What are options? - 4FM3 - homeCollege+of... · · 2011-01-17What are options? ð§A financial...

53

What are options? A financial derivative contract that provides a party the right to buy or sell but not the obligation an underlying at a fixed price by a certain time in the future

Transcript of What are options? - 4FM3 - homeCollege+of... · · 2011-01-17What are options? ð§A financial...

What are options?

A financial derivative contract thatprovides a party the right to buy or sell butnot the obligation an underlying at a fixedprice by a certain time in the future

Types of Options

Call Option An option granting the

right to buy theunderlying

Put Option An option granting the

right to sell theunderlying

Characteristics of Options

Option price, option premium, orpremium

the amount of money a buyer pays andseller receives to engage in an optiontransaction

Characteristics of Options

Exercise price, strike price, striking price,or strike

the fixed price at which the option holdercan buy or sell the underlying

Characteristics of Options

Expiration date

the date on which aderivative contractexpires

Characteristics of Options

Time to expiration

the time remaining inthe life of aderivative, typicallyexpressed in years

Option Pricing Dates

Trading Date Day when option is traded

Option Pricing Dates

Premium Payment Date Day when option

premium has to bepaid

Usually two bankingdays after the tradingdate

Option Pricing Dates

Exercise Date Last day when option

writer accepts exerciseof option

Option Pricing Dates

Expiration Date Last day when option

writer accepts exerciseof option

Option Pricing Dates

Settlement Date (European Options) Two banking days after expiry

date

Option Pricing Dates

Settlement Date (American Options) Two banking days after exercise

date

Principles in Pricing Options

Call options have alower premium, thehigher the exerciseprice

Principles in Pricing Options

Put options have ahigher premium, thelower the exerciseprice

Principles in Pricing Options

Both call and putoptions are cheaperthe shorter the timeto expiration

Concept of Moneyness of an Option

In-the-money (ITM)

At-the-money (ATM)

Out-of-the money (OTM)

Concept of Moneyness of an Option In-the-money

Option that, ifexercised, wouldresult in the valuereceived beingworth more than thepayment required toexercise

Concept of Moneyness of an Option At-the-money

Option in which the underlyingvalue equals the exercise price

Concept of Moneyness of an Option Out-of-the money

Option that, ifexercised wouldrequire the payment ofmore money than thevalue received andtherefore would not becurrently exercised

Characteristics of Options

European option

An option that canbe exercised only atexpiration

Also referred to asEuropean styleexercise

Characteristics of Options

American option

An option that can beexercised on any daythrough the expiration day

Also referred to asAmerican style exercise

Types of Financial Options

Equity Options

Options on individualstocks

Also known as stockoptions

Types of Financial Options

Bond Options

Options in which theunderlying is a bond

Primarily traded inover-the-countermarkets

Types of Financial Options

Interest Rate Options

Options in which theunderlying is aninterest rate

Types of Financial Options

Currency Options

Options that allow theholder to buy (if a call) orsell (if a put) anunderlying currency at afixed exercise rate,expressed as anexchange rate

Types of Financial Options

Options on futures

Options that give theholder the right toenter into a longfutures contract at afixed futures price

Types of Financial Options

Options on Forwards

Option on a forwardcontract

Currency Option P/L ProfileBuyer of a Call

Profit (Loss) = spot rate – (strike price + premium)

Write (seller) of a CallProfit (Loss) = premium – (spot rate – strike price)

Buyer of a PutProfit (Loss) = strike price – (spot price + premium)

Writer (Seller) of a PutProfit (Loss) = premium – (strike price – spot rate)

Option Pricing Sensitivities (The Greek Chorus)

Delta – Spot Rate Sensitivity

Delta (Δ) = Δ premiumΔ spot rate

As the option moves further ITM, delta risestowards 1.0.

As the option moves further OTM, delta fallstowards zero.

The higher the delta (around 0.7, 0.8 or higher),the greater the probability of the option expiringin the money.

