WELCOME TO PRESENTATION ON FINANCIAL INCLUSION NABARD RAJASTHAN REGIONALOFFICE JAIPUR.

26

WELCOME TO WELCOME TO PRESENTATION ON PRESENTATION ON FINANCIAL INCLUSION FINANCIAL INCLUSION NABARD NABARD RAJASTHAN REGIONALOFFICE RAJASTHAN REGIONALOFFICE JAIPUR JAIPUR

-

Upload

maurice-daniel -

Category

Documents

-

view

221 -

download

0

Transcript of WELCOME TO PRESENTATION ON FINANCIAL INCLUSION NABARD RAJASTHAN REGIONALOFFICE JAIPUR.

WELCOME TO WELCOME TO PRESENTATION ON PRESENTATION ON

FINANCIAL INCLUSIONFINANCIAL INCLUSION

NABARD NABARD RAJASTHAN REGIONALOFFICERAJASTHAN REGIONALOFFICE

JAIPURJAIPUR

Structure of PresentationStructure of Presentation

What is Financial Inclusion – various What is Financial Inclusion – various definitions – meaning definitions – meaning

Why Financial Inclusion – National and Why Financial Inclusion – National and State scenario State scenario

How to go about it- Various optionsHow to go about it- Various options

Support available from NABARD Support available from NABARD

Few Initiatives taken by banks Few Initiatives taken by banks

What is Financial InclusionWhat is Financial Inclusion

“ “the the processprocess of ensuring of ensuring access to access to financial servicesfinancial services and and timely and timely and adequate creditadequate credit where needed by where needed by vulnerable groupsvulnerable groups such as weaker such as weaker sections and low income groups at an sections and low income groups at an affordable costaffordable cost.” --- C Rangarajan .” --- C Rangarajan

What is Financial InclusionWhat is Financial Inclusion

“ “expanding access to financial services, such as payments services, savings products, insurance products,

and inflation-protected pensions...” ”

– – Raghuram Committee Raghuram Committee on

Financial Sector Reforms (CFSR)

Financial Inclusion meansFinancial Inclusion means

Basic “no frills” bank account for receiving payments /savings / deposits

Small loan/overdraft facilities

Money transfer facilities

Insurance (life / non-life) services

Financial advisory services

What is Financial InclusionWhat is Financial Inclusion

While financial inclusion, in the narrow

sense, may be achieved to some extent

by offering any one of these financial services, the objective of “Comprehensive Financial Inclusion” would be to provide a holistic set of financial services .

What is Financial Inclusion – few What is Financial Inclusion – few questions questions

BasisBasis - - whether individual, every adult whether individual, every adult family member/householdfamily member/household

CoverageCoverage – only rural or urban – only rural or urban

population is also to be ‘included’ population is also to be ‘included’

What about ‘inclusion of segments like What about ‘inclusion of segments like women, minoritieswomen, minorities’ ’

Why Financial InclusionWhy Financial Inclusion Directive Principles – equal opportunities Directive Principles – equal opportunities

Inclusive growth Inclusive growth

Economic development Economic development

Social development Social development

and and

Business opportunity Business opportunity

Financial Inclusion – Steps taken Financial Inclusion – Steps taken by Banking Industry in India by Banking Industry in India

Nationalisation of BanksNationalisation of Banks

Introduction of Lead Bank SchemeIntroduction of Lead Bank Scheme

Introduction of Priority Sector NormsIntroduction of Priority Sector Norms

Introduction of Service Area ConceptIntroduction of Service Area Concept

Adoption of Villages by Bank BranchesAdoption of Villages by Bank Branches

Formation of Regional Rural BanksFormation of Regional Rural Banks

Strengthening of Cooperatives Strengthening of Cooperatives

Banking Network in IndiaBanking Network in India

• Rural and Semi-urban BranchesRural and Semi-urban Branches

- Commercial Banks- Commercial Banks = 33,000= 33,000

- Regional Rural Banks- Regional Rural Banks = 14,500= 14,500

- Cooperatives- Cooperatives = 106,000= 106,000

TotalTotal = 153,500= 153,500• Avg. No. of villages served per branch – 4 Avg. No. of villages served per branch – 4

Is the distribution equitable ? ?Is the distribution equitable ? ?

