What Has Been Happening to Aggregate Concentration in the ... · What Has Been Happening to...

37

What Has Been Happening to Aggregate Concentration in the U.S. Economy in the 21 st Century? Lawrence J. White & Jasper Yang Stern School of Business New York University [email protected] [email protected] Presentation at CRESSE, Crete, July 1, 2017 1

-

Upload

nguyenlien -

Category

Documents

-

view

218 -

download

0

Transcript of What Has Been Happening to Aggregate Concentration in the ... · What Has Been Happening to...

What Has Been Happening to

Aggregate Concentration in the U.S.

Economy in the 21st Century?

Lawrence J. White & Jasper Yang Stern School of Business New York University [email protected] [email protected] Presentation at CRESSE, Crete, July 1, 2017

1

Overview

Introduction

Why is aggregate concentration interesting?

What should be the measurement basis(es)?

The measurement bases that we use

Data from the U.S. Bureau of the Census

Data from Fortune and Forbes

Conclusion

2

Introduction

Aggregate concentration is the percentage of overall economic activity that is accounted for by the largest X firms

– How “important” are the largest X companies?

Casual impressions from the media are that aggregate concentration is growing

– Lots of mega mergers

– Lots of references to “Big Pharma”, “Big Oil”,

“Wall Street”, “Big Food”, “Big Music”, etc., etc.

But the most recent study of aggregate concentration was for the last quarter of the 20th century 3

Why is aggregate concentration

interesting? (1)

Aggregate concentration has little (if any) relevance to antitrust (competition) policy

– Antitrust is about competition (actual or prospective)

in relevant markets

Where market power is being or could be exercised

– Even if there were only 100 companies in the U.S.

economy, if they were all present in all relevant

markets, then we would expect to see close to

atomistic competition

Except for multi-market contact issues

4

Why is aggregate concentration

interesting? (2)

Instead, the issue of aggregate concentration is about the “tone” or “feel” of an overall economy

– How “important” are the largest X companies?

– What would it feel like to be in an economy where

there were only 100 – or even only 1000 – mega

companies?

There may be trade-offs

– Economies of scale and scope

versus

– A more diverse and diversified economy 5

What should be the measurement basis:

Sales? Sales (revenue or units or “shipments”) is often a

good basis for antitrust purposes in relevant markets

– Standard oligopoly models use “output”

Sales revenue is readily available for publicly traded (large) firms

Sales revenue is the basis for the Fortune “500” ranking

But for aggregation (of sales revenue) across firms in all markets: a double counting problem

– Suppose a vertically integrated company separates into

2 separate companies: a “supplier” and a “customer”… 6

What should be the measurement basis:

Assets? Assets may a basis for antitrust purposes if capacity

is relevant with respect to competition issues

Assets are readily available for publicly traded firms

But for an aggregation across firms in all markets that includes financial institutions: a double counting problem

– A loan by a bank to company counts as an asset for the

bank

– If the company invests the proceeds of the loan into a

factory or machinery or inventories…

Assets may be subject to accounting vagaries 7

What should be the measurement basis:

Employment? Employment is not relevant for antitrust purposes

Employment can be aggregated across companies

Employment data are available for publicly traded companies

Employment (jobs!) and employment growth is an important social issue

– What size firms provide what % of overall employment

(and/or what % of job growth) is often discussed in the

media

But employment numbers don’t tell us about “good jobs” (wages, human capital, etc.)

8

What should be the measurement basis:

Payroll? Payroll does tell us something about labor

income

– Maybe tell us something about income distribution?

Payroll can be aggregated across firms

Payroll is a component of value added

But payroll data ignore fringe benefits

But payroll data are not readily available for individual firms

9

What should be the measurement basis:

Profits? Profits can be aggregated across firms

Profits are available for publicly traded firms

Profits are a component of value added

Profits data are sometimes discussed in the media

– E.g., the % of corporate profits that were attributable

to the financial services sector in the 2000s

But profits data may be subject to accounting vagaries

10

What should be the measurement basis:

What about franchise operations? Franchise arrangements are important for many

multiple-location retail operations

– E.g., fast food, hotels/motels, auto rental agencies

McDonald’s: 90% of U.S. outlets, 82% of worldwide

outlets are owned by franchisees

– But not supermarkets, department stores

Franchisor data includes only royalty payments from franchisees (not brand-wide aggregates)

Is the impact of McDonald’s understated?

