WEST BENGAL LAND REFORMS AND TENANCY TRIBUNAL JUDGEMENT OF ORIGINAL / TRANSFERRED...

56

Page 1 of 56 WEST BENGAL LAND REFORMS AND TENANCY TRIBUNAL JUDGEMENT OF ORIGINAL / TRANSFERRED APPEAL / PETITIONS O.A. No. 605 of 2011 (LRTT) Judgement delivered on 07.03.2012. Present: 1) The Hon’ble Mr. P. K. Chakraborty, Judicial Member 2) The Hon’ble Mr. Md. Ali Mondal, Administrative Member Bench No. Fourth Name (s): Paharpur Cooling Towers Limited and Anr………… Applicants. VERSUS State of West Bengal and Ors…………… Respondents. This application was heard on 21.02.2012 in presence of Mr. A. Pan, Md. A. Alim, Mr. S. Bhagat and Mr. B. Sen, Ld. Counsels for the applicants. Md. Kalamuddin and Mr. P. Dutta, Ld. Govt. Representatives. 1. The instant Original Application (O.A.) being No. 605/2011 has been filed on 03.03.11 u/s. 10 read with Section 6 of the W.B.L.R. &T.T. Act assailing the order of vesting dt. 11.02.2011 of the Ld. Revenue Officer (R.O.), Barasat, North 24 Parganas passed in a proceeding No. 1/2011 initiated on 05.01.11 u/s 14Y, 14L, 14M & 14T (3) read with Sec. 57 of the WBLR Act against M/s Paharpur Cooling Towers Ltd. (hereinafter shortly referred to as PCTL), 8/1/B Diamond Harbour Road, Calcutta 27. Though the remedial measures were available to the applicant u/s. 54 of the WBLR Act against the order of vesting in respect to the O.A. filed, the O.A. was admitted as per direction dt. 31.03.11 passed by the Hon’ble Division Bench, Calcutta High Court passed in A.S.T No. 130 / 11 considering the facts and circumstances of the case. The fact in issue and the lands involved being identical, another O.A. No.

Transcript of WEST BENGAL LAND REFORMS AND TENANCY TRIBUNAL JUDGEMENT OF ORIGINAL / TRANSFERRED...

Page 1 of 56

WEST BENGAL LAND REFORMS AND TENANCY TRIBUNAL

JUDGEMENT OF ORIGINAL / TRANSFERRED

APPEAL / PETITIONS

O.A. No. 605 of 2011 (LRTT)

Judgement delivered on 07.03.2012.

Present:

1) The Hon’ble Mr. P. K. Chakraborty, Judicial Member

2) The Hon’ble Mr. Md. Ali Mondal, Administrative Member

Bench No. Fourth

Name (s): Paharpur Cooling Towers Limited and Anr………… Applicants.

VERSUS

State of West Bengal and Ors…………… Respondents.

This application was heard on 21.02.2012 in presence of

Mr. A. Pan, Md. A. Alim, Mr. S. Bhagat and Mr. B. Sen, Ld. Counsels for the applicants.

Md. Kalamuddin and Mr. P. Dutta, Ld. Govt. Representatives.

1. The instant Original Application (O.A.) being No. 605/2011 has been filed on

03.03.11 u/s. 10 read with Section 6 of the W.B.L.R. &T.T. Act assailing the order of

vesting dt. 11.02.2011 of the Ld. Revenue Officer (R.O.), Barasat, North 24 Parganas

passed in a proceeding No. 1/2011 initiated on 05.01.11 u/s 14Y, 14L, 14M & 14T (3)

read with Sec. 57 of the WBLR Act against M/s Paharpur Cooling Towers Ltd.

(hereinafter shortly referred to as PCTL), 8/1/B Diamond Harbour Road, Calcutta

27. Though the remedial measures were available to the applicant u/s. 54 of the

WBLR Act against the order of vesting in respect to the O.A. filed, the O.A. was

admitted as per direction dt. 31.03.11 passed by the Hon’ble Division Bench, Calcutta

High Court passed in A.S.T No. 130 / 11 considering the facts and circumstances of

the case. The fact in issue and the lands involved being identical, another O.A. No.

Page 2 of 56

707 of 2011 filed with cause title - Paharpur Pragnya Realty Private. Ltd. and Anr.,

Vs. State of West Bengal & Ors., was taken up for hearing simultaneously with this

instant O.A. No. 605 of 2011. The name of this Paharpur Pragnya Realty Private. Ltd.

has been referred to here as PPRPL. Both the Ld. Govt. Representatives and the Ld.

Counsels for the applicants filed affidavit-in-opposition, affidavit-in-reply and

written arguments during hearing. Heard them at length on several dates and finally

on 21.02.12.

The fact of the case as made out by the applicant / petitioner no. 1 i.e. PCTL, is

that one notice dt. 6.01.2011 under the aforesaid sections accompanied by a copy

of the order sheet dt. 5.01.2011 together with the schedule of lands, was

suddenly served upon M/s Paharpur Cooling Tower Ltd, on 7/01/2011 when the

construction works on the lands at Palta was going on in full swing as per sanctioned

plan. In the aforesaid notice the applicant was asked to submit choice of option for

retention on 17.01.2011 as the Ld. Revenue Officer (R.O.), North 24 Parganas,

Barasat was prima-facie satisfied that PCTL owned total 40.64 acres of land at

Mouza Palta, Bhasa and Joka. Mentioned that Mouza Palta fall under P.S. –Noapara,

Dt. 24 Parganas North and the other two mouzas fall under the Dt. South 24

Parganas

The P.C.T.L. prayed for adjournment of the proceeding initiated by the Ld. R.O.

who is the respondent No. 2 of this O.A., vide their letter dt. 13.01.2011. The

said letter was received by the Ld. R.O. on 14.01.2011, considered and the case was

adjourned to 27.01.2011.

On 27.01.2011 one Mr. P.R. Dutta, one representative of the realty division

of PCTL personally appeared and prayed for further time of 6 weeks stating inter

alia that they were not holding land in excess of ceiling. Prayer was considered and

the case was adjourned again to 11.02.2011.

On 11.02.2011 Mr. Dutta again remained present and prayed for 6 weeks

time. The prayer was not considered and order in the proceeding No. 1/11 initiated

on 05.01.11 was passed vesting the entire 11.32 acres of land from Mouza Palta and

5.12 acres of land out of 9.82 acres from Mouza Bhasa. Notice dt. 15.02.2011 was

Page 3 of 56

served on PCTL fixing date of taking possession of the land vested on 23.02.2011

annexing therewith, the schedules of vested and retained lands separately prepared.

1.3 Vide letter dt. 17.02.2011 the PCTL informed the Ld. R.O. that they were not

holding any land in excess of ceiling and that the proceeding itself was without

jurisdiction and cannot be proceeded with in the light of the judgement dt. 17.05.07

of the Divn. Bench of the Hon’ble High Court, Calcutta in the case of Niranjan

Chatterjee –v- State of W.B., 2007 (3) CHN 683. It was also mentioned in the letter

dt. 17.02.2011 that the applicant company was not holding any ceiling excess land and

the applicant requested the Ld. R.O. to keep the proceeding in abeyance / to

permanently stay the same till disposal of the case of Paschim Banga Bhumijibi

Sangha by the Apex Court of India.

On 23.02.2011 possession of 11.32 acres of land at Palta Mouza, P.S. Noapara,

North 24 Parganas was taken over by BL&LRO. One Uttam Barik made over

possession to BL&LRO in presence of Saurav Mukherjee, the authorised

representative of Paharpur Pragnya Realty Private Ltd., remaining present as one of

the witnesses.

Possession of 5.12 acres of land vested was also taken over on 11.03.2011 from

Mouza-Bhasa, Dt. South 24 Parganas.

2. After narrating the fact of the case, Ld. Advocates for the applicant of O.A.

No. 605 of 2011 argued that the lands of all the three mouzas, specially the lands

of Palta mouza falling under Urban Agglomeration, cannot be brought under the

ambit of WBLR Act in terms of Section 14J of the Act. Though it was admitted

that the applicant initially purchased 11.32 acres of land at Palta from National

Textile Corporation (N.T.C.) on 15.10.07, but it was argued further that the

ownership of the lands at Palta mouza on the date of vesting belonged to PPRPL,

the applicant No. 1 of O.A. No. 707 of 2011. Lands of mouza-Joka fall under the

jurisdiction of Town and Country (Planning & Development) Act, 79. It was

vehemently argued that Urban Development Department, Govt. of West Bengal

granted exemption to PCTL to hold vacant land measuring 11.32 acres at Palta

Page 4 of 56

mouza vide its order dt. 02.02.10 and prior to that the lands were transferred to

Bihari Properties Pvt. Ltd. (shortly referred to as BPPL). No ceiling was, at all,

applicable for the lands of mouza Palta under WBLR Act. Jurisdiction and

authority of the R.O. to vest the land without giving adequate opportunity of

hearing and legality of vesting under Section 14T (3) on the face of Hon’ble

Division Bench order dt. 17.05.07 passed in Niranjan Chatterjee Vs. State of

W.B., 2007 (3) CHN 683, were called into question amongst other points.

