What is Happening with Personal Loan Losses? - peeriq.com · • Availability of unsecured personal...

14

What is Happening with Personal Loan Losses? Ram Ahluwalia CEO, PeerIQ Nick Andreadis Head of Data Intelligence Ashish Dole Head of Research

Transcript of What is Happening with Personal Loan Losses? - peeriq.com · • Availability of unsecured personal...

What is Happening with Personal Loan Losses?

Ram Ahluwalia

CEO, PeerIQ

Nick Andreadis

Head of Data Intelligence

Ashish Dole

Head of Research

2

P E E R I Q I N T R O

PeerIQ is a NYC-based data &

analytics firm that enables lenders

and institutional investors to

transact with confidence.

Risk Management Offering

1. Risk Analytics

▪ Benchmarking / Portfolio Mgmt

▪ Valuation Services

▪ Credit Facility Management

2. Data

• TransUnion Derived Credit Insights

• 25+ lenders in a standardized

format

TO D AY ’ S C O N S U M E R C R E D I T PA R A D O X

3

Macro conditions

are strong…

…yet credit

performance is

weakening

How can better data help us reconcile this

contradiction?

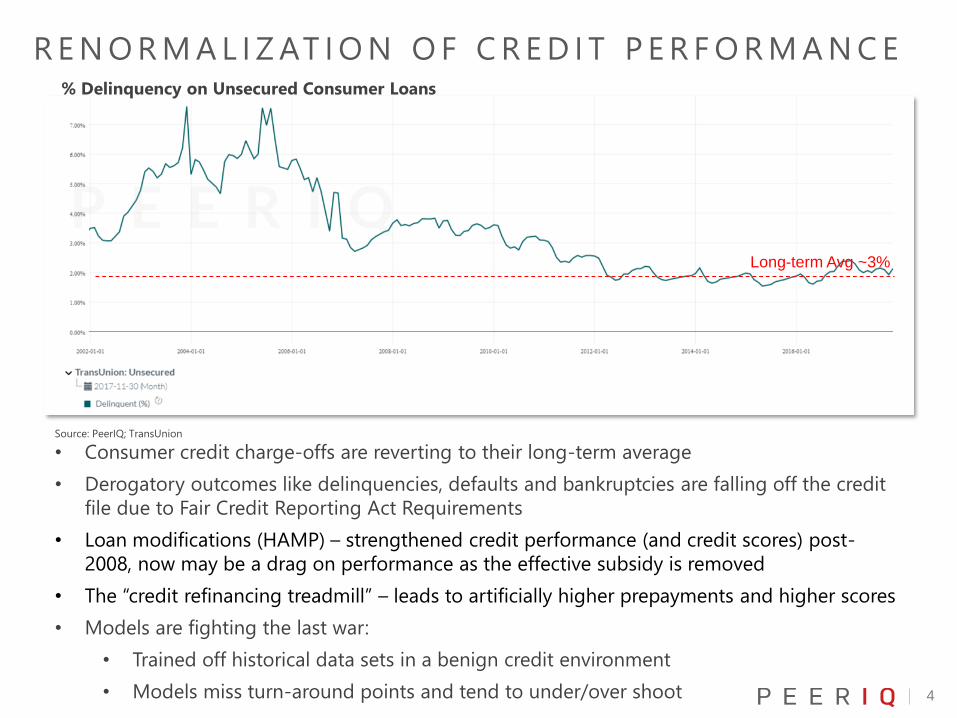

R E N O R M A L I Z AT I O N O F C R E D I T P E R F O R M A N C E

4

• Consumer credit charge-offs are reverting to their long-term average

• Derogatory outcomes like delinquencies, defaults and bankruptcies are falling off the credit

file due to Fair Credit Reporting Act Requirements

• Loan modifications (HAMP) – strengthened credit performance (and credit scores) post-

2008, now may be a drag on performance as the effective subsidy is removed

• The “credit refinancing treadmill” – leads to artificially higher prepayments and higher scores

• Models are fighting the last war:

• Trained off historical data sets in a benign credit environment

• Models miss turn-around points and tend to under/over shoot

Source: PeerIQ; TransUnion

% Delinquency on Unsecured Consumer Loans

Long-term Avg ~3%

M O D E L S F I G H T I N G T H E L A S T WA RWhy FICO is flawed

5

• Traditional credit scores are backward

looking and are designed to rank-order

credit risk

• Not cash-flow oriented and does not

capture underwriting quality of the loan

• Not time-homogenous: A credit score of

700 immediately post-crisis is much stronger

than a 700 credit score pre-crisis

• Wrong measurement: The credit-score

does not evaluate the probability of a

specific loan defaulting, but rather the

probability of the borrower defaulting (e.g.,

ignores payment priority and the

relationship of lender to the borrower)

• Cannot be summarized via averages: FICO

is defined on a logarithmic basis – weighted

averages distort interpretations

• Credit scores have blind spots (ex: ignore

info from 7 years per the FCRA)

Distribution of credit scores on Avant shelf have

not changes significantly over the last two years

However, Avant has:

• Tightened credit quality

• Reduced size of the loan 20% from $5,348

from $6,589

• Reduced Weighted Average Term – 94%

loans are below 36-month term vs. 47% in

Avant 2016-C

Source: PeerIQ

6

(3) To a person which it has reason to believe(A) intends to use the information in connection with a credit transaction involving the consumer on whom the

information is to be furnished and involving the extension of credit to, or review or collection of an account of, the consumer; or