– McDonald’s was ranked #109 for 2015 by Fortune

based on sales (consolidated = worldwide)

If franchisees’ sales were included, the rank would be #31

11

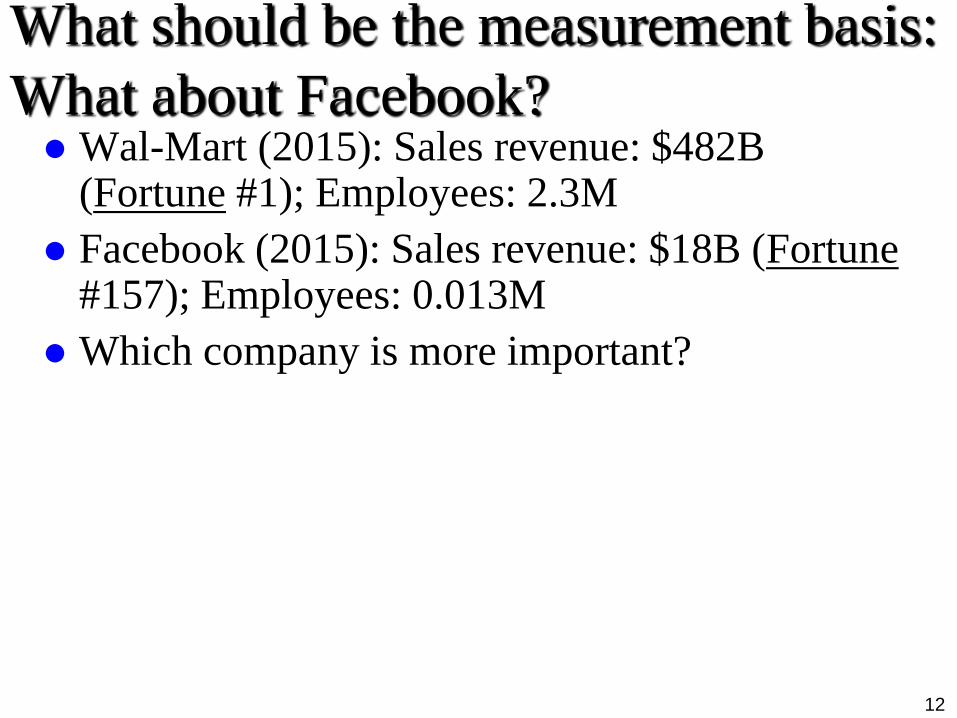

What should be the measurement basis:

What about Facebook? Wal-Mart (2015): Sales revenue: $482B

(Fortune #1); Employees: 2.3M

Facebook (2015): Sales revenue: $18B (Fortune #157); Employees: 0.013M

Which company is more important?

12

What should be the measurement basis:

Value added? Value added may be the best all-around measure

of a company’s impact/importance in the economy

But value added data are generally not available for individual companies

13

What should be the measurement basis:

What about geography? Large companies that are headquartered in the U.S.

often have extensive operations outside the U.S.

– The Fortune and Forbes “500” lists include the

consolidated (worldwide) companies’ data

– The Census Bureau data exclude overseas operations

Large companies that are headquartered outside the U.S. often have extensive operations in the U.S.

– The Fortune and Forbes “500” lists exclude these

companies’ U.S. operations

– The Census Bureau data include these companies’ U.S.

operations

14

The measurement bases: The Bureau of

the Census data Census of Manufactures

– Value added for U.S. manufacturing: 1947-2012

(census years)

Plus an occasional year from the Annual Survey of

Manufactures

Statistics of U.S. Businesses (SUSB)

– Employment and payroll for the U.S. operations of all

companies with operations in the U.S.: 1988-2014

(annual)

Separated into firm employment size “buckets” and a

special compilation of the largest 100, 500, and 1000

companies

15

The measurement bases: the Fortune

and Forbes “500” data

Annual employment and profits for the consolidated companies (worldwide) with headquarters in the U.S.

– Forbes: 1980-2000 (years with consistent, usable data)

But after 2000…

– Fortune: 1993-2016 (years with consistent, usable

data)

