Wellness and Beauty Solutions Limited · In d e p e ndent auditor's report to the members of...

71

Wellness and Beauty Solutions Limited (Formerly known as Total Face Group Limited) ABN 43 169 177 833 Annual Report - 30 June 2019 For personal use only

Transcript of Wellness and Beauty Solutions Limited · In d e p e ndent auditor's report to the members of...

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)

ABN 43 169 177 833

Annual Report - 30 June 2019

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Corporate directory30 June 2019

Corporate directory 2Chairman's letter to shareholders 3Directors' report 5Auditor's independence declaration 19Consolidated statement of profit or loss and other comprehensive income 20Consolidated statement of financial position 22Consolidated statement of changes in equity 23Consolidated statement of cash flows 24Notes to the consolidated financial statements 25Directors' declaration 64Independent auditor's report to the members of Wellness and Beauty Solutions Limited 65Shareholder information 69

1

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Corporate directory30 June 2019

Directors Angelos Giannakopoulos - ChairmanChristine Parkes - Managing DirectorDr Naveen Somia - Non-Executive Director

Company secretary Justin Mouchacca

Registered office Unit 14, 347 Bay RoadCheltenham Victoria 3192Telephone: (03) 9532 2639

Principal place of business Unit 14, 347 Bay RoadCheltenham Victoria 3192 Telephone: (03) 9532 2639

Share register Computershare Investor Services Pty LtdYarra Falls, 452 Johnston Street Abbotsford Victoria 3067 Telephone: (03) 9415 5000

Auditor RSM Australia PartnersLevel 21, 55 Collins Street Melbourne Victoria 3000

Stock exchange listing Wellness and Beauty Solutions Limited shares are listed on the Australian SecuritiesExchange (ASX code: WNB)

Date of Annual General Meeting The Company is proposing to hold its Annual General Meeting on Friday 29November 2019

2

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Chairman’s letter to shareholders30 June 2019

Dear Shareholders

It is my pleasure to present Wellness and Beauty Solutions Limited's (WNB) annual report for the 2019 financial year. This was truly a transformational year for the Company.

Following the acquisition of The Giving Brands Company Pty Ltd (GBCo) in October 2018, extensive Board and executive management changes were made as the initial step of a major strategy reset for the Company. As part of the GBCo acquisition, Ms Christine Parkes was appointed as WNB's Managing Director and CEO in September 2018 and has made an outstanding contribution to the Company since joining. It was my pleasure to join Dr Naveen Somia on the Board asNon-executive Director and Chairman on 10 December 2018.

After acquiring GBCo, your revitalised Board and management team immediately initiated a two-prong strategy tomaximise value for our shareholders. With the inclusion of GBCo, WNB now has two distinct but complementary businesses – a stable of high-profile consumer brands that are owned, licensed or private label (Brands) and a network of clinical spas (Services).

Your refreshed Board and new management team has worked diligently during the year to reshape our network of nine Immersion Clinical Spas and simultaneously integrate the business of GBCo, while also expanding and developing our portfolio of Brands. This has been an outstanding achievement in a compressed timeframe.

To help build understanding of our business and growth strategy, shareholders approved a change of company name to Wellness and Beauty Solutions Limited at the Company's 2018 Annual General Meeting. This was followed by the Company's listing code on the Australian Securities Exchange (ASX) changing to WNB on 3 December 2018.

It has been pleasing to see WNB gain increased attention as an emerging leader in Australian beauty, wellness and lifestyle brands and services and we believe the Company is well placed to capitalise on the burgeoning pro-aging (positive aging) and beauty industry globally.

Our portfolio of GBCo owned, licensed and private label brands was extended during the year with the addition of three product ranges under the internationally-recognised ELLE brand alongside our own tanning range, TANNED that was released in market in late in FY19. These new ranges added to our established licensed tanning range, Jbronze by Jennifer Hawkins. We also designed and manufactured three private label ranges for MYER that will be launched in store in early FY20 and are well advanced on the creation of bespoke lifestyle ranges for a number of key magazines including Country Style and the iconic Australian Women's Weekly in collaboration with publishing house, Bauer Media Group.

GBCo is increasingly being recognised and sought after by brand owners and retailers for our expertise in design, manufacturing, marketing and sale of beauty and wellness product ranges. As part of the consolidated WNB, GBCo has cemented and extended our retail footprint via key relationships with major pharmacy, grocery and department store retailers - including Chemist Warehouse, Priceline, Woolworths and MYER. I'm pleased to report that GBCo performed in line with expectations during the year, contributing revenue of $1.29 million post acquisition in FY19. We look forward to reporting a significant uplift from our Brands business in FY20.

As reported during the financial year, the turnaround of the rebranded Immersion Clinical Spa network's performance was more challenging than anticipated. The divestment of four clinics late in FY18/early FY19 and the closure of two clinics early in the reporting period is reflected in lower annualised revenue from the network of $9.02 million (FY18: $18.35million). After assessing the carrying value of prior acquisitions against their operating performance, the Board of Directorsmade the prudent decision to write down $5.23 million in goodwill.

Under new management, I am pleased to report the performance of the WNB's remaining nine Immersion Clinical Spas showed improvement in the second half, with significant uplift late in the year and the network achieving a close to break- even performance by the end of the period. We are confident there is significant scope for uplift in the clinics' utilisation levels and remain focussed on achieving an improved financial contribution to the Company's performance from our Services business in FY20.

Disappointingly, WNB reported a net loss after tax of $13.4 million for the year. This result was adversely affected by a number of material issues identified by the new management. I am pleased to report that these issues have been resolved. Total revenue from continuing operations in FY19 was $9.97 million (FY18: $14.71 million), in line with the reduced number of clinics. Adoption of a strict corporate cost control program realised a significant reduction in operating expenses from continuing operations, particularly in the second half of the year.

3

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Chairman’s letter to shareholders30 June 2019

Our cash position was strengthened by the injection of funds in October 2018 and, subsequent to the financial year end, we secured a $4 million facility for purchase order (manufacturing) and debtor financing for our Brand business. The terms of this facility provide flexibility to the Company to more effectively manage working capital requirements, particularly for lead time brand manufacturing ensuring adequate headroom to invest in the growth of GBCo’s expanding brand portfolio.

In July 2019, we announced the acquisition of Sydney-based skincare and beauty distributor True Solutions International Pty Ltd. True Solutions is recognised as one of Australia's heritage beauty companies and distributes premium and scientifically validated professional and cosmeceutical skincare and makeup brands as well as a range of medi-spa technologies to more than 1,000 professional aesthetic clinics, beauty salons and spas across Australia and New Zealand.

This acquisition exemplifies our ability to identify and execute on opportunities that deliver revenue growth through cross channel sales. It both enhances WNB's product portfolio with a suite of professional use products and technologies whilst also providing a larger customer network for WNB's existing beauty brands.

I firmly believe WNB has a clear pathway to profitability. Under Christine's leadership and discipline, we have a clear strategy for the delivery of operational improvements in our clinic network and through multiple channels for growth – geographic, cross channel and new product launches – from our brands business to maximise shareholder value.

To the entire WNB team, on behalf of the Board, I extend our gratitude for your hard work and dedication. To our Board ofDirectors and executive management, thank you for your commitment to the enactment of a transformation that is set toposition WNB towards substantial growth.

Yours sincerely

Angelos GiannakopoulosNon-executive Chairman

4

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

The directors present their report, together with the financial statements, on the consolidated entity (referred to hereafter as the 'consolidated entity') consisting of Wellness and Beauty Solutions Limited (referred to hereafter as the 'Company' or 'parent entity') and the entities it controlled at the end of, or during, the year ended 30 June 2019.

DirectorsThe following persons were directors of Wellness and Beauty Solutions Limited during the whole of the financial year and up to the date of this report, unless otherwise stated:

Angelos Giannakopoulos (appointed director and Chairman 10 December 2018)Christine Parkes (appointed 27 September 2018)Dr Naveen SomiaKen Poutakidis (appointed director 27 August 2018, appointed Chairman 26 September 2018, resigned 10 December2018)Paul Fielding (resigned 27 September 2018)

Principal activitiesDuring the financial year the principal continuing activities of the consolidated entity consisted of the provision of goods andservices within the Australian beauty and wellness market, including:● providing non-invasive cosmetic treatments; and● the sale of complementary products.