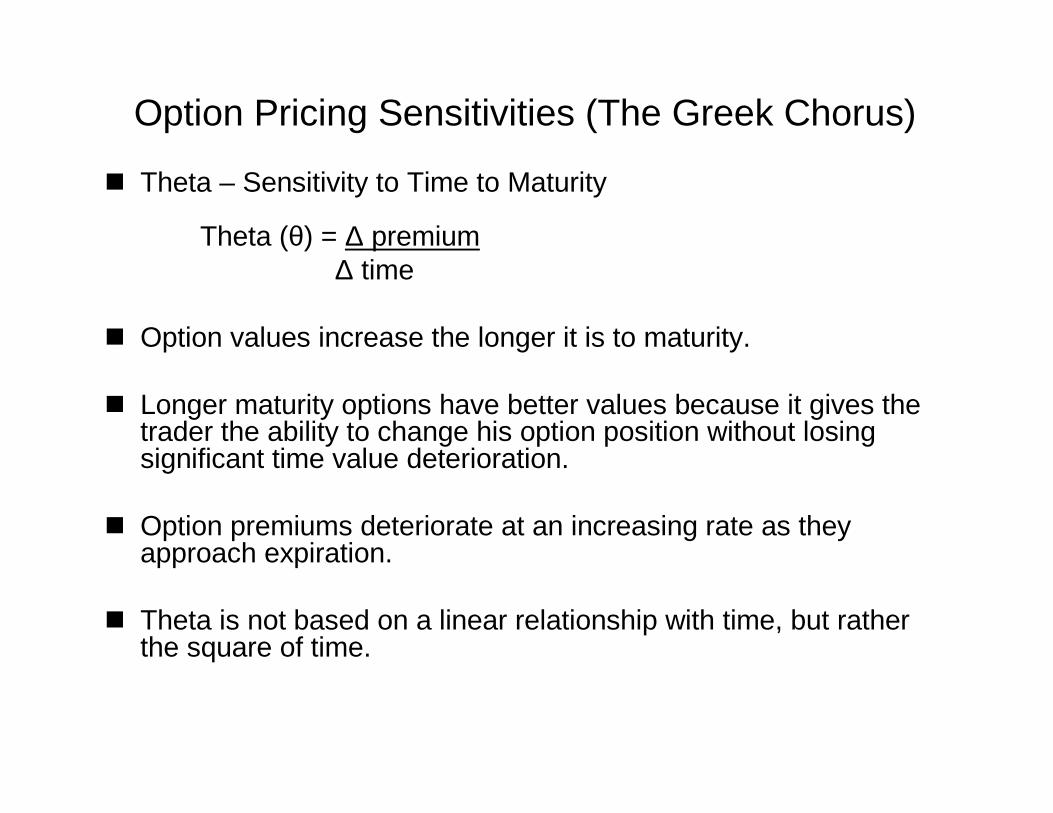

Option Pricing Sensitivities (The Greek Chorus)

Theta – Sensitivity to Time to Maturity

Theta (θ) = Δ premiumΔ time

Option values increase the longer it is to maturity.

Longer maturity options have better values because it gives thetrader the ability to change his option position without losingsignificant time value deterioration.

Option premiums deteriorate at an increasing rate as theyapproach expiration.

Theta is not based on a linear relationship with time, but ratherthe square of time.

Option Pricing Sensitivities (The Greek Chorus)

Vega – Sensitivity to Volatility

Vega = Δ premiumΔ volatility

If volatilities will fall sharply in the near term,traders will write (sell) options now, hoping tobuy them back for a profit right after volatilitiesfall.

This action causes option prices to fall.

Option Pricing Sensitivities (The Greek Chorus)

Rho – Sensitivity to Change in DomesticInterest Rates

Rho (ρ) = Δ premiumΔ Domestic Interest Rate

A call option on foreign currency shouldbe bought before a rise in domesticinterest rates before the option price willincrease.

Option Pricing Sensitivities (The Greek Chorus)

Phi – Sensitivity to Change in ForeignInterest Rates

Phi (Φ) = Δ premiumΔ Foreign Interest Rate

Option Payoff

Payoff of OptionsCall Option

At expiration, a call option is worth eitherzero or the difference between the underlyingprice S and the exercise price X, whicheveris greater

Payoff has to be positive to be exercised

Payoff = max [0, S - X]

Payoff of OptionsPut Option

At expiration, a put option is worth eitherzero or the difference between the exerciseprice X and the underlying price S,whichever is greater

Payoff has to be positive to be exercised

Payoff = max [0, X - S]

Minimum and Maximum Values of Options

• The maximum value of a European put isthe present value of the exercise price.

• The maximum value of an American put isthe exercise price.

Option Pricing and Valuation Determinants

Time Value

Intrinsic Value

Time Value = Option Premium less Intrinsic Value

Call Option = Spot Price less Strike PricePut Option = Strike Price less Spot Price

Intrinsic Value – financial gain if the option is exercisedimmediately.

Time Value – value of an option arising from the time left tomaturity.

