WESTERN AUSTRALIA’S INTERNATIONAL RESOURCES …

40

WESTERN AUSTRALIA’S INTERNATIONAL RESOURCES DEVELOPMENT MAGAZINE September–November 2005 $3 (inc GST) ENVIRONMENTAL BENCHMARK GOLDEN GECKO WINNERS RESOURCES ICON FAREWELL TO WMC IRON ORE KOOLAN ISLAND BACK IN BUSINESS NICKEL THE RAMIFICATIONS FOR RAVENSTHORPE Print post approved PP 665002/00062

Transcript of WESTERN AUSTRALIA’S INTERNATIONAL RESOURCES …

WESTERN AUSTRALIA’S INTERNATIONAL RESOURCES DEVELOPMENT MAGAZINE September–November 2005 $3 (inc GST)

ENVIRONMENTAL BENCHMARKGOLDEN GECKO WINNERS

RESOURCES ICONFAREWELL TO WMC

IRON OREKOOLAN ISLAND BACK IN BUSINESS

NICKELTHE RAMIFICATIONS FOR RAVENSTHORPE

Pri

nt p

ost a

ppro

ved

PP

665

002/

0006

2

From the Director General

DEPARTMENT OF INDUSTRY AND RESOURCESInvestment Services 1 Adelaide Terrace EAST PERTH Western Australia 6004Tel: +61 8 9222 3333 • Fax: +61 8 9222 3862 Email: [email protected]

INTERNATIONAL OFFICESEuropeEuropean Offi ce • 5th fl oor, Australia CentreCorner of Strand and Melbourne PlaceLONDON WC2B 4LG • UNITED KINGDOMTel: +44 20 7240 2881 • Fax: +44 20 7240 6637Email: [email protected] — MumbaiWestern Australian Trade Offi ce93 Jolly Maker Chambers No 29th fl oor, Nariman Point • MUMBAI 400 021 INDIATel: +91 22 5630 3979/74/78 • Fax: +91 22 5630 3977Email: [email protected] — ChennaiWestern Australian Trade Offi ce - Advisory Offi ce 1 Doshi Regency • 876 Poonamallee High Road Kilpauk • Chennai 600 084 • INDIA Tel: +91 44 2640 0407 • Fax: +91 44 2643 0064Email: [email protected] Indonesia — JakartaWestern Australia Trade Offi ce JI H R Rasuna Said Kav C15 - 16, Kuningan Jakarta 12940 • INDONESIA Tel: +62 21 2550 5331 • Fax: +62 21 522 7103Email: [email protected] Indonesia — SurabayaWestern Australian Trade Offi ceGraha Pena 17th fl oor • Jalan Ahmad Yani 88Surabaya 60234 INDONESIATel: +62 31 829 9979 • Fax: +62 31 829 9975Email: [email protected] — TokyoGovernment of Western Australia, Tokyo Offi ce13th fl oor, Fukoku Seimei Building2-2-2 Uchisaiwai-cho Chyoda • TOKYO 100-0011 JAPANTel: +81 3 5157 8281 • Fax: +81 3 5157 8286Email: [email protected] — KobeWestern Australian Government Offi ce6th fl oor, Golden Sun Building • 3-6 Nakayamate-dori4-Chome Chuo-Ku • KOBE 650-0004 JAPANTel: +81 78 242 7705 • Fax: +81 78 242 7707Email: [email protected] — Kuala LumparWestern Australian Trade Offi ce4th fl oor, UBN Tower • 10 Jalan P RamleeKUALA LUMPUR 50250 MALAYSIATel: +60 3 2031 8175/6 • Fax: +60 3 2031 8177Email: [email protected] East — DubaiWestern Australian Trade Offi ce • Emarat AtriumPO Box 58007 • Dubai • UNITED ARAB EMIRATESTel: +971 4 343 3226 • Fax: +971 4 343 3238E-mail: [email protected]’s Republic of China — ShanghaiWestern Australian Trade & Investment PromotionShanghai Representative Offi ce • Room 2208, CITIC Square1168 Nanjing Road West • Shanghai 200041PEOPLE’S REPUBLIC OF CHINATel: +86 21 5292 5899 • Fax: +86 21 5292 5889Email: [email protected]’s Republic of China — HangzhouWestern Australian Trade & Investment Promotion Hangzhou Representative Offi ce Room 910 • World Trade Offi ce Plaza Zhejiang World Trade Centre15 Shuguang Road • Hangzhou 310007 PEOPLES REPUBLIC OF CHINA Tel: +86 571 8795 0296 • Fax: +86 571 8795 0295 Email: [email protected] Korea — SeoulMr Young Chan Yu, Regional DirectorWestern Australian Trade & Investment Offi ce11th Floor, Kyobo Building1 Jongro 1-Ga, Jongro-Gu SeoulTel: +82 2 722 1217 • Fax: +82 2 722 1218Email: [email protected] — TaipeiWA Business Development ManagerAustralian Commerce & Industry Offi ceSuite 2606, International Trade Building#333 Keelung Road Section 1 • TAIPEI 110 TAIWANTel: +886 2 8780 9118 ext 216 • Fax: +886 2 2757 6707Email: nicholas.mckay@austrade,gov.auThailand — BangkokWA Business Development ManagerAustralian Trade Commission • Australian Embassy37 South Sathorn Road • BANGKOK 10120 • THAILANDTel: +662 287 2680 Ext 3307 • Fax: +662 287 2589E-mail: [email protected]

Jim Limerick

Welcome to the latest issue of Prospect magazine, highlighting some of the exciting developments occurring in the Western Australian resources industry.

This edition features the fi rst Prospect interview with State Development Minister Alan Carpenter since he assumed the portfolio in March.

It also highlights the Golden Gecko Awards for Environmental Excellence in the Western Australian Resources Sector. These awards are made annually by the Department of Industry and Resources to companies that demonstrate leadership in environmental performance. Congratulations go to BP Refi nery Kwinana and to Wesfarmers Premier Coal who took out the Golden Gecko Awards for 2005. Minister Alan Carpenter presented the companies with their awards for initiatives going well beyond regulatory compliance.

Elsewhere in this issue we highlight the impact of steadily increasing demand for iron ore, particularly from China, that has spurred increases in the world iron ore price and is seeing new projects being committed and new life being breathed into older ones.

The edition looks at one of Australia’s most historic iron ore mines, Aztec

Resources’ project at Koolan Island where plans are being put in place for the mine to be back in production by the end of next year.

The strong growth in the market also underpins other developments by companies including Mount Gibson Iron and Murchison Metals.

BHP Billiton’s Ravensthorpe nickel project is also moving ahead with extensive work going on to develop community infrastructure in the Ravensthorpe/Hopetoun district to support the development.

The fl ow-on effect of the growth in the resources sector is refl ected in the success of many other businesses associated with the sector. Some of these are highlighted in the summary of resource-based companies among the fi nalists in this year’s Western Australian Industry and Export Awards.

This edition also refl ects on the end of an era for a Western Australian resources icon, with the recent acquisition of WMC Resources by BHP Billiton. WMC, which was part of the mining scene in the State from 1933 and was one of the world’s leading gold miners, emerged as a world-class nickel producer after its discovery of the Kambalda nickel fi eld in the 1960s.

Prospect Western Australian Prospect magazine is published quarterly by the Western Australian Government’s Department of Industry and Resources (DoIR) and Ray Burns Media.

Editorial management: Mark Dixon, DoIR Communications & Marketing Division. Tel: (08) 9222 3895 • Fax: (08) 9222 3069

Advertising management: Ray Burns Media, PO Box 1230, South Perth Western Australia 6951 Tel: (08) 9227 6688 • Mobile: 0408 474 328 Email: [email protected]

Prospect has been compiled in good faith by the Department of Industry and Resources from information and data gathered in the course of the magazine’s production. Opinions expressed in Prospect are those of the authors and not necessarily those of the Department of Industry and Resources. No person or organisation should act on the basis of any matter contained in this publication without considering, and if necessary taking, appropriate professional advice from other sources. The Department of Industry and Resources, its employees and contracted personnel undertake no responsibility to any person or organisation in respect of this publication.

Front cover:

Wesfarmers Premier Coal won a Golden Gecko Award for Environmental Excellence, see page 5 for further details.

UWA student monitoring instrumentation at Wesfarmers Premier Coal rehabilitation site, Lake Kepwari (Western 5B mine lake).