DividendsThere were no dividends paid, recommended or declared during the current or previous financial year.

Review of operationsThe loss for the consolidated entity after providing for income tax amounted to $13,402,000 (30 June 2018: $11,681,000).

Operating results

The loss for the consolidated entity after providing for income tax amounted to $13.402 million (30 June 2018: $11.681 million). This result included the write down in value of $5.278 million of goodwill associated with the Company’s clinic network.

Total revenue from continuing operations in the reporting period was $9.93 million (2018: $14.71 million). This result was supported by the acquisition of The Giving Brands Company Pty Ltd (GBCo) on 8 October 2018. GBCo contributed operating revenue to the consolidated entity of $1.28 million since its acquisition.

Operating revenue from continuing clinic operation, rebranded Immersion Clinical Spas, was down $5.69 million over the previous corresponding period to $9.02 million. (2018: $14.71 million) representing a decrease of 39%. This disappointing result was impacted by a number of factors including the sale of four clinics across May and August 2018, as well as the suspension of operation and subsequent closure of the Canberra and Richmond clinics. At the time the clinics were sold the consolidated entity's liquidity was weak. The sale of these clinics contributed cash to the ongoing operations of the consolidated entity and enable the consolidated entity to continue trading whilst additional capital was raised.

Operating expenses were impacted by the write down in value of the Company’s clinic network by $5.278 million. This reduction was largely driven by the sale of three clinics and the decrease in revenues from continuing operations.

Other significant non-recurrent expenses ($1.58m) were incurred during the reporting period. Key issues included costs relating to the acquisition of The Giving Brands Company Pty Ltd, costs associated with the capital raise activity, losses on the sale of three clinics, the disposal of leased assets, legal expenses and the payment of employee entitlements related to the previous executive management team.

Net cash outflows from operating activities was $7.024 million during the period. Net cash inflow from investing activities in the reporting period was $1.085 million and net cash from financing activities was $6.748 million. The Company held $1.043 million in cash and cash equivalents held at the end of the reporting period (2018: $234,000) and $2.188 million in inventories (2018: $814,000).

5

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

Review of operations

The Company achieved a number of key milestones during the 2019 Financial Year.

Share Placement

On 5 October 2018, 140,000,000 ordinary shares were issued to a number of existing and new institutional andsophisticated investors at a price of $0.05 per share, raising $7M (before costs) to fund working capital for improvement of the clinic network, to complete the GBCo acquisition and fund its business plan, and to repay debt.

Non-renounceable Entitlement Offer

On 8 October 2018, 27,829,537 ordinary shares were issued at a price of $0.05 per share to eligible shareholders under a 1 for 2 non-renounceable Entitlement Offer, raising $1.4M (before costs).

Acquisition of The Giving Brands Company (GBCo)

On 8 October 2018, the consolidated entity acquired The Giving Brands Company Pty Ltd (GBCo) for a total consideration of 51,725,552 fully paid ordinary shares. There was no cash consideration issued. As part of the acquisition, Ms Christine Parkes, Founder and CEO of GBCo, was appointed as Managing Director and CEO of Wellness and Beauty Solutions (formerly Total Face Group).

Reinstatement of Official Quotation

On 10 October 2018 the Company was reinstated to Official Quotation on the Australian Securities Exchange, following completion of a capital raising and the acquisition of GBCo.

Company Name Change

On 30 November 2018, the Company’s name changed to Wellness and Beauty Solutions Limited and the ASX ticker code changed to ASX: WNB on 3 December 2018.

The Giving Brands Company (GBCo)

The Giving Brands Company Pty Ltd, a wholly owned subsidiary of WNB, is a fully integrated brand immersion company that owns, licenses and partners with multiple brands in the wellness, beauty and lifestyle industry. The company has extensive management and operational experience in the development, manufacture, distribution and marketing of brands, a proven track record of creating clear rich brand stories, and strong relationships with retailers.

GBCo’s brands are sold to the professional and retail markets and include: Jbronze, ELLE Makeup, ELLE Kids, ELLE Baby, TANNED, nailKALM, private label brands for MYER, and products under development for Country Style and the Australian Women’s Weekly magazines.

GBCo has strong relationships with major banner groups in the pharmacy sector, including Chemist Warehouse, Priceline and TerryWhite Chemmart. Key relationships for owned, licenced and bespoke brand product ranges were established with Woolworths and Myer during the financial year, further diversifying the Company’s retail footprint.

While sales in the financial year were almost exclusively to Australian retailers, GBCo is well advanced in opening new sales channels in international markets for existing bands and new brands currently under development.

6

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

GBCo’s existing brands include:

● Jbronze by Jennifer Hawkins

GBCo has an exclusive licence agreement for the use of Jbronze by Jennifer Hawkins trademark for its owned tanning range which has been in market since 2013. This licence agreement was extended on 12 June 2019 for a further 3 years, with an additional 2-year option, commencing on 1 July 2019. Jbronze has established a strong market position with banner group pharmacy retailers. In June 2019, WNB announced Jbronze will be sold in 995 Woolworth stores from September 2019, diversifying the brand’s retail channels.

● TANNED

In late June 2019, GBCo launched its 12-product safe sunless tanning range TANNED, with mega influencers Natalie Roser and Kris Smith contracted as brand ambassadors. Both ambassadors’ large network and extensive social media following, with over 1 million Instagram followers, that provides a strong platform to gain immediate brand awareness and retailer engagement.

● nailKALM

GBCo is licenced to manufacture, sell and distribute nailKALM, a product which contains a proprietary active ingredient (derived from blue-green algae) that is clinically proven to provide effective treatment for nails prone to fungal infections. The Australian Podiatry Association has stated that one in 10 adult Australians are affected by nail fungal infections. nailKALM is 100 percent organic and non-toxic, which is its unique selling proposition to the 1.7M nail fungal sufferers in Australia.

● ELLE Makeup, ELLE Kids & ELLE Baby

GBCo has been granted one of 125 licences in the world by ELLE brand owner, Legardere Active Enterprises (LAE), to design, manufacture and retail beauty, skincare and related products for three ranges - ELLE Makeup, ELLE Kids and ELLE Baby. The 4-year licencing contract is for multiple territories in Australasia, Europe and North America.

GBCo’s ELLE Makeup range includes more than 50 individual product lines, and ELLE Kids and ELLE Baby ranges have more than 35 individual products. The Intellectual Property (IP) for all ELLE Kids and ELLE Baby skincare and personal care product formulations are proprietary to GBCo. The three ranges will be launched in market in 1H’20.

MYER - homeware brand ranges

In April 2019, GBCo was contracted by Australian department store MYER to design and manufacture three new private label homeware ranges. The new ‘Only at MYER’ ranges, which include a range of personal care products and unique home fragrancing accessories, have been created exclusively for MYER’s homeware department. The range is on track for delivery in 1H’20.

● Professional and retail - skincare range

GBCo is working with Australian model and influencer Brooke Hogan on new product development and brand creative for its bespoke skincare range for the professional and retail markets. Brooke is contracted to be the brand’s ambassador and has a strong social media following of more than 700,000 followers that will be a key marketing channel for the brand.

Immersion Clinical Spas

The Company owns and operates a network of nine Immersion Clinical Spas in Australia.

The clinics provide non-invasive medical aesthetic (NIMA) and wellness and beauty services using a highly experienced team of doctors, aesthetic nurse consultants, dermal therapists and beauty consultants.

7

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

Ambassador Agreements

The Company signed ambassador agreements with high profile influencers Natalie Roser, Kris Smith and Brooke Hogan as part of GBCo’s brand marketing strategy. The ambassadors each elected to take 2,000,000 fully paid ordinary shares at $0.05 per share in the Company (escrowed for 12 months) as part of their brand ambassador services.