Ld. Govt. Representatives, on the other hand, submitted that after scrutiny of

records the Ld. R.O. was prima facie satisfied that the PCTL was holding land in

excess of ceiling in gross violation of the provisions of Sections 14L and 14Y. In

terms of Section 14J only vacant land cannot be vested. Submitted further that

after the WBLR (Amend.) Act, 1981, all categories of land become vestable under

Section 14T(3) of the LR Act save and except vacant land governed by the UL(C &

R) Act, 1976 and non-agricultural lands of non-agricultural tenants governed by

the provisions of WBNAT Act, 1949. The non-agricultural lands governed by the

provisions of WBNAT Act, 1949 again became vestable by the WBLR (3rd Amend.)

Act, 1986 w.e.f. 09.09.80 along with other lands. PCTL owned 11.32 acres of land

at Palta on 15.10.07 as already admitted by them. As on the date of acquisition

i.e. on 15.10.07, PCTL was holding 40.64 acres of land in total at mouzas Palta,

Bhasa and Joka as per finally published ROR as raiyat, and as built-up structures

cannot be regarded as vacant land, the vesting was justified. On the effect of

order passed in Niranjan Chatterjee’s case, the Ld. Govt. Representatives cited

the following cases:-

(i) Harisadhan Bandyopadhyay & Anr. – Vs- State of West Bengal, (1998) 1

CHN 61

(ii) Pijush Kanti Chowdhury –V- State of W.B. (2007) 2Cal LT 577(HC)

(iii) Mrinal Kanti Paul-V-State of West Bengal, (2000) 1 CLJ 1 (DB)

and submitted that similar orders were passed in Harisadhan Bandhyopadhaya’s

case and Pijush Kanti Chowdhuri’s case where the Hon’ble Apex Court was pleased

to grant stay. Again, in Mrinal Kanti Paul’s case by another Division Bench order,

Page 5 of 56

vesting under Section 14T(3) was held to be justified. They further submitted

that adequate opportunity of hearing was given and that there was no irregularity

in the order passed by the Ld. R.O. The applicant simply wasted time before the

Ld. R.O. and prayed for adjournment stating that they were not holding ceiling

excess land but they did not like to place any factual information as to how and

why 40.46 acres of land stood recorded in their names. Rather, they challenged

the jurisdiction and authority of the Ld. R.O. to vest under Section 14T(3) by

submitting ruling passed in Niranjan Chatterjee’s case (Supra).

3. It is an admitted fact that one company named Shree Mahalakshmi Cotton

Mills Ltd. (shortly SMCML) was having 11.32 acres of land at Mouza-Palta. M/s

Gajraj Pannalal Ltd. became the owner of the said 11.32 acres of land at Mouza

Palta of the said SMCML by virtue of purchase in the year 1960 from the Official

Liquidator when the said SMCML had gone into liquidation. The said industrial

undertaking became sick again and has been closed for a period of more than

three months. Hence, on 12th June, 1972, Jt. Secy. Govt. of India through gazette

notification published in the gazette of India, Extraordinary, Part-II Section 3

Sub Sec. (ii), dated the 12th June, 72, authorized the National Textile Corporation

(shortly NTC) to take over management of the whole of the undertaking of

SMCML, Palta in terms of Sec. 18AA of the Industries (Development &

Regulation) Act, 1951 (65 of 1951).

Thereafter, the sick Textile Undertaking (Nationalisation) Act, 1974 came into

force and SMCML was taken over by central govt. By operation of Sec. 3, 5 & 6 of

the Sick Textile Undertaking (Nationalisation) Act, 1974 and within the meaning of

Sec. 2(j) of the Act, the right, title and interest of SMCML, the said Sick Textile

Undertaking stood transferred to and vested absolutely in the Central Govt. w.e.f.

01.04.1974, the appointed day. Consequently, SMCML stood transferred to and

vested in the NTC by virtue of Sub Sec. (2) the said Section, 3 of the Act.

Consequences of Sec. 4 of the Act became operative w.e.f. 01.04.74. As a result,

SMCML had been functioning as a unit of NTC.

Page 6 of 56

4. In the year 1992 the said unit at Palta was referred to BIFR. On 15.02.02, BIFR

sanctioned the Draft Rehabilitation Scheme (DRS) and approved the sale of assets

including the surplus land, machineries and buildings of the said Sick Textile

Undertaking at Palta under the guidance of BIFR with direction that the sale

proceeds of the land would be used to extend VRS benefits, payments of other

statutory duties and revival of other three units in the State. An assets Sale

Committee (ASC) comprising the representative of Govt. of India, Ministry of

Textile (GoI / MoT), State Govt. CMD of NTC, IDBI, Spl. Director appointed by

BIFR was constituted by (GoI / MoT) under direction of BIFR.

Under specific guidelines issued by BIFR and with the approval of GoI / MoT, a

tender notice was issued inviting bids from interested purchasers for the land at

Palta. The bid of PCTL being the highest was accepted by the Authority and all

redundant assets including surplus plants, building and lands of SMCML were sold to

PCTL by NTC by Regd. Deed dt. 15.10.2007. Details of purchase of 11.32 acres of

land at Palta have been vividly described by the petitioner in O.A. No. 707/11 as well

as in the petition dt. 22.06.2009 vide annexure ‘D’ attached with the O.A. No.

707/11.

5. From the scheme of arrangement made as enclosed in Schedule ‘A’ attached to

the O.A No. 605/11 at page no. 58 it appears that PCTL owned the land measuring

11.32 acres along with building and other permanent and temporary structure of

erstwhile “Mahalaxmi Cotton Mills” at Palta for developing an integral residential

complex. The work of developing the project is known as ‘Palta Project’ / ‘Demerged

Undertaking’. With a view to operate ‘Demerged Undertaking’ independently, PCTL

decided to demerge its Palta Undertaking to Bihari Properties Pvt. Ltd. (BPPL).

6. It has been admitted by the applicant in Para 15 of the instant O.A. as follows,

“ By an order dt. 21st July, 2009 passed by the Hon’ble High Court at

Calcutta in company Ptn. No. 1770/2009 connected with Company Application No. 282

of 2009, a scheme of Arrangement proposed to be made between Bihari Properties

Private Ltd. ( BPPL) and the petitioner No. 1 was sanctioned and in terms thereof,

the Demerged Undertaking comprising of certain assets of the petitioner No. 1

Page 7 of 56

including the said land, as specified in schedule A to the scheme of Arrangement u/s

391 to 394 of the companies Act 1956 between BPPL and the petitioner No. 1 and

their respective shareholder, was ordered to be transferred and vested in BPPL

without any further act or deed and was, thereby, transferred to and vested in the

said BPPL. By virtue of the said order, the petitioner No. 1 presently does not own

any land at Mouza – Palta and the said land is owned by BPPL (since renamed as

Paharpur Pragnya Realty Pvt. Ltd.)”.

7. Hence, it is clear that the land was initially owned and possessed by PCTL by

virtue of purchase through auction of properties of Shree Mahalakshmi Cotton Mills

Ltd. (SMCML) on 15.10.2007 made by NTC. It is an admitted fact the landed

properties of 11.32 acres along with other assets of PCTL are transferred to BPPL as

per scheme of arrangement u/s 391 to 394 of the Companies Act, 1956 made

between PCTL and BBPL and sanctioned by the Hon’ble High Court on 21.07.2009 in

company petition No. 177/09 connected with company application No. 282/09 without

any registered deed subsequent to acquisition by PCTL on 15.10.07. The sanction

dt. 21.07.2009 of the Hon’ble High Court, Calcutta was filed with the Registrar of

Companies, West Bengal on 21.08.09 and the scheme of arrangement of the

‘Demerged Undertaking’ became effective thereafter.

8. Prior to such purchase on 15.10.07, PCTL purchased 9.82 acres of land at

Mouza Bhasa, P.S. Bishnupur and 19.50 acres of land at mouza Joka, P.S. Behala –

both under South 24 Pgs. District. The PCTL Authority admits in its application in

O.A. No. 605 of 2011 at para 16(iii) that by a deed of conveyance dt. 28.03.2003 it

purchased 19.50 acres of land at mouza-Joka from Siemens Limited. In mouza-Bhasa

the Authority further owned 9.82 acres of land. It is stated in para 16(ii) of the

O.A. No. 605 of 2011, “the petitioner no. 1 (i.e. PCTL) is running a factory thereat

employing 250 people since 1992.” For arguments sake, PCTL the petitioner No. 1

against whom vesting proceeding was initiated, may claim that it does not hold land at

Palta w.e.f. 21.07.09, but there is no scope of any denial that PCTL altogether owned

40.64 acres of land including 11.32 acres at Palta as it is PCTL which acquired 11.32

acres of land on 15.10.2007 by purchase through auction. Neither the scheme of

Page 8 of 56

arrangement for demerger with prior sanction of the Hon’ble High Court, Calcutta

nor the change of name of the company from PCTL to PPRPL comes of any help for

PCTL to deny the fact of acquisition of 40.64 acres of land as on 15.10.07. The

object of demerger of Palta Undertaking of PCTL to BPPL as appears from Scheme

of Arrangement at Schedule ‘A’ was to enable PCTL to focus on its core business of

manufacturing of cooling towers and other such business and to simultaneously

provide focus and greater attention to the development of real estate business.