Department ofIndustry and Resources

www.doir.wa.gov.au

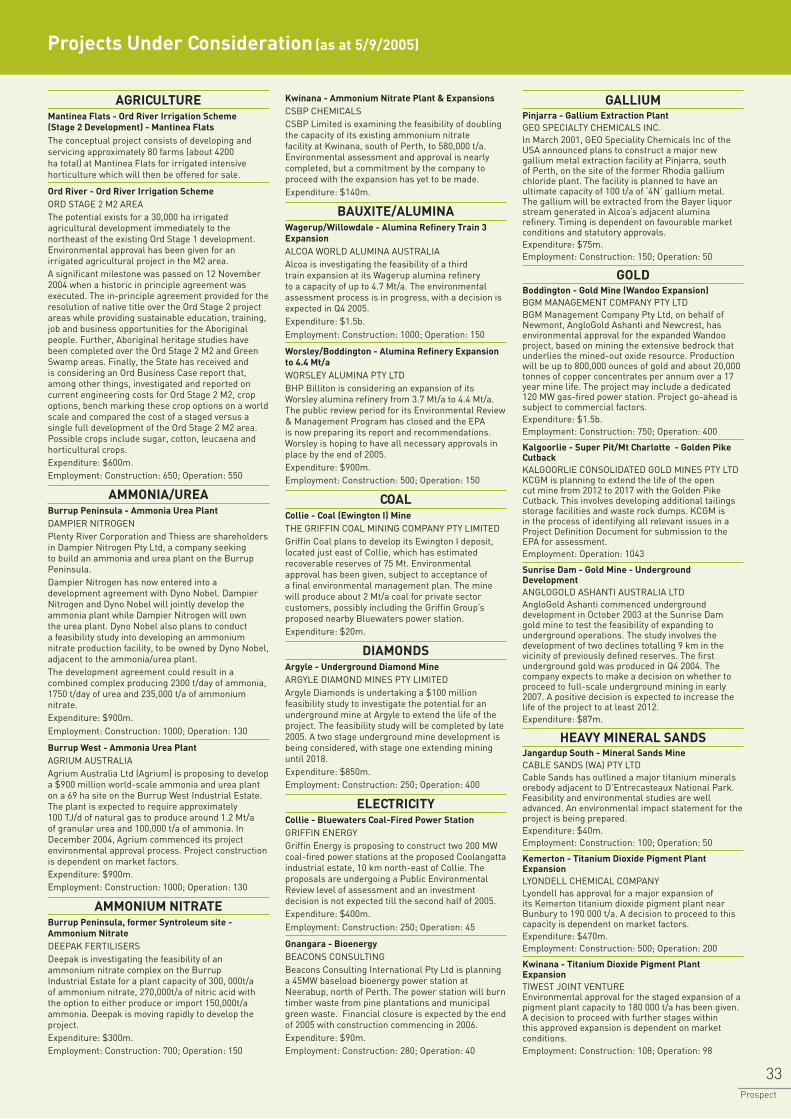

2 Koolan comes back to life

4 Yes Minister... it’s very exciting

5 Golden Gecko recipients set high environmental benchmark

6 Chinese markets embrace juniors

8 World-class Ravensthorpe takes shape

10 Resource-based companies vie for 2005 Industry and Export Awards

12 Kambalda end of an era, new beginning

17 Rock art study

18 MERIWA Means more for your money

20 Petroleum Open Day Conference

36 Resource Map

Koolan Island, in Yampi Sound in the far north of Western Australia

Man of iron: Aztec chairman Ian Burston at the Koolan Island redevelopment.

Koolan comes back to life

One of Australia’s most historic, and highest grade, iron ore mines should be back in production by the end of next year in a A$108 million development.

Owner Aztec Resources has given approval for the redevelopment of Koolan Island, in Yampi Sound in the far north of Western Australia, subject to the usual approval processes and fi nalisation of offtake contracts.

Aztec, which is led by Australian iron ore and mining doyen Ian Burston, said the mine should produce an operating cash surplus of A$583 million, on an EBITDA* basis, through generating total revenues of A$1.4 billion over the proposed nine year life of the operation.

Mr Burston said the company’s bankable feasibility study on the operation had shown Aztec should be able to sustain a fi nancially attractive mining project supplying about four million tonnes a year when in full production.

This year, Aztec is going ahead with several major infrastructure projects to support the development, including detailed engineering design of the jetty shiploader, crushing plant and ancillary work.

Koolan, which is about 130 km north-west of Derby, was previously worked by BHP between 1965 and 1993, producing 68 million tonnes of iron ore. Aztec acquired sole control of the island in 2000 and began drilling in February 2004.

The enticement of the deposits is the high grade.

Koolan is based on three main deposits, Main Pit, Eastern-Barramundi and Mullet-Acacia. In total, through measured, indicated and inferred resources there are 47 million tonnes at 64.7 per cent iron.

In particular, Main has a total of 32.9 million tonnes at 66.3 per cent iron. Infi ll drilling at the site on the inferred resources component has indicated the

continuity, width and grade of the high- grade resource.

Financial modelling of the project is based on a mix of 70 per cent fi nes and the remainder lump ore and Aztec has calculated a fi nancial internal rate of return of 39.7 per cent.

Mr Burston said the company had also committed to a high-grade accommodation camp. About 150 people are expected to be employed on site, on a fl y in-fl y out basis.

“This has been a pretty successful bankable feasibility study,” he said.“We are certainly on track to ship the fi rst iron ore from Koolan Island in late 2006.”

*EBITDA: Earnings before interest, tax, depreciation and amortisation.

Aztec chairman Ian Burston has more than 30 years experience in the resources industry.

He holds a Bachelor of Engineering degree from Melbourne University and a Diploma in Aeronautical Engineering from Royal Melbourne Institute of Technology. He has completed the Insead Management Paris and the Harvard Advanced Management Program in Boston. Mr Burston was awarded the Western Australian Citizen of the Year (category of Industry and Commerce) in 1992, and Order of Australia (General Division) in 1993 and an Honorary Doctor of Science (Curtin University) in 1995.

His career includes former positions as managing director of Portman, managing director and chief executive of Aurora Gold, chief executive offi cer of Kalgoorlie Consolidated Gold Mines; vice president – WA Business Development of CRA, managing director of Hamersley Iron. He was a non-executive director of the Esperance Port Authority for 10 years and is currently a non-executive chairman of Broome Port Authority and Imdex Ltd and a non-executive director of Mincor Resources and AVIVA Corporation.

In April 2001, Ian was one of 11 Australians taken hostage by pro-Chechen rebels while attending a mining

conference in Istanbul, Turkey. Dragged from his bedroom at gunpoint during the night, he and the others were held hostage in the hotel foyer by a dozen rebels wielding AK47 automatic rifl es. The hostages were released 18 hours later without incident.

Ian Burston

By MARK DIXON

3Prospect

Western Australia must focus on capitalising on the favourable environment created by the resources boom to ensure long-term growth continued in the State.

That is the goal for the new Minister for State Development and Energy, Alan Carpenter.

In his fi rst interview with Prospect magazine since assuming the portfolio in March, Mr Carpenter said Western Australia’s high economic growth rate, at 6 per cent and twice that of the national average, allowed the State to play a strong role in supporting further major resource development.

“We are pulling Australia along,” he said.

“I am very lucky to be in this portfolio right now.

“(But) it is important for us to create the pre-position to allow further growth.”

Energy supplies, dwindling exploration and the skills shortage were all issues facing the Government.

However on the positive side, apart from Western Australia’s massive resource base and proximity to dynamic markets, there were several features which set the State apart.

They included Western Australia’s expertise in safety, environmental management, technical developments, the legal system and Government management itself.

But, most importantly: “What is pulling us along is Chinese growth,” Mr Carpenter said. “Really the turbocharging comes from China. I have said that China in 10 years time will be a massive Singapore.”

Western Australia had massive resources, with very few people, over a huge area of land. China had limited supplies but immensely strong demand for resources, an enormous population and was showing it was willing to participate in resource developments overseas.

“It is like a hand and a glove,” Mr Carpenter said. He was particularly keen to see Chinese direct equity participation in major State projects, which began with involvement in the Channar iron ore mine in the Pilbara.

Reversely, Western Australian technical expertise was readily available to back the major Chinese projects either under construction or consideration.

“But that does not mean we have all our eggs in the one basket,” Mr Carpenter said. Strong interest was continuing to be received from traditional trading partner Japan, as well as India and Korea.

India, for example, has been attracted to coal from Collie, in the State’s South West, which would be an export fi rst for the resource. To seal a long-term future for the potential export industry, the Government would need to look at ways to upgrade the Bunbury port.

Also on the port front, strong Chinese demand for Mid West iron ore, which has led to the development and proposed development of several new mines, had prompted a new discussion about the Oakajee port to complement the port of Geraldton.

Mr Carpenter said it was diffi cult for the State Government to have the burden of funding infrastructure on its own.

It was long overdue for the Federal Government to accept that in return for the 90 per cent level of royalties received from Western Australian resource projects Federal funds were required for necessary infrastructure. The major Ravensthorpe nickel project, which came close to stalling because of a lack of Federal fi nancial support for infrastructure, was a case in point.

Another issue which would require Federal intervention related to the dwindling exploration sector in Western Australia, particularly on the gold front.

Greenfi eld exploration was the lifeblood of the future health of the industry and was largely driven by more junior companies.

Mr Carpenter said Australia should follow in Canada’s footsteps, where a fl ow-through share scheme had given great stimulation to the exploration sector.

Under the scheme, put simply, money invested in exploration became tax deductible, which has generated a great deal of market interest in the greenfi elds juniors and permitted the raising of substantial amounts of capital.

It is understood the Federal Resources Minister, Ian Macfarlane, was supportive of the concept, but it was quashed by Federal Cabinet.

“It is policy for us (the Western Australian Government) and we are still pursuing it,” Mr Carpenter said.

Prospect

4

Minister for State Development and Energy: Alan Carpenter MLA

Yes Minister… it’s very exciting

Prospec

4ct

Two companies received the top awards in this year’s Golden Gecko Awards for Environmental Excellence organised by Western Australia’s Department of Industry and Resources.

State Development Minister Alan Carpenter presented the awards to BP Refi nery Kwinana and Wesfarmers Premier Coal for their commitment to environmental excellence.

He also presented Certifi cates of Merit to BHP Billiton and URS Australia, and Woodside Energy.

Mr Carpenter applauded BP Refi nery Kwinana on its Golden Gecko Award for the company’s $9 million ‘Reducing Particulate Emissions’ project.

“This project heralds the fi rst usage of a fi lter on a residue cracker anywhere in the world. The project has signifi cant environmental benefi ts in terms of reduced air emissions, improving aesthetics and reducing metal loadings on the environment,” Mr Carpenter said.

He said sustainability planning by Wesfarmers Premier Coal, while improving environmental management, had seen that company develop innovative community-based programs deemed worthy of receiving a Golden Gecko.

“Former coal mines in the Collie area have been converted into valuable community assets including a recreation and conservation lake, a driver training and motor sports complex, and a freshwater aquaculture precinct,” he said.

Woodside Energy’s Certifi cate of Merit recognised the company’s Trunkline System Expansion Project (TSEP) which involved the construction of a new Trunkline Onshore Terminal at its onshore gas plant on the Burrup Peninsula and the installation of a trunkline from an interfi eld line between the Goodwyn A and North Rankin platforms with minimal environmental impact.

BHP Billiton and URS Australia received a Certifi cate of Merit for a joint initiative

to conduct a site selection pre-feasibility study into the possible development of a land-based liquefi ed natural gas plant on the Pilbara coast of Western Australia.

“These projects go well beyond regulatory compliance and set new industry standards,” Mr Carpenter said.

He said it was pleasing that the State’s major resources companies remained committed to achieving environmental excellence despite enormous production and supply pressures to fuel global commodity demands driven primarily by China’s economic expansion.