Significant changes in the state of affairsThe following significant changes in the state of affairs of the consolidated entity occurred during the financial year:

● on 27 August 2018, Mr Ken Poutakidis, was appointed as a Non-Executive Director of the Company;● on 27 September 2018, Mr Paul Fielding resigned as director and was replaced as Chairman by Mr Ken Poutakidis

and Ms Christine Parkes was appointed as Chief Executive Officer and Managing Director of the Company;● On 28 September 2018, 27,829,537 ordinary shares were issued at a price of $0.05 per share to eligible shareholders

under a 1 for 2 non-renounceable Entitlement Offer, raising $1.4M (before costs);● on 5 October 2018 the Company issued 140,000,000 fully paid ordinary shares at $0.05 per share pursuant to the

share placement to professional and sophisticated investors raising $7M (before costs);;● on 8 October 2018 the Company issued 27,829,537 fully paid ordinary shares at $0.05 per share pursuant to a rights

issue, raising $1.4M (before costs);● on 8 October 2018 the Company acquired 100% of the issued shares of The Giving Brands Company Pty Ltd (GBCo)

and issued 51,725,552 fully paid ordinary shares at $0.05 per share to the vendor of GBCo as consideration for theacquisition;

● on 10 October 2018 the Company was reinstated to Official Quotation on the Australian Securities Exchange,following completion of a capital raising and the acquisition of GBCo;

● on 30 November 2018, the Company changed its name from Total Face Group Limited to Wellness and BeautySolutions Limited;

● on 10 December 2018, Mr Angelos Giannakopoulos was appointed Non-executive Chairman of the Company,replacing Mr Ken Poutakidis, who stepped down from the Board;

● on 26 March 2019 the Company issued 2,000,000 fully paid ordinary shares at $0.05 per share pursuant to anambassador services agreement;

● on 12 April 2019 the Company issued 2,000,000 fully paid ordinary shares at $0.05 per share pursuant to anambassador services agreement;

● on 3 May 2019 the Company issued 2,000,000 fully paid ordinary shares at $0.05 per share pursuant to anambassador services agreement.

There were no other significant changes in the state of affairs of the consolidated entity during the financial year.

Matters subsequent to the end of the financial yearOn 18 July 2019, the Company secured a $4M facility with Timelio Pty Ltd for purchase order (manufacturing) and debtorfinancing for the brand business. This facility gives flexibility to WNB’s debt structure to more effectively manage working capital requirements, particularly for lead time brand manufacturing and provides adequate headroom to invest in growth of GBCo’s expanding brand portfolio.

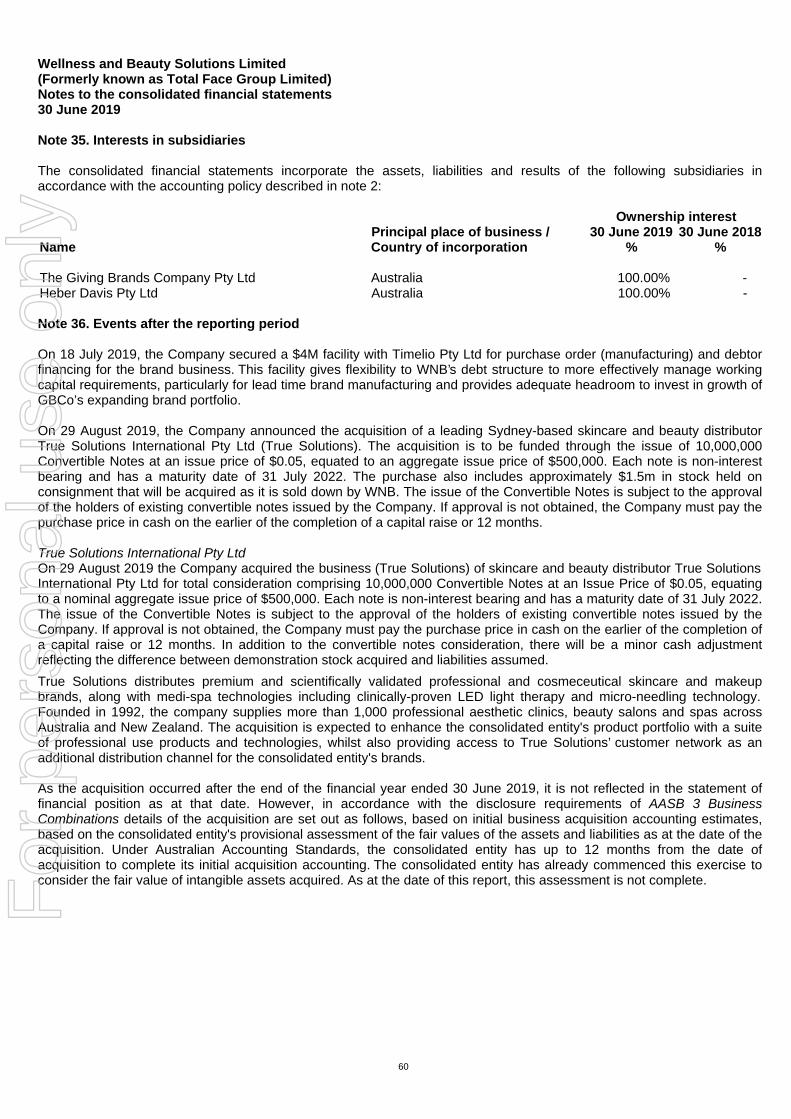

On 29 August 2019, the Company announced the acquisition of a leading Sydney-based skincare and beauty distributor True Solutions International Pty Ltd (True Solutions). The acquisition is to be funded through the issue of 10,000,000 Convertible Notes at an issue price of $0.05, equated to an aggregate issue price of $500,000. Each note is non-interest bearing and has a maturity date of 31 July 2022. The purchase also includes approximately $1.5m in stock held on consignment that will be acquired as it is sold down by WNB. The issue of the Convertible Notes is subject to the approval of the holders of existing convertible notes issued by the Company. If approval is not obtained, the Company must pay the purchase price in cash on the earlier of the completion of a capital raise or 12 months.

No other matter or circumstance has arisen since 30 June 2019 that has significantly affected, or may significantly affect the consolidated entity's operations, the results of those operations, or the consolidated entity's state of affairs in future financial years.

8

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

Likely developments and expected results of operationsThe consolidated entity is positioned to be a powerhouse of Australian beauty, wellness and lifestyle brands and services and is well placed to capitalise on the burgeoning pro-aging (positive aging) and beauty industry globally.

While the turnaround program implemented across the resized Immersion Clinical Spa network has been slower than expected, positive momentum was achieved late in FY19, particularly from our Queensland clinics. The Directors are confident the range of initiatives implemented to boost customer numbers, reduce costs and lift utilisation levels will result in a modest lift in revenues and see the network being cashflow positive in the first half of FY20.

Based on its contracted and projected sales pipeline, the consolidated entity expects its brand business (GBCo) will deliver revenue in the $6-$7M range in FY20.

The consolidated entity has begun integration of the newly acquired Sydney-based skincare and beauty distributor True Solutions International Pty Ltd. True Solutions is recognised as one of Australia's heritage beauty companies and distributes premium and scientifically validated professional and cosmeceutical skincare and makeup brands as well as a range of medi-spa technologies to more than 1,000 professional aesthetic clinics, beauty salons and spas across Australia and New Zealand. True Solutions is expected to add $4M - $5M in annualised revenue to the consolidated entity.

Environmental regulationThe consolidated entity is not subject to any significant environmental regulation under Australian Commonwealth or State law.

Information on directorsName: Angelos Giannakopoulos (appointed director and Chairman 10 December 2018)Title: ChairmanQualifications: B.Bus. (Banking & Finance)Experience and expertise: Mr Giannakopoulos has significant expertise and business experience arising from

his work across capital markets and various industries as a prominent financier and holder of a number of leadership executive roles within the finance industry. He is currently the Victorian and South Australian State Manager for private wealth management firm Ord Minnett, was previously Global Head of Equities for ANZ Banking Group and has also held executive leadership positions with Treasury Corporation of Victoria and the Transport Superannuation Board.