Began in 1954

But before 1993…

16

17

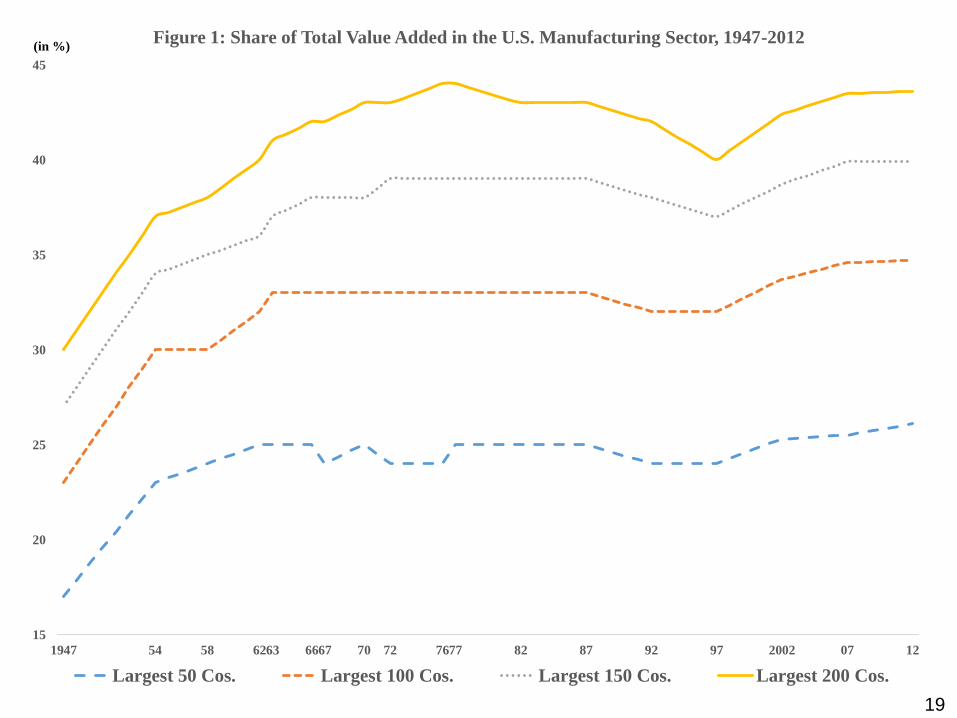

Value added for manufacturing

Bureau of the Census (Census of Manufactures) data

The share of value added attributable to the largest 50, 100, 150, and 200 companies: 1947-2012

– A sharp rise between 1947 and 1954

– A moderate subsequent rise into the 1960s

– Flat for the next 3 decades

– Moderate rise from late 1990s to 2012

Manufacturing as a % of private-sector GDP has been shrinking since the 1950s

18

19

15

20

25

30

35

40

45

1947 54 58 6263 6667 70 72 7677 82 87 92 97 2002 07 12

Figure 1: Share of Total Value Added in the U.S. Manufacturing Sector, 1947-2012

Largest 50 Cos. Largest 100 Cos. Largest 150 Cos. Largest 200 Cos.

(in %)

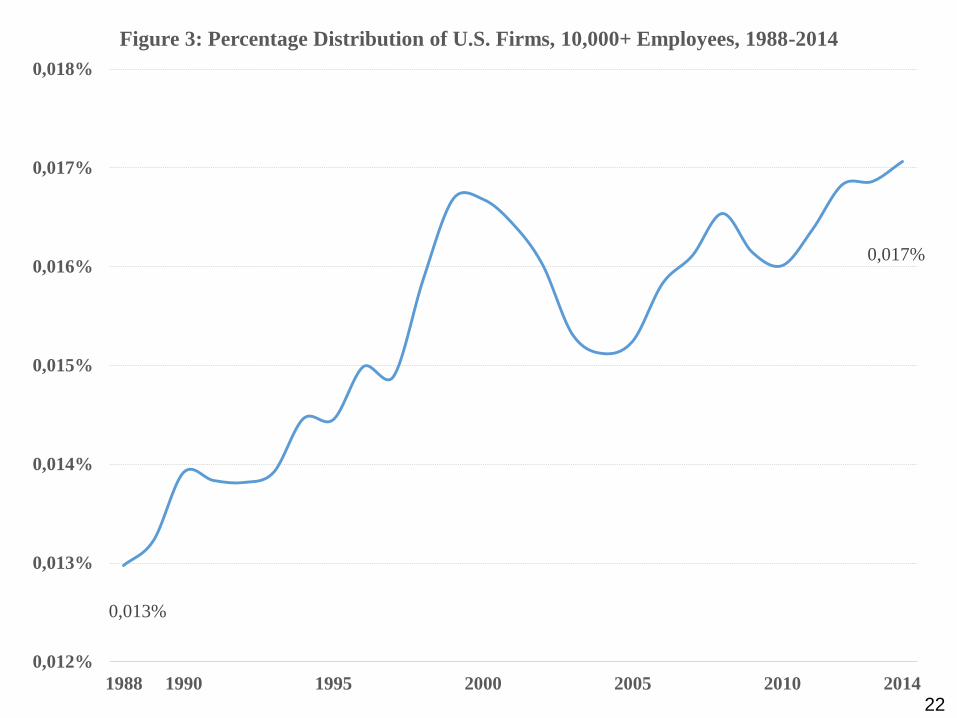

SUSB data: employment and payroll

Bureau of the Census (SUSB) annual data: 1988-2014

Largest bucket: firms with 10,000+ employees

– Increase in the number of largest firms

– Modest increase in their % of all firms

– Sharp increase in their % of private-sector employment,

1993-2001; then a dip; then modest increase 2004-2014

– Average employee size fell 1988-1994; rose 1994-

2004; level 2004-2014

– Varied pattern of their share of private-sector payroll:

overall a net increase

20

643

994

600

650

700

750

800

850

900

950

1000

1988 1990 1995 2000 2005 2010 2014

Figure 2: Numbers of U.S. Firms, 10,000+ Employees, 1988-2014

21

0,013%

0,017%

0,012%

0,013%

0,014%

0,015%

0,016%

0,017%

0,018%

1988 1990 1995 2000 2005 2010 2014

Figure 3: Percentage Distribution of U.S. Firms, 10,000+ Employees, 1988-2014

22

23,81%

28,30%

23%

24%

25%

26%

27%

28%

29%

1988 1990 1995 2000 2005 2010 2014

Figure 4: Percentage Distribution of Employees, 10,000+ Employees, 1988-2014

23

32.528,3

30,423.6 (1994)