The commitment of WA’s resources companies to maintaining the highest standards is not new with Woodside having received Golden Gecko Awards in 1993 and 2001, and BHP Billiton in 1993, 1995, 1997 and 2004. Wesfarmers Premier Coal also received a Certifi cate of Merit in 2003, as did BHP Billiton in 1992, and Woodside in 2002, 2003 and 2004.

“Environmental regulation within the resource sector refl ects increasing community concerns over the impact of resource extraction on the environment, with expectations of accountability, transparency and environmental performance beyond bare minimum compliance,” Mr Carpenter said.

“An important part of environmental regulation is the State Government’s encouragement of practices and standards beyond compliance through public recognition of outstanding excellence in environmental management with the Golden Gecko Awards.”

He said this approach also refl ected a shift in focus on regulatory compliance towards that of encouraging best practice environmental management through increased liaison with industry and stakeholders.

The Golden Gecko Awards, which are in their 14th year, are the highest environmental accolades achievable in the Western Australian mineral and petroleum industries. More information on the awards can be found at www.doir.wa.gov.au/goldengecko. 5

Prospect

Golden Gecko recipients set high environmental benchmark

Alan Carpenter presenting the Golden Gecko award to Michael Glenny of BP Refi nery Kwinana

Wesfarmers Premier Coal: A former coal mine converted to a recreation and conservation lake

Alan Carpenter presenting the Golden Gecko award toPeter Ashton and Patrick Warrand of Wesfarmers Premier Coal

BP Refi nery Kwinana: World-fi rst usage of a fi lter in a residue cracker unit

Prospect

6

Continuing growth in the Chinese market has prompted many new resources developments in Western Australia.

Underpinned by strong demand and the willingness of the Chinese Government to sign long-term contracts, several projects which have been waiting in the wings are now coming on stream.

Those projects include iron ore, mineral sands and oil and gas.

In one example, strong iron ore demand from China, with a 72 per cent increase

in global prices, has seen Murchison Metals commit to a 1 million tonne a year export operation through the port of Geraldton, 400 km to the north of Perth.

Murchison said it had iron ore orders offered by the Chinese steel mills in excess of the 1 Mt/a business plan and was negotiating for long-term (up to 25 years) shipment of 10-15 million tonnes a year.

Managing director Robert Vagnoni said the Jack Hills deposit, which is the focus of the fi rst stage of development, was a high-grade resource which yielded a product in strong demand in China.

“They also like WA producers because of the record of reliability and quality,” he said.

“It is Chinese demand which is driving the development of Jack Hills.”

The company’s strategy was to get started quickly with stage one at a low capital cost of about A$15 million before moving to stage two by 2009. Road trains will truck the ore 200 km to Cue then, with a driver change, a further 300 km to Geraldton. It has been estimated there will be 26 trips per day (or one every 55 minutes).

The recently upgraded Geraldton port can handle the 35-55,000 tonne Handysize vessels and the 70,000 tonne capacity Panamax ships, which are ideal for shallow-draft ports in China.

Also looking to export iron ore through Geraldton in another new development is Midwest Corporation which plans to kickstart its long-term project aspirations with a 1 million tonne a year export operation from its Koolanooka and Blue Hills projects.

The company’s executive director, Jyn Sim Baker, said the direct shipping operation would provide early cashfl ow while other bigger projects such as the A$850 million Koolanooka pellet project were developed. The direct shipping product is graded 58.2 per cent iron (Fe), while the pellet plant is intended to benefi ciate the lower grade magnetite ores (about 32 per cent Fe) to produce 4.5 Mt/a of concentrates or pellets.

Mount Gibson Iron has developed its Tallering Peak hematite mine, 170 km from Geraldton, which is expected to export 2 Mt to China this year, rising to 3 Mt from next year until 2010.

The company then intends to focus on the development of an inferred resource of more than 200 Mt of magnetite, with a further 1 billion tonnes possibly waiting in the wings.

In the State’s north, at Koolan Island, Aztec Resources is looking to fi nalise long-term contracts with three Chinese and two Japanese customers to develop an export operation of about 4 Mt/a, with the fi rst shipment expected to leave in the middle of next year.

New fl oat Western Nickel has identifi ed the Chinese market as a crucial driver in the development of its Highway and Supply Well nickel projects, near Port Hedland.

The company said that China had shown rapid growth in demand for nickel, increasing on an annual average of 17.3 per cent from 1996-2003. “Our forecast growth rate of 5.8 per cent in this light, looks very cautious indeed, but even at this rate of growth it places extreme pressures on global nickel supply,” a company spokesman said.

Chinese markets embrace Juniors

Great Wall of China

By MARK DIXON

Skilled Migration:DIMIA’s Response

n conjunction with seminars and expos currently underway throughout Australia, including Perth and the regions, DIMIA is running a series of

“Australia Need Skills Expos” overseas to enable Australian employers to meet skilled people who are interested in migrating to Australia. The fi rst of these will be held in London (27 -29 September 2005), Amsterdam (3-4 October 2005), Berlin (6-7 October 2005), Chennai (11-13 October 2005). Each of the above events have 30-40 booths for hire. If you are interested inparticipating or being represented in these international expos email [email protected]

ADVERTISMENT

Prospect

8

World-class Ravensthorpe takes shapeOne of the world’s biggest greenfi eld nickel developments has reached major milestones in its quest to be in production by mid 2007.

The A$1.8 billion Ravensthorpe nickel project, owned by BHP Billiton, has to date awarded contracts worth A$900 million, of which 63 per cent is estimated to be spent in Western Australia.

About A$34 million is forecast to be spent in the south east coastal region, which hosts the mine and overall, the project is estimated to be 75 per cent Australian content.

The scale of the project is demonstrated through the volume of infrastructure necessary to support the planned 25-year minelife.

The Department of Industry and Resources (DoIR) has been co-ordinating the delivery of community-based infrastructure with State Government agencies and the shires of Esperance of Ravensthorpe.

The massive upgrade of the Ravensthorpe/Hopetoun district can be shown by the need to construct a new primary school in Hopetoun, middle school facilities in Ravensthorpe, a community services centre (which includes banking, health and licensing facilities) in Hopetoun and upgrading of roads.

Additionally, the Ravensthorpe nickel operation has bought 36 land lots in Hopetoun to build houses for its employees. Further land will be released by LandCorp over the next two years.

The Ravensthorpe Shire was also responsible for the construction of the A$5 million airport which now services the project. The shire is also upgrading and sealing 50 km of road between Hopetoun and Ravensthorpe, a project costed at A$5.9 million.

Also on the road front, A$10.5 million has been pledged to upgrade parts of the South Coast Highway, with the bulk of the work beginning in January next year.

DoIR said the Ravensthorpe nickel project was progressing on schedule with engineering activities at full pace in Perth and the procurement of all major equipment, including autoclaves, tanks and pressure vessels, virtually complete. More than 100 supply and construction contracts have been let.

A BHP Billiton spokesman said 500 contractors’ workers were currently on site, a number which is steadily growing. There will be signifi cant build up in the workforce over the next three months as large steel tank erection and construction of utilities, including the acid plant and power plant, accelerates.

The total construction workforce is estimated at 1200, while 300 direct permanent full-time jobs will be generated.

Ravensthorpe is a laterite nickel deposit, with the ore being treated through a hydrometallurgical process plant that incorporates atmospheric leaching, with the goal to produce up to 50,000 tonnes a year of contained nickel and 1400 tonnes of contained cobalt in an intermediate concentrate product called mixed hydroxide product (or MHP).

It is based on three nickel orebodies, mined by open cut. The orebodies, which were named by original owner Comet Resources, are Halleys, Hale-Bopp and Shoemaker-Levy and contain a proven reserve of 125.3 milliion tonnes of 0.73 per cent nickel and 0.026 per cent cobalt. There is also a probable reserve of 137.9 per cent Mt at 0.57 per cent nickel and 0.026 per cent cobalt.

The MHP will be shipped through the port of Esperance, 155 km from the mine, to BHP Billiton’s Yabulu refi nery in Queensland. Esperance, better known in Western Australia as a holiday destination, currently exports iron ore and nickel concentrates, but the Ravensthorpe Project will involve a quantum leap for the port.

In addition to exporting the MHP, about 500,000 tonnes of formed sulphur will be imported from overseas and 40,000 tonnes a year of magnesia from Queensland.

‘The project represents a massive upgrade for the district’

The port of Esperance will be used to ship the Ravensthorpe product

EIGHT resources related companies have been selected as fi nalists for this year’s prestigious Western Australian Industry and Export Awards.

Competing for their various categories at the 2005 awards are Gold Corporation (Marketing and Design Excellence Award, Large Advanced Manufacturer Export Award and Minerals and Energy Export Award), Neptune Marine Services (Innovation Excellence Award), Tyco Water and Mobilarm (Emerging Exporter Award), MetroCount and Metech (Information and Communications Export Award), Rio Tinto Iron Ore (Minerals and Energy Export Award), Risktec Australasia (Services Export Award and Education Export Award) M&O Group (Services Export Award).

Now in their 17th year, the awards have fi rmly established themselves as WA’s

most prestigious business awards, with the gala presentation evening to be held at the Hyatt Regency on Friday October 14.

Last year saw a record number of entries which culminated in three Western Australian companies taking out national export awards, namely Mt Romance, Hamersley Iron and Australian Gold Reagents.

Premier Geoff Gallop said the list of fi nalists and winners in these awards provide an impressive showcase of WA businesses, highlighting the vital contribution they make to the local economy through job creation and increased prosperity in the community.

Dr Gallop said the awards recognise the importance of exports to the economic development of the State. In fact, almost a third of our Gross State Product is generated by exports - more than any other State.

He said the State already has a strong export culture, with exports from Western Australia in 2004 totalling $35 billion and signifi cantly contributing to the creation of more than 52,500 new jobs last year.

Export category winners automatically compete as fi nalists in the Australian Export Awards to be held at a gala dinner and awards presentation in Sydney in December.

The 2005 Awards, administered by the Department of Industry and Resources (DoIR) are sponsored by The West Australian newspaper, Austal, Austrade, BankWest, Ernst & Young, Fremantle Ports and Export Finance and Insurance Corporation (EFIC), and endorsed by the Chamber of Commerce and Industry of WA, UnionsWA and the Australian Institute of Export (WA) Ltd.