Other current directorships: NoneFormer directorships (last 3 years): NoneInterests in shares: 1,421,895 fully paid ordinary sharesContractual rights to shares: 100,000 convertible notes

Name: Christine Parkes (appointed 27 September 2018)Title: Managing DirectorExperience and expertise: Mrs Parkes has built a reputation in the cosmetic and skincare industry over a 20+

year period and is recognised for brand management, new product development and rebranding. Christine has a strength in strategic marketing; import and export supply, registration and compliance requirements.

Along with Mrs Parkes' experience in cosmetic and skincare manufacturing, she combines her knowledge and experience with an extensive global network of key influencers in the cosmetics and skincare industries to develop, launch, support and grow brands within the retail sector.

Mrs Parkes previously owned a boutique cosmetic and skincare manufacturing company providing invaluable knowledge of the technical and manufacturing processes needed to create, manufacture and distribute cosmetic, skincare and wellness products in domestic and international markets.

Other current directorships: NoneFormer directorships (last 3 years): NoneInterests in shares: 51,725,552 fully paid ordinary shares

9

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

Name: Dr Naveen SomiaTitle: Non- Executive DirectorQualifications: MBBS, PhD, FRACSExperience and expertise: Dr Naveen Somia is a Fellow of the Royal Australasian College of Surgeons and a

member of the Australian Society of Plastic Surgeons (ASPS), the peak body of Specialist Plastic Surgeons in Australia.

Other current directorships: NoneFormer directorships (last 3 years): NoneSpecial responsibilities: Audit & Risk Committee - Chair; Remuneration & Nomination Committee - ChairInterests in shares: -

Name: Ken Poutakidis (appointed director 27 August 2018, appointed Chairman 26September 2018, resigned 10 December 2018)

Title: ChairmanQualifications: B.Bus.Experience and expertise: Mr Poutakidis is corporate adviser and corporate finance executive with 16 years of

finance experience. He is the Managing Director and Founder of Avenue Advisory, a boutique advisory firm providing corporate finance and capital markets advice to emerging companies.

Previously, Mr Poutakidis worked as a management consultant and a corporate finance executive with leading equity firms across Australia and Asia. His particular expertise includes capital raisings, mergers & acquisitions, corporate advisory, asset divestment and strategy development.

Mr Poutakidis has previously served as Chairman of the Boards of Alchemia and Mach7 Technologies, was a non-executive director of Contango Microcap.

Other current directorships: N/A, as is no longer a director at the date of this reportFormer directorships (last 3 years): N/A, as is no longer a director at the date of this reportInterests in shares: N/A, as is no longer a director at the date of this report

Name: Paul Fielding (resigned 27 September 2018)Title: Executive ChairmanQualifications: CAExperience and expertise: Paul is a highly skilled professional with a high degree of commercial acumen and

has the ability to negotiate outcomes in complex and competitive environments. He has worked in the services sector for more than 20 years.

Paul previous successful Directorships took Ingena Group Limited (ASX: IGL) and RXP Services Limited (ASX: RXP) to IPO raising in excess of $50m across both organisations. IGL and RXP experienced significant growth organically and acquisitively in which Paul has played a key role.

Other current directorships: N/A, as is no longer a director at the date of this reportFormer directorships (last 3 years): N/A, as is no longer a director at the date of this reportInterests in shares: N/A, as is no longer a director at the date of this report

'Other current directorships' quoted above are current directorships for listed entities only and excludes directorships of all other types of entities, unless otherwise stated.

'Former directorships (last 3 years)' quoted above are directorships held in the last 3 years for listed entities only and excludes directorships of all other types of entities, unless otherwise stated.

10

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

Company secretaryMr Justin Mouchacca, CA

Mr Mouchacca holds a Bachelor of Business majoring in Accounting. Justin became a Chartered Accountant in 2011 and since July 2019 has been a principal of JM Corporate Services Pty Ltd, specialising in outsourced company secretarial and financial duties. Justin has over 11 years’ experience in the accounting profession including 5 years in the Corporate Secretarial professions and is a company secretary and finance officer for a number of entities listed on the Australian Securities Exchange.

Meetings of directorsThe number of meetings of the Company's Board of Directors ('the Board') held during the year ended 30 June 2019, and the number of meetings attended by each director were:

Nomination andFull Board Remuneration Committee Audit and Risk Committee

Attended Held Attended Held Attended Held

Angelos Giannakopoulos 3 3 - - - -Christine Parkes 5 5 - - - -Dr Naveen Somia 4 6 - - - -Ken Poutakidis 3 3 - - - -Paul Fielding 1 1 - - - -

Held: represents the number of meetings held during the time the director held office.

Remuneration report (audited)The remuneration report details the key management personnel remuneration arrangements for the consolidated entity, in accordance with the requirements of the Corporations Act 2001 and its Regulations.

Key management personnel are those persons having authority and responsibility for planning, directing and controlling the activities of the entity, directly or indirectly, including all directors.

The remuneration report is set out under the following main headings:● Principles used to determine the nature and amount of remuneration● Details of remuneration● Service agreements● Share-based compensation● Additional disclosures relating to key management personnel

Principles used to determine the nature and amount of remunerationThe Board policy for determining the nature and amount of remuneration of key management personnel is agreed by theBoard as a whole.

The objective of the consolidated entity's executive reward framework is to ensure reward for performance is competitive and appropriate for the results delivered. The framework aligns executive reward with the achievement of strategic objectives and the creation of value for shareholders, and it is considered to conform to the market best practice for the delivery of reward. The Board of Directors ('the Board') ensures that executive reward satisfies the following key criteria for good reward governance practices:● competitiveness and reasonableness● acceptability to shareholders● performance linkage / alignment of executive compensation● transparency

11

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

The Remuneration and Nomination Committee ("Committee") was established to advise on remuneration and issues relevant to remuneration policies and practices including those for senior management and non-executive Directors. Theperformance of the consolidated entity depends on the quality of its directors and executives. The remuneration philosophy is to attract, motivate and retain high performance and high quality personnel.

At present, given the number and mix of directors, the Committee does not hold separate meetings and its functions are carried out by the Board.

In accordance with best practice corporate governance, the structure of non-executive director and executive director remuneration is separate.

Non-executive directors remunerationFees and payments to non-executive directors reflect the demands and responsibilities of their role. Non-executive directors' fees and payments are reviewed annually by the Board or the Committee. The Board or Committee may, from time to time, receive advice from independent remuneration consultants to ensure non-executive directors' fees and payments are appropriate and in line with the market. The chairman's fees are determined independently to the fees of other non-executive directors based on comparative roles in the external market. The chairman is not present at anydiscussions relating to the determination of his own remuneration. Non-executive directors do not receive share options,bonus payments or other incentives.

Executive remunerationThe consolidated entity aims to reward executives based on their position and responsibility, with a level and mix of remuneration which has both fixed and variable components.

The executive remuneration and reward framework has four components:● base pay● short-term performance incentives● share-based payments● other remuneration such as superannuation and long service leave

The combination of these comprises the executive's total remuneration.

Fixed remuneration, consisting of base salary and superannuation, are reviewed annually by the Board or Committee based on individual and business unit performance, the overall performance of the consolidated entity and comparable market remunerations.

The short-term incentives ('STI') program is designed to align the targets of the business units with the performancehurdles of executives. STI payments are granted to executives based on specific annual targets and applicable keyperformance indicators ('KPI's') being achieved. KPI's may include profit contribution, customer satisfaction, leadership contribution and product management.

The Company has established a Long Term Incentive Plan (LTIP) that allows for the award of performance-related rights (‘Rights’) subject to the LTIP Rules. The Plan is designed to assist in the motivation, retention and reward of the Company’s Directors and senior executives. In addition, the Plan is designed to align the interests of Directors and senior executives more closely with the interests of shareholders.

To date, no rights have been granted pursuant to the LTIP. The Board will continue to monitor shareholder value and may issue rights under the Plan when considered appropriate.