34.464,4

30.000

30.500

31.000

31.500

32.000

32.500

33.000

33.500

34.000

34.500

35.000

1988 1990 1995 2000 2005 2010 2014

Figure 5: Average Employee Size of Enterprise, 10,000+ Employees, 1988-2014

24

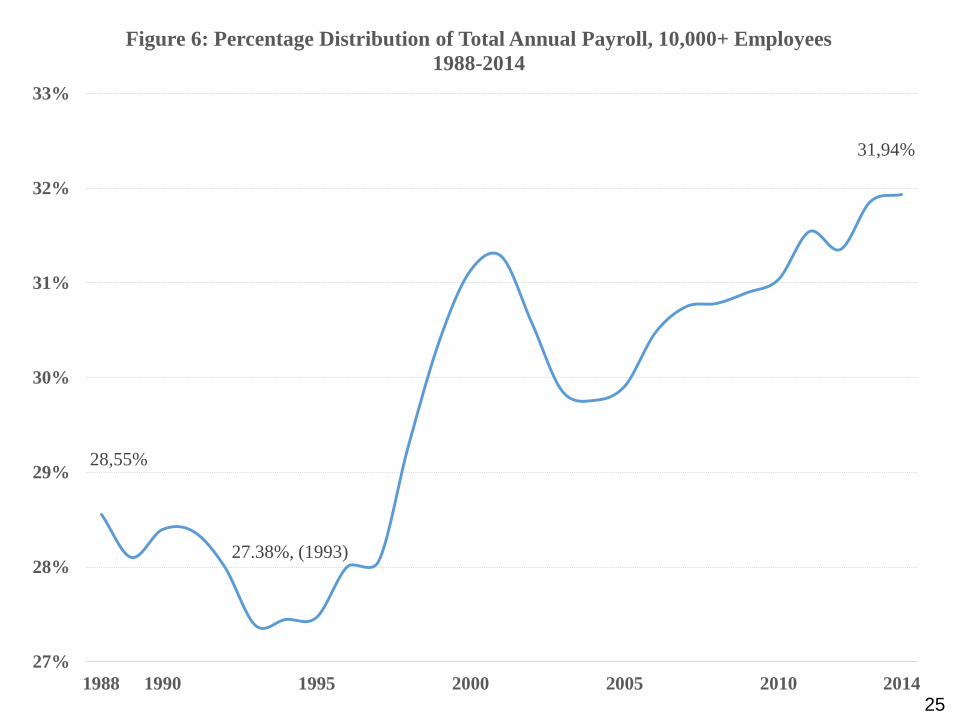

28,55%

27.38%, (1993)