90% villages don’t have a bank branch within 5 km radius

Extent of Financial Exclusion - IndiaExtent of Financial Exclusion - India51.4% of 89.3 million farmer households51.4% of 89.3 million farmer households are are excludedexcluded from both formal/ informal from both formal/ informal sourcessources

Only 27%Only 27% of the total farmer households, of the total farmer households, access formal sources of creditaccess formal sources of credit

66% marginal farmer66% marginal farmer households excluded households excluded

(NSSO data 59(NSSO data 59thth round ) round )

Financial Exclusion in RajasthanFinancial Exclusion in Rajasthan

47.6%47.6% of farmer households are of farmer households are excluded from both formal / informal excluded from both formal / informal sourcessources

Outreach of formal financial institutions Outreach of formal financial institutions is around is around 35% households35% households

SHG / MFI – outreach to about SHG / MFI – outreach to about 25% 25% families in rural areasfamilies in rural areas but cater to only but cater to only limited financial needs limited financial needs

Gradation of FinancialGradation of Financial ExclusionExclusion

Core ExclusionCore Exclusion : Who operate their : Who operate their financial affairs outside the regulated financial affairs outside the regulated financial systemfinancial system

Limited AccessLimited Access : May have a basic : May have a basic bank account but poor financial habits bank account but poor financial habits and little adviceand little advice

Though Included but using Though Included but using inappropriate productsinappropriate products

Reasons for Financial ExclusionReasons for Financial ExclusionPhysical distancePhysical distanceMutual disbelief – poor are not bankable, Mutual disbelief – poor are not bankable, on other side banks and other FIs are not on other side banks and other FIs are not for usfor usLack of appropriate products/servicesLack of appropriate products/servicesLack of awareness, financial illiteracy Lack of awareness, financial illiteracy Processes too tedious and complicated Processes too tedious and complicated

andand AAJ TIME NAHI HAI/STAFF CHHUTTI AAJ TIME NAHI HAI/STAFF CHHUTTI

PAR HAI/ CLOSING HAI, KAL AANA -”.PAR HAI/ CLOSING HAI, KAL AANA -”.

National Rural Financial National Rural Financial Inclusion Plan (NRFIP)Inclusion Plan (NRFIP)

Provide Provide comprehensive financial comprehensive financial servicesservices to to atleast 50%atleast 50% (55.77 (55.77 million) of the excluded rural million) of the excluded rural cultivator and non-cultivator cultivator and non-cultivator households across different states by households across different states by 20122012 through rural / semi-urban through rural / semi-urban branches of CBs & RRBs - remaining branches of CBs & RRBs - remaining households by households by 20152015

Semi-urban / rural branches of CBs / Semi-urban / rural branches of CBs / RRBs to cover RRBs to cover 250 new cultivator and 250 new cultivator and non-cultivator per branch per annumnon-cultivator per branch per annum

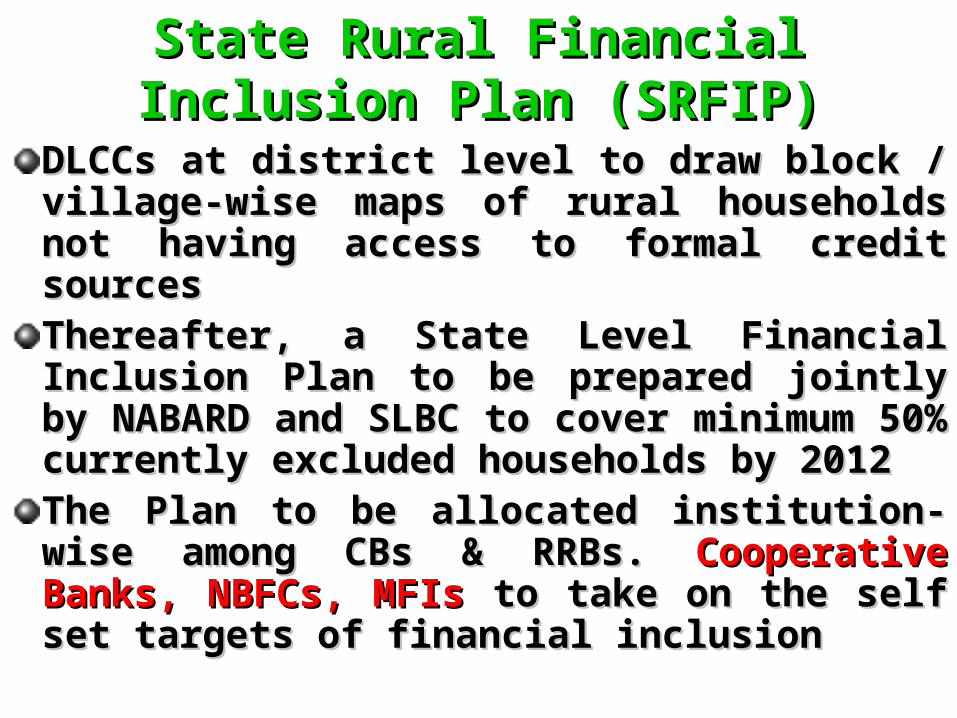

State Rural Financial State Rural Financial Inclusion Plan (SRFIP)Inclusion Plan (SRFIP)