For more information visit www.doir.wa.gov.au/awards

Prospect

10

Resources-based companies vie for 2005 Industry and Export Awards

Gold CorporationGold Corporation, operator of the historic Perth Mint, is dedicated to adding value to Australia’s precious metals before export, and generating consumer interest in, and demand for, precious metals worldwide.

Since its creation in 1987, the corporation has sold more than 14 million coins, representing some 545 tonnes of Australian precious metals, and contributed an estimated $2.7 billion in foreign earnings to Western Australia.

The Perth Mint has also added value to many tonnes of precious metals in the production of coin blanks and coins produced on behalf of overseas issuing authorities.

The corporation has a world presence, with a network of agents located in Hong Kong, Dubai, Japan and Germany, and authorised distributors in the United States, China, Russia, the Ukraine, Japan, Europe, Asia, the Middle East, India, Indonesia, Singapore, the Solomon Islands and throughout Australia.

Gold Corporation also has a strong international reputation for innovative design, high-quality production, marketing excellence and dedicated customer service.

Neptune Marine ServicesNeptune Marine is commercialising the patented Neptune Dry Underwater Welding System that allows permanent in-situ weld repairs to be carried out underwater at a fraction of the cost of using conventional permanent repair methods. The technology has broad application in markets including shipping, oil and gas, infrastructure, defence and hazardous environments.

Proof of the technology was confi rmed through the generation of almost $1 million in revenues in the fi rst 12 months of operation and through the repeat business delivered to the Australian Navy.

After a successful fi rst year, which included the generation of initial export revenues, the company’s primary focus has expanded from building Australian revenues to building multiple revenue streams from south east Asia and the United Arab Emirates.

The potential to create multiple revenue streams out of Asia will result in rapid growth in revenues as a presence is established in each new country and will add to the value of the technology in the signifi cant markets in the northern hemisphere.

Tyco WaterTyco Water, the Kwinana-based steel water pipe manufacturer, recently secured its fi rst major export contract into the Middle East beating international competition to win a signifi cant contract worth $50 million.

Tyco Water’s Kwinana manufacturing facility was established in 1960 and is the only one of its type in Western Australia. A majority of the State’s water supplies fl ow through pipes produced at this plant, manufactured according to the patented design called Sintajoint.

Having spent more than $4 million since 2001 modernising and upgrading the plant to world’s best standards, Tyco Water, as well as servicing local and interstate demand, has now commenced looking to overseas markets, particularly the Middle East and China, to export their patented water pipeline system.

The company has been operating under various owners in Australia for more than 100 years. As Mephan Ferguson it was involved in the supply of pipes for the CY O’Connor Mundaring to Kalgoorlie pipeline, circa 1898.

Resources-based fi nalists

11Prospect

11Prospect

MobilarmMobilarm is a Western Australian-based electronics engineering company specialising in the design and development of intelligent monitoring systems.

The company has recently launched world wide an intelligent crew monitoring and man overboard alarm and tracking system known as MOBi-lert which has won awards in Australia and overseas for its uniqueness and life saving potential.

Although MOBi-lert was developed specifi cally for the commercial and leisure marine markets the technology behind it has been patented around the world. The company is currently working with several coastal patrol organisations to implement the MOBi-lert system into their vessels.

MOBi-lert provides a complete crew monitoring system to revolutionise safety at sea.

MetroCountMetroCount, with its headquarters in Hamilton Hill, offi ces in USA and UK, and global distribution networks, is the world leader in design and manufacture of portable traffi c monitoring equipment and software.

Exported to over 45 countries and with thousands of units in use world-wide, MetroCount’s very popular 5600 Series Vehicle Classifi er uses simple rubber pneumatic tube combined with sophisticated software to give traffi c and municipal engineers unmatched versatility with invaluable road statistics.

Now in the fi nal stages of production, the all-new 5700 Series further extends MetroCount’s lead, providing innovative traffi c survey solutions for medium to long-term studies.

Their latest software package, the industry-leading Traffi c Executive™ v3.1, revolutionises traffi c data gathering and reporting, with fi eld operating software and reports in many languages.

MetroCount’s clients include national and state road authorities, city and county municipalities, national parks, military bases and private traffi c engineering consultants and contractors.

MetechMetech is a technology solution provider to the exploration and mining industry based in Perth. The company currently has four offi ces: Perth, Brisbane, Calgary and Santiago. Metech UK will be operational in late 2005.

Two technologies form the platform for the solutions provided by the Metech Group; acQuire - A Geoscientifi c Data Management Solution and MineSight - A Geologic Modelling and Mine Planning System.

acQuire is developed by Metech and has been installed in a large number of operations and exploration sites worldwide. acQuire is currently installed at 235 sites in 35 countries and the growth in all regions continues at a signifi cant rate.

A new division of the company, Metech Mining Solutions (MMS), has been established to optimise the solution providing model associated with MineSight. The MMS group provides solutions for a number of large operations including Mt Isa Mines (Xstrata Copper), Grasberg (PT Freeport) and Batu Higau (Newmont Gold).

Rio Tinto Iron OreRio Tinto Iron Ore (RTIO), a leading Australian exporter, representing one-quarter of the world’s seaborne traded iron ore supply, is seeking recognition for its efforts to grow and improve an already excellent business.

The iron ore industry is expanding quickly, and RTIO has the capability to bring on further resources in the fastest and most cost effective manner. RTIO holds strategic advantage through long-term relationships and a range of joint ventures with steel and trading industry partners.

It has developed an internal structure that ensures the Pilbara operations are managed in the most effi cient and fl exible manner, and that the business has a capability in expansion.

RTIO aims to be the developer of choice - with continued improvement across a range of health, safety, environment, community, heritage and native title measures. This future growth will ensure RTIO continues to deliver an outstanding economic and community benefi t to Western Australia.

Risktec AustralasiaIncident and emergency response professionals Risktec has continued to grow with the company now recognised as the premium global supplier of Emergency Management Training in the oil and gas sector by many major operating companies.

This recognition has been achieved through the commitment of the company to the customisation of training packages designed specifi cally for each individual client.

Ongoing technological developments like CASS (Client Asset Simulation System), and the ability to superimpose actual incidents onto photographs of the clients’ facilities, enhances the reality and effectiveness of the training.

Shortly after inception, the Risktec Australasia management team committed to the development of a world-class training facility in Jakarta, Indonesia. This commitment to clients and the countries in which they operate is one of the many reasons for the company’s success.

Based around a philosophy of fulltime representation and facilities, Risktec has opened two additional training and simulation centres (Baku and Singapore) during 2004-05 with a further two planned for 05-06.

M&O GroupM&O Group is a global training specialist, with a focus on providing offshore safety and emergency training for the oil and gas industry since 1997. The company was formed by ex-SAS offi cer Rick Parish, with initial start up capital of A$10,000.

Today the company is the second largest provider of training in the oil and gas industry worldwide with annual sales in excess of $25 million.

With training centres and offi ces in nine locations, across fi ve continents, the company has worked with most major oil companies and contractors, helping them make the offshore world a safer place to work. Their target market is emerging oil and gas nations such as West Africa, South America, Middle East and the Caspian Region.

Courses are competency based, using a combination of theory and practical training, to develop the skills and attitudes required to work safely and respond appropriately to many of the emergencies that can occur offshore.

005

W

ES TRALIA

ND

USTRY & E PORT AW

AR

005

W

ES TRALIA

ND

USTRY & E PORT AW

AR

005

W

ES TRALIA

ND

USTRY & E PORT AW

AR

005

W

EST STRALIA

IND

USTRY & EXPORT AW

AR

Prospect

12

Kambalda end of an era, new beginning

WMC Resources, the resources’ icon which played a pivotal role in the State’s development over the past 40 years, has disappeared as a separate corporate entity.

Western Mining Corporation entered the gold mining industry in 1933 and for many decades the group produced more gold than any other company.

Its gold mines included St Ives, Hill 50, the Agnew complex, Lancefi eld and the Central Norseman venture, all in Western Australia. Overseas, it mined gold in Nevada and Brazil.

WMC also played a major role in establishing an alumina industry in Western Australia, one of the world’s biggest, and had a brief fl ing with mineral sands production.

But the world’s third biggest nickel producer came from humble beginnings in that sector.

The impetus for its meteoric rise lies with its part in the one of the greatest mining booms in the nation’s history – the nickel rush of the 1960s.

Before the discovery in 1964 of the Kambalda nickel deposits, WMC had total assets of little more than $15 million, shareholders’ equity of only about $9

million and a net profi t for the year of less than $1.4 million....even allowing for the values of the day, a modest result.

The market value of the company multiplied many times within a year of the fi rst major intersections at Kambalda.

It quickly became a dominant force in the world nickel industry, and went on to develop Olympic Dam, a glittering prize in the recent takeover by BHP Billiton.

The Olympic Dam structure holds a third of the world’s uranium reserves and will provide a fi fth of global production within a decade. It will also be one of the world’s biggest copper producers.

WMC developed great exploration skills as it developed projects in half a dozen minerals - it has been a major producer or had signifi cant interests in gold, alumina and aluminium, uranium, copper, petroleum and natural gas, with operations in several countries.

On what was an historic day for the Australian mining industry on 28 January 1966 massive sulphides were intersected at Kambalda, with 8.3 per cent nickel.

The so-called Poseidon boom dominated share markets at the time, but it was WMC which laid the fi rm foundations of the Australian nickel industry.

In his book on Kambalda, Jeff Gresham points out that there was a considerable amount of luck in that fi rst discovery.

That fi rst historic hole, KD1, went through a barren ultramafi c-basalt contact. If the drilling had been stopped less than 15 metres past the initial contact, a decision that could have been justifi ed on the basis of the surface geology, the rich nickel intersection would have been missed.

The ultramafi c-basalt contact had been made at 130 metres, and the sulphides were not discovered until 145.7 and 184.4 metres, showing how fl ukish some of the world’s major discoveries can be.

The second and third holes in the program were abandoned for various reasons. With only three holes planned, exploration work could well have been prematurely curtailed and the discovery of Kambalda would not have taken place, at least not then.

