WELCOME TO WPA Insurance Panel - Western Pallet … / IsPollution Surety Surplus NoLines Guaranteed...

40

WELCOME TO WPA Insurance Panel January 20, 2014

Transcript of WELCOME TO WPA Insurance Panel - Western Pallet … / IsPollution Surety Surplus NoLines Guaranteed...

WELCOME TO WPA

Insurance Panel

January 20, 2014

MICHAEL OSKOUIAN, CRM, CIC, LUTCF – BIO

Michael is a Vice President within the Willis North America Practice and is located in

Seattle. He specializes in identifying risks and providing valuable solutions within the

areas of Property and Casualty. As a Certified Risk Manager and an Entrepreneur he

understands the business risks owners face every day and has the solutions to mitigate

those risks. Prior to joining Willis, Michael owned an insurance agency in Seattle for

eighteen years (18) employing a staff of 20.

Michael Oskouian, CRM, CIC, LUTCF

(425) 260-4030 Cell

(206) 386-7474 Direct

(206) 386-7400 Office

505 5th Ave S

Suite 200

Seattle, WA 98104

Email: [email protected]

Willis is a Risk Advisor: 100% Transparent

Client Broker Insurer

Client Advisor Broker Insurer

bigger

ANALYTIC/MODELING TOOLS

ANALYTIC/MODELING TOOLS

ANALYTIC/MODELING TOOLS

ANALYTIC/MODELING TOOLS

WHAT UNDERWRITERS REQUIRE

IN A SUBMISSION

Description of Operations

Program Specifications

Value Summaries

Loss History

Policy Form

Engineering

Casualty Expertise Portals

Casualty Communities linking Experts and Evolution

Employee Health and Safety Product Liability

Casualty

General and Auto Liability

Catastrophic & Excess Risks

Collateral and Risk Finance

Casualty Expert Teams

Building Communities of the Best Brokers to build Best Practices and Coverage Specifications

We have assembled 6 Expert Working Groups:

Workers Comp

Auto Liability

General Liability

Product Liability

Umbrella and Excess Liability

Collateral and Risk Finance Teams are comprised of National, Regional and Local Experts with technical expertise in an industry, risk, state or coverage.

National Casualty Practice

Unlocking the Power of Connection

Casualty Expert Team Members are easy to spot by

the Blue Ribbon Banner highlighting their Avatar!

Great Advocates Deliver Value

Cost Reduction in Casualty Costs can deliver more Cash, Capital

and/or Earnings

Casualty Savings drop to the Bottom Line

I have yet to meet a CFO or Treasurer or Risk Manager that feels

their Capital is best deployed in their Risk Management Program.

I have met CFOs and Treasurers that have perceived economic

value in new structures, additional limits or better coverage

Communicate value in a common economic value

Building the Best Team

Willis Service Plan – Best Practices Time Table

Client Name

Client Name ABC Company

Renewal Date 8/1/2014 Today's Date 1/6/2014

Client Coverage Lines / Industry

Workers Compensation

Automobile Liability

General Liability

Property

Construction

Healthcare

Executive Risks

Environmental / Pollution

Surety

Surplus Lines

Guaranteed Cost

Premium Financing

Loss Data

Is WC a part of this placement?

Is AL a part of this placement?

Is GL a part of this placement?

Is Property a part of this placement?

Is Construction a part of this placement?

Is Healthcare a part of this placement?

Is Executive Risks a part of this placement?

Is Environmental / Pollution a part of this placement?

Is Surety a part of this placement?

Does this placement involve SL?

Is this placement a guaranteed cost?

Is Premium Financing an interest?

Does client have credible loss data?

Yes

Yes

Yes

Yes

No

No

No

No

No

No

No

No

Yes

Team Role Assignment

Client ABC Company

Client Advocate Pam

Client Manager Mike

Senior Client Manager Karen

Assistant Client Manager Mary

Placement Specialists / Marketing Steve

Industry Marketing Specialists Rob

Risk Consultant (Claims Specialists) Lori

Loss Control Specialists Jim

Consistently delivering a Great Casualty Program

Best Practices – Casualty Service Plan

ABC Company Willis Service Plan (WSP)