Hence, all such arrangements, as transpires from records, were made for

development, expansion and betterment of the PCTL Company itself.

9. Let us now consider whether the lands measuring 11.32 acres at Palta were

vacant or otherwise computable to determine ceiling as on 15.10.07 u/s 14T of the

WBLR Act 1955. If it were vacant land, the provisions of UL(C & R) Act’ 76 will apply

and such lands cannot be computed with other lands defined in Sec. 2(7) of the

WBLR Act.

The meaning of the vacant land as contained in Sec. 2(q) of UL(C & R) Act’ 76

was expanded by the Hon’ble Divn. Bench of Calcutta High Court in Paschmim Banga

Bhumijibi Krishak Samiti – V- State of W.B., (1996) 2 CHN 212 : 1996 WBLR(Cal) 242

: (1996) 2 Cal LJ 285. The observations of the Hon’ble Divn. Bench made in para 41

are reproduced:

“ In view of the definition of the vacant land as contained in Sec. 2(q) of the Urban

Land Ceiling Act, vacant land shall not include –

(i) Lands mainly used for the purpose of agriculture.

(ii) Lands on which constructions are not permissible under Rules.

(iii) Lands occupied by building with sanction where such Rules exists.

(iv) Lands occupied by building where no such Rule exists, and

(v) Cattles’ space in a village within urban agglomeration.”

From the above observations it is abundantly clear that lands covered by

structures does not fall within the definition of vacant land.

Page 9 of 56

10. From page 60 of the O.A. 707 / 11, it appears that there were structures over

the lands at Palta. The fact of such existing structures is admitted by PCTL and as

such the applicant submitted petition dt. 22.06.09 to the O.S.D. & E.O., Deputy

Secretary, Urban Development Department, Urban Lands Ceiling Branch to get

exemption to develop residential cum commercial complex. The relevant portion from

the application dt. 22.06.2009 is quoted for better appreciation, “The land is

currently full of factory structures. However, before developing the land all

structures would be demolished. Hence, if you grant us exemption with permission to

develop Residential-cum-Commercial Complex, taking the entire land as vacant land

we shall have no problem.” It is not understood as to how the applicant vehemently

denies that the subject land is not covered by the shaded structures and other allied

user of the factory in para 8 of the Affidavit in Reply filed in reply to Affidavit in

Opposition for O.A. No. 707/11 when it was categorically mentioned in their petition

dt. 22.06.09 that the land was full of factory structures and the PCTL Authority

made commitment to the Urban Development Department in the petition dt. 22.06.09

to demolish the structures before developing the lands. Again, such building

materials on lands at Palta mouza are stated to have been demolished in the Tender

Notice floated by NTC prior to sale on 15.10.07. This Tribunal does not like to go

into details as to whether the character of land at Palta was converted under the due

process of law. It does not like to ascertain the exact date when the demolition of

the existing structure was actually effected making the lands as ‘vacant’. But as the

PCTL itself admitted in their petition dated 22.06.09 filed to the Urban Development

Department praying for exemption and stating inter-alia to the effect that there

were structures all over the lands at Palta, it need not be proved that there were

structure on 15.10.07, a date prior to 22.06.09. Be that as it may, it need not be

proved that as on 15.10.2007 i.e. on the date of acquisition of 11.32 acres of land at

Palta, the character of land was Karkhana with buildings / structures constructed

thereon long ago as one Cotton Mill named and styled as SMCML, was in existence

from a period prior to 1960 and the same comes under the ceiling provision under

Page 10 of 56

Chapter IIB of the WBLR Act by definition of land substituted in the WBLR Act by

the WBLR (Amendment) Act 1981.

As the lands at Palta were not vacant as on 15.10.07 and come under the ambit

of WBLR Act, exemption granted by the Urban Development Department, Govt. of

West Bengal from the ceiling provisions of chapter IIB of the WBLR Act, vide order

dt. 02.02.10 as stated in para 15 of the O.A. No. 605/11 comes, in no way, of any

assistance to the applicant. Moreover, Govt. order cannot supersede the force of

Law and cannot nullify the effect of WBLR Act, a special legislation having overriding

effect.

Understandably, a factory is running over 9.82 acres of land at Mouza Bhasa

since 1992. The question whether the lands are being cultivated or not in the past

for a long time is immaterial, but the finding whether lands fall under the ambit of

WBLR Act is the point for adjudication.

As the factory land full of structures cannot be treated as ‘vacant land’ within

the meaning of Section 2(q) of the UL(C & R) Act’ 76, the argument advanced by the

applicant to the effect that the lands at Bhasa not being cultivated for the last 20

years and falling within the territories of UL(C & R) Act’ 76, cannot be computed for

determination of ceiling under WBLR Act, again proves to be futile exercise.

11. Certified copies of finally published LR Record of Rights show that 19.50 acres

of lands of Mouza Joka, P.S. Behala and 9.82 acres of land of Mouza Bhasa, P.S.

Bishnupur and 11.32 acres of land at Mouza Palta, P.S. Noapara recorded in the name

of PCTL as raiyat, are all classified either as ‘Agricultural’, ‘Shali’, ‘Bastu’ and / or

‘Karkhana’ and hence come under the ambit of chapter II B of the WBLR Act and

fall for determination of ceiling u/s 14T (3) / 14T (10) of the Act.

It appears from memo dt. 25.11.03 of ADM & DLLRO, South 24 Parganas that

the classifications of the entire 19.50 acres of land of Mouza Joka, P.S. Behala vide

annexure ‘A’, page No. 80 to the O.A. No. 605/11, were converted from Shali (Argi.)

to Vastu on application by PCTL. So, there is no doubt that the lands of Joka mouza

irrespective of classification as ‘shali’ or ‘bastu’ come under the ambit of WBLR Act.

Page 11 of 56

Since the lands of mouza Bhasa & Palta are covered by buildings and

structures, these lands can not come within the meaning of ‘vacant land’ as defined in

section 2(q) of the ULCR Act, 1976 and in consequence those lands do not come under

the saving provision of section 14J of the WBLR Act, 1955. As such, the said lands

are covered by Section 2(7) of the WBLR Act and legally come under the ceiling

provision of chapter IIB of the WBLR Act, 1955.

11.1 By one supplementary affidavit filed on 28.07.2011 by Paharpur Cooling

Towers Limited & Another, the applicants of O.A. No. 605 of 2011 submitted that

the mouza-Joka falls under the jurisdiction of Kolkata Metropolitan Development

Authority (KMDA) and, consequently, falls within the purview of the West Bengal

Town and Country (Planning & Development) Act, 1979.

Section 4C of the WBLR Act provides that a raiyat desiring to make any

change in area, character and utilization of any plot of land may apply to Collector

for permission. The Collector may, after causing due enquiry and after giving a

chance of hearing to the applicant and other interested persons, pass an appropriate

order. The matters to be covered and conditions to be imposed before passing

appropriate order have been provided for in Rule 5A of the WBLR Rules, 1965.

Clause II of Sub-rule (1) of rule 5A directs that it should be examined if the

conversion of land conforms to the general pattern of use of land in the locality.

In disposing of application under Section 4C, Collector is to consider the

effect of the other Laws on the proposed change. Relevant provisions of the West

Bengal Town and Country (Planning & Development) Act, 1979 are very vital in this

regard. Under this Act, a change in land-use in KMDA area has to be approved by the

Planning Authority or Development Authority under 46 of the Act. Such functions

have now been delegated to the Municipalities and for non-Municipals areas, to the

Zilla Parisad within the KMDA area. To avoid contradictory orders the respective

authorities under the WBLR Act and the WBT & C (P & D) Act, shall have mutual

consultations before disposing an application for conversion but without prejudice to

the provisions of the respective Acts.

Page 12 of 56

Hence, permission granted by Zilla Parisad, South 24 Parganas District for use

of the land as housing complex at mouza Joka as Development Authority, cannot

exempt the applicants to own lands at Joka in excess of ceiling prescribed in the

WBLR Act as both the Acts are operative within their respective fields and

jurisdictions on all the three mouzas including Joka as mentioned hereinbefore and as

WBLR Act has over-riding effect in Section 3 and 14J.

11.2 The Ld. Counsels for the applicant argued with fecundity, sagacity and

steadfast gravity opposing that the lands at three mouzas viz, mouza Joka, Bhasa and

Palta - all situated in the highly urbanized belt, do not come under the purview of the

LR Act. But they could not satisfactorily explain the necessity of getting the

classification of lands of Joka mouza converted from Shali to Bastu, if lands were

vacant as claimed. Lands classified as Bastu obviously come within the ceiling of

WBLR Act. No plausible clarification could be given as to why factory lands at mouza

Palta and Bhasa having structures and buildings thereon, should not be regulated by

the WBLR Act as the definition of land was radically amended by 1981 Amendment

Act taking all lands irrespective of classification under its fold.