This discovery, which was to bring immense benefi ts to Australia and particularly Western Australia, was announced quietly by WMC on 21 February 1966:

“The directors announced that in exploring the Kambalda area 30 miles south of Kalgoorlie for nickel, one drill hole has intersected signifi cant nickel sulphide mineralisation. Additional drill holes are being put down in the area but it will be some time before any evaluation of the discovery can be made.”

By June 1966, site preparation for the fi rst shaft began, and the fi rst nickel concentrate was produced less than 18 months after the drilling of the fi rst exploration hole.

First shipments of concentrates left Esperance for Japan in October 1967, about three weeks after the Kambalda project was offi cially opened by the then Premier David (later Sir David) Brand.

The knowledge and understanding WMC gained in developing the many nickel mines at Kambalda gave the company a head start in the discovery of nickel deposits in the Eastern Goldfi elds.

Ka

Nickel

13Prospect

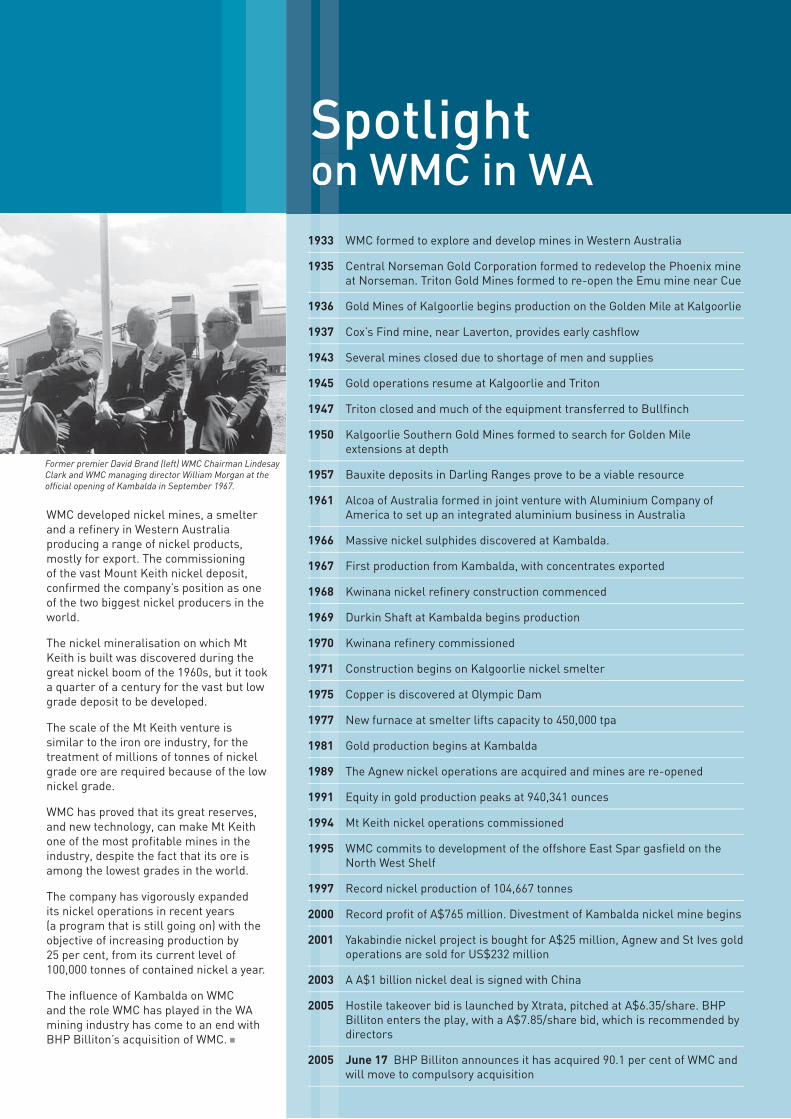

Spotlight on WMC in WASon1933 WMC formed to explore and develop mines in Western Australia

1935 Central Norseman Gold Corporation formed to redevelop the Phoenix mine at Norseman. Triton Gold Mines formed to re-open the Emu mine near Cue

1936 Gold Mines of Kalgoorlie begins production on the Golden Mile at Kalgoorlie

1937 Cox’s Find mine, near Laverton, provides early cashfl ow

1943 Several mines closed due to shortage of men and supplies

1945 Gold operations resume at Kalgoorlie and Triton

1947 Triton closed and much of the equipment transferred to Bullfi nch

1950 Kalgoorlie Southern Gold Mines formed to search for Golden Mile extensions at depth

1957 Bauxite deposits in Darling Ranges prove to be a viable resource

1961 Alcoa of Australia formed in joint venture with Aluminium Company of America to set up an integrated aluminium business in Australia

1966 Massive nickel sulphides discovered at Kambalda.

1967 First production from Kambalda, with concentrates exported

1968 Kwinana nickel refi nery construction commenced

1969 Durkin Shaft at Kambalda begins production

1970 Kwinana refi nery commissioned

1971 Construction begins on Kalgoorlie nickel smelter

1975 Copper is discovered at Olympic Dam

1977 New furnace at smelter lifts capacity to 450,000 tpa

1981 Gold production begins at Kambalda

1989 The Agnew nickel operations are acquired and mines are re-opened

1991 Equity in gold production peaks at 940,341 ounces

1994 Mt Keith nickel operations commissioned

1995 WMC commits to development of the offshore East Spar gasfi eld on the North West Shelf

1997 Record nickel production of 104,667 tonnes

2000 Record profi t of A$765 million. Divestment of Kambalda nickel mine begins

2001 Yakabindie nickel project is bought for A$25 million, Agnew and St Ives gold operations are sold for US$232 million

2003 A A$1 billion nickel deal is signed with China

2005 Hostile takeover bid is launched by Xtrata, pitched at A$6.35/share. BHP Billiton enters the play, with a A$7.85/share bid, which is recommended by directors

2005 June 17 BHP Billiton announces it has acquired 90.1 per cent of WMC and will move to compulsory acquisition

WMC developed nickel mines, a smelter and a refi nery in Western Australia producing a range of nickel products, mostly for export. The commissioning of the vast Mount Keith nickel deposit, confi rmed the company’s position as one of the two biggest nickel producers in the world.

The nickel mineralisation on which Mt Keith is built was discovered during the great nickel boom of the 1960s, but it took a quarter of a century for the vast but low grade deposit to be developed.

The scale of the Mt Keith venture is similar to the iron ore industry, for the treatment of millions of tonnes of nickel grade ore are required because of the low nickel grade.

WMC has proved that its great reserves, and new technology, can make Mt Keith one of the most profi table mines in the industry, despite the fact that its ore is among the lowest grades in the world.

The company has vigorously expanded its nickel operations in recent years (a program that is still going on) with the objective of increasing production by 25 per cent, from its current level of 100,000 tonnes of contained nickel a year.

The infl uence of Kambalda on WMC and the role WMC has played in the WA mining industry has come to an end with BHP Billiton’s acquisition of WMC.

Former premier David Brand (left) WMC Chairman Lindesay Clark and WMC managing director William Morgan at the offi cial opening of Kambalda in September 1967.

Fresh view lifts nickel fi eld

Prospect

14

One name is synonymous with the development of WMC Resources…Arvi Parbo.

Sir Arvi was born in Estonia in 1926 and was educated there and in Germany before migrating to Australia in 1949.

He graduated with a Bachelor of Engineering from the University of Adelaide in 1956 and joined WMC the following year at the Bullfi nch gold mine in Western Australia.

After roles including underground

manager at Nevoria and deputy general

superintendent of Western Australia, Sir

Arvi was appointed general manager in

1968, then managing director in 1971.

In 1974 he became the chairman, a role

he fi lled until 1999. He was also the

chairman of Alcoa Australia from 1978

to 1996 and chairman of BHP from 1989

until1992.

Sir Arvi Parbo.

Fres

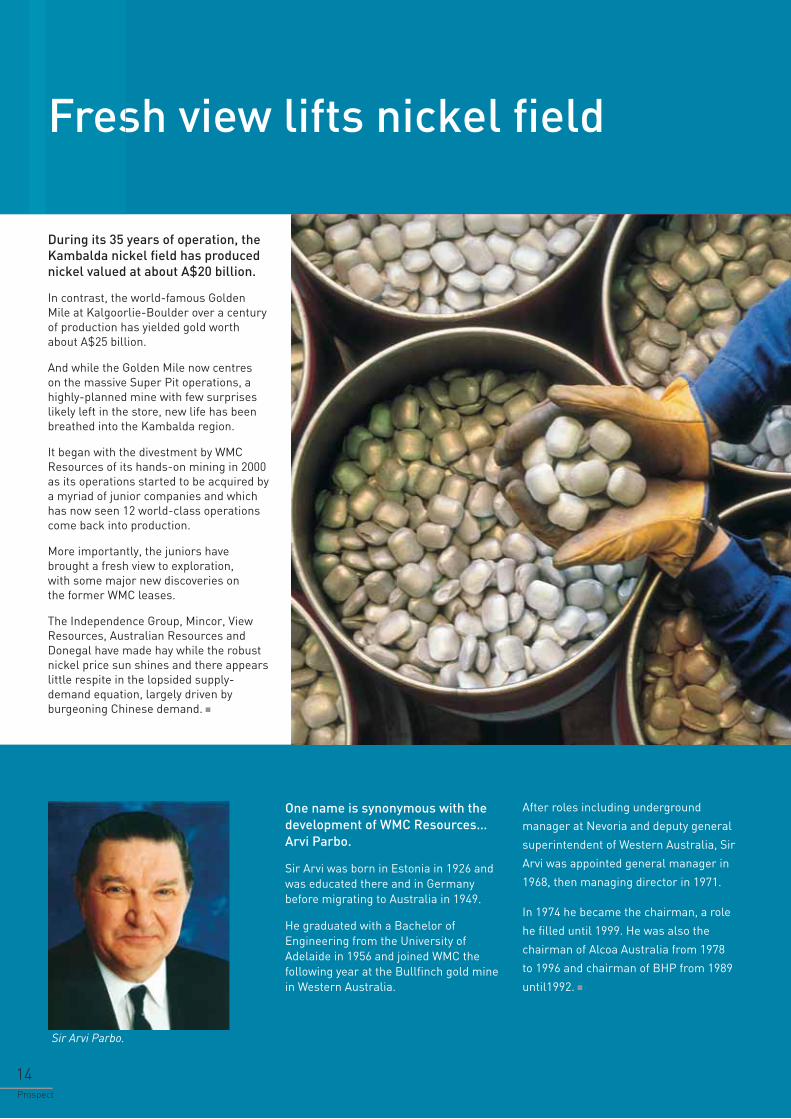

During its 35 years of operation, the Kambalda nickel fi eld has produced nickel valued at about A$20 billion.

