WEEKLY SHIPPING MARKET REPORT -...

18

WEEKLY SHIPPING MARKET REPORT WEEK 26 - 25 TH June – to 2 nd July 2012 - Legal Disclamer The information contained herein has been obtained by various sources. Although every effort has been made to ensure that this information is accurate, complete and up to date, Shiptrade Services S.A. does not accept any responsibility whatsoever for any loss or damage occasioned or claimed, upon reliance on the information, opinions and analysis contained in this report. Researched and compiled by: Shiptrade Services SA, Market Research on behalf of the Sale & Purchase, Dry Cargo Chartering and Tanker Chartering Departments. For any questions please contact: [email protected] Shiptrade Services SA Tel +30 210 4181814 [email protected] 1st Floor, 110/112 Notara Street Fax +30 210 4181142 [email protected] 185 35 Piraeus, Greece www.shiptrade.gr [email protected]

Transcript of WEEKLY SHIPPING MARKET REPORT -...

WEEKLY SHIPPING

MARKET REPORT WEEK 26

- 25TH June – to 2nd July 2012 -

Legal Disclamer

The information contained herein has been obtained by various sources. Although every effort has been made to ensure that this information is accurate, complete and up to date, Shiptrade Services S.A. does not accept any responsibility whatsoever for any loss or damage occasioned or claimed, upon reliance on the information, opinions and analysis contained in this report.

Researched and compiled by: Shiptrade Services SA, Market Research on behalf of the Sale & Purchase, Dry Cargo Chartering and Tanker Chartering Departments. For any questions please contact: [email protected]

Shiptrade Services SA Tel +30 210 4181814 [email protected] 1st Floor, 110/112 Notara Street Fax +30 210 4181142 [email protected] 185 35 Piraeus, Greece www.shiptrade.gr [email protected]

1

Brazilian steel industry experiencing a paradigm shift - Usiminas

BNamericas quoted Mr Julian Eguren CEO of Usiminas as saying that the Brazilian steel industry is experiencing a paradigm shift. He added that "Currently, a steel company should have its own iron ore production as a precondition for competitiveness." According to the executive, the steel industry is still adapting to changes in the iron ore pricing system, which in 2010 moved from the annual benchmark pricing to a quarterly system and subsequently to a spot market. He said that "It's been hard to predict market behavior." Usiminas finance VP Mr Ronald Seckelmann said the steelmaker has resources to finance its mining projects and is not working to increase capital in 2012, although the cash flow environment has been under pressure in recent quarters. He added that "Usiminas' mining projects already have enough resources." Mr Seckelmann's comments come in response to reports saying that Usiminas is preparing an operation of at least BRL 1.5 billion to increase its capital and may also sell assets to leverage investments due to the company's weak operating cash flow. (Business News Americas)

Australia commodity index down 0.7 pct in June-RBA

The Reserve Bank of Australia's (RBA) index of commodity prices fell 0.7 percent in June, from May, due mainly to falls in oil and thermal coal. In May, the index declined by a revised 1.3 percent in special drawing rights (SDR) terms. The index reading of 132.6 in June was 10.5 percent lower than the same month last year. Much of that decline was due to lower prices for iron ore and coking coal. In Australian dollar terms, the index slipped 1.7 percent in June, leaving it down 9.9 percent for the year. (Reuters)

Iran, Iraq and Venezuela form alliance within OPEC to stabilize

petroleum prices

Iran, Venezuela and Iraq have formed an alliance within OPEC to stabilize oil prices in the light of Saudi Arabia’s efforts. UAE and Libya increased oil production to compensate the ban on imports of petroleum from Iran. Saudi Arabia reached an extraction rate of 10 billion barrels daily trying to reduce oil prices to $60. Iranian Petroleum Minister Rostem Qasemi requested Iraqi Petroleum Minister Qerim Al-Ayibi to hold an emergency meeting of OPEC to discuss reduction of quotas for oil extraction. Venezuelan Petroleum Minister Rafael Ramirez is discussing the problem with Ecuador and Algeria. (Tehran Times)

Nickel price decreases push stainless steel values lower

Stainless steel transaction prices are heavily influenced by raw material values. Producers in the Far East amend effective prices to reflect input costs, while mills in Europe and North America issue monthly alloy surcharges, which are based on published prices for the main ingredients of the product. The effect of these surcharges is substantial. For example, while the basis price for type 304 cold rolled coil in Germany has moved within a band of only €50 per tonne, between January and June this year, the difference between the high and low applicable surcharges for that grade, during the same period, is €223 per tonne. Furthermore, the June alloy extra, at €1418 per tonne, is 59 percent of the transaction value. By far the biggest contributor to these input costs is nickel. Even at the current LME figure, less than US$17,000 per tonne, which is very low in terms of recent history, the value of nickel units in grade 304 stainless steel represents over 50 percent of the transaction price of the product. Consequently, participants in the stainless steel market should take notice of factors likely to affect the price of nickel in the short-to-medium term. A surplus in the supply-demand balance is forecast for 2012 and 2013. Growth in consumption by stainless steel makers will be restrained by moderate demand, while industry consolidation, such as the proposed merger between Outokumpu and Inoxum, will lead to the closure of some production facilities. Furthermore, as a traded commodity, nickel prices are affected by the actions of traders and investors who are not connected to any physical operations related to the production or consumption of the metal. While commodities are generally considered a safe long-term bet, many traders earn their living by reacting to short-term fluctuations in the markets. Commodity prices tend to react negatively to periods of intense market stress, such as the present eurozone crisis. Moreover, some observers believe the so-called "commodities supercycle" could be approaching its end, as there are signs of slowing demand growth from China. However, the nickel miners will attempt to redress the balance by delaying or reducing the scale of new projects, or even cutting existing operations. Meanwhile, measures by China, the world's largest nickel producer, to comply with environmental guidelines, could lead to reduced output there. Assuming global economies recover sufficiently to allow a resumption of industrial growth, longer term nickel values would then take on a brighter outlook. (MEPS)

Shipping , Commodities & Financial News

2

In Brief: Stability with Panamaxes falling Capes: steady rates at the bottom Stability at low levels for another week for Capes. BCI saw an increase of 35 points closing at 1190 whereas the average of the 4 TC routes ended up at USD 3,988. In the Atlantic basin, some fresh cargoes lead the fronthaul rates to a modest improve of USD 750 closing at USD 19,500 with the large volume of tonnage at the area to prevent any significant increase. The same sentiment at Transatlantic round which remained stable at low levels closing at USD 4,500. Pacific trade followed similar pattern with the Far East round trips fixed at USD 4,750 reporting an unnoticeable increase of USD 500 mainly due to the oversupply of tonnage competing to cover the Australia iron ore trade which plays a determinant role at the market. Period activity remained stable with an upward trend fixing at USD 9,750 levels for one year. Panamax: The soft movement continues. Although we faced some fresh cargo requirements in the Atlantic at the beginning of the week, the rates did not move upwards because of the too many spot existing positions. In the Med-Black Sea region the final effect as far as rates are concerned was almost the same due to the fact that most of cargoes availability is set on end July – beginning August dates with much spot/prompt tonnage in the area. Thus, Transantlantic rounds closed at USD 8,000 levels, down by over USD 1,000 than last week. Fronthaul trips were mainly fixed at the region of USD 15,000-16,000 plus USD 475k BB basis delivery APS. In the Pacific Basin, the scene was also quite with Australian and Indonesian rounds remaining the main trade options, closing at USD 6,000-7,000 whilst NOPAC was extremely slow. Short period market seems additionally slow this week with quit a few fixtures of 4/6 months at USD 9,000 levels, mostly basis delivery FEAST.