11.3 Letter of the L& LR department as stated to have been forwarded to the

Industrial Reconstruction Deptt. to the effect that the land of Palta Mouza does not

come under the purview of Sec. 6(3) of the WBEA Act 1953 (vide page 59 to the

O.A. No. 707/11), does not authorize the PCTL to purchase land not being vacant in

nature, in excess of ceiling in contravention of Sec. 14L & 14Y of the WBLR Act.

The Ld. R.O. Barasat, North 24 Parganas disposed of the vesting proceeding

No. 1/11 u/s 14L & 14Y amongst other sections. It means he determine the ceiling on

the basis of position existing as on 15.10.2007 when the total quantum of land owned

by PCTL, a raiyat u/s 14M (e), was computed to 40.64 acres. The vesting became

automatically effective w.e.f. 15.10.07 by statutory operation. In a proceeding u/s

14T (3) without invoking Sec. 14L & 14Y, the date of vesting will be operative from

15.02.71 irrespective of date of issue of the vesting order.

11.4 In the application dt. 22.06.09, PCTL authority categorically mentioned that

“the land is currently full of factory structures”. But it is not understood as to how

Page 13 of 56

the Urban Development Department was satisfied while passing the order dt.

02.02.10 under Section 20 of the ULC & R Act, 1976 (at para 7 of the order dt.

02.02.10) that the PCTL was holding vacant land in excess of ceiling and granted

exemption when the recorded classification was ‘path, bastu, bazaar, shali and

karkhana’ and when actual classification as per use also was ‘karkhana’ having full of

structures existing thereon. Such order cannot be binding upon the authorities

under Section 14T of the W.B.L.R. Act to proceed with a vesting proceeding on the

basis of position existing on 15.10.07 even after passing of the order of exemption by

Urban Development Department on 02.02.10. Operation of L.R. Act cannot be

arrested by the impugned order dt. 02.02.10 specially on a date i.e. on 15.10.07 when

there was no existence of the order referred to.

11.5 The applicant did not submit the fact of getting exemption of ceiling under

UL(C&R) Act, 76 from the Urban Development Department vide order dated 02.02.10

for the lands at Palta before the Ld R.O. during hearing. Rather, the issue has been

raised now and citing the order dated 02.02.10 the Ld. Advocates for the applicant

tried to impress upon that until and unless the exemption granted by the Urban

Development Department u/s 20 of the UL(C&R) Act, 76 is declared void by the

competent authority, the lands of Palta cannot be computed for determination of

ceiling under the WBLR Act. It is true that this Tribunal cannot adjudicate the

matter falling under the UL(C&R) Act, 76; but that does not mean that this Tribunal

will keep its eyes closed to ignore the fact in reality. If a man owns several buildings

within Urban Agglomeration Area and if the sum total of lands covered by structures

exceed ceiling, the lands definitely come under the ceiling of the WBLR Act due to

radical change of definition of land by the WBLR(Amend) Act, 81. If a raiyat owns

ceiling excess lands – all governed by the provisions of WBLR Act as on 15.10.07 and

transfer subsequently some of the lands so owned, the extent of land being ceiling

surplus, is liable to vest in the state with effect from 15.10.07 even if the character

of land transferred if changed under due process of law. The legal position u/s 14 U

of the WBLR Act is that the State government may, in the first instance, take

Page 14 of 56

possession, equal in area to the land which is to vest in the State, from out of land

owned by such raiyat and where such recovery is not possible, from the transferee.

It is crystal clear that as on 15.10.07 the lands of Palta covered by structures

and sheds are computable for determination of ceiling under WBLR Act. Even without

making any comment on the order dated 02.02.10 issued by the Urban Development

Department it may be safely said that the lands of Mouza Palta were computable for

determination of ceiling and vesting as per position existing on 15.10.07. The

applicant was not under compulsion to own land governed by the WBLR Act, in excess

of ceiling prescribed therein.

11.6 There is no scope of any consistency between the UL(C&R) Act, 76 and the

WBLR Act, 55. Both the Acts intend to sub-serve common good by managing and

controlling ‘lands’, the material resources of the community and to regulate the

concentration of ‘land’ regarded as the most valuable wealth and means of production

to the common detriment. While UL(C&R) Act, 76 operates only over the vacant

lands in Urban Agglomeration area, the WBLR Act operates in the whole of West

Bengal except Kolkata and with certain exemption on vacant lands as provided in

section 14J of the WBLR Act. Both the Acts are supplementary and cumulative in

their operation which can stand together and function with full vigour side by side in

their own parallel channels.

11.7 The PCTL authority did not disclose the development of facts subsequent to

purchase on 15.10.07. Had the facts of transfer of lands by PCTL to PPRPL and had

the facts of exemption granted by the Urban Development Department been

disclosed to the Ld R.O. during hearing, the PCTL authority could have opted for

retaining the lands at Palta along with other lands within the permissible extent of 7

standard hectares and vesting excess quantum from Joka and or Bhasa Mouzas u/s

14T(3) of the Act. But the applicant did not, at all, co-operate with the Ld. R.O. on

successive dates. Rather, the applicant decided, as appears from records, to

challenge the authority of the Ld. R.O. u/s 14T(3) of the WBLR Act for vesting of

the lands in question.

Page 15 of 56

11.8 Under Section 3 , the WBLR itself has overriding effect. Again, u/s 14J the

ceiling provisions under chapter IIB enjoy the overriding effect containing a non-

abastantee clause like, “ the provisions of the chapter shall have effect

notwithstanding anything to the contrary contained elsewhere in this Act or in any

other law for the time in force or in any custom, usage or contract, express or

implied, or in any agreement, decree, order, decision or award of court, tribunal or

other authority.” These statutory provisions give answer to the question as to

whether on the face of the order dt. 02.02.2010 issued by the urban development

department, the provisions of the WBLR Act will operate, when the nature and

character of land were governed by the provisions of WBLR Act as on 15.10.2007.

UL(C & R) Act 1976 operate on vacant land only and not on the entire lands

within urban agglomeration area. Vesting became effective from 15.10.2007. Only

detection was made by the R.O. on the date of passing the order.

12. Ceiling provisions under Chapter IIB of the WBLR Act came into force with

effect from 15.02.1971. “Ceiling Area” means the extent of land which raiyat shall

be entitled to own in terms of section 14K read with Section 14M of the Act. As per

provisions of Section 14M(e), PCTL as ‘other raiyats’ is entitled to own only 7

standard hectares of land. To arrest the attempts of raiyats to evade ceiling and to

net in more land in the State coffer, retrospective operation of ceiling was given

with effect from 07.08.69 as a measure of legislative device by insertion of section

14P in the Act. From the above discussions made in para 2 to 11, it is amply clear

that the PCTL owned 40.64 acres of lands as on 15.10.07 so far detected and the

entire land either classified as Shali / Bastu or Karkhana (covered by structures) are

computable and come under the ceiling provisions of the WBLR Act, 55. The lands so

owned after 07.08.69 being excess of ceiling prescribed u/s 14M of the WBLR Act,

it was statutory obligation on the part of the PCTL to obtain prior permission of the

government u/s 14Y of the Act.

13. Let us now consider the applicability of the ratio of judgment dt. 17.05.07 passed

in Niranjan Chatterjee Vs. State of W.B., 2007 (3) CHN 683, by the Hon’ble Division

Bench, High Court, Calcutta to the present O.A. In the referred case, the Hon’ble

Page 16 of 56

Division Bench held that the R.O. cannot initiate any proceeding u/s. 14T (3) of the

Act until Section 14V is amended to provide reasonable compensation.

The constitutional validity of the WBLR (Amendment) Act, 1981 and the WBLR

(3rd Amendment) Act, 1986 by which the non-agricultural lands governed by the

provisions of WBNAT Act, 49 were brought under the ambit the WBLR Act by

insertion of Sec. 3A, fell for consideration by the High Court, Calcutta. Hon’ble

Division Bench, High Court, Calcutta in Paschim Banga Bhumijibi Krishak Samity–

State of West Bengal, 1996 WBLR (Cal) 242, shortly hereinafter referred to as

PBBKS’s Case, observed that in terms of radical change in the definition of Sec. 2(7)

read with Sec. 3A (3), the term ‘land’ now means and includes non-agricultural land

occupied by buildings, factories, tank fisheries etc. It was observed further that no

separate norms had been prescribed for payment of ‘amount’ for vesting ceiling

surplus non-agricultural land specially for lands like buildings, factories lying just

outside the periphery of urban agglomeration area. Instead, Govt. adopted the same

principle of Section 14V as is / was applicable for vesting agricultural lands, for

payment of amount.

State Govt. has no intention to oust any raiyat from buildings, factories etc.

and not to pay any ‘amount’ under the existing provisions of the Act. A raiyat is,

within right to retain land up to the ceiling applicable to him in accordance with Sec.

14M & 14T. Thus a raiyat is at liberty to retain his buildings / factories, if there be

any, considered to be the most valuable and not to allow such lands to be vested by

the state under the Act. It is expected that normally raiyats would retain their

valuable lands. The Hon’ble Divn. Bench, however, by judgement dt. 26.07.1996 was

pleased to declare the provisions of Sec. 14V vis-à-vis the definition of land as

contained in Sec. 2(7) and Sec. 3A (3) of the WBLR Act is untra-vires Art. 300A of

the constitution of India. In other words the Hon’ble Divn. Bench declared that only

the amount payable u/s 14V for Sec. 3A(3) component of land as defined in Sec. 2(7)

as ultra vires.