31,94%

27%

28%

29%

30%

31%

32%

33%

1988 1990 1995 2000 2005 2010 2014

Figure 6: Percentage Distribution of Total Annual Payroll, 10,000+ Employees

1988-2014

25

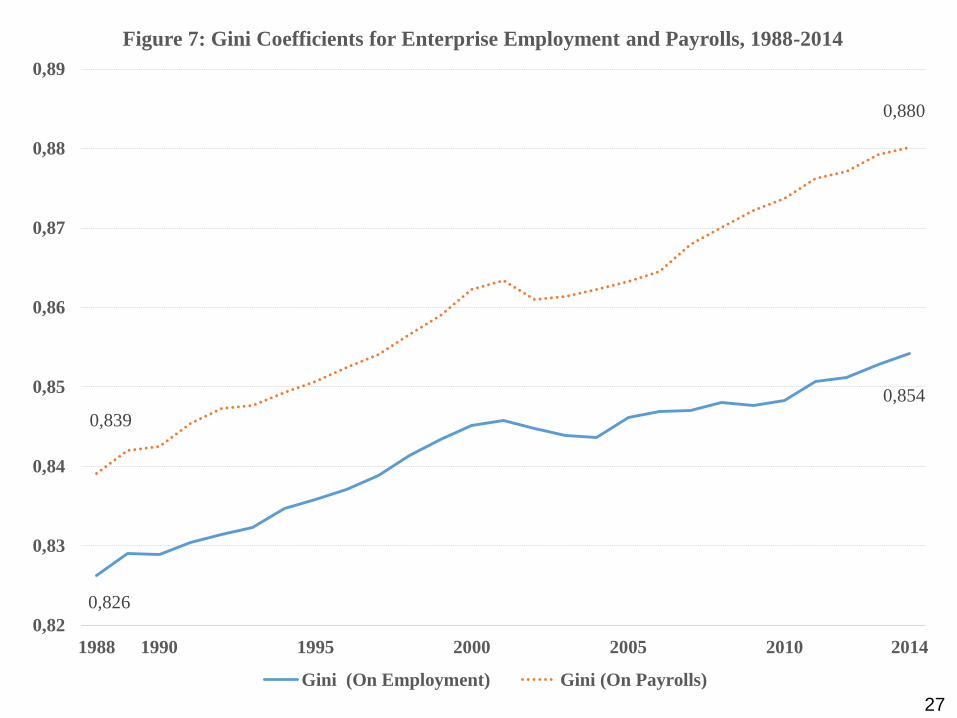

SUSB data: Gini coefficients (1)

Gini coefficients for employment (9-bucket data)

– 1988: 0.826

Equivalent to (for 2 buckets): Largest 8.7% of all firms

employ 91.3% of all employees

– 2014: 0.854

Equivalent to: Largest 7.3% of all firms employ 92.7% of

all employees

Gini coefficients for payroll (9-bucket data)

– 1988: 0.839

– 2014: 0.880

Gini for payroll > Gini for employment: Larger firms tend to pay their employees higher wages

26

0,826

0,854

0,839

0,880

0,82

0,83

0,84

0,85

0,86

0,87

0,88

0,89

1988 1990 1995 2000 2005 2010 2014

Figure 7: Gini Coefficients for Enterprise Employment and Payrolls, 1988-2014

Gini (On Employment) Gini (On Payrolls)

27

SUSB data: Gini coefficients (2)

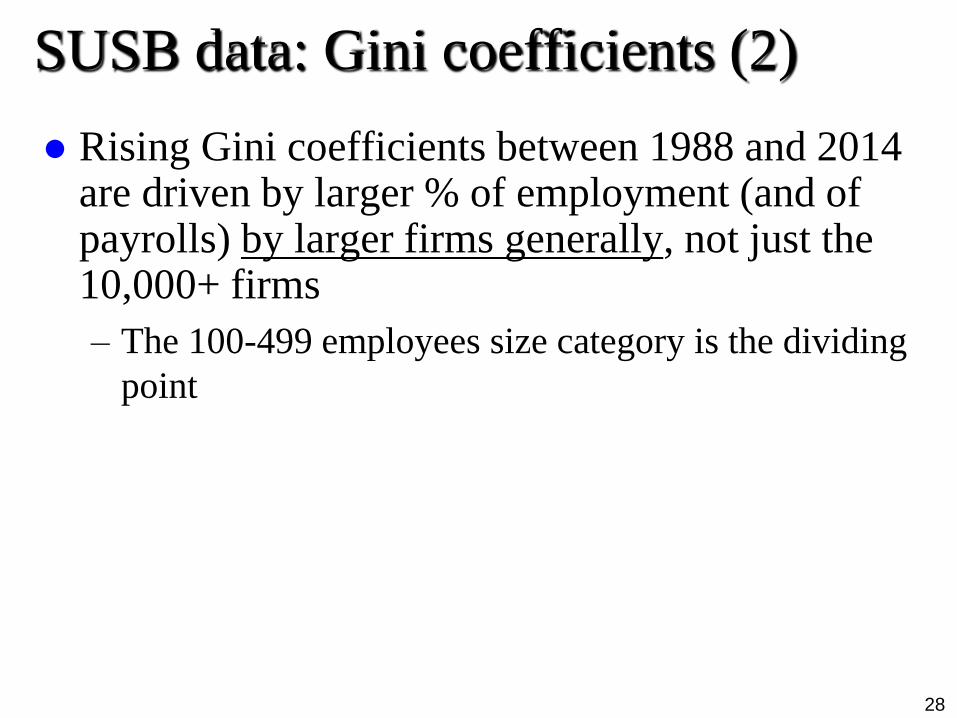

Rising Gini coefficients between 1988 and 2014 are driven by larger % of employment (and of payrolls) by larger firms generally, not just the 10,000+ firms