Supramax: The positive sentiment remains in both basins

The Atlantic market saw depth in cargoes with the fronthaul rates fixed at USD 24,000 as well as the trips from USG to Continent closed at mid USD 20’s. The Transantlantic round voyage remained steady with upward trend ended up at USD 16,500. This week would be described stable in an increasing manner for the Pacific basin. For Nopac rounds basis delivery Japan fixtures have been reported at around USD 10,000 whereas trips from Indonesia with coal to EC India fixed at the range of USD 8,000- USD 9,000 basis delivery South China and at low-mid teens basis delivery dop. Period activity increased by USD 500 fixed at USD 10,500 levels for one year.

Handysize: Index/market at almost the same levels as last week Stability was apparent in both basins with the index increasing 14 points. Atlantic kept on absorbing vessels and the transatlantic round was done at around USD 11,750 levels, slightly higher than the previous week. Intra Black Sea/ East Med orders were covered fix at USD 8/8,500 while trips to USG were paying USD 6/6.500 basis aps Canakkale. Owners opening at West and South Africa had some more options, except from ballasting to ECSA, with some orders to Far East and Med. In the Pacific the round trip remained at USD 7,250 levels as no positive sentiment appeared in the market. Even the backhauls with bagged rice to West Africa did not produce much firm orders thus owners had to fix some short intra Far East trips to cover their vessels up. Owners opening at ECI/WCI suffered from poor rates while even PG was pretty soft. Periods were difficult to be fixed with such low rates offered from charterers as the average of USD 7,500 is not appealing to any owner.

Dry Bulk - Chartering

3

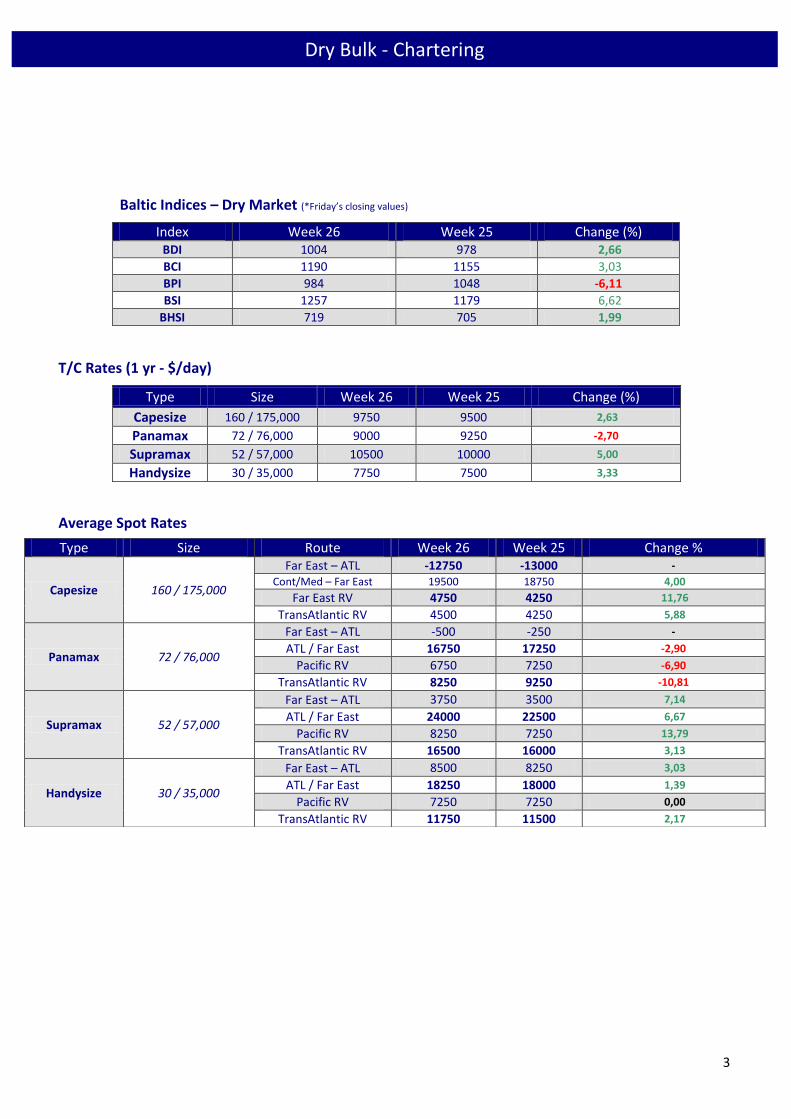

Baltic Indices – Dry Market (*Friday’s closing values)

Index Week 26 Week 25 Change (%) BDI 1004 978 2,66

BCI 1190 1155 3,03

BPI 984 1048 -6,11

BSI 1257 1179 6,62

BHSI 719 705 1,99

T/C Rates (1 yr - $/day)

Type Size Week 26 Week 25 Change (%)

