Werner Enterprises -...

26

Werner Enterprises 34 th Annual Institutional Investors Conference March 4, 2013

Transcript of Werner Enterprises -...

Werner Enterprises

34th Annual Institutional Investors Conference

March 4, 2013

This presentation includes forward-looking statements,

within the meaning of the Private Securities Litigation

Reform Act of 1995. These statements are based on

Werner Enterprises’ current plans, and are not guarantees

of future performance. They are subject to risk and

uncertainties, that could cause actual results, and

company plans and objectives, to differ materially from

those expressed in the forward-looking statements.

Such risks and uncertainties are discussed in the

Company’s Annual Report, on Form 10-K, filed with the

SEC.

DISCLOSURE STATEMENT

1 1

H Premium Truckload Transportation and Logistics Services Provider

2012 Revenue: $2.0 Billion

2012 Net Income: $103 Million

NASDAQ: WERN

Market cap: $1.7 Billion

2012 Quest for Quality Multiple Award Winner in Truckload and 3PL Logistics

ABOUT WERNER ENTERPRISES

2 2

1980

• Deregulation

1986

• IPO

1992

• GPS on all trucks

• Dedicated, Regional

and TC fleets formed

1998

• First to install

electronic driver

logs (EOBR)

1999

• Mexico launch

• Canada designated

fleet formed

2003

• Brokerage and

Intermodal expansion

2006

• Werner Global

Logistics formed

• China launch

2007

• LH fleet reduction

2009

• Safety improvement initiative begins

• Australia launch

2008

• Balanced portfolio

initiative begins

• Fuel MPG initiative

begins

1956

• Founded by

C.L. Werner

2012

• $103M earnings

(record high to date)

THE PATH OF WERNER PROGRESS

3

49% 51% 50%

26% 24% 24%

17% 16% 14% 8% 9% 12%

0%

10%

20%

30%

40%

50%

60%

2010 2011 2012

Retail/CP

Grocery Products

Manuf./Industrial

Logistics/Other% o

f R

evenues*

* top 50 customers

% o

f R

even

ue

s

Vertical:

Customers:

REVENUE SOURCES

5

27% 26% 25%

40% 40% 40%

60% 60% 61%

74% 74% 73%

0%

20%

40%

60%

80%

100%

2010 2011 2012

Top 5

Top 10

Top 25

Top 50

4

Truckload, $280B 37%

Dedicated (Private Fleet),

$277B 37%

LTL, $47B 6%

Rail carload, $56B 8%

Rail intermodal, $15B 2%

U.S. Freight Market Revenues

in billions of $*

* Sources: ATA and Stifel Nicolaus estimates

DOMESTIC FREIGHT MARKET:

MARKET SHARE & GROWTH OPPORTUNITIES

6

$0

$50

$100

$150

$200

$250

$300

TruckloadDedicated

Intermodal

$280B $277B

$15B

Re

ve

nu

e i

n b

illi

on

s

Werner Enterprises Growth Opportunities

Werner % Share Total Freight Market

5

Other

(Pipeline, Air, Water)

$73B

10%

Asset-

Lig

ht

Asset

• Freight Management

• Brokerage

• Intermodal

• Cross Border

• Global Logistics

ONE-WAY TRUCKLOAD

Regional Fleets

Temperature

Controlled

Medium / Long Haul

Team Werner

LOGISTICS

DEDICATED

Van

Temperature

Controlled

Flatbed

Network

Optimization

* Includes Cross Border Asset-Light (MX, CAN) >10% of Revenues

Goal 4Q12

1/3 26%*

1/3 38%

1/3 36%

7

REVENUE PROFILE

6

FREIGHT MARKET UPDATE

8 7

ONE-WAY

TRUCKLOAD

COMPREHENSIVE SOLUTIONS

8

Werner provides complete 3PL supply

chain solutions across all shipping modes

and geographies, from network design

through implementation.

Freight Management

With an asset-backed network of 7,150

trucks, 9,500 alliance carriers and ocean, air

and rail companies, Werner provides

unsurpassed delivery solutions worldwide.

Freight Movement

Providing door-to-door services for

companies of all sizes and industries as they

compete in today’s global marketplace,

sets us apart from our competition.

Global Implementation

Sophisticated technology tools

provide our customers instant visibility across

their supply chain, which enables them to

better manage their business.

