What Do Employees Really Want? Preference-Performance ...

47

What Do Employees Really Want? Preference-Performance Inconsistencies Regarding Work Incentives * Sofia M. Lourenço ISEG/ULisboa and CSG/Advance Research Center [email protected] Cláudia F. Niza * We thank James Werbel, reviewers and participants at AOM 2015 for helpful comments. We gratefully acknowledge financial support from FCT – Fundação para a Ciência e Tecnologia (Portugal), research grant PTDC/EGE-GES/119607/2010 (national funding). All errors remain our own.

Transcript of What Do Employees Really Want? Preference-Performance ...

What Do Employees Really Want?

Preference-Performance Inconsistencies Regarding Work Incentives*

Sofia M. Lourenço

ISEG/ULisboa and CSG/Advance Research Center

Cláudia F. Niza

* We thank James Werbel, reviewers and participants at AOM 2015 for helpful comments. We gratefully

acknowledge financial support from FCT – Fundação para a Ciência e Tecnologia (Portugal), research grant

PTDC/EGE-GES/119607/2010 (national funding). All errors remain our own.

What Do Employees Really Want?

Preference-Performance Inconsistencies Regarding Work Incentives

ABSTRACT

Employee preferences for work incentives have been extensively examined under the assumption

that these preferences provide valuable information for the design of compensation systems.

However, the extent to which providing incentives to match these preferences influences actual

performance has been overlooked. We use a longitudinal field experiment to examine whether

preferences for different incentives influence behavior once the incentive is (or is not) provided.

Specifically, we examine ex-post objective performance data according to the ex-ante incentive

preferences, collected via a questionnaire in the pre-experimental period. The between-subjects

experimental manipulations include one of three incentive motivators: (a) money, (b) feedback

and (c) recognition. Our results show several inconsistencies between stated preferences and

revealed performance behavior. We find that (1) employees report a significantly higher

preference for money and feedback compared to recognition but only money and recognition

improve performance with an equivalent effect size; (2) performance is not higher when

employees are matched with their preferred incentive, except for feedback; and (3) there is no

evidence of a learning effect as the consistency between ex-ante preferences and ex-post

performance is not improved with experience.

Keywords: Incentives; Preferences; Performance; Motivation; Field Experiment

1

What Do Employees Really Want? Preference-Performance Inconsistencies Regarding

Work Incentives

Seminal work by Kovach (1980, 1987) and Heath (1999) suggests that managers

misapprehend what motivates employees. These studies expose that managers exhibit an extrinsic

[monetary] incentives bias, defined by a tendency to overestimate the importance employees

place in monetary rewards and underestimate the valuation that employees give to nonmonetary

incentives such as opportunities for increasing competency or social esteem. These results

spurred the idea that managers tend ‘to push the wrong levers and to develop incentive programs

that don't reflect employee needs’ (Morse 2003) by misunderstanding what motivates employees

- or what employees report to motivate them.

However, are employees better judges of what drives their performance in the workplace?

Over the years, employee surveys have depicted employees’ incentive preferences (Wiley, 1997;

Chiang & Birtch, 2005, 2006, 2012; Bonsdorff, 2011) under the assumption that this would be a

crucial piece of information for organizations.

This standpoint is aligned with the most prominent views in different social sciences

assuming individuals have a stable and well-defined preference structure and that their behavior

is the product of those preferences (Jensen & Meckling, 1979; Ajzen 1991; Lazear, 2000; Shapiro

2005). This premise dominates most conceptual approaches regarding the human behavior in the

workplace. However, there is a lack of evidence regarding the extent to which ex-ante incentive

preferences actually influence ex-post performance under different incentive schemes.

Nevertheless, in several other contexts, research from behavioral decision theory

(Lichtenstein & Slovic, 1995) has demonstrated that preferences can be unstable, volatile and

prone to inconsistencies such as elicitation procedures, temporal framing or the presence of

tangible consequences (Simonson, 2008; Ariely et al 2006; Ariely & Norton, 2007).

2

Overall, the available research in management has been silent on how baseline

preferences for different incentives influence performance when incentive programs are

implemented. Can performance be predicted by incentive preferences? Does the delivery of the

preferred incentive lead to a better performance? Or are incentive preferences good predictors of

performance only after individuals had some experience with incentive schemes? To the best of

our knowledge, these critical questions remain unanswered several decades after Kovach (1980,

1987) and Heath (2003).

Using a longitudinal field experiment, we compare stated preferences for incentives,

collected via a questionnaire in the pre-experimental period, with revealed behavior (objective

performance data) in the experimental period once a new incentive is introduced. Performance is

taken as the proxy for revealed (not stated or self-reported) preferences about incentives (List &

Gallet 2001; List et al 2004; Ajzen et al 2004; Braga & Stramer 2005). Although revealed

preferences are typically analyzed as the behavioral choices people make (Murphy et al 2005;

Miller et al 2011), in an employment setting we take performance levels under some incentive

scheme as the observable behavioral preference for that incentive ceteris paribus. To date there is

no study that examines stated versus revealed preferences (in the form of behavioral

performance) within subjects. Survey data about preferences and experimental evidence about

performance under incentive schemes are typically presented in different studies using distinct

employee samples.

This study analyzes whether ex-ante stated preferences influence the effect of different

incentives on ex-post behavior (performance), both when individuals receive the incentive they

prefer and when they do not. The experimental manipulation entails three incentive motivators

commonly used by organizations (Bandura, 1986; Kluger & DeNisi, 1996; Stajovic & Luthans

3

1997, 2001, 2003; Rynes et al 2005). These conditions (between-subjects) refer to (a) money, (b)

feedback or (c) recognition. Additionally, we investigate the potential moderating role of

experience as a condition that may increase the consistency between ex-ante stated preferences

and ex-post performance using the proxies of tenure and past experience with incentives.

We find several inconsistencies between stated incentive preferences and revealed

performance behavior. We find that individuals’ preferred incentives may not be the ones that

actually improve their performance. We also show that performance is not higher when

employees are matched with their most preferred incentive regardless of how the preferred

incentive is elicited. Moreover, neither tenure nor past experience with the incentive improves the

consistency between ex-ante preferences and ex-post performance. We confront these results with

the various competing explanations for why inconsistencies may occur between stated versus

revealed preferences and propose that the mechanism underlying these inconsistencies is likely to

be some form of lay [workplace] rationalism (Hsee et al 2003) characterized by overweighting

incentives that appear more rational or objective.

This paper makes critical contributions to a variety of management disciplines (Gupta &

Shaw, 2014; Bonner & Sprinkle, 2002; Franceschelli et al 2010; Stajovick & Luthans 2001).

First, we add to the literature by analyzing preference inconsistencies in a workplace context, a

setting in which preference-behavior gaps are under researched (e.g., Kanheman & Thaler 1991).

To the best of our knowledge, no prior study as analyzed how preferences for work incentives

actually translate into performance behavior when that incentive, or a different incentive, is

provided. Second, we show limitations to the predictive validity of reported incentive preferences

and caution against taking stated preferences as the basis for the design of compensation and

incentive schemes. If management and human resources policies aim to improve work

performance they should not take the preferences of the employees at face value. Third, our

4

results show no evidence of learning effects regarding preferences for work incentives. This

insight suggests that some form of intervention may be required to make employees more aware

of their preference inconsistencies. Fourth, this study provides experimental field evidence

examining objective performance data and incentive preferences. A better understanding of those

preferences on the effectiveness of work incentives is a critical element for effective human

resources management (Gerhart & Fang, 2014; Gupta & Shaw, 2014), strategic alignment

(Chiang et al, 2012; Baumman & Stieglitz, 2014) and organizational performance (Brown et al

2003). Nevertheless, experimental evidence has been severely lacking in this research agenda

(Franceschelli et al 2010), particularly in natural organizational settings.

This paper proceeds as follows. We start by reviewing the key literature from

management, economics and psychology about compensation and work motivation that predict to

a large extent a consistency between ex-ante stated preferences and ex-post performance. We

then turn to the literature from behavioral decision theory about preference construction and

stability to expose the limitations of taking reported preferences at face value as predictive of

behavior. The methods and result sections are presented next. We finish by discussing our results

and implications for future research and practice.

LITERATURE REVIEW

The prevalent hypothesis for preference-behavior consistency

Under rational choice theories (Scott, 2000), individuals are conceptualized as being fully

aware of their endogenous preferences. These individuals have both the motivation and the

5

ability to choose between competing alternative scenarios the option that maximizes their utility

(Coleman & Fararo, 1992). Individuals are seen as motivated by the wants or goals that express

their preferences. They act within specific, given constraints and on the basis of the information

that they have about the conditions under which they are acting. Rational choice theories hold

that individuals anticipate the outcomes of alternative courses of action and choose the alternative

that is likely to provide them the greatest utility. Rational choice is the basis of agency theory

(Jensen & Meckling, 1979; Einsenhardt, 1989; Shapiro 2005), which is the main theoretical

framework guiding research in economics about compensation and incentive effects (Lazear,

2000). Agency theory assumes that both parties to the employment relationship are utility

maximizers. Incentive preferences matter for organizations under the assumption that agents are

rational: employees know what best motivates them at work and act upon this information.

Although, most research from organizational behavior and psychology does not share the

strict assumptions of rational choice theories it makes ultimately similar predictions. Theory of

reasoned action (Fishbein 1979), theory of planned behavior (Ajzen 1991) and in general all

expectancy value theories (Vroom, 1954) consider behavior as a deliberative process and choices

result from a calculation of expected benefits. Hence, these theories are ‘rational’ theories in the

sense that behavior is conscientious, deliberative and under peoples’ control. People can self-

report accurately what they prefer, that is, what they like (attitudes) and want (intentions), and

these are considered good proximal determinants of behavior. Content theories of motivation,

represented by Maslow (1970), Alderfer (1972), Herzberg (1966) and McClelland (1976),

generally assert that people have different needs that should be addressed at work. Incentives and

other forms of organizational design should be used to motivate employees and promote work

satisfaction. Thus, these theories implicitly consider that fulfilled needs (i.e. preferences) should

improve performance.

6

In contrast to these broad theories, contingency theory in management (Luthans & Stewart

1977; Kristof‐Brown et al 2005) states that the structure and process of an organization as well as

its members must fit the context (characteristics of the organization's culture, environment,

technology, size, or task). The key concept in a contingent proposition is fit (Drazin & Van de

Ven 1985) whether this is person-job fit, person-environment fit or person-task fit. The

implication that can be drawn from contingency theory to the analysis of the consistency between

ex-ante preferences and ex-post performance is that employees with different characteristics are

expected to respond differently to different incentives. Thus, incentives should match people’s

preferences (Delery & Doty 1996), that is, there should be a fit between the incentives individuals

want and the incentives individuals receive to produce positive effects in performance.