Consolidated entity performance and link to remunerationThe remuneration of the Managing Director is directly linked to the performance of the consolidated entity. The amount of the Managing Director's cash bonus is dependent on the consolidated entity meeting or exceeding Board-approved forecasts.

Voting and comments made at the Company's 28 November 2018 Annual General Meeting ('AGM')At the 28 November 2018 AGM, 98.8% of the votes received supported the adoption of the remuneration report for the year ended 30 June 2018. The Company did not receive any specific feedback at the AGM regarding its remuneration practices.

12

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

Details of remuneration

Amounts of remunerationDetails of the remuneration of key management personnel of the consolidated entity are set out in the following tables.

The key management personnel of the consolidated entity consisted of the following directors of Wellness and Beauty Solutions Limited:● Angelos Giannakopoulos (appointed Non-executive Director and Chairman 10 December 2018)● Christine Parkes (appointed Managing Director 27 September 2018)● Dr Naveen Somia● Ken Poutakidis (appointed Non-executive Director 27 August 2018, appointed Chairman 26 September 2018,

resigned 10 December 2018)● Paul Fielding (resigned 27 September 2018)

And the following persons:● Tim Smith - General Manager (appointed 18 February 2019)● Chris Adnams - Chief Financial Officer (appointed 5 December 2018, resigned 31 May 2019)● Kerstin Grant - Acting Chief Executive Officer (ceased 27 September 2018)● Liza Juegan - Chief Financial Officer and Company Secretary (resigned 16 October 2018)

Post-employment

benefits

Cash salary Cash Super-

Long-termbenefits

Longservice

Share-based

payments

Equity-and fees bonus monetary annuation payments leave settled Total

30 June 2019 $ $ $ $ $ $ $ $

Non-ExecutiveDirectors:AngelosGiannakopoulos(a) 50,000 - - - - - - 50,000Dr Naveen Somia 40,000 - - - - - - 40,000Ken Poutakidis(b) - - - - - - - -Paul Fielding (c) 14,208 - - - - - - 14,208

ExecutiveDirectors:Christine Parkes(d) 202,037 50,000 14,497 22,711 - - - 289,245

Other KeyManagementPersonnel:Tim Smith (e) 66,923 - - 6,358 5,148 - - 78,429Chris Adnams (f) 85,706 - - 8,142 4,871 - - 98,719Kerstin Grant (g) 86,641 - - 16,017 82,068 - - 184,726Liza Juegan (h) 71,046 - - 18,624 142,236 - - 231,906

616,561 50,000 14,497 71,852 234,323 - - 987,233

13

Short-term benefits

Non- Termination

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

(a) Appointed 10 December 2018(b) Mr Ken Poutakidis was appointed 27 August 2018 and resigned 10 December 2018. As agreed, he did not charge a

fee for his director services and therefore did not receive any remuneration.(c) Resigned 27 September 2018(d) Appointed 27 September 2018(e) Appointed 18 February 2019, resigned 30 June 2019(f) Appointed 5 December 2018, resigned 31 May 2019(g) Ceased 27 September 2018(h) Resigned 16 October 2018

Post-employment Long-term

Share-based

payments

Cash salary Cash Super- service Equity-and fees bonus Other annuation leave settled Total

30 June 2018 $ $ $ $ $ $ $

Non-Executive Directors:Paul Fielding 50,000 - - - - - 50,000Dr Naveen Somia 40,000 - - - - - 40,000Lynda Adler* 40,000 - - - - - 40,000

Executive Directors:Joanne Hannah** 211,914 - 15,050 17,584 - - 244,548

Other Key ManagementPersonnel:Kerstin Grant 233,286 - - 22,162 - - 255,448Kathryn Bran*** 126,065 75 13,777 11,621 - - 151,538Liza Juegan 168,950 - - 16,050 - - 185,000

870,215 75 28,827 67,417 - - 966,534

* Resigned 28 June 2018** Resigned 1 May 2018*** Resigned 29 March 2018

14

Short-term benefits benefits benefits

Long

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

The proportion of remuneration linked to performance and the fixed proportion are as follows:

Fixed remuneration At risk - STI At risk - LTIName 30 June 2019 30 June 2018 30 June 2019 30 June 2018 30 June 2019 30 June 2018

Non-Executive Directors:Angelos Giannakopoulos 100% - - - - -Dr Naveen Somia 100% - - - - -Ken Poutakidis 100% - - - - -Paul Fielding 100% 100% - - - -Lynda Adler - 100% - - - -

Executive Directors:Christine Parkes 100% - - - - -Joanne Hannah - 100% - - - -

Other Key ManagementPersonnel:Chris Adnams 100% - - - - -Kerstin Grant - 100% - - - -Liza Juegan 100% 100% - - - -Kathryn Bran - 100% - - - -

Service agreementsRemuneration and other terms of employment for key management personnel are formalised in service agreements. Details of these agreements are as follows:

Name: Christine ParkesTitle: Managing Director and Chief Executive OfficerAgreement commenced: 27th September 2018Term of agreement: 4 yearsDetails: Total Fixed Annual Remuneration - $250,000. Where the executive remains in the

employ of the Company for twelve (12) months, Total Fixed Annual Remuneration will increase to $300,000.

Sign-on Bonus - $50,000.

Short Term Incentive (STI) - STI to a maximum of 25% of annual salary if the Company meets or exceeds the forecast approved by the Board of the Company for each of the Financial Years ending 30 June, 2019, 30 June 2020, 30 June 2021 and 30 June 2022.

Long Term Incentive (LTI) - The executive is eligible to participate in the Company’s LTI plan.

Notice period / termination entitlement - The Executive must give the Company 90 days' notice of cessation. The Company must give 12 months' notice if the Company terminates the executive's employment at any time before the Term, within the first three (3) years from the commencement date. The Company may elect to make payment in lieu of any unserved notice period. Employment may be ended immediately in certain circumstances including misconduct, incapacity and mutual agreement.

Key management personnel have no entitlement to termination payments in the event of removal for misconduct.

15

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

Share-based compensation

Issue of sharesThere were no shares issued to directors and other key management personnel as part of compensation during the yearended 30 June 2019.

OptionsThere were no options over ordinary shares issued to directors and other key management personnel as part of compensation that were outstanding as at 30 June 2019.

There were no options over ordinary shares granted to or vested by directors and other key management personnel as part of compensation during the year ended 30 June 2019.

Additional disclosures relating to key management personnel

ShareholdingThe number of shares in the Company held during the financial year by each director and other members of key management personnel of the consolidated entity, including their personally related parties, is set out below:

Balance at Received Balance atthe start of as part of Disposals/ the end ofthe year remuneration Additions other the year

Ordinary sharesAngelos Giannakopoulos (a) - - 1,421,895 - 1,421,895Christine Parkes (b) - - 51,725,552 - 51,725,552Ken Poutakidis (c) - - 2,033,000 (2,033,000) -Paul Fielding (d) 14,638,799 - - (14,638,799) -Kerstin Grant (d) 300,000 - - (300,000) -Lisa Juegan (d) 146,674 - - (146,674) -

15,085,473 - 55,180,447 (17,118,473) 53,147,447

(a) "Additions" comprises 615,000 shares held at date of appointment and 656,895 shares subsequently acquired on- market. In addition, Mr Giannakopoulos held 100,000 convertible notes upon appointment and continued to holdthese at the end of the financial year.

(b) "Additions" are shares issued as consideration for the Company's acquisition of The Giving Brands Company Pty Ltd (c) "Additions" comprises 1,983,000 shares held at date of appointment and 50,000 shares acquired pursuant to rights

issue. "Other" is the balance of shares held at date of cessation as member of key management personnel. In addition, Mr Poutakidis held 200,000 convertible notes upon appointment and continued to hold these at date of cessation.

(d) "Other" is the balance of shares held at date of cessation as member of key management personnel. In addition, MrFielding held 125,000 convertible notes at the beginning of the year and continued to hold these at date of cessation.

(e) "Other" is the balance of shares held at date of cessation as member of key management personnel.

