Weekly Market Review - mashreqbank.com · Aabar Investments acquired 707,004,044 shares @AED5 per...

10

Weekly Market Review November 9, 2014 – November 15, 2014 November 16, 2014

-

Upload

truongtram -

Category

Documents

-

view

214 -

download

0

Transcript of Weekly Market Review - mashreqbank.com · Aabar Investments acquired 707,004,044 shares @AED5 per...

Weekly Market Review November 9, 2014 – November 15, 2014

November 16, 2014

Page I 2

CONTENTS

International Equity Markets

GCC Equities

Currencies

Commodities

Interest Rates

Equity Markets - Top Most & Bottom Most

Commodity Markets - Top Most & Bottom Most

Page I 3

US retail sales gained 0.3% in October. The 0.3% drop recorded in September’s retail sales was unchanged

Thomson Reuters/University of Michigan household sentiment index rose to 89.4 in November

NFIB Small Business Optimism Index gained 0.8 point to 96.1 in October

Euro zone economy expanded 0.2% QoQ and 0.8% YoY in 3Q2014. In 2Q2014, GDP grew 0.1% QoQ and 0.8% YoY

German economy registered 0.1% QoQ growth in 3Q2014, followed by a revised 0.1% QoQ fall in 2Q2014

France expanded 0.3% QoQ in 3Q2014, beating forecasts. 2Q2014 growth revised to show 0.1% QoQ fall

Greece’s GDP grew 0.7% QoQ in 3Q2014 after expanding 0.3%QoQ in 2Q2014 and 0.8% in 1Q2014

Italy’s economy shrank 0.1% QoQ in 3Q2014. GDP declined 0.2% in 2Q2014

Euro zone industrial output rose 0.6% MoM in September vs. a 1.4% fall recorded in August

British Retail Consortium said October total retail spending was 1.4% higher YoY, compared with 0.8% fall in Sept

Britain’s jobless rate remained unchanged at 6% between July-Sept 2014, matching its lowest level in six years

Poland’s economy expanded 3.3% YoY in 3Q2014, exceeding estimates, after a revised 3.5% gain in 2Q2014

New loans disbursed in China tumbled 36% MoM in October, pointing to deepening economic weakness in 4Q2014

Fiscal expenditure dropped 5.7% YoY in Oct, after rising 6.1% in Sept and 6.2% in Aug on YoY basis

Factory output rose 7.7% in October, higher than 6.9% gain in August but below forecasts

Annual consumer inflation remained near a 5-yr low in Oct at 1.6%. Inflation was flat on MoM basis

Japan consumer confidence index deteriorated for a third straight month to 38.9 in Oct from 39.9 in Sept while service sector sentiment index fell to 44 in Oct from 47.4 in Sept

Russia’s Central bank cuts 2014 growth forecast to 0.3% from 0.4%. It expects zero growth in 2015 and 0.1% in 2016

Mexican industrial production unexpectedly fell 0.1% MoM in Sept after a downwardly revised 0.2% growth in Aug

China, Mexico plan a $2.4bn investment fund to support infra, mining & energy projects; eye $5bn worth oil deal

S&P 500 – 1 year performance Euro Stoxx 600 – 1 year performance

Source: Bloomberg, Mashreq Private Banking

INTERNATIONAL EQUITY MARKETS

Last Close Change 5 Day % YTD %

S&P 500 2,039.82 7.90 0.39 10.36

DJI 17,634.74 60.81 0.35 6.38

Nasdaq Comp 4,688.54 56.01 1.21 12.26

Euro Stoxx 600 335.63 0.38 0.11 2.25

FTSE 100 6,654.37 87.13 1.33 -1.40

Dax 9,252.94 -38.89 -0.42 -3.13

CAC 40 4,202.46 12.57 0.30 -2.18

Nikkei 225 17,490.83 610.45 3.62 7.36

Hang Seng 24,087.38 537.14 2.28 3.35

Brazil - Bovespa 51,772.40 -1,450.45 -2.73 0.51

Russia - Micex 1,500.76 3.65 0.24 -0.22

BSE Sensex 28,046.66 178.03 0.64 32.48

Shanghai Comp 2,478.82 60.65 2.51 17.15

Source: Bloomberg, Mashreq Private Banking

Page I 4

Emirates NBD raised $1bn from the sale of 5-yr bond. The lender will pay a coupon of 3.25% on the notes