Thus, this overview of the literature suggests consistency between stated references and

performance behavior when preferences are met – and this hypothesis is shared by conceptual

approaches that differ in many important aspects. Although distinct in their conceptualization of

the determinants of behavior in the workplace, these theories do not make different predictions

regarding the expected predictive validity of reported preferences to explain behavior.

However, empirical evidence regarding this consistency assumption is lacking. The

empirical literature shows abundant evidence regarding preference for work rewards or incentives

from panel data collected with cross-country surveys (e.g., General Social Survey GSS,

International Social Survey Program ISSP, European Social Survey ESS) (Kovach 1987; Wiley

1997; Morse, 2003; Clark 2005; Dewhurst et al 2009). Overall, this research tends to examine

incentive preference for employees with no significant variable pay component and generally

shows that the strongest preferences are for nonmonetary incentives as doing an “important

work” or “being recognized” in their job. Research more specifically targeting jobs with high

variable pay components (as salesforce) shows that incentive preferences reveal a more balanced

7

mix between monetary and nonmonetary incentives but with monetary incentives generally

taking the lead (Ingram & Bellenger 1983; Bellenger et al 1984; Chonko et al 1992; Lopez et al

2006; Analoui 2000). Nevertheless, to date, this evidence does not show whether these

preferences translate (or not) into work performance. We can only infer that the absence of any

discussion about possible inconsistencies or discrepancies in self-reported preferences in these

studies, signals the assumption that ex-ante preferences are predictive of ex-post performance.

Overall and according to the main theoretical approaches and empirical evidence in the

management literature, we present the following hypotheses:

H1a. Stated incentives preferences will be consistent with revealed preferences i.e., preferred

incentives will be associated with higher performance.

H2a. When incentives preferences are met performance will improve.

Evidence for preference inconsistencies

Although most theoretical frameworks in economics, management and psychology predict

– in more or less explicit terms – a significant consistency between stated preferences and

behavior, differences between what people say and do have been identified. In reasoned action

theories, attitude-intention-behavior gaps have been recognized (Sheeran et al 1999; Sheeran

2002; Gollwitzer et al 2009). In economics, the difference between stated (reported) and revealed

(behavior) preferences is often referred to as hypothetical bias (Ajzen et al 2004; List & Gallet

2001; List et al 2004). Nonetheless, these gaps are not interpreted as ‘inconsistencies’ but as sign

that there are boundary conditions in the theories, that is, the models work better for behaviors

that are e.g., more immediate, more habitual or less controversial.

8

Yet one of the main conclusions from behavioral decision research is that people’s

preferences are often constructed in the process of elicitation and may depend on several external

influences rather than from an internal preference structure (Lichtenstein & Slovic, 1995). Unlike

most well-established theoretical phenomena in management research, the literature on

behavioral decision theory tends to acknowledge that preferences can be volatile and prone to

several inconsistencies (Simonson, 2008) – instead of stable and given for each individual (Ariely

et al 2006; Ariely & Norton, 2007).

Although the evidence for preference inconsistencies is not grounded on strong

conceptualization efforts by contrast to the more theoretically robust hypothesis for preference-

behavior consistency, many empirical irregularities have been reported. Overall, this evidence,

collected in settings different from the workplace, suggests that preferences exhibit inconsistent

patterns. For our work, these findings suggest that performance under a particular incentive may

not be a function of initially stated preferences.

Preference inconsistencies can be originated from several different sources (Harrison &

Rutström 2008) and can be organized in three main categories of explanations: forecasting bias,

different decision modes and lay rationalism. The first category includes the majority of

explanations proposed for preference inconsistencies and it is related to forecasting

mispredictions. In this first category there are three main arguments. First, ex-ante evaluations are

typically expressed in relation to hypothetical future events, which may be mentally constructed

at a too high abstract level to correspond to actual preferences (Robson & Samuelson, 2011).

Construal level theory (Trope & Liberman, 2003) proposes that in construing a distant scenario,

people would be more likely to use stereotypes rather than internal information, generalized

scripts rather than more concrete, non-schematic details and vague rather than situation-specific

goals. Because when thinking about the future irrelevant or inconsistent details are omitted from

9

the abstract representation (Liberman et al 2002), incentive preferences expressed about possible

future incentive programs may be expected to be simpler, less ambiguous, and more prototypical

than concrete representations. Second, it could also be the case that people are not fully aware of

what motivates them and reported preferences may have a negative or no association with

performance (Nisbett & Wilson 1977). Some studies have shown that expressing a preference

may rebound because the act of choosing might actually induce a preference change (Brehm,

1956; Egan et al 2007; Lieberman et al 2001). The underlying motive for this is that introspecting

about one’s preferences may lead people to divert attention to criteria they initially did not

consider (Wilson & Schooler 1991; Wilson et al 1993). Exposing employees to a situation in

which they have to introspect about their preferences for work incentives – as in a questionnaire–

may facilitate the consideration of different utility gains from distinct incentives which in turn

may prompt an internal preference shift with deferred effects. Thirdly, what is wanted at the onset

may not be what is later liked (Dai et al 2010). Studies on affective forecasting (Wilson and

Gilbert 2003) and projection bias (Loewenstein et al 2003) show that people are often

disappointed by the very things they thought they wanted. People routinely mispredict how much

pleasure or displeasure future events will bring and, as a result, sometimes work to bring about

events that do not maximize their happiness (Gilbert et al. 1999). People have been shown to be

wrong about how their positive or negative reactions to future events, particularly if what unfolds

is different from what they had imagined (Chen & Risen 2010). The implication of this research

is that people may believe they would not perform better under a certain incentive , but in fact the

motivational force of that incentive may be stronger than initially predicted.

A second group of explanations is related to the decision mode in which preferences are

reported versus how preferences are experienced. On one hand, inconsistencies can come from

the introduction of real stakes. Incentive schemes in natural organizational settings reflect ‘real

10

stakes’ and have been shown to be truth-revealing, i.e., exposing real behavioral preferences

(Berg et al 2010). These ‘real stakes’ are typically not present when employees self-report their

incentive preferences. Without real incentives, subjects’ preferences may be more liable to

elicitation methods but under tangible consequences, individuals’ behavior is more consistent

with their ‘true’ stable underlying preferences (Berg et al 2010). Therefore, introducing incentive

programs with tangible benefits or costs after eliciting employees’ self-reported preferences may

induce a preference shift because individuals face real consequences. On the other hand, Hsee

and Zhang (2004) propose that choices and predictions are often made in the joint evaluation (JE)

mode where individuals compare multiple options or alternatives. On the other hand, the actual

experience typically takes place in the single evaluation or separate evaluation (SE) mode, in

which experiencers face only the option or scenario they or others have chosen for them. When

presented with different options people can easily compare alternative utilities but in isolation

people do not have a precise idea of exactly how good or how bad the option they are

experiencing is. For our case, this implies that when employees self-report preferences between

different incentives they are in JE but when they are allocated to an incentive condition they are

in SE which may create inconsistencies between stated and revealed preferences (behavior). Hsee

and Zhang (2004) propose that this misprediction is more likely to occur when the alternatives

are merely quantitatively different but less likely when options are qualitatively different which

may suggest greater inconsistencies between reported preferences for monetary incentives and

performance under nonmonetary incentives (and vice-versa).

A final possible explanation for preference-performance inconsistencies may be

originated from a lay rationalism (Hsee et al 2003; Hsee et al 2014) regarding workplace

performance. Lay rationalism refers to a tendency to overweight attributes that appear more

rational and objective and downplay attributes that appear more subjective (Hsee et al 2004). This

11

lay rationalism can be manifested in the form of lay economism or lay ‘scientism (Hsee et al

2003). The former is related to the tendency to base decisions on financial aspects of the options

and neglect experiential aspects. Lay economism represents a tendency in people to focus on

economic calculus, to compare options in terms of economic gains and losses, and to downplay

other experience inducing factors, such as temporal trends and social comparisons. The latter

reflects the tendency in decision-makers to trust hard facts and discount soft preferences. Lay

rationalism thus seem to be based on the desire to base one’s decision on things that are ‘real’,

that is, substantive, material, and more concrete. This lay rationalism is likely to be particularly

marked in the workplace where making a decision on the basis of a hard attribute seems more

objective and rational, and hence more justifiable to colleagues and supervisors. There is also

greater certainty in the relative desirability of the choice options on the hard attribute than on the

soft attribute; therefore it is safer to base professional decisions on hard attributes. However, this

tendency to consider substantive features as more important than psychological experiences, to

prefer options with ‘hard’ attributes rather than subjective ones may hinder experiential

(performance) effects later on when employees are faced with the real consequences of what they

reported to prefer.

Based on the theoretical arguments presented for preference inconsistencies, and

competing with the hypotheses presented in the previous section, we propose the following

hypotheses according to behavioral decision theory:

H1b. Stated incentives preferences will not be consistent with revealed preferences i.e., preferred

incentives will not be associated with higher performance.

H2b. When incentives preferences are met performance will not improve

12

Learning facilitators or debiasing effects: Tenure and past experience

Most of the explanations provided above (forecasting bias, high abstract level of cognitive

representations, lack of motivational awareness, different decision modes between reported

versus experienced preferences) seem to be better applied to situations where people did not have

a sufficient amount of time or experience to fully developed well-established preferences.

Inconsistencies between ex-ante incentives preferences and ex-post performance under different

incentive schemes may be less likely to occur when more learning opportunities have existed to

help estimate the relationship between stated incentive preferences and performance behavior.

We examine tenure and past experience with the different incentives as proxies for learning

opportunities and for the time needed to form well-informed preferences.

Tenure within the organization or experience performing a specific job is expected to

affect an employee’s perception of instrumentality and effectiveness of a certain incentive

(Nyberg et al 2014). Employees will likely believe that prior experience will be representative of

a future experience. Thus, it is reasonable to conclude that the longer an employee’s tenure, better

well-formed her or his attitudes and beliefs about work, motivation and compensation practices

will be. Hence, the consistency between preferences and action should increase with tenure. In

contrast, low-tenured employees have less historical employment outcome evidence to draw upon

when developing their own views about preferences for incentives in the workplace. Thus, the

consistency between their preferences and their actions is likely to be weaker than for high-

tenured employees.

In the case of an existing previous experience with an incentive, incentive preferences

should reflect experienced utility (Kanheman et al 1997). Prior experience with an incentive

13

creates expectations about the degree to which future performance will be linked to it

(Schaubroeck et al., 2008). Key to this premise is that having experience working under an

incentive program has allowed individuals to become aware of their own perceptions, judgments

and behavior in such a situation. Employees without past experience with an incentive are likely

to base their preferences on anticipated utility (Caplin & Leahy, 2001). Thus, in this case,

employees report a preference for the incentive they expect to bring them the highest benefit.