Loans to key management personnel and their related partiesAt 30 June 2019 consolidated entity has an amount receivable from Managing Director Christine Parkes. The loan wasadvanced to her by The Giving Brands Company Pty Ltd (GBCo) prior to its acquisition by the Company. As at the date of acquisition the balance of the loan was $18,986. As at the end of the financial period the balance of the loan was $26,597.

This concludes the remuneration report, which has been audited.

Shares under optionThere were no unissued ordinary shares of Wellness and Beauty Solutions Limited under option outstanding at the date of this report.

Shares issued on the exercise of optionsThere were no ordinary shares of Wellness and Beauty Solutions Limited issued on the exercise of options during the yearended 30 June 2019 and up to the date of this report.

16

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

Indemnity and insurance of officersThe Company has indemnified the directors and executives of the Company for costs incurred, in their capacity as a director or executive, for which they may be held personally liable, except where there is a lack of good faith.

During the financial year, the Company paid a premium in respect of a contract to insure the directors and executives of the Company against a liability to the extent permitted by the Corporations Act 2001. The contract of insurance prohibits disclosure of the nature of the liability and the amount of the premium.

Indemnity and insurance of auditorThe Company has not, during or since the end of the financial year, indemnified or agreed to indemnify the auditor of the Company or any related entity against a liability incurred by the auditor.

During the financial year, the Company has not paid a premium in respect of a contract to insure the auditor of the Company or any related entity.

Proceedings on behalf of the CompanyNo person has applied to the Court under section 237 of the Corporations Act 2001 for leave to bring proceedings on behalf of the Company, or to intervene in any proceedings to which the Company is a party for the purpose of taking responsibility on behalf of the Company for all or part of those proceedings.

Non-audit servicesDetails of the amounts paid or payable to the auditor for non-audit services provided during the financial year by the auditor are outlined in note 29 to the financial statements.

The directors are satisfied that the provision of non-audit services during the financial year, by the auditor (or by another person or firm on the auditor's behalf), is compatible with the general standard of independence for auditors imposed by the Corporations Act 2001.

The directors are of the opinion that the services as disclosed in note 29 to the financial statements do not compromise the external auditor's independence requirements of the Corporations Act 2001 for the following reasons:● all non-audit services have been reviewed and approved to ensure that they do not impact the integrity and objectivity

of the auditor; and● none of the services undermine the general principles relating to auditor independence as set out in APES 110 Code

of Ethics for Professional Accountants issued by the Accounting Professional and Ethical Standards Board, including reviewing or auditing the auditor's own work, acting in a management or decision-making capacity for the Company,acting as advocate for the Company or jointly sharing economic risks and rewards.

Officers of the Company who are former partners of RSM Australia PartnersThere are no officers of the Company who are former partners of RSM Australia Partners.

Rounding of amountsThe Company is of a kind referred to in Corporations Instrument 2016/191, issued by the Australian Securities and Investments Commission, relating to 'rounding-off'. Amounts in this report have been rounded off in accordance with that Corporations Instrument to the nearest thousand dollars, or in certain cases, the nearest dollar.

Auditor's independence declarationA copy of the auditor's independence declaration as required under section 307C of the Corporations Act 2001 is set outimmediately after this directors' report.

AuditorRSM Australia Partners continues in office in accordance with section 327 of the Corporations Act 2001.

17

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Directors' report30 June 2019

This report is made in accordance with a resolution of directors, pursuant to section 298(2)(a) of the Corporations Act2001.

On behalf of the directors

___________________________Angelos GiannakopoulosChairman

30 September 2019

18

For

per

sona

l use

onl

y

RSM Australia Partners

Level 21, 55 Collins Street Melbourne VIC 3000 PO Box 248 Collins Street West VIC 8007

T +61 (0) 3 9286 8000 F +61 (0) 3 9286 8199

www.rsm.com.au

AUDITOR’S INDEPENDENCE DECLARATION

As lead auditor for the audit of the financial report of Wellness and Beauty Solutions Limited and its controlled entities for the year ended 30 June 2019, I declare that, to the best of my knowledge and belief, there have been no contraventions of:

(i) the auditor independence requirements of the Corporations Act 2001 in relation to the audit; and

(ii) any applicable code of professional conduct in relation to the audit.

RSM AUSTRALIA PARTNERS

R B MIANOPartner

30 September 2019Melbourne, Victoria

THE POWER OF BEING UNDERSTOODAUDIT | TAX | CONSULTING

RSM Australia Partners is a member of the RSM network and trades as RSM. RSM is the trading name used by the members of the RSM network. Each member of theRSM network is an independent accounting and consulting firm which practices in its own right. The RSM network is not itself a separate legal entity in any jurisdiction.

RSM Australia Partners ABN 36 965 185 036

Liability limited by a scheme approved under Professional Standards Legislation19

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Consolidated statement of profit or loss and other comprehensive incomeFor the year ended 30 June 2019

ConsolidatedNote 30 June 2019 30 June 2018

$'000 $'000

Revenue from continuing operations 5 9,932 14,708

Other income - 100Interest income 35 26

ExpensesNon refundable deposits lost - (100)Raw materials and consumables used (4,105) (4,637)Contractors (1,515) (1,879)Occupancy expenses (1,666) (1,431)Employee benefits expense (5,153) (5,899)Depreciation and amortisation expense 6 (1,615) (1,364)Impairment expense (5,278) (6,611)(Loss)/Gain on disposal of equipment (209) -Loss on deferred consideration - (309)Impairment of receivables (28) -Consultants (819) (910)Other expenses (2,023) (2,107)Finance costs 6 (590) (322)

Loss before income tax expense from continuing operations (13,034) (10,735)

Income tax expense 7 (135) -

Loss after income tax expense from continuing operations (13,169) (10,735)

Loss after income tax expense from discontinued operations 8 (233) (946)

Loss after income tax expense for the year attributable to the owners ofWellness and Beauty Solutions Limited 24 (13,402) (11,681)

Other comprehensive income for the year, net of tax - -

Total comprehensive income for the year attributable to the owners ofWellness and Beauty Solutions Limited (13,402) (11,681)

Total comprehensive income for the year is attributable to:Continuing operations (13,169) (10,735)Discontinued operations (233) (946)

(13,402) (11,681)

The above consolidated statement of profit or loss and other comprehensive income should be read in conjunction with theaccompanying notes

20

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Consolidated statement of profit or loss and other comprehensive incomeFor the year ended 30 June 2019

ConsolidatedNote 30 June 2019 30 June 2018

$'000 $'000

Cents Cents

Earnings per share for loss from continuing operations attributable to theowners of Wellness and Beauty Solutions LimitedBasic earnings per share 39 (4.57) (8.52)Diluted earnings per share 39 (4.57) (8.52)

Earnings per share for loss from discontinued operations attributable to theowners of Wellness and Beauty Solutions LimitedBasic earnings per share 39 (0.08) (0.75)Diluted earnings per share 39 (0.08) (0.75)

Earnings per share for loss attributable to the owners of Wellness and BeautySolutions LimitedBasic earnings per share 39 (4.66) (9.27)Diluted earnings per share 39 (4.66) (9.27)

The above consolidated statement of profit or loss and other comprehensive income should be read in conjunction with theaccompanying notes

21

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Consolidated statement of financial positionAs at 30 June 2019

ConsolidatedNote 30 June 2019 30 June 2018

$'000 $'000

Assets

Current assetsCash and cash equivalents 9 1,043 234Trade and other receivables 10 298 226Inventories 11 2,188 814Other assets 12 714 253Total current assets 4,243 1,527

Non-current assetsProperty, plant and equipment 13 1,970 3,608Intangibles 14 7,625 10,668Deferred tax 15 - 42Other assets 16 376 348Total non-current assets 9,971 14,666

Total assets 14,214 16,193

Liabilities

Current liabilitiesTrade and other payables 17 2,865 2,596Borrowings 18 2,473 835Provisions 19 278 252Contract liabilities 20 480 250Total current liabilities 6,096 3,933