Abu Dhabi Company for Onshore Oil Operations plans to invest $5-7bn over the next 3 yrs to raise output by 12.5%

Emirates Airline reported an 11.8% YoY increase in its 1HFY2015 net profit to AED1.9bn

S&P affirmed long and short-term foreign & local currency sovereign credit ratings on the Emirate of Sharjah

Dubai Financial Market has included shares of Emaar Malls and Marka in its DFM General Index

Dubai’s Limitless will pledge its future revenues as it attempts a second restructuring of a $1.2bn Islamic loan

Dubai Parks & Resorts (DPR) will offer 40% of its shares in an AED2.5bn IPO that will run from Nov 17-30

Goldman Sachs Group has arranged an AED4.2bn loan for DPR to fund the theme park, to be developed by 3Q2016

Dubai-based Al Habtoor Group is planning to raise around $2.5bn from selling a 30% stake in 1Q2015

MSCI removed 0.5 adjustment factor for Emaar Properties and Dubai Islamic Bank, while weight of First Gulf Bank was raised by other means. 0.5 adjustment factor remained in place for Arabtec Holding and Dana Gas

Abu Dhabi Marine Operating Company signed 3 contracts worth AED11bn for Nasr Full Field Development Project

Aldar Properties plans to spend around AED4bn to finish existing projects over the next 15-18 months

DP World and its subsidiary entered into an agreement to acquire Economic Zones World FZE for $2.6bn

Aabar Investments acquired 707,004,044 shares @AED5 per share of Arabtec Holding raising its stake to 34.93%

Saudi Arabian Mining Co. plans to increase its capital by SR5.6bn through rights offering

S&P has affirmed Dar Al-Arkan Real Estate Development Co’s corporate credit rating with a Stable outlook

MSCI removed 0.5 adjustment factor for Qatar National Bank, Industries Qatar, Doha Bank and Commercial Bank of Qatar. It also added Gulf International Services to the emerging market index in its semi-annual review

Kuwait Foreign Petroleum Exploration Co. plans to increase its production to nearly 200,000 boepd by 2020

Fitch affirmed Investcorp Bank ‘s long and short-term issuer default rating with a Stable outlook