Research performed in non-employment settings shows that anticipated and experienced utility

are not always concordant (Rajagopal & Montgomery, 2011; Ariely & Norton, 2007; Ariely et al

2006). This discrepancy is crucial for compensation practices (Kanheman & Thaler, 1991, 2006).

The reasoning described above for tenure and past experience mostly holds yet again

assuming some consistency and rationality in reported preferences. For instance, although it may

be expected that high tenure employees have superior knowledge and experience about what

drives performance, some studies (e.g., Hinds 1999) show that a greater expertise may actually

interfere with the ability to predict performance determinants. Hinds (199) showed that not only

were higher tenure employees unable to take advantage of their knowledge and experience in

predicting performance drivers, but they were also unable to correct their estimates when they

were prompted with information about their misprediction. There are several other pieces of work

showing that exposing people to learning facilitators and ‘debiasing’ strategies has not always

proven effective in reducing preferences-behavior inconsistencies (Hirt & Markamn 1995;

Weistein & Klein 1995; Elwin 2013). The most widely recommended debiasing strategy is

encouraging people to ‘‘consider the opposite,’’ or to counter-argue their initial response, by

asking themselves, ‘‘what are some reasons that my initial judgment might be wrong?’’ (Schwarz

et al 2007). Evidence shows that the more people try to consider the opposite, the more they often

convince themselves that their initial judgment was right on target (Schwarz et al 2007). Another

14

debiasing strategy, also less effective than expected, is confronting erroneous beliefs with

contradictory evidence. Yet attempts to do so often increase later acceptance of the erroneous

beliefs (Arkes 1991; Sanna et al 2002).

Given this evidence suggesting the possibility for preferences-behavior inconsistencies

resist to, or even be exacerbated with, experiential learning opportunities, we also present

competing hypotheses for the moderating impact of tenure and past experience, namely:

H3a. According to most standard economic and management theories, the consistency

between incentive preferences and revealed performance will improve under learning

facilitators.

H3b. According to behavioral decision theories, the consistency between incentive

preferences and revealed performance will not improve under learning facilitators.

METHODS

Sample and research site

This paper uses data from a previous field experiment (Lourenco 2015). Lourenco (2015)

is study with part-time sales representatives (reps) who conduct product demonstrations in

assigned stores of a major retail chain in the U.S. That study is a field experiment with eight

experimental groups, each one with a different combination of incentives (from the control group

to the group that received monetary incentives, feedback and recognition). This design was used

by Lourenco (2015) to analyze whether different incentives are complements or substitutes. In

15

this paper, and to avoid the potential effects of the interactions among different incentives, we use

only data from the participants that were either in the control group or in the groups that received

only one incentive. Additionally, we use new data questionnaires responded by the participants

before the start and after the end of the experiment. These questionnaires collect information

about participants, including their incentive preferences. Conditioning on being on the selected

experimental groups and having responded to the pre-experimental questionnaire, we obtain a

sample of 119 participants for this study. These participants are mostly male (60%), with a mean

age of 44 years (SD=13.4) and with a mean tenure in the company of 12 months (SD=15).

Income was not measured in absolute terms but in relative ones, as the percentage of income

provided by this work. The average participants’ personal income coming from the work in this

company was 42% (30% of their household income). At baseline, the organization had no

structured incentive program and no performance goals were established. Employees were

compensated via a fixed hourly rate (17 dollars per hour). The manipulations introducing the

different incentives – monetary incentives (hereafter money), feedback and recognition – are

fully described in Lourenco (2015). We describe here the questions used in the questionnaires to

measure incentives preferences.

Pre experimental questionnaire

Before the incentive programs were implemented, employees filled a pre-experimental

questionnaire. The questionnaire included several socio-demographic questions (age, gender,

tenure, income), as well as questions about the rank preference for different incentives,

importance attributed to different incentives and past experience with these incentives.

Preference rankings for the different incentives were elicited using bundles of incentives

in a masked way. Participants were presented with five different bundles of job characteristics

16

(three per bundle), which included the three incentives under analysis and some decoys. These

bundles were: 1. Fair pay, no lay off, monetary incentives; 2. Manager-feedback, relative

feedback and task-feedback; 3. Relative feedback, private recognition, public recognition; 4.

Feedback, monetary incentives, recognition; 5. Autonomy, information, monetary incentives.

Participants were asked to rank each job characteristic within each bundle from 1=most preferred

to 3=least preferred.

Participants were also asked to rate the importance of different job characteristics.

Besides the three incentives under analysis (money, feedback and recognition), the questions also

included some decoys (autonomy and information). The questions posed were: 1. “How

important or unimportant is each characteristic for you to do a good job? (1=not important at all

to 7=extremely important); 2. “How important or unimportant is each characteristic to motivate

you to excel in your job?” (1=not important at all to 7=extremely important); and 3. “Please

indicate the degree to which you would like to have each characteristic present in your job

compared to what you have now” (1=Much less to 7=Much more). The answers to these

questions were aggregated in a single importance index for each incentive (Money =.77;

Feedback =.68; Recognition =.79).

RESULTS

We start our data analysis by examining the consistency between stated preferences (ex-

ante evaluation of different incentives) with revealed preferences (ex-post performance under

each incentive scheme). Reps attribute a higher importance to money (M=5.73 SD=.88) and

17

feedback (M=5.60 SD=.73) (marginally higher for money: paired t-test meanmoney-

meanfeedback=1.67 p<.10) than to recognition (M=5.50 SD=.84). Recognition is rated as

significantly less important than money (paired t-test meanmoney-meanrecognition=2.82 p<.01) and

feedback (paired t-test meanfeedback-meanrecognition=2.23 p<.05). These importance ratings are

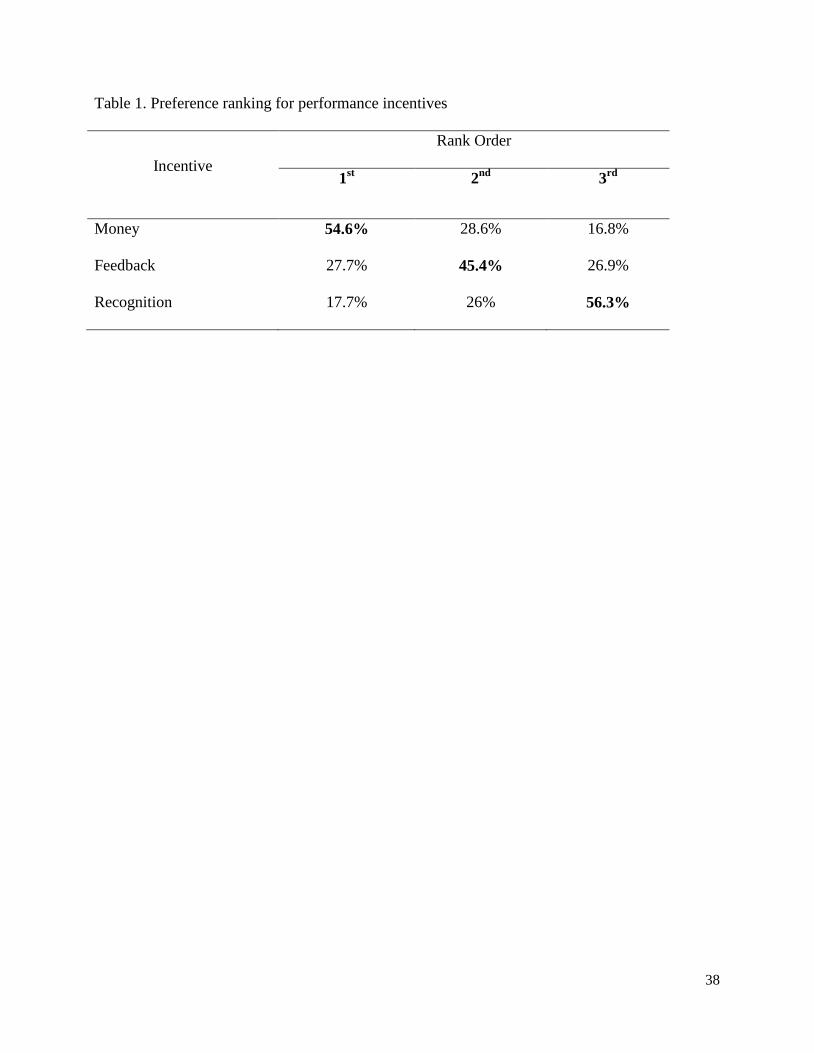

consistent with incentive preference rankings (Table 1): most reps state monetary incentives as

their first preference (54.2%), feedback appears in second place (by 45.4% of participants) and

recognition is the least preferred (56.3%). Overall, stated preferences are consistent between

different elicitation methods.

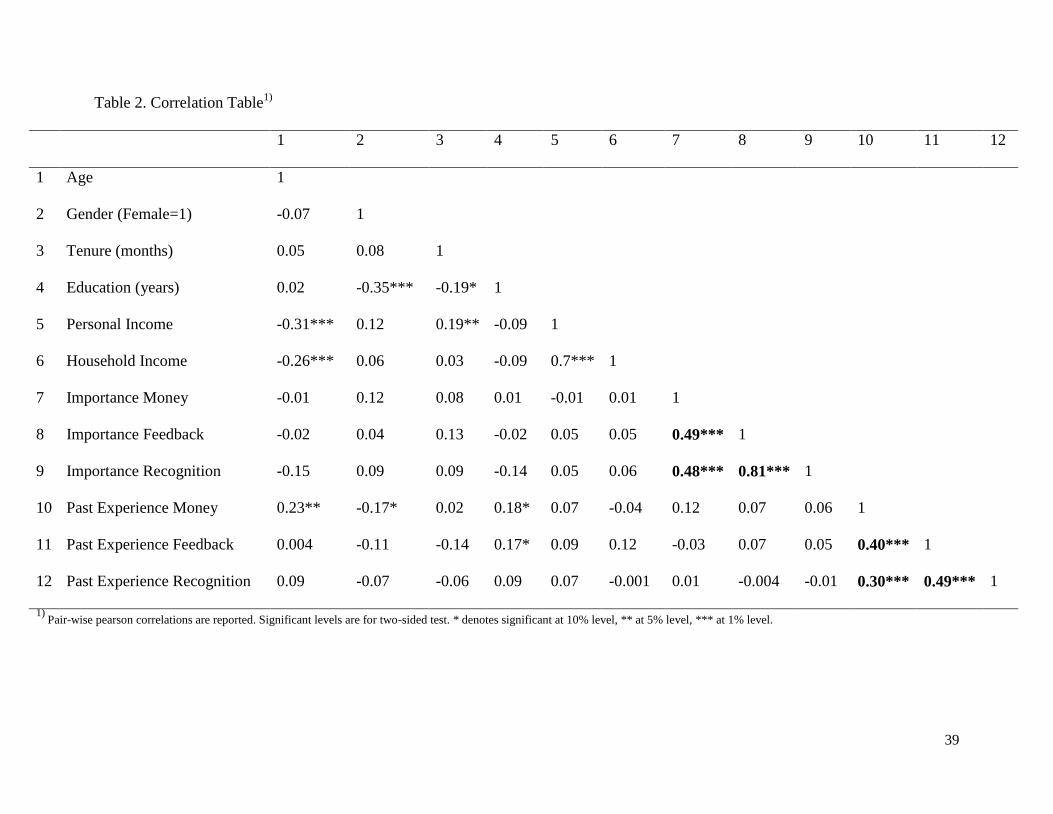

Correlations presented in Table 2 show that importance ratings for different incentives are