Capesize 160 / 175,000 9750 9500 2,63

Panamax 72 / 76,000 9000 9250 -2,70

Supramax 52 / 57,000 10500 10000 5,00

Handysize 30 / 35,000 7750 7500 3,33

Average Spot Rates

Type Size Route Week 26 Week 25 Change %

Capesize 160 / 175,000

Far East – ATL -12750 -13000 -

Cont/Med – Far East 19500 18750 4,00

Far East RV 4750 4250 11,76

TransAtlantic RV 4500 4250 5,88

Panamax 72 / 76,000

Far East – ATL -500 -250 -

ATL / Far East 16750 17250 -2,90

Pacific RV 6750 7250 -6,90

TransAtlantic RV 8250 9250 -10,81

Supramax 52 / 57,000

Far East – ATL 3750 3500 7,14

ATL / Far East 24000 22500 6,67

Pacific RV 8250 7250 13,79

TransAtlantic RV 16500 16000 3,13

Handysize 30 / 35,000

Far East – ATL 8500 8250 3,03

ATL / Far East 18250 18000 1,39

Pacific RV 7250 7250 0,00

TransAtlantic RV 11750 11500 2,17

Dry Bulk - Chartering

4

ANNUAL

APRIL 2012 – JUNE 2012

Dry Bulk - Chartering

5

Dry Bulk - Chartering

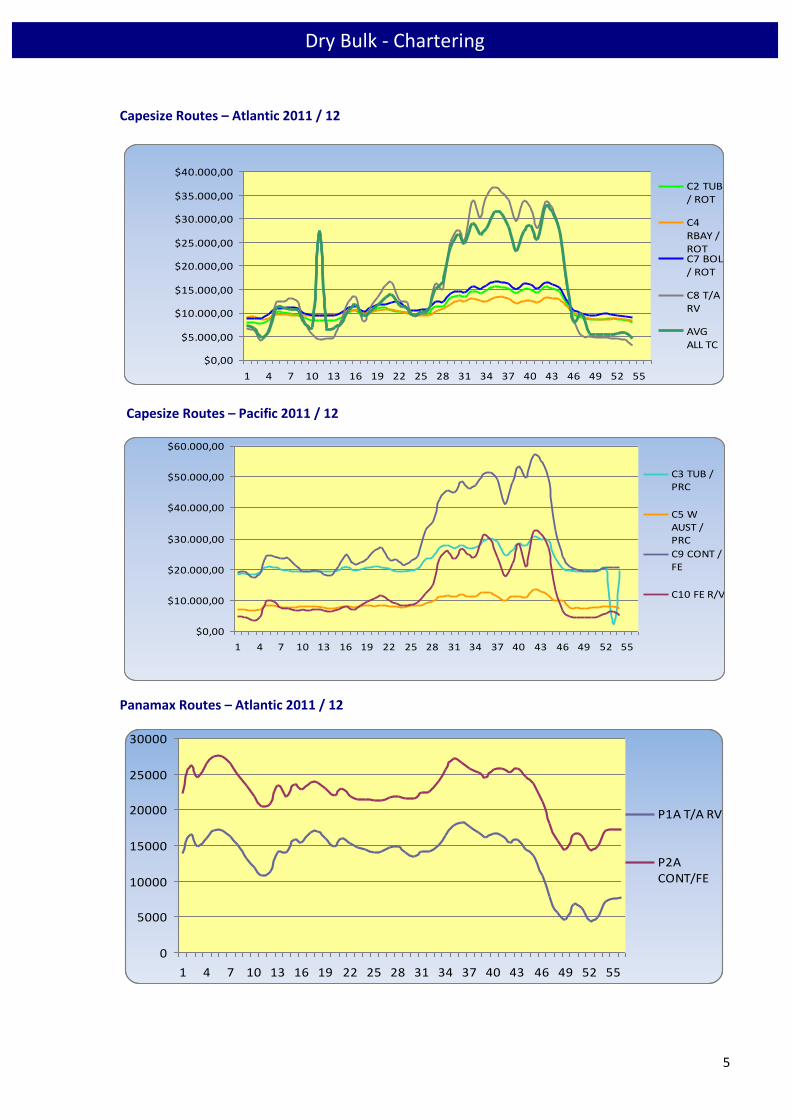

Capesize Routes – Atlantic 2011 / 12

$0,00

$5.000,00

$10.000,00

$15.000,00

$20.000,00

$25.000,00

$30.000,00

$35.000,00

$40.000,00

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55

C2 TUB/ ROT

C4RBAY /ROTC7 BOL/ ROT

C8 T/ARV

AVGALL TC

Capesize Routes – Pacific 2011 / 12

$0,00

$10.000,00

$20.000,00

$30.000,00

$40.000,00

$50.000,00

$60.000,00

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55