In contrast, the world-famous Golden Mile at Kalgoorlie-Boulder over a century of production has yielded gold worth about A$25 billion.

And while the Golden Mile now centres on the massive Super Pit operations, a highly-planned mine with few surprises likely left in the store, new life has been breathed into the Kambalda region.

It began with the divestment by WMC Resources of its hands-on mining in 2000 as its operations started to be acquired by a myriad of junior companies and which has now seen 12 world-class operations come back into production.

More importantly, the juniors have brought a fresh view to exploration, with some major new discoveries on the former WMC leases.

The Independence Group, Mincor, View Resources, Australian Resources and Donegal have made hay while the robust nickel price sun shines and there appears little respite in the lopsided supply-demand equation, largely driven by burgeoning Chinese demand.

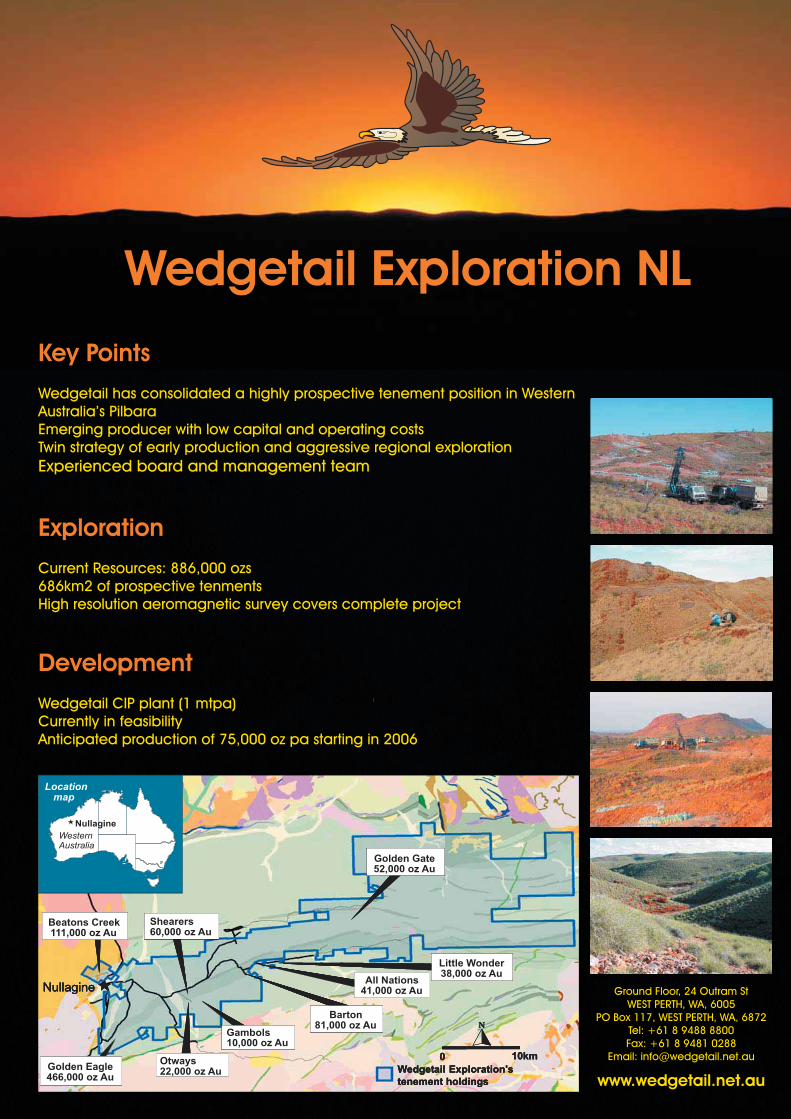

Wedgetail Exploration NL

Current Resources: 886,000 ozs

686km2 of prospective tenments

High resolution aeromagnetic survey covers complete project

Wedgetail has consolidated a highly prospective tenement position in Western

Australia’s Pilbara

Emerging producer with low capital and operating costs

Twin strategy of early production and aggressive regional exploration

Experienced board and management team

Wedgetail CIP plant (1 mtpa)

Currently in feasibility

Anticipated production of 75,000 oz pa starting in 2006

Ground Floor, 24 Outram St

WEST PERTH, WA, 6005

PO Box 117, WEST PERTH, WA, 6872

Tel: +61 8 9488 8800

Fax: +61 8 9481 0288

Email: [email protected]

Key Points

Exploration

Development

www.wedgetail.net.au

Nullagine

Western

Locationmap

0 10km

�

Wedgetail Exploration's

tenement holdings

Golden Eagle466,000 oz Au

All Nations41,000 oz Au

Little Wonder38,000 oz Au

Barton81,000 oz Au

Nullagine

Beatons Creek111,000 oz Au

Golden Gate52,000 oz Au

Shearers60,000 oz Au

Otways22,000 oz Au

Gambols10,000 oz Au

Australia

Nullagine

Western

Locationmap

0 10km

�

Wedgetail Exploration's

tenement holdings

Golden Eagle466,000 oz Au

All Nations41,000 oz Au

Little Wonder38,000 oz Au

Barton81,000 oz Au

Nullagine

Beatons Creek111,000 oz Au

Golden Gate52,000 oz Au

Shearers60,000 oz Au

Otways22,000 oz Au

Gambols10,000 oz Au

0 10km

�

Wedgetail Exploration's

tenement holdings

0 10km

�

Wedgetail Exploration's

tenement holdings

Golden Eagle466,000 oz Au

All Nations41,000 oz Au

Little Wonder38,000 oz Au

Barton81,000 oz Au

Nullagine

Beatons Creek111,000 oz Au

Golden Gate52,000 oz Au

Shearers60,000 oz Au

Otways22,000 oz Au

Gambols10,000 oz Au

Golden Eagle466,000 oz Au

All Nations41,000 oz AuAll Nations

41,000 oz Au

Little Wonder38,000 oz AuLittle Wonder38,000 oz Au

Barton81,000 oz Au

Barton81,000 oz Au

NullagineNullagine

Beatons Creek111,000 oz Au

Golden Gate52,000 oz AuGolden Gate52,000 oz Au

Shearers60,000 oz AuShearers60,000 oz Au

Otways22,000 oz AuOtways22,000 oz Au

Gambols10,000 oz AuGambols10,000 oz Au

Australia

Focused on developing Western Australia’s industry and resources

The Department does this by:

w delivering innovative value-added services to industry

w broadening the State’s economic base

w helping to create new jobs.

The Western Australian Government’s drive for responsible industrial development within the State is led by the Department of Industry and Resources.

The Department seeks to create jobs and broaden the State’s economic base, while at the same time providing care for the environment.

The Department assists in setting policy direction for responsible State development, and provides value-adding services to industry. These services include assistance to identify investment and business development opportunities, and help in working effectively with government.

The Department also provides advice through Western Australian offices, plus a network of overseas trade and investment offices in Europe, the Middle East, China, Japan, India, South Korea, Taiwan, Thailand, Malaysia and Indonesia.

www.doir.wa.gov.au

The Department of Industry and Resources assists the responsible development of the State for the benefit of all Western Australians.

A committee formed to monitor the effect of industrial emissions on the rock art on the Burrup Peninsula in Western Australia’s north-west has released its fi rst interim report.

The fi ndings from the intense scientifi c studies being undertaken show that the industrialised areas on the Burrup have considerably lower concentrations of emissions than cities in Australia.

The Chairman of the Burrup Rock Art Monitoring Management Committee, Associate Professor Frank Murray, said the committee had commissioned the CSIRO to carry out the studies for the monitoring program.

Their work was in two parts and covered the monitoring of air pollutants, microclimate and deposition, and their potential to cause changes in rock art.

He said eminent scientists in the United States and Europe had checked and validated the results of the studies before their release.

“To the best of our knowledge, this program is the most thorough scientifi c study of possible impacts on rock art ever undertaken in Australia,” Professor Murray said.

“We want to ensure at every stage of this work that the reports are of the highest quality and, as part of this, we sent the reports to the most eminent scientists in these fi elds in the US and Europe for scientifi c peer review.

“The international reviewers considered that this is the most intensive rock art monitoring program ever undertaken in Australia, and represents world-class research on weathering processes for rock art.”

He said the Division of Atmospheric Research, CSIRO, Melbourne, prepared the interim report on measurements of air quality on the Burrup Peninsula.

It showed that concentrations of nitrogen dioxide, sulphur dioxide, ammonia, nitric acid and hydrocarbons measured in the industrial part of the peninsula were considerably lower than concentrations measured in cities in Australia and around the world.

There were elevated levels of particulates (dust) in areas close to the major industrial sources of dust, but most areas of the Burrup Peninsula had levels of particulates typical of the whole Pilbara region.

Professor Murray said CSIRO Manufacturing and Infrastructure Technology, Melbourne, prepared the interim report on effects of air pollution on the rock art.

“The report states that the analyses needed to establish a baseline to assess future changes in the rock art have commenced,” he said.

“Tests to establish if there are changes to rock surfaces due to exposure to simulated extreme levels of air pollution

are also underway using highly advanced techniques developed for the study.”

Professor Murray said that for the fi rst time, the studies were starting to provide a complete set of scientifi c data on the effects of industrial emissions on rock art.

“The data will facilitate an informed and accurate discussion to ensure this community treasure is protected both now and into the future,” he said.

The Western Australian Government established the Burrup Rock Art Monitoring Management Committee to carry out the four-year rock art monitoring program. It includes experts in atmospheric science, archaeology, chemistry, land conservation and rock science from the WA Museum, the Chemistry Centre (WA), and the Departments of Environment, Indigenous Affairs, and Industry and Resources and indigenous and local government representatives.