Best Practices Timetable

Action Task Target Date

1. Client Advocacy Report [Annual Review / Stewardship Report] 11/4/2013 - 270

2. Client Service Evaluation [Client Survey]

3. Delivery of the Client Engagement Guide

4. Conduct Analytics Meetings with Incumbent Market [Actuarial / Credit / Underwriting]

5. Needs Analysis / Risk Assessment / Identification Review

6. Prepare for Renewal Strategy Meeting

7. Conduct Team Renewal Strategy Meeting

8. Conduct Client Renewal Strategy Meeting

9. Prepare Submission - Gather and Review Underwriting Data - Losses, Exposures, Coverage Specs & Financials

10. Send Submission to Client and Market(s)

11. Meet with Market(s) to Provide Quotes

12. Analyze Quotation Proposals

13. Prepare Renewal Proposal

14. Present Renewal Proposal to Client

15. Bind Renewals

16. Invoicing

17. Policy Administration - Certs / ID Cards / Posting Notices / UM UIM Forms

18. Renewal Incepts

19. Receive and Review Renewal Policies

20. Deliver Policies to Client

21. Obtain Client Feedback

Note: Blue italic if Action Task should have been completed by today's date.

12/4/2013 - 240

2/2/2014 - 180

2/2/2014 - 180

T 3/14/2014 - 140

I 3/14/2014 - 140

M 3/24/2014 - 130

E 4/3/2014 - 120

5/3/2014 - 90

L 5/3/2014 - 90

I 5/18/2014 - 75

N 6/2/2014 - 60

E 6/12/2014 - 50

6/22/2014 - 40

7/2/2014 - 30

7/12/2014 - 20

7/17/2014 - 15

8/1/2014 0

8/31/2014 30

9/15/2014 45

9/15/2014 45

Consistently delivering a Great Casualty Program

Delivering the Value

> Present Client Advocacy Report - review and meet with Client - obtain BOR's if necessary 11/04/13 Overdue task Pam

> Document discussions with Client 11/04/13 Overdue task Pam

2. 240 Days Prior - Client Service Evaluation [Client Survey] > Client Service Evaluation [Client Survey] 12/04/13 Overdue task Pam

> Formal evaluation of the overall quality and delivery of broking and risk management services using the electronic client survey

and open discussions

12/04/13

Overdue task

Pam

> Discussion about areas or activities currently not covered by the insurance program 12/04/13 Overdue task Pam

> Advise Client about Survey 12/04/13 Overdue task Pam

> Provide and review Client Survey results with the client team 12/04/13 Overdue task Pam

> Prepare and send "Thank You" letter to Client 12/04/13 Overdue task Pam

> Schedule and conduct Client Survey meeting to review the results 12/04/13 Overdue task Pam

> Document discussions with Client 12/04/13 Overdue task Pam

> Conduct Broker Claim Review - (Strategic Outcomes Practice delivers Claim, Risk Control, Safety and Data Analytic consulting services) 12/04/13 Overdue task Mike / Lori

- Evaluate claim reserves - Reserve to present known outcome 12/04/13 Overdue task Mike / Lori

- Audit claim activity 12/04/13 Overdue task Mike / Lori

- Resolution of pending claims 12/04/13 Overdue task Mike / Lori

- Identify subrogation potential 12/04/13 Overdue task Mike / Lori

- Adherence to action plan for claim resolution / closure 12/04/13 Overdue task Mike / Lori

- Evaluate claims servicing account instructions 12/04/13 Overdue task Mike / Lori

- Identify adjuster service issues 12/04/13 Overdue task Mike / Lori

- Evaluate Managed Care and Bill Re-pricing activity 12/04/13 Overdue task Mike / Lori

> Document claim review discussions with Client, Carrier and Client Team 12/04/13 Overdue task Mike / Lori

> Workers' Compensation Experience Modification review 12/04/13 Overdue task Mike / Lori

3. 180 Days Prior - Delivery of the Client Engagement Guide (CEG) > Create Master Marketing File (required for documentation) 02/02/14 Pam

> Prepare Placing File Checklist (PFC) to document compliance requirements and place copy in file (and WPC) 02/02/14 Pam

> Prepare Client Relationship Information Pack (Client Engagement Guide) 02/02/14 Pam

> Present and discuss the following key documents which define the way we work together to the Client: 02/02/14 Pam