C3 TUB /PRC

C5 WAUST /PRC

C9 CONT /FE

C10 FE R/V

Panamax Routes – Atlantic 2011 / 12

0

5000

10000

15000

20000

25000

30000

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55

P1A T/A RV

P2ACONT/FE

6

Dry Bulk - Chartering

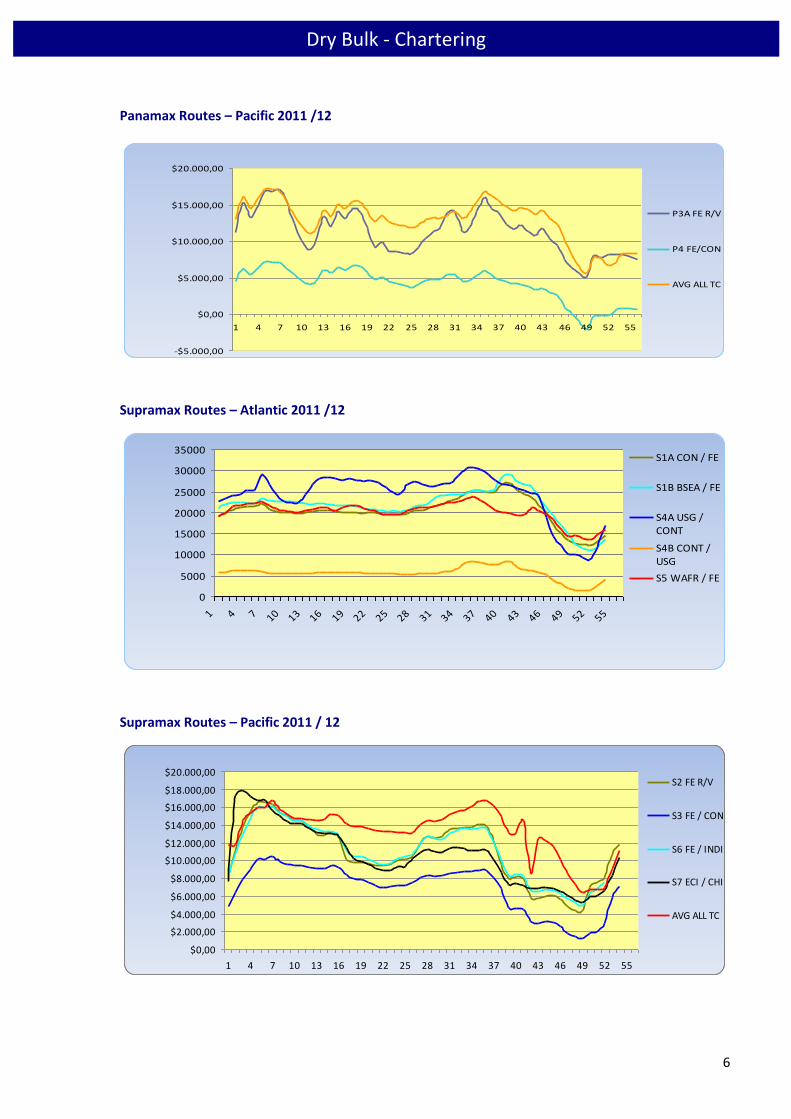

Panamax Routes – Pacific 2011 /12

-$5.000,00

$0,00

$5.000,00

$10.000,00

$15.000,00

$20.000,00

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55

P3A FE R/V

P4 FE/CON

AVG ALL TC

Supramax Routes – Atlantic 2011 /12

0

5000

10000

15000

20000

25000

30000

35000

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55

S1A CON / FE

S1B BSEA / FE

S4A USG /CONT

S4B CONT /USG

S5 WAFR / FE

Supramax Routes – Pacific 2011 / 12

$0,00

$2.000,00

$4.000,00

$6.000,00

$8.000,00

$10.000,00

$12.000,00

$14.000,00

$16.000,00

$18.000,00

$20.000,00

1 4 7 10 13 16 19 22 25 28 31 34 37 40 43 46 49 52 55

S2 FE R/V

S3 FE / CON

S6 FE / INDI

S7 ECI / CHI

AVG ALL TC

7

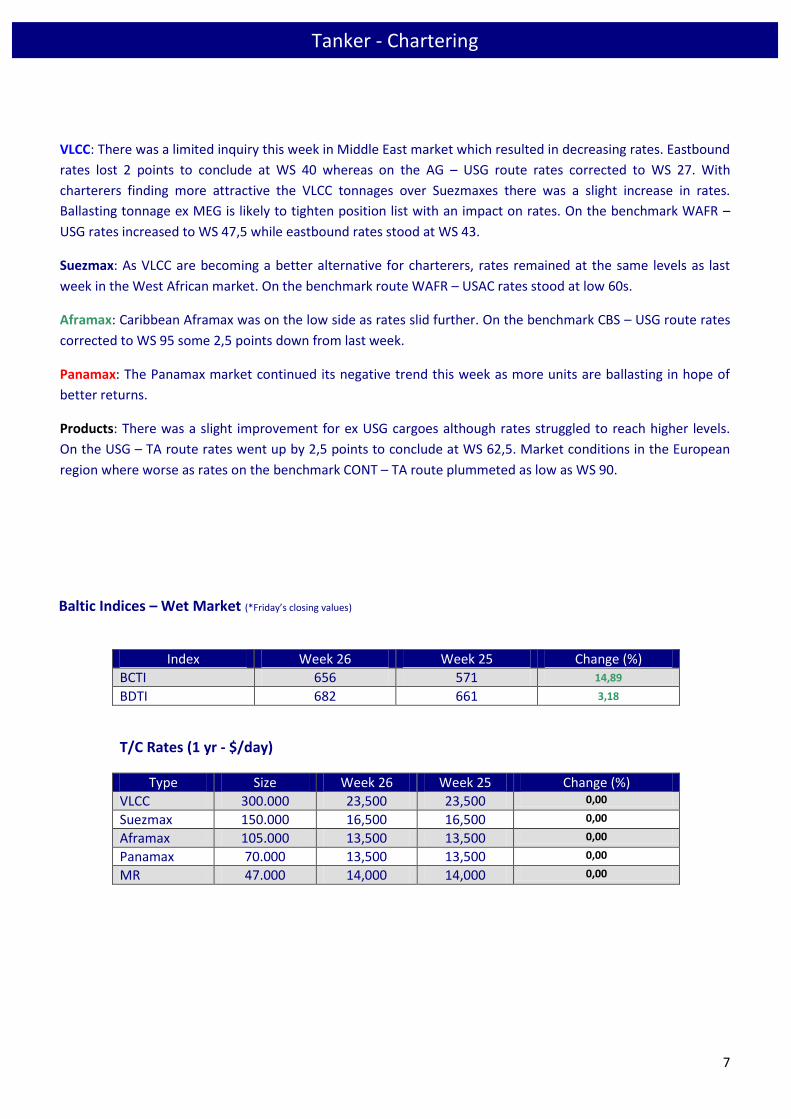

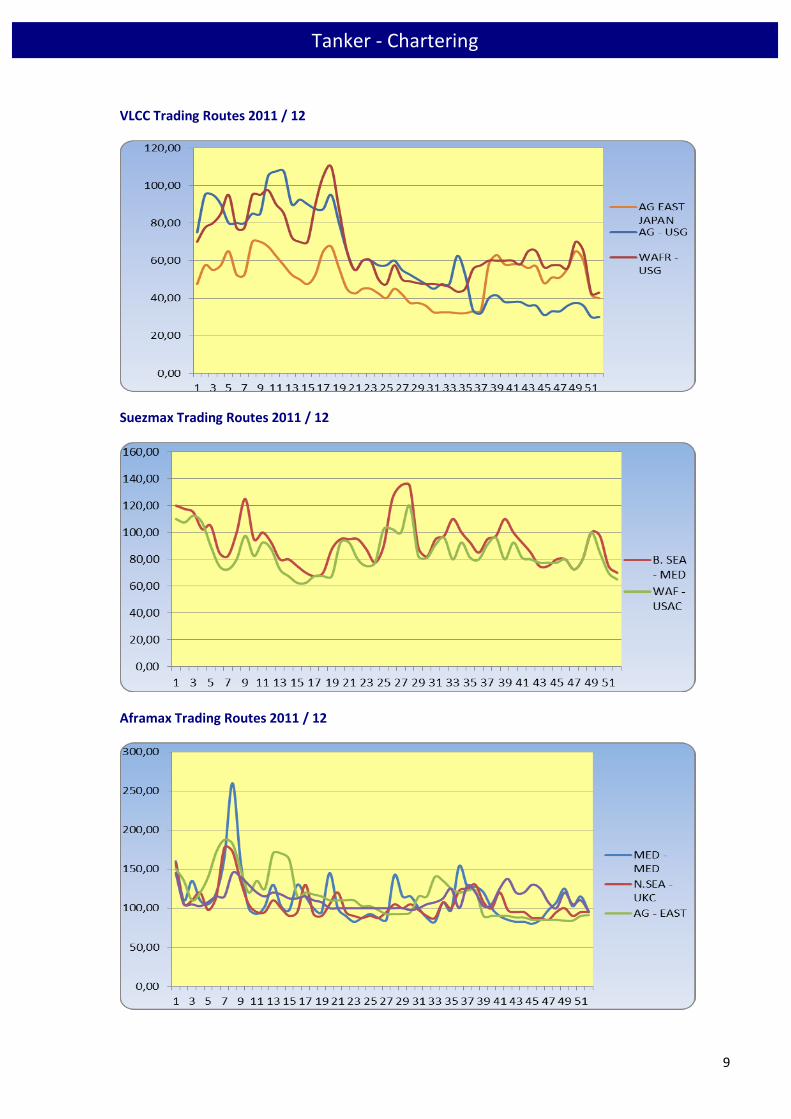

VLCC: There was a limited inquiry this week in Middle East market which resulted in decreasing rates. Eastbound

rates lost 2 points to conclude at WS 40 whereas on the AG – USG route rates corrected to WS 27. With

charterers finding more attractive the VLCC tonnages over Suezmaxes there was a slight increase in rates.