The interim reports and future annual reports will be published on the Department of Industry and Resources website.

Once the studies and international peer assessment of the results are fi nished, the committee will produce a fi nal report for Government and the community, including recommendations for the preservation and conservation of the rock art.

17Prospect

Rock art Study… fi rst results released

g highor the

hat foere stof scierial em

an infon to en

ed

a

ly advancestudy.”

r the arting to

entifi c datamissions

ormed nsure this

Prospect

18

MERIWA Means More for your MoneyM

R

MER

IW

A recent allocation of $2.3 million in State Government funding to Curtin University’s Centre for High Defi nition Geophysics is another success story for the Minerals and Energy Research Institute of Western Australia (MERIWA).

What began as MERIWA project M363 ‘Feasibility of seismic methods for imaging gold deposits in Western Australia’ with initial support of $207,000 has evolved to attract 16 times that amount, including $1million from industry.

The funding will be provided over four years to develop new techniques for the collection, analysis, interpretation and application of new mineral exploration data.

This will allow seismic methodologies developed in the petrochemical industry to be applied to hard-rock and other mineral exploration targets, including gold.

MERIWA executive offi cer David Milton said the project and subsequent Centre of Excellence status emphasised the potential benefi ts that accrue from research grants coordinated through the institute.

The initial research project commenced in January 2004 and quickly engendered enthusiasm from participating mining companies. Within 15 months the skills of the research team had produced identifi able targets that were verifi ed by drilling.

It is also a developing technology that could pay huge dividends for the gold industry.

Western Australia has long been the powerhouse of gold production in Australia but there have been recent signs of declining production - despite high gold prices - and some despair about the predicted run-down of the industry over the next 10 years due to lack of exploration and discoveries.

The application of seismic methods has traditionally been a major exploration tool for the oil and gas industry, yet with minimal successful application to the hard rock minerals industry.

There were strong indications from experimental surveys carried out in the Eastern Goldfi elds in 2001 that structures could be defi ned at shallow enough depths to be of interest to the mining industry and that the images might be even more enlightening if subject to complex reprocessing techniques.

This gave rise to a proposal by Curtin University’s Professor Brian Evans and Dr Milovan Urosevic to develop the complex processing techniques for data to be acquired from several sites in the Eastern Goldfi elds.

With several major mining companies sponsoring the seismic data acquisition work on their leases, the researchers needed a co-ordinating sponsor. The ideal vehicle for this was MERIWA - a small State Government agency with a reputation for effective and effi cient administration of research funds.

“Maintaining the momentum in a successful project is vital and the combined efforts of the Curtin University Department of Exploration Geophysics and its sponsors have persuaded the State Government to ensure that the skills of the research team remain focussed on our mineral future,” Mr Milton said.

MERIWA is an independent State Government agency, partly funded by the Department of Industry and Resources.

Three seismic vibrator trucks working on project M363 in the Eastern Goldfi elds

• Bankable Feasibility Study

completed in December 2004,

with positive results.

• Estimated 20 year mine life

with revenue $A70 million

per annum.

• Project revenue dominated

by zircon, which is in short

supply and has an excellent

market outlook.

• Strong interest from European and East Asian consumers.

• Coburn is currently the third largest greenfields zircon

development project in the world.

• First production scheduled for late 2006.

Head office: Level 2, 33 Richardson Street,

West Perth Western Australia 6005

PO Box 1217, West Perth Western Australia 6872

Telephone: (08) 9226 3130 Facsimile: (08) 9226 3136

Email: [email protected]

ASX Code: GUN

Conference puts focus on petroleum

Prospect

20

More than 200 delegates took part in a one-day conference in Fremantle to discuss the latest developments in the petroleum industry in Western Australia.

The conference provided industry representatives with the opportunity to gather information on major developments and discuss future trends with industry peers.

Directions in petroleum regulation, project approvals, resource management regulations, amendments to petroleum legislation and the coming of age of the National Offshore Petroleum Safety Authority (NOPSA) were some of the topics covered.

Petroleum systems in frontier basins, native vegetation clearing for petroleum activities, the Petroleum Data Centre, land access – pressures and progress, and Commonwealth/State royalty issues were also discussed.

In addition to the presentations, an exhibition displayed current government initiatives and trends in the petroleum industry and provided delegates with an opportunity to network with key government stakeholders.

The Petroleum Open Day was organised by the Western Australian Department of Industry and Resources (DoIR).

“There have been major changes affecting the petroleum industry in the past year including the transition of the safety regulation function to the National Offshore Petroleum Safety Authority (NOPSA) and the WA Department of Consumer and Employment Protection,” DoIR’s Director of Petroleum and Royalties, Bill Tinapple said.

He said the NOPSA transition required amendments to the Petroleum Submerged Lands Act 1982, the Petroleum Act 1967 and the Petroleum Pipelines Act 1969.

“Another change was the transfer to DoIR of the delegation to administer provisions for the clearing of native vegetation (terrestrial and aquatic) under the Environmental Protection Act 1986 (EP Act) for mineral and petroleum activities,” Mr Tinapple said.

As of 1 July 2005 DoIR became responsible for assessing Native Vegetation Clearing Permit applications for the resources sector.

The release of fi ve onshore areas for petroleum exploration in WA was also announced at the conference. This included four blocks from the northern Canning Basin (L05-5, L05-6, L05-7, L05-8) and one block from the Offi cer Basin (L05-9).

“The Canning Basin’s four release areas have proven source rock potential and favourable reservoir development,” Mr Tinapple said.

“There is also good access with unsealed roads to the release areas and the Great Northern Highway lying to the south of the release areas connecting them with the port of Broome.”

L05-6 (4354 km2) is located entirely within the Fitzroy Trough, while L05-5 (3048km2) extends from the northern Fitzroy Trough into the southern Pender Terrace. Release areas L05-7 (2782 km2) and L05-8 (2451 km2) are situated on the Lennard Shelf adjacent to the north-eastern margin of the basin.

Release area L05-9 (17,591km2) is located on the northern Offi cer Basin margin adjacent to the South Australian border.

Mr Tinapple said numerous oil and gas shows had been encountered in the Offi cer Basin, including a gas show at Vines 1 in release area L05-9. Favourable reservoir, seal and source rock associations were present in the basin.

The acreage release is in keeping with the Government’s policy of sustainable development of Western Australia’s oil and gas resources.

There have been major changes affecting the petroleum industry in the past year

p.o. box 9117, floor 20, al attar business tower,

sheikh zayed road, dubai, uae

phone: +971 4 332 0007

fax: +971 4 332 0008

email: [email protected]

The driving force for your energy business

In association with

Prospect

22

@

Gunson Resources has reached fi nalisation on a A$128 million greenfi eld heavy mineral sands mine near Shark Bay, a zircon-driven development which has snared Chinese interest.

Gunson’s Coburn mine will be the third biggest zircon development in the world once in production. Based on the Amy deposit alone, it has a mine life of 20 years. Total revenue over that period is estimated at A$1.8 billion.

Gunson will initially mine the Amy deposit, which is 35 km long and up to 1.1 km wide. Amy is forecast to produce 30,000 tonnes of zircon in the fi rst year, rising to 60,000 tonnes a year from the third year. At a price of US$620 a tonne (zircon is currently trading at US$750/t).

Over the life of the mine, the feasibility study forcecasts a cash operating surplus of A$433 million with an internal rate of return of 19 per cent, based on an exchange rate of A$0.75.

Managing director David Harley said the deposits were found using the “J theory” model of mineral sands mineralisation.

Mr Harley said the Murchison River at one stage drained into Shark Bay. When it eventually diverted to its current exit, at Kalbarri to the south, the heavy sands, containing the mineralisation, had been trapped at Coburn.

Zircon drives new

Coburn mine

Heavy mineral sands stockpile

n

in

m

n

Nickel West is the world's third-largestproducer of nickel-in-concentrate,providing 16 percent of global nickel-in-concentrate production. Nickel West'soperations include the Mt Keith andLeinster operations, the Kalgoorlie Nickel

Nickel WestA member of the BHP Billiton Group191 Great Eastern HwyBelmont WA 6104Telephone +61 8 9479 0500Facsimile +61 8 9479 0513

BHP BILLITON NICKEL WEST

Smelter, Kambalda Concentrator and theKwinana Nickel Refinery. Nickel West isa member of the BHP Billiton Group andwas formed from the West Australiannickel assets that were previously part of WMC Resources Ltd.

bhpbilliton.com

Prospect

24

PROSPECTReaches 10,000 decision makers in the resources sector every quarter

Advertise in the next issue December 05–February 06

Advertising booking deadline 16 November

Ray Burns MediaCo-Publisher of ProspectPO Box 1230South Perth 6951T 0408 474 328E [email protected]

Call Ray Burns now on 0408 474 328 to book your advertisement in the next issue.

‡

Western Australia’s mining sector is one of the big winners under this year’s Premier’s Research Fellowship Program.

The program aims to attract leading researchers to WA from overseas or interstate to conduct scientifi c research that is internationally competitive and of specifi c benefi t to WA.

As a result German Professor Klaus Regenauer-Lieb, of the Johannes Gutenberg-University, has been awarded a scientifi c fellowship.

Premier Geoff Gallop, who recently announced the fellowships along with Science Minister Judy Edwards, said Professor Regenauer-Lieb’s research will assist in further ore discoveries.

“Professor Regenauer-Lieb uses powerful computers to simulate geological processes, leading to a greater understanding of the formation of giant ore bodies. His work will assist WA in identifying new ore deposits in the State.”

Dr Gallop said the fellowship, worth $1million over four years, had been awarded on the advice of the WA Science Council.

“These fellowships aim to build and sustain world-class research teams with international connections, increase the level of external funding brought to the State and signifi cantly enhance research efforts that will benefi t present and future generations of Western Australians,” he said.

“The fellowship program is part of the State Government’s aim of securing WA’s long-term prosperity by investing the benefi ts of our booming economy in education and scientifi c research, especially in key areas such as resources and agriculture.”

Dr Edwards said the fellowship proposed a highly innovative research program that would provide economic benefi ts for WA.