The order dt. 26.07.1996 passed in PBBKS’s case was stayed on 20.03.1998

by the Apex Court in Civil Appeal No. 16879 of 1996. While in SLP No. 1416/97

Page 17 of 56

Hon’ble Apex Court by interim order dt. 16.12.99, directed that status-quo as

regards possession on spot shall be maintained by both sides in connection with the

members of the petitioner’s Sangha who were before the High Court in the writ

petition out of which the SLP arises. On 17.04.2000 the Hon’ble Supreme Court

passed interim order to the effect that vesting order passed on land of members of

petitioner’s Sangha who were before the High Court in the matter out of which SLP

arises, shall not be implemented until further order. Thereafter, further order was

passed on 24.11.2003 when the Hon’ble Apex Court held, “We are of the view that

the authorities of the State shall ensure notwithstanding the vesting orders that

may be passed and mutations that may be effected in the revenue records, no third

party rights should be created and no such third parties be inducted or allowed to

enter upon or squatter on such properties pending disposal of the appeals”. In the

meant time, interpretations are going on as to whether state authorities may, at all,

proceed with the vesting u/s 14T without amending Sec. 14V.

14. The decision dt. 26.07.1996 in PBBKS’s case has evoked the most controversial

issue on the point of payment of ‘amount’ for vesting ceiling surplus land. Vesting as

well as distribution has virtually come to a halt adversely affecting the

implementation of the Directive Principles of the State Policy – the enshrined duties

bestowed upon the state through the Part-IV of the Constitution – the duties which

are considered to be the heart and soul of our constitution. A meticulous and

threadbare discussion is necessary.

15. The W.B. Estates Acquisition Act, 1953 (shortly noted hereinafter as EA Act) as

originally enacted did vest the interest of estate holders and tenure holders only,

they being true intermediaries. In view of definition of intermediary in sec. 2(i) of

the W.B. Estates Acquisition Act, 1953 neither a raiyat under EA Act nor a non-

agricultural tenant under WBNAT Act, 1949, was an intermediary. It was because

estate or right in an estate referred to in Art. 31A, Constitution of India, then could

not embrace the rights and interests of raiyats and under- raiyats or of non-

agricultural tenants or non-agricultural under tenants. The 4th Amendment of the

Constitution of India put the interest of raiyats and under- raiyats at per with

Page 18 of 56

tenure holders. The W.B. Estates Acquisition Act was radically amended thereafter.

The chapter-VI was introduced in the Act. This chapter-VI and the 4th Amendment

of the Constitution vested the interest of raiyats and under- raiyats in the state

subject to right to retain Khas land to the permissible limit. This vesting took effect

from 14.04.1956.

But as to non-agricultural tenants or non-agricultural under tenants they were

neither intermediaries nor there was any provision to treat them as if they were

intermediaries. The result was that the interest of non-agricultural tenants governed

by the West Bengal Non-Agricultural Tenancy Act, 1949 did not vest and they could

hold lands without limit. Only the proprietary right of the intermediary in the non-

agricultural lands vested in the state u/s 4 of the WBEA Act.1953.

The West Bengal Estates Acquisition Act did not impose any ceiling limit on non-

agricultural land held by non-agricultural tenant as per provisions of WBNAT Act,

1949 although the same (EA Act) applied to all classes of land so far as abolition of

intermediaries are concerned. The WBLR Amendment Act’ 81 sought to break

concentration of non-agricultural lands as material resources of the community and

means of production. The definition of land existing in the L.R. Act also prior to

Amendment Act, 1981 could not cover non-agricultural land and could not prescribe

any ceiling on non-agricultural lands as well as lands held by non-agricultural tenants

governed by the WBNAT Act’ 49, so far. Both the E.A. Act and the L.R. Act unduly

discriminated the owners of agricultural lands when compared with the owners of

non-agricultural lands. The WBLR (Amendment) Bill, 1981 intended to do away with

such discriminations / disparities.

The WBLR (Amend) Act’ 81 was brought on the statute for twin purposes with

retrospective effect from 07.08.69. The purposes were (i) to bring all types of land

including non-agricultural land irrespective of classification, under the fold of the

WBLR Act and (ii) to net in the non-agricultural tenants so far governed by the

WBNAT Act’ 49 under its purview. Purpose (i) was served by the provisions of the

WBLR Amendment Act’ 81. Some inherent difficulties, however, crept in to make the

purpose (ii) effective.

Page 19 of 56

These difficulties experienced in respect of purpose (ii) were sought to be

removed by amending sec. 3A as was introduced in the WBLR Act by the West

Bengal Land Reforms (Amend.) Act, 1981, by subsequent amendment i.e. by the

WBLR (3rd Amend) Act, 1986. Non-agricultural lands (the deemed estates), of non-

agricultural tenants (the deemed intermediaries), vested in the state with effect

from 09.09.80 free from incumbrances by insertion of such modified Sec. 3A in the

WBLR Act. Sections 61 to 63 introduced by the WBLR (Am) Act, 1981 were made

parts of the main Act. i.e the WBLR Act. , 1955 w.e.f 07.08.1969. The WBNAT Act.,

1949 stood repealed from 07.08.1969. All classes of lands are now intended to be

calculated within the same ceiling limit.

16. The concept of payment of compensation, if the land is not acquired by the State

for public purpose from within the ceiling, has become an old chapter now after

introduction of 2nd proviso to Article 31A(1) by the Constitution (17th Amendment)

Act, 1964 (Shortly CA17). Section 14V of the West Bengal Land Reforms Act

provides for basis of calculating amount for vesting of land in excess of ceiling.

In terms of this Section the State Government shall pay for vesting of any

land in the State under the provisions of this Act after possession of such land is

taken under Sub-section (3) of Section 14T, to the person or persons having any

interest therein, an amount equal to 15 times the land revenue or its equivalent

assessed for such land or where such land revenue has not been assessed or is not

required to be assessed, an amount calculated at Rs.135/- for an area of 0.4047

hectares.

The basis of calculation of amount for vesting of land in excess of ceiling was

there in the WBLR Act when vesting of non-agricultural lands of Non-agricultural

tenants governed by the WBNAT Act, 1949 was out of the purview of the WBLR Act.

It is for the 1st time in the land tenure history of West Bengal, the Non-agricultural

tenants under the WBNAT Act, 1949 have been brought under the definition of

intermediary to abrogate their rights to hold limitless Non-agricultural land and to

bring them under the ambit of ceiling prescribed in the WBLR Act under Section

14-M by insertion of Section 3A in the main Act by WBLR (Amendment) Act, 1981.

Page 20 of 56

Section 61 to 63 were inserted in the WBLR Act 1955 and the WBNAT Act, 1949

stood repealed w.e.f. 07/08/1969 by Section 63 so inserted. The Section 3A as

subsequently modified by the WBLR (Amendment) Act, 1986, makes an independent

provision for vesting of all rights and interests of NATS and under tenants governed

by the WBNAT Act, 1949. The WBLR (3rd Amendment) Act fixes a specific date i.e.

09/09/1980 on which this Section 3A shall be deemed to have come into force and

shall have the effect of vesting of the rights of Non-agricultural Tenants (NAT.s)

and under tenants to the State. This Section 3A is substantially similar to and

comparable with Section 52 under Chapter VI of the WBEA Act, 1953.

17. By Section 3A of the WBLR Act the non-agricultural lands (the deemed

estates) of the NAT.s ( the deemed intermediaries), vested in the State and the

operation of Section 5 and 5A of the WBEA Act, 1953 were made applicable, mutatis

mutandis, to non-agricultural tenants under the WBNAT Act, 1949.

Section3A of the WBLR Act speaks as follows:-

‘3A. Rights of non-agricultural tenants and under tenants in non-agricultural land to

vest in the State –

(1) The rights and interests of non-agricultural tenants and under tenants under

the WBNAT Act, 1949 (WB Act – XX of 1949) shall vest in the State free from all

encumbrances, and the provisions of Sections 5 and 5A of the WBEA Act, 1953

(W.B. Act – 1 of 1954) shall apply, with such modifications as may be necessary,

mutatis mutandis to all such non-agricultural tenants and under tenants as if such

non-agricultural tenants and under tenants were intermediaries and the lands held by

them were estates and a person holding under a non-agricultural tenant and under

tenant were a raiyat.

Explanation:- Nothing in Section 5 and 5A of the WBEA Act, 1953 shall be

construed to affect in any way the vesting of rights and interests of a non-

agricultural tenant or under tenant, under the WBNAT Act, 1949 in the State under

sub-section (1) of this Section.

xxxxx xxxxx xxxxx

(3) Every intermediary:-

Page 21 of 56

(a) whose land held in his khas possession has vested ion the State

under Sub-section (1) or

(b) whose estates or interests, other than land in his khas possession

have vested in the State under sub-section (1) shall be entitled to

receive an amount to be determined in accordance with the

provisions of Section 14V.

xxx xxx xxx

(5) This section shall be deemed to have come into force on and from the 9th

Sept,1980.