Ballasting tonnage ex MEG is likely to tighten position list with an impact on rates. On the benchmark WAFR –

USG rates increased to WS 47,5 while eastbound rates stood at WS 43.

Suezmax: As VLCC are becoming a better alternative for charterers, rates remained at the same levels as last

week in the West African market. On the benchmark route WAFR – USAC rates stood at low 60s.

Aframax: Caribbean Aframax was on the low side as rates slid further. On the benchmark CBS – USG route rates

corrected to WS 95 some 2,5 points down from last week.

Panamax: The Panamax market continued its negative trend this week as more units are ballasting in hope of

better returns.

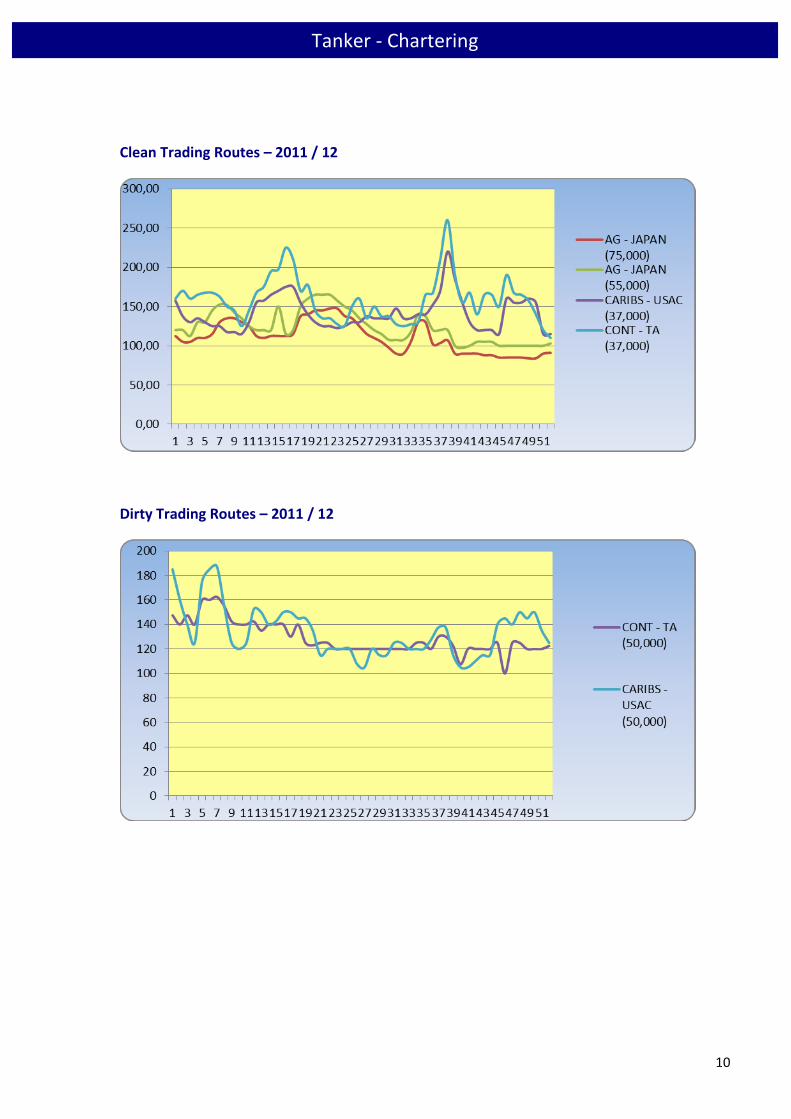

Products: There was a slight improvement for ex USG cargoes although rates struggled to reach higher levels.

On the USG – TA route rates went up by 2,5 points to conclude at WS 62,5. Market conditions in the European

region where worse as rates on the benchmark CONT – TA route plummeted as low as WS 90.

Baltic Indices – Wet Market (*Friday’s closing values)

Index Week 26 Week 25 Change (%)

BCTI 656 571 14,89

BDTI 682 661 3,18

T/C Rates (1 yr - $/day)

Type Size Week 26 Week 25 Change (%)