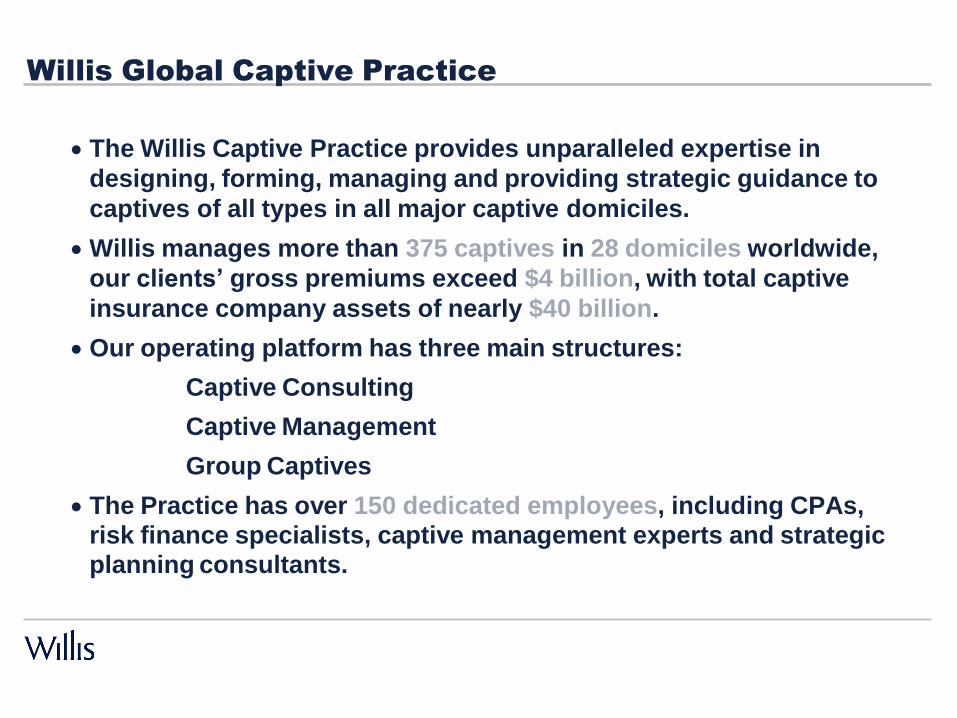

Willis Global Captive Practice

The Willis Captive Practice provides unparalleled expertise in

designing, forming, managing and providing strategic guidance to

captives of all types in all major captive domiciles.

Willis manages more than 375 captives in 28 domiciles worldwide,

our clients’ gross premiums exceed $4 billion, with total captive

insurance company assets of nearly $40 billion.

Our operating platform has three main structures:

Captive Consulting

Captive Management

Group Captives

The Practice has over 150 dedicated employees, including CPAs, risk finance specialists, captive management experts and strategic planning consultants.

The Americas

Les Boughner

Executive VP & MD of the Willis Captive Management Practice

Group Captives

Randy Boomgarden

Alembic

Craig Ream

Construction Solutions

Consulting/Sales

Sean Rider – New York

Richard W. Wright – New Jersey

Anne Marie Towle - Chicago

Kathleen Waslov – Employee Benefits

Bruce Whitmore - Healthcare

Willis Management

(Bermuda), Ltd.

Oliver Heyliger

Willis Management

(Cayman), Ltd.

Barbados

Stephen Gray

Willis Management

(Vermont), Ltd.

New York, South

Carolina, Tennessee

David Guerino

Willis Management

(Hawaii)

Arizona, Nevada,

Utah

Jason Palmer

Willis Captive Practice

Captive Consulting

New Captive Feasibility

Strategic Consulting for Mature Captives

Captive Management

Liaison with Actuaries, Regulators, Auditors

Ongoing servicing

Preparation of captive financials

Ongoing filing maintenance

Shareholder Board of Directors meeting

Group Captives

Willis Captive Consulting Practice

Strategic Consulting for Mature Captives

Our various efforts classed as “strategic consulting for mature captives” aim at assessing and maximizing how an organization achieves value from an existing captive vehicle. As organizations change and regulatory, domicile, tax, and risk tolerance regimes morph over time, the efficacy of captives and their utilization opportunities also change. Our services are focused on helping captive owners determine the optimal use, structure, and/or winding down of a captive.