For vesting of excess Non-agricultural land in Khas possession held u/s 3A (3)

subject to right for retention as raiyat up to permissible ceiling prescribed in

Chapter – IIB and also for vesting of tenanted lands held u/s 3A (3), w.e.f 09.09.80,

every Non-agricultural tenant –cum- intermediary is entitled to receive amount as

per calculation u/s 14-V of the WBLR Act. No separate norm has been fixed for

determination of Amount for vesting of such Non-agricultural lands. Rather, the

criteria fixed for giving the ‘amount’ for vesting of ceiling excess agricultural lands

has been made applicable for Non-agricultural lands.

18. The First Amendment introduced Article 31A into the Constitution with

retrospective effect as well as Article 31B. Art.31A of the constitution provides that

a law in respect of the acquisition by the State of any estate or of any rights

therein or the extinguishment or modification of any such rights shall not be deemed

to be void on the ground that it is inconsistent with or takes away or abridges any of

the rights conferred by Art.14, Art.19 or Art.31.

About Art.31A the court said :-

“……………………if Article 31A were not enacted some of the main purposes of the

Constitution would have been delayed and eventually defeated and that by the first

Amendment the Constitutional edifice was not impaired but strengthened.” Waman

Rao versus Union of India (AIR 1981 SC 283 and 284)

Page 22 of 56

The Fourth Amendment amended the First Amendment. Article 31A(1)

obliterates Articles 14, 19 and 31 totally and completely for the laws falling within its

scope. In this connection, the Court stated:-

“…………………….every case in which the protection of fundamental right is

withdrawn will not necessarily result in damaging or destroying the basic structure of

the Constitution. The question as to whether the basic structure is damaged or

destroyed in any given case, would depend upon which particular Article of Part III is

in issue and whether what is withdrawn is quintessential to the basic structure of the

Constitution.”

19. Art. 31-B along with 9th Schedule was added in the Constitution by the

Constitution (1st Amendment) Act, 1951 (CA1). Art. 13(2) of the Constitution

invalidates a law inconsistent with a Fundamental Right. Art. 31B extends a

protective umbrella to such a law, if it is included in the 9th schedule. Art. 31B is, in

substance and reality, a constitutional device employed to protect State laws from

being declared void under Art. 13(2). Art. 31B is retrospective in nature. When a

statute declared unconstitutional by a court is later included in the 9th Schedule, it is

to be considered as having been in that Schedule from its inception. A blanket

protection is given to the statute mentioned in the 9th schedule, however violative of

Fundamental Rights it may be. Even when an Act is declared unconstitutional, it is

revived as soon as it is included in the 9th Schedule.

9th Schedule is an interesting innovation in the area of Constitutional

Amendments. A new technique of bypassing judicial review was initiated. Any act

incorporated in the 9th Schedule became fully protected against any challenge in

court of law under any Fundamental Right. Even an Act declared invalid by a court

becomes valid retrospectively after being incorporated in the 9th Schedule.

To begin with only Acts abolishing Zamindary were included in the Schedule.

Thus only 13 State Acts named therein were put beyond any challenge in courts for

contravention of F.R. s . But Schedule IX swelled and swelled in course of time as all

kinds of statues have been included therein to protect them for judicial review.

Hence, it was held that the Acts and Regulations included in the 9th schedule would

Page 23 of 56

not receive the protection ipso facto. Each law has to be examined individually for

determining whether the Constitutional amendments by which it has been put in the

9th schedule, damages or destroys the basic structure of the constitution in any

manner. There is no justification for making the additions to the 9th schedule with a

view to conferring a blanket protection on the laws included therein. The Apex Court

held, “The various constitutional amendments, by which the additions were made in

the 9th schedule on or after April 24, 1973, will be held valid only if they do not

damage or destroy the basic structure of the constitutions.”- Waman Rao, -V- Union

of India, AIR 1981 SC at 283-284.

20. A brief setting & origin of the Art. 31C is contained in the Objects and Reasons

of the Constitution (25th Amendment) Act, 1971, which shows that the amendment

was introduced with the main object of getting over the difficulties placed in the

way of giving effect to the Directive Principles (D.P.s) of State policy. In other

words, while Art. 31C permitted the Parliament to make any law giving effect to the

policy of the State towards securing the principles contained in clause (b) and (c) of

Art. 39, such law could not be declared void even if such a course of action violates

or abridges any of the rights conferred by Art. 14, 19 or 31.

Another crucial stage in this history of Art. 31C arose when the famous CA42

was passed by the Parliament. Whereas in the 25th amendment, the protective

umbrella given by the Constitution was restricted to laws passed only to promote

objects in clause (b) & (c) of Art. 39, by virtue of 42nd amendment the limitations

which were confined to Clause (b) & (c) of Art. 39 were taken away and the Art. was

given a much wider connotation. A complete, irrevocable and impregnable

constitutional protection was given to the laws passed to implement the Directive

Principles contained in all the clauses laid down in Part IV of the Constitution. By

legislating the Acts or laws giving effect to all or any of the principles laid down in

Part-IV of the Constitution would be protected by the umbrella contained in Art. 31C

and would be immune from challenge on the ground that they were violative & Art. 14

& 19.

Taking into consideration the decision passed by the S.C. in the cases.:-

Page 24 of 56

1. Kesavananda Bharati Vs. State of Kerala, AIR 1973, SC 1461

2. Minerva Mills Ltd. Vs. Union of India, AIR 1980 SC 1789.

3. Womman Rao Vs. Union of India AIR 1981 SC 271. &

4. Sanjeev Coke Co Vs. Bharat Coking Coal Co. AIR1983 SC 239;

the Constitutional Bench, of the Apex Court, constituting of 5 Judges, held on

31.10.1983 in State of Tamil Nadu Vs. Abu Kavur Bai & Ors. AIR 1984 SC 326 334,

“(i) Art. 31 C, as introduced by the 25th Amendment is constitutionally valid in

all respects.

(ii) An important facet of Art. 31C, is that there should be a close nexus

between the statute passed by the legislature and the objects mentioned in clauses

(b) & (c) of Act. 39…………………………. If the nexus is present in the law, then the

protection of Act. 31C becomes complete and irrevocable. Furthermore, a

declaration in the Act regarding the purpose mentioned in Art. 39 (b) & (c) may

generally be evidence of the nexus between the law and the objects of Art. 39(b) &

(c)”.

On the question whether compensation is necessary to be given in a case where

Art. 31C applies, the Court further held,

“(iii) If Art. 31C is taken, to exclude Art. 31(2) the question of compensation

becomes irrelevant and otiose.

(iv) In view of Art. 31C, the court cannot strike down the Act merely because

the compensations for taking over the transport services or its units is not provide

for.

(v) That in view of the express provisions of 31C which excludes Art. 31(2)

also, where a property is required is public interest for the avowed purpose of giving

effect to the principles enshrined in Art. 39(b) & (c), no compensation is necessary

and Art. 31(2) is out of harm’s way.

(vi) That even if the law provides for compensation, the court cannot go into

the details or adequacy of the compensation and it is sufficient for the state to

prove that the compensation was reasonable and not monstrous or illusory so as to

shock the conscience of the court.”

Page 25 of 56

The court further observed,

“Once Art. 31C applies, the net of the protective umbrella is so made as to cut

at the root of even Art. 31(2) which alone survives after Bharati’s case.

Art. 31C by virtue of 25th Amendment has knocked out the word ‘compensation’

and has substituted the word ‘amount’ which gives ample discretion to the state to

fix a reasonable amount if the property of an individual is taken over for public

purpose. ……………… Even an apology for public purpose would be sufficient to

comply with the conditions required by Art. 31(2)”.

Mentioned that all the above decisions and observations were made in 1983

taking into consideration that Art. 31(2) was in existence. The extent & purport of

remarks is easily understandable when the Art. 31(2) is nowhere in the Constitution.

21. The ostensible purpose of repealing Art. 31 & 19 (1) (f), specially Art. 31(2) is

to free the legislature from the restraint of paying any amount for vesting of the

land being ceiling surplus by regulatory / prohibitory laws to effectuate Directive

Principles. Such laws may be enacted by the State legislature under Entry 18, List II

of the 7th Schedule. If such laws are protected by Art. 31A(1)(a), Art. 31B and / or

by Art. 31C, they become immune from challenge even if no compensations /

amount is provided as held by the Apex Court in the State of Kerala V Gwalior Rayon

& Silk Mfg. Co. Ltd., AIR 1973 SC 2734, 2751., State of Tamil Nadu Vs. L. Abu Kavur

Bai & ors. AIR 1984 Sc. 326, 334.

The WBEA Act was enacted for abolishing of all intermediaries and acquisition

of their rights in estates by the State. The concept was ‘acquisition’. The field of

legislation may be debated as to whether it was under Entry 18 of list II or under

Entry 42 of list III or under both of the 7th schedule. All the intermediaries were

affected/ abolished. But for vesting of lands by application of WBLR Act, only those

raiyats having ceiling excess lands are affected. Here, the concept of WBLR Act, is

only ‘modification’ of the rights over ceiling surplus land held by raiyats. Here, the

field of legislation exclusively under Entry No 18 of list 7th of the II schedule. The

concept of acquisition has now been totally shifted to Entry 42, List –III of the 7th

schedule w.e.f. 20.04.1964, the date of coming into force of CA17 under the

Page 26 of 56

legislative powers conferred by Art 246 of the constitution. Now, ‘acquisition’

means compulsorily taking property by the state by the power of Eminent Domain in

Entry 42, List-III when such property falls within the ceiling prescribed by the Spl.