VLCC 300.000 23,500 23,500 0,00

Suezmax 150.000 16,500 16,500 0,00

Aframax 105.000 13,500 13,500 0,00

Panamax 70.000 13,500 13,500 0,00

MR 47.000 14,000 14,000 0,00

Tanker - Chartering

8

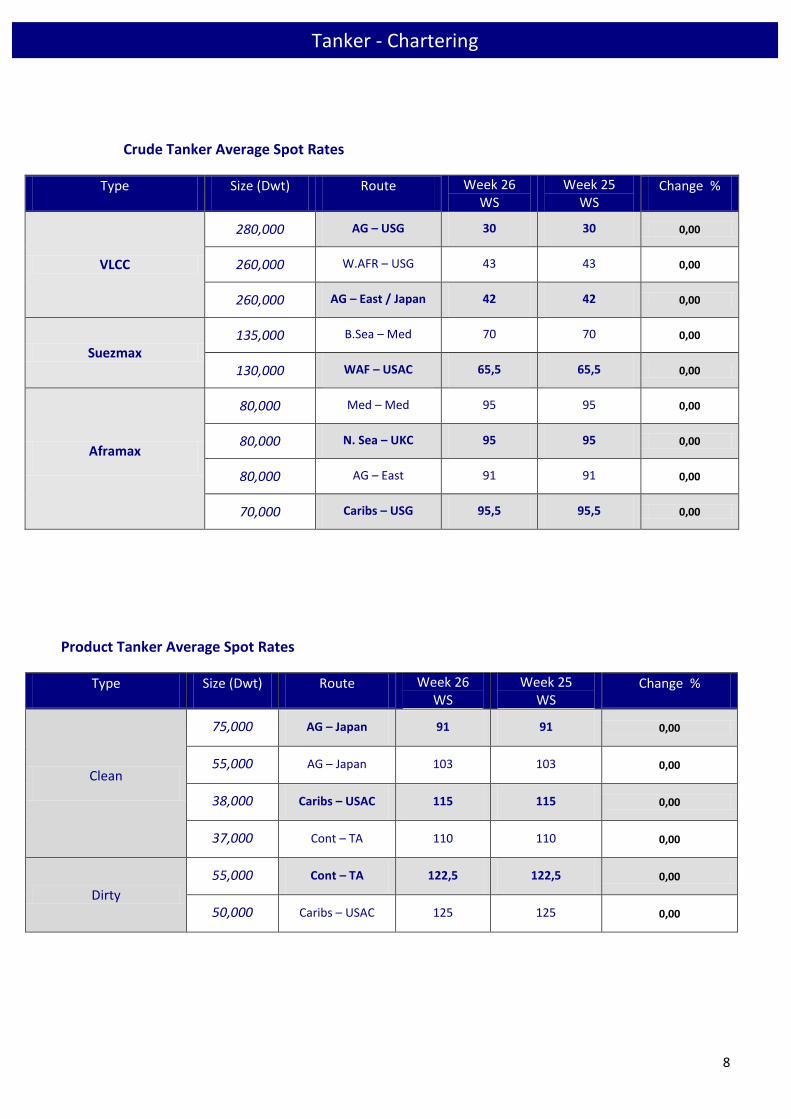

Crude Tanker Average Spot Rates

Type Size (Dwt) Route Week 26 WS

Week 25 WS

Change %

VLCC

280,000 AG – USG 30 30 0,00

260,000 W.AFR – USG 43 43 0,00

260,000 AG – East / Japan 42 42 0,00

Suezmax 135,000 B.Sea – Med 70 70 0,00

130,000 WAF – USAC 65,5 65,5 0,00

Aframax

80,000 Med – Med 95 95 0,00

80,000 N. Sea – UKC 95 95 0,00

80,000 AG – East 91 91 0,00

70,000 Caribs – USG 95,5 95,5 0,00

Product Tanker Average Spot Rates

Type Size (Dwt) Route Week 26 WS

Week 25 WS

Change %

Clean

75,000 AG – Japan 91 91 0,00

55,000 AG – Japan 103 103 0,00

38,000 Caribs – USAC 115 115 0,00

37,000 Cont – TA 110 110 0,00

Dirty

55,000 Cont – TA 122,5 122,5 0,00

50,000 Caribs – USAC 125 125 0,00

Tanker - Chartering

9

VLCC Trading Routes 2011 / 12

Suezmax Trading Routes 2011 / 12

Aframax Trading Routes 2011 / 12

Tanker - Chartering

10

Clean Trading Routes – 2011 / 12

Dirty Trading Routes – 2011 / 12

Tanker - Chartering

11

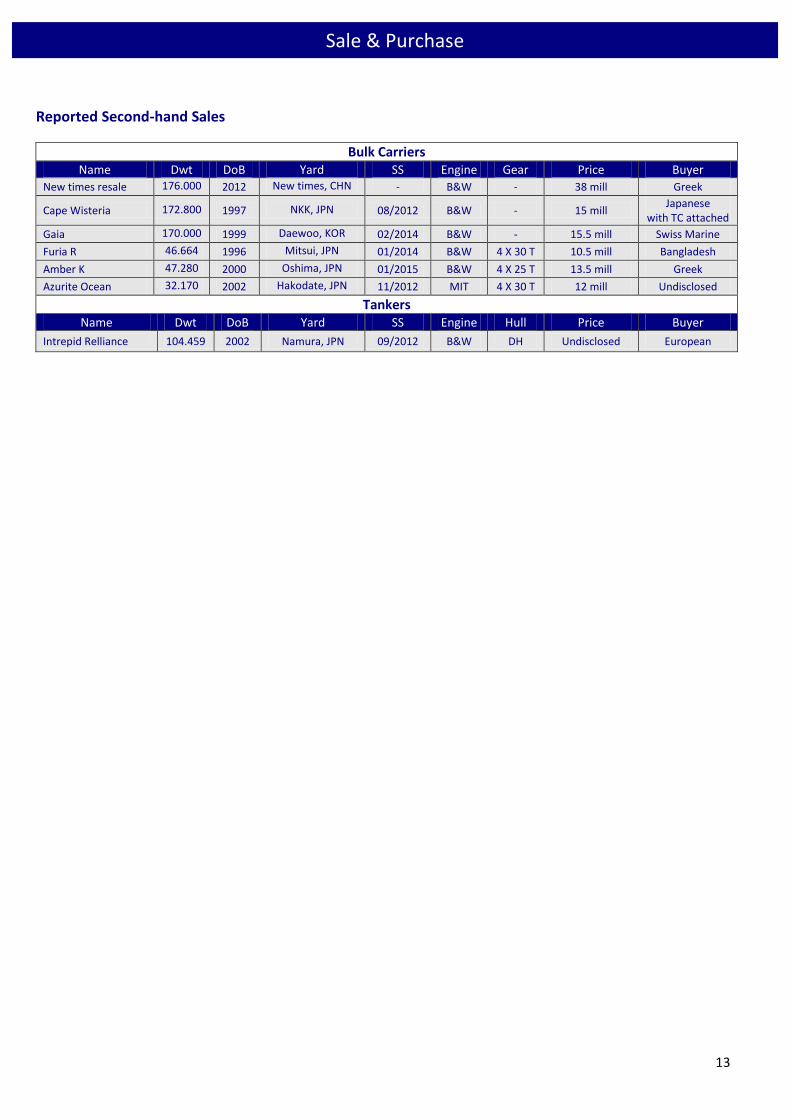

Buyers chasing Large bulkers

Numerous sales have been reported last week in the dry sector where buyers show willingness to seize current price levels.

Focus has been on vessels built in the nineties as well as modern tonnages. In the tanker sector, activity was significantly

lower with few reported transactions.

Capesize M/V “Gaia” (169,963 DWT built in 1999 in Daewoo, KRS) is reported sold for USD 15,5 Mill to Greek buyers.

Modern Panamax M/V “Oceanic Breeze” (77,075 DWT built in 2005 in Namura, JPN) is reported sold to Greek buyers as

well for USD 21,3 Mill.

The most notable tanker sale this week has been of Aframax M/T “Intrepid Reliance” (104,403 DWT built in 2002 in Namura,

JPN). The vessel was reported sold to European buyers to an undisclosed sum.