Periodic brainstorming with key members of the captive owner’s management group and other service partners to consider risk retention levels and alternatives, additional lines of coverage, what-if scenarios, domicile issues, etc.

Interpretation and analysis of actuarial, financial, and other captive data; Attendance and participation at captive board meetings; Keeping the captive’s leadership current with captive industry, domicile, tax and accounting changes

and assessing the impact of these changes; Providing an independent voice in vendor assessment and assisting in RFP processes as needed; Evaluating risk areas where the captive’s participation would enhance protection and reduce cost-of-

risk; Evaluation of the ongoing efficacy of a captive, and management of the outcomes of that analysis.

Lines of Business

TRADITIONAL EXPANDED EMERGING

Workers’ Compensation

Auto Liability

General Liability

Professional and Products

Liability

Director and Officer Liability

Employment Practices

Liability

Environmental Liability

Product or Service

Extended Warranty

Property and Business

Interruption

EE Benefits

Terrorism (TRIA)

Shipping Coverage

Title and Private Mortgage

Insurance

Equipment Maintenance

Construction Exposures

Trade Credit Risk

Cyber-Risk

Managed Care Errors and

Omissions

Self-Insured Medical

Stop-Loss (non-

ERISA)

Reputation/Brand/Loss

of Income Risks

Intellectual Property

(patent, trademark,

copyright)

Product Recall

Coverage

Medicare “Fraud and

Abuse” Insurance

Lease Residual Value

Risk

Punitive Damages

Coverage

Types of Captive Utilization

Retained Risk

Finance

Risk Transfer

Rate Arbitrage

Access to

Capacity

Entrepreneurial

Utilizations

Infrastructure for

providing

transparency,

validation, and

rationalization of

retained risk

positions

Enhancing risk

management

efforts

Accelerating tax

treatment of

deductible

liabilities

Reinsurance

market cost of risk

transfer is less

than commercial

retail cost of risk

transfer

Better use of

capital to retain

risk than transfer it

Managing total

cost of risk

Federal programs

(TRIA)

Reinsurance

capacity, which

may not be

otherwise

accessible in

commercial retail

market (trade

credit risk, +10 yr

pollutions risks)

Franchisee

programs

Consumer facing

insurance

programs

(warranty, service

contract, point of

sale insurances,

etc)

Affiliate business

(vendors, VAPs,

distributors, etc)

Agency captives

3rd party business

831b / Microcaptives

• Underwriting income for the captive is tax free.

• Can be utilized as a wealth transfer and estate planning vehicle

for private companies.

• Willis will only become involved with Microcaptives when there is a

sustainable business plan.

831b / Microcaptives

Under the provisions of the United States Tax Code

§831(b), a tax election may be available to U.S. Property

and Casualty ("P&C") Insurers (Small Insurance

Companies) with written premiums less than $1.2 million

dollars. If properly structured, the insurance company is

taxed on net investment income only and not on

underwriting income. Non-taxed underwriting income, if any

will accrue to the captive’s surplus and dividends and may

be eligible for the dividends received deduction when

distributed to the corporate shareholder(s) or parent, and

dividends distributed to an individual owner are taxed at the

capital gains rate

The aim is to put our clients in a superior

information position

Resilience example: ERM Maturity Model

Framework Element Immature Basic Mature Advanced World-Class

Risk Identification

No formal process for

identification of risks

Annual risk

identification exercise

for key projects and

sites

Key corporate risks

identified with limited

interaction among

groups

Business risks

frequently identified

with assessment of

likelihood, impact and

mitigating actions;

cross-group work

All major risks regularly

identified. Robust

process also surfaces

new and emerging

risks

Risk Assessment and Prioritization

No formal process for

assessment of risks

Limited analysis to

assess and provide

insight. Major business

risks discussed at

Business Unit level

Prioritization of key

risks across the group

with detailed

quantification of

selected risks

Prioritization based on

aggregation of all

business risks across

the group; risk

tolerance known and

included in assessment

Prioritization of

aggregated risks

across group with

classification by key

underlying risk drivers

and company-killer

scenarios

Risk Mitigation and Financing Options

Little or no systematic

development and

comparison of options;

external risk reporting

requirements

sometimes not met

Methodologies for risk

categories identified

and used inconsistently;

compliance mentality

Options compared

within business units

using consistent

methods but done

within functions

primarily

Company-wide

comparison of options,

but within functions

(finance, operations,

insurance, construction,

etc)