unrelated to socio-demographics (age, gender, tenure, and education) but particularly relevant,

and in contrast to the literature, our results show independence between income and the

importance attributed to different incentives. The degree to which participants are dependent of

the income provided by their work at the company is unrelated to the importance they attribute to

monetary and non-monetary incentives. The table also shows positive and statistically significant

correlations among importance ratings of the different incentive. Noticeably, there is a higher

correlation between the importance attributed to the two nonmonetary incentives (feedback and

recognition r=0.81 p<0.001) than between monetary incentives and feedback (r=0.49 p<0.001) or

monetary incentives and recognition (r=0.48 p<0.001). These correlations suggest some

aggregated evaluation of nonmonetary incentives by contrast to money. Finally, the table also

shows positive and statistically significant correlations among past experiences with the different

Insert Table 1 about here

18

incentives. Also in this case, there is a higher correlation between the experience with feedback

and recognition, than with money and feedback, or money and recognition.

Although stated preferences for incentives reveal consistency between different elicitation

methods, we now compare these preferences with actual performance (sales relative to goals).We

use a simplified model from Lourenco (2015) because we dropped the groups that received

multiple treatments. The model is the following:

𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑆𝑎𝑙𝑒𝑠/𝐺𝑜𝑎𝑙𝑠𝑖𝑡

= 𝛼0 + 𝛿1 𝑀𝑂𝑁𝐸𝑌𝑖 + 𝛿2 𝐹𝐸𝐸𝐷𝑖 + 𝛿3 𝑅𝐸𝐶𝑖 + 𝛾1𝑀𝑂𝑁𝐸𝑌𝑖 ∗ 𝐸𝑋𝑃

+ 𝛾2𝐹𝐸𝐸𝐷𝑖 ∗ 𝐸𝑋𝑃 + 𝛾3𝑅𝐸𝐶𝑖 ∗ 𝐸𝑋𝑃 + ∑ 𝜔𝑡 𝑊𝐸𝐸𝐾𝑆𝑖𝑡

𝑡=12

𝑡=1

+ 휀𝑖𝑡

(Equation 1)

where i represents reps and t represents weeks. Average Sales/Goalsit is the performance of rep i

in week t; MONEY, FEED, and REC are dummy variables that are equal to 1 if the rep was

randomly assigned to the monetary incentive, feedback, or recognition conditions, respectively,

and are equal to 0 otherwise. EXP is a dummy variable that is equal to 1 in the weeks of the

experiment, and is equal to 0 otherwise; WEEKS is a set of 12 dummy variables for each week

other than the first of the 13 weeks of data; and 휀𝑖𝑡 is the error term for rep i in week t. EXP, the

dummy variable for the experimental period is omitted from the regression because it is perfectly

collinear with the WEEKS dummy variables for the weeks in the experimental period. Because

Insert Table 2 about here

19

our setting is the retailing industry, it is important to control for seasonality effects which are

captured in the WEEKS dummy variables. The results are qualitatively unchanged if the EXP

dummy variable is included and the WEEKS dummy variables are dropped.

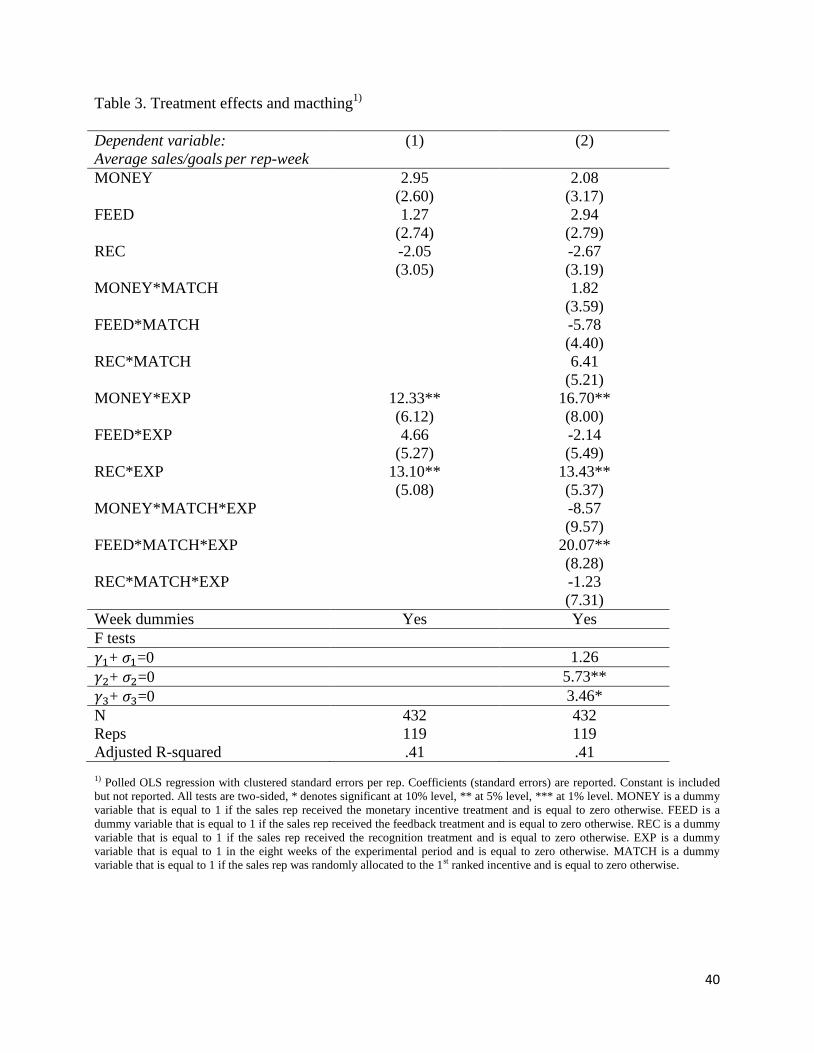

Column 1 of table 3 reports the results of this model estimated with a pooled OLS

regression and clustered standard errors by rep. Notice that the results from this column are

qualitatively unchanged from the ones reported in Lourenco (2015) but the point estimates are

slightly different because we restrict our sample to reps who answered the pre-experimental

questionnaire and for whom we were able to collect incentive preferences. We find that the group

receiving a monetary incentive increases performance by about 12 percentage points (pp)

(𝛾1=12.33, p-value<.05) while the group receiving recognition improves performance by about

13 pp (𝛾3=13.10 p-value<.01). These two effects are not statistically different. Participants in the

feedback group do not improve performance in comparison the control group (𝛾2=4.66, p-

value>.10).1 Therefore, on average (and between subjects) revealed preferences (performance

behavior) for money seem to be consistent with stated preferences (self-reported in the

questionnaire). However, this is not the case with non-monetary incentives. There is a significant

discrepancy between stated preferences and performance behavior for feedback and recognition.

The former seems to be overestimated by reps as their stated choice (second in the rankings) does

not translate into higher performance. The latter is strongly underestimated as it is the least

preferred incentive but has an effect similar to the most preferred (money).

1 For a more comprehensive discussion of main effects – out of the scope of this paper - we address the reader to

Lourenco (2015).

Insert Table 3 about here

20

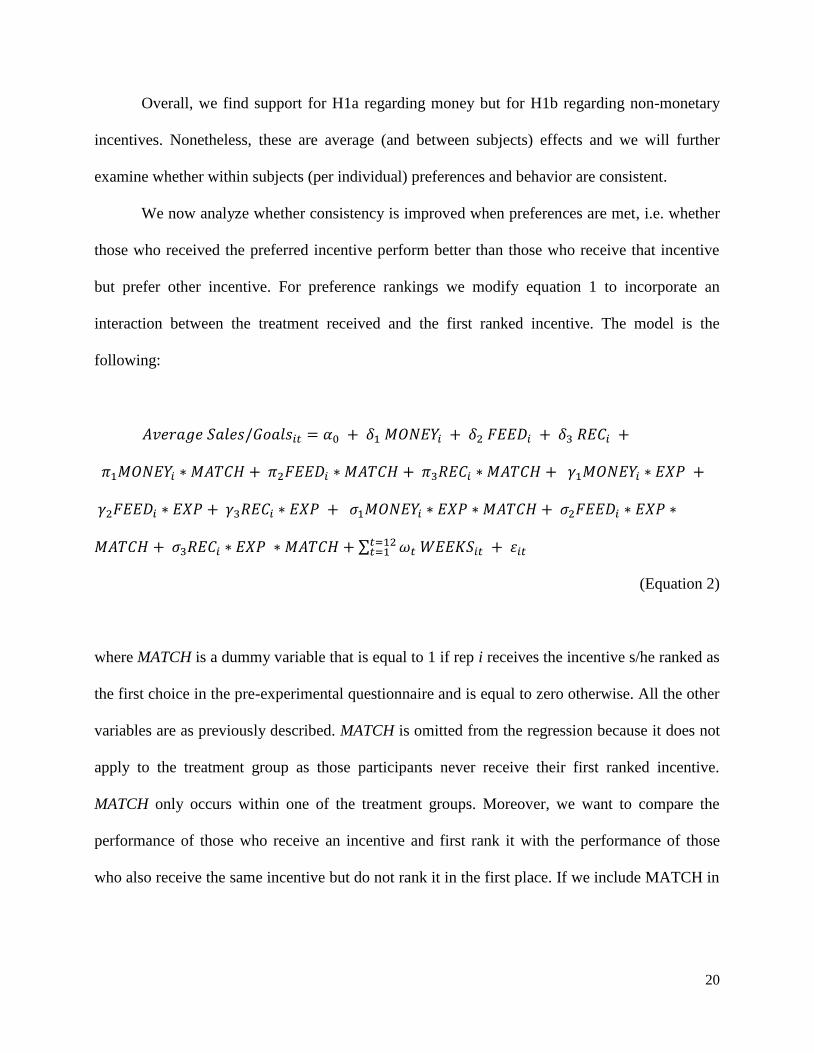

Overall, we find support for H1a regarding money but for H1b regarding non-monetary

incentives. Nonetheless, these are average (and between subjects) effects and we will further

examine whether within subjects (per individual) preferences and behavior are consistent.