– The 100-499 employees size category is the dividing

point

28

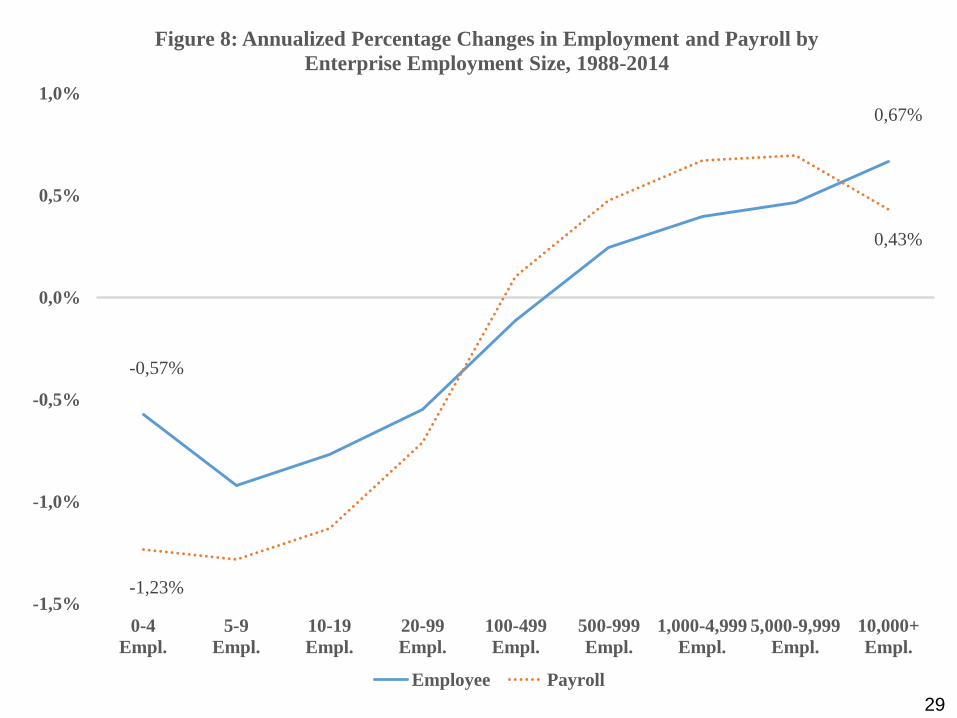

-0,57%

0,67%

-1,23%

0,43%

-1,5%

-1,0%

-0,5%

0,0%

0,5%

1,0%

0-4

Empl.

5-9

Empl.

10-19

Empl.

20-99

Empl.

100-499

Empl.

500-999

Empl.

1,000-4,999

Empl.

5,000-9,999

Empl.

10,000+

Empl.