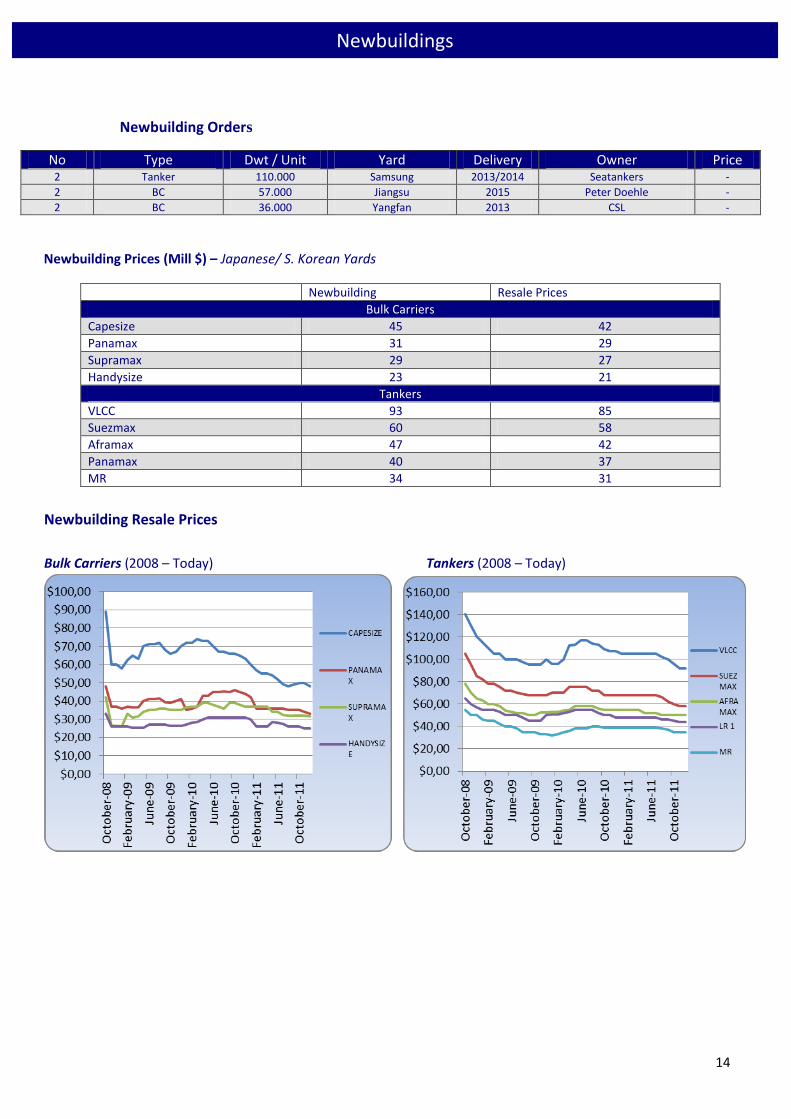

NEWBUILDINGS

In the newbuilding market, we have seen 6 vessels reported to have been contracted.

2 Tankers (Aframax)

4 Bulk carriers (Handysize, Supramax)

DEMOLITION

In Bangladesh end buyers have started to offer for various vessels in view of steel plate prices providing them with some

confidence. The Indian market has started seeing some signs of confidence after many weeks of depressed business.

Pakistan is showing its preference for tankers with buyers still there to acquire tonnages. Chinese market has slowed down

it activity with buyers simply being patient.

Sale & Purchase

12

Indicative Market Values – ( 5 yrs old / Mill $ )

Bulk Carriers

Week 26 Week 25 Change %

Capesize 34 34 0.00

Panamax 22 22 0.00

Supramax 19 19 0.00

Handysize 17 17 0.00

Tankers

VLCC 58 58 0.00

Suezmax 44 44 0.00

Aframax 27 27 0.00

Panamax 27 27 0.00

MR 23 23 0.00

Weekly Purchase Enquiries

SHIPTRADE P/E WEEKLY INDEX

0

50

100

150

200

250

300

350

01-07/3/201

1

08-14/3/201

1

15-21/03/20

11

22-28/03/20

11

29/03

-4/4/201

1

5/4/-11/4/20

11

12-18/4/201

1

19-25/4/201

1

26/4-2/5/2011

3-9/5/2011

10-16/5/201

1

17-23/5/201

1

24-30/5/201

1

31/5-6/6/2011

7-13/6/2011

14-20/6/201

1

21-27/6/201

1

28/6-4/7/2011

5-11/7/2011

12-18/7/201

1

19-25/7/201

1

26/7-1/8/2011

2-8/8/2011

9-15/8/2011

16-21/8/201

1

22-29/8/201

1

30/8-05/9/201

1

06-12/9/201

1

13-19/9/201

1

20-26/9/201

1

27/9-3/10/201

1

4-10/10/201

1

11-17/10/20

11

18-24/10/20

11

25-31/10/20

11

1-7/11/2011

8-14/11/201

1

15-21/11/20

11

22-28/11/20

11

29/11

-5/12/20

11

6-12/12/201

1

13-19/12/20

11

20-26/12/20

11

27/12

/2011

-9/1/2012

10-16/1/201

2

17-23/1/201

2

24-30/1/201

2

31/1-6/2/2012

7-13/2/2012

14-20/02/20

12

21-27/02/20

12

28/2-5/03/201

2

6-12/03/201

2

13-19/03/20

12

20-26/03/20

12

27/3-2/4/2012

3-9/4/2012

10-16/4/201

2

17-23/4/201

2

24/4-1/5/2012

2-8/5/2012

9-15/5/2012

16-22/5/201

2

23-29/5/201

2

30/5-5/6/2012

6-12/6/2012

13-19/6/201

2

20-26/6/201

2

27/6-3/7/2012

KOREA CHINA SPORE

KCS GREECE OTHER

SUM Series8 Series9

Series10 Series11 Series12

Series13 Series14

Sale & Purchase

13

Reported Second-hand Sales

Bulk Carriers Name Dwt DoB Yard SS Engine Gear Price Buyer

New times resale 176.000 2012 New times, CHN - B&W - 38 mill Greek

Cape Wisteria 172.800 1997 NKK, JPN 08/2012 B&W - 15 mill Japanese

with TC attached

Gaia 170.000 1999 Daewoo, KOR 02/2014 B&W - 15.5 mill Swiss Marine

Furia R 46.664 1996 Mitsui, JPN 01/2014 B&W 4 X 30 T 10.5 mill Bangladesh

Amber K 47.280 2000 Oshima, JPN 01/2015 B&W 4 X 25 T 13.5 mill Greek

Azurite Ocean 32.170 2002 Hakodate, JPN 11/2012 MIT 4 X 30 T 12 mill Undisclosed

Tankers Name Dwt DoB Yard SS Engine Hull Price Buyer

Intrepid Relliance 104.459 2002 Namura, JPN 09/2012 B&W DH Undisclosed European

Sale & Purchase

14

Newbuilding Orders

No Type Dwt / Unit Yard Delivery Owner Price 2 Tanker 110.000 Samsung 2013/2014 Seatankers -

2 BC 57.000 Jiangsu 2015 Peter Doehle -

2 BC 36.000 Yangfan 2013 CSL -

Newbuilding Prices (Mill $) – Japanese/ S. Korean Yards

Newbuilding Resale Prices

Bulk Carriers

Capesize 45 42

Panamax 31 29

Supramax 29 27

Handysize 23 21

Tankers

VLCC 93 85

Suezmax 60 58

Aframax 47 42

Panamax 40 37

MR 34 31

Newbuilding Resale Prices

Bulk Carriers (2008 – Today) Tankers (2008 – Today)

Newbuildings

15

Demolition Sales

Vessel Type Built Dwt Ldt Buyer Country Price Antarctic Star Reefer 1983 8.298 3.802 Bangladesh 330

Frio Hamburg Reefer 1988 6.538 3.230 Bangladesh 330

Cougar Tanker 1989 46.538 9.550 Pakistan Undisclosed

With 280 T bunkers ROB upon Delivery

Demolition Prices ($ / Ldt)