We now analyze whether consistency is improved when preferences are met, i.e. whether

those who received the preferred incentive perform better than those who receive that incentive

but prefer other incentive. For preference rankings we modify equation 1 to incorporate an

interaction between the treatment received and the first ranked incentive. The model is the

following:

𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑆𝑎𝑙𝑒𝑠/𝐺𝑜𝑎𝑙𝑠𝑖𝑡 = 𝛼0 + 𝛿1 𝑀𝑂𝑁𝐸𝑌𝑖 + 𝛿2 𝐹𝐸𝐸𝐷𝑖 + 𝛿3 𝑅𝐸𝐶𝑖 +

𝜋1𝑀𝑂𝑁𝐸𝑌𝑖 ∗ 𝑀𝐴𝑇𝐶𝐻 + 𝜋2𝐹𝐸𝐸𝐷𝑖 ∗ 𝑀𝐴𝑇𝐶𝐻 + 𝜋3𝑅𝐸𝐶𝑖 ∗ 𝑀𝐴𝑇𝐶𝐻 + 𝛾1𝑀𝑂𝑁𝐸𝑌𝑖 ∗ 𝐸𝑋𝑃 +

𝛾2𝐹𝐸𝐸𝐷𝑖 ∗ 𝐸𝑋𝑃 + 𝛾3𝑅𝐸𝐶𝑖 ∗ 𝐸𝑋𝑃 + 𝜎1𝑀𝑂𝑁𝐸𝑌𝑖 ∗ 𝐸𝑋𝑃 ∗ 𝑀𝐴𝑇𝐶𝐻 + 𝜎2𝐹𝐸𝐸𝐷𝑖 ∗ 𝐸𝑋𝑃 ∗

𝑀𝐴𝑇𝐶𝐻 + 𝜎3𝑅𝐸𝐶𝑖 ∗ 𝐸𝑋𝑃 ∗ 𝑀𝐴𝑇𝐶𝐻 + ∑ 𝜔𝑡 𝑊𝐸𝐸𝐾𝑆𝑖𝑡𝑡=12𝑡=1 + 휀𝑖𝑡

(Equation 2)

where MATCH is a dummy variable that is equal to 1 if rep i receives the incentive s/he ranked as

the first choice in the pre-experimental questionnaire and is equal to zero otherwise. All the other

variables are as previously described. MATCH is omitted from the regression because it does not

apply to the treatment group as those participants never receive their first ranked incentive.

MATCH only occurs within one of the treatment groups. Moreover, we want to compare the

performance of those who receive an incentive and first rank it with the performance of those

who also receive the same incentive but do not rank it in the first place. If we include MATCH in

21

the regression it will refer to one of the treatment groups and the interactions will show the

differential effect of MATCH for the other incentives.

Column 2 of table 3 shows the results of the previous model estimated with a pooled OLS

regression with clustered standard errors by rep. This column corroborates the prior results from

column 1, with a statistically significant main effect for money and recognition, but not for

feedback. More importantly, we find that the interaction between the manipulations and MATCH

is not statistically significant for money (𝜎1= -8.57, p-value >0.10) and recognition (𝜎3= -1.23, p-

value >0.10), but is positive and statistically significant for feedback (𝜎2= 20.07, p-value <0.05).

This evidences that money (recognition) is not more effective for those who ex-ante rank money

(recognition) as their preferred incentive in comparison to others who also receive that incentive

but do not rank it as their preferred incentive. This is not the case for feedback. Those who rank

feedback as their preferred incentive perform better than others who also receive feedback but

prefer other incentive. Moreover, F tests at the bottom of table 3 show that the sum of the main

treatment effect and the interaction effect is not statistically significant for money, while it is

significant for feedback and recognition. These results show that reps who prefer and receive

money do not perform differently from the control group, while those who receive money but do

not prefer it do. Conversely, reps who prefer and receive feedback perform better than the control

group while those who receive feedback but do not prefer it do not. Finally, reps who prefer and

receive recognition perform better than the control group, which is also the case for reps who

receive recognition but do not prefer it. This suggests that money works for those who actually do

not say that they prefer it, feedback works only for those who prefer it, and recognition seems to

work for everyone regardless of their preferences. Overall column 2 of table 3, shows that those

who receive their first rank incentive do not perform better than others who also receive that

22

incentive but do not rank it first, except for feedback. Thus, H2a is only corroborated for

feedback, while H2b is supported for money and recognition.

Because preference rankings (ordinal scale) may be a crude measure of preferences, we

will now analyze if preference ratings (continuous scale) are related with performance. These

ratings are more powerful in the sense that they reflect the strength of preference (Crump et al

2012; Butler et al 2013), or the magnitude of the importance attributed to a specific incentive

(Blumenschein et al 1998; DeLeon et al 2009). Strength of preference and not only which

incentive is preferred in ordinal terms is a finer analysis to understand the preference-

performance relationship (Crump et al 2012; List et al 2004). Preference ratings are based on the

responses to the Likert-scale questions about the importance of each incentive. Equation 3

presents the model used to estimate the impact of the importance ratings on the treatment effects.

𝐴𝑣𝑒𝑟𝑎𝑔𝑒 𝑆𝑎𝑙𝑒𝑠/𝐺𝑜𝑎𝑙𝑠𝑖𝑡

= 𝛼0 + 𝜃 1 𝐼𝑀𝑃𝑀𝑂𝑁𝐸𝑌 + 𝜃 2 𝐼𝑀𝑃𝐹𝐸𝐸𝐷 + 𝜃 3 𝐼𝑀𝑃𝑅𝐸𝐶 + 𝛿1 𝑀𝑂𝑁𝐸𝑌𝑖

+ 𝛿2 𝐹𝐸𝐸𝐷𝑖 + 𝛿3 𝑅𝐸𝐶𝑖 + 𝜋1𝑀𝑂𝑁𝐸𝑌𝑖 ∗ 𝐼𝑀𝑃𝑀𝑂𝑁𝐸𝑌 + 𝜋2𝐹𝐸𝐸𝐷𝑖

∗ 𝐼𝑀𝑃𝐹𝐸𝐸𝐷 + 𝜋3𝑅𝐸𝐶𝑖 ∗ 𝐼𝑀𝑃𝑅𝐸𝐶 + 𝜇 1 𝐼𝑀𝑃𝑀𝑂𝑁𝐸𝑌 ∗ 𝐸𝑋𝑃 + 𝜇 2 𝐼𝑀𝑃𝐹𝐸𝐸𝐷

∗ 𝐸𝑋𝑃 + 𝜇 3 𝐼𝑀𝑃𝑅𝐸𝐶 ∗ 𝐸𝑋𝑃 + 𝛾1𝑀𝑂𝑁𝐸𝑌𝑖 ∗ 𝐸𝑋𝑃 + 𝛾2𝐹𝐸𝐸𝐷𝑖 ∗ 𝐸𝑋𝑃

+ 𝛾3𝑅𝐸𝐶𝑖 ∗ 𝐸𝑋𝑃 + 𝜎1𝑀𝑂𝑁𝐸𝑌𝑖 ∗ 𝐸𝑋𝑃 ∗ 𝐼𝑀𝑃𝑀𝑂𝑁𝐸𝑌 + 𝜎2𝐹𝐸𝐸𝐷𝑖 ∗ 𝐸𝑋𝑃

∗ 𝐼𝑀𝑃𝐹𝐸𝐸𝐷 + 𝜎3𝑅𝐸𝐶𝑖 ∗ 𝐸𝑋𝑃 ∗ 𝐼𝑀𝑃𝑅𝐸𝐶 + ∑ 𝜔𝑡 𝑊𝐸𝐸𝐾𝑆𝑖𝑡

𝑡=12

𝑡=1

+ 휀𝑖𝑡

(Equation 3)

23

where IMPMONEY (IMPFEED/IMPREC) is the standardized average of the three

questions in 7 point Likert-scales about the importance of monetary incentives

(feedback/recognition) previously described. Equation 3 is estimated with a pooled OLS

regression with standard errors clustered by rep.

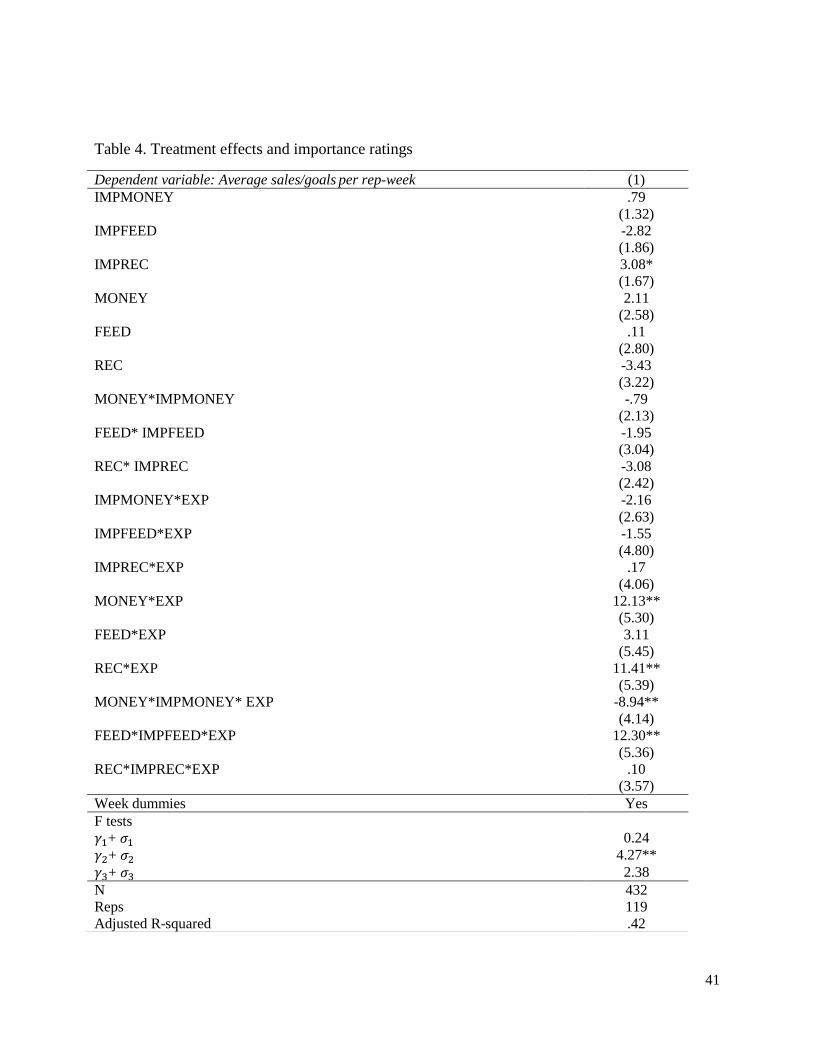

Table 4 shows a positive and statistically significant main effect for money and

recognition, and no effect for feedback. These effects are consistent with those reported in table