Last Close Change 5 Day % YTD %

Dubai 4,657.29 251.14 5.70 38.21

Abu Dhabi 4,953.36 163.08 3.40 15.45

Saudi Tadawul 9,681.66 32.38 0.34 13.43

Qatar Index 13,729.78 139.29 1.02 32.28

Kuwait Index 7,201.26 66.65 0.93 -4.61

Oman MSM 30 7,013.45 92.22 1.33 2.62

Bahrain All

Share 1,430.31 -10.65 -0.74 14.53

Egypt EGX 30 9,260.18 -160.57 -1.70 36.52

Istanbul 100

Index 81,211.55 3,253.80 4.17 19.78

Source: Bloomberg, Mashreq Private Banking

DFMGI – 1 year performance Saudi Tadawul – 1 year performance

GCC EQUITIES

Source: Bloomberg, Mashreq Private Banking

Page I 5

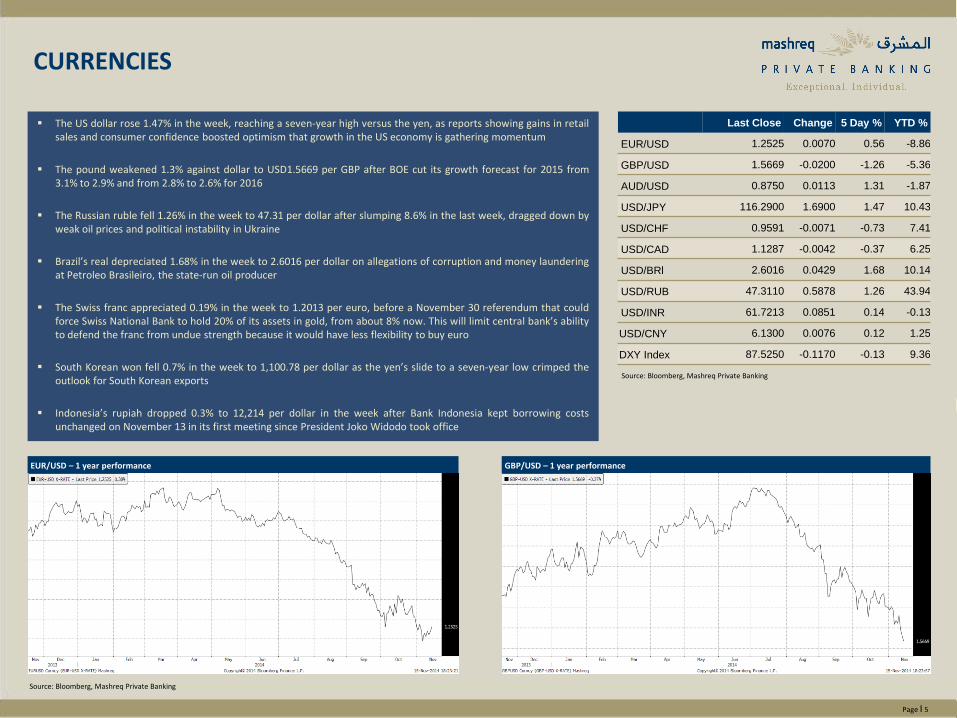

The US dollar rose 1.47% in the week, reaching a seven-year high versus the yen, as reports showing gains in retail sales and consumer confidence boosted optimism that growth in the US economy is gathering momentum

The pound weakened 1.3% against dollar to USD1.5669 per GBP after BOE cut its growth forecast for 2015 from 3.1% to 2.9% and from 2.8% to 2.6% for 2016

The Russian ruble fell 1.26% in the week to 47.31 per dollar after slumping 8.6% in the last week, dragged down by weak oil prices and political instability in Ukraine

Brazil’s real depreciated 1.68% in the week to 2.6016 per dollar on allegations of corruption and money laundering at Petroleo Brasileiro, the state-run oil producer

The Swiss franc appreciated 0.19% in the week to 1.2013 per euro, before a November 30 referendum that could force Swiss National Bank to hold 20% of its assets in gold, from about 8% now. This will limit central bank’s ability to defend the franc from undue strength because it would have less flexibility to buy euro

South Korean won fell 0.7% in the week to 1,100.78 per dollar as the yen’s slide to a seven-year low crimped the outlook for South Korean exports

Indonesia’s rupiah dropped 0.3% to 12,214 per dollar in the week after Bank Indonesia kept borrowing costs unchanged on November 13 in its first meeting since President Joko Widodo took office