“Professor Regenauer-Lieb is also committed to raising science awareness and developing young WA scientists,” she said.

The professor will be appointed by The University of Western Australia in association with CSIRO Exploration and Mining.

Mining gains from science fellowships

25Prospect

Investing in Our Future

Placer Dome is one of the world’s largest and most successful gold mining companies.

Headquartered in Vancouver, Canada, we have interests in 16 mines in 7 countries and employ

more than 13,000 people worldwide.

Through focussed investment in exploration and project development, Placer Dome is actively

searching for and advancing quality projects that will drive future production growth.

We look forward to collaborating with existing and new partners as we continue to build on our

successful exploration and development programs.

www.placerdome.comW

Level 2, 189 Coronation DriveMilton QLD 4064(GPO Box 465, Brisbane QLD 4001)Australia

Phone: 07 3510 6700 Graham FollandFax: 07 3510 6740 General Manager, Corporate

& Project Development

A recent report by Access Economics highlights the continued strength of the Western Australian economy along with good prospects for further jobs and export growth.

The Budget Monitor for September says that WA’s business investment to output ratio is the strongest of any State, describing WA as a ‘pipeline to prosperity’.

The report follows the release of labour force data showing the unemployment rate in WA had reached an equal record low of 4.4 per cent.

ABS fi gures show WA’s domestic economy had grown strongly at 5.5 per cent in 2004-05, compared with a national annual growth rate of 4.2 per cent.

“With increasing business investment, the State looks like continuing to make further gains in its share of Australia’s output and population,” the Budget Monitor says.

The report gives the State’s fi nances a tick of approval, highlighting healthy budget surpluses across the outlook period, with net debt levels to remain consistent with the State Government’s fi nancial targets.

The report’s key fi ndings include:

• revenue windfalls have been largely outside the Government’s control and due in signifi cant part to strong demand for WA’s iron ore and petroleum exports;

• the Government’s election commitments and other cost and demand pressures have been accommodated without impacting greatly on the Budget bottom line;

• the general Government net operating balance is now at proportionally stronger levels than those in NSW and Victoria; and

• the Government has ramped-up capital spending, with the net debt-to-revenue ratio projected to remain below the 47 per cent target limit.

The State Government has committed a record $15.8 billion capital works program over the next four years.

WA business investment strongest in country

W

Prospect

26

Specialists in Earthmoving, Mining and Construction Equipment

HIRE • BUY • SELL (08) 9274 7820

www.plantman.com.au

LUM

INOS

ITY

2286

16-20 Military Rd, Bellevue, Perth WA PO Box 60, Burswood WA Australia 6100Fax: (08) 9274 7809 All Hours: 0418 906 601 [email protected] Ph: +(61) (8) 9274 7820 International Fax: +(61) (8) 9274 7809

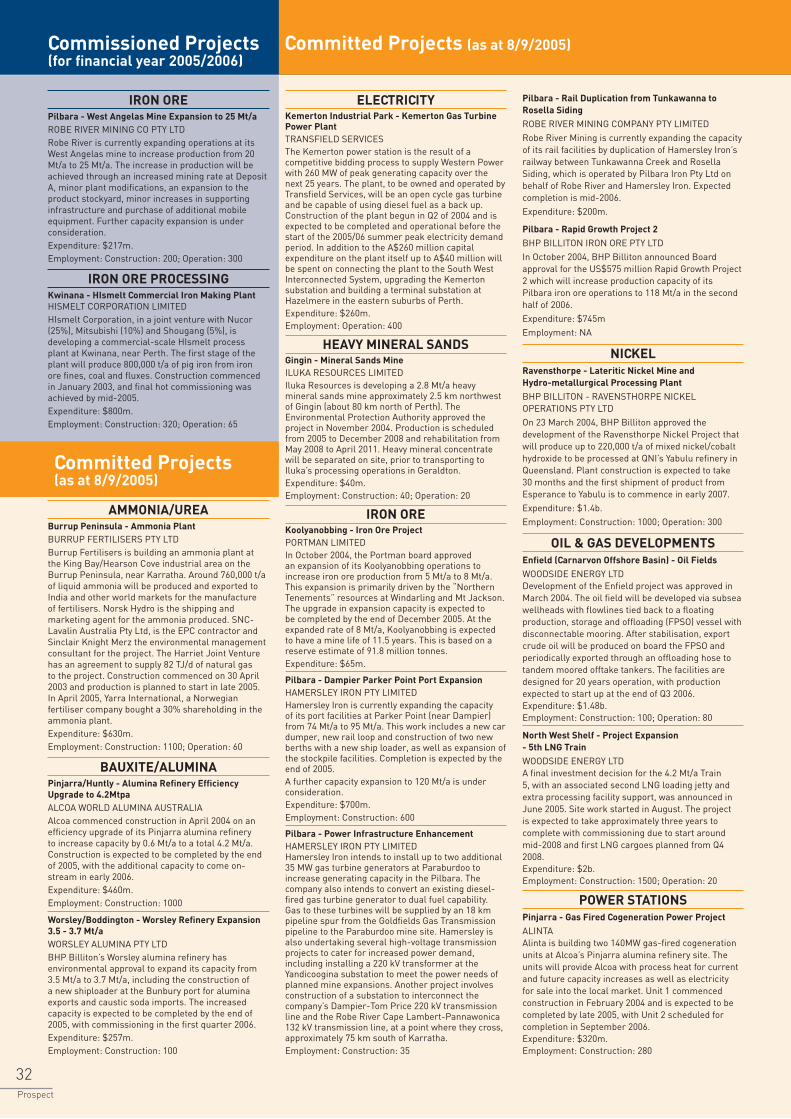

Signifi cant resource projects underway or planned in Western Australia

Prospect magazine is produced quarterly by the Department of Industry and Resources as an internationally circulated publication that showcases Western Australia’s mineral and petroleum industries.

And we are online. Prospect attracts up to 18,000 website hits an issue, which signifi cantly adds to the more than 10,000 printed copies of the magazine already distributed.

Prospect is aimed at industry executives, fi nanciers, suppliers and other people involved in the world’s most exciting industry.

Prospect can be downloaded from the internet by visiting the Department’s website at: www.doir.wa.gov.au

ProspectSubscription/Change of addressABN: 69 410 35 356

Visit us online

Name

Position

Organisation

Address

Type of business

Phone Number

Please tick the appropriate boxPlease add me to your mailing list to receive Prospect magazine. I would like a subscription for

one year @ $12 (incl. GST)

two years @ $22 (incl. GST)

three years @ $32 (incl. GST)

My cheque made out to the Department of Industry and Resources, is enclosed OR please debit the amount to my credit card using the following details:

Type of card: Visa Bankcard Mastercard

Expiry date

This form will become a tax invoice for GST purposes when payment is made.

Change of address (please make changes required on one of your old labels).

Please photocopy or cut coupon and mail to:

Prospect subscriptions, Information Centre, Department of Industry and Resources, Mineral House, 100 Plain Street, East Perth, Western Australia 6004

Project value

(estimated A$m)

Employment

Construction Permanent

Iron and steelAztec Resources Koolan Island mine 108 n/a 220

BHP Billiton future growth strategy 3500 n/a n/a

Extension Hill 550 400 210

Fortescue Metals Group mine, rail and port 2000 1500 300

Gindalbie Metals mine and pellet plant 720 200 175

Grange Resources Southdown magnetite mine 640 n/a n/a

Hamersley Iron’s port and rail expansions 700 800 195

Hope Downs iron ore mine 1000 1000 300

Kwinana HIsmelt pig iron and steel plant 800 320 65

Midwest Corporation iron ore pellet project 540 1200 266

Midwest Corporation Weld Range mine 850 900 220

Mineralogy (Cape Preston) mine and pellet plant 1400 2000 400

Robe River rail program 200 100 10

West Angelas mine expansion to 25Mt/a 217 200 300

Yandicoogina expansion 290 330 n/a

Sub total 15365 10450 2961

Nickel/cobaltGoongarrie mine 1400 1000 300

Ravensthorpe mine 1400 1000 300

Sub total 2800 2000 600

PetrochemicalsAgrium Ammonia Urea plant 900 100 300

Burrup Fertilisers ammonia plant 630 1100 60

Dampier Nitrogen ammonia–urea plant 900 1000 130

Sub total 2430 2200 490

GasEnfi eld oilfi eld development 1480 100 80

Gorgon project 11000 3000 600

LNG Train-4 and trunkline 2400 2500 80

LNG Train-5 project 2000 2000 70

Onslow LNG plant 4000 2500 150

Santos Mutineer–Exeter oilfi eld development 480 540 90

Santos Tern–Petrel gasfi eld development 1000 n/a n/a

Woodside Pluto LNG plant 5000 150 1500

Sub total 27360 10790 2570

OtherAlcoa Pinjarra alumina refi nery optimisation 440 1000 n/a

Alcoa Wagerup refi nery Train-3 expansion 1500 1000 150

Argyle diamonds 850 250 500

Boddington Wandoo gold mine expansion 1500 750 400

Burrup Ammonium nitrate 300 700 150

Griffi n coal-fi red power station 400 250 40

Kemerton titanium dioxide pigment plant expansion 470 500 200

Ord irrigation (stage 2) project 600 650 550

Sunrise Dam underground gold project 87 n/a n/a

Telfer gold mine expansion 1400 1222 620

Transfi eld gas turbine power plant 260 n/a 400

Worsley refi nery expansion 900 500 150Sundry projects (Projects valued at less than A$200 million) — at least another 2000 2000 300

Sub total 10707 8822 3460

TOTAL 58662 34262 10081

ww

w.d

oir.w

a.go

v.au

THE BIG PICTURE Economic trends

Prospect

28

Strong growth in the global economy continues... but downside risks persistThe global economy continues to expand solidly, with the two major drivers of recent growth, the United States and China, providing the major impetus. More recently, the Japanese economy has begun to perform more strongly, with activity broadening from largely export-led growth into improving domestic demand. Latin America, Eastern Europe and India are also providing stimulus to global demand. In contrast, a number of East Asian economies have slowed moderately due to weaker global ITC trade. The Euro area remains the global soft spot.