3. More importantly, the table shows the interactions between the different incentives and the

importance attributed to those incentives which are also consistent with the results of table 3 that

used the incentive rankings. Table 4 shows a negative and statistically significant interaction

between MONEY and IMPMONEY during the experiment (𝜎1=-13.24, p-value<.01). This

suggests that the higher the importance attributed to monetary incentives, the smaller the impact

of monetary incentives on performance. We investigate further this relationship and find, in

untabulated results of equation 1, that monetary incentives have a positive effect on performance

for the group who rates the importance of monetary incentives below median and no effect for

those who rate it above median. The F test for the sum of main effect and interaction with

IMPMONEY is not statistically significant (γ1 + σ1=12.13-8.94= 3.19, F test for 𝛾1 + 𝜎1 = 0 is

0.24, p-value>.10). This evidence confirms that those who rate the importance of monetary

incentives high do not perform differently from the control group, while those who rate the

importance of monetary incentives low actually improve their performance, relatively to the

control group, when they receive this incentive.

Insert Table 4 about here

24

Table 4 also shows a positive and significant interaction between feedback and the

importance attributed to feedback (𝜎2=12.30, p-value=<.05). Because the feedback main effect is

not statistically significant per se (𝛾2=3.11, p-value>.10), this positive interaction suggests that

feedback is only effective for those who rate the importance of feedback high. The F-test for the

sum of the main effect of feedback and interaction with IMPFEED confirms our expectation. The

sum is positive and statistically significant (γ2 + σ2=3.11+12.30= 15.41, F-test for 𝛾2 + 𝜎2=0 is

4.27, p-value<.05). We also investigate further this relationship and find, in untabulated results of

equation 1, that feedback has a positive effect on performance for the group who rates the

importance of feedback above median and no effect for those who rate it below median. Thus,

this evidence confirms that those who rate the importance of feedback high improve their

performance relatively to the control group once they start receiving feedback, while those who

rate the importance of feedback low actually do not improve relatively to the control group, when

they receive this incentive.

Lastly, we find that the interaction between recognition and the importance attributed to

recognition is not statistically significant (𝜎3=.10, p-value>.10). Because the recognition main

effect is statistically significant per se (𝛾3=11.41, p-value<.05), the non-significant interaction

suggests that recognition is effective regardless of the importance attributed to recognition. Even

though the F-test for the sum of the main effect of recognition with the interaction with IMPREC

is (weakly) not statistically significant (γ3 +σ3=11.41+.10= 11.51, F-test for 𝛾3 + 𝜎3=0 is

2.38, p-value=.13), our analysis by partitions confirms our speculation. In untabulated results of

equation 1, we find that recognition has a positive effect on performance for both the group who

rates the importance of recognition above median and for the group who rates the importance of

recognition below median. Thus, this evidence confirms that regardless of the ex ante importance

25

attributed to recognition, this incentive works for all performers regardless how they rate its

importance as they all improve relatively to the control group once they start receiving

recognition.

Overall, the results presented in table 4 are overwhelmingly consistent with those present

in table 3, and we conclude that H2a is only corroborated for feedback, while H2b is supported

for money and recognition.

To analyze the moderating effects of tenure and past experience with the different

incentives, we run full interacted models of equations 2 and 3 as well as partitions of those

models.

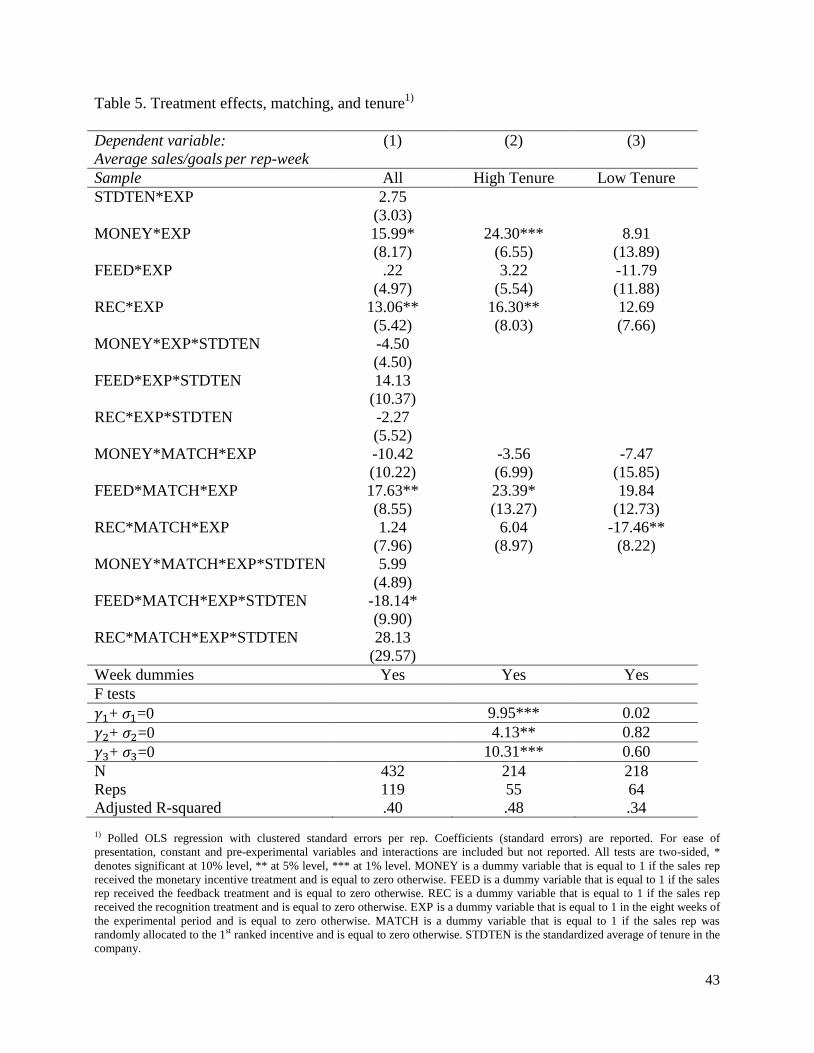

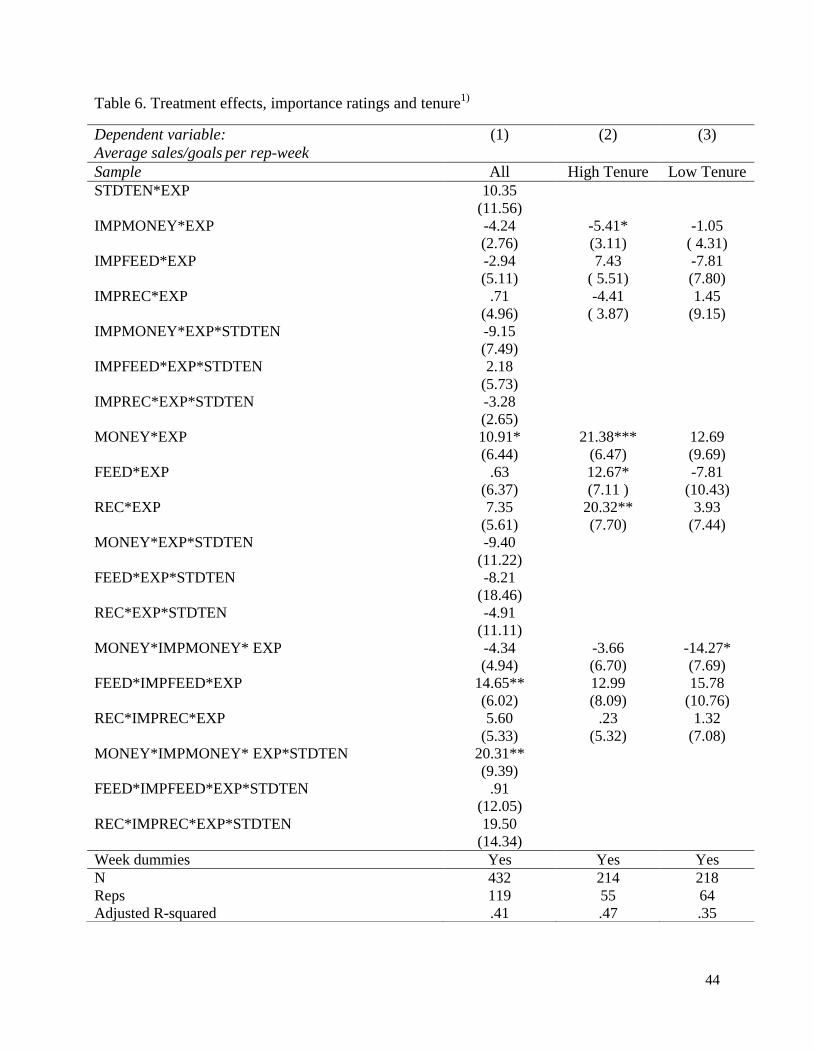

Table 5 and 6 show the results for the moderating effect of tenure. The results show that a

higher tenure is not associated with a better consistency between ex-ante preferences (first ranked

incentive or higher importance ratings) and performance suggesting that these preference

inconsistencies do not seem to result from an insufficient work experience. Untabulated results

show that this is also the case of past experience with the different incentives, similarly

suggesting no learning effects. Therefore, H3a is rejected and H3b is supported.

Robustness tests

To evaluate the robustness of our results, we performed several additional tests. We start

by estimating our models with a Tobit regression to account for the fact that our data is censored

Insert Table 5 about here

Insert Table 6 about here

26

at the bottom. Performance is the ratio of sales relative to goals and hence cannot be below 0. The

results reported hold in this specification. We also estimated our models with fixed and random

effects per rep and the results are also qualitatively unchanged. Finally, we explore whether the

importance attributed to a given incentive impacts the effect of the other incentives. We run

equation 3 three times again using as the importance variable i) IMPMONEY, ii) IMPFEED, and

iii) IMPREC. Untabulated results show that there are no statistically significant interactions

between the importance attributed to one incentive and the manipulation of other incentives.