Law enacted to effectuate Directive Principles.

The Apex court was so long holding the view that even amount not being

arbitrary/illusory , was payable to the land owner/ property holder for vesting of

their right over land held in excess of ceiling prescribed by statue as because the

rights to receive such amount was existing u/A 31(2) as Fundament Right under the

constitution. Now, Art 31(2) is no longer in existence. When the Art. 31(2) was in

force, a person could be deprived of his property right u/A 31(1) now transformed

into Art 300A. Hence, it may be logically concluded that no raiyat is entitled to get

any amount for vesting of his ceiling surplus land by a statute manifestly and

pointedly made for the purpose of giving effect to and serving the object of Art

39(b) & (c) and if such statute falls within the letter and spirit of Art 39(b).

22. i) Before 4th Amendment ‘adequate’ and ‘just’ compensation was payable for

acquisition / deprivation of property guaranteed as Fundamental Rights as Art. 31(2)

/ 31(1) was there in the Constitution.

ii) After 4th Amendment compensation was payable only if land was

compulsorily acquired by the State for public purpose u/A 31(2) and not for

deprivation of property u/A 31(1). Adequacy of compensation was also made non-

justiciable.

iii) After 17th Amendment compensation at least at market price was payable

only for acquisition / compulsory acquisition of land within the ceiling under the 2nd

proviso of Art. 31A(1) read with Art. 31(2). Though adequacy of compensation was

made non-justiciable, state was under obligation to compensate a person for

acquisition of land in excess of ceiling, as in the amended Art. 31(2) containing the

word ‘compensation’ was still retained in the Constitution even after 17th Amendment.

iv) After insertion of Art. 31C by 25th Amendment the word ‘compensation’ was

knocked out by the word ‘amount’. Now the Hon’ble Supreme Court interpreted that

word ‘amount’ was not the same concept as ‘Compensation’. Nevertheless, the

Page 27 of 56

principles of ‘amount’ payable should not be ‘arbitrary’ or illusory as the right to

receive the amount was linked still with the Fundamental Right in Art. 31(2). It was

emphasized by Shelat & Grover, JJ in Kesavananda case that “the right to receive

the amount continues to be the Fundamental Right” under Art. 31(2) and, in a

democracy, legislature cannot use its power in an arbitrary manner.

v) By the 44th Amendment the Art. 31(2) has been deleted and the Art. 31(1)

has been transformed as Art. 300A. The ostensible purpose of repealing Art. 31

specially 31(2), is to free the legislature from the restraint of paying amount of

property acquired, if held in excess of ceiling fixed by a statute.

vi) When the acquisition of land within the ceiling for public purpose is under

contemplation, then only question of payment of compensation, at least at market

value, arises as provided in the 2nd proviso of Art. 31A(1). Such acquisition is made on

the basis of an enactment made under Entry-42, List-III of the 7th schedule under

the rule making powers of the state under Art. 246. ‘Public purpose’ and

‘compensation’ – the two essential elements / ingredients and inseparable

concomitants are linked with the concept of Eminent Domain. Indian version of

Eminent Domain is found in Entry 42, List-III which says ‘acquisitioning and

requisitioning of property’. The ideas of ‘public purpose’ and ‘compensation’ are thus

inherent in Entry 42, List –III of the 7th Schedule. State of W.B. Vs Union of India,

AIR 1963 SC 1241.

vii) If the payment of amount is linked with Art. 31(2) for vesting of ceiling

surplus land under special Act like WBLR Act, question of paying of amount does not

arise at all as the Art. 31(2) has now become non-existent and as the Act on agrarian

reforms enjoys the protective umbrella of Arts. 31A, 31B & 31C of the Constitution

and cannot be declared ultra-vires.

WBLR Act is a special regulation on Agrarian Reforms to effectuate Directive

Principles underlying Arts. 39(b) & 39(c). One of the purposes of the WBLR Act is to

vest lands held in excess of ceiling by a raiyat. To vest such ceiling surplus land as a

measure to consolidate lands relating to land reforms is not an Act on acquisition.

Rather, the enactment is for ‘modification’ of rights of raiyats in land within the

Page 28 of 56

meaning of Art. 31A (1) (a) in respect of ceiling surplus lands without adopting the

procedure of acquisition. For such vesting of ceiling surplus land the State cannot

perhaps be forced to pay any ‘amount’ which was so long based on Art. 31(2) now

stands repealed after 44th Amendment. Here the field of legislations is connected

under Entry 18, List –II of the 7th Schedule.

23. The WBLR Act is a piece of social legislation for agrarian reform. The object

of the legislation is to break up the concentration of ownership and control of the

material resources of the community and to so distribute the same as best to sub-

serve the common good, as enjoined by Art. 39(b) of the Constitution. Having regard

to the quantity of land available in the State of West Bengal, which has the highest

per capita density in the whole of the country, the ceiling limits appear to be

reasonable and fair. For equitable distribution of natural resources, it was essential

to design the act as it is so that the surplus land is available for distribution to the

landless peasantry. The Act makes available to each person of the community living

below the poverty line, to some extent the minimum means of subsistence. In order,

therefore, to reconcile the fundamental rights of the community as a whole with

the individual rights of the more fortunate section of the community, it was

fundamentally necessary to make the impugned legislation to secure to a certain

extent the rights of that part of the community which is denied its legitimate share

in the means of livelihood.

The broad objectives of any legislation relating to agrarian reforms are materially

four viz., (1) to maximize the agricultural output and productivity, (2) a fair and

equitable distribution of agricultural income, (3) increase in employment

opportunities, and (4) a social or ethical order. Though the abolition of the Zamindari

system in the State of West Bengal was an important step forward, the feudal

structure remained so far as the peasants were concerned. These objectives have

been achieved through progressive legislation like WBLR Act, 1955 together with its

amendments specially amendments of ‘81 and ’86 in achieving the policy of the

Articles 39(b) and 39(c) of the Constitution of India.

Page 29 of 56

24. In the matter of Paschim Banga Bhumijibi Krishak Samity – Vs. – State of

West Bengal, 1996 W.B.L.R. (Cal) 242, the Hon’ble Divn. Bench, Cal. H.C. made the

following observations and comments amongst others.

i) 1981 Amendment Act was sought to be used as complementary to the WBEA Act,

1953 as that Act would not impose any ceiling limit for others classes of land though

the same applied to all classes of land ( Para-153).

ii) It is not disputed that the object of the Amending Acts, of 1981 & 1986 if upheld,

would be for public purpose. The only question, therefore, is as to whether just

compensation is required to be paid or not. (Para-69)

iii) By reason of 1981 Amendment Act, Sec. 2(7) has undergone a drastic change

which brings within its purview, lands of every description (Para-33).

iv) In terms of Item No. 18 of the List-II of the 7th Schedule of the Constitution of

India there cannot be any doubt that the state has the legislative competence to

make any legislation both in respect of agricultural land as also non-agricultural land.

(Para-34).

v) It is not disputed that although in terms of the provisions of the Permanent

Settlement Regulation, 1973 (Bengal Code No. 1 of 1973) there existed no distinction

between an agricultural land or a non-agricultural land, it is beyond any cavil of doubt

that agricultural land and non-agricultural land became subject matter of separate

Laws as the purpose of such tenancies were different. At that relevant time such

distinction was irrelevant as all lands belonged to the zamindars. However, the

nature of tenancy would depend upon the terms of grant by the Zamindars to the

tenants. Agricultural lands were governed by the provisions of the B.T. Act whereas

Non.-Agricultural lands were governed by the provisions of Transfer of Property Act

and the provisions of Non-Agricultural Tenancy Act, 1949. (Para-30).

vi) By reason of Sec. 63 which was inserted by the W.B.Act No. L of 1981 published

in the gazette dt. 24.03.1986 with retrospective effect from 07.08.1969, provision

of the WBNAT Act was made inapplicable (Para-36).

vii) The said Act (1981 Amendment Act) has to be construed in the light of the

WBEA Act as also Urban Land Ceiling Act. (Para-44).

Page 30 of 56

viii) In view of the definition of the vacant land as contained in Sec. 2(q) of the

Urban Land Ceiling Act, vacant land shall not include (Para 41):-

(1) Lands mainly used for the purpose of Agriculture.

(2) Lands on which constructions are not permissible under rules.

(3) Lands occupied by building with sanction where such rule exists.