Options compared

across company and

across functions in

single language of risk

and decisions made

accordingly

Risk Strategy and Action Plans

Risk Implementation

No action plan for risk

management and

finance exists

Little or no follow-

through on option

recommendations;

poor results in key risk

management metrics

One or more action

plans exists within one

or more functions and

one or more business

units

Some key risks are

managed resulting in

fewer surprises; but

little or no preparation

for major risk response

Functions each have

an independent action

plan with limited or no

communication with

other functions;

business units may

have action plans

Functions implement

their action plans well

and business units

track progress of these

functional plans

Action plans completed

annually within

functions and business

units in consistent

manner

Top management

tracks business unit

and function progress

and oversees

implementation

Board has ‘owners’ of

key ‘black swan’

scenarios and is

continuously engaged

in assessing action

plans, all of which are

in single risk language

Board receives

updates on actions

regularly, participates

in simulation exercises

and guides

management

IMP

LE

ME

NTA

TIO

N

RIS

K S

TR

AT

EG

Y

How Willis GSCG Thinks About Risk

Client Risk Landscape

Risk Insight Steps Solution Choices

6. Retain

- Balance Sheet

- Captive

1. 2. 3. 4. 5. 7. Transfer Understand Client and

Define Risk Tolerance

Identify Priority

Model Loss Frequency

Calculate CCoRSM

- To Insurers - To Capital

Industry Dynamics

Exposures and Risks

and Severity Markets

8. Mitigate

Data gathering, preparation and provision

9. Avoid

Risk financing options Risk management options

Earthquake Loss OEP Curve 8

)

($mn 7

ss o L 6

ed l el 5 d o M 4

3

2 Policy Programme Activation Exhaustion

1

-

- 200 400 600 800 1,000

Return Period (yrs)

$ M

illio

ns

Mo

de

lle

d L

os

s (

$m

n)

Proprietary Tools and Processes

FIASM (Financial Impact Analysis)

Measures an organizations risk tolerance based on pre-determined ranges

of variability in key financial metrics

5

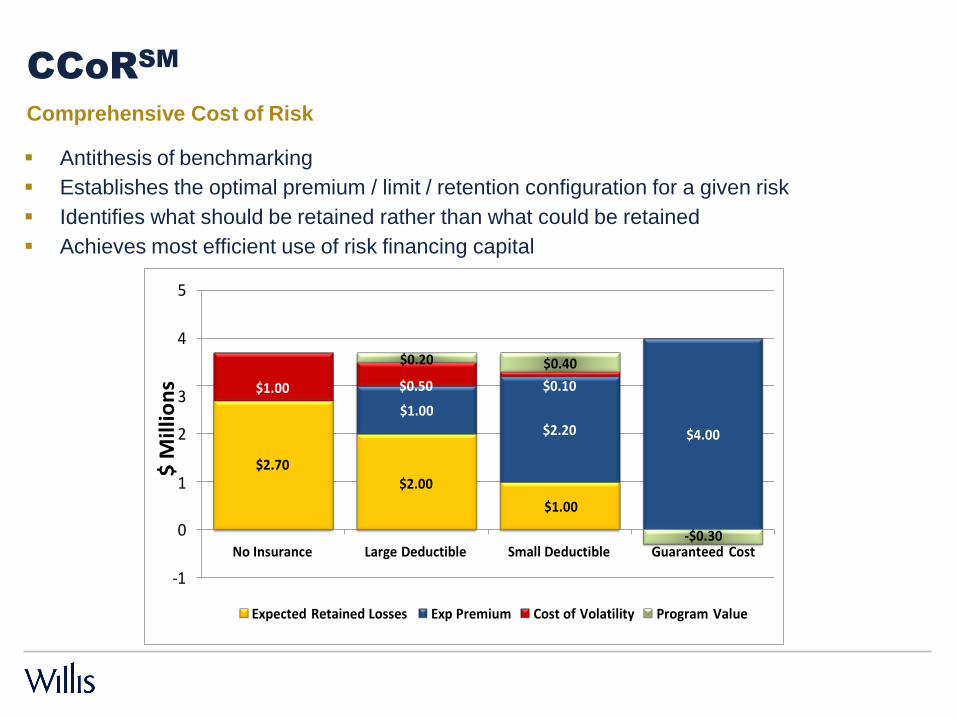

CCoRSM (Comprehensive Cost of Risk) Identifies technically optimal risk financing program structure for a given risk