Last Close Change 5 Day % YTD %

EUR/USD 1.2525 0.0070 0.56 -8.86

GBP/USD 1.5669 -0.0200 -1.26 -5.36

AUD/USD 0.8750 0.0113 1.31 -1.87

USD/JPY 116.2900 1.6900 1.47 10.43

USD/CHF 0.9591 -0.0071 -0.73 7.41

USD/CAD 1.1287 -0.0042 -0.37 6.25

USD/BRl 2.6016 0.0429 1.68 10.14

USD/RUB 47.3110 0.5878 1.26 43.94

USD/INR 61.7213 0.0851 0.14 -0.13

USD/CNY 6.1300 0.0076 0.12 1.25

DXY Index 87.5250 -0.1170 -0.13 9.36

EUR/USD – 1 year performance GBP/USD – 1 year performance

Source: Bloomberg, Mashreq Private Banking

CURRENCIES

Source: Bloomberg, Mashreq Private Banking

Page I 6

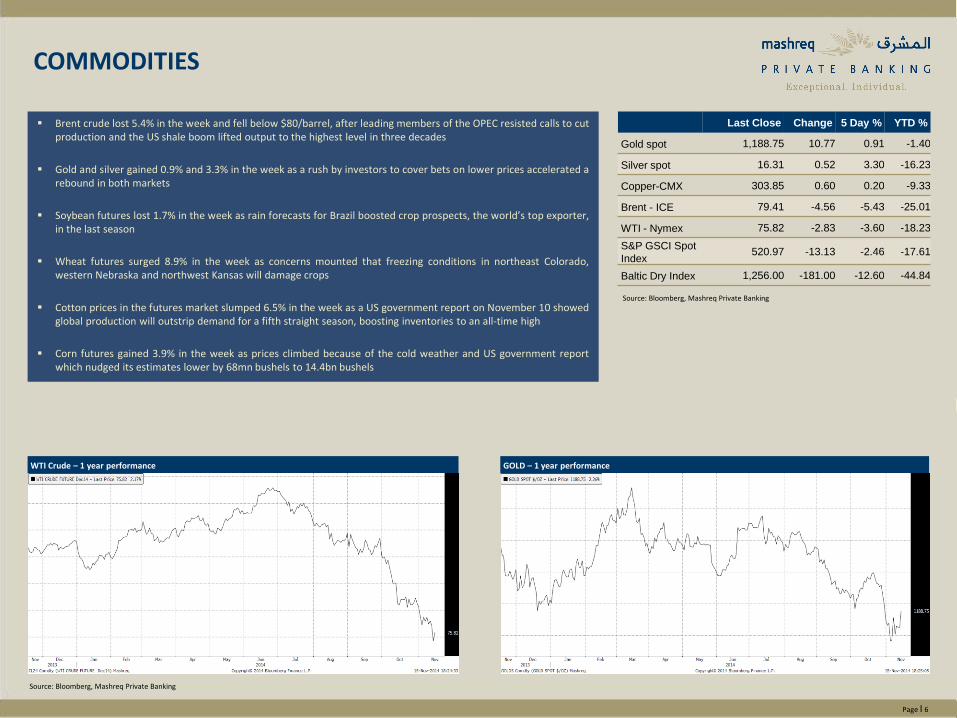

Brent crude lost 5.4% in the week and fell below $80/barrel, after leading members of the OPEC resisted calls to cut production and the US shale boom lifted output to the highest level in three decades

Gold and silver gained 0.9% and 3.3% in the week as a rush by investors to cover bets on lower prices accelerated a rebound in both markets

Soybean futures lost 1.7% in the week as rain forecasts for Brazil boosted crop prospects, the world’s top exporter, in the last season

Wheat futures surged 8.9% in the week as concerns mounted that freezing conditions in northeast Colorado, western Nebraska and northwest Kansas will damage crops

Cotton prices in the futures market slumped 6.5% in the week as a US government report on November 10 showed global production will outstrip demand for a fifth straight season, boosting inventories to an all-time high

Corn futures gained 3.9% in the week as prices climbed because of the cold weather and US government report which nudged its estimates lower by 68mn bushels to 14.4bn bushels