Non-current liabilitiesBorrowings 21 1,481 3,221Provisions 22 174 30Total non-current liabilities 1,655 3,251

Total liabilities 7,751 7,184

Net assets 6,463 9,009

EquityIssued capital 23 36,710 25,854Accumulated losses 24 (30,247) (16,845)

Total equity 6,463 9,009

The above consolidated statement of financial position should be read in conjunction with the accompanying notes22

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Consolidated statement of changes in equityFor the year ended 30 June 2019

Issued Retainedcapital profits Total equity

Consolidated $'000 $'000 $'000

Balance at 1 July 2017 25,300 (5,164) 20,136

Loss after income tax expense for the year - (11,681) (11,681)Other comprehensive income for the year, net of tax - - -

Total comprehensive income for the year - (11,681) (11,681)

Transactions with owners in their capacity as owners:Contributions of equity, net of transaction costs (note 23) 554 - 554

Balance at 30 June 2018 25,854 (16,845) 9,009

Issued Retainedcapital profits Total equity

Consolidated $'000 $'000 $'000

Balance at 1 July 2018 25,854 (16,845) 9,009

Loss after income tax expense for the year - (13,402) (13,402)Other comprehensive income for the year, net of tax - - -

Total comprehensive income for the year - (13,402) (13,402)

Transactions with owners in their capacity as owners:Contributions of equity, net of transaction costs (note 23) 10,856 - 10,856

Balance at 30 June 2019 36,710 (30,247) 6,463

The above consolidated statement of changes in equity should be read in conjunction with the accompanying notes23

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Consolidated statement of cash flowsFor the year ended 30 June 2019

ConsolidatedNote 30 June 2019 30 June 2018

$'000 $'000

Cash flows from operating activitiesReceipts from customers (inclusive of GST) 11,392 20,117Payments to suppliers and employees (inclusive of GST) (18,055) (21,532)Interest received 14 10Interest and other finance costs paid (375) (322)

Net cash used in operating activities 37 (7,024) (1,727)

Cash flows from investing activitiesPayments for investments (8) (2,670)Payments for property, plant and equipment (236) (397)Payments for intangibles (147) -Payments for other non-current assets - (303)Proceeds from disposal of businesses 8 1,400 1,424Proceeds from disposal of property, plant and equipment 10 -Net cash acquired on business acquisition 66 -

Net cash from/(used in) investing activities 1,085 (1,946)

Cash flows from financing activitiesProceeds from issue of shares 8,391 -Proceeds from borrowings 209 -Proceeds from issue of convertible notes 20 1,290Proceeds from related party loan - 534Share issue transaction costs (422) -Repayment of borrowings (1,450) (615)Release of security deposit - 50

Net cash from financing activities 6,748 1,259

Net increase/(decrease) in cash and cash equivalents 809 (2,414)Cash and cash equivalents at the beginning of the financial year 234 2,648

Cash and cash equivalents at the end of the financial year 9 1,043 234

The above consolidated statement of cash flows include cash flows from discontinued operations as detailed in Note 8.

The above consolidated statement of cash flows should be read in conjunction with the accompanying notes24

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Notes to the consolidated financial statements30 June 2019

Note 1. General information

The financial statements cover Wellness and Beauty Solutions Limited as a consolidated entity consisting of Wellness and Beauty Solutions Limited and the entities it controlled at the end of, or during, the year. The financial statements are presented in Australian dollars, which is Wellness and Beauty Solutions Limited's functional and presentation currency.

Wellness and Beauty Solutions Limited is a listed public company limited by shares, incorporated and domiciled in Australia. Its registered office and principal place of business is:

Unit 14, 347 Bay RoadCheltenham VIC 3192Australia

A description of the nature of the consolidated entity's operations and its principal activities are included in the directors' report, which is not part of the financial statements.

The financial statements were authorised for issue, in accordance with a resolution of directors, on 30 September 2019. The directors have the power to amend and reissue the financial statements.

Note 2. Significant accounting policies

The principal accounting policies adopted in the preparation of the financial statements are set out below. These policies have been consistently applied to all the years presented, unless otherwise stated.

New or amended Accounting Standards and Interpretations adoptedThe consolidated entity has adopted all of the new or amended Accounting Standards and Interpretations issued by theAustralian Accounting Standards Board ('AASB') that are mandatory for the current reporting period.

Any new or amended Accounting Standards or Interpretations that are not yet mandatory have not been early adopted.

The following Accounting Standards and Interpretations are most relevant to the consolidated entity:

AASB 9 Financial InstrumentsThe consolidated entity has adopted AASB 9 from 1 July 2018. The standard introduced new classification andmeasurement models for financial assets. A financial asset shall be measured at amortised cost if it is held within abusiness model whose objective is to hold assets in order to collect contractual cash flows which arise on specified dates and that are solely principal and interest. A debt investment shall be measured at fair value through other comprehensive income if it is held within a business model whose objective is to both hold assets in order to collect contractual cash flows which arise on specified dates that are solely principal and interest as well as selling the asset on the basis of its fair value. All other financial assets are classified and measured at fair value through profit or loss unless the entity makes an irrevocable election on initial recognition to present gains and losses on equity instruments (that are not held-for-trading or contingent consideration recognised in a business combination) in other comprehensive income ('OCI'). Despite these requirements, a financial asset may be irrevocably designated as measured at fair value through profit or loss to reduce the effect of, or eliminate, an accounting mismatch. For financial liabilities designated at fair value through profit or loss, the standard requires the portion of the change in fair value that relates to the entity's own credit risk to be presented in OCI (unless it would create an accounting mismatch). New impairment requirements use an 'expected credit loss' ('ECL') modelto recognise an allowance. Impairment is measured using a 12-month ECL method unless the credit risk on a financialinstrument has increased significantly since initial recognition in which case the lifetime ECL method is adopted. For receivables, a simplified approach to measuring expected credit losses using a lifetime expected loss allowance is available.

The adoption of AASB 9 did not have a material impact on the consolidated entity's financial statements and no adjustments were required.

25

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Notes to the consolidated financial statements30 June 2019

Note 2. Significant accounting policies (continued)

AASB 15 Revenue from Contracts with CustomersThe consolidated entity has adopted AASB 15 from 1 July 2018. The standard provides a single comprehensive model forrevenue recognition. The core principle of the standard is that an entity shall recognise revenue to depict the transfer of promised goods or services to customers at an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. The standard introduced a new contract-based revenue recognition model with a measurement approach that is based on an allocation of the transaction price. This is described further in the accounting policies below. Credit risk is presented separately as an expense rather than adjusted against revenue. Contracts with customers are presented in an entity's statement of financial position as a contract liability, a contract asset, or a receivable, depending on the relationship between the entity's performance and the customer's payment. Customer acquisition costs and costs to fulfil a contract can, subject to certain criteria, be capitalised as an asset and amortised over the contract period.

The consolidated entity has concluded that revenue from its sales should be recognised either at the point in time or over the time, when (or as) the consolidated entity satisfies performance obligations by transferring the promised services to its customers and generally this will take place at a point in time.

In applying AASB 15, the consolidated entity has elected to use the modified retrospective approach, with any adjustment required being recognised on 1 July 2018 in retained earnings.

The adoption of AASB 15 did not have a material impact on the timing or the amount of revenue recognition.

Going concernThe financial statements have been prepared on the going concern basis, which contemplates continuity of normal business activities and the realisation of assets and discharge of liabilities in the normal course of business.

As disclosed in the financial statements, the consolidated entity incurred a loss of $13.402 million and had net cash outflows from operating activities of $7.024 million for the year ended 30 June 2019. As at that date the consolidated entity had net current liabilities of $1.853 million.

These factors indicate a material uncertainty which may cast significant doubt as to whether the consolidated entity will continue as a going concern and therefore whether it will realise its assets and extinguish its liabilities in the normal course of business and at the amounts stated in the financial report.