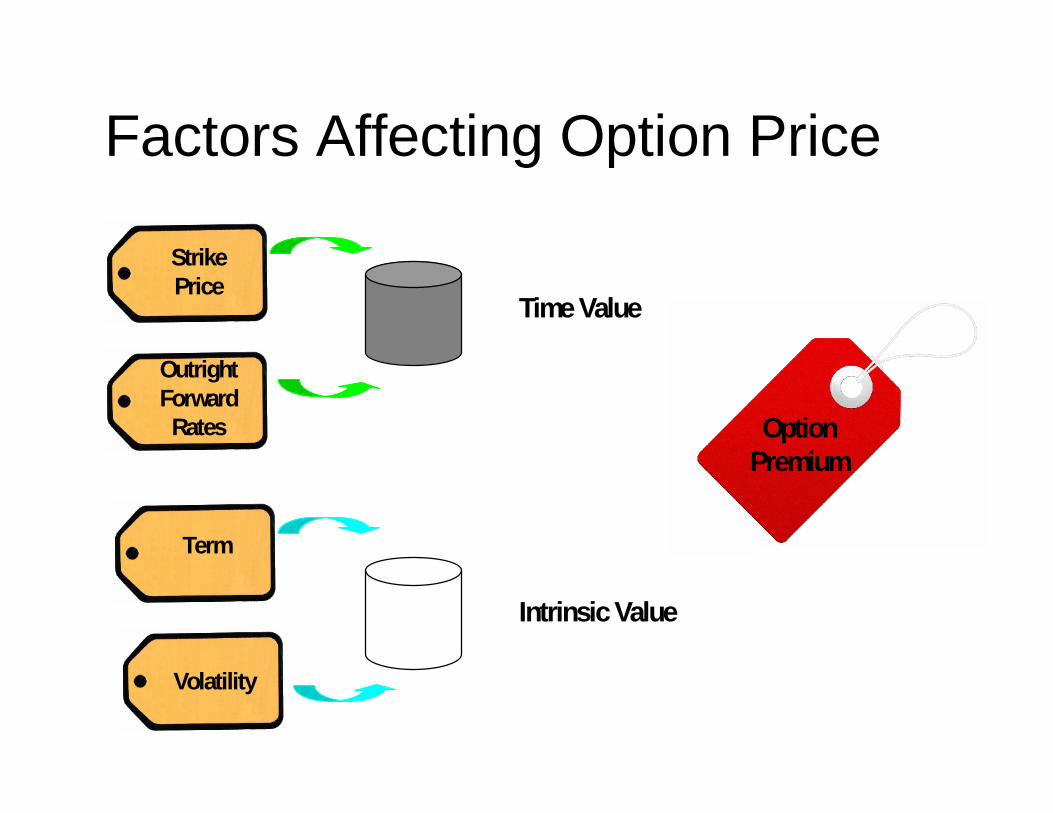

Factors Affecting Option Price

Time Value

Intrinsic Value

OptionPremium

StrikePrice

OutrightForward

Rates

Term

Volatility

Three Types of Volatility

Historic Volatility

Forward-Looking Volatility

Implied Volatility

Three Types of Volatility

Historic Volatility

Standard deviation ofthe continuouslycompounded returnon an asset estimatedfrom historical data

Three Types of Volatility

Forward-LookingVolatility

Recent historicvolatility adjusted forexpected marketoutlook

Three Types of Volatility

Implied Volatility

Volatility implied froman option price usingBlack-Scholes that willequal the observedmarket price of theoption

Black-Scholes-Merton Model A model for pricing European options on stocks,

developed by Fischer Black, Myron Scholes, and RobertMerton in 1973.

c = S0 N(d1) – X e-rT N(d2)p = X e-rT [1 - (d2)] – S[1 - N(d1)]

whered1= ln(S/X) + [rc + (σ/2)]T / σ √ Td2 = d1 - σ √ Tσ = annualized standard deviation of the continuously

compounded return on the stockrc = continuously compounded risk-free rate of returnT = timeN( ) = Cumulative Normal DistributionFunction

Put-Call Parity

c0 + X / ( 1 + r )t = p0 + S0

Where:c0 = European call optionp0 = European put optionX = risk free bondS0 = the underlying assetr = annual interest ratet = time in years

Put-Call Parity

An equation expressingthe equivalence (parity)of a portfolio of a call anda bond with a portfolio ofa put and the underlying,which leads to therelationship between putand call prices

Pricing Options

Binomial Model – a model for pricingoptions in which the underlying price canmove to only one of two possible newprices

It’s used for discrete time option pricing Binomial tree – a diagram representing

price movements of the underlying in abinomial model

Kinds of Binomial Models

One Period Binomial Model Two Period Binomial Model N period Binomial Model

Assumptions of Binomial Option PricingModel

• Market is frictionless• Investors are price takers• Short selling is allowed, with full use of

proceeds• Borrowing and lending at the risk free rate

is permitted• Future stock prices will have one or two

possible values

Hedge Ratio

H = cu - cd

S0(u –d)

Synthetic Forward Contract

A contract consisting of a long call, a shortput, and a long risk free bond with a facevalue equal to the exercise price minus theforward price.

Black Model

• Model for pricing European options onfutures.

• Used frequently to price interest rateoptions.

Black Modelc0 = e-r T [f0 ( T ) N(d1 ) – X N(d2 )]

p0 = e-r T (X[1-N(d2)]– f0 (T)[1- N(d1)]

Whered1 = ln [f0 (T) / X] + ( σ2 / 2 ) T

σ √Td2 = d1 - σ √Tf0 (T) = the futures price

![Ð Ð£Ð Ð Ð Ð§Ð Ð«Ð Ð Ð Ð Ð Ð Ð Ð Ñ Ð°Ð¹Ñ · 2019-12-28 · ^ h I m [ e q g b c ^ h ] h \ j d h f i e _ d k g h ] h [ Z g d \ k v d h ] h h [ k e m ] h \ m](https://static.fdocuments.in/doc/165x107/5ece00dee612f130492ec9b5/-2019-12-28-.jpg)