Technological Advantages

FUEL PRICE TRENDS

10

$1.20

$1.40

$1.60

$1.80

$2.00

$2.20

$2.40

$2.60

$2.80

$3.00

$3.20

$3.40

$3.60

$3.80

$4.00

$4.20

$4.40

$4.60

$4.80

$5.00

Pri

ce

Pe

r G

all

on

(in

$)

2009 2010 2011 2012 2013

*Dept. of Energy (DOE) fuel price survey (Nat'l avg.) of truck stops used by shippers/carriers for billing fuel surcharges.

Fuel price includes fuel taxes.

1Q 2Q 3Q 4Q

9

GREEN INITIATIVES

10

Werner Enterprises is a SmartWaySM Transport partner. SmartWay is a collaboration

between the EPA and the freight industry, to increase energy efficiency and reduce air

pollution. Werner has earned a Shipper Index Factor score (SIF) of 1.25, the highest possible

score.

Fuel Efficiency Initiatives:

Aerodynamic Trucks

Installation of fuel idling reduction equipment, including Espar heaters and APU’s

MPH optimization

Out of route mile and empty mile reduction

Trailer skirts

Tire-inflation systems

Alternate Fuel Initiatives:

Testing LNG and CNG trucks

Werner’s Impact:

5 years of MPG improvement

Continued MPG improvement opportunities

150,000 ton reduction in carbon footprint from MPG improvement, last 3 years

0%

1%

2%

3%

4%

5%

6%

7%

8%

2007 2008 2009 2010 2011 2012

Hu

nd

red

s

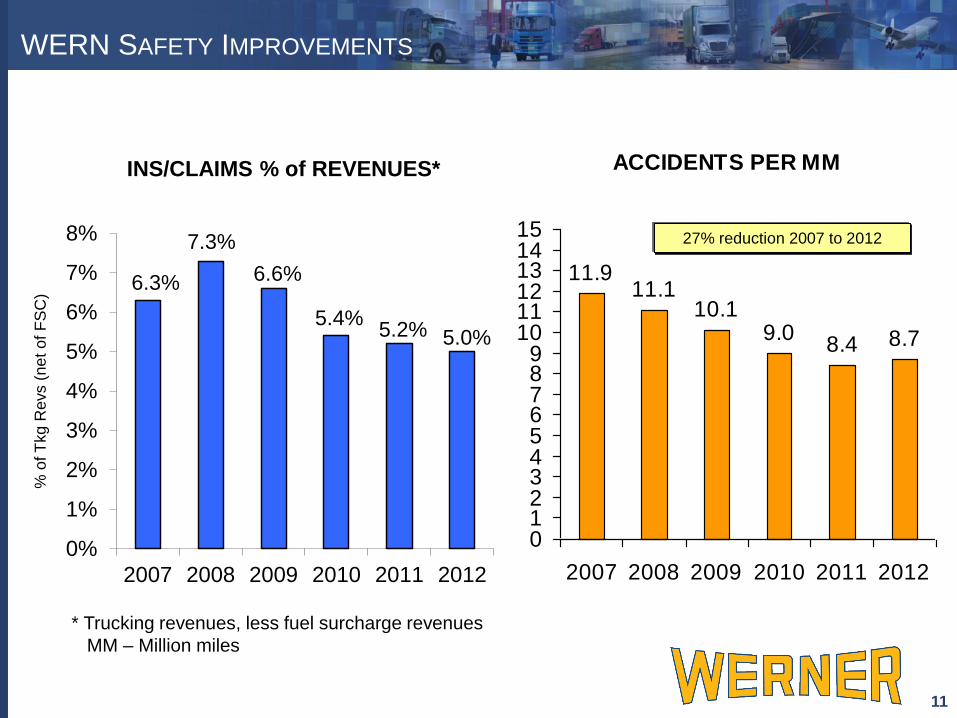

INS/CLAIMS % of REVENUES* ACCIDENTS PER MM

11.911.1

10.19.0

8.4 8.7

0123456789

101112131415

2007 2008 2009 2010 2011 2012

27% reduction 2007 to 2012

WERN SAFETY IMPROVEMENTS

12 11

* Trucking revenues, less fuel surcharge revenues

MM – Million miles

% o

f T

kg R

evs (

ne

t o

f F

SC

)

6.3%

7.3%

6.6%

5.4% 5.2% 5.0%

REGULATORY – HOS AND EOBR

12

HOS impact on shippers

Utilization decrease per tractor in the market

Decreased driver wage potential

Decreases capacity, increases the number of tractors needed to haul the same amount of goods

Overall impact, higher transportation costs

The FMCSA announced various changes

effective February 2012, with a compliance

date of July 2013.