(B) intends to use the information for employment purposes; or(C) intends to use the information in connection with the underwriting of insurance involving the consumer; or(D) intends to use the information in connection with a determination of the consumer's eligibility for a license or

other benefit granted by a governmental instrumentality required by law to consider an applicant's financial responsibility or status; or

(E) intends to use the information, as a potential investor or servicer, or current insurer, in connection with a valuation of, or an assessment of the credit or prepayment risks associated with, an existing credit obligation;

(F) otherwise has a legitimate business need for the information(i) in connection with a business transaction that is initiated by the consumer; or(ii) to review an account to determine whether the consumer continues to meet the terms of the

account.(G) executive departments and agencies in connection with the issuance of government-sponsored individually-

billed travel charge cards.

P E R M I S S I B L E P U R P O S E

• Ambiguity on whether permissible purpose extends beyond whole loan investors to bond

investors.

• Limits the ability of ABS and warehouse lenders investors to risk manage and control for

the effects from “derogs” and loan mods

• Reach out to your regulator and trade associations (SFIG, SIFMA, MLA) to level-up the

health and integrity of our capital markets

I N C R E A S E D S U P P LY O F C R E D I T

7

• Credit availability is at an all-

time high – driven by new

entrants and rising credit

scores

• Credit growth YOY (8%) has

outpaced growth in GDP

and personal income

• Competition for market

share can lead to looser

underwriting standards

• Availability of unsecured

personal loans can increase

borrower indebtedness

post-origination (especially

if the loans are not used for

debt consolidation)

Source: PeerIQ; TransUnion

Source: PeerIQ; St. Louis Fed

P E R S O N A L LO A N S A R E N OT S U B S T I T U T I N G

F O R C R E D I T C A R D O R OT H E R D E BT

8

• Personal loans are used to refinance high rate debt less than 20%. Borrowers see the

personal loan as another type of borrowing instrument

• Behavior varies by segment. Initial analytics indicates super-prime borrowers are

taking down personal loans; where as subprime has more paydown

Source: PeerIQ; TransUnion

% of Balance Used to Refi Other Debt

P R I O R I T Y O F PAY M E N T S I S S H I F T I N G

9

• Delinquencies on Unsecured Consumer Loans are second only to

those on Auto loans

• Payment priority has shifted 3x in the case of auto

• New channels and technology are leading to more rapid shifts in

consumer behavior (e.g., the “Lyft effect”, cell phones, new

digital spaces, etc.)

% Delinquent by Consumer Credit Asset Class

D R I V E R S O F C R E D I T P E R F O R M A N C E

10

• Renormalization of credit performance

• “Derogs” falling off the bureau

• Loan modifications

• “Credit refinancing treadmill”

• Increased supply of credit / underwriting

• Personal loans shifting from debt refi to general purpose

• Priority of payments is shifting

• Outlook

O U T LO O K

11

Consumer Relationship

“Big Tech”

Money Center Banks

/ Wealth Management

“FinTech”

Community Banks /

Credit Unions

• Competition to own the Customer

• New entrants: “Big Tech” (e.g.,

Intuit, Paypal, Amazon, Google)

• Secured Lending - $300 Bn – in a

few short years, is now half the

size of the credit card industry by

targeting Super Prime borrowers

• Lenders with captive customer

acquisition channels and novel data

are selecting quality borrowers. A

few examples:

• Amazon Lending -$3 Bn in small-

business loans originated

• Big Tech + Big Bank:

Chase/Amazon; Barclays/Uber

• FinTech + Small Banks: unique

origination channels (POS), new

products

12

P E E R I Q C O N S U M E R C R E D I T I N S I G H T S

ABS/Whole Loan

Investor

Segment Objectives Addressed

• Buy/Sell a bond or resid

• Provide capital

to/purchase loans from

originator

Sample Questions Addressed

• How is the are loans in a particular

credit tier performing? Has

performance improved or

deteriorated over time?

• What returns should I expect if I

invest in a given asset class/credit

tier?

• How has underwriting changed over

time?

Macro Funds,

Large PE,

Economists

• Assess the overall state of

the economy

• Identify trades based on

larger macroeconomic

trends

• Strategic view into

portfolio companies or

potential targets

• How “healthy” is the US consumer?

• Is credit more or less available than

in the past?

• How has consumer behavior

changed over time? Are credit dollars

being allocated in the same way as

the past?

• How does US consumer credit

compare to other macro data items

(GDP, etc.)

Non Bank

Originators,

Regional Banks, &

Credit Unions

• Adjust pricing/marketing

strategy based on macro

factors

• Asses risk to existing

portfolio based on

consumer behavior

• How has the source of credit

changed over time (bank vs. non

bank, etc.)

• Are there particular credit tiers/sub

segments of the population that are

over/underperforming?

• Is my pricing in line with the market?

• Are consumers seeking out more or

less credit than in the past

13

C O N S U M E R C R E D I T I N S I G H T S E X A M P L E

• Analyze multiple vintages and observe borrower attributes at various points over the life of the

vintage.

• Utilization on revolving products reveals significant differences across the vantage bands, with

Subprime borrowers decreasing their utilization and Prime borrowers increasing utilization

Source: PeerIQ; TransUnion

14

• Subscribe to newsletter:

• Download research:

www.peeriq.com/research

• Request a Demo

Q & A