(4) Land occupied by building where no such rule exits, and

(5) Cattles’ Space in a Village within urban agglomeration

ix) The provisions of the WBLR Act have no application in respect of matters

covered by Urban Ceiling Act. However, it is made clear that the said Act will have

application to agricultural lands situated within the said Area.(Para-50)

x) In terms of Sec. 2(7) of the said Act land includes lands of every description

which in turn includes the lands which are saved by reason of the provision of the

Urban Ceiling Act. (Para-42)

xi) Whereas in terms of the Urban Ceiling Act buildings and other structures are

exempted from the purview of Urban Ceiling Act, the same comes within the purview

of Sec. 3A as also Chapter-IIB of the said Act (Para-43).

xii) The liability to pay land revenue was introduced by way of Sec. 22 and 23 of the

WBLR Act which came into force w.e.f. 25.09.1965 by the WBLR (Amend.) Act 1965.

Prior thereto, in terms of Sec. 40 & 41 of the WBEA Act, the land revenue was

payable at Rs. 9/- per acre. Thus, Rs. 135/- was fixed as compensation being 15

times the land revenue i.e. Rs. 9/- per acre payable under the WBEA Act. (Para 86 &

87).

xiii) Sec. 14V of the said Act provides for the basis, the principles of computing the

compensation as being the 15 times the land revenue or at a rate of Rs. 135/- per

acre of land. (Para -86).

xiv) Sub. Sec. (3) of Sec. 3A of the said Act provides for entitlement on the part of

the intermediaries to receive an amount to be determined in accordance with the

provision of Sec. 14V. In view of the definition of land as contained in Sec. 2(7) of

the Act, therefore, compensation at the same rate would be payable for all types of

land. It may be noticed that there was no provision for payment of land revenue in

Page 31 of 56

respect of non-agricultural lands and rent used to be paid in terms of the agreement.

(Para-88).

xv) the land revenue ex-facie, therefore, cannot be the basis for computing the

amount of compensation for acquisition and the lands falling under the non-

agricultural tenancies, buildings, factories etc. because land revenue was payable by

an estate and in terms of the provision of the WBEA Act, vis-à-vis the said Act, land

revenue was to be paid in respect of agricultural land only. There cannot, therefore,

be any doubt whatsoever that in case of non-agricultural land or a building or a

factory, adoption of land revenue as computing the amount payable by way of

compensation is not a relevant criteria and, thus, must be held to be illegal (Para-89).

xvi) Having not laid down different principles for payment of compensation on

different types of land and keeping in view the definition of land, encompassing land

of every description and keeping in view the patent absurdity in computation of the

valuation the onus shifts to the state to show that the valuation is reasonable. (Para-

100).

xvii) A person holding vacant land in an urban agglomeration will get compensation in

terms of Sec. 11 of the Urban Ceiling Act whereas persons holding similar types of

land just beyond the periphery of urban agglomeration will not get even a fraction of

such compensation. (Para-102).

xviii) For the reasons aforesaid, we have no other option but to hold that he

provisions of Sec. 14V vis-à-vis the definition of land as contained in Sec. 2(7) and

Sec. 3A (3) of the said Act is ultra-vires Act. 300A of the constitution of India.

(Para-111).

From the observations it is clear that the Hon’ble Divn Bench, Calcutta has

declared the amount for Sec. 3A(3) component of land as defined in Sec. 2(7) as

ultra-virus and Sec. 3A(3) component of land includes lands belonging to non-

agricultural tenant and non-agricultural under – tenant who was so long governed by

NAT Act, 1949.

25. Art. 31A (1) (a) envisages:

i) Acquisition by the state of estate or any rights therein; or

Page 32 of 56

ii) Extinguishment of the rights of the holder; of

iii) Modification of any such right.

‘Acquisition’ involves transfer of ownership of the property to the state or a

corporation owned or controlled by it. ‘Extinguishment’ signifies complete

termination of the rights which can be effectuated without acquisition by the state.

In ‘modification’ also the state is not the beneficiary

“A law fixing ceiling agricultural land is protected by Art. 31A (1) (a).”

(Atma Ram –V-State of Punjab AIR 1959 SC 519; Kunjakutty –V- State of

Kerala AIR 1972 SC 2097; Ambika Prasad –V- State of U.P. AIR 1980 SC 1762.)

“Again, a law abolishing big landed estates is also protected by Art. 31A(1) (a).”

(Jadab Singh-V- Himachal Pradesh Admn. AIR 1960 SC 1080.)

The word ‘acquisition’ appearing in the WBEA Act and the word ‘Vesting’

appearing in the WBLR Act are apparently similar; but there are differences

between the Acts. Some of the salient differences are tabulated hereunder.

The West Bengal Land

Reforms Act, 1955

(Shortly LR Act)

The West Bengal Estates Acquisition Act,

1953(Shortly EA Act)

1. The field of legislation is

entirely and exclusively

under Entry No. 18, List –

II of the 7th Schedule

under Art. 246

The field of legislation for acquisition fall is

under Entry No. 42 List –III as well as Entry

No. 18, List –II of the 7th Schedule under

Art. 246.

2. The L.R. Act is an Act to

reform the land relating

to land tenure consequent

on the vesting of all

estates. It is an Act to

fix ceiling on land holding

by raiyats. It is an Act

The EA Act was made with the sole object of

abolition of all intermediaries and for

acquisition of their estates and of rights of

intermediaries therein. Proprietary rights

vested in the state by statutory observation

subject to their rights for retention.

Page 33 of 56

for ‘modification’ of

rights of raiyats in the

estate without involving

the provisions of

acquisition. ‘Modification’

in the sense that a raiyat

is not entitled to own the

entire lands under his

possession but only to the

extent permissible in

ceiling. It aims at

distributing ceiling surplus

lands amongst the poor,

landless and others. It

takes care for protection

of bargadars / SC & ST

people. It modifies the

right of tenants so far

governed by the WBNAT

Act, 1949

3. Here the concept of

taking over ceiling surplus

land is ‘vesting’ and not

‘acquisition’. It is dynamic

Act. The obligation for

which ‘amount’ was payable

was the existence of Art.

31(2). The right to

receive the ‘amount’ not

even being adequate or

Here the concept of taking all lands was

acquisition on payment of compensation. For

acquisition of estates under the EA Act, the

obligation of payment of compensation was

there in the statute. The 2nd proviso of Art.

31A(1) was not there in the constitution when

the EA Act was implemented. The obligation

for which compensation was payable was the

existence of Art. 31(2) as a Fundamental

Right. It is a static Act / one day Act. The

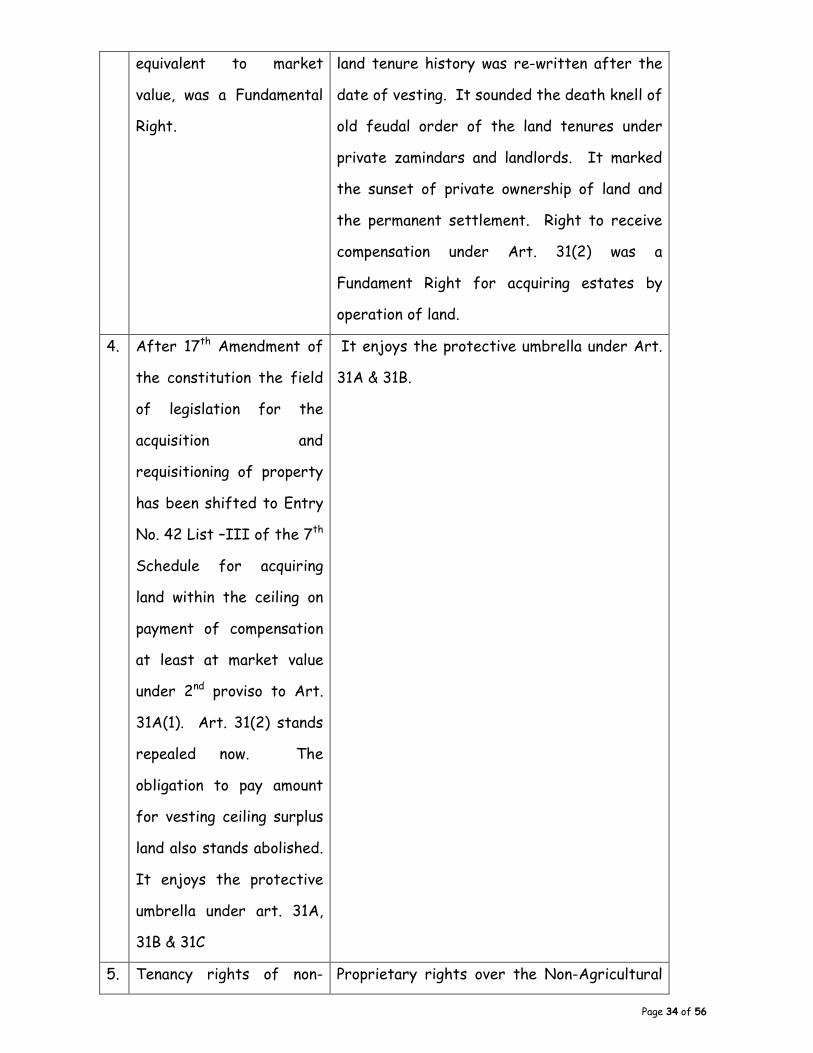

Page 34 of 56

equivalent to market

value, was a Fundamental

Right.

land tenure history was re-written after the

date of vesting. It sounded the death knell of

old feudal order of the land tenures under

private zamindars and landlords. It marked

the sunset of private ownership of land and