Primary rule changes 34 hour restarts will

now need to include two consecutive periods

between 1 a.m. and 5 a.m. Mandatory break

period.

The latest highway reauthorization bill dubbed

Moving Ahead for Progress in the 21st Century Act

(MAP 21) was passed June 2012. EOBR mandates

in this bill states that all motor carriers that must file

a record of duty status (RODS), and will be required

to do so with an electronic logging device.

SUPPLY – CAPACITY

Source: KeyBanc

13

Including owner

operators, truckload

capacity at public

fleets is nearly 20

percent below peak

4Q06 levels

23,000

25,000

27,000

29,000

31,000

33,000

2Q

05

3Q

05

4Q

05

1Q

06

2Q

06

3Q

06

4Q

06

1Q

07

2Q

07

3Q

07

4Q

07

1Q

08

2Q

08

3Q

08

4Q

08

1Q

09

2Q

09

3Q

09

4Q

09

1Q

10

2Q

10

3Q

10

4Q

10

1Q

11

2Q

11

3Q

11

4Q

11

1Q

12

2Q

12

Total Public Truckload Fleet Capacity

3Q

12

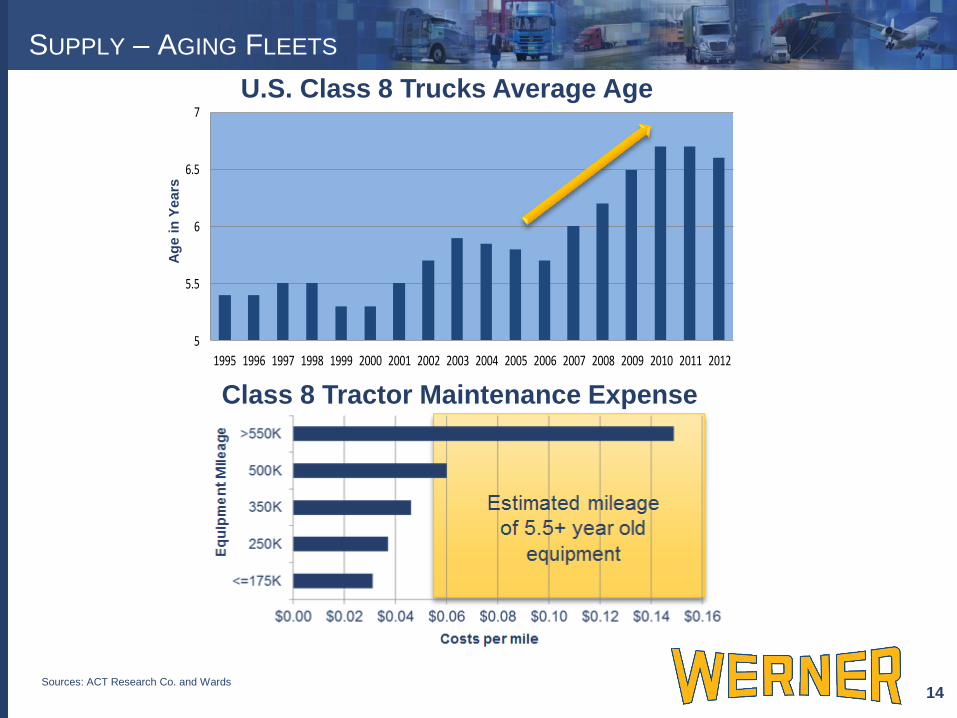

Sources: ACT Research Co. and Wards

SUPPLY – AGING FLEETS

14

U.S. Class 8 Trucks Average Age

5

5.5

6

6.5

7

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Ag

e i

n Y

ea

rs

Class 8 Tractor Maintenance Expense

DR

IVE

R

MA

RK

ET

15 Sources: BLS OES, ACT Research Co.

2010 U.S. Census Driver Age

Profiles

“…to attract the higher share of workers needed

for the 10 year growth projection, the trucking

industry must return to the wage position that

prevailed in the 1990s.”

- ATA

“Roughly 25 percent of the driver workforce

has been eliminated from the industry during

the past 10 years as a result of demographic

and health issues... the largest group of

drivers are aged 35 to 54.”