Bangladesh China India Pakistan

Dry 370 340 350 350

Wet 390 360 380 380

Demolition Prices

Bulk Carriers (2008 – Today) Tankers (2008 – Today)

Demolitions

16

Shipping Stocks

Commodities

Commodity Week 26 Week 25 Change (%) Brent Crude (BZ) 100,65 92,10 9,28

Natural Gas (NG) 2,85 2,68 6,34

Gold (GC) 1619 1575 2,79

Copper (LME) 4,08 3,33 22,52

Wheat (W) 306,44 296,88 3,22

Dry Bulk

Company Stock Exchange Week 26 Week 25 Change % Baltic Trading Ltd (BALT) NYSE 3,44 3,63 -5,23

Diana Shipping Inc (DSX) NASDAQ 7,78 7,28 6,87

Dryships Inc (DRYS) NASDAQ 2,19 2,13 2,82

Euroseas Ltd (ESEA) NASDAQ 1,18 1,10 7,27

Excel Maritime Carriers (EXM) NYSE 0,56 0,57 -1,75

Eagle Bulk Shipping Inc (EGLE) NASDAQ 3,16 3,61 -12,47

Freeseas Inc (FREESE) NASDAQ 0,73 0,67 8,96

Genco Shipping (GNK) NYSE 3,05 2,93 4,10

Navios Maritime (NM) NYSE 3,32 3,24 2,47

Navios Maritime PTN (NMM) NYSE 13,59 13,49 0,74

Paragon Shipping Inc (PRGN) NASDAQ 0,54 0,59 -8,47

Star Bulk Carriers Corp (SBLK) NASDAQ 0,72 0,73 -1,37

Seanergy Maritime Holdings Corp (SHIP) NASDAQ 2,07 2,49 -16,87

Safe Bulkers Inc (SB) NYSE 6,17 6,09 1,31

Golden Ocean (GOGL) Oslo Bors (NOK) 3,87 4,02 -3,73

Tankers Capital Product Partners LP (CPLP) NASDAQ 7,56 7,38 2,44

TOP Ships Inc (TOPS) NASDAQ 1,68 1,71 -1,75

Tsakos Energy Navigation (TNP) NYSE 4,87 4,90 -0,61

Other

Aegean Maritime Petrol (ANW) NYSE 5,35 5,09 5,11

Danaos Corporation (DAC) NYSE 4,15 4,35 -4,60

StealthGas Inc (GASS) NASDAQ 5,81 5,90 -1,53

Rio Tinto (RIO) NYSE 47,81 46,53 2,75

Vale (VALE) NYSE 19,85 19,16 3,60

ADM Archer Daniels Midland (ADM) NYSE 29,52 29,28 0,82

BHP Billiton (BHP) NYSE 65,30 63,31 3,14

Financial Market Data

17

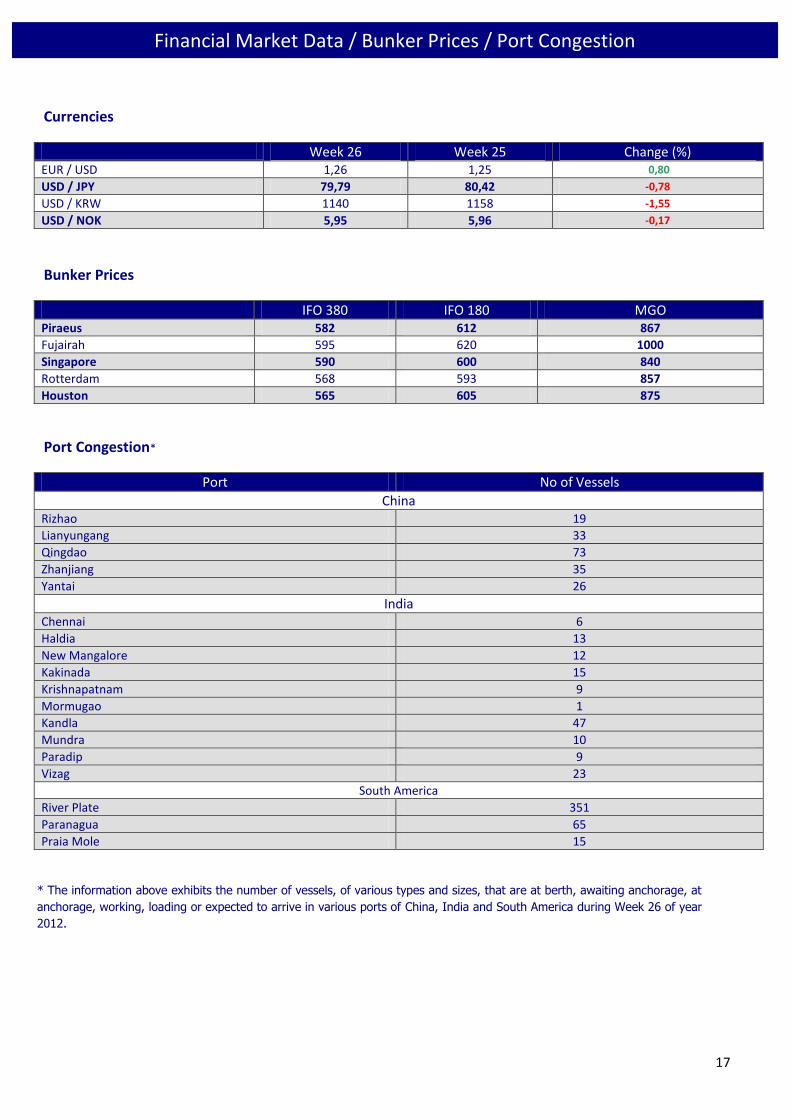

Currencies

Week 26 Week 25 Change (%) EUR / USD 1,26 1,25 0,80

USD / JPY 79,79 80,42 -0,78

USD / KRW 1140 1158 -1,55

USD / NOK 5,95 5,96 -0,17

Bunker Prices

IFO 380 IFO 180 MGO Piraeus 582 612 867

Fujairah 595 620 1000

Singapore 590 600 840

Rotterdam 568 593 857

Houston 565 605 875

Port Congestion*

Port No of Vessels

China Rizhao 19

Lianyungang 33

Qingdao 73

Zhanjiang 35

Yantai 26

India

Chennai 6

Haldia 13

New Mangalore 12

Kakinada 15

Krishnapatnam 9

Mormugao 1

Kandla 47

Mundra 10

Paradip 9

Vizag 23

South America

River Plate 351

Paranagua 65

Praia Mole 15

* The information above exhibits the number of vessels, of various types and sizes, that are at berth, awaiting anchorage, at

anchorage, working, loading or expected to arrive in various ports of China, India and South America during Week 26 of year

2012.

Financial Market Data / Bunker Prices / Port Congestion