4

$0.20 $0.40

3 $1.00 $0.50 $0.10

$1.00

2 $2.20 $4.00

$2.70

1 $2.00

and quantifies volatility of retained risk $1.00

0

-1

-$0.30

No Insurance Large Deductible Small Deductible Guaranteed Cost

Expected Retained Losses Exp Premium Cost of Volatility Program Value

PRISMSM (Privacy Risk Insurance Strategy Model)

Quantifies privacy risk data and identifies optimal insurance program

structure WISDOMSM (Willis Integrated Solutions Directors & Officers Model)

Quantifies D&O risk, identifies optimal insurance structure

Natural Catastrophe Analysis Modeling and managing natural catastrophe (nat. cat) risk

Earthquake Loss OEP Curve

8

7

6

5

4

3

2 Policy Activation

1

Programme

Exhaustion

-

- 200 400 600 800 1,000

Return Period (yrs)

FIA

Financial Impact Analysis

Establish the “surprise” negative

deviations in key financial metrics that a

company is able to sustain in a given year

Model the company's financials to

demonstrate the impact of increasing

levels of retained downside risks on these

metrics

Incorporate the output into a risk financing

strategy that achieves lowest cost of risk

within the acceptable range of tolerance

$ M

illi

on

s

CCoRSM

Comprehensive Cost of Risk

Antithesis of benchmarking

Establishes the optimal premium / limit / retention configuration for a given risk

Identifies what should be retained rather than what could be retained

Achieves most efficient use of risk financing capital

5

4 $0.20 $0.40

3 $1.00 $0.50 $0.10

$1.00

2 $2.20 $4.00

$2.70 1 $2.00

$1.00

0

-$0.30

No Insurance Large Deductible Small Deductible Guaranteed Cost

-1

Expected Retained Losses Exp Premium Cost of Volatility Program Value

Pro

bab

ilit

y (

%)

CCoRSM

100%

90%

80%

70%

60%

After risk financing

(Including Prem)

Before risk financing

50%

40%

30%

Risk Volatility

20%

10% Risk Volatility

0%

Expected Loss

2.7 3.2

4.2

Impact ($MM)

12.7

Value of Various Privacy Breach Insurance Structures

(Safety Level = 99.9% )

3,000,000 33,481

2,500,000 358,606 512,596

500,000 2,000,000

1,400,000

1,744,727 750,000

1,500,000 1,260,518

1,245,083 1,000,000 936,118 721,090

389,377

500,000 976,881 617,918 522,893 567,036 559,116

0

No Insurance 25M/25M xs 2M 50M/35M xs 2M 100M/50M xs 5M 175M/175M xs 10M

Expected Retained Losses Cost of Volatility Premium Value "Break-Even" Premium

CU

MU

LA

TIV

E P

RO

BA

BIL

ITY

(C

ON

FID

EN

CE

LE

VE

Cu

mu

lati

ve

Pro

bab

ilit

y

PRISMSM

Privacy Risk Insurance Strategy Model

Analytic model used to quantify privacy risk

Accesses a proprietary database of thousands of

privacy risks

0.25

0.20

0.15

100%

90%

80%

70%

60%

Probability Distribution of Total Records Affected

(Actual Total Records Affected vs Selected Distribution)

Adjusts industry data relative to client-specific

risks and controls

Applies Monte Carlo simulation to generate

several thousand hypothetical loss years

Utilizes CCoRSM to determine the optimal

privacy insurance program structure

0.10

0.05

0.00

2006 2007 2008 2009 2010 2011

Historical Breach Frequency Projected Breach Frequency

50%

40%

30%

20%

10%

0%

1 10 100 1,000 10,000 100,000 1,000,000 10,000,000 100,000,000

Total Records Affected (Logarithmic Scale)

Actual Total Records Affected Selected Severity Distribution

UNINSURED LOSS PROBABILITY DISTRIBUTIONS

100.0%

95.0%

90.0%

85.0%

80.0%

75.0%

70.0%

65.0%

60.0%

55.0%

50.0%

$100 $1,000 $10,000 $100,000 $1,000,000 $10,000,000 $100,000,000

AGGREGATE ANNUAL LOSSES

Discovery, Notification, Response Regulatory Fines All Other Insurable Costs Total