- Logistics Management

DRIVER MARKET

Driver Wages Relative to Food Prep

Workers

$0

$50

$100

$150

$200

$250

$300

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013 g

oal

Mill

ion

s o

f D

olla

rs

Cash Flow from Operations Cap Ex, Net

CASH FLOW AND CAP EX

15

* Increased cap ex in 2006 and 2007 prior to 2007 EPA engine emission change.

**Higher cap ex in 2011 and 2012 as we reduced the average age of our fleet from 2.8 years to 2.3 years.

*

16

*

$150M

$100M

**

**

ENHANCING SHAREHOLDER RETURN

16

$0

$20

$40

$60

$80

$100

$120

$140

$160

$180

$200

2006 2007 2008 2009 2010 2011 2012

Mil

lio

ns o

f $

$0.00

$0.25

$0.50

$0.75

$1.00

$1.25

$1.50

$1.75

$2.00

$2.25

$2.50

2006 2007 2008 2009 2010 2011 2012

Share repurchases

Dividends

Special dividends

$99M

$128M

$169M

$104M

$ Per Share

$1.28

$1.76

$2.36

$1.45 $130M

$1.80

Total 2006 - 2012: $ Per Share

Share repurchases $203M $2.72

Dividends $98M $1.38

Special Dividends $501M $6.95

$802M $11.05

17

$.70 $50M

$122M $1.70

-10%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

8%

10%

7,000

7,200

7,400

7,600

7,800

8,000

8,200

8,400

8,600

8,800

9,000

9,200

2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

% C

ha

nge

YO

Y

Ave

rage

# o

f Tru

cks

In S

erv

ice

Average # of Trucks in Service % Change YOY

Keep fleet count flat, focused on reaching TL

OI% target of 11%

TRUCKS

17 18

1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12

Miles Per Truck YOY Miles Per Truck % Change

MILES PER TRUCK TRENDS – LAST 16 QUARTERS

19

% C

ha

ng

e Y

OY

5%

4%

2%

1%

-5%

-4%

-3%

-2%

-1%

0%

3%

OP

IN

C -

% O

F R

EV

EN

UE

S

EP

S

$.10

$.15

$.22

$.29

$.18

$.29

$.38 $.42

$.26

$.33

$.40

$.34

$.25

$.33

$.40

$.35

$0.00

$0.05

$0.10

$0.15

$0.20

$0.25

$0.30

$0.35

$0.40

$0.45

2009 2010 2011 2012

1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q 1Q 2Q 3Q 4Q

OPERATING MARGIN TRENDS*

23

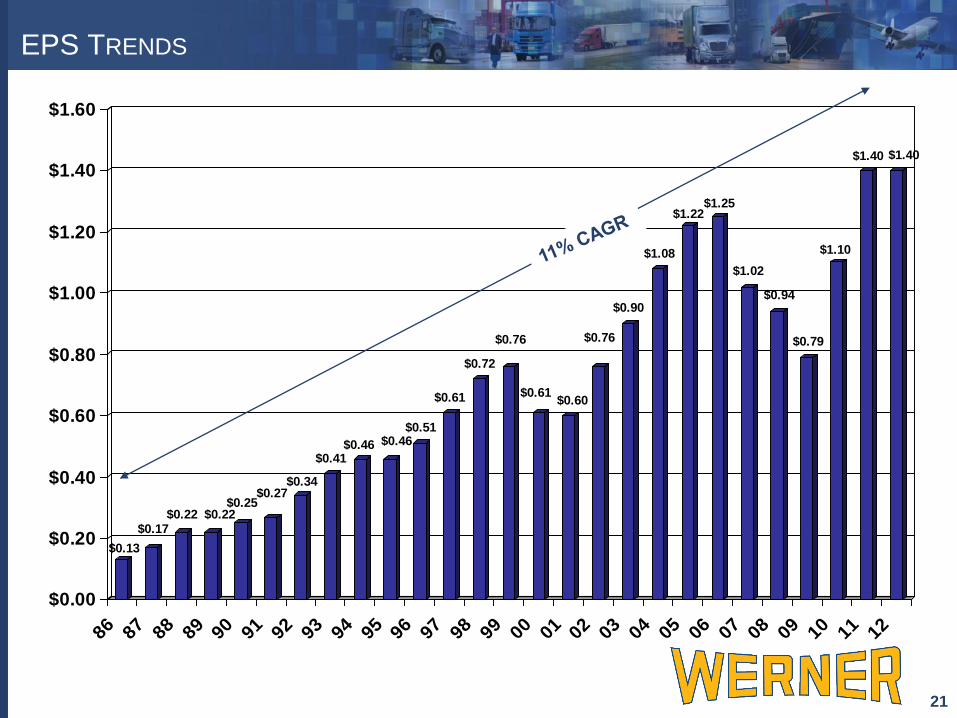

EPS TRENDS

* Total Company (Trucking and Logistics)