Figure 8: Annualized Percentage Changes in Employment and Payroll by

Enterprise Employment Size, 1988-2014

Employee Payroll

29

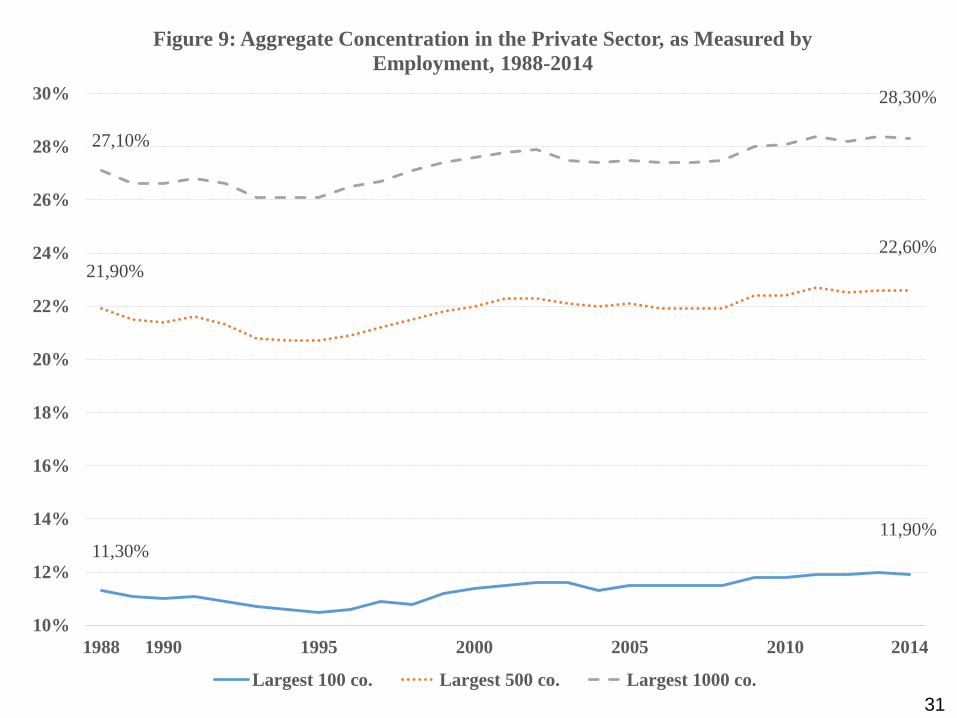

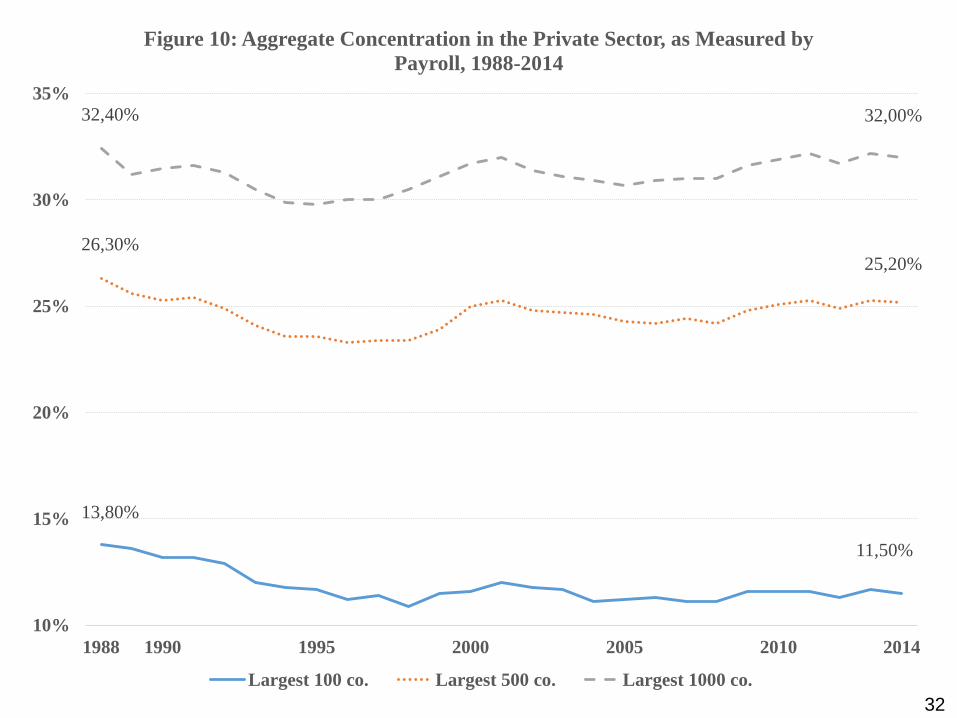

SUSB data: largest firms

Largest 100, 500, 1000 firms: employment %

– Mild decrease from 1988 to mid 1990s; mild increase

since then

– Aggregate concentration slightly higher in 2014 than in

1988

Largest 100, 500, 1000 firms: payroll %

– Aggregate concentration slightly lower in 2014 than in

1988; more pronounced for largest 100

Largest 100 firms as of 2014

– % employment > % payroll: The largest 100 have

lower payroll/employee than for companies generally

30

11,30%

11,90%

21,90%

22,60%

27,10%

28,30%

10%

12%

14%

16%

18%

20%

22%

24%

26%

28%

30%

1988 1990 1995 2000 2005 2010 2014

Figure 9: Aggregate Concentration in the Private Sector, as Measured by

Employment, 1988-2014

Largest 100 co. Largest 500 co. Largest 1000 co.

31

13,80%

11,50%

26,30% 25,20%

32,40% 32,00%

10%

15%

20%

25%

30%

35%

1988 1990 1995 2000 2005 2010 2014

Figure 10: Aggregate Concentration in the Private Sector, as Measured by

Payroll, 1988-2014

Largest 100 co. Largest 500 co. Largest 1000 co.