WISDOMSM

Willis Integrated Solutions Directors & Officers Model

Analytic tool used to quantify D&O risks for

public companies

Generates a frequency distribution based

on industry, market cap, and a robust

proprietary database of historic D&O

losses

Generates a severity distribution using the

proprietary database of historic D&O

losses

Combines frequency and severity

distributions, simulating thousands of

hypothetical loss years using Monte Carlo

Simulation

Utilizes CCoRSM to determine the optimal

D&O insurance program structure

Earthquake Loss OEP Curve 8

)

($mn 7

ss o L 6

ed l el 5 d o

M 4

3

2 Policy Programme Activation Exhaustion

1

-

- 200 400 600 800 1,000

Return Period (yrs)

Mo

dell

ed

Lo

ss

($m

n)

Natural Catastrophe Analysis

Strategic CAT review

High level review and mapping of a client’s natural hazard

exposures on a regional or global basis.

CAT Modeling

Use of natural catastrophe models to quantify a client’s portfolio

Earthquake Loss OEP Curve

8

7

6

5

losses at an aggregate level and compare against their current

retention levels and CAT limits in their insurance program

4

3

2 Policy Activation

1

-

Programme

Exhaustion

- 200 400 600 800 1,000

Return Period (yrs)

CAT Risk Engineering

On-site risk engineering surveys for individual facilities that are

identified as having high levels of localized property damage and

business interruption exposures. Provision of cost-effective

improvement measures to reduce the exposure.

1 2 3

LossPIQSM

Overview

Prospective Identification & Quantification

Quantifies low frequency / high severity risks where loss data is scare or non-existent

Identifies most plausible future loss scenarios

Willis develops a loss model for each risk and populates it with risk impact types and cost

drivers

Expert client team disassembles each major scenario into 3 sub-scenarios and then by

consensus assigns impact and likelihood parameters

Model aggregates data and generates an overall loss distributions curve of the risk

Synthesize most

plausible future

scenarios

Transition qualitative

into quantitative

measurement

Integrate with historical

and public domain data,

run simulations

DENIAL OF ACCESS COSTS

Notification Recovery Site Invocation Alternative Accommodations

# of Locations % of Events

This Would Occur

# Days

Low

# Days

High

% of Events

This Would Occur

# of Alt

Sites

# Years

Rental

% of Events

This Would Occur

Scenario Subscenario Description/Comments Likelihood Low High

DOA - Natural Event Anticipated UK Southern Severe Snow DOA - Natural Event Mid Range London Flood DOA - Natural Event Worst Case Pandemic Affecting >30%

DOA - Man Made Event Anticipated Building evacuation DOA - Man Made Event Mid Range Terrorist non-CBNR attack DOA - Man Made Event Worst Case Terrorist CBNR attack

Information Security Breach Anticipated Unauthorized access Information Security Breach Mid Range Data leakage Information Security Breach Worst Case Malicious cyber attack

Infrastructure Failure Anticipated Power/cooling outage Infrastructure Failure Mid Range Data corruption Infrastructure Failure Worst Case Multiple data center losses Inadequate Planning Anticipated Included in other scenarios Inadequate Planning Mid Range Included in other scenarios Inadequate Planning Worst Case Included in other scenarios

Third Party/Vendor Error Anticipated Virus Third Party/Vendor Error Mid Range Connectivity/network outage Third Party/Vendor Error Worst Case SBSA domain security outage

Regulatory Censure Anticipated Greater regulatory oversight/fines Regulatory Censure Mid Range Conditions on license/fines>$10M Regulatory Censure Worst Case Loss or suspension of license/removal of senior mgt

DOA - Political/Social Unrest Anticipated Industrial action DOA - Political/Social Unrest Mid Range Large scale civil unrest DOA - Political/Social Unrest Worst Case Civil war in South Africa