Additionally, the results are consistent with the ones present in table 4, both for the main effects

and the interactions.

DISCUSSION AND CONCLUSION

We use a longitudinal field experiment to examine how preferences for different

incentives (money, recognition and feedback) influence the effectiveness of those incentives on

performance behavior. We analyze ex-post objective performance data from different incentive

manipulations in light of ex-ante incentive preferences collected in the pre-experimental period

via a questionnaire. Results from our study expose several inconsistencies in employee

preferences for performance incentives drawn from a natural organizational setting.

First, we show that average preference rankings do not translate into corresponding

performance levels. Employees attribute a significantly higher importance to monetary incentives

and feedback in terms of their motivational role for job performance and significantly less to

recognition. This rank order in stated preferences for different incentives is robust to the

elicitation method (ordinal or continuous scales). The importance attributed to different

incentives does not significantly vary per age, tenure or income. We find that these stated

27

preferences tend to be on average discrepant with actual performance (revealed preferences). Our

results show that on average (and between subjects) employees prefer money and this incentive

yields a significant performance improvement. However, employees overestimate the impact of

feedback because this is the second preferred incentive but yields on average no significant

improvement in performance. This overestimated effect may be due to the frequent use of

feedback in organizations as one of the most common reinforcers to influence employees’

behavior (Balcazar et al. 1985; Kluger & DeNisi, 1996; Alvero et al., 2001). Familiarity may

inflate the perception of effectiveness. Finally, employees underestimate the impact of

recognition as this is the least preferred incentive but yields a performance improvement similar

to money. This is likely due to the discounted impact of peer effects and social comparison

processes in the workplace. Second, by analyzing within subjects preferences and behavior we

find further inconsistencies. Employees who receive their first ranked incentive performed no

better than those who received that incentive but did not rank it first, except for the feedback

condition. Specifically, we find that money only works for those who do not rank it first (or rate

its importance below median), feedback works only for those who rank it first (or rate it above

median), and recognition works for everyone regardless of their preferences. Finally, there is no

evidence of learning effects, which suggests that these biases may be grounded in lay rationalism,

and hence more likely to be resistant to experimental learning because it is not grounded on

cognitive misperceptions (as most forecasting bias are) but in more engrained shared belief

systems that may not be easily confronted.

Our results pose two key questions to be discussed. On one hand why performance is not

improved when employees receive their preferred incentive. On the other hand, why there seems

to be no evidence of learning effects. Regarding the former, it may have been the case that

employees reported their preferences regarding their perception of how different incentives

28

impact their motivation, satisfaction or attention in the workplace – and may not know exactly

what improves their objective performance. For instance, employees may react negatively to the

implementation of recognition programs in the organization, expecting to benefit more from

monetary incentives or feedback in terms of their performance and satisfaction. But we call

special attention to the fact the different incentives were not evaluated and ranked in abstract

terms or regarding expected preferences for the general population. The questions were posed

specifically about their impact in employees performance, both their preferred ranking between

incentives and their importance to strive at work (“How important or unimportant is each

characteristic for you to do a good job?; “How important or unimportant is each characteristic to

motivate you to excel in your job?”). Therefore, an overall positive significant relationship

between stated preferences and performance would have been a natural result if employees truly

knew their preferences. It could also be that in most organizations employees do not have voice

regarding which incentives are implemented. People repeatedly accept the default options that

have been chosen by others (Carroll et al 2009). In workplace settings, regulated by contractual

arrangements and hierarchical work relationships, employees may not expect to have any

influence regarding organizational compensation decisions and thus no expectation violation

occurs (Morrison & Robinson 1997) – and this acceptance may prevent employees to perform

poorly when companies implement incentives that were not desired. People may also accept

defaults because they believe that the person who set the default was making a carefully

considered decision (Madrian & Shea, 2001; Beshears et al., 2008) and this effect is a plausible

scenario in employer-employee relationships.

Preference strength moderates performance effects in very distinct ways according to

different incentives and this effect is likely to be explained by the specificity of (expected versus

experienced) utility gains from each incentive. The negative impact of the importance attributed

29

to money may be due to the unmet expectations of utility gains from monetary incentives.

Research has shown that people who place too much importance on monetary rewards may

actually be working against their experienced utility because the utility gains from money do not

match the high expectations (Frey & Jengen 2001: Kanhneman et al 1997). On the other hand,

the strong and positive effect of a preference for feedback may be explained by the fact that –

from all three incentives under analysis -feedback is the one that provides the more intangible or

‘intrinsic’ benefits. Thus only employees that report very high importance ratings on such an

incentive are likely to experience the utility gains from receiving it. Finally, the null effect of

preference strength for recognition suggests that public acknowledgment of competence is a

shared preference by all employees (with or without clear awareness on their part). There is

abundant evidence that people underestimate the power of social influence and that individuals

do not fully realize how much their behavior is influenced by the expectation of positive

reinforcement from others (e.g., Carr & Walton, 2014; Exline et al 2004).

Regarding the latter, this question raises more intricate challenges. The absence of

positive results from tenure and experience with incentives (both previous experience and pre-

post experimental changes in reported preferences) do not seem to support most of the proposed

explanations about the sources of preference inconsistencies being grounded in forecasting errors

that should be reduced with experiential learning. In this regard, Meyvis et al 2010 explored why

people might fail to learn from experience, even when the experience itself has not been

forgotten. They propose that, aside from a failure to accurately recall their experience, people

also persist in their forecasting errors because they misremember their initial forecast. A bias to

recall their forecast as consistent with their actual experience obscures people’s forecasting error.

As a result, people are unlikely to realize the need to update their forecasting strategies and

continue to rely on those same strategies for subsequent forecasts. Thus, either people are not

30

using experience to update their preferences or (as we propose the most suitable justification) the

reasons lie outside forecasting errors. The results seem to offer support for the lay rationalism

hypothesis which is the mechanism more likely to be resistant to experimental learning because it

is not grounded on cognitive misperceptions (as most forecasting bias are) but in more engrained

shared belief systems that may not be easily confronted.

Nevertheless, overall results show that giving employees what they claim to prefer does

not result in significantly better work performance which is contrary to the assumptions of most

standard theories in economics and management. Taken together these results highlight the

limited predictive power of stated preferences for work incentives with respect to their translation

into objective performance measures. Hence, caution should be used in taking preferences at face

value and actually designing incentive systems based on stated preferences. These inconsistencies

call attention to the need for rethinking how employee reward preferences should be taken into

consideration when developing incentive programs. These results highlight the need for

employee education regarding work motivation because lay conceptions are likely to have a

strong impact in job choices and employee responses to organizational incentive programs

including job satisfaction, organizational commitment and turnover intentions (e.g., Misra et al

2013). There may be the need to consider both tailored incentive programs according to

individual preferences – as it could be the case of feedback – but also the power of fundamental

motivational processes as illustrated by the recognition condition – that appear to strike core

human needs to which employees respond to regardless of their stated preferences. Money seems

to fulfil (on average) preferences for work incentives but the key insight to be conveyed to

employees should be that an overemphasis placed on the importance on monetary incentives may

be counterproductive by reducing the experienced utility from money.

31

This study is not without caveats. Although field experiments score high on internal

validity, the generalization of the results may be a concern as the field experiment was done in a

single research site. As such, the characteristics of this firm and of its employees may play a role.

For example, the fact that participants are paid an hourly wage poses the question that our results

may not apply to more fixed-pay contractual arrangements. Theory also cautions about the

measurement of incentive preferences. Different elicitation methods may lead to different

answers about those preferences. We tried to overcome this issue, by using two different methods

and the results our overwhelmingly consistent.

These limitations represent several avenues for future research. On one hand, it would be

interesting to analyze whether our results hold in settings where employees are paid a fixed salary

at the end of the month and not an hourly wage. This type of contracts may lead to different

preferences as monetary incentives may be more or less relevant in total pay. On the other hand,

and to avoid the criticism associated with a stated preference, future studies can give employees

the actual choice of their incentive (and not just a stated preference) and analyze performance

after the implementation of the desired incentive.

32

References

Ajzen, I., Brown, T. C., and Carvajal, F. 2004. Explaining the discrepancy between intentions

and actions: The case of hypothetical bias in contingent valuation. Personality and social

psychology bulletin, 30(9), 1108-1121.

Alderfer, C. P. 1972. Existence, Relatedness, and Growth; Human Needs in Organizational

Settings. New York: Free Press.

Analoui, F. 2000. What motivates senior managers? The case of Romania. Journal of Managerial

Psychology, 15(4), 324-340.

Alvero, A. M., Bucklin, B. R., and Austin, J. 2001. An objective review of the effectiveness and

essential characteristics of performance feedback in organizational settings (1985-1998).

Journal of Organizational Behavior Management, 21(1), 3-29.

Ariely, D., Loewenstein, G., and Prelec, D. 2006. Tom Sawyer and the construction of value.

Journal of Economic Behavior and Organization, 60(1), 1-10.

Ashraf, N., Bandiera, O., and Jack, K. 2013. No margin, no mission? A Field Experiment on

Incentives for public service delivery. Working paper, Harvard Business School.

Baker, G. P., Jensen, M. C., and Murphy, K. J. 1988. Compensation and incentives: Practice vs.

theory. The journal of Finance, 43(3), 593-616.

Balcazar, F., Hopkins, B. L., and Suarez, Y. 1985. A critical, objective review of performance

feedback. Journal of Organizational Behavior Management, 7(3-4), 65-89.

Bandura, A. 1986. Social foundations of Thought and Action. Englewood Cliffs, NJ: Prentice

Hall.

Baumann, O., and Stieglitz, N. 2014. Rewarding value‐creating ideas in organizations: The

power of low‐powered incentives. Strategic Management Journal, 35(3), 358-375.

Bareket-Bojmel, L., Hochman, G., and Ariely, D. 2014. It’s (Not) All About the Jacksons Testing

Different Types of Short-Term Bonuses in the Field. Journal of Management,

0149206314535441.

Bellé, N. 2013. Experimental evidence on the relationship between public service motivation and

job performance. Public Administration Review, 73(1), 143-153.

Bellenger, D. N., Wilcox, J. B., and Ingram, T. N. 1984. An examination of reward preferences

for sales managers. Journal of Personal Selling and Sales Management, 4(2), 1-6.

Berg, J. E., Dickhaut, J. W., and Rietz, T. A. 2010. Preference reversals: The impact of truth-

revealing monetary incentives. Games and Economic Behavior, 68(2), 443-468.