20

2

3

4

5

6

7

8

9

10

11

1Q 2Q 3Q 4Q

2009 2010 2011 2012

EPS TRENDS

24

$0.13

$0.17$0.22 $0.22

$0.25$0.27

$0.34

$0.41$0.46 $0.46

$0.51

$0.61

$0.72

$0.76

$0.61$0.60

$0.76

$0.90

$1.08

$1.22$1.25

$1.02

$0.94

$0.79

$1.10

$1.40 $1.40

$0.00

$0.20

$0.40

$0.60

$0.80

$1.00

$1.20

$1.40

$1.60

86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

21

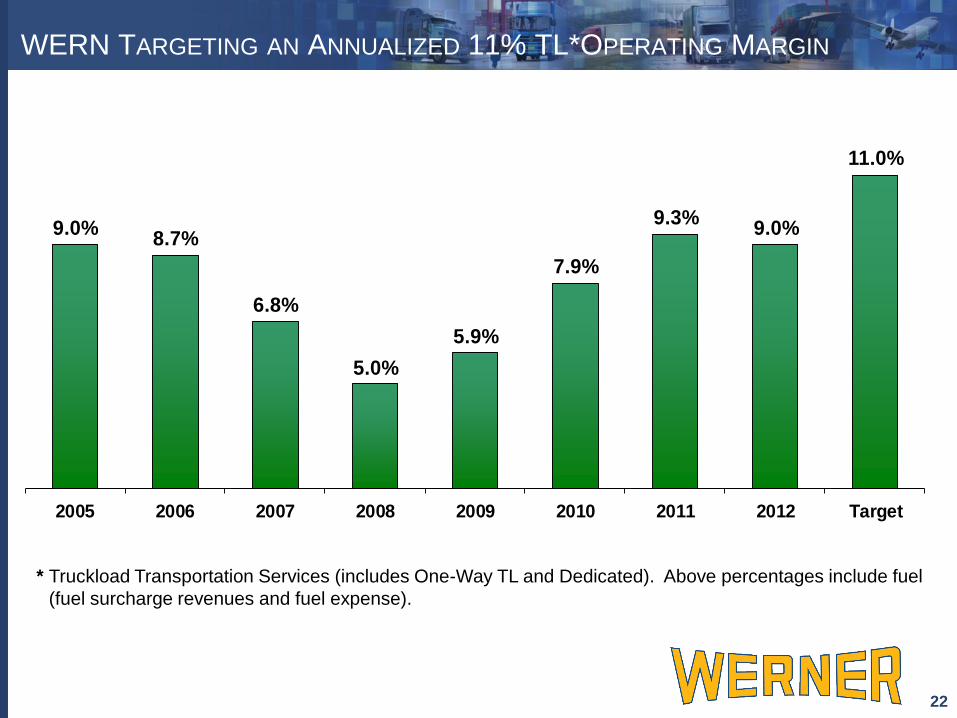

9.0%8.7%

6.8%

5.0%

5.9%

7.9%

9.3%9.0%

11.0%

2005 2006 2007 2008 2009 2010 2011 2012 Target

* Truckload Transportation Services (includes One-Way TL and Dedicated). Above percentages include fuel

(fuel surcharge revenues and fuel expense).

WERN TARGETING AN ANNUALIZED 11% TL*OPERATING MARGIN

25 22

11.3%8.8% 8.1% 7.5%

11.1%14.5% 13.6% 15.0%

2006 2007 2008 2009 2010 2011 2012 Target

ROE

6.9%5.4% 5.2% 4.6%

6.6%8.4% 7.7%

9.0%

2006 2007 2008 2009 2010 2011 2012 Target

ROA

WERN TARGETING A 15% ROE & 9% ROA

26 23

RETURN ON INVESTED CAPITAL (ROIC*) VS. SHARE PRICE GROWTH

20 24

*ROIC is a non-GAAP measure. Net income plus net interest expense, divided by average invested capital.

$5

$10

$15

$20

$25

1%2%3%4%5%6%7%8%9%

10%11%12%13%14%15%16%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012

Share Price (year-end) ROIC*

Re

turn

on

Investe

d C

apital

Share

Pri

ce (

year-

en

d)

27 25