Anticipated Mid Range Worst Case

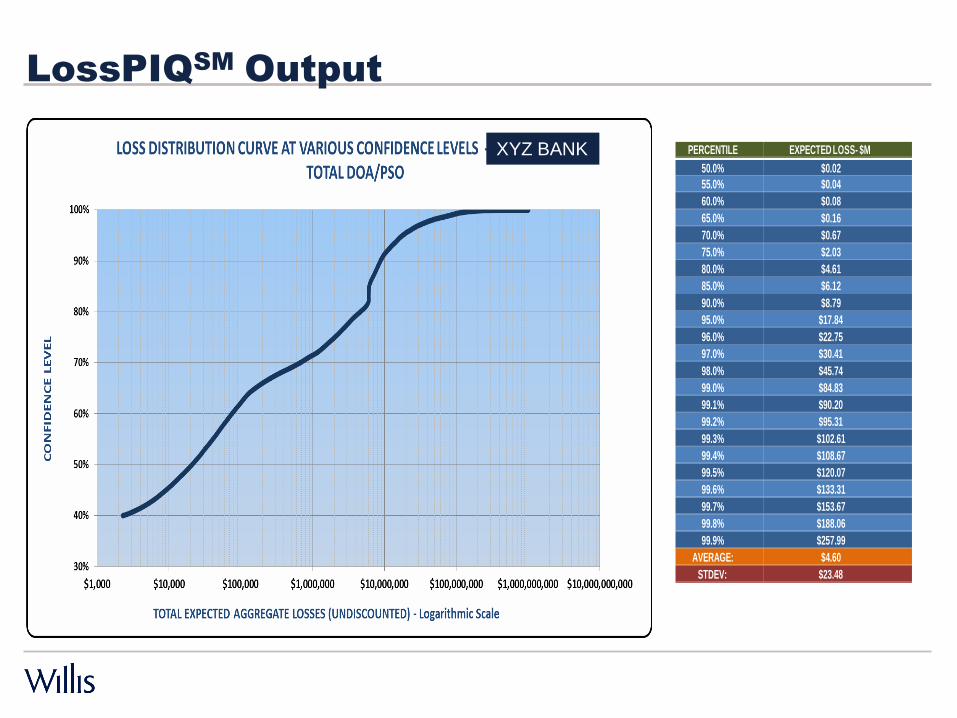

LossPIQSM

Risk Register

XYZ BANK

PERCENTILE EXPECTED LOSS- $M

50.0% $0.02

55.0% $0.04

60.0% $0.08

65.0% $0.16

70.0% $0.67

75.0% $2.03

80.0% $4.61

85.0% $6.12

90.0% $8.79

95.0% $17.84

96.0% $22.75

97.0% $30.41

98.0% $45.74

99.0% $84.83

99.1% $90.20

99.2% $95.31

99.3% $102.61

99.4% $108.67

99.5% $120.07

99.6% $133.31

99.7% $153.67

99.8% $188.06

99.9% $257.99

AVERAGE: $4.60

STDEV: $23.48

LossPIQSM

Output

XYZ BANK

RAPIDSM

Risk Assessment Probability & Impact Diagnostic

FEATURES

Consensus driven process to identify, assess, and communicate enterprise risk

Can be used across an enterprise or on a surgical basis

Comprehensive, accelerated, and cost effective

Fully articulates and prioritizes the major risks to achieving business objectives

Surfaces emerging and unforeseen risks

Generates high impact, real time graphics

Built-in module for Improvement Planning

Risk Optimizer

Combines CCoRSM and FIA

CCoRSM establishes optimal structure by line of coverage

FIA establishes corporate risk tolerance level

Probability of collective retentions breaching tolerance is determined

Individual retentions are adjusted to accommodate overall tolerance and risk appetite

Analytics are periodically recalculated to accommodate changes in both risks and

financials

Program structure is adjusted as necessary to maintain the lowest cost within the risk

tolerance level

Pro

b.

of

Ex

ce

ed

ing

$50M

Ab

ove

Exp

ecte

d C

ost

Risk Optimizer

Risk Optimizer

(Expected Cost vs Probability of Exceeding $50M Risk Tolerance,

Excluding No Insurance)

1.90%

1.85%

1.80%

Current

1.75%

1.70%

1.65%

1.60%

13622

(12622)

13612 (12612)

13412

(12412)

13411

33412

33411

(32411)

36.0 36.5 37.0 37.5 38.0 38.5 39.0 39.5 40.0

Millions

Expected Cost (Premium + Discounted Expected Retained Losses)

We are honored to be part of

Western Pallet Association.

THANK YOU