DLCCs at district level to draw block / DLCCs at district level to draw block / village-wise maps of rural households not village-wise maps of rural households not having access to formal credit sourceshaving access to formal credit sourcesThereafter, a State Level Financial Inclusion Thereafter, a State Level Financial Inclusion Plan to be prepared jointly by NABARD and Plan to be prepared jointly by NABARD and SLBC to cover minimum 50% currently SLBC to cover minimum 50% currently excluded households by 2012excluded households by 2012The Plan to be allocated institution-wise The Plan to be allocated institution-wise among CBs & RRBs. among CBs & RRBs. Cooperative Banks, Cooperative Banks, NBFCs, MFIsNBFCs, MFIs to take on the self set targets to take on the self set targets of financial inclusionof financial inclusion

Financial Inclusion – how to go Financial Inclusion – how to go about itabout it

Traditional approachTraditional approach Improvement in existing system – Improvement in existing system –

reintroduce Service area approach to reintroduce Service area approach to bring in accountability bring in accountability

Extending network - using existing Extending network - using existing extension setups like Farmers’ clubs, extension setups like Farmers’ clubs, KVKs KVKs

Evolving new models of effective Evolving new models of effective outreach–Business Facilitators / outreach–Business Facilitators / Business CorrespondentsBusiness Correspondents

Financial Inclusion – how to Financial Inclusion – how to go about itgo about it

Traditional approachTraditional approach Community based approach like SHGs, Community based approach like SHGs,

JLGs Improving credit literacy through JLGs Improving credit literacy through camps camps

Introduce “Only Field Work Days Introduce “Only Field Work Days (OFDs) in rural/semi urban branches(OFDs) in rural/semi urban branches

Target approach as per NRFIP Target approach as per NRFIP

Financial Inclusion – how to Financial Inclusion – how to go about itgo about it

New approachNew approach Leveraging on technology based Leveraging on technology based

solutions solutions Public Private Partnership mode – Public Private Partnership mode –

take new players on board take new players on board

Efforts initiated for FI in RajasthanEfforts initiated for FI in Rajasthan

Adoption of Adoption of 6 pilot districts6 pilot districts for 100% for 100% financial inclusion financial inclusion

Implementation of Implementation of Bhamashah YojnaBhamashah Yojna by GORby GOR

SHG- Bank Linkage programmeSHG- Bank Linkage programme

Supported MFIs to help them reach Supported MFIs to help them reach out to poor out to poor

Mobile phone based banking Mobile phone based banking

Financial Inclusion – Efforts of NABARDFinancial Inclusion – Efforts of NABARD Two funds namely Two funds namely Financial Inclusion Financial Inclusion & Promotion Fund (FIF& Promotion Fund (FIF) and ) and Financial Financial Inclusion Technology Fund (FITF)Inclusion Technology Fund (FITF), each , each having initial corpus of having initial corpus of Rs. 500 croreRs. 500 crore have have been constituted by the GOI and placed been constituted by the GOI and placed with NABARDwith NABARD Each fund is to be equally contributed Each fund is to be equally contributed by GOI, RBI and NABARD with annual by GOI, RBI and NABARD with annual accretionsaccretions Eligible organisations to avail the funds Eligible organisations to avail the funds for greater financial inclusionfor greater financial inclusion

Financial Inclusion Fund (FIF) Financial Inclusion Fund (FIF)

Eligible Purposes :Eligible Purposes : Funding support for Funding support for capacity building capacity building inputs to BCs / BFsinputs to BCs / BFs Providing promotional support to Providing promotional support to institutions such as Resource Centres, institutions such as Resource Centres, Farmers Service Centres, RUDSETIsFarmers Service Centres, RUDSETIs to to enable them to provide improved technical enable them to provide improved technical and financial services (including and financial services (including counseling)counseling)

Financial Inclusion Promotion Financial Inclusion Promotion Technology Fund (FITF)Technology Fund (FITF)

Encouraging user friendly Encouraging user friendly technology solutionstechnology solutions

Providing financial support to technological Providing financial support to technological solutions aimed at providing affordable financial solutions aimed at providing affordable financial services to the disadvantaged sections of the services to the disadvantaged sections of the societysociety

Creating a common technology infrastructure Creating a common technology infrastructure with comprehensive credit informationwith comprehensive credit information

Funding support to technologies facilitating the Funding support to technologies facilitating the documentation for processing of loansdocumentation for processing of loans

Providing viability gap / pilot project funding for Providing viability gap / pilot project funding for unproven but potential technological interventionsunproven but potential technological interventions