32

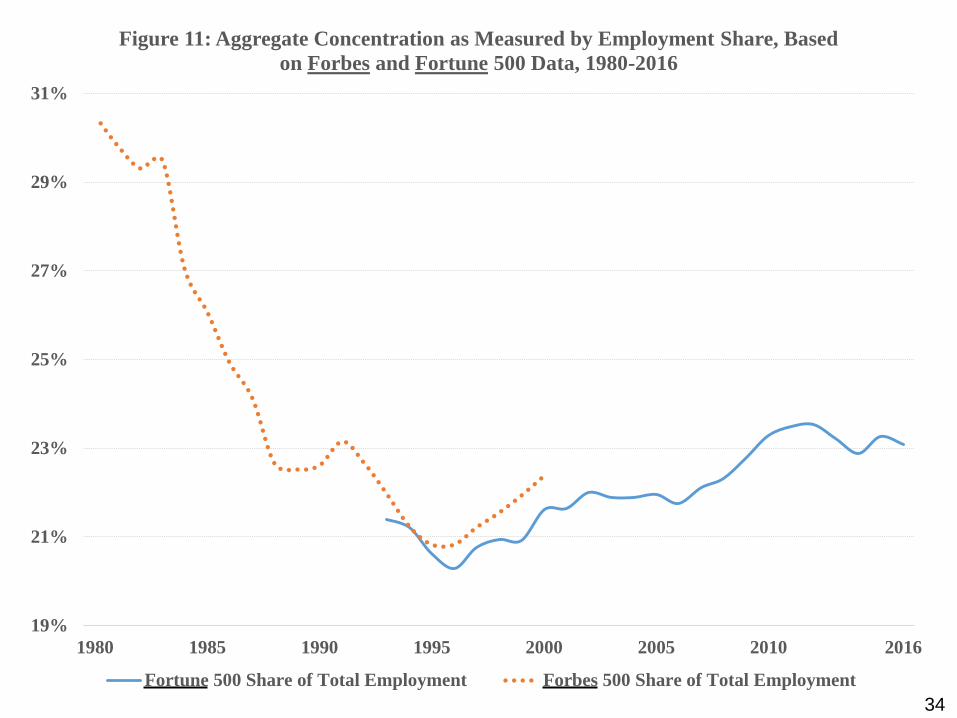

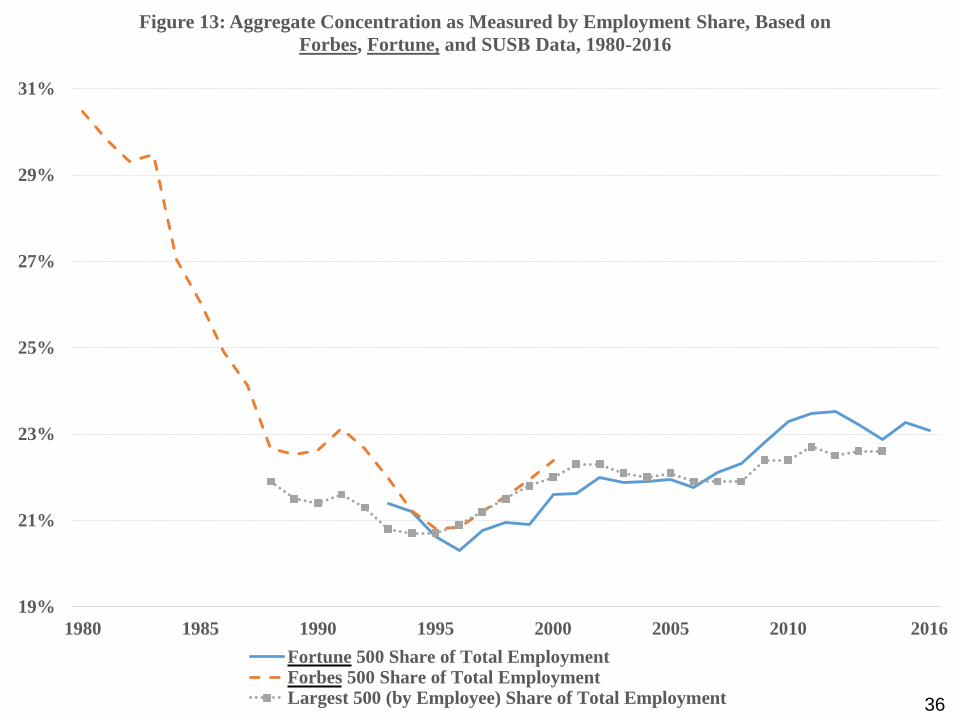

Fortune & Forbes “500” data

Fortune (1993-2016) and Forbes (1980-2000) “500” annual data

– The overlapping years are reasonably consistent

– Employment data are consistent with SUSB data for the

overlapping years

Employment

– Sharp fall in aggregate concentration from 1980 to mid

1990s; modest increases since then

Profits

– Rise and fall in reasonable patterns

– Variable over the years; probably a decrease since mid

1980s 33

34

19%

21%

23%

25%

27%

29%

31%

1980 1985 1990 1995 2000 2005 2010 2016

Figure 11: Aggregate Concentration as Measured by Employment Share, Based

on Forbes and Fortune 500 Data, 1980-2016

Fortune 500 Share of Total Employment Forbes 500 Share of Total Employment

35

0%

20%

40%

60%

80%

100%

120%

1980 1985 1990 1995 2000 2005 2010 2016

Figure 12: Aggregate Concentration as Measured by Profits Share, Based on

Forbes and Fortune 500 Data, 1980-2016

Fortune 500 Share of Total Corporate Profits Forbes 500 Share of Total Corporate Profits

19%

21%

23%

25%

27%

29%

31%

1980 1985 1990 1995 2000 2005 2010 2016

Figure 13: Aggregate Concentration as Measured by Employment Share, Based on

Forbes, Fortune, and SUSB Data, 1980-2016

Fortune 500 Share of Total EmploymentForbes 500 Share of Total EmploymentLargest 500 (by Employee) Share of Total Employment 36

Conclusion

Aggregate concentration has been rising moderately during the first 1½ decades of the 21st century

Aggregate concentration is probably still below the levels of the early 1980s

– Clear for employment

– Probable for profits

Are these trends desirable?

What has been driving these trends?

37