) UK guidance notes

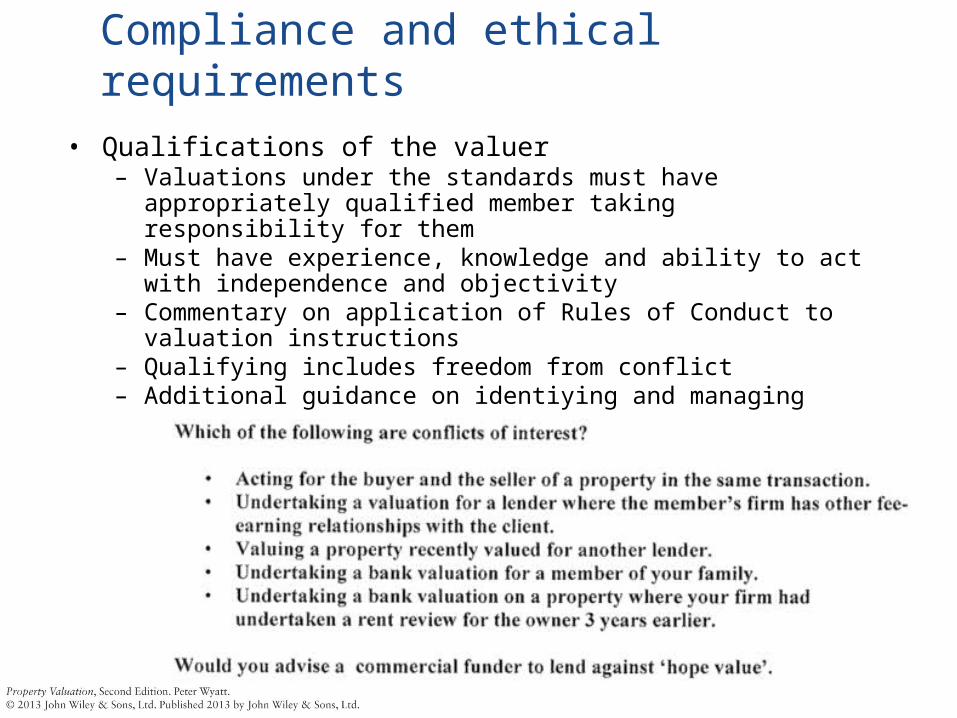

a) Valuation standardsCompliance and ethical requirements

• Qualifications of the valuer– Valuations under the standards must have appropriately qualified member

taking responsibility for them– Must have experience, knowledge and ability to act with independence

and objectivity– Commentary on application of Rules of Conduct to valuation instructions– Qualifying includes freedom from conflict– Additional guidance on identiying and managing conflicts of interest when

undertaking valuations

Terms of engagement• RoC require terms to be confirmed in writing for all work

undertaken for a client• RB extends general requirement in relation to valuation work• Important that valuer and client are clear about purpose of

valuation and assumptions valuer will make• Checklist of 17 minimum things to include• Assumptions:

– All valuations are subject to assumptions– No such thing as a standard assumption which can be implied without

being stated– Made where reasonable for valuer to accept something as fact

without specific investigation– Special assumptions arise mainly where it is necessary to assume

something is different from status quo or where it is an assumption that would not normally be made by a purchaser in the market

Bases of valuation• MV

– International definition agreed in 1993– Supported by conceptual framework– Basis for all valuations– Will normally need qualification or assumption to apply in correct context

(e.g. with VP, subject to lease, as an operational entity, as an individual item for removal, etc.)

• MR– Adaptation of MV to a recurring rather than a single payment– Must be quoted in context of assumed lease terms– Must be accompanied by assumed basic lease terms (e.g.

inclusive/exclusive, FRI/IRI, etc., duration, review pattern, incentives, etc.)• Fair Value• Special Value• Synergistic Value

Assumptions and Special Assumptions

• Knowing basis of valuation is not enough• For valuation to be credible and useful the whole scenario

of hypothetical transaction must be set out• Assumptions and special assumptions need to be thought

about and explained to client before proceeding

Investigations• No such thing as a minimum standard of inspection• Extent of inspection (if any) depends on the terms of

engagement• Investigations• Verification of information

Reports• Signatory must be an individual• List of mandatory contents – echo those in terms of

engagement• Do not use Formal / Informal to describe reports• Provisional valuations – any changes made should have an

audit trail

b) Guidance Notes• Valuation certainty• Valuation of individual trade related properties• Valuation of portfolios and groups of properties• Personal property• Plant and equipment• Depreciated replacement cost method of valuation for

financial reporting

c) UK valuation standardsi. Valuations for financial statements

• Relevant to valuations under UK GAAP, e.g.– Non-listed companies– Public sector – local authorities– Registered Social Landlords

• Eventually will disappear as either IFRS adopted or UK GAAP merges with IFRS• EUV – the additional assumptions

– …the buyer is granted VP…– …of all parts of the property required by the business…– …disregarding potential alternative uses…– …disregarding …any other characteristics of the property that would cause the MV

to differ from that needed to replace the remaining service potential at least cost• DRC

– Required reporting basis under UK GAAP for specialised property– For all other purposes, including valuations under international accounting

standards, it is regarded as a method used to derive MV (or any appropriate basis)– Used only where there is no sales evidence– Use of DRC approach must be disclosed

ii. Financial Statements – Specific Applications (UKPS2)• UK Listing Rules• Takeover Code• Authorised Unit Trusts• Unregulated Unit Trusts• Pension Funds• Insurance Company Assets

All have subtle variations on rules or specific reporting requirements

iii. Valuation of residential property

• Residential mortgage valuations– Specification agreed with CML – sets out generally accepted duties

and limitation for undertaking residential mortgage work– Recognises that these valuations mostly undertaken on pro forma

style reports with no scope for commentary

iv. Regulated Purpose Valuations

• What is a RPV?– Financial statements under IAS or UK GAAP– Listing particulars and circulars– Takeovers and mergers– Unit trusts (authorised and unregulated)– Pension funds (not SIPPS)– Insurance company assets

• Matters addressed– Rotation of personnel– Extent and duration of relationship between a valuer’s firm and

client– Fee earning relationship between valuer’s firm and client –

expressed in 5% bands of total turnover– All must be disclosed in report

e) UK Guidance Notes• Land and buildings apportionments for lease classification

under IFRS• EU directives and regulations relevant to valuation• Valuations for CGT, IHT and SDLT• Local authority disposal of land for less than best

consideration• Analysis of commercial lease transactions• Valuations for charities