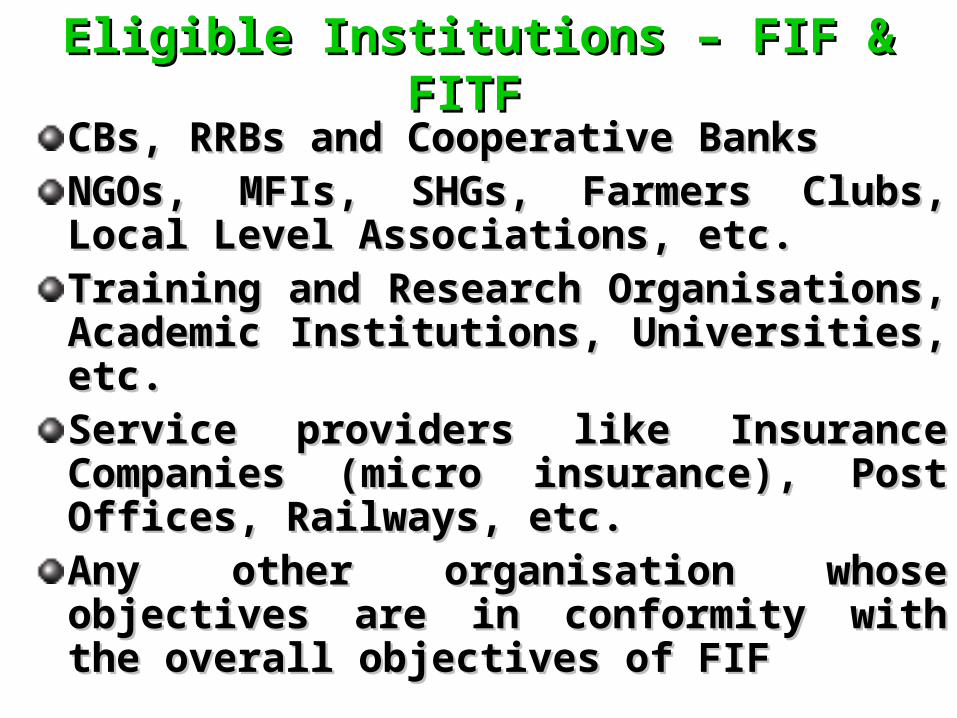

Eligible Institutions – FIF & FITF Eligible Institutions – FIF & FITF

CBs, RRBs and Cooperative BanksCBs, RRBs and Cooperative BanksNGOs, MFIs, SHGs, Farmers Clubs, Local NGOs, MFIs, SHGs, Farmers Clubs, Local Level Associations, etc.Level Associations, etc.Training and Research Organisations, Training and Research Organisations, Academic Institutions, Universities, etc.Academic Institutions, Universities, etc.Service providers like Insurance Service providers like Insurance Companies (micro insurance), Post Companies (micro insurance), Post Offices, Railways, etc.Offices, Railways, etc.Any other organisation whose objectives Any other organisation whose objectives are in conformity with the overall are in conformity with the overall objectives of FIFobjectives of FIF

Financial Inclusion Initiatives by BanksFinancial Inclusion Initiatives by Banks Set up 100 centres in agri-lending branches for Set up 100 centres in agri-lending branches for agriculture counseling – SBIagriculture counseling – SBI Use of handheld devices and bio-metric cards in Use of handheld devices and bio-metric cards in a village of Tamilnadu – IOB, UBI a village of Tamilnadu – IOB, UBI Introduce 198 Village Knowledge Centre for Introduce 198 Village Knowledge Centre for imparting knowledge to the farmers – UBI, Dena imparting knowledge to the farmers – UBI, Dena Bank Bank Introduced “Union Mitr” Scheme” (90) for Introduced “Union Mitr” Scheme” (90) for providing financial education and debt counseling providing financial education and debt counseling services to rural population, free of cost – UBIservices to rural population, free of cost – UBI Introduced Dena Bhoomiheen Kisan Credit Card Introduced Dena Bhoomiheen Kisan Credit Card Scheme(Rs.25,000) for Tenant farmers, oral lessees, Scheme(Rs.25,000) for Tenant farmers, oral lessees, share croppers and landless labourers – Dena Bankshare croppers and landless labourers – Dena Bank

FINANCIAL FINANCIAL INCLUSIONINCLUSION

TOGETHER WE CAN TOGETHER WE CAN

ANDAND

WE WILL - - -! WE WILL - - -!

![NABARD [Volume 10]](https://static.fdocuments.in/doc/165x107/543912e6afaf9fbe2e8b4c91/nabard-volume-10.jpg)