Beshears, J., Choi, J. J., Laibson, D., and Madrian, B. C. 2008. How are preferences revealed?

Journal of Public Economics, 92(8), 1787-1794.

Blumenschein, K., Johannesson, M., Blomquist, G. C., Liljas, B., and O'Conor, R. M. 1998.

Experimental results on expressed certainty and hypothetical bias in contingent valuation.

Southern Economic Journal, 169-177.

Bonner, S. E., Hastie, R., Sprinkle, G. B., and Young, S. M. 2000. A review of the effects of

financial incentives on performance in laboratory tasks: Implications for management

accounting. Journal of Management Accounting Research, 12(1), 19-64.

Bonner, S. E., and Sprinkle, G. B. 2002. The effects of monetary incentives on effort and task

performance: theories, evidence, and a framework for research. Accounting, Organizations

and Society, 27(4), 303-345.

Bonsdorff, M. E. 2011. Age-related differences in reward preferences. The International Journal

of Human Resource Management, 22(06), 1262-1276.

33

Brown, M. P., Sturman, M. C., and Simmering, M. J. 2003. Compensation policy and

organizational performance: The efficiency, operational, and financial implications of pay

levels and pay structure. Academy of Management Journal, 46(6), 752-762.

Butler, D., Isoni, A., Loomes, G., and Tsutsui, K. 2013. Beyond choice: investigating the

sensitivity and validity of measures of strength of preference. Experimental Economics, 1-

27.

Caplin, A., and Leahy, J. 2001. Psychological expected utility theory and anticipatory feelings.

Quarterly Journal of economics, 55-79.

Carr, P. B., and Walton, G. M. (2014). Cues of working together fuel intrinsic motivation.

Journal of Experimental Social Psychology, 53, 169-184.

Carroll, G. D., Choi, J. J., Laibson, D., Madrian, B. C., and Metrick, A. 2009. Optimal Defaults

and Active Decisions. The Quarterly journal of economics, 124(4), 1639-1674.

Chen, M. K., and Risen, J. L. 2010. How choice affects and reflects preferences: revisiting the

free-choice paradigm. Journal of Personality and Social Psychology, 99(4), 573.

Chiang, F. F., and Birtch, T. A. 2005. A taxonomy of reward preference: Examining country

differences. Journal of International Management, 11(3), 357-375.

Chiang, F. F., and Birtch, T. A. 2006. An empirical examination of reward preferences within and

across national settings. Management International Review, 46(5), 573-596.

Chiang, F. F., and Birtch, T. A. 2012. The Performance Implications of Financial and Non‐Financial Rewards: An Asian Nordic Comparison. Journal of Management Studies, 49(3),

538-570.

Chonko, L. B., Tanner Jr, J. F., and Weeks, W. A. 1992. Selling and sales management in action:

reward preferences of salespeople. Journal of Personal Selling and Sales Management,

12(3), 67-75.

Clark, A. E. 2005. Your money or your life: Changing job quality in OECD countries. British

Journal of Industrial Relations, 43(3), 377-400.

Crump, R. T., and Llewellyn-Thomas, H. A. 2012. The importance of measuring strength-of-

preference scores for health care options in preference-sensitive care. Journal of clinical

epidemiology, 65(8), 887-896.

Dai, X., Brendl, C. M., and Ariely, D. 2010. Wanting, liking, and preference construction.

Emotion, 10(3), 324.

Dane, E., and George, J. 2014. Unpacking Affective Forecasting and Its Ties to Project Work In

Organizations. Academy of Management Review, 39(2):181-201.

DeLeon, I. G., Frank, M. A., Gregory, M. K., and Allman, M. J. 2009. On the correspondence

between preference assessment outcomes and progressive‐ratio schedule assessments of

stimulus value. Journal of applied behavior analysis, 42(3), 729-733.

Dewhurst, M., Guthridge, M., and Mohr, E. 2009. Motivating people: Getting beyond money.

McKinsey Quarterly, 1(4), 12-15.

Dohmen, T., and Falk, A. 2011. Performance pay and multidimensional sorting: Productivity,

preferences, and gender. The American Economic Review, 556-590.

Dysvik, A., and Kuvaas, B. 2011. Intrinsic motivation as a moderator on the relationship between

perceived job autonomy and work performance. European Journal of Work and

Organizational Psychology, 20(3), 367-387.

Durham, C. C., and K. Bartol. 2000. Pay for performance. In Handbook of Principles of

Organizational Behavior edited by E. A. Locke. Oxford, England: Blackwell, 150-165.

34

Egan, L. C., Bloom, P., and Santos, L. R. 2010. Choice-induced preferences in the absence of

choice: Evidence from a blind two choice paradigm with young children and capuchin

monkeys. Journal of Experimental Social Psychology, 46(1), 204-207.

Ellingsen, T., and M. Johannesson. 2007. Paying respect. The Journal of Economic Perspectives

21 (4) 135-150.

Eisenhardt, K. M. 1988. Agency-and institutional-theory explanations: The case of retail sales

compensation. Academy of Management journal, 31(3), 488-511.

Eisenhardt, K. M. 1989. Agency theory: An assessment and review. Academy of management

review, 14(1), 57-74.

Exline, J. J., Single, P. B., Lobel, M., and Geyer, A. L. (2004). Glowing praise and the envious

gaze: Social dilemmas surrounding the public recognition of achievement. Basic and

Applied Social Psychology, 26(2-3), 119-130.

Franceschelli, I., Galiani, S., and Gulmez, E. 2010. Performance pay and productivity of low-and

high-ability workers. Labour Economics, 17(2), 317-322.

Frey, B. S., and Jegen, R. 2001. Motivation crowding theory. Journal of economic surveys,

15(5), 589-611.

Gerhart, B., and Fang, M. 2014. Pay for (individual) performance: Issues, claims, evidence and

the role of sorting effects. Human Resource Management Review, 24(1), 41-52.

Gilbert, D. T., Gill, M. J., and Wilson, T. D. 2002. The future is now: Temporal correction in

affective forecasting. Organizational Behavior and Human Decision Processes, 88(1), 430-

444.

Gupta, N., and Shaw, J. D. 2014. Employee compensation: The neglected area of HRM research.

Human Resource Management Review, 24(1), 1-4.

Hackman, J. R., and Oldham, G. R. (1980). Job Diagnostic Survey (JDS). Hackman, JR/Oldham,

GR (1980): Work redesign. Reading, Company. S, 275-294.

Harrison, G. W., and Rutström, E. E. 2008. Experimental evidence on the existence of

hypothetical bias in value elicitation methods. Handbook of experimental economics

results, 1(5), 752-767.

Heath, C. 1999. On the social psychology of agency relationships: Lay theories of motivation

overemphasize extrinsic incentives. Organizational behavior and human decision

processes, 78(1), 25-62.

Herzberg, F. 1966. Work and the nature of man. Oxford: OUP.

Heyman, J., and D. Ariely. 2004. Effort for payment a tale of two markets. Psychological Science

15 (11): 787-793.

Hölmstrom, B. 1999. Moral hazard and observability. The Bell Journal of Economics, 74-91.

Ingram, T. N., and Bellenger, D. N. 1983. Personal and organizational variables: Their relative

effect on reward valences of industrial salespeople. Journal of Marketing Research, 198-

205.

Jensen, M. C. and W. H. Meckling. 1976. Theory of the Firm: Managerial Behavior, Agency

Costs and Ownership Structure. Journal of Financial Economics 3 (4): 305-360.

Kahneman, D., and Thaler, R. 1991. Economic analysis and the psychology of utility:

applications to compensation policy. The American Economic Review, 341-346.

Kahneman, D., and Thaler, R. H. 2006. Anomalies: Utility maximization and experienced utility.

The Journal of Economic Perspectives, 20(1), 221-234.

Kahneman, D., Wakker, P. P., and Sarin, R. 1997. Back to Bentham? Explorations of

experienced utility. The Quarterly Journal of Economics, 375-405.

35

Kovach, K. A. 1980. Why motivational theories don’t work. SAM Advanced Management

Journal, 45(2), 54-59.

Kovach, K. A. 1987. What motivates employees? Workers and supervisors give different

answers. Business Horizons, 30(5), 58-65.

Kosfeld, M., and S. Neckermann. 2011. Getting more work for nothing? Symbolic awards and

worker performance. American Economic Journal: Microeconomics 3 (3): 86-99.

Kluger, A. N., and DeNisi, A. 1996. The effects of feedback interventions on performance: a

historical review, a meta-analysis, and a preliminary feedback intervention theory.

Psychological bulletin, 119(2), 254–284.

Latham, G. P., and Locke, E. A. 1991. Self-regulation through goal setting. Organizational

behavior and human decision processes, 50(2), 212-247.

Larkin, I., Pierce, L., and Gino, F. 2012. The psychological costs of pay‐for‐performance:

Implications for the strategic compensation of employees. Strategic Management Journal,

33(10), 1194-1214.

Lazear, E. P. 2000. The power of incentives. American Economic Review, 410-414.

Lee, H. J., Iijima, Y., and Reade, C. 2011. Employee preference for performance-related pay:

predictors and consequences for organizational citizenship behavior in a Japanese firm. The

international journal of human resource management, 22(10), 2086-2109.

Lee, M. S., Yu, C. T., Martin, T. L., and Martin, G. L. 2010. On the relation between reinforcer

efficacy and preference. Journal of applied behavior analysis, 43(1), 95-100.

Leuven, E., Oosterbeek, H., Sonnemans, J., and Van Der Klaauw, B. 2011. Incentives versus

sorting in tournaments: Evidence from a field experiment. Journal of Labor Economics,

29(3), 637-658.

Lichtenstein, S., and Slovic, P. (Eds.). 2006. The construction of preference. Cambridge

University Press.

List, J. A. 2001. Do explicit warnings eliminate the hypothetical bias in elicitation procedures?

Evidence from field auctions for sportscards. American economic review, 1498-1507.

Lopez, T. B., Hopkins, C. D., and Raymond, M. A. 2006. Reward preferences of salespeople:

how do commissions rate? Journal of Personal Selling and Sales Management, 26(4), 381-

390.

Lourenco, S. M. 2015. Monetary Incentives, Feedback and Recognition – Complements or

Substitutes? Evidence from a Field Experiment in a Retail Services Company. The

Accounting Review (in press)

Loewenstein, G., O'Donoghue, T., and Rabin, M. 2003. Projection bias in predicting future

utility. The Quarterly Journal of Economics, 1209-1248.

Markham, S. E., D. Scott, and G. McKee. 2002. Recognizing good attendance: A longitudinal

quasi-experimental field study. Personnel Psychology 55: 639-660.