Last Close Change 5 Day % YTD %

Gold spot 1,188.75 10.77 0.91 -1.40

Silver spot 16.31 0.52 3.30 -16.23

Copper-CMX 303.85 0.60 0.20 -9.33

Brent - ICE 79.41 -4.56 -5.43 -25.01

WTI - Nymex 75.82 -2.83 -3.60 -18.23

S&P GSCI Spot

Index 520.97 -13.13 -2.46 -17.61

Baltic Dry Index 1,256.00 -181.00 -12.60 -44.84

WTI Crude – 1 year performance GOLD – 1 year performance

Source: Bloomberg, Mashreq Private Banking

COMMODITIES

Source: Bloomberg, Mashreq Private Banking

Page I 7

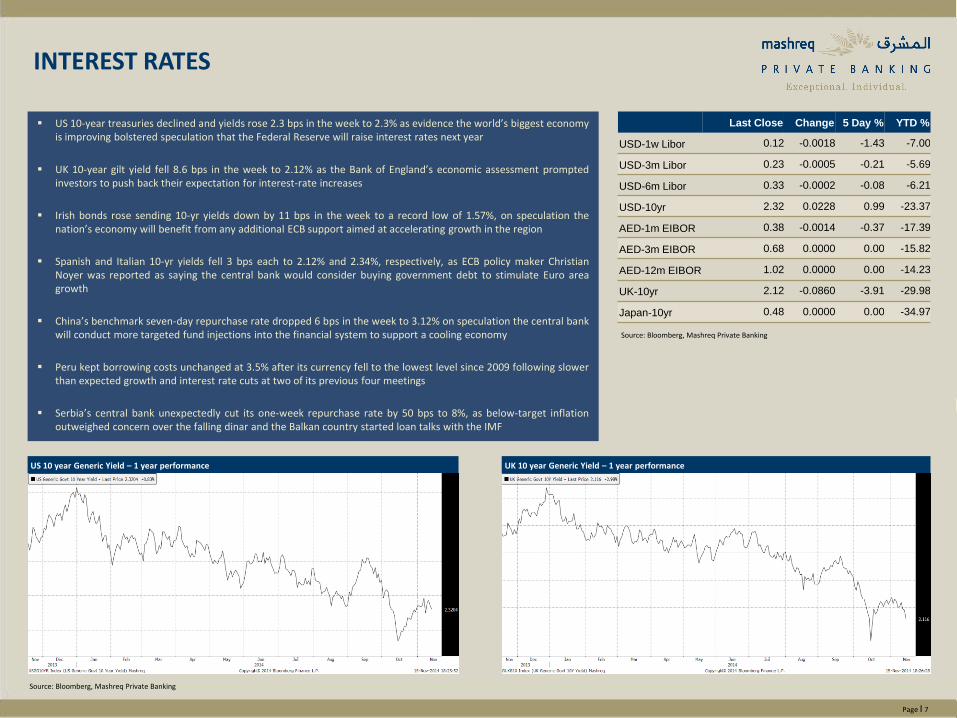

US 10-year treasuries declined and yields rose 2.3 bps in the week to 2.3% as evidence the world’s biggest economy is improving bolstered speculation that the Federal Reserve will raise interest rates next year

UK 10-year gilt yield fell 8.6 bps in the week to 2.12% as the Bank of England’s economic assessment prompted investors to push back their expectation for interest-rate increases

Irish bonds rose sending 10-yr yields down by 11 bps in the week to a record low of 1.57%, on speculation the nation’s economy will benefit from any additional ECB support aimed at accelerating growth in the region

Spanish and Italian 10-yr yields fell 3 bps each to 2.12% and 2.34%, respectively, as ECB policy maker Christian Noyer was reported as saying the central bank would consider buying government debt to stimulate Euro area growth

China’s benchmark seven-day repurchase rate dropped 6 bps in the week to 3.12% on speculation the central bank will conduct more targeted fund injections into the financial system to support a cooling economy

Peru kept borrowing costs unchanged at 3.5% after its currency fell to the lowest level since 2009 following slower than expected growth and interest rate cuts at two of its previous four meetings

Serbia’s central bank unexpectedly cut its one-week repurchase rate by 50 bps to 8%, as below-target inflation outweighed concern over the falling dinar and the Balkan country started loan talks with the IMF

Last Close Change 5 Day % YTD %

USD-1w Libor 0.12 -0.0018 -1.43 -7.00

USD-3m Libor 0.23 -0.0005 -0.21 -5.69

USD-6m Libor 0.33 -0.0002 -0.08 -6.21

USD-10yr 2.32 0.0228 0.99 -23.37

AED-1m EIBOR 0.38 -0.0014 -0.37 -17.39

AED-3m EIBOR 0.68 0.0000 0.00 -15.82

AED-12m EIBOR 1.02 0.0000 0.00 -14.23

UK-10yr 2.12 -0.0860 -3.91 -29.98

Japan-10yr 0.48 0.0000 0.00 -34.97

US 10 year Generic Yield – 1 year performance UK 10 year Generic Yield – 1 year performance

Source: Bloomberg, Mashreq Private Banking

INTEREST RATES

Source: Bloomberg, Mashreq Private Banking

Page I 8

Ref Country Weekly Change Weekly Change

(USD Adj.)

1 Ukraine -9.27% -15.17%

2 Argentina -7.92% -7.96%

3 Montenegro -4.72% -4.18%

4 Mexico -2.79% -2.74%

5 Brazil -2.73% -4.33%

6 Venezuela -2.46% -2.46%

7 Bulgaria -2.18% -1.64%

8 Greece -2.17% -1.62%

9 Colombia -2.13% -4.80%

10 Cyprus -2.08% -1.53%

Ref Country Weekly Change Weekly Change

(USD Adj.)

1 Nigeria 6.49% 2.80%

2 Dubai−UAE 5.70% 5.70%

3 Turkey 4.17% 5.47%

4 Japan−Nikkei 3.62% 2.11%

5 Abu Dhabi−UAE 3.40% 3.40%

6 Laos 3.19% 3.15%

7 Kenya 2.65% 2.48%

8 China 2.51% 2.38%

9 Hong Kong 2.28% 2.26%

10 Norway 2.10% 3.08%

WEEKLY

Ref Country YTD Change YTD Change (USD Adj.)