The Directors believe that there are reasonable grounds to believe that the consolidated entity will be able to continue as a going concern, after consideration of the following factors:● On 18 July 2019, the consolidated entity secured a $4m facility with Timelio Pty Ltd which will support its working

capital requirements;● Management will continue to be focussed on achieving the forecasted growth of the consolidated entity;● The consolidated entity expects to raise further equity capital within the 12 months from reporting date;● The consolidated entity will attempt to secure projected new revenue contracts as per its cash forecast for the next

financial year; and● Management expects to manage its operating expenditures prudently and in line with its budget for the next financial

year.

Accordingly, the Directors believe that the consolidated entity will be able to continue as a going concern and that it is appropriate to adopt the going concern basis in the preparation of the financial report.

The financial report does not include any adjustments relating to the amounts or classification of recorded assets or liabilities that might be necessary if the consolidated entity does not continue as a going concern.

Basis of preparationThese general purpose financial statements have been prepared in accordance with Australian Accounting Standards and Interpretations issued by the Australian Accounting Standards Board ('AASB') and the Corporations Act 2001, as appropriate for for-profit oriented entities. These financial statements also comply with International Financial Reporting Standards as issued by the International Accounting Standards Board ('IASB').

26

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Notes to the consolidated financial statements30 June 2019

Note 2. Significant accounting policies (continued)

Historical cost conventionThe financial statements have been prepared under the historical cost convention, except for, where applicable, therevaluation of financial assets and liabilities at fair value through profit or loss, financial assets at fair value through other comprehensive income, investment properties, certain classes of property, plant and equipment and derivative financial instruments.

Critical accounting estimatesThe preparation of the financial statements requires the use of certain critical accounting estimates. It also requires management to exercise its judgement in the process of applying the consolidated entity's accounting policies. The areas involving a higher degree of judgement or complexity, or areas where assumptions and estimates are significant to the financial statements, are disclosed in note 3.

Parent entity informationIn accordance with the Corporations Act 2001, these financial statements present the results of the consolidated entity only. Supplementary information about the parent entity is disclosed in note 33.

Principles of consolidationThe consolidated financial statements incorporate the assets and liabilities of all subsidiaries of Wellness and Beauty Solutions Limited ('Company' or 'parent entity') as at 30 June 2019 and the results of all subsidiaries for the year then ended. Wellness and Beauty Solutions Limited and its subsidiaries together are referred to in these financial statements as the 'consolidated entity'.

Subsidiaries are all those entities over which the consolidated entity has control. The consolidated entity controls an entity when the consolidated entity is exposed to, or has rights to, variable returns from its involvement with the entity and has the ability to affect those returns through its power to direct the activities of the entity. Subsidiaries are fully consolidated from the date on which control is transferred to the consolidated entity. They are de-consolidated from the date that control ceases.

Intercompany transactions, balances and unrealised gains on transactions between entities in the consolidated entity are eliminated. Unrealised losses are also eliminated unless the transaction provides evidence of the impairment of the asset transferred. Accounting policies of subsidiaries have been changed where necessary to ensure consistency with the policies adopted by the consolidated entity.

The acquisition of subsidiaries is accounted for using the acquisition method of accounting. A change in ownership interest, without the loss of control, is accounted for as an equity transaction, where the difference between the consideration transferred and the book value of the share of the non-controlling interest acquired is recognised directly in equity attributable to the parent.

Where the consolidated entity loses control over a subsidiary, it derecognises the assets including goodwill, liabilities andnon-controlling interest in the subsidiary together with any cumulative translation differences recognised in equity. The consolidated entity recognises the fair value of the consideration received and the fair value of any investment retained together with any gain or loss in profit or loss.

Operating segmentsOperating segments are presented using the 'management approach', where the information presented is on the samebasis as the internal reports provided to the Chief Operating Decision Makers ('CODM'). The CODM is responsible for the allocation of resources to operating segments and assessing their performance.

27

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Notes to the consolidated financial statements30 June 2019

Note 2. Significant accounting policies (continued)

Revenue recognitionThe consolidated entity recognises revenue as follows:

Revenue from contracts with customersRevenue is recognised at an amount that reflects the consideration to which the consolidated entity is expected to be entitled in exchange for transferring goods or services to a customer. For each contract with a customer, the consolidated entity: identifies the contract with a customer; identifies the performance obligations in the contract; determines the transaction price which takes into account estimates of variable consideration and the time value of money; allocates the transaction price to the separate performance obligations on the basis of the relative stand-alone selling price of each distinct good or service to be delivered; and recognises revenue when or as each performance obligation is satisfied in a manner that depicts the transfer to the customer of the goods or services promised.

Variable consideration within the transaction price, if any, reflects concessions provided to the customer such as discounts, rebates and refunds, any potential bonuses receivable from the customer and any other contingent events. Such estimates are determined using either the 'expected value' or 'most likely amount' method. The measurement of variable consideration is subject to a constraining principle whereby revenue will only be recognised to the extent that it is highly probable that a significant reversal in the amount of cumulative revenue recognised will not occur. The measurement constraint continues until the uncertainty associated with the variable consideration is subsequently resolved. Amounts received that are subject to the constraining principle are recognised as a refund liability.

Sale of goodsRevenue from the sale of goods is recognised at the point in time when the customer obtains control of the goods, which isgenerally at the time of delivery.

Rendering of servicesRevenue from a contract to provide services is recognised at a point in time as the services are rendered based on either a fixed price or an hourly rate.

InterestInterest revenue is recognised as interest accrues using the effective interest method. This is a method of calculating theamortised cost of a financial asset and allocating the interest income over the relevant period using the effective interest rate, which is the rate that exactly discounts estimated future cash receipts through the expected life of the financial asset to the net carrying amount of the financial asset.

Other revenueOther revenue is recognised when it is received or when the right to receive payment is established.

Income taxThe income tax expense or benefit for the period is the tax payable on that period's taxable income based on theapplicable income tax rate for each jurisdiction, adjusted by the changes in deferred tax assets and liabilities attributable to temporary differences, unused tax losses and the adjustment recognised for prior periods, where applicable.

Deferred tax assets and liabilities are recognised for temporary differences at the tax rates expected to be applied when the assets are recovered or liabilities are settled, based on those tax rates that are enacted or substantively enacted, except for:● When the deferred income tax asset or liability arises from the initial recognition of goodwill or an asset or liability in a

transaction that is not a business combination and that, at the time of the transaction, affects neither the accountingnor taxable profits; or

● When the taxable temporary difference is associated with interests in subsidiaries, associates or joint ventures, and the timing of the reversal can be controlled and it is probable that the temporary difference will not reverse in theforeseeable future.

Deferred tax assets are recognised for deductible temporary differences and unused tax losses only if it is probable that future taxable amounts will be available to utilise those temporary differences and losses.

28

For

per

sona

l use

onl

y

Wellness and Beauty Solutions Limited(Formerly known as Total Face Group Limited)Notes to the consolidated financial statements30 June 2019

Note 2. Significant accounting policies (continued)

The carrying amount of recognised and unrecognised deferred tax assets are reviewed at each reporting date. Deferred tax assets recognised are reduced to the extent that it is no longer probable that future taxable profits will be available for the carrying amount to be recovered. Previously unrecognised deferred tax assets are recognised to the extent that it is probable that there are future taxable profits available to recover the asset.

Deferred tax assets and liabilities are offset only where there is a legally enforceable right to offset current tax assets against current tax liabilities and deferred tax assets against deferred tax liabilities; and they relate to the same taxable authority on either the same taxable entity or different taxable entities which intend to settle simultaneously.

Wellness and Beauty Solutions Limited (the 'head entity') and its wholly-owned Australian subsidiaries have formed an income tax consolidated group under the tax consolidation regime. The head entity and each subsidiary in the tax consolidated group continue to account for their own current and deferred tax amounts. The tax consolidated group has applied the 'separate taxpayer within group' approach in determining the appropriate amount of taxes to allocate to members of the tax consolidated group.

In addition to its own current and deferred tax amounts, the head entity also recognises the current tax liabilities (or assets) and the deferred tax assets arising from unused tax losses and unused tax credits assumed from each subsidiary in the tax consolidated group.