1 Argentina 80.85% 38.54%

2 Dubai−UAE 38.21% 38.20%

3 Egypt 36.52% 32.62%

4 India 32.48% 32.65%

5 Qatar 32.28% 32.24%

6 Sri Lanka 26.86% 26.66%

7 Slovenia 25.81% 14.66%

8 Pakistan 24.08% 28.52%

9 Serbia 23.71% 7.67%

10 Philippine 22.54% 21.07%

YTD

Ref Country YTD Change YTD Change (USD Adj.)

1 Russia -30.66% -30.66%

2 Greece -23.39% -30.18%

3 Portugal -21.36% -28.33%

4 Nigeria -14.39% -20.05%

5 Austria -14.01% -21.63%

6 Cyprus -12.70% -20.44%

7 Malta -9.88% -17.86%

8 Jamaica -8.58% -14.15%

9 Latvia -8.56% -16.66%

10 Estonia -6.78% -15.04%

EQUITY MARKETS - TOP MOST & BOTTOM MOST

Source: Bloomberg, Mashreq Private Banking

Page I 9

Ref Commodity Weekly Change

1 Natural Gas -8.88%

2 Cotton -6.50%

3 Gasoil -5.77%

4 Brent Crude -4.77%

5 Gasoline -4.34%

6 WTI Crude -3.60%

7 Heat Oil -3.34%

8 Bean Meal -2.69%

9 Tin -2.37%

10 Lumber -2.20%

Ref Commodity Weekly Change

1 Wheat 8.94%

2 Ethanol 7.28%

3 Coffee 5.26%

4 Orange Juice 5.01%

5 Lean Hogs 4.39%

6 Corn 3.88%

7 Silver 3.82%

8 Live Cattle 2.04%

9 Rubber 1.97%

10 Gold 1.35%

WEEKLY

Ref Commodity YTD Pct Change

1 Coffee 73.44%

2 Feeder Cattle 43.97%

3 Live Cattle 26.54%

4 Aluminium 12.32%

5 Nickel 12.09%

6 Zinc 9.93%

7 Lean Hogs 8.49%

8 Palladium 7.39%

9 Ethanol 5.70%

10 Cocoa 5.09%

YTD

Ref Commodity YTD Pct Change

1 Rubber -31.42%

2 Cotton -29.35%

3 Brent Crude -28.33%

4 Gasoline -26.68%

5 Gasoil -26.08%

6 WTI Crude -22.96%

7 Rough Rice -22.82%

8 Soybeans -22.10%

9 Natural Gas/ICE -22.01%

10 Heat Oil -21.48%

COMMODITY MARKETS - TOP MOST & BOTTOM MOST

Source: Bloomberg, Mashreq Private Banking

Page I 10

IMPORTANT NOTICE

This report was prepared by the Private Banking Unit of Mashreqbank psc (“Mashreq”) in the United Arab Emirates (“U.A.E.”). Mashreq is regulated by the Central Bank of the U.A.E. This report is provided for informational purposes and private circulation only and should not be construed as an offer to sell or a solicitation to buy any security or any other financial instrument or adopt any hedging, trading or investment strategy. Prior to investing in any product, we recommend that you consult with a professional financial advisor, taking into consideration investment objectives, financial circumstances and tax implication. While based on information believed to be reliable, we do not guarantee and make no express or implied representation as to the accuracy of this report or complete description of the securities markets or developments referred to in this report. The information, opinions, forecasts (if any), assumptions or estimates contained in this report are as of the date indicated and are subject to change at any time without prior notice. The stated price of any securities mentioned in this report is as of the date indicated and is not a representation that any transaction can be effected at this price. The risks related to investment products described in this report are not all encompassing and investors should refer to the relevant investment offer document for detailed information and applicable terms and conditions. Investment products, including treasury products, are not guaranteed by Mashreq or any of its affiliates or subsidiaries unless stated otherwise and are subject to investment risk, including loss of principal. Investment products are not government insured. Past performance is not an indicator of future performance. US persons (US Citizens; US Green Card Holders; Resident Aliens subject to US income taxes for IRS purposes) are not eligible for any of the investment products introduced by Mashreq unless stated otherwise. This report is for distribution only under such circumstances as may be permitted by applicable law. Neither Mashreq nor its officers, directors or shareholders or other persons shall be liable for any direct, indirect, incidental or other damages including loss of profits arising in any way from the information contained in this report. This report is intended solely for the use by the intended recipients and the contents shall not be reproduced, redistributed or copied in whole or in part for any purpose without Mashreq’s prior express consent.